Embed Size (px)

Citation preview

- 1 -

BANK HANDLOWY W WARSZAWIE S.A.3Q 2008 consolidated financial results

- 2 -

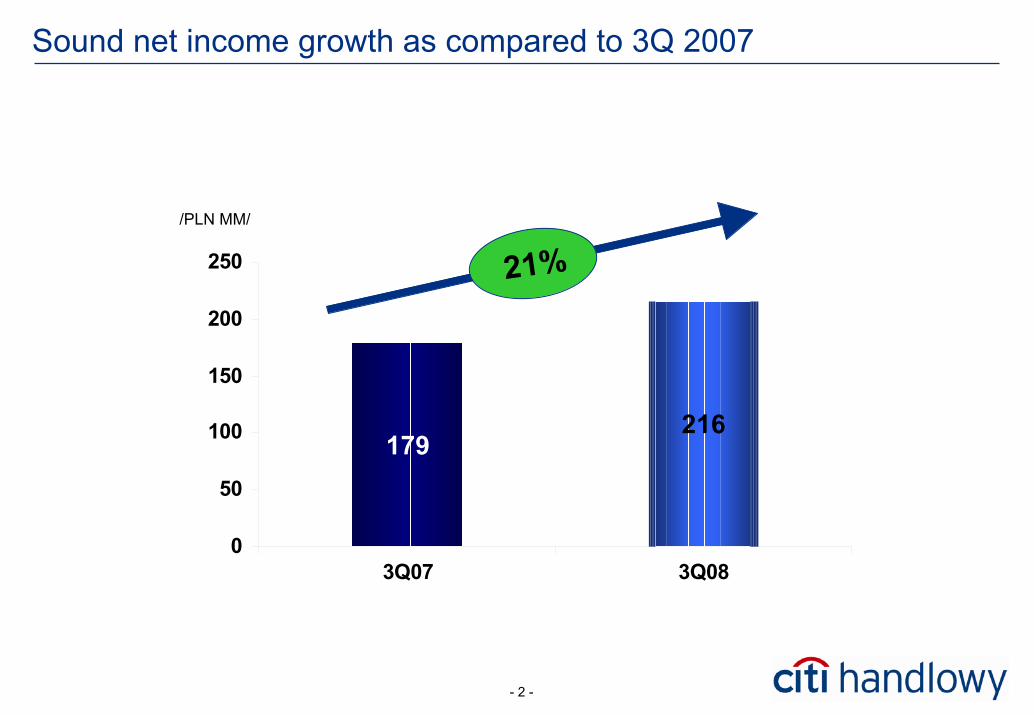

Sound net income growth as compared to 3Q 2007

216179

0

50

100

150

200

250

3Q07 3Q08

/PLN MM/

21%

- 3 -

P&L lines impact on net income 3Q 2008 vs. 3Q 2007/PLN MM/

69

28 12

216179

741

0

50

100

150

200

250

NETINCOME

3Q07

Treasury Fees Interests Netimpairment losses

Other NETINCOME

3Q 08

22%(3Q08/3Q07)

Fees result

9%(3Q08/3Q07)

Net interest income

3,4%by 0,4 pp

(3Q08/3Q07)Net interest

margin

2%(3Q08/3Q07)

Expenses and depreciation

12 mln

(3Q08/3Q07)Net impairment

losses

73%(3Q08/3Q07)

Treasury result

- 4 -

Major financial ratios

3Q 20083Q 2007 2Q 2008

14.9%

1.9%

61 %

12.9%**

16.3%

13.8%

1.8%

63 %

11.6%

14.9%

17.4%

2.3%

56 %

12.3%

15.6%

ROE*

ROE

ROA*

Cost / Income

CAR

* based on annualized net income

**CAR calculated as at December 31, 2007

- 5 -

Banking sector liquidityFunding gap of non-financial sector

(deposits - loans)66

.4

-12.

5

7.6

7.6

7.3 8.1

6.4

5.7

0.2

6.4

-30.

3

-50

-25

0

25

50

75

3Q 2006 3Q 2007 4Q 2007 1Q 2008 2Q 2008 3Q 2008

PLN B

Banking Sector Citi Handlowy

Source: NBP (Polish central bank), financial statements of Citi Handlowy

- 6 -

CAR

CAR

12,1%

12,4%

12,9%

11,6%

10,8%

11,0%11,8%

10,8%

12,3%

8%

9%

10%

11%

12%

13%

14%

3Q07 4Q07 1Q08 2Q08 3Q08

Banking sector Citi Handlowy

- 7 -

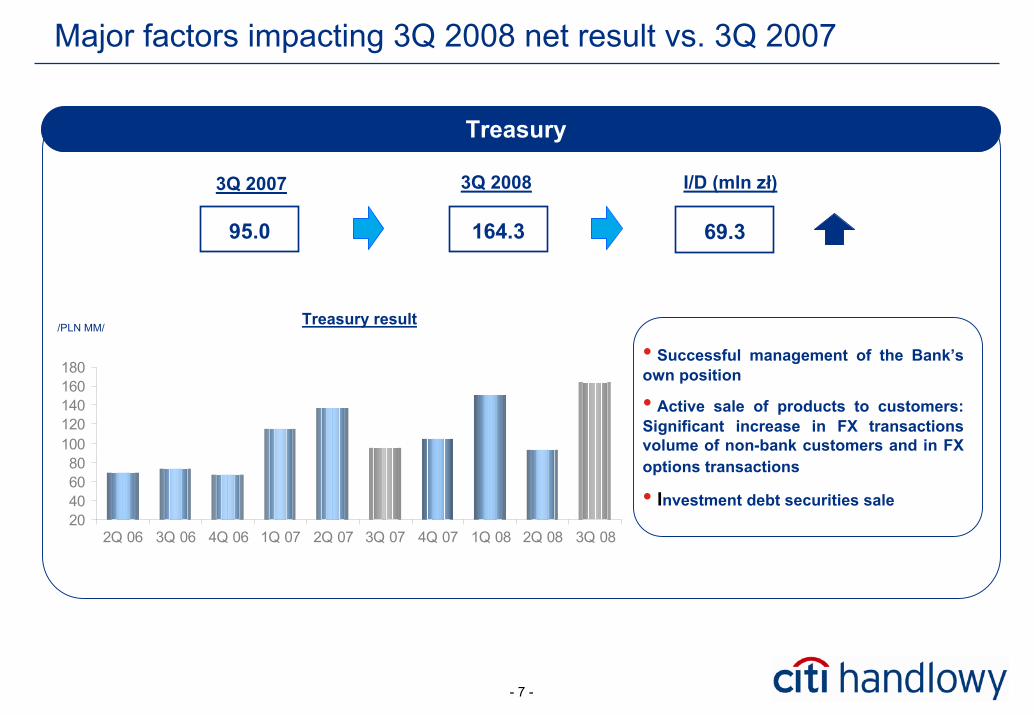

Major factors impacting 3Q 2008 net result vs. 3Q 2007

164.3

3Q 2007 3Q 2008 I/D (mln zł)

69.395.0

Treasury result/PLN MM/

Treasury

• Successful management of the Bank’s own position

• Active sale of products to customers: Significant increase in FX transactions volume of non-bank customers and in FXoptions transactions

• Investment debt securities sale20406080

100120140160180

2Q 06 3Q 06 4Q 06 1Q 07 2Q 07 3Q 07 4Q 07 1Q 08 2Q 08 3Q 08

- 8 -

Treasury

Proprietary management result

High volatility of the proprietary management result

*/

Proprietary management

2Q 06 3Q 06 4Q 06 1Q 07 2Q 07 3Q 07 4Q 07 1Q 08 2Q 08 3Q 08

49%(3Q08/3Q07)

FX result (FX spot)

51%(3Q08/3Q07)

Customer activity result

Customer activity

Customer activity result*/

2Q 06 3Q 06 4Q 06 1Q 07 2Q 07 3Q 07 4Q 07 1Q 08 2Q 08 3Q 08

*Scale on charts is incomparable

- 9 -

Major factors impacting 3Q 2008 net result vs. 3Q 2007

/mld zł/ Mutual funds net inflow (market) WSE turnover (market)

Fees & commissions result

/mld zł/

25%(3Q08/3Q07)

Custody services

34%(3Q08/3Q07)

Investment and insurance products

44%(3Q08/3Q07)

Brokerage fees

0

20

40

60

80

100

120

140

1Q 07 2Q 07 3Q 07 4Q 07 1Q 08 2Q 08 3Q 08

-15

-10

-5

0

5

10

15

1Q 07 2Q 07 3Q 07 4Q 07 1Q 08 2Q 08 3Q 08

- 10 -

Major factors impacting 3Q 2008 net result vs. 3Q 2007

Net interest income and net interest margin

(11%)(3Q08/3Q07)

AFS portfolio income

28%(3Q08/3Q07)

Interests from loans – non-

financial sector

37%(3Q08/3Q07)

Interests from credit cards

/PLN MM/

150170190210230250270290310330350

1Q 06 2Q 06 3Q 06 4Q 06 1Q 07 2Q 07 3Q 07 4Q 07 1Q 08 2Q 08 3Q 082,6%

2,7%

2,8%

2,9%

3,0%

3,1%

3,2%

3,3%

3,4%

3,5%Net interest result Net interest margin

- 11 -

Major factors impacting 3Q 2008 net result vs. 3Q 2007

(22.6)

3Q 2007 3Q 2008 I/D (mln zł)

(12.0)(10.6)

/PLN MM/ Net impairment losses

Net impairment losses

(30)(20)(10)

010203040

2Q 06 3Q 06 4Q 06 1Q 07 2Q 07 3Q 07 4Q 07 1Q 08 2Q 08 3Q 08

- 12 -

Expenses under control – strategy delivery

177

198 196

171

0

50

100

150

200

250

300

350

400

3Q2007 3Q2008

/PLN MM/ 376 367(2%)

(4%)

(1%)

3Q07 2Q08 3Q08GCG 69% 68% 65%CMB 54% 57% 48%Total 61% 63% 56%

Cost / Income

Retail Bank (GCG)Corporate Bank (CMB)

● Corporate: lower staff expenses and staff expenditures, decrease of technological expenses

● Retail: Expenses of the segment went down slightely, higher expenses related to increased acquisition and portfolio growth were compensated by growing effectiveness of the segment and lower marketing spending

- 13 -

Balance sheet structure improvement

6.1 4.0

6.57.1

8.77.1

5.14.8

14.112.5

31.12.07 30.09.082.0 2.74.4 3.0

5.6

7.1 6.0

19.819.8

5.6

31.12.07 30.09.08

Financial sector

Trading portfolio

Other assets

Loans – non-financial sector

Assets

13%

9%(6%)

(5%) 38.9

(18%)

37.138.9

0%

(15%)

(34%)

37.1 (5%) /PLN MM/

0%(32%)

Liabilities

/PLN MM/

Deposits – non-financial sector

Deposits – financial sector

EquityAFS

Trading portfolio

Other liabilities

13%(3Q08/4Q07)

Loans to non-financial sector

71%up by 8 pp

(3Q08/4Q07)

Loans / deposits ratio

38%up by 6 pp

(3Q08/4Q07)

Loans’ share in total assets

12,3%up by 0,7 pp

(3Q08/2Q08)

Capital Adequacy Ratio

- 14 -

Loans

Non-financial sector loans

0123456789

30.06.08 30.09.08

Market

Corporate loans

(3%)

7%

7%

0123456

30.06.08 30.09.08

Retail loans

4%

Market (excl. mortgage)

8%

Corporate loans: including public sector and local government institutionsSource: Bank’s estimates, data pro-forma, in PLN billion

- 15 -

Deposits

02468

101214

30.06.08 30.09.08

Corporate deposits

(4%)

(5%)

(2%)

Market

4%

TermCurrent

024

68

30.06.08 30.09.08

5%

(6%)

Retail deposits

(2%)Market

5%

Non-financial sector deposits

Corporate deposits including public sector and local government institutions

Source: Bank’s estimates, data pro-forma, in PLN billion

- 16 -

Results of the third quarter – corporate banking

Achievements of the Bank for corporates

130 %Growth of

transactions volumes concluded by On Line Trading

Platformcompared to

analogous period of 2007

3-year loan agreement was signed with FMCG segment player for the

amount of

40 million USD

Almost 80% growth of volumes level on

hedging by customerstheir FX exposure by

options(IIIQ2008/ IIIQ2007)

50 % Growth of the

number of customers on On Line Trading

Platform(IIIQ2008/ IIIQ2007)

- 17 -

Results of the third quarter – corporate banking

Prepaid payment cards Citi Handlowy – market leader

Innovative solution with a wide spectrum of use:

� social benefit card

� instrument in contests and promotions

� tool used in incentive programmes

70%Market share

90% Growth of issued cards at

the end of the III quarter 2008 as compared to analogous

period of 2007

420,000 cards

prepaid were issued as at the end of September 2008

- 18 -

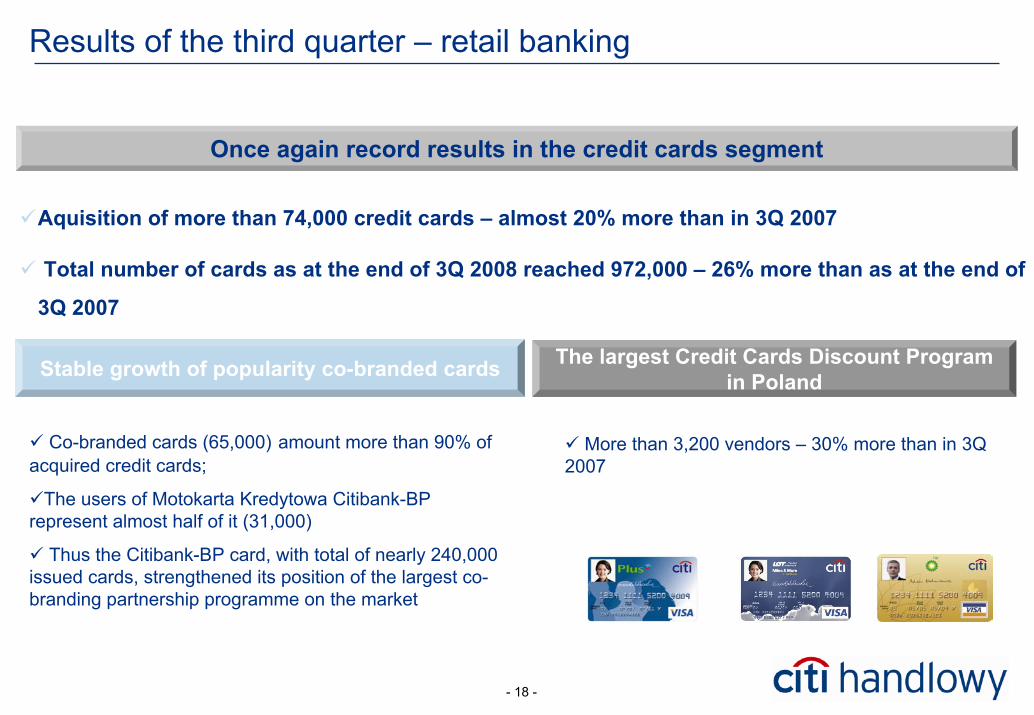

Results of the third quarter – retail banking

Once again record results in the credit cards segment

�Aquisition of more than 74,000 credit cards – almost 20% more than in 3Q 2007

� Total number of cards as at the end of 3Q 2008 reached 972,000 – 26% more than as at the end of

3Q 2007

The largest Credit Cards Discount Program in PolandStable growth of popularity co-branded cards

� Co-branded cards (65,000) amount more than 90% of acquired credit cards;

�The users of Motokarta Kredytowa Citibank-BPrepresent almost half of it (31,000)

� Thus the Citibank-BP card, with total of nearly 240,000 issued cards, strengthened its position of the largest co-branding partnership programme on the market

� More than 3,200 vendors – 30% more than in 3Q 2007

- 19 -

Innovations for customer – retail banking

Safety and comfort for individual customers

� Innovative SMS service which helps holders of Citibank Credit Cards to locate the Discount Program partners

� Shopping in the Internet for instalments with Citibank Credit Cards – customer is enabled to independently set up instalment plans on his/her Citibank Credit Card payments, this via the eCard served internet shops

SMS with adresses of the nearest vendors, whereattractive discounts can

be obtained

CitibankOnline↑20%

(IIQ2008 vs. IIIQ2008)The growth of the number of customers, which

decided on Online Statements (255,000)

One motion for new customers for gaining retail products of the Bank

(current account in PLN and other currencies, deposit accounts, credit line in the account, credit card and

insurance products)

- 20 -

Prospect for the Polish Economy

• Euro zone recession will likely contribute to economic slowdown in Poland

• Risk of heightened market volatility due to global financial crisis

• Economic growth weakness opens doors for interest rate cuts in Poland

Unfavourable External Environment Increased Financial Market Volatility

Likely Substantial Rate Cuts

4.0

4.5

5.0

5.5

6.0

6.5

7.0

Jul-0

7

Oct

-07

Jan-

08

Apr

-08

Jul-0

8

Oct

-08

Jan-

09

Apr

-09

Jul-0

9

Oct

-09

NBP reference rate (%) Forecast

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

1q08 2q08 3q08 4q08 1q09 2q09 3q09 4q09

Poland - GDP (% YoY) Euro Area (% YoY)

3.1

3.2

3.3

3.4

3.5

3.6

3.7

3.8

3.9

4.0

Jul-0

8

Aug

-08

Sep

-08

Oct

-08

Nov

-08

EUR/PLN exchange rate

Sources: NBP, Eurostat, GUS, Citi Handlowy forecasts.

- 21 -

- 22 -

3Q 2008 results

PLN MM 3Q 2007 3Q 2008I/ (D) I/ (D) %

Net interest income 306,8 335,0 28,2 9%Net fee and commission income 191,3 150,1 (41,2) (22%)Dividend income 3,5 0,4 (3,1) (89%)Treasury 95,0 164,3 69,3 73%Equity instruments result 0,3 0,0 (0,3) (100%)Other operating revenue 18,0 11,2 (6,8) (38%)Revenue 614,9 661,1 46,2 8%Expenses and depreciation (375,7) (367,2) (8,5) (2%)Total operating expenses (349,0) (343,1) (5,8) (2%)Depreciation (26,7) (24,1) (2,6) (10%)Income on fixed assets sale 0,5 1,3 0,8 155%Movements in provisions (10,6) (22,6) (12,0) 113%Share in subs' profits 0,0 0,0 (0,0) -EBIT 229,2 272,5 43,4 19%Corporate tax (50,3) (56,8) 6,5 13%

Net profit 178,8 215,7 36,9 21%

3Q08/3Q07

- 23 -

Corporate banking 3Q 2008 results

PLN MM 3Q 2007 3Q 2008I/ (D) I/ (D) %

Net interest income 138,6 128,5 (10,1) (7%)Net fee and commission income 78,8 62,0 (16,9) (21%)Dividend income 3,5 0,4 (3,1) (89%)Treasury 86,9 154,2 67,3 77%Equity instruments result 0,3 0,0 (0,3) (100%)Other operating revenue 18,1 13,9 (4,2) (23%)Revenue 326,2 358,9 32,7 10%Expenses and depreciation (177,3) (170,7) (6,6) (4%)Total operating expenses (158,5) (154,9) (3,6) (2%)Depreciation (18,8) (15,8) (2,9) (16%)Income on fixed assets sale 0,5 1,0 0,6 117%Movements in provisions 6,7 (4,0) (10,7) nmShare in subs' profits 0,0 0,0 (0,0) -EBIT 156,2 185,2 29,1 19%

3Q08/3Q07

- 24 -

Retail banking 3Q 2008 results

PLN MM 3Q 2007 3Q 2008I/ (D) I/ (D) %

Net interest income 168,3 206,6 38,3 23%Net fee and commission income 112,5 88,2 (24,3) (22%)Dividend income 0,0 0,0 0,0 - Treasury 8,1 10,1 2,0 25%Equity instruments result 0,0 0,0 0,0 - Other operating revenue (0,1) (2,7) (2,5) nmRevenue 288,7 302,2 13,4 5%Expenses and depreciation (198,4) (196,5) (1,9) (1%)Total operating expenses (190,4) (188,2) (2,2) (1%)Depreciation (8,0) (8,2) 0,3 4%Income on fixed assets sale 0,0 0,2 0,2 1167%Movements in provisions (17,4) (18,6) (1,3) 7%Share in subs' profits 0,0 0,0 0,0 - EBIT 73,0 87,3 14,3 20%

3Q08/3Q07