Embed Size (px)

Citation preview

FINANCIAL INSTITUTIONS

CREDIT OPINION9 November 2018

Update

RATINGS

Banco Modal S.A.Domicile Rio de Janeiro, Rio de

Janeiro, Brazil

Long Term CRR Ba3

Type LT Counterparty RiskRating - Fgn Curr

Outlook Not Assigned

Long Term Debt Not Assigned

Long Term Deposit B1

Type LT Bank Deposits - FgnCurr

Outlook Stable

Please see the ratings section at the end of this reportfor more information. The ratings and outlook shownreflect information as of the publication date.

Analyst Contacts

AlexandreAlbuquerque

+55.11.3043.7356

VP-Senior [email protected]

Farooq Khan [email protected]

Vicente Gomez +52.55.1555.5304Associate [email protected]

Aaron Freedman +52.55.1253.5713Associate Managing [email protected]

» Contacts continued on last page

CLIENT SERVICES

Americas 1-212-553-1653

Asia Pacific 852-3551-3077

Japan 81-3-5408-4100

EMEA 44-20-7772-5454

Banco Modal S.A.Update to credit analysis

SummaryBanco Modal S.A.'s (Modal) baseline credit assessment (BCA) of b1 takes into considerationthe bank's reliance on market funds, deteriorating profitability, moderate capitalization, highlevel of charge offs and high level of concentrations. The bank's ample liquidity, partiallyoffsetting these challenges. The standalone assessment also factors in the risks associatedwith the bank's large exposure to merchant banking investments.

The deposit and senior debt ratings of B1 are based on Modal's BCA of b1, and do not benefitfrom any parental and government support uplift, given our assessment of a low probabilityof support, owing to the bank's modest market share in domestic deposits.

Exhibit 1

Rating Scorecard - Key financial ratios

1.8% 8.4%

-0.8%

13.4% 67.7%

-13%

-3%

7%

17%

27%

37%

47%

57%

67%

77%

-2%

0%

2%

4%

6%

8%

10%

12%

Asset Risk:Problem Loans/

Gross Loans

Capital:Tangible Common

Equity/Risk-WeightedAssets

Profitability:Net Income/

Tangible Assets

Funding Structure:Market Funds/

Tangible BankingAssets

Liquid Resources:Liquid Banking

Assets/TangibleBanking Assets

Solvency Factors (LHS) Liquidity Factors (RHS)

Banco Modal S.A. (BCA: b1) Median b1-rated banks

So

lve

ncy F

acto

rs

Liq

uid

ity F

acto

rs

Source: Moody's Financial Metrics

THIS REPORT WAS REPUBLISHED ON 14 NOVEMBER 2018 TO INCLUDE A PARAGRAPH ON PAGE 3 REGARDING THEBANK'S LOAN BOOK AND A PARAGRAPH ON PAGE 4 DISCUSSING POTENTIAL FUTURE EARNINGS GENERATIONFROM FEE-BASED ACTIVITIES, INCLUDING 'MODALMAIS' DIGITAL PLATFORM.

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

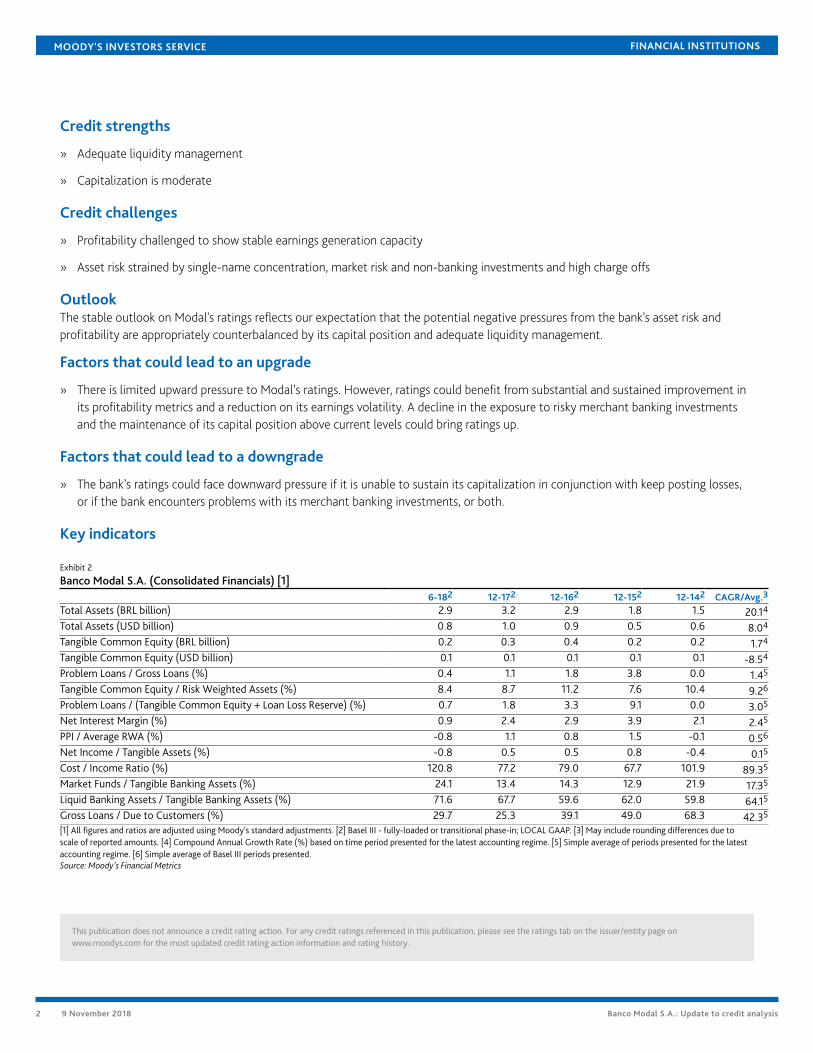

Credit strengths

» Adequate liquidity management

» Capitalization is moderate

Credit challenges

» Profitability challenged to show stable earnings generation capacity

» Asset risk strained by single-name concentration, market risk and non-banking investments and high charge offs

OutlookThe stable outlook on Modal's ratings reflects our expectation that the potential negative pressures from the bank's asset risk andprofitability are appropriately counterbalanced by its capital position and adequate liquidity management.

Factors that could lead to an upgrade

» There is limited upward pressure to Modal’s ratings. However, ratings could benefit from substantial and sustained improvement inits profitability metrics and a reduction on its earnings volatility. A decline in the exposure to risky merchant banking investmentsand the maintenance of its capital position above current levels could bring ratings up.

Factors that could lead to a downgrade

» The bank’s ratings could face downward pressure if it is unable to sustain its capitalization in conjunction with keep posting losses,or if the bank encounters problems with its merchant banking investments, or both.

Key indicators

Exhibit 2

Banco Modal S.A. (Consolidated Financials) [1]6-182 12-172 12-162 12-152 12-142 CAGR/Avg.3

Total Assets (BRL billion) 2.9 3.2 2.9 1.8 1.5 20.14

Total Assets (USD billion) 0.8 1.0 0.9 0.5 0.6 8.04

Tangible Common Equity (BRL billion) 0.2 0.3 0.4 0.2 0.2 1.74

Tangible Common Equity (USD billion) 0.1 0.1 0.1 0.1 0.1 -8.54

Problem Loans / Gross Loans (%) 0.4 1.1 1.8 3.8 0.0 1.45

Tangible Common Equity / Risk Weighted Assets (%) 8.4 8.7 11.2 7.6 10.4 9.26

Problem Loans / (Tangible Common Equity + Loan Loss Reserve) (%) 0.7 1.8 3.3 9.1 0.0 3.05

Net Interest Margin (%) 0.9 2.4 2.9 3.9 2.1 2.45

PPI / Average RWA (%) -0.8 1.1 0.8 1.5 -0.1 0.56

Net Income / Tangible Assets (%) -0.8 0.5 0.5 0.8 -0.4 0.15

Cost / Income Ratio (%) 120.8 77.2 79.0 67.7 101.9 89.35

Market Funds / Tangible Banking Assets (%) 24.1 13.4 14.3 12.9 21.9 17.35

Liquid Banking Assets / Tangible Banking Assets (%) 71.6 67.7 59.6 62.0 59.8 64.15

Gross Loans / Due to Customers (%) 29.7 25.3 39.1 49.0 68.3 42.35

[1] All figures and ratios are adjusted using Moody's standard adjustments. [2] Basel III - fully-loaded or transitional phase-in; LOCAL GAAP. [3] May include rounding differences due toscale of reported amounts. [4] Compound Annual Growth Rate (%) based on time period presented for the latest accounting regime. [5] Simple average of periods presented for the latestaccounting regime. [6] Simple average of Basel III periods presented.Source: Moody's Financial Metrics

This publication does not announce a credit rating action. For any credit ratings referenced in this publication, please see the ratings tab on the issuer/entity page onwww.moodys.com for the most updated credit rating action information and rating history.

2 9 November 2018 Banco Modal S.A.: Update to credit analysis

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

ProfileModal is an investment bank, with BRL2.9 billion of assets as of June 2018. The bank's main businesses are advisory, capital market,brokerage, and merger and acquisition services. The bank is small compared with Brazil's overall banking system, with a market share ofless than 1% each in terms of deposits, assets and loans as of June 2018. Created in 1996, Modal has offices in Rio de Janeiro and SaoPaulo, and a branch in the Cayman Islands.

Detailed credit considerationsThis assessment takes into account Modal's Prudencial Conglomerate financial statements, which include the statements of BancoModal S.A. and its subsidiaries, and Modal Administradora de Recursos Ltda.

Asset risk strained by single-name concentration, market risk and non-banking investments and high charge offsThe b1 score for Asset Risk reflects the inherent borrower concentration in Modal's loan book and relevant non-lending credit risks.Also, it is somewhat weighted by the bank's exposure to market risk, which represented 8.9% of its total capital requirement as of June2018, though down from the 25% of the same period last year.

Modal's total credit risk exposure, including loans, private securities and guarantees, declined by 20.6% in the 12 months ended June2018. This decline was driven mainly by a sharp decline in the bank's loan book (-27%).

The problem loan ratio was equivalent to 0.4% as of June 2018, and experienced high volatility in the last years, which reflects thefacts that (1) the bank's loan book is somewhat concentrated, and (2) there are still negative pressures arising from the economicenvironment. In addition, the bank presented charge offs equivalent to 4.8% of the bank's gross loans as of June 2018.

However, the bank's reserve coverage is still ample as loan loss reserves represented a high 727% of problem loans as of June 2018,which can give an ample loss absorbing cushion against unexpected losses.

Modal has a meaningful volume of investments allocated to merchant banking. In the last few years, the fair value assessment of theseinvestments resulted in gains that are accounted for directly in the bank’s shareholders' equity. Although an impairment analysis ofthese investments is carried out each six to 12 months, the continued success and future valuation of these investments is difficult toforecast with any certainty because these investments are mostly in non-financial private companies with limited transparency.

Risks related to high borrower concentration remains a concern, particularly when compared to same rated peers. This challengereflects Modal’s exposure to a limited number of sectors and will continue to expose asset quality to potentially high volatility. As ofJune 2018, the bank’s exposure to the infrastructure sector, including loans and private securities, represented about 27% of the bank’stotal loans. That said, we expect that the bank will maintain reasonable levels of reserves for loan losses, which will help mitigate assetrisks.

Capitalization is moderateThe b2 Capital score reflects Moody's capital measure, represented by the ratio of tangible common equity to risk-weighted assets(TCE/RWA) of 8.4% as of June 2018, which declined from 11.2% in December 2016. The sharp drop in capital levels was because of asignificant increase in intangible assets, which we deduct from TCE because such assets do not have good extraordinary loss absorptioncapacity.

However, Modal has reported adequate regulatory capital, illustrated by its Common Equity Tier 1 ratio of 12.8% as of June 2018compared with 13.9% as of June 2017. The trend of Modal’s capital position will be directly linked to its ability to generate capital withinternal results to support its ongoing growth in operations.

Profitability challenged to show stable earnings generation capacityThe caa2 profitability score captures the potential challenges arising from Modal's ability to sustain stable earnings in a slow businessenvironment. Also, the score takes into account the revenue contribution from segments that are more subject to volatility, includinginvestment banking, sales, and trading and merchant banking.

As such the bank posted a net income to tangible banking assets of -0.8% due to a lower net interest income, net interest margincompressed to 0.87% from the last three year average of 3%. At the same time the bank efficiency worsened due to higher

3 9 November 2018 Banco Modal S.A.: Update to credit analysis

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

administrative and personnel expenses. The operating expense increased 47% year-over-year, while its loan book contracted asignificantly 27%.

Historically, Modal has recorded meaningful volumes of unrealized gains, which were equivalent to 0.4% of its tangible assets as ofJune 2018. The current unrealized gains are mainly related to the positive evaluation of the bank's merchant banking investments andsecurities. The unrealized gains and losses are incorporated into our profitability assessment when they become effectively realized.Therefore, the bank's stock of unrealized gains may benefit its future results if they are realized at current levels.

Moody’s expects future earnings recurrence to improve in the next 12 to 18 months as Modal focuses on enhancing fee-based incomeactivities, that helps to insulate earnings volatility from trading and credit. To this end, the bank is promoting its newly created digitalplatform ModalMais, which will add more granular revenues, and increasing its mutual and private equity funds activities, includingcustody and administration services. That said, we will continue to closely monitor the bank’s ability to implement its business plan andto consistently improve its recurring earnings.

Large volume of liquid resourcesThe Combined Liquidity score of baa3 captures the bank's large volume of liquid assets.

Modal holds a large volume of liquid resources even after deducting the illiquid investments from its securities portfolio, mainlyincluding its merchant banking investments, and other instruments with lower liquidity, such as debentures. The bank also maintains afavorable tenor gap in the maturity of its assets and liabilities.

Modal's rating is supported by the Moderate- Macro Profile of BrazilBrazil's Moderate- Macro Profile reflects the large size and diversified nature of the country's economy, more credible monetary policy,increasing commitment to addressing corruption and improving overall government effectiveness, and very low susceptibility toexternal shocks. However, Brazil's economic rebound, which began in 2017 after a deep two-year recession, has been weaker thanexpected, reflecting the high degree of uncertainty surrounding policy continuity beyond 2019.

Although public-sector banks continue to account for a substantial portion of total credit, loans granted by them have beencontracting since 2015, which has reduced the market distortions created by their previous aggressive lending policies. Moderateeconomic growth in 2018 and 2019 will support modest lending growth over the next 12 months. Consequently, banks will face little tono pressure on their funding needs, while low interest rates and low inflation will improve borrowers' repayment capacity, leading to astabilization in asset quality.

Support and structural considerationsGovernment supportWe believe there is a low likelihood of government support for Modal's rated deposits, given its modest market share of deposits inBrazil.

Counterparty Risk (CR) AssessmentCR Assessments are opinions of how counterparty obligations are likely to be treated if a bank fails and are distinct from debt anddeposit ratings in that they (1) consider only the risk of default rather than both the likelihood of default and the expected financial losssuffered in the event of default, and (2) apply to counterparty obligations and contractual commitments rather than debt or depositinstruments. The CR Assessment is an opinion on the counterparty risk related to a bank’s covered bonds, contractual performanceobligations (servicing), derivatives (e.g., swaps), letters of credit, guarantees and liquidity facilities.

Modal's CR Assessment is positioned at Ba3(cr)/Not Prime(cr)The CR Assessment is one notch above the bank's adjusted BCA of b1, and, therefore, above the bank's deposit rating, reflecting ourview that the probability of default is lower at the operating obligations than at the level of deposits. Modal's CR Assessment does notbenefit from government support because such support is not incorporated in the bank's deposit ratings.

Counterparty Risk Rating (CRR)Moody’s Counterparty Risk Ratings are opinions of the ability of entities to honor the uncollateralized portion of non-debt counterpartyfinancial liabilities (CRR liabilities) and also reflect the expected financial losses in the event such liabilities are not honored. CRR

4 9 November 2018 Banco Modal S.A.: Update to credit analysis

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

liabilities typically relate to transactions with unrelated parties. Examples of CRR liabilities include the uncollateralized portion ofpayables arising from derivatives transactions and the uncollateralized portion of liabilities under sale and repurchase agreements. CRRsare not applicable to funding commitments or other obligations associated with covered bonds, letters of credit, guarantees, servicerand trustee obligations, and other similar obligations that arise from a bank performing its essential operating functions.

Modal's CRR is positioned at Ba3/Not PrimeModal's global local and foreign currency CRRs are positioned at Ba3 and Not Prime, one notch above the bank's adjusted BCA,reflecting the lower probability of default of CRR liabilities and our expectation of a normal level of loss given default.

About Moody's Bank ScorecardOur scorecard is designed to capture, express and explain in summary form our Rating Committee’s judgment. When read inconjunction with our research, a fulsome presentation of our judgment is expressed. As a result, the output of our scorecardmay materially differ from that suggested by raw data alone (though it has been calibrated to avoid the frequent need for strongdivergence). The scorecard output and the individual scores are discussed in rating committees and may be adjusted up or down toreflect conditions specific to each rated entity.

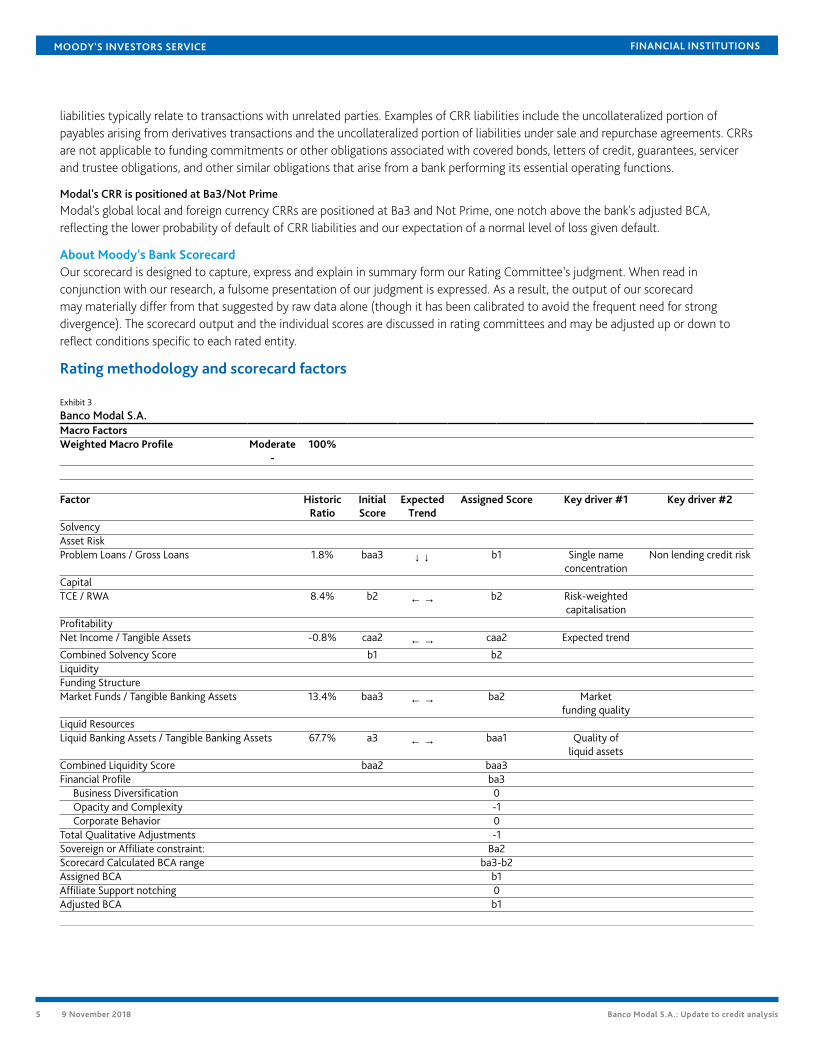

Rating methodology and scorecard factors

Exhibit 3

Banco Modal S.A.Macro FactorsWeighted Macro Profile Moderate

-100%

Factor HistoricRatio

InitialScore

ExpectedTrend

Assigned Score Key driver #1 Key driver #2

SolvencyAsset RiskProblem Loans / Gross Loans 1.8% baa3 ↓ ↓ b1 Single name

concentrationNon lending credit risk

CapitalTCE / RWA 8.4% b2 ← → b2 Risk-weighted

capitalisationProfitabilityNet Income / Tangible Assets -0.8% caa2 ← → caa2 Expected trend

Combined Solvency Score b1 b2LiquidityFunding StructureMarket Funds / Tangible Banking Assets 13.4% baa3 ← → ba2 Market

funding qualityLiquid ResourcesLiquid Banking Assets / Tangible Banking Assets 67.7% a3 ← → baa1 Quality of

liquid assetsCombined Liquidity Score baa2 baa3Financial Profile ba3

Business Diversification 0Opacity and Complexity -1Corporate Behavior 0

Total Qualitative Adjustments -1Sovereign or Affiliate constraint: Ba2Scorecard Calculated BCA range ba3-b2Assigned BCA b1Affiliate Support notching 0Adjusted BCA b1

5 9 November 2018 Banco Modal S.A.: Update to credit analysis

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

Instrument class Loss GivenFailure notching

AdditionalNotching

Preliminary RatingAssessment

GovernmentSupport notching

Local CurrencyRating

ForeignCurrency

RatingCounterparty Risk Rating 1 0 ba3 0 Ba3 Ba3Counterparty Risk Assessment 1 0 ba3 (cr) 0 Ba3 (cr) --Deposits 0 0 b1 0 B1 B1[1] Where dashes are shown for a particular factor (or sub-factor), the score is based on non-public information.Source: Moody's Financial Metrics

6 9 November 2018 Banco Modal S.A.: Update to credit analysis

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

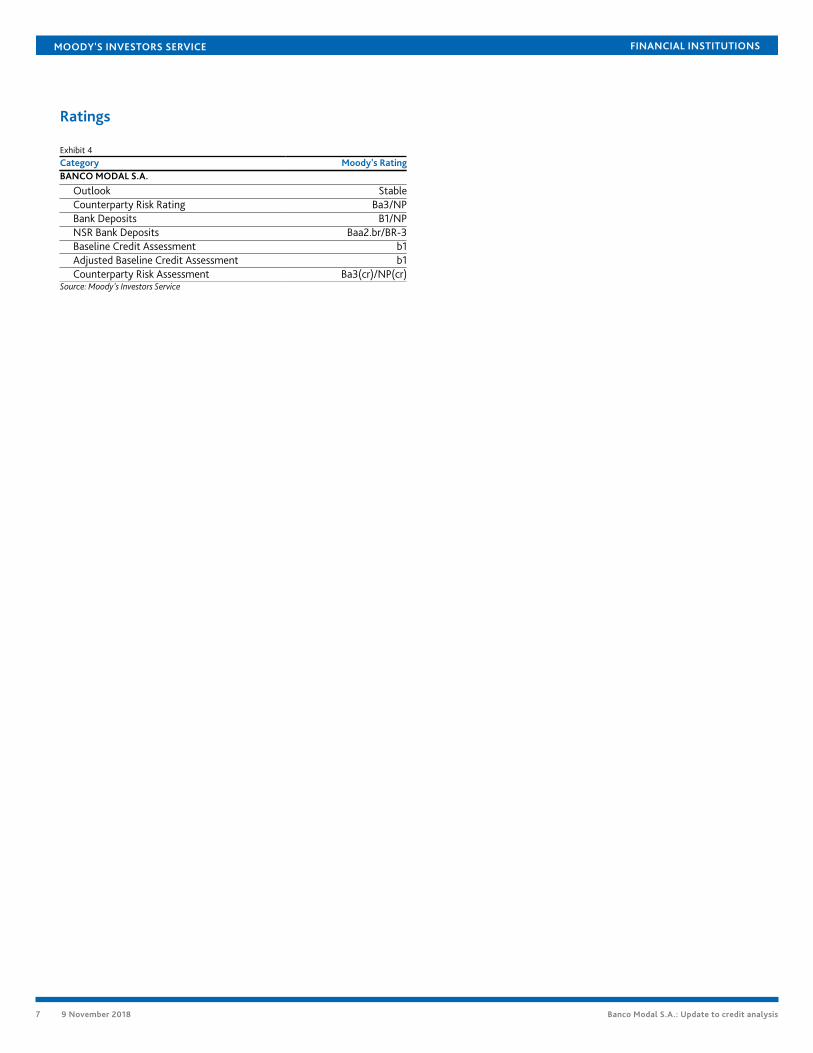

Ratings

Exhibit 4Category Moody's RatingBANCO MODAL S.A.

Outlook StableCounterparty Risk Rating Ba3/NPBank Deposits B1/NPNSR Bank Deposits Baa2.br/BR-3Baseline Credit Assessment b1Adjusted Baseline Credit Assessment b1Counterparty Risk Assessment Ba3(cr)/NP(cr)

Source: Moody's Investors Service

7 9 November 2018 Banco Modal S.A.: Update to credit analysis

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

© 2018 Moody’s Corporation, Moody’s Investors Service, Inc., Moody’s Analytics, Inc. and/or their licensors and affiliates (collectively, “MOODY’S”). All rights reserved.

CREDIT RATINGS ISSUED BY MOODY'S INVESTORS SERVICE, INC. AND ITS RATINGS AFFILIATES (“MIS”) ARE MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDITRISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND MOODY’S PUBLICATIONS MAY INCLUDE MOODY’S CURRENT OPINIONS OF THERELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES. MOODY’S DEFINES CREDIT RISK AS THE RISK THAT AN ENTITYMAY NOT MEET ITS CONTRACTUAL, FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT. CREDIT RATINGSDO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKET VALUE RISK, OR PRICE VOLATILITY. CREDIT RATINGS AND MOODY’SOPINIONS INCLUDED IN MOODY’S PUBLICATIONS ARE NOT STATEMENTS OF CURRENT OR HISTORICAL FACT. MOODY’S PUBLICATIONS MAY ALSO INCLUDE QUANTITATIVEMODEL-BASED ESTIMATES OF CREDIT RISK AND RELATED OPINIONS OR COMMENTARY PUBLISHED BY MOODY’S ANALYTICS, INC. CREDIT RATINGS AND MOODY’SPUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT AND DO NOTPROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. NEITHER CREDIT RATINGS NOR MOODY’S PUBLICATIONS COMMENT ON THESUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. MOODY’S ISSUES ITS CREDIT RATINGS AND PUBLISHES MOODY’S PUBLICATIONS WITH THE EXPECTATIONAND UNDERSTANDING THAT EACH INVESTOR WILL, WITH DUE CARE, MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FORPURCHASE, HOLDING, OR SALE.

MOODY’S CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT INTENDED FOR USE BY RETAIL INVESTORS AND IT WOULD BE RECKLESS AND INAPPROPRIATE FORRETAIL INVESTORS TO USE MOODY’S CREDIT RATINGS OR MOODY’S PUBLICATIONS WHEN MAKING AN INVESTMENT DECISION. IF IN DOUBT YOU SHOULD CONTACTYOUR FINANCIAL OR OTHER PROFESSIONAL ADVISER. ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW,AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTEDOR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANYPERSON WITHOUT MOODY’S PRIOR WRITTEN CONSENT.

CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT INTENDED FOR USE BY ANY PERSON AS A BENCHMARK AS THAT TERM IS DEFINED FOR REGULATORY PURPOSESAND MUST NOT BE USED IN ANY WAY THAT COULD RESULT IN THEM BEING CONSIDERED A BENCHMARK.

All information contained herein is obtained by MOODY’S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as wellas other factors, however, all information contained herein is provided “AS IS” without warranty of any kind. MOODY'S adopts all necessary measures so that the information ituses in assigning a credit rating is of sufficient quality and from sources MOODY'S considers to be reliable including, when appropriate, independent third-party sources. However,MOODY’S is not an auditor and cannot in every instance independently verify or validate information received in the rating process or in preparing the Moody’s publications.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability to any person or entity for anyindirect, special, consequential, or incidental losses or damages whatsoever arising from or in connection with the information contained herein or the use of or inability to use anysuch information, even if MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers is advised in advance of the possibility of such losses ordamages, including but not limited to: (a) any loss of present or prospective profits or (b) any loss or damage arising where the relevant financial instrument is not the subject of aparticular credit rating assigned by MOODY’S.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability for any direct or compensatorylosses or damages caused to any person or entity, including but not limited to by any negligence (but excluding fraud, willful misconduct or any other type of liability that, for theavoidance of doubt, by law cannot be excluded) on the part of, or any contingency within or beyond the control of, MOODY’S or any of its directors, officers, employees, agents,representatives, licensors or suppliers, arising from or in connection with the information contained herein or the use of or inability to use any such information.

NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCHRATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY’S IN ANY FORM OR MANNER WHATSOEVER.

Moody’s Investors Service, Inc., a wholly-owned credit rating agency subsidiary of Moody’s Corporation (“MCO”), hereby discloses that most issuers of debt securities (includingcorporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by Moody’s Investors Service, Inc. have, prior to assignment of any rating,agreed to pay to Moody’s Investors Service, Inc. for appraisal and rating services rendered by it fees ranging from $1,500 to approximately $2,500,000. MCO and MIS also maintainpolicies and procedures to address the independence of MIS’s ratings and rating processes. Information regarding certain affiliations that may exist between directors of MCO andrated entities, and between entities who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more than 5%, is posted annually atwww.moodys.com under the heading “Investor Relations — Corporate Governance — Director and Shareholder Affiliation Policy.”

Additional terms for Australia only: Any publication into Australia of this document is pursuant to the Australian Financial Services License of MOODY’S affiliate, Moody’s InvestorsService Pty Limited ABN 61 003 399 657AFSL 336969 and/or Moody’s Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL 383569 (as applicable). This document is intendedto be provided only to “wholesale clients” within the meaning of section 761G of the Corporations Act 2001. By continuing to access this document from within Australia, yourepresent to MOODY’S that you are, or are accessing the document as a representative of, a “wholesale client” and that neither you nor the entity you represent will directly orindirectly disseminate this document or its contents to “retail clients” within the meaning of section 761G of the Corporations Act 2001. MOODY’S credit rating is an opinion asto the creditworthiness of a debt obligation of the issuer, not on the equity securities of the issuer or any form of security that is available to retail investors. It would be recklessand inappropriate for retail investors to use MOODY’S credit ratings or publications when making an investment decision. If in doubt you should contact your financial or otherprofessional adviser.

Additional terms for Japan only: Moody's Japan K.K. (“MJKK”) is a wholly-owned credit rating agency subsidiary of Moody's Group Japan G.K., which is wholly-owned by Moody’sOverseas Holdings Inc., a wholly-owned subsidiary of MCO. Moody’s SF Japan K.K. (“MSFJ”) is a wholly-owned credit rating agency subsidiary of MJKK. MSFJ is not a NationallyRecognized Statistical Rating Organization (“NRSRO”). Therefore, credit ratings assigned by MSFJ are Non-NRSRO Credit Ratings. Non-NRSRO Credit Ratings are assigned by anentity that is not a NRSRO and, consequently, the rated obligation will not qualify for certain types of treatment under U.S. laws. MJKK and MSFJ are credit rating agencies registeredwith the Japan Financial Services Agency and their registration numbers are FSA Commissioner (Ratings) No. 2 and 3 respectively.

MJKK or MSFJ (as applicable) hereby disclose that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferredstock rated by MJKK or MSFJ (as applicable) have, prior to assignment of any rating, agreed to pay to MJKK or MSFJ (as applicable) for appraisal and rating services rendered by it feesranging from JPY200,000 to approximately JPY350,000,000.

MJKK and MSFJ also maintain policies and procedures to address Japanese regulatory requirements.

REPORT NUMBER 1149288

8 9 November 2018 Banco Modal S.A.: Update to credit analysis

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

Analyst Contacts

Alexandre Albuquerque +55.11.3043.7356VP-Senior [email protected]

Farooq Khan [email protected]

Vicente Gomez +52.55.1555.5304Associate [email protected]

Aaron Freedman +52.55.1253.5713Associate [email protected]

CLIENT SERVICES

Americas 1-212-553-1653

Asia Pacific 852-3551-3077

Japan 81-3-5408-4100

EMEA 44-20-7772-5454

9 9 November 2018 Banco Modal S.A.: Update to credit analysis