Embed Size (px)

Citation preview

Back to EU Member states

NEXIA

Property and TaxationProperty and Taxation

Back to EU Member states

Instructions

This document provides basic information on the taxation of property inthe EU member states and non EU countries. It is not intended to be a detailed analysis of all taxation issues, but a general introduction which can be used as a starting point when advising or working with clients.Assuming more detailed information is required, then the author for eachcountry can be contacted.

John Voyez Smith & Williamson

Tel: 00 44 (0)20 7131 4285Email: [email protected]

Back to EU Member states

EU Member States

AustriaBelgiumBulgariaCyprusCzech RepublicDenmarkEstoniaFinlandFranceGermanyGreeceHungaryIrelandItaly Latvia

LithuaniaLuxembourgMaltaNetherlandsPolandPortugalRomaniaRussiaSlovakiaSloveniaSpainSwedenUkraineUnited Kingdom

Back to EU Member states

Non EU Countries

1. Croatia

Back to EU Member states

[Country Name]

Contents

1. Introduction – why buy real estate?

2. Contact details

3. Forms of property ownership

4. Taxes and other costs on property acquisitions

5. Issues during Ownership

6. Disposal of property

7. Non resident owners of property

8. Sundry issues

Back to EU Member states

1. Introduction - Austria

Why buy real estate ?

a) Backgrounds• Austria is a world wide leader in nature protection• Solid values - no speculative bubbles • Centrally situated in Europe – a four hours drive to the

Adriatic seab) Civil law• Ownership and mortgages are recorded in the land title

register which is open to the public

Back to EU Member states

2. Contact Details

Mag. Wolfgang Korp K & E Wirtschaftstreuhand Gesellschaft m.b.H. Wirtschaftsprüfungs- und Steuerberatungsgesellschaft Hofgasse 3 A-8010 Graz, Austria Tel.: +43 316 38 46 40 Fax: +43 316 38 46 40 - 20 Mobile +43 664 [email protected] www.ketreuhand.at

Back to EU Member states

3. Form of property ownership

The usual form in Austria is outright freehold by individuals or legal entities

Longterm rental agreements with the option to outright freehold are usual for factory estates

Holyday property and luxury business estates often are rented for limited time

Back to EU Member states

4. Taxes and other costs on property acquisition

Acquisition is subject to a transfer tax of 3,5 %

The registration fee is 1% on the purchase

Price.

Back to EU Member states

5. Issues during ownership

Ownership is subject to a local tax of about 0,4 to 0,84 % of the tax value which is generally lower than fair value.

VAT for rent is generally 20%, for housing rent 10%.

Back to EU Member states

6. Disposal of property

Capital gains are only taxable for individuals if theproperty has been held for less than 10 years.

Capital gains within businesses are normal income.

There is no inheritance or gift tax.

Back to EU Member states

7. Non resident owners of property

Most double tax agreements allow Austria to tax the rental income.

The same principle is for capital gains.

Acquisition of real estate not to be used as principal residence or business to be founded there is restricted in some tourist regions equally for foreigners as for Austrians.

Back to EU Member states

8. Sundry issues

Acquisition by non EU individuals or non EU legal entities is subject to approval of a local authority.

Such approval is easier to get if the Property is purchased by an Austrian legal entity or is needed for founding a business. Foreigners may also use the Austrian Privatstiftung (a legal entity) to invest in Austrian real estate.

Back to EU Member states

Back to EU Member states

Belgium

Contents

1. Introduction – why buy real estate?

2. Contact details

3. Forms of property ownership

4. Taxes and other costs on property acquisitions

5. Issues during Ownership

6. Disposal of property

7. Non resident owners of property

8. Sundry issues

Back to EU Member states

1. Introduction - BelgiumAcquiring real estate is often seen as a solid investment as the value fluctuations are fairly limited compared to movable property (especially shares)

Moreover, Belgium provides for a fairly beneficial taxation regime for physical persons on residential real estate. First of all, taxation on effective rental income is avoided and secondly future capital gains are generally exempt. For companies and professional users, real estate is not regarded any different from other business assets. However, real estate leases may offer tax planning opportunities.

Belgian real estate taxation is however becoming increasingly complicated due to the fact that the 3 regions (i.e. Brussels, Flanders and the Walloon Region, have acquired increasing taxation power

Only the income tax (strictu sensu) and VAT have remained federal taxes. Registration duties and the property tax are now regulated by the different regions. As a result thereof, tax rates, tax reliefs, … vary across the country.

Specifically for the property tax, it is important to note that also the provinces and communities are allowed to place important surcharges. It follows that the effective real estate tax burden can vary substantially across the country. Specific and detailed advice has become inevitable.

Back to EU Member states

2. Contact Details

Edwin Vervoort

Tax Partner

VGD Accountants en Belastingconsulenten

Schaliënstraat 5 Bus 3

2000 Antwerpen

Tel.: + 32 (0)3 247 43 00

Direct: + 32 (0)3 247 43 43

Fax: + 32 (0)3 247 43 02

Filip Viaene

VGD Accountants en Belastingconsulenten

Kortrijksestraat 99

8520 Kuurne

Tel + 32 (056) 35 85 51

Direct + 32 (056) 36 37 15

Fax +32 (056) 37 07 15

Back to EU Member states

3. Form of property ownership Besides full ownership, Belgian civil law (applicable to the 3 regions) provides for a number of “partial ownerships”. The most common are:

- usufruct or “vruchtgebruik” being the legal right to use and derive benefit from a property that belongs to another person- long lease or “erfpacht”, implying full ownership over the land and the buildings for a limited period of time- building and planting right or “opstalrecht”, allowing to build on someone elses land and becoming full owner of the building for a limited period of time

The last 2 “partial ownerships” are governed by civil law principles that are older than the Belgian State itself. Nevertheless, they have remain popular as they are often used within the framework of a real estate leasing for industrial premises, offices, storage spaces, etc.

Real estate leasing works in exactly the same way as movables leasing. Upon instruction of the company, a leasing company will buy an existing building or construct a new one. The lessor hereby takes out a long-term lease on the building in question (usually 15 to 20 years). At the end of the lease, the lessor can acquire ownership of the building by exercising the purchase option.

Real estate leasing offers a number of advantages, amongst others the 100% financing, transfer option of the contract, no collateral demanded … For new buildings (cfr. point 4 hereafter), the lease can be subject to VAT. For existing buildings, a 0,2% registration duty will be applicable on the cumulative lease payments.

Depending on whether or not the periodically payments allow to reconstruct the initial investment capital with interest (the so-called full pay out), the lease can be an on or off balance operation.

Back to EU Member states

4. Taxes and other costs on property acquisition

Registration tax is generally applicable to sales or exchanges of Belgian real estate. Since registration tax is a regional tax, the rates vary. In Flanders, the rate is generally 10% whereas in Brussels and the Wallon Region a 12,5% rate applies. Houses with a limited notional rental value can be acquired at a reduced rate of 5% in Flanders or 6% in the other regions provided certain conditions are met.

“New” buildings can be sold under 21% VAT, and thus with exemption of registration tax provided certain formalities are met. A building is considered as “new” for VAT until December 31 of the second year following the [year of occupation] of putting into use. Up until now, VAT could only apply to buildings but never to land itself. The sale of land always remained taxable with registration duties.

Recently, the EU has ordered Belgium to alter its legislation. Belgium will be obliged to allow that soil which is sold together with a “new” building is sold under VAT (and thus with exemption of registration tax). So far, it is uncertain how the federal state and the regions will alter their legislation. It is equally unclear whether they will impose 21% VAT or a reduced rate.

Mortgages on Belgian real estate trigger a 1% registration tax. In Flanders, a draft bill is pending to abolish this 1% tax as of January 1, 2009. So far, Brussels and the Walloon Region will not abolish the 1% right.

Apart from registration tax and/or VAT, also notary fees will become due. These fees depend on the transaction amount involved and on the file costs implemented by the public notary.

Back to EU Member states

5. Issues during ownership

Property tax

All the real estate is listed in the national land registry and an annual net rental income is assigned to it, the so-called cadastral income. This value corresponds to the deemed net rental income of the property and is yearly “indexed” to adjust for today’s prices. The cadastral income is revised if the characteristics of the property change (i.e. extension, rebuild, ...). The property tax is equal to a percentage of the aforementioned indexed cadastral income. To calculate it, you need to know the regional tax rate plus the provincial and community additions, as there is is no harmonization at the federal level.

The quality of the [owner] landlord (i.e. physical person or company) is irrelevant in determining the amount of property tax. The property tax can form a deductible expense for income tax purposes for a company or a professional user, but it is not to be considered an advance payment, withholding tax or alike.

Back to EU Member states

5. Issues during ownership….(cont’d

Income tax – physical persons

The own family home is in principle fully tax exempt. Moreover, anyone deciding to take the plunge and acquire a property can benefit from a substantial tax cut.Since 2005, the law permits a new overall deduction of interest, capital redemption and life insurance premiums paid by the taxpayer who buys, builds or converts his own and only home.

When the owner does not rent out a property (other than his own family home), he is charged on the basis of his cadastral income multiplied by an coefficient (1,40). In case the owner of a property rents out his property to a person that uses it for professional purposes or to a company, the owner will be taxed on the effective rental income. If the hirer does not use the property for professional purposes, the owner is taxed like in the first situation. Certain cost deductions are allowed, but these fall outside the scope of this text.

Income tax – companies

Companies are always taxable on the effectively received rental income minus the proven costs, regardless of the capacity of the tenant (i.e. professional use or not, company or physical person).

Back to EU Member states

6. Disposal of property

Physical persons

If the real estate was a professionally used asset, any capital gain will be considered as taxable profit under the ordinary progressive tax rates. Capital gains realized on the disposal of other real estate (being part of ones private patrimonium), are in principle tax exempt.

However, when a building is sold off within 5 years after the date of acquisition, the capital gain will be taxed at a flat rate of 16,5%. When land is sold off within 5 years after the date of acquisition, the capital gain is taxed at 33%. If the land is sold off between the fifth and eight year after acquisition, the rate is reduced to 16,5%.

The calculation of the taxable capital gain is specifically described in the income tax code. For specific cases, please contact one of the persons mentioned before.

Companies

Companies are always taxable on the realised capital gain (i.e. sales price minus net book value). There is no separate taxation rate provided for (it is possible to spread out the payment of capital gain tax in case of reinvestment of the selling price). Realised capital losses on the sale of real estate are tax deductible (assuming that the transaction prices were set at arm’s length).

Back to EU Member states

7. Non resident owners of property

• a withholding tax on the sales proceeds of real estate is due in case of non-resident sellers. To the extent the foreign owner has no permanent establishment or permanent basis in Belgium, the withholding tax is liberatory. In case the Belgian real estate was part of a Belgian permanent establishment of permanent basis, the withholding tax will be settled with the overall tax due in Belgium.

• for non-resident physical persons, the real estate tax can be liberatory if they do not obtain other taxable income in Belgium and to the extent a certain threshold is not exceeded.

Belgian law contains no limitations on the acquisition or sale of real estate for foreign companies or foreign physical persons. There are however a few tax regulations that specifically apply to non-residents, the most important being:

Back to EU Member states

8. Sundry issuesLike registration tax and property tax, environmental legislation also rests with the regions. In Flanders for instance, it is impossible to sell off real estate without obtaining a soil certificate. Such a soil certificate normally indicates that the government has no indication of soil contamination. Under certain circumstances however, a soil investigation will be imposed and/or soil decontamination will need to be processed before the real estate can be sold off.

In the Walloon region, no such stringent legislation applies. Nevertheless, taking into account the overall trend in western Europe, it is likely that at some moment in time, the Walloon region will implement similar legislation. In 2004 a regional Walloon decree was launched, but it has not (yet?) entered into force.

Apart form environmental legislation, also building regulations are fairly stringent. All new building activity and nearly all adaptation works to an existing building need a formal permit. If not, the building site can be sealed and, next to paying fines, the landlord may be forced to restore the building into its original state.

For advice about these specific regulations, public notaries and architect agencies may be an important source of information, next to your accounting firm.

Back to EU Member states

Back to EU Member states

Bulgaria

Contents

1. Introduction – why buy real estate?

2. Contact details

3. Forms of property ownership

4. Taxes and other costs on property acquisitions

5. Issues during Ownership

6. Disposal of property

7. Non resident owners of property

8. Sundry issues

Back to EU Member states

1. Introduction – Bulgaria

This should be a brief introduction as to why real estate might be acquired eg. residential owner, business owner occupier, business owner investor, holiday property, residential investment etc.

Back to EU Member states

2. Contact Details

[Name 1][firm][telephone][email address]

[Name 2][firm][telephone][email address]

Back to EU Member states

3. Form of property ownership

[For example, outright freehold, leasehold rental etc for private persons and businesses]

Back to EU Member states

4. Taxes and other costs on property acquisition

[For example, a brief note on property tax (stamp duty), VAT, legal fees, funding costs etc for private persons and businesses]

Back to EU Member states

5. Issues during ownership

[For example local taxes due, VAT payable rental income/payment etc for private persons and businesses]

Back to EU Member states

6. Disposal of property

[For example capital taxes, inheritance tax, legal fees etc for private individuals and businesses]

Back to EU Member states

7. Non resident owners of property

[For example, the treatment of rental income, property development, gains on disposal etc for private persons and corporates]

Back to EU Member states

8. Sundry issues

[For example, any miscellaneous comments which may be of relevance for property investors not covered elsewhere eg. registering a property interest, building legislation etc.]

Back to EU Member states

Back to EU Member states

Cyprus

Contents

1. Introduction – why buy real estate?

2. Contact details

3. Forms of property ownership

4. Taxes and other costs on property acquisitions

5. Issues during Ownership

6. Disposal of property

7. Non resident owners of property

8. Sundry issues

Back to EU Member states

1. Introduction – Cyprus

This should be a brief introduction as to why real estate might be acquired eg. residential owner, business owner occupier, business owner investor, holiday property, residential investment etc.

Back to EU Member states

2. Contact Details

[Name 1][firm][telephone][email address]

[Name 2][firm][telephone][email address]

Back to EU Member states

3. Form of property ownership

[For example, outright freehold, leasehold rental etc for private persons and businesses]

Back to EU Member states

4. Taxes and other costs on property acquisition

[For example, a brief note on property tax (stamp duty), VAT, legal fees, funding costs etc for private persons and businesses]

Back to EU Member states

5. Issues during ownership

[For example local taxes due, VAT payable rental income/payment etc for private persons and businesses]

Back to EU Member states

6. Disposal of property

[For example capital taxes, inheritance tax, legal fees etc for private individuals and businesses]

Back to EU Member states

7. Non resident owners of property

[For example, the treatment of rental income, property development, gains on disposal etc for private persons and corporates]

Back to EU Member states

8. Sundry issues

[For example, any miscellaneous comments which may be of relevance for property investors not covered elsewhere eg. registering a property interest, building legislation etc.]

Back to EU Member states

Back to EU Member states

Czech Republic

Contents

1. Introduction – why buy real estate?

2. Contact details

3. Forms of property ownership

4. Taxes and other costs on property acquisitions

5. Issues during Ownership

6. Disposal of property

7. Non resident owners of property

8. Sundry issues

Back to EU Member states

1. Introduction – Czech Republic

This should be a brief introduction as to why real estate might be acquired eg. residential owner, business owner occupier, business owner investor, holiday property, residential investment etc.

Back to EU Member states

2. Contact Details

[Name 1][firm][telephone][email address]

[Name 2][firm][telephone][email address]

Back to EU Member states

3. Form of property ownership

[For example, outright freehold, leasehold rental etc for private persons and businesses]

Back to EU Member states

4. Taxes and other costs on property acquisition

[For example, a brief note on property tax (stamp duty), VAT, legal fees, funding costs etc for private persons and businesses]

Back to EU Member states

5. Issues during ownership

[For example local taxes due, VAT payable rental income/payment etc for private persons and businesses]

Back to EU Member states

6. Disposal of property

[For example capital taxes, inheritance tax, legal fees etc for private individuals and businesses]

Back to EU Member states

7. Non resident owners of property

[For example, the treatment of rental income, property development, gains on disposal etc for private persons and corporates]

Back to EU Member states

8. Sundry issues

[For example, any miscellaneous comments which may be of relevance for property investors not covered elsewhere eg. registering a property interest, building legislation etc.]

Back to EU Member states

Back to EU Member states

Denmark

Contents

1. Introduction – why buy real estate?

2. Contact details

3. Forms of property ownership

4. Taxes and other costs on property acquisitions

5. Issues during Ownership

6. Disposal of property

7. Non resident owners of property

8. Sundry issues

Back to EU Member states

1. Introduction - Denmark

This should be a brief introduction as to why real estate might be acquired eg. residential owner, business owner occupier, business owner investor, holiday property, residential investment etc.

Back to EU Member states

2. Contact Details

[Name 1][firm][telephone][email address]

[Name 2][firm][telephone][email address]

Back to EU Member states

3. Form of property ownership

[For example, outright freehold, leasehold rental etc for private persons and businesses]

Back to EU Member states

4. Taxes and other costs on property acquisition

[For example, a brief note on property tax (stamp duty), VAT, legal fees, funding costs etc for private persons and businesses]

Back to EU Member states

5. Issues during ownership

[For example local taxes due, VAT payable rental income/payment etc for private persons and businesses]

Back to EU Member states

6. Disposal of property

[For example capital taxes, inheritance tax, legal fees etc for private individuals and businesses]

Back to EU Member states

7. Non resident owners of property

[For example, the treatment of rental income, property development, gains on disposal etc for private persons and corporates]

Back to EU Member states

8. Sundry issues

[For example, any miscellaneous comments which may be of relevance for property investors not covered elsewhere eg. registering a property interest, building legislation etc.]

Back to EU Member states

Back to EU Member states

Estonia

Contents

1. Introduction – why buy real estate?

2. Contact details

3. Forms of property ownership

4. Taxes and other costs on property acquisitions

5. Issues during Ownership

6. Disposal of property

7. Non resident owners of property

8. Sundry issues

Back to EU Member states

1. Introduction - Estonia

This should be a brief introduction as to why real estate might be acquired eg. residential owner, business owner occupier, business owner investor, holiday property, residential investment etc.

Back to EU Member states

2. Contact Details

[Name 1][firm][telephone][email address]

[Name 2][firm][telephone][email address]

Back to EU Member states

3. Form of property ownership

[For example, outright freehold, leasehold rental etc for private persons and businesses]

Back to EU Member states

4. Taxes and other costs on property acquisition

[For example, a brief note on property tax (stamp duty), VAT, legal fees, funding costs etc for private persons and businesses]

Back to EU Member states

5. Issues during ownership

[For example local taxes due, VAT payable rental income/payment etc for private persons and businesses]

Back to EU Member states

6. Disposal of property

[For example capital taxes, inheritance tax, legal fees etc for private individuals and businesses]

Back to EU Member states

7. Non resident owners of property

[For example, the treatment of rental income, property development, gains on disposal etc for private persons and corporates]

Back to EU Member states

8. Sundry issues

[For example, any miscellaneous comments which may be of relevance for property investors not covered elsewhere eg. registering a property interest, building legislation etc.]

Back to EU Member states

Back to EU Member states

Finland

Contents

1. Introduction – why buy real estate?

2. Contact details

3. Forms of property ownership

4. Taxes and other costs on property acquisitions

5. Issues during Ownership

6. Disposal of property

7. Non resident owners of property

8. Sundry issues

Back to EU Member states

1. Introduction - Finland

This should be a brief introduction as to why real estate might be acquired eg. residential owner, business owner occupier, business owner investor, holiday property, residential investment etc.

Back to EU Member states

2. Contact Details

[Name 1][firm][telephone][email address]

[Name 2][firm][telephone][email address]

Back to EU Member states

3. Form of property ownership

[For example, outright freehold, leasehold rental etc for private persons and businesses]

Back to EU Member states

4. Taxes and other costs on property acquisition

[For example, a brief note on property tax (stamp duty), VAT, legal fees, funding costs etc for private persons and businesses]

Back to EU Member states

5. Issues during ownership

[For example local taxes due, VAT payable rental income/payment etc for private persons and businesses]

Back to EU Member states

6. Disposal of property

[For example capital taxes, inheritance tax, legal fees etc for private individuals and businesses]

Back to EU Member states

7. Non resident owners of property

[For example, the treatment of rental income, property development, gains on disposal etc for private persons and corporates]

Back to EU Member states

8. Sundry issues

[For example, any miscellaneous comments which may be of relevance for property investors not covered elsewhere eg. registering a property interest, building legislation etc.]

Back to EU Member states

Back to EU Member states

France

Contents

1. Introduction – why buy real estate?

2. Contact details

3. Forms of property ownership

4. Taxes and other costs on property acquisitions

5. Issues during Ownership

6. Disposal of property

7. Non resident owners of property

8. Sundry issues

Back to EU Member states

1. Introduction - France

This should be a brief introduction as to why real estate might be acquired eg. residential owner, business owner occupier, business owner investor, holiday property, residential investment etc.

Back to EU Member states

2. Contact Details

[Name 1][firm][telephone][email address]

[Name 2][firm][telephone][email address]

Back to EU Member states

3. Form of property ownership

[For example, outright freehold, leasehold rental etc for private persons and businesses]

Back to EU Member states

4. Taxes and other costs on property acquisition

[For example, a brief note on property tax (stamp duty), VAT, legal fees, funding costs etc for private persons and businesses]

Back to EU Member states

5. Issues during ownership

[For example local taxes due, VAT payable rental income/payment etc for private persons and businesses]

Back to EU Member states

6. Disposal of property

[For example capital taxes, inheritance tax, legal fees etc for private individuals and businesses]

Back to EU Member states

7. Non resident owners of property

[For example, the treatment of rental income, property development, gains on disposal etc for private persons and corporates]

Back to EU Member states

8. Sundry issues

[For example, any miscellaneous comments which may be of relevance for property investors not covered elsewhere eg. registering a property interest, building legislation etc.]

Back to EU Member states

Back to EU Member states

Germany

Contents

1. Introduction – why buy real estate?

2. Contact details

3. Forms of property ownership

4. Taxes and other costs on property acquisitions

5. Issues during Ownership

6. Disposal of property

7. Non resident owners of property

8. Sundry issues

Back to EU Member states

1. Introduction - Germany

There are several reasons as to why a person would buy or build property in Germany. Amongst them are the following:

• Investment: Real estate is an important and necessary asset in any diversified portfolio. This applies to private persons as well as to institutional investors. Furthermore as of January 2008 special tax rules now apply for real estate investment trusts.

• Owner occupation: There are two main aspects to buying property in Germany; first to use as a holiday home and second to reside permanently in Germany.

• Business use: If a foreign company intends to set up a subsidiary or a permanent establishment in Germany, it could be advantageous to buy or build their business premises instead of leasing them.

Back to EU Member states

2. Contact Details

Mr Carsten FrankeEbner Stolz Moenning BachemTel.: 0049 40 370 97 – 169Email: [email protected]

Mr Sten GuenselEbner Stolz Moenning BachemTel.: 0049 711 2049 - 1258Email: [email protected]

Back to EU Member states

3. Form of property ownership

The main forms of property ownership in regards to both private persons and companies are:

• Freehold• Leasehold• Rental• Statutory heritable building right (“Erbbaurecht”)

Back to EU Member states

4. Taxes and other costs on property acquisition

There are four important matters of expenses which must first be considered by the purchaser of German property.

• Real property transfer tax (“Grunderwerbsteuer”)

In general, subject to the real property transfer tax is the transfer of ownership with some exceptions. In January 2006 the federal states were being granted authority to autonomously determine the real property transfer tax rate. Nevertheless in practice the real property transfer tax rate amounts to 3.5 % of the assessable property value. Exceptions can be seen for example in Berlin and Hamburg where the tax rate has been increased to 4.5 %.

Notwithstanding any agreements to other effect the real property transfer tax must be paid in half by the buyer and in half by the seller. However in practice, it is normally agreed, that the purchaser pays the entire real property transfer tax.

Back to EU Member states

4. Taxes and other costs on property acquisition (cont’d…)• VAT (“Umsatzsteuer”)

Usually, the acquisition of property is exempt from VAT. However, if the seller and the buyer are both entrepreneurs, the option of VAT can be utilised, so that the sale is subject to 19% VAT. The exercise of this option may be advantageous for the seller to avoid input VAT repayments in some cases; the buyer is likely to agree on this if he is able to claim the VAT from the purchase as input VAT.

If the buyer is a private person, the acquisition is always exempt from VAT.

• Cost for notary and entry in land registerThe cost for the notary and for the land register entry amounts to approximately 0.5 - 2 % of the purchase price. The cost is dependant on several factors (for example entry of a mortgage) and must be paid usually by the buyer.

• Estate agent fees (Maklergebühr)Estate agent fees (also known as ‘courtage’) are often calculated at about 5 – 7 % of the purchase price. The fees are not regulated by law and as such are negotiable.

Back to EU Member states

5. Issues during ownership One must always distinguish the use of the property for private, business or rental purposes. • Private residential use / rental use

The German property could basically be used for two purposes. On the one hand it could be used for private residential purposes (for example as family home or as a holiday house). In this case German income tax would not apply.

On the other hand the German property could be used by a private person for achieving rental income. The rental income is subject to income tax. The rental income will be assessed at revenues basically less cost for building depreciation (2% p.a.), operation, maintenance and interest.

• Business use / rental use within a business

On the one hand the property can be used as business premises. In this case the business activities on the property usually create a permanent establishment in Germany.

Furthermore the property can be used for rental purposes within a business. If the German property is used for rental purposes within a business the income is subject to income tax. The rental income is determined as the difference between the rental revenue and the deductible business expenses (for example interest cost within the interest deduction limitation, depreciation, operation, maintenance costs, etc.) on an accrual basis. The building may basically be depreciated over its expected life-span (usually 3 % p.a.).

Back to EU Member states

5. Issues during ownership (contd…)

The German tax burden depends on the legal form of the investor. If the owner of the German property is a corporation the realised rental income is subject to corporate tax as well as, in most cases, trade income tax. The corporate tax rate amounts to 15 % plus 5.5 % solidarity surcharge thereon. The trade income tax depends on the municipal rate fixed by the municipality, the average trade income tax rate amounts to 14 %. Altogether, the average nominal tax rate of corporations would be approximately 30 %.

If the activities of the Corporate Investor are limited to the management of property assets and if the Corporate Investor elects to do so, he may enter the so called “extended exemption regime“ (erweiterte Grundstückskürzung) and therefore avoid paying trade income tax. The exemption is only applicable if the investor would be considered as ‘not in the business of trading in real estate’.

• Real estate taxProperty owners will be charged with real estate tax every calendar year. The tax amount is calculated as the sum of assessed value multiplied by the tax rate (2.6 ‰ - 6.0 ‰) and the municipal rate fixed by the municipality (usually between 350 % - 550 %). In the case of the use for business or rental purposes the real transfer tax is deductible for income tax matters.

• Net wealth tax („Vermögenssteuer“)Net wealth tax has not been levied since 1997.

Back to EU Member states

6. Disposal of property

The capital gains from the disposal of property are usually subject to corporate or income tax. A capital gain is calculated as the difference between the property’s purchase price and its book value plus any disposal costs.

In cases where the seller is a private person the tax liability of a capital gain from the disposal of German property is dependent on how the property has been used by the seller. If the property has been used by the owner for own residential purposes the capital gain is usually tax exempt. If this is not the case then the capital gain is subject to income tax plus solidarity surcharge thereon (maximum nominal tax rate would be 47 %) within 10 years after acquisition.

If the seller is a corporate investor then the capital gain from the disposal of the property is subject to a corporate tax rate of 15.82 % (including solidarity surcharge) as well as, in usual circumstances, trade income tax. As a result the capital gains are subject to an nominal tax rate of approximately 30 %. Under certain circumstances the trade income tax may be avoided there the seller successfully enters the “extended exemption regime” (see section 5.2). For the taxation of non resident corporate investor see section 7.

Furthermore, provisions for roll-over relief exist in Germany for businesses so that the taxation of the capital the capital gain from the disposal of German property may be avoided for a period of time. However it must be recognized that the utilization of the German roll-over relief system is dependant on the fulfilment of strict conditions.

Back to EU Member states

7. Non resident owners of property

The following description highlights the distinction between a direct investment in Germany by a private person and by a corporate investor. In both circumstances it is assumed that no German subsidiary has been or will be established in Germany due to the investment. Both the private investor and the corporate investor are subject to limited tax liability.

In cases where the property has been rented out by a private person the revenues minus the tax deductible expenses (e.g. depreciation, operation, interest, maintenance) is subject to German income tax plus solidarity surcharge. The maximum tax rate for a single individual as of 2009 is about 47 %. The rental income is calculated on a cash basis and the foreign investor is obliged to file a tax return in Germany.

Concerning the taxation of capital gains from the disposal of property, there are no differences to the taxation regulations attached to of a resident owner (therefore see section 6.)

Back to EU Member states

7. Non resident owners of property (contd…)

The Corporate Investor is subject to limited tax liability with respect to all the rental income and capital gains resulting from the use and sale of the German property. Unless the Corporate Investor does not have a permanent establishment in Germany the realized rental income is only subject to corporate income tax and solidarity surcharge. Under German law, a permanent establishment of the corporate investor is established if it has a fixed place of business in Germany which serves its business activities. Usually, the Corporate Investor does not create a permanent establishment in Germany if it merely holds legal title to German property which is leased to third party.

Taking effect from 1 January 2009 rental income of corporate investors will be calculated on an accrual basis. As mentioned above the Corporate Investor can deduct certain expenses as long as they have been incurred in relation to the rental income.

In general, interest costs are deductible. However, as from January 2008 the interest deduction limitation also applies to non-resident corporate investors. Accordingly, the tax deducibility of interest costs may be limited to 30 % of the taxable EBITDA if the net interest costs are higher than EUR 1 million (minimum threshold) and the corporate investor is part of a companies group.

Back to EU Member states

8. Sundry issues

Since the beginning of 2008 property investments in Germany can be conducted via German Real estate investment trusts (GREIT). The purpose of the introduction of the GREIT was to attract property investments to Germany by using the international accepted vehicle of a REIT. The GREIT should enable property fund raising on a broad basis. A GREIT is a stock corporation listed at the stock exchange. The GREIT can be tax favourable if certain conditions are met.

The German double taxation treaties usually grant the right to tax to the state of source. Double taxation then will be eliminated for some countries by the credit method whilst for others by the exemption method.

Back to EU Member states

Back to EU Member states

Greece

Contents

1. Introduction – why buy real estate?

2. Contact details

3. Forms of property ownership

4. Taxes and other costs on property acquisitions

5. Issues during Ownership

6. Disposal of property

7. Non resident owners of property

8. Sundry issues

Back to EU Member states

1. Introduction - Greece

This should be a brief introduction as to why real estate might be acquired eg. residential owner, business owner occupier, business owner investor, holiday property, residential investment etc.

Back to EU Member states

2. Contact Details

[Name 1][firm][telephone][email address]

[Name 2][firm][telephone][email address]

Back to EU Member states

3. Form of property ownership

[For example, outright freehold, leasehold rental etc for private persons and businesses]

Back to EU Member states

4. Taxes and other costs on property acquisition

[For example, a brief note on property tax (stamp duty), VAT, legal fees, funding costs etc for private persons and businesses]

Back to EU Member states

5. Issues during ownership

[For example local taxes due, VAT payable rental income/payment etc for private persons and businesses]

Back to EU Member states

6. Disposal of property

[For example capital taxes, inheritance tax, legal fees etc for private individuals and businesses]

Back to EU Member states

7. Non resident owners of property

[For example, the treatment of rental income, property development, gains on disposal etc for private persons and corporates]

Back to EU Member states

8. Sundry issues

[For example, any miscellaneous comments which may be of relevance for property investors not covered elsewhere eg. registering a property interest, building legislation etc.]

Back to EU Member states

Back to EU Member states

Hungary

Contents

1. Introduction – why buy real estate?

2. Contact details

3. Forms of property ownership

4. Taxes and other costs on property acquisitions

5. Issues during Ownership

6. Disposal of property

7. Non resident owners of property

8. Sundry issues

Back to EU Member states

1. Introduction - Hungary

This should be a brief introduction as to why real estate might be acquired eg. residential owner, business owner occupier, business owner investor, holiday property, residential investment etc.

Back to EU Member states

2. Contact Details

[Name 1][firm][telephone][email address]

[Name 2][firm][telephone][email address]

Back to EU Member states

3. Form of property ownership

[For example, outright freehold, leasehold rental etc for private persons and businesses]

Back to EU Member states

4. Taxes and other costs on property acquisition

[For example, a brief note on property tax (stamp duty), VAT, legal fees, funding costs etc for private persons and businesses]

Back to EU Member states

5. Issues during ownership

[For example local taxes due, VAT payable rental income/payment etc for private persons and businesses]

Back to EU Member states

6. Disposal of property

[For example capital taxes, inheritance tax, legal fees etc for private individuals and businesses]

Back to EU Member states

7. Non resident owners of property

[For example, the treatment of rental income, property development, gains on disposal etc for private persons and corporates]

Back to EU Member states

8. Sundry issues

[For example, any miscellaneous comments which may be of relevance for property investors not covered elsewhere eg. registering a property interest, building legislation etc.]

Back to EU Member states

Back to EU Member states

Ireland

Contents

1. Introduction – why buy real estate?

2. Contact details

3. Forms of property ownership

4. Taxes and other costs on property acquisitions

5. Issues during Ownership

6. Disposal of property

7. Non resident owners of property

8. Sundry issues

Back to EU Member states

1. Introduction - Ireland

This should be a brief introduction as to why real estate might be acquired eg. residential owner, business owner occupier, business owner investor, holiday property, residential investment etc.

Back to EU Member states

2. Contact Details

[Name 1][firm][telephone][email address]

[Name 2][firm][telephone][email address]

Back to EU Member states

3. Form of property ownership

[For example, outright freehold, leasehold rental etc for private persons and businesses]

Back to EU Member states

4. Taxes and other costs on property acquisition

[For example, a brief note on property tax (stamp duty), VAT, legal fees, funding costs etc for private persons and businesses]

Back to EU Member states

5. Issues during ownership

[For example local taxes due, VAT payable rental income/payment etc for private persons and businesses]

Back to EU Member states

6. Disposal of property

[For example capital taxes, inheritance tax, legal fees etc for private individuals and businesses]

Back to EU Member states

7. Non resident owners of property

[For example, the treatment of rental income, property development, gains on disposal etc for private persons and corporates]

Back to EU Member states

8. Sundry issues

[For example, any miscellaneous comments which may be of relevance for property investors not covered elsewhere eg. registering a property interest, building legislation etc.]

Back to EU Member states

Back to EU Member states

Italy

Contents

1. Introduction – why buy real estate?

2. Contact details

3. Forms of property ownership

4. Taxes and other costs on property acquisitions

5. Issues during Ownership

6. Disposal of property

7. Non resident owners of property

8. Sundry issues

Back to EU Member states

1. Introduction - Italy

This should be a brief introduction as to why real estate might be acquired eg. residential owner, business owner occupier, business owner investor, holiday property, residential investment etc.

Back to EU Member states

2. Contact Details

[Name 1][firm][telephone][email address]

[Name 2][firm][telephone][email address]

Back to EU Member states

3. Form of property ownership

[For example, outright freehold, leasehold rental etc for private persons and businesses]

Back to EU Member states

4. Taxes and other costs on property acquisition

[For example, a brief note on property tax (stamp duty), VAT, legal fees, funding costs etc for private persons and businesses]

Back to EU Member states

5. Issues during ownership

[For example local taxes due, VAT payable rental income/payment etc for private persons and businesses]

Back to EU Member states

6. Disposal of property

[For example capital taxes, inheritance tax, legal fees etc for private individuals and businesses]

Back to EU Member states

7. Non resident owners of property

[For example, the treatment of rental income, property development, gains on disposal etc for private persons and corporates]

Back to EU Member states

8. Sundry issues

[For example, any miscellaneous comments which may be of relevance for property investors not covered elsewhere eg. registering a property interest, building legislation etc.]

Back to EU Member states

Back to EU Member states

Lativa

Contents

1. Introduction – why buy real estate?

2. Contact details

3. Forms of property ownership

4. Taxes and other costs on property acquisitions

5. Issues during Ownership

6. Disposal of property

7. Non resident owners of property

8. Sundry issues

Back to EU Member states

1. Introduction - Latvia

This should be a brief introduction as to why real estate might be acquired eg. residential owner, business owner occupier, business owner investor, holiday property, residential investment etc.

Back to EU Member states

2. Contact Details

[Name 1][firm][telephone][email address]

[Name 2][firm][telephone][email address]

Back to EU Member states

3. Form of property ownership

[For example, outright freehold, leasehold rental etc for private persons and businesses]

Back to EU Member states

4. Taxes and other costs on property acquisition

[For example, a brief note on property tax (stamp duty), VAT, legal fees, funding costs etc for private persons and businesses]

Back to EU Member states

5. Issues during ownership

[For example local taxes due, VAT payable rental income/payment etc for private persons and businesses]

Back to EU Member states

6. Disposal of property

[For example capital taxes, inheritance tax, legal fees etc for private individuals and businesses]

Back to EU Member states

7. Non resident owners of property

[For example, the treatment of rental income, property development, gains on disposal etc for private persons and corporates]

Back to EU Member states

8. Sundry issues

[For example, any miscellaneous comments which may be of relevance for property investors not covered elsewhere eg. registering a property interest, building legislation etc.]

Back to EU Member states

Back to EU Member states

Lithuania

Contents

1. Introduction – why buy real estate?

2. Contact details

3. Forms of property ownership

4. Taxes and other costs on property acquisitions

5. Issues during Ownership

6. Disposal of property

7. Non resident owners of property

8. Sundry issues

Back to EU Member states

1. Introduction - Lithuania

This should be a brief introduction as to why real estate might be acquired eg. residential owner, business owner occupier, business owner investor, holiday property, residential investment etc.

Back to EU Member states

2. Contact Details

[Name 1][firm][telephone][email address]

[Name 2][firm][telephone][email address]

Back to EU Member states

3. Form of property ownership

[For example, outright freehold, leasehold rental etc for private persons and businesses]

Back to EU Member states

4. Taxes and other costs on property acquisition

[For example, a brief note on property tax (stamp duty), VAT, legal fees, funding costs etc for private persons and businesses]

Back to EU Member states

5. Issues during ownership

[For example local taxes due, VAT payable rental income/payment etc for private persons and businesses]

Back to EU Member states

6. Disposal of property

[For example capital taxes, inheritance tax, legal fees etc for private individuals and businesses]

Back to EU Member states

7. Non resident owners of property

[For example, the treatment of rental income, property development, gains on disposal etc for private persons and corporates]

Back to EU Member states

8. Sundry issues

[For example, any miscellaneous comments which may be of relevance for property investors not covered elsewhere eg. registering a property interest, building legislation etc.]

Back to EU Member states

Back to EU Member states

Luxembourg

Contents

1. Introduction – why buy real estate?

2. Contact details

3. Forms of property ownership

4. Taxes and other costs on property acquisitions

5. Issues during Ownership

6. Disposal of property

7. Non resident owners of property

8. Sundry issues

Back to EU Member states

1. Introduction - Luxembourg

This should be a brief introduction as to why real estate might be acquired eg. residential owner, business owner occupier, business owner investor, holiday property, residential investment etc.

Back to EU Member states

2. Contact Details

[Name 1][firm][telephone][email address]

[Name 2][firm][telephone][email address]

Back to EU Member states

3. Form of property ownership

[For example, outright freehold, leasehold rental etc for private persons and businesses]

Back to EU Member states

4. Taxes and other costs on property acquisition

[For example, a brief note on property tax (stamp duty), VAT, legal fees, funding costs etc for private persons and businesses]

Back to EU Member states

5. Issues during ownership

[For example local taxes due, VAT payable rental income/payment etc for private persons and businesses]

Back to EU Member states

6. Disposal of property

[For example capital taxes, inheritance tax, legal fees etc for private individuals and businesses]

Back to EU Member states

7. Non resident owners of property

[For example, the treatment of rental income, property development, gains on disposal etc for private persons and corporates]

Back to EU Member states

8. Sundry issues

[For example, any miscellaneous comments which may be of relevance for property investors not covered elsewhere eg. registering a property interest, building legislation etc.]

Back to EU Member states

Back to EU Member states

Malta

Contents

1. Introduction – why buy real estate?

2. Contact details

3. Forms of property ownership

4. Taxes and other costs on property acquisitions

5. Issues during Ownership

6. Disposal of property

7. Non resident owners of property

8. Sundry issues

Back to EU Member states

1. Introduction - MaltaThe property market has long been one of the most valuable asset classes in Malta with both development and construction considered as a solid investment yielding a satisfactory margin. Malta offers a wide range of both commercial and residential property, in very distinct locations. There is a broad selection of office space available: a firm can choose between purpose built office blocks, converted houses or flats or a location within some of the new, large mixed use areas currently under development. On the residential side, Malta has long been renowned for quiet retreats in the form of converted farmhouses and traditional houses of character while at the same time providing the possibility of acquiring high class apartments in new residential complexes at prices which are still considerably lower than the equivalent in mainland Europe.

Back to EU Member states

3. Form of property ownership

The main distinction that is normally made with respect to forms of property ownership is that of whether it being residential, commercial or industrial.

Within each segment one can decide to either rent or outright purchase a property for their specific use. When it comes to commercial properties there are various designated areas that are more suited for commercial dealings.

Malta offers very attractive industrial rentals. With the help of the Malta Enterprise, a government agency, incoming firms can be directed towards the right location whilst offering rates that normally average out at €10 per m².

Back to EU Member states

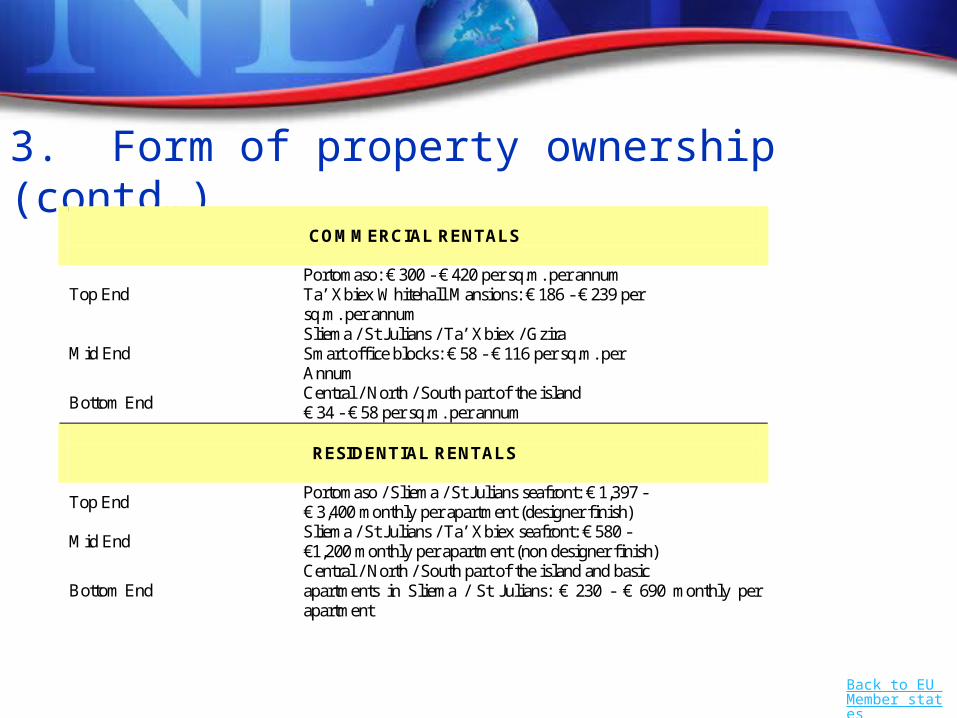

3. Form of property ownership (contd…)

COMMERCIAL RENTALS

Top End Portomaso: € 300 - € 420 per sq.m. per annum Ta’ Xbiex Whitehall Mansions: € 186 - € 239 per sq.m. per annum

Mid End Sliema / St Julians / Ta’ Xbiex / Gzira Smart office blocks: € 58 - € 116 per sq.m. per Annum

Bottom End Central / North / South part of the island € 34 - € 58 per sq.m. per annum

RESIDENTIAL RENTALS

Top End Portomaso / Sliema / St Julians seafront: € 1,397 - € 3,400 monthly per apartment (designer finish)

Mid End Sliema / St Julians / Ta’ Xbiex seafront: € 580 - €1,200 monthly per apartment (non designer finish)

Bottom End Central / North / South part of the island and basic apartments in Sliema / St Julians: € 230 - € 690 monthly per apartment

Back to EU Member states

4. Taxes and other costs on property acquisition

All property bought in Malta is subject to stamp duty at the rate of €5 per €100 or part thereof, which payment is due to the Commissioner of Inland Revenue. This percentage is based on the higher of the consideration and market value of the property and is paid in two stages, 1% at the time of signing of the preliminary agreement (konvenju) and the remaining 4% settled at the time of signing of the contract of sale. There is no property tax that is applicable to immovable property in Malta.

Notarial fees are normally circa 1% of the selling price of the immovable property and are paid by the purchaser.

Back to EU Member states

6. Disposal of property The disposal of immovable property situated in Malta gives rise to income tax. There exist two methods of settlement of this tax. A complete exemption from tax is applicable where the immovable property has been the registered main residence of the person who is making the disposal for a minimum of three years and is being sold within a year of when it was vacated.

In all other cases the following tax regime will apply:

On the signing of the Final Deed of Sale, provided the property that is being transferred has been owned for less than 5 years the seller is given an option on how to be taxed. He can either choose to be taxed under the regime whereby tax is paid on the selling price as reduced by a number of allowable deductions or he can choose to be taxed under the new Final Property Transfer Tax system whereby a final withholding tax of 12% of the transfer value is applied. If the immovable property is held for more than 5 years the aforesaid option is not available and in this instance the final withholding tax of 12% is applicable.

Apart from the above agency costs associated with the sale of property normally range from 3.5% to 5% of the total selling price of the immovable property in question.

Back to EU Member states

7. Non resident owners of property Non residents wishing to acquire immovable property in Malta require a special permit and may do so only under certain conditions. The resale of immovable property by a non-resident is allowed as long as this is to a Maltese resident. A release permit is required in other cases. Repatriation of full resale price, including profits, is allowed without complications. Since Malta joined the European Union in 2004 many of the previous restrictions have been abolished for EU citizens.

Mortgages are available for property purchase by non-residents or non-Maltese citizens residing in the islands. Renting out of property purchase is allowed in special circumstances. More than one property can be purchased in Malta by a company or trust if located in particular designated areas.

All EU citizens who have resided in Malta for a minimum of 5 years at any time preceding the date of acquisition may freely acquire immovable property without the necessity of obtaining a permit.

Back to EU Member states

7. Non resident owners of property (contd…)

Rental of property by non-residents

Non-residents have through the years realised that property in Malta yields a good return and many have opted to purchase and subsequently rent immovable property. Rentals for short or long term lets are governed by contractual lease agreements. Letting agents and property brokers generally charge fees of one month’s rental.

The letting of immovable property is exempt from Value Added Tax (VAT) except where the lessor is a limited liability company.

A non-resident deriving income from the rental of property in Malta has to be registered with the Inland Revenue Department. Payments made to non-residents in respect of rent are required by law to be made net of withholding tax at rates stipulated by law which differ according to whether the payment is being made to an individual or a limited liability company.

Back to EU Member states

8. Sundry issues

The price brackets that are normally associated with immovable property vary considerably. One would expect to pay in the region of €72,000 to €320,000 for an apartment depending on the location, whilst the cost of a village house or a farmhouse will range between €175,000 to €480,000. Prices for high end apartments, town houses and farmhouses vary between €800,000 to €2million.

Over the years the Maltese property market has enjoyed a growth rate of 8% per annum, this rate increasing to between 12% and 15% during 2005 and 2006. As an investment, property in Malta does offer some excellent opportunities. One of the advantages of Malta’s small size is that commuting times between Malta International Airport and an office is rarely greater than 20 minutes and it almost never takes more than 40 minutes to get to anywhere else on the island.

Besides appreciating in value, investment in the Maltese property market is an ideal rental investment with returns averaging 5% per annum, in a destination with over 7000 years of history, culture and over 300 days of sunshine.

Back to EU Member states

Back to EU Member states

Netherlands

Contents

1. Introduction – why buy real estate?

2. Contact details

3. Forms of property ownership

4. Taxes and other costs on property acquisitions

5. Issues during Ownership

6. Disposal of property

7. Non resident owners of property

8. Sundry issues

Back to EU Member states

1. Introduction - Netherlands

There are several reasons for businesses to buy, build or rent real estate in the Netherlands. Below is an outline of the main reasons for both businesses and private individuals.

Businesses

The Netherlands provides a strategic location to serve the markets within Europe. The central geographical position of the Netherlands, combined with accessibility and an excellent infrastructure are some of the reasons why numerous European, American and Asian companies have established their facilities in the Netherlands.

Since January 2007 the Dutch tax environment for international companies has become very attractive. The corporate tax rate has been lowered to 25.5%, which is well below the EU national average. Dividend tax has been reduced from 25% to 15%. Furthermore, a patent box with a 10% tax rate on income from innovations was introduced. Combined with other traditional features of the Dutch tax system (wide tax treaty network, participation exemption, 30% tax break for highly qualified foreign employees) the fiscal climate is one more reason to establish or expand European operations in the Netherlands.

Back to EU Member states

1. Introduction – Netherlands (cont’d…)

Private individuals

The Netherlands has a high standard of living, while maintaining an affordable life for its residents. The costs of living, housing, education and cultural activities are lower than in most Western-European countries. This makes it a very attractive place to live or to have a holiday home.

In the Netherlands people (and businesses) have long seen the benefits of buying property. In general buying is cheaper than renting for private individuals. The flexible mortgage system and tax reimbursement make it very attractive for the people who plan to stay for at least a few years. However, the Netherlands is one of the most densely populated countries in the world. This leads to situations, particularly around the major cities, where property demand exceeds supply and therefore prices become inflated beyond the reach of many potential buyers.

Back to EU Member states

2. Contact Details

Please contact one of our contact partners (tax) for more information.

KroeseWevers Tax ConsultantsEnschede office Emmen officeHans Eppink Marcel KocksTel: +31 (0)53 850 49 00 Tel: +31 (0)591 65 78 00Fax: +31 (0)53 850 49 01 Fax: +31 (0)591 61 91 [email protected]

KroeseWevers Tax Consultants is a member of Nexia Netherlandswww.kroesewevers.nl

Back to EU Member states

3. Form of property ownership The ownership of real estate is defined and regulated in the Dutch Civil Code (Burgerlijk Wetboek). The owner has the uninhibited use and enjoyment of the real estate. Ownership may however be subject to thefollowing restrictions:• Rights of other persons to the real estate• Restrictions arising out of legislation in force.

These restrictions aim at protecting rights of third parties including the government as representative forthe general interest.

Other important statute laws regarding real estate outside the Dutch Civil Code are in force, for instance, land registration (Kadasterwet).

The jurisdiction in the Netherlands recognises several forms of property ownership in which exist:Full ownership• Co-ownership• Long lease• Apartment• Servitudes• Superficies.

There are also some secondary real rights like pledge, mortgage and use.

Back to EU Member states

4. Taxes and other costs on property acquisition

Transfer tax

Real estate transfer tax (RETT) is charged for private individuals and businesses on the acquisition of Dutch real estate at 6% on the higher of the fair market value and the purchase price of the property. Also the acquisition of shares in an entity owning Dutch property can under circumstances be qualified as a deemed acquisition of property and thus be subjected to transfer tax at 6% of the market value of the underlying property, although exemptions may apply. When the property is newly constructed there is no levy of transfer tax.

VAT

VAT is generally due at the standard rate of 19% on any supply of goods and services in the Netherlands and the import of goods into the Netherlands. VAT registration is compulsory for any VAT taxable person (i.e. an individual or entity which independently carries on a business activity) irrespective of their residence, making VAT taxable supplies in the Netherlands. However, for foreign suppliers certain exceptions may be applicable whereby the customer has to self-account for the VAT due. As a result, the foreign supplier does not have to register in the Netherlands.

Back to EU Member states

4. Taxes and other costs on property acquisition (contd…)

The sale of real estate is VAT exempt, unless the property is newly constructed or less than two years old (19% VAT). However, if certain conditions are met, there is an option for businesses to let the supply become taxable.

If the property is newly constructed (or less than two years old) the Transfer tax is replaced with the 19% VAT.

Transaction costs

Total transaction costs are between 10% and 13%, of the total dwelling price for existing property, including the transfer tax (6%) legal fees and registration fees and estate agent’s commission. This is moderate by international

standards. The bulk of these costs are paid by the buyer.

Back to EU Member states

5. Issues during ownershipOwner-occupied propertyIf private individuals own a property that serves as a principal residence (at least six months a year), they should add an amount to their income in this respect. This amount is known as the notional rental value. It is a percentage of the market value of the owner-occupied property. This value is determined by the authorities of the Dutch municipality in which the property is situated. The notional rental value can be offset against interest and charges of (mortgage) loans, and against payments towards a ground lease or building and planting rights in relation to the owner-occupied property. The notional rental value only applies to the property that serves as the principal residence. For second homes – e.g., a holiday home – and other immovable property another system applies (see next). For businesses there is no such a tax on the use of property.

Rental incomeFor private persons the annual income tax on renting property is 30%. In reality it is not really an income tax, but a flat tax, with 30% levied on the assumed rental yield. The basis of this assumption is that a rental yield of 4% is made on the property. In effect, an annual tax of 1.2% is imposed on the average value (start and end of the year) of the property minus the mortgage (loan). So if your rental property yields more than 4%, the proportionate tax rate is lower.

Back to EU Member states

5. Issues during ownership (contd…)If the real estate forms part of the individual’s business enterprise or the real estate itself is very actively exploited, the individuals will be subject to income tax at progressive rates of up to 52%.

For businesses rental income on property is taxed at the standard rate of corporate income tax (CIT). As of 1 January 2009, the standard rate of CIT in the Netherlands is 25.5%, with the first € 100,000 being taxed at 20%. CIT is payable by Dutch-resident entities as well as by non-resident entities. CIT is reportable to the tax authorities on an accounting year basis. For specially defined investment institutions CIT is charged at 0% provided certain strict conditions are met.

DepreciationFor businesses, depreciation on real estate has been restricted to the assessed value, the so called WOZ, which is determined by local municipality annually. Only if the real estate is used for the companies own business depreciation is restricted to 50% of the assessed value.

VATAs a rule, rent is exempt from VAT. Parties may, however, opt for VAT-increased rent if 90% or more of the business activities of the tenant are subject to VAT.

Property taxProperty tax is charged annually by the local authorities in the Netherlands on ownership based on the market value of the property. The use of property is no longer taxed by local authorities since the year 2006. Typical rates of property tax are generally between 0.1% and 0.3% for the owner of a property.

Back to EU Member states

6. Disposal of propertyCapital gainsIn general no capital gains tax is levied on the profits realized on the sale of property owned by a private individual.

For businesses capital gains are generally chargeable to CIT at the standard rate. However, taxation of capital gains realised on the disposal of certain fixed assets such as real estate can be deferred by forming a tax-free reinvestment reserve. Such a reserve generally requires the replacement within 3 years of the disposed asset by an asset with a similar economic function.

The Dutch participation exemption, effectively exempts capital gains derived from a sale of shares in a qualifying subsidiary (having at least 5% of the shares).

Inheritance taxProperty acquired by inheritance or gift from an individual (living in the Netherlands) is subject to inheritance or gift tax. Several forms of wealth transfer such as gifts made by the testator within 180 days prior to death and the proceeds of a life insurance contract for which the testator paid the premiums are treated as an inheritance for tax purposes. Property acquired through inheritance or gift is valued at fair market value less liabilities (debts such as tax debts, funeral costs, and other expenses).

The tax is generally paid by the recipient. For both gifts and inheritances, a large number of exemptions apply.

The heirs are also required to pay transfer tax and it is calculated on the value or sales price of the acquired Dutch property at the current tax rate of 6 %. Transfer tax can be offset by gift tax on property.

Back to EU Member states

7. Non resident owners of property

Non resident owners of property are still liable for Dutch income tax in case of owning property here. They will be regarded as non-resident taxpayers for Dutch tax purposes. If someone is considered as a non-resident taxpayer, income tax in the Netherlands has to be paid on the Dutch income. However, this income need not always be taxable in the Netherlands: it may be that the Netherlands is not allowed to tax certain income under a tax treaty that the Netherlands has concluded with the country of residence.

Back to EU Member states

8. Sundry issues

System of registrationThe territory of the Netherlands is divided into land registry parcels. Each of these parcels is recorded separately with the name of the titleholders. Lease agreements, rental agreements and other facts that relate to personal rights with respect to a registered property cannot be entered in the register. Ownership of the property is only acquired by the purchaser after registration of a certified copy of the notarial deed of transfer. This also applies for the other forms of ownership and real rights mentioned in paragraph 3. Non registered rights regarding real estate cannot be invoked against a purchaser in good faith if these rights should be registered.

FinancingDutch law does not contain specific rules for entering into a loan agreement for the financing of a real estate acquisition, it provides more for rules pertaining to the furnishing of securities. In real estate financing in the Netherlands, the mortgage is still the pre-eminent form of security and most financing is still in the form of mortgage-backed loans. For the creation of mortgage rights a notarial deed and registration is needed. It is a principle of Dutch law that all creditors have resource against all assets of their debtor. Mortgages give priority against specific assets.

Back to EU Member states

Back to EU Member states

Poland

Contents

1. Introduction – why buy real estate?

2. Contact details

3. Forms of property ownership

4. Taxes and other costs on property acquisitions

5. Issues during Ownership

6. Disposal of property

7. Non resident owners of property

8. Sundry issues

Back to EU Member states

1. Introduction - Poland

This should be a brief introduction as to why real estate might be acquired eg. residential owner, business owner occupier, business owner investor, holiday property, residential investment etc.

Back to EU Member states

2. Contact Details

[Name 1][firm][telephone][email address]

[Name 2][firm][telephone][email address]

Back to EU Member states

3. Form of property ownership

[For example, outright freehold, leasehold rental etc for private persons and businesses]

Back to EU Member states

4. Taxes and other costs on property acquisition

[For example, a brief note on property tax (stamp duty), VAT, legal fees, funding costs etc for private persons and businesses]

Back to EU Member states

5. Issues during ownership

[For example local taxes due, VAT payable rental income/payment etc for private persons and businesses]

Back to EU Member states

6. Disposal of property

[For example capital taxes, inheritance tax, legal fees etc for private individuals and businesses]

Back to EU Member states

7. Non resident owners of property

[For example, the treatment of rental income, property development, gains on disposal etc for private persons and corporates]

Back to EU Member states

8. Sundry issues

[For example, any miscellaneous comments which may be of relevance for property investors not covered elsewhere eg. registering a property interest, building legislation etc.]

Back to EU Member states

Back to EU Member states

Portugal

Contents

1. Introduction – why buy real estate?

2. Contact details

3. Forms of property ownership

4. Taxes and other costs on property acquisitions

5. Issues during Ownership

6. Disposal of property

7. Non resident owners of property

8. Sundry issues

Back to EU Member states

1. Introduction - Portugal

This should be a brief introduction as to why real estate might be acquired eg. residential owner, business owner occupier, business owner investor, holiday property, residential investment etc.

Back to EU Member states

2. Contact Details

[Name 1][firm][telephone][email address]

[Name 2][firm][telephone][email address]

Back to EU Member states

3. Form of property ownership

[For example, outright freehold, leasehold rental etc for private persons and businesses]

Back to EU Member states

4. Taxes and other costs on property acquisition

[For example, a brief note on property tax (stamp duty), VAT, legal fees, funding costs etc for private persons and businesses]

Back to EU Member states

5. Issues during ownership

[For example local taxes due, VAT payable rental income/payment etc for private persons and businesses]

Back to EU Member states

6. Disposal of property

[For example capital taxes, inheritance tax, legal fees etc for private individuals and businesses]

Back to EU Member states

7. Non resident owners of property

[For example, the treatment of rental income, property development, gains on disposal etc for private persons and corporates]

Back to EU Member states

8. Sundry issues

[For example, any miscellaneous comments which may be of relevance for property investors not covered elsewhere eg. registering a property interest, building legislation etc.]

Back to EU Member states

Back to EU Member states

Romania

Contents

1. Introduction – why buy real estate?

2. Contact details

3. Forms of property ownership

4. Taxes and other costs on property acquisitions

5. Issues during Ownership

6. Disposal of property

7. Non resident owners of property

8. Sundry issues

Back to EU Member states

1. Introduction - Romania

This should be a brief introduction as to why real estate might be acquired eg. residential owner, business owner occupier, business owner investor, holiday property, residential investment etc.

Back to EU Member states

2. Contact Details

[Name 1][firm][telephone][email address]

[Name 2][firm][telephone][email address]

Back to EU Member states

3. Form of property ownership

[For example, outright freehold, leasehold rental etc for private persons and businesses]

Back to EU Member states

4. Taxes and other costs on property acquisition