Embed Size (px)

Citation preview

BACKGROUND

The Economic andPolicy Implications ofRepealing theCorporate AlternativeMinimum Tax

By

Terrence R. Chorvat, Assistant ProfessorGeorge Mason University School of Law

Michael S. Knoll, ProfessorUniversity of Pennsylvania Law School and

The Wharton School

February 2002, Number 40PAPER

Tax Foundation Background PaperISSN 1527-0408

©2002 Tax Foundation

* * *

Price: $25Subscription for four issues: $60

* * *

Tax Foundation1250 H Street, NW

Suite 750Washington, DC 20005

202-783-2760 Tel202-783-6868 Fax

About the Tax FoundationIn 1937, civic-minded businessmen envisioned an independent group of researchers who, by gathering

data and publishing information on the public sector in an objective, unbiased fashion, could counsel govern-ment, industry and the citizenry on public finance.

Six decades later, in a radically different public arena, the Tax Foundation continues to fulfill the missionset out by its founders. Through newspapers, radio, television, and mass distribution of its own publications,the Foundation supplies objective fiscal information and analysis to policymakers, business leaders, and thegeneral public.

The Tax Foundation's research record has made it an oft-quoted source in Washington and state capitals,not as the voice of left or right, not as the voice of an industry or even of business in general, but as an advo-cate of a principled approach to tax policy, based on years of professional research.

Today, farsighted individuals, businesses, and charitable foundations still understand the need for soundinformation on fiscal policy. As a nonprofit, tax exempt 501(c)(3) organization, the Tax Foundation reliessolely on their voluntary contributions for its support.

About the AuthorsMichael S. Knoll is Professor of Law and Real Estate within the Law and Wharton Schools of the Univer-

sity of Pennsylvania. Dr. Knoll received his J.D., cum laude, and his Ph.D. in Economics from the University ofChicago. Dr. Knoll is a noted expert in tax, finance, and real estate law and international trade and forensiceconomics. He has served as a visiting scholar at Boston University, New York University, Columbia University,the University of Toronto, Georgetown University, and the University of Virginia. Most recently he has written“Tax Planning, Effective Marginal Tax Rates and the Structure of the Income Tax,” (Tax Law Review, 2001), and“Of Fruit and Trees: The Relationship Between Income and Wealth Taxes,” (Southern California Law Review,2000).

Terrence R. Chorvat is Assistant Professor of Law at George Mason University. Professor Chorvat is aleading young expert in international taxation. He holds an LL.M. in Taxation from New York University, wherehe served an Acting Assistant Professor for two years. He received his J.D from the University of Chicago, andhis B.A. from Northwestern. He has published a number of articles in the tax field, including “Ambiguity andIncome Taxation” (Cardozo Law Review, 2001), “Ending the Taxation of Foreign Business Income” (ArizonaLaw Review, 2000) and “Taxing International Corporate Income Efficiently” (Tax Law Review, 2000).

Table of Contents

Executive Summary ................................................................................... 1

Introduction............................................................................................... 2

Background ................................................................................................ 2

The History of the Corporate AMT.............................................................. 3

The Structure of the Corporate AMT and Calculation ofAMT Liability ................................................................................................. 4

Depreciation ..................................................................................................... 6

Net Operating Losses ....................................................................................... 6

Foreign Tax Credits ......................................................................................... 6

Adjusted Current Earnings.............................................................................. 6

Completion Methods ....................................................................................... 7

Excess of Depletion ......................................................................................... 7

Intangible Drilling Costs ................................................................................. 7

How the Corporate AMT Affects Firms’ Behavior ................................... 7

The Corporate AMT Discourages Investment ............................................ 8

The Corporate AMT Misallocates Resources .............................................. 8

The Corporate AMT Increases Tax Planning and Compliance Costs ....... 10

The Corporate AMT is Poor Fiscal Policy ................................................... 11

The Response to Arguments in Favor of a Corporate AMT.................... 12

Claim: The Corporate AMT Improves “Fairness” ...................................... 12

Claim: The Corporate AMT Is Necessary to DiscourageInvestment in Tax Preferred Assets ............................................................ 13

Claim: The Corporate AMT is Necessary to RestrainCorporations’ Use of Tax Shelters .............................................................. 13

Conclusion ................................................................................................. 14

Notes ........................................................................................................... 15

1

Executive SummaryThe corporate alternative minimum

tax (AMT) was enacted in its current formin 1986 in response to claims that manylarge corporations were making excessiveuse of deductions and other tax prefer-ences to significantly reduce or eliminatetheir corporate income tax liability. Meantto ensure that profitable corporations paysome income tax, the corporate AMT in-stead raises little revenue, distorts invest-ment incentives and imposes heavy com-pliance costs.

Over the last fifteen years, there havebeen many calls for the repeal of the cor-porate AMT, but until last year, none everresulted in legislation that passed eitherhouse of Congress. On October 24, 2001,the House of Representatives passed, aspart of a broad economic stimulus pack-age, a provision that would repeal the cor-porate AMT. The Senate did not follow suitwhen it considered its own version of thestimulus bill, and in December the Presi-dent removed corporate AMT repeal fromthe agenda in an ultimately unsuccessfulattempt to get other provisions of the billthrough Congress. Current economic stim-ulus proposals would significantly reform,but not repeal, the corporate AMT.

In 1998, the most recent year forwhich official data are available, 18,360firms paid an additional $3.4 billion in taxbecause of the AMT. Future corporate AMTcollections are likely to be lower, around$1 billion per year, due to significantchanges enacted in 1997 that took full ef-fect in 1999. In comparison, the regularcorporate income tax raises about $200billion annually.

The corporate AMT is a parallel taxstructure, meaning that any firm that maybe affected must keep separate recordsspecific to the intricacies of the corporateAMT in addition to its regular tax and reg-ular accounting records. This requirementand the inherent complexity of the corpo-rate AMT make compliance inordiately

expensive. In fact, compliance costs asso-ciated with the corporate AMT are likelyto exceed net tax receipts.

The corporate AMT has significanteconomic effects beyond the high associ-ated compliance costs. Due to its specialrules governing depreciation, foreign taxcredits, and net operating losses—all in-tended to capture more corporate incomein the taxable base—the corporate AMTactually discourages investment and mis-

allocates scarce resources. These distor-tions ultimately result in fewer jobs, low-er wages, higher prices, and slower eco-nomic growth.

Proponents of the corporate AMT,whether they recognize these distortionsand costs or not, argue that the tax im-proves fairness, discourages investment intax preferred assets, and is necessary toprevent corporations from using tax shel-ters to eliminate their income tax liabili-ty. It is not clear, however, that the AMTdoes improve fairness or limit the abilityof corporations to avoid taxes. In any case,the corporate AMT is an extremely ineffi-cient method of addressing these per-ceived problems. Much better would beto address policy concerns through the

The corporate AMT does not increaseefficiency or improve fairness in anymeaningful way. It nets little money forthe government, imposes compliancecosts that in some years are actuallylarger than collections, and encouragesfirms to cut back or shift theirinvestments. The Congress’s bipartisanJoint Committee on Taxation wasundoubtedly correct in recommendingthat it be repealed.

2

regular corporate income tax code andeliminate the complexity and inefficien-cies associated with the corporate AMT.

The corporate AMT does not advanceany legitimate purpose; that is, it does notincrease efficiency or improve fairness inany meaningful way. It nets little moneyfor the government—roughly $1 billion ayear going forward. It imposes heavy com-pliance costs that in some years are actu-ally larger than collections, and it encour-ages firms to cut back or shift theirinvestments. The Congress’s bipartisanJoint Committee on Taxation was un-doubtedly correct in recommending thatit be repealed.

IntroductionThe corporate alternative minimum

tax (AMT) was first enacted in responseto stories in the media about profitablecorporations paying little or no federalincome tax. Meant to ensure that profit-able corporations pay some income tax,the corporate AMT instead raises little rev-enue, distorts investment incentives, andimposes heavy compliance costs.

The corporate AMT was enacted in itscurrent form in 1986 in response toclaims that many large corporations weremaking excessive use of deductions andother tax preferences to significantly re-duce or eliminate their corporate incometax liability. Over the last fifteen years,there have been many calls for the repealof the corporate AMT.1 Until last year,however, none of these calls ever resultedin a piece of legislation that passed eitherhouse of Congress. On October 24, 2001,the House of Representatives passed, aspart of a broad economic stimulus pack-age, a provision that would repeal the cor-porate AMT. The Senate did not followsuit when it considered its own version ofthe stimulus bill, and in December thePresident removed repeal of the corporateAMT from the agenda in an ultimately un-successful attempt to get other provisionsof the bill through Congress. Because thecorporate AMT continues to be an itemfor debate, now is a good time to examineits economic consequences.

BackgroundIn 1998, the most recent year for

which official data are available, 18,360firms paid additional tax because of theAMT. In that year, the Treasury collected$3.4 billion in taxes from the corporateAMT.2 This figure, however, does not re-flect the likely level of current and futurecollections for two reasons. First, signifi-cant changes enacted in 1997 were notfully implemented until 1999. Thesechanges are expected to reduce corporate

3

AMT collections by over $2 billion peryear.3 Second, corporations are able toclaim a credit against their regular incometax for alternative minimum tax paymentsmade in previous years. In some years,such as 1997 and 1998, total creditsclaimed exceed total collections. In theseyears, net corporate AMT receipts are neg-ative. Taking these two factors into ac-count, going forward, net corporate AMTcollections are expected to average about$1 billion per year.

In comparison, the regular corporateincome tax raises about $200 billion annu-ally.4 Thus, the corporate AMT accountsfor only about one half of one percent oftotal corporate income tax collections. Al-though taxes raised by the corporate AMThave been and will continue to be small,the economic activity affected by the taxis not.

One way to measure the relative eco-nomic impact of the corporate AMT is tolook at the percentage of total assets heldby affected firms. The Department of theTreasury recently reported, “Over one-quarter of all corporate assets were heldby companies paying higher taxes [in1998] due to the AMT.” The Treasury re-port also noted that the manufacturingsector is particularly hard hit by the cor-porate AMT. “Over one-half of all manufac-turing assets were held by companies pay-ing higher taxes under the AMT.”5

These latest data are in line with pastyears. According to a 1995 General Ac-counting Office study, during the first fiveyears that the current form of the corpo-rate AMT was in effect (from 1987through 1991), 49 percent of corporationswith more than $50 million in assets hadtheir tax payments increased in at leastone year. The corporations that paid theAMT in at least one year between 1987and 1991 accounted for 66.2 percent ofall assets held in corporate form.6

The History of the Corporate AMTIn 1969, Congress adopted a minimum

tax for both individuals and corporations.

The corporate minimum tax, which wasknown as an “add-on” minimum tax, wasseparate from the regular corporate in-come tax and was paid in addition to it.The base for this tax was so-called “taxpreferences” enjoyed by the taxpayer rath-er than the taxpayer’s income. Selectedtax preferences in excess of the $30,000exemption amount were subject to a 10percent tax.7 Other than an increase inthe tax rate to 15 percent in 1976, thisearly form of the minimum tax was large-

ly unchanged until the Tax Reform Act of1986 (TRA’86).

In 1986, Congress adopted the corpo-rate AMT in its current form, respondingto policy analyses and press reports thatclaimed many large and seemingly profit-able corporations paid very little or no in-come tax.8 According to the Senate Fi-nance Committee’s report on TRA’86, theprincipal objective in enacting the corpo-rate AMT was to ensure that profitablecorporations would not “avoid significanttax liability by using various exclusions,deductions and credits,” to which they areentitled under the regular tax but whichmay result in taxable income that is notviewed as accurately reflecting profitabil-ity.9

Interestingly, other provisions ofTRA’86 itself reduced the need for a cor-porate AMT by altering many of the pref-erences that enabled corporations to re-duce their tax liability. Chief among thesechanges was a modification to deprecia-

The corporate AMT raises little revenue,distorts investment incentives, andimposes heavy compliance costs.Moreover, it does not further itspurported goal of improving the fairnessof the tax system.

4

tion rules. Under previous law, the Accel-erated Cost Recovery System (ACRS) hadgreatly accelerated the depreciation de-ductions that firms could use on their taxreturns as compared with the straight-linedepreciation that they typically reportedto their investors. As a result, many oth-erwise profitable corporations were ableto report positive income on their finan-cial reports while reporting little or notaxable income on their corporate returns.

The new tax depreciation system in-troduced by TRA’86, which applies to allproperty placed in service after 1987, isoften referred to as modified ACRS(MACRS). Depreciation under MACRS isfaster than straight-line depreciation, butit is significantly slower than the depreci-ation available between 1981 and 1986under ACRS. Therefore, MACRS wouldhave solved part of the perceived problemof financially profitable corporations pay-ing too little tax by directly attacking theproblem that the corporate AMT ad-dressed indirectly.

Because of various problems with thecorporate AMT, Congress enacted somesignificant changes to the tax in 1997.

That is when Congress altered the depre-ciation rules under the AMT to bring themmore in line with the depreciation rulesfor regular taxable income. This signifi-cantly altered the size of total AMT collec-tions. Prior to 1997, corporate AMT col-lections were approximately $4 billionper year. The Joint Committee on Taxa-tion estimated that the 1997 changeswould reduce AMT payments by approxi-mately $2 billion per year.

The Structure of the CorporateAMT and Calculation of AMTLiability

The corporate AMT operates as a sep-arate corporate income tax parallel to theregular corporate income tax. Unlike theearlier add-on minimum tax that it re-placed, the current corporate AMT re-quires affected corporations to calculatetheir tax liability under two parallel taxsystems. First, a corporation calculates itsincome tax liability under the regular cor-porate income tax; then it must calculateits tax liability under the corporate AMT.As the phrase “alternative minimum tax”implies, the corporation pays the greaterof its regular tax liability or its liabilityunder the AMT. Accordingly, if a corpora-tion’s regular tax liability exceeds its liabil-ity under the AMT, it pays its regular taxliability. If, however, its liability under theAMT is greater than its liability under theregular tax, it must pay its regular tax andan additional payment of the difference.10

The additional payment of the differencebetween the tax liability calculated underthe regular corporate tax rules and thecorporate AMT rules is referred to as theAMT liability.11

In two principal ways the corporateAMT differs from the regular corporateincome tax. First, the corporate AMT rateof 20 percent is substantially below theregular corporate income tax rate of 35percent.12 Second, the tax base for thecorporate AMT, alternative minimum tax-able income (AMTI), is broader than theregular corporate income tax base.13

AMTI is calculated by adding certainpreferences and adjustments to regulartaxable income. Preferences and adjust-ments are items a corporation may take toreduce regular taxable income but whichare disallowed under the AMT. The slow-er depreciation allowed under AMT rulesis the primary adjustment accounted forin the expanded AMTI base. In addition,the AMT imposes restrictions on the useof net operating losses and the foreign taxcredit and requires a so-called “adjustment

Almost all credits against regularcorporate tax, such as the research anddevelopment credit, are disallowedagainst the AMT.

5

for current earnings.”The starting point for determining a

taxpayer’s AMT is its regular taxable in-come. In general, all rules that apply in de-termining taxable income apply in deter-mining AMTI as well. A taxpayer’s regularincome tax liability after the foreign taxcredit, but before other tax credits is re-ferred to as its regular tax liability. Thetaxpayer then adds back various “prefer-ences” and adjustments. AMTI is then re-duced by an exemption amount. The tax-payer’s tentative AMT liability (oftencalled the tentative tax) is determined byapplying the AMT tax rate to the taxpay-er’s AMTI, less any exemption amount.

The AMT permits deductions for oper-ating losses (NOLs) from prior years.However, the amount of this deductioncannot exceed 90 percent of AMTI beforethe NOL is taken into account. Almost allcredits against regular corporate tax, suchas the research and development credit,are disallowed against the AMT. The onlycredit that is allowed is the foreign taxcredit, which must be computed separate-ly for regular and AMT tax purposes.14

The corporation is allowed a creditagainst its regular tax liability for prioryears’ minimum taxes paid. If a taxpayerstarts paying the corporate AMT and nev-er returns to paying the regular tax, thenthe AMT liabilities it pays over the yearsare permanent increases in its tax liabili-ty. Alternatively, if the taxpayer sometimespays AMT but thereafter pays the regulartax often enough and in large enoughamounts so that it exhausts its AMT cred-its, then the effect of the AMT is to accel-erate the taxpayer’s tax payments, not toincrease them. In fact, in both 1997 and1998 the amount of taxes collected by theAMT was less than the amount of AMTcredit claimed against regular corporatetax payments. In 1997, the AMT resultedin $3.9 billion in taxes while the regularcorporate income tax was reduced by$4.1 billion due to AMT credits claimed.In 1998, the AMT resulted in $3.3 billionin collections, while $3.4 billion in AMT

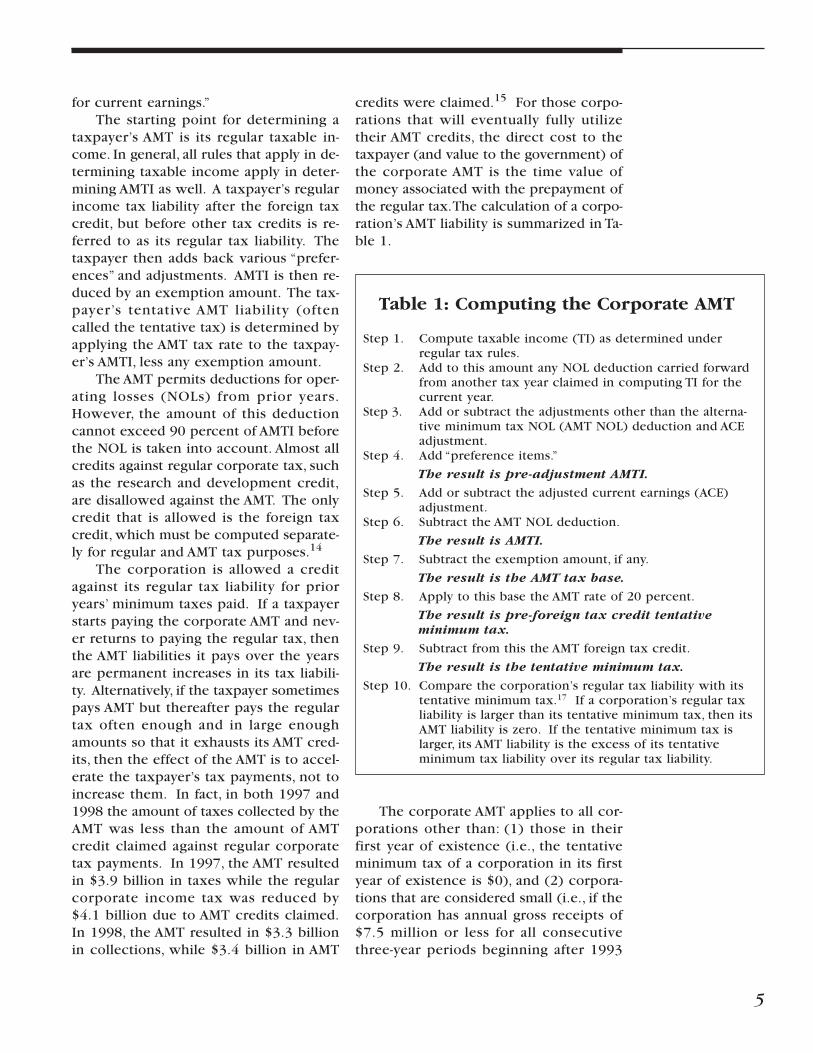

credits were claimed.15 For those corpo-rations that will eventually fully utilizetheir AMT credits, the direct cost to thetaxpayer (and value to the government) ofthe corporate AMT is the time value ofmoney associated with the prepayment ofthe regular tax. The calculation of a corpo-ration’s AMT liability is summarized in Ta-ble 1.

The corporate AMT applies to all cor-porations other than: (1) those in theirfirst year of existence (i.e., the tentativeminimum tax of a corporation in its firstyear of existence is $0), and (2) corpora-tions that are considered small (i.e., if thecorporation has annual gross receipts of$7.5 million or less for all consecutivethree-year periods beginning after 1993

Table 1: Computing the Corporate AMT

Step 1. Compute taxable income (TI) as determined underregular tax rules.

Step 2. Add to this amount any NOL deduction carried forwardfrom another tax year claimed in computing TI for thecurrent year.

Step 3. Add or subtract the adjustments other than the alterna-tive minimum tax NOL (AMT NOL) deduction and ACEadjustment.

Step 4. Add “preference items.”

The result is pre-adjustment AMTI.

Step 5. Add or subtract the adjusted current earnings (ACE)adjustment.

Step 6. Subtract the AMT NOL deduction.

The result is AMTI.

Step 7. Subtract the exemption amount, if any.

The result is the AMT tax base.

Step 8. Apply to this base the AMT rate of 20 percent.

The result is pre-foreign tax credit tentativeminimum tax.

Step 9. Subtract from this the AMT foreign tax credit.

The result is the tentative minimum tax.

Step 10. Compare the corporation’s regular tax liability with itstentative minimum tax.17 If a corporation’s regular taxliability is larger than its tentative minimum tax, then itsAMT liability is zero. If the tentative minimum tax islarger, its AMT liability is the excess of its tentativeminimum tax liability over its regular tax liability.

6

and ending before the tax year in ques-tion).16

The seven most important “prefer-ence” items and other differences be-tween the regular income tax and theAMT definition of income are deprecia-tion, net operating losses (NOL), foreigntax credits, adjusted current earnings,completion methods, excess of depletion,and intangible drilling costs.

DepreciationThe largest difference between AMTI

and regular taxable income results fromthe depreciation methods used under thetwo systems. Under the AMT, the methodof depreciation for property, other thanreal property, is the 150 percent decliningbalance method. Under the regular taxsystem, taxpayers will generally use the200 percent (double) declining balancemethod.18 Property placed in service be-fore 1999 has a longer depreciable lifeunder the AMT rules than under regulartax rules. For property placed in servicein 1999 or later, the depreciable lives un-der the corporate AMT and the regular tax

rules are the same. Conforming the de-preciable lives cuts AMT tax collectionsalmost in half.

Net Operating LossesAMTI is computed using the AMT

NOL deduction rather than the regular taxNOL deduction. The amount of the AMTNOL that may be deducted from AMTIcannot exceed 90 percent of AMTI beforethe AMT NOL is taken into account. Under

the regular tax, if a corporation has suffi-cient NOLs from prior years, it can reduceits taxable income for the current yeardown to zero. This allows the corporationto average out taxable income over sever-al years, which is viewed as more accu-rately reflecting the company’s total tax-able income.

Foreign Tax CreditsThe AMT foreign tax credit is calculat-

ed in much the same way as the foreigntax credit allowed under the regular tax,except that the foreign tax credit limit iscalculated using AMTI instead of taxableincome. The foreign tax credit limit isequal to the total U.S. tax (calculated be-fore the foreign tax credit) multiplied bya fraction of foreign source income in thenumerator and total worldwide income inthe denominator. For AMT purposes, theforeign tax credit limit, the amount ofworldwide income, and amount of foreignsource income are recalculated using AMTrules. The amount of U.S. tax is also recal-culated using AMT liability. When calculat-ing the foreign tax credit limit for AMTpurposes, the amount of the credit takencannot exceed 90 percent of the AMT(calculated without taking into accountthe credit and the AMT net operatingloss).

Adjusted Current EarningsOne of the most administratively bur-

densome of the differences between thetwo taxes results from the rules dealingwith “adjusted current earnings” (ACE). Acorporation’s AMTI for any tax year is in-creased by 75 percent of the excess of thecorporation’s ACE over its AMTI deter-mined without regard to the ACE adjust-ment and the AMT NOL.19

ACE is determined by statutory rulesused for calculating “earnings and profits.”This is a separate definition from eitherAMTI or regular taxable income, althoughit too, like AMTI, is calculated by startingwith regular taxable income and thenmaking various adjustments. Specifically,

One of the most administrativelyburdensome differences betweencalculating regular tax liability and AMTliability results from the rules dealingwith adjusted current earnings (ACE).

7

Corporations that pay the AMT have theirdepreciation schedules stretched out, theirdepletion allowances reduced, and theiruse of NOLs and foreign tax creditscurtailed.

tax-exempt interest is included, the last-in,first-out method of accounting cannot befully used, the installment sale method isdisallowed, and the 70 percent dividendsreceived deduction is disallowed. The ACEadjustment requires that a corporationkeep at least three sets of books to calcu-late its taxes: one for regular tax, one for“normal” AMTI and a third for the ACEadjustments.

Completion MethodsAMTI is computed using the percent-

age-of-completion method of accountingfor long-term contracts other than home-construction contracts. This method re-quires a corporation to “book” income as-sociated with work in progress ratherthan waiting until the full contract hasbeen completed. In contrast, the complet-ed contract method, which is often al-lowed for regular tax purposes, allows thetaxpayer to defer income until a contractis complete rather than having to includeportions in gross income as the work pro-ceeds.

Excess of DepletionThe excess of any percentage deple-

tion deductions over the year-end adjust-ed AMT basis of the property on whichthe deduction is claimed is considered apreference and so must be added back toAMTI.

Intangible Drilling CostsWith respect to oil, gas and geother-

mal properties, intangible drilling costs(IDCs) are a preference to the extent thatthe excess IDCs for the tax year exceed65 percent of the net income from theproperties for the year, unless the corpo-ration elects to amortize them over a 60-month period.

How the CorporateAMT Affects Firms’Behavior

Proponents of the corporate AMT fre-quently justify it as an attempt to preventprofitable corporations from using somany deductions, credits and other legalpreferences that they do not have to payany tax or pay only a token amount. Al-though the corporate AMT can increasetax collections from profitable firms thatwould otherwise pay little or no federalincome tax, it does more than just in-crease corporate income tax collections.The AMT affects a wide range of behavior.

The corporate AMT affects decisionsmade and actions taken by firms becauseit changes the tax consequences of these

choices. Corporations that pay the AMThave their depreciation schedulesstretched out, their depletion allowancesreduced, and their use of NOLs and for-eign tax credits curtailed. These changes,which increase their tax bills, are at leastpartially offset by AMT credits they re-ceive for the additional tax they pay as aresult of the corporate AMT. These cred-its can be used in future years to offsettheir regular tax liability. However, be-cause these credits cannot be used to re-duce taxes below what they would bewith the corporate AMT, many companiescarry AMT credits on their books foryears. Companies with excess credits

8

“Loopholes” that the AMT curtails are thesame incentives that Congress bestowedto encourage such investment. Thecorporate AMT preferences andadjustments reduce the value of theseincentives, thereby discouraging affectedfirms from making such investments.

have their taxes increased by the AMT andhave their incentives altered by it thesame as corporations that currently paythe AMT. This is one reason why the cor-porate AMT can have effects that are dis-proportionate to total taxes collected.

There are four basic classes of argu-ment against the corporate AMT. First, itdiscourages investment. Second, it misal-locates resources. Third, it is administra-tively burdensome. Fourth, it makes forpoor fiscal policy.

The Corporate AMT DiscouragesInvestment

The corporate AMT discourages affect-ed firms from investing in plant, equip-ment and other productive activities.There are two reasons for this. First andmost obviously, “loopholes” that the AMTcurtails are the same incentives that Con-gress bestowed to encourage such invest-ment. The corporate AMT preferences andadjustments reduce the value of these in-

centives, thereby discouraging affectedfirms from making such investments.

Second and less obviously, the re-duced corporate AMT rate, coupled withcorporate AMT credits that can be usedagainst the corporation’s regular tax liabil-ity in the future, reduce the effective mar-ginal tax rate for firms affected by thecorporate AMT. Such a reduction in thefirm’s effective marginal tax rate willmake tax-advantaged investments less at-

tractive. Thus, not only are AMT firms dis-couraged from investing in plant andequipment, they are also discouragedfrom such activities as advertising and re-search because these are expendituresthat can be immediately expensed. On theother hand, the reduction in tax rate ex-perienced by AMT firms will encouragethem to invest in activities that are not taxadvantaged, such as increasing cash re-serves.

The most frequently reported adjust-ments and preferences on regular corpo-rate tax returns are for depreciation andthe ACE adjustment.20 The rationale forproviding such incentives is that the in-vestments have beneficial effects on theeconomy that go beyond the private re-turn earned by the investor. If the exist-ence of so-called positive externalities canjustify the special tax benefits, then itmakes no sense to provide these benefitsthrough one provision of the tax code(the regular corporate income tax) and totake them away with another (the corpo-ration AMT). Alternatively, if they are notjustified, they should not be provided inthe tax code at all.

The Corporate AMT MisallocatesResources

The corporate AMT not only discour-ages investment, but also misallocates re-sources because it changes who makesspecific investments, the legal form theseinvestments take, how they are financed,and when they occur. These changes areall costly, and economically wasteful.

One of the keys to understanding theconsequences of the corporate AMTcomes from recognizing that it does notdirectly affect all firms. The corporateAMT does not prevent all firms from usingtypical tax preferences including deduc-tions. It only affects a firm whose tax lia-bility is increased or would be increasedby the corporate AMT if the firm claimedall deductions, credits and other prefer-ences permitted under the regular tax.21

The investment incentives of firms that

9

have not had their tax liabilities affectedby the corporate AMT are not changed.The corporate AMT, thus, introduces anunlevel playing field between AMT andregular firms because the tax paid on thesame investment varies depending uponwhether a firm is paying the regular taxor the AMT.

Moreover, it is not surprising thatfirms in specific industries (such as man-ufacturing, mining and public utilities) aremore likely to be affected by the corpo-rate AMT than those in other industries.This is because the AMT decreases theexpected value of any deductions taken inyears in which the corporation will gen-erate a loss by reducing the amount ofdeductions and restricting the use ofNOLs. This reduces the incentive to in-vest in depreciable property, engage inresearch and development, or incur anyother deductible expenses, including sal-aries of new hires. This change in invest-ment incentives is not tied in any rationalway to any legitimate governmental pur-pose (e.g., improving the efficiency of theeconomy or the provision of publicgoods).

The AMT also influences the form cer-tain investments take. One of the largestand most important differences betweenthe corporate AMT and the regular corpo-rate income tax is the treatment of depre-ciation. For tax purposes, the lessor ofleased property is generally consideredthe owner and therefore is able to depre-ciate the leased property. The lessee can-not depreciate the property but can de-duct lease payments from its regulartaxable income. Because lease expensesare not an adjustment or preference item,an AMT firm that leases property does notsuffer the same disadvantage as a firm thatowns property. Moreover, many of thebenefits of accelerated depreciation canbe passed through to the lessee in theform of reduced lease payments.22 Thus,to the extent that the AMT causes firms tolease instead of own property, the effectis to impose additional costs of writing

leases and the agency costs from separat-ing the user from the residual claimant.

The AMT also discourages firms fromusing debt relative to equity to financecapital investments. Because dividendsand retained earnings are not deductiblefrom corporate income but interest pay-

ments are, a firm with more debt in itscapital structure will (other things beingequal) report smaller taxable income andpay a smaller tax liability. This smaller li-ability makes it more likely that the debt-financed firm will have to pay corporateAMT than an equity-financed corporation.Thus, the corporate AMT encourages firmsto use less debt than they otherwisewould.

The AMT can also influence the tim-ing of investment. Because AMT firmshave higher hurdle rates for investment indepreciable property than other firms,they have a greater incentive to investbefore they are subject to the AMT or af-ter they come out of it. This encouragesfirms to shift the timing of their invest-ments, an especially undesirable resultfrom a general economic perspective be-cause of the cyclical effects of the AMT.

Finally, because AMT liability is calcu-lated on a consolidated basis, firms thatexpect to find themselves subject to theAMT have an incentive to merge with oth-er firms. If the combined entity wouldnot be subject to the AMT, but one of thetwo entities individually would, then thecorporations have reduced their joint taxliability through the merger.23 This incen-tive is likely to be especially strong in thecase of conglomerate mergers becausethe incomes of the various businesses are

The tax compliance costs of firms subjectto the corporate AMT are 18 to 26 percenthigher than firms that are not subject tothe corporate AMT.

10

Because more firms are subject to theAMT during economic downturns thanduring periods of growth, the corporateAMT increases collections duringrecessions and decreases them duringbooms. This artificially accentuatesnatural market cycles and thereby tendsto destabilize the economy.

likely to be uncorrelated. As a result, theconstituent firms of a conglomerate canprobably offset one another’s tentativeAMT liability. The investigation of themany tax planning costs associated withmergers and the preparation for mergersis outside the scope of this paper. Sufficeit to say that the costs are considerable,and like all the other costs described inthis section, they arise because of the cor-porate AMT and not for an economicallybeneficial reason.

The Corporate AMT Increases TaxPlanning and Compliance Costs

The corporate AMT complicates thetax system and makes compliance morecostly. According to a 1995 survey of largecorporations conducted by Joel Slemrod

and Marsha Blumenthal, the tax compli-ance costs of firms subject to the corpo-rate AMT are 18 to 26 percent higher thanfirms that are not subject to the corporateAMT.24 Most of the additional cost is de-rived from supplementary planning,record keeping, and form completion re-quired by the corporate AMT rules. Forexample, instead of calculating theamount of tax owed once, the corporateAMT requires that each corporation thatmight potentially have to pay the tax keepat least three sets of general accountingrecords: one for regular tax compliancepurposes, one for AMTI calculations, and

a third for the ACE adjustments. Withinthese three sets of books, each firm mustkeep as many as five sets of depreciationrecords.

For two reasons, the Slemrod and Blu-menthal estimates of AMT compliancecosts cannot be directly translated into anestimate of the aggregate cost of all busi-nesses complying with the corporate AMT.First, firms that are subject to the corpo-rate AMT are likely to have more compli-cated tax returns and more complex taxsituations. For example, they are likely touse more depreciable property in theirbusinesses and have the additional cost ofdealing with those rules. This would sug-gest that the Slemrod and Blumenthalnumbers overestimate the increased costof complying with the corporate AMT.

Second, many companies that do nothave their tax liabilities increased by thecorporate AMT still must make AMT calcu-lations and maintain the necessaryrecords. Of the 365 respondents in thesurvey, 198 firms were not currently sub-ject to the corporate AMT, yet 184 of the198 kept the necessary records and madethe relevant corporate AMT calculations.That non-AMT firms must keep therecords necessary to calculate the corpo-rate AMT suggests that Slemrod and Blu-menthal’s estimate of the additional com-pliance costs incurred by AMT firms couldunderestimate the total cost of complyingwith the corporate AMT.

Another detail of the methodologyimplies that their findings may substantial-ly underestimate aggregate compliancecosts. Specifically, to quantify AMT compli-ance costs, Slemrod and Blumenthal com-pared the compliance costs of firms cur-rently paying the AMT with those who arenot, but they did not exclude the AMT-re-lated compliance costs of the firms in thelatter group. Instead, these AMT-relatedcompliance costs are incorporated intothe firm’s overall compliance costs and as-sumed to be associated with the compa-ny’s regular tax liability. This assumptionminimizes the difference between the

11

compliance costs faced by AMT firms andcompliance costs faced by regular taxfirms.

The Slemrod and Blumenthal surveyprovides further support for the claimthat costs of complying with the corpo-rate AMT are very high. Three hundredand fifteen of the 365 tax officers whoresponded to the survey provided a re-sponse to the question, “What aspect ofthe current federal tax code was most re-sponsible for the cost of complying withthe tax system?” The two most frequent-ly mentioned provisions were deprecia-tion (118 responses) and the corporateAMT (115 responses). The third most fre-quently mentioned provision was the uni-form capitalization (UNICAP) rules (85 re-sponses) and the fourth was compliancewith international or foreign taxes (44 re-sponses).

The survey also asked, “What featuresof the Tax Reform Act of 1986 most con-tributed to complexity?” The answer mostoften given was the corporate AMT, whichwas mentioned by more than half of theresponders. Specifically, of the 311 firmsresponding to the question, 189 men-tioned the corporate AMT. The next mostcommon response, with 138 mentions,was the UNICAP rules.

Finally, Slemrod and Blumenthal askedrespondents to suggest reforms thatwould simplify compliance. Of the 256respondents answering this question, 75recommended greater uniformity betweenfederal and state tax systems and 42 rec-ommended greater uniformity betweentaxable income and financial accountingincome. However, the current tax provi-sion that drew the most criticism was thecorporate AMT. Sixty-two respondents sin-gled it out: 38 called for its elimination, 11recommended it be simplified, and 13proposed that the ACE adjustment beeliminated. In contrast, only 19 surveysmentioned the UNICAP rules and only 13surveys mentioned the foreign tax credit.

Another indication of the high compli-ance costs associated with the corporate

AMT is the amount of money that corpo-rations spend each year just filling out IRSpaperwork. A previous Tax Foundationpaper included an estimate based on IRSpaperwork calculations that corporationsspend some 17.3 million hours just fillingout AMT-related tax forms. At a very con-servative cost of $34.66 per hour, this to-tals $600.1 million per year.25

The Corporate AMT is Poor FiscalPolicy

As a matter of fiscal policy, policymakers frequently wish to reduce taxeswhen the economy is in a slump and toincrease taxes when the economy is indanger of overheating. The idea is thatputting money into private hands canstimulate spending that will bring theeconomy out of a recession or possiblyprevent one from occurring. Similarly, re-moving money from the private sectorwhen the economy is in danger of over-heating can help stave off an inflationaryspiral.

Putting aside arguments for or againstthis general policy, the problem with us-ing taxes as an instrument of fiscal policyis that it takes time to enact tax policychanges and additional time for thosechanges to have a real economic impact.

Because of the delay in seeing an effectfrom tax changes, economists are skepti-cal of the use of targeted tax policy as aninstrument of fiscal policy.

However, tax polices that automatical-ly decrease revenues when the economyis turning down and increase collectionsin booms are viewed by many economistsas having a stabilizing effect on the econ-

The most common arguments advancedin favor of the corporate AMT take thebroad form that a corporate AMT willmake the tax system fairer.

12

omy. Thus, income tax systems, whetherflat or progressive, are often viewed asmore fiscally prudent than head taxes be-cause collections decrease during reces-sions and increase during booms. Thecorporate AMT, however, works in exact-ly the opposite direction. Because morefirms are subject to the AMT during eco-nomic downturns than during periods ofgrowth, the corporate AMT increases col-lections during recessions and decreasesthem during booms. This artificially accen-tuates natural market cycles and therebytends to destabilize the economy.

As an instrument of fiscal policy, thecorporate AMT does more than take mon-ey out of private hands during recessions.It also tends to discourage corporationsfrom investing in new plant and equip-ment.

Corporations are pushed into the AMTduring recessions because their incomesfall. Because firms subject to the AMThave higher hurdle rates for investmentthan firms subject to the regular incometax, the AMT discourages firms from in-vesting during recessions. Because in-creased investment is one road out of re-cession, the corporate AMT has theundesirable effect of making such in-creased investment and economic recov-ery less likely. The ultimate effect is typi-cally the artificial prolongation ofeconomic downturns.

The Response toArguments in Favorof a Corporate AMT

Having described the argumentsagainst the corporate AMT — that it dis-courages investment, misallocates resourc-es, creates excess compliance costs, and iscontrary to sound fiscal policy — we turnto the proponents. The most commonarguments are that it improves the fair-ness of the tax system; that it discourag-es investment in tax preferred assets; andthat it is necessary to prevent corpora-tions from using tax shelters to eliminatetheir income tax liability.

Claim: The Corporate AMTImproves “Fairness”

The most common arguments ad-vanced in favor of the corporate AMT takethe broad form that a corporate AMT willmake the tax system fairer. This argumentusually takes one of two different forms:corporations should pay more in taxes;and a corporate AMT promotes verticalfairness. In its simplest form, the argumentthat corporations should pay higher taxescan be summarized by the often-citedquotation of Robert S. McIntyre, the direc-tor of Citizens for Tax Justice, “It’s a scan-dal when members of the Fortune 500pay less in taxes than the people whowipe their floors or type their letters.”26

At some level, this observation has an ob-vious emotional appeal. The balancesheets and income statements of manycorporations show large cash flows andassets, including sometimes large amountsof cash on hand. It seems obvious thatthey can pay taxes. There are, however,two problems with this line of argument.

First, even assuming that corporationsshould pay more taxes, the corporate AMTis an especially poor way of seeing thatthey do. Because of its high compliancecosts, low yield, and the misallocations it

13

causes, the corporate AMT is a very inef-ficient way to collect taxes from corpora-tions.27 Far more effective would be toeliminate the corporate AMT and eitherraise the corporate tax rate (less than onepercent) or reduce across the board thepreferences that reduce firms’ taxable in-come relative to their economic or bookincome. Indeed, either change could eas-ily replace the taxes collected by the cor-porate AMT while at the same time prac-tically eliminating the full cost ofcomplying with the corporate AMT.

Second, it is important to rememberthat corporations do not pay taxes, peoplepay taxes. Ultimately, the economic bur-den of the corporate income tax, includ-ing the AMT, must be borne by individualworkers, customers, and shareholders.28

While the specific incidence of the corpo-rate income tax has been a particularlycontentious issue, the fact remains thatpeople pay taxes and the fairness of thecorporate AMT should be evaluated basedon its consequences for individuals.

Many proponents of the corporateAMT justify the corporate AMT by arguingthat it extracts tax dollars from wealthierpeople, increasing tax progressivity, or aseconomists would say, improving verticalequity.29 There is a long-standing and ex-tensive debate over whether the tax sys-tem should be progressive and if so, howprogressive.30 We do not intend to join inthat debate in this paper, but what can besaid here is that eliminating the corporateAMT would have little if any effect on theoverall progressivity of the corporate in-come tax or taxes in general.

If proponents argue that the corpo-rate AMT increases progressivity becausewealthier people invest in AMT-suscepti-ble corporations, then they are probablyincorrect. There is probably no differencein the wealth of the shareholders in firmsthat are affected by the AMT and thosethat are not.

Alternatively, if proponents argue thatthe corporate AMT increases progressivi-ty by taxing capital, which is more often

owned by the wealthy, the argument hassome merit. However, any increase in cor-porate taxes would have the same effect.Accordingly, if a general increase in corpo-rate taxes is desirable, Congress shouldincrease corporate tax collections direct-ly either by raising tax rates or cuttingback on the preferential treatment provid-ed within the code, such as accelerateddepreciation. Either would raise corpo-rate taxes without incurring the compli-ance and other inefficiency costs associat-ed with the corporate AMT.

Claim: The Corporate AMT IsNecessary to DiscourageInvestment in Tax Preferred Assets

Another argument that is sometimesmade in support of the corporate AMT isthat it discourages investment in tax pre-ferred assets. As described above, much ofthe impact of the AMT is to change theform of the investment rather than to pre-vent it. Of course, to some extent thecorporate AMT does discourage invest-ment in tax preferred assets. However, itdoes so in a manner that is much morecostly than simply reducing preferences.A better policy would be to reduce pref-erences across the board. If lawmakersthink depreciation is too rapid or the de-pletion allowance for oil or natural gas istoo high, they should change it directly.

The current compromise—large pref-erences and a corporate AMT—is a poorsolution. It is the worst of both alterna-tives, akin to giving with the left hand andtaking with the right. It does not gener-ally discourage firms from making the taxfavored investments. It only discouragesthose firms that are subject to the AMTfrom doing so.

Claim: The Corporate AMT isNecessary to RestrainCorporations’ Use of Tax Shelters

Another argument that is sometimesmade by proponents of the corporateAMT, or is at least implied by their com-ments, is that the corporate AMT is neces-

14

sary to prevent corporations from usingabusive tax shelters to eliminate their tax-es. In the last five years or so, the mediahas focused a bright light on corporatetax shelters. As a result, there is a concernthat corporations are making widespreaduse of abusive tax shelters. The propo-nents of the corporate AMT are con-cerned that its repeal would unleash thetax shelter market.

There are several facts that runcounter to this claim. First, there are le-gal and nonlegal constraints on tax shel-ter activity. Admittedly, these constraintsare imperfect, but they do operate. Sec-ond, and more to the point, the corporateAMT does little to constrain such activitybecause a corporation’s managers can stilleliminate their firm’s tax liability throughtax shelters. The corporate AMT simplyrequires them to use more shelters. Thecost of this additional sheltering activity isprobably minimal (because the docu-ments are already drawn up and sheltersare often priced as a percentage of the taxsaved), but any extra time spent creatingor finding additional shelters is time notspent in economically productive activity.

ConclusionFor the first time since its enactment

fifteen years ago, Congress had before it areal opportunity to repeal the corporateAMT. Repeal would have had significantpositive economic effects without sub-stantially reducing the federal govern-ment’s corporate income tax collections.The corporate AMT does not advance anylegitimate purpose (it does not increaseefficiency or improve fairness in anymeaningful way); it nets little money forthe government (roughly $1 billion a yeargoing forward); it imposes heavy compli-ance costs (likely larger than net collec-tions); and it encourages firms to cut backor shift their investments.

15

Notes1 See, for examples, “Statement of Mark A.

Bloomfield and Margo Thorning, AmericanCouncil for Capital Formation, Before theHouse Committee on Ways and Means,” June 6,1991, and Andrew Lyon, Cracking the Code:Making Sense of the Corporate AlternativeMinimum Tax (1997) pp. 129–137.

2 Patrice Treubert and William P. Jauquet,“Corporate Income Tax Returns–1998” SOIBulletin, Summer 2001, Volume 21, No. 1, pp.66–99.

3 Joint Committee on Taxation, Estimated BudgetEffects of the Conference Agreement on theRevenue Provisions of H.R. 2014, the “TaxpayerRelief Act of 1997,” JCX-39-97, July 30, 1997,p. 3.

4 John S. Barry, “The Corporate Tax Burden,” TaxFoundation Special Report No. 107, October2001, Tax Foundation, Washington, DC.

5 “Treasury Releases Data on the CorporateAlternative Minimum Tax,” Treasury News, TheDepartment of the Treasury, PO-762, November6, 2001.

6 “Experience with the Corporate AlternativeMinimum Tax,” (Washington, DC: GeneralAccounting Office), GAO/GGD-95-88, April1995.

7 Unlike the current corporate AMT, tax creditswere not restricted.

8 For example, Citizens for Tax Justice issued areport stating that more than 100 of theFortune 500 corporations had not paid anyfederal income tax in at least one year duringthe early 1980s. Robert S. McIntyre and DavidWilhem, “Corporate Taxpayers and CorporateFreeloaders: Four Years of Continuing, LegalizedTax Avoidance by America’s Largest Corpora-tions 1981-1984,” (1985). Many similar studieshad been issued for a number of years. Seee.g., Thomas Edsall, “Study Says Some FirmsPaid No U.S. Taxes,” The Washington Post,December 15, 1981.

9 Senate Committee on Finance, “Report on theTax Reform Act of 1986,” Report No. 99-313,May 29, 1986, Title XI — Minimum TaxProvisions.

10 For purposes of determining whether acorporation’s AMT liability or its regular taxliability is larger, the regular tax does notinclude the accumulated earnings tax, thepersonal holding company tax, the built-ingains tax, the tax on excess passive income ofS corporations and additional taxes due to aninvestment credit recapture or low-incomehousing recapture.

11 This definition of a corporation’s AMT taxliability ensures that the additional revenueraised by the corporate AMT equals thecorporate AMT liability.

12 For large corporations, the regular corporateincome tax is 35 percent. It is progressive atlower income levels and provides for recaptureof the benefit of lower rates at higher incomesas described in the following table:

Taxable Income Tax Rate

$50,000 or less 15%$50,000 to $75,000 25%$75,000 to $100,000 34%$100,000 to $335,000 39%$335,000 to $10,000,000 34%$10,000,000 to $15,000,000 35%$15,000,000 to $18,333,333 38%over $18,333,333 35%

The extra 5 percent tax on income between$100,000 and $335,000 and the extra 3percent tax on income between $15,000,000and $18,333,333 are intended to “catch up” onthe lower rates applied under $75,000 andunder $10,000,000. The net effect is that if acorporation’s taxable income is above$335,000, but less than $10,000,000, theaverage tax rate on all income is 34 percent; ifcorporate income is above $18,333,333, theaverage tax rate on all income is 35%.

13 The corporate AMT provides that tax isassessed on AMTI less an exemption amount.The maximum exemption amount for corpora-tions is $40,000. It is phased out at the rate of25 cents for every dollar of AMTI in excess of$150,000. Thus, the exemption amount is $0for corporations having AMTI of $310,000 ormore. For most corporations, the exemptionamount will be zero, so they are effectivelytaxed at a 20 percent flat rate.

14 The credit is equal to the foreign income taxespaid, however it is subject to a limit equal tothe amount of U.S. income tax owed (beforetaking the foreign tax credit into account)multiplied by the foreign source income of thetaxpayer divided by the worldwide income ofthe taxpayer. This must be calculated separate-ly for AMT purposes because both the amountof U.S. tax owed and the definition of incomeare different for AMT purposes that for regulartax purposes.

15 Treubert and Jauquet, ibid., p. 66.16 Regulated investment companies (RICs) and

real estate investment trusts (REITs), which areexempt from the regular tax, are not subject toAMT. Organizations that operate in theseforms have to apportion items among theirshareholders who will include them in theirown individual AMT calculations. The charac-ter as preference items is determined at theentity level, which is then passed through toshareholders. The AMT applies on a consolidat-ed basis and the AMT liability must be comput-ed on a consolidated basis. Foreign corpora-tions are also subject to the AMT, but only ontheir income and deductions that are effective-

16

ly connected with the conduct of a U.S. tradeor business.

17 For the purpose of this calculation, the regulartax liability is calculated without AMT credits.

18 With both the 150 and 200 percent decliningbalance methods, the taxpayer switches to thestraight-line method for the first tax year forwhich the straight-line method (using theadjusted basis as of the beginning of the year)yields a higher allowance. If, however, thetaxpayer uses the straight-line depreciation forregular tax purposes, it also will use thatmethod for AMT purposes. For purposes ofboth the AMT and the regular tax, real proper-ty is depreciated on a straight-line basis.

19 Likewise, a corporation’s AMTI is reduced by75 percent of the excess of the corporation’spre-adjustment AMTI over its ACE. Thereduction cannot exceed the excess of thetotal positive adjustments for all prior yearsover the total negative adjustments for all prioryears.

20 Lyon, ibid., pp. 40-41.21 A corporation’s tax liability is increased by the

corporate AMT if it pays the tax, has AMTcredits that it cannot currently use becausethat would drive its AMT liability below itsregular liability, or is paying the regular tax andhas declined to make investments that wouldhave put it into the corporate AMT. At themargin, such firms are all under the AMT. TheDepartment of the Treasury recently reportedthat in 1998, 30,226 companies had increasedtax liabilities due to the corporate AMT. 18,352companies actually paid the AMT and 11,874companies “had their use of tax credits limitedby AMT rules.” “Treasury Releases Data on theCorporate Alternative Minimum Tax,” TreasuryNews, The Department of the Treasury, PO-762,November 6, 2001.

22 The Department of the Treasury estimated that84 percent of the benefits went to the lessees.“Preliminary Report on Safe-Harbor LeasingActivity in 1981,” 15 Tax Notes 85 (1982).

23 This benefit exists whether the AMT firmeventually uses its credits or not, but thebenefit of a merger is greater if it does notexhaust them because there is a permanentreduction in tax from the merger if it does notexhaust the credits, but only a timing benefit ifit eventually would use its credits.

24 Joel B. Slemrod and Marsha Blumenthal, “TheIncome Tax Compliance Cost of Big Business,”Public Finance Quarterly, Vol.24, No. 4,October 1996, pp. 411-438.

25 J. Scott Moody, “The Cost of Complying withthe U.S. Federal Income Tax,” Tax FoundationBackground Paper, No. 35, November 2000,Tax Foundation.

26 As reported in Jeffrey H. Birnbaum and Alan S.Murray, Showdown at Gucci Gulch: Lawmak-ers, Lobbyists and the Unlikely Triumph ofTax Reform (New York, NY: Random House)1987, p. 12.

27 Some economists advocate replacing thecorporate income tax with a value added tax(VAT) on the grounds that the corporateincome tax is a particularly inefficient tax. SeeHarvey Rosen, Public Finance, 5th ed. (Colum-bus, OH: McGraw-Hill Higher Education) 1999,p. 449

28 Michael L. Marlow, Ph.D., “A Primer on theCorporate Income Tax: Incidence, Efficiency,and Equity Issues,” Tax Foundation Back-ground Paper, No. 38, November 2001, TaxFoundation, Washington, DC.

29 A tax system is progressive if the ratio of thetax paid by an individual to his income tendsto increase with his income. That is to say, aprogressive tax system is one in which theaverage tax rate is an increasing function ofincome.

30 Joseph Bankman and Thomas Griffith, “SocialWelfare and the Rate Structure: A New Look atProgressive Taxation,” 75 California Law Review,December 1987, pp. 1905–1967.