Embed Size (px)

Citation preview

Foreword p.3

Section one: Executive summary p.4

Section two: Introduction p.7

Section three: Transport infrastructure p.9

Section four: Transport infrastructureand its effect on business p.20

Section five: Governmenttransport initiatives p.23

Appendix one: Sample profile p.29

Appendix two: Participatingchambers p.30

The British Chambers of Commerce is thenational body for a powerful and influentialNetwork of Accredited Chambers ofCommerce across the UK; a Network thatdirectly serves not only its memberbusinesses, but the wider business community.

Representing 100,000 businesses whotogether employ more than 5 millionemployees, the British Chambers ofCommerce is The Ultimate BusinessNetwork. Every Chamber sits at the veryheart of its local community working withbusinesses to grow and develop by sharingopportunities, knowledge and know-how.

Written and researched by:Gareth Elliott, Policy Adviser

Acknowledgements:Chris Hannant, Head of Policy

The British Chambers of Commerce65 Petty FranceSt. James’s ParkLondonSW1H 9EUTel: 020 7654 5800Fax: 020 7654 5819Email: [email protected]: http://www.britishchambers.org.uk

CONTENTS

Designed and printed by EVC GraphicDesign and Print, Pangbourne, Berkshire,UK, a registered 14001 environmentalprinter. Printed on paper from a managedsustainable source, using pulp that is TCF& ECF, and printed with vegetable soyabased inks.

ABOUTUS

FOREWORD

3

David Frost

Director General

British Chambers of Commerce

Transport is critical to the economy and in a

time of economic downturn it is essential that

our transport networks are up to the task.

Unfortunately, however, the picture that has

been painted by our businesses is one of despair.

Our roads are congested and our railways

cannot cope with the demand placed on them.

Airports have reached their capacity and

passengers and airlines are being forced

elsewhere. The grim result of decades of

underinvestment is that over the last 12 months

the cost of congestion to British business is

£23.2 billion, a staggering rise of £5.7 billion over

the year.

As I have travelled across the country businesses

have told me that the inadequate state of our

transport infrastructure is affecting their ability

to operate. Many firms are finding it difficult to

attract or retain staff due to difficulties in travel

to and from the workplace while delays due to

travel are resulting in missed deadlines. Recent

increases in the price of fuel have only

exacerbated the problem forcing businesses to

raise prices or postpone investments adding

pressure on an already delicate economy.

What this survey highlights is the need for a

long term strategy that is prepared to take

drastic action to improve and upgrade our

dilapidated transport networks. High profile

projects such as the third runway at Heathrow

and a new high speed railway must happen.

Amending the definition of overcrowding on the

railways does nothing to solve the problem

except infuriating already uncomfortable

passengers. Short term schemes such as high

occupancy vehicle lanes or extra rail carriages,

while helpful, are merely sticking plasters which

do nothing to answer the long term problem of

capacity. It is essential we look long term. If our

transport system cannot cope now how do we

expect it to when future projections of

population growth are taken into account? If the

UK is to maintain its position in the world it must

invest in its infrastructure. A first rate country

cannot operate with a third rate network.

INTRODUCTIONTwelve months on from the previous transport

survey and the cost to British business of an

inadequate transport system continues to rise. Our

transport networks are struggling to cope under

the demand. Congestion on the roads, railways

and at our major airports is stifling British

business. It affects companies in several ways, lost

business, recruitment difficulties, wasted time and

above all increased costs. The debate over the

rising price of fuel has highlighted the difficulty

businesses have faced trying to cope. Over the

last 12 months the cost to business of the poor

state of Britain’s infrastructure has risen by a

staggering £5.7 billion pounds to a total of

£23.2bn. This survey highlights the urgent need

for investment in our transport infrastructure. As

the economy begins to slow down transport must

not become a victim of the credit crunch. British

business needs to be able to access a high quality

and efficient transport network in order to access

new and existing markets. Major projects such as

a third runway at Heathrow and a new high speed

railway must not be put to one side but should

be brought forward. Indeed, opportunities for

further public investment during this economic

downturn they should be directed at transport

improvements. However, the government must

plan early. We don’t want to see major projects

trapped in an overly complex planning process

when they are required now.

THE ROAD NETWORKThe road network continues to dominate transport

flows with nearly all businesses using it and three

quarters claiming it is essential. However, as usage

continues to increase, congestion remains the

prime concern of businesses. Over four fifths

claim that congestion locally, regionally and

nationally is a problem. At a local level this is

largely put down to peak time flows such as the

school run but nationally the sheer volume of

traffic is the biggest problem with poor road

design, planning delays and the lack of alternative

transportation adding to the problem. This has

been exacerbated over the last year due to the

high price of oil which has resulted in an increase

in running costs for over five sixths of businesses.

Even as the price of oil has dropped it is likely

that the era of cheap oil is over and will continue

to represent an added cost to business. In a

further blow to the economy many firms have

been forced either to raise prices to cover costs or

have been forced to postpone investment

decisions. Nearly a quarter of businesses surveyed

claimed that they have become less competitive

over the last 12 months due to poor infrastructure.

THE RAIL NETWORKThe railways are reaching critical capacity. Already

the government has been forced to amend its

own definition of overcrowding to shield the true

extent of the problem. Nearly a quarter of

businesses have indicated that they have

increased their usage of the network but this is

due, in part, to rising congestion on the roads.

However, as the railways are stretched businesses

are concerned at the growing expense of using

rail. Over two thirds of businesses rated a

reduction in fares as the most important aspect to

address on the rail network. Punctuality and

reliability still rank high although the inability to

park at stations was rated as the third highest

issue that needs improving. This reflects a

growing unease that congestion is pricing people

off the roads yet subsequent rises in rail fares and

reducing capacity is making rail less attractive. If

the government is to fulfil its policy of modal shift

to public transport it must address these issues.

High Speed Rail was also rated highly by

businesses as a necessary improvement. As

capacity reaches its limits the railway network will

require new infrastructure and a new high speed

rail network will release capacity on the traditional

network while also allowing more freight to be

taken on rail. It is therefore important that the

government considers high speed rail in

association with capacity problems.

THE AIR NETWORKAir transport remains critical to the success of the

UK economy with nine out of ten businesses

claiming they have maintained or increased their

usage of the air network. At a time when

businesses are becoming more internationally

focussed now is not the time to restrict airport

expansion. Two out of every five businesses claim

that Heathrow, the UK’s only major hub airport, is

important to their business operations rising to

three fifths for larger organisations. Capacity

constraints threaten its position and already we

are seeing evidence that businesses are beginning

to look to continental airports in order to conduct

business. Roughly a third of businesses stated that

access to non-UK airports is important, rising to

two in five businesses in the North of England and

Scotland. At a time when the global economic

outlook is so uncertain it is important that we

maintain our international links.

4

SECTIONONE:

EXECUTIVESUMMARY

Capacity constraints at our major airports are also

having negative affects on the passenger

experience. Nearly 40% of businesses stated that

the number one priority for the air transport

network to improve is the management of

passengers. As gateways to the UK it is imperative

that our airports provide an efficient and

exemplary service. The recent debacle following

the opening of Terminal 5 did much to damage

the UK’s reputation as a place to come to or to do

business in.

MOVEMENT OF FREIGHTFreight movement continues to rely heavily on the

road network with almost all businesses using the

road network as opposed to only one in ten who

use rail. The dominance of road continues to be

down to the lack of alternatives that offer the

flexibility, responsiveness and timeliness of road.

Although rail is considered the best alternative to

road its low usage suggests it continues to find it

difficult to compete on a level playing field. The

government has stated that it wants to transfer

freight from road to rail. This survey suggests that

there is more work needed before this can

become a reality. Improvements to rail freight

terminals or extra capacity on the network could

go a long way to making rail freight a practical

reality.

TRANSPORT INFRASTRUCTURE AND ITS EFFECTON BUSINESSThe inadequacies of the transport system are

having serious consequences on the ability of

businesses to operate. Nine out of ten businesses

have experienced increased operating costs while

four fifths claimed a loss of man hours. Over half of

those surveyed stated that they have lost business

or are suffering recruitment difficulties. This all adds

up to a real cost which on average is estimated at

£17,350 per business. On a national scale this

equates to a staggering £23.2 billion pounds, a rise

of £5.7 billion over the last 12 months.

These costs have been exacerbated over the last

year by rising fuel costs. Nearly nine in ten

businesses stated that the price of oil has led to

increased running costs. While a third have passed

this cost on to customers, adding to inflationary

pressures, a quarter have stated that they have

been forced to curtail investment in their

company while a similar amount have found it

difficult to compete.

TRANSPORT INITIATIVES TO COMBATCONGESTIONThe need to upgrade the network is paramount

yet what is clear from this survey is that the

business community remain sceptical about

government initiatives to ease congestion. Just

under half of businesses favoured road widening

and the building of new roads as opposed to

roughly a third who preferred hard shoulder

running or a fifth who indicated a preference for

high occupancy vehicle lanes. Support for some

kind of national road pricing scheme, backed up

by up-front investment in public transport or a

re-evaluation of road user taxation, remained

static reflecting confusion over the government’s

general strategy. However, businesses indicated

that they would resist attempts by government to

raise revenue through business only taxes for

infrastructure improvements.

PLANNINGPlanning remains a major cause of frustration

among businesses. Ninety five per cent believe

that the planning of the UK’s major transport

infrastructure schemes takes too many years to

materialise while nine out of ten agreed that major

transport schemes are too bureaucratic in their

design and implementation. This frustration was

represented by the overwhelming support, four

fifths of all businesses, for the Infrastructure

Planning Commission as proposed in the

government’s Planning Bill. The BCC strongly

supports the Planning Bill’s proposals to reform

the system. In these challenging times, we believe

that the removal of undue barriers on public

investment in infrastructure projects of critical

national importance for our economic and energy

future must be prioritised.

ENVIRONMENTAs the economy worsens it is encouraging to see

that the business community has not lessened its

willingness to take measures to reduce its

environmental impact. Nearly two thirds of those

responding indicated that they had implemented

at least one measure in response to the

environment agenda. Two out of five businesses

had introduced working from home strategies

while a third have implemented IT and e-business

solutions. Reflecting concerns about congestion

and the wishes of employees nearly a third of

businesses have introduced flexi-time or

staggered working hours.

5

SECTIONONE:

EXECUTIVESUMMARY

RECOMMENDATIONS:The UK’s transport infrastructure is still built

around its Victorian foundations. This report

points to the failings and inadequacies of the

transport network and points to the urgent need

for a complete revision of current transport policy.

The BCC recommends that:

� As the economic downturn begins to bite we

urge the government to bring forward public

spending proposals on infrastructure projects

that can quickly release capacity onto our

transport network. Infrastructure investment

will enhance the productivity of all transport

modes and ensure the wheels of the economy

keep on turning.

� A new north-south high speed rail line is

needed as a matter of urgency. The

construction of a truly high speed rail network

will relieve pressure on existing conventional

lines freeing up capacity for freight and

commuter services.

� As an island trading nation the ability of the

UK to access international markets is vital. The

decision on Heathrow’s third runway cannot be

delayed. Heathrow is the UK’s only major hub

airport providing connectivity to the rest of

the world. Without expansion the UK will lose

direct connections and will become a feed-in

airport to European airports. Any expansion

must meet strict environmental criteria.

� Due to the nature of the planning process and

the complicated arrangements between

regional, local and national bodies there are

several important road enhancement projects

that are unnecessarily delayed. We urge the

government to prioritise and fast-track those

projects that offer the best return on

investment.

� The planning system currently takes too long

and is too bureaucratic. It is therefore essential

that the government’s proposals for national

policy statements and an Infrastructure

Planning Commission are implemented in full.

6

SECTIONONE:

EXECUTIVESUMMARY

2.1 BACKGROUNDBritish business requires an effective transport

network. A survey undertaken by the British

Chambers of Commerce (BCC) amongst

Chamber Members in 2007 revealed that the

network is failing British business, and as a result

the economy was suffering.

As things stand, the BCC does not believe that

the government’s attempts to address failings in

the transport system are translating into the

improvements that businesses need to see.

It believes that the reputation of the UK as an

accessible nation and a good place to do

business is being undermined by a woefully

inadequate transport system; the ability of

business to compete in a global market place is

at stake, as are jobs and the future economic

attractiveness of the UK as a vibrant and

competitive economy.

2.2 BUSINESS AND RESEARCH OBJECTIVESThe research objectives of this study are to:

1. Determine usage and relative importance ofroad, rail, sea and air transport;

2. Understand the perceived impact of thecurrent transport infrastructure on business,in terms of business costs, lost opportunities,decisions on business growth and location;and

3. Establish opinion on possible solutions to thetransport problems and issues ofsustainability.

2.3 SAMPLE AND RESPONSE RATEIn all, 48 Accredited Chambers chose to

participate in the study. 40 Chambers provided

data allowing Research by Design Ltd to

automate the initial invitation to participate and

subsequent reminder emails with the remaining

8 supporting the online survey only. Fieldwork

was undertaken between 28th August and

23rd September 2008.

In total 2,675 business members responded to

the 2008 Transport Survey. 2,363 replied to an

invitation to participate in the survey

administered by Research by Design Ltd, and 312

completed a survey administered in-house by

selected Chambers. Appendix 1 provides profile

details of respondents to the survey.

2.4 ANALYSIS AND REPORTINGThis report provides the findings given by the

total sample (all member businesses). It also

provides the findings of sub-groups of the total

sample, defined by number of employees,

business sector, and region/country, where they

are statistically significant compared to the

national picture.

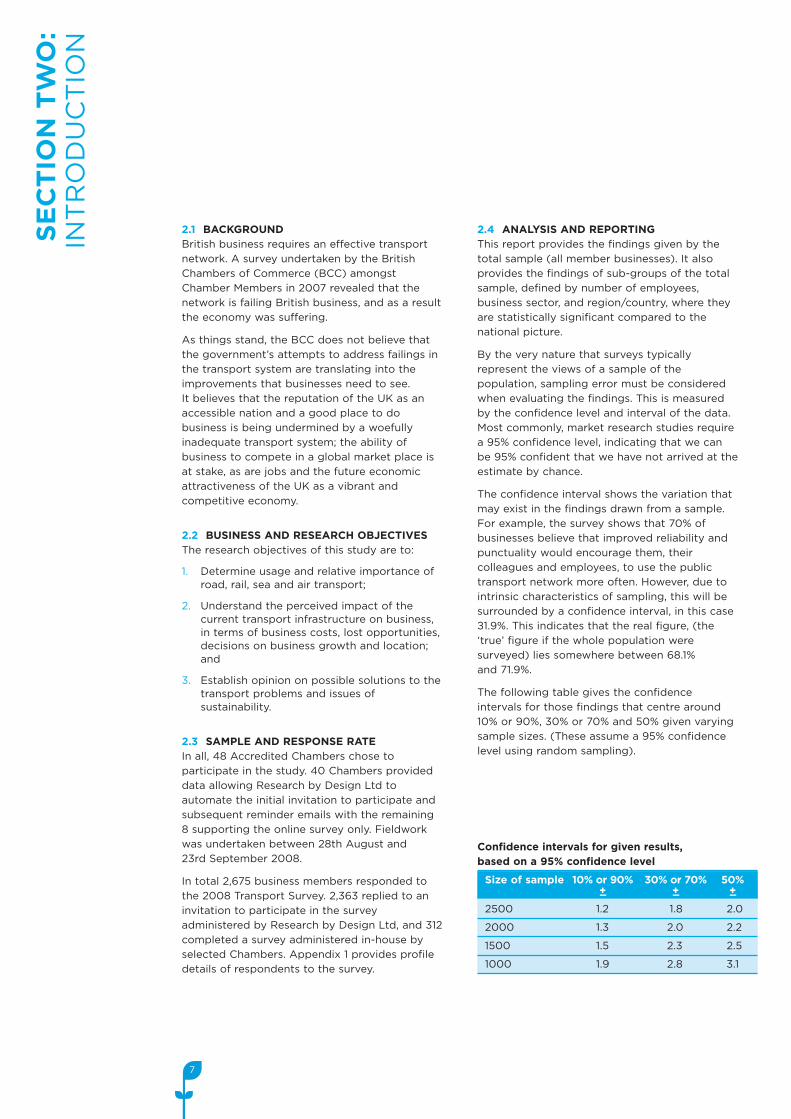

By the very nature that surveys typically

represent the views of a sample of the

population, sampling error must be considered

when evaluating the findings. This is measured

by the confidence level and interval of the data.

Most commonly, market research studies require

a 95% confidence level, indicating that we can

be 95% confident that we have not arrived at the

estimate by chance.

The confidence interval shows the variation that

may exist in the findings drawn from a sample.

For example, the survey shows that 70% of

businesses believe that improved reliability and

punctuality would encourage them, their

colleagues and employees, to use the public

transport network more often. However, due to

intrinsic characteristics of sampling, this will be

surrounded by a confidence interval, in this case

±1.9%. This indicates that the real figure, (the

‘true’ figure if the whole population were

surveyed) lies somewhere between 68.1%

and 71.9%.

The following table gives the confidence

intervals for those findings that centre around

10% or 90%, 30% or 70% and 50% given varying

sample sizes. (These assume a 95% confidence

level using random sampling).

7

SECTIONTWO:

INTRODUCTION

Confidence intervals for given results,based on a 95% confidence level

Size of sample 10% or 90% 30% or 70% 50%+_ +_ +_

2500 1.2 1.8 2.0

2000 1.3 2.0 2.2

1500 1.5 2.3 2.5

1000 1.9 2.8 3.1

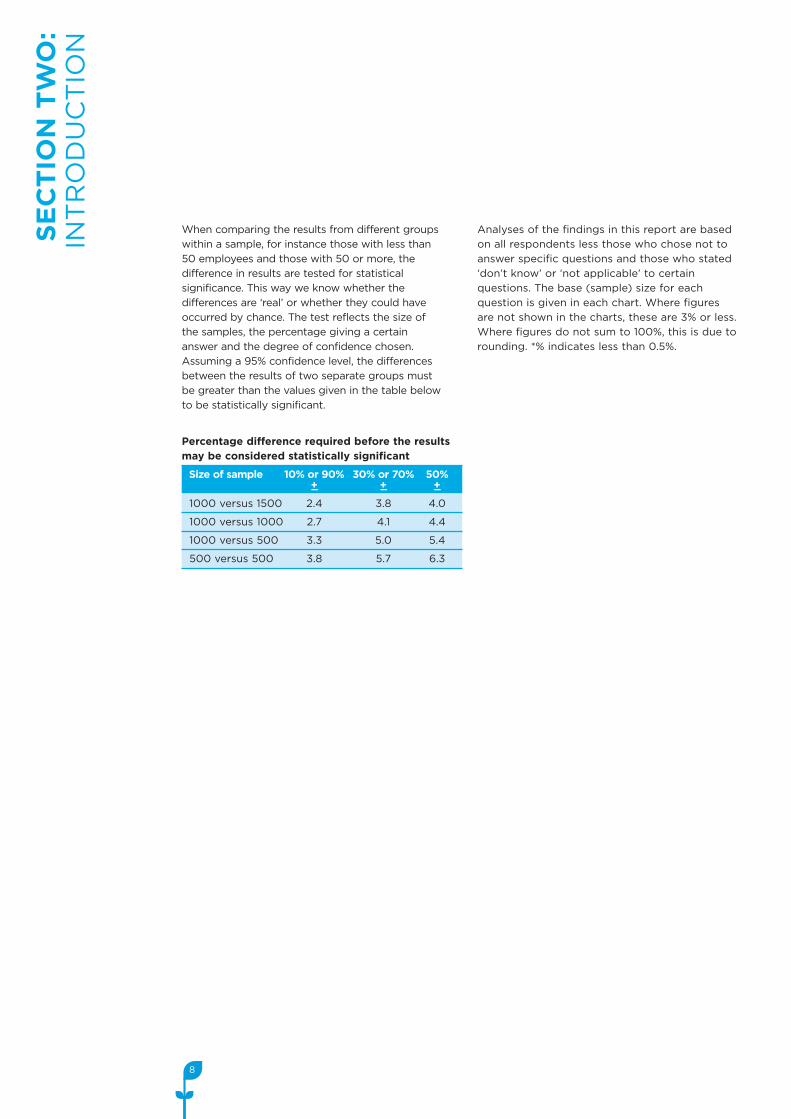

When comparing the results from different groups

within a sample, for instance those with less than

50 employees and those with 50 or more, the

difference in results are tested for statistical

significance. This way we know whether the

differences are ‘real’ or whether they could have

occurred by chance. The test reflects the size of

the samples, the percentage giving a certain

answer and the degree of confidence chosen.

Assuming a 95% confidence level, the differences

between the results of two separate groups must

be greater than the values given in the table below

to be statistically significant.

Analyses of the findings in this report are based

on all respondents less those who chose not to

answer specific questions and those who stated

‘don’t know’ or ‘not applicable’ to certain

questions. The base (sample) size for each

question is given in each chart. Where figures

are not shown in the charts, these are 3% or less.

Where figures do not sum to 100%, this is due to

rounding. *% indicates less than 0.5%.

8

Percentage difference required before the resultsmay be considered statistically significant

Size of sample 10% or 90% 30% or 70% 50%+_ +_ +_

1000 versus 1500 2.4 3.8 4.0

1000 versus 1000 2.7 4.1 4.4

1000 versus 500 3.3 5.0 5.4

500 versus 500 3.8 5.7 6.3

SECTIONTWO:

INTRODUCTION

9

SECTIONTHREE:

TRANSPORT

INFRASTRUCTURE

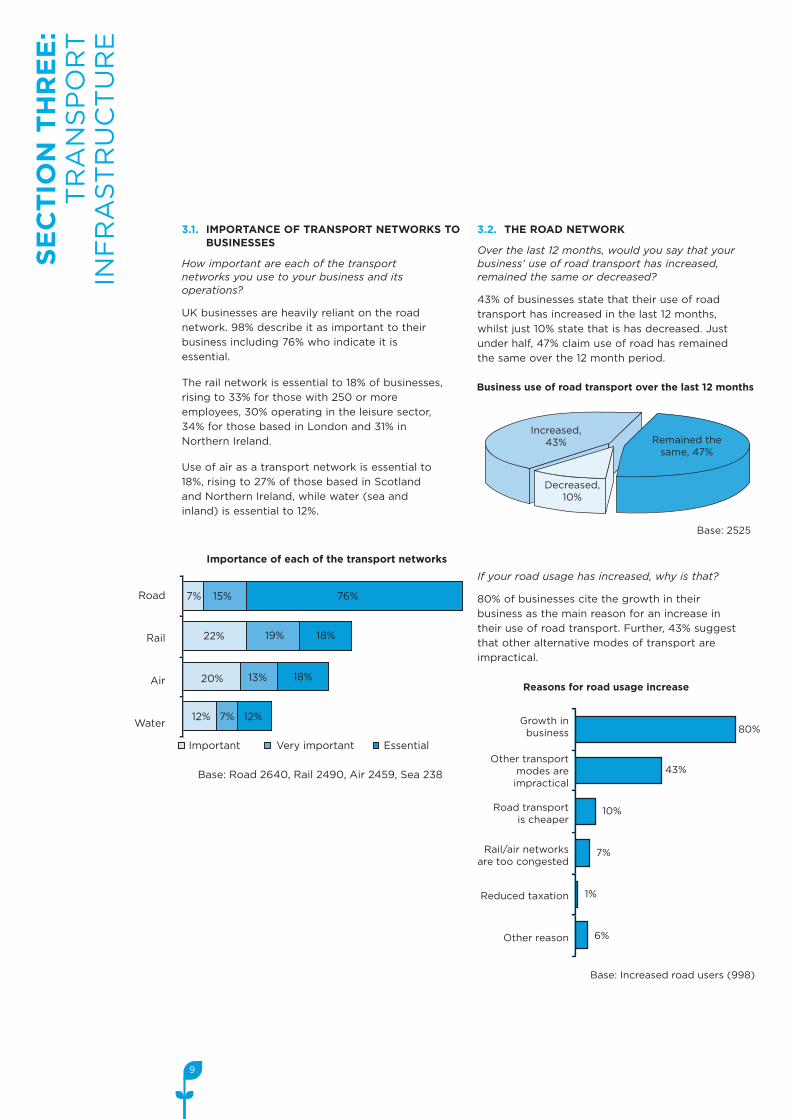

3.1. IMPORTANCE OF TRANSPORT NETWORKS TOBUSINESSES

How important are each of the transportnetworks you use to your business and itsoperations?

UK businesses are heavily reliant on the road

network. 98% describe it as important to their

business including 76% who indicate it is

essential.

The rail network is essential to 18% of businesses,

rising to 33% for those with 250 or more

employees, 30% operating in the leisure sector,

34% for those based in London and 31% in

Northern Ireland.

Use of air as a transport network is essential to

18%, rising to 27% of those based in Scotland

and Northern Ireland, while water (sea and

inland) is essential to 12%.

3.2. THE ROAD NETWORK

Over the last 12 months, would you say that yourbusiness’ use of road transport has increased,remained the same or decreased?

43% of businesses state that their use of road

transport has increased in the last 12 months,

whilst just 10% state that is has decreased. Just

under half, 47% claim use of road has remained

the same over the 12 month period.

If your road usage has increased, why is that?

80% of businesses cite the growth in their

business as the main reason for an increase in

their use of road transport. Further, 43% suggest

that other alternative modes of transport are

impractical.

Road

Rail

Air

Water

Importance of each of the transport networks

Base: Road 2640, Rail 2490, Air 2459, Sea 238

7%

7%

15% 76%

19% 18%

18%13%

22%

20%

12% 12%

Important Very important Essential

Business use of road transport over the last 12 months

Base: 2525

Increased,43%

Decreased,10%

Remained thesame, 47%

Growth inbusiness

Other transportmodes areimpractical

Road transportis cheaper

Rail/air networksare too congested

Reduced taxation

Other reason

Reasons for road usage increase

80%

43%

10%

7%

1%

6%

Base: Increased road users (998)

10

SECTIONTHREE:

TRANSPORT

INFRASTRUCTURE

Fuel costs

Change inbusiness needs

Roadcongestion

Increasedtaxation

Rail ischeaper

Air ischeaper

Otherreason

Reasons for road usage decrease

57%

41%

38%

14%

11%

2%

19%

Base: Decreased road users (238)

Problem of road congestion for business

41%

Base: 2435 2404 2322

A significantproblem

Somewhatof aproblem

Not aproblemat all 15%

Locally Regionally Nationally

45%

40%

44%

46%

46%

39%

15%15% 10%

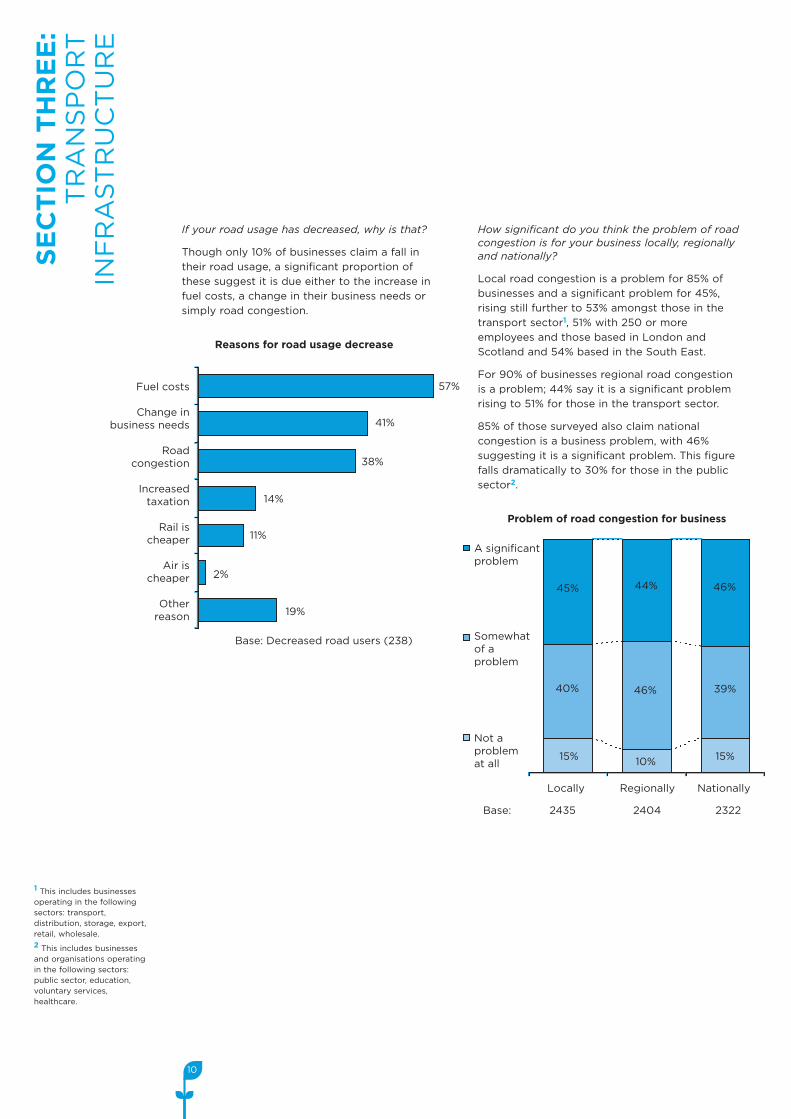

If your road usage has decreased, why is that?

Though only 10% of businesses claim a fall in

their road usage, a significant proportion of

these suggest it is due either to the increase in

fuel costs, a change in their business needs or

simply road congestion.

How significant do you think the problem of roadcongestion is for your business locally, regionallyand nationally?

Local road congestion is a problem for 85% of

businesses and a significant problem for 45%,

rising still further to 53% amongst those in the

transport sector1, 51% with 250 or more

employees and those based in London and

Scotland and 54% based in the South East.

For 90% of businesses regional road congestion

is a problem; 44% say it is a significant problem

rising to 51% for those in the transport sector.

85% of those surveyed also claim national

congestion is a business problem, with 46%

suggesting it is a significant problem. This figure

falls dramatically to 30% for those in the public

sector2.

1 This includes businessesoperating in the followingsectors: transport,distribution, storage, export,retail, wholesale.

2 This includes businessesand organisations operatingin the following sectors:public sector, education,voluntary services,healthcare.

11

SECTIONTHREE:

TRANSPORT

INFRASTRUCTURE

Main causes of congestion

Base: 2401 2291 2211Local roads A roads Motorways87%

23%

3%

52%

75%78%

49%49%

24%

48%53%

47%44%

54%

61%

10% 10%8%

16%

44%46%

Schoolrun

Sheer volumeof traffic

Poor roaddesign &planning

Lack ofalternatives

Poor drivingbehaviour

Roadaccidents

Otherproblems

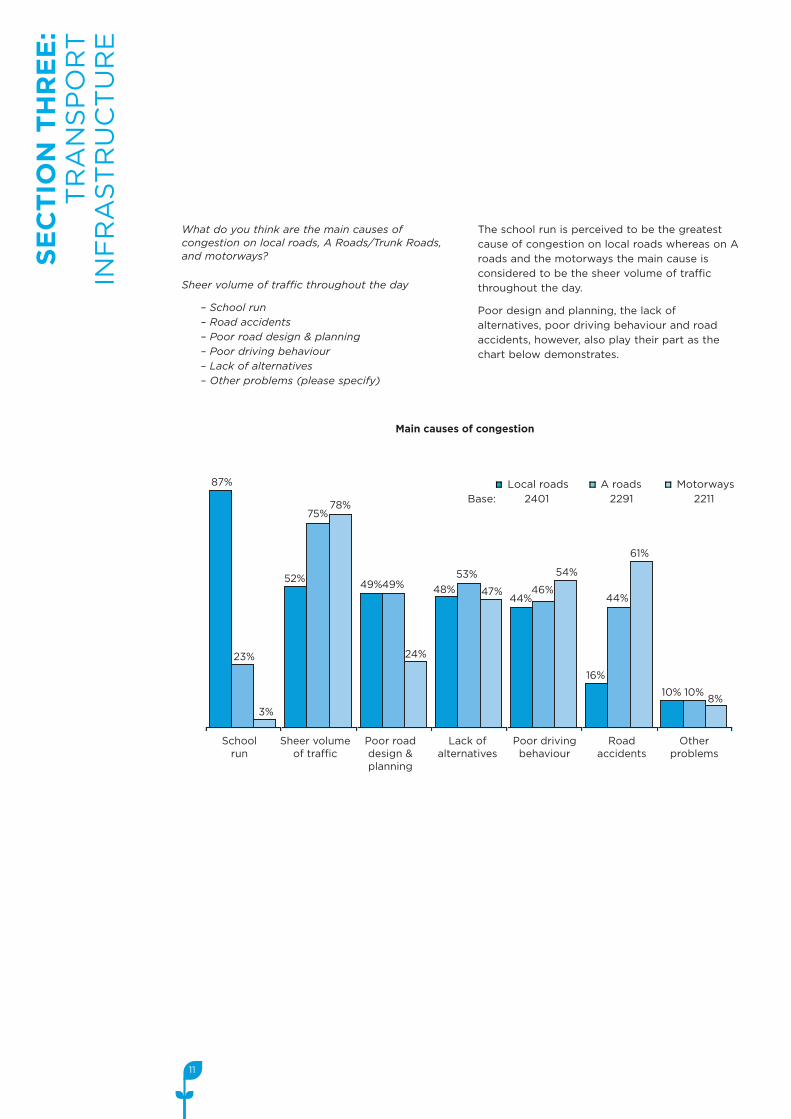

What do you think are the main causes ofcongestion on local roads, A Roads/Trunk Roads,and motorways?

Sheer volume of traffic throughout the day

– School run– Road accidents– Poor road design & planning– Poor driving behaviour– Lack of alternatives– Other problems (please specify)

The school run is perceived to be the greatest

cause of congestion on local roads whereas on A

roads and the motorways the main cause is

considered to be the sheer volume of traffic

throughout the day.

Poor design and planning, the lack of

alternatives, poor driving behaviour and road

accidents, however, also play their part as the

chart below demonstrates.

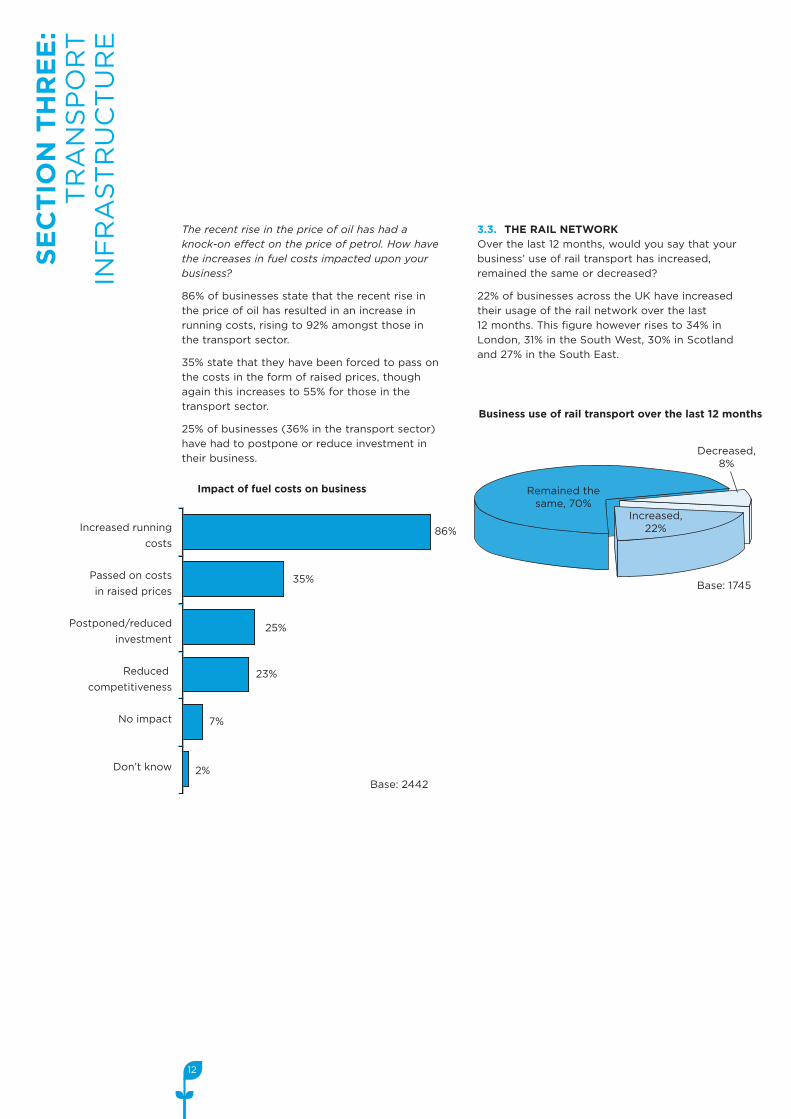

The recent rise in the price of oil has had aknock-on effect on the price of petrol. How havethe increases in fuel costs impacted upon yourbusiness?

86% of businesses state that the recent rise in

the price of oil has resulted in an increase in

running costs, rising to 92% amongst those in

the transport sector.

35% state that they have been forced to pass on

the costs in the form of raised prices, though

again this increases to 55% for those in the

transport sector.

25% of businesses (36% in the transport sector)

have had to postpone or reduce investment in

their business.

3.3. THE RAIL NETWORKOver the last 12 months, would you say that your

business’ use of rail transport has increased,

remained the same or decreased?

22% of businesses across the UK have increased

their usage of the rail network over the last

12 months. This figure however rises to 34% in

London, 31% in the South West, 30% in Scotland

and 27% in the South East.

12

SECTIONTHREE:

TRANSPORT

INFRASTRUCTURE

Increased runningcosts

Passed on costsin raised prices

Postponed/reducedinvestment

Reducedcompetitiveness

No impact

Don’t know

Impact of fuel costs on business

Base: 2442

86%

35%

25%

23%

7%

2%

Business use of rail transport over the last 12 months

Base: 1745

Decreased,8%

Remained thesame, 70%

Increased,22%

SECTIONTHREE:

TRANSPORT

INFRASTRUCTURE

13

Road network istoo congested

Easier accessto city centre

Ability to work on trains

Environmental reasons

Change inbusiness needs

Rail transport is cheaper

Improved schedulingand capacity

Concerns about security at airports

Other

Reasons for rail usage increase

Base: Increased rail users (377)

54%

54%

53%

29%

20%

19%

12%

2%

5%

Poor scheduling

Other transportcheaper

Change inbusiness needs

Other transportless congested

Environmentalreasons

Other

Reasons for rail usage decrease

Base: Decreased rail users (132)

52%

51%

29%

14%

2%

9%

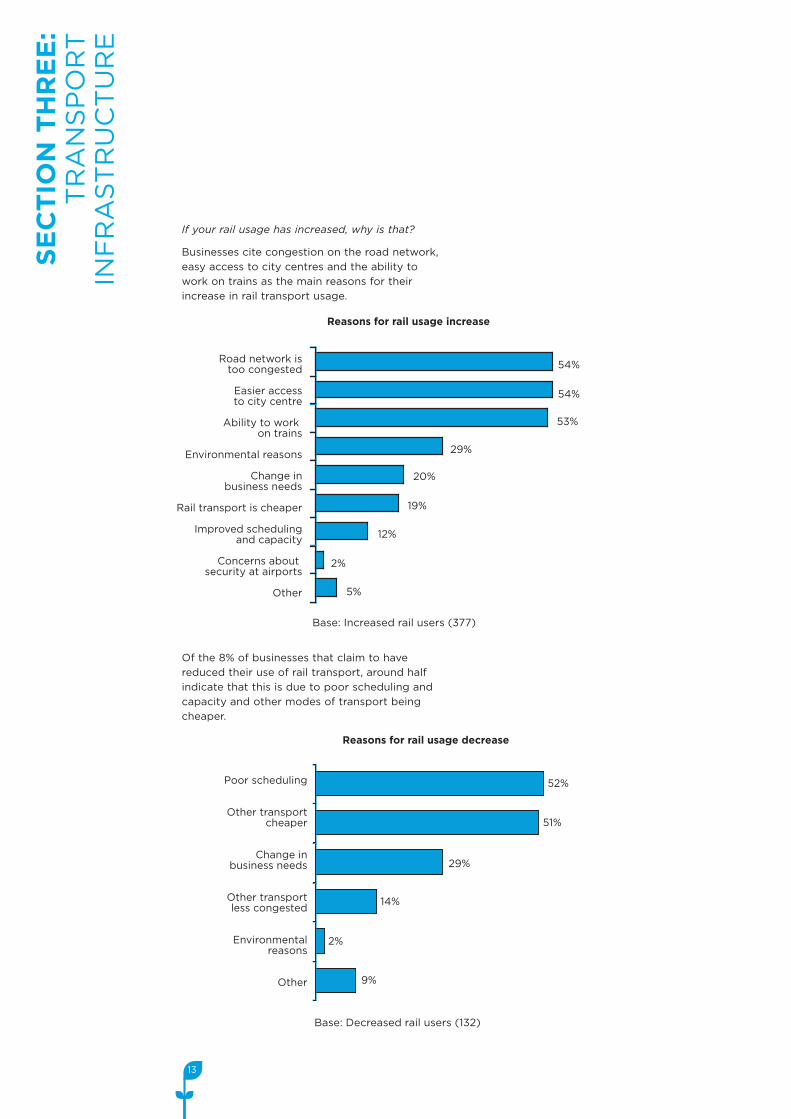

If your rail usage has increased, why is that?

Businesses cite congestion on the road network,

easy access to city centres and the ability to

work on trains as the main reasons for their

increase in rail transport usage.

Of the 8% of businesses that claim to have

reduced their use of rail transport, around half

indicate that this is due to poor scheduling and

capacity and other modes of transport being

cheaper.

14

SECTIONTHREE:

TRANSPORT

INFRASTRUCTURE

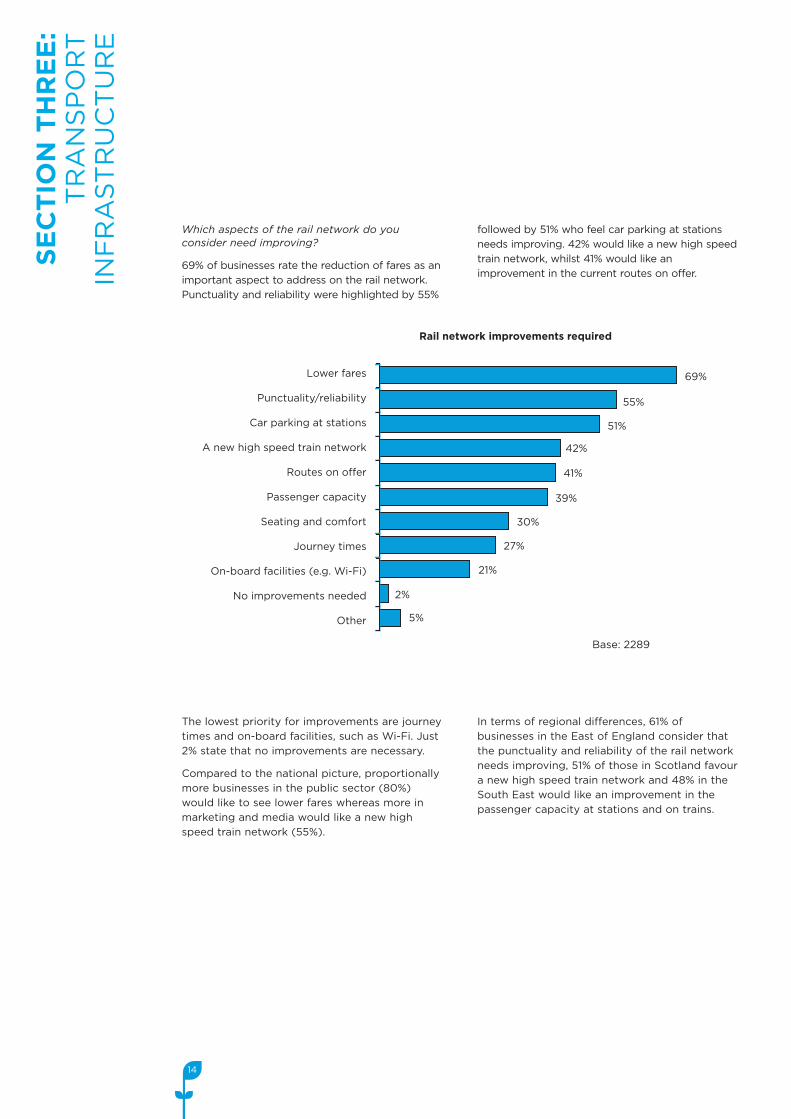

Which aspects of the rail network do youconsider need improving?

69% of businesses rate the reduction of fares as an

important aspect to address on the rail network.

Punctuality and reliability were highlighted by 55%

followed by 51% who feel car parking at stations

needs improving. 42% would like a new high speed

train network, whilst 41% would like an

improvement in the current routes on offer.

The lowest priority for improvements are journey

times and on-board facilities, such as Wi-Fi. Just

2% state that no improvements are necessary.

Compared to the national picture, proportionally

more businesses in the public sector (80%)

would like to see lower fares whereas more in

marketing and media would like a new high

speed train network (55%).

In terms of regional differences, 61% of

businesses in the East of England consider that

the punctuality and reliability of the rail network

needs improving, 51% of those in Scotland favour

a new high speed train network and 48% in the

South East would like an improvement in the

passenger capacity at stations and on trains.

Lower fares

Punctuality/reliability

Car parking at stations

A new high speed train network

Routes on offer

Passenger capacity

Seating and comfort

Journey times

On-board facilities (e.g. Wi-Fi)

No improvements needed

Other

Rail network improvements required

Base: 2289

69%

55%

51%

42%

41%

39%

30%

27%

21%

2%

5%

15

SECTIONTHREE:

TRANSPORT

INFRASTRUCTURE

3.4. THE AIR NETWORK

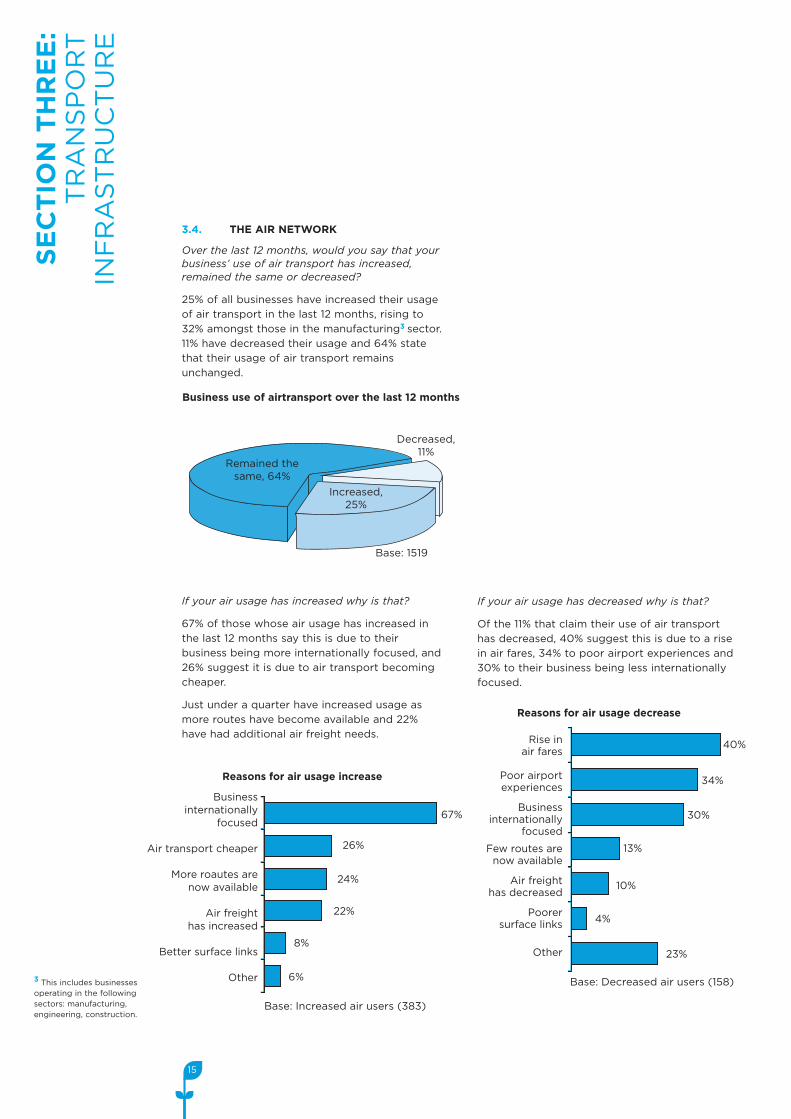

Over the last 12 months, would you say that yourbusiness’ use of air transport has increased,remained the same or decreased?

25% of all businesses have increased their usage

of air transport in the last 12 months, rising to

32% amongst those in the manufacturing3 sector.

11% have decreased their usage and 64% state

that their usage of air transport remains

unchanged.

If your air usage has increased why is that?

67% of those whose air usage has increased in

the last 12 months say this is due to their

business being more internationally focused, and

26% suggest it is due to air transport becoming

cheaper.

Just under a quarter have increased usage as

more routes have become available and 22%

have had additional air freight needs.

Business use of airtransport over the last 12 months

Base: 1519

Decreased,11%

Remained thesame, 64%

Increased,25%

Businessinternationally

focused

Air transport cheaper

More roautes arenow available

Air freighthas increased

Better surface links

Other

Reasons for air usage increase

Base: Increased air users (383)

67%

26%

24%

22%

8%

6%

Rise inair fares

Poor airportexperiences

Businessinternationally

focused

Few routes arenow available

Air freighthas decreased

Poorersurface links

Other

Reasons for air usage decrease

Base: Decreased air users (158)

40%

34%

30%

13%

10%

4%

23%

If your air usage has decreased why is that?

Of the 11% that claim their use of air transport

has decreased, 40% suggest this is due to a rise

in air fares, 34% to poor airport experiences and

30% to their business being less internationally

focused.

3 This includes businessesoperating in the followingsectors: manufacturing,engineering, construction.

Management of

passengers

Punctuality/reliability

Transfer/waiting times

Lower fares

Routes on offer

Seating and comfort

Aspect of air transport considered to need improving the most

Base: 1855 to 1957

1st - Highest priority 2nd 3rd 4th 5th 6th

39% 25% 16% 6% 6% 8%

35% 23% 23% 8% 7% 5%

26% 28% 22% 12% 7% 6%

26% 20% 25% 11% 9% 9%

23% 24% 23% 11% 8% 10%

14% 20% 24% 14% 14% 14%

16

SECTIONTHREE:

TRANSPORT

INFRASTRUCTURE

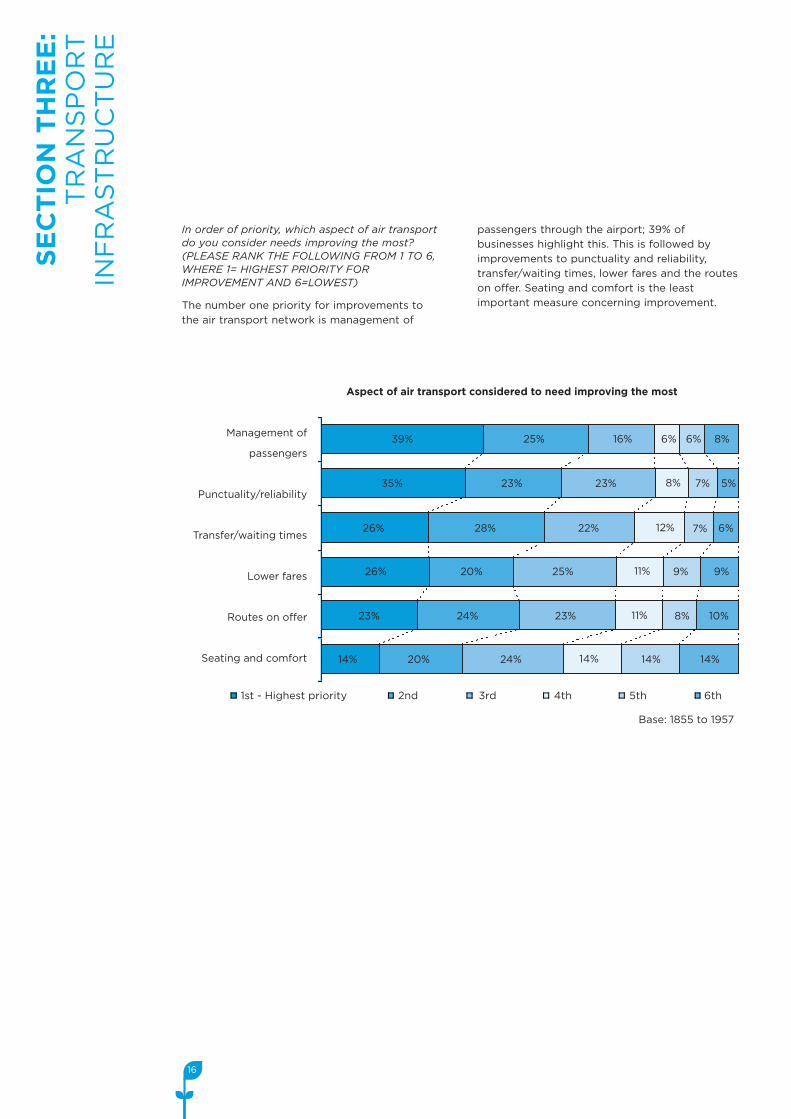

In order of priority, which aspect of air transportdo you consider needs improving the most?(PLEASE RANK THE FOLLOWING FROM 1 TO 6,WHERE 1= HIGHEST PRIORITY FORIMPROVEMENT AND 6=LOWEST)

The number one priority for improvements to

the air transport network is management of

passengers through the airport; 39% of

businesses highlight this. This is followed by

improvements to punctuality and reliability,

transfer/waiting times, lower fares and the routes

on offer. Seating and comfort is the least

important measure concerning improvement.

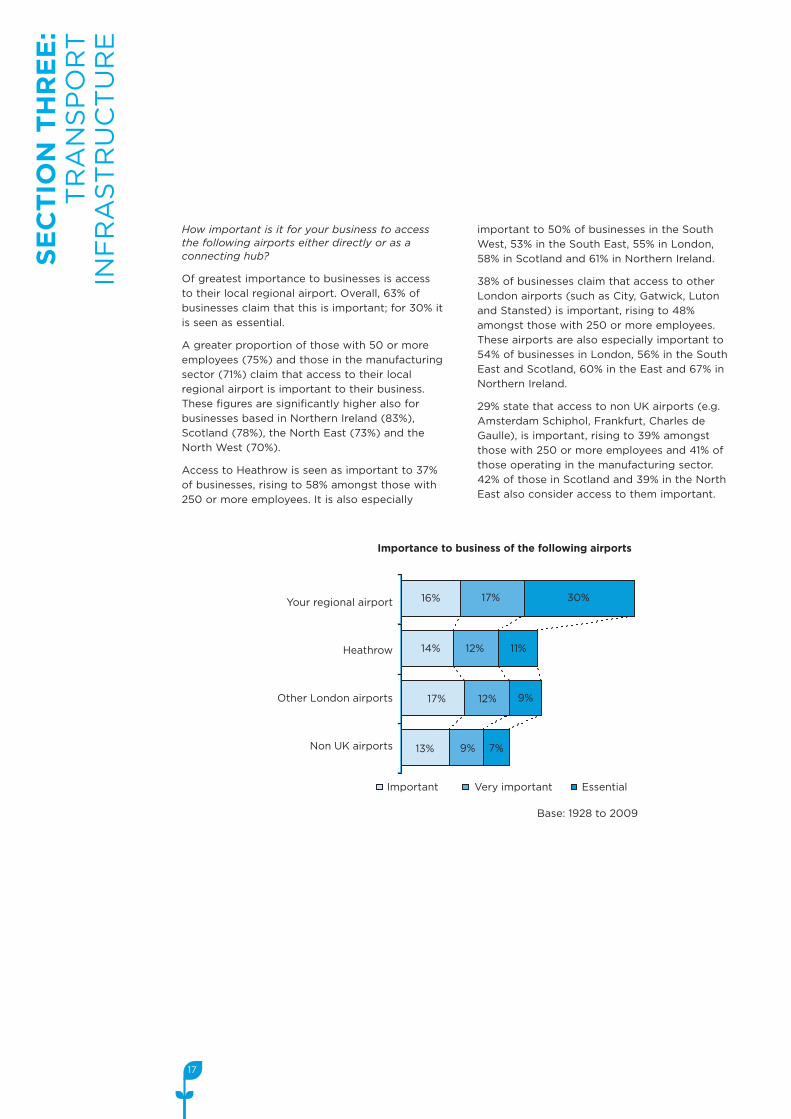

How important is it for your business to accessthe following airports either directly or as aconnecting hub?

Of greatest importance to businesses is access

to their local regional airport. Overall, 63% of

businesses claim that this is important; for 30% it

is seen as essential.

A greater proportion of those with 50 or more

employees (75%) and those in the manufacturing

sector (71%) claim that access to their local

regional airport is important to their business.

These figures are significantly higher also for

businesses based in Northern Ireland (83%),

Scotland (78%), the North East (73%) and the

North West (70%).

Access to Heathrow is seen as important to 37%

of businesses, rising to 58% amongst those with

250 or more employees. It is also especially

important to 50% of businesses in the South

West, 53% in the South East, 55% in London,

58% in Scotland and 61% in Northern Ireland.

38% of businesses claim that access to other

London airports (such as City, Gatwick, Luton

and Stansted) is important, rising to 48%

amongst those with 250 or more employees.

These airports are also especially important to

54% of businesses in London, 56% in the South

East and Scotland, 60% in the East and 67% in

Northern Ireland.

29% state that access to non UK airports (e.g.

Amsterdam Schiphol, Frankfurt, Charles de

Gaulle), is important, rising to 39% amongst

those with 250 or more employees and 41% of

those operating in the manufacturing sector.

42% of those in Scotland and 39% in the North

East also consider access to them important.

17

SECTIONTHREE:

TRANSPORT

INFRASTRUCTURE

Your regional airport

Heathrow

Other London airports

Non UK airports

Importance to business of the following airports

Base: 1928 to 2009

Important Very important Essential

13%

12%

12% 11%

30%

14%

16%

17%

17%

7%9%

9%

18

SECTIONTHREE:

TRANSPORT

INFRASTRUCTURE

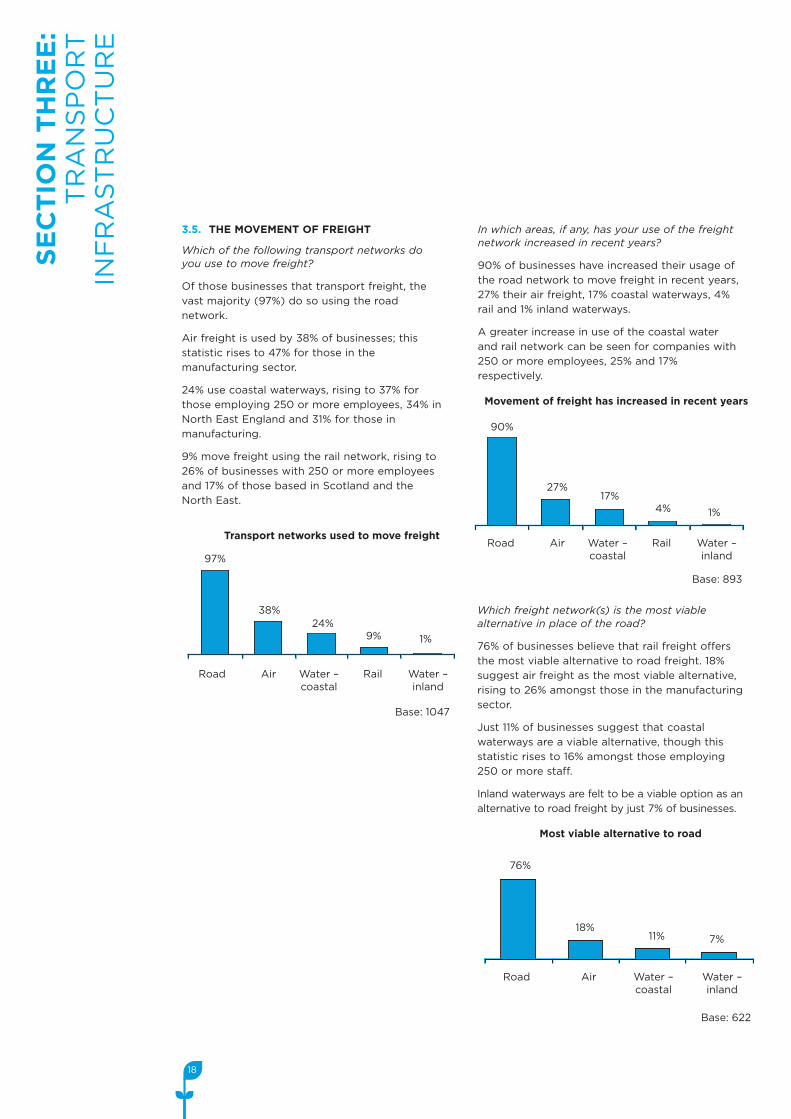

3.5. THE MOVEMENT OF FREIGHT

Which of the following transport networks doyou use to move freight?

Of those businesses that transport freight, the

vast majority (97%) do so using the road

network.

Air freight is used by 38% of businesses; this

statistic rises to 47% for those in the

manufacturing sector.

24% use coastal waterways, rising to 37% for

those employing 250 or more employees, 34% in

North East England and 31% for those in

manufacturing.

9% move freight using the rail network, rising to

26% of businesses with 250 or more employees

and 17% of those based in Scotland and the

North East.

In which areas, if any, has your use of the freightnetwork increased in recent years?

90% of businesses have increased their usage of

the road network to move freight in recent years,

27% their air freight, 17% coastal waterways, 4%

rail and 1% inland waterways.

A greater increase in use of the coastal water

and rail network can be seen for companies with

250 or more employees, 25% and 17%

respectively.

Transport networks used to move freight

M

97%

38%24%

Road Air Water –coastal

Rail Water –inland

9% 1%

1

Base: 1047

B

Movement of freight has increased in recent years

90%

Road Air Water –coastal

Rail Water –inland

R

27%17%

1%4%

Base: 893

Most viable alternative to road

76%

18%11%

Road Air Water –coastal

Water –inland

7%

Base: 622

Which freight network(s) is the most viablealternative in place of the road?

76% of businesses believe that rail freight offers

the most viable alternative to road freight. 18%

suggest air freight as the most viable alternative,

rising to 26% amongst those in the manufacturing

sector.

Just 11% of businesses suggest that coastal

waterways are a viable alternative, though this

statistic rises to 16% amongst those employing

250 or more staff.

Inland waterways are felt to be a viable option as an

alternative to road freight by just 7% of businesses.

19

SECTIONTHREE:

TRANSPORT

INFRASTRUCTURE

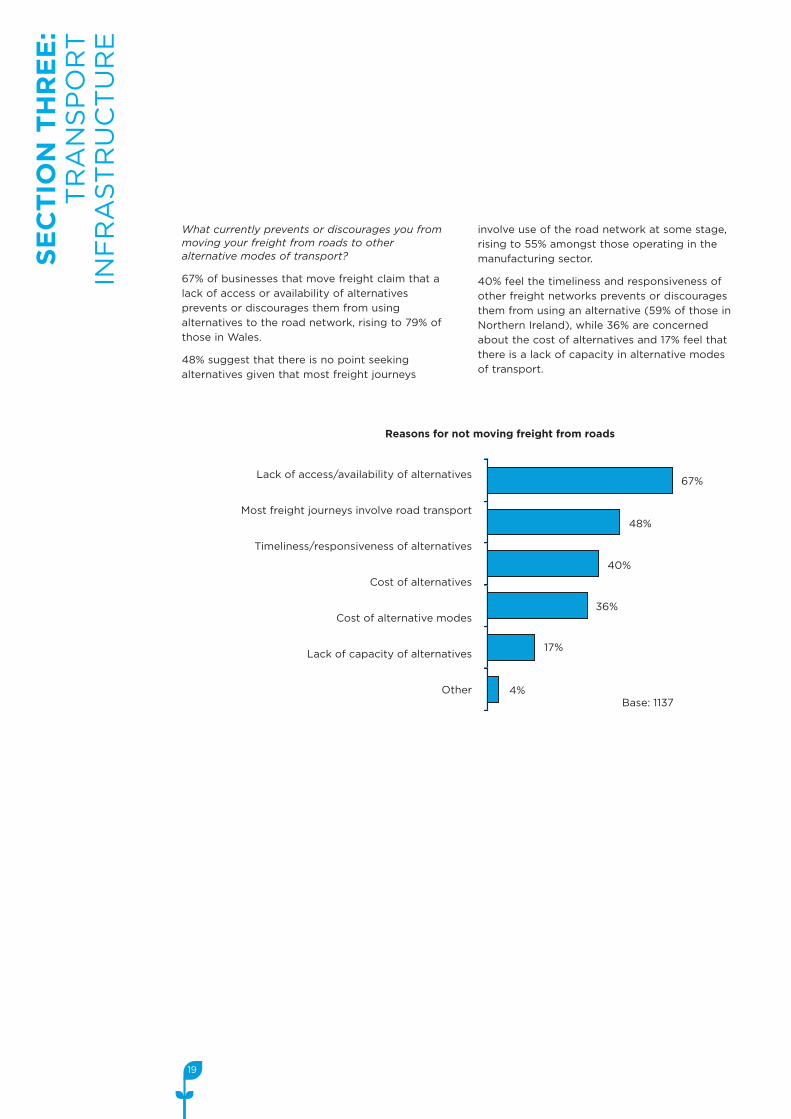

What currently prevents or discourages you frommoving your freight from roads to otheralternative modes of transport?

67% of businesses that move freight claim that a

lack of access or availability of alternatives

prevents or discourages them from using

alternatives to the road network, rising to 79% of

those in Wales.

48% suggest that there is no point seeking

alternatives given that most freight journeys

involve use of the road network at some stage,

rising to 55% amongst those operating in the

manufacturing sector.

40% feel the timeliness and responsiveness of

other freight networks prevents or discourages

them from using an alternative (59% of those in

Northern Ireland), while 36% are concerned

about the cost of alternatives and 17% feel that

there is a lack of capacity in alternative modes

of transport.

Lack of access/availability of alternatives

Most freight journeys involve road transport

Timeliness/responsiveness of alternatives

Cost of alternatives

Cost of alternative modes

Lack of capacity of alternatives

Other

Reasons for not moving freight from roads

67%

48%

40%

36%

17%

4%Base: 1137

20

SECTIONFOUR:

TRANSPORTINFRASTRUCTURE

ANDITSEFFECTONBUSINESS

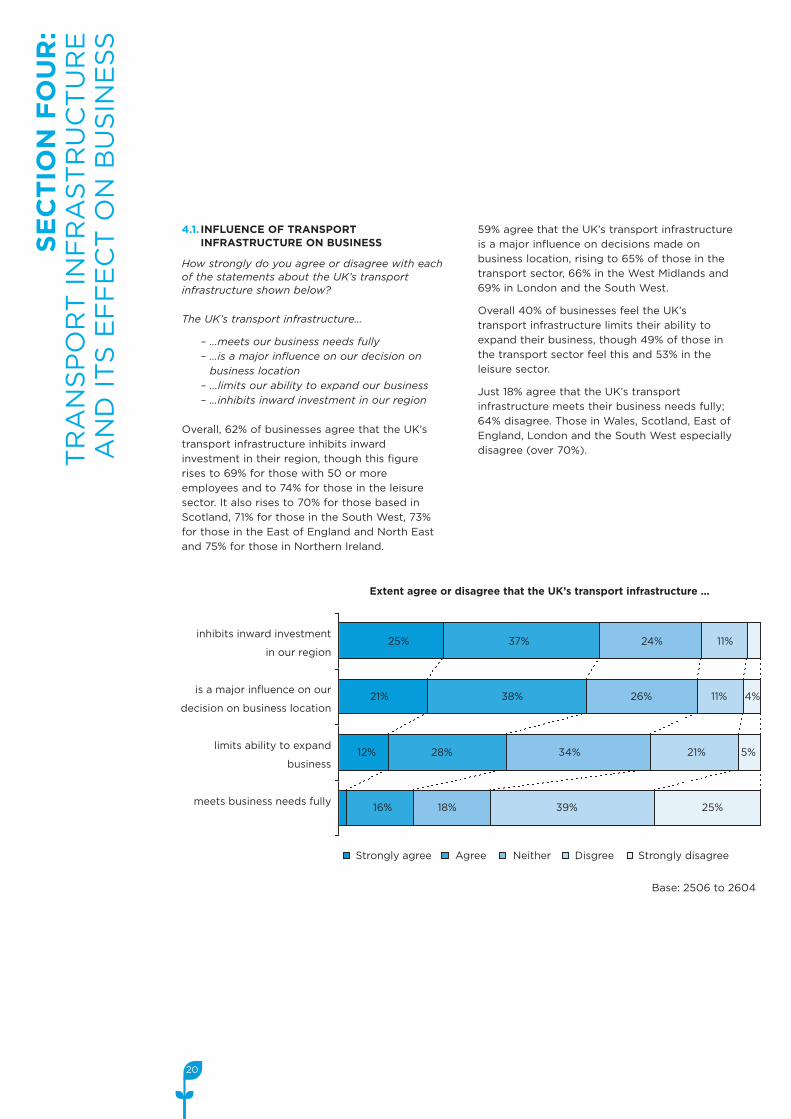

4.1. INFLUENCE OF TRANSPORTINFRASTRUCTURE ON BUSINESS

How strongly do you agree or disagree with eachof the statements about the UK’s transportinfrastructure shown below?

The UK’s transport infrastructure…

– …meets our business needs fully– …is a major influence on our decision onbusiness location

– ...limits our ability to expand our business– …inhibits inward investment in our region

Overall, 62% of businesses agree that the UK’s

transport infrastructure inhibits inward

investment in their region, though this figure

rises to 69% for those with 50 or more

employees and to 74% for those in the leisure

sector. It also rises to 70% for those based in

Scotland, 71% for those in the South West, 73%

for those in the East of England and North East

and 75% for those in Northern Ireland.

59% agree that the UK’s transport infrastructure

is a major influence on decisions made on

business location, rising to 65% of those in the

transport sector, 66% in the West Midlands and

69% in London and the South West.

Overall 40% of businesses feel the UK’s

transport infrastructure limits their ability to

expand their business, though 49% of those in

the transport sector feel this and 53% in the

leisure sector.

Just 18% agree that the UK’s transport

infrastructure meets their business needs fully;

64% disagree. Those in Wales, Scotland, East of

England, London and the South West especially

disagree (over 70%).

inhibits inward investment

in our region

is a major influence on our

decision on business location

limits ability to expand

business

meets business needs fully

Extent agree or disagree that the UK’s transport infrastructure …

Base: 2506 to 2604

Strongly agree Strongly disagreeAgree Neither Disgree

18% 39% 25%16%

28% 34% 21% 5%12%

38% 26% 11% 4%21%

37% 24% 11%25%

21

SECTIONFOUR:

TRANSPORTINFRASTRUCTURE

ANDITSEFFECTONBUSINESS

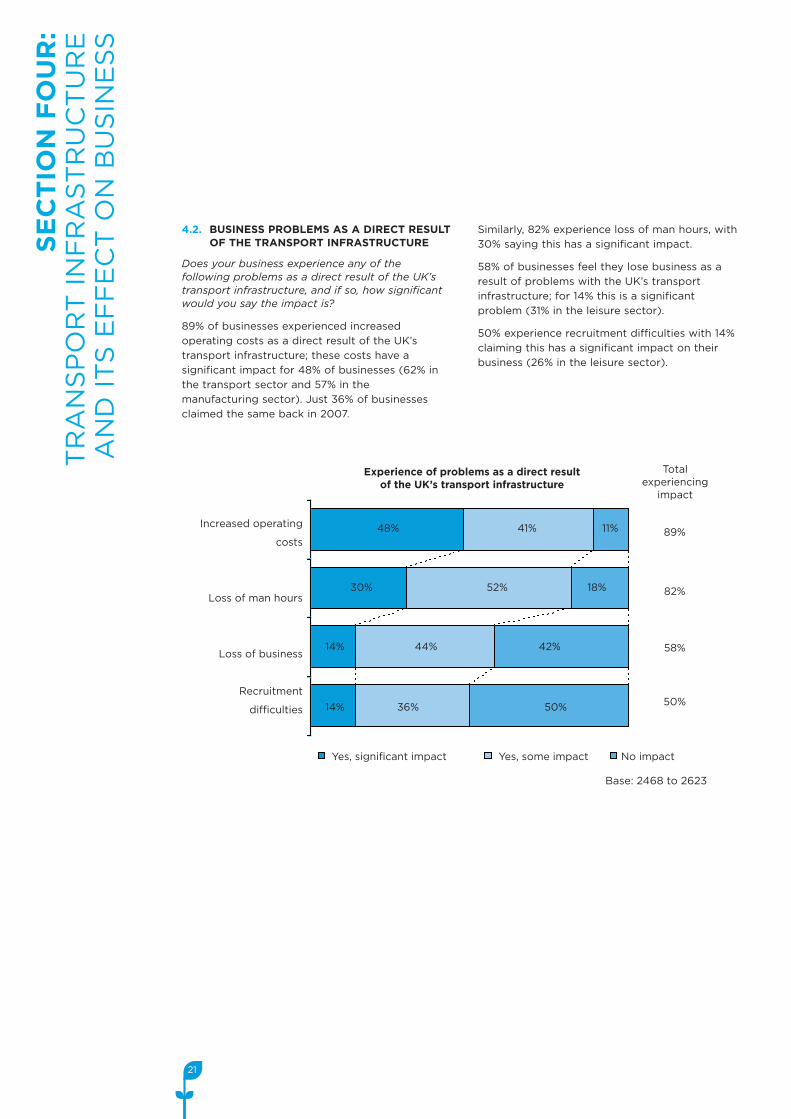

4.2. BUSINESS PROBLEMS AS A DIRECT RESULTOF THE TRANSPORT INFRASTRUCTURE

Does your business experience any of thefollowing problems as a direct result of the UK’stransport infrastructure, and if so, how significantwould you say the impact is?

89% of businesses experienced increased

operating costs as a direct result of the UK’s

transport infrastructure; these costs have a

significant impact for 48% of businesses (62% in

the transport sector and 57% in the

manufacturing sector). Just 36% of businesses

claimed the same back in 2007.

Similarly, 82% experience loss of man hours, with

30% saying this has a significant impact.

58% of businesses feel they lose business as a

result of problems with the UK’s transport

infrastructure; for 14% this is a significant

problem (31% in the leisure sector).

50% experience recruitment difficulties with 14%

claiming this has a significant impact on their

business (26% in the leisure sector).

Increased operating

costs

Loss of man hours

Loss of business

Recruitment

difficulties

Experience of problems as a direct resultof the UK’s transport infrastructure

Base: 2468 to 2623

Yes, significant impact Yes, some impact No impact

Totalexperiencing

impact

89%

82%

58%

50%50%36%14%

14% 44%

48% 41% 11%

52%30% 18%

42%

22

SECTIONFOUR:

TRANSPORTINFRASTRUCTURE

ANDITSEFFECTONBUSINESS

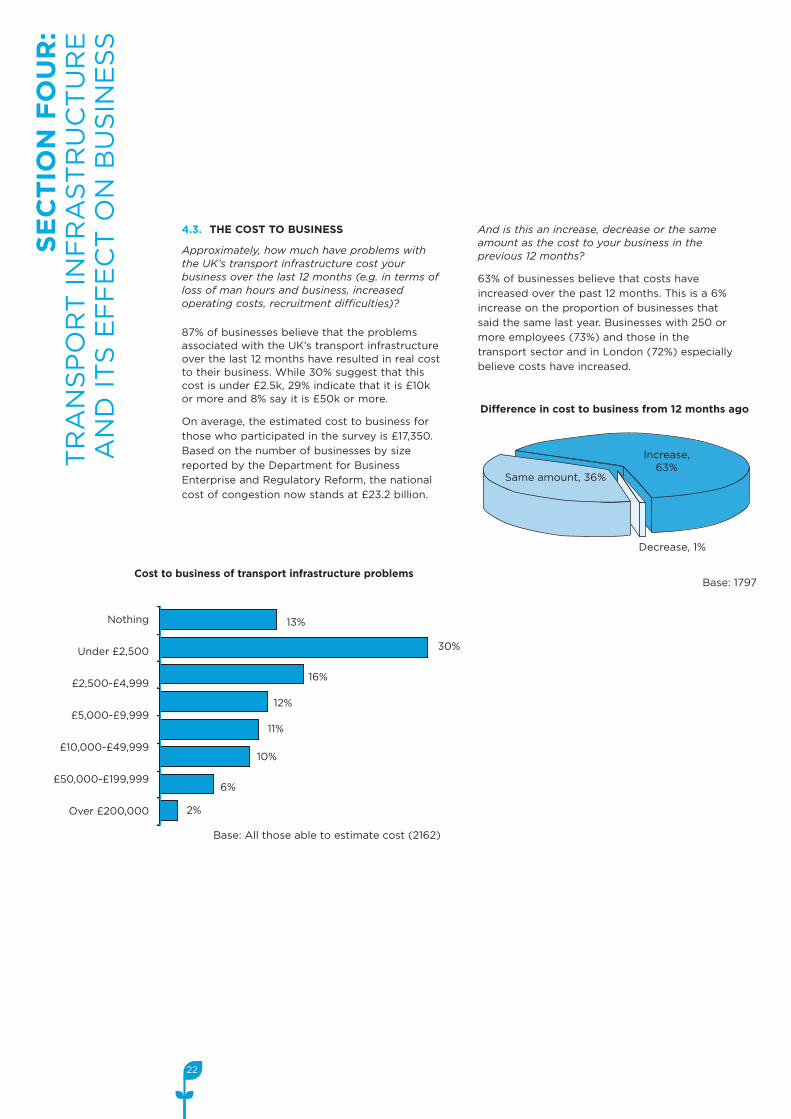

4.3. THE COST TO BUSINESS

Approximately, how much have problems withthe UK’s transport infrastructure cost yourbusiness over the last 12 months (e.g. in terms ofloss of man hours and business, increasedoperating costs, recruitment difficulties)?

87% of businesses believe that the problemsassociated with the UK’s transport infrastructureover the last 12 months have resulted in real costto their business. While 30% suggest that thiscost is under £2.5k, 29% indicate that it is £10kor more and 8% say it is £50k or more.

On average, the estimated cost to business for

those who participated in the survey is £17,350.

Based on the number of businesses by size

reported by the Department for Business

Enterprise and Regulatory Reform, the national

cost of congestion now stands at £23.2 billion.

And is this an increase, decrease or the sameamount as the cost to your business in theprevious 12 months?

63% of businesses believe that costs have

increased over the past 12 months. This is a 6%

increase on the proportion of businesses that

said the same last year. Businesses with 250 or

more employees (73%) and those in the

transport sector and in London (72%) especially

believe costs have increased.

Nothing

Under £2,500

£2,500-£4,999

£5,000-£9,999

£10,000-£49,999

£50,000-£199,999

Over £200,000

Cost to business of transport infrastructure problems

Base: All those able to estimate cost (2162)

6%

11%

10%

16%

13%

30%

12%

2%

Di�erence in cost to business from 12 months ago

Base: 1797

Decrease, 1%

Increase,63%

Same amount, 36%

5.1. ROAD PRICING

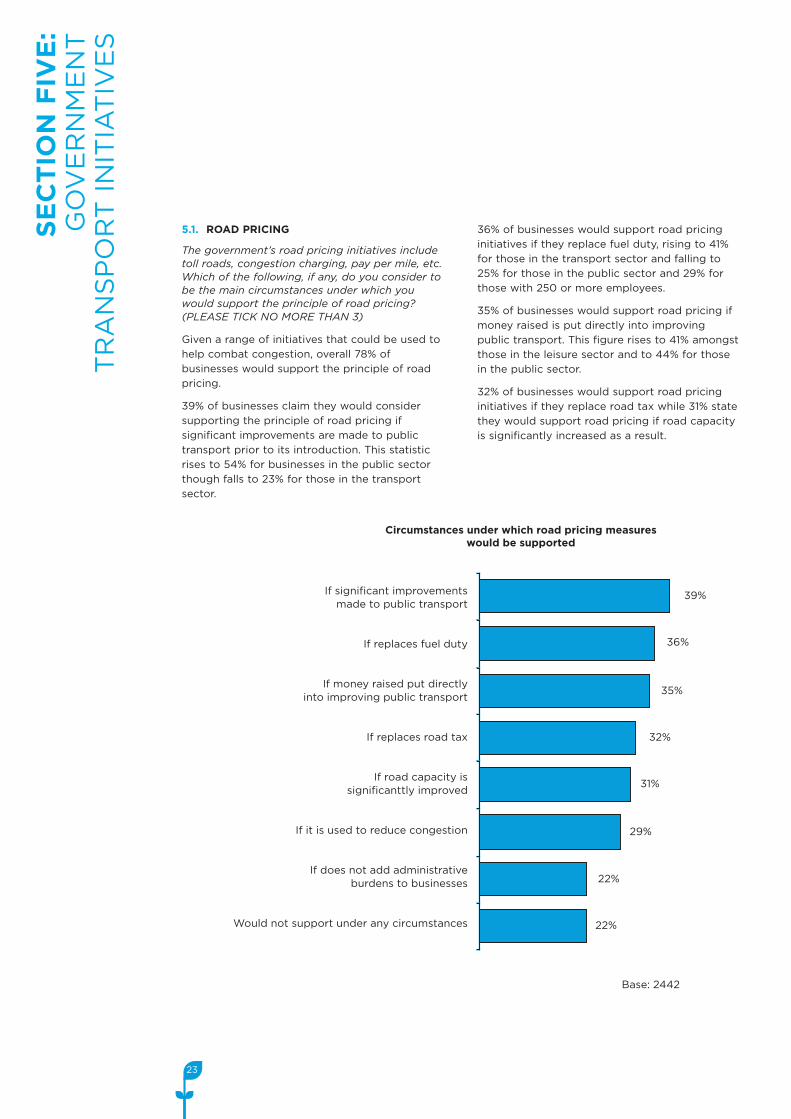

The government’s road pricing initiatives includetoll roads, congestion charging, pay per mile, etc.Which of the following, if any, do you consider tobe the main circumstances under which youwould support the principle of road pricing?(PLEASE TICK NO MORE THAN 3)

Given a range of initiatives that could be used to

help combat congestion, overall 78% of

businesses would support the principle of road

pricing.

39% of businesses claim they would consider

supporting the principle of road pricing if

significant improvements are made to public

transport prior to its introduction. This statistic

rises to 54% for businesses in the public sector

though falls to 23% for those in the transport

sector.

36% of businesses would support road pricing

initiatives if they replace fuel duty, rising to 41%

for those in the transport sector and falling to

25% for those in the public sector and 29% for

those with 250 or more employees.

35% of businesses would support road pricing if

money raised is put directly into improving

public transport. This figure rises to 41% amongst

those in the leisure sector and to 44% for those

in the public sector.

32% of businesses would support road pricing

initiatives if they replace road tax while 31% state

they would support road pricing if road capacity

is significantly increased as a result.

23

SECTIONFIVE:

GOVERNMENT

TRANSPORTINITIATIVES

If significant improvementsmade to public transport

If replaces fuel duty

If money raised put directlyinto improving public transport

If replaces road tax

If road capacity issignificanttly improved

If it is used to reduce congestion

If does not add administrativeburdens to businesses

Would not support under any circumstances

Circumstances under which road pricing measureswould be supported

39%

36%

35%

32%

31%

29%

22%

22%

Base: 2442

Compared to 2007, a significantly greater

proportion of businesses this year would support

road pricing if it replaces fuel duty (32% vs. 36%)

and does not add administrative burdens to

businesses (18% vs. 22%). However there is a 3%

fall in support for road pricing this year for a

scheme that makes significant improvements to

public transport and one that reduces congestion.

24

SECTIONFIVE:

GOVERNMENT

TRANSPORTINITIATIVES

Road pricing measures would support to combat congestion 2007 2008

If significant improvements made to public transport 42% 39%

If replaces fuel duty 32% 36%

If money raised put directly into improving public transport 34% 35%

If replaces road tax 31% 32%

If road capacity is significantly improved 29% 31%

If used to reduce congestion 32% 29%

If does not add administrative burdens to businesses 18% 22%

Would not support under any circumstances 22% 22%

Statistically significant differences shown in bold Base: 2568 2442

5.2. GOVERNMENT SCHEMES TO REDUCECONGESTION

In order to reduce congestion on the nationalroad network the government has proposed thefollowing schemes. What do you most favour?

44% of businesses most favour road widening as

a way to reduce congestion on the national road

network, rising to 52% for those based in the

North East. 41% prefer the building of new roads,

31% the use of the hard shoulder (46% in the

West Midlands where this initiative was first

piloted on the M42) and 21% the use of high

occupancy vehicle lanes.

Road widening

Building of new roads

Use of the hard shoulder

High OccupancyVehicle lanes

Toll lanes

National road pricing

None of these

Don’t know

Government national schemes favoured to reduceroad congestion

44%

41%

31%

21%

18%

9%

11%

5%Base: 2443

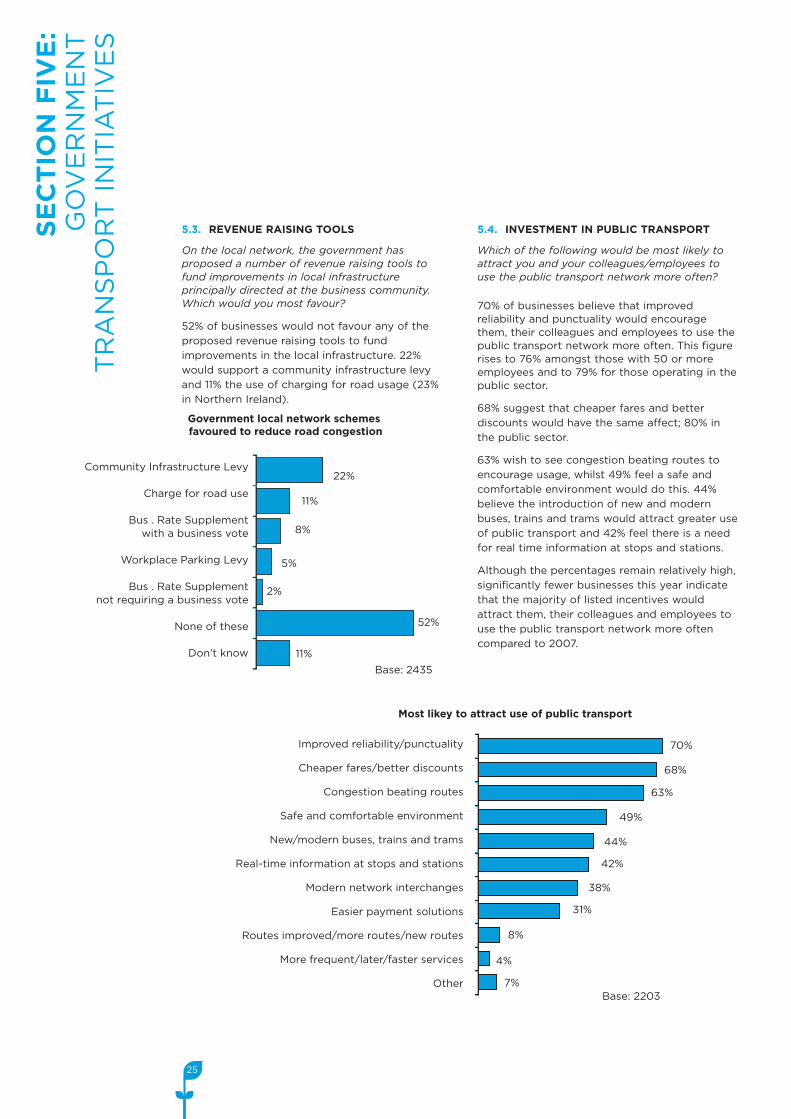

5.3. REVENUE RAISING TOOLS

On the local network, the government hasproposed a number of revenue raising tools tofund improvements in local infrastructureprincipally directed at the business community.Which would you most favour?

52% of businesses would not favour any of the

proposed revenue raising tools to fund

improvements in the local infrastructure. 22%

would support a community infrastructure levy

and 11% the use of charging for road usage (23%

in Northern Ireland).

5.4. INVESTMENT IN PUBLIC TRANSPORT

Which of the following would be most likely toattract you and your colleagues/employees touse the public transport network more often?

70% of businesses believe that improvedreliability and punctuality would encouragethem, their colleagues and employees to use thepublic transport network more often. This figurerises to 76% amongst those with 50 or moreemployees and to 79% for those operating in thepublic sector.

68% suggest that cheaper fares and better

discounts would have the same affect; 80% in

the public sector.

63% wish to see congestion beating routes to

encourage usage, whilst 49% feel a safe and

comfortable environment would do this. 44%

believe the introduction of new and modern

buses, trains and trams would attract greater use

of public transport and 42% feel there is a need

for real time information at stops and stations.

Although the percentages remain relatively high,

significantly fewer businesses this year indicate

that the majority of listed incentives would

attract them, their colleagues and employees to

use the public transport network more often

compared to 2007.

25

SECTIONFIVE:

GOVERNMENT

TRANSPORTINITIATIVES

Community Infrastructure Levy

Charge for road use

Bus . Rate Supplementwith a business vote

Workplace Parking Levy

Bus . Rate Supplementnot requiring a business vote

None of these

Don’t know

Government local network schemesfavoured to reduce road congestion

11%

22%

8%

5%

2%

52%

11%

Base: 2435

Improved reliability/punctuality

Cheaper fares/better discounts

Congestion beating routes

Safe and comfortable environment

New/modern buses, trains and trams

Real-time information at stops and stations

Modern network interchanges

Easier payment solutions

Routes improved/more routes/new routes

More frequent/later/faster services

Other

Most likey to attract use of public transport

70%

68%

63%

49%

44%

42%

38%

31%

8%

4%

7%Base: 2203

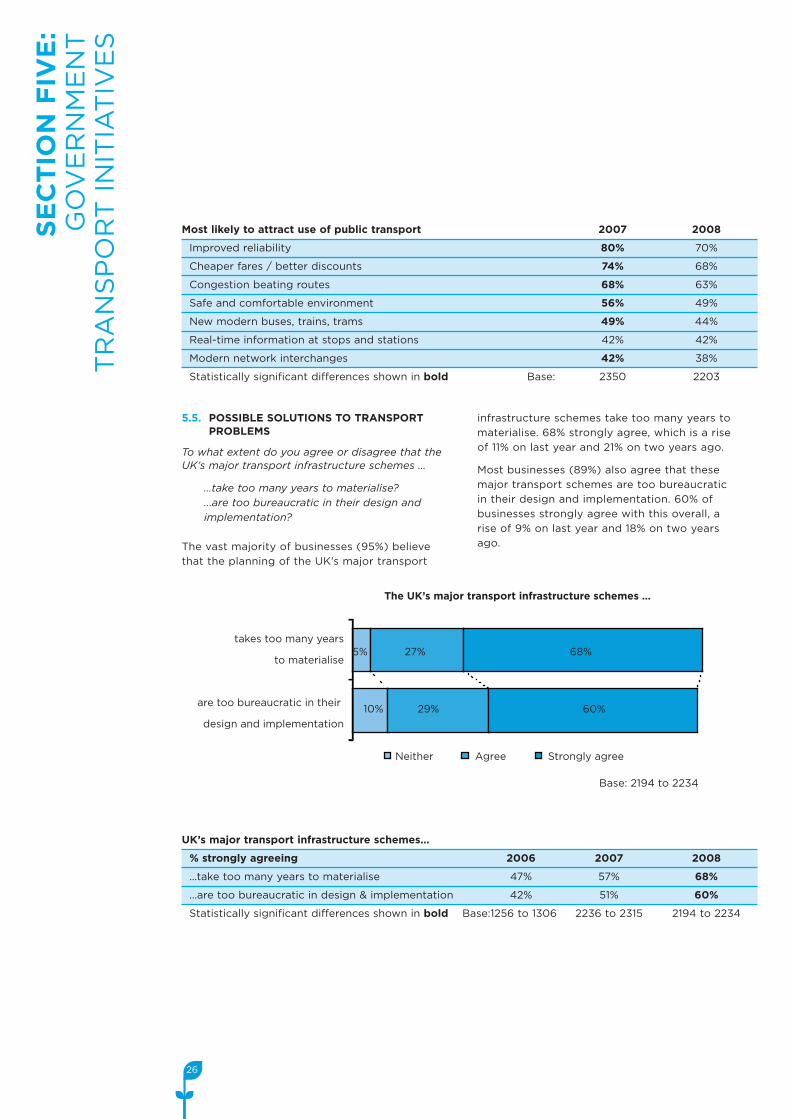

5.5. POSSIBLE SOLUTIONS TO TRANSPORTPROBLEMS

To what extent do you agree or disagree that theUK’s major transport infrastructure schemes …

…take too many years to materialise?...are too bureaucratic in their design andimplementation?

The vast majority of businesses (95%) believe

that the planning of the UK’s major transport

infrastructure schemes take too many years to

materialise. 68% strongly agree, which is a rise

of 11% on last year and 21% on two years ago.

Most businesses (89%) also agree that these

major transport schemes are too bureaucratic

in their design and implementation. 60% of

businesses strongly agree with this overall, a

rise of 9% on last year and 18% on two years

ago.

26

SECTIONFIVE:

GOVERNMENT

TRANSPORTINITIATIVES

Most likely to attract use of public transport 2007 2008

Improved reliability 80% 70%

Cheaper fares / better discounts 74% 68%

Congestion beating routes 68% 63%

Safe and comfortable environment 56% 49%

New modern buses, trains, trams 49% 44%

Real-time information at stops and stations 42% 42%

Modern network interchanges 42% 38%

Statistically significant differences shown in bold Base: 2350 2203

UK’s major transport infrastructure schemes…

% strongly agreeing 2006 2007 2008

…take too many years to materialise 47% 57% 68%

…are too bureaucratic in design & implementation 42% 51% 60%

Statistically significant differences shown in bold Base:1256 to 1306 2236 to 2315 2194 to 2234

takes too many years

to materialise

are too bureaucratic in their

design and implementation

The UK’s major transport infrastructure schemes …

Base: 2194 to 2234

Neither Agree Strongly agree

5% 27% 68%

10% 29% 60%

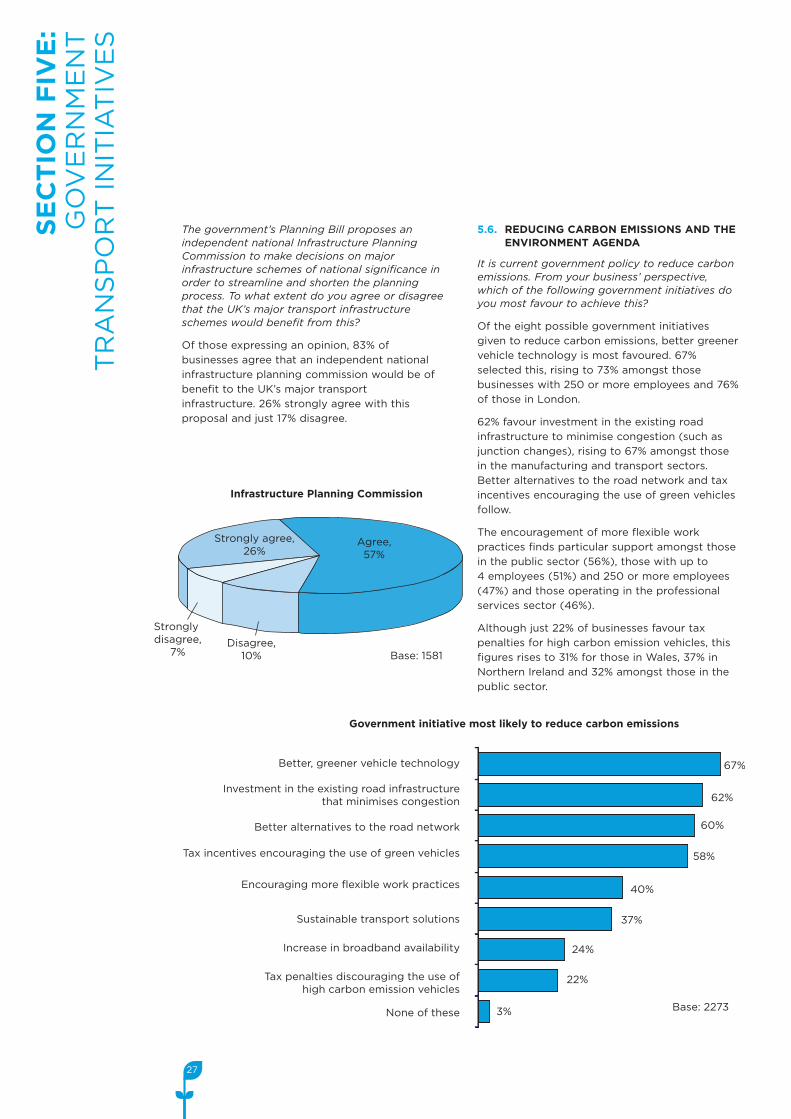

The government’s Planning Bill proposes anindependent national Infrastructure PlanningCommission to make decisions on majorinfrastructure schemes of national significance inorder to streamline and shorten the planningprocess. To what extent do you agree or disagreethat the UK’s major transport infrastructureschemes would benefit from this?

Of those expressing an opinion, 83% of

businesses agree that an independent national

infrastructure planning commission would be of

benefit to the UK’s major transport

infrastructure. 26% strongly agree with this

proposal and just 17% disagree.

5.6. REDUCING CARBON EMISSIONS AND THEENVIRONMENT AGENDA

It is current government policy to reduce carbonemissions. From your business’ perspective,which of the following government initiatives doyou most favour to achieve this?

Of the eight possible government initiatives

given to reduce carbon emissions, better greener

vehicle technology is most favoured. 67%

selected this, rising to 73% amongst those

businesses with 250 or more employees and 76%

of those in London.

62% favour investment in the existing road

infrastructure to minimise congestion (such as

junction changes), rising to 67% amongst those

in the manufacturing and transport sectors.

Better alternatives to the road network and tax

incentives encouraging the use of green vehicles

follow.

The encouragement of more flexible work

practices finds particular support amongst those

in the public sector (56%), those with up to

4 employees (51%) and 250 or more employees

(47%) and those operating in the professional

services sector (46%).

Although just 22% of businesses favour tax

penalties for high carbon emission vehicles, this

figures rises to 31% for those in Wales, 37% in

Northern Ireland and 32% amongst those in the

public sector.

27

SECTIONFIVE:

GOVERNMENT

TRANSPORTINITIATIVES

Infrastructure Planning Commission

Base: 1581Disagree,

10%

Stronglydisagree,

7%

Agree,57%

Strongly agree,26%

Better, greener vehicle technology

Investment in the existing road infrastructurethat minimises congestion

Better alternatives to the road network

Tax incentives encouraging the use of green vehicles

Encouraging more flexible work practices

Sustainable transport solutions

Increase in broadband availability

Tax penalties discouraging the use ofhigh carbon emission vehicles

None of these

Government initiative most likely to reduce carbon emissions

67%

62%

60%

58%

40%

37%

24%

22%

3% Base: 2273

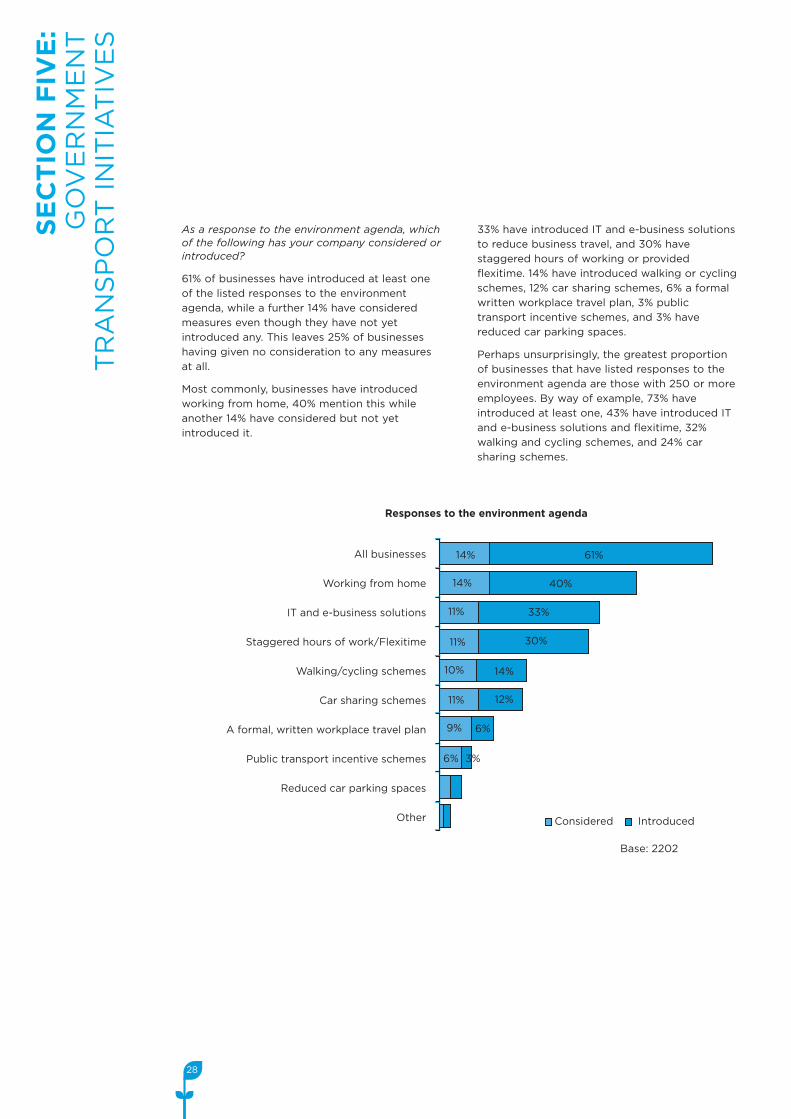

As a response to the environment agenda, whichof the following has your company considered orintroduced?

61% of businesses have introduced at least one

of the listed responses to the environment

agenda, while a further 14% have considered

measures even though they have not yet

introduced any. This leaves 25% of businesses

having given no consideration to any measures

at all.

Most commonly, businesses have introduced

working from home, 40% mention this while

another 14% have considered but not yet

introduced it.

33% have introduced IT and e-business solutions

to reduce business travel, and 30% have

staggered hours of working or provided

flexitime. 14% have introduced walking or cycling

schemes, 12% car sharing schemes, 6% a formal

written workplace travel plan, 3% public

transport incentive schemes, and 3% have

reduced car parking spaces.

Perhaps unsurprisingly, the greatest proportion

of businesses that have listed responses to the

environment agenda are those with 250 or more

employees. By way of example, 73% have

introduced at least one, 43% have introduced IT

and e-business solutions and flexitime, 32%

walking and cycling schemes, and 24% car

sharing schemes.

28

SECTIONFIVE:

GOVERNMENT

TRANSPORTINITIATIVES

All businesses

Working from home

IT and e-business solutions

Staggered hours of work/Flexitime

Walking/cycling schemes

Car sharing schemes

A formal, written workplace travel plan

Public transport incentive schemes

Reduced car parking spaces

Other

Responses to the environment agenda

Base: 2202

Considered Introduced

61%

40%

33%

30%

14%

12%

6%

6%

9%

11%

11%

11%

14%

14%

10%

3%

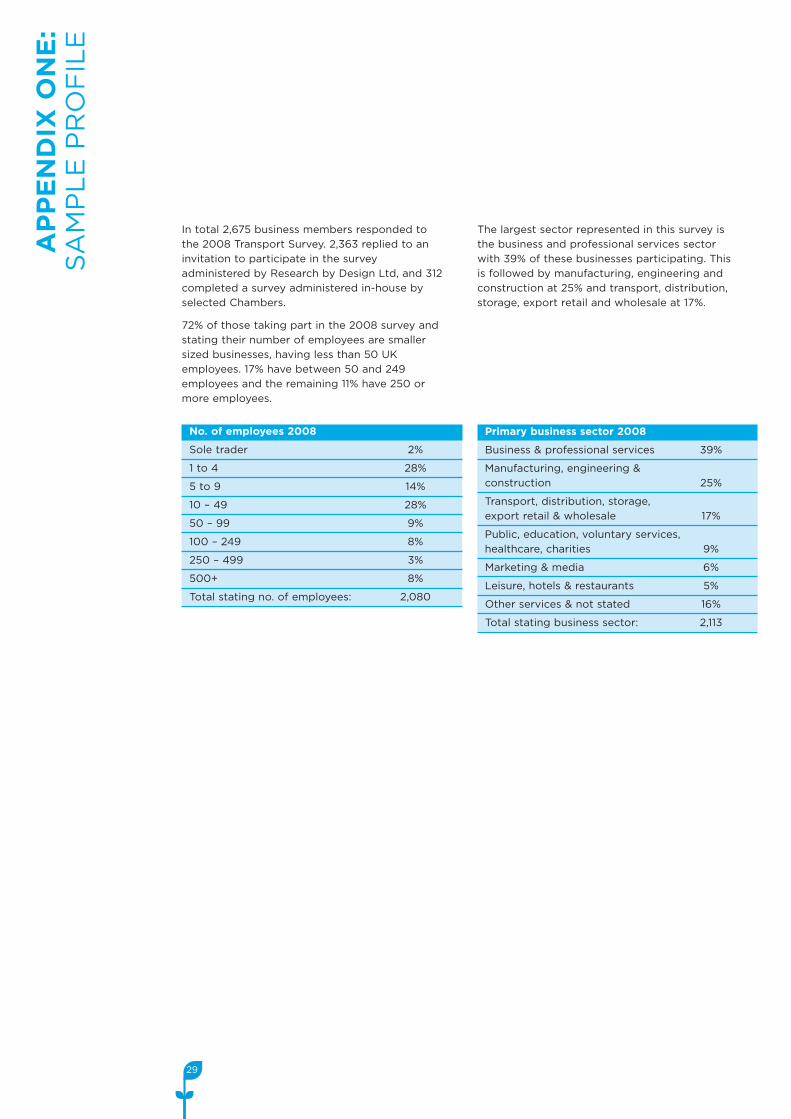

In total 2,675 business members responded to

the 2008 Transport Survey. 2,363 replied to an

invitation to participate in the survey

administered by Research by Design Ltd, and 312

completed a survey administered in-house by

selected Chambers.

72% of those taking part in the 2008 survey and

stating their number of employees are smaller

sized businesses, having less than 50 UK

employees. 17% have between 50 and 249

employees and the remaining 11% have 250 or

more employees.

The largest sector represented in this survey is

the business and professional services sector

with 39% of these businesses participating. This

is followed by manufacturing, engineering and

construction at 25% and transport, distribution,

storage, export retail and wholesale at 17%.

29

APPENDIXONE:

SAMPLEPROFILE

No. of employees 2008

Sole trader 2%

1 to 4 28%

5 to 9 14%

10 – 49 28%

50 – 99 9%

100 – 249 8%

250 – 499 3%

500+ 8%

Total stating no. of employees: 2,080

Primary business sector 2008

Business & professional services 39%

Manufacturing, engineering &

construction 25%

Transport, distribution, storage,

export retail & wholesale 17%

Public, education, voluntary services,

healthcare, charities 9%

Marketing & media 6%

Leisure, hotels & restaurants 5%

Other services & not stated 16%

Total stating business sector: 2,113

CHAMBERS PARTICIPATING IN THE SURVEY

Businesses who participated in the survey aremembers of the following 48 Chambers.

Aberdeen and Grampian Chamber of Commerce

Ayrshire Chamber of Commerce & Industry

Barnsley and Rotherham Chamber of Commerce

& Industry

Bedfordshire & Luton Chamber of Commerce

Birmingham Chamber of Commerce & Industry

Bradford Chamber of Commerce & Industry

Cambridgeshire Chamber of Commerce

Chambers of Commerce North West

Channel Chamber of Commerce

Chester, Ellesmere Port & North Wales Chamber

of Commerce

Coventry & Warwickshire Chamber of Commerce

Cumbria Chamber of Commerce & Industry

Derbyshire Chamber of Commerce

Doncaster Chamber of Commerce

Dorset Chamber of Commerce & Industry

East Lancashire Chamber of Commerce

Edinburgh Chamber of Commerce

Essex Chamber of Commerce

Fife Chamber of Commerce

Greater Manchester Chamber of Commerce

Hereford & Worcestershire Chamber of

Commerce

Hertfordshire Chamber of Commerce & Industry

Hull and Humber Chamber of Commerce,

Industry & Shipping

Kent Invicta Chamber of Commerce

Leeds Chamber of Commerce & Industry

Leicestershire Chamber of Commerce

Lincolnshire Chamber of Commerce & Industry

Liverpool Chamber of Commerce & Industry

Mid Yorkshire Chamber of Commerce & Industry

Milton Keynes & North Bucks Chamber of

Commerce

Newport & Gwent Chamber of Commerce

Norfolk Chamber of Commerce & Industry

North East Chamber of Commerce

North and Western Lancashire Chamber of

Commerce

North Staffordshire Chamber of Commerce &

Industry

Northern Ireland Chamber of Commerce &

Industry

Portsmouth & South East Hampshire Chamber of

Commerce & Industry

Renfrewshire Chamber of Commerce

Sheffield Chamber of Commerce & Industry

Shropshire Chamber of Commerce & Enterprise

Southern Staffordshire Chamber of Commerce &

Industry

St Helens Chamber

Suffolk Chamber of Commerce

Surrey Chambers of Commerce

Sussex Enterprise

Thames Valley Chamber of Commerce & Industry

West Wales Chamber of Commerce

York and North Yorkshire Chamber of Commerce

30

APPENDIXTWO:

PARTICIPATING

CHAMBERS

BRITISH CHAMBERS OF COMMERCE65 PETTY FRANCE

LONDON SW1H 9EU

UNITED KINGDOM

T +44 (0)20 7654 5800

F +44 (0)20 7654 5819

www.britishchambers.org.uk