Embed Size (px)

Citation preview

ASIA PACIFIC FORUM ON FINANCIAL INCLUSION Shanghai, March 19th – 22nd , 2014

PT. BANK RAKYAT INDONESIA (PERSERO) Tbk

1

“Bank Rakyat Indonesia’s Experience on Financial Inclusion”

Delivered by: Budi Satria

BRI General Manager

2

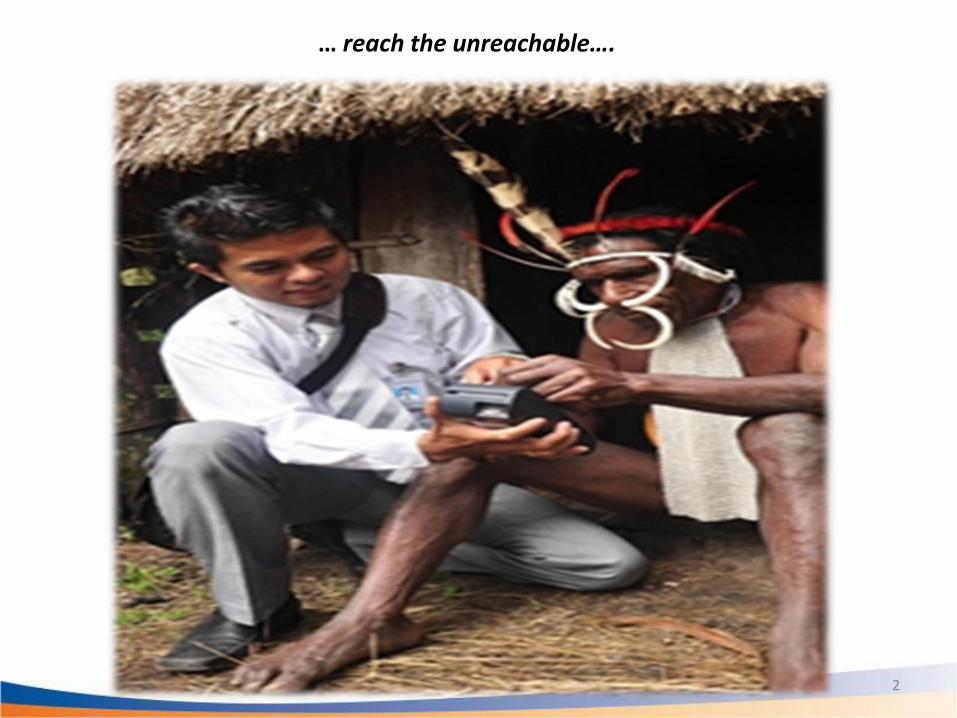

… reach the unreachable….

3

• Productive Age Population:

173.9 Million • Number of MSMEs:

56.53 Million Units • Accessibility Ratio (Bank Account:Total Population):

47.1% • Number of Bank:

120 Commercial Banks with 18,558 offices

1,635 Rural Banks with 4,678 offices Source: Laporan Perekonomian Indonesia 2012

Statistik Perbankann Indonesia Des 2013

Indonesia at a Glance

4

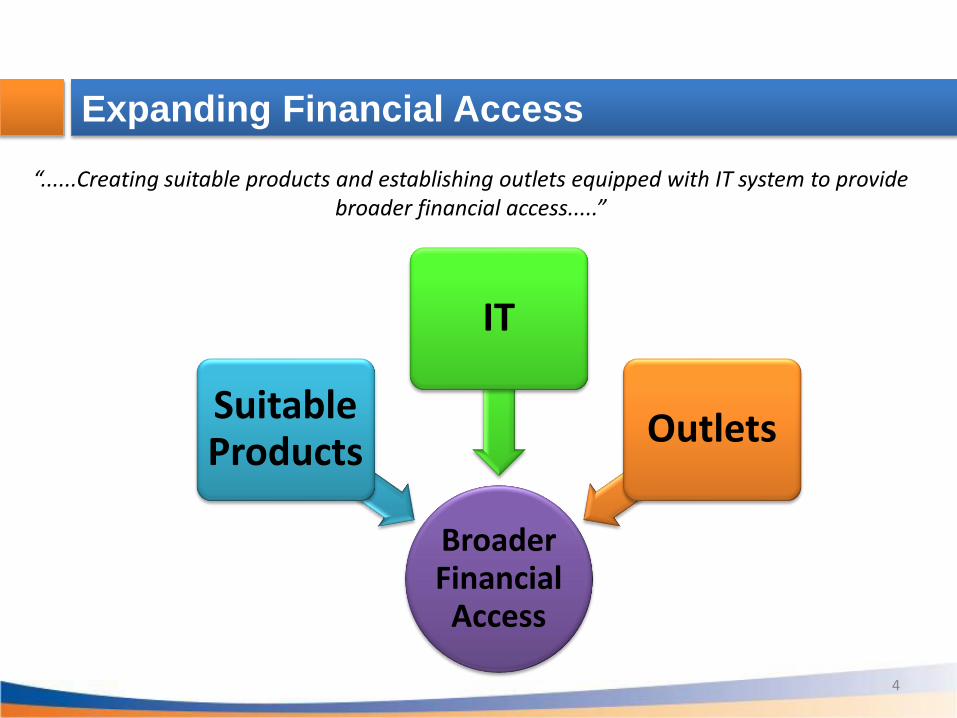

Expanding Financial Access

“......Creating suitable products and establishing outlets equipped with IT system to provide broader financial access.....”

Broader Financial

Access

Suitable Products

IT

Outlets

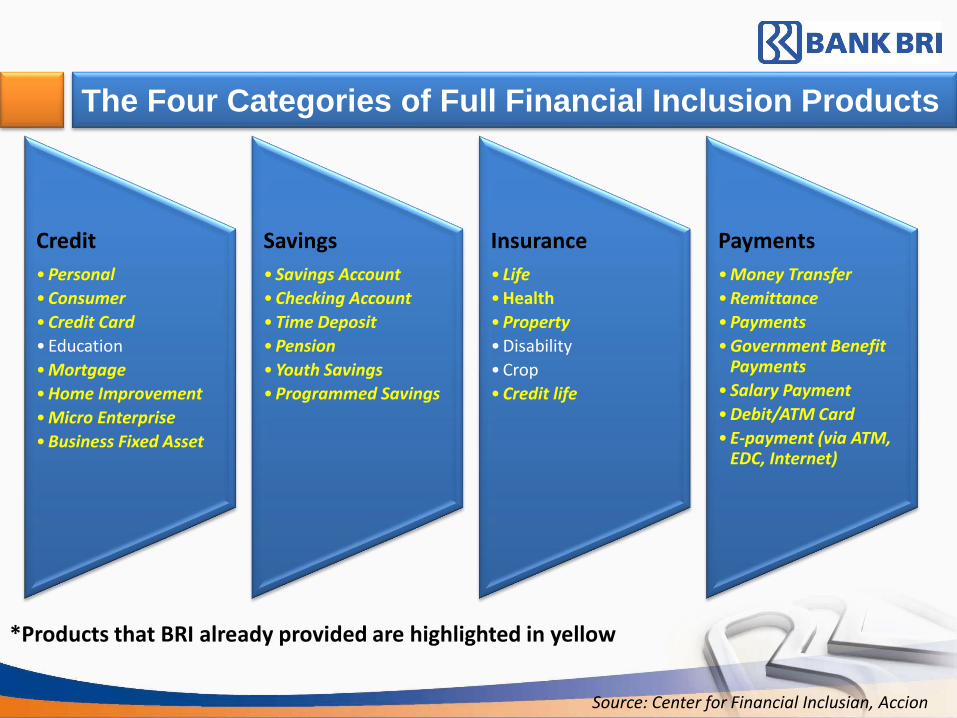

The Four Categories of Full Financial Inclusion Products

Credit

•Personal

•Consumer

•Credit Card

•Education

•Mortgage

•Home Improvement

•Micro Enterprise

•Business Fixed Asset

Savings

• Savings Account

•Checking Account

•Time Deposit

•Pension

•Youth Savings

•Programmed Savings

Insurance

• Life

•Health

•Property

•Disability

•Crop

•Credit life

Payments

•Money Transfer

•Remittance

•Payments

•Government Benefit Payments

• Salary Payment

•Debit/ATM Card

•E-payment (via ATM, EDC, Internet)

*Products that BRI already provided are highlighted in yellow

Source: Center for Financial Inclusian, Accion

6

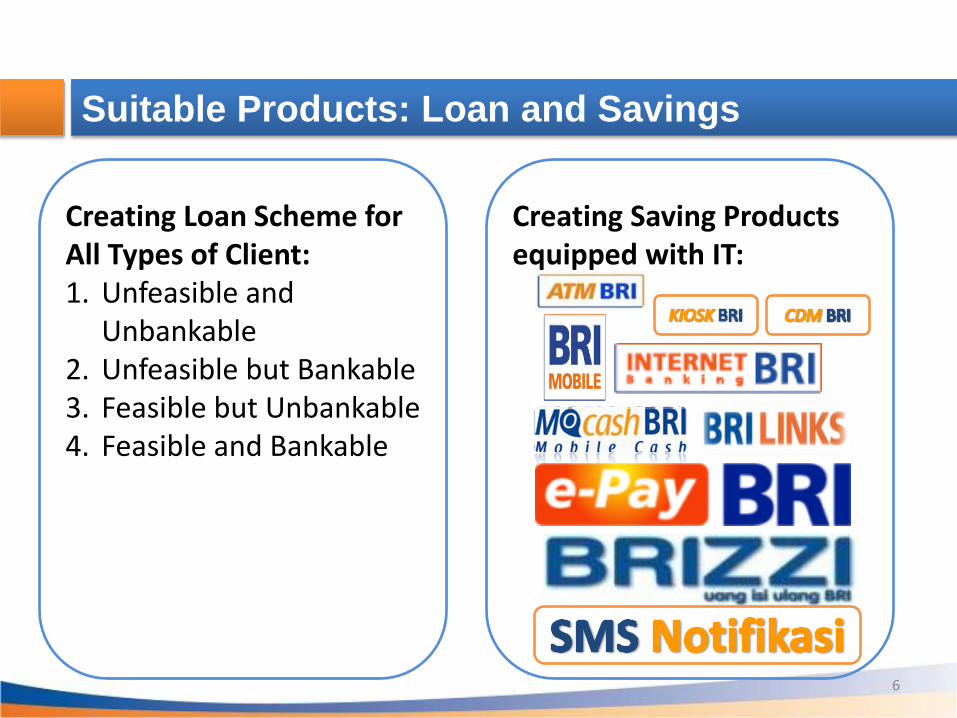

Suitable Products: Loan and Savings

Creating Loan Scheme for All Types of Client: 1. Unfeasible and

Unbankable 2. Unfeasible but Bankable 3. Feasible but Unbankable 4. Feasible and Bankable

Creating Saving Products equipped with IT:

7

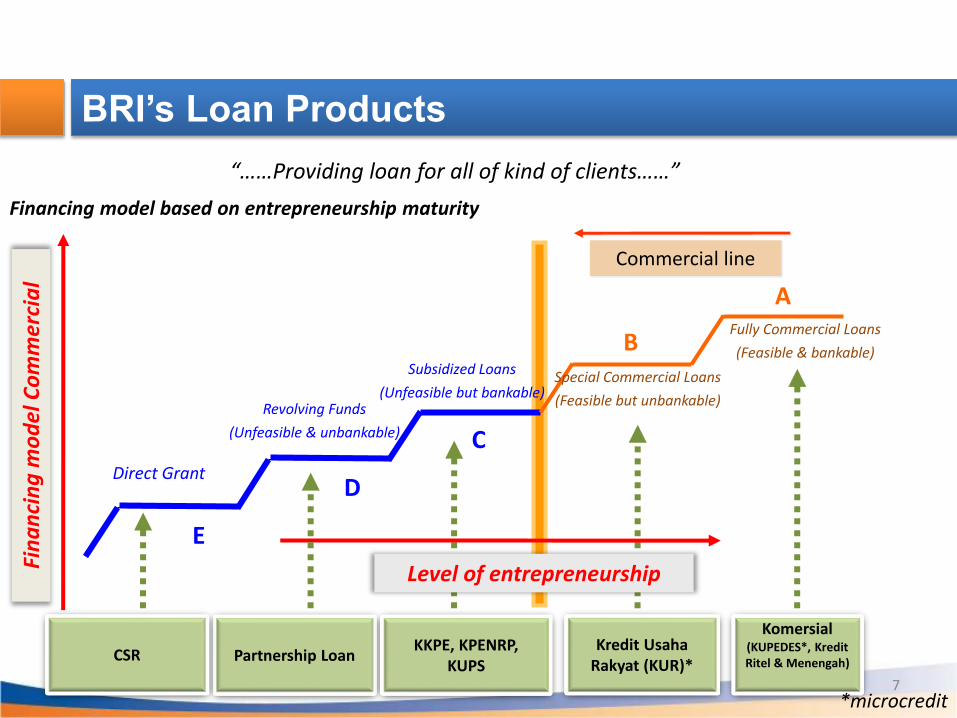

BRI’s Loan Products

Direct Grant

Revolving Funds

(Unfeasible & unbankable)

Subsidized Loans

(Unfeasible but bankable)

Special Commercial Loans

(Feasible but unbankable)

Fully Commercial Loans

(Feasible & bankable)

A

Level of entrepreneurship

B

C

D

E

Financing model based on entrepreneurship maturity

Fin

an

cin

g m

od

el C

om

mer

cia

l

Commercial line

Partnership Loan KKPE, KPENRP,

KUPS Kredit Usaha

Rakyat (KUR)*

Komersial (KUPEDES*, Kredit Ritel & Menengah)

CSR

“……Providing loan for all of kind of clients……”

*microcredit

8

BRI’s Outlet: The Most Extensive and Largest Network

Milestones - Networks

E-Channel

Conventional Outlet

* include 3 overseas offices

Outlet Distribution - Trend

Hybrid Branch

All outlet real time online,

E-Buzz, Teras BRI,

BRILink, Internet Banking

MoCash

TerasBRI Mobile

Mobile Banking

CDM,

Cash Management

2013

2012

2011

2009

2007

2006

BRIZZI2010

Outlet 2009 2010 2011 2012 2013Head Office 1 1 1 1 1Regional Office 17 18 18 18 18Branch Office* 406 413 431 446 453Sub-Branch Office 434 470 502 545 565BRI Unit 4,538 4,649 4,849 5,000 5,144Cash Office 728 822 870 914 950Teras BRI 217 617 1,304 1,778 2,212Teras BRI Mobile 100 350 465Total 6,341 6,990 8,075 9,052 9,808

E-Channel 2009 2010 2011 2012 2013

ATM 3,778 6,085 7,292 14,292 18,292

EDC 6,398 12,719 31,590 44,715 85,936

CDM 22 39 89 92 192

Kiosk 60 96 100 100 100

E-Buzz 1 2 19 42 50

Total 10,259 18,941 39,090 59,241 104,570

9

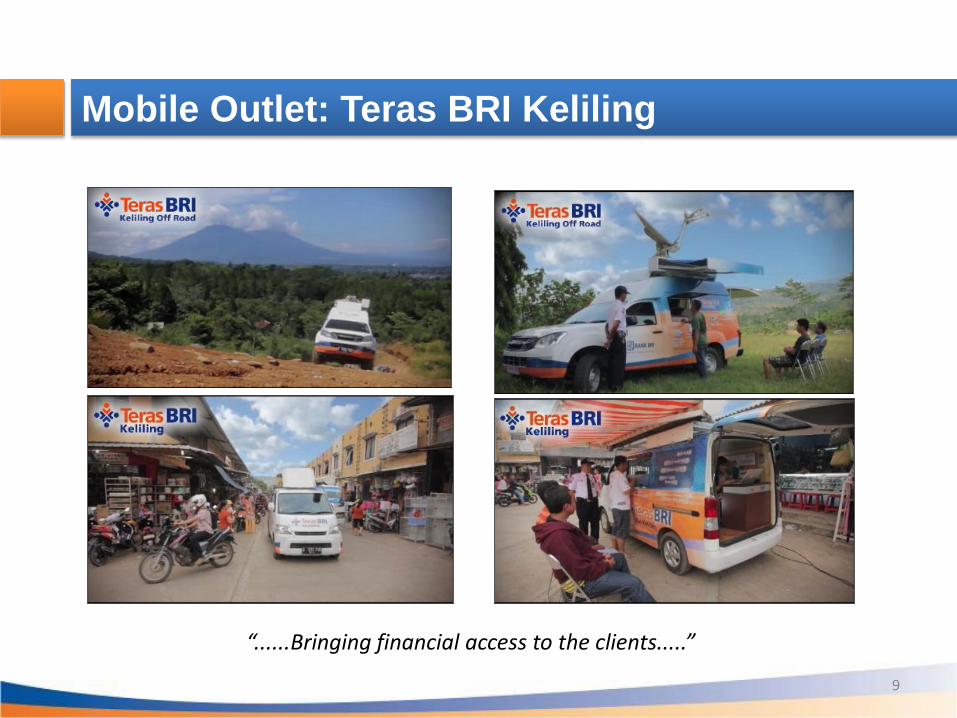

Mobile Outlet: Teras BRI Keliling

“......Bringing financial access to the clients.....”

10

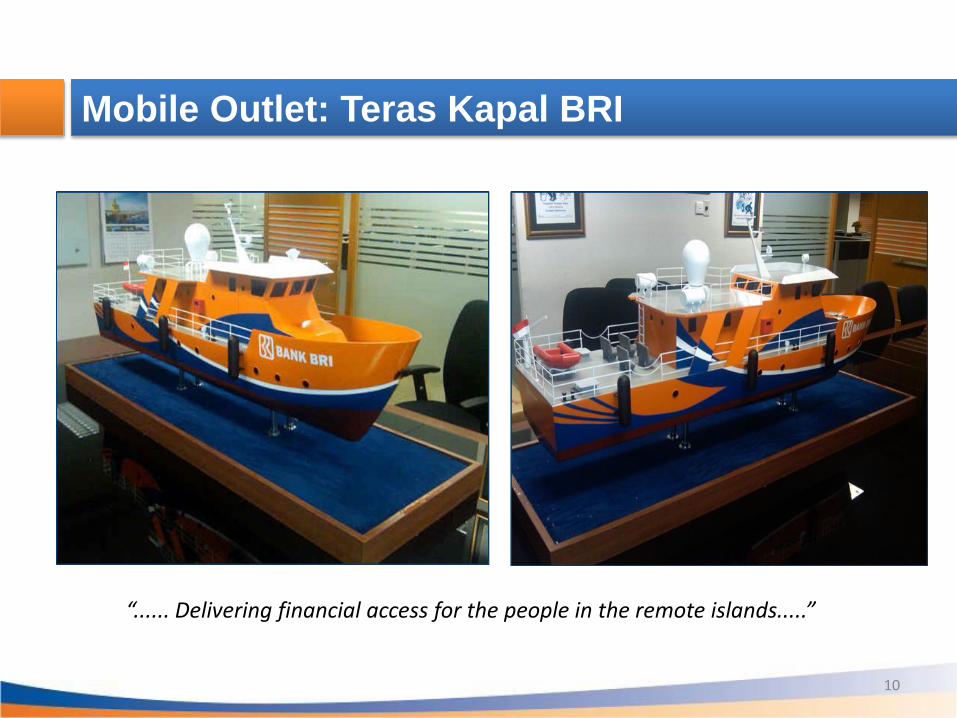

Mobile Outlet: Teras Kapal BRI

“...... Delivering financial access for the people in the remote islands.....”

11

Mobile Outlet: E-Buzz BRI

“......Providing financial education as well as financial access.....”

12

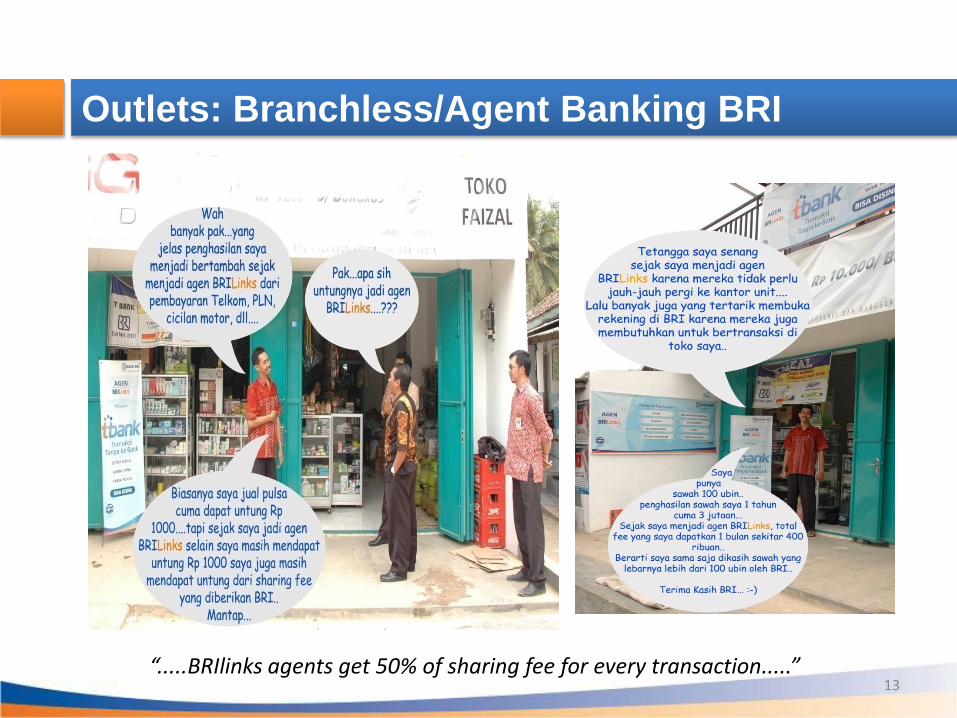

Outlets: Branchless/Agent Banking BRI

“.....Delivering financial access through mutual partnership with agents.....”

*212#

13

Outlets: Branchless/Agent Banking BRI

“.....BRIlinks agents get 50% of sharing fee for every transaction.....”

14

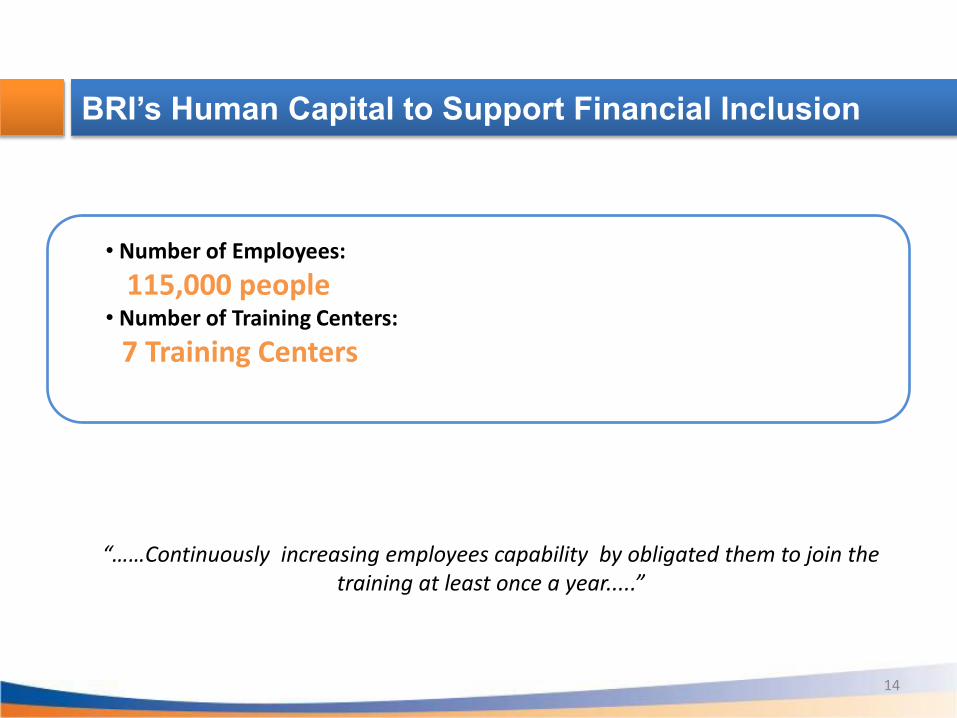

BRI’s Human Capital to Support Financial Inclusion

“……Continuously increasing employees capability by obligated them to join the training at least once a year.....”

• Number of Employees:

115,000 people • Number of Training Centers:

7 Training Centers

15

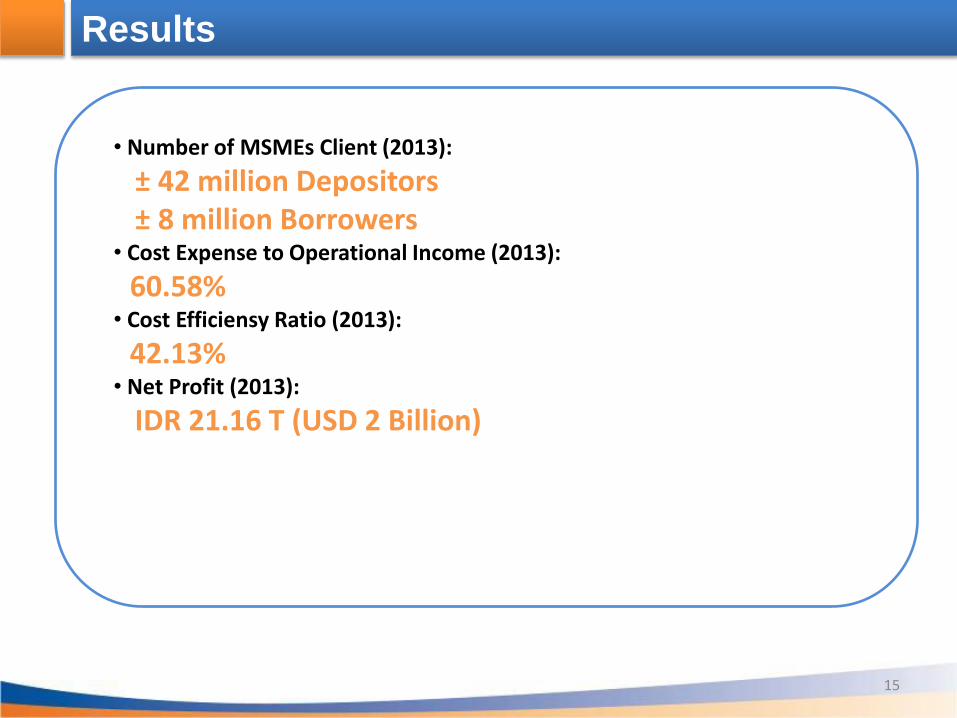

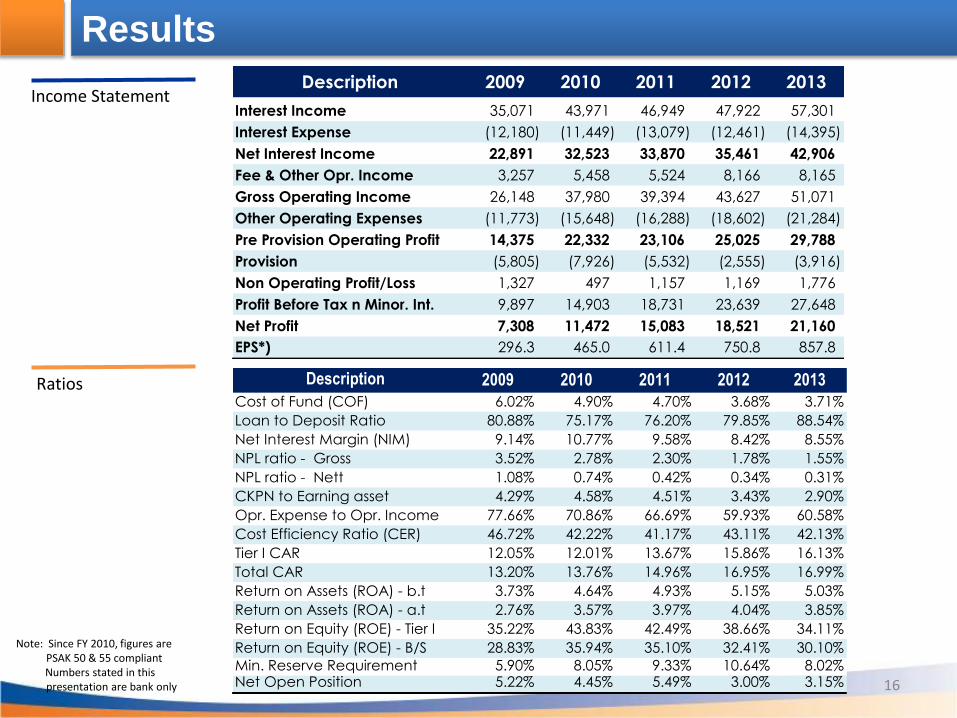

Results

• Number of MSMEs Client (2013):

± 42 million Depositors ± 8 million Borrowers • Cost Expense to Operational Income (2013):

60.58% • Cost Efficiensy Ratio (2013):

42.13% • Net Profit (2013):

IDR 21.16 T (USD 2 Billion)

16

Results

Income Statement

Ratios

Note: Since FY 2010, figures are PSAK 50 & 55 compliant

Numbers stated in this presentation are bank only

Description 2009 2010 2011 2012 2013

Interest Income 35,071 43,971 46,949 47,922 57,301

Interest Expense (12,180) (11,449) (13,079) (12,461) (14,395)

Net Interest Income 22,891 32,523 33,870 35,461 42,906

Fee & Other Opr. Income 3,257 5,458 5,524 8,166 8,165

Gross Operating Income 26,148 37,980 39,394 43,627 51,071

Other Operating Expenses (11,773) (15,648) (16,288) (18,602) (21,284)

Pre Provision Operating Profit 14,375 22,332 23,106 25,025 29,788

Provision (5,805) (7,926) (5,532) (2,555) (3,916)

Non Operating Profit/Loss 1,327 497 1,157 1,169 1,776

Profit Before Tax n Minor. Int. 9,897 14,903 18,731 23,639 27,648

Net Profit 7,308 11,472 15,083 18,521 21,160

EPS*) 296.3 465.0 611.4 750.8 857.8

Description

Cost of Fund (COF) 6.02% 4.90% 4.70% 3.68% 3.71%

Loan to Deposit Ratio 80.88% 75.17% 76.20% 79.85% 88.54%

Net Interest Margin (NIM) 9.14% 10.77% 9.58% 8.42% 8.55%

NPL ratio - Gross 3.52% 2.78% 2.30% 1.78% 1.55%

NPL ratio - Nett 1.08% 0.74% 0.42% 0.34% 0.31%

CKPN to Earning asset 4.29% 4.58% 4.51% 3.43% 2.90%

Opr. Expense to Opr. Income 77.66% 70.86% 66.69% 59.93% 60.58%

Cost Efficiency Ratio (CER) 46.72% 42.22% 41.17% 43.11% 42.13%

Tier I CAR 12.05% 12.01% 13.67% 15.86% 16.13%

Total CAR 13.20% 13.76% 14.96% 16.95% 16.99%

Return on Assets (ROA) - b.t 3.73% 4.64% 4.93% 5.15% 5.03%

Return on Assets (ROA) - a.t 2.76% 3.57% 3.97% 4.04% 3.85%

Return on Equity (ROE) - Tier I 35.22% 43.83% 42.49% 38.66% 34.11%

Return on Equity (ROE) - B/S 28.83% 35.94% 35.10% 32.41% 30.10%

Min. Reserve Requirement 5.90% 8.05% 9.33% 10.64% 8.02%Net Open Position 5.22% 4.45% 5.49% 3.00% 3.15%

2012 20132009 2010 2011

Disclaimer: This presentation has been prepared by PT Bank Rakyat Indonesia (Persero) Tbk (Bank BRI) independently and is circulated for the purpose of general information only. It is not intended to the specific person who may receive this report. The information in this report has been obtained from sources which we deem reliable. No warranty (expressed or implied) is made to the accuracy or completeness of the information. All opinions and estimations included in this report constitute our judgment as of this date and are subject to change without prior notice. We disclaim any responsibility or l i a b i l i t y w i t h o u t p r i o r n o t i c e o f B a n k B R I a n d / o r t h e i r r e s p e c t i v e e m p l o y e e s and/or agents whatsoever arising which may be brought against or suffered by any person as a result of acting in reliance upon the whole or any part of the contents of this report and neither Bank BRI and/or its affiliated companies and/or their respective employees and/or agents accepts liability for any errors, omissions, negligent or otherwise, in this report and any inaccuracy herein or omission here from which might otherwise arise.

Terima Kasih

Please Visit www. bri.co.id

www.ivpbri.com