Embed Size (px)

Citation preview

Country Report

Bangladesh

December 2007

Economist Intelligence Unit 26 Red Lion Square London WC1R 4HQ United Kingdom

The Economist Intelligence Unit

The Economist Intelligence Unit is a specialist publisher serving companies establishing and managing operations across national borders. For 60 years it has been a source of information on business developments, economic and political trends, government regulations and corporate practice worldwide.

The Economist Intelligence Unit delivers its information in four ways: through its digital portfolio, where the latest analysis is updated daily; through printed subscription products ranging from newsletters to annual reference works; through research reports; and by organising seminars and presentations. The firm is a member of The Economist Group.

London The Economist Intelligence Unit 26 Red Lion Square London WC1R 4HQ United Kingdom Tel: (44.20) 7576 8000 Fax: (44.20) 7576 8500 E-mail: [email protected]

New York The Economist Intelligence Unit The Economist Building 111 West 57th Street New York NY 10019, US Tel: (1.212) 554 0600 Fax: (1.212) 586 0248 E-mail: [email protected]

Hong Kong The Economist Intelligence Unit 60/F, Central Plaza 18 Harbour Road Wanchai Hong Kong Tel: (852) 2585 3888 Fax: (852) 2802 7638 E-mail: [email protected]

Website: www.eiu.com

Electronic delivery This publication can be viewed by subscribing online at www.store.eiu.com.

Reports are also available in various other electronic formats, such as CD-ROM, Lotus Notes, online databases and as direct feeds to corporate intranets. For further information, please contact your nearest Economist Intelligence Unit office.

Copyright © 2007 The Economist Intelligence Unit Limited. All rights reserved. Neither this publication nor any part of it may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without the prior permission of The Economist Intelligence Unit Limited.

All information in this report is verified to the best of the author's and the publisher's ability. However, the Economist Intelligence Unit does not accept responsibility for any loss arising from reliance on it.

ISSN 0269-431X

Symbols for tables �n/a� means not available; ��� means not applicable

Printed and distributed by Patersons Dartford, Questor Trade Park, 151 Avery Way, Dartford, Kent DA1 1JS, UK.

Bangladesh 1

Monthly Report December 2007 www.eiu.com © The Economist Intelligence Unit Limited 2007

Bangladesh

Executive summary 2 Highlights

Outlook for 2008-09 3 Political outlook 4 Economic policy outlook 5 Economic forecast

Monthly review: December 2007 9 The political scene 11 Economic policy 12 Economic performance

Data and charts 14 Annual data and forecast 15 Quarterly data 16 Monthly data 17 Annual trends charts 18 Monthly trends charts

Country snapshot 19 Political structure

Editors: Fung Siu (editor); Danny Richards (consulting editor)

Editorial closing date: November 27th 2007

All queries: Tel: (44.20) 7576 8000 E-mail: [email protected] Next report: To request the latest schedule, e-mail [email protected]

2 Bangladesh

Monthly Report December 2007 www.eiu.com © The Economist Intelligence Unit Limited 2007

Executive summary

Highlights

December 2007

• Preparations are under way for civic and parliamentary elections in 2008, but doubts remain about whether the Election Commission can meet a series of deadlines before the polls are held.

• Emergency rule is expected to continue in the early part of the forecast period.

• Despite a range of electoral reforms, the next election battle will be fought between long-standing rivals, the Awami League and the Bangladesh Nationalist Party (BNP)!the two largest political parties.

• The Economist Intelligence Unit has revised up its forecast for international oil prices. Oil prices (dated Brent Blend) are now expected to average US$78/barrel in 2008 (up from US$69.5 previously).

• In the light of the latest trade data and the devastation caused by Cyclone Sidr, we have revised down our GDP forecast for fiscal year 2007/08 (July-June) to 5.8% (from 6.2% previously).

• Consumer prices are expected to average 8.2% in 2008, before easing to 6.5% in 2009 as international oil prices fall from record highs.

• In 2008-09 the taka is expected to depreciate against the US dollar as inflation remains relatively high in Bangladesh and the trade deficit swells to record levels against a backdrop of persistently high international oil prices.

• The Election Commission remains confident of holding municipal elections in March 2008.

• The current administration has said that it hopes to create more special courts to deal with a raft of corruption cases arising from its anti-graft campaign.

• Political reform talks between the Election Commission and a faction of the BNP were postponed in November.

• Comments from Ali Ahsan Mohammad Mojaheed, the secretary-general of Jamaat-e-Islami, to the effect that there are no war criminals in the country, have triggered a national outcry.

• The caretaker government continues to ignore recommendations from multi-lateral lenders and has maintained the subsidy on fuel. Bangladesh Bank (the central bank) left key interest rates unchanged in November.

• The annual inflation rate fell to 9.6% in September (latest available data) from an eight-year high of 10.1% in August.

• Falling export receipts and a rising import bill pushed the current-account balance into deficit in July-August.

Outlook for 2008-09

Monthly review

Bangladesh 3

Monthly Report December 2007 www.eiu.com © The Economist Intelligence Unit Limited 2007

Outlook for 2008-09 Political outlook

The political scene will remain unsettled for much of the forecast period. Preparations for the next parliamentary election are under way, overseen by the Election Commission and the military. The commission faces a busy timetable in 2008: it hopes to hold civic elections in five cities by March, and to finalise the electoral register in July before setting a date for the parliamentary poll, probably in October. The immediate task for the Election Commission is to ensure that the electoral register is ready for all five city corporation polls by January. The logistics of holding a parliamentary election in October could be complicated by inclement weather. This year, heavier than normal monsoon rains killed hundreds of people and displaced 10m during July-September, while in November thousands more were killed by Cyclone Sidr. Bangladesh is vulnerable to cyclones, which occur during March-May and September-December. A repeat of such weather patterns in 2008 could force millions of voters to seek temporary accommodation, making it difficult for the Election Commission to maintain accurate records.

It is not clear whether the government will lift the state of emergency before the civic polls, but the Economist Intelligence Unit expects emergency rule to continue until the parliamentary election. This is primarily because of the caretaker government"s determination to implement sweeping reforms to the electoral process before the poll. The government is currently drafting a pro-posal for amendments to the existing city corporation and municipality laws to bar the same person from becoming a representative in parliament as well as on a local government body. It has already taken steps to ban politicians convicted of a criminal offence from taking part in the forthcoming parlia-mentary poll. The next task is to persuade the main political parties to hold leadership elections!for the first time for decades!and to introduce a new electoral register. However, the government"s reluctance to lift the state of emergency, and the growing influence of the army (particularly in roles usually reserved for civilians), will heighten fears of a return to full military rule. Besides maintaining law and order, military officials are also responsible for vital administrative tasks, such as the preparation of voter identity cards.

Once preparations for the next election and the associated electoral reforms have been completed, the caretaker government will be able to claim that is has reinforced the electoral process. What it will not be able to do, however, is to move the country away from a two-party political system. Political opinion is so strongly polarised in Bangladesh that the parliamentary contest will again pit the Awami League against the Bangladesh Nationalist Party. Mohammad Yunus, a Nobel peace prize winner and the founder of a microcredit provider, Grameen Bank, tried to offer a credible alternative to the two main political parties by forming his own party in February 2007. However, citing the lack of a support base for the new party, he abandoned his plan in April. The lifting of a ban on indoor political meetings is unlikely to tempt Professor Yunus back

Domestic politics

4 Bangladesh

Monthly Report December 2007 www.eiu.com © The Economist Intelligence Unit Limited 2007

into politics, partly because of his reluctance to make the compromises required in order to obtain the necessary support from the army.

In focus

Caretaker governments in Bangladesh

The current constitution provides for a unique arrangement for preparing parlia-mentary elections. The outgoing government hands over power to a caretaker government made up of non-partisan "advisers", whose mandate is to make preparations for the poll. This transfer of power occurred in October 2006, but was marred by controversy after the president, Iajuddin Ahmed, appointed himself as chief adviser (head of the caretaker government). Following weeks of violent street protests and persistent concerns about the ability of the caretaker government to hold a free and fair legislative poll, in January 2007 Iajuddin Ahmed resigned as chief adviser, cancelled the election and declared a state of emergency. A new interim administration, with Fakhruddin Ahmed as chief adviser, was appointed the next day and continues to govern. re

Relations with India are set to improve in the coming months, following a series of meetings between high-ranking Indian officials and members of the Bangladeshi caretaker government. Despite India"s construction of a fence along its 2,500-mile border with Bangladesh to keep out illegal migrants, India seems keen to strengthen economic ties with its smaller neighbour. The Indian government is currently reviewing its policy on foreign direct investment (FDI) from Bangladesh with a view to lifting the current restrictions. In an attempt to raise awareness of products manufactured in Bangladesh, the Federation of Indian Chambers of Commerce and Industry plans to hold a "Made in Bangladesh" exhibition in the Indian capital, New Delhi, in March 2008.

Economic policy outlook

Fiscal policy will remain expansionary over the forecast period. Liberalisation in the banking sector is expected to continue in 2008-09, although progress is likely to be slow. Of the four nationalised commercial banks, negotiations on the sale of Rupali Bank!which began in 2006!have yet to be concluded between Prince Bandar of Saudi Arabia and the Bangladeshi caretaker government. One priority for the current administration and future govern-ments will be to find ways to boost the electricity supply. Besides plans to increase the capacity of existing generating plants, the caretaker government also hopes to lay the groundwork for the construction of a nuclear power station. Bangladesh Bank (BB, the central bank) is expected to maintain an accommodative monetary policy stance during the early part of the forecast period, having pledged in September not to raise interest rates in the near term despite persistent inflationary pressures and strong credit growth.

Bangladesh will continue to post a budget deficit in the forecast period as revenue expansion fails to keep pace with growth in spending. Like the pre-vious administration, the interim government faces a difficult task in achieving its revenue target, owing to the narrow nature of the tax base and low rates of

Fiscal policy

International relations

Policy trends

Bangladesh 5

Monthly Report December 2007 www.eiu.com © The Economist Intelligence Unit Limited 2007

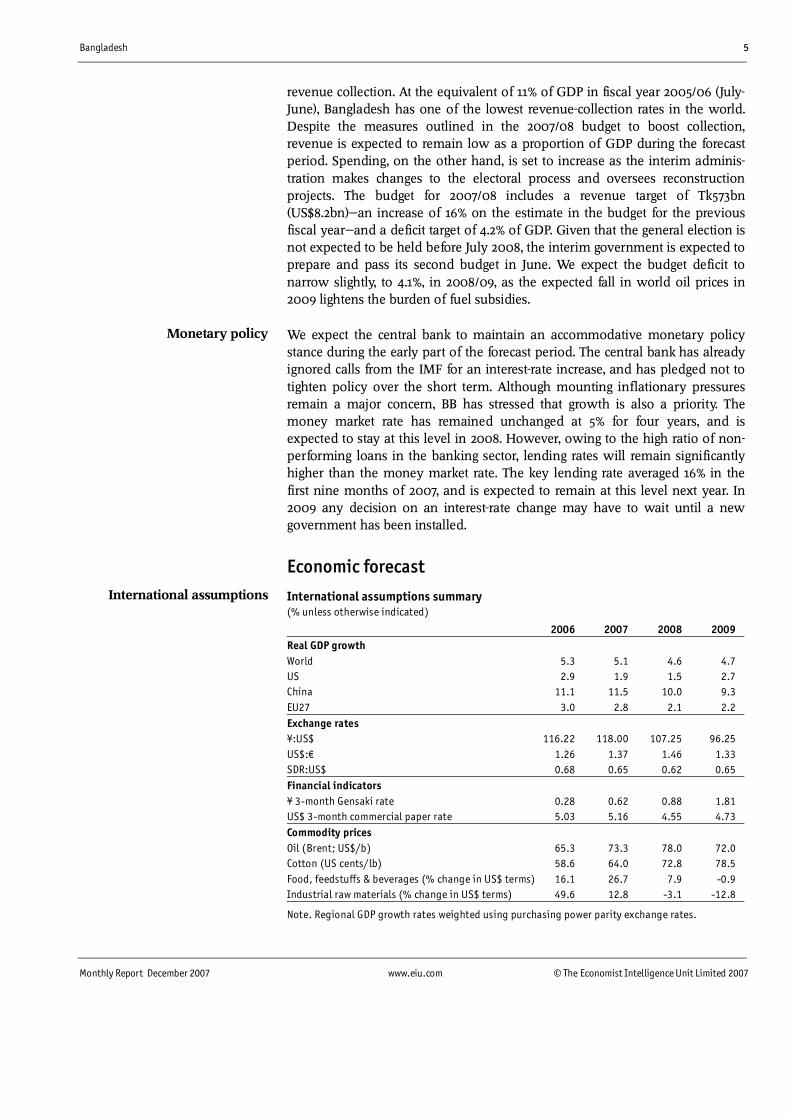

revenue collection. At the equivalent of 11% of GDP in fiscal year 2005/06 (July-June), Bangladesh has one of the lowest revenue-collection rates in the world. Despite the measures outlined in the 2007/08 budget to boost collection, revenue is expected to remain low as a proportion of GDP during the forecast period. Spending, on the other hand, is set to increase as the interim adminis-tration makes changes to the electoral process and oversees reconstruction projects. The budget for 2007/08 includes a revenue target of Tk573bn (US$8.2bn)!an increase of 16% on the estimate in the budget for the previous fiscal year!and a deficit target of 4.2% of GDP. Given that the general election is not expected to be held before July 2008, the interim government is expected to prepare and pass its second budget in June. We expect the budget deficit to narrow slightly, to 4.1%, in 2008/09, as the expected fall in world oil prices in 2009 lightens the burden of fuel subsidies.

We expect the central bank to maintain an accommodative monetary policy stance during the early part of the forecast period. The central bank has already ignored calls from the IMF for an interest-rate increase, and has pledged not to tighten policy over the short term. Although mounting inflationary pressures remain a major concern, BB has stressed that growth is also a priority. The money market rate has remained unchanged at 5% for four years, and is expected to stay at this level in 2008. However, owing to the high ratio of non-performing loans in the banking sector, lending rates will remain significantly higher than the money market rate. The key lending rate averaged 16% in the first nine months of 2007, and is expected to remain at this level next year. In 2009 any decision on an interest-rate change may have to wait until a new government has been installed.

Economic forecast

International assumptions summary (% unless otherwise indicated)

2006 2007 2008 2009

Real GDP growth World 5.3 5.1 4.6 4.7

US 2.9 1.9 1.5 2.7

China 11.1 11.5 10.0 9.3

EU27 3.0 2.8 2.1 2.2

Exchange rates ¥:US$ 116.22 118.00 107.25 96.25

US$:� 1.26 1.37 1.46 1.33

SDR:US$ 0.68 0.65 0.62 0.65

Financial indicators ¥ 3-month Gensaki rate 0.28 0.62 0.88 1.81

US$ 3-month commercial paper rate 5.03 5.16 4.55 4.73

Commodity prices Oil (Brent; US$/b) 65.3 73.3 78.0 72.0

Cotton (US cents/lb) 58.6 64.0 72.8 78.5

Food, feedstuffs & beverages (% change in US$ terms) 16.1 26.7 7.9 -0.9

Industrial raw materials (% change in US$ terms) 49.6 12.8 -3.1 -12.8

Note. Regional GDP growth rates weighted using purchasing power parity exchange rates.

International assumptions

Monetary policy

6 Bangladesh

Monthly Report December 2007 www.eiu.com © The Economist Intelligence Unit Limited 2007

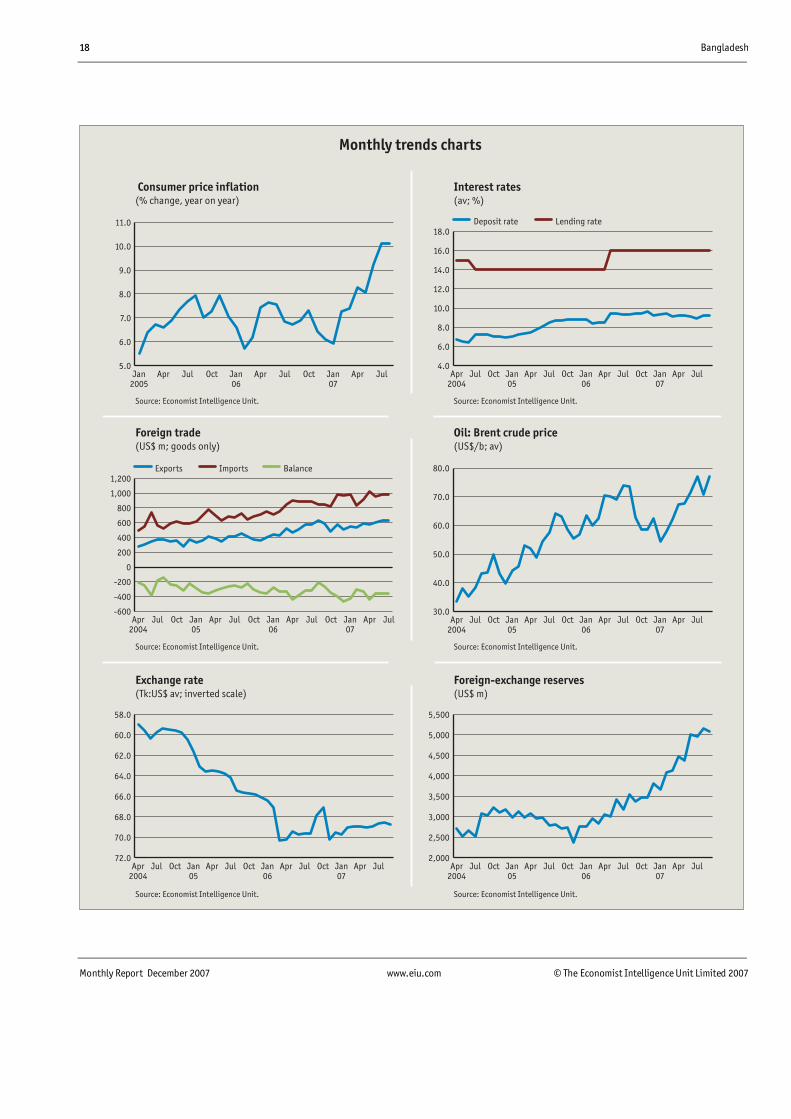

Bangladesh"s external environment is likely to become slightly less favourable in 2008 as economic growth slows in the US and the euro area. Real GDP growth in the US, which absorbs around 25% of Bangladeshi exports, is forecast to slow to 1.5% next year, down from an estimated 1.9% in 2007. Economic growth in the euro area (the destination of more than 30% of Bangladeshi exports) is also forecast to lose momentum, to a more limited extent, slowing from an estimated 2.6% in 2007 to 1.9% in 2008. The external environment is expected to improve slightly in 2009 as economic growth in the US picks up to 2.7%, but growth in the euro zone is forecast to remain sluggish. In the light of the continued tightness in the oil market and a potentially worse geopolitical risk outlook, we have raised our forecast for oil prices in 2008. We now expect crude oil prices (dated Brent Blend) to average US$78/barrel, representing a 6% increase on 2007. Owing to the fact that Bangladesh imports nearly all of the crude petroleum that it requires, high world oil prices will have a detrimental effect on Bangladesh"s balance of trade and are expected to contribute to record trade deficits in 2008 and 2009.

In view of the latest trade data and the damage caused to the fishing industry along the south-western coast by Cyclone Sidr in November, we have revised down our GDP forecast for 2007/08 and 2008/09. We now expect real GDP growth to slow to 5.8% in 2007/08 (6.2% previously) from 6.5% in 2006/07, as the agricultural sector struggles to overcome the devastating effects of the recent floods and cyclone. Assuming normal rainfall in 2008/09, a strong recovery in the agricultural sector should boost real GDP growth to 6.2% in that year.

Record levels of remittance inflows are expected to spur consumer spending in 2007/08 and 2008/09, and will help to prop up the balance of payments. The main near-term risk to economic growth is inflation, which peaked at an eight-year high in August 2007. The fear is that high inflation could entrench itself, particularly since the central bank (unlike its counterparts in the region) has not tightened monetary policy and is unlikely to do so in the near future. There are also signs that domestic and foreign investment have weakened in recent months. Domestic firms have been reluctant to expand capacity, with many wary of attracting the attentions of the Anti-Corruption Commission, which appears determined to investigate all cases of unexplained wealth. This means that, unlike in the past, investments are being scrutinised by the commission.

The composition of growth in 2007/08 and 2008/09 will be similar to that in 2006/07, as record inflows of workers" remittances underpin activity in the services sector, and manufacturing industry continues to make a strong contribution. Rates of growth in the agricultural sector will again lag behind those in manufacturing and services in 2007/08, as the sector strives to overcome the devastation caused by the floods and Cyclone Sidr, which destroyed crops and left thousands dead in the second half of 2007.

Upward price pressures!particularly those resulting from rising food costs!are expected to persist throughout the forecast period. Although the caretaker government has tried to curb increases in imported food prices, the damage caused to crops by the floods in July-August and the cyclone in November is expected to lead to a spike in overall food prices in the short term. A survey of

Inflation

Economic growth

Bangladesh 7

Monthly Report December 2007 www.eiu.com © The Economist Intelligence Unit Limited 2007

essential food items conducted by the Trading Corporation of Bangladesh, a department of the Ministry of Commerce, revealed year-on-year price increases of up to 80% in September. Food prices will continue to be inflated by the hoarding of goods by local food merchants and by the rising cost of imports from India, which is a major supplier of food to Bangladesh via both formal and informal routes. We expect consumer price inflation in 2008 to average 8.2%. Food price inflation should ease in 2009, assuming that harvests return to normal, and consumer price inflation is thus forecast to moderate slightly, to 6.5%, in that year.

We expect the floating exchange-rate system to be kept in place in 2008-09. The central bank adopted a floating exchange-rate system in 2003. Owing to the vigilance of BB, erratic movements in the taka have been prevented. The taka depreciated gradually against the US dollar in 2003-06, but owing to record levels of remittances and the weakness of the dollar the taka is set to show no overall change in value in 2007. However, this stability is not expected to continue over the forecast period, when we expect the taka to depreciate slightly against the US dollar. The taka is forecast to average Tk69.4:US$1 in 2008 and Tk71:US$1 in 2009, as inflation remains relatively high in Bangladesh and as the trade deficit widens to record levels against a backdrop of persistently high international oil prices.

In the light of the latest trade data and the upward revision to our forecast for international oil prices, we now expect a more pronounced deterioration in Bangladesh"s merchandise trade balance (fob-fob basis) in 2008-09. The trade deficit is now set to widen in 2008 to US$5.6bn (US$4.1bn previously), from an estimated US$4.3bn in 2007, and to rise to US$5.8bn in 2009. The expected widening is largely attributable to a growing import bill for oil, as volumes remain large and international prices stay high. Imports are forecast to continue to grow in both volume and value terms in 2008 as demand for petroleum products and some industrial raw materials remains strong. The absolute value of imports will continue to exceed that of exports by a wide margin throughout the forecast period. Nevertheless, merchandise export growth will be helped by a gradual decline in the value of the taka against the US dollar. Owing to record inflows of workers" remittances, the current-account will post small surpluses in 2008 and in 2009.

External sector

Exchange rates

8 Bangladesh

Monthly Report December 2007 www.eiu.com © The Economist Intelligence Unit Limited 2007

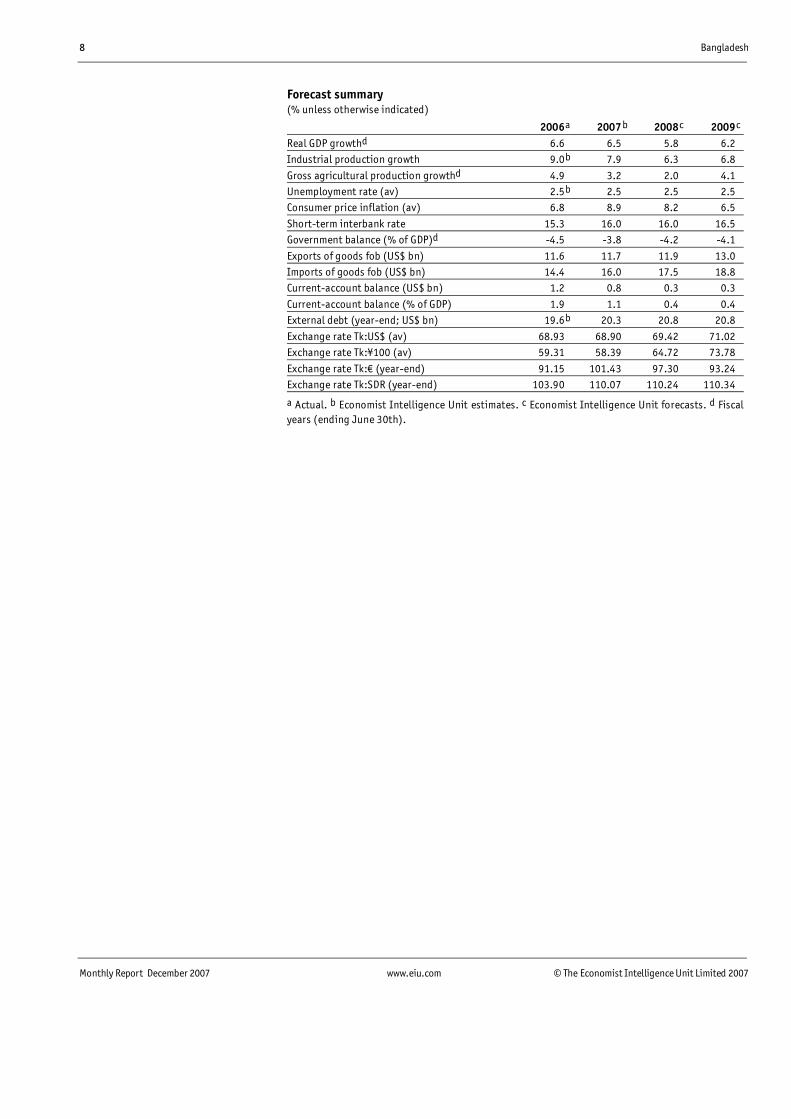

Forecast summary (% unless otherwise indicated)

2006 a 2007 b 2008c 2009c

Real GDP growthd 6.6 6.5 5.8 6.2

Industrial production growth 9.0 b 7.9 6.3 6.8

Gross agricultural production growthd 4.9 3.2 2.0 4.1

Unemployment rate (av) 2.5 b 2.5 2.5 2.5

Consumer price inflation (av) 6.8 8.9 8.2 6.5

Short-term interbank rate 15.3 16.0 16.0 16.5

Government balance (% of GDP)d -4.5 -3.8 -4.2 -4.1

Exports of goods fob (US$ bn) 11.6 11.7 11.9 13.0

Imports of goods fob (US$ bn) 14.4 16.0 17.5 18.8

Current-account balance (US$ bn) 1.2 0.8 0.3 0.3

Current-account balance (% of GDP) 1.9 1.1 0.4 0.4

External debt (year-end; US$ bn) 19.6 b 20.3 20.8 20.8

Exchange rate Tk:US$ (av) 68.93 68.90 69.42 71.02

Exchange rate Tk:¥100 (av) 59.31 58.39 64.72 73.78

Exchange rate Tk:� (year-end) 91.15 101.43 97.30 93.24

Exchange rate Tk:SDR (year-end) 103.90 110.07 110.24 110.34

a Actual. b Economist Intelligence Unit estimates. c Economist Intelligence Unit forecasts. d Fiscal years (ending June 30th).

Bangladesh 9

Monthly Report December 2007 www.eiu.com © The Economist Intelligence Unit Limited 2007

Monthly review: December 2007

The political scene

Bangladesh has been without an elected government for the past 12 months. The military-backed caretaker government has reiterated its commitment to hold a parliamentary election before the end of 2008. The head of the caretaker government, Fakhruddin Ahmed, said in mid-November that the parliamentary poll might even be held sooner than the date for the contest specified in the roadmap produced by the Election Commission, namely the final months of 2008, but he declined to give a specific date. It appears that the commission is on track with the commitments set out in the election roadmap announced in July 2007. Municipal elections are scheduled for March 2008. Progress has been made on creating a new voters� list (complete with photographs) of some 80.5m names. In an important step, the judiciary has been freed from executive control. The move is in line with a Supreme Court decision made at the start of the current decade, a ruling that was ignored by subsequent governments. However, it remains to be seen to what extent this will free the courts from political influence. The civil administration is trying to rebuild other democratic institutions and to modernise the civil service.

As ever, there is speculation over whether the military, or the administration that it backs, will stick to the election timetable. Political gatherings remain restricted. The state of emergency has remained firmly in place, and the caretaker government has given no indication of when it will be lifted. Citizen�s rights are severely curtailed. Meanwhile, A T M Shamsul Huda, the chief election commissioner, said in early November that the commission would ask the government to agree to a partial lifting of the state of emergency two months ahead of the municipal elections. Mr Huda apparently envisages a situation in which emergency rule will be relaxed in the areas where municipal elections are due, but not necessarily in other parts of the country. These elections to the city corporations will be the first real political test for the current administration. If they go according to plan, this will send a strong signal to voters and the international community that the interim government is committed to the democratic process and does not intend to hold on to power indefinitely.

The administration�s legitimacy continues to depend largely on its anti-corruption drive. Two former prime ministers, Khaleda Zia of the Bangladesh Nationalist Party (BNP) and Sheikh Hasina Wajed of the Awami League (AL), are still in jail awaiting trial. As of November 14th, a total of 15 corruption cases had been heard, while another 34 were still before the courts, according to the Anti-Corruption Commission. The sentences meted out to politicians, businessmen and gangsters so far range from three to 20 years" imprisonment. Senior commission officials have said that 200 high-profile people are being prosecuted. Five special courts are not enough to deal with the flood of cases, and more are in the process of being created.

Preparations are under way to hold elections by end-2008

The anti-corruption drive continues unabated

10 Bangladesh

Monthly Report December 2007 www.eiu.com © The Economist Intelligence Unit Limited 2007

In early November the president of the World Bank, Robert Zoellick, in the course of a �listening tour� of South Asia, came to monitor progress in a country where until recently dishonesty in public life was so prevalent that Bangladesh regularly topped global corruption league tables. Mr Zoellick called for a transparent battle against corruption, consistent with the rule of law.

Political parties in Bangladesh are in a shambles. The BNP has split. One faction, the so-called reformers, are led by Saifur Rahman, a former finance minister. The other is led by Khandaker Delwar Hossain, a loyal supporter of Mrs Zia, and has her stamp of approval: Mrs Zia has stated that he is the acting leader of the BNP. Both groups claim that they represent the real BNP. In early November the Election Commission took the controversial decision to invite the �reformer� faction to talks that it has been holding with other political parties in preparation for the parliamentary poll. However, owing to a legal challenge filed by Zia loyalists, the commission then decided to postpone the meeting until the high court had ruled on which of the two factions should be treated as the real BNP. The meeting, had it gone ahead, would have meant that a significant share of the electorate (namely those supporting Mrs Zia) would not have been represented at the talks. The media have questioned the Electoral Commission"s independence. If the past is any guide, a loss of credibility on the part of the commission could be disastrous. The body had a reputation of being partisan until the current administration took over at the start of this year, and was often accused of helping the previous BNP-led coalition government to rig the election scheduled to take place in January 2007 (and subsequently cancelled).

It is not clear what the political scene will look like in the future without "the two begums" (ladies of rank), Mrs Zia and Sheikh Hasina, both of whom still command considerable popular support. The reality is that, apart from Mrs Zia, Sheikh Hasina and a former military ruler, Hossain Mohammad Ershad, there are no other politicians in Bangladesh capable of garnering enough popular support to win a national election.

One fear in Bangladesh is that Islamists!both the fundamentalist fringe and more moderate elements!could fill the political vacuum that the suspension of democracy has created. Events following the publication of an allegedly blasphemous cartoon by the Prothom Alo, the country�s largest-selling Bengali-language daily newspaper, in September seemed to confirm this. Motiur Rahman, the paper"s editor, had to apologise to religious leaders for publishing the cartoon. Islamic groups burned copies of the paper for weeks, and the authorities jailed the cartoonist.

But a more recent development suggests that Islamic forces might come under severe pressure in the near future. In late October Ali Ahsan Mohammad Mojaheed, the secretary-general of an Islamist political party, Jamaat-e-Islami, said that there were no war criminals in the country. Mr Mojaheed�s remark triggered a national outcry. The active role that Jamaat and its student arm, Islami Chhatra Shangha, played in the war of independence in 1971 and the atrocities that some of their members committed against Bangladeshis is well documented. A National People"s Enquiry Commission was formed in 1993 and

The Election Commission sparks controversy

Jamaat comes under pressure

Bangladesh 11

Monthly Report December 2007 www.eiu.com © The Economist Intelligence Unit Limited 2007

was charged with the task of investigating the activities of suspected war criminals and collaborators. Many of the individuals on the commission"s list at that time were active members of Jamaat; they included Matiur Rahman Nizami, the current head of the party.

Thirty-six years after independence, Bangladesh�s society is still deeply divided along the lines of supporters of the independence movement and those who opposed it. Those who were found guilty of war crimes by the commission were never tried. The leader of the current caretaker government said in mid-November this year that steps would not be taken to try those accused of war crimes during the war, as this would detract from the administration"s primary aim of organising elections. The AL has already said that it wants Jamaat to be banned. Others want all religious-based parties banned. Although the caretaker government denies it, the issue presents an extraordinary opportunity. Commentators believe that the current government"s legacy would be impreg-nable against criticism in other areas if, under its watch, impunity were to come to an end not only for the corrupt but also for those who played an active role in the atrocities committed in 1971.

Economic policy

The negative short-term consequences of the government"s anti-corruption drive are becoming more apparent. Foreign and domestic investment has stalled. Garment exports have plummeted. In early November Bangladesh Bank (the central bank) sold US$80m of its foreign reserves to finance oil imports. Strong remittances are helping to underpin private consumption, but inflation remains high. The central bank has ruled out both a tightening of monetary policy and a rise in fuel prices, which the government subsidises, and has said that the country might have to consider the issue of sovereign bonds.

The nature of economic policymaking has changed significantly under the current administration. Judged by its actions during its first ten months of office, some distinct characteristics have emerged. One is an increasingly populist approach to economic policy. Equipped with a tenuous constitution, and in the absence of a popular mandate, the caretaker government has, with a few exceptions!the closure of jute mills, for example!shied away from measures that could prove unpopular with the public. The refusal to tighten monetary policy and raise fuel prices, despite stubbornly high inflation, are the most prominent examples of this tendency.

Another is the outspoken rejection of policy recommendations by the IMF and the World Bank. A few months ago the caretaker government decided not to enter into a new agreement with the Fund. The popular feeling is that economic policy should be made in the capital, Dhaka, and should not be restricted by conditions laid down by multilateral lenders, which are not popular in Bangladesh. Open criticism of such lenders is a popular pastime among educated Bangladeshis. Even the country�s foremost economist, Mohammad Yunus, a Nobel peace prize winner, had few kind words for the World Bank following a meeting with Mr Zoellick in early November. Mr Yunus told reporters that the Bank should increase sharply the proportion of its lending

The caretaker government adopts a populist stance

12 Bangladesh

Monthly Report December 2007 www.eiu.com © The Economist Intelligence Unit Limited 2007

devoted to microcredit programmes. He also called for major reforms to the Bank, whose country offices, he said, operated like post offices waiting for directives from headquarters and should be autonomous.

A second characteristic of current government policy is economic nationalism. In October the Board of Investment imposed a five-year limit on the duration of work permits for foreigners, saying that the country needed more jobs for locals. The board"s executive chairman, Mohammad Mohsin, said that heavily overpopulated Bangladesh could not afford to accommodate foreign workers for very long. Bangladesh has at least 100,000 foreigners working in industry and commerce, although officials say that only 10,000 of them have legal work permits. The decision to limit the duration of permits was partly prompted by the conclusions of a taskforce that found that some foreign workers in Bangladesh concealed their full income in order to evade tax. At the same time, there has been no recent news regarding the big foreign investment projects proposed for the natural-resources sector. It is not clear whether the current administration is able and willing to sign these deals or to create a policy framework that would make it easier for an elected government to do so in the future.

Despite local antipathy towards donor agencies, aid is flooding in. Soon after the declaration of the state of emergency on January 11th this year, donors saw a window of opportunity to speed up the process of turning impoverished Bangladesh into a middle-income country. In early November the Asian Development Bank approved a US$150m loan to support a good-governance programme. Much of the money will go towards strengthening the Anti-Corruption Commission. By late November more than US$500m in aid, including US$250m from the World Bank and US$100m from Saudi Arabia, had been pledged to help those affected by Cyclone Sidr, which devastated the south-west coast of the country.

Economic performance

The central bank said in mid-November that it expected economic growth to slow from 6.5% in fiscal year 2006/07 (July-June) to around 6% in 2007/08. The bank said that economic growth would be held back by the devastating floods in July-September and the cyclone in November, both 0f which destroyed huge quantities of crops and damaged infrastructure. It said that inflation would average 7% in 2007/08.

The external environment has also deteriorated. If the current trend of falling garment exports, which account for about three-quarters of total exports, continues, the country will find it difficult to finance its imports. In July garment exports fell by 23.6% year on year, to US$345m. The value of knitwear exports also declined at a similar pace in that month. Provisional data indicate a stronger performance for garment exports in September. Industry lobby groups maintain that the recovery seen in September will continue. The total value of exports fell by 11.5% year on year in the first two months of the current fiscal year. The main factors behind the sharp decline in exports are continuing political uncertainty, labour unrest and poor work standards. All of these factors

Economic growth is set to slow

Bangladesh 13

Monthly Report December 2007 www.eiu.com © The Economist Intelligence Unit Limited 2007

are likely to have led buyers to review the sourcing of goods from Bangladesh. Import payments, on the other hand, increased by 12.2% year on year to US$2.7bn in July-August, according to the central bank.

Rapidly rising prices still present the biggest downside risk to the economy. Annual consumer price inflation slowed to 9.6% in September from an eight-year high of 10.1% in August, according to central bank data. But inflation remained well above the bank�s target range of 6.5-7% for the current fiscal year. Inflation was driven by an 11.1% year-on-year spike in food prices, while prices for non-food items rose by 7.4% year on year. The central bank believes that inflation could slow to 6-6.5% in 2008/09, assuming that the country manages to produce more food and reduce expensive grain imports. The central bank governor, Salehuddin Ahmed, made it clear that the government had no plans to reduce the (currently heavy) subsidies on domestic fuel prices!a policy measure recommended by the World Bank. It is not clear for how long subsidies, which put considerable strain on the government"s fiscal position, will remain sustainable.

An important source of inflation remains the high import price of foodgrains. However, questions have been raised about the accuracy of recent inflation data. A statistician at the Bureau of Statistics has complained to international donors that the figures that the agency have compiled differ from published inflation data. Ordinary people cite the rise in prices for essential food items as their main concern since the caretaker government came to office in January.

According to data from the central bank, the trade balance deteriorated in the first two months of 2007/08. Bangladesh posted a trade deficit of US$717m in July-August, compared with a deficit of US$156m in the year-earlier period. The deterioration reflects falling exports and rising imports, according to the latest central bank data. Higher current transfers continued to underpin a generally weakening external account. The current-account balance recorded a deficit of US$68m in the two-month period, compared with a surplus of US$389m in July-August 2006. On the capital account, foreign direct investment fell by 0.4% year on year in July-August 2007, to US$132m. Foreign-exchange reserves, meanwhile, declined from US$5.4bn at end-October to US$5bn on November 13th, following a bi-monthly payment of US$462m to the Asian Clearing Union.

The central bank intervened in the currency market in the first half of November to rein in import-led inflation. It sold US$109m in US dollars through the interbank system in an attempt to strengthen the taka. The bank said that the measure was a temporary one, and that it was designed to make imports of food and oil cheaper. The taka stood at Tk68.64:US$1 on November 14th, compared with Tk69:US$1 at the start of 2007. The Trading Corporation of Bangladesh, a department of the Ministry of Commerce, has said that the prices of six major essential items (rice, flour, lentils, edible oil, potatoes and onions), the main drivers of high inflation, increased by up to 80% year on year in September.

Inflation is the primary concern

The current-account balance falls sharply

The central bank moves to stabilise the taka

14 Bangladesh

Monthly Report December 2007 www.eiu.com © The Economist Intelligence Unit Limited 2007

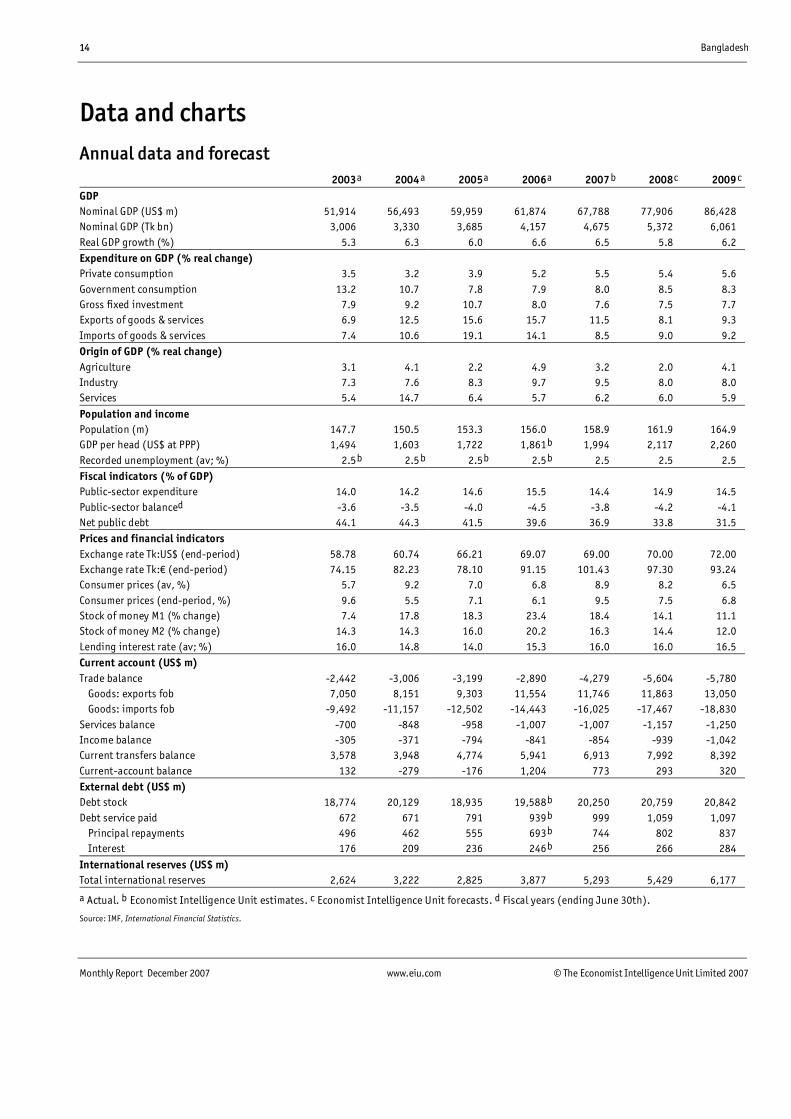

Data and charts Annual data and forecast

P ro d uc t io n to rem o v e

2003a 2004a 2005a 2006a 2007 b 2008c 2009c

GDP

Nominal GDP (US$ m) 51,914 56,493 59,959 61,874 67,788 77,906 86,428

Nominal GDP (Tk bn) 3,006 3,330 3,685 4,157 4,675 5,372 6,061

Real GDP growth (%) 5.3 6.3 6.0 6.6 6.5 5.8 6.2

Expenditure on GDP (% real change)

Private consumption 3.5 3.2 3.9 5.2 5.5 5.4 5.6

Government consumption 13.2 10.7 7.8 7.9 8.0 8.5 8.3

Gross fixed investment 7.9 9.2 10.7 8.0 7.6 7.5 7.7

Exports of goods & services 6.9 12.5 15.6 15.7 11.5 8.1 9.3

Imports of goods & services 7.4 10.6 19.1 14.1 8.5 9.0 9.2

Origin of GDP (% real change)

Agriculture 3.1 4.1 2.2 4.9 3.2 2.0 4.1

Industry 7.3 7.6 8.3 9.7 9.5 8.0 8.0

Services 5.4 14.7 6.4 5.7 6.2 6.0 5.9

Population and income

Population (m) 147.7 150.5 153.3 156.0 158.9 161.9 164.9

GDP per head (US$ at PPP) 1,494 1,603 1,722 1,861b 1,994 2,117 2,260

Recorded unemployment (av; %) 2.5b 2.5b 2.5b 2.5b 2.5 2.5 2.5

Fiscal indicators (% of GDP)

Public-sector expenditure 14.0 14.2 14.6 15.5 14.4 14.9 14.5

Public-sector balanced -3.6 -3.5 -4.0 -4.5 -3.8 -4.2 -4.1

Net public debt 44.1 44.3 41.5 39.6 36.9 33.8 31.5

Prices and financial indicators

Exchange rate Tk:US$ (end-period) 58.78 60.74 66.21 69.07 69.00 70.00 72.00

Exchange rate Tk:� (end-period) 74.15 82.23 78.10 91.15 101.43 97.30 93.24

Consumer prices (av, %) 5.7 9.2 7.0 6.8 8.9 8.2 6.5

Consumer prices (end-period, %) 9.6 5.5 7.1 6.1 9.5 7.5 6.8

Stock of money M1 (% change) 7.4 17.8 18.3 23.4 18.4 14.1 11.1

Stock of money M2 (% change) 14.3 14.3 16.0 20.2 16.3 14.4 12.0

Lending interest rate (av; %) 16.0 14.8 14.0 15.3 16.0 16.0 16.5

Current account (US$ m)

Trade balance -2,442 -3,006 -3,199 -2,890 -4,279 -5,604 -5,780

Goods: exports fob 7,050 8,151 9,303 11,554 11,746 11,863 13,050

Goods: imports fob -9,492 -11,157 -12,502 -14,443 -16,025 -17,467 -18,830

Services balance -700 -848 -958 -1,007 -1,007 -1,157 -1,250

Income balance -305 -371 -794 -841 -854 -939 -1,042

Current transfers balance 3,578 3,948 4,774 5,941 6,913 7,992 8,392

Current-account balance 132 -279 -176 1,204 773 293 320

External debt (US$ m)

Debt stock 18,774 20,129 18,935 19,588b 20,250 20,759 20,842

Debt service paid 672 671 791 939b 999 1,059 1,097

Principal repayments 496 462 555 693b 744 802 837

Interest 176 209 236 246b 256 266 284

International reserves (US$ m)

Total international reserves 2,624 3,222 2,825 3,877 5,293 5,429 6,177

a Actual. b Economist Intelligence Unit estimates. c Economist Intelligence Unit forecasts. d Fiscal years (ending June 30th).

Source: IMF, International Financial Statistics.

Bangladesh 15

Monthly Report December 2007 www.eiu.com © The Economist Intelligence Unit Limited 2007

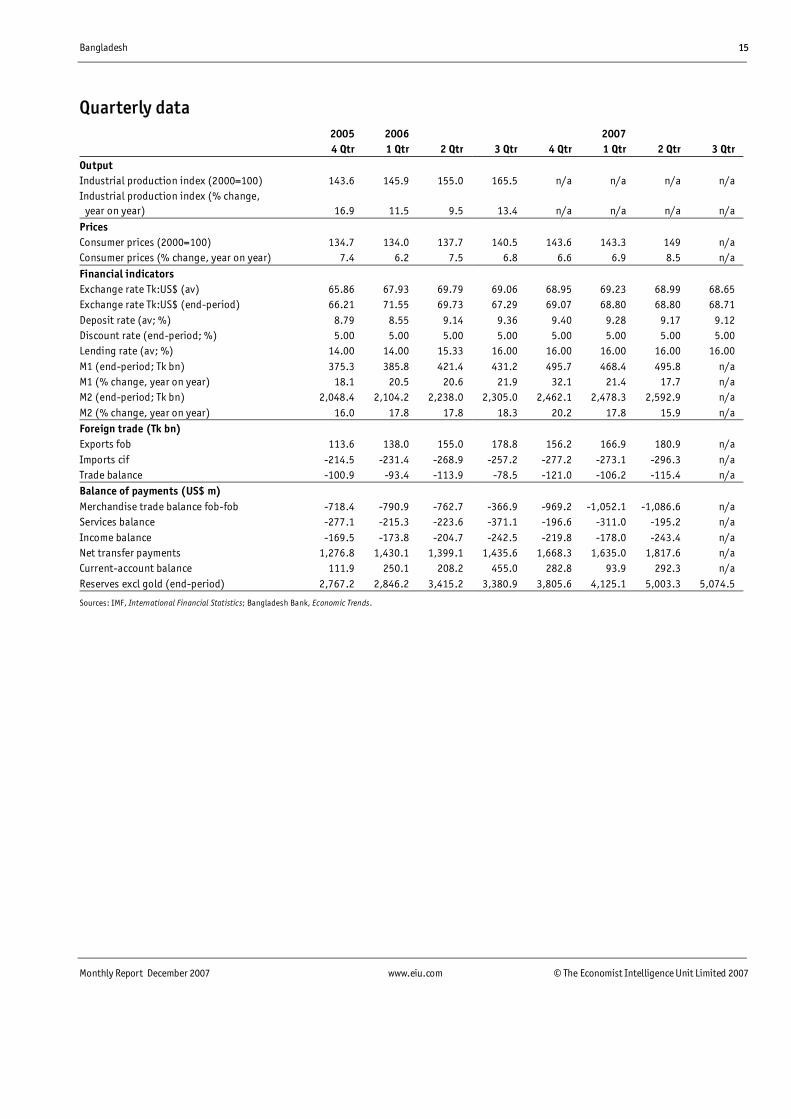

Quarterly data P ro d uc t io n to rem o v e

2005 2006 2007

4 Qtr 1 Qtr 2 Qtr 3 Qtr 4 Qtr 1 Qtr 2 Qtr 3 Qtr

Output

Industrial production index (2000=100) 143.6 145.9 155.0 165.5 n/a n/a n/a n/a

Industrial production index (% change, year on year) 16.9 11.5 9.5 13.4 n/a n/a n/a n/a

Prices

Consumer prices (2000=100) 134.7 134.0 137.7 140.5 143.6 143.3 149 n/a

Consumer prices (% change, year on year) 7.4 6.2 7.5 6.8 6.6 6.9 8.5 n/a

Financial indicators

Exchange rate Tk:US$ (av) 65.86 67.93 69.79 69.06 68.95 69.23 68.99 68.65

Exchange rate Tk:US$ (end-period) 66.21 71.55 69.73 67.29 69.07 68.80 68.80 68.71

Deposit rate (av; %) 8.79 8.55 9.14 9.36 9.40 9.28 9.17 9.12

Discount rate (end-period; %) 5.00 5.00 5.00 5.00 5.00 5.00 5.00 5.00

Lending rate (av; %) 14.00 14.00 15.33 16.00 16.00 16.00 16.00 16.00

M1 (end-period; Tk bn) 375.3 385.8 421.4 431.2 495.7 468.4 495.8 n/a

M1 (% change, year on year) 18.1 20.5 20.6 21.9 32.1 21.4 17.7 n/a

M2 (end-period; Tk bn) 2,048.4 2,104.2 2,238.0 2,305.0 2,462.1 2,478.3 2,592.9 n/a

M2 (% change, year on year) 16.0 17.8 17.8 18.3 20.2 17.8 15.9 n/a

Foreign trade (Tk bn)

Exports fob 113.6 138.0 155.0 178.8 156.2 166.9 180.9 n/a

Imports cif -214.5 -231.4 -268.9 -257.2 -277.2 -273.1 -296.3 n/a

Trade balance -100.9 -93.4 -113.9 -78.5 -121.0 -106.2 -115.4 n/a

Balance of payments (US$ m)

Merchandise trade balance fob-fob -718.4 -790.9 -762.7 -366.9 -969.2 -1,052.1 -1,086.6 n/a

Services balance -277.1 -215.3 -223.6 -371.1 -196.6 -311.0 -195.2 n/a

Income balance -169.5 -173.8 -204.7 -242.5 -219.8 -178.0 -243.4 n/a

Net transfer payments 1,276.8 1,430.1 1,399.1 1,435.6 1,668.3 1,635.0 1,817.6 n/a

Current-account balance 111.9 250.1 208.2 455.0 282.8 93.9 292.3 n/a

Reserves excl gold (end-period) 2,767.2 2,846.2 3,415.2 3,380.9 3,805.6 4,125.1 5,003.3 5,074.5

Sources: IMF, International Financial Statistics; Bangladesh Bank, Economic Trends.

16 Bangladesh

Monthly Report December 2007 www.eiu.com © The Economist Intelligence Unit Limited 2007

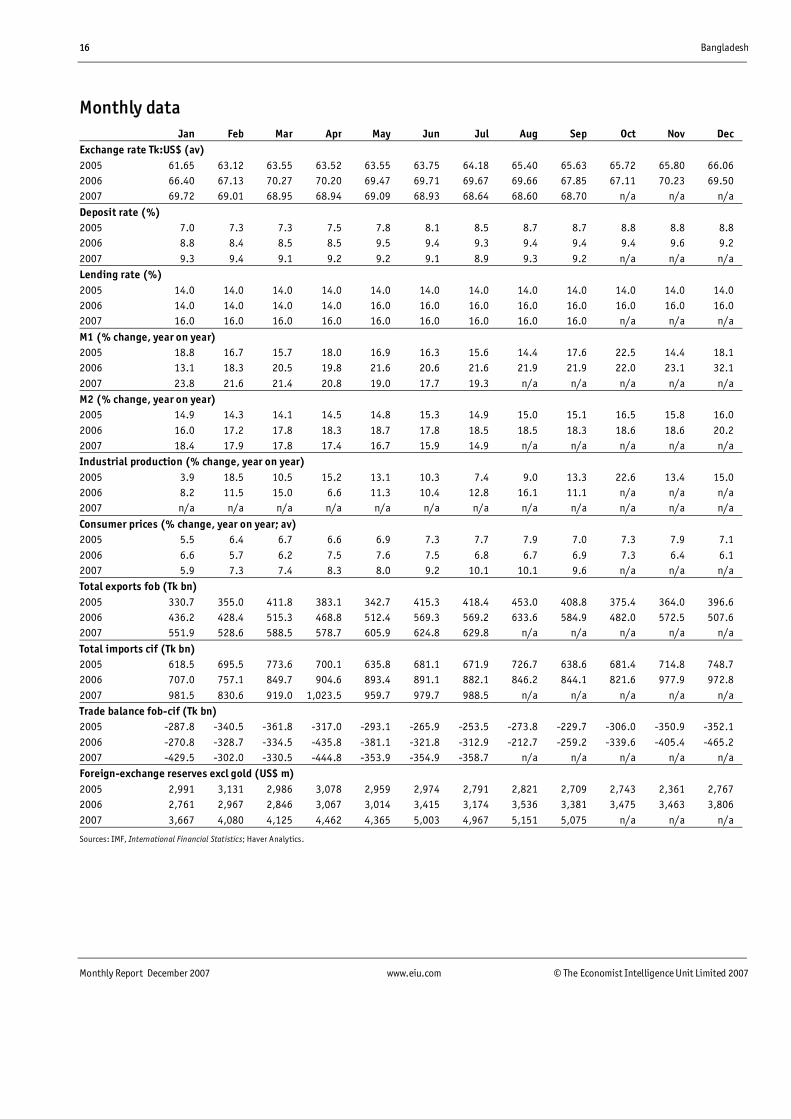

Monthly data P ro d uc t io n to rem o v e

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Exchange rate Tk:US$ (av) 2005 61.65 63.12 63.55 63.52 63.55 63.75 64.18 65.40 65.63 65.72 65.80 66.06

2006 66.40 67.13 70.27 70.20 69.47 69.71 69.67 69.66 67.85 67.11 70.23 69.50

2007 69.72 69.01 68.95 68.94 69.09 68.93 68.64 68.60 68.70 n/a n/a n/a

Deposit rate (%) 2005 7.0 7.3 7.3 7.5 7.8 8.1 8.5 8.7 8.7 8.8 8.8 8.8

2006 8.8 8.4 8.5 8.5 9.5 9.4 9.3 9.4 9.4 9.4 9.6 9.2

2007 9.3 9.4 9.1 9.2 9.2 9.1 8.9 9.3 9.2 n/a n/a n/a

Lending rate (%) 2005 14.0 14.0 14.0 14.0 14.0 14.0 14.0 14.0 14.0 14.0 14.0 14.0

2006 14.0 14.0 14.0 14.0 16.0 16.0 16.0 16.0 16.0 16.0 16.0 16.0

2007 16.0 16.0 16.0 16.0 16.0 16.0 16.0 16.0 16.0 n/a n/a n/a

M1 (% change, year on year) 2005 18.8 16.7 15.7 18.0 16.9 16.3 15.6 14.4 17.6 22.5 14.4 18.1

2006 13.1 18.3 20.5 19.8 21.6 20.6 21.6 21.9 21.9 22.0 23.1 32.1

2007 23.8 21.6 21.4 20.8 19.0 17.7 19.3 n/a n/a n/a n/a n/a

M2 (% change, year on year) 2005 14.9 14.3 14.1 14.5 14.8 15.3 14.9 15.0 15.1 16.5 15.8 16.0

2006 16.0 17.2 17.8 18.3 18.7 17.8 18.5 18.5 18.3 18.6 18.6 20.2

2007 18.4 17.9 17.8 17.4 16.7 15.9 14.9 n/a n/a n/a n/a n/a

Industrial production (% change, year on year) 2005 3.9 18.5 10.5 15.2 13.1 10.3 7.4 9.0 13.3 22.6 13.4 15.0

2006 8.2 11.5 15.0 6.6 11.3 10.4 12.8 16.1 11.1 n/a n/a n/a

2007 n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a

Consumer prices (% change, year on year; av) 2005 5.5 6.4 6.7 6.6 6.9 7.3 7.7 7.9 7.0 7.3 7.9 7.1

2006 6.6 5.7 6.2 7.5 7.6 7.5 6.8 6.7 6.9 7.3 6.4 6.1

2007 5.9 7.3 7.4 8.3 8.0 9.2 10.1 10.1 9.6 n/a n/a n/a

Total exports fob (Tk bn) 2005 330.7 355.0 411.8 383.1 342.7 415.3 418.4 453.0 408.8 375.4 364.0 396.6

2006 436.2 428.4 515.3 468.8 512.4 569.3 569.2 633.6 584.9 482.0 572.5 507.6

2007 551.9 528.6 588.5 578.7 605.9 624.8 629.8 n/a n/a n/a n/a n/a

Total imports cif (Tk bn) 2005 618.5 695.5 773.6 700.1 635.8 681.1 671.9 726.7 638.6 681.4 714.8 748.7

2006 707.0 757.1 849.7 904.6 893.4 891.1 882.1 846.2 844.1 821.6 977.9 972.8

2007 981.5 830.6 919.0 1,023.5 959.7 979.7 988.5 n/a n/a n/a n/a n/a

Trade balance fob-cif (Tk bn) 2005 -287.8 -340.5 -361.8 -317.0 -293.1 -265.9 -253.5 -273.8 -229.7 -306.0 -350.9 -352.1

2006 -270.8 -328.7 -334.5 -435.8 -381.1 -321.8 -312.9 -212.7 -259.2 -339.6 -405.4 -465.2

2007 -429.5 -302.0 -330.5 -444.8 -353.9 -354.9 -358.7 n/a n/a n/a n/a n/a

Foreign-exchange reserves excl gold (US$ m) 2005 2,991 3,131 2,986 3,078 2,959 2,974 2,791 2,821 2,709 2,743 2,361 2,767

2006 2,761 2,967 2,846 3,067 3,014 3,415 3,174 3,536 3,381 3,475 3,463 3,806

2007 3,667 4,080 4,125 4,462 4,365 5,003 4,967 5,151 5,075 n/a n/a n/a

Sources: IMF, International Financial Statistics; Haver Analytics.

Bangladesh 17

Monthly Report December 2007 www.eiu.com © The Economist Intelligence Unit Limited 2007

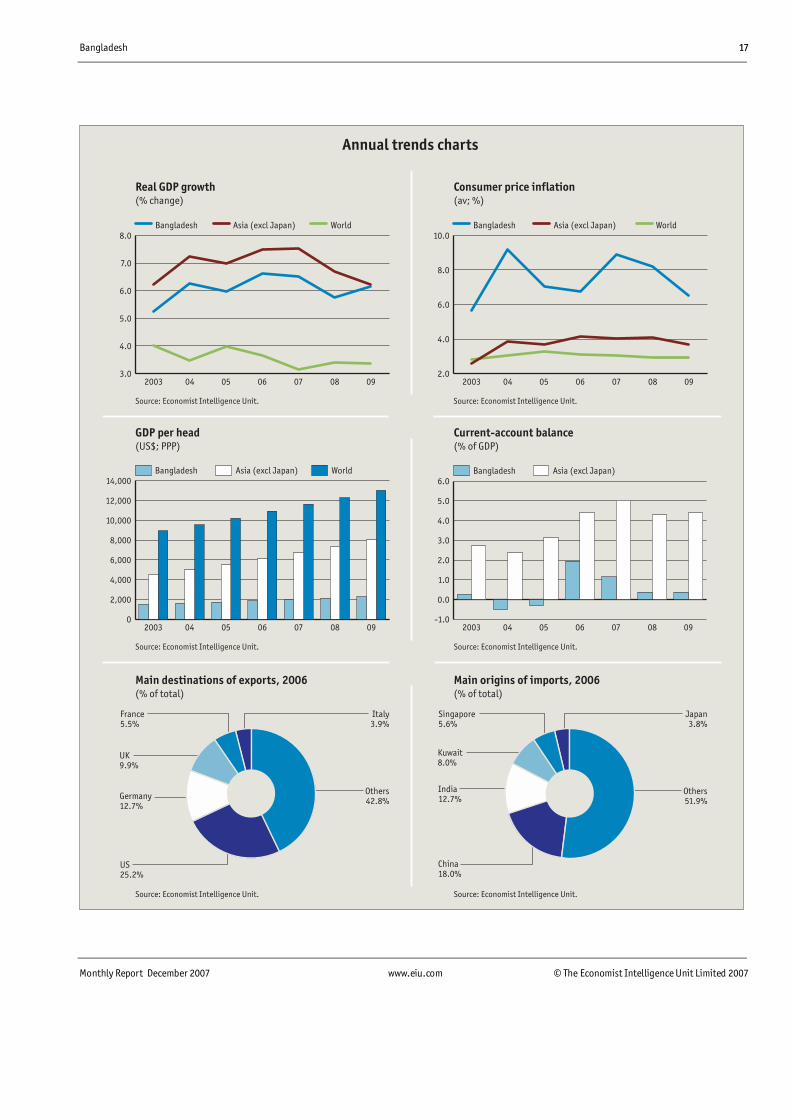

Annual trends charts P ro d uc t io n to rem o v e

Annual trends charts

GDP per head(US$; PPP)

Current-account balance(% of GDP)

Source: Economist Intelligence Unit. Source: Economist Intelligence Unit.

Source: Economist Intelligence Unit. Source: Economist Intelligence Unit.

3.0

4.0

5.0

6.0

7.0

8.0 World Asia (excl Japan) Bangladesh

09080706050420032.0

4.0

6.0

8.0

10.0 World Asia (excl Japan) Bangladesh

0908070605042003

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0 Asia (excl Japan) Bangladesh

09080706050420030

2,000

4,000

6,000

8,000

10,000

12,000

14,000 World Asia (excl Japan) Bangladesh

0908070605042003

Real GDP growth(% change)

Consumer price inflation(av; %)

Main destinations of exports, 2006(% of total) (% of total)

Main origins of imports, 2006

France5.5%

US25.2%

Italy3.9%

Others42.8%

Singapore5.6%

China18.0%

Japan3.8%

Others51.9%

Source: Economist Intelligence Unit. Source: Economist Intelligence Unit.

UK9.9%

Germany12.7%

Kuwait8.0%

India12.7%

18 Bangladesh

Monthly Report December 2007 www.eiu.com © The Economist Intelligence Unit Limited 2007

Monthly trends charts P ro d uc t io n to rem o v e

Monthly trends charts

Consumer price inflation(% change, year on year)

Interest rates(av; %)

Foreign trade(US$ m; goods only)

Oil: Brent crude price(US$/b; av)

Exchange rate(Tk:US$ av; inverted scale)

Foreign-exchange reserves(US$ m)

2,000

2,500

3,000

3,500

4,000

4,500

5,000

5,500

JulAprJan07

OctJulAprJan06

OctJulAprJan05

OctJulApr2004

30.0

40.0

50.0

60.0

70.0

80.0

JulAprJan07

OctJulAprJan06

OctJulAprJan05

OctJulApr2004

5.0

6.0

7.0

8.0

9.0

10.0

11.0

JulAprJan07

OctJulAprJan06

OctJulAprJan2005

72.0

70.0

68.0

66.0

64.0

62.0

60.0

58.0

JulAprJan07

OctJulAprJan06

OctJulAprJan05

OctJulApr2004

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0 Lending rate Deposit rate

JulAprJan07

OctJulAprJan06

OctJulAprJan05

OctJulApr2004

-600

-400

-200

0

200

400

600

800

1,000

1,200 Balance Imports Exports

JulAprJan07

OctJulAprJan06

OctJulAprJan05

OctJulApr2004

Source: Economist Intelligence Unit.Source: Economist Intelligence Unit.

Source: Economist Intelligence Unit.Source: Economist Intelligence Unit.

Source: Economist Intelligence Unit.Source: Economist Intelligence Unit.

Bangladesh 19

Monthly Report December 2007 www.eiu.com © The Economist Intelligence Unit Limited 2007

Country snapshot

Political structure

People"s Republic of Bangladesh

Parliamentary democracy, following a constitutional amendment in September 1991. On the expiry of a government"s term in office, a caretaker government takes office to administer a general election. However, on January 11th 2007 the parliamentary election scheduled for later that month was cancelled and a state of emergency declared. A military-backed caretaker government took office on January 12th

Under the constitution, executive powers lie with the caretaker government until the prime minister of a new administration is sworn in following a parliamentary election

A unicameral parliament, consisting of 300 members directly elected by geographical constituencies; the legislature is elected for a five-year term

The caretaker government plans to hold the next parliamentary election towards the end of 2008

The term of the caretaker government expires when a new prime minister is sworn in; until then affairs of state are conducted by the president and the "advisers" who make up the caretaker government. The current, unelected and military-backed caretaker government is carrying out reforms to the electoral system in preparation for a poll to elect a new, democratic government

Bangladesh Nationalist Party (BNP); Awami League (AL); Jatiya (Ershad) and various Jatiya Party factions; Jamaat-e-Islami (Jamaat); Liberal Democratic Party (LDP); Jatiya Samajtantrik Dal (JSD); Islami Oikyo Jote (IOJ)

President Iajuddin Ahmed

Chief adviser, home affairs, establishment & Election Commission secretariat Fakhruddin Ahmed

Agriculture, fishery & environment Chowdhury Sajjadul Karim Communications & transport Major-general M A Matin Education & cultural affairs Ayub Quadri Finance, planning & commerce Mirza Azizul Islam Foreign affairs Iftekhar Ahmed Chowdhury Health, family welfare, water & religious affairs Major-general A S M Matuir Rahman Law, justice & parliamentary affairs, land & information Mainul Hosein Local government, rural development co-operatives, labour Anwarul Iqbal Power, food & disaster management Tapan Chowdhury Women, children affairs, industries & textiles Geeteara S Choudhury

Salehuddin Ahmed

The executive

Form of government

National legislature

National elections

Main political organisations

Advisers

Central bank governor

National government

Official name

Caretaker government

![Reiserapport - Bangladesh 2007[1] - LandInfo · fact finding mission to Bangladesh in November 2007. ... (AL) ble den første statsministeren i Bangladesh. I 1975 ... I 2001 vant](https://img.pdfslide.net/doc/110x75/5b8655097f8b9a162d8cbba0/reiserapport-bangladesh-20071-landinfo-fact-finding-mission-to-bangladesh.jpg)