Embed Size (px)

DESCRIPTION

Bankieri No.10 - January 2014

Citation preview

No.

10

Jan

uary

201

4

Publication of the Albanian Association of Banks

“DEBT AND INDEBTEDNESS”“DEBT AND INDEBTEDNESS”

AAB MEMBERS

www.aab.al

No.

10

Jan

uary

201

4

Publication of the Albanian Association of Banks

“DEBT AND INDEBTEDNESS”“DEBT AND INDEBTEDNESS”

The Albanian Security Interest System, in the frame of latest changes and amendments by Sokol ELMAZAJ and Sabina LALAJ

Risk-based internal audit plan in banking sector – Some key considerations by Holtjana BELLO

Increasing Public Debt – doing a “bad” thing for good reason by Spiro BRUMBULLI

BANKIERI is the official publication

of the Albanian Association of

Banks which mainly focus the

Albanian banking industry. Bankieri

provide readers with valuable

information on the financial

industry's developments in general,

and of commercial banks in

particular.

ContentsEDITOR’S DESK

Are we drowned in (bad) debt??? by Elvin MEKA

FRONTLINEPrivate debt in Albania – a lackluster existenceby Altin HOTI

BANKING SYSTEM

INTERVIEW

JOURNALIST’S CORNER

EXPERTS’ FORUM

ECONOMIST CORNER

SOCIAL CAPITAL

BALKAN NET

TECH TOPICS

FINANCIAL AUDITORIUM

AAB

p.5

p.6

Bank of Albania’s platform for handling non-performing loans – A new approach by Gerond ZIU

Intesa Sanpaolo Bank Albania – standing firm in Albania - Interview with Silvio PEDRAZZI

DEBT – the ubiquitous reality by Aurora SULÇE

Security roof by Roland TASHI

Stabilization - The keyword for the financial sectorby Enkeleda SHEHI

Monetary policies: price stability versus financial stability by Adrian CIVICI

Banks' Activity

Interbalkan News

Online communication secrecy by Oerd CUKALLA

Issues and views on private bankingby Roberto RUOZI

Albanian Association of Banks Activities

p.14

p.9

p.13

p.11

p.17

p.19

p.22

p.25

p.27

p.33

p.35

p.38

p.41

p.43

BankieriNo. 10, January 2014

Publication of Albanian Association of Banks

Editorial Team:

Elvin MekaEditor-in-Chief

Junida Tafaj (Katroshi)Eftali PeçiCoordinators

Anduena ManushiEditor

Alban NexhipiPhotographer

Design & Layout: Ladybird Creations

Editorial Board:Seyhan PENCABLIGILAAB Chairman & CEO of Banka Kombëtare Tregtare

Ioannis KOUGIONASAAB Vice Chairman & CEO of NBG Bank Albania

Christian CANACARISAAB Executive Committee Member & CEO of Raiffeisen Bank Albania

Periklis DROUGKASAAB Executive Committee Member & CEO of Alpha Bank

Frédéric BLANCAAB Executive Committee Member & CEO of Societe Generale Albania

Bozhidar TODOROVAAB Executive Committee Member & CEO of First Investment Bank

Endrita XHAFERAJSecretary General, Albanian Association of Banks

Hysen ÇELAChairman of Albanian Institute of Authorized Chartered Auditors (IEKA)

Adrian CIVICIPresident & Head of Doctoral SchoolEuropean University of Tirana

Spiro BRUMBULLIChief of Cabinet, Ministry of Finance

Enkeleda SHEHIChairwoman of Albanian Financial Supervision Authority

ALBANIAN ASSOCIATION OF BANKSBulevardi: “Dëshmorët e Kombit”, TWIN TOWERSTower I, Floor 6, A3, TiranaTel: +355 4 2280 371; Fax: +355 4 2280 359E-mail: [email protected]; www.aab.al

Printed by:

World-class publishers in economics speaking Albanian through UET Press by Andi BIDOLLARI p.31

www.aab.al • BANKIERI • 5

EDITOR’S DESK

Debt is not the-word-of-the-day, instead it is pretty much in vogue, everywhere we go ev-

erywhere we read or about economics, on a 24/7 basis. It came into the limelight in the aftermath of the latest financial and economic crises of 2008, especially at European countries, which are prac-tically drowned in debt. The last remembered hot debate, in a global scale, about debt was the third world debt crisis and especially the Latin Ameri-can debt crisis. One of the “magic” solutions, along with IMF interventions, was the brilliant idea of U.S. Treasury Secretary, Mr. Nicholas F. Brady to “securitize” it, by issuing Brady bonds. But the size of such debt and the indebted coun-tries’ typology has nothing in common with the current debt situation in Europe, including both public and private debt, and the “magic” nowa-days is sought at regulators’ and regulations’ level.

But what’s about Albania? Are we drowned in debt? No one could give an exhaustive reply, as figures and situations cannot help form an ex-haustive and one-off response. Currently, there is no “scientific” level of debt burden efficiency and riskiness, except in the area of corporate finance; instead there are only some pre-defined criteria and recommendations about public debt, which as a rule, are deliberately breached by those who have established them. When talking about debt we should consider both the public and the pri-vate one and in terms of numbers, such debt bur-den is not alarming; instead the public debt is fac-ing a yellow light, but the private one is deemed

ARE WE DROWNED IN (BAD) DEBT???

by Dr Elvin MEKA1

Editor-in-Chief

as relatively low, when compared to regional economies, not to mention developed countries.

But why worrying about debt, as long as its burden seems to be not at red alert? Unfortu-nately, gross and nominal debt figures are a bit tricky and misleading. The real problem is not how much debt you owe, but how much repay-ment power you got with, and how stable your future cash flows are. This is the root of argument for the Albanian debtor, either government, busi-ness or household. As the economy has entered a low-growth-but-prolonged-path and the econom-ic expectations for households and businesses seem bleak, they just curb expenses, investments and employment, thus contributing less for state budget. Furthermore, debt repayment power and base has been compromised and deteriorated continuously, since 2009, thus piling up non-per-forming loans at banks. So, the vicious circle be-comes self-sustained and bank financing become a precious, hard-to-find, hard-to-sell reality. This credit crunch turns into liquidity and payments’ crunch, which feeds up non-performing loans even further. Definitely, the problem is not the original debt, but the ever-increasing outstanding one, which is becoming the elephant in the room and bankers are staying with it, in front of it. In-tuitively, this is called systemic risk.

Once, John Maynard Keynes quoted: “If you owe your banker a thousand pounds, you are at his mercy. If you owe your banker a million pounds, he is at your mercy.”

So, who is drowned in (bad) debt???

The real problem is not how much debt you owe, but how much repayment power you got with, and how stable your future cash flows are. This is the root of argument for the Albanian debtor, either government, business or household.

1 Head of Department of Finance, EUT-UET

6 • BANKIERI • www.aab.al

FRONT LINE

PRIVATE DEBT IN ALBANIA – A LACKLUSTER EXISTENCE

Since the outbreak of the recent fi-nancial crisis, the borrowing be-

came the “monster evil”, we cannot live without, whereas the destabili-zation of macroeconomic parameters has transferred the economists’ atten-tion toward issues related, primarily, to the public debt. Such situation and discussion has, in fact, overshad-owed another kind of debt, typically the private debt. The analysis of such, is perhaps even more important, as its negative impact on economic growth is, in qualitative terms, larger than the public debt’s one.

Private debt generally refers to debt that various entities (natural, legal persons) borrow form the finan-cial system, i.e. money to finance con-sumption or investments. It is quite understandable the role of financing entities that generate aggregate de-mand, either through consumption or through investment, particularly in the context of an economic crisis. In other words, financing business projects, or fostering consumer de-mand, just gives a momentum to the economic growth and the economic mechanism as a whole, by improv-ing macroeconomic parameters,

by Mr Altin HOTI, PhDDean of Faculty of Economy

“LUARASI” University

whereas, the debt for private invest-ments is by far, in terms of priority, the most important one. The econom-ic impact of investments is broader, on the economic chains, and with a wider timespan, given that invest-ments have different duration, when compared to consumption. Within Albanian reality, this kind of debt has a far more deep impact on economic growth, especially in circumstances where alternative sources of financ-ing business projects, out of banking channels, are quite limited. Also, in an economy where the private sec-tor is the major GDP contributor, the main impact on economic growth is therefore produced by private debt, whereas the public debt has a small effect, or plays an indirect role. The importance of private debt goes beyond its contribution and impact on economic growth. Some econo-mists at the University of Cambridge have concluded that “the rapid growth of private debt burden inevitably leads to deflation and debt crisis, while the criti-cal level of sovereign debt only inhibits the pace of economic growth. The analy-sis of long-term historical records of both debt indicators have emphasized the pri-

mary role that private borrowing plays in building the financial stability1” Also, financial crises have a much greater impact on the dynamics of the econ-omy, compared to budgetary crisis. The collapse of the financial sector in the US during ‘30s reduced the GDP level by 30 percent, while debt crisis in Argentina reduced it by 20 per-cent2.

Stimulating the private borrowing growth is an imperative, not because of a low private debt-to-GDP ratio, but for the sake

of an acute need to ensure real economic growth, production and employment, at a time when, as World Bank’s experts

put it, the impact of Central Bank’s monetary policy is almost exhausted, with relation to promoting lending.

Within the Albanian reality, this kind of debt has a far more deep impact on economic growth, especially in circumstances where alternative sources of financing business projects, out of banking channels, are quite limited.

1 Jordà, Òscar, Moritz Schularick, and Alan M Taylor (2013), “Sovereigns versus Banks: Crises, Causes and Consequences”, CEPR Discussion Paper 9678. 2 Reinhart, Carmen M and Kenneth S Rogoff (2009), This Time is Different: Eight Centuries of Financial Folly, Princeton, NJ: Princeton University Press.

www.aab.al • BANKIERI • 7

What’s about private debt in Albania?According to INSTAT and Bank of Albania, by end-2008, the private debt amounted at approx. ALL 3.89 billion, where 65.4 % was business loans and the remaining 34.6 % the household loans. The year 2011 fea-tured a sustainable trend of lending growth rate, averaging at an annual 11 percent, while the 2012 witnessed a clear sluggish growth dynamics, with a meagre rate of 2.43 %, and such trend continued even through-out 2013, which recorded negative growth rates. In October 2013 the private debt stock decreases by -2.77 percent, compared to end-2012. It’s worth saying that, to a great extent, the decreasing demand for busi-ness loans, was the key contributor to this reduction, which in turn, has even larger effects on the economy. As regards the trend of consumer lending, it has been negative since the beginning of 2009, without any strong deviation. The reason behind such behavior is somewhat under-standable, in the frame of financial crisis, which was transferred to Al-bania. The psychological reasons are chiefly associated with declining trust and confidence, as well as the implementation of new rules by par-ent banks, following one of the deep-est crises in their countries of origin. Here below, we can list some prob-lems related to private debt in Alba-nia:(1) The low level lending rates and its

slowing pace, which does not stimulate economic growth quite enough, instead it has stimulated “usury”, loan sharks and barter trade. Such situation has in-creased informal cash flows, has reduced the effectiveness of mon-etary policy, as well as the effi-ciency of government agencies’ policies in general, in addressing this problem. Moreover, the pri-vate debt-to-GDP ratio is approx. 41 percent and is considered as a low rate (compared to developed countries, e.g. US, where such ra-tio is over 250 percent for 2008, including non-bank sector; Portu-gal and Greece had, in 2009, a pri-vate debt level (excluding non-bank sector) of 200 % and 100 % of GDP, respectively), which reveals an economy operating be-low its potential;

(2) The banking sector “monopoly” in financing business projects, the public sector monopsony in uti-lizing bank financing of Treasury Bills, with minimal risks and timely guaranteed payment in-stallments, thus maximizing the commercial banks apathy;

(3) Non-performing loans. The in-crease to current levels is related to a large extent with the so-much-discussed issue of public debt. This indicator is, at the same time, one of the key factors, caus-ing the sharp drop of bank lend-ing rates. In a time when businesses are insolvent, not merely by temporary liquidity problems, the “lifeboat” of fur-ther debt, cannot avoid bankrupt-cy at the end, thus increasing even further the problem loans rate;

(4) Lack of liquidity, not in the bank-ing system, but in the real econo-my. In other words, we have a good stock of deposits, which are not optimally channeled towards financing the real sector. Typical-ly, lowering debt figure, by in-creasing savings, turns into a paradox: the rapid growth of de-posits/savings deepens the reces-sion and increases the debt burden, as the economy lacks proper and sufficient funding.

Addressing the private debt issue in AlbaniaStimulating the private borrowing growth is an imperative, not because of a low private debt-to-GDP ratio, but for the sake of an acute need to ensure real economic growth, pro-duction and employment, at a time when, as World Bank’s experts put it, the impact of Central Bank’s mone-tary policy is almost exhausted, with relation to promoting lending. Low-ering the refinancing rate is currently a theoretical measure, which does not produce real results, because it is for the high level of non-performing loans and many other factors that are inhibiting banks and businesses to lend and borrow, respectively. In such conditions, some comprehen-sive steps should be taken with, be-yond monetary policy, as follows:(1) Identifying priority sectors, as

well as their priority classifica-tion, as some sectors have reached saturation with respect to their role and weight in the economic growth and GDP (e.g. the con-struction sector). According to the World Bank, also, some sectors of the economy are fully saturated to generate real economic growth through domestic demand3. This would require a necessary dia-logue/joint roundtable between stakeholders (commercial banks, central bank, government, busi-nesses), to set out these priorities, in order to channel real financings with minimum risks;

(2) Developing and deepening the financial market with new instru-ments (e.g. corporate bonds, etc.), in which commercial banks will play the primary role, in order to increase private debt, and also ensuring a risk distribution/mini-mization, through diversification.

(3) Increasing the active role of banks in risk-taking and economic-fi-nancial assistance, as this would create more flexibility in lending channels, by increasing not only the loan amount, but also its qual-ity.

(4) Conducting a rapid resolution of government debt on to business-es, which would give a positive impulse to the real sector of econ-omy, by increasing business abil-ity to repay non-performing loans and mutual trust between banks and businesses, to relieve fund injection, a so-much welcomed event in the economy.

…we have a good stock of deposits, which are not optimally channeled towards financing the real sector. Typically, lowering debt figure, by increasing savings, turns into a paradox: the rapid growth of deposits/savings deepens the economic downturn and increases the debt burden, as the economy lacks proper and sufficient funding.

3 http://www.worldbank.org/content/dam/Worldbank/document/eca/Albania-Policy-Briefs-2013.pdf

8 • BANKIERI • www.aab.al

www.aab.al • BANKIERI • 9

FRONTLINE

It is practically impossible for a country’s economy to develop

without borrowing. The use of bor-rowings by public finance manage-ment is driven by the need to cover numerous expenditures and to im-prove public services quality, to cope with difficult situation, in times of economic downturn, and the invest-ment needs, necessary to spur eco-nomic development and welfare. The fact whether the debt is a “bad” thing for a good reason, is out of question. The real question and issue for public borrowing policies is how much debt is affordable. The economic history is full of different cases, about the role played by public borrowing. A manageable debt (meaning that there are repayment capacities and oppor-tunities) represents a success story; an uncontrollable debt (typically playing with figures, thus hiding the truth for a certain period of time, fear-ing a cease of funding) has led to the miserably situation, instability and depression. Although the economic theory justifies and supports public borrowing, a well-accepted formula, about the optimal size of the public debt, is yet to come. Despite the fact that, the European Union (EU) has set for member states a debt limit re-quirement of not higher than 60 per-

INCREASING PUBLIC DEBT – DOING A “BAD” THING FOR GOOD REASON

by Dr Spiro BRUMBULLIHead of Cabinet

Ministry of Finance

If the debt level is considered high for the country’s economic power and GDP growth rates do not guarantee the obligations’ repayment, therefore

government spending cuts are part of an economic austerity regime, where even the tax regime changes, in

order to contribute to increased revenues.

cent and a budget deficit not more than 3 percent of GDP, respectively, such criteria, as the latest debt crisis showed, was not respected.

The size of public debt is not just a matter of numbers. Usually, after the debt figure appears the type of cur-rency, which means that those mon-ies must be repaid. Here is the key to solve the debt size. What are the repaying power and capacities of an economy? Should the government’s current state of affairs do not guar-antee debt repayment it is bound to collect more money. Collecting more money means higher taxes, as the

main way for a government to col-lect revenues is through the tax sys-tem. Higher debt means higher taxes. Debt repayment is not in the hands of the borrower, in the sense that it can choose to pay now or later on. Debt is an obligation and the failure to repay has grave consequences for a coun-try. Every government definitely wants to avoid international auster-ity measures and is keen to negotiate with lenders for acceptable solutions. But the debt is not written-off. It may be restructured with both parties’ consent. This means that the borrow-er can neither show its teeth to the lender, nor ignoring or denying the debt. History shows examples, espe-cially in power transition periods in the hands of dictators, when the debt is refused or otherwise denied. But this is a temporary event, because af-ter the system’ change, the first thing to be negotiated are old debts.

Public debt management requires prudent and responsible behav-ior to public finances. Developing the economy via borrowing is not an option given for free. Countries which have borrowed endlessly, in the name of making heavy invest-ments but with insufficient returns from such investments, which will affect debt repayment, do not repre-sent any success stories. They are in dire situations, with deep political and financial instability, with an in-flationary situation and high costs to the economy and society, in restoring

Establishing financial discipline in paying all bills on time, halting investments which are not supported with budgetary funds, strict monitoring of budget expenditures, reining on investments which go beyond incomes, tight control on carry-forward liabilities’ repayments, etc., are measures planned to be implemented, with the purpose of establishing a new behavior and approach towards public finances.

10 • BANKIERI • www.aab.al

macroeconomic stability. Albania’s current situation has a tendency to-wards macroeconomic imbalances with risky consequences in main-taining macroeconomic stability. The pretended development of previous years, based on debt growth, has caused macroeconomic imbalances to be more significant and sensitive. A sizeable amount of money is spent, rather not well-studied, in the name of infrastructure development and based upon the argument that invest-ments will be repaid by increased fu-ture revenues. Public debt is expect-ed to reach 69 percent of GDP in 2013, or about ALL 936 billion. The weak-ening of fiscal discipline by remov-ing the only defense instrument, as the ceiling of 60 percent, equal to the level set for EU member countries, has just weakened the discipline of public finances.

Often the real debt is disguised behind reporting inaccurate figures. In underdeveloped countries with poor infrastructure, cooking books and manipulation are quite present. In our case, for example, the un-disclosed government obligations, owed to business for unpaid public works, lack of VAT refund and pre-paid income tax, has affected the debt by a 4 percent increase. There are other obligations, only mentioned, but not certified yet, like: court deci-sions, obligations to ex-owners and ex-political prisoners, obligations of state-owned enterprises, etc. We are witnessing a chain of payment de-linquencies and barter phenomena within the economy, due to lack of li-

quidity. The saturated debt situations should be handled with professional-ism and sacrifice. If the debt level is considered high for the country’s economic power and GDP growth rates do not guarantee the obliga-tions’ repayment, therefore govern-ment spending cuts are part of an economic austerity regime, where even the tax regime changes, in order to contribute to increased revenues. The toughest measures in an eco-nomic austerity are wage reductions and job cuts. This is an undesirable, but inevitable situation. Resolving the debt payment issue by printing money is even more problematic than defaulting on it.

Debt reduction is not achieved through monetary measures. Fiscal policy is important, because it reduc-es excessive costs and expenditures, expands fiscal space to increase rev-enues, but this is not enough, yet. Economic growth is the only guar-antee to reduce debt. If we analyze both indicators for calculating public debt (the numerator of the ratio, rep-resented by borrowing and the de-nominator, represented by GDP), it is obvious that this ratio is inversely re-lated to GDP. So, an increase of GDP, other things being equal, reduces the debt ratio. Also, a reduced borrowing (i.e. budget deficit reduction) will im-pact the reduction of such indicator positively, but is difficult, in the med-term, to lower borrowing to that ex-tent, which could impact a reduction in the debt level. Thus, it is advisable to spur economic growth, because it is the only way to create stability,

through creating new jobs and ex-panding taxable income basis. In this case, fiscal policy has a unique role in stimulating the economy, through in-centives it injects into certain sectors. Economic austerity regime is tempo-rary, usually lasting for several years, until the economy rebounds, but it guarantees the restoring of macroeco-nomic balance. Currently, Greece is under an economic austerity regime. By contrast, Albania negotiated with the IMF a flexible three-year deal, which is expected to be approved by respective board in January-February 2014. According to a flexible agree-ment, debt management is conduct-ed by developing new methods, and aims at stopping default and helps in preventing the situation to deterio-rate towards bankruptcy.

Notwithstanding the regime that applies to put public debt under control, it is important that lessons drawn from a certain situation will not be repeated and a new practice will be implemented, hereafter. In case of Albania, establishing finan-cial discipline in paying all bills on time, halting investments which are not supported with budgetary funds, strict monitoring of budget expendi-tures, reining on investments which go beyond incomes, tight control on carry-forward liabilities’ repay-ments, etc., are measures planned to be implemented, with the purpose of establishing a new behavior and ap-proach towards public finances.

Countries which have borrowed endlessly, in the name of making heavy investments but with insufficient returns from such investments, which will affect debt repayment, do not represent any success stories.

www.aab.al • BANKIERI • 11

JOURNALIST’S CORNER

DEBT – THE UBIQUITOUS REALITY

There are endless articles on debt, written by different media, over

the past two years. Furthermore, it is more than obvious that DEBT has been the most frequently quoted word, at economic section of broad-casted news, or newspapers. In No-vember 2012, the former Mr. Berisha Government lifted the legal debt lim-it of 60% of GDP, a move which en-couraged further growth of such in-dicator. The former opposition, now sitting in the government, pledged to reduce the debt burden. Now it is not only impossible, but seems to be the only device to get public finances and the economy out of the crisis. Along with a debt increase by ALL 22 bil-lion, as projected by the normative act to revise the last year’s budget, the new government has just negoti-ated a new debt deal of US$ 300 mil-lion with IMF and a loan of US$ 350 million with the World Bank, due to be fully formalized by end-January.

If we go down further, we’ll see that businesses are not better off. They are drowned in debts with banks, as the former government still owed them millions of dollars, for unpaid public works already done by them. Their debt saga goes on with payables, unpaid salaries and wages. If we turn to individuals, the situa-tion becomes even more painful. Per-sonal borrowings from relatives and friends, even buying-on-credit to next door grocery, are piling up to their bank loans. This is the result, yielded by the recent Bank of Albania’s sur-vey, where out of 1,210 households surveyed across the country, 33% were indebted and a part of debt was financing consumption. Even energy sector companies, like: KESH and CEZ Shpërndarje are report-ing multi-zeroes debt figures; not to

by Ms Aurora SULÇE

mention other public utilities, such as water companies. Everything has en-tered a vicious circle, where debts are not solving anything, and everyone owes to everyone. There are theories in economics, which point out that “a loan may be taken for investment purpos-es, which in turn, yield development.” This is certainly not the case for Al-bania. The combination of a debt level, deemed to exceed 72% of GDP, with an annual economic growth not higher than 1.3%, does not leave any imagination for economic develop-ment, instead turns the country into a los-making venture (the growth rate for 2014 is forecasted at 2.1 %). Actu-ally, we pay, on average, 6% interest rate for each ALL borrowed, which equals 3.6 % of GDP. This means that growth does not fuel development and well-being, instead, is goes for servicing debt.

What will happen and what should we do? Again, the only so-

Everything has entered a vicious circle, where debts are not solving anything, and everyone owes to everyone. There are theories in economics, which point out that “a loan may be taken for investment purposes, which in turn, yield development.”

This is certainly not the case for Albania.

lution remains debt: a new debt to repay an old debt, a popular and productive economic theory, when the new debt is dealt with a lower in-terest rate than the current one. Such a debt was negotiated with IMF and the World Bank, but all scenarios in-clude inherited costs, which will, un-doubtedly, be borne by the new gov-ernment and inevitably, by all of us and the generations to come. These are economic and political costs, as it will increase pressure on future fiscal and budgetary policies. Is this the right way? Now there is no more time for such reflections, as unfortu-nately, this is the only way available.

As for citizens the heaven must wait, at least until the new govern-ment debt creates a discharge valve in the economy. So, the focal point is that, how fast such effects will be incorporated in the everyday life and unavoidably, within the Albanian fi-nancial system!”

12 • BANKIERI • www.aab.al

www.aab.al • BANKIERI • 13

INTESA SANPAOLO BANK ALBANIA –

STANDING FIRM IN ALBANIA

INTERVIEW

Mr Silvio Pedrazzi,Chief Executive Officer,

Intesa Sanpaolo Bank - Albania

BANKIERI: FIRST OF ALL, I WISH YOU ALL THE BEST FOR YOUR NEW POSITION WITH THE BANK. WHAT ARE YOUR FIRST IMPRESSIONS ABOUT THE ALBANIAN BANKING SYSTEM IN TERMS OF DEVELOPMENT, COMPETI-TION AND PRODUCTS?Thank you very much indeed for the wishes, I’m really glad and honored to serve as CEO in Intesa Sanpaolo Bank Albania. First impression is quite positive even if banking industry, in general, is facing a very challenging period across all the countries. As far as the Albanian one is concerned, we can observe lights and shadows. If on one hand the system is very well capitalized and liquid, on the other hand the level of profitability is definitely low and deteriorating, mainly due to the unsatisfactory quality of the assets. Of course banks, as the other indus-tries, are suffering a stagnating environment but I believe the economy will soon pick up. Under these circumstanc-es, given also the extraordinary low level of interest rates, the competition will increase; key success factors will be the ability to optimize costs, an effective risk management approach as well as the quality of human resources. On the business side, customer care, meaning the capability to address customers’ needs and the transparency of the commercial proposals, will make a huge difference be-tween banks.

BANKIERI: AS OF ONE THE LEADING BANKING GROUPS IN ITALY, AND IN THE FRAMEWORK OF BIG REGULATORY MOVEMENTS IN THE EUROZONE, IS THERE ANY CHANGE IN THE BANK’S BUSINESS STRATEGY IN ALBANIA, FOR THE YEARS TO COME? Intesa Sanpaolo Group is definitely one of the most solid,

liquid and balanced banking group in the Eurozone, more-over the relationship between Italy and Albania is strategic. Our goal is quite clear: we’ll keep on developing both cor-porate and retail, consolidating and improving our posi-tion.

BANKIERI: COULD YOU PLEASE NAME SOME KEY ACHIEVEMENTS FOR 2013 AND SEVERAL KEY PRIORITIES OF THE BANK DURING 2014?In the last year Intesa Sanpaolo Bank - Albania achieved excellent results, implementing also a number of projects aimed at setting the pre-conditions for further business developments. I think, among others, of the implementa-tion of sophisticated tools for risk management, introduc-tion of a full set of customer oriented policies as well as a strong and effective cost management system.As far as the this new year is concerned, we have planned several important investments and started the upgrade of the IT System which, for instance, will enable the Bank to provide customers with the most updated mobile technology. In addition, we are going to launch a number of new and innovative products aiming at the satisfaction of customers’ needs. Specific attention will be paid to the segments we deem strategic for the local economy including agriculture, tourism, manufacturing as well as energy production; SMEs will enjoy a new business attitude. For retail too, new products are coming soon.

BANKIERI: WHAT COULD BE THE MOST DISTINGUISHING FEATURE OF INTESA SANPAOLO BANK – ALBANIA?Proximity to customers, transparency, fairness, rapidity and technology.

Intesa Sanpaolo Group is definitely one of the most solid, liquid and balanced banking

groups in the Eurozone, moreover the relationship between Italy and Albania is

strategic. Our goal is quite clear: we’ll keep on developing both corporate and retail,

consolidating and improving our position.

14 • BANKIERI • www.aab.al

BANKING SYSTEM

BANK OF ALBANIA’S PLATFORM FOR HANDLING NON-PERFORMING LOANS – A NEW APPROACH

One, out of many problems the Albanian economy is being

faced now is the non-performing loans phenomenon, which has been increasing, since 2008. Bank of Alba-nia has shown its early concern about the phenomenon and has warned banks to take necessary precautions and measures, to anticipate such phe-nomenon, which can be summarized as follow: enhancing risk manage-ment quality, establishing appropri-ate structures, conducting timely and healthy loan restructuring, perform-ing stress-test analysis and increasing capital resources, in accordance with stress-test analysis’ results. These are accompanied with relevant legal and regulatory amendments, aiming at early handling of the phenomenon, either for banks or other institutions, where the most important are: chang-es and amendments of the banking act, amendments to the regulation “On credit risk management”, or re-laxing regulatory requirements for loan restructuring.

However, the high rate of non-

by Mr Gerond ZIUHead of Supervision Office for

Systemic BanksSupervision Department,

Bank of Albania

performing loans has shown that important factors, which may affect in mitigating this phenomenon, have not worked with all their possible po-tential. The difficulties encountered during the collateral enforcement did not help enough in delivering relevant messages to individual eco-nomic operators about their respon-sibilities to payback their obligations due to banks. It was expected that, the phenomenon of writing-off prob-lem loans from banks’ balance sheets, to be the word of the day (although it doesn’t mean, in any case, that bor-rowers would bypass their respon-sibilities to repay their obligations); typically it didn’t. Current fiscal legal framework has adversely affected banks, by inhibiting them in writing-off problems loans, due to loose inter-pretation space, created in this case. In this regard, it can be said that the non-performing loan rate does not represent the actual loan quality un-der the influence of distorting factors. Loan restructuring is an event, with expectations of facilitating borrow-ers’ repayment ability and by provid-ing a deeper breath for the country’s economy as a whole.

Legal initiatives and regulatory changes have been typically associ-ated with reducing the non-perform-ing loans’ level, by way of creating a suitable environment with expected positive impacts. Amendments to the Civil Procedure Code aimed at increasing the efficiency of the col-lateral enforcement process, both in

terms of reducing bureaucracy and facilitating liquidation conditions of pledged properties, by ensuring a broader match with market offers. Amendments to the Minister of Fi-nance’s Guidelines on clarifying the meaning of bad debt for financial institutions, is expected to ease the loan write-off process and thus low-ering the artificiality level of non-performing loans. Bank of Albania’s package of measures, effective earlier this year, was intended to provide positive incentives in economic and financial environment, at least until the end of 2014, by relaxing regu-latory requirements to encourage credit to economy. Bank of Alba-nia’s regulatory changes, in relaxing regulatory criterions for restructured

The issue of loan restructuring has drawn a constant attention to the Bank of Albania, and along with relaxing regulatory changes made in the beginning of the year, it

will get further attention, in the frame of recent initiative to introduce the platform handling non-performing loans.

The purpose of this platform is to analyze and handle troubled borrowers, or those that have showed signs of problems in individual banks’ portfolios. Banks are required, as the first step of platform’s implementation, to report all outstanding business loans, except those classified as “standard”.

www.aab.al • BANKIERI • 15

loans’ classification and provision-ing, have also created conditions to encourage this process. This is sup-ported also with Bank of Albania’s publication of two guidelines for loan restructuring, one for business loans and the other for individuals ones, which drive both parties to en-ter into a restructuring relationship. Bank of Albania, has, through con-stant messages since the breakout of international financial crisis, aimed at raising banking system’s awareness to perform early loan restructurings, as one of the most important instru-ments to assist business activity con-tinuity and the economy as a whole. Similar practices have been followed by countries which have been faced with severe financial crisis; they have undertaken large-scale restructuring in the economy, for which the most representative ones are the cases of England, South Korea and Turkey. The issue of loan restructuring has drawn a constant attention to the Bank of Albania, and along with re-laxing regulatory changes made in the beginning of the year, it will get further attention, in the frame of re-cent initiative to introduce the plat-form handling non-performing loans. This platform was developed by Bank of Albania, in cooperation with the Financial Sector Advisory Center (FinSAC), in Vienna. The center was

established by the World Bank and aims to provide technical assistance on regulatory and supervision issues for the financial sector, central banks and financial regulators in Europe and Central Asia. FinSAC will assist the implementation process of this platform, through the services of a specialized company with interna-tional experience, including the re-gion Albania belongs to.

The purpose of this platform is to analyze and handle troubled borrow-ers, or those that have showed signs of problems in individual banks’ portfolios. Banks are required, as the first step of platform’s implementa-tion, to report all outstanding busi-ness loans, except those classified as “standard” (as prescribed by Regula-tion: “On Credit Risk Management”). In addition to general information of exposure to the borrower, reporting requirements include also those re-garding its financial records for the past three years, as well as pledged collaterals. A certain number of bor-rowers will be selected, out of this re-ported list, where recovery possibili-ties and opportunities will be indi-vidually analyzed. The selection will be made taking into consideration a number of factors: the loan size, the economic sector in which it operates, geographic location, level of expo-sure to the system, etc. The goal is

to perform the most representative selection, at system level, both in quantitative and qualitative aspects, in order to achieve the widest impact possible, not only for banks but also for the country’s economy.

Banks will be required, for each selected borrowers, to prepare a re-covery plan. A detailed analysis of the recovery possibilities and oppor-tunities will be conducted in parallel, with the help of the consulting com-pany, through the use of its method-ology. The results of these analyzes will be consulted with those of banks and discussed with them to reach an appropriate and sustainable solution for borrowers, as well as for banks. This would create an opportunity not only at increasing options for tai-lored solutions, according to borrow-ers’ difficulties but also in applying them at the entire portfolio’s level, by establishing a good basis for future experience.

In order to provide the exer-cise with a more stable feature, and to have a complete coverage of all banks, the results of the exercise will be further analyzed, to assess the possibility of intervention in the mar-ket with further policies. As the ini-tial identified element, in this regard, is the prescription of regulatory re-quirements, asking for a greater pres-ence of banks’ Boards of Directors in the analysis and monitoring of large borrowers, as well as in drafting and periodic reviewing of recovery plans for these borrowers. Further areas, which will be identified for regulatory changes and ways of their implementation, will be thoroughly discussed with all banks.

Banks will be required, for each selected borrowers, to prepare a recovery plan. A detailed analysis of the recovery possibilities and opportunities, will be conducted in parallel, with the help of the consulting company, through the use of its methodology.

16 • BANKIERI • www.aab.al

www.aab.al • BANKIERI • 17

INTERVISTABANKING SYSTEM

SECURITY ROOF

by Mr Roland TASHIChairman,

AAB Bank Security Committee

Security should be considered a “product” of activity and commitment of security structures, leadership,

stakeholders and interested and certified operators, as a roof that will protect and guarantee normal working

and business conditions for the banking system.

flourishing and booming, which rea-ched the finish line in 1997, with qua-si-war consequences.

Security should be considered a “product” of activity and commit-ment of security structures, leader-ship, stakeholders and interested and certified operators, as a roof that will protect and guarantee normal wor-king and business conditions for the banking system. Subsequently, this obtained “product” will serve as a public good, which is then utilized either by those who work and have relationship with the bank, or more widely, by the general public. A que-stion naturally arises: how should the “security roof” stand upright, which should be its pillars, so as to ensure its initial existence, and then to be efficient, protective and stable? It should be understood beforehand, that all businesses, especially finan-cial ones, where money is their base product and in this context, they are the hardest hit by crime and in-sider’s abusive actions, should have very clear concepts about security, and that their activity cannot begin without establishing initially the re-spective security unit, which would draft and implement the whole pro-tection system to guarantee a normal course of the activity.

The first pillar is represented by a special functioning structure, wi-thin the organizational tree of a bank or other financial businesses, which performs security duties, only. De-

Albania entered the capitalist eco-nomy a bit later, compared to

other countries in the region. This fact, and the anxiety and rush to milk the “product” of the new social system, along with many social and economic changes, called for a total reshaped concept of security, natio-nal security and public safety, crea-ting new concepts for human securi-ty, business security and especially, central bank, banking and financial system security, which gradually began to form and enter the path of capitalist development.

Security in the banking and finan-cial system, which began to shape its structure either form the local busi-ness or also the foreign one, would turn to be the keyword and guaran-tee for a smooth functioning of the system, to avoid creating security violations precedents and creating disturbances and social unrest. Insuf-ficient attention towards banks, not only in terms of physical protection and security, was followed by dra-matic events during the first half of 90s, when pyramid schemes were

spite that this is a requirement impo-sed by Bank of Albania’s regulations some banks have not established or appointed special security units or specialists. The security and pro-tection duties’ oversight are passed to employees who perform other du-ties, mainly of administrative nature. The main task of this “pillar” should

It should be understood beforehand, that all businesses, especially financial ones, where money is their base product and in this context, they are the hardest hit by crime and insider’s abusive actions, should have very clear concepts about security, and that their activity cannot begin without establishing initially the respective security unit, which would draft and implement the whole protection system to guarantee a normal course of the activity.

18 • BANKIERI • www.aab.al

be: forecasting (opportunities’ re-duction) and protection (consequen-ces’ reduction). The experience of a professional security specialist plays a particularly important role in predi-cting, assessing and interpreting spe-cific situations at a bank, company, or any other organization. Rather, his lack leads to an escalated exposure level against risk and increasing eco-nomic costs to reduce consequences. One of the influential consequences in the business remains the reputatio-nal risk, which along with economic costs, affects public confidence, espe-cially to the banking business, where sensitivity and attention is even gre-ater.

The second pillar is the legal and regulatory basis. Security structures should operate only on legal grounds, according to administrative acts and practices, approved by leadership. It should be mentioned that, given the scope and tasks they perform, the security structures have direct or indirect access, through electronic se-curity systems, cameras, etc., in vital and sensitive areas, procedures and practices for the institution. In this respect, should their activity is not “disciplined” by a full administrati-ve practice, with separated authori-ties and powers, it could increase the probability that, certain segments of such structures may abuse, escalate exposure to risks, thus damaging the

institution.The third pillar relates to orga-

nizing and operating physical pro-tection, bank’s active protection, through human resources, by using security services performed by bank employees, or employees of Physical Security and Protection Companies (PSPC-SHRSF). Although the third pillar is positioned in the center, as the backbone of the “security roof”, it remains the most vulnerable and su-sceptible. This is so, because the indi-vidual, who is in charge as the secu-rity officer, who serves as teller or as the operator, or performs the role of monetary values’ transporter/escort, or the individual who faces a crime scene, directly and physically, shall bear and suffer the psychophysical and psychosocial consequences. The effective harmonization of protection measures through human resources with those electronic and technical ones, not only increases the level of service’s efficiency, but also protects and keeps the individual away from the psychological damage.

The fourth pillar relates with the functioning of electronic security and other safeguards that are designed to operate without physical presence of individuals. Undoubtedly, it is an im-portant and “hard-to-corrupt” pillar, which the more sophisticated it is, the more it prevents abusive and robbery acts, and the more it helps security

structures to increase the protection level of the facilities, and especially human resources. The “electronic protection”, otherwise known as passive protection, through techno-logical devices and systems, opera-tes on a “non-stop basis”. It provides protection to business, its assets and cash, during the rest of the day, and holidays, when the institution does not use human resources’ securi-ty service. It should be emphasized that, data obtained and archived by electronic security systems, especial-ly those provided by closed circuit television system (CCTV), access control entries’ data, etc., will serve as material evidence for crime exper-ts and law enforcement agencies, in cases of burglaries, insider robberies, and other various abusive situations. Electronic protection systems must follow contemporary technological developments; banks and all inte-rested institutions shall implement and install programs and advanced systems that enable full disclosure of any abusive event, or crime scene.

The fifth pillar consists in conti-nuous training of bank, institution or enterprise’s employees, regarding se-curity and caretaking issues at work. Notwithstanding that, staff training and information about all risks asso-ciated or affected by their workplace is a legal requirement, it should be considered a “must” and business policies’ priority, at any level what-soever

Pursuant to Bank of Albania’s re-quirements, banks get physical secu-rity and transport & escort monetary value services by a PSPC-SHRSF. It is quite important that, given the speci-fic feature such services have for ban-ks, the PSPC’s employees must have specific periodic training, about the manner of service conduct and per-formance, responsive actions, in case of any bank or armored vehicle rob-bery and most important, when and how and to use guns. In many ban-king business units, which operate in downtowns with great frequency movement of citizens and vehicles, the use of firearms by untrained em-ployees would cause more problems than the consequences of a robbery.

www.aab.al • BANKIERI • 19

EXPERTS’ FORUM

market as a whole, enhancing coordi-nation between regulators’ actions in both domestic and crossborder level, as well as strengthening the supervi-sory and regulatory standards, in an international scale.

Although, when talking about financial sector and crises, we refer primarily to banking market and banking system crises, leaving in disguise the other components of fi-nancial markets, such as: insurance market, private pension funds and securities market, which are not of less importance. These segments of the financial sector, if developed pro-perly, turns into important elements of an effective and healthy financial system. Through their contribution to the expansion and deepening of the financial system, they would ser-

It is already known the fact that the financial system constitutes the

cornerstone of a modern economy. In one way or another, each of us is in a constant contact with the financial system. In the emerging economies, financial system has also a significant importance, because its performance and development affects widely the overall development of the economy. A sound and modern financial sector contributes to the economy’s health. Meanwhile, the financial crisis, as the history shows and the recent global financial crisis of 2007-2008 confir-med, causes serious consequences for a country’s economy and popu-lation. Sometimes, restoring it takes several years to complete, which is quite a costly process. In this regard, it is quite important to prevent the occurrence of crises and adopt early and immediate measures, to mini-mize their consequences whenever they are unavoidable. Lessons drawn from the past financial crisis, have led to an increased emphasis on re-gulatory and supervisory process of financial sector, and have driven the attention not only on each financial institutions’ performance, but also on promoting stability in the financial

ve as a solid basis for capital forma-tion, economic growth and prospe-rity. The operators in the financial markets (life and non- life insurance companies, voluntary private pen-sion funds or investment funds and other intermediaries) provide ad-ditional financing channels for the economy, via their services, whose importance increases when lending channel is stagnant; provide long-term savings opportunities and ri-sk-averse products, diminish poten-tial financial and social problems in the future, alongside with their costs, increase investment alternatives for the general public and help out the general well-being of the population. Meeting these goals requires that fi-nancial market operators and finan-cial market itself must be managed properly, to assure their soundness and efficiency.

The same considerations are va-lid for Albania, despite the underde-veloped stage of its financial sector. For this reason, the keyword for the financial sector, in the medium term, will be “the stabilization”. What does the market stabilization literal-ly mean for the Albanian Financial Supervisory Authority (AFSA)? Su-rely, that does not mean and does not presume that the financial market in the country is currently unstable at all, or unable to operate. Rather, AFSA uses the term “stabilization”

STABILIZATION - THE KEYWORD FOR THE FINANCIAL SECTOR

AFSA will undertake a package of measures for the financial market in the medium term (2014-2016), which is

aimed to foster financial markets’ development, expand the range of financial products, improve consumer protection

and education, support financial reforms, and increase the effectiveness of market regulation and supervision.

The stabilization strategy could not be implemented by AFSA efforts alone, instead through a close cooperation with other institutions, particularly the World Bank and International Monetary Fund.

by Ms Enkeleda SHEHIChairwoman,

Albanian Financial Supervisory Authority, AFSA

20 • BANKIERI • www.aab.al

www.aab.al • BANKIERI • 21

population. In this regard, AFSA plays an instrumental role, which means underpinning supervisory capacity to ensure prudential su-pervision of pension funds and their sustainability.

5. Improving the functioning of in-surance market, by setting up well-defined standards regarding minimum reserves, liquidity, im-plementing the risk-based super-vision, or through the adoption of measures with long-term impact, such as developing programs to

ensure the services’ accountabili-ty and protection from risks ari-sing from natural disasters.

The stabilization strategy could not be implemented by AFSA efforts alone, instead through a close cooperation with other institutions, particularly the World Bank and International Monetary Fund. The stabilization of financial sector consistutes the keyword for financial sector, becau-se, at the end, it serves to the intere-sts of every citizen in Albania.

Lessons drawn from the past financial crisis, have led to an increased emphasis on regulatory and supervisory process of financial sector, and have driven the attention not only on each financial institutions’ performance, but also on promoting stability in the financial market as a whole, enhancing coordination between regulators’ actions in both domestic and crossborder level, as well as strengthening the supervisory and regulatory standards, in an international scale.

to depict a package of measures to be undertaken, by the Authority, for the financial market in the med-term period of 2014-2016. This package aims to foster financial markets’ de-velopment, expand the range of fi-nancial products, improve consumer protection and education, support financial reforms, and increase the ef-fectiveness of market regulation and supervision. Accomplishing these objectives will lead to strengthening of stability in the markets, which, on the other side, contributes to an in-creased economic stability. In other words, AFSA will undertake stabili-zation measures to ensure stability.

In other words, stabilization is ba-sed on these pillars:1. Strengthening the AFSA’s inde-

pendence, especially financial and operational independence, as a prerequisite to improve the ef-fectiveness of regulatory and su-pervisory process.

2. Supporting consumer protection, by identifying measures to increa-se transparency and simplicity to disclose information to financial institutions customers. Consumer protection is supposed to be reali-zed through promoting a sound competition in the financial mar-ket, which means providing pro-ducts at a reasonable cost to cu-stomers, without sacrificing or je-opardizing service continuity and benefits that a customer expects to receive from financial institu-tions, such as: damage repaymen-ts by insurance companies, real returns from investments funds, or pension payments from private pension funds.

3. Implementing the consolidated supervision, which means a new stage in the supervision process of financial institutions, through the combination and coordina-tion of supervisory competences of AFSA and Bank of Albania, on banks and investment funds. This calls for the need to strengthen the actual cooperation, to achieve an effective supervision of liqui-dity and market risks.

4. Supporting the development of pension’s third pillar and establi-shing the second one, as part of pensions’ reform. These mean a thoroughly reform in pension schemes of the country, in order to manage risks arising from demo-graphic changes, and to provide mechanisms for maintaining and enhancing the well-being of the

22 • BANKIERI • www.aab.al

THE ALBANIAN SECURITY INTEREST SYSTEM, IN THE FRAME OF LATEST CHANGES AND AMENDMENTS

EXPERTS’ FORUM

Mr Sokol ELMAZAJPartner, BOGA & ASSOCIATES

Ms Sabina LALAJSenior Associate, BOGA & ASSOCIATES

The year 2013 is marked with some important changes and amend-

ments in the legal framework as re-gards sthe security interest system, financial collateral and payments.1. The financial collateralDuring the first half of 2013, the Al-banian Parliament endorsed the Law On Payment System (no. 133/2013), which entered into force on 29 May 2013. The law introduced, inter alia, the financial collateral, in line with the Directive 98/26/EC of the Euro-pean Parliament and of the Council of 19 May 1998 “On Settlement Final-ity in Payment and Securities Settle-ment Systems”, as amended and the Directive 2002/47/EC of the Europe-an Parliament and of the Council of 6 June 2002 “On Financial Collateral Arrangements”.

The financial collateral is a new type of security interest that can be taken over cash and/or financial in-struments to secure repayment of loans and other obligations. The law defines “cash” as “…money credited to an account in any currency, or simi-lar claims for the repayment of money, such as monetary deposits…”, while financial instruments, as “…shares of joint-stock companies, either foreign or local, and other securities equivalent to shares in joint-stock companies, bonds and other forms of debt instruments, if these are negotiable on capital markets and any other securities which are nor-mally dealt in and which give the right to acquire any such shares, bonds or other securities by subscription, purchase or exchange or which give rise to a cash settlement (excluding instruments of

payment), including units in collective investment undertakings, money market instruments, precious metals credited in an account and claims relating to or rights in or in respect of any of the fore-going…”.

The financial collateral over finan-cial instruments is created by written agreement and is perfected by either transferring the possession of collat-eral to the collateral taker, or when the financial instruments are held, transferred or subject to any measure in such a manner that the collateral taker, or a person acting on its behalf, has the possession or the control of the financial instruments. The same applies to the financial collateral over cash, possession of which is trans-ferred to the collateral taker or trans-ferred in a special account, or is held, transferred or subject to any measure so as to be in the possession or under the control of the collateral taker, or a person acting on the collateral taker’s

behalf. The collateral taker notifies the debtor of the performed transfer by acknowledging the claim on the cash or the debtor’s obligation to rec-ognize explicitly the existence of the financial collateral agreement.

The financial collateral is an in-strument that can be used only among legal entities, the individuals are excluded, where at least one of the parties in the financial collateral agreement is the Republic of Albania, the Bank of Albania, a foreign central bank, a local bank or financial insti-tution, a foreign bank or financial institution or entity similar to a bank or financial institution, a settlement agent, an operator or another local or international public authority. En-forcement of the financial collateral appears to be easy and does not in-volve courts and/or any other public authority. 2. Security interest over intangible assets Since 1 January 2000, when the Se-curing Charges Law (no. 8537, dated 18.10.1999) entered into force, securi-ty interest in the form of the securing charge over intangible assets (includ-ing without being limited to shares in limited liability companies and/or nominal shares in joint-stock compa-nies, receivables, contractual rights, etc.) was created by written agree-ment of the parties and perfected by registration with the Securing Charg-es Registry without loss of possession of the security interest offeror. After 13 years, starting from 29 May 2013, this type of security over intangible assets is no longer available, because

Practically, the effective perfection and/or enforcement of the pledge, taken under the Civil Code over intangible assets, is very questionable.

The ambiguities in the law and lack of consolidated case law or jurisprudence does not give proper guarantee, that a security interest should give, to the secured party when it comes to taking and enforcing a pledge over intangible assets under the Civil Code.

by &

www.aab.al • BANKIERI • 23

of certain amendments in the Secur-ing Charges Law passed by the Al-banian Parliament (no. 132/2013). According to the amendments, the securing charge cannot be taken over intangible movable properties, secu-rities, instruments and accounts. This amendment does not affect the secu-rity interest that can continue to be taken in the form of securing charge over tangible movable assets. This means that assets, such as shares in limited liability companies, unlim-ited and/or limited liability partner-ships, nominal shares in joint-stock companies, receivables, contractual rights, etc., can no longer be subject of a securing charge.

Actually, the security interest over intangible assets, such as those mentioned above, may, under the provisions of Civil Code, be taken in the form of pledge. The Civil Code (art. 546) defines the pledge as a se-curity interest that can be taken over movable properties or over rights of bearer or over the usufruct of such property or right. The pledge is per-fected by transferring possession of the property or title to the pledgee or to a third party, appointed by agree-ment of the parties. Additionally, according to the second paragraph of art. 143 of the Code, stating that “…the provisions related to movable properties are applicable to all other rights…”, theoretically, it is possible to take a pledge over intangible as-sets. Furthermore, pursuant to art. 547 of the Code, it is possible to take pledge over shares (i.e. in unlimited and/or limited partnerships, limited liability companies, joint-stock com-panies) and perfect it by registration in the book of shareholders.

Practically, the effective perfection and/or enforcement of the pledge taken under the Civil Code over in-tangible assets, including those men-

Insofar as it concerns the pledge over receivables and other contractual rights, the question that arises is how the possession of such rights will be transferred from pledgor to pledgee and in which way third parties will become aware of the existence of such pledge?

tion above, is very questionable in Albania. In case of the pledge over shares in limited liabilities compa-nies, unlimited and/or limited part-nerships, the question that arises is “what is the book of shareholders?” We can presume what it can be, but do not find any definition of such book in the Civil Code and/or in the Law on Entrepreneurs and Compa-nies (law no. 9901, dated 14.04.2008, amended). It is a practice to file and publish the pledge agreement with the National Center of Registration (NCR), but would that constitute perfection of the pledge as required by the Civil Code, or would the com-mercial register kept NCR be consid-ered as the “book of shareholders”? The same question is valid for the pledge over shares in joint stock com-panies. In the Law on Entrepreneurs and Companies that we find the defi-nition of “shares register” rather than “book of shareholders”. Thus, would the shares register defined by Law on Entrepreneurs and Companies be considered the book of shareholders referred to by the Civil Code?

Insofar, as it concerns the pledge over receivables and other contrac-tual rights, the question that arises is how the possession of such rights will be transferred from pledgor to pledgee and in which way third parties will become aware of the ex-istence of such pledge? The answer to this question is the assignment of

rights under the provisions of art. 499 to 507 of the Civil Code, but that is not a common practice, yet. The enforcement of the pledge taken un-der the Civil Code remains unclear. According the Code (art. 556), the pledge is enforced by the sale of the pledged asset, upon authorization of the court. The courts are not required to be involved, only in case of pledge enforcement over receivables and/or contractual rights, according to art. 557. In principle, the court authoriza-tion is a court decision and as such it can be appealed by the pledgor in a superior court (i.e. courts of appeals and Supreme Court). As the practice shows, the appealing process of court decisions is time-consuming and hampers the enforcement process, thus harming the lenders’ interests.

Conclusively, it may be said that ambiguities in the law and lack of consolidated case law or jurispru-dence does not give proper guaran-tee, that a security interest should give to the secured party, when it comes to taking and enforcing a pledge over intangible assets, under the Civil Code.

Such gaps require changes in le-gal framework, either by introducing in the Civil Code a chapter explain-ing how the pledge over intangible assets is perfected and enforced, or reinstate those provisions in the Se-curing Charges Law, that were re-pealed by the latest amendments.

24 • BANKIERI • www.aab.al

www.aab.al • BANKIERI • 25

EXPERTS’ FORUM

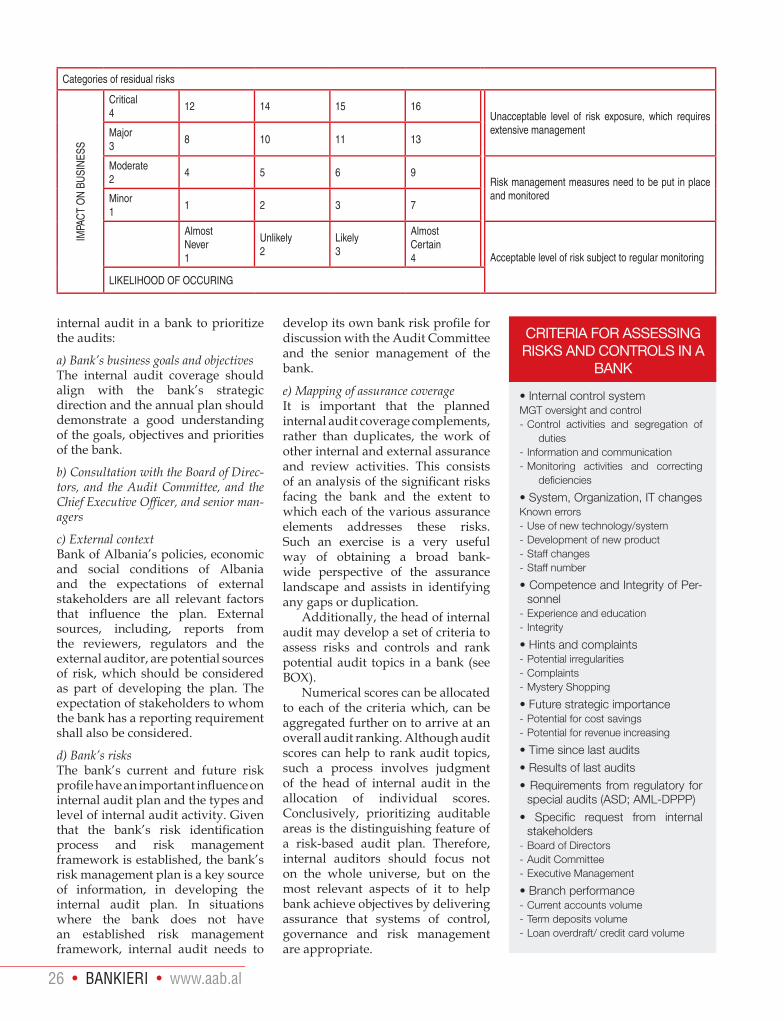

raised is how can we decide where we should focus our attention? So the issue becomes not “what is the size of universe?”, as this is an exhaustive ex-ercised, but rather “what is the extent of the focus for our internal audit plan in strategic and operational terms?”1 .. I offer a view of how a head of internal audit in a bank might advise an audit committee over the components of the internal audit plan.

The head of internal audit should look where the board gets assurance from. This requires an analysis of three lines of defense, in which inher-ent and residual risks are assessed. At this stage we should assume that residual risk is likely to fall into one of three categories:• Red - an unacceptable level of

risks remains, which is above the risk appetite of the board.

• Yellow – the level of risk expo-sure requires constant monitoring by executive management.

• Green – a level of risk that is un-likely to cause business disrup-tion.

Three areas of internal audit activityIn the red area the management

will implement solutions to bring

One of the questions I’m regularly asked in my professional and

academic capacity is how to quantify my organization’s internal audit uni-verse. To this question, my reply is “well it’s good to be an internal auditor rather than a scientist.” Professor Brian Cox writing in the Wall Street Journal in April 2013 explained: “Quantum theory tells us that the universe we expe-rience emerges from a bewildering, coun-terintuitive maelstrom of interactions be-tween infinity of recalcitrant sub-atomic articles.” Believe me, defining the in-ternal audit universe is much simple than that, although the principles may be similar.

The definition of internal au-dit quoted in the International Professional Practices Framework (IPPF) give us a clear steer that “we should be concerned with the organiza-tion’s operation; in other words, every-thing that our organization encompasses and interacts with.” In such terms, the quantification of the scope of opera-tions and their review clearly repre-sent a massive task. Then the question

exposure within the risk appetite of the board. Internal audit activ-ity is likely to be of a consultancy nature.

In the yellow area there is a con-trol risk line where, if key controls fail, the organization would be exposed to unacceptable or even catastrophic risk. This is where internal audit needs to provide assurance-based work as third line of defense.

The green area is likely to feature operational activity. Therefore some compliance audit may be appropriate to reassure the board about the continuity of control and to contribute to overarching opinion relating to control, gover-nance and risk management. The essential aspect of the in-

ternal audit plan is therefore a risk-based analysis, featuring not only the areas of perceived greatest risk, but also key controls within them. Then, it raises the question how to assess areas of greatest risks and controls built to manage the risks? How to define the auditable areas to be rec-ommended to the audit committee for attention? The following factors should be considered by the head of

RISK-BASED INTERNAL AUDIT PLAN IN BANKING SECTOR – SOME KEY CONSIDERATIONS

Internal auditors should focus not on the whole universe, but on the most relevant aspects of it to help bank achieve objectives by delivering assurance that systems of control,

governance and risk management are appropriate.

by Ms Holtjana BELLOPartner/Consultant

Risk & Audit Consulting

1. Pritchard,R.(2013). ” What planet are you on?”, July/ August 2013, p.22

26 • BANKIERI • www.aab.al

internal audit in a bank to prioritize the audits:

a) Bank’s business goals and objectivesThe internal audit coverage should align with the bank’s strategic direction and the annual plan should demonstrate a good understanding of the goals, objectives and priorities of the bank.

b) Consultation with the Board of Direc-tors, and the Audit Committee, and the Chief Executive Officer, and senior man-agers

c) External contextBank of Albania’s policies, economic and social conditions of Albania and the expectations of external stakeholders are all relevant factors that influence the plan. External sources, including, reports from the reviewers, regulators and the external auditor, are potential sources of risk, which should be considered as part of developing the plan. The expectation of stakeholders to whom the bank has a reporting requirement shall also be considered.

d) Bank’s risks The bank’s current and future risk profile have an important influence on internal audit plan and the types and level of internal audit activity. Given that the bank’s risk identification process and risk management framework is established, the bank’s risk management plan is a key source of information, in developing the internal audit plan. In situations where the bank does not have an established risk management framework, internal audit needs to

develop its own bank risk profile for discussion with the Audit Committee and the senior management of the bank.

e) Mapping of assurance coverageIt is important that the planned internal audit coverage complements, rather than duplicates, the work of other internal and external assurance and review activities. This consists of an analysis of the significant risks facing the bank and the extent to which each of the various assurance elements addresses these risks. Such an exercise is a very useful way of obtaining a broad bank-wide perspective of the assurance landscape and assists in identifying any gaps or duplication.

Additionally, the head of internal audit may develop a set of criteria to assess risks and controls and rank potential audit topics in a bank (see BOX).

Numerical scores can be allocated to each of the criteria which, can be aggregated further on to arrive at an overall audit ranking. Although audit scores can help to rank audit topics, such a process involves judgment of the head of internal audit in the allocation of individual scores. Conclusively, prioritizing auditable areas is the distinguishing feature of a risk-based audit plan. Therefore, internal auditors should focus not on the whole universe, but on the most relevant aspects of it to help bank achieve objectives by delivering assurance that systems of control, governance and risk management are appropriate.

• Internal control systemMGT oversight and control- Control activities and segregation of

duties- Information and communication- Monitoring activities and correcting

deficiencies

• System, Organization, IT changesKnown errors- Use of new technology/system- Development of new product- Staff changes- Staff number

• Competence and Integrity of Per-sonnel

- Experience and education- Integrity

• Hints and complaints- Potential irregularities- Complaints- Mystery Shopping

• Future strategic importance- Potential for cost savings- Potential for revenue increasing

• Time since last audits

• Results of last audits

• Requirements from regulatory for special audits (ASD; AML-DPPP)

• Specific request from internal stakeholders

- Board of Directors- Audit Committee- Executive Management

• Branch performance - Current accounts volume- Term deposits volume- Loan overdraft/ credit card volume

CRITERIA FOR ASSESSING RISKS AND CONTROLS IN A

BANK

Categories of residual risksIM

PAC

T O

N B

USI

NES

S

Critical4

12 14 15 16Unacceptable level of risk exposure, which requires extensive managementMajor

38 10 11 13

Moderate2

4 5 6 9Risk management measures need to be put in place and monitoredMinor

11 2 3 7

AlmostNever1

Unlikely2

Likely3

AlmostCertain4 Acceptable level of risk subject to regular monitoring

LIKELIHOOD OF OCCURING

www.aab.al • BANKIERI • 27

MONETARY POLICIES: PRICE STABILITY VERSUS FINANCIAL STABILITY

ECONOMIST CORNER

by Prof.Dr. Adrian CIVICIPresident & Head of Doctoral School

European University of Tirana, EUT – UET

The global financial and economic crisis of 2008-2013, confronted

monetary policy with new challeng-es, regarding their relationships and implications with the overall finan-cial stability and debt and budget deficits management policies, in par-ticular. The most fundamental ques-tion made to monetary policies is whether they should play a more im-portant role in maintaining financial stability, reducing negative effects of sovereign debts and improving the overall economic health, along with their “classic” mandate, in the field of price stability and inflation control? Actually, this is so-much-present the-oretical and academic debate, within scientific environments, central banks and universities, although it hasn’t reach an exhausted and consensus response among experts and scholars of monetary policy. The fact in the spotlight is that, before the financial crisis there did exist an almost ab-solute consensus on tasks and scope of monetary policy, whereas during the post-crisis period links between monetary policy and financial stabil-ity are still in an ongoing study and analysis process.

Debates about monetary policy, during the last 3-4 decades, have

Current global financial crisis brought to the limelight the importance of financial stability and showed clearly

that, the objective of price stability alone is not sufficient to guarantee macroeconomic stability and especially

sovereign debt issues and budget deficits.

been focused on links between infla-tion and economic activity, while the issue of financial stability/instabil-ity is seen as a fairly side objective of it. Experts explain this by the fact that, during the second half of the twentieth century, developed coun-tries’ economies have been never faced with a financial crisis, similar to the last global crisis. Such econo-

mies moved from a period of high inflation and stagflation of 1970s, to a non-inflationary period in 1980s, concluding that “inflation had not pro-duced a sustainable economic growth and any reduction of unemployment, rather it led to a monetary instability, with negative consequences for growth and employment”. Meanwhile, this disinflation produced a reduction in macroeconomic volatility.

Beyond debates over favorable macroeconomic effects of this period, impacting the restructuring of many economies, or the improved man-agement techniques, it seems that there is a broad consensus regarding positive effect, produced by mon-etary policies pursued, during this period. Firstly, long inflation’s long-term evolution was determined by monetary policies, which set “price stability” as their main objective, i.e. inflation stabilization or inflation targeting; secondly, the objective of price stability does not have count-able costs for the economic activity, in a time when monetary policies, aimed at spurring economic growth, at the price of high inflation, had failed. The idea that ensuring price stability was the best contribution, that monetary policy can provide for economic growth and employment had triumphed, while central banks were focused more on flexible infla-tion targeting, rather than adhere to a strict inflation targeting; third, the

Central banks should be more attentive to consider in their decision-making analysis for monetary policy, the elements which cause financial imbalances, as the crisis showed that financial risks are also price stability risks, which implies an expanding horizon for monetary policies and a change in their communication with the general public and economic stakeholders.

28 • BANKIERI • www.aab.al

role inflation anticipation had played in the inflationary process itself, i.e. the positive effect of promises and the trust in central banks, that they would stick hard to the objective of price stability, fourth, the consensus that central banks needed a solid le-gal and institutional framework, ca-pable to reinvigorate the authority and credibility of monetary policy and their focus on the objective of price stability.