Embed Size (px)

Citation preview

- 1 -

Bandwidth Intensive Applications: Demand Trends, Usage Forecasts, and Comparative Costs

Bharat Rao Associate Professor of Management

5 Metrotech Center Polytechnic University

Brooklyn, New York, 11201 USA

Bojan Angelov Doctoral Student in Technology Management

5 Metrotech Center Polytechnic University

Brooklyn, New York, 11201 USA

Last updated: July 4, 2005 This material is based upon work supported by the National Science Foundation under Grant No. ANI-0312376. Any opinions, findings and conclusions or recommendations expressed in this material are those of the author(s) and do not necessarily reflect the views of the NSF.

- 2 -

Bandwidth Intensive Applications:

Demand Trends, Usage Forecasts, and Comparative Costs 1. Introduction The rollout of high speed bandwidth infrastructure supports several new and interesting applications and services that would otherwise be impossible to support and deliver. In this paper, we describe key current and emerging applications relevant to a high speed bandwidth context. We describe the major types of connectivity currently available in the market, and possible applications that they support. We describe how some of these applications and services are more suited for a dynamic bandwidth-on-demand type of provisioning. 2. Background & Methodology During the first year of this NSF supported study, we conducted a survey among large corporations from different industries (finance, retail, education, IT, and entertainment) asking for their bandwidth utilization behavior, the technologies and applications they use and how they use them. However, since most of the information that we needed was considered strictly confidential and proprietary, we needed additional information in order to model the bandwidth demand correctly. At the same time we tried to build effective relationships with several service providers because we consider their customer data and network measurements to be of great importance in modeling the bandwidth demand (for fast file transfer) in the business sector. In addition, we searched various publicly available resources (such as Internet documents, journal papers, government reports, and public notices) for information on bandwidth usage and projections for future consumption. Based on our research, we identified several existing applications, along with a few emerging ones, to be increasingly interesting with regards to the bandwidth-on-demand service offering. They include Video Conferencing, Storage Area Networks and Video on Demand. Our analysis consists of the following components:

Analysis of the current state of technology supporting the application, the current demand for the application, and other related applications.

Technical and economic feasibility of the application and a summary of available forecasts and trends.

3. Types of Bandwidth Provisioning Metro Ethernet Network (MEN) A Metro Ethernet Network is the generally defined as the network that bridges or comments geographically separated enterprise LANs while also connection across the

- 3 -

WAN or backbone networks that are generally owned by service providers. The Metro Ethernet Networks provide connectivity services across Metro geography utilizing Ethernet as the core protocol and enabling broadband applications. The ethernet is a widely deployed cost-effective and well-known technology, and Ethernet interfaces are available on a plethora of data communication/telecommunication devices. Standards-complaint interfaces are available for 10/100/1000 Mbps and the standard of 10Gbps Ethernet was ratified in the IEEE in 2002. In Metropolitan Area Networks (MANs), Ethernet has the potential to cost-effective increase network capability and offer a wide range of service offering in a scalable, simple and flexible manner. An Ethernet based MAN is generally termed a Metro Ethernet Network (MEN). Some services providers have extended the MEN- like technology for the Wide Area Network (WAN) as well [1]. Leased Line Market A leased line market is sales of lease for permanent connection to the Internet. Some common leased models include: T1 A T-1 line is a high-speed digital connection capable of transmitting data at a rate of approximately 1.544 million bits per second. Small and medium sized companies with heavy network traffic typically use T-1 line. It is large enough to send and receive very large text files, graphics, sounds, and databases instantaneously, and is the fastest speed commonly used to connect networks to the Internet. Sometimes referred to as a leased line, a T-1 is basically too large and too expensive for individual home use. T3 A T-3 line is a super high-speed connection capable of transmitting data at a rate of 45 million bps (bits per second). A T-3 line represents a bandwidth equal to about 672 regular voice grade telephone lines, which is wide enough to transmit full motion, real-time video, and very large databases over a busy network. A T-3 line is typically installed as a major networking artery for large corporations and universities with high volume network traffic. For example, the backbones of the major Internet service providers are comprised of T-3 lines. OC 3 Short for Optical Carrier, used to specify the speed of fiber optic networks conforming to the SONET standard. The table shows the speeds for common OC levels. OC = Speed OC-1 = 51.85 Mbps OC-3 = 155.52 Mbps OC-12 = 622.08 Mbps OC-24 = 1.244 Gbps OC-48 = 2.488 Gbps

- 4 -

OC-192 = 9.952 Gbps OC-255 = 13.21 Gbps Typical pricing for dedicated line broadband provisioning is detailed below [2]: T-1 - 1.544 megabits per second (24 DS0 lines) Ave. cost $400.-$650./mo. T-3 - 43.232 megabits per second (28 T1s) Ave. cost $6,000.-$16,000./mo. OC-3 - 155 megabits per second (100 T1s) Ave. cost $20,000.-$45,000./mo. OC-12 - 622 megabits per second (4 OC3s) no estimated price available OC-48 - 2.5 gigabits per seconds (4 OC12s) no estimated price available OC-192 - 9.6 gigabits per second (4 OC48s) no estimated price available Virtual Private Network (VPN) Market Virtual private network is a network that is constructed by using public wires to connect nodes. For example, there are a number of systems that enable you to create networks using the Internet as the medium for transporting data. These systems use encryption and other security mechanisms to ensure that only authorized users can access the network and that the data cannot be intercepted. The market for VPN is addressed as VPN Market. IPsec tunnels and MPLS VPNs IPsec Tunnels IPSec is a suite of protocols that seamlessly integrate security features, such as authentication, integrity, and confidentiality, into IP. For example, you can use Cisco Secure Policy Manager to create IPSec tunnels between devices that support these protocols. IPSec tunnels enable peers to securely transmit information over an un-trusted or public IP network [5]. The Cisco Secure Policy Manager enables tunneling in two ways: a) Policy Enforcement Point-to-Policy Enforcement Point. Policy Enforcement Point-to-Policy Enforcement Point tunnels enable you to securely transmit data between two Policy Enforcement Points across an un-trusted or public network, enabling you to create a virtual private network (VPN) between a main office and a remote office, and b) Policy Distribution Point-to-Policy Enforcement Point. A Policy Distribution Point is the component of Cisco Secure Policy Manager that issues command sets to your Policy Enforcement Points (such as PIX Firewalls or Cisco Secure IDS Sensors.). Policy Distribution Point-to-Policy Enforcement Point tunnels enable you to securely transmit Policy Enforcement Point configuration information to Policy Enforcement Points over an un-trusted or public network [3, 4].

- 5 -

MPLS Virtual Private Networks The IP virtual private network (VPN) feature for Multiprotocol Label Switching (MPLS) allows a Cisco IOS network to deploy scalable IPv4 Layer 3 VPN backbone services. An IP VPN is the foundation companies use for deploying or administering value-added services including applications and data hosting network commerce, and telephony services to business customers. In private local area networks (LANs), IP-based intranets have fundamentally changed the way companies conduct their business. Companies are moving their business applications to their intranets to extend over a wide area network (WAN). Companies are also embracing the needs of their customers, suppliers, and partners by using extranets (an intranet that encompasses multiple businesses). With extranets, companies reduce business process costs by facilitating supply-chain automation, electronic data interchange (EDI), and other forms of network commerce. To take advantage of this business opportunity, service providers must have an IP VPN infrastructure that delivers private network services to businesses over a public infrastructure [6]. 4. High Speed Bandwidth Applications Video Telephony Video telephony (VT) is full-duplex, real-time audio-visual communication between or among end users. The idea of the video telephone, also called the videophone, is about as old as the telephone itself [7]. Video telephony leverages the intelligence of IP telephony to provide advanced features that are not available in traditional IP videoconferencing deployments like call forwarding, call hold, call park, class of service restrictions, ad-hoc conferencing, bandwidth controls, enhanced digit manipulation, and call rerouting. Moreover it is advantageous as enterprises can retain their existing H.320 and H.323 investments and benefit from a user-friendly, more feature-rich environment for large-scale video deployments. The anticipated growth of Video Telephony market segment is projected to rise from $21 million from 2003 to almost $180 million in 2008, achieving a compounded growth rate of almost 53 percent [8].

10-20% of US households are expected to use simultaneous voice-video communication from their homes, with less than 10% of videophones. Life-size video displays will play a small role in corporate communications and may be deployed in 10% of the largest global corporations [9].

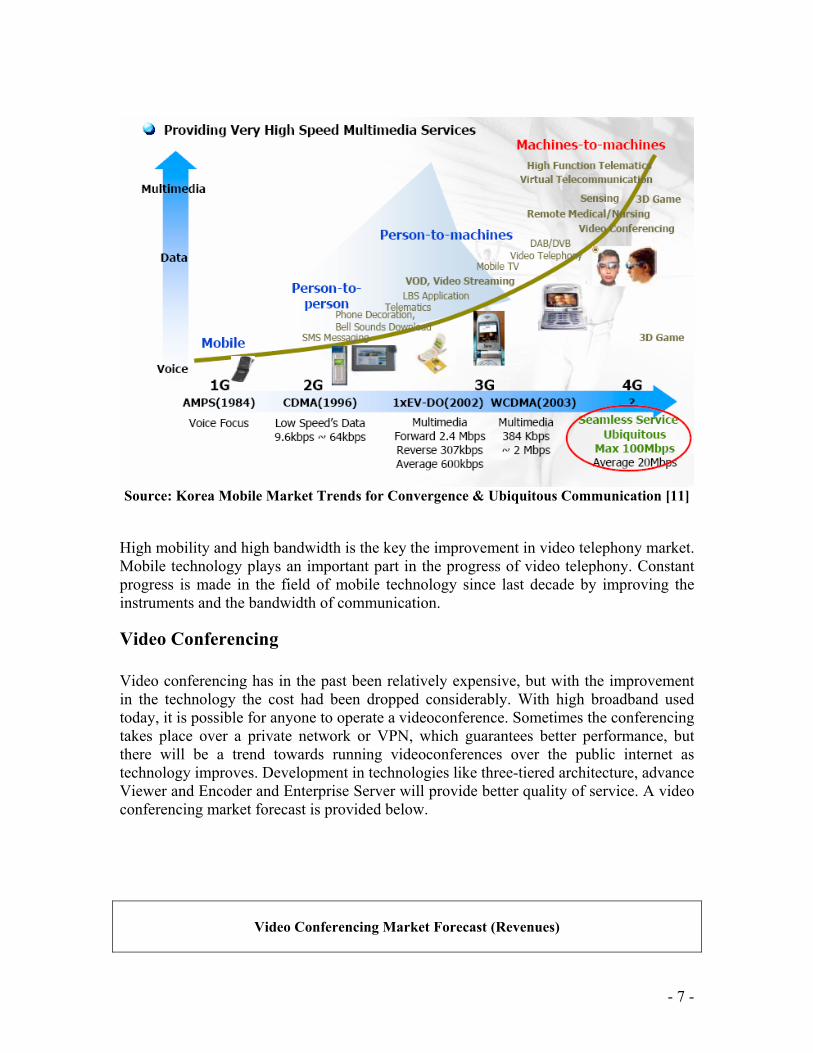

High mobility and high bandwidth is the key the improvement in video telephony market. Mobile technology plays an important part in the progress of video telephony. Constant progress is made in the field of mobile technology since last decade by improving the instruments and the bandwidth of communication.

- 6 -

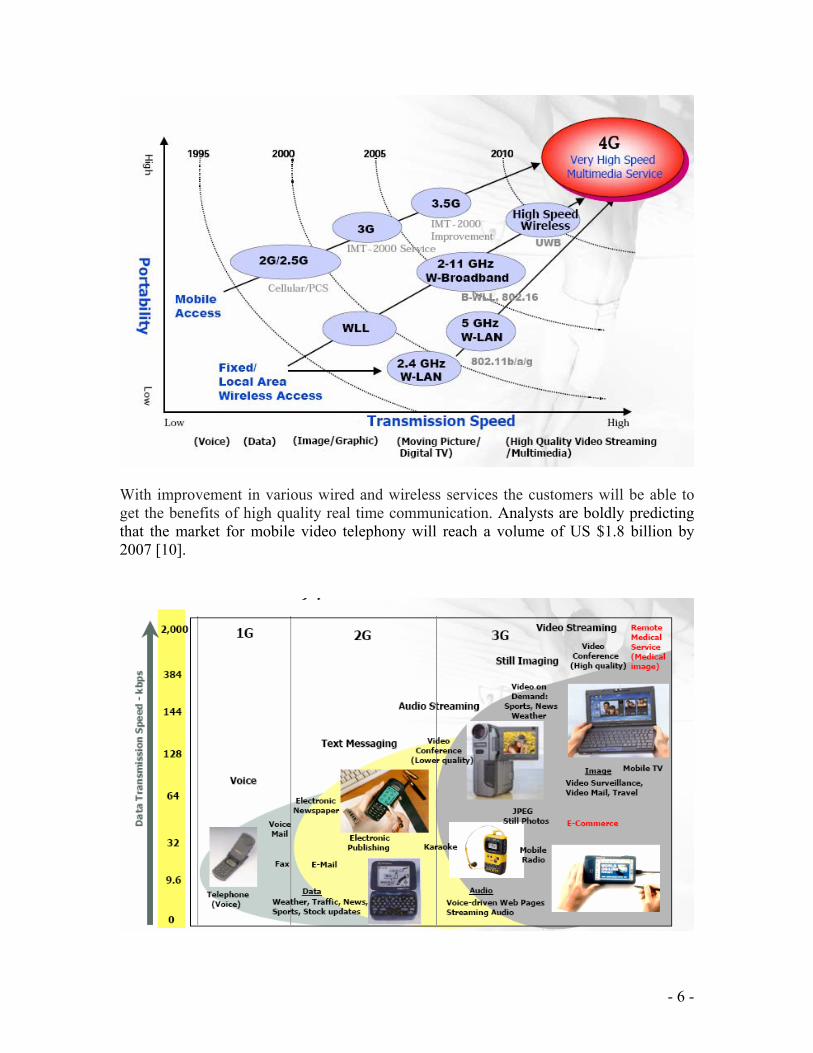

With improvement in various wired and wireless services the customers will be able to get the benefits of high quality real time communication. Analysts are boldly predicting that the market for mobile video telephony will reach a volume of US $1.8 billion by 2007 [10].

- 7 -

Source: Korea Mobile Market Trends for Convergence & Ubiquitous Communication [11]

High mobility and high bandwidth is the key the improvement in video telephony market. Mobile technology plays an important part in the progress of video telephony. Constant progress is made in the field of mobile technology since last decade by improving the instruments and the bandwidth of communication.

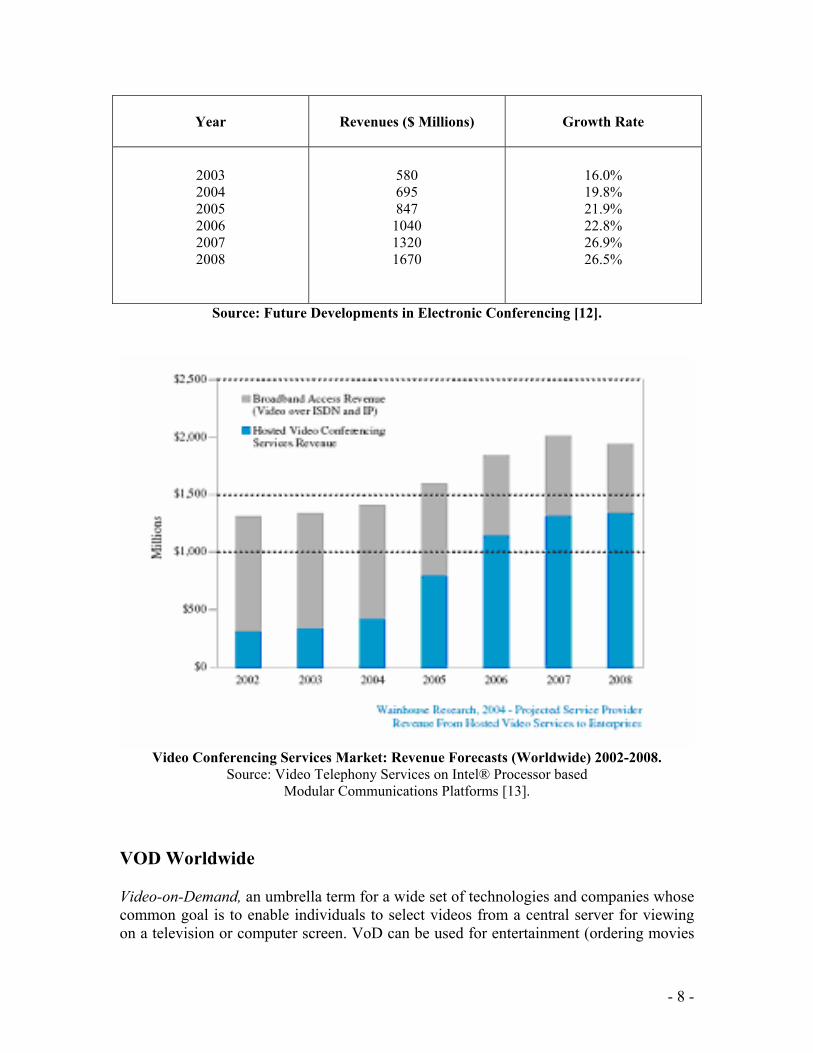

Video Conferencing Video conferencing has in the past been relatively expensive, but with the improvement in the technology the cost had been dropped considerably. With high broadband used today, it is possible for anyone to operate a videoconference. Sometimes the conferencing takes place over a private network or VPN, which guarantees better performance, but there will be a trend towards running videoconferences over the public internet as technology improves. Development in technologies like three-tiered architecture, advance Viewer and Encoder and Enterprise Server will provide better quality of service. A video conferencing market forecast is provided below.

Video Conferencing Market Forecast (Revenues)

- 8 -

Year

Revenues ($ Millions)

Growth Rate

2003 2004 2005 2006 2007 2008

580 695 847

1040 1320 1670

16.0% 19.8% 21.9% 22.8% 26.9% 26.5%

Source: Future Developments in Electronic Conferencing [12].

Video Conferencing Services Market: Revenue Forecasts (Worldwide) 2002-2008.

Source: Video Telephony Services on Intel® Processor based Modular Communications Platforms [13].

VOD Worldwide

Video-on-Demand, an umbrella term for a wide set of technologies and companies whose common goal is to enable individuals to select videos from a central server for viewing on a television or computer screen. VoD can be used for entertainment (ordering movies

- 9 -

transmitted digitally), education (viewing training videos), and videoconferencing (enhancing presentations with video clips) [14]. Although VoD is being used somewhat in all these areas, it is not yet widely implemented. VoD's biggest obstacle is the lack of a network infrastructure that can handle the large amounts of data required by video.

VOD may be categorized as follows: Interactive Video On Demand, Near Video On Demand, Subscription Video on Demand, True Video on Demand and Quasi Video on Demand.

Interactive Video on Demand (IVOD)

Interactive Video on Demand is an extension of VOD (Video on Demand) in which additional functions such as fast forward, fast rewind, and pause are implemented. An IVOD system has three components: (1) the user's "Set-top Box", (2) the network, and the (3) servers with archives of movies (or whatever the server is offering to show.) The clients' set-top boxes are how they communicate with the IVOD server. Many of the IVOD functions are the same kinds of functions you have with your VCR.

Near Video on Demand (NVOD)

A particular movie is advertised to start every 15 minutes or so over a particular channel. You pay your money electronically and select what time and day you want to start watch the movie. A small portion of the movie is sent and stored on your buffer or hard drive, most of the movie is viewed from (off of) the server of the company offering the NVOD service. This contrasts with VOD where typically the whole movie is sent to you ahead of time for storage on your hard drive and for you to view off of your hard drive. You can fast forward, rewind, pause etc. with NVOD.

Subscription Video on Demand (SVOD)

Subscription-based Movies allow users to be able to watch certain movies from a package at any time, or to join on a movie that is already playing. Generally movie packages are scheduled events (VOD & NVOD); SVOD makes it possible for subscribers to have unlimited access to certain movies as part of a package for a fixed monthly fee.

Quasi Video on Demand (QVOD)

Same as Near Video on Demand except that the show only will be sent to the subscribers if a minimum number of subscribers sign up for it.

True Video On Demand (TVOD)

The ideal VOD service where individual users would get immediate responses when interacting with the VOD system. With TVOD, the user can not only order the program, but be able to do any VCR-like commands on the VOD system with the same quick

- 10 -

response time as it is when working a VCR. This increased speed of the response time can significantly increase the cost of operating the VOD system. An alternative is NVOD as it reduces the cost by increasing the waiting time. TVOD is however currently being offered and costs associated with it continue to go down.

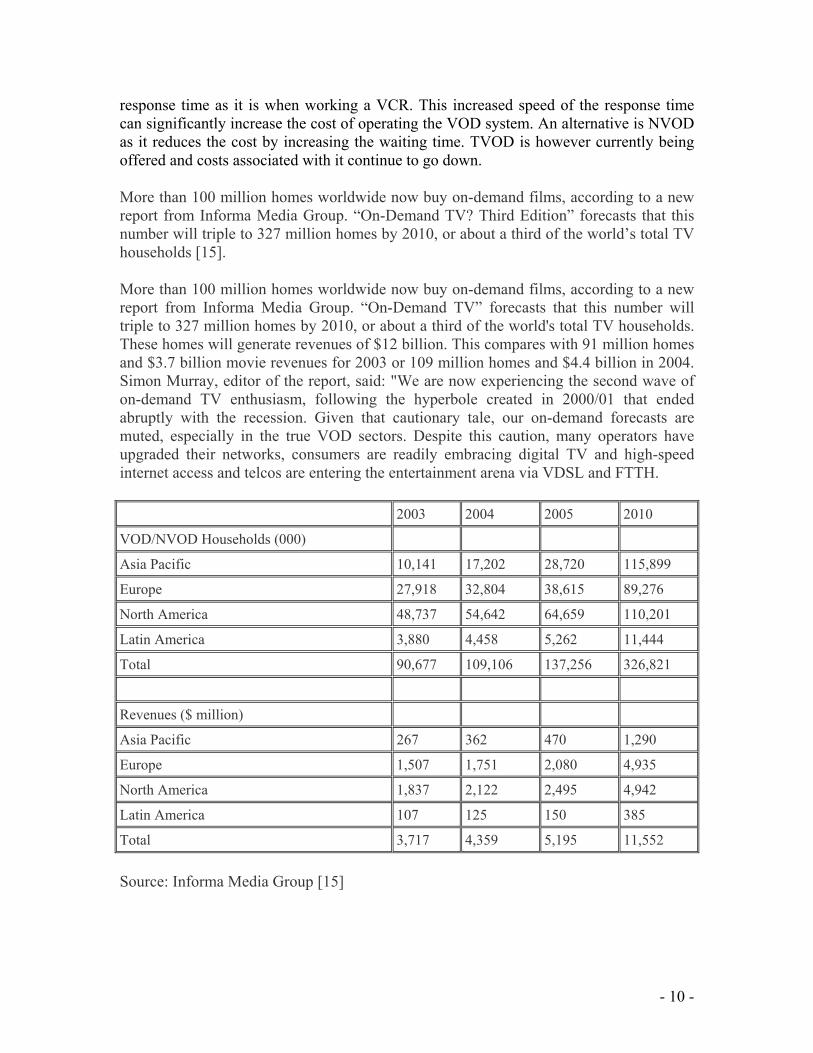

More than 100 million homes worldwide now buy on-demand films, according to a new report from Informa Media Group. “On-Demand TV? Third Edition” forecasts that this number will triple to 327 million homes by 2010, or about a third of the world’s total TV households [15].

More than 100 million homes worldwide now buy on-demand films, according to a new report from Informa Media Group. “On-Demand TV” forecasts that this number will triple to 327 million homes by 2010, or about a third of the world's total TV households. These homes will generate revenues of $12 billion. This compares with 91 million homes and $3.7 billion movie revenues for 2003 or 109 million homes and $4.4 billion in 2004. Simon Murray, editor of the report, said: "We are now experiencing the second wave of on-demand TV enthusiasm, following the hyperbole created in 2000/01 that ended abruptly with the recession. Given that cautionary tale, our on-demand forecasts are muted, especially in the true VOD sectors. Despite this caution, many operators have upgraded their networks, consumers are readily embracing digital TV and high-speed internet access and telcos are entering the entertainment arena via VDSL and FTTH.

2003 2004 2005 2010

VOD/NVOD Households (000)

Asia Pacific 10,141 17,202 28,720 115,899

Europe 27,918 32,804 38,615 89,276

North America 48,737 54,642 64,659 110,201

Latin America 3,880 4,458 5,262 11,444

Total 90,677 109,106 137,256 326,821

Revenues ($ million)

Asia Pacific 267 362 470 1,290

Europe 1,507 1,751 2,080 4,935

North America 1,837 2,122 2,495 4,942

Latin America 107 125 150 385

Total 3,717 4,359 5,195 11,552

Source: Informa Media Group [15]

- 11 -

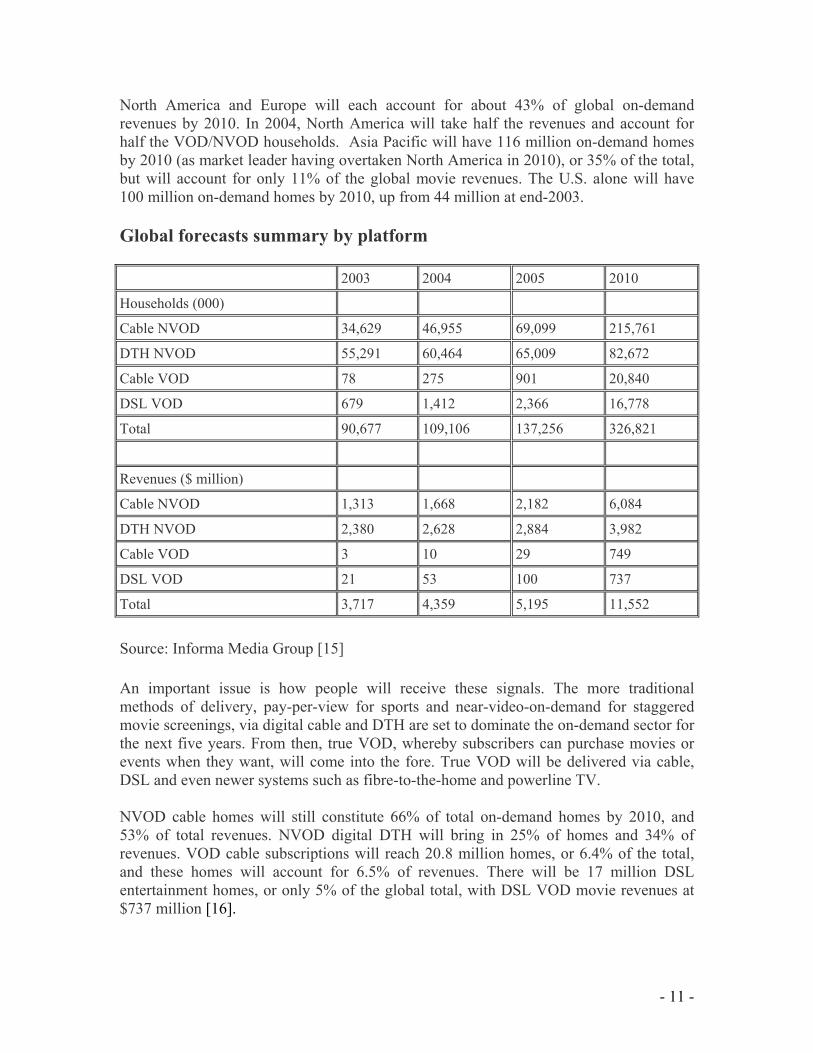

North America and Europe will each account for about 43% of global on-demand revenues by 2010. In 2004, North America will take half the revenues and account for half the VOD/NVOD households. Asia Pacific will have 116 million on-demand homes by 2010 (as market leader having overtaken North America in 2010), or 35% of the total, but will account for only 11% of the global movie revenues. The U.S. alone will have 100 million on-demand homes by 2010, up from 44 million at end-2003.

Global forecasts summary by platform

2003 2004 2005 2010

Households (000)

Cable NVOD 34,629 46,955 69,099 215,761

DTH NVOD 55,291 60,464 65,009 82,672

Cable VOD 78 275 901 20,840

DSL VOD 679 1,412 2,366 16,778

Total 90,677 109,106 137,256 326,821

Revenues ($ million)

Cable NVOD 1,313 1,668 2,182 6,084

DTH NVOD 2,380 2,628 2,884 3,982

Cable VOD 3 10 29 749

DSL VOD 21 53 100 737

Total 3,717 4,359 5,195 11,552

Source: Informa Media Group [15] An important issue is how people will receive these signals. The more traditional methods of delivery, pay-per-view for sports and near-video-on-demand for staggered movie screenings, via digital cable and DTH are set to dominate the on-demand sector for the next five years. From then, true VOD, whereby subscribers can purchase movies or events when they want, will come into the fore. True VOD will be delivered via cable, DSL and even newer systems such as fibre-to-the-home and powerline TV. NVOD cable homes will still constitute 66% of total on-demand homes by 2010, and 53% of total revenues. NVOD digital DTH will bring in 25% of homes and 34% of revenues. VOD cable subscriptions will reach 20.8 million homes, or 6.4% of the total, and these homes will account for 6.5% of revenues. There will be 17 million DSL entertainment homes, or only 5% of the global total, with DSL VOD movie revenues at $737 million [16].

- 12 -

Storage Area Network (SAN) A Storage Area Network (SAN) is a high-speed special-purpose network (or sub network) that interconnects different kinds of data storage devices with associated data servers on behalf of a larger network of users. Typically, a SAN is part of the overall network of computing resources for an enterprise. A SAN is usually clustered in close proximity to other computing resources such as IBM z990 mainframes but may also extend to remote locations for backup and archival storage, using wide area network carrier technologies such as ATM or SONET. SAN Market Size for small-to-midsize business There is an emerging demand for networked storage solutions custom-built to the needs of the Medium Business. This market segment has tremendous purchasing power; the overall SMB (small-to-midsize business) market segment represents 7.8 million companies. iSCSI iSCSI is Internet SCSI (Small Computer System Interface), an Internet Protocol (IP)-based storage networking standard for linking data storage facilities, developed by the Internet Engineering Task Force (IETF). By carrying SCSI commands over IP networks, iSCSI is used to facilitate data transfers over intranets and to manage storage over long distances. The iSCSI protocol is among the key technologies expected to help bring about rapid development of the (SAN) market, by increasing the capabilities and performance of storage data transmission. FC Fibre Channel over IP (FCIP or FC/IP, also known as Fibre Channel tunneling or storage tunneling) is an Internet Protocol (IP)-based storage networking technology developed by the Internet Engineering Task Force (IETF). FCIP mechanisms enable the transmission of Fibre Channel (FC) information by tunneling data between SAN facilities over IP networks; this capacity facilitates data sharing over a geographically distributed enterprise. One of two main approaches to storage data transmission over IP networks, FCIP is among the key technologies expected to help bring about rapid development of the SAN market by increasing the capabilities and performance of storage data transmission. FCIP Versus iSCSI The other method, iSCSI, generates SCSI codes from user requests and encapsulates the data into IP packets for transmission over an Ethernet connection. Intended to link geographically distributed SANs, FCIP can only be used in conjunction with Fibre Channel technology; in comparison, iSCSI can run over existing Ethernet networks. SAN connectivity, through methods such as FCIP and iSCSI, offers benefits over the traditional point-to-point connections of earlier data storage systems, such as higher

- 13 -

performance, availability, and fault-tolerance. A number of vendors, including Cisco, Nortel, and Lucent have introduced FCIP-based products (such as switches and routers). A hybrid technology called Internet Fibre Channel Protocol (iFCP) is an adaptation of FCIP that is used to move Fibre Channel data over IP networks using the iSCSI protocols.

FCIP and iSCSI (Rates) The use of data storage is increasing in various businesses, with time as more advance applications are used, requiring more data storage space. Information growth is so intense, in fact, that spending on data storage is expected to outstrip server spending by 2005. And, according to a study by Merrill Lynch and McKinsey & Company 1, annual growth of data storage capacity will average a startling 76% over the next five years. To optimize data storage IT managers are working on new data storage techniques to get the most out of available resources, For years, adding storage meant purchasing additional servers, tape libraries, and disk enclosures to attach to the server - a costly and inefficient approach that left large amounts of storage capacity and computing power unused. Today, storage area networks (SAN) - high-speed networks that connects multiple storage devices so that they may be accessed on all servers in a local area network (LAN) or wide area network (WAN) - have been proven to reduce management costs as a percentage of overall storage costs.

Some other benefits of SANs are Increased disk utilization, Reduced data center/rack floor space, Improved data availability, Improved LAN/WAN performance, Reduced storage maintenance costs, Improved protection of critical data, Reduced CPU loads on servers to free up more computing power.

The iSCSI (Internet SCSI) protocol extends the cost benefits of SANs by allowing users to create storage networks using existing Ethernet technology, eliminating the need for costly proprietary alternatives such as fibre channel (FC). With iSCSI, expanding storage to keep pace with data growth is as simple and economical as purchasing a disk array or adding drives to an existing disk array.

One-way is to determine total cost of ownership (TCO) for the iSCSI approach and compare it to the two alternatives: a fibre channel SAN or traditional direct-attached storage (DAS).

Finance and IT would estimate TCO for each technology to determine its relative value. To complete the evaluation, IT would itemize the following hardware and software costs to deploy an iSCSI SAN, a fibre channel SAN, and a traditional SCSI DAS solution:

- 14 -

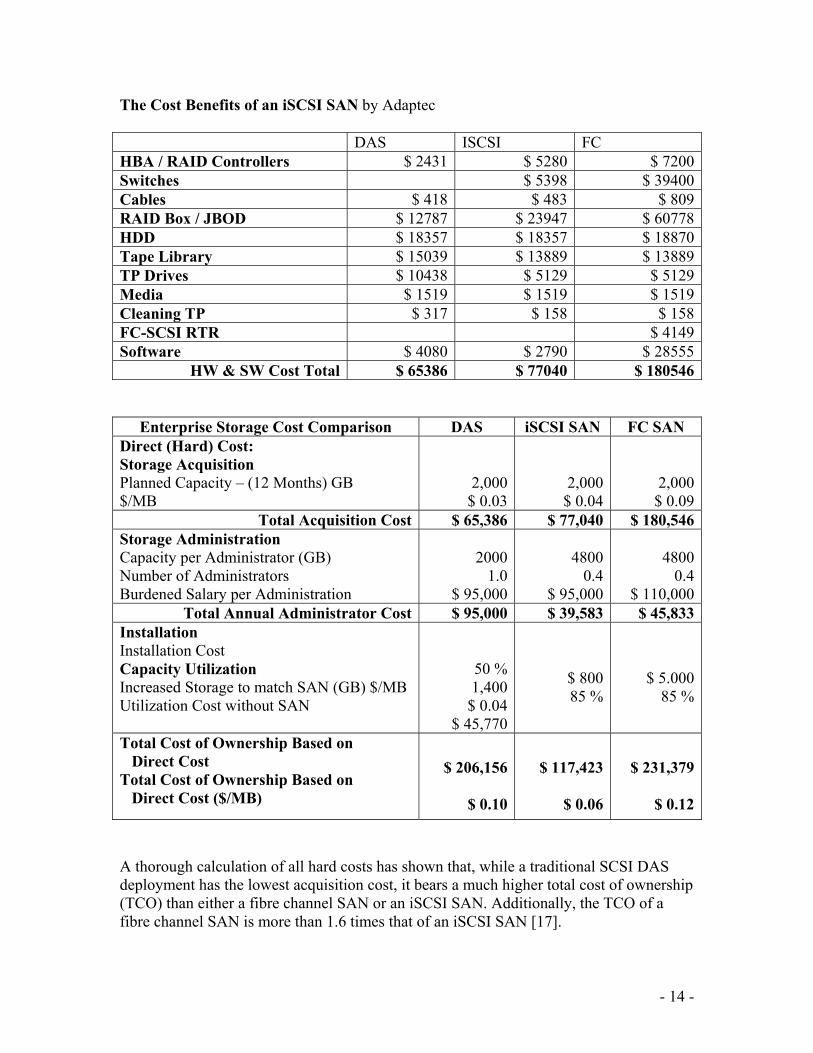

The Cost Benefits of an iSCSI SAN by Adaptec DAS ISCSI FC HBA / RAID Controllers $ 2431 $ 5280 $ 7200Switches $ 5398 $ 39400Cables $ 418 $ 483 $ 809RAID Box / JBOD $ 12787 $ 23947 $ 60778HDD $ 18357 $ 18357 $ 18870Tape Library $ 15039 $ 13889 $ 13889TP Drives $ 10438 $ 5129 $ 5129Media $ 1519 $ 1519 $ 1519Cleaning TP $ 317 $ 158 $ 158FC-SCSI RTR $ 4149Software $ 4080 $ 2790 $ 28555

HW & SW Cost Total $ 65386 $ 77040 $ 180546

Enterprise Storage Cost Comparison DAS iSCSI SAN FC SAN Direct (Hard) Cost: Storage Acquisition Planned Capacity – (12 Months) GB $/MB

2,000$ 0.03

2,000 $ 0.04

2,000$ 0.09

Total Acquisition Cost $ 65,386 $ 77,040 $ 180,546Storage Administration Capacity per Administrator (GB) Number of Administrators Burdened Salary per Administration

20001.0

$ 95,000

4800

0.4 $ 95,000

48000.4

$ 110,000Total Annual Administrator Cost $ 95,000 $ 39,583 $ 45,833

Installation Installation Cost Capacity Utilization Increased Storage to match SAN (GB) $/MB Utilization Cost without SAN

50 %1,400$ 0.04

$ 45,770

$ 800 85 %

$ 5.00085 %

Total Cost of Ownership Based on Direct Cost Total Cost of Ownership Based on Direct Cost ($/MB)

$ 206,156

$ 0.10

$ 117,423

$ 0.06

$ 231,379

$ 0.12

A thorough calculation of all hard costs has shown that, while a traditional SCSI DAS deployment has the lowest acquisition cost, it bears a much higher total cost of ownership (TCO) than either a fibre channel SAN or an iSCSI SAN. Additionally, the TCO of a fibre channel SAN is more than 1.6 times that of an iSCSI SAN [17].

- 15 -

References [1] The Metro Ethernet Forum “Metro Ethernet Network – A Technical Review” 2004 URL: http://www.metroethernetforum.org/PDFs/WhitePapers/metro-ethernet-networks.pdf last accessed June 14th, 2005. [2] Infobahn, Inc. “Research Information” 2004

[3] Cisco Systems Inc. "Learn More About IPSec Tunnels” 2000, URL: http://www.cisco.com/univercd/cc/td/doc/product/ismg/policy/ver22/ipsec/ch01.htm#xtocid256341 last accessed June 15th, 2005.

[4] Jean-Francois Nadeau “Ipsec practical configurations for Linux Freeswan 1.x”09 May 2001 URL: http://jixen.tripod.com last accessed June 20th, 2005. [5] Tom Eastep “IPSEC Tunnels” 2004, URL: http://www.shorewall.net/IPSEC.htm last accessed June 1st, 2005. [6] Cisco IOS Release 12.0(5)T “MPLS Virtual Private Networks”? 03 September 2004, URL: http://www.cisco.com/univercd/cc/td/doc/product/software/ios120/120newft/120t/120t5/vpn.htm last accessed June 1st, 2005.

[7] Tech Target (2005), URL: http://searchenterprisevoice.techtarget.com last accessed June 1, 2005. [8] JB Fowler, Xiangdong Fu, Pradeep Bardia Texas instruments “How to Create IP Videophone Systems” February 2005, URL: www.ti.com/dmedianewsmar05vdpwhtp last accessed June 1, 2005. [9] Giancarlo Prati “National Consortium Interuniversitario for the Rome Telecommunications” 25 January 2002, URL: http://www.isoc.it/tavolarotonda/prati/tsld005.htm last accessed June 1, 2005. [10] Swisscom “The One - Global Communication Services for Carriers, Network and Service Providers” URL: http://www.swisscom.com/FxRes/NR/rdonlyres/C713A700-D298-4931-B417-69E031235322/0/OneWorld_0304_e.pdf last accessed June 1, 2005. [11] SK Telecom “Korea Mobile Market Trend for Convergence & Ubiquitous Communication” 4 March 2004, URL: http://www.itu.int/osg/spu/ni/futuremobile/presentations/sktelecom-presentation.pdf last accessed June 1, 2005. [12] Raymond James “Future Developments in Electronic Conferencing” URL: http://www.ideafocus.com/news&events/Future%20Developments%20in%20Electronic%20Conferencing.pdf last accessed June 1, 2005. [13] Intel Communication Alliance “Video Telephony Services on Intel® Processorbased Modular Communications Platforms” 2004, URL: http://www.intel.com/netcomms/serviceproviders/downloads/30271001.pdf last accessed June 1, 2005.

- 16 -

[14] Newton’s Dictionary, “What is Video on Demand?,” URL: http://www.usfca.edu/fac-staff/morriss/651/tech_projects/VOD/full.html last accessed June 1, 2005. [15] Informa Media Group. “On-Demand TV?” Third Edition [16] Informa Media “On-demand movies taken by 100 million homes”, 8th June, 2004. [17] Adaptec, Inc. “The Cost Benefits of an iSCSI SAN” 2003, URL: http://www.adaptec.com/worldwide/product/markeditorial.html?sess=no&language=English+US&cat=%2FTechnology%2FiSCSI&prodkey=wp_tco_iscsi_san last accessed June 1, 2005. Other References

http://www.itfacts.biz/ http://www.webopedia.com/