Embed Size (px)

Citation preview

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, LEGAL ENTITY DISCLOSURE AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

7 November 2016Americas/United States

Equity ResearchElectric Utilities

Azure Power Global Limited (AZRE)

INITIATION Rating OUTPERFORMPrice (04-Nov-16,US$) 16.95Target price (US$) 21.0052-week price range 16.95 - 13.65Market cap (US$ m) 439*Stock ratings are relative to the coverage universe in each analyst's or each team's respective sector.¹Target price is for 12 months.[V] = Stock Considered Volatile (see Disclosure Appendix)

Research AnalystsMaheep Mandloi

212 325 [email protected]

Patrick Jobin212 325 0843

Andrew Hughes212 325 8277

Tapping High Growth Indian Solar Market with Differentiated Model to Boost Returns■ Initiating with an Outperform Rating and a $21 Target Price: We initiate

coverage of Azure Power (AZRE), an Indian solar independent power producer (IPP) with 1 GW of contracted assets. Our positive thesis is predicated upon (1) a booming solar market expected to grow at a 50%+ CAGR through 2022 driven by policy initiatives, (2) attractive project returns benefitting from global module oversupply, and (3) a differentiated strategy delivering lower costs. We note potential volatility around quarterly earnings given the seasonality, inherent lumpiness of large-project development, and limited track record operating as a public company. Our constructive stance, however, is based on long-term value creation and supportive secular trends.

■ A Large Growing Solar Opportunity: We forecast solar demand in India to grow from 5 GW in 2016 to 18 GW by 2020 driven by (1) strong government support to achieve 100 GW of solar by 2022 and (2) potential further demand elasticity, as solar PPAs are competitive with traditional coal/gas today.

■ Attractive Economics and Visible Growth: AZRE has benefitted from a decline in module costs (down 29% ytd) and non-module costs (down 59% over 5 years) which results in unlevered returns >16% (>40% levered). AZRE operates 357 MWs and has contracted 648 MWs to be built by CY17.

■ Differentiated Strategy with Proven Track Record: AZRE has differentiated in-house EPC capabilities that drive a 12-15% cost advantage. The company has maintained healthy mid-teens project returns by not being the lowest bidder and avoiding states with higher credit and curtailment risk.

■ Valuation Reflects Backlog, Upside from Future Project Wins: Our $21 target price is based on 7.5x our CY18 EBITDA est, which we believe reflects the value of the portfolio by 2018. We see several sources of further upside beyond $21 due to (1) multiple expansion as asset performance is further appreciated by markets, and (2) backlog growth. We see risks from counterparty credit, curtailment, FX, interest rates, and capital availability to fund growth.

Share price performance

A ZRE.N S& P 5 0 0 IN D EX

O ct - 1 6 O ct - 1 6 O ct - 1 6 N o v- 1 61 3

1 4

1 5

1 6

1 7

On 04-Nov-2016 the S&P 500 INDEX closed at 2085.18Daily Oct12, 2016 - Nov04, 2016, 10/12/16 = US$14.6

Quarterly EPS Q1 Q2 Q3 Q42016A - - - -2017E -0.18 -0.11 -0.16 -0.022018E 0.30 0.18 0.03 0.13

Financial and valuation metricsYear 3/16A 3/17E 3/18E 3/19EEPS (CS adj.) (US$) (1.26) (0.46) 0.64 1.37Prev. EPS (US$)P/E (x) -13.5 -36.7 26.5 12.3P/E rel. (%) -72.5 -199.1 161.7 84.3EBITDA (US$ m) 27 51 120 172EV/EBITDA (current) 26.4 13.8 5.9 4.1Net debt (US$ m) 269 442 736 767FFO/Interest -0.5 0.2 0.8 1.1FFO/Total Debt -0.04 0.01 0.06 0.10

Number of shares (m) 25.92 IC (current, US$ m) 360.30BV/share (Next Qtr., US$) 5.4 EV/IC (x) 1.7Net debt (Next Qtr., US$ m) 306.8 Dividend (current, US$) -Net debt/tot eq (Next Qtr.,%) 243.6 Dividend yield (%) -Source: Company data, Thomson Reuters, Credit Suisse estimates

7 November 2016

Azure Power Global Limited (AZRE) 2

Azure Power Global Limited (AZRE)Price (04 Nov 2016): US$16.95; Rating: OUTPERFORM; Target Price: US$21.00; Analyst: Maheep MandloiIncome Statement 3/16A 3/17E 3/18E 3/19ERevenue (US$ m) 39.6 68.0 137.7 194.8EBITDA 27 51 120 172Depr. & amort. (10) (18) (33) (43)EBIT (US$) 16 33 87 129Net interest exp (30) (41) (62) (74)PBT (US$) (19) (14) 25 55Income taxes (5) 4 (9) (19)Profit after tax (24) (10) 17 36Minorities 0 0 0 0Reported net income (US$) (25) (11) 17 36Other NPAT adjustments 0 1 0 0Adjusted net income (24) (10) 17 36Cash Flow 3/16A 3/17E 3/18E 3/19EEBIT 16 33 87 129Net interest (30) (41) (62) (74)Change in working capital 4 (17) 7 (5)CAPEX (137) (332) (351) (107)Free cashflow to the firm (126) (337) (293) (31)Aquisitions - - - -Divestments - - - -Cash flow from investments (138) (326) (351) (107)Cashflow from financing activities 115 158 (0) 0Changes in Net Cash/Debt (13) (173) (293) (31)Balance Sheet (US$) 3/16A 3/17E 3/18E 3/19EAssetsCash & cash equivalents 59 110 64 67Total current assets 73 133 98 105Total assets 470 845 1,130 1,201LiabilitiesTotal current liabilities 68 76 83 84Total liabilities 379 622 888 921Total liabilities and equity 470 845 1,130 1,201Net debt 269 442 736 767Per share 3/16A 3/17E 3/18E 3/19ENo. of shares (wtd avg) 20 23 26 26CS adj. EPS (1.26) (0.46) 0.64 1.37Prev. EPS (US$)Dividend (US$) 0.00 0.00 0.00 0.00Free cash flow per share (6.47) (14.84) (11.17) (1.20)Earnings 3/16A 3/17E 3/18E 3/19ESales growth (%) 133.2 71.5 102.5 41.5EBIT growth (%) (4.6) 104.6 162.4 47.9Net profit growth (%) (4185.7) 57.1 259.7 114.9EPS growth (%) (4185.7) 63.2 238.4 114.9EBITDA margin (%) 67.1 74.8 87.0 88.3EBIT margin (%) 40.9 48.8 63.3 66.1Pretax margin (%) (48.8) (20.8) 18.5 28.0Net margin (%) (61.8) (15.5) 12.2 18.5Valuation 3/16A 3/17E 3/18E 3/19EEV/Sales (x) 17.87 12.97 8.53 6.19EV/EBITDA (x) 26.4 13.8 5.9 4.1EV/EBIT (x) 43.7 26.6 13.5 9.4P/E (x) (13.5) (36.7) 26.5 12.3Price to book (x) 1.9 2.0 1.7Asset turnover 0.1 0.1 0.1 0.2Returns 3/16A 3/17E 3/18E 3/19EROE stated-return on (%) (393.4) (6.8) 8.1 15.1ROIC (%) 0.1 0.0 0.1 0.1Gearing 3/16A 3/17E 3/18E 3/19ENet debt/equity (%) 295.6 198.3 303.9 273.9Interest coverage ratio (X) 0.5 0.8 1.4 1.7

Company BackgroundAzure Power is a leading India solar project developer and independent power producer.

Blue/Grey Sky Scenario

Our Blue Sky Scenario (US$) 36.00Our blue sky value of $36 is based on a 9x of 2018 EBITDA assuming a faster installation growth. We assume company's installation grows to 1.8GW by CY18 and 2.5 GW by CY19, raises additional $200m in capital.

Our Grey Sky Scenario (US$) 15.00Our grey sky value of $15 implies 7x CY18 EBITDA for the currently contracted portfolio. Our grey sky scenario assumes that the company does not grow beyond the current contracted asset base.

Share price performance

A ZRE.N S& P 5 0 0 IN D EX

O ct - 1 6 O ct - 1 6 O ct - 1 6 N o v- 1 61 3

1 4

1 5

1 6

1 7

On 04-Nov-2016 the S&P 500 INDEX closed at 2085.18Daily Oct12, 2016 - Nov04, 2016, 10/12/16 = US$14.6

Source: Company data, Thomson Reuters, Credit Suisse estimates

7 November 2016

Azure Power Global Limited (AZRE) 3

Table of ContentsKey Charts 4

Investment Thesis 5

(1) A Large, Growing Opportunity for Solar Development in India...........................5

(2) Attractive Project Returns and Highly Visible Growth.........................................5

(3) Differentiated Strategy and Proven Track Record ..............................................6

(4) Valuation Reflects Current Backlog, Upside from Future Project Wins ..............7

Investment Risks......................................................................................................7

Catalysts and Events to Monitor ..............................................................................8

Solar in India — A Large, Growing Opportunity 9

Company Overview 14

Model Drivers 19

Earnings Outlook and Valuation 23

Valuation ................................................................................................................25

Investment Risks 27

Appendix 29

Company Management..........................................................................................29

Management Compensation ..................................................................................30

Board Composition.................................................................................................30

Shareholders..........................................................................................................31

Detailed Financials.................................................................................................32

Azure Power's Projects ..........................................................................................34

Solar in India ..........................................................................................................37

7 November 2016

Azure Power Global Limited (AZRE) 4

Key ChartsFigure 1: Growing Solar Demand in India… Figure 2: …Bolstered by Declining Solar PPAs

0.0 0.6 0.8 1.0 1.12.0

5.07.0

10.012.0

18.0

0.4% 0.6% 0.9%1.6%

2.5%

3.7%

5.1%

7.1%

0.02.04.06.08.0

10.012.014.016.018.020.0

2010 2011 2012 2013 2014 2015E2016E2017E2018E2019E2020E

GW

Solar demand, GW Solar generation as % of total mix

CAGR of 55%

bubble size -100 MW 500 MW

$ 0.04

$ 0.06

$ 0.08

$ 0.10

$ 0.12

$ 0.14

$ 0.16

$ 0.18

$ 0.20

Aug-10 Dec-11 May-13 Sep-14 Jan-16India

wt av

g PPA

bids

, $/kW

h -(U

SD/IN

R of

65)

Source: Company data, Credit Suisse estimates. Source: Company data, Credit Suisse estimates.

Figure 3: Declining Module/System Cost Figure 4: Attractive Project Returns

2.101.30 1.30

0.80 0.50 0.50 0.48 0.39

1.40

1.00 0.90

0.700.40 0.35 0.43 0.35

3.50

2.30 2.20

1.50

0.90 0.85 0.91 0.74

$ -

$ 0.50

$ 1.00

$ 1.50

$ 2.00

$ 2.50

$ 3.00

$ 3.50

$ 4.00

FY10

A

FY11

A

FY12

A

FY13

A

FY14

A

FY15

A

FY16

A

FY17

E

Module cost $/w BOS cost $/w

Current spot module price is <40c/w

Unlevered project IRR sensitivity to PPA and cash costCapex - cash cost/watt

$ 0.60 $ 0.65 $ 0.70 $ 0.75 $ 0.80PPA 4.00 15.4% 13.9% 12.7% 11.6% 10.6%

INR/kwh 4.25 16.6% 15.0% 13.7% 12.6% 11.5%4.50 17.8% 16.2% 14.8% 13.5% 12.5%4.75 19.1% 17.3% 15.8% 14.5% 13.4%5.00 20.3% 18.4% 16.8% 15.5% 14.3%5.25 21.5% 19.6% 17.9% 16.4% 15.2%5.40 22.3% 20.2% 18.5% 17.0% 15.7%

*Note - doesn't include VGF, assumes EPC margin of 12%

current cost

currentPPA

IRR benefits from cost declines while PPAs remain the sameSource: Company data, Credit Suisse estimates. Source: Company data, Credit Suisse estimates.

Note: Single project economics model available on request.

Figure 5: Visible Growth with Multi-Year Backlog Figure 6: Upside from Future Wins and Rerating

371

1,025

1,355 1,495

1,050

-

200

400

600

800

1,000

1,200

1,400

1,600

CY16E CY17E CY18E CY19E

MW operating MWs committed

New auctions on 3-month horizon – 2.4 GWNTPC 350SECI 1,275MP state utility 750Punjab state utility 15Other central agencies 10Total MW 2,400

Scenario TP Assumptions

Base $211.35 GW operational by 2018

Bull $36Growth in line with market, access to capital

Bear $15Only 1 GW of contracted backlog

Source: Company data, Credit Suisse estimates. Source: Company data, Credit Suisse estimates.

7 November 2016

Azure Power Global Limited (AZRE) 5

Investment ThesisWe initiate coverage of AZRE with an Outperform rating and a $21 target price. In our view, Azure Power is well positioned in a structurally power deficit country with a large and fast-growing solar market as its local focus, differentiated development strategy, and disciplined approach in solar bids that deliver attractive project returns.

(1) A Large, Growing Opportunity for Solar Development in IndiaWe forecast that solar demand in India will grow from 2 GW in 2015 to 5 GW in 2016 and grow at a CAGR of 38% through 2020. Demand in the country is driven by a strong federal level policy that targets 100 GW of installed solar capacity by 2022. Total installed capacity of 8.6 GWs as of September 2016 represents just 1% of energy consumption, 2.5% of total installed generation capacity, and 5% of peak electricity demand, and it has room for growth given higher penetration levels in major solar markets today (Germany at 48% of peak demand, Japan at 23%). In addition to policy support, we also expect demand for solar to potentially grow due to demand elasticity, as solar tariffs are now cheaper than imported fossil fuels and even wind energy. Solar also proves to be an economic option to meet the growing energy demand as the country reduces its power deficit (5% average deficit in the past five years) and increases per capita consumption (which at 1,010 kWh/yr is among the lowest in the world today).

Figure 7: We Forecast Demand Grows to 58 GW by 2020, While the Country Targets 100 GW by 2022

Figure 8: Solar PPAs Have Declined 48% in the Past Five Years and Are Cheaper Than Other Tech

1 1 1 25

7

10

12

18

1 24 6

11

18

28

40

58

0

10

20

30

40

50

60

70

2010 2012 2014 2016E 2018E 2020E

GW

Previous year installed capacityNew installed capacity

59.7%CAGR

$ 0.15

$ 0.13

$ 0.08 $ 0.08

$ 0.07

$ 0.05

$ -

$ 0.02

$ 0.04

$ 0.06

$ 0.08

$ 0.10

$ 0.12

$ 0.14

$ 0.16

Gas -peaker

Solar2011

Solar2014

Wind Solar2016

Coal

Leve

lized

PPA

/tariff

-$/k

Wh

48% decline in 5 years

Source: MNRE, Company data, Credit Suisse estimates. Source: Company data, Credit Suisse estimates.

(2) Attractive Project Returns and Highly Visible GrowthAZRE is fully funded to build its contracted portfolio of 1GW of projects with an attractive 16% unlevered returns or 40%+ equity returns for projects under construction. The company benefits from an in-house EPC development strategy that saves ~12-15% margin on system cost thereby resulting in cost efficiencies of ~$0.10/w at today's

7 November 2016

Azure Power Global Limited (AZRE) 6

construction cost. However, the company's higher unlevered returns (~200 bps above threshold) are a result of steeper-than-expected decline in module prices (down 29% or $0.15/w YTD versus down 65% over five years in spot market) while the PPAs in the backlog contracted through reverse bids remain unchanged. We calculate that every $0.05/w reduction in system costs increases unlevered IRR by ~100 bps. While sustaining these high returns beyond the contracted portfolio could be difficult due to intensifying competition, we expect new projects would be bid at healthy unlevered returns of ~14% (and >20% equity returns).

Figure 9: Attractive Project IRRs Have Room to Grow with Lower PPAs

Figure 10: Strong Visibility in Future Auctions

Unlevered project IRR sensitivity to PPA and cash cost

Capex - cash cost/watt$ 0.60 $ 0.65 $ 0.70 $ 0.75 $ 0.80

PPA 4.00 15.4% 13.9% 12.7% 11.6% 10.6%INR/kwh 4.25 16.6% 15.0% 13.7% 12.6% 11.5%

4.50 17.8% 16.2% 14.8% 13.5% 12.5%4.75 19.1% 17.3% 15.8% 14.5% 13.4%5.00 20.3% 18.4% 16.8% 15.5% 14.3%5.25 21.5% 19.6% 17.9% 16.4% 15.2%5.40 22.3% 20.2% 18.5% 17.0% 15.7%

*Note - doesn't include VGF, assumes EPC margin of 12%

current cost

currentPPA

returns on backlog 8.6 9.4

18.0 2.4

79.6

100

-

10

20

30

40

50

60

70

80

90

100

Instal

led G

W

Tend

ers t

o be i

nstal

led

Total

bids

tend

ered

Tend

ers e

xpec

ted in

2016

Futur

e ten

ders

2022

targ

et

Source: Company data, Credit Suisse estimates. Source: Company data, MNRE, Credit Suisse estimates.

(3) Differentiated Strategy and Proven Track RecordIn a highly competitive solar industry driven by limited barriers to project development, Azure Power differentiates itself from competition as (1) in-house EPC reduces cash costs for project under development by 12-15%, increases leverage ratio to ~80-85% compared with ~75% for peers, and hence results in higher equity returns; (2) the company has deliberately avoided states with higher counterparty risk and has 49% of PPAs with federally backed AA/AAA-rated NTPC and SECI as well as 37% with BB/BBB-rated states Punjab and Karnataka; and (3) management has avoided being the lowest cost bidder in many projects despite strong competition as it leverages its local expertise and in-house visibility on system prices.

Development expertise is focal. While we believe more entrants will aggressively pursue the Indian solar market, the multi-year lead and local connections, coupled with the in-house EPC capabilities that reduce costs and accelerate commercialization of value enhancing technologies and techniques, will enable Azure Power to continue to earn healthy returns above its cost of capital in the near to medium term.

7 November 2016

Azure Power Global Limited (AZRE) 7

Figure 11: Azure Power's Counterparty Exposure in the Contracted Backlog

Figure 12: Azure Power's PPA Premium over Lowest Competitive Bids

Counterparty MWs as % of total Credit ratingNTPC 292 29.0% AAAPunjab state 222 22.1% BB+SECI 198 19.7% AAKarnataka state 150 14.9% BBB+/B-AP state 50 5.0% BBChhattisgarh state 30 3.0% AGujarat state 10 1.0% A+UP state 10 1.0%Bihar state 10 1.0%Ordinance factory 7 0.7%Rooftop 26 2.6%Total 1,005

0%

2%

4%

6%

8%

10%

12%

14%

16%

Punja

b 2.2

Punja

b 3.1

Gujar

at 1.1

Rajas

than 1

Rajas

than 2

.2Ra

jastha

n 3.2

Rajas

than 4

Karn

ataka

2Ch

hattis

garh

1.1

Chha

ttisga

rh 1.

3An

dhra

Pra

desh

1Ma

hara

shtra

1.1

Delhi

1.2

Karn

ataka

3.2

Punja

b 4.1

Punja

b 4.3

Uttar

Pra

desh

2An

dhra

Pra

desh

3

prem

ium ov

er lo

wer b

idder

, %

Source: Company data, Credit Suisse estimates. Source: Company data, MNRE, Credit Suisse estimates.

(4) Valuation Reflects Current Backlog, Upside from Future Project WinsOur target price of $21 reflects a 7.5x CY18 EV/EBITDA multiple, which assumes 1.35 GW of projects are operational by CY18 with enough cash buffer to grow ~10%/yr organically. The multiple just slightly above traditional Indian IPPs reflects lower long-term commodity risk. (Traditional Indian IPPs trade at 6x-9x, with an average of 7.3x.) Our target price also represents a 13% equity discount rate on DCF of contracted project cash flows. Given the low-risk nature of these cash flows, we believe a 13% equity rate is appropriate. (We note that this is a burn down value, as it doesn't assume any future growth.) We see upside from future project wins and calculate equity value of $36/sh under our blue sky where operational MWs grow to 2.5 GW by 2019 (a 53% CAGR over contracted MWs and in-line with demand growth). Our grey sky scenario values the stock at $15/sh and doesn't include any future growth in projects.

Investment RisksWe see the following risks associated with realizing our $21 target price.

■ Seasonality and lumpiness: We note potential volatility around quarterly earnings given the seasonality, inherent lumpiness of large-project development, and limited track record operating as a public company.

■ FX Risk: Investors are exposed to FX risks, as the company's operations are INR denominated. INR has depreciated 8%/yr on average in the past five years.

■ Interest Rate Risk: 72% of current debt (and all new debt) is floating and INR denominated and is based of RBI's repo rate, which increases risks to interest rate volatility. On the flip side, the company could benefit from rate spread compression as the sector evolves.

7 November 2016

Azure Power Global Limited (AZRE) 8

■ Competition for New Awards: Project development is highly competitive in India and project returns on new awards are predicated on rational bidding behavior by developers.

■ Capital Needs for Growth: We believe that the company remains fully funded to build 1.35 GW of projects by 2018 and then grow organically at ~10%/yr. However, achieving the company's target of 5 GW of committed and operating projects by 2020 would require additional capital, in our view.

■ Counterparty and Curtailment Risk: PPAs with state-owned electricity distribution companies (discoms) may have higher counterparty risk given the perceived risk of non-payments and curtailments for renewable projects. The company has tried to avoid contracts with discoms with lower credit ratings. In the 1 GW of contracted backlog, federally backed entities with AA/AAA credit ratings (NTPC and SECI) represent 49% of contracts, while states with >BB ratings represent 46% of contracts.

■ Policy Changes: Current solar demand is aided by federal/state government bids that are guided by the 100 GW national solar mission. Solar policy could change in the future due to political developments or other factors, though such a scenario looks unlikely since solar is one of the cheapest sources of electricity in the country. We could see positive impact if new policy measures are introduced to create a carbon market or strictly enforce renewable procurement obligations.

Catalysts and Events to Monitor■ Demonstrating Growth Through Project Wins in Upcoming Auctions: Growth

beyond the 1 GW of contracted assets depends on the company's ability to win new projects in upcoming auctions at >14% unlevered project returns. The company expects 2.4 GW of new tenders in the next two to three months, and its prior win rate of 10% implies additional 200-300 MWs of project wins. A 100 GW target implies 15 GW/yr auctions from 2017 to 2022.

■ Cost Declines amid Oversupplied Market: We currently expect solar system costs to decline ~14% through CY16 and an additional 6% in CY17, the decline primarily driven by a sharp decline in module costs. We could see upside to estimates from even lower costs stemming from lower-than-expected global demand in 2017.

■ Lock-Up Expirations: Current shareholders excluding insiders (15.8m shares or 61.1% of outstanding shares) have a 180-day lock-up period post-IPO ending April 10, 2017. CDPQ (4.167m shares or 16.1% of total) has a 270-day lock-up period ending July 9, 2017.

7 November 2016

Azure Power Global Limited (AZRE) 9

Solar in India — A Large, Growing OpportunityWe forecast solar demand in India will grow from 2 GW in 2015 to 5 GW in 2016 and then grow at an annual CAGR of 38% until 2020. Demand in the country is primarily driven by the central government target to achieve 100 GW of solar capacity by 2022, a power deficit country with one of the world's fastest-growing electricity demands, and declining solar system costs making it cheaper than most other sources of energy (including gas, coal, and wind) on an LCOE basis.

Figure 13: India Is the Fastest-Growing Solar MarketFigure 14: India Renewable Target Requires Solar Installations of ~15GW/Yr

1 3 4 11 11 15 17 18 20 22 22

1 2 3 5 6

7 10 7

11 15 19

1 1 2

6 9 8

6 6 6

6 6

0 1

1

1 1

2 5 7

10 12

18

16 16 13

7 7

7 6 6

6

6

7

3 4 6

6 11

13 16 19

22

25

28

2127 29

3645

5359 63

74

87

99

2010 2012 2014 2016E 2018E 2020E

Dema

nd (G

Ws)

Othermarkets

Europe

India

Japan

US

China

44

92

33 5 1 175

0

20

40

60

80

100

120

140

160

180

200

8-2016 Solar Wind Biomass Small Hydro

Installedrenewablecapacity

Additional 2022renewable

target

GW

Source: Credit Suisse estimates. Source: MNRE, Credit Suisse estimates.

Strong Policy SupportLearning from other countries, the Indian government launched a National Solar Mission (NSM) policy in 2010 that targets 100 GW of solar operating capacity by 2022. The deployment has been planned over three phases, with Phase 1 from 2012 to 2013, Phase 2 from 2013 to 2017, and Phase 3 from 2017 to 2022. The country had targeted 2 GW of solar installations in FY16, growing to 12 GW in FY17, 15 GW in FY18, and then ramping up to 17.5 GW by FY21. Our demand estimates ramping gradually from 5 GW in 2016 to 12 GW in 2019 and 18 GW in 2020, which seems conservative compared with the country's target because (1) the 100 GW target includes 40 GW of rooftop projects (versus <1 GW installed today), which we believe would ramp slower than targeted as these projects have smaller ticket sizes and require more customer education, and (2) a tight capital market for a nascent industry.

Under the national solar mission, central and state governments issue RfPs to meet the targets. In a reverse bidding mechanism, developers either bid for the lowest subsidy (either long-term feed in tariff adder or upfront viability gap funding) or bid for the lowest PPA without subsidy below the benchmark tariff decided by the government regulator. This reverse auction policy differs compared with other major solar markets that have fixed

7 November 2016

Azure Power Global Limited (AZRE) 10

FiTs for qualifying assets (e.g., in Germany, Spain, China etc.). A fixed FiT provides a higher degree of certainty to investors but does put undue burden on the tax payers if timely FiT reductions do not match system costs decline, giving investors the ability to dramatically over earn. We view the Indian reverse auction system as a more sustainable and healthy system that provides for more stable growth.

The country also revised its renewable purchase obligations (RPO) for the states, which now requires 17% of renewable generation by 2022 (versus the prior target of 15% by 2020) and includes solar carve out. The RPO targets renewable penetration levels of 11.5%, 14.25%, and 17% in FY17/18/19, with solar carve-outs of 2.75%, 4.75%, and 6.75% in FY17/18/19 (excludes hydro), respectively. The RPO seems in-line with the national solar mission targets.

Solar projects are also eligible to receive ten-year tax holiday during the first 15 years of operation. During the tax holiday period, the corporate tax rate of 34% is reduced to a minimum alternative tax rate of 21%.

A Reverse Bid Process with Room for Multiple Winners

Despite being a highly competitive market, Indian solar auctions have room for multiple winners at different PPA price points. The bids don’t have just one winner, instead the bids are designed so that each auction is won by a group of developers. Bids are accepted at the quoted tariffs (with or without an upfront subsidy) starting with the lowest bid until the total auctioned capacity is reached.

Higher Sunshine and Near Load CentersIndia receives an average sunshine (5.1 hrs/day) across the country that is higher compared with other major solar markets. (The top two in the solar market are the United States with 4.7 hrs/day and China with 3.6 hrs/day on average.) This equates to a ~21% capacity factor (or plant load factor).

Regions with strong solar insolation are spread across the country and are closer to load centers, unlike in China where the majority of higher sunshine regions are in the sparsely populous western states, requiring significant investments in west-to-east transmission capacities.

7 November 2016

Azure Power Global Limited (AZRE) 11

Figure 15: India Solar Radiation Is Higher in Western and Southern States… Figure 16: .. Near Higher Population Regions

Source: MNRE. Source: Census of India.

Growing Energy Demand in a Power Deficit CountryIndia's electricity demand has grown by mid to high single % digits every year over the past decade, in-line with the country's GDP growth rate. Energy demand is expected to grow at 9% in 2017 versus a real GDP growth expectation of 7.7%. Demand has increased due to industrial growth but also as the country tries to bridge its energy deficit that averaged at a deficit of 5% in the past five years from 2011 to 2016. In addition, per capital energy consumption is also expected to grow, which at 1,010 kWh/yr is among the lowest globally compared with >10,000 kWh/yr in United States and >3,700 kWh/yr in China.

Growing Renewable Demand

Energy in the country is predominantly sourced from fossil fuels, which represent ~70% of the total installed capacity base that generates ~74% total electricity. Solar represents only ~3% of installed capacity today and generates ~1% of total electricity. The country plans to increase its renewable mix to reduce pollution levels and reduce its fuel import bill. Under the Paris Climate Change Agreement signed in September 2016, the country has agreed to produce ~40% of electricity with non-fossil fuel sources by 2030 (from 26% today).

7 November 2016

Azure Power Global Limited (AZRE) 12

Figure 17: India's Growing Energy DemandFigure 18: A Heavily Fossil Fuel Dependent Market Today

523 546 559 591 632

691 739

777 831 862

937 998 1,002

1,067 1,114

559.2

672

884 914 957

1,010 1,075

0

200

400

600

800

1,000

1,200

400

600

800

1,000

1,200

1,400

2001

-02

2002

-03

2003

-04

2004

-05

2005

-06

2006

-07

2007

-08

2008

-09

2009

-10

2010

-11

2011

-12

2012

-13

2013

-14

2014

-15

2015

-16

Per c

apita

cons

umpti

on, k

Wh/y

r

Ener

gy co

nsum

ption

, TW

h

Energy consumption, TWh Per capita consumption kWh/yr

Coal61%Gas

8%Diesel0%

Nuclear2%

Hydro14%

Wind9%

Solar3%

Other renewables

3%

Installed capacity by type of technology

Source: CEA, Credit Suisse estimates. Source: CEA, Credit Suisse estimates.

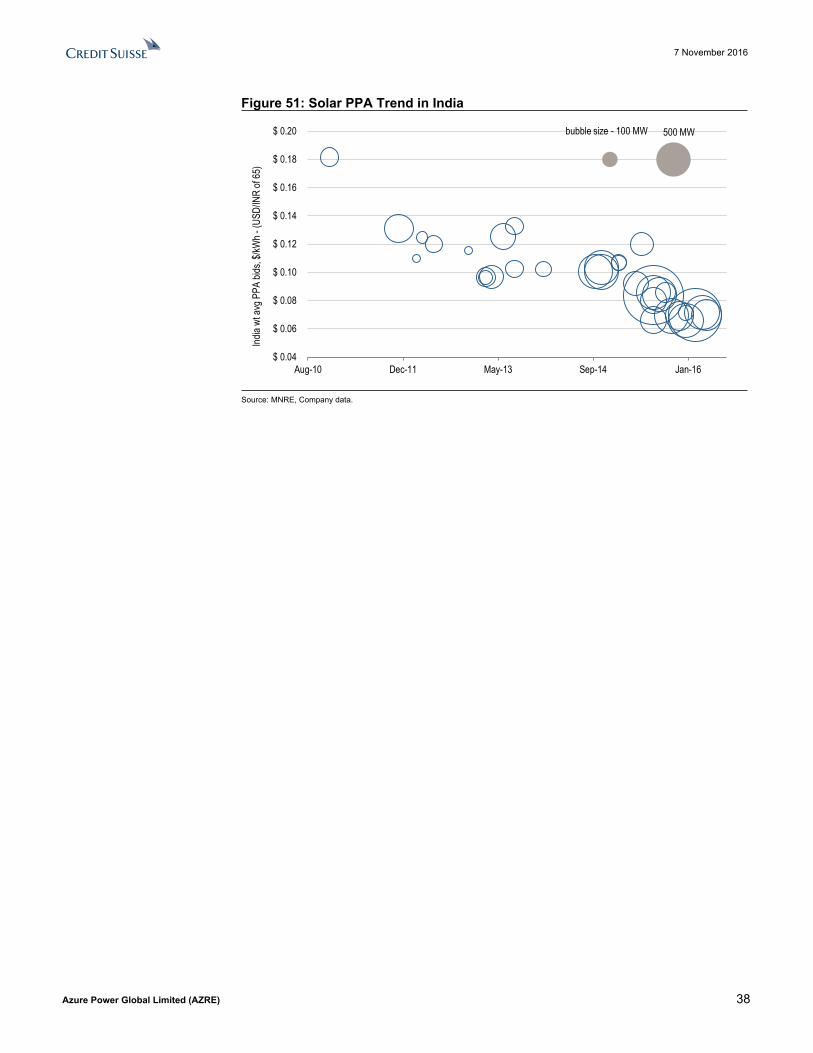

Demand Elasticity from Declining Solar Module Prices and PPAs As evident from Figure 19, project sizes in the country have increased from a couple of MWs in 2011 to hundreds of MWs as project economics have improved due to declining system costs. Solar PPAs have declined by 46% in the past five years, while benchmark solar system prices have declined 75% in the same duration.

Solar tariffs today are cheaper than other technologies for a new build project. Variable cost of energy produced from low-cost imported natural gas projects is ~INR 3-5/kWh, (assuming landed LNG prices of ~$5-6/MMBtu), while the all-in tariff for solar projects is already at INR 4/kWh in higher sunshine states today. Solar tariffs are also cheaper compared with recent coal tariffs signed at INR 4.9/kWh and wind tariffs of INR 4.93/kWh.

7 November 2016

Azure Power Global Limited (AZRE) 13

Figure 19: Solar PPAs Have Declined 46% Since 2011

Figure 20: Benchmark Solar Costs Have Also Declined 75% in the Past Five Years

bubble size -100 MW 500 MW

$ 0.04

$ 0.06

$ 0.08

$ 0.10

$ 0.12

$ 0.14

$ 0.16

$ 0.18

$ 0.20

Aug-10 Dec-11 May-13 Sep-14 Jan-16

India

wt av

g PPA

bids

, $/kW

h -(U

SD/IN

R of

65)

$ 3.84

$ 3.26

$ 1.90

$ 1.49 $ 1.15

$ 0.95 $ 0.79

$ -

$ 0.50

$ 1.00

$ 1.50

$ 2.00

$ 2.50

$ 3.00

$ 3.50

$ 4.00

$ 4.50

2010

-11

2011

-12

2012

-13

2013

-14

2014

-15

2015

-16

2016

-17

CERC

benc

hmar

k PV

cost

/watt

Source: MNRE, Credit Suisse estimates. Source: CERC.

7 November 2016

Azure Power Global Limited (AZRE) 14

Company OverviewAzure Power is an Indian solar project developer and IPP. The company develops, constructs, owns, and operates utility scale and distributed solar assets in India.

The company was founded in 2008 by CEO Inderpreet Wadhwa, developed its first project in 2009, and has since won ~1 GW of projects under various auctions, representing a 10% win rate. As of July 2016, the company has installed 357 MW of projects that are now operational, representing a CAGR of 114% in the past four years. In addition, 390 MW projects are under construction, while 298 MW of projects are contracted but yet to start construction. Azure Power has 360 full-time employees, of which 37 are in project development, 135 in EPC, 72 in O&M, and 116 handling Management and Administrative tasks.

While projects generally fetch 14% unlevered returns (300-400 bps above current project debt terms), the company expects to achieve a strong 16.6% unlevered return on the projects in the backlog mainly due to the recent decline in module and system prices, which was not priced in when the contracts were bid. The company also benefits from in-house EPC and higher leverage which results in equity IRRs of >40%.

Figure 21: Azure Power's History

SK Gupta joins as CFOGlen Minyard joins R&D team

Azure founded by Inderpreet Wadhwa Rob Kelly joins board2008 2009 2010 2011 2012 2013 2014 2015 2016

Installed 1st utility scale project Installed first rooftop project *IPOAnnounced 100 MW target in 3-5 years

Cummulative MWsinstalled

248 417 1,0052 2 17 17 55 89

2 - - - - - 5 - 10 - - - -35

- - - - - 15 19 20

120

10 6

88

2 12

55

230

150

100 90

02468101214161820

-

50

100

150

200

250

Q4 20

09Q1

2010

Q2 20

10Q3

2010

Q4 20

10Q1

2011

Q2 20

11Q3

2011

Q4 20

11Q1

2012

Q2 20

12Q3

2012

Q4 20

12Q1

2013

Q2 20

13Q3

2013

Q4 20

13Q1

2014

Q2 20

14Q3

2014

Q4 20

14Q1

2015

Q2 20

15Q3

2015

Q4 20

15Q1

2016

Q2 20

16Q3

2016

Q4 20

16Q1

2017

Q2 20

17Q3

2017

Q4 20

17

PPA

-INR

/kWh

MWs i

nsta

lled

Total MW PPA - Wt avg, Rs/kWh (RHS)

Source: Company data, Credit Suisse estimates.

Figure 22: Typical Utility Scale Solar Bid Execution

Source: Company data, Credit Suisse estimates.

7 November 2016

Azure Power Global Limited (AZRE) 15

CustomersAzure Power signs PPA agreements with utilities (federal or state owned) and private entities (commercial contracts). Of the 1GW portfolio, 969 MWs are utility scale projects with a weighted average PPA of INR 5.98/kWh or $0.0892/kWh. The customer base includes NTPC, an AAA-rated federal government owned generator (292 MWs or 29% of contracted portfolio); SECI, an AA-rated federal government backed agency (198 MWs or 19.7% of portfolio); distribution companies owned by Indian states (482 MWs or 48% of portfolio); and commercial offtakers (33 MWs or 3.3% of total). The customer mix could tilt more toward central government entities in the future, as management is expected to give preference to bids with lower counterparty risk. We could see upside in commercial and rooftop mix as adoption increases due to lower costs, though higher upfront financing cost will remain a bottleneck.

Suppliers■ Modules: Solar modules represent >50% of total system cost for Azure Power. The

company's annual module requirements of ~650 MWs represent just 1% of global module demand. The company sources c-Si modules from Asian suppliers like HQCL and other China-based tier-1 manufacturers. The company also sources thin-film CdTe modules from FSLR.

■ Inverters: The company procures inverters from domestic manufacturers like Schneider Electric India and Bonfiglioli Renewable Power Conversion as well international supplier like SMA Solar.

■ Purchase orders are generally priced at prevailing spot prices, giving the company the flexibility to take advantage of declining component prices. The company doesn't have any long-term fixed-priced contracts.

AZRE's Current Operating Portfolio and BacklogAs of June 2016, Azure Power has a total backlog of ~1GW of which 357 MWs of projects are operational, 390 MW are under construction, and 258 MW are committed and yet to be constructed.

We forecast that the company will grow its operating portfolio to 1GW by 2017, 1.35 GW by 2018, and 1.5 GW by 2019, resulting in EBITDA of $105/$165/$186m in the three years, respectively.

7 November 2016

Azure Power Global Limited (AZRE) 16

Figure 23: Azure Power Project List—Operational and CommittedProject Names COD Capacity Tariff Offtaker Utility rating Credit rating PPA duration

Calendar Qtr (MW) (Rs/kWh) YearsOperationalPunjab 1 Q4 2009 2 17.91 NTPC Vidyut Vyapar Nigam AAA 25Punjab 2.1 Q3 2014 15 7.67 Punjab State Power Corporation Limited A+ BB+ 25Punjab 2.2 Q4 2014 15 7.97 Punjab State Power Corporation Limited A+ BB+ 25Punjab 2.3 Q4 2014 4 8.28 Punjab State Power Corporation Limited A+ BB+ 25Punjab 3.1 Q1 2016 24 7.19 Punjab State Power Corporation Limited A+ BB+ 25Punjab 3.2 Q1 2016 4 7.33 Punjab State Power Corporation Limited A+ BB+ 25Gujarat 1.1 Q2 2011 5 15.00 Gujarat Urja Vikas Nigam Limited A+ 25Gujarat 1.2 Q4 2011 5 15.00 Gujarat Urja Vikas Nigam Limited A+ 25Rajasthan 1 Q4 2011 5 11.94 NTPC Vidyut Vyapar Nigam Limited AAA 25Rajasthan 2.1 Q1 2013 20 8.21 NTPC Vidyut Vyapar Nigam Limited AAA 25Rajasthan 2.2 Q1 2013 15 8.21 NTPC Vidyut Vyapar Nigam Limited AAA 25Rajasthan 3.1 Q2 2015 20 5.45 Solar Energy Corporation of India AA 25Rajasthan 3.2 Q2 2015 40 5.45 Solar Energy Corporation of India AA 25Rajasthan 3.3 Q2 2015 40 5.45 Solar Energy Corporation of India AA 25Rajasthan 4 Q4 2015 5 5.45 Solar Energy Corporation of India AA 25Karnataka 1 Q1 2015 10 7.47 Bangalore Electricity Supply Company Limited B+ 25Karnataka 2 Q1 2016 10 6.66 Bangalore Electricity Supply Company Limited B+ 25Uttar Pradesh 1 Q1 2015 10 8.99 Uttar Pradesh Power Corporation Limited C+ 12Chhattisgarh 1.1 Q2 2015 10 6.44 Chhattisgarh State Power Distribution Company Limited B+ 25Chhattisgarh 1.2 Q2 2015 10 6.45 Chhattisgarh State Power Distribution Company Limited B+ 25Chhattisgarh 1.3 Q3 2015 10 6.46 Chhattisgarh State Power Distribution Company Limited B+ 25Delhi 1.1 Q4 2015 1 5.43 Solar Energy Corporation of India AA 25Andhra Pradesh 1(4) Q1 2016 50 5.89 Southern Power Distribution Company of Andhra Pradesh LimitedB+ 25Bihar 1 Q3 2016 10 8.39 North Bihar Power Distribution Company Limited and South Bihar Power Distribution Company LimitedB+ 25Operational Capacity 340 7.01

Under ConstructionMaharashtra 1.1 Q3 2016 2 5.50 Ordinance Factory Bhandara 25Maharashtra 1.2 Q4 2016 5 5.31 Ordinance Factory Ambajhari 25Delhi 1.2 Q2 2016 2 5.45 Solar Energy Corporation of India AA 25Karnataka 3.1 Q4 2016 50 6.89 Chamundeshwari Electricity Supply Corporation Limited B 25Karnataka 3.2 Q1 2017 40 6.93 Hubli Electricity Supply Company Limited C+ 25Karnataka 3.3 Q1 2017 40 6.96 Gulbarga Electricity Supply Company Limited B 25Punjab 4.1 Q1 2017 50 5.62 Punjab State Power Corporation Limited A+ BB+ 25Punjab 4.2 Q1 2017 50 5.63 Punjab State Power Corporation Limited A+ BB+ 25Punjab 4.3 Q1 2017 50 5.64 Punjab State Power Corporation Limited A+ BB+ 25Andhra Pradesh 2 Q2 2017 100 5.12 NTPC VidyutVyapar Nigam Limited AAA 25Capacity Under Construction 389 5.93

CommittedUttar Pradesh 2 Q2 2017 50 4.78 NTPC Vidyut Vyapar Nigam Limited AAA 25Telangana 1(5) Q3 2017 100 4.67 NTPC Limited AAA 25Andhra Pradesh 3(5) ND. (EST Q4 2017) 50 4.43 Solar Energy Corporation of India AA 25Uttar Pradesh 3 ND. (EST Q4 2017) 40 4.43 Solar Energy Corporation of India AA 25Capacity Committed 240 4.60

Commercial RooftopCommissionedGujarat Rooftops 2013 2.50 Torrent Power Limited 25DLF (total) 2013-2016 1.90 DLF Limited 25Uttar Pradesh Rooftop 1 Q1 2015 0.56 Indosolar Limited 25Delhi Rooftop 1 Q2 2015 0.06 Delhi Gymkhana Club Limited 25Delhi Rooftop 2 Q2 2015 0.18 Taj Sats Air Catering Limited 20Delhi Rooftop 3 Q2 2016 0.45 Indraprastha Power Generation Co. Limited 25Punjab Rooftop 1 Q3 2015 1.00 JCBL Limited 25Punjab Rooftop 2(7) Q2 2016 10.00 Punjab State Power Corporation Limited A+ BB+ 25Operational rooftop 16.64

Under ConstructionOberoi (total) Q2 2016 0.84 Oberoi Resorts/EIH Limited 15Delhi Rooftop 3 Q4 2016 0.55 Indraprastha Power Generation Co. Limited 25Under Construction rooftop 1.39

CommittedTamil Nadu Rooftop 1 Q1 2017 0 Pennar Industries Limited 20Delhi Rooftop 4 Q3 2017 14 Delhi Metro Rail Corporation 25Odisha Rooftop 1 Q2 2017 4 Green Energy Development Corporation of Odisha 25Committed rooftop 18.2

Total Capacity (all projects) 1,005.2

Source: Company data, Credit Suisse estimates.

7 November 2016

Azure Power Global Limited (AZRE) 17

Differentiated Strategy and Proven Track RecordIn an increasingly competitive project development business, Azure Power stands out among competition, as it has (1) a proven track record in the country with >10% win rate in ~8.5 GW projects tendered since 2012; (2) a different development strategy with in-house EPC resulting in 12-15% cost savings; (3) disciplined selective bidding to reduce counterparty risk and maintain project returns, as 49% of the current portfolio is contracted with central government-backed entities NTPC and SECI (AAA/AA rated); and (4) investments from developments banks (IFC, German bank DEG, French bank PROPARCO) and venture capital (Helion Ventures, Foundation Capital) attesting to quality of assets and belief in management.

Figure 24: Win Rate of ~10% in Prior Auctions Figure 25: Mix of Projects by Counterparties

42 154 768

8%

12%

10%

0%

2%

4%

6%

8%

10%

12%

14%

-

100

200

300

400

500

600

700

800

900

2010-2012 2012-2014 2014-2016

Win

rate,

%

MWs

MWs won in prior auctions Win rate in tenders participated

Counterparty MWs as % of total Credit ratingNTPC 292 29.0% AAAPunjab state 222 22.1% BB+SECI 198 19.7% AAKarnataka state 150 14.9% BBB+/B-AP state 50 5.0% BBChhattisgarh state 30 3.0% AGujarat state 10 1.0% A+UP state 10 1.0%Bihar state 10 1.0%Ordinance factory 7 0.7%Rooftop 26 2.6%Total 1,005

Source: Company data, Credit Suisse estimates. Source: Company data, Credit Suisse estimates.

Growth VisibilityThe company has built 357 MWs to date and contracted an additional 649 MWs, giving visibility of ~1 GW projects operational by 2017. Given the company's proven track record and local expertise, we expect the company could win additional awards to take total operating portfolio to 1.35 GW by 2018 and 1.5 GW by 2019. We expect the organic growth would stem from existing cash reserves and cash flow from the operating portfolio. The government's 100 GW target by 2022 implies additional 91 GW of bids would be issued until 2022 (run rate of 15+ GW/yr). In the very near term, we expect 2.4 GW of bidding activity this year.

7 November 2016

Azure Power Global Limited (AZRE) 18

Figure 26: Growth Expectations

371

1,025

1,355 1,495

-

200

400

600

800

1,000

1,200

1,400

1,600

CY16E CY17E CY18E CY19EMW

s

MW Operating

$ 40

$ 105

$ 165 $ 186

$ - $ 20 $ 40 $ 60 $ 80

$ 100 $ 120 $ 140 $ 160 $ 180 $ 200

CY16E CY17E CY18E CY19E

$m

EBITDA

537

1,336

2,214

2,549

-

500

1,000

1,500

2,000

2,500

3,000

CY16E CY17E CY18E CY19E

GWh

Energy generated, GWh

Source: Company data, Credit Suisse estimates.

CompetitionIndian solar auctions are highly competitive, and the Top 20 project developers in the country represent 81% of the total bids in the country. While Azure Power's backlog of ~1 GW represents 6% of total bids announced in the country to date, other competitors in the top 20 include conglomerates (24% of total bids), IPP and infrastructure developers (11.5% of total), and other renewable developers (7% of total bids), though pure-play solar developers have won the most projects (36% of total bids),

The market has seen some consolidation as bidders with lower returns exit the market. Tata power acquired ~1 GW of Welspun energy projects in June 2016 for an EV of $1.21/w, and the media suggests that Greenko will acquire SunEdison's 390 MW operating assets for $315m assets and an additional 800 MW of development pipeline.

Figure 27: Competitive Market

Contracted projects as of Aug 2016 OperationalUnder

Development Contractedas % of

totalAdani 688 1,292 1,980 11%ACME 565 1,085 1,650 9%SunEdison 440 1,176 1,616 9%ReNew Power 231 1,358 1,589 9%Tata Power (incl 1 GW of Welspun Energy) 760 518 1,278 7%Azure 357 698 1,055 6%NTPC 357 510 867 5%Hero Future Energies 40 513 553 3%Suzlon - 515 515 3%Hindustan Power 145 282 427 2%Mytrah - 419 419 2%Solairedirect 110 258 368 2%SBG Cleantech (Softbank) - 350 350 2%SkyPower - 350 350 2%Shapporji Pallonji 105 185 290 2%Mahindra 75 195 270 1%RattanIndia 5 266 271 2%First Solar 150 100 250 1%Essel 107 118 225 1%OPG Power 5 207 212 1%

Subtotal of top-20 4,141 10,395 14,535 81%Total bids 18,024

Source: Company data, Mercom, Credit Suisse estimates.

7 November 2016

Azure Power Global Limited (AZRE) 19

Model DriversAttractive Project Returns Despite Low PPAsWe calculate unlevered returns for projects in the backlog of 16.6%, which is primarily driven by a system cost of $0.77/w, average PPA of INR 5.40/kWh ($0.08/kWh) flat lined for 25 years, 2000 hrs of annual sunshine (22% of capacity factor), 0.6%/yr panel degradation, 3% O&M costs with a 5.7% annual inflation escalator, no renewal value, straight-line depreciation over the 25 years, a tax rate of 34% through the life of project but for a 21% minimum alternative tax due to tax holiday from year six to year 15, and inverter replacements every 11th year.

We calculate equity project returns of >40%, assuming 75% of project leverage (calculated on system cost and including a 12% in-house EPC margin), cost of debt of 10%, and debt amortization over 15 years.

The primary driver of higher returns is the sharp drop in module prices this year (down 29% YTD or down $0.15/w in spot market). We calculate that a ~$0.10/w system cost reduction has enabled the company to capture 2% points above threshold unlevered IRRs.

In addition, the company also benefits from in-house EPC, which saves >$0.10/w versus competitors, and has a disciplined approach to not be the lowest PPA bidder in auctions.

Figure 28: Attractive Economics for Projects in the BacklogAssumptionsSystem size MW 50 USD/INR 67.51

System cost, $/w $0.87 $/w PPA 5.40 INR/kWh Debt/capital 75.0%EPC margin captured (as % of cost) 12.0% PPA escalator 0.0% Cost of Debt 10.0%Net system cost, $/w $ 0.77 $/w VGF - INR/watt Debt duration 15Net system cost, INR/w 52 INR/watt O&M 0.3 INR/watt/yrSystem life 25 years O&M escalator 5.7% EPC margin (pre-tax) 18.2%panel derate 0.6% PPA duration 25 yearsInverter cost - 11th year 4.1 INR/watt Residual discount 100% Cost of equity for NPV 12%Inverter cost - 21st year 3.4 INR/watt

D&A schedule 25 year straight lineSunhours 2,200 hrs/yr Tax rate 34% curtailment 0.0%DC/AC efficiency 90.0% MAT rate 21%Net utilization/PLF 22.6% Tax holiday duration, yr 10

Unlevered economics 1 2 3 4 5 6 7 8 9 10 11...Energy generated, GWh 99 98 98 97 97 96 95 95 94 94 93Operating cash flow 379 376 373 371 368 417 413 410 407 403 240Capex, INR mm (2,582.26)FCF - unlevered (2,204) 376 373 371 368 417 413 410 407 403 240

Unlevered IRR, contracted 16.6%Unlevered PPA PV, $/w $ 0.87

Levered economics 1 2 3 4 5 6 7 8 9 10 11...FCFE (295) 94 101 108 115 173 179 186 192 198 45

Levered IRR, contracted 41%Equity NPV (INR mm) 922Equity NPV ($/w) $ 0.27

Source: Company data, Credit Suisse estimates.

7 November 2016

Azure Power Global Limited (AZRE) 20

Project Costs—Benefits from Lower Spot Prices and In-House EPCSystem cost have declined from $3.50/w in 2010 to $0.59/w by YE16, and management has managed to keep it below competition and benchmark prices due to an in-house EPC. We forecast the company will achieve a system cost of $0.72/w in CY17, $0.66/w in CY18, and $0.60/w in CY19.

Figure 29: AZRE's System Cost Has Declined at a 20% CAGR Since 2010

Figure 30: ... and Is Below CERC's Benchmark Capital Cost Assumptions

2.10

1.30 1.300.80

0.50 0.50 0.48 0.39 0.36

1.40

1.00 0.90

0.70

0.40 0.35 0.430.35 0.33

3.50

2.30 2.20

1.50

0.90 0.85 0.910.74 0.69

$ -

$ 0.50

$ 1.00

$ 1.50

$ 2.00

$ 2.50

$ 3.00

$ 3.50

$ 4.00

FY10

A

FY11

A

FY12

A

FY13

A

FY14

A

FY15

A

FY16

A

FY17

E

FY18

E

Module cost $/w BOS cost $/w

declined at 20% compounded rate $ 3.84

$ 3.26

$ 1.90

$ 1.49

$ 1.15 $ 0.95

$ 0.79

$ -

$ 0.50

$ 1.00

$ 1.50

$ 2.00

$ 2.50

$ 3.00

$ 3.50

$ 4.00

$ 4.50

2010

-11

2011

-12

2012

-13

2013

-14

2014

-15

2015

-16

2016

-17

CERC

benc

hmar

k PV

cost

/watt

Source: Company data, Credit Suisse estimates. Source: Company data, Credit Suisse estimates, CERC.

Deliberately Trying to Not Be the Lowest BidderComparing Azure Power's project PPAs with the lowest competing bids, we find that Azure Power's bids have been on an average INR 0.32/kWh above the lowest bids (or $0.004/kWh). Based on our single project model, we calculate that every INR 0.10/kWh higher PPA increases unlevered project returns by ~40bps.

Figure 31: Azure Power Bid Premium over Lowest Bids—Deliberate Attempt to Not Be the Lowest Bidder

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

Punja

b 2.1

Punja

b 2.2

Punja

b 2.3

Punja

b 3.1

Punja

b 3.2

Gujar

at 1.1

Gujar

at 1.2

Rajas

than 1

Rajas

than 2

.1Ra

jastha

n 2.2

Rajas

than 3

.1Ra

jastha

n 3.2

Rajas

than 3

.3Ra

jastha

n 4Ka

rnata

ka 1

Karn

ataka

2Ut

tar P

rade

sh 1

Chha

ttisga

rh 1.

1Ch

hattis

garh

1.2

Chha

ttisga

rh 1.

3De

lhi 1.

1An

dhra

Pra

desh

1Bi

har 1

Maha

rash

tra 1.

1Ma

hara

shtra

1.2

Delhi

1.2

Karn

ataka

3.1

Karn

ataka

3.2

Karn

ataka

3.3

Punja

b 4.1

Punja

b 4.2

Punja

b 4.3

Andh

ra P

rade

sh 2

Uttar

Pra

desh

2Te

langa

na 1

Andh

ra P

rade

sh 3

prem

ium ov

er lo

wer b

idder

, %

Source: Company data, MNRE, Credit Suisse estimates.

7 November 2016

Azure Power Global Limited (AZRE) 21

Financing—Cost of Debt Continues to DeclineAzure Power's projects are 80-85% levered, and hence cost of debt becomes an important driver in equity returns. We calculate that a 100 bps decline in cost of debt results in ~400 bps higher equity return for projects in the backlog.

Project debt is predominantly sourced from domestic banks, is INR denominated, and is priced a spread on RBI's base rate.

While weighted average interest rate is ~10% today, we expect it will decline in the future due to (1) a general declining trend in RBI's base rate (down 50 bps YTD and down 150 bps since early 2015) and (2) rate compression as lenders get more comfortable with 25-yr fixed cash flows backed by state-owned enterprises and with no commodity fuel price risk; we calculate rate spread of ~4-5% for projects constructed compared with ~3.5% for new term sheets and ~1% spread for NTPC's green bond issued in September 2016 to fund renewable assets.

Figure 32: RBI's Base Rate (Repo Rate) Has Declined 50 bps YTD and 150bps Since Early 2015

Figure 33: Rate Spread Compression Chart

6.00%

6.50%

7.00%

7.50%

8.00%

8.50%

Mar-13 Mar-14 Mar-15 Mar-16

RBI R

EPO

rate latest term

sheet

NTPC green bond

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

quarterly rate spread progression from 2014 to 2016

Source: Company data, Credit Suisse estimates. Source: Company data, Credit Suisse estimates.

7 November 2016

Azure Power Global Limited (AZRE) 22

Figure 34: Unlevered Project Economics SensitivityUnlevered project IRR sensitivity to PPA and cash cost

Capex - cash cost/watt12.9% $ 0.60 $ 0.65 $ 0.70 $ 0.75 $ 0.80

PPA 4.00 15.4% 13.9% 12.7% 11.6% 10.6%INR/kwh 4.25 16.6% 15.0% 13.7% 12.6% 11.5%

4.50 17.8% 16.2% 14.8% 13.5% 12.5%4.75 19.1% 17.3% 15.8% 14.5% 13.4%5.00 20.3% 18.4% 16.8% 15.5% 14.3%5.25 21.5% 19.6% 17.9% 16.4% 15.2%5.50 22.8% 20.7% 18.9% 17.4% 16.1%

*Note - doesn't include VGF, assumes EPC margin of 12% of cost

Unlevered project IRR sensitivity to PPA and VGFVGF INR/watt

12.9% 5.0 6.0 7.0 8.0 9.0PPA 4.00 12.3% 12.5% 12.7% 12.9% 13.1%

INR/kwh 4.25 13.3% 13.5% 13.7% 13.9% 14.2%4.50 14.3% 14.5% 14.7% 15.0% 15.2%4.75 15.3% 15.5% 15.8% 16.0% 16.3%5.00 16.3% 16.5% 16.8% 17.0% 17.3%5.25 17.3% 17.5% 17.8% 18.1% 18.3%5.50 18.3% 18.5% 18.8% 19.1% 19.4%

*Note - assumes system cost of $0.87/w, EPC margin of 12% of cost

Source: Company data, Credit Suisse estimates.

Figure 35: Current Benchmark Tariff with No VGF Requires Project Cash Cost of $0.65/w or LowerUnlevered project IRR sensitivity to VGF and cash cost

Capex - cash cost/watt12.9% $ 0.50 $ 0.55 $ 0.60 $ 0.65 $ 0.70 $ 0.75

VGF $ - - 21.8% 19.4% 17.5% 15.8% 14.5% 13.3%$/w and $ 0.01 1.0 22.3% 19.8% 17.8% 16.1% 14.7% 13.5%

INR/w $ 0.03 2.0 22.7% 20.2% 18.1% 16.4% 14.9% 13.7%$ 0.04 3.0 23.2% 20.6% 18.5% 16.7% 15.2% 13.9%$ 0.06 4.0 23.7% 21.0% 18.8% 17.0% 15.5% 14.1%$ 0.07 5.0 24.2% 21.4% 19.2% 17.3% 15.7% 14.4%$ 0.09 6.0 24.8% 21.9% 19.5% 17.6% 16.0% 14.6%$ 0.10 7.0 25.3% 22.3% 19.9% 17.9% 16.3% 14.8%$ 0.12 8.0 25.9% 22.8% 20.3% 18.2% 16.5% 15.1%$ 0.13 9.0 26.5% 23.2% 20.7% 18.6% 16.8% 15.3%$ 0.15 10.0 27.1% 23.7% 21.1% 18.9% 17.1% 15.6%

VGF $/w VGF INR/w

*Assumes no EPC margin, PPA of 4.43INR/kWh

Source: Company data, Credit Suisse estimates.

7 November 2016

Azure Power Global Limited (AZRE) 23

Earnings Outlook and ValuationKey Metrics

The company focuses on six key metrics: (1) Energy generated (in GWh), representing revenue earning electricity produced in the period; (2) the corresponding utilization or plant load factor (PLF); (3) revenues in the period; (4) average cash cost of system installed in the period reported in $/w; (5) MW operating exiting the period; and (6) MW committed, which represents project bids won/contracted and either in development or yet to be constructed.

Seasonality

We would like to note that Azure Power's revenues are seasonal and much stronger in CQ2/CQ3 quarters (ending June and September) due to higher sunshine in those quarters versus CQ1/CQ4.

FY16 Review (Ending March 2016)

In FY 2016, the company reported total energy generation of 365 GWh (up 184% y/y) and revenues of $39.6m (up 133% y/y). The growth in energy generated and revenues was driven by 230 MW of projects installed in the period (340 MWs operating exiting the period), mainly because Rajasthan 3.1, 3.2, and 3.3; Chhattisgarh 1; Rajasthan 4; and Punjab 3 projects came online in the year. Average PPA tariff for projects operating was $0.09/kWh (down 12% y/y). Total committed projects increased to 625 MWs (from 374 MWs in FY15), mainly because the company won 481 MWs of tenders in the period. PLF was 18.1% in the year and was below 18.7% in FY15 and average PLF of ~20% for projects in the country due to project ramp up in the year. The company reported adjusted EBITDA of $26.6m in the period (up 186% y/y).

C2Q16 Review (Quarter Ending June 2016)

In the June-ending quarter, the company reported 147 GWh of energy generated, total revenues of $15.1m, and implied average PPA tariff of $0.09/kWh. MWs operating increased by 6 MWs to 346 MWs in the quarter, while MWs committed decreased by a similar magnitude to 619 MWs. No new projects were won in the quarter, though the company did win 90 MW of projects in July, which brings the total portfolio to 1050 MWs. PLF of 19.7% was higher in the quarter due to seasonality. The company reported Adj EBITDA of $12m in the period, while we calculate run rate annualized EBITDA of $47m exiting the period.

FY 2017 and 2018 Earnings Outlook

In FY 2017 (ending March 2017), we estimate energy generated to grow to 664 GWh (up 82% y/y), with a PLF of 18.9% and total revenues of $68m (up 71% y/y). We estimate total MWs operational will increase to 750 MWs (up 121% y/y). We estimate annual EBITDA of $51m in the period and a run rate annualized EBITDA of $114m exiting the March 2017 quarter. We estimate diluted EPS of ($0.46).

In FY 2018 (ending March 2018), we estimate energy generated to grow to 1,559 GWh (up 135% y/y), with a PLF of 20.1% and total revenues of $138m (up 103% y/y). We forecast total operational portfolio to grow to 1.2 GWs. We estimate annual EBITDA of 120m in the period and a run rate EBITDA of $160m exiting the March 2018 quarter. We estimate diluted EPS of $0.64 (up 240% y/y).

CY 2017 and 2018 Earnings Outlook

In CY 2017 (ending December), we estimate energy generated to grow to 1,336 GWh (up 149% y/y), with a PLF of 20% and total revenues of $122m. Total projects operational will increase to 1,025 MWs. We estimate annual EBITDA of $105m in the period and a run rate EBITDA of $138m exiting 2017. We estimate diluted EPS of $0.49.

7 November 2016

Azure Power Global Limited (AZRE) 24

In CY 2018 (ending December), we estimate energy generation of 2,214 GWh (up 66% y/y), with a PLF of 20.2% and total revenues of $186m (up 53% y/y). We forecast total MWs operational to increase to 1,025 MWs. We estimate annual EBITDA of $165m in the period and a run rate EBITDA of $179m exiting 2018. We estimate diluted EPS of $1.25 (up 152% y/y).

Liquidity

The company had a cash balance of $46m in June 2016 and $172m post the IPO after including $25m from IFC-GIF investment, $75m from private placement with CDPQ, and $26.3m of net proceeds from primary offering (ex shoe).

We forecast that, with a 82% debt leverage on new projects, the company can fund 1 GW of installed capacity exiting CY17, 1.35 GW exiting CY18, and 1.5 GW exiting CY19 with a conservative cash low point of $60m.

Figure 36: AZRE Earnings Model and Key Operating MetricsINCOME STATEMENT & KEY METRICS FY15A FY16A FY17E FY18E FY19E FY20E CY17E CY18E CY19ERevenues $ 17.0 $ 39.6 $ 68 $ 138 $ 195 $ 214 $ 122 $ 186 $ 211

Project Cash Operating Expenses $ 2.8 $ 4 $ 7 $ 11 $ 12 $ 6 $ 10 $ 12D&A $ 10.4 $ 18 $ 33 $ 43 $ 47 $ 29 $ 42 $ 46

Total Cost of Energy Sales $ 13 $ 22 $ 40 $ 54 $ 59 $ 35 $ 52 $ 58Gross Profit $ 26.4 $ 46 $ 98 $ 141 $ 156 $ 87 $ 134 $ 153

Gross Margin % 66.7% 68.3% 70.9% 72.3% 72.6% 71.0% 72.1% 72.6%Operating Expenses $ 10.2 $ 13 $ 10 $ 12 $ 13 $ 10 $ 12 $ 13

Memo: Total operating cash costs $ 13.0 $ 17 $ 18 $ 23 $ 25 $ 17 $ 22 $ 25EBITDA $ 9.3 $ 26.6 $ 51 $ 120 $ 172 $ 189 $ 105 $ 165 $ 186

Operating Income (EBIT) $ 16.2 $ 33.2 $ 87.1 $ 128.9 $ 142.6 $ 76 $ 123 $ 140(-) Net Int expense $ (30.5) $ (41) $ (62) $ (74) $ (74) $ (55) $ (73) $ (75)memo: Net interest rate 9.7% 7.4% 7.8% 8.9% 9.1% 7.3% 8.9% 9.0%

FX Loss/Gain $ (5.1) $ (7) $ - $ - $ - $ (1) $ - $ -Profit Before Tax (PBT) $ (19.4) $ (14.1) $ 25.4 $ 54.6 $ 68.6 $ 20 $ 50 $ 65Income tax benefit (expense) $ (4.9) $ 4.0 $ (8.6) $ (18.6) $ (23.3) $ (7) $ (17) $ (22)

Memo: Effective Tax rate (25.1)% 28.0% 34.0% 34.0% 34.0% 34.0% 34.0% 34.0%NCI $ (0.1) $ (0.3) $ (0.3) $ (0.3) $ (0.3) $ (0.3) $ (0.3) $ (0.3)Net Income / (Loss) $ (16.4) $ (24.5) $ (10.5) $ 16.8 $ 36.1 $ 45.3 $ 13 $ 33 $ 43

EPS diluted $ (0.46) $ 0.64 $ 1.37 $ 1.73 $ 0.49 $ 1.25 $ 1.65Basic share count, mm 22.4 25.9 25.9 25.9 25.9 25.9 25.9Diluted share count, mm 19.5 19.5 22.7 26.2 26.2 26.2 26.2 26.2 26.2

Key Operating Metrics FY15A FY16A FY17E FY18E FY19E FY20E CY17E CY18E CY19EEnergy generated, GWh 128 365 664 1,559 2,327 2,603 1,336 2,214 2,549Plant load factor (utillization) 18.7% 18.1% 18.9% 20.1% 20.3% 20.3% 20.0% 20.2% 20.3%Revenues, $mm $ 17.0 $ 39.6 $ 68.0 $ 137.7 $ 194.8 $ 214.5 $ 122 $ 186 $ 211Total system cost $/w $ 0.85 $ 0.91 $ 0.74 $ 0.69 $ 0.64 $ 0.58 $ 0.57 $ 0.45 $ 0.49MW Operating 110 340 750 1,200 1,405 1,520 1,025 1,355 1,495MW Committed but not yet built 374 625 265 (185) (390) (505) (10) (340) (480)MW Operating + Committed 484 965 1,015 1,015 1,015 1,015 1,015 1,015 1,015Operating runrate EBITDA, $m $ 114 $ 160 $ 185 $ 198 $ 138 $ 179 $ 195

Source: Company data, Credit Suisse estimates.

7 November 2016

Azure Power Global Limited (AZRE) 25

ValuationOur base-case scenario assumes the company installs and operates 1.35 GW of projects by CY18 (versus the current contracted portfolio of ~1GW) with enough cash buffer to help grow organically at 10%/yr thereafter. We arrive at a target price of $21 by comparing relative multiples for India based IPPs and by comparing equity returns for U.S. projects.

■ Our target price of $21 represents 7.5x our base-case 2018 CY EBITDA of $165m, which is better than the average 2018 EV/EBITDA multiple of 7.3x for India-based thermal IPPs given Azure Power's projects do not carry any fuel price risk, while being exposed to a similar sovereign and counterparty risk

■ Our target price of $21 implies a cost of equity of ~13% on equity cash flows on the contracted backlog. This return profile represents a 5% spread over equity returns of ~7-8% for U.S.-based solar projects, which is in-line with the ~5% country risk premium spread

We also calculate implied equity values under a blue sky scenario (continued growth with easy access to capital markets) and a grey sky scenario (no further project wins and a multiple in-line with thermal generators).

■ In a blue sky scenario, we assume the company grows in-line with demand growth in India (a 50%+ CAGR) and installs 1.8 GW by CY18 and 2.5 GW by CY19. We also assume that the company would be able to raise an additional $200m in equity capital to fund. A 9x EV/EBITDA implies a blue sky value of $36/sh

■ Our grey sky scenario assumes that the company does not grow beyond the current contracted asset base. Our grey sky equity value of $15 implies 7x CY18 EBITDA for the currently contracted portfolio. Our grey sky value also implies a 16% equity discount rate to the present value of contracted project cash flows.

7 November 2016

Azure Power Global Limited (AZRE) 26

Figure 37: Comps Table for Indian IPPs, Indian Renewable Developers, and U.S. YieldCosComps for CY ending December

Local Curr Price Market Cap EV(Local Curr) $m $m CY2016 CY2017 CY2018 CY2016 CY2017 CY2018

Indian IPPAdani Power Ltd ADAN.BO INR 25.40 $ 1,321 $ 8,782 na 20.7x 16.0x 7.7x 7.4x 7.5x 6.5xCESC Ltd CESC.BO INR 585.90 $ 1,166 $ 3,315 12.8x 8.9x 6.8x 7.7x 6.9x 6.0x 5.0xJSW Energy Ltd JSWE.BO INR 62.70 $ 1,543 $ 3,701 9.5x 8.8x 8.2x 6.2x 6.0x 6.1x 3.6xNHPC Ltd NHPC.BO INR 26.25 $ 4,376 $ 6,820 10.5x 9.5x 8.6x 8.2x 7.6x 7.0x 3.0xNTPC Ltd NTPC.BO INR 153.40 $ 18,988 $ 35,290 13.3x 11.9x 10.3x 11.6x 9.9x 8.6x 5.3xReliance Power Ltd RPOL.BO INR 44.10 $ 1,850 $ 6,449 8.6x 8.2x 7.8x 8.6x 8.4x 8.8x 6.2xSJVN Ltd SJVN.BO INR 31.25 $ 1,942 $ 1,909 9.2x 8.9x 9.3x 5.8x 5.8x 6.0x naTata Power Company Ltd TTPW.BO INR 74.65 $ 3,027 $ 9,250 15.7x 12.4x 10.4x 7.8x 7.3x 7.2x 5.3x

Average 11.4x 11.2x 9.7x 8.0x 7.4x 7.2x 5.0x

Indian renewable operatorsSuzlon Energy Ltd SUZL.NS INR 14.35 $ 1,082 $ 2,665 596.2x 13.5x 9.6x 12.0x 9.3x 8.4x 7.1xMytrah Energy Ltd MYT.L GBp 48.63 $ 99 $ 731 2,019.6x 448.8x 356.4x 6.8x 4.9x 4.0x 5.8x

US YieldCosNextera Energy Partners LP NEP USD 27.00 $ 1,464 $ 5,599 24.4x 18.6x 16.4x 8.8x 6.7x 5.4x 6.5xNRG Yield Inc NYLD.K USD 15.05 $ 2,693 $ 8,176 18.0x 13.8x 12.0x 10.0x 9.1x 8.4x 6.7x8Point3 Energy Partners LP CAFD.O USD 15.03 $ 1,188 $ 1,882 16.8x 22.4x 14.5x 28.6x 18.7x 13.8x 10.5xPattern Energy Group Inc PEGI.O USD 21.30 $ 1,835 $ 4,409 na 95.4x 53.5x 14.5x 11.7x 10.1x 8.5xTerraForm Power Inc TERP.O USD 11.41 $ 1,592 $ 4,822 52.6x 26.2x na 9.3x 9.2x na 6.2xTerraForm Global Inc GLBL.O USD 3.70 $ 659 $ 1,346 19.0x 14.4x na 7.2x 6.0x 5.7x 3.7x

Average 26.2x 31.8x 24.1x 13.1x 10.2x 8.7x 7.0x

US SolarFirst Solar Inc FSLR.O USD 34.51 $ 3,532 $ 2,229 7.8x 17.6x 12.4x 3.8x 5.1x 3.9x (2.2)xSunPower Corp SPWR.O USD 6.40 $ 884 $ 2,664 21.3x 13.7x 6.2x 8.8x 7.5x 6.0x 5.9x

Average 14.5x 15.6x 9.3x 6.3x 6.3x 4.9x

Azure Power Global Ltd AZRE.N USD 16.92 $ 438 $ 920 na 46.0x 14.2x 20.5x 8.9x 5.8x 10.7x

* Multiples based on current EV

EV/EBITDAP/E NetDebt / CY16 EBITDA

Source: Company data, Thomson Reuters, Credit Suisse estimates.

7 November 2016

Azure Power Global Limited (AZRE) 27

Investment RisksSeasonality and lumpiness:

We note potential volatility around quarterly earnings due to seasonality and project lumpiness. Solar energy generation is higher in CQ2/CQ3 quarters and lower in CQ4/CQ1 quarters (up to 30-40% difference) which results in significant volatility around quarterly revenue numbers. Also, the inherent lumpiness of large-project development could make it difficult to correctly estimate quarterly earnings.

Currency Risk

The company is exposed to FX risk since all of the revenues and operating costs are in Indian rupees, but solar modules are priced in USD (which is ~50% of total capex). Also, 28% of current debt is USD denominated. Investors are directly exposed to FX risk since the company's reporting currency is INR, while the stock is listed in the United States and is priced in USD. The INR has depreciated 6% in the past year and average of 8.7%/yr in the past five years against the USD.

At the project level, every 5% depreciation in INR versus the USD reduces unlevered project returns by 50bps.

Interest Rate Risk

Earnings are exposed to interest rate variation, as the majority of existing debt (72% of total) is floating and priced at a spread to RBI's base rate (REPO rate), which had increased by 75 bps in 2013-14 but has declined ~150bps since early 2015. However, a floating interest rate gives the company the option to take advantage of declines in base rates and spread compression as banks get more comfortable with solar projects.

A 0.5% point increase in interest rate for projects in the backlog reduces project equity returns by 2.3% (and vice versa).

Figure 38: FX Volatility Figure 39: RBI Repo Rate

30

35

40

45

50

55

60

65

70

75

Jul-0

6

Jul-0

7

Jul-0

8

Jul-0

9

Jul-1

0

Jul-1

1

Jul-1

2

Jul-1

3

Jul-1

4

Jul-1

5

Jul-1

6

USD/

INR

6.00%

6.50%

7.00%

7.50%

8.00%

8.50%

Mar-13 Mar-14 Mar-15 Mar-16

RBI R

EPO

rate

Source: Company data, Credit Suisse estimates. Source: RBI, Credit Suisse estimates.

7 November 2016

Azure Power Global Limited (AZRE) 28

Future Growth Depends on Ability to Win Bids Amid Competitive Pressures

The company has been successful at winning bids at 14-16% unlevered returns without being the lowest cost bidder in the past. However, sustaining future project returns above threshold levels of low-mid teens could be difficult given strong competition. Limited barriers to entry have resulted in a growing competition from traditional IPPs, conglomerates, and international project developers that could bid at lower returns either driven by irrational expansion strategy or access to lower cost of capital. We have seen such behavior in the recent past when SunEdison emerged as the lowest cost bidder in >1 GW of projects and was driven by the assumption of access to lower cost capital from YieldCos capital.

Curtailment and Counterparty Risk

Azure Power has not reported any curtailments by PPA offtakers to date and has deliberately tried to avoid signing PPAs with state electricity boards with lower credit scores or higher instances of curtailments (e.g., Rajasthan, Maharashtra, and Tamil Nadu). Contracts with the central government-backed entities represent 49% of total MWs (NTPC and SECI—AAA/AA rated), while states represent 48% of projects (>BB+ rated).

Every 5% of energy curtailed through the life of the project results in a 1% point reduction in unlevered project IRR.

Figure 40: Higher Exposure to Federal Govt-Owned Entities or States with Better Credit Ratings

Counterparty MWs as % of total Credit rating INR/kWh $/kWhNTPC 292 29.0% AAA 5.48 $ 0.08Punjab state 222 22.1% BB+ 6.20 $ 0.09SECI 198 19.7% AA 4.99 $ 0.07Karnataka state 150 14.9% BBB+/B- 6.94 $ 0.10AP state 50 5.0% BB 5.89 $ 0.09Chhattisgarh state 30 3.0% A 6.45 $ 0.10Gujarat state 10 1.0% A+ 15.00 $ 0.22UP state 10 1.0% 8.99 $ 0.13Bihar state 10 1.0% 8.39 $ 0.13Ordinance factory 7 0.7% 5.36 $ 0.08Rooftop 26 2.6% n/a n/aTotal 1,005 5.82 $ 0.09

Wt avg PPA

Source: Company data, CRISIL, Care ratings, Fitch ratings, ICRA, Credit Suisse.

Policy Risk

While solar projects are economic on an LCOE basis, the primary driver of solar demand in the country still remains the federal government's policy to achieve 100 GW of solar capacity by 2022 under the national solar mission. The government could lower its solar target if integrating solar electricity in the grid becomes difficult due to a decentralized higher day time peak generation.

We see limited risks to retroactive changes to PPA contracts since the projects were won under a transparent reverse bid process and are already very low (unlike in Spain or Italy in 2010-2012 where the governments retroactively reduced FiTs that were very high, funded by tax payers, and did not factor in sharp decline in panel prices).

7 November 2016

Azure Power Global Limited (AZRE) 29

AppendixCompany ManagementAzure Power was founded in 2008 by CEO Inderpreet Wadhwa. Relevant management team members are detailed in Figure 41.

Figure 41: Company Management OverviewName Position Age Bio

Inderpreet Singh Wadhwa CEO 43

Mr. Inderpreet Wadhwa founded Azure Power in 2008 and has since served as the company's CEO and Director. He has served as VP or Loyalty Lab, and a Sr Director at Oracle. He graduated from Haas School of Business at the University of California Berkeley in 2002. He owns 1.76m shares or 6.8% of total outstanding shares.

Harkanwal Singh Wadhwa COO 71

Mr. Harkanwal Singh Wadhwa has been the company's COO and Director since Nov 2008 and is responsible for government relationships and internal operations of the company. Previously, he has served as Chief MD of National Insurance Company (a state-owned non-life insurance organization). He has 40 years of experience in financial services industry in India.

Surendra Kumar Gupta CFO 63

Mr. Gupta is the CFO of Azure Power since May 2011. Previously, My Gupta has served as the CFO of Al-Suwaidi Holding Company from 2007 to 2010, a Saudi Arabia-based EPC and maintenance company in the oil&gas industry. He has 37+ years of international and domestic experience handling strategic business planning, managing business operations, and corporate finance. He has a Bachelor's degree in Commerce from Delhi University and is a certified Chartered Accountant.

Preet Sandhu Sr VP Construction 47Mr. Preet Sandhu has served as the Sr VP of construction since 2010 where he manages engineering and construction of Azure's projects. He has 19 years of experience in civil construction and project development in transportation, energy, and land development.

Sandeep Chopra CEO Rooftop Business 43Mr. Sandeep Chopra heads the company's rooftop solar business since 2016 and has previously served as the company's head of strategy and supply chain management in 2013-2016. He has 15 years of global experience in process re-engineering, project management, and finance.

Mohor Sen Sr VP HR 66

Mr. Mohor Sen heads HR at Azure since 2014 and has provided consulting services to the company in 2013-14. He has 40 years of experience working and consulting for corporations in project management, human resources, organizational development and strategic communications. He has a Bachelor's degree in technology from IIT Delhi, and Master's of Science from University of Manchester, UK.

Glen Minyard Sr VP R&D 61

Mr. Glen Minyard serves as the company's Sr VP of R&D since September 2010. Previously he was the president of US-based Minyard Solar Electric from 2001 to 2014, and engineering and production manager at NREL from 1992 to 2001. He has 35years of experience in the solar industry and has participated in the design and construction of over 5000 solar power plants globally. He received his associate degree in Electronic Technology from College of the Redwoods, California and is a Certified CA Electrical Contractor.

Source: Company data, Credit Suisse estimates.

7 November 2016

Azure Power Global Limited (AZRE) 30

Management CompensationManagement compensation is comprised of a fixed salary and additional bonuses based on performance. In addition, the executives and board members have also been allocated stock options, which vest annually over a four-year period from the date of grant.

Figure 42: Company Management PayFY16

Name Salary Bonus eligigble Total Cash Total cash growth y/yInderpreet Singh Wadhwa CEO $ 298,507 $ 149,254 $ 447,761 $ 199,003 125.0%Harkanwal Singh Wadhwa COO $ 170,569Preet Sandhu VP Construction $ 118,887 $ 15,299 $ 134,186 $ 105,385 27.3%Surendra Kumar Gupta CFO $ 132,281 $ 18,393 $ 150,674 $ 127,528 18.2%Sandeep Chopra CEO Rooftop $ 139,043 $ 28,340 $ 167,383 $ 148,219 12.9%Mohor Sen VP HR $ 92,934 $ 10,875 $ 103,809 $ 85,328 21.7%Glen Minyard VP R&D $ 204,285 $ 13,477 $ 217,762 $ 222,689 (2.2)%

FY17 agreement

Source: Company data, Assumes USDINR = 67.

Board CompositionThe ten member board is comprised of two company executives (Mr. Indepreet Singh Wadhwa and Harkanwal Singh Wadhwa), two independent members (Rob Kelly, ex-CFO at SCTY, and Arno Harris, the founder of Recurrent Energy), four investor nominated members (William Elmore, nominated by Foundation Capital; Sanjeev Aggarwal, – nominated by Helion Venutre Partners, Barney Rush – nominated by IFC; and one to be nominated by CDPQ), and two Mauritius resident members (to qualify under Mauritius incorporation rules).

We believe the board structure is healthy.

Figure 43: Board Composition

Board of Directors Other positions/experience Audit Compensation IndependentExecutives Inderpreet Singh Wadhwa CEO

Harkanwal Singh Wadhwa COOInvestors William Elmore Nominated by, and co-founder Foundation Capital ✓

Sanjeev Aggarwal Nominated by, and co-founder Helion Venture Partners ✓ ✓ ✓

Barney S. Rush Nominated by IFC, ISO-NE board member ✓ ✓

<TBD> Nominated by CDPQ ✓

Independent Rob Kelly Ex-CFO at SolarCity, Calpine ✓ ✓

Arno Harris Founder Recurrent Energy ✓ ✓

Mauritius resident directorsEric Ng Yim OnMuhammad Khalid Peyrye

Committees

Source: Company data, Credit Suisse estimates.

7 November 2016

Azure Power Global Limited (AZRE) 31

ShareholdersFigure 44: Shareholder Structure and Potential DilutionShareholders Pre-IPO share change Post-IPO ownership %Inderpreet (IW Green) 1,647,952 1,647,952 6.4%DEG 893,025 (388,889) 504,136 1.9%Proparco 1,038,417 (388,889) 649,528 2.5%IFC 2,794,901 (388,889) 2,406,012 9.3%Helion 3,426,173 3,426,173 13.2%FC India 3,667,029 3,667,029 14.1%GIF (includes $25m raised in Sep 2016) 5,189,453 5,189,453 20.0%Others 849,918 849,918 3.3%CDPQ - 4,166,667 4,166,667 16.1%IPO Investors - 3,409,091 3,409,091 13.2%Total sharecount 19,506,868 6,409,091 25,915,959

Potential dilution from options (treasury method)Dilution shares wt strike price proceeds sharesESOP - pre IPO 525,280 $ 7.23 $ 3,797,446 314,311

Potential dilution, shares 314,311

Source: Company data, Credit Suisse estimates.

7 November 2016

Azure Power Global Limited (AZRE) 32

Detailed Financials