Embed Size (px)

Citation preview

8/3/2019 Banking Industry Newsletter

http://slidepdf.com/reader/full/banking-industry-newsletter 1/9

Highlights o recent accounting and regulatory issues December 2011

Banking industry hot topics

This document provides highlights o recent

accounting and regulatory issues rom theFASB, SEC, PCAOB, Federal DepositInsurance Corporation (FDIC), Oce o the Comptroller o the Currency (OCC),and the Board o Governors o the FederalReserve System (FRB). This bulletinsummarizes critical topics, includingthe state o the banking industry, SECreporting issues, bank regulator updates,

FASB developments and PCAOB updates.

A. State o the banking industry

At a recent industry event, ormer Senator Evan Bayh providedan update on the banking industry as it relates to the U.S.

economy. He expects that recovery rom the past three or our

years o economic sluggishness will begin to improve, but it

will not be a speedy recovery. He cited personal consumption,

capital investment, exports and government as the key building

blocks to economic improvement, but noted that these

underlying agents or growth in our economy are going to be

anemic or a long time, ushering in a period o scal austerity.

In Bayh’s opinion, the best way to solve a scal problem is

through rapid growth, which is unlikely to happen in today’s

economy. He noted that slower economic growth and nancial

austerity at the ederal level will lead to increased politicalvolatility, and since each party is at odds with the other, nding

the middle ground, where progress is usually made, is more

dicult. Such intense opposition leads to decision-making

gridlock, and progress is only made when there is a crisis, such

as the debt ceiling or spiking interest rates.

In relation to the banking and nancial services industry,

Bayh pointed out that with a closely divided Congress and the

likelihood that the next presidency could go either way (but

he gives a slight advantage to President Obama), the current

group o regulators will continue to make decisions. For

example, Dodd-Frank will continue to be implemented, and the

Consumer Financial Protection Bureau (CFPB) will continueto operate without a head, which means they will be unable

to promulgate new rules and regulations. More generally,

Bayh expects that in a politically unstable and economically

sluggish environment, nancial institutions — particularly large,

complex ones — will remain scapegoats or angry voters.

Contents

1 A. State o the banking industry2 B. SEC compliance and reporting matters2 Update rom the Ofce o the Chie Accountant2 Avenues or consultation2 Status o consideration o use o IFRS in U.S.

reporting

3 Update rom the Division o Corporation Finance3 Frequent areas o SEC sta comment7 C. PCAOB matters7 Standard-setting agenda8 Inspection fndings or fnancial institutions8 D. Regulatory Chie Accountants Panel

8 E. FASB update9 Major projects9 Troubled debt restructurings

8/3/2019 Banking Industry Newsletter

http://slidepdf.com/reader/full/banking-industry-newsletter 2/9

Despite his gloomy predictions, Bayh ended on an

optimistic note, concluding that, over the past 200 years,

the American people have overcome numerous signicant

challenges not unlike the ones the country must tackle today.

B. SEC compliance and reporting matters

Update rom the Ofce o the Chie Accountant

In his remarks, James Kroeker, SEC Chie Accountant in the

Oce o the Chie Accountant (OCA), spoke o the intent o

the OCA to be proactive in identiying weaknesses in nancialreporting beore they become a crisis. In this vein, in addition to

lling the role o Deputy Chie Accountant or Policy Support

and Market Monitoring in 2010, the OCA is planning the rst

roundtable in its Financial Reporting Series (FRS). The purpose

o this roundtable series, which will include perspectives rom

investors, nancial statement preparers, auditors and others,

is to acilitate a discussion o existing pressures or emerging

issues in nancial reporting. The rst roundtable will ocus

on uncertain measures in nancial reporting and whether the

appropriate level o inormation about uncertainty is being

provided in current disclosures.

Avenues or consultation

Kroeker reminded rms o the various avenues or consulting

with OCA and also other divisions o the SEC, such as the

Division o Corporation Finance (CorpFin). This includes

ormal written submissions, as well as inormal telephone and

“no-name” inquiries. While inormal inquires are accepted, they

cannot be relied on as ormal positions o the SEC sta.

Registrants should expect to be treated proessionally in

the consultation process and have their matters dealt with in

a timely manner, but Kroeker advised registrants to not wait

until the day beore a ling deadline to make their inquiry.Additionally, i a registrant is consulting with other agencies,

such as the FASB, it should advise OCA that such consultations

are underway.

Status o consideration o use o IFRS in U.S. reporting

Kroeker reported on the status o the SEC’s Work Plan

regarding IFRS, including a high-level discussion o the

progress reports and related papers issued throughout 2010 and

2011, the most recent being the May 2011 staff paper, Work

Plan for the Consideration of Incorporating International

Financial Reporting Standards into the Financial Reporting

System for U.S. issuers. This paper was not a proposal, but wasintended to explore a method o bringing IFRS into the U.S.

reporting system that had not been ully vetted. The SEC sta

has received approximately 130 comments in response to the

paper, which expressed a wide array o views. They are now

analyzing those comments to inorm uture recommendations

to the Commission.

While the SEC sta continues the Work Plan, they plan

to issue more progress reports in the near uture. They are

working aggressively to be able to make a recommendation or

the Commission’s consideration in 2011. However, Kroeker did

state that this timing is dependent on FASB and IASB progress.

Banking industry hot topics

The SEC held its inaugural FRS roundtable on “Measurement

Uncertainty in Financial Reporting” on Nov. 8, 2011.

Disclosure consideration or second or junior lien loans

Full details o the SEC Work Plan, as well as status updates, reports and other

developments are available on the SEC’s portal: Spotlight on Work Plan or

Global Accounting Standards.

2

8/3/2019 Banking Industry Newsletter

http://slidepdf.com/reader/full/banking-industry-newsletter 3/9

Update rom the Division o Corporation Finance

Craig Olinger, Deputy Chie Accountant in CorpFin,

discussed recent changes within CorpFin. The most notable

in the banking industry is the creation o the new AD Oce

12 to oversee and review the lings o the 65 largest nancial

institutions, with the largest investment banks coming into this

group in the near uture. Additionally, Olinger discussed recent

stang changes, including the ongoing search or a new chie

accountant or the Division to replace Wayne Carnall.

Frequent areas o SEC sta commentAs an introduction to the topic o requent areas o SEC

sta comment on registrant lings, Olinger noted some best

practices or resolving issues noted in CorpFin review, which

include:

• Assembleathoroughresponse,includingindicationof

where revisions have been or will be made to previously

led documents.

• DonotassumetheSECstaffdisagreeswiththeaccounting

treatment or reporting o the registrant.

• Callforclaricationasneeded.

• Maintaincontemporaneousdocumentationforcomplexor

highly judgmental accounting and reporting matters.

Olinger teed up the discussion o requent areas o comment

across all registrant types. Stephanie Hunsaker, Associate Chie

Accountant in CorpFin, and John Donohue, Proessional

Accounting Fellow in OCA, then elaborated on requent areas

o SEC sta comment specic to the banking industry. Those

areas o requent comment are presented in the ollowing pages.

Asset quality issues

Although not a new ocus area as it relates to nancial

institutions, CorpFin continues to issue a signicant number o

comments related to asset quality matters. Hunsaker ocused

on three broad topics: second lien loans, matters specic to

smaller community banks and modications and troubled debt

restructurings (TDRs).

• Secondorjuniorlienloans

– In situations where second lien loans were not identied

as a separate portolio segment, investors may need more

inormation to understand the allowance methodologyor the second lien loan class. In order to understand

potential exposure in this area, CorpFin is asking

registrants to elaborate on:

•Whatinformationisavailableregardingthe

perorming status o the rst lien.

•Howthatinformation,orlackthereof,isfactored

into the allowance or loan loss.

Banking industry hot topics

Disclosure consideration or second or junior lien loans

Registrants should consider the August 2009 CorpFin “Sample Letter Sent to

Public Companies on MD&A Disclosure Regarding Provisions and Allowances

or Loan Losses,” which includes disclosure issues related to second or juniorlien loans.

– Because trends in rst liens’ delinquency rates dier

rom those o second liens, SEC sta is requesting

expanded disclosure around delinquency trends and

charge-o rates o second liens, which generally have

lower delinquency rates than rst liens, but higher

charge-o rates.

• Smallercommunitybanks

– Trends show that smaller community banks are

continuing to increase allowances or loan loss reserves,

while larger institutions are decreasing reserve levels.

Disclosure is needed to allow investors to understand

the trends and expectations going orward related to the

underlying loans and the allowance or loan losses.

3

8/3/2019 Banking Industry Newsletter

http://slidepdf.com/reader/full/banking-industry-newsletter 4/9

– Requests or expanded inormation regarding appraisals,

including timeliness o appraisals, whether adjustments

are made to appraisals, and what is done at the institution

during interim dates between appraisals. As a related

matter, the SEC sta is asking about related charge-

o policies, including timing o charge-os and how

adjustments to appraisals aect charge-o policies.

– For purchased and credit impaired loans, especially as

they relate to ailed banks, comments are being issued

regarding:

•howtheinitialfairvalueandvariousloanpoolsweredetermined;

•whetherallloanswereaccountedfor,either

directly or indirectly, in accordance with FASB

Accounting Standards Codication® (ASC) 310- 30,

Loans and Debt Securities Acquired with

Deteriorated Credit Quality; and

•ongoingaccountingpolicieswithrespectto

adjustments and expectations o cash fows on

dierent loan pools and related impact on

the FDIC receivable.

• Modicationsandtroubleddebtrestructurings

– Transparent disclosures are critical around the types o modication programs a bank employs.

– Disclosures should be robust regarding those

modication programs that result in TDRs and those

that do not.

Credit loss disclosures

The SEC highlighted areas they have commented on related to a

company’s application o the disclosure requirements resulting

rom FASB Accounting Standards Update (ASU) 2010-20,

Receivables: Disclosures about the Credit Quality of Financing

Receivables and the Allowance for Credit Losses.

• Creditqualityindicators

– SEC sta has noted that the disclosed indicators are

not at the same granular level used internally and should

be expanded accordingly. For example, the SEC sta has

noted that they have questioned whether a disclosure

that only dierentiates between perorming and

nonperorming commercial loans is consistent with

management’s internal practice.

– Enhanced disclosures are needed about how indicators

relate to likelihood o loss.

– Disclosures are not clear i loan-to-values ratios have

been updated, as well as the ongoing monitoring policies

or such ratios.

– Credit quality indicators should be disclosed or

consumer loans.

• Charge-offandnon-accrualpolicies

– Disclosures should be specic to the class level.

– Disclosing that policies are “consistent with bank

regulatory requirements” is not adequate, as a nancial

statement user may not know the explicit regulatory

requirements. Companies should clearly describe theirpolicies so that nancial statement users can compare

them to other institutions.

– In instances where disclosure indicates that loans are

charged o “when management determines the loan

is no longer probable o collection,” the SEC sta has

questioned management’s criteria or determining this

judgmental actor.

– I the period or moving a loan to nonaccrual status

exceeds the period or charging o a loan, comments

have been issued as to the theory around this policy and

whether it is in accordance with U.S. GAAP.

– The sta has also questioned policies about resuminginterest on non-accrual loans once a loan no longer

meets the disclosed nonaccrual threshold (or example,

they have questioned situations in which the disclosed

threshold is 90 days past due and a loan is returned to

nonaccrual status when the loan is 89 days past due)

Banking industry hot topics

ASU 2010-20

Grant Thornton’s New Development Summary “ASU enhances credit quality

disclosures – fnancing receivables and allowance or credit losses,” provides

a summary o the disclosure requirements in ASU 2010-20 that generally

went into eect or public companies in 2010 and are eective or nonpublic

entities in 2011 fnancial statements.

4

8/3/2019 Banking Industry Newsletter

http://slidepdf.com/reader/full/banking-industry-newsletter 5/9

Transfers of non-performing assets

The SEC is seeing creative structures designed to get loans,

especially non-perorming loans, o o the entity’s balance

sheet. Accordingly, CorpFin’s review has ocused on

accounting and disclosure concerns o these transactions.

• Related to accounting guidance, relevant guidance includes

variable interest entity (VIE) guidance in ASC 810-10 in

evaluating entities used to get loans o-balance sheet. I

consolidation o the counterparty (or example, a special

purpose vehicle) is not required, either ASC 860, Transfers and

Servicing, or ASC 360-20, Real Estate Sales, likely applies.• Asitpertainstodisclosures,disclosuresshouldbetailored

to t each transaction. There is no checklist, but disclosures

need to be transparent and complete such that a user o

the nancial statements can understand the impact on key

perormance measures.

Loss contingencies

The SEC understands that litigation is a sensitive matter.

However, this sensitivity does not relieve a registrant rom

its obligations to report loss contingencies under ASC 450,

Loss Contingencies, and litigation matters under Regulation

S-K. Hunsaker reminded the audience o the ollowing

considerations:

• Withrespecttoreasonablypossiblelossorrangeofloss:

– Aggregation o claims is acceptable.

– “With condence or precision” is not a threshold

required by ASC 450.– Avoid surprising investors. The SEC sta becomes

concerned when there are big surprises in registrants’

lings. For example, making a leap rom disclosures

stating a matter is immaterial to a large settlement

in a subsequent period. The closer to settlement, the

more estimable the matter. The evaluation o adequacy

o disclosure should be continuous and updated as acts

become known.

– Consideration should also be given to mortgage

repurchase litigation matters and potential exposure in

that area.

• Forlosscontingencydisclosures,registrantsshouldusewords in the accounting standard in its disclosures to reduce

instances o unclear language.

• Third-partyrecoveries(suchasinsurancerecoveries)should

be a separate asset on the balance sheet.

Sovereign debt exposures

With respect to sovereign debt, particularly exposure related to

European sovereign debt, Donohue mentioned the various areas

where disclosure or such exposures is required:

• GuideIIIrequirementtodiscussforeignriskexposure.

• ASC320-10-50-1providesguidanceonsecuritytypesfor

nancial statement disclosure.

• Disclosuresshouldbegrossexposuresandnotnetofother

potential recoveries.

On the topic o the U.S. debt downgrade, the SEC has not

taken a position as to specic application o U.S. GAAP or any

impairment required or registrants holding U.S. government

obligations.

Banking industry hot topics

Disclosure consideration or second or junior lien loans

Grant Thornton has issued the ollowing publications on Variable Interest

Entities and Transers and Servicing.

• Variable interest entity analysis – ASC 810, Consolidation, as amended

by ASU 2009-17

• Transers o fnancial assets – Implementation guidance on ASC 860, as

amended by Statement 166

Transfers to and from held-to-maturity portfolios

Mainly as it relates to debt securities, the SEC sta has noted

registrants transerring some securities into or out o the held-

to-maturity portolio. In this regard, Donohue stated that ASC

320-10-25, Investments-Debt and Equity Securities, sets a high

threshold or not tainting the remaining portolio. Accordingly,

the SEC sta takes a very rigorous approach to evaluating

the accounting in this situation. I considering transerring

securities out o the held-to-maturity portolio, consider:

• ConsultationwithOCAishighlyrecommended.• InadditiontothedisclosuresinASC320-10-50,discuss

in the ling the circumstances that changed management’s

intent with respect to the transerred securities and why that

does not taint the remaining portolio, including reerences

to relevant accounting guidance ollowed.

5

8/3/2019 Banking Industry Newsletter

http://slidepdf.com/reader/full/banking-industry-newsletter 6/9

Non-GAAP measures

The SEC issued Compliance & Disclosure Interpretations on

this topic in January 2010, in an attempt to clariy guidance so

that management could discuss their business in the same way

that they manage it. However, this does not permit use o non-

GAAP disclosures that are misleading. Misleading disclosures

should not be used in any SEC ling, in a registrant’s earnings

releases or calls, or on its website. A ew reminders were given

with respect to common comments on non-GAAP measures:

• Anon-GAAPmeasurecontinuestobe“non-GAAP”even

i calculated based on numbers on the ace o the incomestatement.

• Pre-taxpre-provisionnetprot(PPNP)iscommonlyused

in the banking industry, but must be properly labeled as

non-GAAP. Additionally, registrants should not reer to a

variationofthePPNPcalculationas“core”PPNP.

• WithrespecttoBaselIIIcapitalratios,sincetheyarenotyet

required by regulations, they are non-GAAP measures and

should be properly disclosed and reconciled as such.

Goodwill impairment

With the issuance o the revised goodwill standard (ASU 2011-

08, Testing Goodwill for Impairment), the SEC sta expects tosee the ollowing changes in registrant disclosures:

• Updatedpolicydisclosures.

• MD&Ashoulddiscloseifqualitativescreenisfailedandthe

results o the subsequent quantitative test.

Mortgage servicing rights

In cases where a registrant has disclosed a wide range o

assumptions used in determining the value o mortgage

servicing rights, CorpFin sta have requested more granular

disclosures by loan type or interest rate.

Fair value measurements and third-party pricing services

While raised in the context o PCAOB standard-setting

projects, Kroeker did note that in addition to audit work around

third-party pricing services, the SEC itsel is also examining

registrants’ practices as they relate to use o third-parties intheir evaluation o air value measurements, particularly Level

2 measurements. Kroeker emphasized that while management

may certainly utilize the work o a third-party pricing service in

its valuation eorts, the ultimate responsibility or complying

with U.S. GAAP and maintaining and assessing internal control

over nancial reporting rests with management. Thereore,

management must understand the valuation models, inputs and

assumptions the third party is using in order to be responsible

or the company’s books and records and internal controls.

Kroeker was clear that an understanding o the underlying

inormation used by the third-party pricing service is critical to

providing appropriate disclosure in the nancial statements, aswell as in management’s discussion and analysis (MD&A).

Banking industry hot topics

Additional guidance

Grant Thornton has issued a New Development Summary on ASU 2011-08:

“Qualitative goodwill assessment option — FASB issues new guidance to

simpliy goodwill impairment testing”

SEC Regulations Committee

This issue was also discussed at the Sept. 27, 2011, joint meeting o The

Center or Audit Quality (CAQ) SEC Regulations Committee and the SEC sta.

The CAQ has published highlights o that meeting.

6

8/3/2019 Banking Industry Newsletter

http://slidepdf.com/reader/full/banking-industry-newsletter 7/9

Other planned rulemaking activity

Below is a summary o the PCAOB’s standard-setting agenda.

C. PCAOB matters

Standard-setting agenda

Kroeker discussed the PCAOB standard-setting agenda. He

emphasized that this activity not only impacts auditors but

also registrants. In many cases, the proposed or contemplated

rulemaking does not consist o details o how to do an audit,

but rather standards that are responsive to investors’ desire or

more inormation about public company audits, particularly

coming out o the nancial crisis. Kroeker highlighted the

ollowing topics.

Concept Release on Possible Revisions to PCAOB Standards

Related to Reports on Audited Financial Statements and

Related Amendments to PCAOB Standards

Released in June 2011, this Concept Release explores the

ollowing changes related to auditors’ reporting whether:

• thereshouldbeaseparateauditordiscussionandanalysis

(AD&A) to accompany audit reports and whether

• auditorsshouldhavearoleauditingmanagement’s

disclosures contained in MD&A.

The comment period or this concept release closedSept. 30, 2011.

Concept Release on Auditor Independence and Audit Firm

Rotation

Released in August 2011, this Concept Release explores whether

audit rm objectivity and independence would be strengthened

by certain changes, including “term limits” on the auditor-client

relationship.

Comments on the Concept Release are due Dec. 14, 2011.

Audit transparency

Released in July 2009, the Concept Release, Requiring the

Engagement Partner to Sign the Audit Report explored whether

audit partners should be specically identied in audit reports,

in addition to the audit rm. Additionally, it considered how

multinational audits are conducted and whether other rms that

have a role in an audit should be identied.

Banking industry hot topics

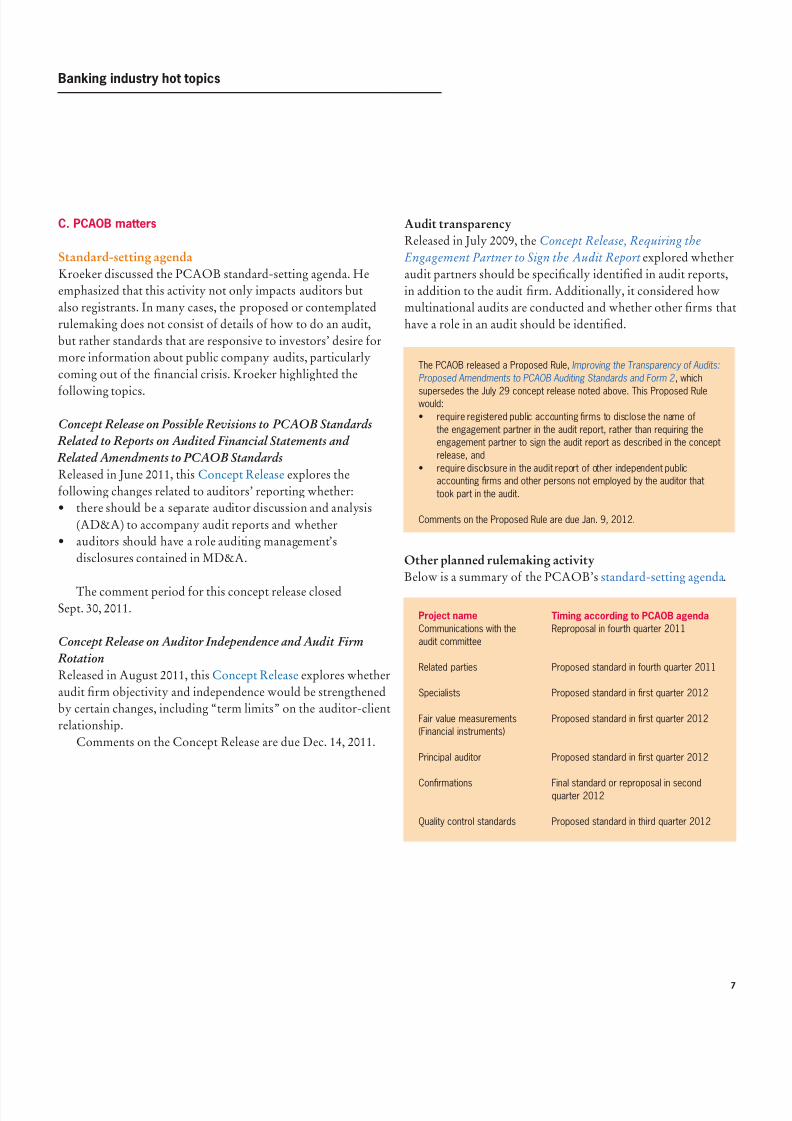

The PCAOB released a Proposed Rule, Improving the Transparency of Audits:

Proposed Amendments to PCAOB Auditing Standards and Form 2 , which

supersedes the July 29 concept release noted above. This Proposed Rulewould:

• requireregisteredpublicaccountingrmstodisclosethenameof

the engagement partner in the audit report, rather than requiring the

engagement partner to sign the audit report as described in the concept

release, and

• requiredisclosureintheauditreportofotherindependentpublic

accounting frms and other persons not employed by the auditor that

took part in the audit.

Comments on the Proposed Rule are due Jan. 9, 2012.

Project name

Communications with the

audit committee

Related parties

Specialists

Fair value measurements

(Financial instruments)

Principal auditor

Confrmations

Quality control standards

Timing according to PCAOB agenda

Reproposal in ourth quarter 2011

Proposed standard in ourth quarter 2011

Proposed standard in frst quarter 2012

Proposed standard in frst quarter 2012

Proposed standard in frst quarter 2012

Final standard or reproposal in secondquarter 2012

Proposed standard in third quarter 2012

7

8/3/2019 Banking Industry Newsletter

http://slidepdf.com/reader/full/banking-industry-newsletter 8/9

Inspection fndings or fnancial institutions

George Wilert, Deputy Director in the PCAOB’s Oce o

Research and Analysis, and Glenn Tempro, Associate Director

in the PCAOB’s Division o Registration and Inspections,

presented common inspection ndings as they relate to audits

o banks and savings institutions. First, they highlighted overall

inspection observations contained in the Report on Observations

of PCAOB Inspectors Related to Audit Risk Areas Affected by

the Economic Crisis, published in September 2010. Then, they

presented more granular ndings as they relate to nancial

institutions, ocusing on the ollowing recurring themes:• auditingfairvaluemeasurements,

• litigationandothercontingenciesarisingfrommortgageand

other loan activities, and

• auditingtheallowanceforloanloss.

D. Regulatory Chie Accountants Panel

Robert Storch, FDIC Chie Accountant, Steven Merriett,

FRB Assistant Director and Chie Accountant-Supervision,

and Kathy Murphy, OCC Chie Accountant, presented on a

recent Regulatory Chie Accountants Panel. Murphy began

by discussing the topics on which the OCC receives the most

questions, which include allowance or loan losses. She notedthat overall, the credit quality indicators are stabilizing and

improving, particularly or large corporate and credit card

portolios; however, there is still a signicant amount o risk with

certain portolios, such as commercial and residential real estate.

Another common topic is troubled debt restructuring.

Murphy does not expect that there will be signicant

changes as a result o ASU 2011-02, Receivables: A Creditor’s

Determination of Whether a Restructuring Is a Troubled

Debt Restructuring, and believes that the clarications are

consistent with previous interagency guidance. As a result o

the new guidance, she indicated that the OCC expects nancial

institutions to update their TDR policies and include additional

analysis and documentation, particularly as it relates to

insignicant delays.

Murphy also touched upon published data and uses or

nancial statements, saying since there are so many areas where

judgment and estimates are required, the more data a bank has,

the more helpul it can be or nancial statement purposes.

A list o helpul data is available at the OCC’s website.

E. FASB update

Major projects

Larry Smith, FASB board member, gave an update on the joint

FASB-IASB and FASB-only projects that are in process. Smith

spent most o his time on the nancial instruments project

and leasing, but he also covered consolidations and revenue

recognition. For the most up-to-date status o these projects,

reer to the inormation on the FASB Technical Plan and

Project Updates page. O note, Smith indicated the ollowing:

• TheFASBplanstore-exposetheproposedleasingandrevenue recognition standards. The FASB has not yet

discussed whether it will re-expose any components o the

nancial instruments project.

• BothBoardsarecurrentlyworkingonarevisedimpairment

model. The current thinking is to create a model based on

expected credit losses. The model would group loans into

three buckets that would capture the deterioration o credit

quality in the loan portolio.

• TheFASBplanstonishitsdeliberationsonclassication

and measurement and jointly discuss with the IASB the

dierences in the FASB model and IFRS 9, Financial

Instruments (IFRS 9 is a nal standard issued by the IASBon classication and measurement). Under the FASB’s

current thinking, loans and deposits will generally be at

amortized cost, debt securities will be at air value with

changesinfairvaluerecognizedinnetincome(FVNI)or

air value with changes in air value recognized in other

comprehensive income (FVOCI), and equity securities will

generallybeatFVNI.

• TheIASBhascompleteditsredeliberationsonhedging,

however the FASB does not expect to redeliberate hedging

until the Boards discuss their dierences in classication and

measurement.

Banking industry hot topics

8

8/3/2019 Banking Industry Newsletter

http://slidepdf.com/reader/full/banking-industry-newsletter 9/9

Troubled debt restructurings

In the question and answer session, Smith claried the eective

date o the new disclosures (rom ASU 2010-20, Disclosures

about the Credit Quality of Financing Receivables and the

Allowance for Credit Losses) about troubled debt restructurings

in ASC 310-10-50-31 through 50-35. In the Codication,

the transition or those disclosures currently reerences the

transition and eective date related to ASU 2011-02, thereore

some have interpreted that those disclosures are not eective

or nonpublic entities until 2012. He claried that the FASB

did not intend to change the eective date o those disclosuresor nonpublic entities and that the eective date or nonpublic

entities should thereore be the rst annual reporting period

ending on or ater Dec. 15, 2011, (Dec. 31, 2011, or calendar

year-end entities). This is consistent with the transition

guidance in ASU 2010-20. The FASB sta is reportedly

working to clariy this inconsistency.

Banking industry hot topics

For more inormation

For more inormation about the topics

covered in this document, contact:

Jack Katz

National Managing Partner, Financial Services

Grant Thornton LLP

T 212.542.9660

Nichole Jordan

National Banking and Securities Leader

Grant Thornton LLP

T 212.624.5310

Visit www.GrantThornton.com/

fnancialservices.

© Grant Thornton LLP

All rights reserved

U.S. member frm o

Grant Thornton International Ltd

This Grant Thornton LLP bulletin provides inormation and comments on current accounting

issues and developments. It is not a comprehensive analysis o the subject matter covered

and is not intended to provide accounting or other advice or guidance with respect to the

matters addressed in the bulletin. All relevant acts and circumstances, including the pertinent

authoritative literature, need to be considered to arrive at conclusions that comply with matters

addressed in this bulletin.

For additional inormation on topics covered in this bulletin, contact your Grant Thornton LLP adviser.

9