Embed Size (px)

Citation preview

B A N K O F C A N A D A

FinancialSystem Review

December 2003

Members of the Editorial Committee

David Longworth, Chair

Agathe CôtéClyde GoodletJohn HelliwellPaul C. JenkinsTiff Macklem

Dinah MacleanJohn Murray

Graydon PaulinGeorge Pickering

James PowellDenis Schuthe

Jack SelodyRobert Turnbull

Jill MoxleyLea-Anne Solomonian

(Editors)

The Bank of Canada’s Financial System Review is published semi-annually. Copies maybe obtained free of charge by contacting

Publications Distribution, Communications Department, Bank of Canada, Ottawa,Ontario, Canada K1A 0G9Telephone: (613) 782-8248; e-mail: [email protected]

Please forward any comments on the Financial System Review to

Public Information, Communications Department, Bank of Canada, Ottawa,Ontario, Canada K1A 0G9Telephone: (613) 782-8111, 1-800-303-1282; e-mail: [email protected]

Web site: <http://www.bankofcanada.ca>

Bank of CanadaDecember 2003

Contents

Developments and Trends ............................................................ 1

Introduction ............................................................................................ 3

Highlighted Issues .................................................................................... 4

The Macrofinancial Environment ............................................................... 11

The Financial System................................................................................ 22

Reports ...................................................................................... 31

Introduction ............................................................................................ 33

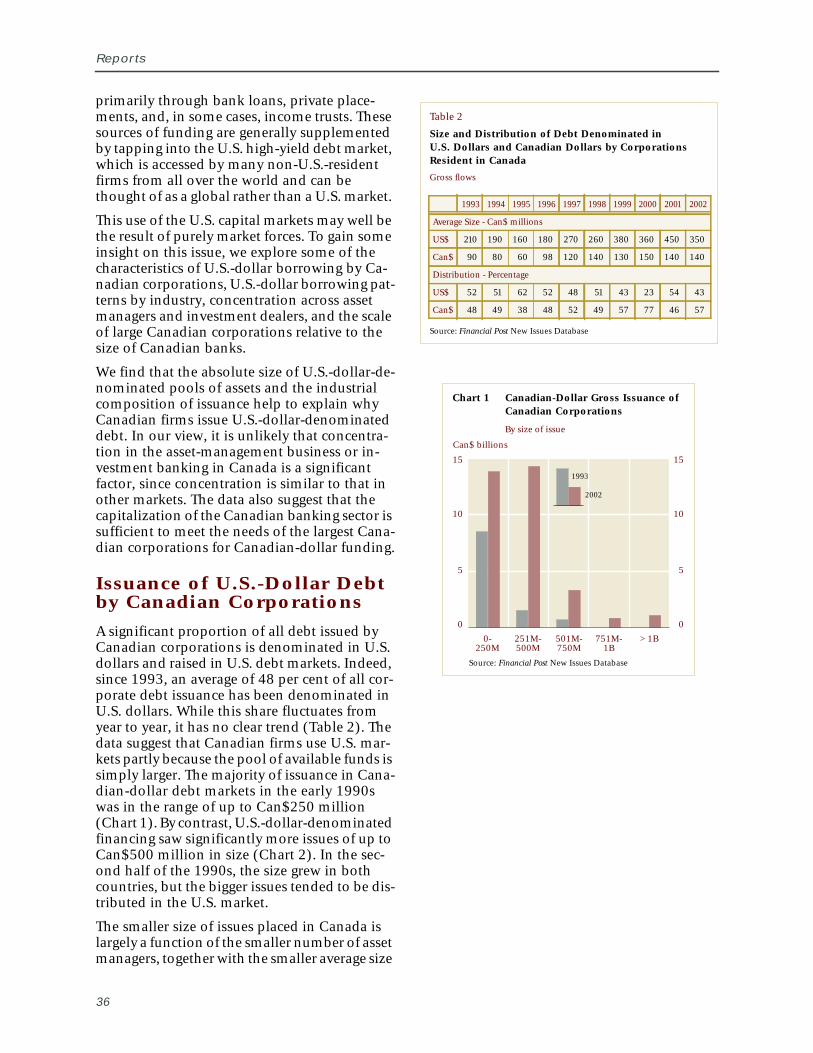

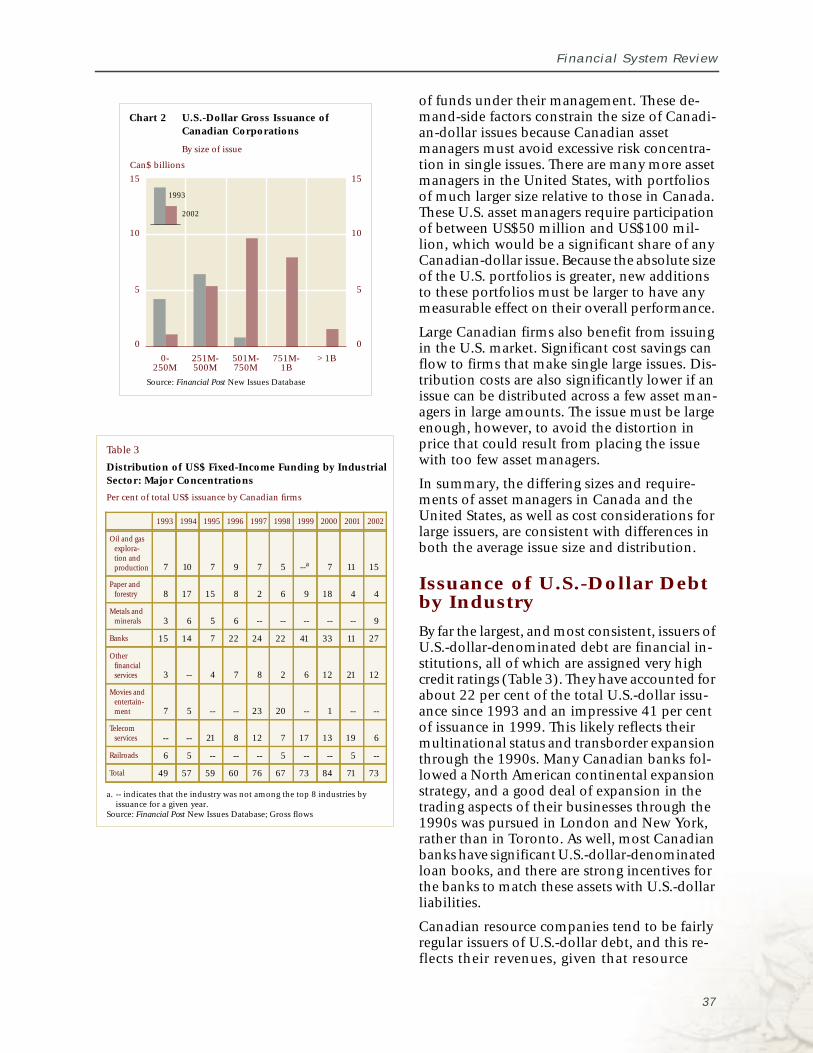

Development of the Canadian Corporate Debt Market:Some Stylized Facts and Issues ................................................................... 35

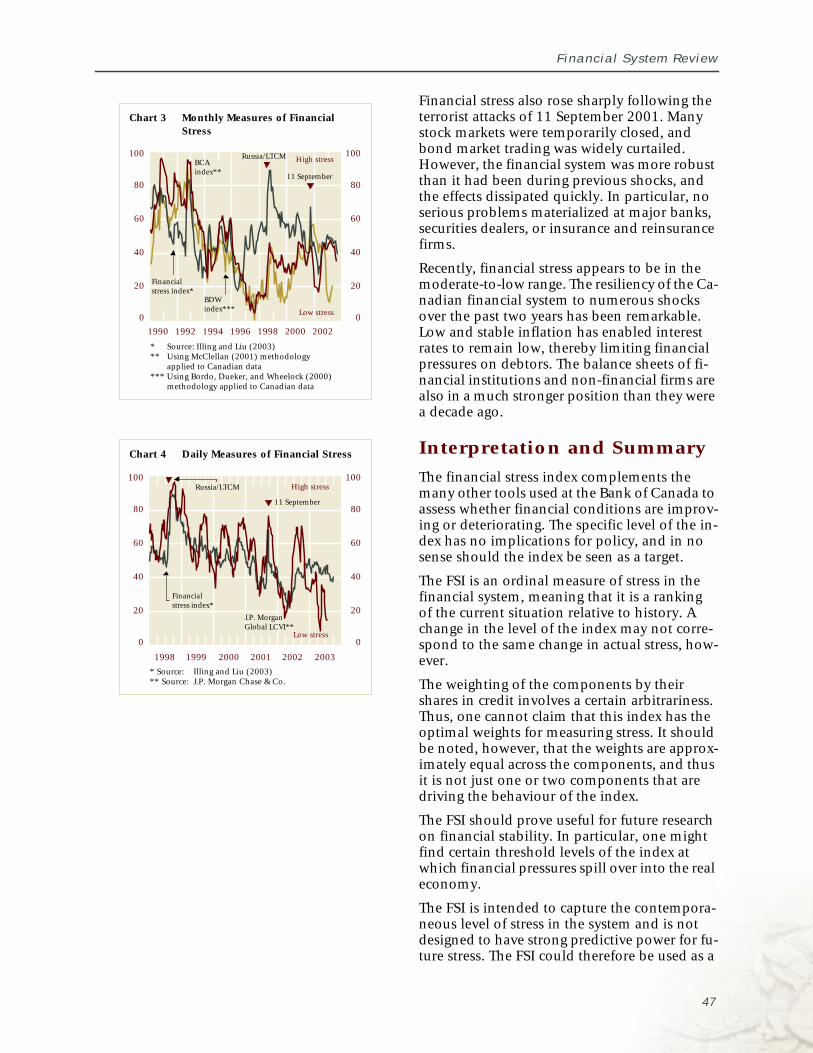

Measuring Financial Stress........................................................................ 43

Policy and Infrastructure Developments ........................................ 49

Introduction ............................................................................................ 51

Restoring Investor Confidence: Background on RecentDevelopments in Canada .......................................................................... 53

Transparency in the Canadian Fixed-Income Market:Opportunities and Constraints ................................................................... 59

Policy Issues in Retail Payments ................................................................. 65

Research Summaries ................................................................... 69

Introduction ............................................................................................ 71

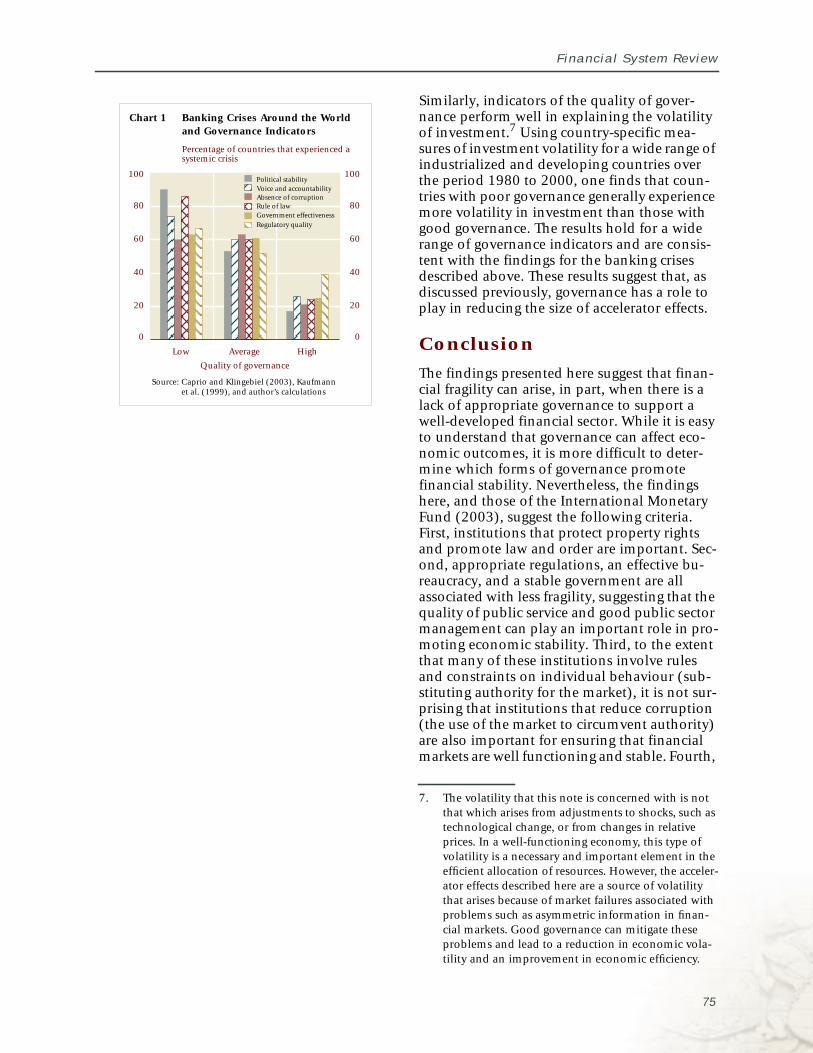

Governance and Financial Fragility............................................................ 73

Income Trusts: Understanding the Issues..................................................... 77

Valuation of Canadian- versus U.S.-Listed Equities:Is There a Discount? ................................................................................. 81

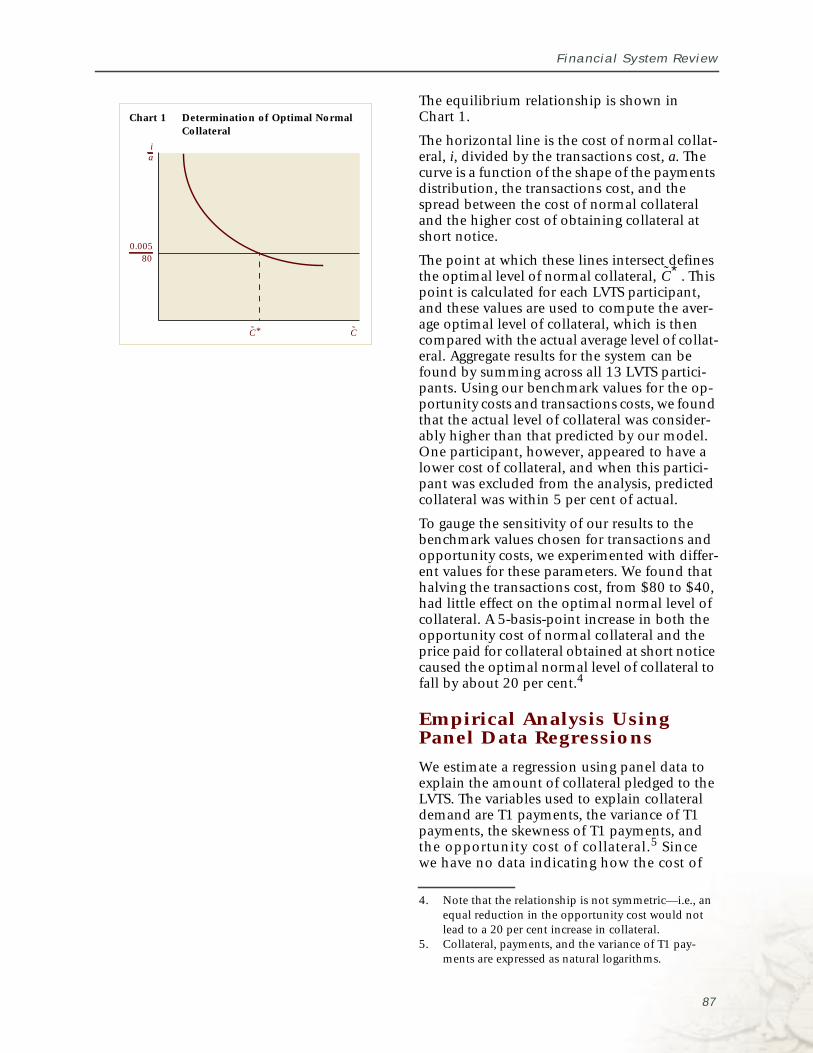

Excess Collateral in the LVTS: How Much Is Too Much? ............................... 85

Developments

and

Trends

Notes

The material in this document is based on information available to 3 Decemberunless otherwise indicated.

The phrase “major banks” in Canada refers to the six largest Canadian commercialbanks by asset size: the Bank of Montreal, CIBC, National Bank, RBC Financial Group,Scotiabank, and TD Bank Financial Group.

Financial System Review

Introduction

This section of the Financial SystemReview examines the recent performanceof the Canadian financial system and thefactors, both domestic and international,that are influencing it. In each issue, oneor more subjects of particular interest arediscussed as highlighted topics.

A key development during the second half of2003 is the substantial improvement in the glo-bal macrofinancial environment. The economicoutlook for the industrialized economies, afterdeteriorating during the first half of the year,has been revised upwards since the summer. Fi-nancial institutions in the United States and Eu-rope are reporting improved financial results.Nevertheless, risks associated with global im-balances remain, and in Canada the strongerdollar will affect the financial positions of thosesectors with a strong net export orientation.

Key Points

• An improving economic environmentand a stabilization in corporate creditquality have contributed to better resultsfor financial institutions.

• The risks associated with the ability ofCanadian households to meet theirfinancial obligations under changingfinancial conditions appear to be withinmanageable levels.

• The financial system has experiencedsome significant changes in the prices offinancial assets, but has responded in aresilient fashion.

Stronger economic conditions have helped tostabilize the earlier decline in corporate creditquality, both globally and in Canada. Defaultrates and credit-rating downgrades on corporatedebt have diminished. A declining need to addto loan-loss provisions contributed to thestrong increase in profitability reported byCanadian banks in the second half of the year.Canadian banks have fared well over the currentbusiness cycle, compared with earlier cycles,attesting to their strong underlying position.Other financial institutions have also reportedimproved results.

In the face of past heightened losses on corpo-rate lending exposures, the relative strength ofthe Canadian household sector has been a wel-come source of support for the financial sector.An assessment of the potential impact of chang-es to the financial environment, such as higherinterest rates or a fall in housing prices, on theability of households to service their debt sug-gests that the risks in this area are within man-ageable levels.

In the context of an improving economic envi-ronment and an increase in investors’ appetitefor risk, there were some large movements in fi-nancial prices during recent quarters. Yields onlong-term bonds fell to very low levels in June,before subsequently rising. Equity prices haverisen steadily since the second quarter, as inves-tors anticipate improved corporate earnings.Against the background of rapidly growing U.S.international indebtedness, global exchangerates have been dominated by a decline in thevalue of the U.S. dollar, such that the Canadiandollar has appreciated significantly. The Cana-dian financial system has adapted to thesechanging conditions in a resilient fashion.

International efforts to buttress investor confi-dence in capital markets, including revised stan-dards for financial reporting and auditing, havecontinued. The importance of better oversight

3

Developments and Trends

Chart 2 Distribution of Lending by FinancialInstitutions, 2003

Chart 1 Household and Business Credit

Year-over-year rate of growth

Source: Bank of Canada

Source: Bank of Canada, based on year-to-date averagebalances as of October 2003

Other financialinstitutions

Charteredbanks

Residentialmortgagecredit

11%

20%

9%

Charteredbanks

Consumercredit

Other financialinstitutions

5%

Businesscredit

55%

0

2

4

6

8

10

0

2

4

6

8

10

2000 2001 2002 2003

%

Total household credit

Total business credit

and of high-quality financial reporting has re-cently been emphasized by the expanding in-vestigation of trading practices in the U.S.mutual fund industry, which has revealed fur-ther issues related to market conduct.

Highlighted Issues

Issues discussed in this section include the re-cent evolution of the financial position of thehousehold sector and the financial performanceof the Canadian banking sector over the currenteconomic cycle.

Financial position of theCanadian household sector

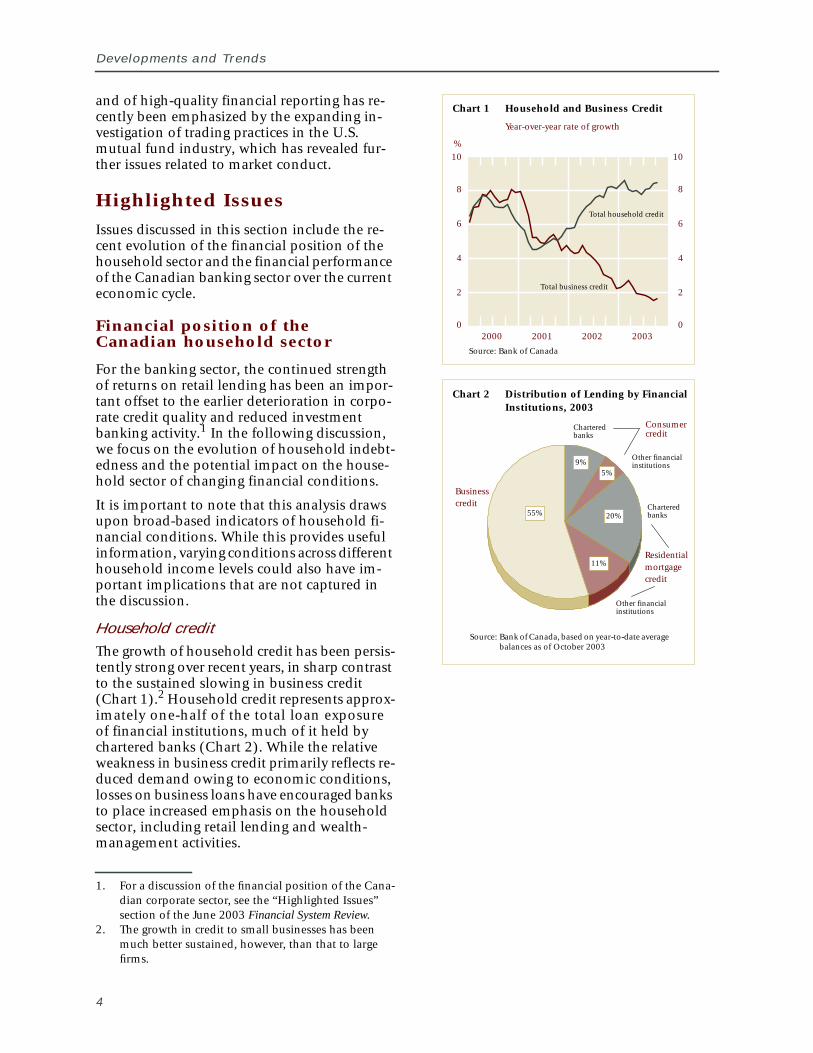

For the banking sector, the continued strengthof returns on retail lending has been an impor-tant offset to the earlier deterioration in corpo-rate credit quality and reduced investmentbanking activity.1 In the following discussion,we focus on the evolution of household indebt-edness and the potential impact on the house-hold sector of changing financial conditions.

It is important to note that this analysis drawsupon broad-based indicators of household fi-nancial conditions. While this provides usefulinformation, varying conditions across differenthousehold income levels could also have im-portant implications that are not captured inthe discussion.

Household creditThe growth of household credit has been persis-tently strong over recent years, in sharp contrastto the sustained slowing in business credit(Chart 1).2 Household credit represents approx-imately one-half of the total loan exposureof financial institutions, much of it held bychartered banks (Chart 2). While the relativeweakness in business credit primarily reflects re-duced demand owing to economic conditions,losses on business loans have encouraged banksto place increased emphasis on the householdsector, including retail lending and wealth-management activities.

1. For a discussion of the financial position of the Cana-dian corporate sector, see the “Highlighted Issues”section of the June 2003 Financial System Review.

2. The growth in credit to small businesses has beenmuch better sustained, however, than that to largefirms.

4

Financial System Review

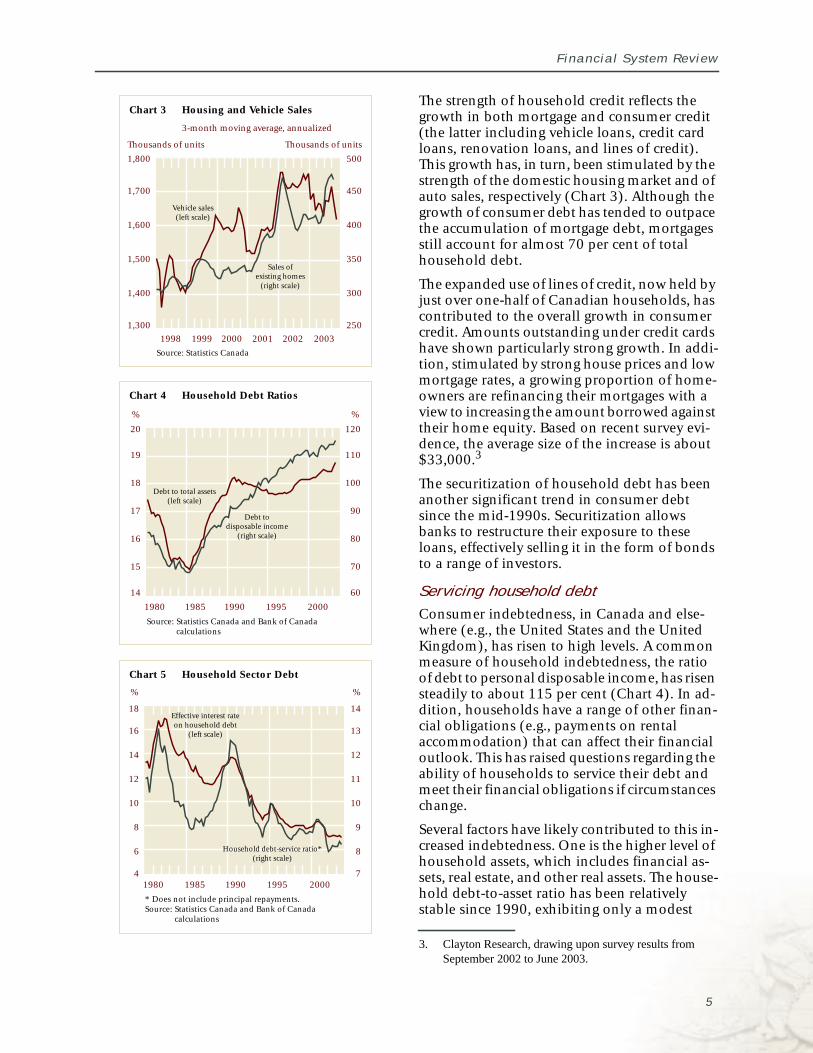

Chart 4 Household Debt Ratios

Source: Statistics Canada and Bank of Canadacalculations

14

15

16

17

18

19

20

60

70

80

90

100

110

120

1980 1985 1990 1995 2000

Debt todisposable income

(right scale)

Debt to total assets(left scale)

% %

Chart 5 Household Sector Debt

* Does not include principal repayments.Source: Statistics Canada and Bank of Canada

calculations

%

4

6

8

10

12

14

16

18

7

8

9

10

11

12

13

14

1980 1985 1990 1995 2000

Effective interest rateon household debt

(left scale)

Household debt-service ratio*(right scale)

%

Chart 3 Housing and Vehicle Sales

3-month moving average, annualized

Source: Statistics Canada

Thousands of units

1998 1999 2000 2001 2002 2003

Thousands of units

1,300

1,400

1,500

1,600

1,700

1,800

250

300

350

400

450

500

Vehicle sales(left scale)

Sales ofexisting homes

(right scale)

The strength of household credit reflects thegrowth in both mortgage and consumer credit(the latter including vehicle loans, credit cardloans, renovation loans, and lines of credit).This growth has, in turn, been stimulated by thestrength of the domestic housing market and ofauto sales, respectively (Chart 3). Although thegrowth of consumer debt has tended to outpacethe accumulation of mortgage debt, mortgagesstill account for almost 70 per cent of totalhousehold debt.

The expanded use of lines of credit, now held byjust over one-half of Canadian households, hascontributed to the overall growth in consumercredit. Amounts outstanding under credit cardshave shown particularly strong growth. In addi-tion, stimulated by strong house prices and lowmortgage rates, a growing proportion of home-owners are refinancing their mortgages with aview to increasing the amount borrowed againsttheir home equity. Based on recent survey evi-dence, the average size of the increase is about$33,000.3

The securitization of household debt has beenanother significant trend in consumer debtsince the mid-1990s. Securitization allowsbanks to restructure their exposure to theseloans, effectively selling it in the form of bondsto a range of investors.

Servicing household debtConsumer indebtedness, in Canada and else-where (e.g., the United States and the UnitedKingdom), has risen to high levels. A commonmeasure of household indebtedness, the ratioof debt to personal disposable income, has risensteadily to about 115 per cent (Chart 4). In ad-dition, households have a range of other finan-cial obligations (e.g., payments on rentalaccommodation) that can affect their financialoutlook. This has raised questions regarding theability of households to service their debt andmeet their financial obligations if circumstanceschange.

Several factors have likely contributed to this in-creased indebtedness. One is the higher level ofhousehold assets, which includes financial as-sets, real estate, and other real assets. The house-hold debt-to-asset ratio has been relativelystable since 1990, exhibiting only a modest

3. Clayton Research, drawing upon survey results fromSeptember 2002 to June 2003.

5

Developments and Trends

upward trend in recent years. Financial innova-tion and more efficient financial intermediation(between borrowers and lenders) have also fa-cilitated credit growth.

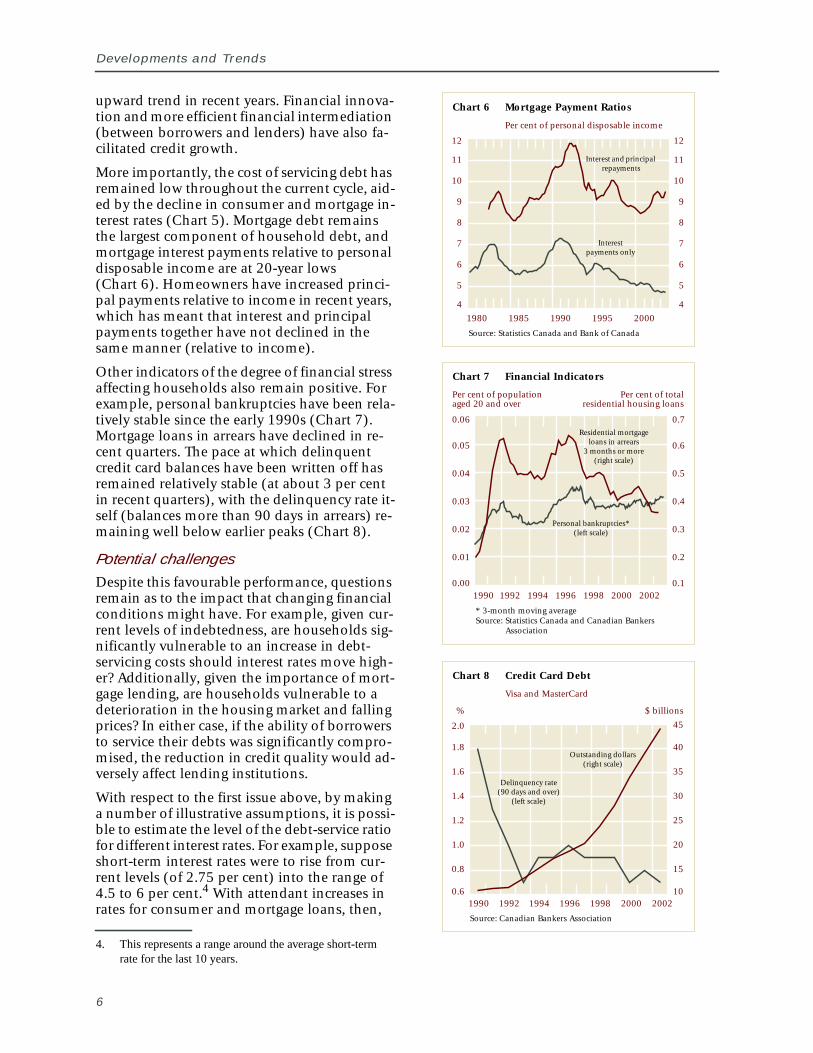

More importantly, the cost of servicing debt hasremained low throughout the current cycle, aid-ed by the decline in consumer and mortgage in-terest rates (Chart 5). Mortgage debt remainsthe largest component of household debt, andmortgage interest payments relative to personaldisposable income are at 20-year lows(Chart 6). Homeowners have increased princi-pal payments relative to income in recent years,which has meant that interest and principalpayments together have not declined in thesame manner (relative to income).

Other indicators of the degree of financial stressaffecting households also remain positive. Forexample, personal bankruptcies have been rela-tively stable since the early 1990s (Chart 7).Mortgage loans in arrears have declined in re-cent quarters. The pace at which delinquentcredit card balances have been written off hasremained relatively stable (at about 3 per centin recent quarters), with the delinquency rate it-self (balances more than 90 days in arrears) re-maining well below earlier peaks (Chart 8).

Potential challengesDespite this favourable performance, questionsremain as to the impact that changing financialconditions might have. For example, given cur-rent levels of indebtedness, are households sig-nificantly vulnerable to an increase in debt-servicing costs should interest rates move high-er? Additionally, given the importance of mort-gage lending, are households vulnerable to adeterioration in the housing market and fallingprices? In either case, if the ability of borrowersto service their debts was significantly compro-mised, the reduction in credit quality would ad-versely affect lending institutions.

With respect to the first issue above, by makinga number of illustrative assumptions, it is possi-ble to estimate the level of the debt-service ratiofor different interest rates. For example, supposeshort-term interest rates were to rise from cur-rent levels (of 2.75 per cent) into the range of4.5 to 6 per cent.4 With attendant increases inrates for consumer and mortgage loans, then,

4. This represents a range around the average short-termrate for the last 10 years.

6

Chart 6 Mortgage Payment Ratios

Per cent of personal disposable income

Source: Statistics Canada and Bank of Canada

4

5

6

7

8

9

10

11

12

4

5

6

7

8

9

10

11

12

1980 1985 1990 1995 2000

Interestpayments only

Interest and principalrepayments

Chart 8 Credit Card Debt

Visa and MasterCard

Source: Canadian Bankers Association

% $ billions

0.6

0.8

1.0

1.2

1.4

1.6

1.8

1990 1992 1994 1996 1998 2000 2002

2.0

Outstanding dollars(right scale)

Delinquency rate(90 days and over)

(left scale)

10

15

20

25

30

35

40

45

Chart 7 Financial Indicators

* 3-month moving averageSource: Statistics Canada and Canadian Bankers

Association

Per cent of populationaged 20 and over

Per cent of total residential housing loans

0.00

0.01

0.02

0.03

0.04

0.05

0.06

0.1

0.2

0.3

0.4

0.5

0.6

0.7

1990 1992 1994 1996 1998 2000 2002

Personal bankruptcies*(left scale)

Residential mortgageloans in arrears

3 months or more(right scale)

Financial System Review

under some simplifying assumptions, the debt-service ratio would climb into the correspondingrange of 8.5 to 10.5 per cent.5 Even at these lev-els, however, the debt-service ratio would re-main well below earlier peaks (recall Chart 5).

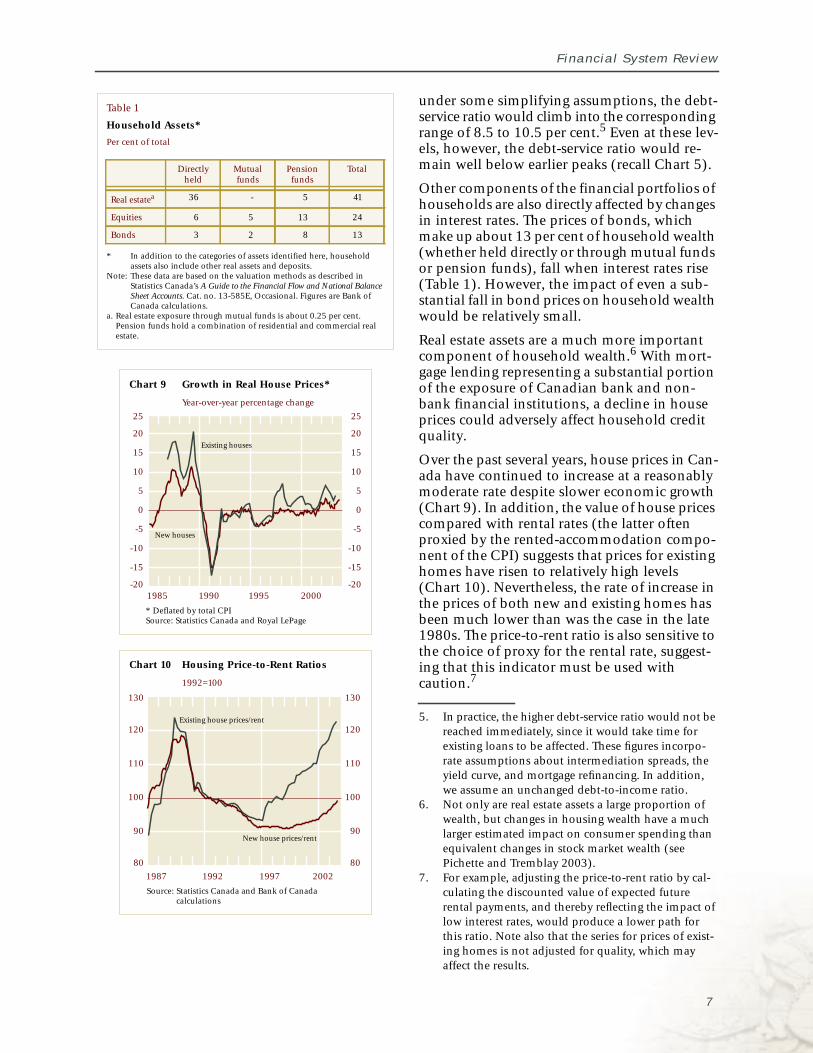

Other components of the financial portfolios ofhouseholds are also directly affected by changesin interest rates. The prices of bonds, whichmake up about 13 per cent of household wealth(whether held directly or through mutual fundsor pension funds), fall when interest rates rise(Table 1). However, the impact of even a sub-stantial fall in bond prices on household wealthwould be relatively small.

Real estate assets are a much more importantcomponent of household wealth.6 With mort-gage lending representing a substantial portionof the exposure of Canadian bank and non-bank financial institutions, a decline in houseprices could adversely affect household creditquality.

Over the past several years, house prices in Can-ada have continued to increase at a reasonablymoderate rate despite slower economic growth(Chart 9). In addition, the value of house pricescompared with rental rates (the latter oftenproxied by the rented-accommodation compo-nent of the CPI) suggests that prices for existinghomes have risen to relatively high levels(Chart 10). Nevertheless, the rate of increase inthe prices of both new and existing homes hasbeen much lower than was the case in the late1980s. The price-to-rent ratio is also sensitive tothe choice of proxy for the rental rate, suggest-ing that this indicator must be used withcaution.7

5. In practice, the higher debt-service ratio would not bereached immediately, since it would take time forexisting loans to be affected. These figures incorpo-rate assumptions about intermediation spreads, theyield curve, and mortgage refinancing. In addition,we assume an unchanged debt-to-income ratio.

6. Not only are real estate assets a large proportion ofwealth, but changes in housing wealth have a muchlarger estimated impact on consumer spending thanequivalent changes in stock market wealth (seePichette and Tremblay 2003).

7. For example, adjusting the price-to-rent ratio by cal-culating the discounted value of expected futurerental payments, and thereby reflecting the impact oflow interest rates, would produce a lower path forthis ratio. Note also that the series for prices of exist-ing homes is not adjusted for quality, which mayaffect the results.

Chart 10 Housing Price-to-Rent Ratios

1992=100

Source: Statistics Canada and Bank of Canadacalculations

80

90

100

110

120

130

80

90

100

110

120

130

1987 1992 1997 2002

Existing house prices/rent

New house prices/rent

Chart 9 Growth in Real House Prices*

Year-over-year percentage change

* Deflated by total CPISource: Statistics Canada and Royal LePage

-20

-15

-10

-5

0

5

10

15

20

25

-20

-15

-10

-5

0

5

10

15

20

25

1985 1990 1995 2000

New houses

Existing houses

Table 1

Household Assets*

Per cent of total

* In addition to the categories of assets identified here, householdassets also include other real assets and deposits.

Note: These data are based on the valuation methods as described inStatistics Canada’s A Guide to the Financial Flow and National BalanceSheet Accounts. Cat. no. 13-585E, Occasional. Figures are Bank ofCanada calculations.

a. Real estate exposure through mutual funds is about 0.25 per cent.Pension funds hold a combination of residential and commercial realestate.

Directlyheld

Mutualfunds

Pensionfunds

Total

Real estatea 36 - 5 41

Equities 6 5 13 24

Bonds 3 2 8 13

7

Developments and Trends

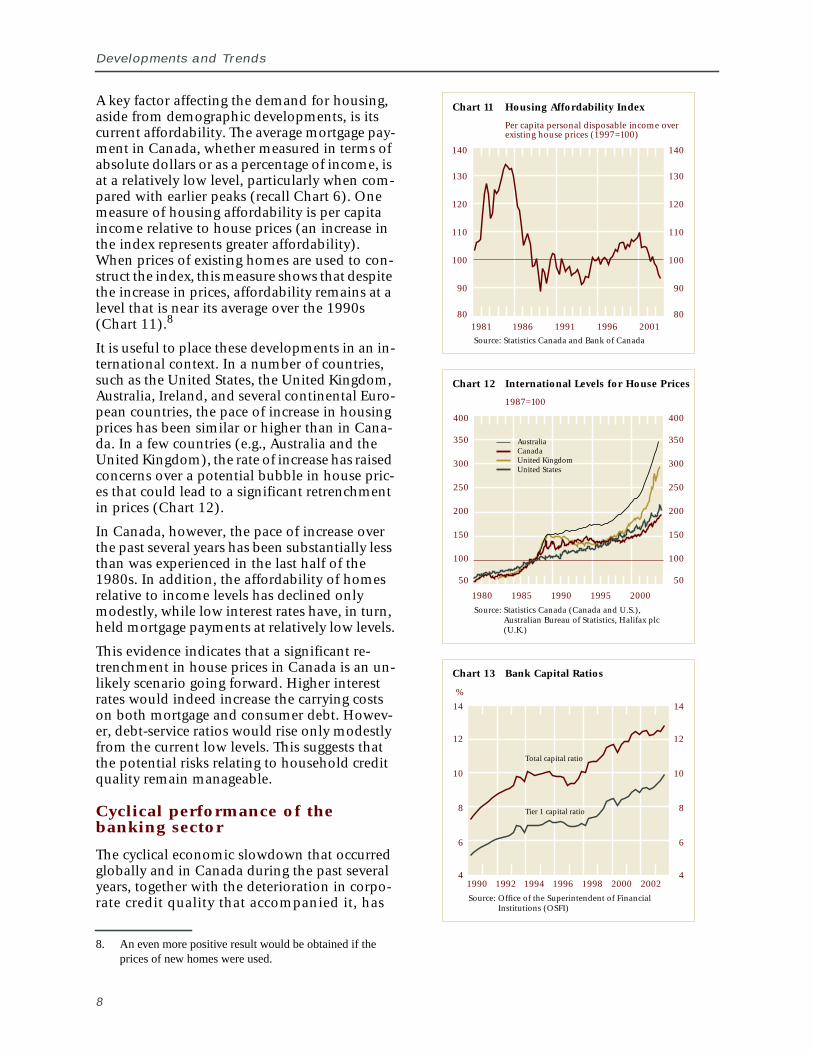

A key factor affecting the demand for housing,aside from demographic developments, is itscurrent affordability. The average mortgage pay-ment in Canada, whether measured in terms ofabsolute dollars or as a percentage of income, isat a relatively low level, particularly when com-pared with earlier peaks (recall Chart 6). Onemeasure of housing affordability is per capitaincome relative to house prices (an increase inthe index represents greater affordability).When prices of existing homes are used to con-struct the index, this measure shows that despitethe increase in prices, affordability remains at alevel that is near its average over the 1990s(Chart 11).8

It is useful to place these developments in an in-ternational context. In a number of countries,such as the United States, the United Kingdom,Australia, Ireland, and several continental Euro-pean countries, the pace of increase in housingprices has been similar or higher than in Cana-da. In a few countries (e.g., Australia and theUnited Kingdom), the rate of increase has raisedconcerns over a potential bubble in house pric-es that could lead to a significant retrenchmentin prices (Chart 12).

In Canada, however, the pace of increase overthe past several years has been substantially lessthan was experienced in the last half of the1980s. In addition, the affordability of homesrelative to income levels has declined onlymodestly, while low interest rates have, in turn,held mortgage payments at relatively low levels.

This evidence indicates that a significant re-trenchment in house prices in Canada is an un-likely scenario going forward. Higher interestrates would indeed increase the carrying costson both mortgage and consumer debt. Howev-er, debt-service ratios would rise only modestlyfrom the current low levels. This suggests thatthe potential risks relating to household creditquality remain manageable.

Cyclical performance of thebanking sector

The cyclical economic slowdown that occurredglobally and in Canada during the past severalyears, together with the deterioration in corpo-rate credit quality that accompanied it, has

8. An even more positive result would be obtained if theprices of new homes were used.

8

Chart 11 Housing Affordability Index

Per capita personal disposable income overexisting house prices (1997=100)

Source: Statistics Canada and Bank of Canada

80

90

100

110

120

130

140

80

90

100

110

120

130

140

1981 1986 1991 1996 2001

Chart 13 Bank Capital Ratios

Source: Office of the Superintendent of FinancialInstitutions (OSFI)

4

6

8

10

12

14

4

6

8

10

12

14

1990 1992 1994 1996 1998 2000 2002

%

Total capital ratio

Tier 1 capital ratio

Chart 12 International Levels for House Prices

1987=100

Source: Statistics Canada (Canada and U.S.),Australian Bureau of Statistics, Halifax plc(U.K.)

50

100

150

200

250

300

350

400

50

100

150

200

250

300

350

400

1980 1985 1990 1995 2000

AustraliaCanadaUnited KingdomUnited States

Financial System Review

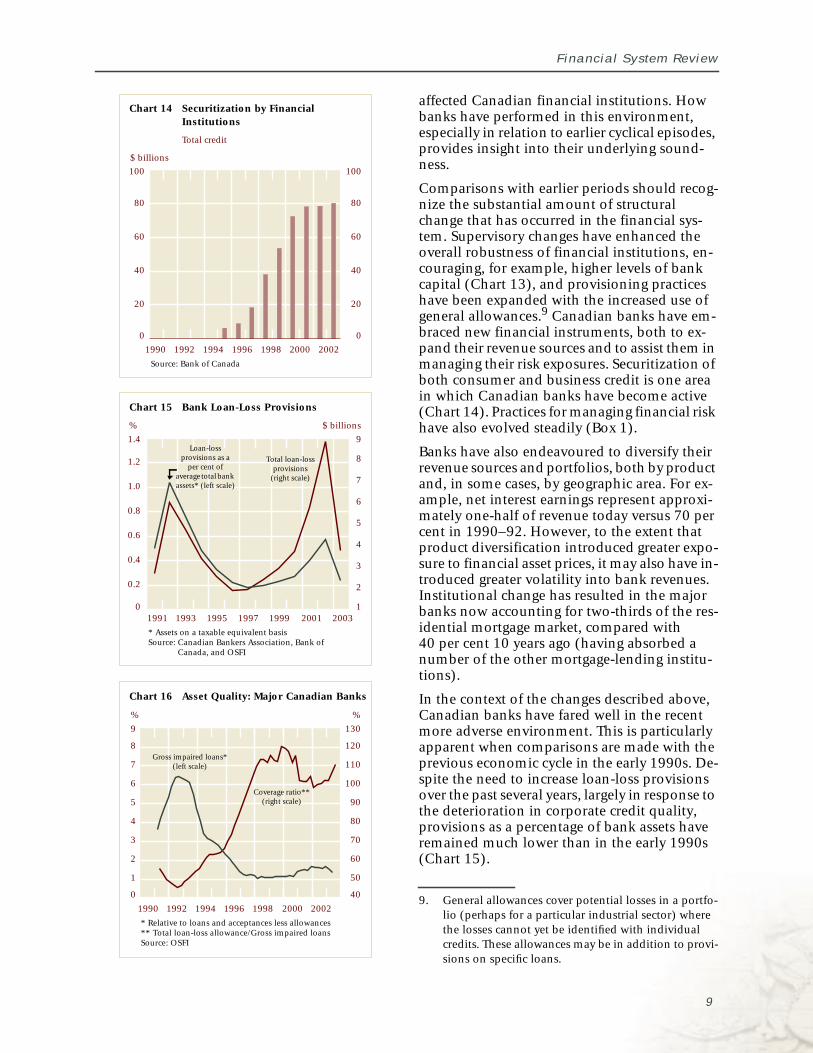

affected Canadian financial institutions. Howbanks have performed in this environment,especially in relation to earlier cyclical episodes,provides insight into their underlying sound-ness.

Comparisons with earlier periods should recog-nize the substantial amount of structuralchange that has occurred in the financial sys-tem. Supervisory changes have enhanced theoverall robustness of financial institutions, en-couraging, for example, higher levels of bankcapital (Chart 13), and provisioning practiceshave been expanded with the increased use ofgeneral allowances.9 Canadian banks have em-braced new financial instruments, both to ex-pand their revenue sources and to assist them inmanaging their risk exposures. Securitization ofboth consumer and business credit is one areain which Canadian banks have become active(Chart 14). Practices for managing financial riskhave also evolved steadily (Box 1).

Banks have also endeavoured to diversify theirrevenue sources and portfolios, both by productand, in some cases, by geographic area. For ex-ample, net interest earnings represent approxi-mately one-half of revenue today versus 70 percent in 1990–92. However, to the extent thatproduct diversification introduced greater expo-sure to financial asset prices, it may also have in-troduced greater volatility into bank revenues.Institutional change has resulted in the majorbanks now accounting for two-thirds of the res-idential mortgage market, compared with40 per cent 10 years ago (having absorbed anumber of the other mortgage-lending institu-tions).

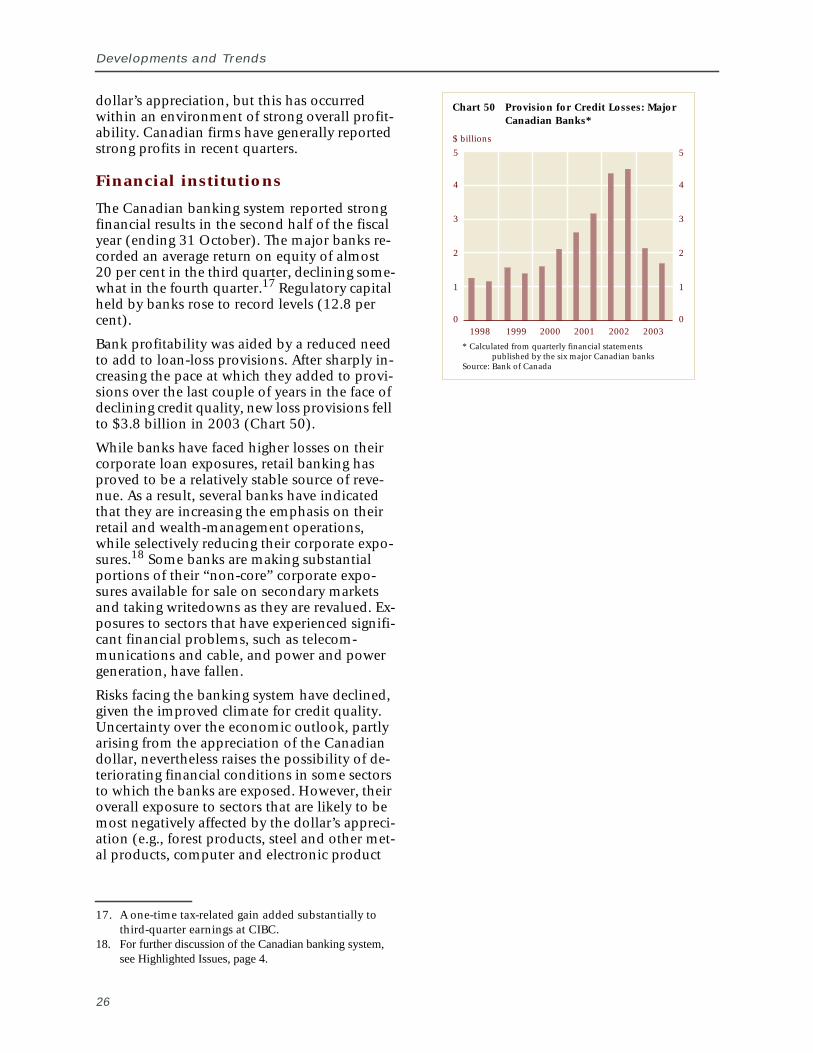

In the context of the changes described above,Canadian banks have fared well in the recentmore adverse environment. This is particularlyapparent when comparisons are made with theprevious economic cycle in the early 1990s. De-spite the need to increase loan-loss provisionsover the past several years, largely in response tothe deterioration in corporate credit quality,provisions as a percentage of bank assets haveremained much lower than in the early 1990s(Chart 15).

9. General allowances cover potential losses in a portfo-lio (perhaps for a particular industrial sector) wherethe losses cannot yet be identified with individualcredits. These allowances may be in addition to provi-sions on specific loans.

Chart 14 Securitization by FinancialInstitutions

Total credit

Source: Bank of Canada

$ billions

0

20

40

60

80

100

0

20

40

60

80

100

1990 1992 1994 1996 1998 2000 2002

Chart 15 Bank Loan-Loss Provisions

* Assets on a taxable equivalent basisSource: Canadian Bankers Association, Bank of

Canada, and OSFI

% $ billions

1991 1993 1995 1997 1999 2001 20030

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1

2

3

4

5

6

7

8

9Loan-loss

provisions as aper cent of

average totalbankassets* (left scale)

Total loan-lossprovisions

(right scale)

Chart 16 Asset Quality: Major Canadian Banks

* Relative to loans and acceptances less allowances** Total loan-loss allowance/Gross impaired loansSource: OSFI

%

0

1

2

3

4

5

6

7

8

9

40

50

60

70

80

90

100

110

120

130

1990 1992 1994 1996 1998 2000 2002

Gross impaired loans*(left scale)

Coverage ratio**(right scale)

%

9

Developments and Trends

10

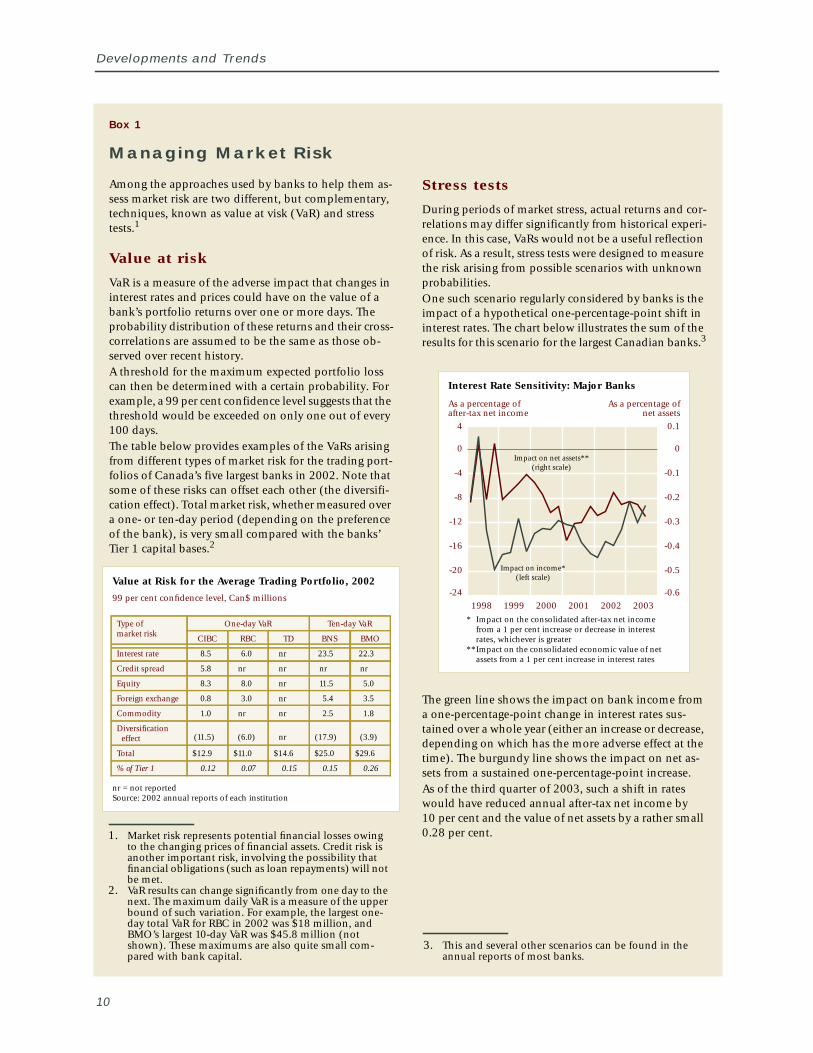

Among the approaches used by banks to help them as-sess market risk are two different, but complementary,techniques, known as value at visk (VaR) and stresstests.1

Value at risk

VaR is a measure of the adverse impact that changes ininterest rates and prices could have on the value of abank’s portfolio returns over one or more days. Theprobability distribution of these returns and their cross-correlations are assumed to be the same as those ob-served over recent history.A threshold for the maximum expected portfolio losscan then be determined with a certain probability. Forexample, a 99 per cent confidence level suggests that thethreshold would be exceeded on only one out of every100 days.The table below provides examples of the VaRs arisingfrom different types of market risk for the trading port-folios of Canada’s five largest banks in 2002. Note thatsome of these risks can offset each other (the diversifi-cation effect). Total market risk, whether measured overa one- or ten-day period (depending on the preferenceof the bank), is very small compared with the banks’Tier 1 capital bases.2

Stress tests

During periods of market stress, actual returns and cor-relations may differ significantly from historical experi-ence. In this case, VaRs would not be a useful reflectionof risk. As a result, stress tests were designed to measurethe risk arising from possible scenarios with unknownprobabilities.One such scenario regularly considered by banks is theimpact of a hypothetical one-percentage-point shift ininterest rates. The chart below illustrates the sum of theresults for this scenario for the largest Canadian banks.3

The green line shows the impact on bank income froma one-percentage-point change in interest rates sus-tained over a whole year (either an increase or decrease,depending on which has the more adverse effect at thetime). The burgundy line shows the impact on net as-sets from a sustained one-percentage-point increase.As of the third quarter of 2003, such a shift in rateswould have reduced annual after-tax net income by10 per cent and the value of net assets by a rather small0.28 per cent.

Value at Risk for the Average Trading Portfolio, 2002

99 per cent confidence level, Can$ millions

nr = not reportedSource: 2002 annual reports of each institution

Type ofmarket risk

One-day VaR Ten-day VaR

CIBC RBC TD BNS BMO

Interest rate 8.5 6.0 nr 23.5 22.3

Credit spread 5.8 nr nr nr nr

Equity 8.3 8.0 nr 11.5 5.0

Foreign exchange 0.8 3.0 nr 5.4 3.5

Commodity 1.0 nr nr 2.5 1.8

Diversificationeffect (11.5) (6.0) nr (17.9) (3.9)

Total $12.9 $11.0 $14.6 $25.0 $29.6

% of Tier 1 0.12 0.07 0.15 0.15 0.26

Interest Rate Sensitivity: Major Banks

As a percentage of As a percentage ofafter-tax net income net assets

* Impact on the consolidated after-tax net incomefrom a 1 per cent increase or decrease in interestrates, whichever is greater

**Impact on the consolidated economic value of netassets from a 1 per cent increase in interest rates

Impact on income*(left scale)

Impact on net assets**(right scale)

-24

-20

-16

-12

-8

-4

0

4

-0.6

-0.5

-0.4

-0.3

-0.2

-0.1

0

0.1

1998 1999 2000 2001 2002 2003

Box 1

Managing Market Risk

3. This and several other scenarios can be found in theannual reports of most banks.

1. Market risk represents potential financial losses owingto the changing prices of financial assets. Credit risk isanother important risk, involving the possibility thatfinancial obligations (such as loan repayments) will notbe met.

2. VaR results can change significantly from one day to thenext. The maximum daily VaR is a measure of the upperbound of such variation. For example, the largest one-day total VaR for RBC in 2002 was $18 million, andBMO’s largest 10-day VaR was $45.8 million (notshown). These maximums are also quite small com-pared with bank capital.

Financial System Review

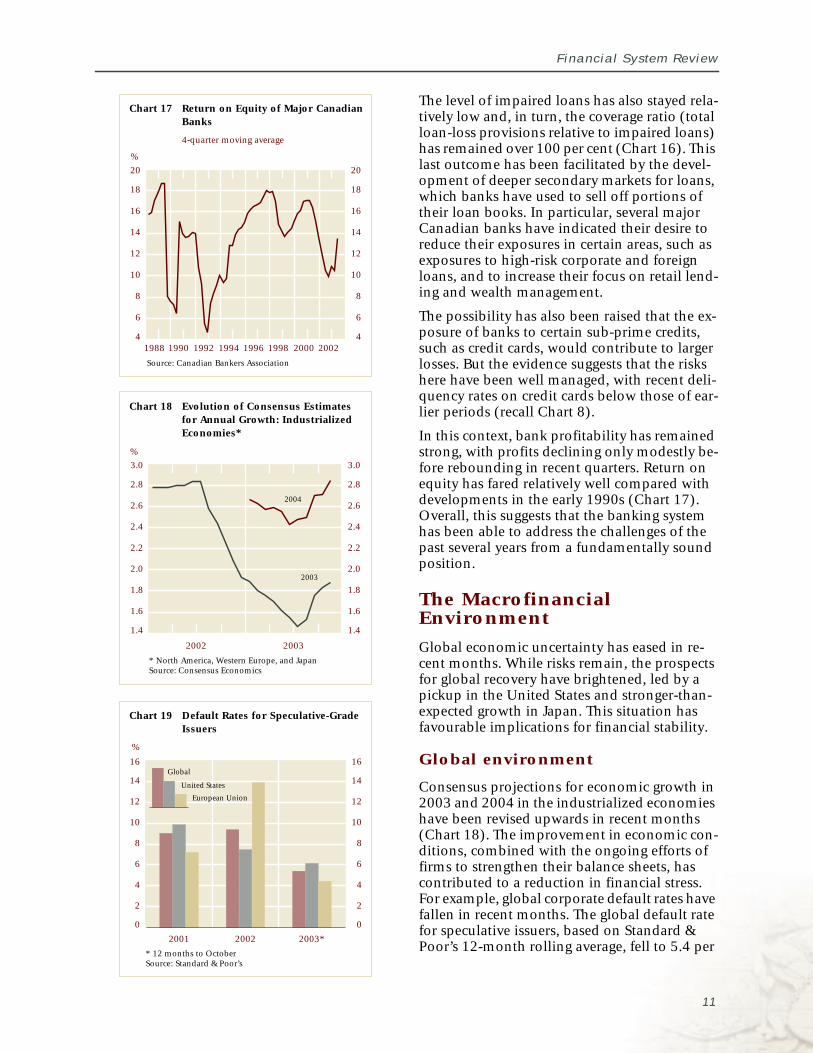

The level of impaired loans has also stayed rela-tively low and, in turn, the coverage ratio (totalloan-loss provisions relative to impaired loans)has remained over 100 per cent (Chart 16). Thislast outcome has been facilitated by the devel-opment of deeper secondary markets for loans,which banks have used to sell off portions oftheir loan books. In particular, several majorCanadian banks have indicated their desire toreduce their exposures in certain areas, such asexposures to high-risk corporate and foreignloans, and to increase their focus on retail lend-ing and wealth management.

The possibility has also been raised that the ex-posure of banks to certain sub-prime credits,such as credit cards, would contribute to largerlosses. But the evidence suggests that the riskshere have been well managed, with recent deli-quency rates on credit cards below those of ear-lier periods (recall Chart 8).

In this context, bank profitability has remainedstrong, with profits declining only modestly be-fore rebounding in recent quarters. Return onequity has fared relatively well compared withdevelopments in the early 1990s (Chart 17).Overall, this suggests that the banking systemhas been able to address the challenges of thepast several years from a fundamentally soundposition.

The MacrofinancialEnvironment

Global economic uncertainty has eased in re-cent months. While risks remain, the prospectsfor global recovery have brightened, led by apickup in the United States and stronger-than-expected growth in Japan. This situation hasfavourable implications for financial stability.

Global environment

Consensus projections for economic growth in2003 and 2004 in the industrialized economieshave been revised upwards in recent months(Chart 18). The improvement in economic con-ditions, combined with the ongoing efforts offirms to strengthen their balance sheets, hascontributed to a reduction in financial stress.For example, global corporate default rates havefallen in recent months. The global default ratefor speculative issuers, based on Standard &Poor’s 12-month rolling average, fell to 5.4 per

Chart 18 Evolution of Consensus Estimatesfor Annual Growth: IndustrializedEconomies*

Chart 17 Return on Equity of Major CanadianBanks

4-quarter moving average

Source: Canadian Bankers Association

* North America, Western Europe, and JapanSource: Consensus Economics

%

%

4

6

8

10

12

14

16

18

20

4

6

8

10

12

14

16

18

20

1988 1990 1992 1994 1996 1998 2000 2002

1.4

1.6

1.8

2.0

2.2

2.4

2.6

2.8

3.0

1.4

1.6

1.8

2.0

2.2

2.4

2.6

2.8

3.0

2002 2003

2003

2004

Chart 19 Default Rates for Speculative-GradeIssuers

* 12 months to OctoberSource: Standard & Poor’s

0

2

4

6

8

10

12

14

16

0

2

4

6

8

10

12

14

16

%

European Union

United States

Global

2001 2002 2003*

11

Developments and Trends

cent at the end of October from 9.4 per cent atthe end of last year (Chart 19). The global creditratio for downgrades per upgrade fell to 2.0 inthe third quarter, from 3.1 in the second, and4.6 in the first, and the proportion of issues un-der review for possible downgrading declined.

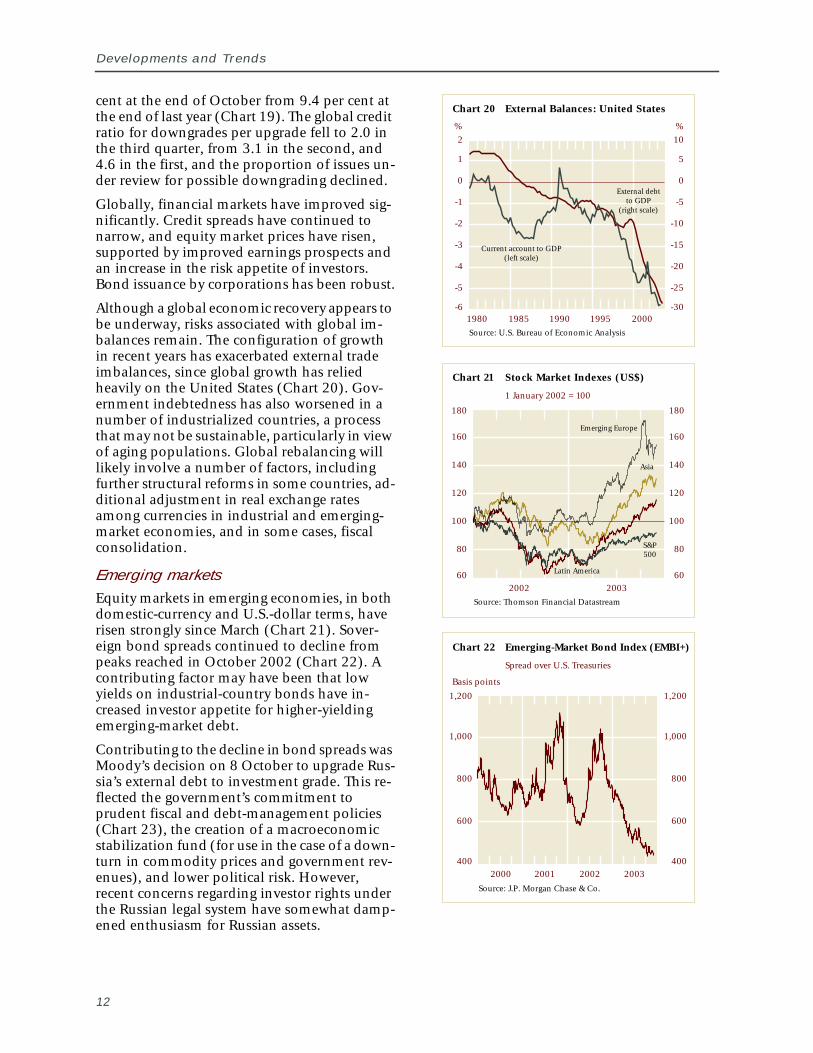

Globally, financial markets have improved sig-nificantly. Credit spreads have continued tonarrow, and equity market prices have risen,supported by improved earnings prospects andan increase in the risk appetite of investors.Bond issuance by corporations has been robust.

Although a global economic recovery appears tobe underway, risks associated with global im-balances remain. The configuration of growthin recent years has exacerbated external tradeimbalances, since global growth has reliedheavily on the United States (Chart 20). Gov-ernment indebtedness has also worsened in anumber of industrialized countries, a processthat may not be sustainable, particularly in viewof aging populations. Global rebalancing willlikely involve a number of factors, includingfurther structural reforms in some countries, ad-ditional adjustment in real exchange ratesamong currencies in industrial and emerging-market economies, and in some cases, fiscalconsolidation.

Emerging marketsEquity markets in emerging economies, in bothdomestic-currency and U.S.-dollar terms, haverisen strongly since March (Chart 21). Sover-eign bond spreads continued to decline frompeaks reached in October 2002 (Chart 22). Acontributing factor may have been that lowyields on industrial-country bonds have in-creased investor appetite for higher-yieldingemerging-market debt.

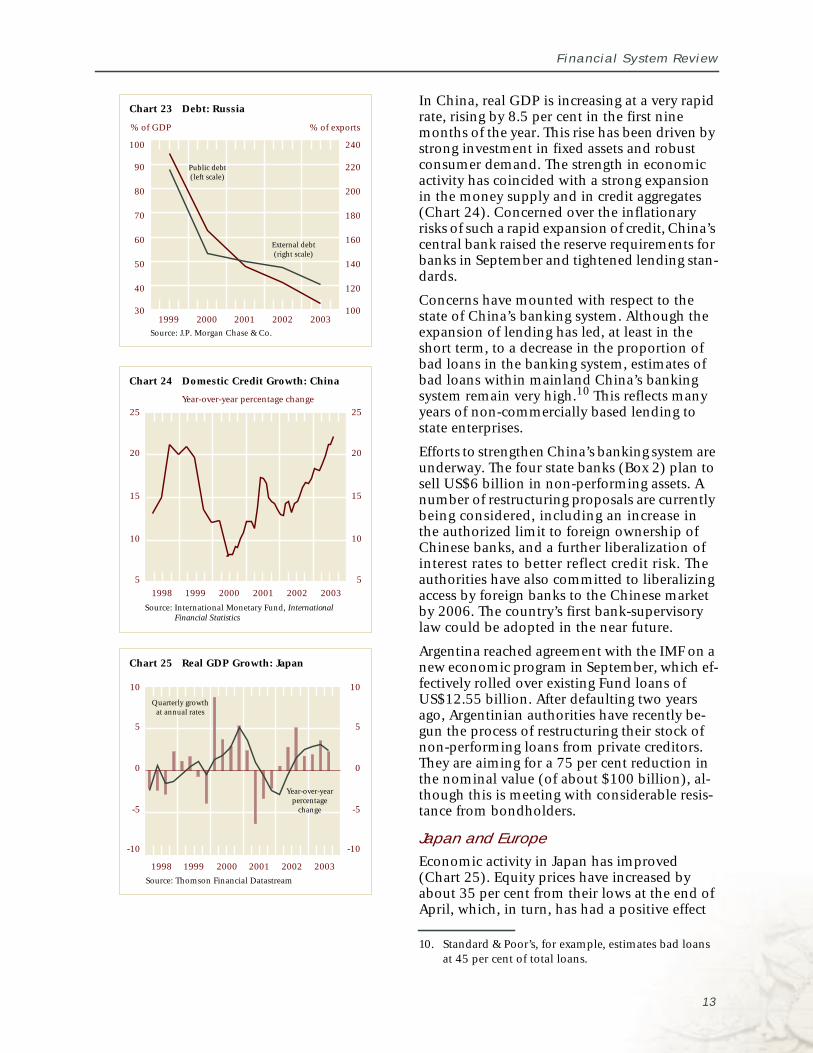

Contributing to the decline in bond spreads wasMoody’s decision on 8 October to upgrade Rus-sia’s external debt to investment grade. This re-flected the government’s commitment toprudent fiscal and debt-management policies(Chart 23), the creation of a macroeconomicstabilization fund (for use in the case of a down-turn in commodity prices and government rev-enues), and lower political risk. However,recent concerns regarding investor rights underthe Russian legal system have somewhat damp-ened enthusiasm for Russian assets.

12

Chart 20 External Balances: United States

Source: U.S. Bureau of Economic Analysis

%

-6

-5

-4

-3

-2

-1

0

1

2

-30

-25

-20

-15

-10

-5

0

5

10

1980 1985 1990 1995 2000

Current account to GDP(left scale)

External debtto GDP

(right scale)

%

Chart 21 Stock Market Indexes (US$)

1 January 2002 = 100

Source: Thomson Financial Datastream

60

80

100

120

140

160

180

60

80

100

120

140

160

180

2002 2003

Asia

Latin America

S&P500

Emerging Europe

Chart 22 Emerging-Market Bond Index (EMBI+)

Spread over U.S. Treasuries

Source: J.P. Morgan Chase & Co.

Basis points

400

600

800

1,000

1,200

400

600

800

1,000

1,200

2000 2001 2002 2003

Financial System Review

In China, real GDP is increasing at a very rapidrate, rising by 8.5 per cent in the first ninemonths of the year. This rise has been driven bystrong investment in fixed assets and robustconsumer demand. The strength in economicactivity has coincided with a strong expansionin the money supply and in credit aggregates(Chart 24). Concerned over the inflationaryrisks of such a rapid expansion of credit, China’scentral bank raised the reserve requirements forbanks in September and tightened lending stan-dards.

Concerns have mounted with respect to thestate of China’s banking system. Although theexpansion of lending has led, at least in theshort term, to a decrease in the proportion ofbad loans in the banking system, estimates ofbad loans within mainland China’s bankingsystem remain very high.10 This reflects manyyears of non-commercially based lending tostate enterprises.

Efforts to strengthen China’s banking system areunderway. The four state banks (Box 2) plan tosell US$6 billion in non-performing assets. Anumber of restructuring proposals are currentlybeing considered, including an increase inthe authorized limit to foreign ownership ofChinese banks, and a further liberalization ofinterest rates to better reflect credit risk. Theauthorities have also committed to liberalizingaccess by foreign banks to the Chinese marketby 2006. The country’s first bank-supervisorylaw could be adopted in the near future.

Argentina reached agreement with the IMF on anew economic program in September, which ef-fectively rolled over existing Fund loans ofUS$12.55 billion. After defaulting two yearsago, Argentinian authorities have recently be-gun the process of restructuring their stock ofnon-performing loans from private creditors.They are aiming for a 75 per cent reduction inthe nominal value (of about $100 billion), al-though this is meeting with considerable resis-tance from bondholders.

Japan and EuropeEconomic activity in Japan has improved(Chart 25). Equity prices have increased byabout 35 per cent from their lows at the end ofApril, which, in turn, has had a positive effect

10. Standard & Poor’s, for example, estimates bad loansat 45 per cent of total loans.

Chart 23 Debt: Russia

Source: J.P. Morgan Chase & Co.

% of GDP % of exports

1999 2000 2001 2002 2003

External debt(right scale)

Public debt(left scale)

30

40

50

60

70

80

90

100

100

120

140

160

180

200

220

240

Chart 24 Domestic Credit Growth: China

Year-over-year percentage change

Source: International Monetary Fund, InternationalFinancial Statistics

5

10

15

20

25

5

10

15

20

25

1998 1999 2000 2001 2002 2003

Chart 25 Real GDP Growth: Japan

Source: Thomson Financial Datastream

-10

-5

0

5

10

-10

-5

0

5

10

1998 1999 2000 2001 2002 2003

Quarterly growthat annual rates

Year-over-yearpercentage

change

13

14

Developments and Trends

The Chinese banking system is dominated by the “big-four” state commercial banks (SCBs): the Industrial andCommercial Bank of China, the Agricultural Bank ofChina, the Bank of China, and the China ConstructionBank. These banks have sectoral lending responsibili-ties, with the Bank of China being responsible for for-eign exchange and trade finance. The bulk of theirlending has been directed to state-owned enterprises.Together, the SCBs account for about two-thirds of thetotal assets of the country’s banking system. Four gov-ernment-owned asset-management companies were es-tablished in 1999 to facilitate the resolution of baddebts at the large state banks.

China also has three policy banks: the State Develop-ment Bank, the Export-Import Bank of China, and theAgriculture Development Bank. Their principal role isto finance infrastructure and other long-term projectssupported by the state. Their assets represent about10 per cent of total banking assets.

Ten joint-stock medium-sized commercial banks arealso in operation. In most cases, these are owned bystate enterprises or public sector entities. Four of thesebanks are listed on the domestic stock markets. In re-cent years, these institutions have expanded at a briskpace through mergers with other banks and strategic al-liances with foreign banks. The banking system also in-cludes more than 100 city commercial banks, about

30,000 rural credit co-operatives, and a host of tradeand investment corporations.

Participation by foreign banks is negligible because ofthe various restrictions they face in the conduct of theirbusiness. Foreign banks can engage in local-currencybusiness only in specific geographic areas. They are notable to take retail deposits, and lending is subject toquantity restrictions. Foreign banks are, however, ex-pected to play an increasing role in the Chinese finan-cial system in the future, following China’s accession tothe WTO. In 2004, foreign banks will be able to conductunfettered domestic-currency business with Chineseenterprises, and geographic restrictions will be lifted. In2007, they will be able to conduct local-currency busi-ness with Chinese individuals and will have full nation-al treatment.

In recent years, foreign banks have tried to increase theirpenetration of the Chinese banking market. In Decem-ber 2001, the HSBC and the International Finance Cor-poration (IFC), the private investment arm of the WorldBank, bought, respectively, 8 and 5 per cent of the Bankof Shanghai, one of the largest city commercial banks.The IFC recently bought a 1.6 per cent stake in the Min-sheng Bank, the only privately owned bank in China.China’s banking regulator will allow foreign banks tohold up to 25 per cent of a Chinese bank in the future,compared with the current limit of 15 per cent.

Box 2

The Structure of the Chinese Banking System

Chart 26 Gross Financial Liabilities: GeneralGovernment

Per cent of GDP

Source: Organisation for Economic Co-operation andDevelopment

40

60

80

100

120

140

160

40

60

80

100

120

140

160

1990 1995 2000

United States

Japan

Euro area

on bank profitability (since banks hold a largeamount of shares in non-financial corpora-tions). Corporate bankruptcies have generallydeclined, and credit downgrades in the thirdquarter were lower than a year ago. The situa-tion remains difficult, however, with most ob-servers expecting only modest growth over themedium term accompanied by persistent defla-tion. Government indebtedness is rising rapid-ly, a situation that does not appear sustainableover the longer term (Chart 26).

Efforts to revitalize the banking sector continue.Many of Japan’s largest banks have announcedplans to improve internal efficiency and reducetheir workforce. The Bank of Japan has also an-nounced plans to extend its program of pur-chasing stocks from banks to help improve theirbalance sheets. At the end of September, howev-er, the Industrial Revitalisation Corporation an-nounced that its own appraisal of assets used ascollateral by the six problem borrowers it has

Financial System Review

Chart 28 Real GDP Growth: United States

Chart 29 Corporate Profit: United States

Profit as a share of GDP

Chart 27 House Price Index: United Kingdom

Year-over-year percentage change

Source: Halifax plc

Source: U.S. Bureau of Economic Analysis

Source: Thomson Financial Datastream

-10

0

10

20

30

40

-10

0

10

20

30

40

1987 1992 1997 2002

-2

0

2

4

6

8

10

-2

0

2

4

6

8

10

1998 1999 2000 2001 2002 2003

3

4

5

6

7

3

4

5

6

7

1990 1992 1994 1996 1998 2000 2002

Quarterly growth atannual rates

Year-over-yearpercentage change

agreed to support was lower than the assess-ment of the original lending banks. This mayimply the need for further increases to loan-lossreserves. At the end of November, the govern-ment nationalized Ashikaga Bank.

Economic activity in Europe remains weak, withonly limited growth in the euro zone in the lastthree quarters. This has contributed to ongoingpressure on the European corporate sector.Credit downgrades continued to outpace up-grades by a wide margin in the third quarter.Twenty-five per cent of the companies rated atthe parent level in Europe were listed with anegative bias, a proportion similar to the situa-tion last year. Owing to Germany’s weak econo-my and the pressures on its banking sector,some corporations there are experiencing in-creased difficulty in obtaining bank loans.

In the United Kingdom, the rate of increase inhousing prices continues to moderate (Chart 27).Nevertheless, concerns over a possible bubblein this sector remain (recall Chart 12). Sincepersonal debt is at an elevated level, a signifi-cant decline in house prices could have animportant adverse impact on the financial healthof the household sector.

The European insurance sector has come underconsiderable pressure in recent years, owingpartly to lower valuations for equity assets andhigher insurance payments. This has been re-flected in a series of credit-rating downgrades,with Standard & Poor’s and Fitch recentlydowngrading the large German reinsurer Mu-nich Re. The German government announcedthat it would provide support to domestic insur-ers by allowing them to deduct from taxes theirlosses on equities. More generally, insurancecompanies have moved to raise additional cap-ital to buttress their financial positions.

United StatesEconomic activity in the United States strength-ened considerably in the third quarter (Chart 28).Although some of this rebound may reflect tempo-rary factors, such as a large contribution fromrecent tax relief, analysts have become moreconfident about the possibility of a sustainedrecovery. Corporate profits have risen signifi-cantly (Chart 29), and there is some evidenceof a turnaround in employment.

U.S. corporations continue to improve theirbalance sheets. Total liabilities as a per cent of

15

Developments and Trends

Chart 30 Household Debt: United States

Per cent of personal disposable income

Source: U.S. Federal Reserve Board

10

12

14

16

18

20

10

12

14

16

18

20

1980 1985 1990 1995 2000

Debt-service payments

Financial obligations

Chart 31 Return on Assets: All InstitutionsInsured by the FDIC

Source: U.S. Federal Deposit Insurance Corporation

0.8

1.0

1.2

1.4

0.8

1.0

1.2

1.4

1992 1997 2002

%

Table 2

Largest U.S. Banks (by assets)

As of 31 December 2002

Source: U.S. Federal Deposit Insurance Corporation

$billion

Citigroup 1,097

Bank of America/FleetBoston 851

J.P. Morgan Chase & Co. 759

Wells Fargo 349

Wachovia 341

Per cent of total bank assets 48

cash flow have declined recently, although theratio remains elevated by historical standards.

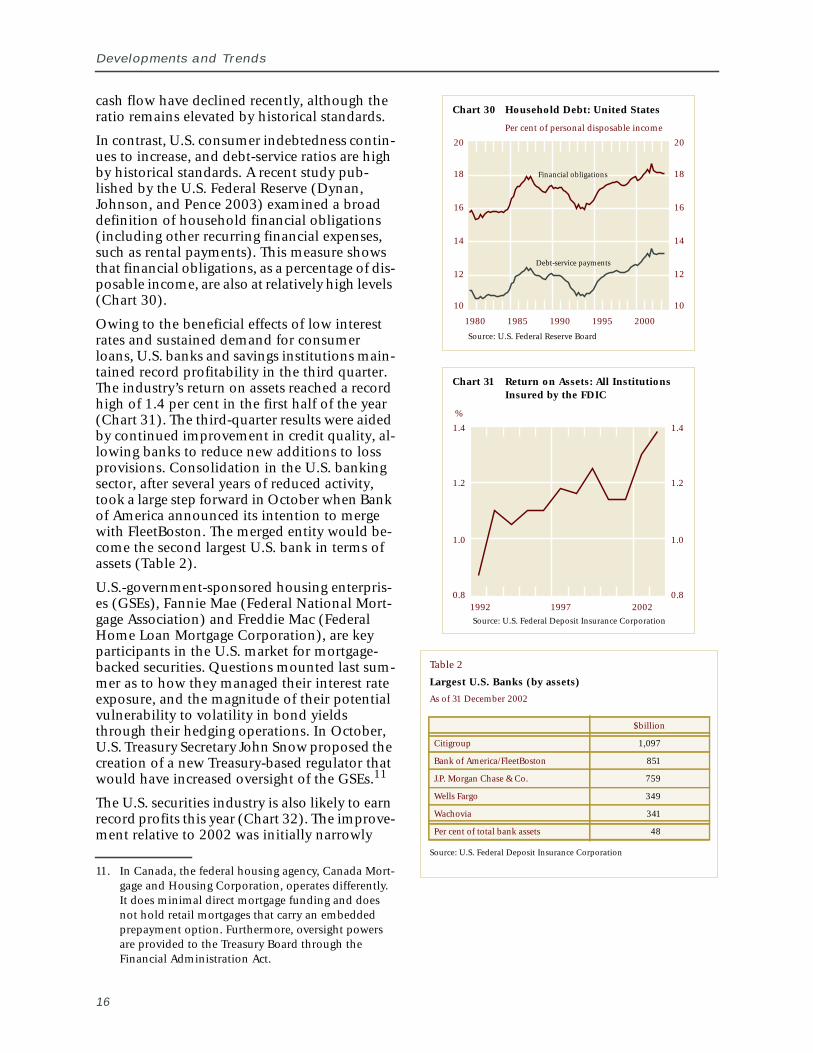

In contrast, U.S. consumer indebtedness contin-ues to increase, and debt-service ratios are highby historical standards. A recent study pub-lished by the U.S. Federal Reserve (Dynan,Johnson, and Pence 2003) examined a broaddefinition of household financial obligations(including other recurring financial expenses,such as rental payments). This measure showsthat financial obligations, as a percentage of dis-posable income, are also at relatively high levels(Chart 30).

Owing to the beneficial effects of low interestrates and sustained demand for consumerloans, U.S. banks and savings institutions main-tained record profitability in the third quarter.The industry’s return on assets reached a recordhigh of 1.4 per cent in the first half of the year(Chart 31). The third-quarter results were aidedby continued improvement in credit quality, al-lowing banks to reduce new additions to lossprovisions. Consolidation in the U.S. bankingsector, after several years of reduced activity,took a large step forward in October when Bankof America announced its intention to mergewith FleetBoston. The merged entity would be-come the second largest U.S. bank in terms ofassets (Table 2).

U.S.-government-sponsored housing enterpris-es (GSEs), Fannie Mae (Federal National Mort-gage Association) and Freddie Mac (FederalHome Loan Mortgage Corporation), are keyparticipants in the U.S. market for mortgage-backed securities. Questions mounted last sum-mer as to how they managed their interest rateexposure, and the magnitude of their potentialvulnerability to volatility in bond yieldsthrough their hedging operations. In October,U.S. Treasury Secretary John Snow proposed thecreation of a new Treasury-based regulator thatwould have increased oversight of the GSEs.11

The U.S. securities industry is also likely to earnrecord profits this year (Chart 32). The improve-ment relative to 2002 was initially narrowly

11. In Canada, the federal housing agency, Canada Mort-gage and Housing Corporation, operates differently.It does minimal direct mortgage funding and doesnot hold retail mortgages that carry an embeddedprepayment option. Furthermore, oversight powersare provided to the Treasury Board through theFinancial Administration Act.

16

Financial System Review

Chart 32 Securities Industry: United States

NYSE member broker-dealers

Source: U.S. Securities Industry Association

US$ billions US$ billions

-5

0

5

10

15

20

25

30

-50

0

50

100

150

200

250

300

1990 1995 2000

Annualpre-tax profits

(left scale)

Annualgross revenue(right scale)

based (particularly in bond trading and issu-ance), but in the third quarter there wasevidence that revenue growth has broadened.

Corporate governance and financialoversightEfforts to increase investor confidence in finan-cial reporting and auditing standards are beingundertaken globally. In July, an internationaltask force, commissioned by the InternationalFederation of Accountants (IFAC) and chairedby John Crow, former Governor of the Bank ofCanada, released its report, Rebuilding PublicConfidence in Financial Reporting: An Interna-tional Perspective. The report stresses that recentfinancial scandals are symptoms of deeperproblems and proposes a range of actions to ad-dress low credibility in financial reporting.12

The International Accounting Standards Board(IASB) and U.S. Financial Accounting StandardsBoard (FASB) are spearheading efforts to bringabout greater convergence in global accountingrules. The IASB met with U.S. and Canadian of-ficials in October to review progress, but it isgenerally accepted that the process will take sev-eral years. The FASB will soon release proposedaccounting changes that would bring U.S. rulesmore closely in line with international stan-dards.

To promote confidence in global auditing stan-dards, a new Public Interest Oversight Boardwill be established to monitor the internationalauditing standards established by the IFAC’s In-ternational Auditing and Assurance StandardsBoard.

In the United States, hedge funds and mutualfunds, both of which have become increasinglyimportant investment vehicles, have come un-der increased scrutiny. A staff report from theSecurities and Exchange Commission (SEC) re-cently recommended that hedge-fund managersbe required to register with the SEC as invest-ment advisers. The hedge funds would thenhave to provide information to the SEC thatcould be used to conduct audits.

12. Appendix 3 of the report contains a useful summaryof the international initiatives that have been under-taken. A more recent summary of Canadian initia-tives may be found in the article by Armstrong,page 53 of this Review.

17

Developments and Trends

Chart 33 Aggregate Funded Status forS&P 500 Companies: OtherRetirement Benefits*

Deficit

* Excludes pension plansSource: CSFB Research

$ billions

0

50

100

150

200

250

300

350

0

50

100

150

200

250

300

350

2000 2001 2002

Chart 35 Pension Underfunding:United States

Insured single-employer plans

* e = estimate for 2003Source: U.S. Pension Benefit Guaranty Corporation

US$ billions

0

50

100

150

200

250

300

350

400

450

0

50

100

150

200

250

300

350

400

450

1998 1999 2000 2001 2002 2003

e*

Chart 34 Mercer Pension Health Index:Canada

Ratio of assets to liabilities

Source: Mercer Human Resource Consulting Limited

80

90

100

110

120

130

80

90

100

110

120

130

1998 1999 2000 2001 2002 2003

%

The U.S. mutual fund industry has also comeunder investigation as a result of questionablesales and trading practices. The investigationshave led to a number of internal company au-dits to identify the scope of these activities, andsome firms have set aside funds to cover thecosts of litigation and potential investor restitu-tion. In some cases, large investors have re-leased specific mutual fund companies fromtheir investment advisory roles, but the overallimpact on investor confidence is not yet clear.There is a broadening array of proposals regard-ing improved oversight of the mutual fund in-dustry.

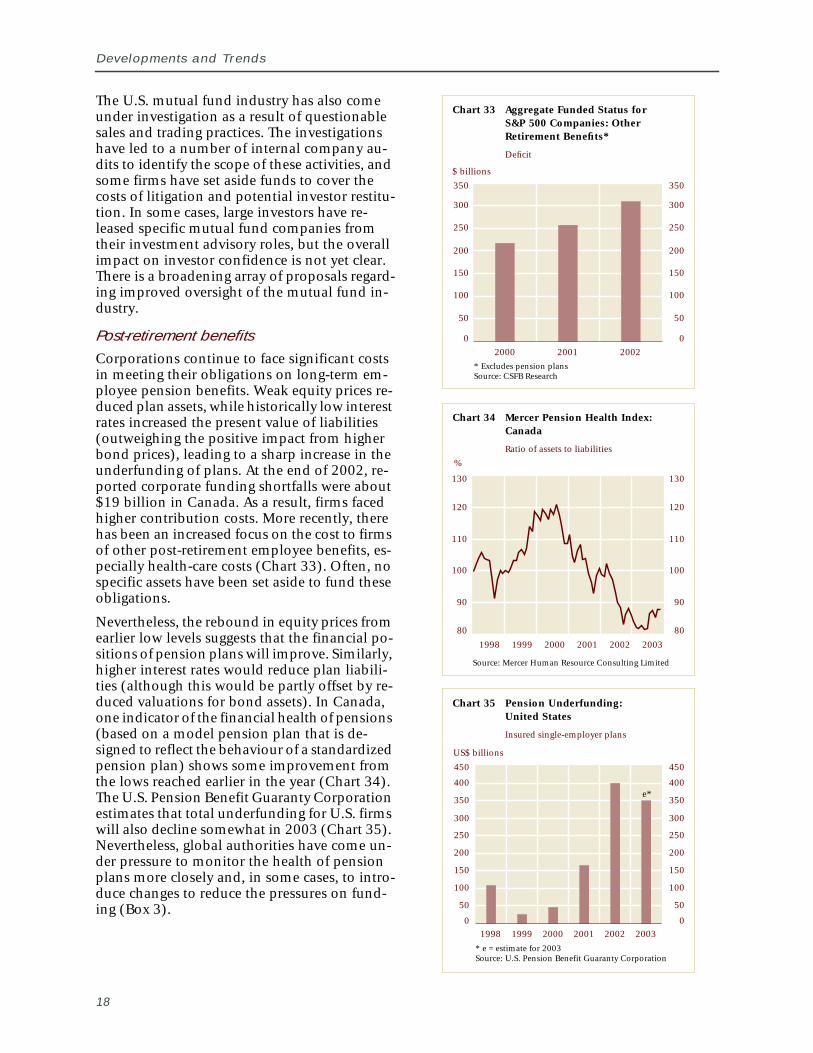

Post-retirement benefitsCorporations continue to face significant costsin meeting their obligations on long-term em-ployee pension benefits. Weak equity prices re-duced plan assets, while historically low interestrates increased the present value of liabilities(outweighing the positive impact from higherbond prices), leading to a sharp increase in theunderfunding of plans. At the end of 2002, re-ported corporate funding shortfalls were about$19 billion in Canada. As a result, firms facedhigher contribution costs. More recently, therehas been an increased focus on the cost to firmsof other post-retirement employee benefits, es-pecially health-care costs (Chart 33). Often, nospecific assets have been set aside to fund theseobligations.

Nevertheless, the rebound in equity prices fromearlier low levels suggests that the financial po-sitions of pension plans will improve. Similarly,higher interest rates would reduce plan liabili-ties (although this would be partly offset by re-duced valuations for bond assets). In Canada,one indicator of the financial health of pensions(based on a model pension plan that is de-signed to reflect the behaviour of a standardizedpension plan) shows some improvement fromthe lows reached earlier in the year (Chart 34).The U.S. Pension Benefit Guaranty Corporationestimates that total underfunding for U.S. firmswill also decline somewhat in 2003 (Chart 35).Nevertheless, global authorities have come un-der pressure to monitor the health of pensionplans more closely and, in some cases, to intro-duce changes to reduce the pressures on fund-ing (Box 3).

18

19

Financial System Review

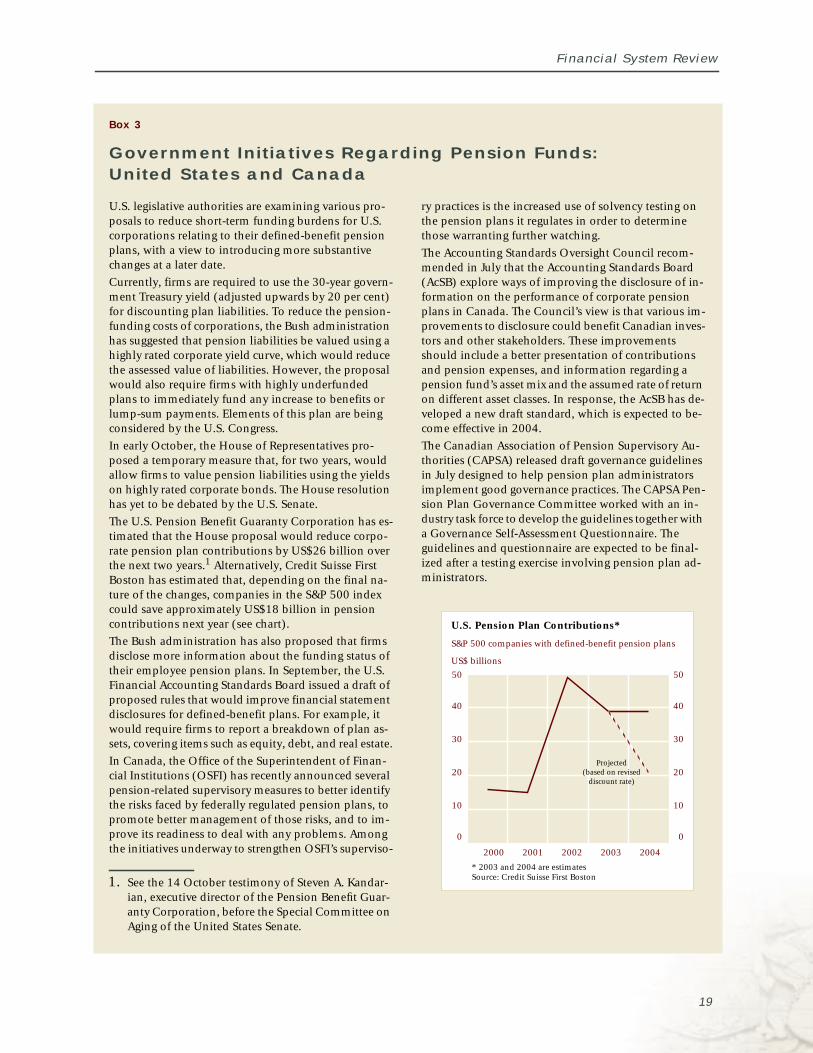

U.S. legislative authorities are examining various pro-posals to reduce short-term funding burdens for U.S.corporations relating to their defined-benefit pensionplans, with a view to introducing more substantivechanges at a later date.

Currently, firms are required to use the 30-year govern-ment Treasury yield (adjusted upwards by 20 per cent)for discounting plan liabilities. To reduce the pension-funding costs of corporations, the Bush administrationhas suggested that pension liabilities be valued using ahighly rated corporate yield curve, which would reducethe assessed value of liabilities. However, the proposalwould also require firms with highly underfundedplans to immediately fund any increase to benefits orlump-sum payments. Elements of this plan are beingconsidered by the U.S. Congress.

In early October, the House of Representatives pro-posed a temporary measure that, for two years, wouldallow firms to value pension liabilities using the yieldson highly rated corporate bonds. The House resolutionhas yet to be debated by the U.S. Senate.

The U.S. Pension Benefit Guaranty Corporation has es-timated that the House proposal would reduce corpo-rate pension plan contributions by US$26 billion overthe next two years.1 Alternatively, Credit Suisse FirstBoston has estimated that, depending on the final na-ture of the changes, companies in the S&P 500 indexcould save approximately US$18 billion in pensioncontributions next year (see chart).

The Bush administration has also proposed that firmsdisclose more information about the funding status oftheir employee pension plans. In September, the U.S.Financial Accounting Standards Board issued a draft ofproposed rules that would improve financial statementdisclosures for defined-benefit plans. For example, itwould require firms to report a breakdown of plan as-sets, covering items such as equity, debt, and real estate.

In Canada, the Office of the Superintendent of Finan-cial Institutions (OSFI) has recently announced severalpension-related supervisory measures to better identifythe risks faced by federally regulated pension plans, topromote better management of those risks, and to im-prove its readiness to deal with any problems. Amongthe initiatives underway to strengthen OSFI’s superviso-

ry practices is the increased use of solvency testing onthe pension plans it regulates in order to determinethose warranting further watching.

The Accounting Standards Oversight Council recom-mended in July that the Accounting Standards Board(AcSB) explore ways of improving the disclosure of in-formation on the performance of corporate pensionplans in Canada. The Council’s view is that various im-provements to disclosure could benefit Canadian inves-tors and other stakeholders. These improvementsshould include a better presentation of contributionsand pension expenses, and information regarding apension fund’s asset mix and the assumed rate of returnon different asset classes. In response, the AcSB has de-veloped a new draft standard, which is expected to be-come effective in 2004.

The Canadian Association of Pension Supervisory Au-thorities (CAPSA) released draft governance guidelinesin July designed to help pension plan administratorsimplement good governance practices. The CAPSA Pen-sion Plan Governance Committee worked with an in-dustry task force to develop the guidelines together witha Governance Self-Assessment Questionnaire. Theguidelines and questionnaire are expected to be final-ized after a testing exercise involving pension plan ad-ministrators.

U.S. Pension Plan Contributions*

S&P 500 companies with defined-benefit pension plans

* 2003 and 2004 are estimatesSource: Credit Suisse First Boston

US$ billions

0

10

20

30

40

50

0

10

20

30

40

50

2000 2001 2002 2003 2004

Projected(based on revised

discount rate)

Box 3

Government Initiatives Regarding Pension Funds:United States and Canada

1. See the 14 October testimony of Steven A. Kandar-ian, executive director of the Pension Benefit Guar-anty Corporation, before the Special Committee onAging of the United States Senate.

Developments and Trends

Canadian developments

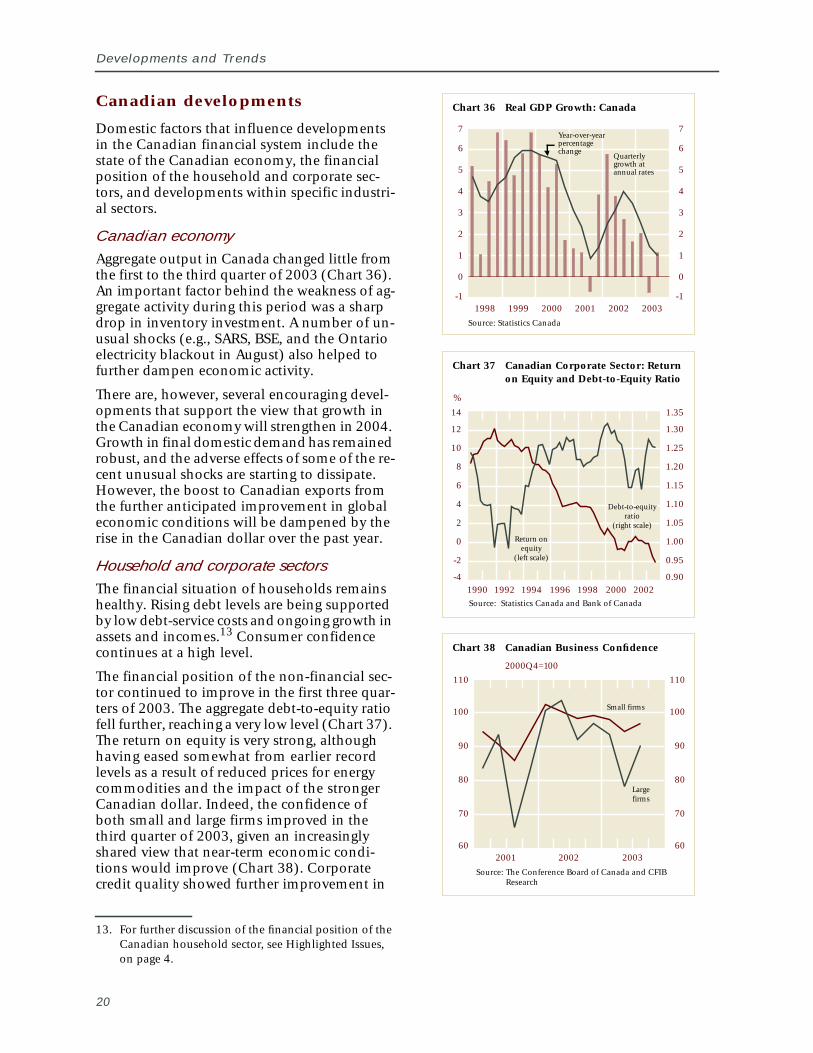

Domestic factors that influence developmentsin the Canadian financial system include thestate of the Canadian economy, the financialposition of the household and corporate sec-tors, and developments within specific industri-al sectors.

Canadian economyAggregate output in Canada changed little fromthe first to the third quarter of 2003 (Chart 36).An important factor behind the weakness of ag-gregate activity during this period was a sharpdrop in inventory investment. A number of un-usual shocks (e.g., SARS, BSE, and the Ontarioelectricity blackout in August) also helped tofurther dampen economic activity.

There are, however, several encouraging devel-opments that support the view that growth inthe Canadian economy will strengthen in 2004.Growth in final domestic demand has remainedrobust, and the adverse effects of some of the re-cent unusual shocks are starting to dissipate.However, the boost to Canadian exports fromthe further anticipated improvement in globaleconomic conditions will be dampened by therise in the Canadian dollar over the past year.

Household and corporate sectorsThe financial situation of households remainshealthy. Rising debt levels are being supportedby low debt-service costs and ongoing growth inassets and incomes.13 Consumer confidencecontinues at a high level.

The financial position of the non-financial sec-tor continued to improve in the first three quar-ters of 2003. The aggregate debt-to-equity ratiofell further, reaching a very low level (Chart 37).The return on equity is very strong, althoughhaving eased somewhat from earlier recordlevels as a result of reduced prices for energycommodities and the impact of the strongerCanadian dollar. Indeed, the confidence ofboth small and large firms improved in thethird quarter of 2003, given an increasinglyshared view that near-term economic condi-tions would improve (Chart 38). Corporatecredit quality showed further improvement in

13. For further discussion of the financial position of theCanadian household sector, see Highlighted Issues,on page 4.

20

Chart 36 Real GDP Growth: Canada

Source: Statistics Canada

-1

0

1

2

3

4

5

6

7

-1

0

1

2

3

4

5

6

7

1998 1999 2000 2001 2002 2003

Year-over-yearpercentagechange

Quarterlygrowth atannual rates

Chart 37 Canadian Corporate Sector: Returnon Equity and Debt-to-Equity Ratio

Source: Statistics Canada and Bank of Canada

1990 1992 1994 1996 1998 2000 2002

%

-4

-2

0

2

4

6

8

10

12

14

0.90

0.95

1.00

1.05

1.10

1.15

1.20

1.25

1.30

1.35

Debt-to-equityratio

(right scale)

Return onequity

(left scale)

Chart 38 Canadian Business Confidence

2000Q4=100

Source: The Conference Board of Canada and CFIBResearch

60

70

80

90

100

110

60

70

80

90

100

110

2001 2002 2003

Largefirms

Small firms

Financial System Review

Chart 39 Credit-Rating Downgrades: Canada

Source: Moody’s and Standard & Poor’s

0

5

10

15

20

0

5

10

15

20

2001 2002 2003

Moody’s

Standard & Poor’s

Chart 40 Farm Cash Receipts

Cattle and calves

Chart 41 Real Output Growth: Steel

Source: Statistics Canada

Source: Statistics Canada

$ billions

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

1998 1999 2000 2001 2002 2003

-20

30

-20

-10

0

10

20

30

1998 1999 2000 2001 2002 2003

Year-over-yearpercentage

change

Quarterly growth atannual rates

-10

0

10

20

the third quarter, as the number of companiesdowngraded continued to decline, with few de-faults recorded to date in 2003 (Chart 39).

IndustryAlthough the financial condition of the overallnon-financial corporate sector is relativelyhealthy, some industries continue to be underfinancial stress. Activity levels and profitabilityin the airline and aerospace manufacturing in-dustries fell sharply in the second quarter fromalready-low levels, mainly owing to the adverseeconomic effects of the SARS outbreak. As a re-sult, some firms in these industries are restruc-turing their operations and balance sheets.More recently, there has been a partial recoveryof activity in the airline industry.

The financial situation in Canada’s livestocksector has also deteriorated, following the ap-pearance of one case of BSE in Alberta(Chart 40). However, a number of countrieshave partially lifted the ban on Canadian beefproducts since early August.

The financial positions of many of those sectorswith a strong net export orientation continue to beadversely affected by the appreciation of the Cana-dian dollar. In particular, the rise in the value ofthe Canadian dollar is likely to have an especiallysignificant negative impact on the profitability ofhigh-tech manufacturing industries. Indeed, prof-itability in the electronic and computer manufac-turing industry deteriorated in the third quarter of2003, with manufacturers of telecommunicationsequipment still facing weak demand.

As well, steel manufacturers have seen their fi-nancial positions worsen considerably(Chart 41), given weak demand and prices, thestrong dollar, and high costs for raw materialsand energy. While producers of non-ferrousmetals and forest products would typically ben-efit from the marked increase in global pricesfor both non-ferrous metals and lumber, a ma-jor offsetting factor has been the appreciation ofthe Canadian dollar.

The near-term financial prospects of NorthAmerican automakers remain weak owing toglobal excess capacity, the high cost of sales in-centives, and the need to shore up their pensionplans. Credit ratings have come under down-ward pressure.14

14. In recent months, the credit ratings of Ford andDaimlerChrysler have been downgraded.

21

Developments and Trends

Chart 42 Yield for 10-Year Benchmark Bonds

Source: Thomson Financial Datastream

%

2

4

6

8

10

12

2

4

6

8

10

12

1990 1996 2000 2003

UnitedStates

1992 1994 1998 2002

Canada

Chart 43 Global Bond Markets: Total Returns

Year-over-year percentage change

Source: Bank of Canada calculations

-15

-10

-5

0

5

10

15

-15

-10

-5

0

5

10

15

U.S. Canada Germany U.K. Japan

14 April 2003 to13 June 2003

13 June 2003 to2 September 2003

Chart 44 Spreads on Investment-GradeSecurities: Canada

Source: Merrill Lynch

A

AA

BBB

Basis points

0

50

100

150

200

250

300

350

0

50

100

150

200

250

300

350

2001 2002 2003

The Financial System

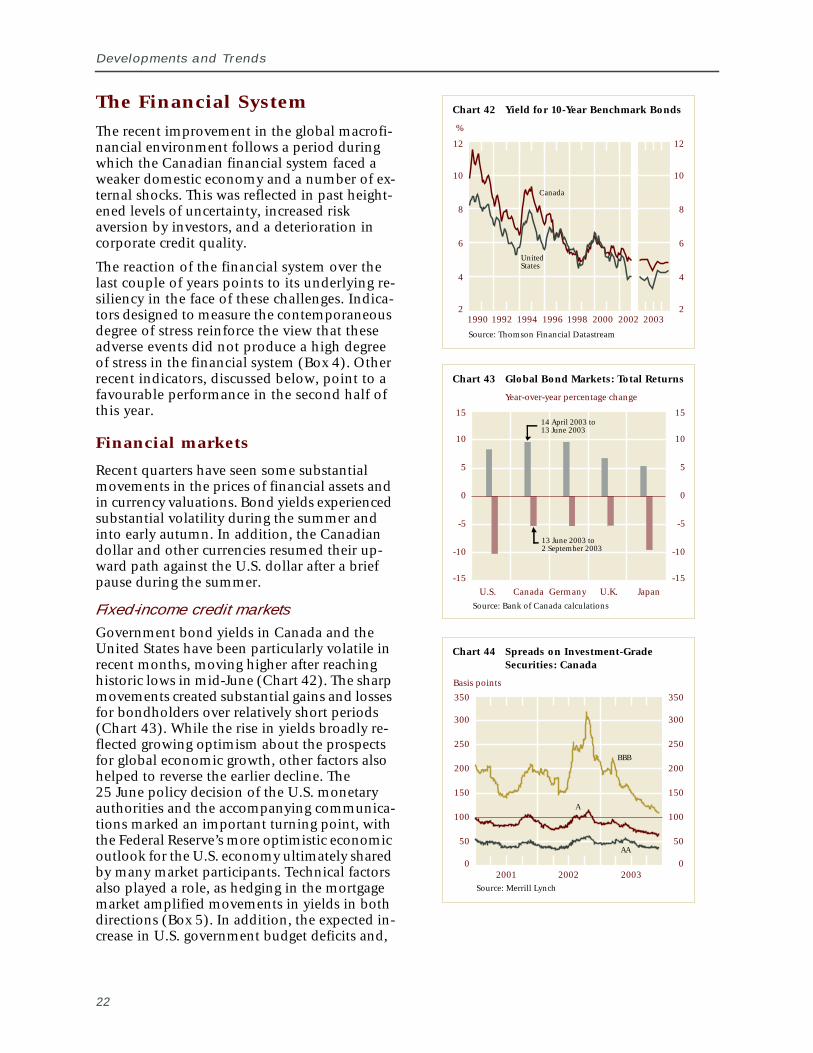

The recent improvement in the global macrofi-nancial environment follows a period duringwhich the Canadian financial system faced aweaker domestic economy and a number of ex-ternal shocks. This was reflected in past height-ened levels of uncertainty, increased riskaversion by investors, and a deterioration incorporate credit quality.

The reaction of the financial system over thelast couple of years points to its underlying re-siliency in the face of these challenges. Indica-tors designed to measure the contemporaneousdegree of stress reinforce the view that theseadverse events did not produce a high degreeof stress in the financial system (Box 4). Otherrecent indicators, discussed below, point to afavourable performance in the second half ofthis year.

Financial markets

Recent quarters have seen some substantialmovements in the prices of financial assets andin currency valuations. Bond yields experiencedsubstantial volatility during the summer andinto early autumn. In addition, the Canadiandollar and other currencies resumed their up-ward path against the U.S. dollar after a briefpause during the summer.

Fixed-income credit marketsGovernment bond yields in Canada and theUnited States have been particularly volatile inrecent months, moving higher after reachinghistoric lows in mid-June (Chart 42). The sharpmovements created substantial gains and lossesfor bondholders over relatively short periods(Chart 43). While the rise in yields broadly re-flected growing optimism about the prospectsfor global economic growth, other factors alsohelped to reverse the earlier decline. The25 June policy decision of the U.S. monetaryauthorities and the accompanying communica-tions marked an important turning point, withthe Federal Reserve’s more optimistic economicoutlook for the U.S. economy ultimately sharedby many market participants. Technical factorsalso played a role, as hedging in the mortgagemarket amplified movements in yields in bothdirections (Box 5). In addition, the expected in-crease in U.S. government budget deficits and,

22

23

Financial System Review

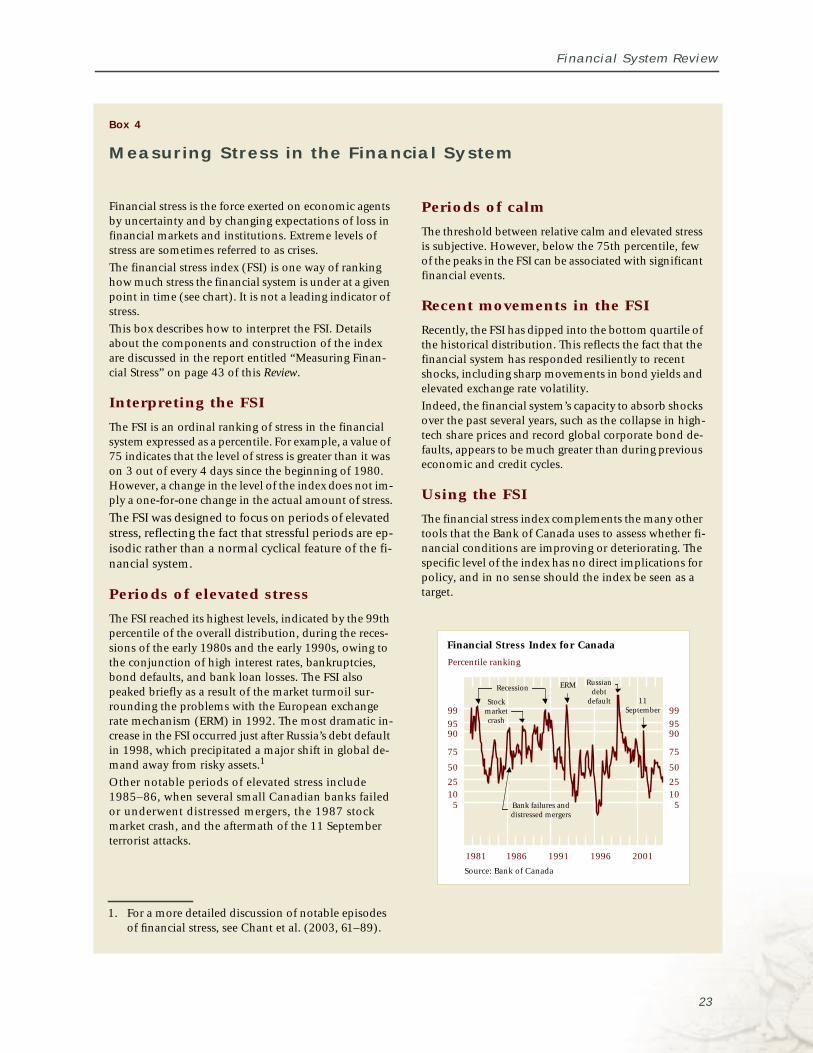

Financial stress is the force exerted on economic agentsby uncertainty and by changing expectations of loss infinancial markets and institutions. Extreme levels ofstress are sometimes referred to as crises.

The financial stress index (FSI) is one way of rankinghow much stress the financial system is under at a givenpoint in time (see chart). It is not a leading indicator ofstress.

This box describes how to interpret the FSI. Detailsabout the components and construction of the indexare discussed in the report entitled “Measuring Finan-cial Stress” on page 43 of this Review.

Interpreting the FSI

The FSI is an ordinal ranking of stress in the financialsystem expressed as a percentile. For example, a value of75 indicates that the level of stress is greater than it wason 3 out of every 4 days since the beginning of 1980.However, a change in the level of the index does not im-ply a one-for-one change in the actual amount of stress.

The FSI was designed to focus on periods of elevatedstress, reflecting the fact that stressful periods are ep-isodic rather than a normal cyclical feature of the fi-nancial system.

Periods of elevated stress

The FSI reached its highest levels, indicated by the 99thpercentile of the overall distribution, during the reces-sions of the early 1980s and the early 1990s, owing tothe conjunction of high interest rates, bankruptcies,bond defaults, and bank loan losses. The FSI alsopeaked briefly as a result of the market turmoil sur-rounding the problems with the European exchangerate mechanism (ERM) in 1992. The most dramatic in-crease in the FSI occurred just after Russia’s debt defaultin 1998, which precipitated a major shift in global de-mand away from risky assets.1

Other notable periods of elevated stress include1985–86, when several small Canadian banks failedor underwent distressed mergers, the 1987 stockmarket crash, and the aftermath of the 11 Septemberterrorist attacks.

Periods of calm

The threshold between relative calm and elevated stressis subjective. However, below the 75th percentile, fewof the peaks in the FSI can be associated with significantfinancial events.

Recent movements in the FSI

Recently, the FSI has dipped into the bottom quartile ofthe historical distribution. This reflects the fact that thefinancial system has responded resiliently to recentshocks, including sharp movements in bond yields andelevated exchange rate volatility.

Indeed, the financial system’s capacity to absorb shocksover the past several years, such as the collapse in high-tech share prices and record global corporate bond de-faults, appears to be much greater than during previouseconomic and credit cycles.

Using the FSI

The financial stress index complements the many othertools that the Bank of Canada uses to assess whether fi-nancial conditions are improving or deteriorating. Thespecific level of the index has no direct implications forpolicy, and in no sense should the index be seen as atarget.

Financial Stress Index for Canada

Source: Bank of Canada

Percentile ranking

25

50

75

909599

510

1986 1991 1996 20011981

25

50

75

909599

510

Stockmarketcrash

Recession ERM

Bank failures anddistressed mergers

Russiandebt

default 11September

Box 4

Measuring Stress in the Financial System

1. For a more detailed discussion of notable episodesof financial stress, see Chant et al. (2003, 61–89).

Developments and Trends

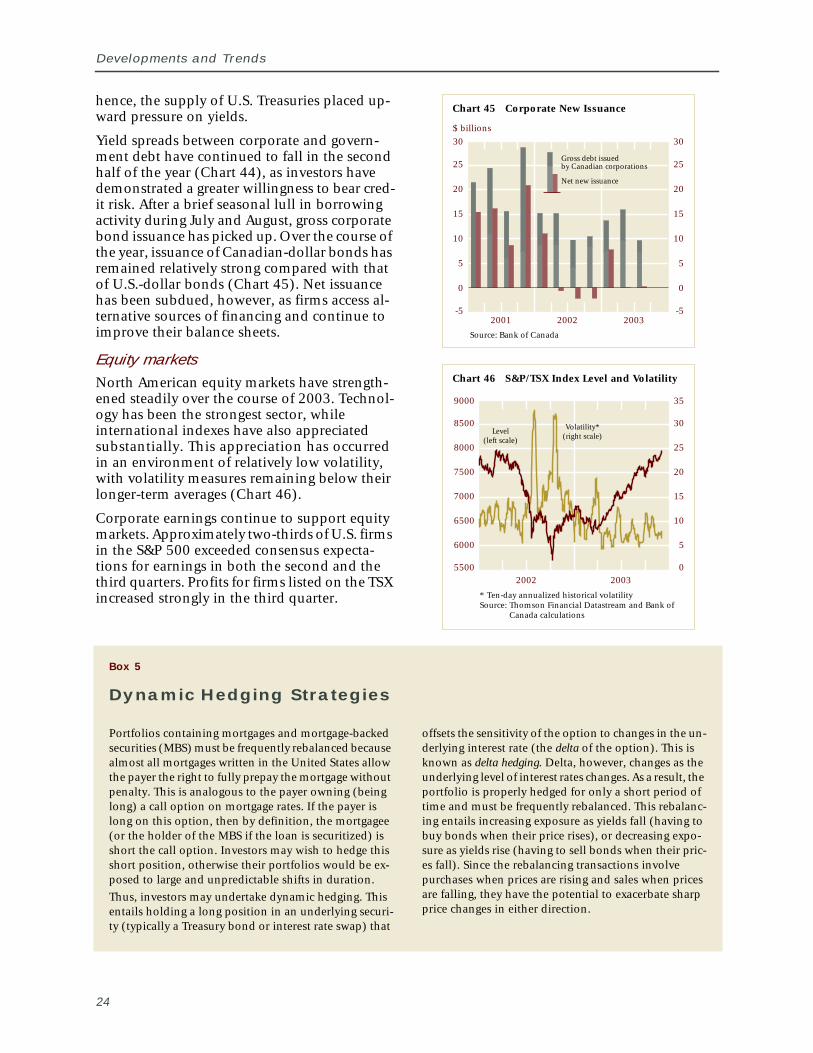

hence, the supply of U.S. Treasuries placed up-ward pressure on yields.

Yield spreads between corporate and govern-ment debt have continued to fall in the secondhalf of the year (Chart 44), as investors havedemonstrated a greater willingness to bear cred-it risk. After a brief seasonal lull in borrowingactivity during July and August, gross corporatebond issuance has picked up. Over the course ofthe year, issuance of Canadian-dollar bonds hasremained relatively strong compared with thatof U.S.-dollar bonds (Chart 45). Net issuancehas been subdued, however, as firms access al-ternative sources of financing and continue toimprove their balance sheets.

Equity marketsNorth American equity markets have strength-ened steadily over the course of 2003. Technol-ogy has been the strongest sector, whileinternational indexes have also appreciatedsubstantially. This appreciation has occurredin an environment of relatively low volatility,with volatility measures remaining below theirlonger-term averages (Chart 46).

Corporate earnings continue to support equitymarkets. Approximately two-thirds of U.S. firmsin the S&P 500 exceeded consensus expecta-tions for earnings in both the second and thethird quarters. Profits for firms listed on the TSXincreased strongly in the third quarter.

24

Portfolios containing mortgages and mortgage-backedsecurities (MBS) must be frequently rebalanced becausealmost all mortgages written in the United States allowthe payer the right to fully prepay the mortgage withoutpenalty. This is analogous to the payer owning (beinglong) a call option on mortgage rates. If the payer islong on this option, then by definition, the mortgagee(or the holder of the MBS if the loan is securitized) isshort the call option. Investors may wish to hedge thisshort position, otherwise their portfolios would be ex-posed to large and unpredictable shifts in duration.

Thus, investors may undertake dynamic hedging. Thisentails holding a long position in an underlying securi-ty (typically a Treasury bond or interest rate swap) that

Box 5

Dynamic Hedging Strategies

Chart 46 S&P/TSX Index Level and Volatility

* Ten-day annualized historical volatilitySource: Thomson Financial Datastream and Bank of

Canada calculations

5500

6000

6500

7000

7500

8000

8500

9000

0

5

10

15

20

25

30

35

2002 2003

Level(left scale)

Volatility*(right scale)

Chart 45 Corporate New Issuance

Source: Bank of Canada

$ billions

-5

0

5

10

15

20

25

30

-5

0

5

10

15

20

25

30

2001 2002 2003

Net new issuance

Gross debt issuedby Canadian corporations

offsets the sensitivity of the option to changes in the un-derlying interest rate (the delta of the option). This isknown as delta hedging. Delta, however, changes as theunderlying level of interest rates changes. As a result, theportfolio is properly hedged for only a short period oftime and must be frequently rebalanced. This rebalanc-ing entails increasing exposure as yields fall (having tobuy bonds when their price rises), or decreasing expo-sure as yields rise (having to sell bonds when their pric-es fall). Since the rebalancing transactions involvepurchases when prices are rising and sales when pricesare falling, they have the potential to exacerbate sharpprice changes in either direction.

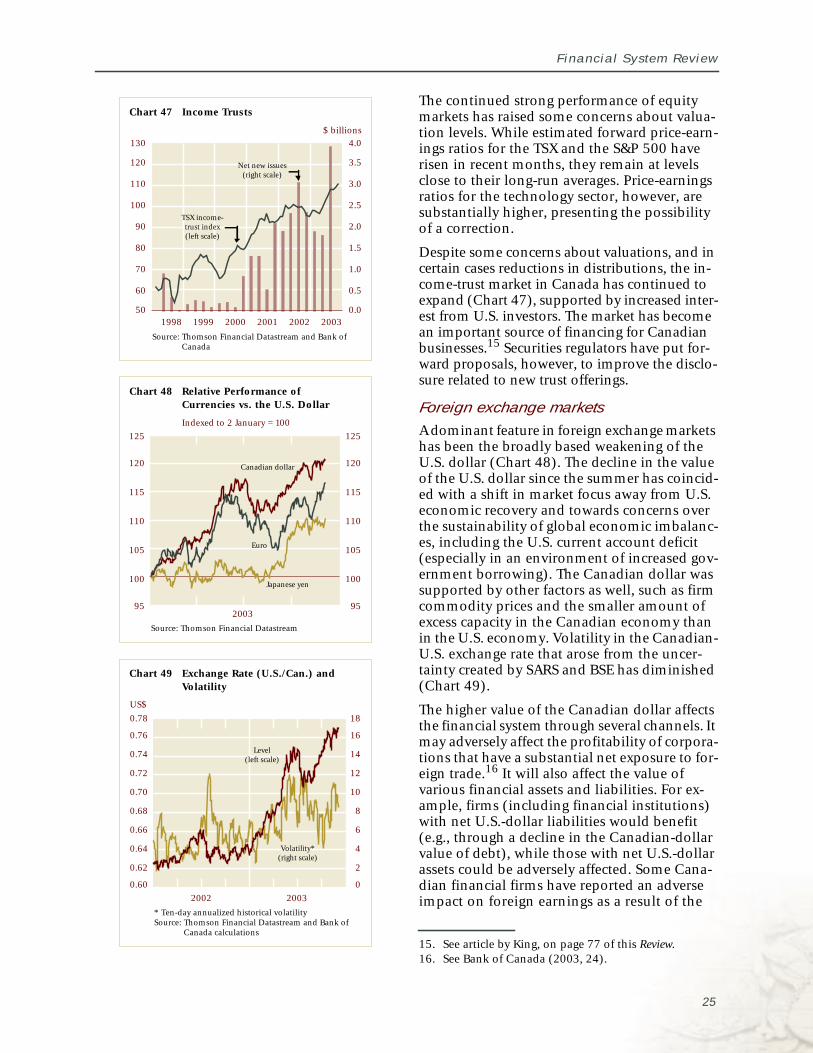

Financial System Review

The continued strong performance of equitymarkets has raised some concerns about valua-tion levels. While estimated forward price-earn-ings ratios for the TSX and the S&P 500 haverisen in recent months, they remain at levelsclose to their long-run averages. Price-earningsratios for the technology sector, however, aresubstantially higher, presenting the possibilityof a correction.