Embed Size (px)

Citation preview

Balance Sheet: Reporting Liabilities

Publication Date: June 2021

Balance Sheet: Reporting Liabilities

Copyright © 2021 by

DELTACPE LLC

All rights reserved. No part of this course may be reproduced in any form or by any means, without permission in

writing from the publisher.

The author is not engaged by this text or any accompanying lecture or electronic media in the rendering of legal,

tax, accounting, or similar professional services. While the legal, tax, and accounting issues discussed in this

material have been reviewed with sources believed to be reliable, concepts discussed can be affected by changes

in the law or in the interpretation of such laws since this text was printed. For that reason, the accuracy and

completeness of this information and the author's opinions based thereon cannot be guaranteed. In addition,

state or local tax laws and procedural rules may have a material impact on the general discussion. As a result, the

strategies suggested may not be suitable for every individual. Before taking any action, all references and citations

should be checked and updated accordingly.

This publication is designed to provide accurate and authoritative information in regard to the subject matter

covered. It is sold with the understanding that the publisher is not engaged in rendering legal, accounting, or other

professional service. If legal advice or other expert advice is required, the services of a competent professional

person should be sought.

—-From a Declaration of Principles jointly adopted by a committee of the American Bar Association and a

Committee of Publishers and Associations.

All numerical values in this course are examples subject to change. The current values may vary and may not be

valid in the present economic environment.

Course Description

A liability is a legal debt or obligation that arises during business operations. A current liability, such as accounts

payable, is payable within one year. A noncurrent liability, such as bonds payable, long-term loan, and finance

lease, is an obligation that is due in over a year. This course discusses generally accepted accounting principles

(GAAP) for reporting both current and noncurrent liabilities on the balance sheet.

Learning Objectives

After completing this course, you should be able to:

1. Recognize basic principles of reporting liabilities on the balance sheet

2. Identify classification and characteristics of liabilities

3. Recognize the appropriate rules to account for contingencies

4. Identify accounting procedures for accounts payable and deferred revenues

5. Recognize rules for the troubled debt, environmental liabilities, and lessee accounting

6. Recognize the accounting procedures for bonds payable and notes with no stated rate of interest

Field of Study Accounting

Level of Knowledge Intermediate

Prerequisite Basic Accounting

Advanced Preparation None

Table of Contents Chapter 1: Financial Reporting Standards ...................................................................................... 1

Objectives of Financial Reporting ................................................................................................................1

Characteristics of Liabilities ........................................................................................................................4

Present Obligation .............................................................................................................................................................. 4

Obligation to Provide Economic Benefits ........................................................................................................................... 6

Recognition and Measurement ...................................................................................................................8

Current Liabilities ................................................................................................................................................................ 9

Noncurrent Liabilities ........................................................................................................................................................ 11

Loss Contingencies ............................................................................................................................................................ 12

Review Questions − Section 1 ................................................................................................................... 17

Fair Value Accounting ............................................................................................................................... 19

General Rules .................................................................................................................................................................... 20

Scope ................................................................................................................................................................................. 21

The Fair Value Hierarchy ................................................................................................................................................... 22

Disclosure Requirements .................................................................................................................................................. 24

Fair Value Option ..................................................................................................................................... 28

Scope ................................................................................................................................................................................. 28

Election Dates ................................................................................................................................................................... 29

Presentation and Disclosures ............................................................................................................................................ 30

Other Matters .......................................................................................................................................... 31

Risks and Uncertainties ..................................................................................................................................................... 31

Exit or Disposal Activities .................................................................................................................................................. 33

IFRS Connection ................................................................................................................................................................ 35

Review Questions − Section 2 .................................................................................................................. 36

Chapter 2: Current Liabilities .......................................................................................................... 38

Accounts Payable ..................................................................................................................................... 38

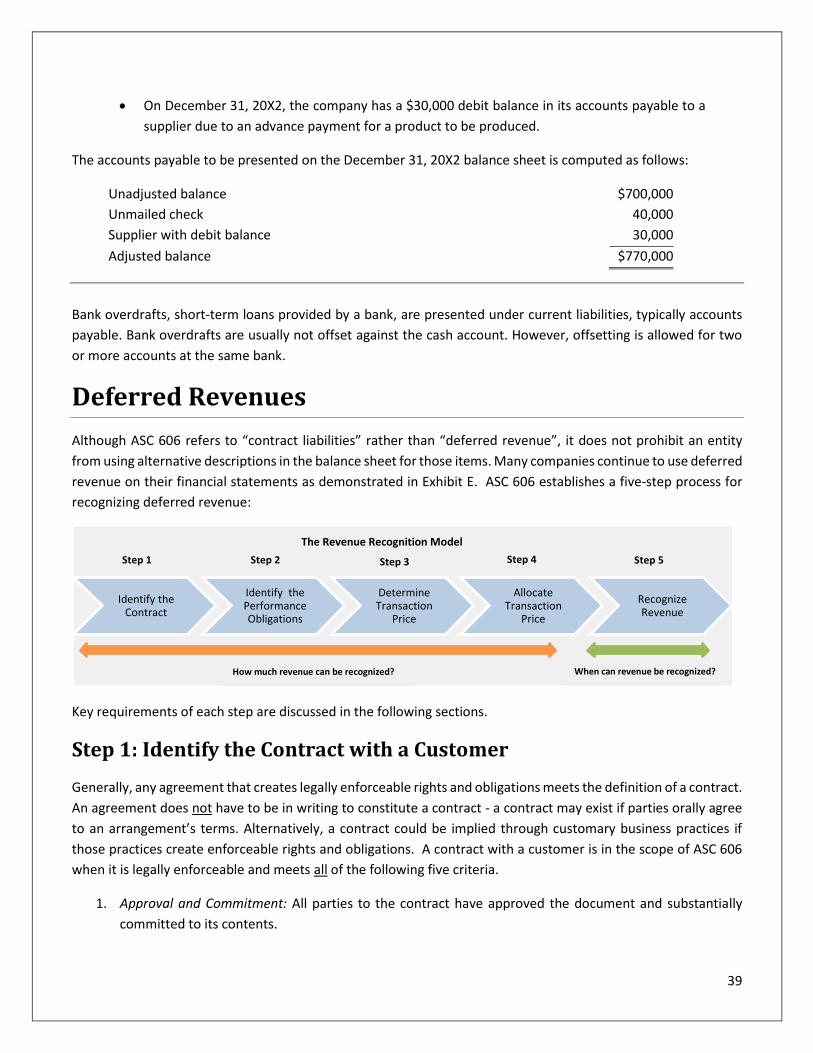

Deferred Revenues ................................................................................................................................... 39

Step 1: Identify the Contract with a Customer ................................................................................................................. 39

Step 2: Identify the Performance Obligations................................................................................................................... 40

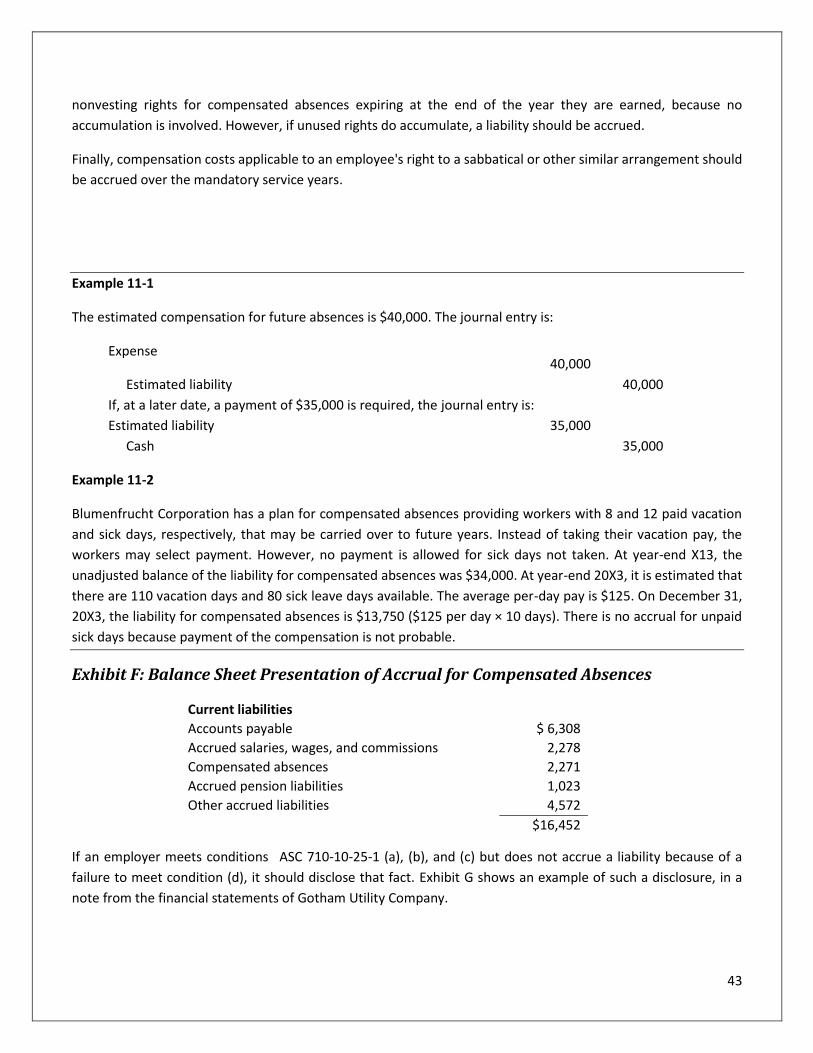

Compensated Absences .................................................................................................................................................... 42

Other Matters .......................................................................................................................................... 44

Callable Obligations .......................................................................................................................................................... 44

Troubled Debt Restructuring ............................................................................................................................................ 45

Termination Benefits (Early Retirement) .......................................................................................................................... 47

Environmental Liabilities ................................................................................................................................................... 48

Review Questions − Section 3 .................................................................................................................. 49

Chapter 3: Noncurrent Liabilities ................................................................................................... 52

Bond Accounting ...................................................................................................................................... 52

General Rules .................................................................................................................................................................... 52

Convertible Debt ...................................................................................................................................... 58

General Rules .................................................................................................................................................................... 58

Inducement Offer to Convert Debt to Equity ................................................................................................................... 61

Early Extinguishment of Debt .................................................................................................................... 64

Short-Term Obligations Refinanced........................................................................................................... 67

Review Questions − Section 4 .................................................................................................................. 69

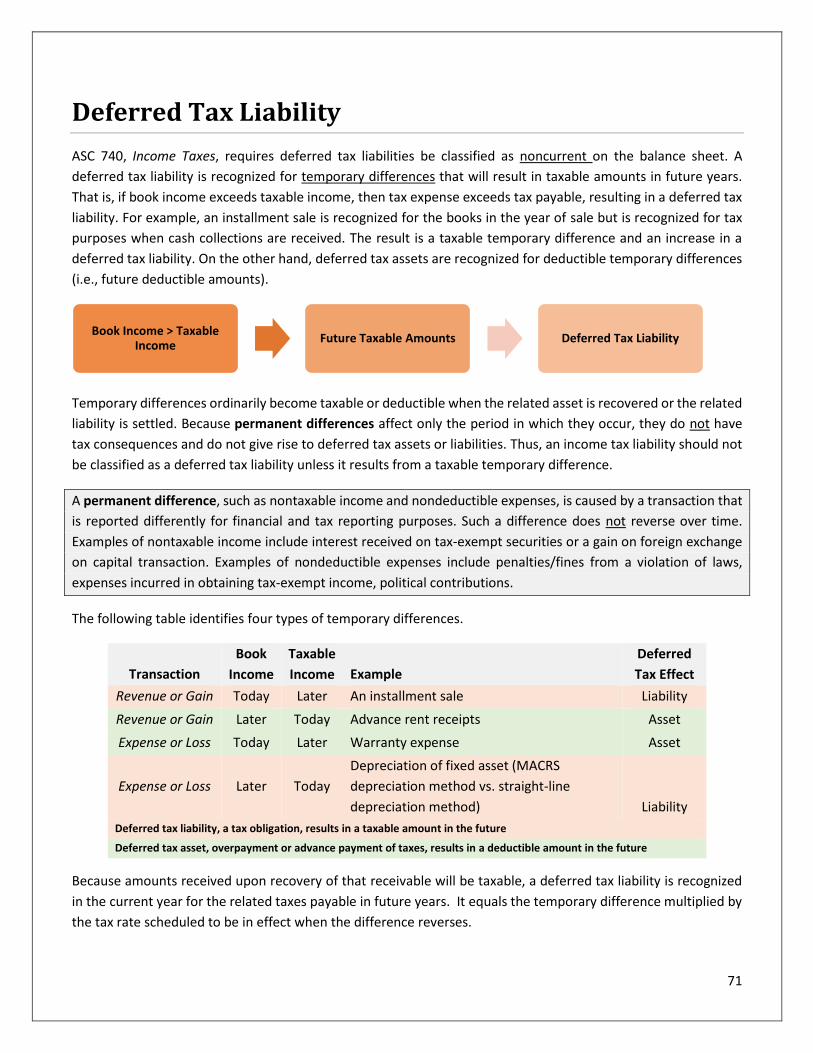

Deferred Tax Liability ............................................................................................................................... 71

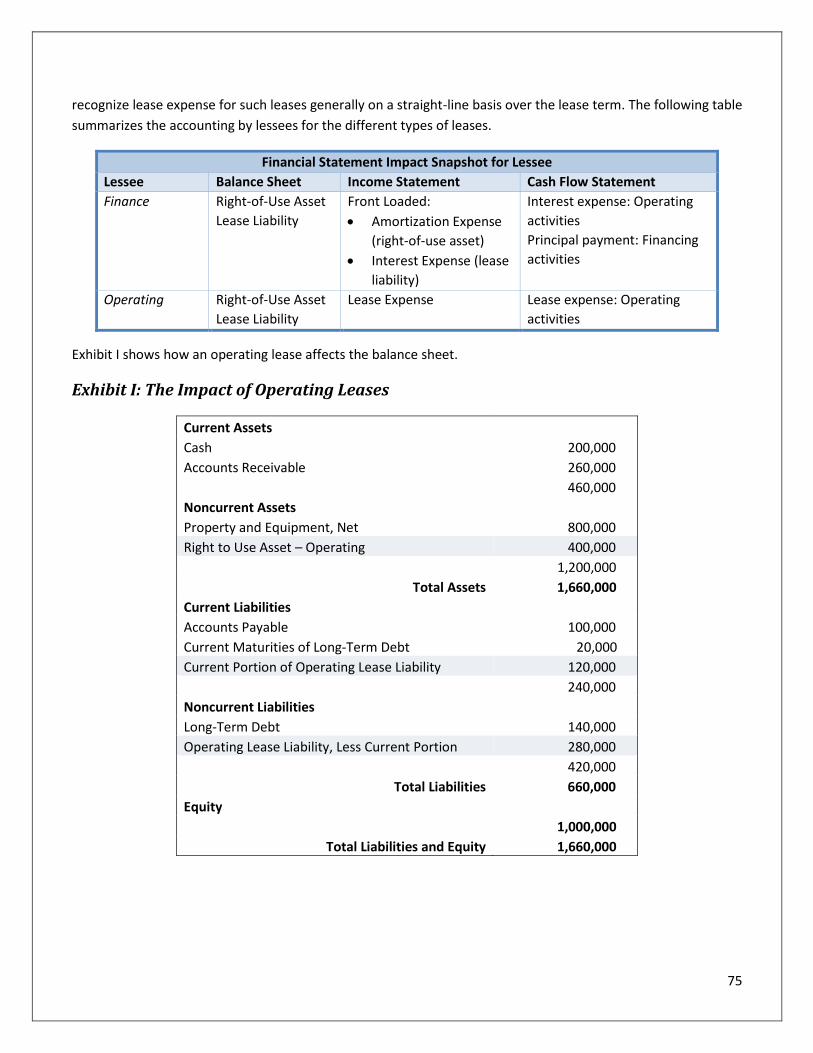

Lease Obligations ..................................................................................................................................... 73

General Rules .................................................................................................................................................................... 73

Disclosure Requirements .................................................................................................................................................. 76

Other Matters .......................................................................................................................................... 78

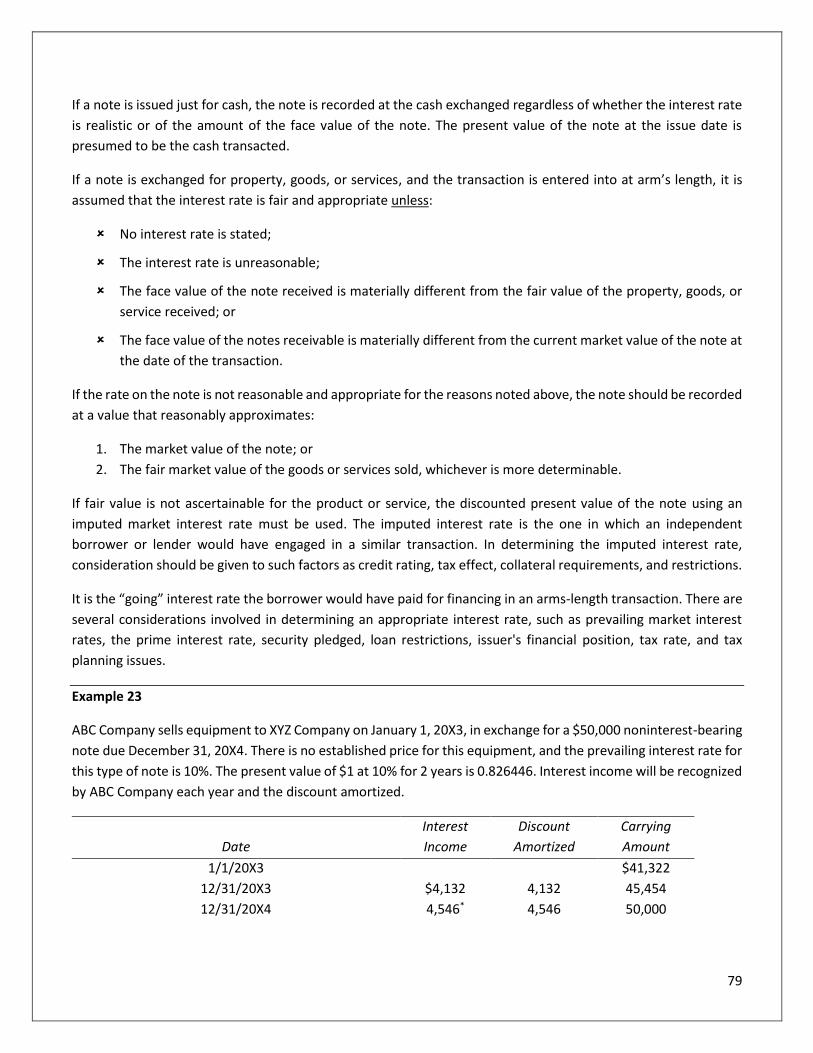

Interest on Noninterest Notes Payable ............................................................................................................................ 78

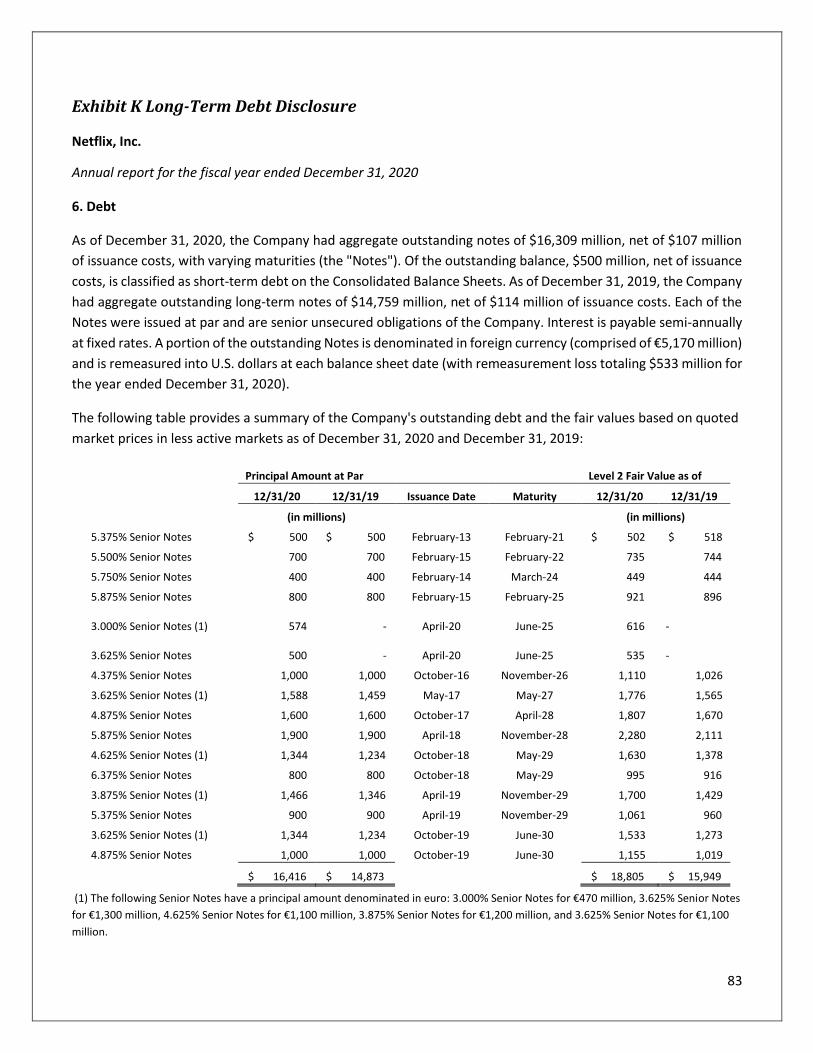

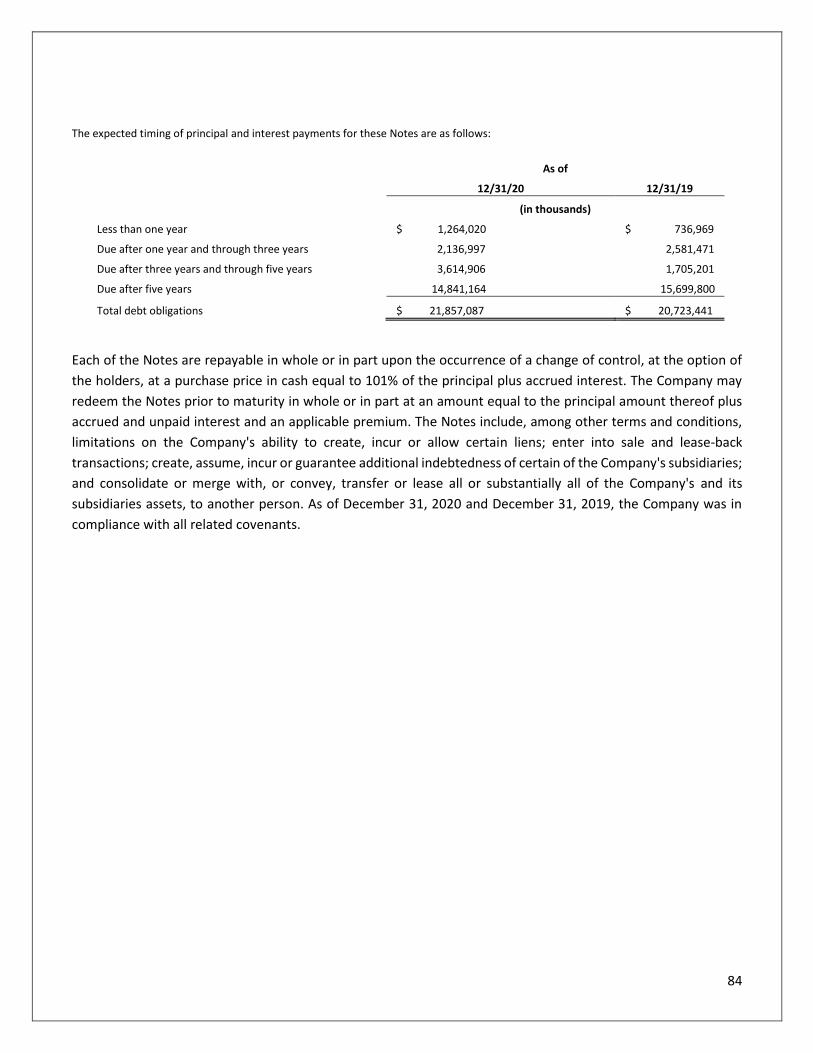

Presentation and Disclosure of Long-Term Debt .............................................................................................................. 82

Review Questions − Section 5 .................................................................................................................. 85

Glossary ..................................................................................................................................................... 87

Index .......................................................................................................................................................... 89

Appendix ................................................................................................................................................... 90

Review Question Answers ........................................................................................................................ 94

Review Questions − Section 1 .................................................................................................................. 94

Review Questions − Section 2 .................................................................................................................. 96

Review Questions − Section 3 .................................................................................................................. 98

Review Questions − Section 4 ................................................................................................................ 101

Review Questions − Section 5 ................................................................................................................ 103

1

Chapter 1: Financial Reporting Standards

“A statement of financial position provides information about an entity’s assets, liabilities, and equity and their

relationships to each other at a moment in time. The statement delineates the entity’s resource structure—major

classes and amounts of assets—and its financing structure—major classes and amounts of liabilities and equity.”

Statement of Financial Accounting Concepts No. 5

Objectives of Financial Reporting

Financial statements are a central feature of financial reporting; a principal means of communicating financial

information to those outside an entity. There are two different types of elements of financial statements:

1. Assets, liabilities, and equity describe resources or claims to or interests in resources at a specified date

2. The effects of transactions and other events and circumstances affect an entity during specified time

intervals (reporting periods). In a business entity, this consist of comprehensive income and its

components—revenues, expenses, gains, and losses—and investments by owners and distributions to

owners

The three main financial statements are the balance sheet or the statement of financial position, income

statement, and statement of cash flows. The balance sheet portrays the financial position of an entity at a

particular point in time (as of a specific date), including an entity’s:

1. Assets (economic resources): What it owns, such as cash, land, and equipment;

2. Liabilities (economic obligations): How much it owes to vendors and lenders, such as loans payable and

mortgage payable; and

3. Owners' equity: Residual interest remaining after assets have been reduced by liabilities.

A balance sheet, a snapshot of the entity's financial position, delineates its resource structure. It provides

information about an entity’s assets, liabilities, and equity and their relationships to each other at a moment in

time. Balance sheets are usually presented in comparative form. Comparative statements include the current

year’s statement and statements of one or more of preceding accounting periods. Comparative statements help

evaluate and analyze trends and relationships.

Entities routinely incur liabilities in exchange transactions to acquire the funds, goods, and services they need to

operate. For example:

2

✓ Borrowing cash (acquiring funds) obligates an entity to repay the amount borrowed;

✓ Acquiring assets on credit obligates an entity to pay for the assets; and

✓ Selling products with a warranty or guarantee obligates an entity to stand ready to either pay cash or repair

or replace any products that prove defective.

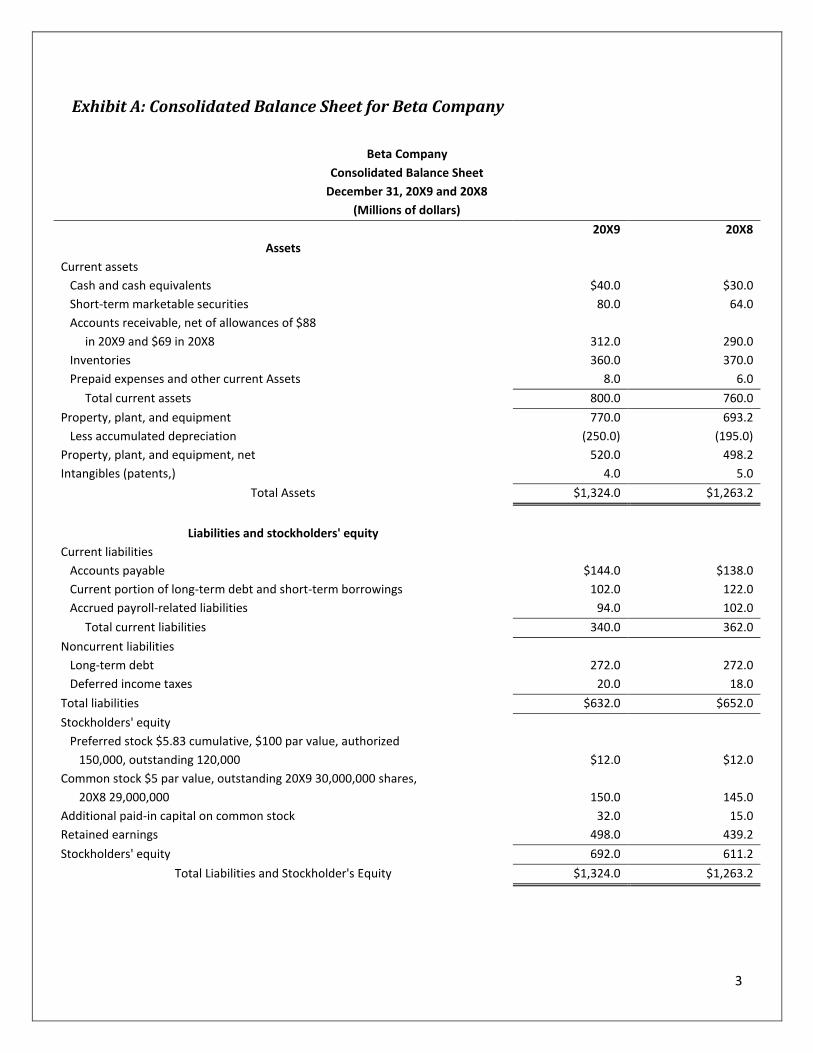

Exhibit A shows a comparative balance sheet for the Beta Company.

According to Concepts Statement No. 8, Conceptual Framework for Financial Reporting:

“The objective of general purpose financial reporting is to provide financial information about the reporting entity

that is useful to existing and potential investors, lenders, and other creditors in making decisions about providing

resources to the entity. Those decisions involve buying, selling, or holding equity and debt instruments and

providing or settling loans and other forms of credit.”

If financial information is to be useful, it must be relevant and faithfully represent what it purports to represent.

The usefulness of financial information is enhanced if it is comparable, verifiable, timely, and understandable.

The fundamental qualities under relevance are predictive value and confirmatory value, which is information that

is capable of making a difference in one of those decisions only if it will help users to make new predictions,

confirm or correct prior predictions, or both. Concepts Statement No. 8 specifies that financial information has:

• Predictive value if it can be used as an input to processes employed by users to predict future outcomes

• Confirmatory value if it provides feedback (confirms or changes) about previous evaluations

Materiality is mentioned as an aspect of relevance. Materiality is entity-specific. The omission or misstatement of

an item in a financial report is material if, in light of surrounding circumstances, the magnitude of the item is such

that it is probable that the judgment of a reasonable person relying upon the report would have been changed or

influenced by the inclusion or correction of the item.

Faithful representation means that financial information represents the substance of an economic phenomenon

rather than merely representing its legal form. It has three characteristics:

1. Completeness

2. Neutrality

3. Free from error

A complete depiction includes all information necessary for a user to understand the phenomenon being shown,

together with all necessary descriptions and explanations. A neutral depiction is without bias in the selection or

presentation of financial information. Concepts Statement No. 8 explains that it is not slanted, weighted,

emphasized, deemphasized, or otherwise manipulated to increase the probability that financial information will

be received favorably or unfavorably by users. Free from error means:

• There are no errors or omissions in the description of the phenomenon; and

• The process/procedures used to generate the reported information have been selected and applied with

no errors in the process.

3

Exhibit A: Consolidated Balance Sheet for Beta Company

Beta Company

Consolidated Balance Sheet

December 31, 20X9 and 20X8

(Millions of dollars)

20X9 20X8

Assets

Current assets

Cash and cash equivalents $40.0 $30.0

Short-term marketable securities 80.0 64.0

Accounts receivable, net of allowances of $88

in 20X9 and $69 in 20X8 312.0 290.0

Inventories 360.0 370.0

Prepaid expenses and other current Assets 8.0 6.0

Total current assets 800.0 760.0

Property, plant, and equipment 770.0 693.2

Less accumulated depreciation (250.0) (195.0)

Property, plant, and equipment, net 520.0 498.2

Intangibles (patents,) 4.0 5.0

Total Assets $1,324.0 $1,263.2

Liabilities and stockholders' equity

Current liabilities

Accounts payable $144.0 $138.0

Current portion of long-term debt and short-term borrowings 102.0 122.0

Accrued payroll-related liabilities 94.0 102.0

Total current liabilities 340.0 362.0

Noncurrent liabilities

Long-term debt 272.0 272.0

Deferred income taxes 20.0 18.0

Total liabilities $632.0 $652.0

Stockholders' equity

Preferred stock $5.83 cumulative, $100 par value, authorized

150,000, outstanding 120,000 $12.0 $12.0

Common stock $5 par value, outstanding 20X9 30,000,000 shares,

20X8 29,000,000 150.0 145.0

Additional paid-in capital on common stock 32.0 15.0

Retained earnings 498.0 439.2

Stockholders' equity 692.0 611.2

Total Liabilities and Stockholder's Equity $1,324.0 $1,263.2

4

Characteristics of Liabilities

“A liability is a present obligation of an entity to transfer an economic benefit.”

Concepts Statement No. 8: Chapter 4, Elements of Financial Statements

In July 2020, the Financial Accounting Standards Board (FASB) issued a proposed chapter (Chapter 4: Elements of

Financial Statements) of Concepts Statement No.8 for defining 10 elements of financial statements (e.g. assets,

liabilities, equity). This proposed chapter would replace Concepts Statement No. 6 and clarify the definition of the

elements in Concepts Statement No. 6 by:

✓ Clearly identifying the right or obligation that gives rise to an asset or a liability;

✓ Eliminating terminology that makes the definitions of assets and liabilities difficult to understand and

apply;

✓ Clarifying the distinction between liabilities and equity and between revenues and gains and expenses

and losses; and

✓ Modifying the distinctions in equity for not-for-profit entities

While not considered authoritative, Concepts Statements serve as the framework that the FASB uses to create

requirements in future standards.

According to Concepts Statement No. 8, a liability has the following two essential characteristics:

1. Present obligation: An entity must have an obligation that exists at the financial statement date.

2. Obligation to provide economic benefits: The obligation requires an entity to transfer or otherwise provide

economic benefits to others

Typically, obligations incurred in exchange transactions are contractual based on written or oral agreements to

pay cash or to provide goods or services to specified or determinable entities on demand at specified or

determinable dates or on the occurrence of specified events.

Each characteristic is addressed in the following sections.

Present Obligation

A liability requires that an entity be obligated to perform or act in a certain manner. Most liabilities are legally

enforceable through binding contracts, agreements, rules, statutes, or other requirements upheld by a judicial

system or government. In a financial reporting context:

✓ An obligation is any condition that binds an entity to some performance or action.

✓ Something is binding on an entity if it requires performance.

✓ Performance is what the entity is required to do to satisfy the obligation.

5

Although most liabilities are based on a foundation of legal rights and duties, the existence of a legally enforceable

claim is not a prerequisite for an obligation to qualify as a liability.

An obligation of an entity to itself cannot be a liability. That is, liabilities must involve other parties, society, or

law. For example, in the absence of external requirements a company is not obligated to maintain its plant and

equipment. Some obligations require nonreciprocal transfers from an entity to one or more other entities.

Example of such obligations include:

✓ Taxes imposed by governments;

✓ Donations pledged to charitable entities; and

✓ Cash dividends declared but not yet paid.

To have a liability, an entity must have an obligation that exists at the financial statement date. Although the

settlement date of the liability may occur in the future, the entity must present the obligation at the financial

statement date.

Transactions or other events expected to occur in the future do not in and of themselves give rise to obligations

today. For instance, an intention to purchase equipment; equipment does not in and of itself create a liability.

However, a contractual obligation that requires an entity to pay more than the fair value of the equipment at the

transaction date may create a liability before it is received, reflecting what the entity might have to pay to undo

the unfavorable contract.

Various circumstances give rise to business risks. The sources of risk can arise from an entity’s objectives, the

nature of its operations/industry, the regulatory environment in which it operates, and its size and complexity.

Business risk is not a present obligation, though at some point in the future an event may occur that creates a

present obligation.

Concepts Statement No. 8 explains that the essence of distinguishing business risks from liabilities is determining

the point in time when an entity has a present obligation. For example, the operation of a passenger airline is

considered a business risk. Airlines have the business risk that a plane might crash, creating liabilities for the

airlines. However, those business risks do not produce a present obligation for the consequences of a plane crash

that has yet to occur. Other examples of business risks include:

• Selling goods in overseas markets might expose an entity to the risk of future cash flow fluctuations

because of changes in foreign exchange rates

• Technological developments may make a particular product obsolete

• Operating in a highly specialized industry might expose an entity to the risk that it will be unable to attract

sufficient skilled staff to sustain its operating activities

Companies usually discuss business risks in the forward-looking statements of their Annual Report Form 10-K as

demonstrated in Exhibit B.

6

To be presently obligated, an entity must be bound, either legally or in some other way, to perform or act in a

certain way such as constructive obligations. A constructive obligation is created, inferred, or construed from the

facts in a particular situation rather than contracted by agreement with another entity or imposed by the

government. Examples of constructive obligations include:

✓ Policies and practices for sales returns and those for warranties in the absence of a contract may create a

present obligation.

✓ Companies pay their employees for vacation or year-end bonuses every year.

Determining whether an entity is bound by an obligation to a third party in the absence of legal enforceability is

often extremely difficult. Thus, the concepts of constructive obligations must be applied with great care.

Obligation to Provide Economic Benefits

The obligation establishes the responsibility of the entity to fulfill the requirements of the obligation or otherwise

satisfy or settle the obligation in different ways such as:

• Transferring cash or other assets

• Providing services

• Granting a right to use an asset

• Replacing that obligation with another obligation

• Converting the obligation to equity

• Transferring shares of the entity

Such obligations are often documented including:

1. How the entity is required to fulfill the obligation; and

2. When—by a specified date or when specified events occur

For example, a company receives a payment from its customer resulting in an obligation if the company receiving

it is expected to provide a product on a certain day or refund the payment if the product is not provided.

If arrangements allow or require settlement of obligations by the issuance of a variable number of the entity’s

own shares, those shares are essentially being used in lieu of assets to settle an obligation and therefore meet the

definition of a liability.

In some cases, the amount and timing of settlement or performance associated with a present obligation are

uncertain; commonly referred to as stand-ready obligations. With a stand-ready obligation, an entity’s timing of

settlement or performance, the amount of economic benefits that the entity will transfer, or both are not known

at the financial reporting date. Examples of stand-ready obligations include:

✓ Warranties: The warranty issuer recognizes its liability arising from its obligation to provide warranty

coverage. The amount of the warranty depends on an uncertain future event; the product developing a fault

during the warranty period. However, that uncertainty does not affect the existence of a present obligation

7

to provide warranty coverage. Instead, the uncertainty about whether the product will require repair or

replacement is reflected in the measurement of the liability.

In non-contractual situations, an entity may implicitly warrant a product and, as a result, that entity would

stand ready to provide services.

✓ Guarantees: Writing a guarantee creates a present obligation even if an outflow resulting from the guarantee

is remote. The uncertainty of the payment affects the measurement of the guarantee, not the existence of an

obligation to honor the guarantee if called upon to do so.

✓ Options: An entity formally documents that it will act in a certain way in the future if called upon by the holder

of the option. Even though the external party (option holder) may never exercise the option, the entity that

wrote the option is obligated to act as required by the option contract.

Present obligations with uncertain amounts and timing are referred to as contingent liabilities.

Although both stand-ready obligations and business risks can result in an outflow of economic benefits, stand-

ready obligations are liabilities because they involve present obligations. As mentioned, a business risk does not

give rise to a present obligation. Thus, the existence of a present obligation distinguishes stand-ready obligations

(and more generally liabilities) from business risks.

Exhibit B: Forward-Looking Statements

Netflix, Inc.

Annual report for the fiscal year ended December 31, 2020

Risks Related to Our Business

Changes in competitive offerings for entertainment video, including the potential rapid adoption of piracy-based video

offerings, could adversely impact our business.

The market for entertainment video is intensely competitive and subject to rapid change. Through new and existing

distribution channels, consumers have increasing options to access entertainment videos. The various economic models

underlying these channels include subscription, transactional, ad-supported, and piracy-based models. All of these have

the potential to capture meaningful segments of the entertainment video market. Piracy, in particular, threatens to

damage our business, as its fundamental proposition to consumers is so compelling and difficult to compete against:

virtually all content for free. Furthermore, in light of the compelling consumer proposition, piracy services are subject to

rapid global growth. Traditional providers of entertainment video, including broadcasters and cable network operators, as

well as internet-based e-commerce or entertainment video providers are increasing their streaming video offerings.

Several of these competitors have long operating histories, large customer bases, strong brand recognition, exclusive rights

to certain content, and significant financial, marketing, and other resources. They may secure better terms from suppliers,

adopt more aggressive pricing and devote more resources to product development, technology, infrastructure, content

acquisitions and marketing. New entrants may enter the market or existing providers may adjust their services with unique

offerings or approaches to providing entertainment video. Companies also may enter into business combinations or

alliances that strengthen their competitive positions. If we are unable to successfully or profitably compete with current

8

and new competitors, our business will be adversely affected, and we may not be able to increase or maintain market

share, revenues or profitability.

If government regulations relating to the internet or other areas of our business change, we may need to alter the

manner in which we conduct our business or incur greater operating expenses.

The adoption or modification of laws or regulations relating to the internet or other areas of our business could limit or

otherwise adversely affect the manner in which we currently conduct our business. As our service and others like us gain

traction in international markets, governments are increasingly looking to introduce new or extend legacy regulations to

these services, in particular those related to broadcast media and tax. For example, recent changes to European law enable

individual member states to impose levies and other financial obligations on media operators located outside their

jurisdiction. We anticipate that several jurisdictions may, over time, impose greater financial and regulatory obligations on

us. In addition, the continued growth and development of the market for online commerce may lead to more stringent

consumer protection laws, which may impose additional burdens on us. If we are required to comply with new regulations

or legislation or new interpretations of existing regulations or legislation, this compliance could cause us to incur additional

expenses or alter our business model.

Changes in laws or regulations that adversely affect the growth, popularity or use of the internet, including laws impacting

net neutrality, could decrease the demand for our service and increase our cost of doing business. Certain laws intended

to prevent network operators from discriminating against the legal traffic that traverses their networks have been

implemented in many countries, including across the European Union. In others, the laws may be nascent or non-existent.

Furthermore, favorable laws may change, including for example, in the United States where net neutrality regulations

were repealed. Given uncertainty around these rules, including changing interpretations, amendments or repeal, coupled

with potentially significant political and economic power of local network operators, we could experience discriminatory

or anti-competitive practices that could impede our growth, cause us to incur additional expense or otherwise negatively

affect our business.

Recognition and Measurement

“For items that meet criteria for recognition, disclosure by other means is not a substitute for recognition in

financial statements.”

Statement of Financial Accounting Concepts No. 5

Recognition is the process of formally recording or incorporating an item into the financial statements as an asset,

liability, revenue, expense, or the like. Recognition includes the depiction of an item in both words and numbers,

with the amount included in the totals of the financial statements. For a liability, recognition involves recording

not only acquisition or incurrence of the item but also later changes in it, including changes that result in removal

from the financial statements.

According to Statement of Financial Accounting Concepts No. 5, liabilities are recognized in the balance sheet

when the following four criteria are met, subject to a cost-benefit constraint and a materiality threshold:

9

1. Definitions: The item meets the definition of a liability;

2. Measurability: It has a relevant attribute measurable with sufficient reliability;

3. Relevance: The information about it is capable of making a difference in user decisions; and

4. Reliability: The information is representationally faithful, verifiable, and neutral.

Cost-benefit constraint means that the expected benefits from recognizing a particular item should justify the

perceived costs of providing and using the information. Materiality indicates that an item and information about

it need not be recognized in a set of financial statements if the item is not large enough to be material and the

aggregate of individually immaterial items is not large enough to be material to those financial statements.

A classified balance sheet generally breaks down liabilities into two categories; current liabilities and noncurrent

liabilities. Liabilities are typically listed on the balance sheet in order of shortest term to longest term to help users

understand what is due and when at a glance.

Current Liabilities

Current liabilities are those to be paid or liquidated from current assets or created from other current liabilities.

They are due on demand or within one year or the normal operating cycle of the business, whichever is greater.

Current liabilities may arise in which:

• The payee and amount are known.

• The payee is not known but the amount may be reasonably estimated.

• The payable is known but the amount must be estimated.

• The liability arises from a loss contingency.

In general, current liabilities include:

✓ Obligations that by their terms are or will be due on demand within one year (or the operating cycle, if

longer); and

✓ Obligations that are or will be callable by the creditor within one year because of a violation of a debt

covenant. An exception exists, however, if the creditor has waived or subsequently lost the right to

demand repayment for more than one year (or the operating cycle, if longer) from the balance sheet date.

Thus, the following transactions may result in current liabilities:

1. Payables incurred in the acquisition of materials and supplies are used in the production of goods or in

providing services offered for sale

2. Collections are received in advance of the delivery of goods or performance of services

3. Debts arise from operations directly related to the operating cycle, such as accruals for wages, salaries,

commissions, rentals, royalties and income, and other taxes

4. Liabilities whose regular and ordinary liquidation is expected to occur within a relatively short period,

usually 12 months, such as:

10

• Short-term debts arising from the acquisition of capital assets

• Serial maturities of long-term obligations

• Amounts required to be extended within one year under sinking fund provisions

5. Agency liabilities are amounts withheld by the company from employees or customers for taxes owed to

federal, state, or local taxing agencies.

6. The liability for an underfunded defined benefit plan may be classified as a current liability, noncurrent

liability, or a combination of both.

7. Obligations are due on demand or within one year even if liquidation is not anticipated within that period.

8. Long-term obligations that are or will be callable by the creditor either because the debtor's violation of

a provision of the debt agreement at the balance sheet date makes the obligation callable or because of

the violation.

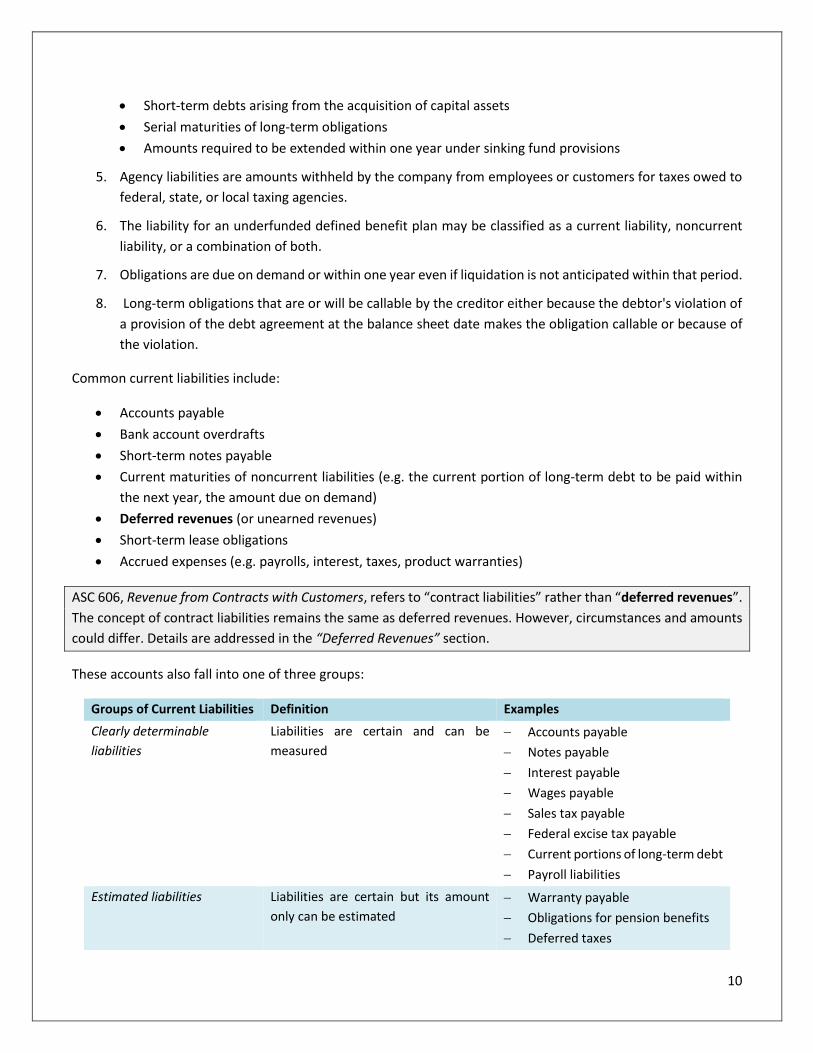

Common current liabilities include:

• Accounts payable

• Bank account overdrafts

• Short-term notes payable

• Current maturities of noncurrent liabilities (e.g. the current portion of long-term debt to be paid within

the next year, the amount due on demand)

• Deferred revenues (or unearned revenues)

• Short-term lease obligations

• Accrued expenses (e.g. payrolls, interest, taxes, product warranties)

ASC 606, Revenue from Contracts with Customers, refers to “contract liabilities” rather than “deferred revenues”.

The concept of contract liabilities remains the same as deferred revenues. However, circumstances and amounts

could differ. Details are addressed in the “Deferred Revenues” section.

These accounts also fall into one of three groups:

Groups of Current Liabilities Definition Examples

Clearly determinable

liabilities

Liabilities are certain and can be

measured

− Accounts payable

− Notes payable

− Interest payable

− Wages payable

− Sales tax payable

− Federal excise tax payable

− Current portions of long-term debt

− Payroll liabilities

Estimated liabilities Liabilities are certain but its amount

only can be estimated

− Warranty payable

− Obligations for pension benefits

− Deferred taxes

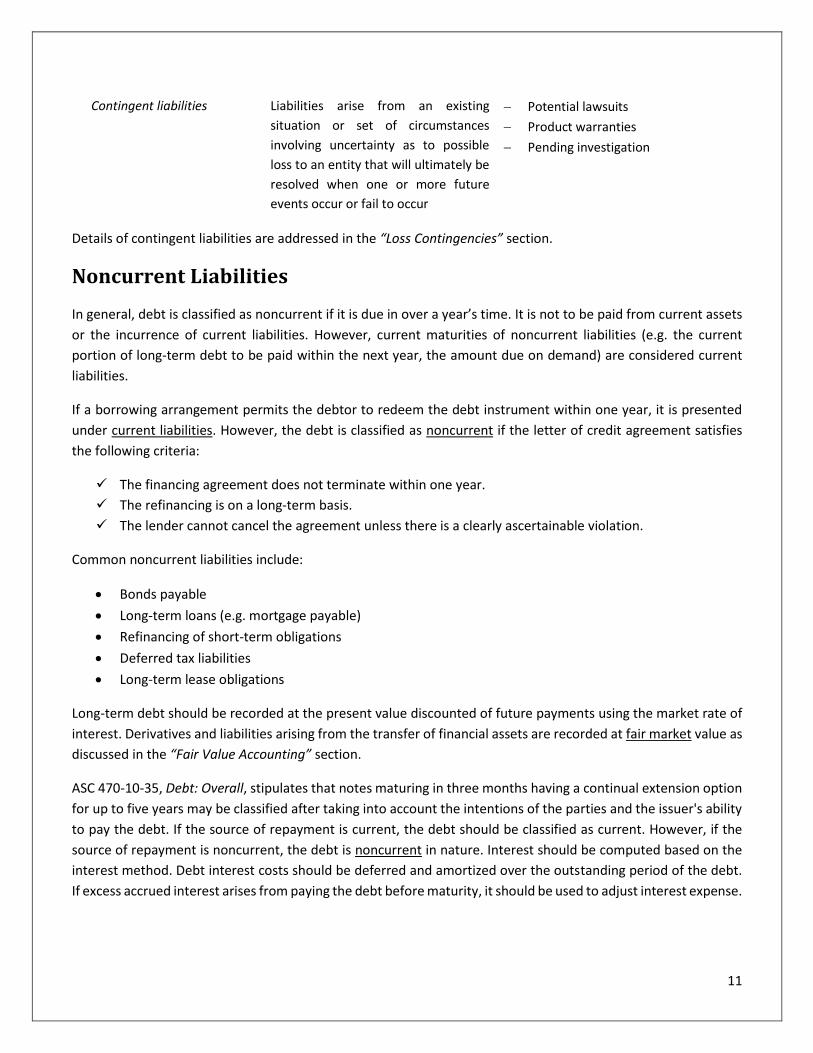

11

Contingent liabilities Liabilities arise from an existing

situation or set of circumstances

involving uncertainty as to possible

loss to an entity that will ultimately be

resolved when one or more future

events occur or fail to occur

− Potential lawsuits

− Product warranties

− Pending investigation

Details of contingent liabilities are addressed in the “Loss Contingencies” section.

Noncurrent Liabilities

In general, debt is classified as noncurrent if it is due in over a year’s time. It is not to be paid from current assets

or the incurrence of current liabilities. However, current maturities of noncurrent liabilities (e.g. the current

portion of long-term debt to be paid within the next year, the amount due on demand) are considered current

liabilities.

If a borrowing arrangement permits the debtor to redeem the debt instrument within one year, it is presented

under current liabilities. However, the debt is classified as noncurrent if the letter of credit agreement satisfies

the following criteria:

✓ The financing agreement does not terminate within one year.

✓ The refinancing is on a long-term basis.

✓ The lender cannot cancel the agreement unless there is a clearly ascertainable violation.

Common noncurrent liabilities include:

• Bonds payable

• Long-term loans (e.g. mortgage payable)

• Refinancing of short-term obligations

• Deferred tax liabilities

• Long-term lease obligations

Long-term debt should be recorded at the present value discounted of future payments using the market rate of

interest. Derivatives and liabilities arising from the transfer of financial assets are recorded at fair market value as

discussed in the “Fair Value Accounting” section.

ASC 470-10-35, Debt: Overall, stipulates that notes maturing in three months having a continual extension option

for up to five years may be classified after taking into account the intentions of the parties and the issuer's ability

to pay the debt. If the source of repayment is current, the debt should be classified as current. However, if the

source of repayment is noncurrent, the debt is noncurrent in nature. Interest should be computed based on the

interest method. Debt interest costs should be deferred and amortized over the outstanding period of the debt.

If excess accrued interest arises from paying the debt before maturity, it should be used to adjust interest expense.

12

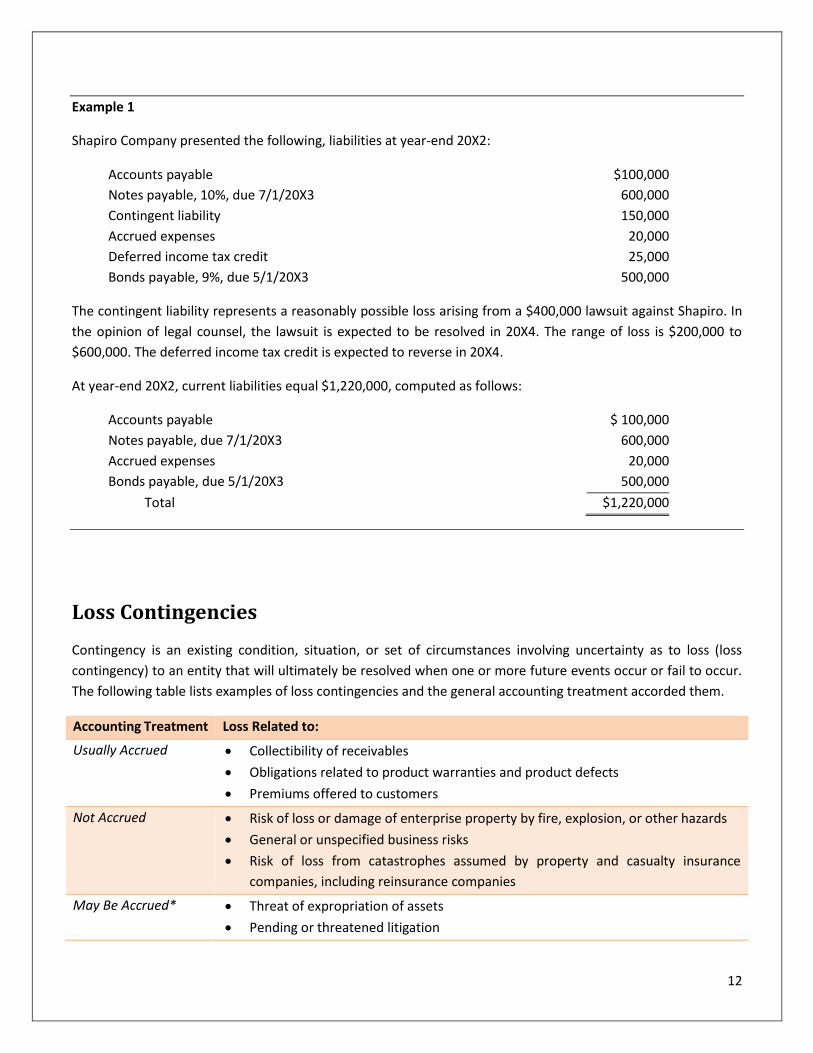

Example 1

Shapiro Company presented the following, liabilities at year-end 20X2:

Accounts payable $100,000

Notes payable, 10%, due 7/1/20X3 600,000

Contingent liability 150,000

Accrued expenses 20,000

Deferred income tax credit 25,000

Bonds payable, 9%, due 5/1/20X3 500,000

The contingent liability represents a reasonably possible loss arising from a $400,000 lawsuit against Shapiro. In

the opinion of legal counsel, the lawsuit is expected to be resolved in 20X4. The range of loss is $200,000 to

$600,000. The deferred income tax credit is expected to reverse in 20X4.

At year-end 20X2, current liabilities equal $1,220,000, computed as follows:

Accounts payable $ 100,000

Notes payable, due 7/1/20X3 600,000

Accrued expenses 20,000

Bonds payable, due 5/1/20X3 500,000

Total $1,220,000

Loss Contingencies

Contingency is an existing condition, situation, or set of circumstances involving uncertainty as to loss (loss

contingency) to an entity that will ultimately be resolved when one or more future events occur or fail to occur.

The following table lists examples of loss contingencies and the general accounting treatment accorded them.

Accounting Treatment Loss Related to:

Usually Accrued

• Collectibility of receivables

• Obligations related to product warranties and product defects

• Premiums offered to customers

Not Accrued

• Risk of loss or damage of enterprise property by fire, explosion, or other hazards

• General or unspecified business risks

• Risk of loss from catastrophes assumed by property and casualty insurance

companies, including reinsurance companies

May Be Accrued*

• Threat of expropriation of assets

• Pending or threatened litigation

13

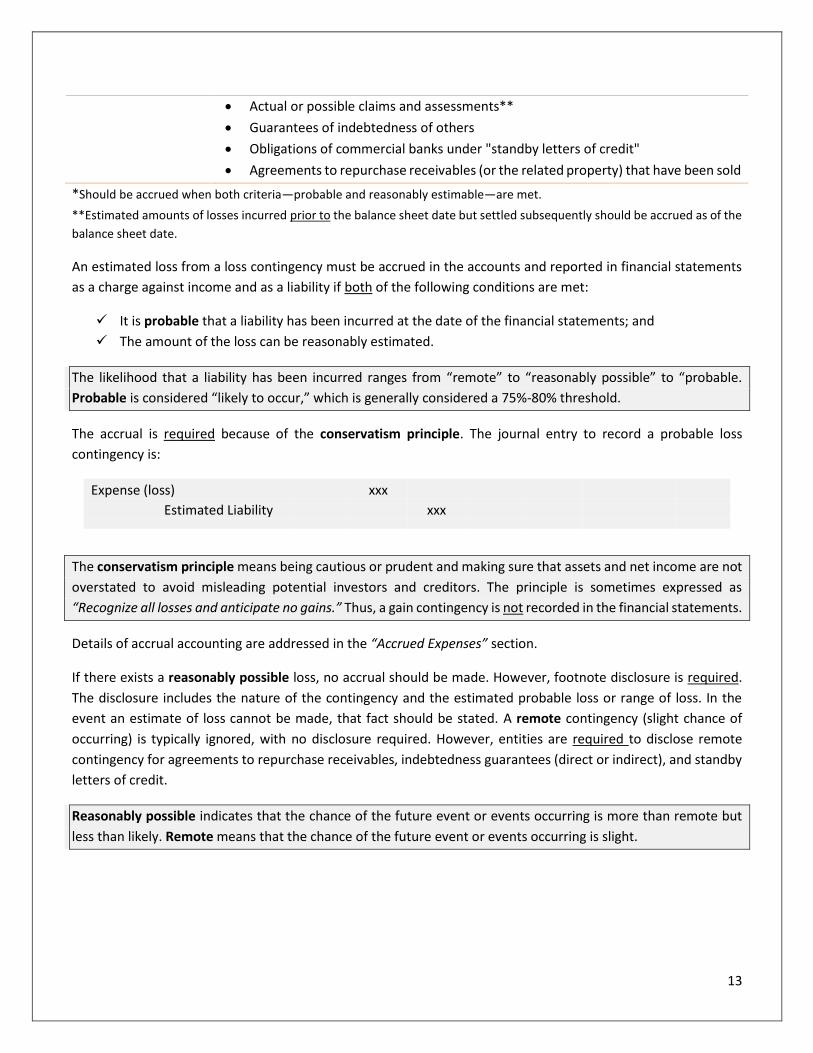

• Actual or possible claims and assessments**

• Guarantees of indebtedness of others

• Obligations of commercial banks under "standby letters of credit"

• Agreements to repurchase receivables (or the related property) that have been sold

*Should be accrued when both criteria—probable and reasonably estimable—are met.

**Estimated amounts of losses incurred prior to the balance sheet date but settled subsequently should be accrued as of the

balance sheet date.

An estimated loss from a loss contingency must be accrued in the accounts and reported in financial statements

as a charge against income and as a liability if both of the following conditions are met:

✓ It is probable that a liability has been incurred at the date of the financial statements; and

✓ The amount of the loss can be reasonably estimated.

The likelihood that a liability has been incurred ranges from “remote” to “reasonably possible” to “probable.

Probable is considered “likely to occur,” which is generally considered a 75%-80% threshold.

The accrual is required because of the conservatism principle. The journal entry to record a probable loss

contingency is:

Expense (loss) xxx

Estimated Liability xxx

The conservatism principle means being cautious or prudent and making sure that assets and net income are not

overstated to avoid misleading potential investors and creditors. The principle is sometimes expressed as

“Recognize all losses and anticipate no gains.” Thus, a gain contingency is not recorded in the financial statements.

Details of accrual accounting are addressed in the “Accrued Expenses” section.

If there exists a reasonably possible loss, no accrual should be made. However, footnote disclosure is required.

The disclosure includes the nature of the contingency and the estimated probable loss or range of loss. In the

event an estimate of loss cannot be made, that fact should be stated. A remote contingency (slight chance of

occurring) is typically ignored, with no disclosure required. However, entities are required to disclose remote

contingency for agreements to repurchase receivables, indebtedness guarantees (direct or indirect), and standby

letters of credit.

Reasonably possible indicates that the chance of the future event or events occurring is more than remote but

less than likely. Remote means that the chance of the future event or events occurring is slight.

14

Example 2

A company cosigned a loan guaranteeing the indebtedness if the borrower defaults on it. The likelihood of default

is remote. This is an exception to the rule that remote contingencies need not be disclosed because it represents

a guarantee of indebtedness and thus requires disclosure.

No accrual is made for general (unspecified) contingencies, such as for self-insurance and hurricane losses.

However, footnote disclosure and appropriation of retained earnings can be made for such contingencies. To be

accrued, the future loss must be specific and measurable, such as freight or parcel post losses.

If the loss amount is within a range, the accrual should be based on the best estimate within that range. If no

amount within the range is better than any other amount, the minimum amount of the range should be accrued.

There should be the disclosure of the maximum loss. If later events indicate that the minimum loss initially accrued

is insufficient, an additional loss must be accrued in the year this becomes evident. This accrual is treated as a

change in estimate. If a probable loss cannot be estimated, it should be footnoted.

Example 3

XYZ Company is involved in a tax dispute with the Internal Revenue Service (IRS). As of December 31, 20X3, XYZ

Company believed that an unfavorable outcome is probable and the amount of loss may be in the range of $2.5

million to $3.5 million. After year-end, when the 20X3 financial statements had been issued, XYZ Company settled

with the IRS and accepted an offer of $3 million. Because a range of loss is involved, it is appropriate to accrue the

minimum amount or $2.5 million for 20X3 year-end.

A company may offer potential customers premiums (something free or for a minimal charge, such as samples) to

stimulate product sales. The customer may be required to return evidence of the purchase of certain products

(e.g. box top) to get the premium. A nominal cash payment may be necessary. A current liability arises for the

amount of anticipated redemptions in the next year. If the premium and redemption period is for more than one

year, an estimated liability must be allocated to the current and noncurrent portions.

If there is a loss contingency at year-end but no asset impairment or liability incurrence exists (e.g., uninsured

equipment), footnote disclosure should be made. If there is a loss contingency occurring after year-end but before

the audit report date, subsequent event disclosure should be made. An explanatory paragraph should be provided

regarding the contingency.

Unasserted claims exist when the claimant has elected not to assert the claim or because the claimant lacks

knowledge of the existence of the claim. If it is probable that the claimant will assert the unasserted claim, and it

is either probable or reasonably possible that the outcome will be unfavorable, the unasserted claim should be

disclosed in the financial statements. Contingent consideration in a business combination relates to an additional

amount paid by the acquirer to the shareholders of the acquiree when certain conditions (such as meeting futures

earnings targets) are met. Under ASC 805-30-25-5 through 25-7, the acquisition method requires that the

contingency be measured at fair value and a liability be recorded at the closing date. Subsequent changes in the

fair value of contingent consideration are recorded in earnings.

15

Exhibit C shows how a company discloses its loss contingency.

Exhibit C: Loss Contingencies

General Electric Company

Annual report for the fiscal year ended December 31, 2020

Alstom legacy legal matters. On November 2, 2015, we acquired the Thermal, Renewables and Grid businesses from

Alstom. Prior to the acquisition, the seller was the subject of two significant cases involving anti-competitive activities and

improper payments: (1) in January 2007, Alstom was fined €65 million by the European Commission for participating in a

gas-insulated switchgear cartel that operated from 1988 to 2004 (that fine was later reduced to €59 million), and (2) in

December 2014, Alstom pled guilty in the United States to multiple violations of the Foreign Corrupt Practices Act and paid

a criminal penalty of $772 million. As part of GE’s accounting for the acquisition, we established a reserve amounting to

$858 million for legal and compliance matters related to the legacy business practices that were the subject of these and

related cases in various jurisdictions, including the previously reported legal proceedings in Slovenia that are described

below. The reserve balance was $858 million and $875 million at December 31, 2020, and December 31, 2019, respectively.

Regardless of jurisdiction, the allegations relate to claimed anti-competitive conduct or improper payments in the pre-

acquisition period as the source of legal violations and/or damages. Given the significant litigation and compliance activity

related to these matters and our ongoing efforts to resolve them, it is difficult to assess whether the disbursements will

ultimately be consistent with the reserve established. The estimation of this reserve involved significant judgment and

may not reflect the full range of uncertainties and unpredictable outcomes inherent in litigation and investigations of this

nature, and at this time we are unable to develop a meaningful estimate of the range of reasonably possible additional

losses beyond the amount of this reserve. Damages sought may include disgorgement of profits on the underlying business

transactions, fines and/or penalties, interest, or other forms of resolution. Factors that can affect the ultimate amount of

losses associated with these and related matters include the way cooperation is assessed and valued, prosecutorial

discretion in the determination of damages, formulas for determining fines and penalties, the duration and amount of

legal and investigative resources applied, political and social influences within each jurisdiction, and tax consequences of

any settlements or previous deductions, among other considerations. Actual losses arising from claims in these and related

matters could exceed the amount provided.

In connection with alleged improper payments by Alstom relating to contracts won in 2006 and 2008 for work on a state-

owned power plant in Šoštanj, Slovenia, the power plant owner in January 2017 filed an arbitration claim for damages of

approximately $430 million before the International Chamber of Commerce Court of Arbitration in Vienna, Austria. In

February 2017, a government investigation in Slovenia of the same underlying conduct proceeded to an investigative phase

overseen by a judge of the Celje District Court. In September 2020, the relevant Alstom legacy entity was served with an

indictment, which we had anticipated as we are working with the parties to resolve these matters.

16

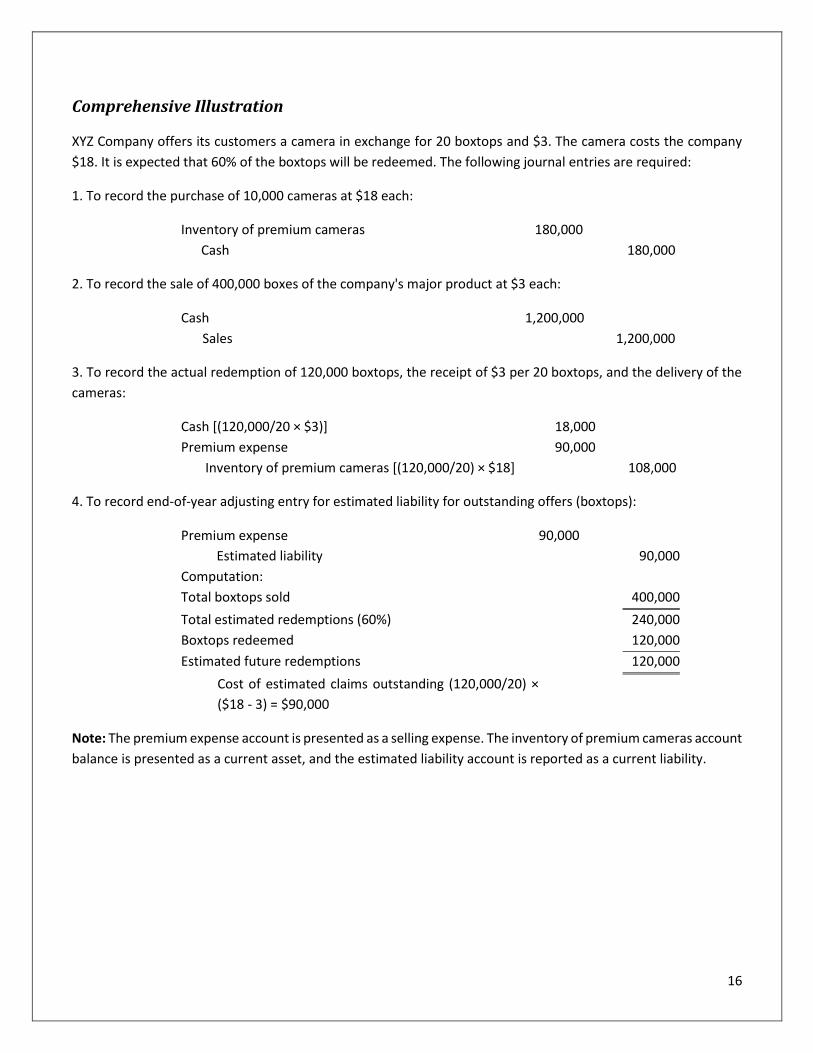

Comprehensive Illustration

XYZ Company offers its customers a camera in exchange for 20 boxtops and $3. The camera costs the company

$18. It is expected that 60% of the boxtops will be redeemed. The following journal entries are required:

1. To record the purchase of 10,000 cameras at $18 each:

Inventory of premium cameras 180,000

Cash 180,000

2. To record the sale of 400,000 boxes of the company's major product at $3 each:

Cash 1,200,000

Sales 1,200,000

3. To record the actual redemption of 120,000 boxtops, the receipt of $3 per 20 boxtops, and the delivery of the

cameras:

Cash [(120,000/20 × $3)] 18,000

Premium expense 90,000

Inventory of premium cameras [(120,000/20) × $18] 108,000

4. To record end-of-year adjusting entry for estimated liability for outstanding offers (boxtops):

Premium expense 90,000

Estimated liability 90,000

Computation:

Total boxtops sold 400,000

Total estimated redemptions (60%) 240,000

Boxtops redeemed 120,000

Estimated future redemptions 120,000

Cost of estimated claims outstanding (120,000/20) ×

($18 - 3) = $90,000

Note: The premium expense account is presented as a selling expense. The inventory of premium cameras account

balance is presented as a current asset, and the estimated liability account is reported as a current liability.

17

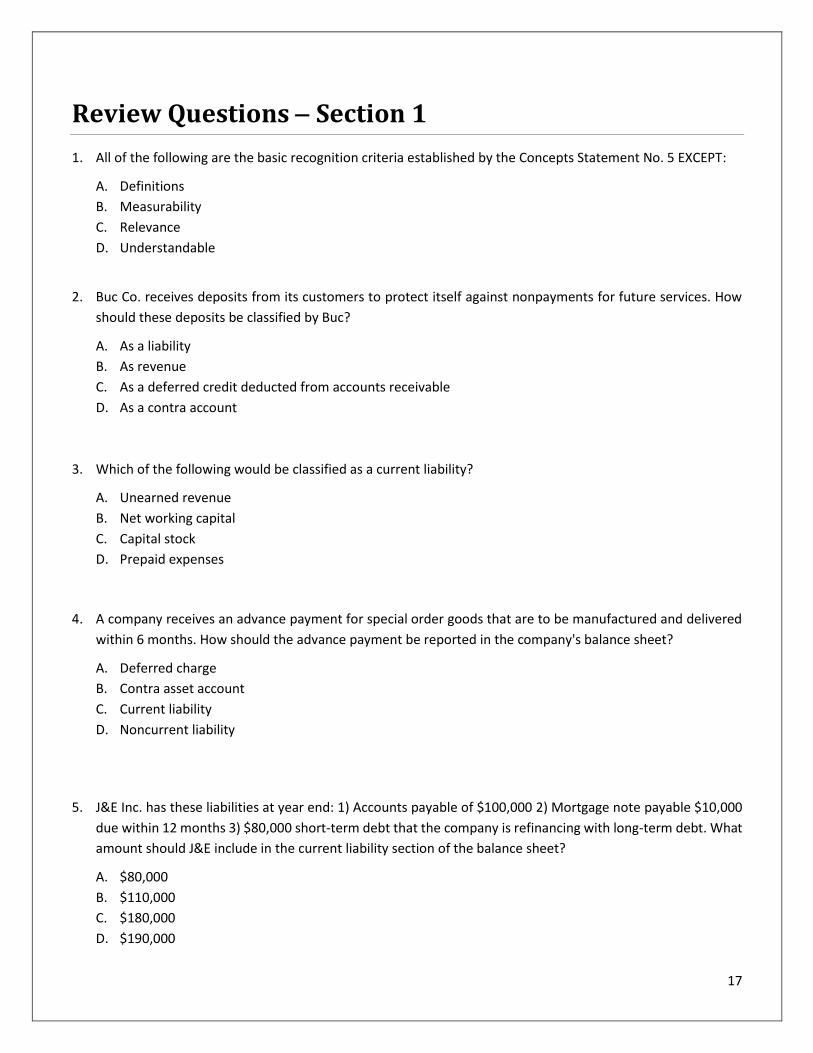

Review Questions − Section 1

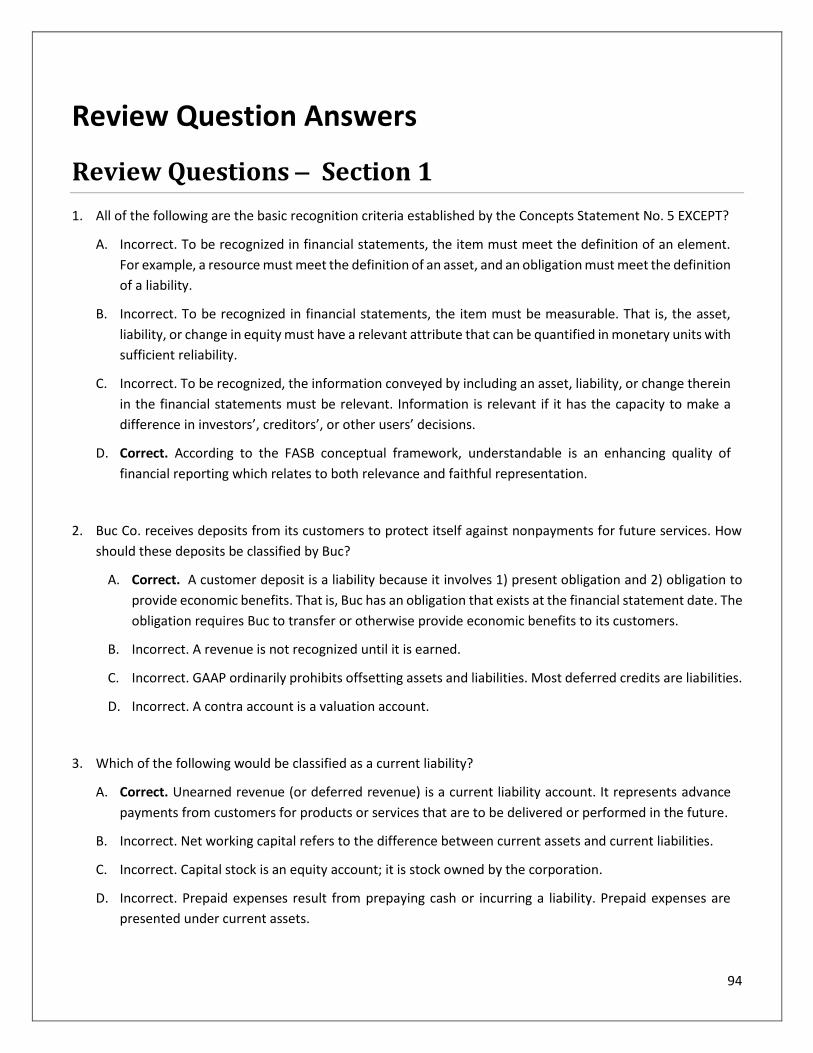

1. All of the following are the basic recognition criteria established by the Concepts Statement No. 5 EXCEPT:

A. Definitions

B. Measurability

C. Relevance

D. Understandable

2. Buc Co. receives deposits from its customers to protect itself against nonpayments for future services. How

should these deposits be classified by Buc?

A. As a liability

B. As revenue

C. As a deferred credit deducted from accounts receivable

D. As a contra account

3. Which of the following would be classified as a current liability?

A. Unearned revenue

B. Net working capital

C. Capital stock

D. Prepaid expenses

4. A company receives an advance payment for special order goods that are to be manufactured and delivered

within 6 months. How should the advance payment be reported in the company's balance sheet?

A. Deferred charge

B. Contra asset account

C. Current liability

D. Noncurrent liability

5. J&E Inc. has these liabilities at year end: 1) Accounts payable of $100,000 2) Mortgage note payable $10,000

due within 12 months 3) $80,000 short-term debt that the company is refinancing with long-term debt. What

amount should J&E include in the current liability section of the balance sheet?

A. $80,000

B. $110,000

C. $180,000

D. $190,000

18

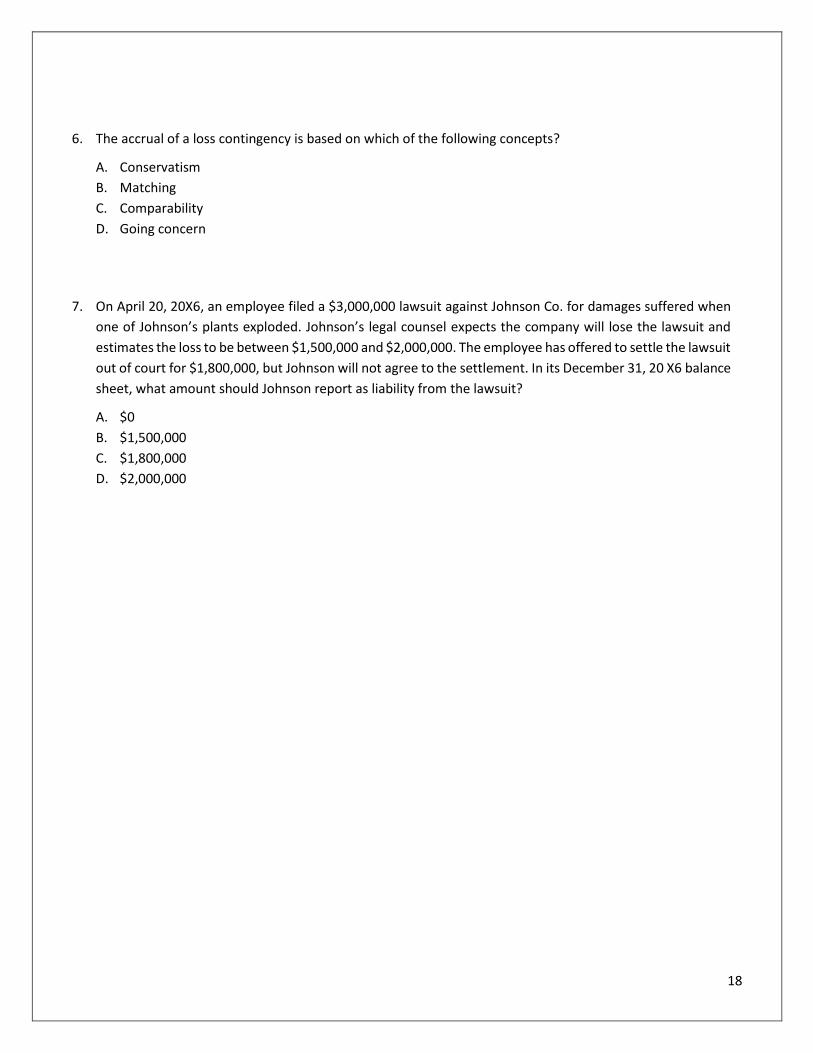

6. The accrual of a loss contingency is based on which of the following concepts?

A. Conservatism

B. Matching

C. Comparability

D. Going concern

7. On April 20, 20X6, an employee filed a $3,000,000 lawsuit against Johnson Co. for damages suffered when

one of Johnson’s plants exploded. Johnson’s legal counsel expects the company will lose the lawsuit and

estimates the loss to be between $1,500,000 and $2,000,000. The employee has offered to settle the lawsuit

out of court for $1,800,000, but Johnson will not agree to the settlement. In its December 31, 20 X6 balance

sheet, what amount should Johnson report as liability from the lawsuit?

A. $0

B. $1,500,000

C. $1,800,000

D. $2,000,000

19

Fair Value Accounting

Fair values are commonly used in financial reports and have increased in business importance in recent years.

Elaborate financial instruments and risk management practices have created financial statement elements for

which historical cost is less meaningful, increasing the relevance for fair value and fluctuations in fair value. Fair

value information may be more useful than the historical cost for certain types of assets and liabilities and in

certain industries.

ASC 820, Fair Value Measurements, provides a framework for determining fair value for GAAP purposes containing

the following key concepts:

1. Fair value is a market-based measurement, not an entity-specific measurement.

2. Fair value is the price to sell an asset or transfer a liability (an exit price), not the price that is paid to acquire

the asset or received to assume the liability (an entry price).

3. The definition of fair value and the measurement framework applies to assets, liabilities, and instruments

measured at fair value classified in stockholders’ equity.

4. A fair value measurement should be determined based on the assumptions that market participants would

use in pricing the asset or liability.

5. The concepts of highest and best use and valuation in a fair value measurement are only relevant in measuring

the fair value of nonfinancial assets, not financial assets or liabilities.

6. The fair value hierarchy provides a basis for considering market-participant assumptions and distinguishes

between:

✓ Market-participant assumptions developed based on market data that are independent of the entity

(observable inputs); and

✓ An entity’s own assumptions about market-participant assumptions developed based on the best

information available in the particular circumstances, including assumptions about the risk inherent

in inputs or valuation techniques (unobservable inputs)

Observable inputs should be maximized and unobservable inputs should be minimized.

Observable inputs reflect market data obtained from independent sources, while unobservable inputs reflect

an entity’s market assumptions.

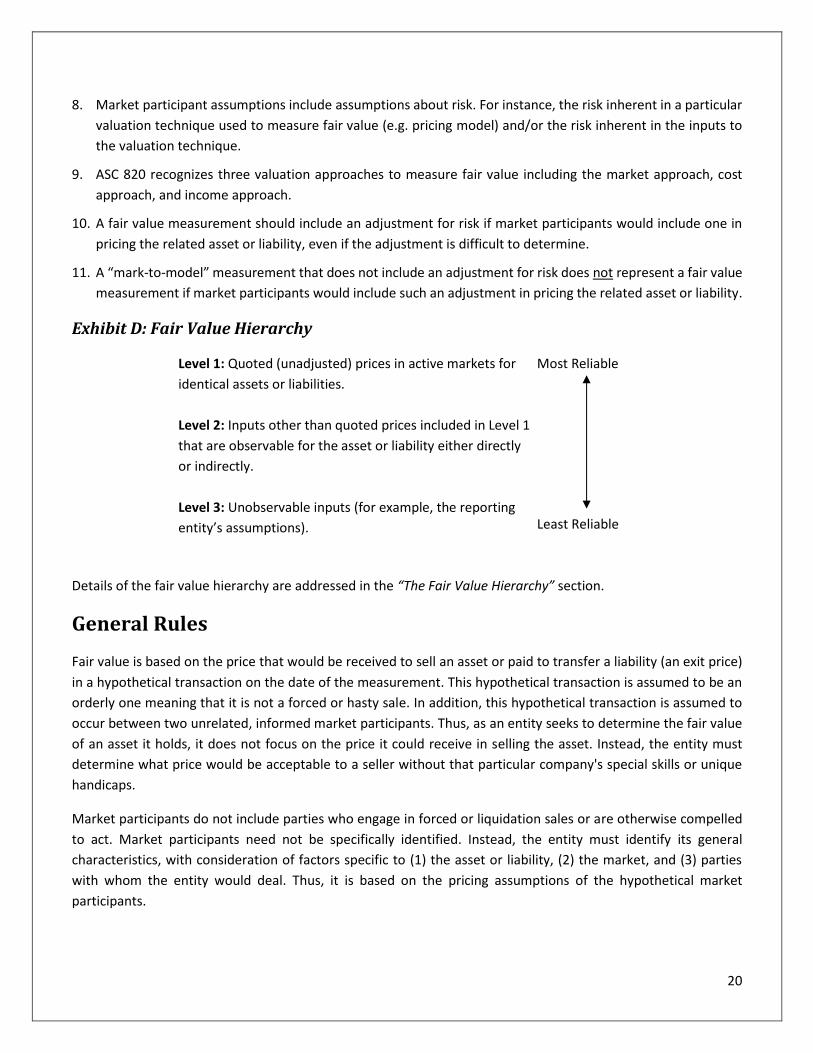

7. The fair value hierarchy prioritizes the inputs to valuation techniques used to measure fair value into three

broad levels. The levels range from the highest priority, which is assigned to quoted prices (unadjusted) in

active markets for identical assets or liabilities (Level 1), to the lowest priority, which is assigned to

unobservable inputs (Level 3).

As shown in Exhibit D, the fair value hierarchy is divided into three broad levels.

20

8. Market participant assumptions include assumptions about risk. For instance, the risk inherent in a particular

valuation technique used to measure fair value (e.g. pricing model) and/or the risk inherent in the inputs to

the valuation technique.

9. ASC 820 recognizes three valuation approaches to measure fair value including the market approach, cost

approach, and income approach.

10. A fair value measurement should include an adjustment for risk if market participants would include one in

pricing the related asset or liability, even if the adjustment is difficult to determine.

11. A “mark-to-model” measurement that does not include an adjustment for risk does not represent a fair value

measurement if market participants would include such an adjustment in pricing the related asset or liability.

Exhibit D: Fair Value Hierarchy

Level 1: Quoted (unadjusted) prices in active markets for

identical assets or liabilities.

Level 2: Inputs other than quoted prices included in Level 1

that are observable for the asset or liability either directly

or indirectly.

Level 3: Unobservable inputs (for example, the reporting

entity’s assumptions).

Most Reliable

Least Reliable

Details of the fair value hierarchy are addressed in the “The Fair Value Hierarchy” section.

General Rules

Fair value is based on the price that would be received to sell an asset or paid to transfer a liability (an exit price)

in a hypothetical transaction on the date of the measurement. This hypothetical transaction is assumed to be an

orderly one meaning that it is not a forced or hasty sale. In addition, this hypothetical transaction is assumed to

occur between two unrelated, informed market participants. Thus, as an entity seeks to determine the fair value

of an asset it holds, it does not focus on the price it could receive in selling the asset. Instead, the entity must

determine what price would be acceptable to a seller without that particular company's special skills or unique

handicaps.

Market participants do not include parties who engage in forced or liquidation sales or are otherwise compelled

to act. Market participants need not be specifically identified. Instead, the entity must identify its general

characteristics, with consideration of factors specific to (1) the asset or liability, (2) the market, and (3) parties

with whom the entity would deal. Thus, it is based on the pricing assumptions of the hypothetical market

participants.

21

A fair value measurement for liability should take into account the risk that the obligation will not be fulfilled

(nonperformance risk). In evaluating this risk, the reporting entity's credit risk should be considered. In addition,

in measuring the fair value of a liability, the quoted price of the asset should not be adjusted for any limitation on

its sale.

A fair value measurement assumes the transaction takes place in the principal market for the asset or liability. The

principal market is one in which the reporting entity would sell the asset or transfer the liability with the greatest

volume and activity level. If there is no principal market, then the most advantageous market should be used. The

most advantageous market is one in which the reporting entity would sell the asset or transfer the liability with

the price that maximizes the amount that would be received for the asset or minimizes the amount that would be

paid to transfer the liability after considering the transaction costs.

In measuring fair value, valuation techniques in conformity with the market, income, and cost approaches should

be used:

1. Under the “market approach,” the prices for market transactions for identical or comparable assets or

liabilities are used. One example of a market approach is matrix pricing. This is a mathematical method used

primarily to value debt securities that are not actively traded. The securities do have readily available quoted

prices. The price of the security is estimated by comparing it to other securities with an active market, and

that have similar maturities, coupon rates, credit rating, etc.

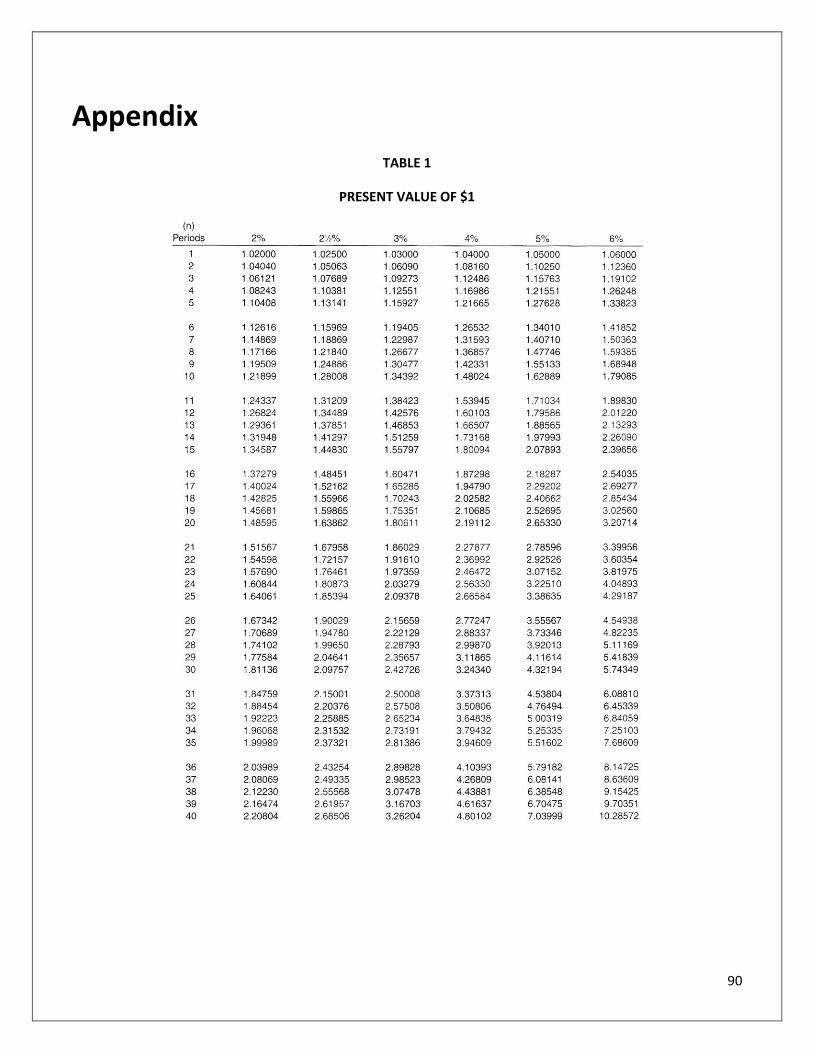

2. Under the “income approach,” valuation techniques are used to convert future amounts (e.g., profits, cash

flows) to a present value amount. For example, future cash flows are discounted to their present value amount

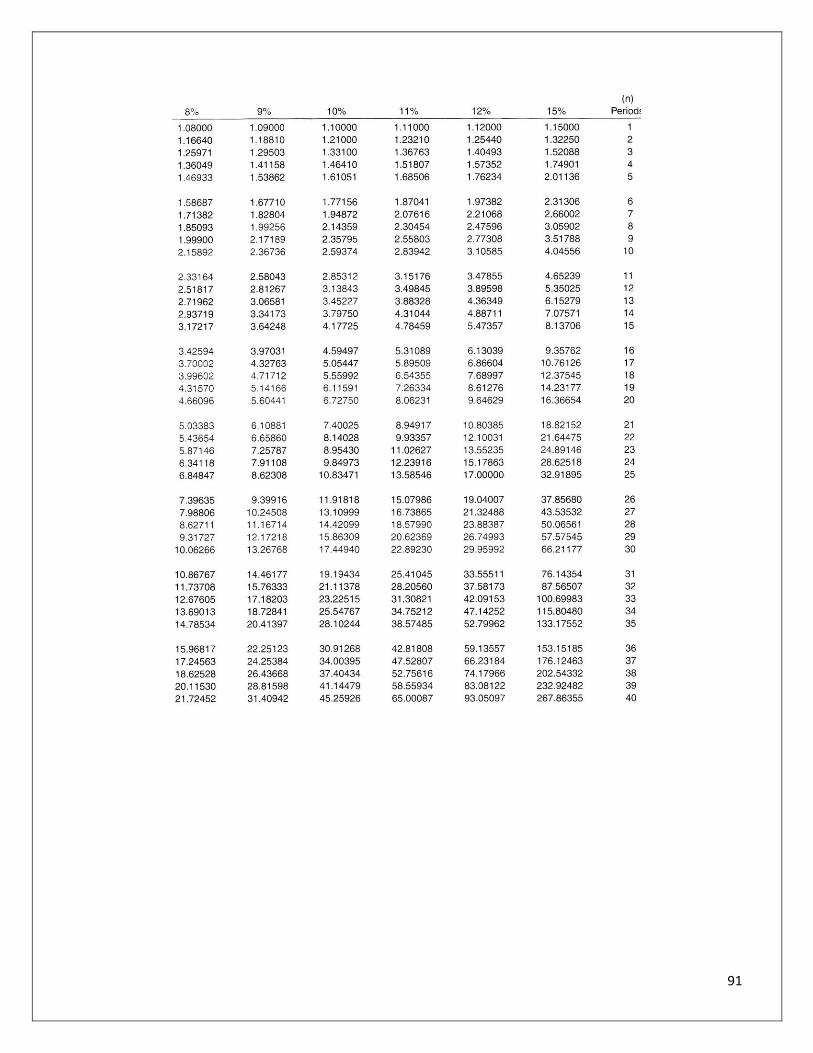

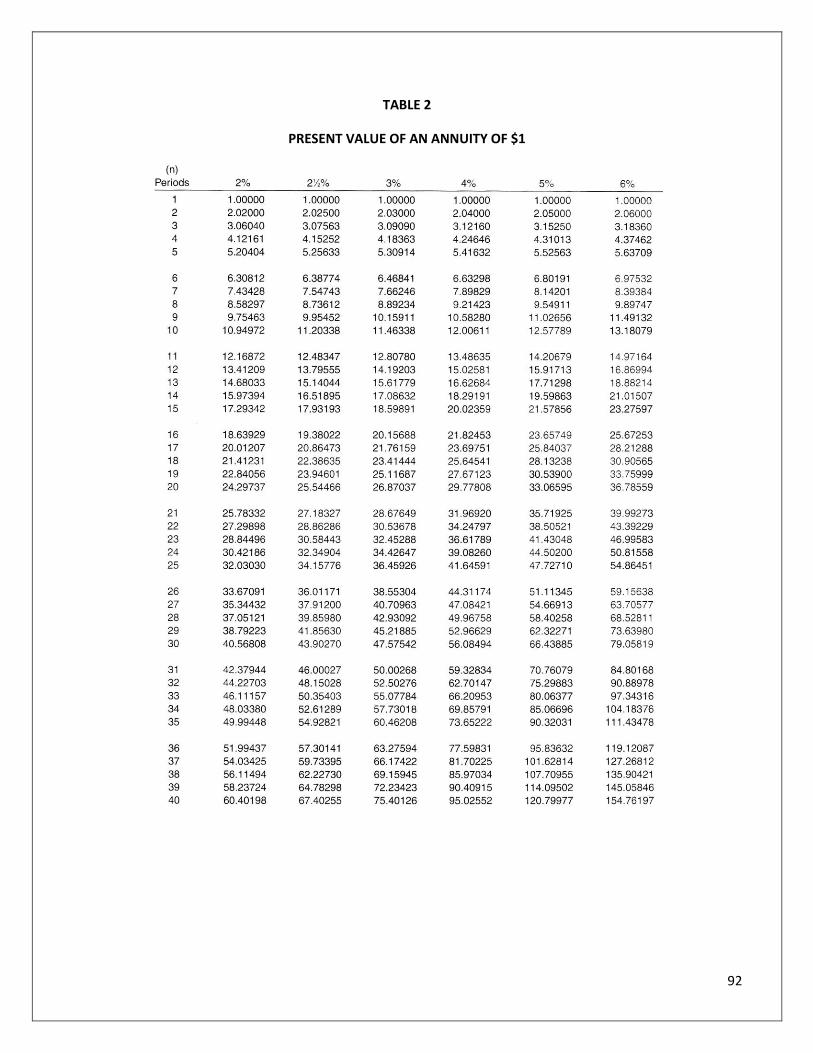

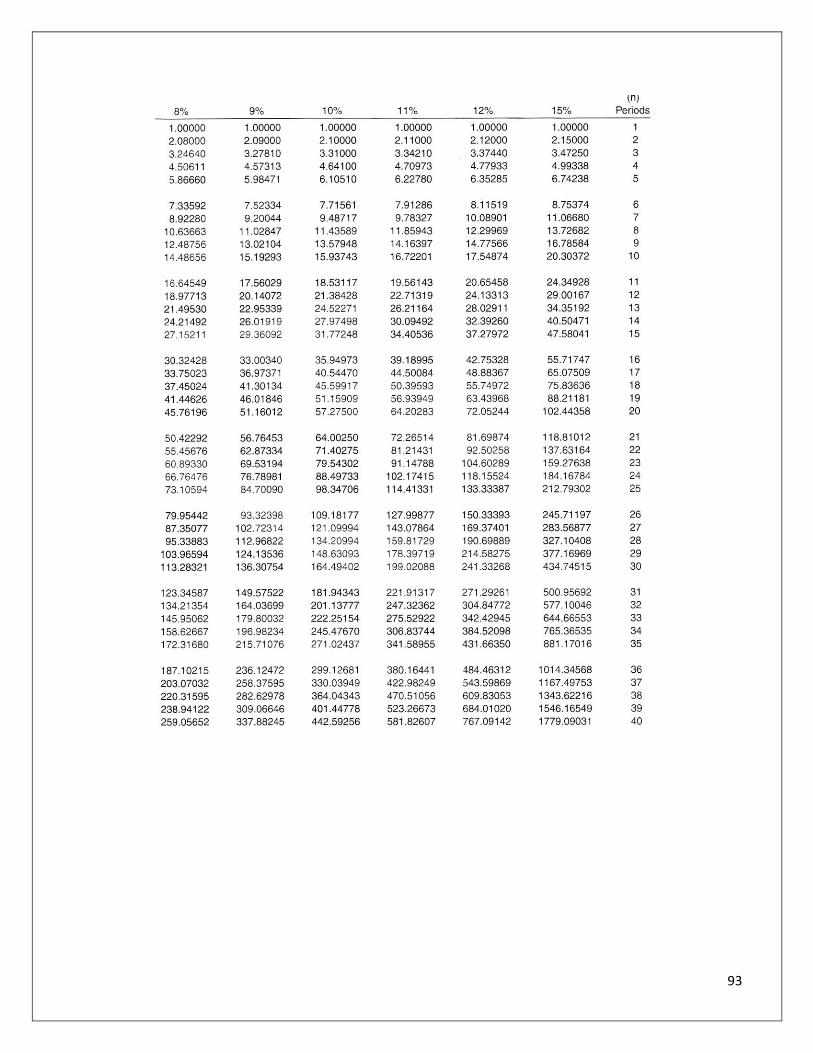

using the present value tables (Tables 1 and 2 in the Appendix). The measurement is based on market

expectations of the future amounts. Examples of these valuation techniques are present value determination,

option pricing models, and the multiyear excess earnings method (to value goodwill).

3. The “cost approach” is based on the amount that would be required to replace an asset's service capability

(current replacement cost). An example is the cost to purchase or build a substitute asset of comparable utility

after adjusting for obsolescence.

Depending on the circumstances, a single or multiple valuation technique may be needed. Input availability and

reliability associated with the asset or liability may influence the selection of the best-suited valuation method.

Scope

ASC 820 applies when accounting pronouncements require or permit fair value measurements, measurements

based on fair value (e.g. fair value less the costs to sell), and disclosures about fair value measurements, except

for:

1. Share-based payment transactions addressed under ASC 505-50 Equity and ASC 718 Compensation −

Stock Compensation (excluding ASC 718-40, which is within the scope of ASC 820); and

2. Accounting pronouncements require or permit measurements that are similar to fair value but that are

NOT intended to measure fair value, including both of the following:

22

The measurement of the standalone selling price

ASC 330 Inventory

3. Recognition and measurement of revenue from contracts with customers under ASC 606 Revenue from

Contracts with Customers

4. Recognition and measurement of gains and losses upon the derecognition of nonfinancial assets under

ASC 610-20 Other Income

Standalone selling price is the price at which an entity would sell a promised good or service separately to a

customer.

ASC 820 does not eliminate certain practicability exceptions presented in other accounting standards. ASC 820-

10-15-3 indicates those practicability exceptions, which include:

1. The use of a transaction price (an entry price) to measure fair value (an exit price) at initial recognition.

For instance, ASC 820 does not impact the ability under ASC 460 to initially measure the fair value (an exit

price) of a guarantee using a transaction price (an entry price).

2. Instruments for which fair value is not reasonably determinable such as:

• Nonmonetary assets under ASC 845 and ASC 605-20-25 and 605-20-50

• Asset retirement obligations under ASC 410-20 and ASC 440-10-50 and 440-10-55

• Restructuring obligations under ASC 420

• Participation rights under ASC 715-30 and 715-60

3. The use of particular measurement methods referred to in ASC 805-20-30-10 allows measurements other

than fair value for specified assets acquired and liabilities assumed in a business combination.

4. Financial assets or financial liabilities of a consolidated variable interest entity that is a collateralized

financing entity when the financial assets or financial liabilities are measured using the measurement

alternative in ASC 810-10-30-10 through 30-15 and ASC 810-10-35-6 through 35-8.

5. Instruments for which fair value cannot be reasonably estimated, such as noncash consideration promised

in a contract under ASC 606-10-32-21 through 32-24.

A collateralized financing entity is a variable interest entity that holds financial assets, issues beneficial interests

in those financial assets, and has no more than nominal equity.

The Fair Value Hierarchy

Inputs to Fair Value Measurement

Under ASC 820, Level 1 inputs are the most reliable and are quoted prices in active markets for identical assets or

liabilities. Level 2 inputs are of intermediate reliability and are prices for similar (but not identical) assets or

liabilities or observable market inputs used in a valuation model. Level 3 inputs are unobservable inputs such as

internal cash flow forecasts, discount rate estimations, and so forth.

23

Level 1 inputs are based on quoted prices (unadjusted) in active markets for identical assets or liabilities that the

reporting entity can access at the measurement date. Thus, Level 1 is the most reliable as it is based on or prices

or quotes from exchanges or listed markets (e.g. Chicago Board of Trade, London Stock Exchange, Tokyo Stock

Exchange, or New York Stock Exchange and Euronext).

Level 2 inputs are those (except quoted prices included within Level 1) that are observable for the asset or liability,

either directly or indirectly. If the asset or liability has a specified (contractual) term, a Level 2 input must be

observable for substantially the full term of the asset or liability. Included as Level 2 inputs are:

1. Quoted prices for similar assets or liabilities in active markets.

2. Quoted prices for similar or identical assets or liabilities in markets that are not active namely in markets

having few transactions, noncurrent prices, price quotations that vary significantly, or very limited public

information.

3. Inputs excluding quoted prices that are observable for the asset or liability. Examples are:

✓ Interest rates observable at often quoted intervals

✓ Credit spreads

✓ Implied volatilities

4. Market-corroborated inputs; inputs derived in most part from observable market data by correlation or

other means.

Adjustments to Level 2 inputs vary depending on factors specific to the asset or liability. Those factors include:

• The location or condition of the asset or liability;

• Market volume and activity level; and

• The extent to which the inputs relate to comparable items to the asset or liability.

A major adjustment to the fair value measurement may result in a Level 3 measurement.

Examples of Level 2 inputs for particular assets and liabilities are discussed in the “Comprehensive Illustrations: 1.

Level 2 Inputs” section.

Level 3 inputs are unobservable for the asset or liability. Unobservable inputs are used to measure fair value to

the extent that observable inputs are unavailable. This allows for cases in which there is little or no market activity

for the asset or liability at the measurement date. Unobservable inputs reflect the reporting entity's own

assumptions about the assumptions (e.g., risk) that market participants would use in pricing the asset or liability.

If an input used to measure fair value is based on bid and ask prices, the price within the bid-ask spread that is

most representative of fair value shall be used to measure fair value regardless of where in the fair value hierarchy

the input falls.

Examples of Level 3 inputs for particular assets and liabilities are discussed in the “Comprehensive Illustrations: 2.

Level 3 Inputs” section.

24

Inactive Market

ASC 820 also addresses valuations in markets that were previously active, but are inactive in the current reporting

period. It provides guidance for estimating fair value when the volume and activity level for the asset or liability

have significantly decreased.

If the reporting entity decides there has been a major decrease in the volume and level of activity for the asset or

liability relative to normal market activity for the asset or liability, transactions or quoted prices may not be

determinative of fair value. Further analysis is needed, and a significant adjustment to the transaction or quoted

prices may be necessary to estimate fair value. Significant adjustments also may be needed in other situations (for

instance, when a price for a similar asset requires significant adjustment to make it more comparable to the asset

being measured or when the price is old).

Even in cases where there has been a significant decrease in the volume and level of activity for the asset or

liability regardless of the valuation technique used, the objective of a fair value measurement remains the same.

Determining the price at which willing market participants would transact at the measurement date under current

market conditions if there has been a significant decrease in the volume and level of activity for the asset or

liability depends on the facts and circumstances and requires the use of judgment. However, a reporting entity's

intention to hold the asset or liability is not relevant in estimating fair value. As mentioned, fair value is a market-

based measurement, not an entity-specific measurement.

Even if there has been a significant decrease in the volume and level of activity for the asset or liability, it is not

appropriate to conclude that all transactions are not orderly (that is, distressed or forced).

Disclosure Requirements

Disclosures are mandated for fair value measurements to improve financial statement user understanding.

Specifically, ASC 820 requires disclosures designed to provide users of financial statements with additional

transparency regarding:

1. The valuation techniques and inputs that a reporting entity uses to arrive at its measures of fair value,

including judgments and assumptions that the entity makes

2. The uncertainty in the fair value measurements as of the reporting date

3. How changes in fair value measurements affect an entity’s performance and cash flows

ASC 820-10-50-1D indicates that when complying with the disclosure requirements, a reporting entity should

consider all of the following:

✓ The level of detail necessary to satisfy the disclosure requirements

✓ How much emphasis to place on each of the various requirements

✓ How much aggregation or disaggregation to undertake

✓ Whether users of financial statements need additional information to evaluate the quantitative

information disclosed

25

The fair value disclosures fall into two categories. The first category is for assets (and liabilities) that are measured

at fair value on a recurring basis. Examples are trading securities, available-for-sale securities, and derivatives.

These items are reported at their fair values on every reporting date. For items measured at fair value on a

recurring basis, the first required valuation input disclosure is a simple table with the assets as the rows and the

three input levels as the columns.

Most balance sheet items are not reported at fair value on a recurring basis but are occasionally reported at fair

value. A common example is impaired assets. The required disclosure for assets reported at fair value on a

nonrecurring basis. With items reported at fair value on a nonrecurring basis, it is unlikely that Level 1 inputs will

be available in the disclosure. A reconciliation of the beginning and ending balances is required for any assets or

liabilities measured at fair value on a recurring basis that use Level 3 (that is, significant unobservable inputs)

during the period.

26

Comprehensive Illustrations

Illustration 1: Level 2 Inputs

ASC 820 provides the following examples of Level 2 inputs for particular assets and liabilities.

820-10-55-21

Examples of Level 2 inputs for particular assets and liabilities include the following:

a. Receive-fixed, pay-variable interest rate swap based on the London Interbank Offered Rate (LIBOR) swap rate.

A Level 2 input would be the LIBOR swap rate if that rate is observable at commonly quoted intervals for

substantially the full term of the swap.

b. Receive-fixed, pay-variable interest rate swap based on a yield curve denominated in a foreign currency. A

Level 2 input would be the swap rate based on a yield curve denominated in a foreign currency that is

observable at commonly quoted intervals for substantially the full term of the swap. That would be the case

if the term of the swap is 10 years and that rate is observable at commonly quoted intervals for 9 years,

provided that any reasonable extrapolation of the yield curve for Year 10 would not be significant to the fair

value measurement of the swap in its entirety.

c. Receive-fixed, pay-variable interest rate swap based on a specific bank’s prime rate. A Level 2 input would be

the bank’s prime rate derived through extrapolation if the extrapolated values are corroborated by observable

market data, for example, by correlation with an interest rate that is observable over substantially the full

term of the swap.

d. Three-year option on exchange-traded shares. A Level 2 input would be the implied volatility for the shares