Embed Size (px)

Citation preview

Bank of Sierra Leone

Annual Reportand

Statement of Accountsfor year ended 31st December 2016

TABLE OF CONTENT

List of Tables............................................................................................................................. ivList of Figures............................................................................................................................ vAbbreviations............................................................................................................................ viForeword by the Governor........................................................................................................ 7Board of Directors, as at 31st December 2016........................................................................... 9Management of the BSL as at 31st December 2016.................................................................... 10Bank of Sierra Leone Organiational Structure 2016....................................................................... 12Vision Statement, Mission Statement and Mandate of the Bank................................................... 13

1.0 GOVERNANCE........................................................................................................ 141.1 The Board of Directors................................................................................................. 141.1.1 Functions of the Board.................................................................................................. 141.2 The Monetary Policy Committee................................................................................... 15

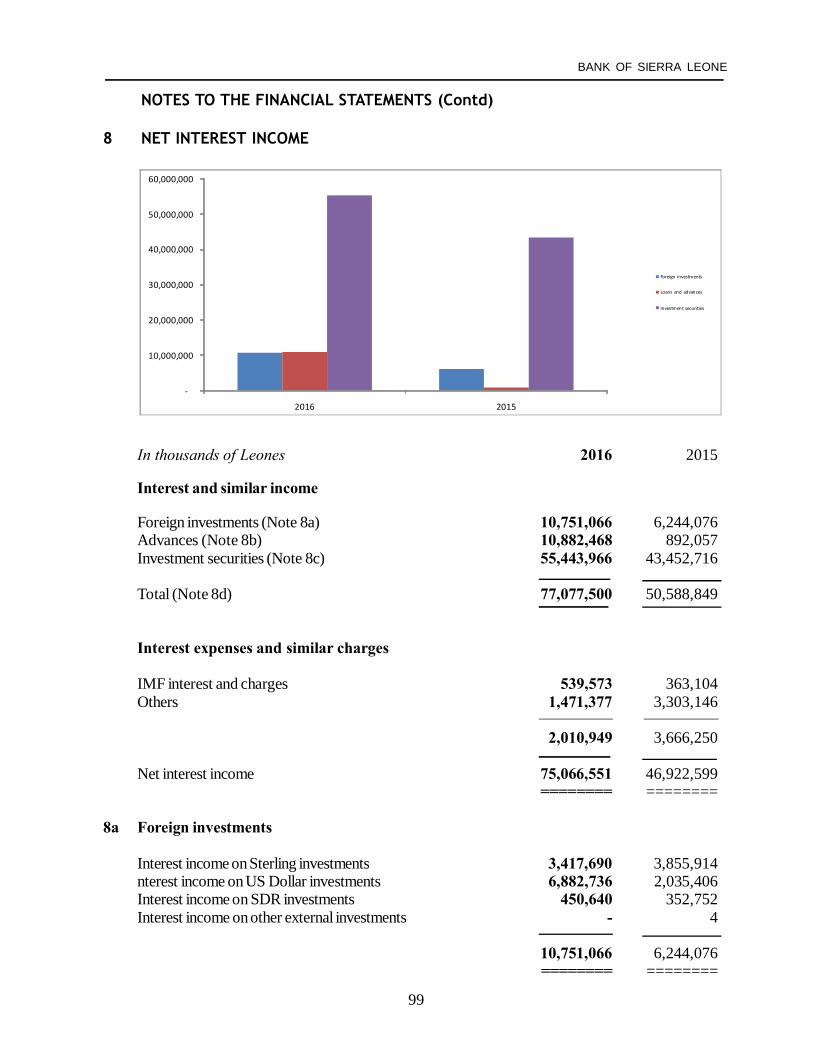

2.0 DEVELOPMENTS IN THE GLOBAL ECONOMY................................................ 162.1 Global Output Growth.................................................................................................. 162.2 Advanced Economies................................................................................................... 162.3 Emerging Market and Developing Economies................................................................ 162.4 Sub-Saharan Africa...................................................................................................... 172.5 Global Inflation............................................................................................................ 172.6 Commodity Prices........................................................................................................ 182.6.1 Crude Oil………………………………………………….……………………….... 182.6.2 Iron Ore…………………………………………………..………………………..... 19

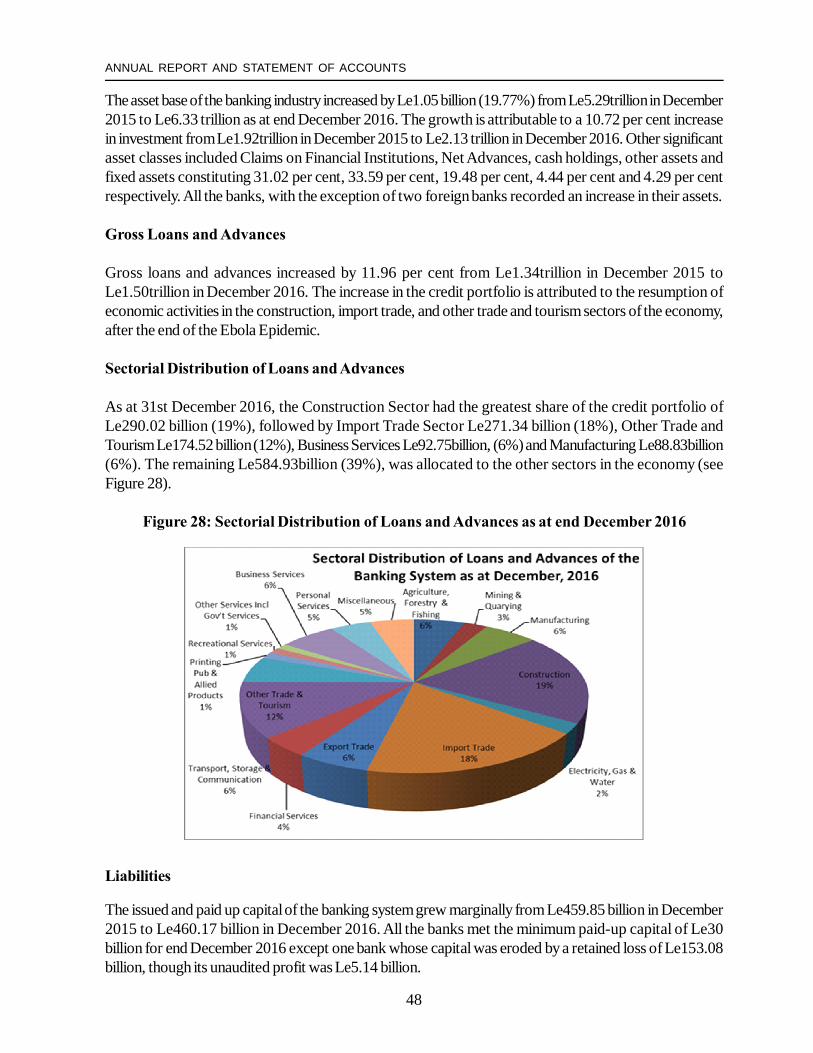

3.0 DEVELOPMENTS IN THE SIERRA LEONE ECONOMY................................... 193.1 Economic Growth.......................................................................................................... 193.1.1 Agriculture……………………………………………………………………............. 203.1.2 Manufacturing…………………………………………………………………............ 203.1.3 Construction…………………………………..…………………………….…........... 203.1.4 Mining………………………………………………………………………............... 213.1.5 Electricity Generation…………………………………………………………............. 213.1.6 Tourism………………………………………..…………….……………….…......... 223.2 Price Development.………............................................................................................ 223.3 Fiscal Policy and Government Budgetary Operations...................................................... 243.3.1 Government Revenue…………………………….........……………………….….…. 243.3.2 Government Expenditure…………………………..…………………….……............ 273.3.3 Budget Deficit and Financing…………………………………………………............. 27

4.0 MONETARY DEVELOPMENTS.............................................................................. 284.1 Monetary Policy Stance and Challenges.......................................................................... 284.2 Developments in Monetary Aggregates........................................................................... 284.3 Interest Rates................................................................................................................. 294.4 Developments in Government securities Market............................................................... 30

ii

5.0 EXTERNAL SECTOR DEVELOPMENTS 335.1 Overview of the External Sector...................................................................................... 335.2 Exports......................................................................................................................... 335.3 Imports......................................................................................................................... 35

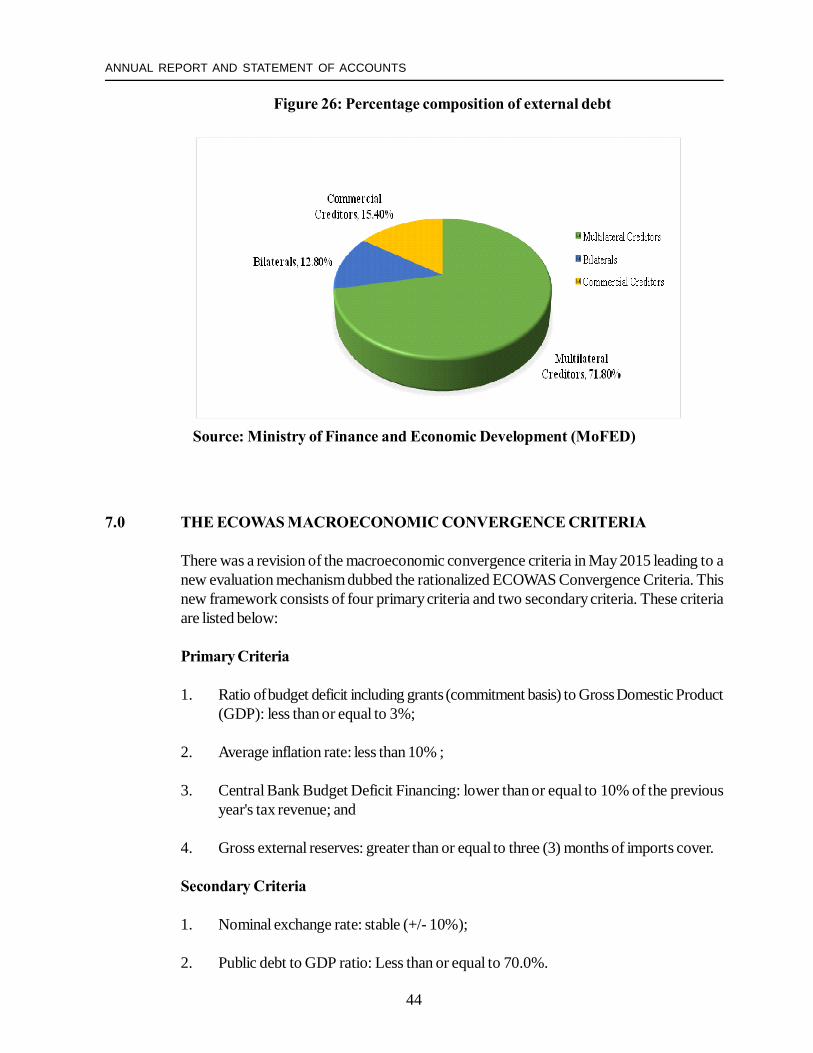

6.0 DEVELOPMENTS IN THE FOREIGN EXCHANGE MARKET 356.1 Overview....................................................................................................................... 356.2 Foreign Exchange Flows............................................................................................... 366.3 Purchases and sales of foreign exchange by commercial banks........................................ 366.4 Receipts into and Payments from Customers Foreign Currency (CFC) accounts............. 366.5 Foreign Exchange Auction.............................................................................................. 376.6 Sectorial Distribution of Auction Funds........................................................................... 376.7 Foreign Exchange Rate Movements.............................................................................. 386.8 Reserves Management................................................................................................... 396.8.1 Foreign Exchange Assets……………………………………………………………... 396.8.2 Investment Activities………………………………………………..…….................. 426.8.3 Foreign Currency Management……………………………...……………….............. 436.9 External Debt............................................................................................................... 43

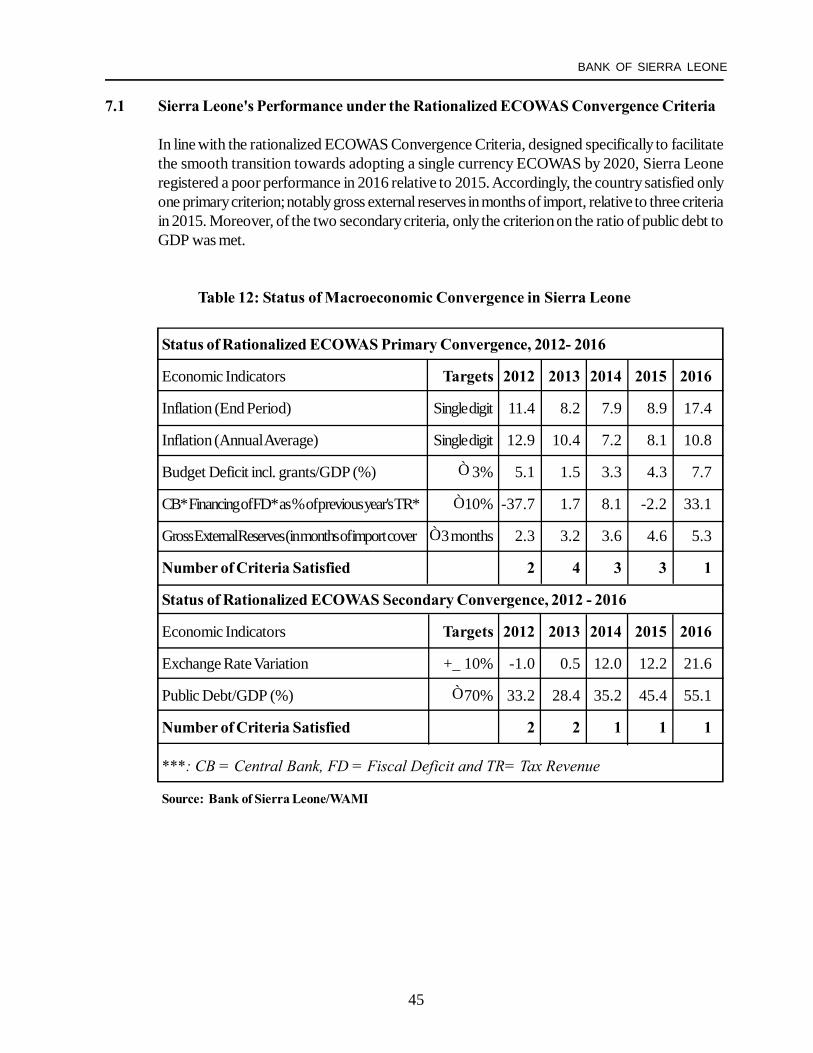

7.0 THE ECOWAS MACROECONOMIC CONVERGENCE 447.1 Sierra Leone's Performance under the Rationalized ECOWAS Convergence Criteria.... 45

8.0 FINANCIAL SECTOR DEVELOPMENTS 468.1 Structure of the Financial Sector..................................................................................... 468.1.1 Commercial Banks…………………………………………………………………… 468.2 Community Banks......................................................................................................... 478.3 Discount Houses.......................................................................................................... 558.4 Foreign Exchange Bureaux............................................................................................ 558.5 Microfinance Institutions (MFIs).................................................................................... 608.5.1 Deposit-Taking Microfinance Institutions…………………………………………....... 608.5.2 Credit-Only Microfinance Institutions (COMFIs)……………...………………….......... 608.5.3 Operating Performance……………………………………………….……………... 618.6 Anti-Money Laundering/Combating the Finance of Terrorism (AML/CFT)……………. 628.7 Customer complaints and investigations………………………………………….......... 628.8 Regulatory Framework…………………………………………................................. 62

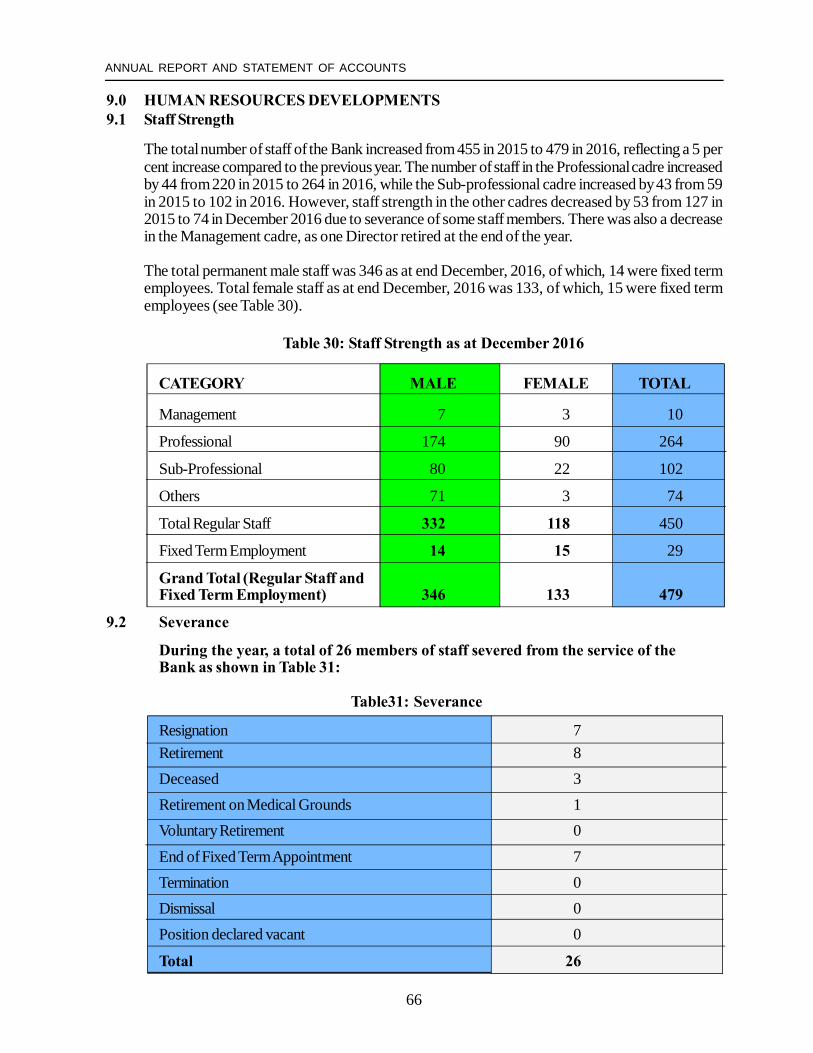

9.0 HUMAN RESOURCES DEVELOPMENTS 669.1 Staff Strength…………………………………………................................................ 669.2 Severance………………………………………….................................................... 669.3 Training - 2016………………………………………….............................................. 67

iii

LIST OF TABLES

Table 1: Meetings of the Bank of Sierra Leone Board................................................................ 15

Table 2: Committees and Membership of the Board.................................................................. 15

Table 3: Global Growth............................................................................................................ 17

Table 4: Global Inflation........................................................................................................... 17

Table 5: GDP Growth Rates by Sector...................................................................................... 19

Table 6: Government Fiscal Operation....................................................................................... 26

Table 7: Stock of Marketable Government Securities Outstanding by Holder (in Millions of Leones)..... 32

Table 8: International Trade and Reserves (US Dollars)............................................................. 34

Table 9: Bank of Sierra Leone Foreign Exchange Cash Flow (2015 & 2016 Inflows)................ 40

Table 10: Bank of Sierra Leone Foreign Exchange Cash Flow (2015 & 2016 outflows)............. 41

Table 11: Currencies Holdings by the Bank of Sierra Leone at End Dec 2015 & 2016............... 43

Table 12: Status of Macroeconomic Convergence in Sierra Leone............................................. 45

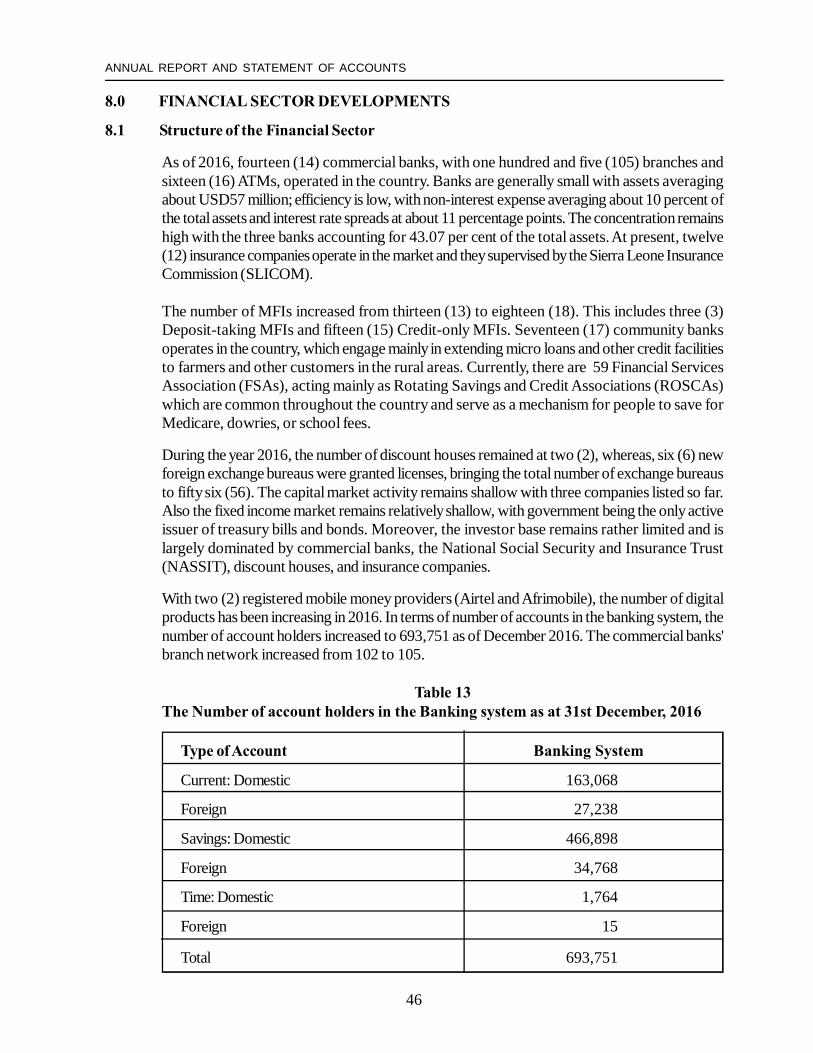

Table 13: The Number of account holders in the Banking system as at 31st December, 2016..... 46

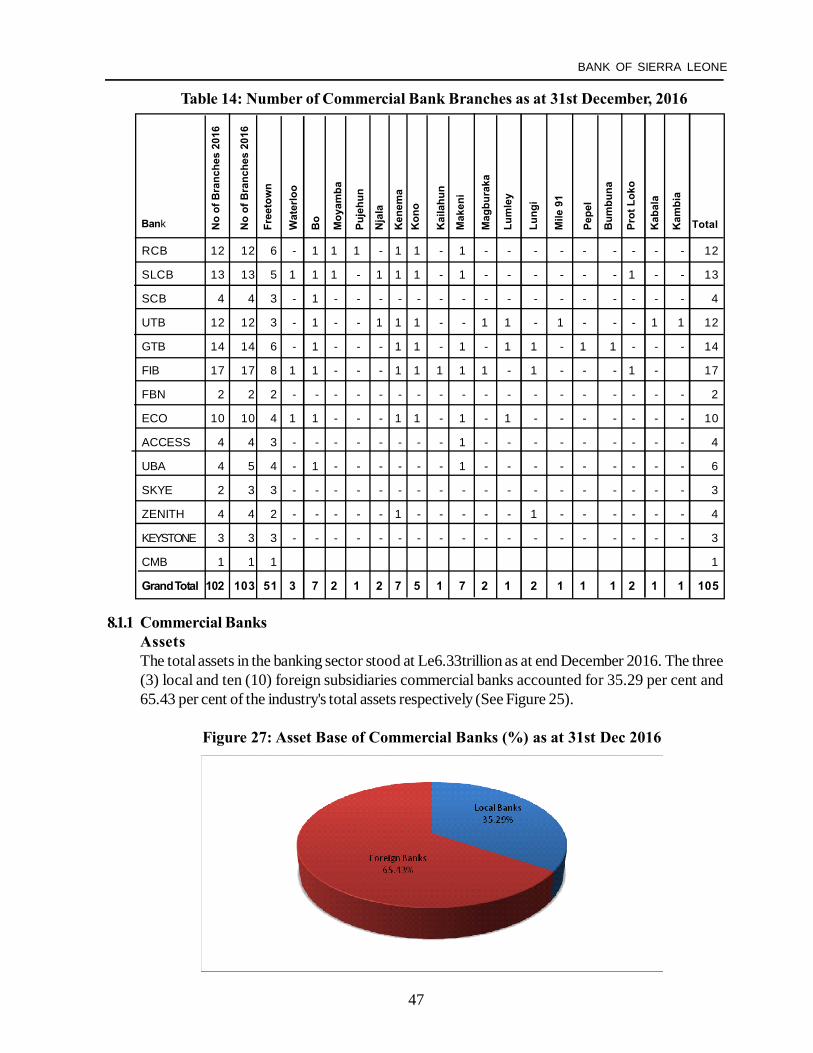

Table 14: Number of Commercial Bank Branches as at 31st December, 2016........................... 47

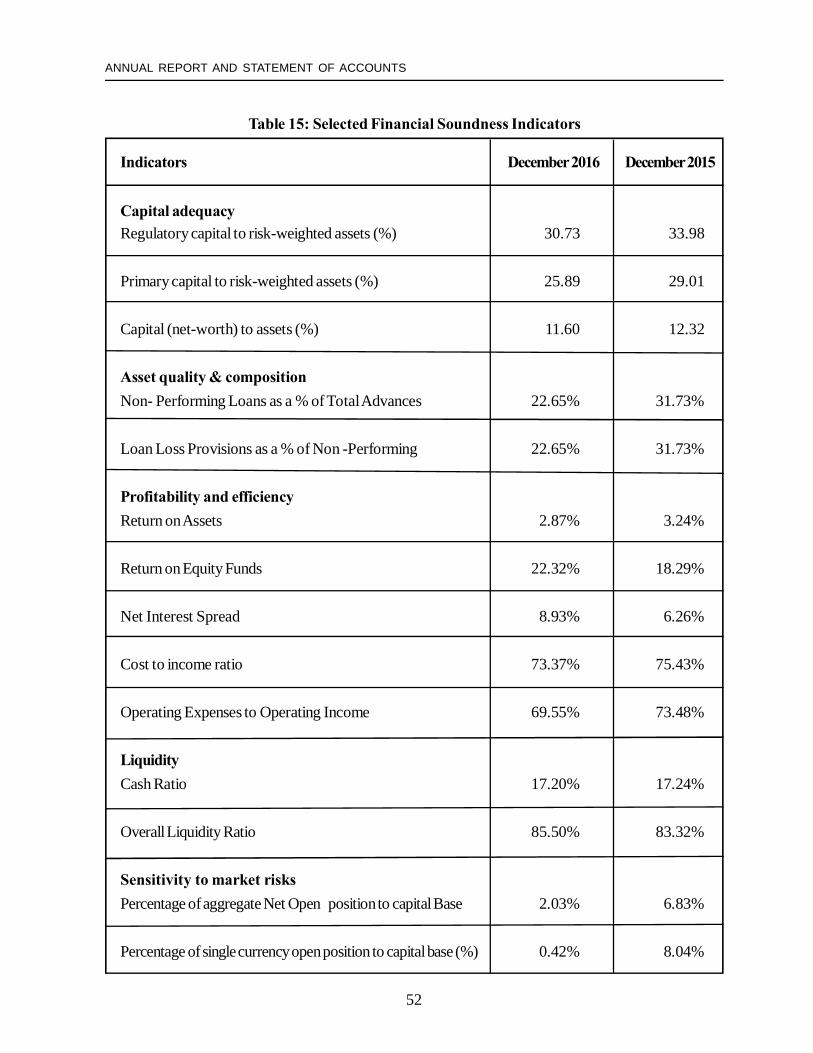

Table 15: Selected Financial Soundness Indicators..................................................................... 52

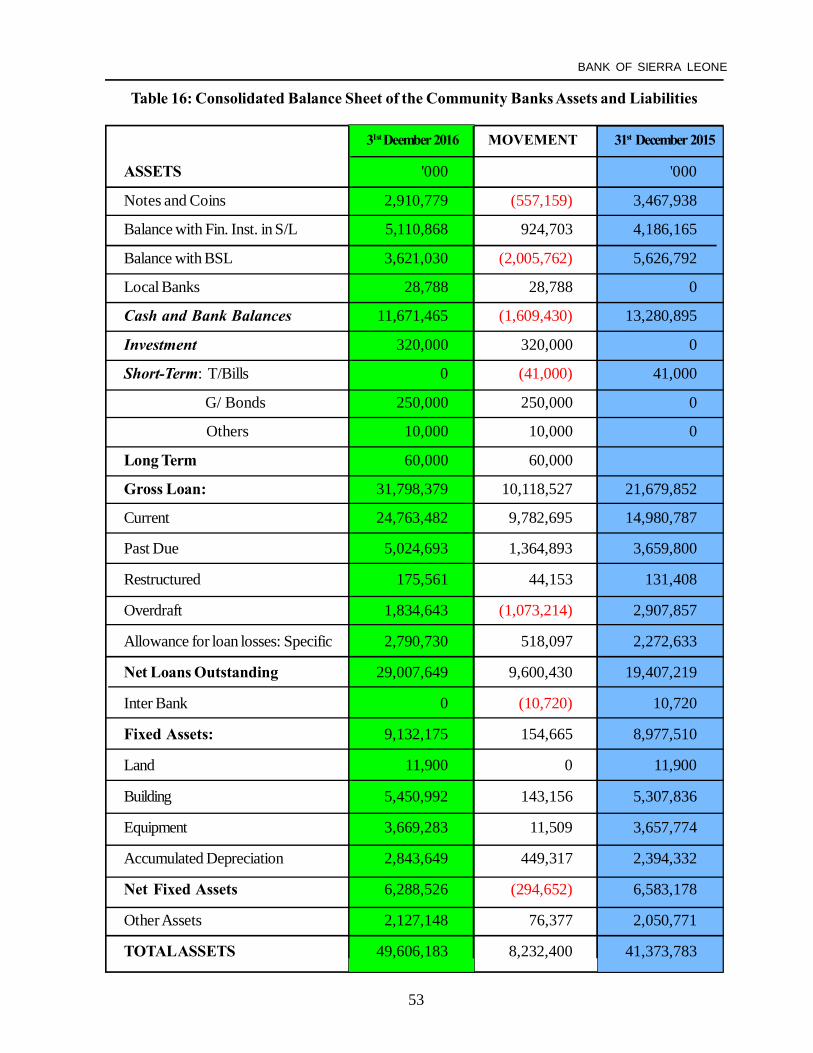

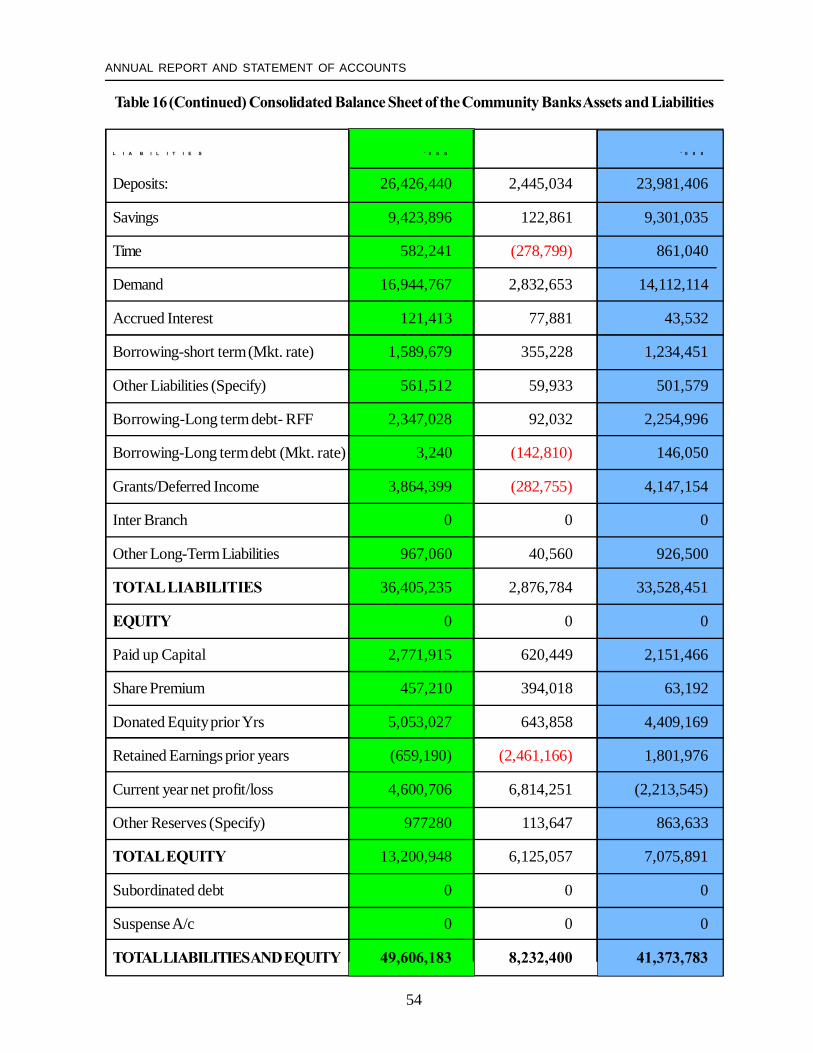

Table 16: Consolidated Balance Sheet of the Community Banks Assets and Liabilities................ 53

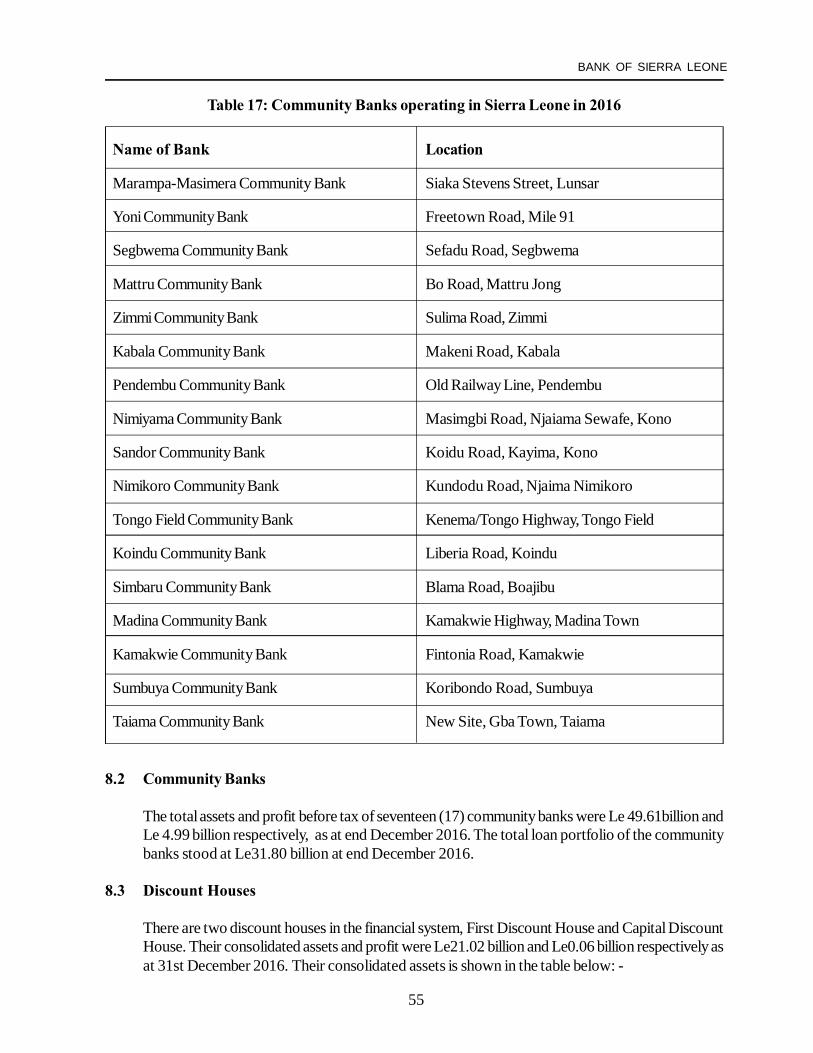

Table 17: Community Banks operating in Sierra Leone in 2016.................................................. 55

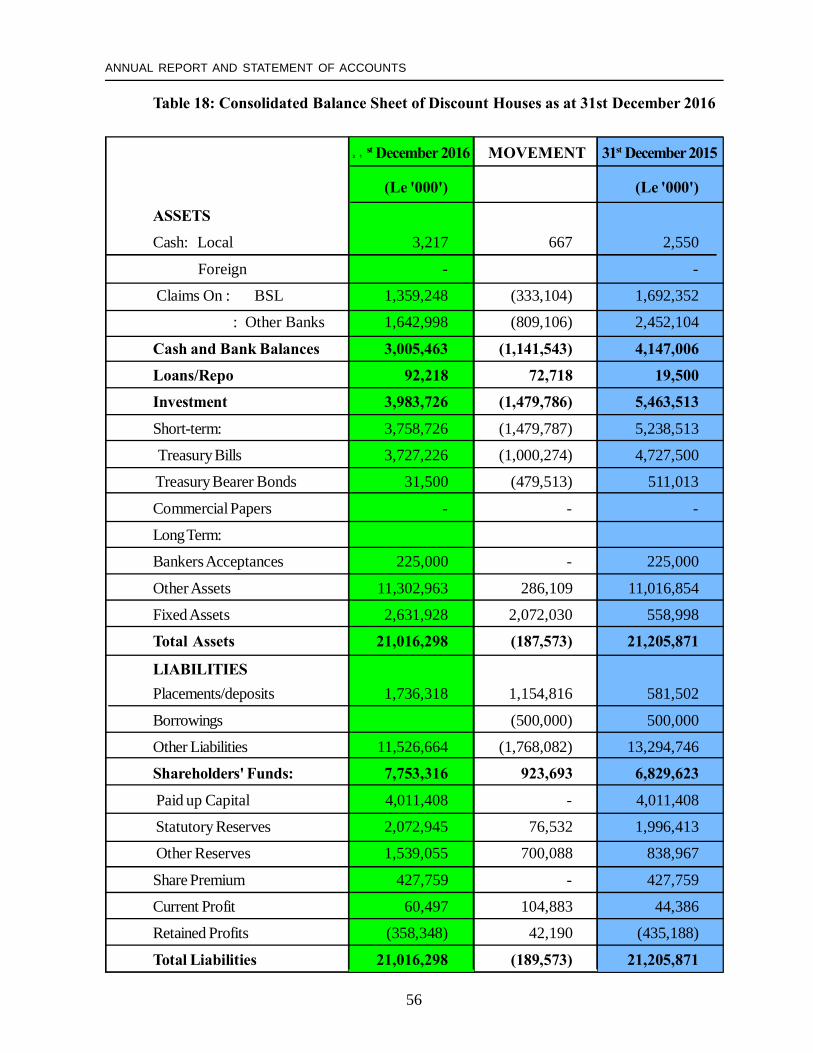

Table 18: Consolidated Balance Sheet of Discount Houses as at 31st December 2016............... 56

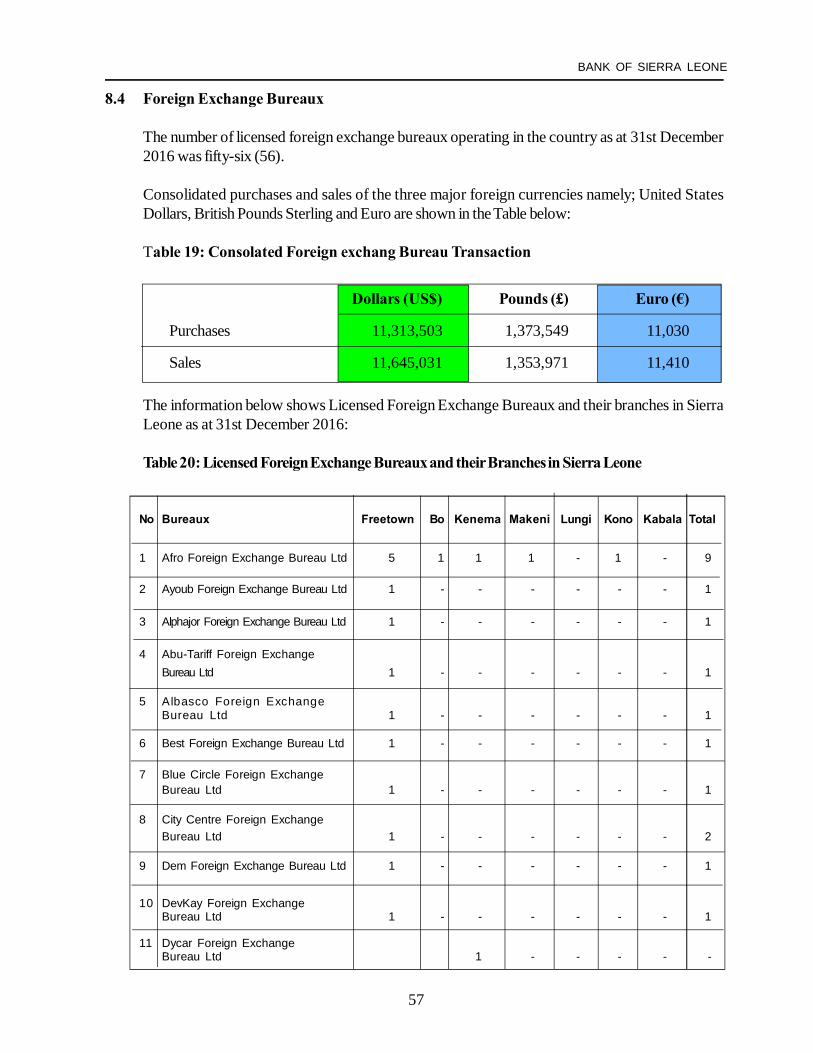

Table 19: Consolidated Foreign Exchange Bureau Transaction................................................... 57

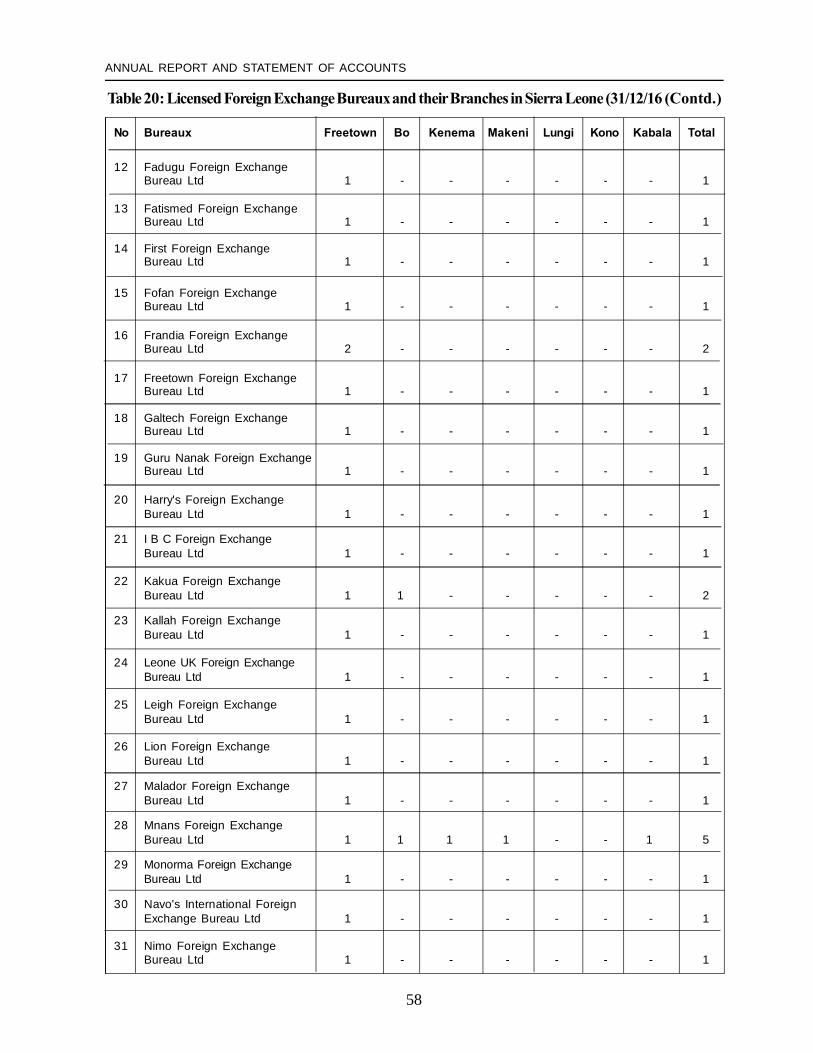

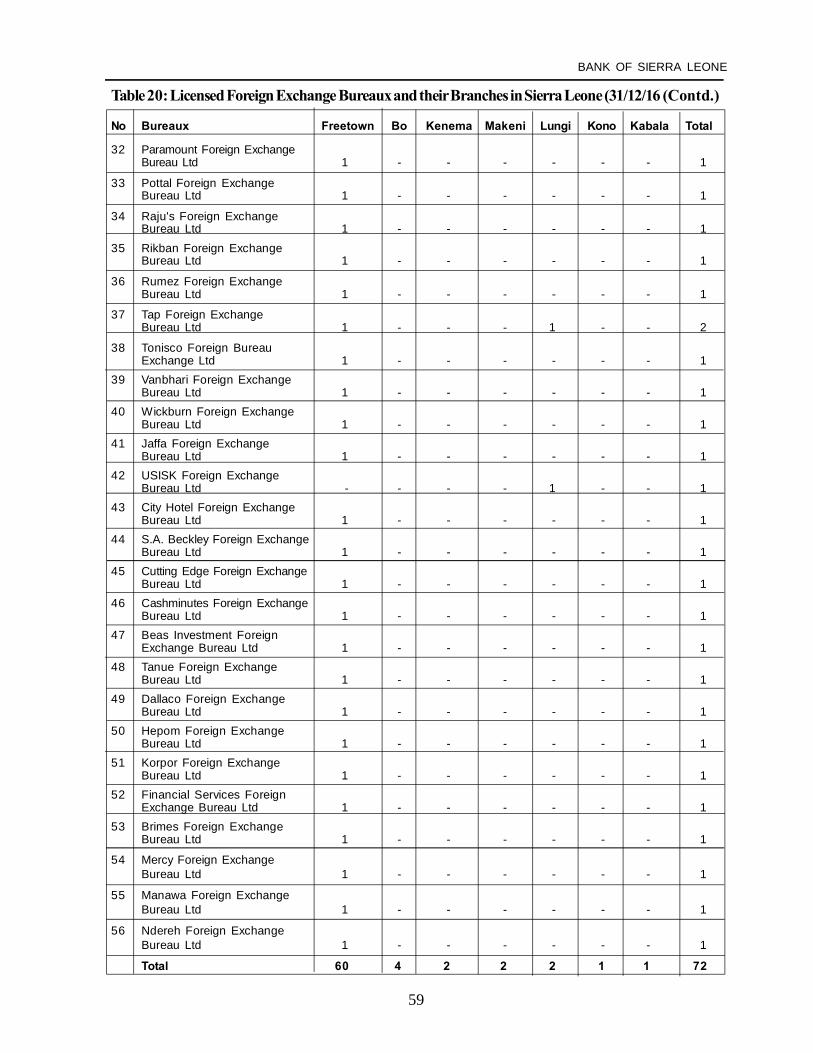

Table 20: Licensed Foreign Exchange Bureaux and their Branches in Sierra Leone (31/12/16).... 57

Table 21: Credit -only microfinance institutions as at 31st December 2016................................. 60

Table 22: The pre-tax profit/loss position of COMFIs at end December 2016............................ 61

Table 23: Portfolio, Financial and Non-Financial Information as at end December 2016............. 61

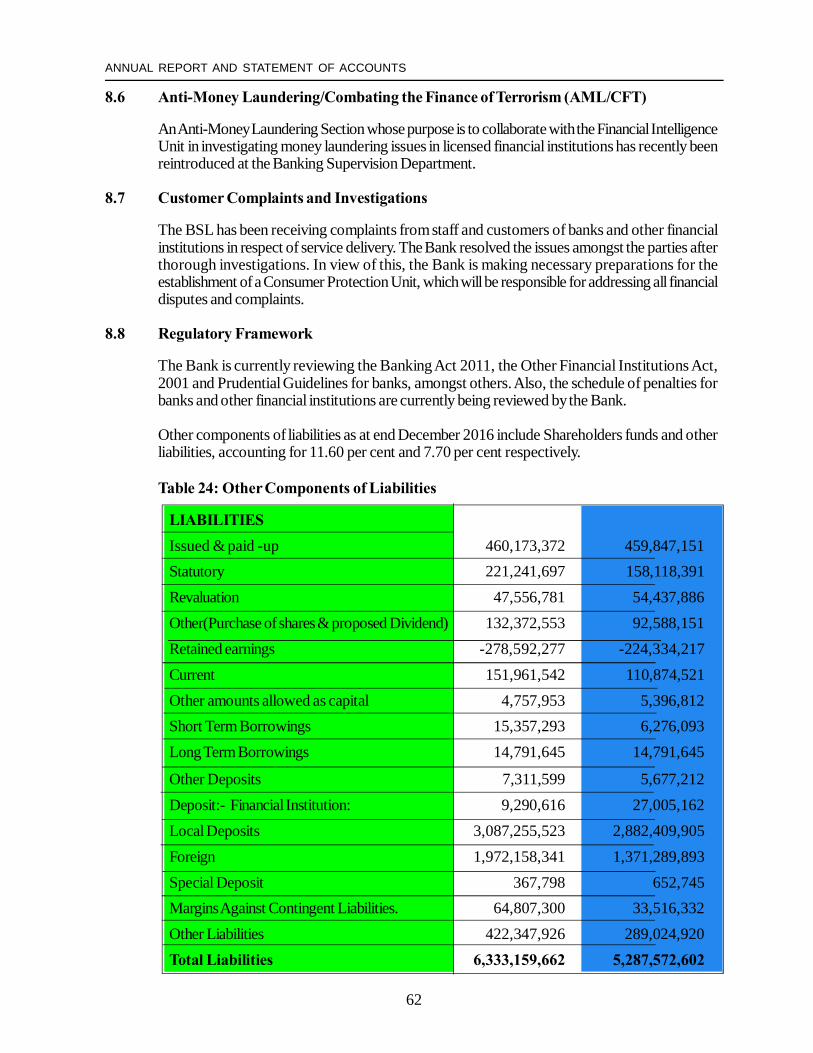

Table 24 Other Components of Liabilities.................................................................................. 62

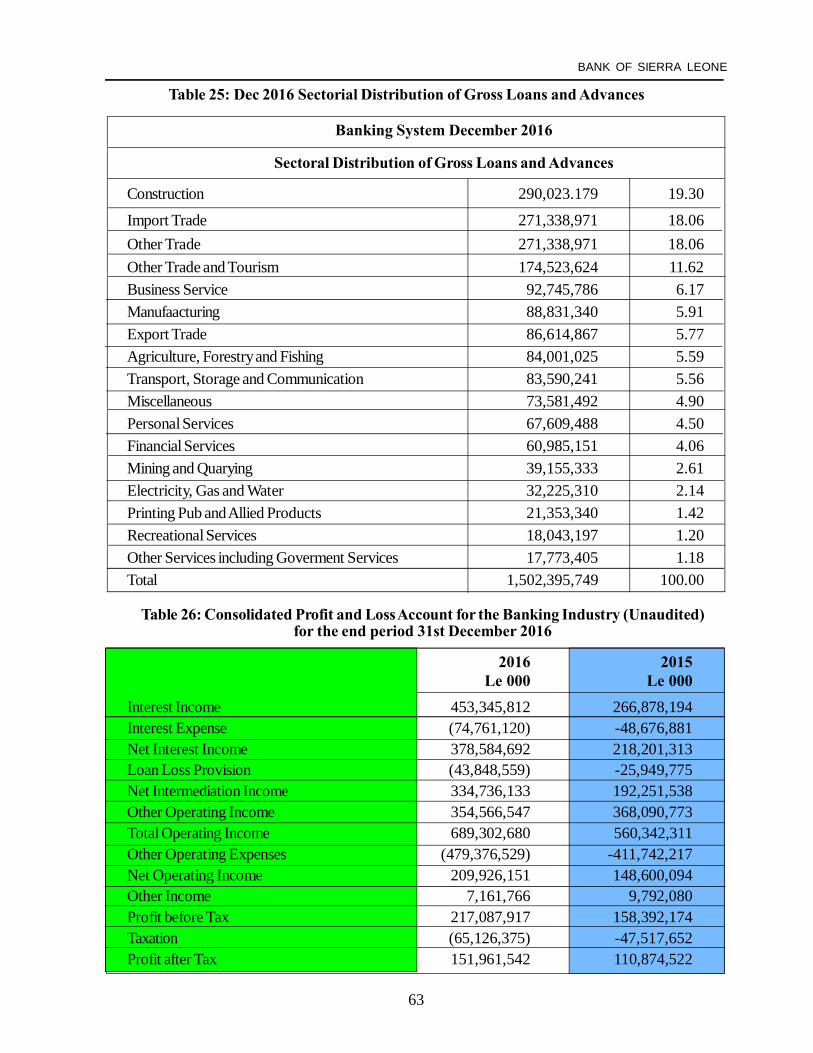

Table 25: Dec 2016 Sectorial Distribution of Gross Loans and Advances................................... 63Table 26: Consolidated Profit and Loss Account for the Banking Industry (Unaudited) for the end

period 31st December 2016...................................................................................... 63

Table 27:Consolidated Balance Sheet of Banking System as at 31st December 2016 ( Asset).. 64

Table 28 Consolidated Balance Sheet of Banking System as at 31st December 2016 (Liabilities).64

Table 29: Financial Performance Indicators of the Banking System ............................................ 65

Table 30 Staff Strength as at December 2016........................................................................... 66

Table 31: Severance................................................................................................................. 66iv

LIST OF FIGURES

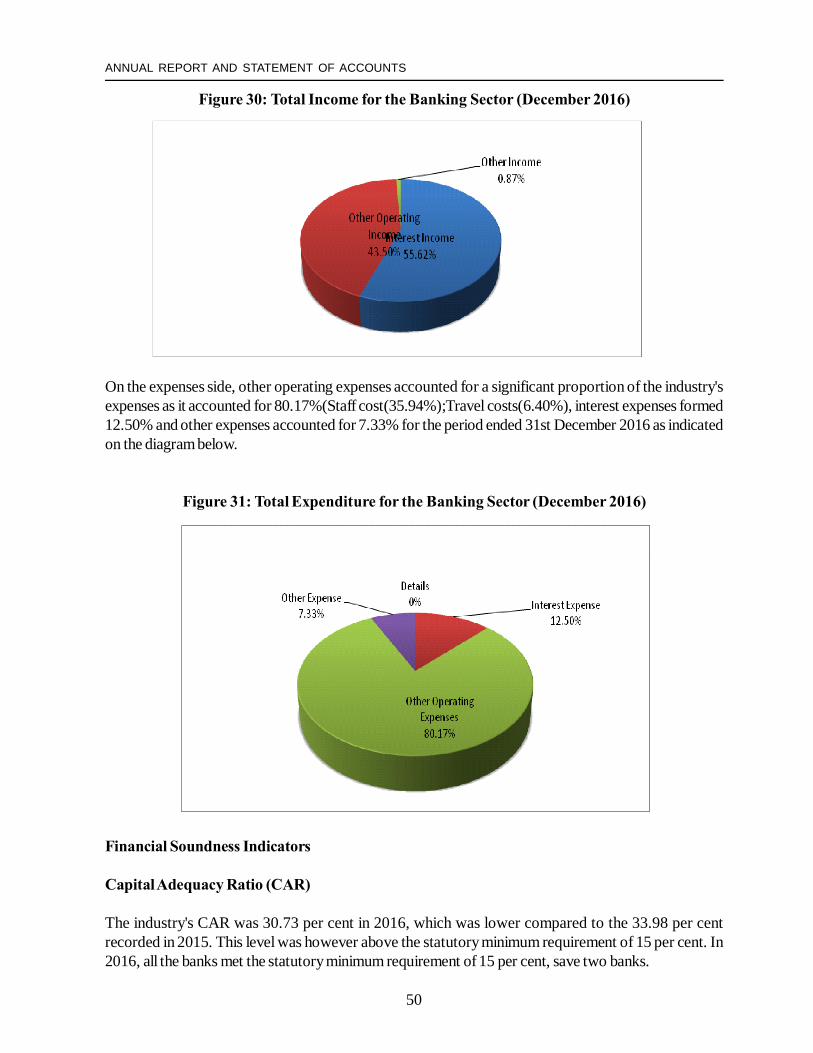

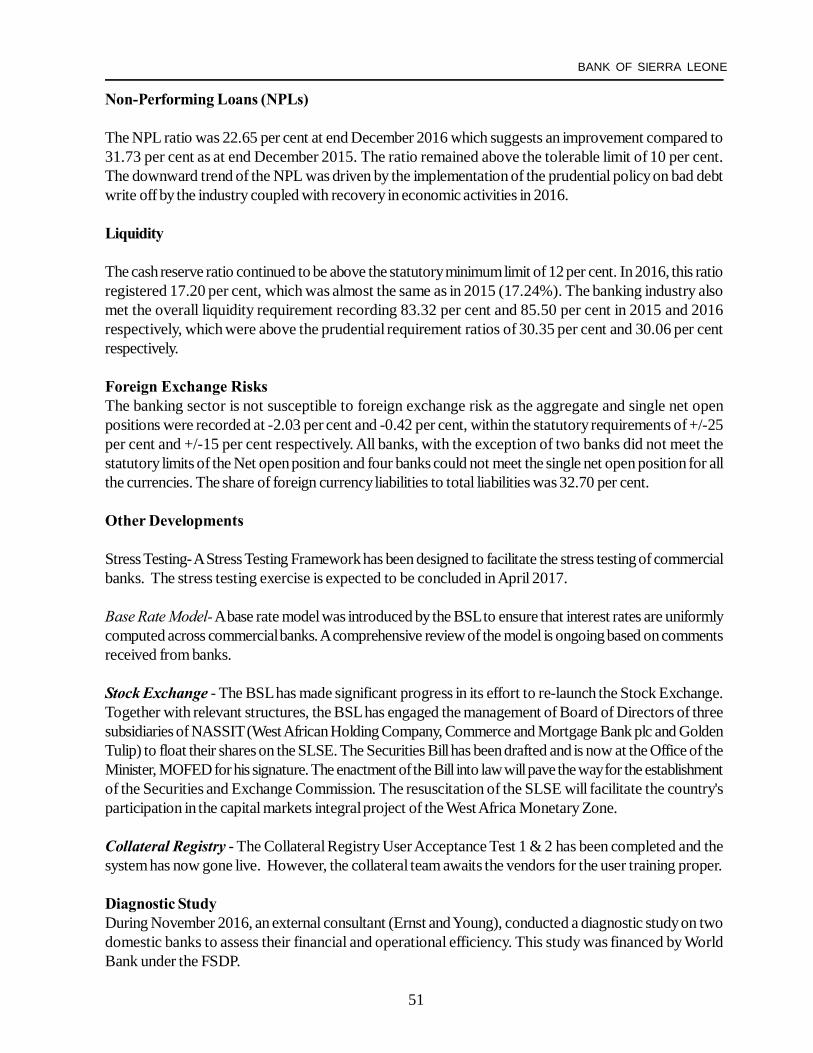

Figure 1: Crude Oil Prices........................................................................................................ 18Figure 2: Iron Ore Price............................................................................................................ 19Figure 3: Percentage Contributions to GDP by Sector 2016...................................................... 20Figure 4: Monthly Electricity Generation.................................................................................... 21Figure 5: Tourists Arrival by Country of Origin........................................................................... 22Figure 6: Tourists Arrival by Purpose......................................................................................... 22Figure 7: Trends in Headline, Food and Non-Food Inflation....................................................... 23Figure 8: Contribution of main components to Annual Inflation................................................... 23Figure 9: Headline and Core Inflation........................................................................................ 24Figure 10: Trends in Revenue, Expenditure & Budget Deficit...................................................... 25Figure 11a: Expenditure Disaggregation in 2015......................................................................... 27Figure 11b: Expenditure Disaggregation in 2016.......................................................................... 27Figure 12: Trend in the Yields of Government Securities in the Primary and Secondary Markets 30Figure 13: Stock of Government Securities by Tenure.............................................................. 31Figure 14: Holdings of Government Securities by Sector (In Billions of Leones) 31Figure 15: External Trade, 2016................................................................................................ 33Figure 16: Composition of Imports 2016................................................................................... 35Figure 17: Commercial Banks Purchases and Sales of Foreign exchange.................................... 36Figure 18: Receipt into Payment from CFC Account.................................................................. 37Figure 19: Demand and Supply in the Auction (USD 000).......................................................... 37Figure 20: Sectorial Distribution of Auction Funds January- December 2016............................... 38Figure 21: Exchange Rate Depreciation (y-o-y).......................................................................... 38Figure 22: Exchange Rates Spread as per Market Segments...................................................... 39Figure 23: Gross Foreign Reserves............................................................................................ 39Figure 24: Actual Investments Income by Currencies, converted in US Dollars........................... 42Figure 25: Actual Investments Income by Currencies, converted in US Dollars........................... 42Figure 26: Percentage composition of external debt.................................................................... 44Figure 27: Asset Base of Commercial Banks (%) as at 31st Dec 2016....................................... 47Figure 28: Sectorial Distribution of Loans and Advances as at end December 2016.................... 48Figure 29: Growth of Key Financial Indicators........................................................................... 49Figure 30: Total Income for the Banking Sector (December 2016)............................................. 50Figure 31: Total Expenditure for the Banking Sector (December 2016)....................................... 50

v

Abbreviations:

AfDB - African Development BankBIS - Bank for International SettlementBOP - Balance of PaymentsBSL - Bank of Sierra LeoneCFC - Customers Foreign CurrencyCIF - Cost, Insurance and FreightCPI - Consumer Price IndexECOWAS - Economic Community of West African StatesEMSL - Eclipse Microfinance Sierra LeoneGDP - Gross Domestic ProductGFER - Gross Foreign Exchange ReservesGoSL - Government of Sierra LeoneGW/hr - Giga-Watts per HourHIPC - Heavily Indebted Poor CountriesIDA - International Development AssociationIFAD - International Fund for Agriculture DevelopmentIMF - International Monetary FundM2 - Broad MoneyMER - Monthly Economic ReviewMIF - Microfinance InstitutionsMoFED - Ministry of Finance and Economic DevelopmentMPC - Monetary Policy CommitteeMPR - Monetary Policy RateNDA - Net Domestic AssetsNERS - National Ebola Recovery StrategyNFA - Net Foreign AssetsNMA - National Minerals AgencyODC - Other Depository CorporationOFID - OPEC Fund for International DevelopmentOIN - Other Items NetOPEC - Organization of the Petroleum Exporting CountriesPTMO - Precious Minerals Trading OfficeRM - Reserve MoneySDF - Standing Deposit FacilitySLF - Standing Lending FacilitySSA - Sub-Saharan AfricaWAIFEM - West African Institute for Financial and Economic ManagementWB - World BankWTI - West Texas Intermediate

vi

7

BANK OF SIERRA LEONE

FOREWORD BY THE GOVERNOR

The Sierra Leone economy registered remarkable growth, with the economy expanding by 6.3 per centin 2016, after a significant contraction of 20.6 per cent in 2015. Improved performance in construction,transport and communications, trade, manufacturing and services sectors largely accounted for this outturnin the domestic economy. The Government's Post Ebola Recovery Strategy and consistent pro-growthmeasures coupled with accommodative monetary and fiscal policies in the first half of the year 2016, alsohelped stimulate aggregate demand in the economy.

Notwithstanding the aforesaid recovery, there were several challenges, especially in the conduct of monetarypolicy. The supply-side shocks to domestic food production, coupled with the continued depreciation ofthe exchange rate led to inflation persistence in the second half of the year. Consequently, headline inflationincreased sharply to 17.41 per cent in December 2016 from 8.38 per cent in December 2015.

The conduct of monetary policy in 2016 was aimed at achieving an end year inflation target of 9.5 percent, ensure adequate provision of credit to meet private sector needs, maintaining stability of the exchangerate and keeping gross international reserves at a level equivalent to about three months of imports ofgoods and services. In addition to maintaining stability in the financial sector, monetary policy was tailoredto also support the government's Post Ebola Recovery Initiatives

On that note, monetary policy was largely neutral in the first half of 2016, with the Monetary Policy Rate(MPR) kept unchanged at 9.5 per cent. The motivation for maintaining a neutral policy stance was tosupport the economy's recovery process in the face of negative output gap and subdued inflationaryoutcomes. However, in the second half of 2016, monetary policy management was challenged by thepersistent pressures in the foreign exchange market and higher than budgeted fiscal deficit, which hadknock on effects on inflation and inflation expectations.

In response, the BSL adopted a tight monetary policy stance by increasing the MPR from 9.5 per cent to10.5 per cent in quarter two and further to 11 per cent by the end of the year. The objective was to reinin the second round effects of the supply side induced inflationary pressures, anchor medium to long terminflation expectations at levels consistent with the Bank's medium term inflation target of single digit, and tocurb the exchange rate pressures in the foreign exchange market. The Bank continued to be vigilant toupside risk to the inflation outlook that could emerge from both external and domestic environment.

External sector developments resulted in a trade deficit of USD433.39mn compared to a deficit of USD1,017.11mn in 2015. The improvement in the trade position reflected the combined effects of a recovery inexport receipts-especially with the resumption of iron ore exports- and a decline in payments for imports.Notwithstanding the development in the trade balance, the Gross International Reserves of the Bank ofSierra Leone declined from US$580.26mn in 2015 to US$503.79mn in 2016, but was enough to cover3.8 months of imports of goods and services.

The BSL's supervisory policy continued to focus on the achievement of financial sector stability throughappropriate supervisory actions, including on-site and off-site surveillance.

The health of the banking sector remained resilient to both external and domestic shocks. More specifically,the banking sector recorded improvements in the capital adequacy position, liquidity, and profitability.Although data on asset quality improved significantly, the relatively high non-performing loans of the bankingsystem remains a regulatory concern and are closely monitored.

8

ANNUAL REPORT AND STATEMENT OF ACCOUNTS

During the year, the Bank continued to support the Government's economic reform program. To this end,all targets under the IMF supported ECF program were successfully met. Consequently, in September2016, Sierra Leone successfully completed the sixth and final review under the Extended Credit Facilityof the IMF. Furthermore, the Bank participated in the successful negotiation of the new three year ECFprogram with the Fund.

In 2016, the BSL embarked on a range of reforms aimed at strengthening its capacity to deliver on itsmandate. In a bid to enhance the effectiveness of monetary policy, the BSL in September 2016, introducedinto its monetary policy framework an interest rate corridor system. The corridor consists of overnightdeposit and lending facilities. These facilities offer commercial banks the opportunity to place funds withand obtain funds from the Bank, on an overnight basis. The introduction of the corridor system alsohelped to enhance the transparency and effectiveness of the transmission of monetary policy impulses tothe real economy.

The BSL also strengthened efforts to promote secondary market trading of treasury bills by introducing aPrimary Dealership System which allowed the Bank to migrate from retail to wholesale trading ofGovernment's Securities in the Primary Market.

This system also facilitates secondary trading in treasury securities, as it enhances the transfer of title forgovernment securities. Furthermore, it permits the Bank to have greater flexibility to engage in OpenMarket Operations.

In conclusion, I would like to take this opportunity to thank the Board of Directors of the Bank for theirsupport and guidance throughout the year. I would also like to extend my gratitude to the entire staff of theBank for their continued commitment and support as we work towards setting the right macroeconomicenvironment that supports a sustainable growth path.

Kaifala Marah (Dr.) Governor

9

BANK OF SIERRA LEONE

Dr. Kaifala Marah Dr. Ibrahim L. Stevens Governor and Chairman of the Board Deputy Governor Member

Mr. S. N. Dumbuya PC Mohamed D. Benya V Member Member

Mr. Winstanley Bankole Johnson Mrs. Rosaline Y. Fadika Dr. Richard C. M'Bayo Member Member Member

Board of Directors as at 31st December 2016

10

ANNUAL REPORT AND STATEMENT OF ACCOUNTS

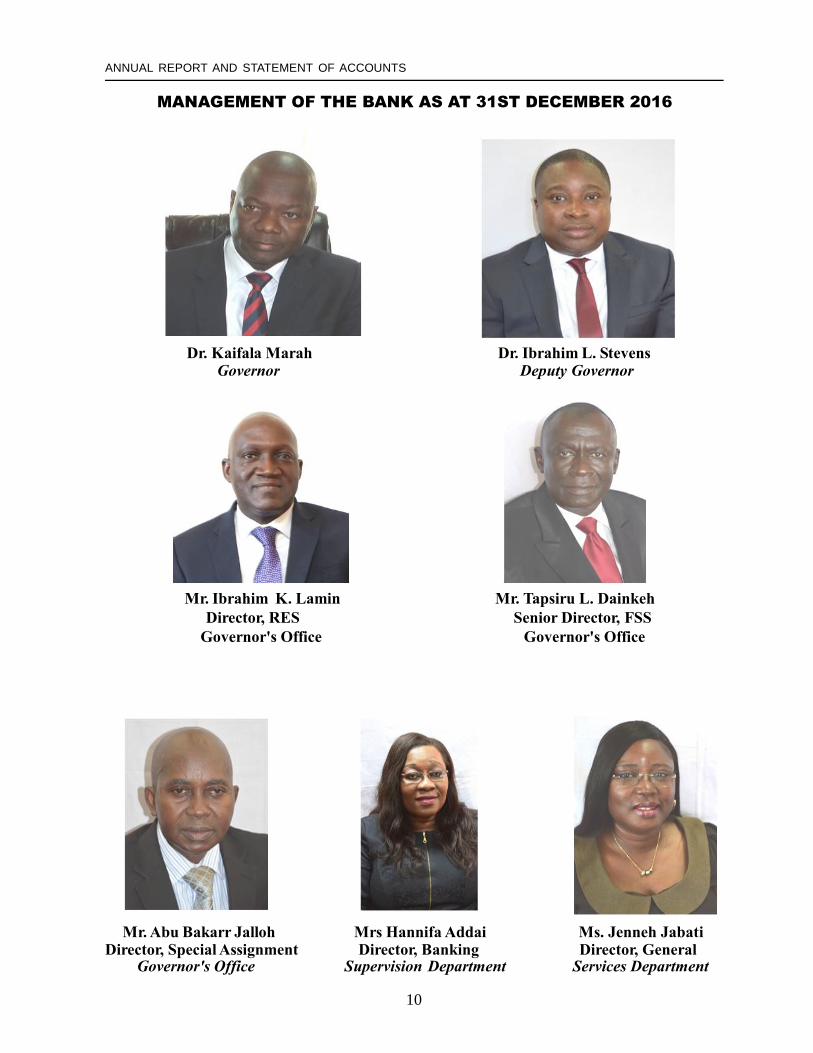

MANAGEMENT OF THE BANK AS AT 31ST DECEMBER 2016

Dr. Kaifala Marah Dr. Ibrahim L. Stevens Governor Deputy Governor

Mr. Ibrahim K. Lamin Mr. Tapsiru L. Dainkeh Director, RES Senior Director, FSS Governor's Office Governor's Office

Mr. Abu Bakarr Jalloh Mrs Hannifa Addai Ms. Jenneh JabatiDirector, Special Assignment Director, Banking Director, General Governor's Office Supervision Department Services Department

11

BANK OF SIERRA LEONE

Mr. Ralph Ansumana Mr. Richard J D Sowa Mrs. Mary May Kargbo Director, Banking Director, Secretary's Director, Special Duty Department Department Governor's Office

Mr. Abdul Aziz Sowe Mr. Abdul Bundu Ms. Hawa E. Kallon Director Acting Director Acting DirectorFinance Department Internal Audit Department Human Resources Department

Mr. Gibao Flee Mr. Morlai Bangura Ms. Fatima Mansaray Acting Director Acting Director Acting DirectorFinancial Markets Department Research Management Information Systems

Department

12

ANNUAL REPORT AND STATEMENT OF ACCOUNTS

BANK OF SIERRA LEONE ORGANIZATIONAL STRUCTURE -2016

BOARD OF

DIRECTORS

GOVERNOR

DEPUTY

GOVERNOR

INTERNAL AUDIT

DEPT

MIS

DEPT

HUMAN

RESOURCESs

DEPT

BANKING

SUPERVISION

DEPT

FINANCIAL

MARKETS

DEPT

FINANCE

DEPT

BANKING

DEPT

RESEARCH

DEPTSECRETARY’S

DEPT

OFFICE OF THE GOVERNOR

GENERALSERVICES

DEPT

Security UnitProcurement Unit F S D Unit

13

BANK OF SIERRA LEONE

Vision StatementTo create a modern, effective and dynamic Central Bank that serves the overall financial, growth anddevelopment requirements of Sierra Leone

Mission StatementTo formulate and implement monetary and supervisory policies to foster a sound economic and financialenvironment.

Objectives and Functions of the Bank

(1) The main objective of the Bank as specified in Section 4 of the Bank of Sierra Leone Act 2011, isto achieve and maintain price stability.

(2) Without prejudice to subsection (1), the Bank shall:

(a) Formulate and implement monetary policy, financial regulation and prudential standards;

(b) Act as banker, adviser and fiscal agent of the Government;

(c) Formulate and implement the foreign exchange policy of Sierra Leone;

(d) Conduct foreign-exchange operations;

(e) Own, hold and maintain the official international reserves including the reserves of gold;

(f) Issue and manage the currency of Sierra Leone;

(g) Establish, promote, license and oversee sound and efficient payment and securities settlement systems;

(h) License, register, regulate and supervise financial institutions as specified in this Act or any otherenactment;

(i) Act as a depository for funds from international organizations.

14

ANNUAL REPORT AND STATEMENT OF ACCOUNTS

1.0 GOVERNANCE

1.1 The Board of Directors

The Bank of Sierra Leone Act 2011 provides for a Board which shall consist of the Governor as theChairman, the Deputy Governor and five Non-Executive Directors, all of whom shall be appointedby the President subject to approval by Parliament.

The Governor and the Deputy Governor shall each be appointed for a term of five years and shallbe eligible for reappointment for another term only.

The Directors of the Board, who shall be persons with experience in economics, finance, banking,accounting and law, shall hold office for a term of three years and shall be eligible for reappointmentfor another term only

1.1.1 Functions of the Board

According to Section 17 of the Bank of Sierra Leone Act 2011, the functions of the Board are:

a) determine the organization of the Bank, including the establishment and location of branches,representative offices and operations facilities;

b) determine the general policies and adopt internal rules applicable to the administration and operationsof the Bank;

c) approve the annual budget of the Bank;

d) approve the audited accounts, annual reports and other formal reports and financial statements ofthe Bank;

e) determine denomination and design of banknotes, coins and their issuance and handling;f) appoint committees consisting of members of the Board or members of the Bank's staff and determine

their responsibilities;

g) assess risks and formulate contingency plans for the on-going operations and security of the Bank;

h) adopt the rules of procedure for meetings of the Board;

i) exercise all powers that are not specifically reserved for the Governor; and

j) perform other functions prescribed by the Act.

15

BANK OF SIERRA LEONE

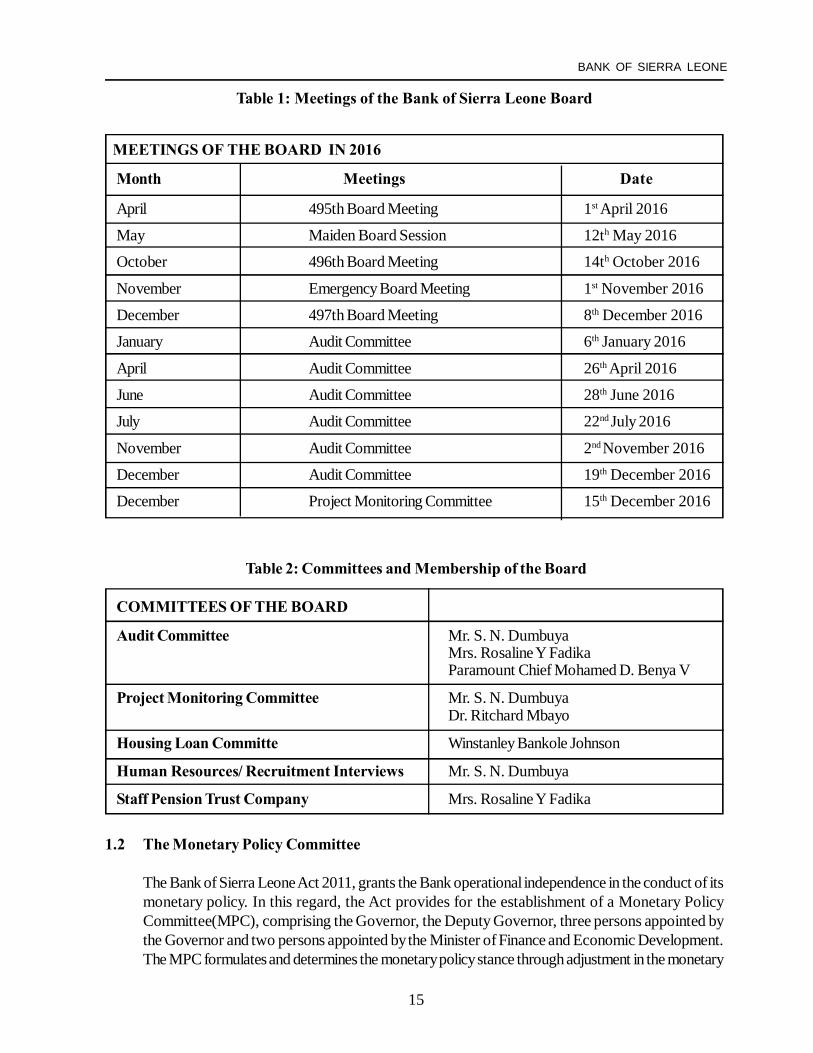

Table 1: Meetings of the Bank of Sierra Leone Board

MEETINGS OF THE BOARD IN 2016

Month Meetings Date

April 495th Board Meeting 1st April 2016

May Maiden Board Session 12th May 2016

October 496th Board Meeting 14th October 2016

November Emergency Board Meeting 1st November 2016

December 497th Board Meeting 8th December 2016

January Audit Committee 6th January 2016

April Audit Committee 26th April 2016

June Audit Committee 28th June 2016

July Audit Committee 22nd July 2016

November Audit Committee 2nd November 2016

December Audit Committee 19th December 2016

December Project Monitoring Committee 15th December 2016

Table 2: Committees and Membership of the Board

COMMITTEES OF THE BOARD

Audit Committee Mr. S. N. DumbuyaMrs. Rosaline Y FadikaParamount Chief Mohamed D. Benya V

Project Monitoring Committee Mr. S. N. DumbuyaDr. Ritchard Mbayo

Housing Loan Committe Winstanley Bankole Johnson

Human Resources/ Recruitment Interviews Mr. S. N. Dumbuya

Staff Pension Trust Company Mrs. Rosaline Y Fadika

1.2 The Monetary Policy Committee

The Bank of Sierra Leone Act 2011, grants the Bank operational independence in the conduct of itsmonetary policy. In this regard, the Act provides for the establishment of a Monetary PolicyCommittee(MPC), comprising the Governor, the Deputy Governor, three persons appointed bythe Governor and two persons appointed by the Minister of Finance and Economic Development.The MPC formulates and determines the monetary policy stance through adjustment in the monetary

16

ANNUAL REPORT AND STATEMENT OF ACCOUNTS

policy rate. The decisions of the MPC are informed by an assessment of the balance of risksbetween inflation and economic growth, based on developments in the domestic and internationalenvironments.

The MPC meets on a quarterly basis and held four meetings in 2016. The decisions on the monetarypolicy stance is communicated through a monetary policy statement, which is published on theBank's website and local newspapers, 48 hours after the MPC meetings.

As at end December 2016, the MPC comprised:

l Dr Kaifala Marah, Governor, Bank of Sierra Leone;

l Dr Ibrahim L Stevens, Deputy Governor, Bank of Sierra Leone;

l Mr Edmund Koroma, Financial Secretary, Ministry of Finance and Economic Development;

l Dr Milton B Ashley, Acting Head, Department of Banking and Finance, IPAM, Universityof Sierra Leone

l Mr Ibrahim K Lamin, Director, Financial Markets Department, Bank of Sierra Leone.

l Mr Mohamed Mansaray, Director, Research Department, Bank of Sierra Leone.

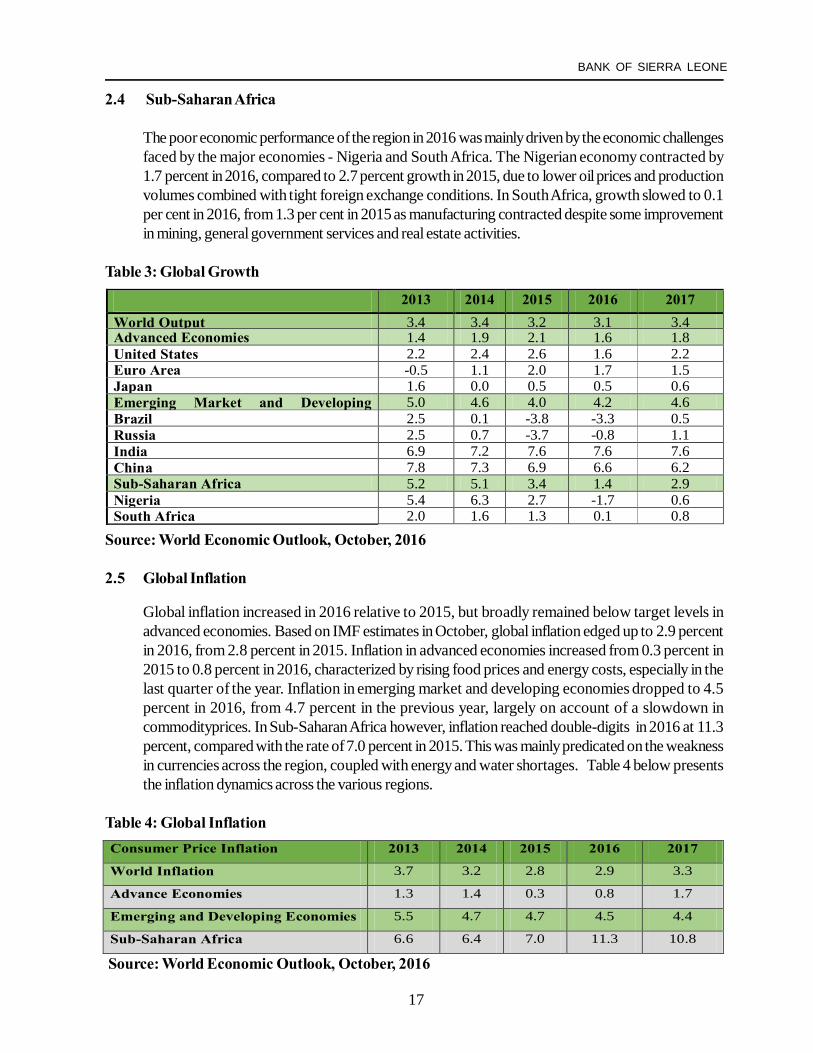

2.0 DEVELOPMENTS IN THE GLOBAL ECONOMY

2.1 Global Output Growth

Based on the World Economic Outlook (IMF, October 2016), World output growth was estimatedat 3.1 percent in 2016 against 3.2 percent in 2015. Growth in advanced economies declined to 1.6percent in 2016 from 2.1 percent in 2015. Similarly, growth in Sub-Saharan Africa declined from3.4 percent in 2015 to 1.4 percent in 2016, driven mainly by poor economic conditions in Nigeriaand South Africa - the major economies in the region. However, growth in emerging markets anddeveloping economies improved to 4.2 percent from the 4.0 percent recorded in 2015 as Russiaand Brazil were gradually emerging out of recession.

2.2 Advanced Economies

Amongst advanced economies, the United States recorded a modest growth of 1.6 percent in2016 compared with 2.6 percent in 2015 mainly driven by a slowdown in business activity. Growthin the euro area also dropped to 1.7 percent in 2016 after recording a growth of 2.0 percent in2015. Notwithstanding, growth in Japan remained unchanged at 0.5 percent in 2016, as the countrycontinues to recover from it poor performance in the preceding four years to 2015.

2.3 Emerging Market and Developing Economies

Contraction of growth in Brazil and Russia moderated in 2016. The two economies contracted by3.3 percent and 0.8 percent compared with contraction rates of 3.8 percent and 3.7 percentrespectively, in 2015. Growth in India remained at 7.6 percent, the same level as in 2015, whilegrowth in China slowed to 6.6 percent from 6.9 percent in 2015.

17

BANK OF SIERRA LEONE

2.4 Sub-Saharan Africa

The poor economic performance of the region in 2016 was mainly driven by the economic challengesfaced by the major economies - Nigeria and South Africa. The Nigerian economy contracted by1.7 percent in 2016, compared to 2.7 percent growth in 2015, due to lower oil prices and productionvolumes combined with tight foreign exchange conditions. In South Africa, growth slowed to 0.1per cent in 2016, from 1.3 per cent in 2015 as manufacturing contracted despite some improvementin mining, general government services and real estate activities.

Table 3: Global Growth

Source: World Economic Outlook, October, 2016

2.5 Global Inflation

Global inflation increased in 2016 relative to 2015, but broadly remained below target levels inadvanced economies. Based on IMF estimates in October, global inflation edged up to 2.9 percentin 2016, from 2.8 percent in 2015. Inflation in advanced economies increased from 0.3 percent in2015 to 0.8 percent in 2016, characterized by rising food prices and energy costs, especially in thelast quarter of the year. Inflation in emerging market and developing economies dropped to 4.5percent in 2016, from 4.7 percent in the previous year, largely on account of a slowdown incommodityprices. In Sub-Saharan Africa however, inflation reached double-digits in 2016 at 11.3percent, compared with the rate of 7.0 percent in 2015. This was mainly predicated on the weaknessin currencies across the region, coupled with energy and water shortages. Table 4 below presentsthe inflation dynamics across the various regions.

Table 4: Global Inflation

Source: World Economic Outlook, October, 2016

2013 2014 2015 2016 2017

World Output 3.4 3.4 3.2 3.1 3.4 Advanced Economies 1.4 1.9 2.1 1.6 1.8 United States 2.2 2.4 2.6 1.6 2.2

Euro Area -0.5 1.1 2.0 1.7 1.5 Japan 1.6 0.0 0.5 0.5 0.6

Emerging Market and Developing 5.0 4.6 4.0 4.2 4.6 Brazil 2.5 0.1 -3.8 -3.3 0.5 Russia 2.5 0.7 -3.7 -0.8 1.1 India 6.9 7.2 7.6 7.6 7.6 China 7.8 7.3 6.9 6.6 6.2 Sub-Saharan Africa 5.2 5.1 3.4 1.4 2.9 Nigeria 5.4 6.3 2.7 -1.7 0.6

South Africa 2.0 1.6 1.3 0.1 0.8

Consumer Price Inflation 2013 2014 2015 2016 2017

World Inflation 3.7 3.2 2.8 2.9 3.3

Advance Economies 1.3 1.4 0.3 0.8 1.7

Emerging and Developing Economies 5.5 4.7 4.7 4.5 4.4

Sub-Saharan Africa 6.6 6.4 7.0 11.3 10.8

Source: World Economic Outlook, October, 2016

18

ANNUAL REPORT AND STATEMENT OF ACCOUNTS

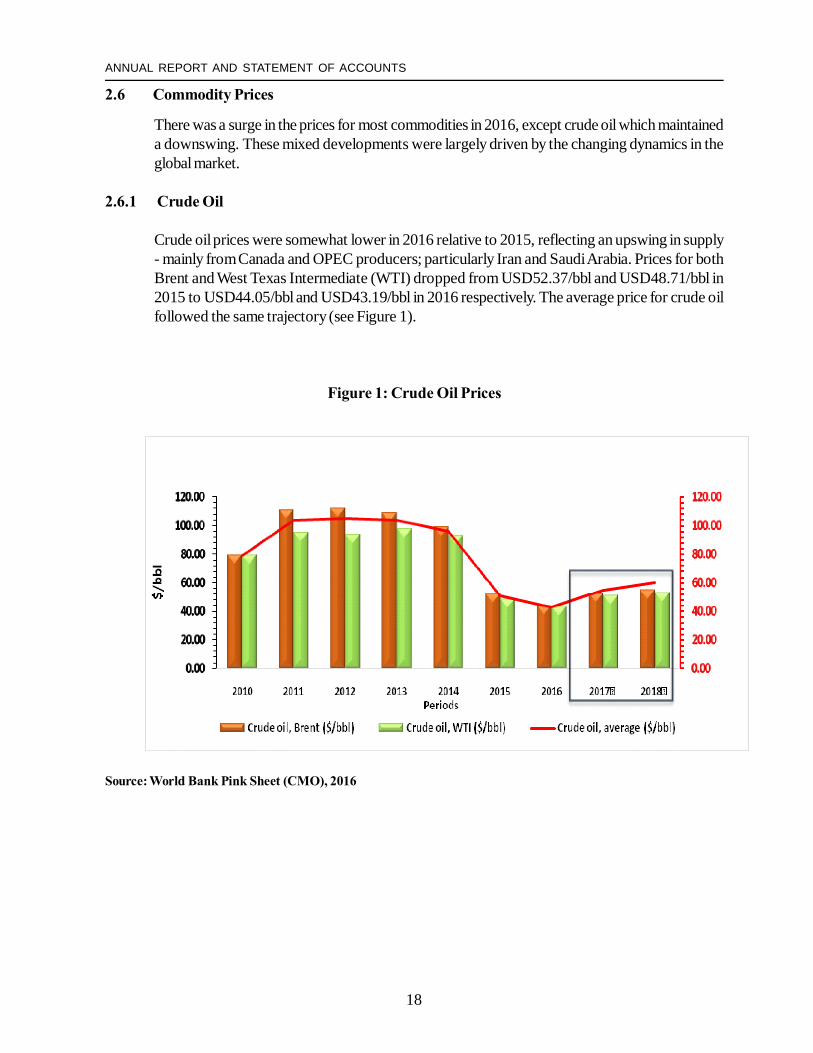

2.6 Commodity Prices

There was a surge in the prices for most commodities in 2016, except crude oil which maintaineda downswing. These mixed developments were largely driven by the changing dynamics in theglobal market.

2.6.1 Crude Oil

Crude oil prices were somewhat lower in 2016 relative to 2015, reflecting an upswing in supply- mainly from Canada and OPEC producers; particularly Iran and Saudi Arabia. Prices for bothBrent and West Texas Intermediate (WTI) dropped from USD52.37/bbl and USD48.71/bbl in2015 to USD44.05/bbl and USD43.19/bbl in 2016 respectively. The average price for crude oilfollowed the same trajectory (see Figure 1).

Figure 1: Crude Oil Prices

Source: World Bank Pink Sheet (CMO), 2016

19

BANK OF SIERRA LEONE

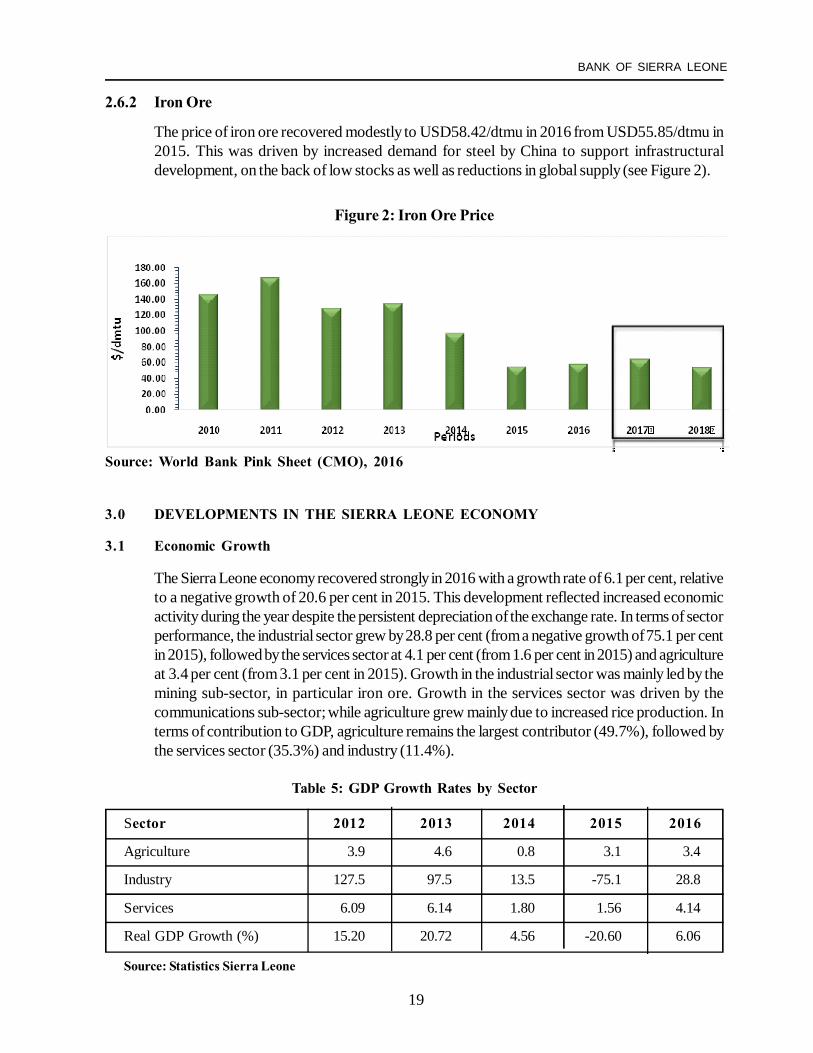

2.6.2 Iron Ore

The price of iron ore recovered modestly to USD58.42/dtmu in 2016 from USD55.85/dtmu in2015. This was driven by increased demand for steel by China to support infrastructuraldevelopment, on the back of low stocks as well as reductions in global supply (see Figure 2).

Figure 2: Iron Ore Price

Source: World Bank Pink Sheet (CMO), 2016

3.0 DEVELOPMENTS IN THE SIERRA LEONE ECONOMY

3.1 Economic Growth

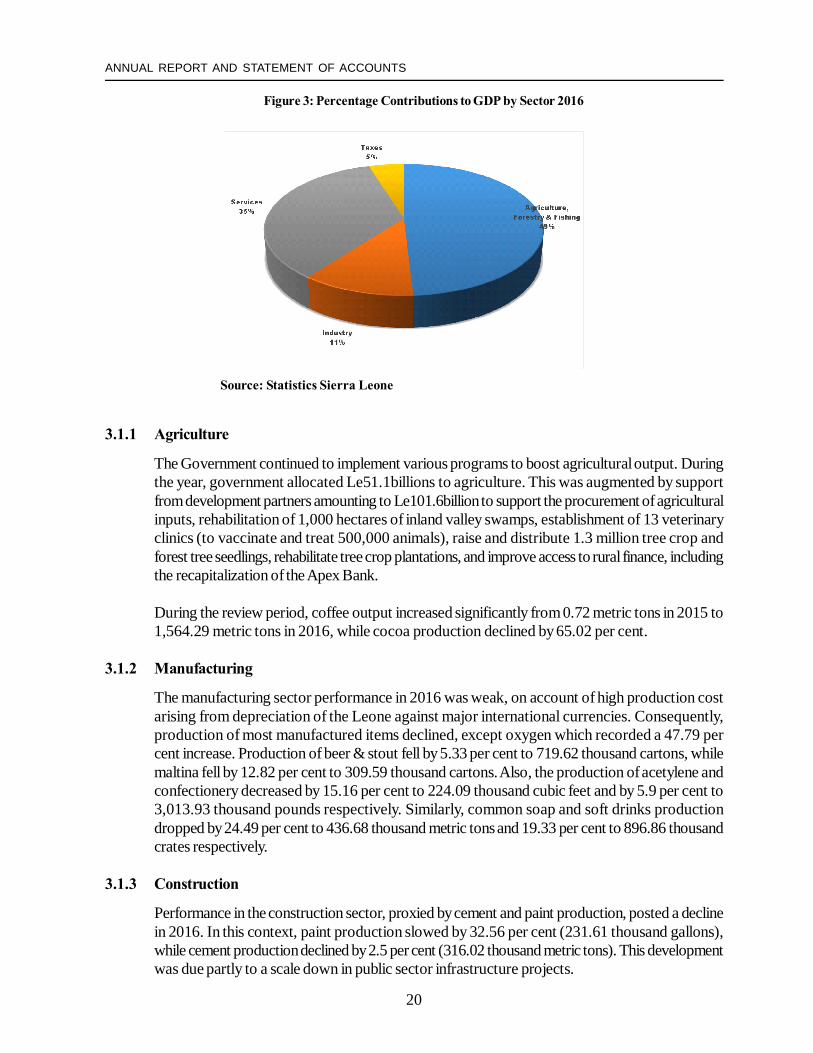

The Sierra Leone economy recovered strongly in 2016 with a growth rate of 6.1 per cent, relativeto a negative growth of 20.6 per cent in 2015. This development reflected increased economicactivity during the year despite the persistent depreciation of the exchange rate. In terms of sectorperformance, the industrial sector grew by 28.8 per cent (from a negative growth of 75.1 per centin 2015), followed by the services sector at 4.1 per cent (from 1.6 per cent in 2015) and agricultureat 3.4 per cent (from 3.1 per cent in 2015). Growth in the industrial sector was mainly led by themining sub-sector, in particular iron ore. Growth in the services sector was driven by thecommunications sub-sector; while agriculture grew mainly due to increased rice production. Interms of contribution to GDP, agriculture remains the largest contributor (49.7%), followed bythe services sector (35.3%) and industry (11.4%).

Table 5: GDP Growth Rates by Sector

Sector 2012 2013 2014 2015 2016

Agriculture 3.9 4.6 0.8 3.1 3.4

Industry 127.5 97.5 13.5 -75.1 28.8

Services 6.09 6.14 1.80 1.56 4.14

Real GDP Growth (%) 15.20 20.72 4.56 -20.60 6.06

Source: Statistics Sierra Leone

20

ANNUAL REPORT AND STATEMENT OF ACCOUNTS

Figure 3: Percentage Contributions to GDP by Sector 2016

Source: Statistics Sierra Leone

3.1.1 Agriculture

The Government continued to implement various programs to boost agricultural output. Duringthe year, government allocated Le51.1billions to agriculture. This was augmented by supportfrom development partners amounting to Le101.6billion to support the procurement of agriculturalinputs, rehabilitation of 1,000 hectares of inland valley swamps, establishment of 13 veterinaryclinics (to vaccinate and treat 500,000 animals), raise and distribute 1.3 million tree crop andforest tree seedlings, rehabilitate tree crop plantations, and improve access to rural finance, includingthe recapitalization of the Apex Bank.

During the review period, coffee output increased significantly from 0.72 metric tons in 2015 to1,564.29 metric tons in 2016, while cocoa production declined by 65.02 per cent.

3.1.2 Manufacturing

The manufacturing sector performance in 2016 was weak, on account of high production costarising from depreciation of the Leone against major international currencies. Consequently,production of most manufactured items declined, except oxygen which recorded a 47.79 percent increase. Production of beer & stout fell by 5.33 per cent to 719.62 thousand cartons, whilemaltina fell by 12.82 per cent to 309.59 thousand cartons. Also, the production of acetylene andconfectionery decreased by 15.16 per cent to 224.09 thousand cubic feet and by 5.9 per cent to3,013.93 thousand pounds respectively. Similarly, common soap and soft drinks productiondropped by 24.49 per cent to 436.68 thousand metric tons and 19.33 per cent to 896.86 thousandcrates respectively.

3.1.3 Construction

Performance in the construction sector, proxied by cement and paint production, posted a declinein 2016. In this context, paint production slowed by 32.56 per cent (231.61 thousand gallons),while cement production declined by 2.5 per cent (316.02 thousand metric tons). This developmentwas due partly to a scale down in public sector infrastructure projects.

21

BANK OF SIERRA LEONE

3.1.4 Mining

Mining activities improved in 2016 compared to 2015. Diamond production increased by 9.81per cent to 549.10 thousand carats compared to 500.04 thousand carats in 2015. Of this total,industrial diamonds accounted for 23.96 per cent, while gem accounted for 76.12 per cent.Production increases were also recorded for rutile, gold and iron ore. Rutile production grew by17.87 per cent to 148.54 thousand metric tons, Gold rose by 74.43 percent to 6.04 thousandounces, and Iron ore production expanded by 265.17 percent to 6,175.96 thousand metric tons.In contrast, Bauxite production dropped by 3.13 per cent to 1,429.59 thousand metric tons,Ileminite by 25.33 percent to 28.10 thousand metric tons, and Zircon by 4.32 percent to 1.33thousand metric tons.

3.1.5 Electricity Generation

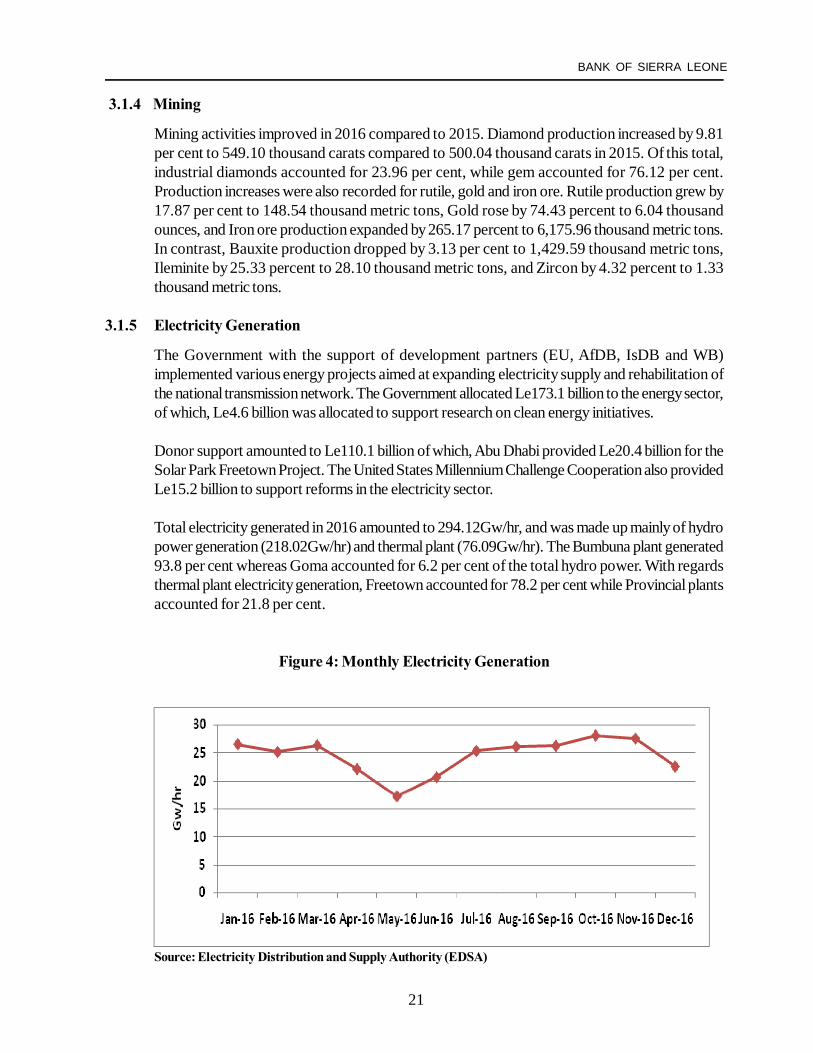

The Government with the support of development partners (EU, AfDB, IsDB and WB)implemented various energy projects aimed at expanding electricity supply and rehabilitation ofthe national transmission network. The Government allocated Le173.1 billion to the energy sector,of which, Le4.6 billion was allocated to support research on clean energy initiatives.

Donor support amounted to Le110.1 billion of which, Abu Dhabi provided Le20.4 billion for theSolar Park Freetown Project. The United States Millennium Challenge Cooperation also providedLe15.2 billion to support reforms in the electricity sector.

Total electricity generated in 2016 amounted to 294.12Gw/hr, and was made up mainly of hydropower generation (218.02Gw/hr) and thermal plant (76.09Gw/hr). The Bumbuna plant generated93.8 per cent whereas Goma accounted for 6.2 per cent of the total hydro power. With regardsthermal plant electricity generation, Freetown accounted for 78.2 per cent while Provincial plantsaccounted for 21.8 per cent.

Figure 4: Monthly Electricity Generation

Source: Electricity Distribution and Supply Authority (EDSA)

22

ANNUAL REPORT AND STATEMENT OF ACCOUNTS

3.1.6 Tourism

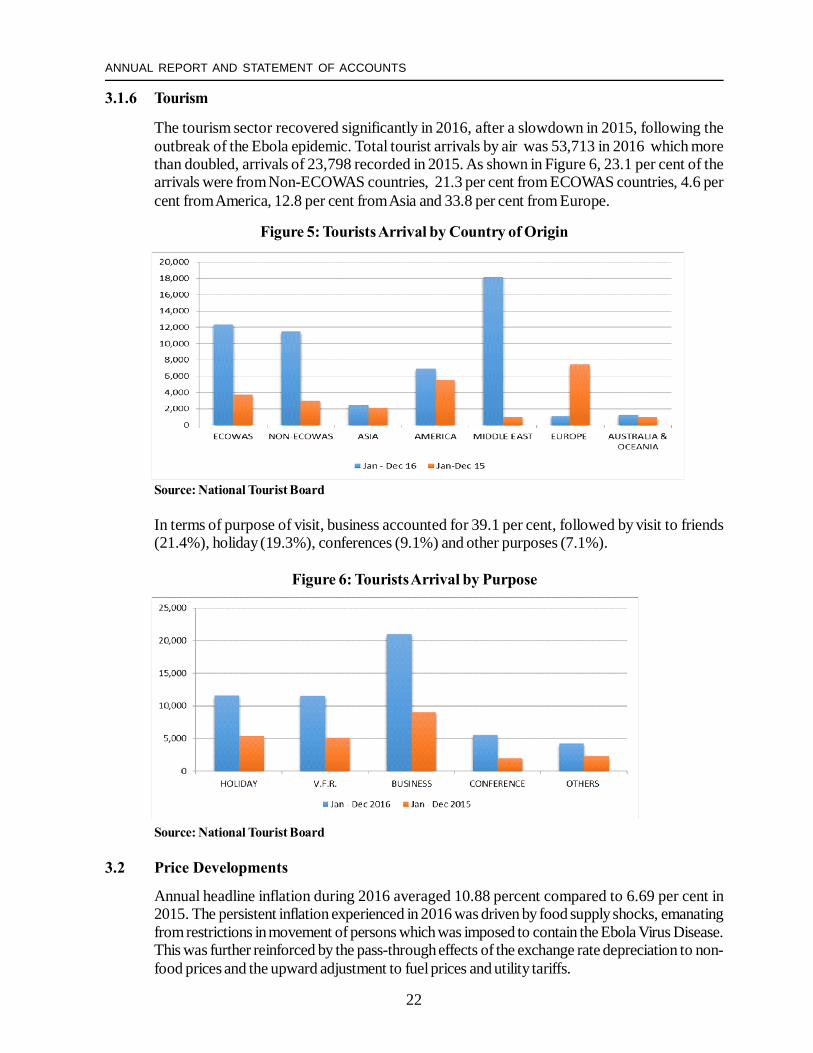

The tourism sector recovered significantly in 2016, after a slowdown in 2015, following theoutbreak of the Ebola epidemic. Total tourist arrivals by air was 53,713 in 2016 which morethan doubled, arrivals of 23,798 recorded in 2015. As shown in Figure 6, 23.1 per cent of thearrivals were from Non-ECOWAS countries, 21.3 per cent from ECOWAS countries, 4.6 percent from America, 12.8 per cent from Asia and 33.8 per cent from Europe.

Figure 5: Tourists Arrival by Country of Origin

Source: National Tourist Board

In terms of purpose of visit, business accounted for 39.1 per cent, followed by visit to friends(21.4%), holiday (19.3%), conferences (9.1%) and other purposes (7.1%).

Figure 6: Tourists Arrival by Purpose

Source: National Tourist Board

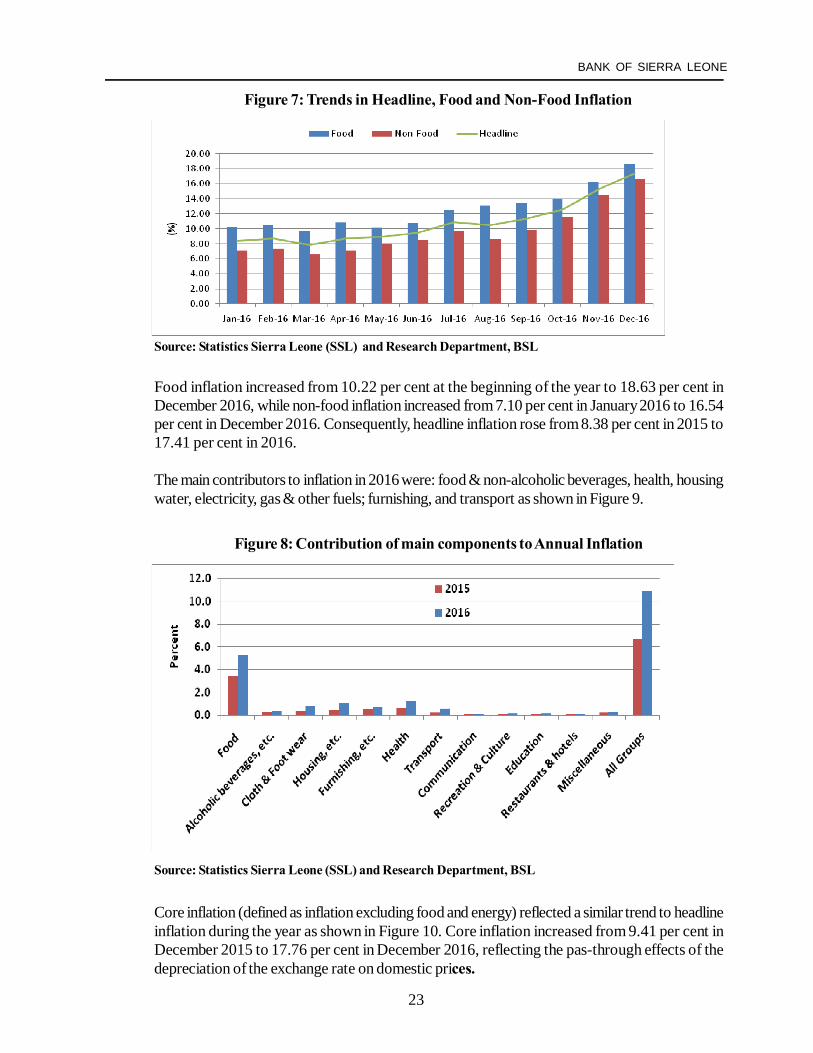

3.2 Price Developments

Annual headline inflation during 2016 averaged 10.88 percent compared to 6.69 per cent in2015. The persistent inflation experienced in 2016 was driven by food supply shocks, emanatingfrom restrictions in movement of persons which was imposed to contain the Ebola Virus Disease.This was further reinforced by the pass-through effects of the exchange rate depreciation to non-food prices and the upward adjustment to fuel prices and utility tariffs.

23

BANK OF SIERRA LEONE

Source: Statistics Sierra Leone (SSL) and Research Department, BSL

Food inflation increased from 10.22 per cent at the beginning of the year to 18.63 per cent inDecember 2016, while non-food inflation increased from 7.10 per cent in January 2016 to 16.54per cent in December 2016. Consequently, headline inflation rose from 8.38 per cent in 2015 to17.41 per cent in 2016.

The main contributors to inflation in 2016 were: food & non-alcoholic beverages, health, housingwater, electricity, gas & other fuels; furnishing, and transport as shown in Figure 9.

Figure 8: Contribution of main components to Annual Inflation

Source: Statistics Sierra Leone (SSL) and Research Department, BSL

Core inflation (defined as inflation excluding food and energy) reflected a similar trend to headlineinflation during the year as shown in Figure 10. Core inflation increased from 9.41 per cent inDecember 2015 to 17.76 per cent in December 2016, reflecting the pas-through effects of thedepreciation of the exchange rate on domestic prices.

Figure 7: Trends in Headline, Food and Non-Food Inflation

24

ANNUAL REPORT AND STATEMENT OF ACCOUNTS

Figure 9: Headline and Core Inflation

Source: Statistics Sierra Leone (SSL) and Research Department, BSL

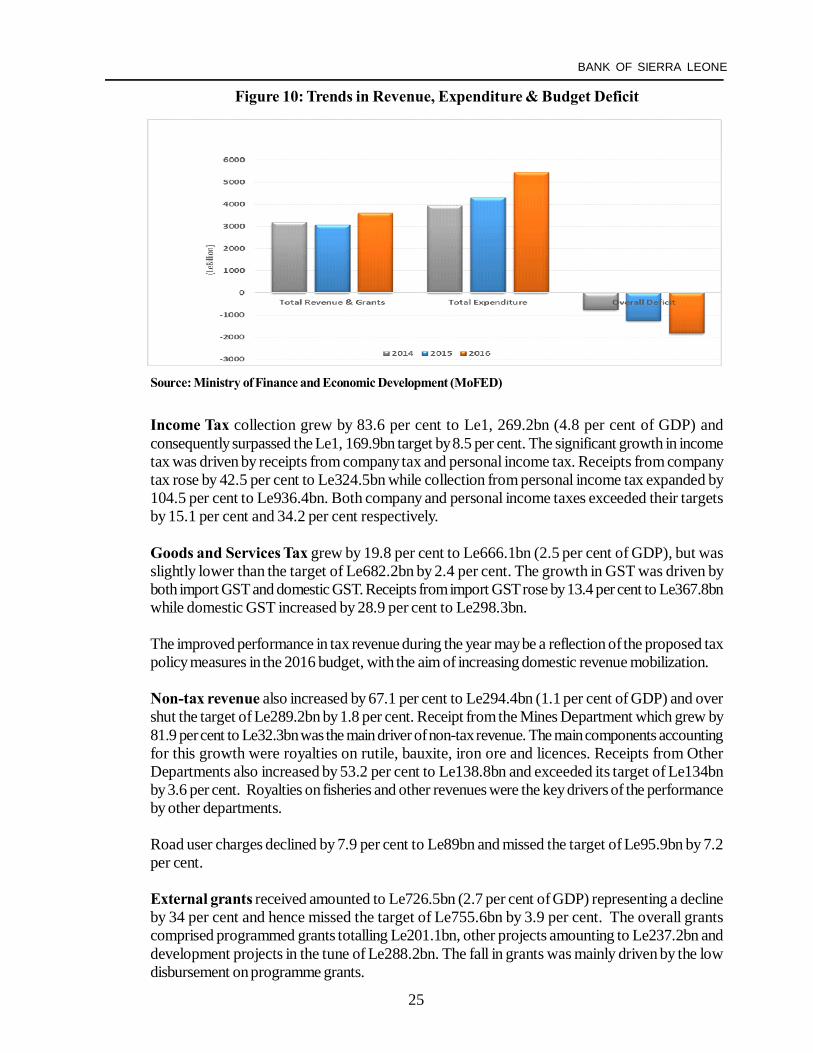

3.3 Fiscal Policy and Government Budgetary Operations

The 2016 budget was driven by the National Ebola Recovery Strategy (NERS). The strategyfocused on fiscal sustainability through enhanced domestic revenue mobilization and expenditurerationalization with the aim of strengthening resilience and building a diversified economy.

Government fiscal deficit including grants in 2016 was 6.9 per cent of GDP against a targeteddeficit of 4.5 per cent. Overall fiscal deficit excluding grants was 9.6 per cent of GDP comparedto a target of 7.3 per cent.

3.3.1 Government Revenue

Government revenue including grants, grew by 18.2 per cent to Le3, 615.2bn and exceededthe target of LeLe3, 553.5bn by 1.7 per cent. The improvement in revenue was mainly attributedto the increase in domestic revenue collection.

Tax revenue increased by 48.6 per cent to Le2, 505.4bn (9.4 per cent of GDP) andexceeded the target of Le2, 412.8bn by 3.8 per cent. Tax revenue during the period accountedfor 69.3 per cent of total revenue and grants compared to 55.1 per cent in 2015. Thisimprovement in revenue collection was reflected in all the main tax categories: Customs andExcise, Income Tax and Goods and Services Tax (GST).

Customs and Excise receipts increased by 29.8 per cent to Le570.1bn (2.2 per cent of GDP)and exceeded the budgeted target of Le560.8bn by 1.7 per cent. This expansion was on accountof increases in receipts from import taxes by 68.3 per cent to Le381.6bn, and growth in otherexcise duties by 24 per cent to Le20bn.

25

BANK OF SIERRA LEONE

Figure 10: Trends in Revenue, Expenditure & Budget Deficit

Source: Ministry of Finance and Economic Development (MoFED)

Income Tax collection grew by 83.6 per cent to Le1, 269.2bn (4.8 per cent of GDP) andconsequently surpassed the Le1, 169.9bn target by 8.5 per cent. The significant growth in incometax was driven by receipts from company tax and personal income tax. Receipts from companytax rose by 42.5 per cent to Le324.5bn while collection from personal income tax expanded by104.5 per cent to Le936.4bn. Both company and personal income taxes exceeded their targetsby 15.1 per cent and 34.2 per cent respectively.

Goods and Services Tax grew by 19.8 per cent to Le666.1bn (2.5 per cent of GDP), but wasslightly lower than the target of Le682.2bn by 2.4 per cent. The growth in GST was driven byboth import GST and domestic GST. Receipts from import GST rose by 13.4 per cent to Le367.8bnwhile domestic GST increased by 28.9 per cent to Le298.3bn.

The improved performance in tax revenue during the year may be a reflection of the proposed taxpolicy measures in the 2016 budget, with the aim of increasing domestic revenue mobilization.

Non-tax revenue also increased by 67.1 per cent to Le294.4bn (1.1 per cent of GDP) and overshut the target of Le289.2bn by 1.8 per cent. Receipt from the Mines Department which grew by81.9 per cent to Le32.3bn was the main driver of non-tax revenue. The main components accountingfor this growth were royalties on rutile, bauxite, iron ore and licences. Receipts from OtherDepartments also increased by 53.2 per cent to Le138.8bn and exceeded its target of Le134bnby 3.6 per cent. Royalties on fisheries and other revenues were the key drivers of the performanceby other departments.

Road user charges declined by 7.9 per cent to Le89bn and missed the target of Le95.9bn by 7.2per cent.

External grants received amounted to Le726.5bn (2.7 per cent of GDP) representing a declineby 34 per cent and hence missed the target of Le755.6bn by 3.9 per cent. The overall grantscomprised programmed grants totalling Le201.1bn, other projects amounting to Le237.2bn anddevelopment projects in the tune of Le288.2bn. The fall in grants was mainly driven by the lowdisbursement on programme grants.

26

ANNUAL REPORT AND STATEMENT OF ACCOUNTS

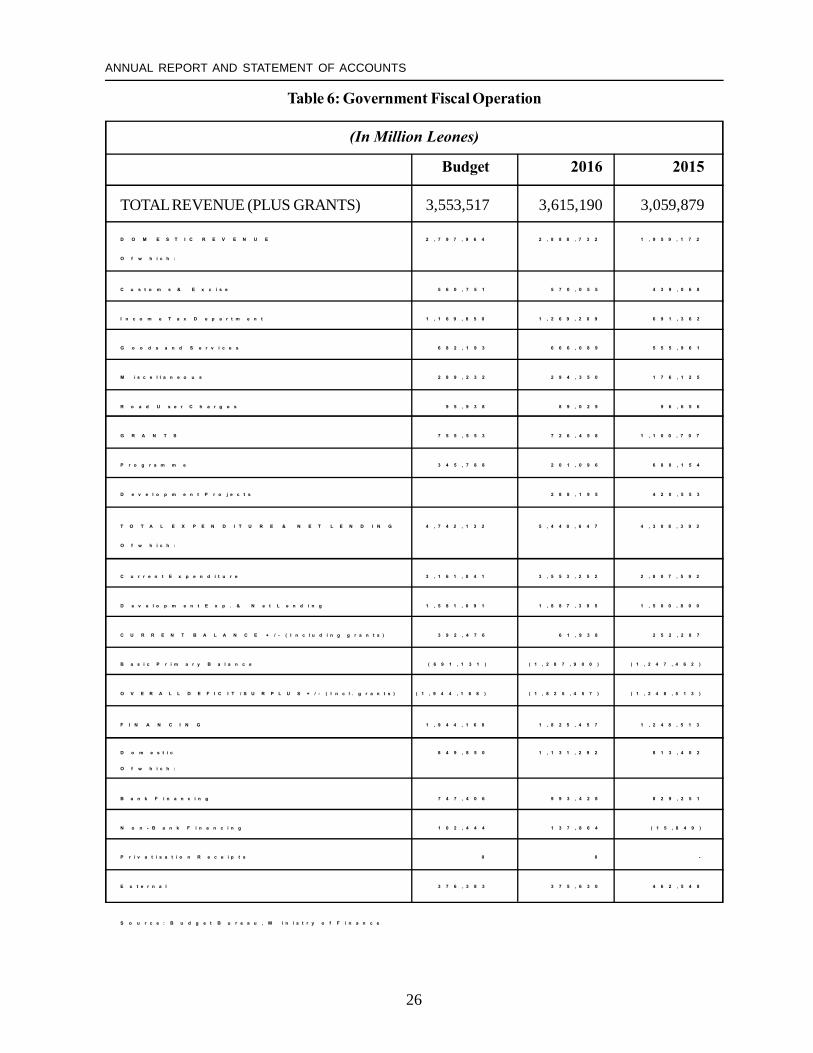

Table 6: Government Fiscal Operation

(In Million Leones)

Budget 2016 2015

TOTAL REVENUE (PLUS GRANTS) 3,553,517 3,615,190 3,059,879

D O M E S T I C R E V E N U E 2 , 7 9 7 , 9 6 4 2 , 8 8 8 , 7 3 2 1 , 9 5 9 , 1 7 2

O f w h i c h :

C u s t o m s & E x c i s e 5 6 0 , 7 5 1 5 7 0 , 0 5 5 4 3 9 , 0 6 8

I n c o m e T a x D e p a r t m e n t 1 , 1 6 9 , 8 5 0 1 , 2 6 9 , 2 0 9 6 9 1 , 3 6 2

G o o d s a n d S e r v i c e s 6 8 2 , 1 9 3 6 6 6 , 0 8 9 5 5 5 , 9 6 1

M i s c e l l a n e o u s 2 8 9 , 2 3 2 2 9 4 , 3 5 0 1 7 6 , 1 2 5

R o a d U s e r C h a r g e s 9 5 , 9 3 8 8 9 , 0 2 9 9 6 , 6 5 6

G R A N T S 7 5 5 , 5 5 3 7 2 6 , 4 5 8 1 , 1 0 0 , 7 0 7

P r o g r a m m e 3 4 5 , 7 8 8 2 0 1 , 0 9 6 6 8 0 , 1 5 4

D e v e l o p m e n t P r o j e c t s 2 8 8 , 1 9 5 4 2 0 , 5 5 3

T O T A L E X P E N D I T U R E & N E T L E N D I N G 4 , 7 4 2 , 1 3 2 5 , 4 4 0 , 6 4 7 4 , 3 0 8 , 3 9 2

O f w h i c h :

C u r r e n t E x p e n d i t u r e 3 , 1 6 1 , 0 4 1 3 , 5 5 3 , 2 5 2 2 , 8 0 7 , 5 9 2

D e v e l o p m e n t E x p . & N e t L e n d i n g 1 , 5 8 1 , 0 9 1 1 , 8 8 7 , 3 9 5 1 , 5 0 0 , 8 0 0

C U R R E N T B A L A N C E + / - ( I n c l u d i n g g r a n t s ) 3 9 2 , 4 7 6 6 1 , 9 3 8 2 5 2 , 2 8 7

B a s i c P r i m a r y B a l a n c e ( 6 9 1 , 1 3 1 ) ( 1 , 2 8 7 , 9 0 0 ) ( 1 , 2 4 7 , 4 6 2 )

O V E R A L L D E F I C I T / S U R P L U S + / - ( I n c l . g r a n t s ) ( 1 , 9 4 4 , 1 6 8 ) ( 1 , 8 2 5 , 4 5 7 ) ( 1 , 2 4 8 , 5 1 3 )

F I N A N C I N G 1 , 9 4 4 , 1 6 8 1 , 8 2 5 , 4 5 7 1 , 2 4 8 , 5 1 3

D o m e s t i c 8 4 9 , 8 5 0 1 , 1 3 1 , 2 9 2 8 1 3 , 4 0 2

O f w h i c h :

B a n k F i n a n c i n g 7 4 7 , 4 0 6 9 9 3 , 4 2 8 8 2 9 , 2 5 1

N o n - B a n k F i n a n c i n g 1 0 2 , 4 4 4 1 3 7 , 8 6 4 ( 1 5 , 8 4 9 )

P r i v a t i s a t i o n R e c e i p t s 0 0 -

E x t e r n a l 3 7 6 , 3 8 3 3 7 5 , 6 3 0 4 6 2 , 5 4 8

S o u r c e : B u d g e t B u r e a u , M i n i s t r y o f F i n a n c e

27

BANK OF SIERRA LEONE

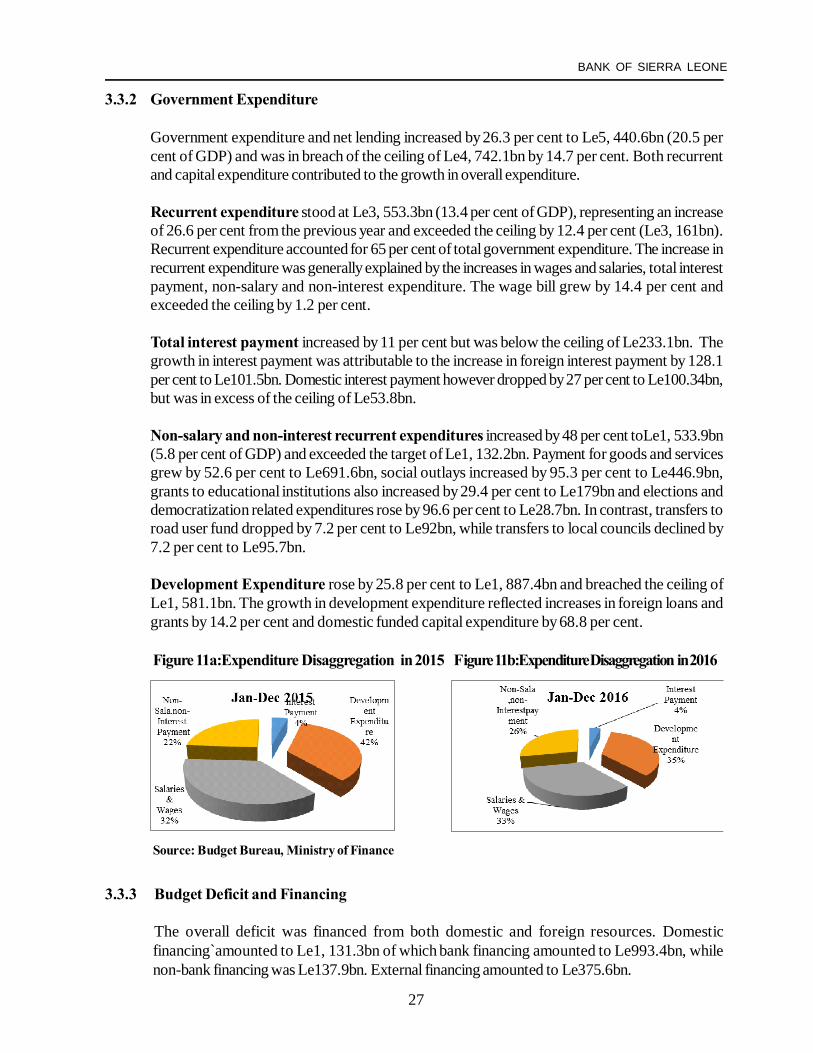

3.3.2 Government Expenditure

Government expenditure and net lending increased by 26.3 per cent to Le5, 440.6bn (20.5 percent of GDP) and was in breach of the ceiling of Le4, 742.1bn by 14.7 per cent. Both recurrentand capital expenditure contributed to the growth in overall expenditure.

Recurrent expenditure stood at Le3, 553.3bn (13.4 per cent of GDP), representing an increaseof 26.6 per cent from the previous year and exceeded the ceiling by 12.4 per cent (Le3, 161bn).Recurrent expenditure accounted for 65 per cent of total government expenditure. The increase inrecurrent expenditure was generally explained by the increases in wages and salaries, total interestpayment, non-salary and non-interest expenditure. The wage bill grew by 14.4 per cent andexceeded the ceiling by 1.2 per cent.

Total interest payment increased by 11 per cent but was below the ceiling of Le233.1bn. Thegrowth in interest payment was attributable to the increase in foreign interest payment by 128.1per cent to Le101.5bn. Domestic interest payment however dropped by 27 per cent to Le100.34bn,but was in excess of the ceiling of Le53.8bn.

Non-salary and non-interest recurrent expenditures increased by 48 per cent toLe1, 533.9bn(5.8 per cent of GDP) and exceeded the target of Le1, 132.2bn. Payment for goods and servicesgrew by 52.6 per cent to Le691.6bn, social outlays increased by 95.3 per cent to Le446.9bn,grants to educational institutions also increased by 29.4 per cent to Le179bn and elections anddemocratization related expenditures rose by 96.6 per cent to Le28.7bn. In contrast, transfers toroad user fund dropped by 7.2 per cent to Le92bn, while transfers to local councils declined by7.2 per cent to Le95.7bn.

Development Expenditure rose by 25.8 per cent to Le1, 887.4bn and breached the ceiling ofLe1, 581.1bn. The growth in development expenditure reflected increases in foreign loans andgrants by 14.2 per cent and domestic funded capital expenditure by 68.8 per cent.

Figure 11a:Expenditure Disaggregation in 2015 F igure 11b:Expenditure Disaggregation in 2016

Source: Budget Bureau, Ministry of Finance

3.3.3 Budget Deficit and Financing

The overall deficit was financed from both domestic and foreign resources. Domesticfinancing`amounted to Le1, 131.3bn of which bank financing amounted to Le993.4bn, whilenon-bank financing was Le137.9bn. External financing amounted to Le375.6bn.

28

ANNUAL REPORT AND STATEMENT OF ACCOUNTS

4.0 Monetary Developments

4.1 Monetary Policy Stance and Challenges

Monetary policy in 2016 was geared towards achieving an end-year inflation target of 9.5 percent,stability of the exchange rate and accumulation of a level of international reserves equivalent tothree months of imports of goods and services. In addition, monetary policy was tailored tosupport the Government's Post Ebola Recovery Priorities.

During the year 2016, the implementation of monetary policy was challenged by significantdepreciation of the exchange rate, food supply shock and upward adjustments in the pump priceof fuel and electricity tariffs, which together had knock-on effects on domestic prices. Consequently,domestic prices remained high throughout the year resulting to an inflation rate of 17.41 per cent,as of December 2016 which was above the end year target of 9.5 percent.

Notwithstanding the price developments, the Monetary Policy Committee (MPC) in its quarterone and two meetings maintained Monetary Policy Rate at 9.5 per cent, motivated by the need tosupport the economic recovery process in the face of negative output gap.

However, in the second half of the year, to contain the second round effects of additional supply-side inflationary shocks, coupled with the depreciation of the exchange rate, the MPC judged thattightening of monetary policy was warranted. Consequently, the MPR was raised cumulatively by150 basis points from 9.5 per cent in June 2016 to 11.0 per cent in December 2016.

To further improve on the transmission of monetary policy signals and limit interest rate volatility inthe money market, BSL in September 2016 introduced an Interest Rate Corridor System. Thiscorridor consists of a Standing Deposit Facility (SDF) rate set at the lower bound and a StandingLending Facility (SLF) set at the upper bound, both accessible at the discretion of the commercialbanks. At the inception of this corridor, the SDF rate was set at 400 basis points below the MPRand the SLF set at100 basis point above the MPR.

4.2 Developments in Monetary Aggregates

Broad Money (M2) expanded by 16.49 per cent, higher than the 11.34 per cent growth raterecorded in the preceding year, but was within end of year ECF program target of 17.9 per cent.The expansion in M2 was attributed to the increase in Net Domestic Assets (NDA) of the bankingsystem, which was reinforced by a moderate growth in Net Foreign Assets (NFA) of the bankingsystem. The NDA expanded by 31.69 per cent and contributed 13.10 per cent to the growth inM2. The increase in NDA was mostly as a result of fiscal operations which was financed mainlyby the banking system through increased utilization of 'Ways and Means Accounts' (from Le24.34bnin December 2015 to Le48.18bn in December 2016) and increases in government security holdingsby commercial banks amounting to (Le267.52bn).

In addition, the growth in NDA was reinforced by credit extended to the private sector bycommercial banks. Private sector credit registered a 16.93 per cent increase, far higher than the2.15 per cent growth recorded in the preceding year of 2015.

29

BANK OF SIERRA LEONE

In terms of sectorial distribution of private sector credit, the construction sector benefited themost with Le 290.02mn, followed by import trade amounting to Le 271.34mn and other sectorsas shown in Figure 13.

NFA expanded by 5.78 per cent and contributed to the growth in M2 by 3.40 per cent. Thisgrowth in NFA was mainly driven by foreign currency importation by commercial banks(Le10.47bn), export receipts and royalties paid by mining companies (Le39.70bn) and increasein the claims on overseas banks by commercial banks (Le329.32bn). Other inflows included theIMF and other donor partners in respect to the ECF programme (Le583.59bn), Airtel capitalgain tax (Le30bn), and BSL's interest income from BIS (Le11.79bn).

However the growth in NFA was moderated due to significant autonomous outflows during theyear such as; wholesale foreign exchange auction, salaries, wages and allowances for embassiesand foreign missions, rehabilitation of roads and medical projects by the government, debt servicesand subscriptions to development partners, payment for reprinting of banknotes and revaluationeffect on foreign assets and liabilities arising from the depreciation of the Leone against the USdollar and other major international currencies.

On the liability side of M2, currency-in-circulation increased by 7.57 per cent while demanddeposits increased by 6.62 per cent. Foreign currency deposits and time deposits increased by56 per cent and 24 per cent respectively, reflecting capital accumulation through the bankingsystem .

Reserve Money (RM) increased by 24.50 per cent, which is higher than the 10.46 per centgrowth recorded in 2015, and slightly above the program target (23.9%).

4.3 Interest Rates

Yields rates in government securities market generally increased in 2016, except for the interestrate on one year treasury bond which remained unchanged at 5 per cent. As at end December,2016, average yield on 91 days treasury bills increased by 830 basis points, from 1.08 per centin December, 2015 to 9.38 per cent in December, 2016 while the 182 days and 364 daysincreased by 1,306 and 2,031 basis points from 3.11 per cent to 16.17 per cent and 9.91 percentto 30.22 per cent respectively for the same period. The yield on the 364 days treasury bills wasrelatively high and rose up to 33.21 per cent on 17th November, 2016.

In the interbank market, the average weighted yield increased by 680 basis points from 2.86 percent in December 2015 to 9.66 per cent as at end December, 2016. Figure 13 below shows thetrend in the yields/rates of government securities in the primary and interbank markets.

The interest rate on savings deposits declined from 2.54 per cent to 2.38 per cent, whereasinterest rates on time deposits with different maturities declined as follows: 1-month from 2.73 percent to 2.57 per cent, 3-months from 2.98 per cent to 2.87 per cent and 6-months from 4.20 percent to 4.07 per cent. Interest rate on the twelve months' time deposit decreased slightly from6.59 per cent to 5.84 per cent, whereas the rate on nine months' time deposits was unchanged at3.38 per cent. On the lending side, the average lending rate by commercial banks moved downslightly from the range of 18.12 - 24.80 per cent to 17.92 - 24.77 per cent.

30

ANNUAL REPORT AND STATEMENT OF ACCOUNTS

Figure 12: Trend in the Yields of Government Securitiesin the Primary and Secondary Markets

Source: Bank of Sierra Leone

4.4 Developments in Government Securities Market

The primary market for Government securities in 2016, exhibited oversubscription in the 364 daysT-bills while the 91 and 182 days T-bills were under-subscribed. The one year Treasury bond wasalso largely undersubscribed in 2016. At the same time, a two years treasury bond was discontinueddue to persistent under-subscription.

The stock of marketable government securities increased by 28.06 per cent from Le2, 248.41bnrecorded in 2015, to Le2, 879.32bn in 2016. During the year, demand for Government securitieswas skewed towards the long end of the market, as the stock of the 364 days T- bills accounted for91.07 per cent in 2016.

Consequently, the 364 days T-bills increased by Le785.10bn (42.73%) from Le1, 837.23bn toLe2, 622.33bn for the same periods. On the other hand, the stock of 182 days T-bills dropped byLe151.05bn (66.58%) from Le226.85bn at end December 2015, to Le75.80bn as at end December2016, Similarly, the stock of 91 days T-bills decreased by Le20.27bn (42.35%) to Le27.59bn in2016.

With regard to the treasury bonds, the stock of one year Treasury bond decreased by Le30.95bn(40.34%) from Le76.72bn at end December, 2015 to Le45.77bn as at end December, 2016,whereas that for the two year treasury bonds increased from Le59.72bn at end December 2015 toLe66.75bn as at end December 2016. During 2016, the Government also issued 5 Year TreasuryBonds to NASSIT valued at Le41.07bn

31

BANK OF SIERRA LEONE

Figure 13: Stock of Government Securities by Tenure

Source: Bank of Sierra Leone

In 2016, holdings of marketable Government securities (see Figure 14) increased in all sectors,with commercial banks, as a major holder, increased their holdings by Le270.84bn (13.91%) toLe2, 217.28bn. Similarly, BSL holdings increased substantially by Le222.21bn to Le244.53bn in2016, mainly due to the outright purchase of T-bills from the banks to provide liquidity to themarket. Non-Bank Public Sector holdings (excluding NASSIT) increased by Le77.65bn fromLe191.67bn as at end December, 2015 to Le269.32bn as at end December, 2016. NASSITholdings also increased by Le60.21bn from Le87.98bn as at end December, 2015 to Le148.19bnas at end December, 2016.

Figure 14: Holdings of Government Securities by Sector (In Billions of Leones)

Source: Bank of Sierra Leone

With regards developments in the secondary market, the volume of interbank transactionsamounted to Le1, 370.58bn in 2016, about 54.74 per cent higher compared to the volumerecorded in 2015. As a result of liquidity constraints, commercial banks accessed the BSL'sStanding Lending Facility for the amount of Le1, 074.00bn in 2016, despite the injection ofLe608.19bn through outright purchase of T-bills by BSL.

32

ANNUAL REPORT AND STATEMENT OF ACCOUNTS

Table 7: Stock of Marketable Government Securities Outstanding by Holder (in Millions of Leones)

Dec-15 Dec-16 Change

91 Days Treasury Bearer Bonds 47,868.75 27,594.20 (20,274.15)Bank of Sierra Leone 5,090.15 - (5,090.15)Commercial Banks 21,721.55 16,965.20 (4,763.35)Non-Bank Public 19,711.40 19,636.40 (9,075.00)Nassit 1,345.65 - (1,345.65)

182 Days Treasury Bearer Bonds 226,852.75 75,802.95 (151,049.80)Bank of Sierra Leone 4,505.20 6,295.15 1,789.95Commercial Banks 195,751.15 59,658.30 (136,092.85Non-Bank Public 26,596.40 9,849.50 (16,746.90)Nassit - - -

364 Days Treasury Bearer Bonds 1,837,233.25 2,622,329.15 785,095.90Bank of Sierra Leone 6,540.50 229,041.65 222,501.15Commercial Banks 1,725,972.10 2,130,666.00 404,693.90Non-Bank Public 69,574.05 206,988.20 137,414.15Nassit 35,146.60 55,633.30 20,486.70

1Year Treasury Bonds 76,720.25 45,773.85 (30,946.40)Bank of Sierra Leone 6,184.65 9,195.45 3,010.80Commercial Banks - - -Non-Bank Public 70,535.60 36,578.40 (33,957.20)Nassit - - -

2Years Treasury Bonds 59,736.65 66,751.65 7,015.00Bank of Sierra Leone - - -Commercial Banks 3,000.00 10,000.00 7,000.00Non-Bank Public 5,249.65 5,264.65 15.00Nassit 51,487.00 51,487.00 -

5Years Treasury Bonds - 41,071.80 41,071.80Bank of Sierra Leone - - -Commercial Banks - - -Non-Bank Public - - -Nassit - 41,071.80 21,071.80

Total 2,248,411.65 2,879,324.00 630,912.35Bank of Sierra Leone 22,320.50 244,532.25 222,211.75Commercial Banks 1,946,4444.80 2,217,282.50 270,837.70Non-Bank Public 191,667.10 269,317.15 77,650.05Nassit 87,979.25 149,192.10 60,212.85

Source: Bank of Sierra Leone

33

BANK OF SIERRA LEONE

5.0 External Sector Developments

5.1 Overview of the External Sector

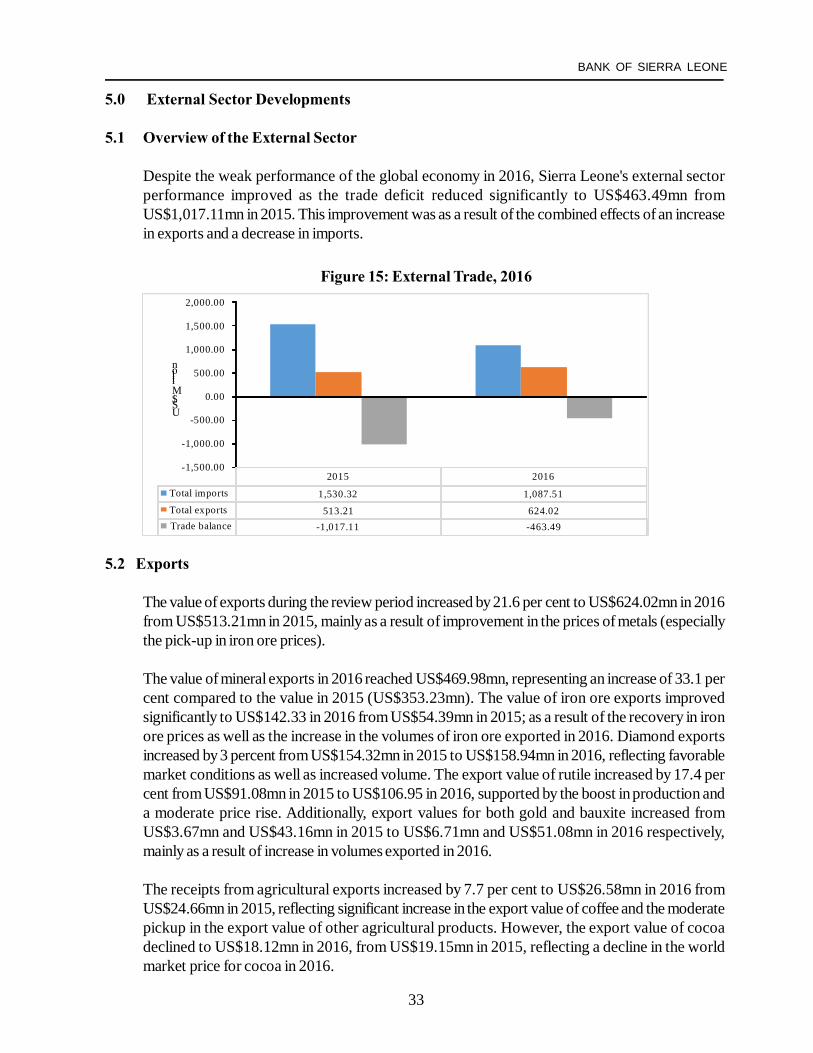

Despite the weak performance of the global economy in 2016, Sierra Leone's external sectorperformance improved as the trade deficit reduced significantly to US$463.49mn fromUS$1,017.11mn in 2015. This improvement was as a result of the combined effects of an increasein exports and a decrease in imports.

Figure 15: External Trade, 2016

5.2 Exports

The value of exports during the review period increased by 21.6 per cent to US$624.02mn in 2016from US$513.21mn in 2015, mainly as a result of improvement in the prices of metals (especiallythe pick-up in iron ore prices).

The value of mineral exports in 2016 reached US$469.98mn, representing an increase of 33.1 percent compared to the value in 2015 (US$353.23mn). The value of iron ore exports improvedsignificantly to US$142.33 in 2016 from US$54.39mn in 2015; as a result of the recovery in ironore prices as well as the increase in the volumes of iron ore exported in 2016. Diamond exportsincreased by 3 percent from US$154.32mn in 2015 to US$158.94mn in 2016, reflecting favorablemarket conditions as well as increased volume. The export value of rutile increased by 17.4 percent from US$91.08mn in 2015 to US$106.95 in 2016, supported by the boost in production anda moderate price rise. Additionally, export values for both gold and bauxite increased fromUS$3.67mn and US$43.16mn in 2015 to US$6.71mn and US$51.08mn in 2016 respectively,mainly as a result of increase in volumes exported in 2016.

The receipts from agricultural exports increased by 7.7 per cent to US$26.58mn in 2016 fromUS$24.66mn in 2015, reflecting significant increase in the export value of coffee and the moderatepickup in the export value of other agricultural products. However, the export value of cocoadeclined to US$18.12mn in 2016, from US$19.15mn in 2015, reflecting a decline in the worldmarket price for cocoa in 2016.

2015 2016Total imports 1,530.32 1,087.51Total exports 513.21 624.02Trade balance -1,017.11 -463.49

-1,500.00

-1,000.00

-500.00

0.00

500.00

1,000.00

1,500.00

2,000.00

US$ Million

34

ANNUAL REPORT AND STATEMENT OF ACCOUNTS

Table 8: International Trade and Reserves (US Dollars)

Jan-Dec'15 Jan-Dec'16

Merchandise Imports 1,530,320.5 1,087,509.0Consumer Goods 342,274.6 580.0123.8of which Food 527,864.2 298,730.4 Rice 141,490.0 96,887.3Beverages and Tobacco 43,609.8 38,455.3Crude Materials 41,372.3 48,767.0Mineral Fuels and Lubricants of which 277,957.7 183,748.2Fuel 245,481.4 98,691.4Animal and Vegetable Oils 8,539.8 5,088.9Chemicals 51,848.1 75,072.5Manufactured Goods 121,595.2 124,384.3Machinery and Transport Equipment 334,805.4 206,934.4Other Imports 122,727.9 106,327.8Merchandise Exports 513,207.2 624,019.2of which - -Mineral Exports 353,227.8 469,979.2Diamonds 154,320.0 158,939.5Bauxite 43,160.0 51,077.1Rutile 91,081.6 106,953.5Gold 3,667.8 6,708.6Ilmenite 5,296.6 3,141.3Iron Ore 54,386.0 142,333.0Zircom 1,272.5 826.2Other Minerals /1 43.4 -Agricultural Exports 24,657.7 26,567.7Coffee 1,346.0 3,416.5Cocoa 19,148.7 18,115.4Piassava - -Fish and Shrimps 4,163.0 5,035.8Others 110,802.3 122,721.1Re-exports 24,519.4 4,751.2Trade Balance (1,017,113.3) (463,489.8)Foreign Reserves ($mn) 580.3 503.79

Source: National Revenue Authority (NRA)

35

BANK OF SIERRA LEONE

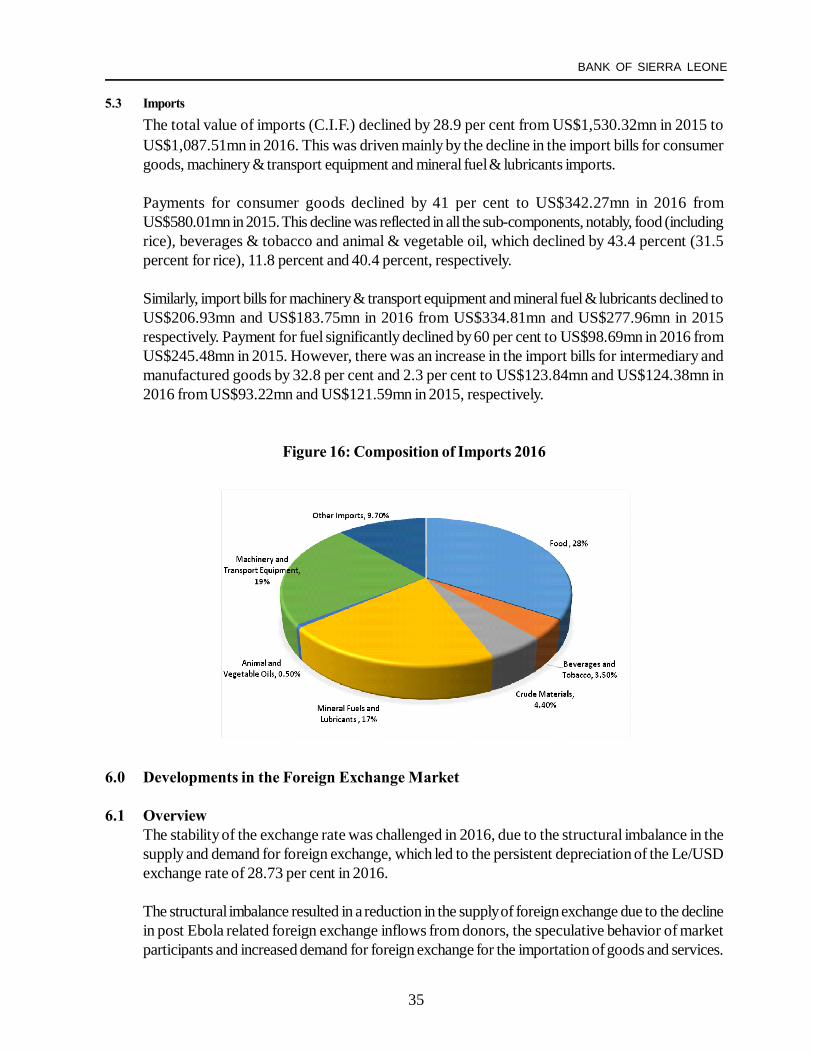

5.3 Imports

The total value of imports (C.I.F.) declined by 28.9 per cent from US$1,530.32mn in 2015 toUS$1,087.51mn in 2016. This was driven mainly by the decline in the import bills for consumergoods, machinery & transport equipment and mineral fuel & lubricants imports.

Payments for consumer goods declined by 41 per cent to US$342.27mn in 2016 fromUS$580.01mn in 2015. This decline was reflected in all the sub-components, notably, food (includingrice), beverages & tobacco and animal & vegetable oil, which declined by 43.4 percent (31.5percent for rice), 11.8 percent and 40.4 percent, respectively.

Similarly, import bills for machinery & transport equipment and mineral fuel & lubricants declined toUS$206.93mn and US$183.75mn in 2016 from US$334.81mn and US$277.96mn in 2015respectively. Payment for fuel significantly declined by 60 per cent to US$98.69mn in 2016 fromUS$245.48mn in 2015. However, there was an increase in the import bills for intermediary andmanufactured goods by 32.8 per cent and 2.3 per cent to US$123.84mn and US$124.38mn in2016 from US$93.22mn and US$121.59mn in 2015, respectively.

Figure 16: Composition of Imports 2016

6.0 Developments in the Foreign Exchange Market

6.1 OverviewThe stability of the exchange rate was challenged in 2016, due to the structural imbalance in thesupply and demand for foreign exchange, which led to the persistent depreciation of the Le/USDexchange rate of 28.73 per cent in 2016.

The structural imbalance resulted in a reduction in the supply of foreign exchange due to the declinein post Ebola related foreign exchange inflows from donors, the speculative behavior of marketparticipants and increased demand for foreign exchange for the importation of goods and services.

36

ANNUAL REPORT AND STATEMENT OF ACCOUNTS

6.2 Foreign Exchange FlowsThe total amount traded in the Foreign exchange market in 2016 was USD1.18bn, a 32.72 percent decline compared to the amount traded in 2015. The monthly average amount traded in 2016was USD0.98bn compared to USD0.15bn in 2015.

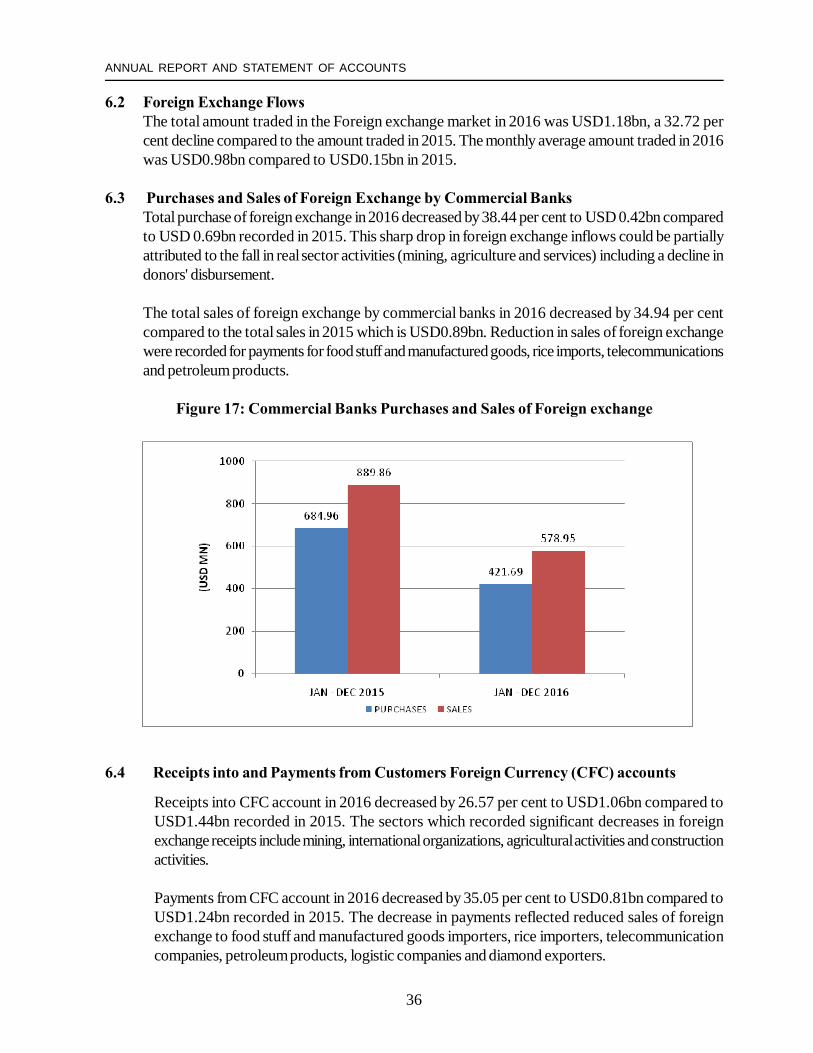

6.3 Purchases and Sales of Foreign Exchange by Commercial BanksTotal purchase of foreign exchange in 2016 decreased by 38.44 per cent to USD 0.42bn comparedto USD 0.69bn recorded in 2015. This sharp drop in foreign exchange inflows could be partiallyattributed to the fall in real sector activities (mining, agriculture and services) including a decline indonors' disbursement.

The total sales of foreign exchange by commercial banks in 2016 decreased by 34.94 per centcompared to the total sales in 2015 which is USD0.89bn. Reduction in sales of foreign exchangewere recorded for payments for food stuff and manufactured goods, rice imports, telecommunicationsand petroleum products.

Figure 17: Commercial Banks Purchases and Sales of Foreign exchange

6.4 Receipts into and Payments from Customers Foreign Currency (CFC) accounts

Receipts into CFC account in 2016 decreased by 26.57 per cent to USD1.06bn compared toUSD1.44bn recorded in 2015. The sectors which recorded significant decreases in foreignexchange receipts include mining, international organizations, agricultural activities and constructionactivities.

Payments from CFC account in 2016 decreased by 35.05 per cent to USD0.81bn compared toUSD1.24bn recorded in 2015. The decrease in payments reflected reduced sales of foreignexchange to food stuff and manufactured goods importers, rice importers, telecommunicationcompanies, petroleum products, logistic companies and diamond exporters.

37

BANK OF SIERRA LEONE

Figure 18: Receipt into Payment from CFC Account

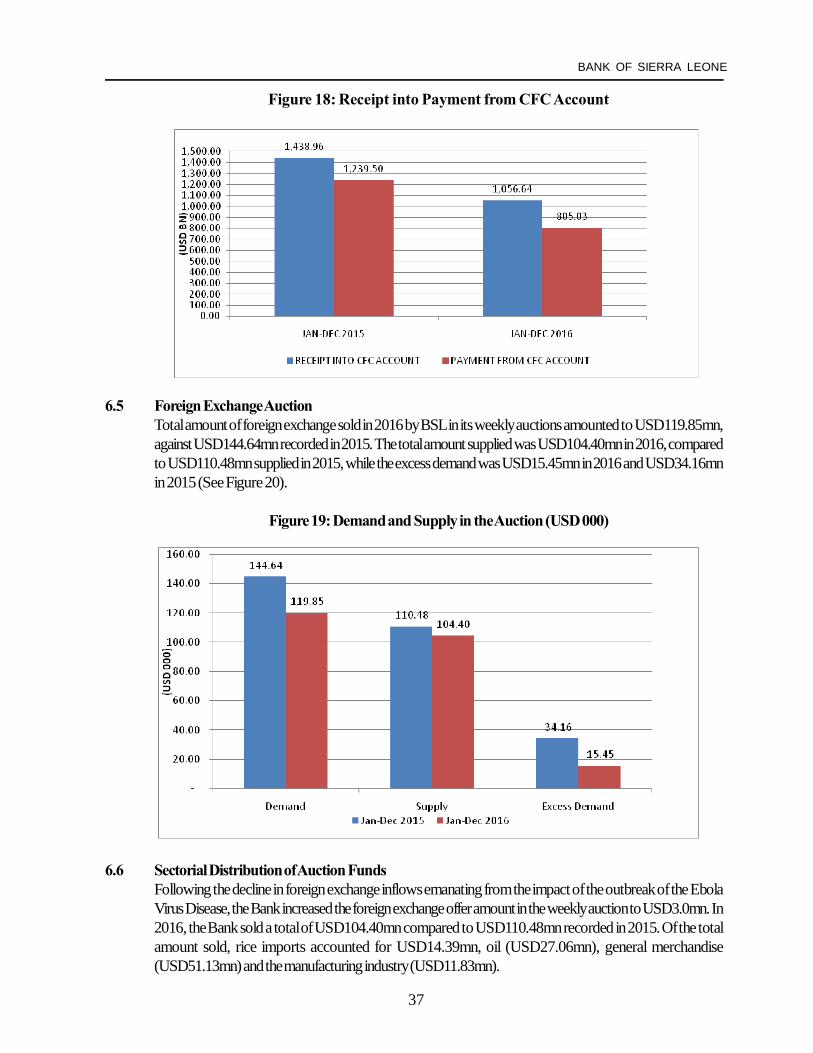

6.5 Foreign Exchange AuctionTotal amount of foreign exchange sold in 2016 by BSL in its weekly auctions amounted to USD119.85mn,against USD144.64mn recorded in 2015. The total amount supplied was USD104.40mn in 2016, comparedto USD110.48mn supplied in 2015, while the excess demand was USD15.45mn in 2016 and USD34.16mnin 2015 (See Figure 20).

Figure 19: Demand and Supply in the Auction (USD 000)

6.6 Sectorial Distribution of Auction FundsFollowing the decline in foreign exchange inflows emanating from the impact of the outbreak of the EbolaVirus Disease, the Bank increased the foreign exchange offer amount in the weekly auction to USD3.0mn. In2016, the Bank sold a total of USD104.40mn compared to USD110.48mn recorded in 2015. Of the totalamount sold, rice imports accounted for USD14.39mn, oil (USD27.06mn), general merchandise(USD51.13mn) and the manufacturing industry (USD11.83mn).

38

ANNUAL REPORT AND STATEMENT OF ACCOUNTS

Figure 20: Sectorial Distribution of Auction Funds January- December 2016

6.7 Foreign Exchange Rate MovementsReflecting the developments in the volume of the transaction, the year-on-year exchange rate ofthe Leone against the United States dollar depreciated in 2016 as following: the official ratedepreciated by 28.73 per cent, BSL auction rate by 28.07 per cent and commercial banks' rateby 30.73 per cent. The parallel market rate also depreciated by 28.58 per cent.

In principle, the continuous depreciation of the Leone against major international currencies reflectsincreased demand relative to the supply of foreign exchange. However, the mismatch betweengovernment revenue and expenditure, coupled with the aggressive bidding by some commercialbanks for donor funds which were auctioned offshore by international brokerage firms have alsocontributed to the instability of the exchange rate. Speculative behavior by some market participantsalso contributed to the pressure in the market.

The spread in the official BSL rates remained constant at 2 per cent. However, the spreads in thecommercial banks and parallel market rates varied. While the spread in the commercial banks'rate was slightly above 3 per cent (reflecting the tightness in the market and limited flow of foreignexchange), the spread in the parallel market was mostly below 2 per cent (see Figure 22).

Figure 21: Exchange Rate Depreciation (y-o-y)

39

BANK OF SIERRA LEONE

Figure 22: Exchange Rates Spread as per Market Segments

6.8 Reserves Management

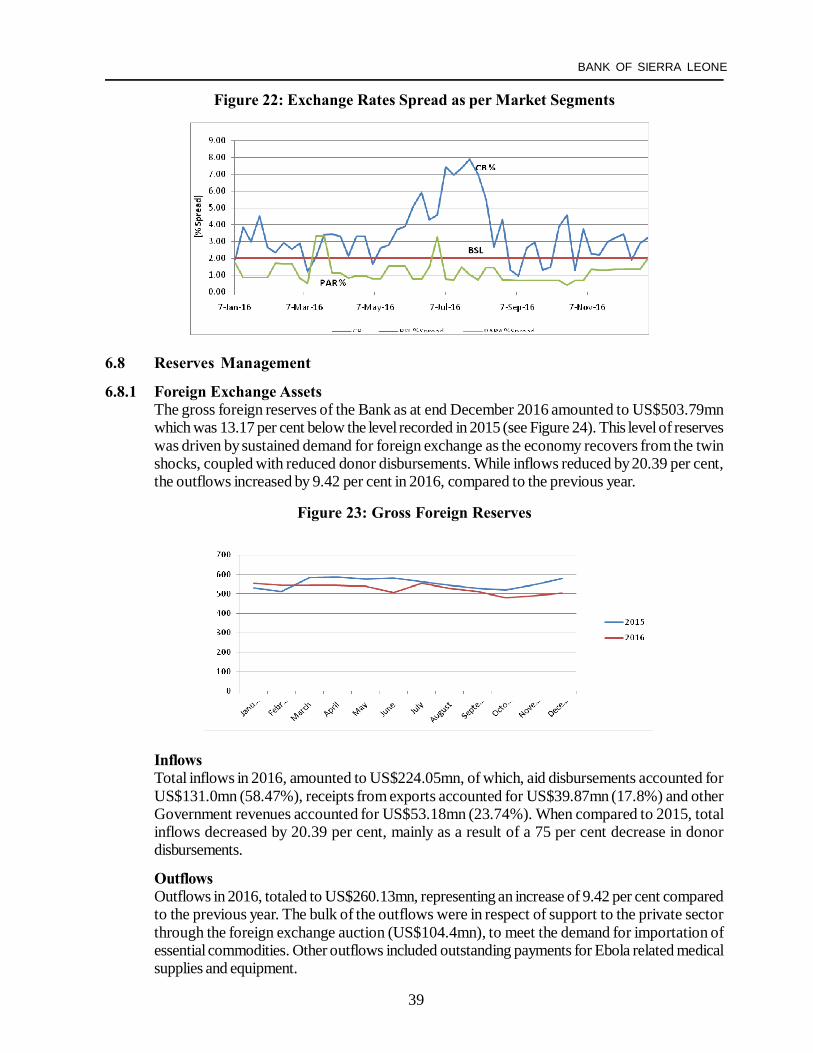

6.8.1 Foreign Exchange AssetsThe gross foreign reserves of the Bank as at end December 2016 amounted to US$503.79mnwhich was 13.17 per cent below the level recorded in 2015 (see Figure 24). This level of reserveswas driven by sustained demand for foreign exchange as the economy recovers from the twinshocks, coupled with reduced donor disbursements. While inflows reduced by 20.39 per cent,the outflows increased by 9.42 per cent in 2016, compared to the previous year.

Figure 23: Gross Foreign Reserves

InflowsTotal inflows in 2016, amounted to US$224.05mn, of which, aid disbursements accounted forUS$131.0mn (58.47%), receipts from exports accounted for US$39.87mn (17.8%) and otherGovernment revenues accounted for US$53.18mn (23.74%). When compared to 2015, totalinflows decreased by 20.39 per cent, mainly as a result of a 75 per cent decrease in donordisbursements.

OutflowsOutflows in 2016, totaled to US$260.13mn, representing an increase of 9.42 per cent comparedto the previous year. The bulk of the outflows were in respect of support to the private sectorthrough the foreign exchange auction (US$104.4mn), to meet the demand for importation ofessential commodities. Other outflows included outstanding payments for Ebola related medicalsupplies and equipment.

40

ANNUAL REPORT AND STATEMENT OF ACCOUNTS

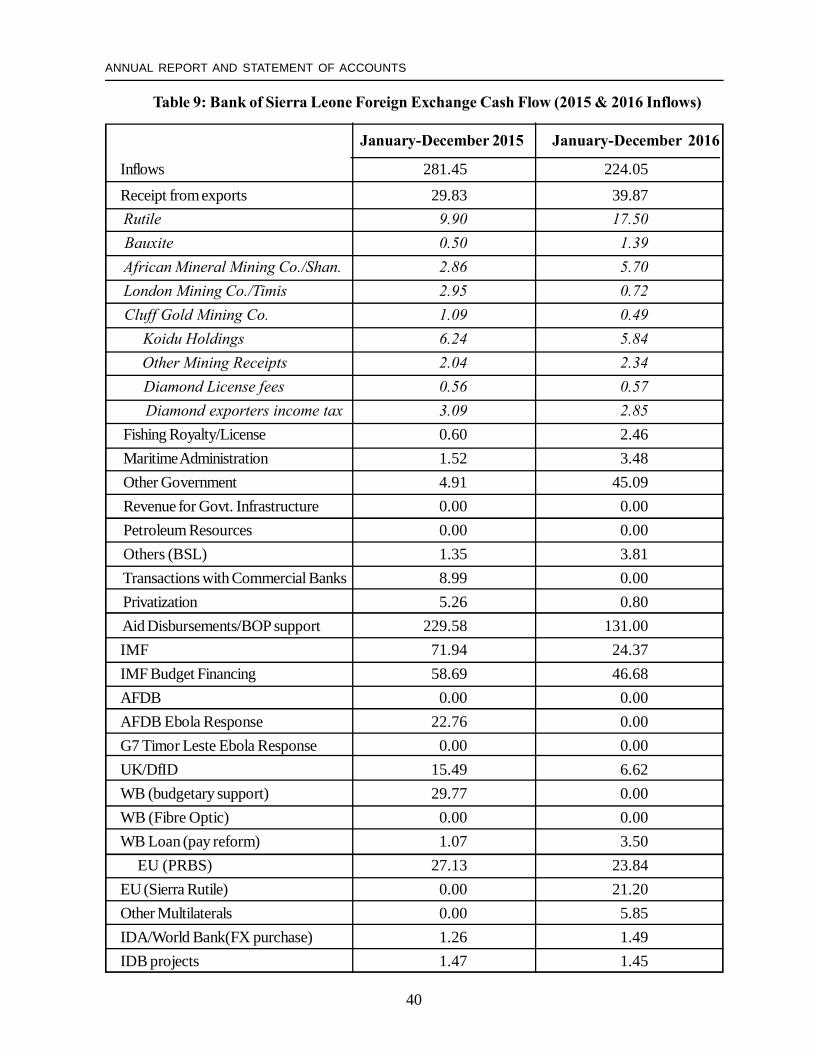

Table 9: Bank of Sierra Leone Foreign Exchange Cash Flow (2015 & 2016 Inflows)

January-December 2015 January-December 2016

Inflows 281.45 224.05Receipt from exports 29.83 39.87 Rutile 9.90 17.50 Bauxite 0.50 1.39 African Mineral Mining Co./Shan. 2.86 5.70 London Mining Co./Timis 2.95 0.72 Cluff Gold Mining Co. 1.09 0.49 Koidu Holdings 6.24 5.84 Other Mining Receipts 2.04 2.34 Diamond License fees 0.56 0.57 Diamond exporters income tax 3.09 2.85 Fishing Royalty/License 0.60 2.46 Maritime Administration 1.52 3.48 Other Government 4.91 45.09 Revenue for Govt. Infrastructure 0.00 0.00 Petroleum Resources 0.00 0.00 Others (BSL) 1.35 3.81 Transactions with Commercial Banks 8.99 0.00 Privatization 5.26 0.80 Aid Disbursements/BOP support 229.58 131.00IMF 71.94 24.37IMF Budget Financing 58.69 46.68AFDB 0.00 0.00AFDB Ebola Response 22.76 0.00G7 Timor Leste Ebola Response 0.00 0.00UK/DfID 15.49 6.62WB (budgetary support) 29.77 0.00WB (Fibre Optic) 0.00 0.00WB Loan (pay reform) 1.07 3.50 EU (PRBS) 27.13 23.84EU (Sierra Rutile) 0.00 21.20Other Multilaterals 0.00 5.85IDA/World Bank(FX purchase) 1.26 1.49IDB projects 1.47 1.45

41

BANK OF SIERRA LEONE

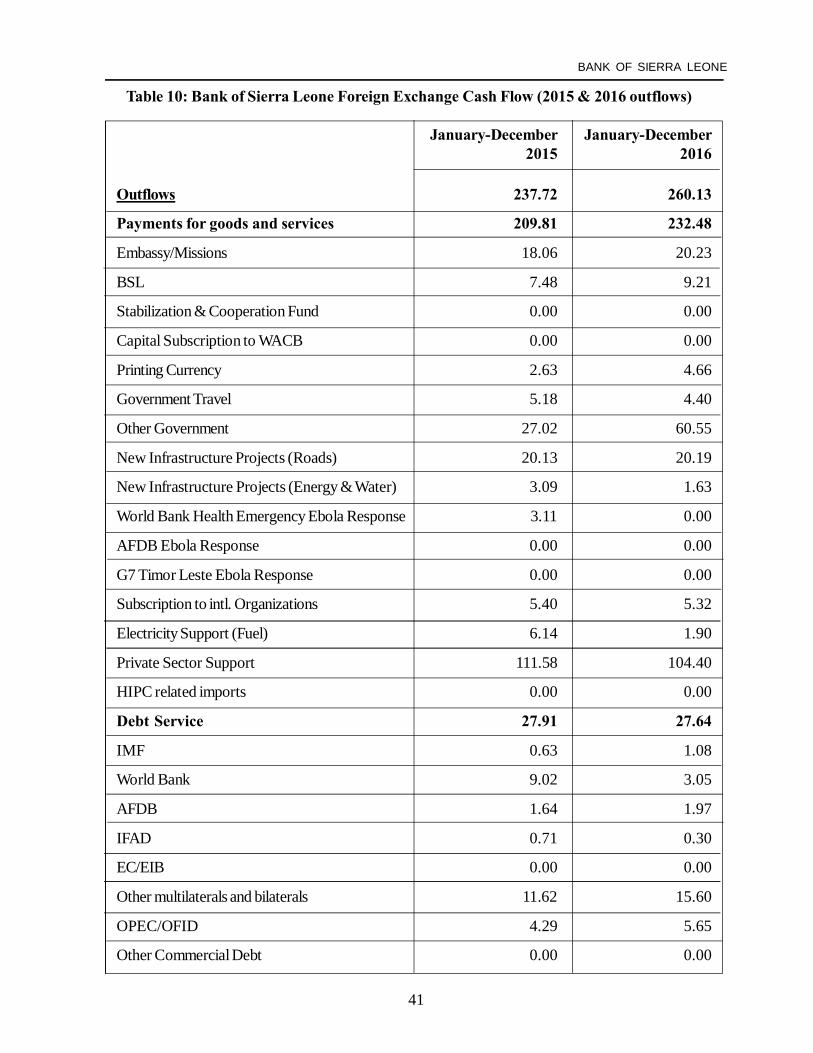

Table 10: Bank of Sierra Leone Foreign Exchange Cash Flow (2015 & 2016 outflows)

January-December January-December2015 2016

Outflows 237.72 260.13

Payments for goods and services 209.81 232.48

Embassy/Missions 18.06 20.23

BSL 7.48 9.21

Stabilization & Cooperation Fund 0.00 0.00

Capital Subscription to WACB 0.00 0.00

Printing Currency 2.63 4.66

Government Travel 5.18 4.40

Other Government 27.02 60.55

New Infrastructure Projects (Roads) 20.13 20.19

New Infrastructure Projects (Energy & Water) 3.09 1.63

World Bank Health Emergency Ebola Response 3.11 0.00

AFDB Ebola Response 0.00 0.00

G7 Timor Leste Ebola Response 0.00 0.00

Subscription to intl. Organizations 5.40 5.32

Electricity Support (Fuel) 6.14 1.90

Private Sector Support 111.58 104.40

HIPC related imports 0.00 0.00

Debt Service 27.91 27.64

IMF 0.63 1.08

World Bank 9.02 3.05

AFDB 1.64 1.97

IFAD 0.71 0.30

EC/EIB 0.00 0.00

Other multilaterals and bilaterals 11.62 15.60

OPEC/OFID 4.29 5.65

Other Commercial Debt 0.00 0.00

42

ANNUAL REPORT AND STATEMENT OF ACCOUNTS

6.8.2 Investment ActivitiesExternal investments in 2016, were in compliance with the BSL's Investment Guidelines.With regards currency composition, external investments were held in US dollar (US$),British Pound (GBP) and Special Drawing Rights (SDR). During the year 2016, the Bankinvested in short term fixed deposits with duration up to 3 months and overnight sweepfacility with Federal Reserve Bank NY.

Returns on the Bank's investment were influenced by the amount invested, the rate of interestand the duration of the investment. As shown in Figure 25, actual income earned by currencies(converted in US$) in 2016 amounted to US$1,545,207.66. Earnings on US$ depositsaccounted for 60.23 per cent, followed by GBP 35.14 per cent and SDR 4.63 per cent. Thelow performance on GBP investment was as a result of reduction in the deposit interest ratefrom 0.40 per cent to 0.06 per cent during 2016, whereas the encouraging performance inUS$ deposits was as a result of increase in interest rate by FED in the first and third quartersof 2016.

Figure 24: Actual Investments Income by Currencies, converted in US Dollars

Overall, the external investment of BSL in 2016 has improved compared to 2015(see Figure 23).

Figure 25: Actual Investments Income by Currencies, converted in US Dollars

43

BANK OF SIERRA LEONE

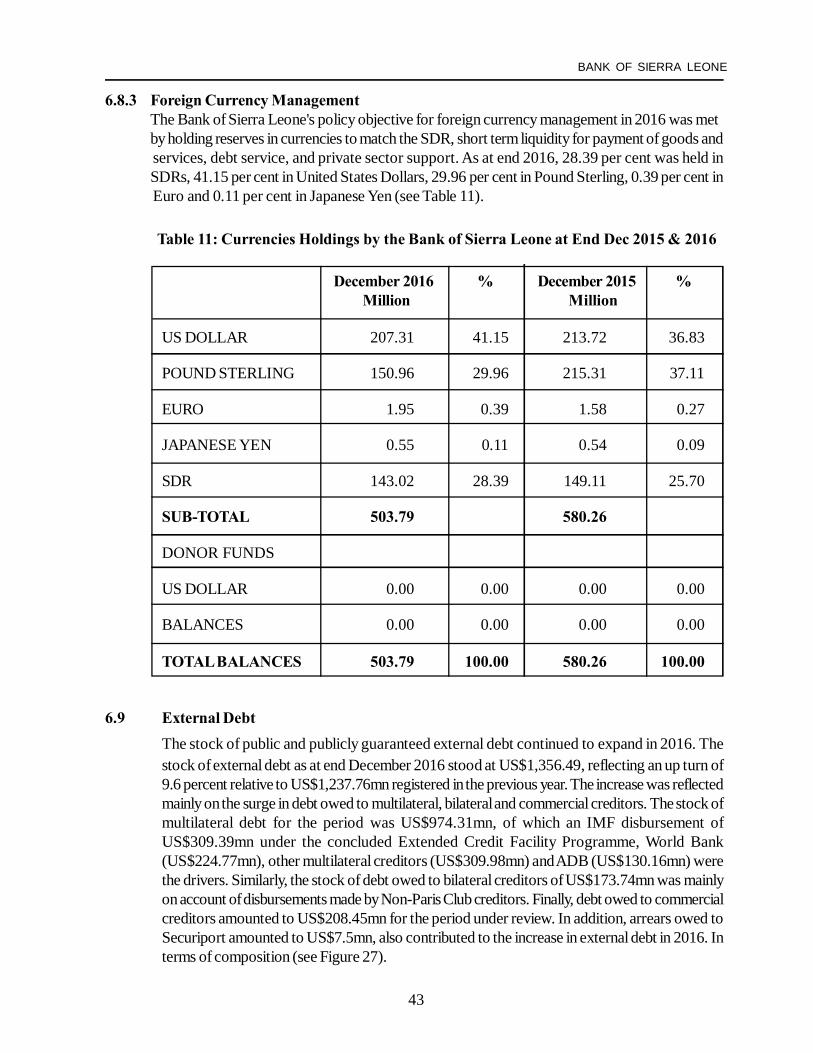

6.8.3 Foreign Currency ManagementThe Bank of Sierra Leone's policy objective for foreign currency management in 2016 was metby holding reserves in currencies to match the SDR, short term liquidity for payment of goods andservices, debt service, and private sector support. As at end 2016, 28.39 per cent was held inSDRs, 41.15 per cent in United States Dollars, 29.96 per cent in Pound Sterling, 0.39 per cent inEuro and 0.11 per cent in Japanese Yen (see Table 11).

Table 11: Currencies Holdings by the Bank of Sierra Leone at End Dec 2015 & 2016

December 2016 % December 2015 %Million Million

US DOLLAR 207.31 41.15 213.72 36.83

POUND STERLING 150.96 29.96 215.31 37.11

EURO 1.95 0.39 1.58 0.27

JAPANESE YEN 0.55 0.11 0.54 0.09

SDR 143.02 28.39 149.11 25.70

SUB-TOTAL 503.79 580.26

DONOR FUNDS

US DOLLAR 0.00 0.00 0.00 0.00

BALANCES 0.00 0.00 0.00 0.00

TOTAL BALANCES 503.79 100.00 580.26 100.00