Embed Size (px)

Citation preview

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 1/59

MINOR PROJECTON

COMPARISON BETWEEN THE SERVICES PROVIDED BYVARIOUS BANKS

Submitted in partial fulfillment of requirement of BBA (Bachelor of Business Administration),

SUBMITTED TO: SUBMITTED BY:Ms. vaishali ManojProject Guide BBA 5th sem

Roll No: 9208970029

Session 2009-2012

1

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 2/59

ACKNOWLEDGEMENT

I am honored to express my gratitude to all the people who were

always a great help to me in achieving this milestone. I could never

complete this task without valuable contributions from my teachers

and faculty. I express my heart full indebt ness and owe a deep

sense of gratitude to all of them including my guide Mrs. Vaishali

I am extremely thankful to all my friends without whom it was never

possible to complete this project.

MANOJBBA-5th sem

2

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 3/59

TABLE OF CONTENTS

CHAPTER 1: INTRODUCTION

1. Executive summary2. Overview of banking3. Banking in India4. Bank profile

• ICICI

• SBI

CHAPTER 2: RESEARCH METHODOLOGY1. Research objective2. Data analysis3. Sampling design4. Limitation of the study

CHAPTER 3: DATA ANAYSIS AND INTERPRETATION

CHAPTER 4: RECOMMENTATIONS AND CONCULSION

CHAPTER 5: BIBLIOGRAPHY

3

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 4/59

QUESTIONNARIE

INTRODUCTION

EXECUTIVE SUMMARY

The banking sector in India has made remarkable progress since the economic

reforms in 1991. New private sector banks have brought the necessary

competition into the industry and spearheaded the changes towards higher

utilization of technology, improved customer service and innovative products.

Customers are now becoming increasingly conscious of their rights and aredemanding more than ever before. The recent trends show that most banks are

shifting from a “product-centric model” to a “customer-centric model” as customer

satisfaction has become one of the major determinants of business growth. In

this context, prioritization of preferences and close monitoring of customer

satisfaction have become essential for banks. Keeping these in mind, an attempt

has been made in this study to compare the services provided by various banks.

To be precious and for easy comparison the basis of comparison is services

provided by public bank vs. services provided by private bank. In this report the

public bank is State Bank of India and the private bank is ICICI Bank. This project

help in anaylsising the reasons and conclusion that customer prefer which bank

among the two i.e. private bank or public bank.

4

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 5/59

BANKS

A bank is a financial intermediary that accepts deposits and channels those

deposits into lending activities, either directly or through capital markets. A bank

connects customers with capital deficits to customers with capital surpluses.

Banking is generally a highly regulated industry, and government restrictions on

financial activities by banks have varied over time and location. The current set of

global bank capital standards is called Basel II.

The oldest bank still in existence is Monte dei Paschi di Siena, headquartered in

Siena, Italy, which has been operating continuously since 1472.

History

The word bank was borrowed in Middle English from Middle French banque,

from Old Italian banca, from Old High German banc, bank "bench, counter".

Benches were used as desks or exchange counters during the Renaissance by

Florentine bankers, who used to make their transactions atop desks covered by

green tablecloths.

Banking in the modern sense of the word can be traced to medieval and early

Renaissance Italy, to the rich cities in the north like Florence, Venice and Genoa.

The Bardi and Peruzzi families dominated banking in 14th century Florence,

establishing branches in many other parts of Europe. Perhaps the most famous

Italian bank was the Medici bank, set up by Giovanni Medici in 1397. The earliest

known state deposit bank, Banco di San Giorgio (Bank of St. George), was

founded in 1407 at Genoa, Italy.

Banks can be traced back to ancient times even before money when temples were used to store commodities. During the 3rd century AD, banks in Persia and

other territories in the Persian Sassanid Empire issued letters of credit known as

Ṣakks Muslim traders are known to have used the cheque or ṣakk system since

the time of Harun al-Rashid (9th century) of the Abbasid Caliphate. In the 9th

century, a Muslim businessman could cash an early form of the cheque in China

5

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 6/59

drawn on sources in Baghdad, a tradition that was significantly strengthened in

the 13th and 14th centuries, during the Mongol Empire. Fragments found in the

Cairo Geniza indicate that in the 12th century cheque remarkably similar to our

own were in use, only smaller to save costs on the paper. They contain a sum to

be paid and then the order "May so and so pay the bearer such and such an

amount". The date and name of the issuer are also apparent.

Banking

Banks act as payment agents by conducting checking or current accounts for

customers, paying cheque drawn by customers on the bank, and collecting

cheque deposited to customers' current accounts. Banks also enable customer

payments via other payment methods such as telegraphic transfer , EFTPOS,

and ATM.

Banks borrow money by accepting funds deposited on current accounts, by

accepting term deposits, and by issuing debt securities such as banknotes and

bonds. Banks lend money by making advances to customers on current

accounts, by making installment loans, and by investing in marketable debt

securities and other forms of money lending.

Banks provide almost all payment services, and a bank account is considered

indispensable by most businesses, individuals and governments. Non-banks that

provide payment services such as remittance companies are not normally

considered an adequate substitute for having a bank account.

Banks borrow most funds from households and non-financial businesses, and

lend most funds to households and non-financial businesses, but non-bank

lenders provide a significant and in many cases adequate substitute for bankloans, and money market funds, cash management trusts and other non-bank

financial institutions in many cases provide an adequate substitute to banks for

lending savings to.

6

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 7/59

Channels

Banks offer many different channels to access their banking and other services:

• ATM is a machine that dispenses cash and sometimes takes deposits

without the need for a human bank teller . Some ATMs provide additional

services.

• A branch is a retail location

• Call center

• Mail: most banks accept check deposits via mail and use mail to

communicate to their customers, e.g. by sending out statements

• Mobile banking is a method of using one's mobile phone to conductbanking transactions

• Online banking is a term used for performing transactions, payments etc.

over the Internet

• Relationship Managers, mostly for private banking or business banking,

often visiting customers at their homes or businesses

• Telephone banking is a service which allows its customers to perform

transactions over the telephone without speaking to a human

• Video banking is a term used for performing banking transactions or

professional banking consultations via a remote video and audio

connection. Video banking can be performed via purpose built banking

transaction machines (similar to an Automated teller machine), or via a

videoconference enabled bank branch.

Products

Retail

• Business loan

• Cheque account

• Credit card

7

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 8/59

• Home loan

• Insurance advisor

• Mutual fund

• Personal loan

• Savings account

Wholesale

• Capital raising (Equity / Debt / Hybrids)

• Mezzanine finance

• Project finance

• Revolving credit

• Risk management (FX, interest rates, commodities, derivatives)

Types of Banks

Banks' activities can be divided into retail banking, dealing directly with

individuals and small businesses; business banking, providing services to mid-

market business; corporate banking, directed at large business entities; private

banking, providing wealth management services to high net worth individuals and

families; and investment banking, relating to activities on the financial markets.

Most banks are profit-making, private enterprises. However, some are owned by

government, or are non-profit organizations.

Types of Retail Banks

• Commercial bank: the term used for a normal bank to distinguish it from

an investment bank. After the Great Depression, the U.S. Congress

required that banks only engage in banking activities, whereas investment

banks were limited to capital market activities. Since the two no longer

have to be under separate ownership, some use the term "commercial

bank" to refer to a bank or a division of a bank that mostly deals with

deposits and loans from corporations or large businesses.

8

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 9/59

• Community banks: locally operated financial institutions that empower

employees to make local decisions to serve their customers and the

partners.

• Community development banks: regulated banks that provide financial

services and credit to under-served markets or populations.

• Postal savings banks: savings banks associated with national postal

systems.

• Private Banks: banks that manage the assets of high net worth individuals.

Historically a minimum of USD 1 million was required to open an account;

however, over the last years many private banks have lowered their entry

hurdles to USD 250,000 for private investors.

• Offshore banks: banks located in jurisdictions with low taxation and

regulation. Many offshore banks are essentially private banks.• Savings bank: in Europe, savings banks take their roots in the 19th or

sometimes even 18th century. Their original objective was to provide

easily accessible savings products to all strata of the population. In some

countries, savings banks were created on public initiative; in others,

socially committed individuals created foundations to put in place the

necessary infrastructure. Nowadays, European savings banks have kept

their focus on retail banking: payments, savings products, credits and

insurances for individuals or small and medium-sized enterprises. Apart

from this retail focus, they also differ from commercial banks by their

broadly decentralized distribution network, providing local and regional

outreach—and by their socially responsible approach to business and

society.

• Building societies and Landesbanks: institutions that conduct retail

banking.

• Ethical banks: banks that prioritize the transparency of all operations and

make only what they consider to be socially-responsible investments.

• A Direct or Internet-Only bank is a banking operation without any physical

bank branches, conceived and implemented wholly with networked

computers.

9

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 10/59

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 11/59

Unlike most other regulated industries, the regulator is typically also a participant

in the market, i.e. a government-owned (central) bank. Central banks also

typically have a monopoly on the business of issuing banknotes. However, in

some countries this is not the case. In the UK, for example, the Financial

Services Authority licenses banks, and some commercial banks (such as the

Bank of Scotland) issue their own banknotes in addition to those issued by the

Bank of England, the UK government's central bank.

Banking law is based on a contractual analysis of the relationship between the

bank (defined above) and the customer —defined as any entity for which the bank

agrees to conduct an account.

The law implies rights and obligations into this relationship as follows:

1. The bank account balance is the financial position between the bank and

the customer: when the account is in credit, the bank owes the balance to

the customer; when the account is overdrawn, the customer owes the

balance to the bank.

2. The bank agrees to pay the customer's cheque up to the amount standing

to the credit of the customer's account, plus any agreed overdraft limit.

3. The bank may not pay from the customer's account without a mandate

from the customer, e.g. a cheque drawn by the customer.

4. The bank agrees to promptly collect the cheque deposited to the

customer's account as the customer's agent, and to credit the proceeds to

the customer's account.

5. The bank has a right to combine the customer's accounts, since each

account is just an aspect of the same credit relationship.

6. The bank has a lien on cheque deposited to the customer's account, to the

extent that the customer is indebted to the bank.

7. The bank must not disclose details of transactions through the customer's

account—unless the customer consents, there is a public duty to disclose,

the bank's interests require it, or the law demands it.

11

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 12/59

8. The bank must not close a customer's account without reasonable notice,

since cheque is outstanding in the ordinary course of business for several

days.

These implied contractual terms may be modified by express agreement

between the customer and the bank. The statutes and regulations in force withina particular jurisdiction may also modify the above terms and/or create new

rights, obligations or limitations relevant to the bank-customer relationship.

Some types of financial institution, such as building societies and credit unions,

may be partly or wholly exempt from bank license requirements, and therefore

regulated under separate rules.

The requirements for the issue of a bank license vary between jurisdictions buttypically include:

1. Minimum capital

2. Minimum capital ratio

3. 'Fit and Proper' requirements for the bank's controllers, owners, directors,

and/or senior officers

Approval of the bank's business plan as being sufficiently prudent and plausible.

Size of global banking industry

Assets of the largest 1,000 banks in the world grew by 6.8% in the 2008/2009

financial year to a record $96.4 trillion while profits declined by 85% to $115bn.

Growth in assets in adverse market conditions was largely a result of

recapitalisation. EU banks held the largest share of the total, 56% in 2008/2009,

down from 61% in the previous year. Asian banks' share increased from 12% to

14% during the year, while the share of US banks increased from 11% to 13%.

Fee revenue generated by global investment banking totaled $66.3bn in 2009, up

12% on the previous year.

12

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 13/59

The United States has the most banks in the world in terms of institutions (7,085

at the end of 2008) and possibly branches (82,000).This is an indicator of the

geography and regulatory structure of the USA, resulting in a large number of

small to medium-sized institutions in its banking system. As of Nov 2009, China's

top 4 banks have in excess of 67,000 branches (ICBC: 18000+, BOC: 12000+,

CCB: 13000+, ABC: 24000+) with an additional 140 smaller banks with an

undetermined number of branches. Japan had 129 banks and 12,000 branches.

In 2004, Germany, France, and Italy each had more than 30,000 branches—

more than double the 15,000 branches in the UK.

Banks in the economy

Economic functions

The economic functions of banks include:

1. Issue of money, in the form of banknotes and current accounts subject to

cheque or payment at the customer's order. These claims on banks canact as money because they are negotiable and/or repayable on demand,

and hence valued at par. They are effectively transferable by mere

delivery, in the case of banknotes, or by drawing a cheque that the payee

may bank or cash.

2. Netting and settlement of payments – banks act as both collection and

paying agents for customers, participating in interbank clearing and

settlement systems to collect, present, be presented with, and pay

payment instruments. This enables banks to economies on reserves held

for settlement of payments, since inward and outward payments offset

each other. It also enables the offsetting of payment flows between

geographical areas, reducing the cost of settlement between them.

13

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 14/59

3. Credit intermediation – banks borrow and lend back-to-back on their own

account as middle men.

4. Credit quality improvement – banks lend money to ordinary commercial

and personal borrowers (ordinary credit quality), but are high quality

borrowers. The improvement comes from diversification of the bank's

assets and capital which provides a buffer to absorb losses without

defaulting on its obligations. However, banknotes and deposits are

generally unsecured; if the bank gets into difficulty and pledges assets as

security, to rise the funding it needs to continue to operate, this puts the

note holders and depositors in an economically subordinated position.

5. Maturity transformation – banks borrow more on demand debt and short

term debt, but provide more long term loans. In other words, they borrow

short and lend long. With a stronger credit quality than most other borrowers, banks can do this by aggregating issues (e.g. accepting

deposits and issuing banknotes) and redemptions (e.g. withdrawals and

redemptions of banknotes), maintaining reserves of cash, investing in

marketable securities that can be readily converted to cash if needed, and

raising replacement funding as needed from various sources (e.g.

wholesale cash markets and securities markets).

Bank crisis

Banks are susceptible to many forms of risk which have triggered occasional

systemic crises. These include liquidity risk (where many depositors may request

withdrawals in excess of available funds), credit risk (the chance that those who

owe money to the bank will not repay it), and interest rate risk (the possibility that

the bank will become unprofitable, if rising interest rates force it to pay relatively

more on its deposits than it receives on its loans).

Banking crises have developed many times throughout history, when one or

more risks have materialized for a banking sector as a whole. Prominent

examples include the bank run that occurred during the Great Depression, the

14

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 15/59

U.S. Savings and Loan crisis in the 1980s and early 1990s, the Japanese

banking crisis during the 1990s, and the sub prime mortgage crisis in the 2000s.

Risk and capital

Banks face a number of risks in order to conduct their business, and how well

these risks are managed and understood is a key driver behind profitability, and

how much capital a bank is required to hold. Some of the main risks faced by

banks include:

• Credit risk: risk of loss arising from a borrower who does not make

payments as promised.

• Liquidity risk: risk that a given security or asset cannot be traded quickly

enough in the market to prevent a loss (or make the required profit).• Market risk: risk that the value of a portfolio, either an investment portfolio

or a trading portfolio, will decrease due to the change in value of the

market risk factors.

• Operational risk: risk arising from execution of a company's business

functions.

The capital requirement is a bank regulation, which sets a framework on how

banks and depository institutions must handle their capital. The categorization of

assets and capital is highly standardized so that it can be risk weighted (see risk-

weighted asset).

15

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 16/59

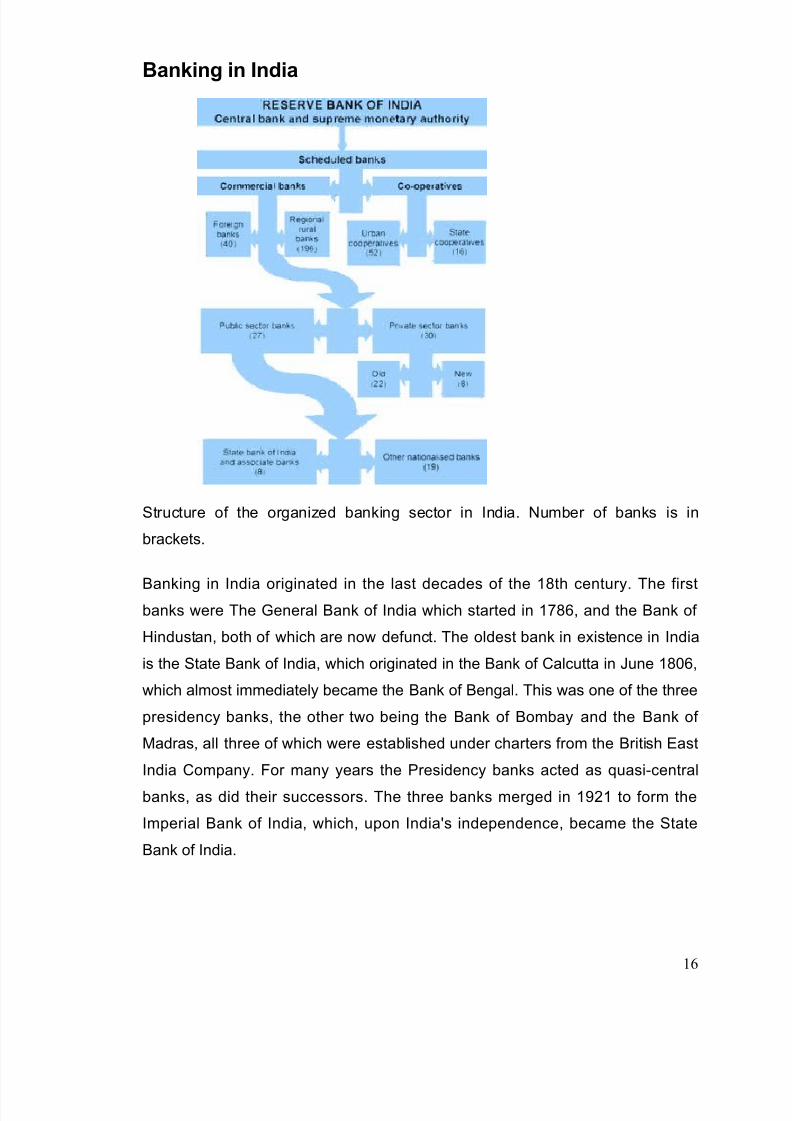

Banking in India

Structure of the organized banking sector in India. Number of banks is in

brackets.

Banking in India originated in the last decades of the 18th century. The firstbanks were The General Bank of India which started in 1786, and the Bank of

Hindustan, both of which are now defunct. The oldest bank in existence in India

is the State Bank of India, which originated in the Bank of Calcutta in June 1806,

which almost immediately became the Bank of Bengal. This was one of the three

presidency banks, the other two being the Bank of Bombay and the Bank of

Madras, all three of which were established under charters from the British East

India Company. For many years the Presidency banks acted as quasi-central

banks, as did their successors. The three banks merged in 1921 to form the

Imperial Bank of India, which, upon India's independence, became the State

Bank of India.

16

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 17/59

Indian merchants in Calcutta established the Union Bank in 1839, but it failed in

1848 as a consequence of the economic crisis of 1848-49. The Allahabad Bank,

established in 1865 and still functioning today, is the oldest Joint Stock bank in

India.(Joint Stock Bank: A company that issues stock and requires shareholders

to be held liable for the company's debt) It was not the first though. That honor

belongs to the Bank of Upper India, which was established in 1863, and which

survived until 1913, when it failed, with some of its assets and liabilities being

transferred to the Alliance Bank of Shimla.

When the American Civil War stopped the supply of cotton to Lancashire from

the Confederate States, promoters opened banks to finance trading in Indian

cotton. With large exposure to speculative ventures, most of the banks opened in

India during that period failed. The depositors lost money and lost interest in

keeping deposits with banks. Subsequently, banking in India remained the

exclusive domain of Europeans for next several decades until the beginning of

the 20th century.

Foreign banks too started to arrive, particularly in Calcutta, in the 1860s. The

Comptoire d'Escompte de Paris opened a branch in Calcutta in 1860, and

another in Bombay in 1862; branches in Madras and Puducherry, then a French

colony, followed. HSBC established itself in Bengal in 1869. Calcutta was themost active trading port in India, mainly due to the trade of the British Empire,

and so became a banking center.

The Bank of Bengal, which later merged with the Bank of Bombay and the Bank

of Madras to form the Imperial Bank of India in 1921.

The first entirely Indian joint stock bank was the Oudh Commercial Bank,

established in 1881 in Faizabad. It failed in 1958. The next was the Punjab National Bank, established in Lahore in 1895, which has survived to the present

and is now one of the largest banks in India.

Around the turn of the 20th Century, the Indian economy was passing through a

relative period of stability. Around five decades had elapsed since the Indian

17

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 18/59

Mutiny, and the social, industrial and other infrastructure had improved. Indians

had established small banks, most of which served particular ethnic and religious

communities.

The presidency banks dominated banking in India but there were also some

exchange banks and a number of Indian joint stock banks. All these banksoperated in different segments of the economy. The exchange banks, mostly

owned by Europeans, concentrated on financing foreign trade. Indian joint stock

banks were generally under capitalized and lacked the experience and maturity

to compete with the presidency and exchange banks. This segmentation let Lord

Curzon to observe, "In respect of banking it seems we are behind the times. We

are like some old fashioned sailing ship, divided by solid wooden bulkheads into

separate and cumbersome compartments."

The period between 1906 and 1911, saw the establishment of banks inspired by

the Swadeshi movement. The Swadeshi movement inspired local businessmen

and political figures to found banks of and for the Indian community. A number of

banks established then have survived to the present such as Bank of India,

Corporation Bank, Indian Bank, Bank of Baroda, Canara Bank and Central Bank

of India.

The fervour of Swadeshi movement lead to establishing of many private banks in

Dakshina Kannada and Udupi district which were unified earlier and known by

the name South Canara ( South Kanara ) district. Four nationalized banks started

in this district and also a leading private sector bank. Hence undivided Dakshina

Kannada district is known as "Cradle of Indian Banking".

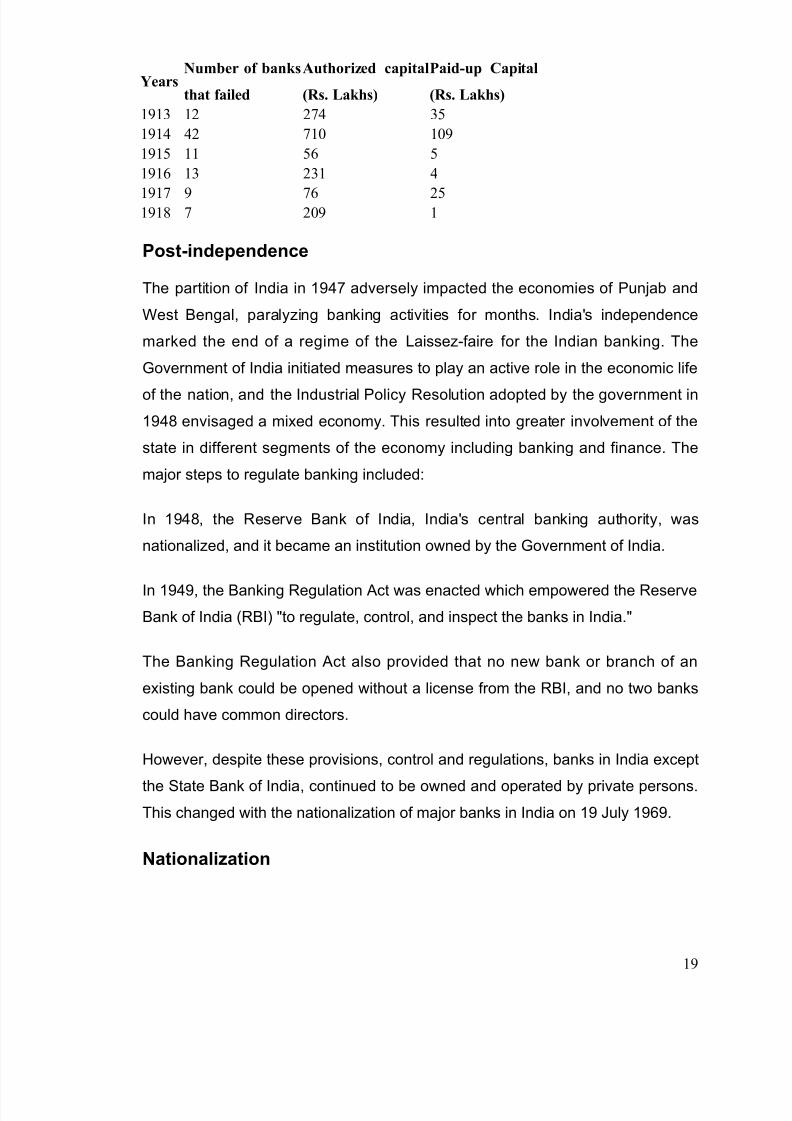

During the First World War (1914-1918) through the end of the Second World

War (1939-1945), and two years thereafter until the independence of India werechallenging for Indian banking. The years of the First World War were turbulent,

and it took its toll with banks simply collapsing despite the Indian economy

gaining indirect boost due to war-related economic activities. At least 94 banks in

India failed between 1913 and 1918 as indicated in the following table:

18

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 19/59

YearsNumber of banks

that failed

Authorized capital

(Rs. Lakhs)

Paid-up Capital

(Rs. Lakhs)

1913 12 274 35

1914 42 710 109

1915 11 56 5

1916 13 231 4

1917 9 76 251918 7 209 1

Post-independence

The partition of India in 1947 adversely impacted the economies of Punjab and

West Bengal, paralyzing banking activities for months. India's independence

marked the end of a regime of the Laissez-faire for the Indian banking. The

Government of India initiated measures to play an active role in the economic life

of the nation, and the Industrial Policy Resolution adopted by the government in

1948 envisaged a mixed economy. This resulted into greater involvement of the

state in different segments of the economy including banking and finance. The

major steps to regulate banking included:

In 1948, the Reserve Bank of India, India's central banking authority, was

nationalized, and it became an institution owned by the Government of India.

In 1949, the Banking Regulation Act was enacted which empowered the Reserve

Bank of India (RBI) "to regulate, control, and inspect the banks in India."

The Banking Regulation Act also provided that no new bank or branch of an

existing bank could be opened without a license from the RBI, and no two banks

could have common directors.

However, despite these provisions, control and regulations, banks in India except

the State Bank of India, continued to be owned and operated by private persons.

This changed with the nationalization of major banks in India on 19 July 1969.

Nationalization

19

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 20/59

The RBI was nationalized on January 1, 1949 in terms of the Reserve Bank of

India (Transfer to Public Ownership) Act, 1948 (RBI, 2005b. By the 1960s, the

Indian banking industry had become an important tool to facilitate the

development of the Indian economy. At the same time, it had emerged as a large

employer, and a debate had ensued about the possibility to nationalize the

banking industry. Indira Gandhi, the-then Prime Minister of India expressed the

intention of the GOI in the annual conference of the All India Congress Meeting in

a paper entitled "Stray thoughts on Bank Nationalization." The paper was

received with positive enthusiasm. Thereafter, her move was swift and sudden,

and the GOI issued an ordinance and nationalized the 14 largest commercial

banks with effect from the midnight of July 19, 1969. Jayaprakash Narayan, a

national leader of India, described the step as a " masterstroke of political

sagacity." Within two weeks of the issue of the ordinance, the Parliament passedthe Banking Companies (Acquisition and Transfer of Undertaking) Bill, and it

received the presidential approval on 9 August 1969.

A second dose of nationalization of 6 more commercial banks followed in 1980.

The stated reason for the nationalization was to give the government more

control of credit delivery. With the second dose of nationalization, the GOI

controlled around 91% of the banking business of India. Later on, in the year

1993, the government merged New Bank of India with Punjab National Bank. It

was the only merger between nationalized banks and resulted in the reduction of

the number of nationalized banks from 20 to 19. After this, until the 1990s, the

nationalized banks grew at a pace of around 4%, closer to the average growth

rate of the Indian economy.

Liberalization

In the early 1990s, the then Narsimha Rao government embarked on a policy of

liberalization, licensing a small number of private banks. These came to be

known as New Generation tech-savvy banks, and included Global Trust Bank

(the first of such new generation banks to be set up), which later amalgamated

with Oriental Bank of Commerce, Axis Bank(earlier as UTI Bank), ICICI Bank and

20

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 21/59

HDFC Bank. This move, along with the rapid growth in the economy of India,

revitalized the banking sector in India, which has seen rapid growth with strong

contribution from all the three sectors of banks, namely, government banks,

private banks and foreign banks.

The next stage for the Indian banking has been set up with the proposedrelaxation in the norms for Foreign Direct Investment, where all Foreign Investors

in banks may be given voting rights which could exceed the present cap of 10%,

at present it has gone up to 74% with some restrictions.

The new policy shook the Banking sector in India completely. Bankers, till this

time, were used to the 4-6-4 method (Borrow at 4%; Lend at 6%; Go home at 4)

of functioning. The new wave ushered in a modern outlook and tech-savvy

methods of working for traditional banks. All this led to the retail boom in India.

People not just demanded more from their banks but also received more.

Currently (2007), banking in India is generally fairly mature in terms of supply,

product range and reach-even though reach in rural India still remains a

challenge for the private sector and foreign banks. In terms of quality of assets

and capital adequacy, Indian banks are considered to have clean, strong and

transparent balance sheets relative to other banks in comparable economies in

its region. The Reserve Bank of India is an autonomous body, with minimal

pressure from the government. The stated policy of the Bank on the Indian

Rupee is to manage volatility but without any fixed exchange rate-and this has

mostly been true.

With the growth in the Indian economy expected to be strong for quite some

time-especially in its services sector-the demand for banking services, especially

retail banking, mortgages and investment services are expected to be strong.One may also expect M&as, takeovers, and asset sales.

In March 2006, the Reserve Bank of India allowed Warburg Pincus to increase its

stake in Kotak Mahindra Bank (a private sector bank) to 10%. This is the first

time an investor has been allowed to hold more than 5% in a private sector bank

21

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 22/59

since the RBI announced norms in 2005 that any stake exceeding 5% in the

private sector banks would need to be vetted by them.

In recent years critics have charged that the non-government owned banks are

too aggressive in their loan recovery efforts in connection with housing, vehicle

and personal loans. There are press reports that the banks' loan recovery effortshave driven defaulting borrowers to suicide.

Top 10 Banking Companies in India

22

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 23/59

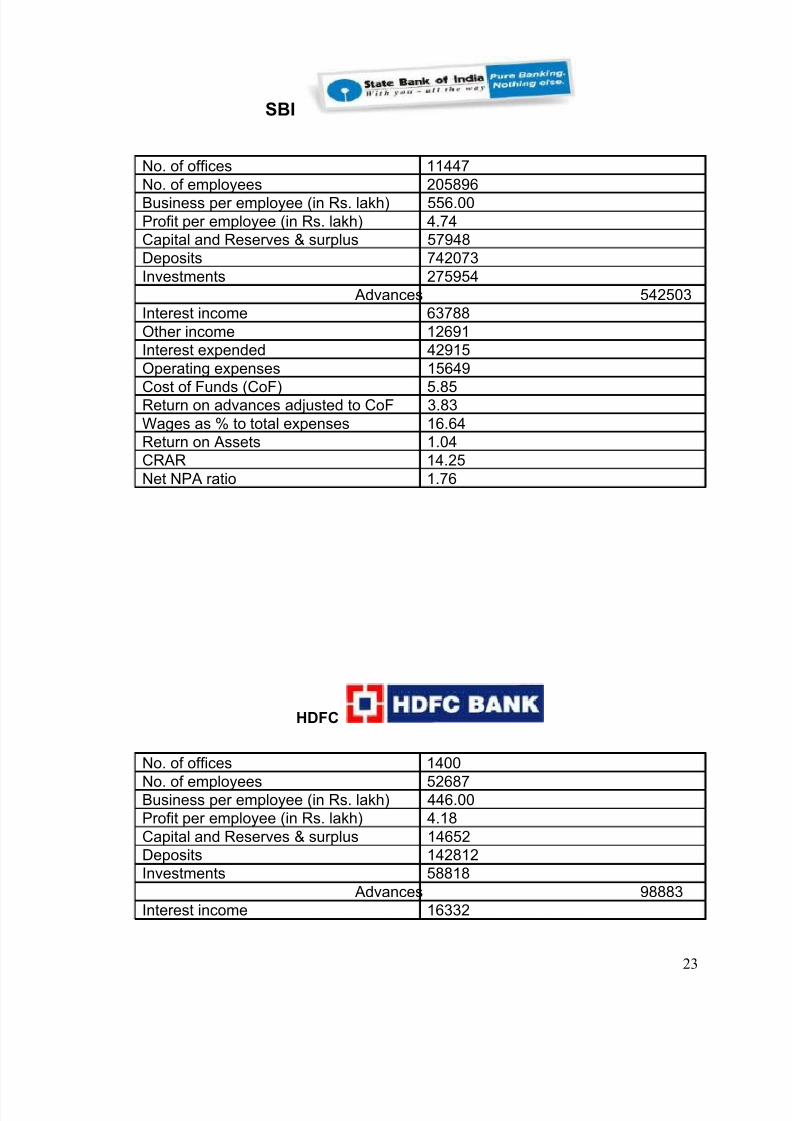

SBI

No. of offices 11447No. of employees 205896Business per employee (in Rs. lakh) 556.00Profit per employee (in Rs. lakh) 4.74Capital and Reserves & surplus 57948Deposits 742073Investments 275954

Advances 542503Interest income 63788Other income 12691Interest expended 42915Operating expenses 15649

Cost of Funds (CoF) 5.85Return on advances adjusted to CoF 3.83Wages as % to total expenses 16.64Return on Assets 1.04CRAR 14.25Net NPA ratio 1.76

HDFC

No. of offices 1400

No. of employees 52687Business per employee (in Rs. lakh) 446.00Profit per employee (in Rs. lakh) 4.18Capital and Reserves & surplus 14652Deposits 142812Investments 58818

Advances 98883Interest income 16332

23

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 24/59

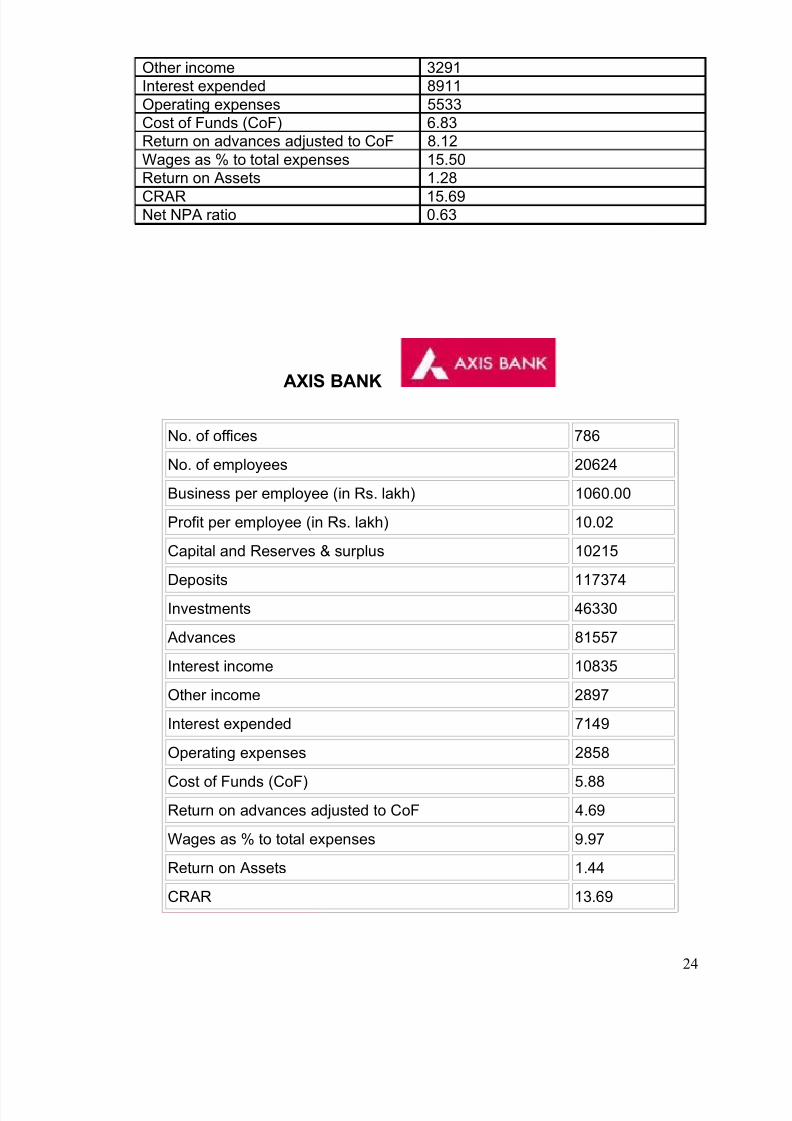

Other income 3291Interest expended 8911Operating expenses 5533Cost of Funds (CoF) 6.83Return on advances adjusted to CoF 8.12Wages as % to total expenses 15.50Return on Assets 1.28

CRAR 15.69Net NPA ratio 0.63

AXIS BANK

No. of offices 786

No. of employees 20624

Business per employee (in Rs. lakh) 1060.00

Profit per employee (in Rs. lakh) 10.02

Capital and Reserves & surplus 10215

Deposits 117374

Investments 46330

Advances 81557

Interest income 10835

Other income 2897

Interest expended 7149

Operating expenses 2858

Cost of Funds (CoF) 5.88Return on advances adjusted to CoF 4.69

Wages as % to total expenses 9.97

Return on Assets 1.44

CRAR 13.69

24

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 25/59

Net NPA ratio 0.40

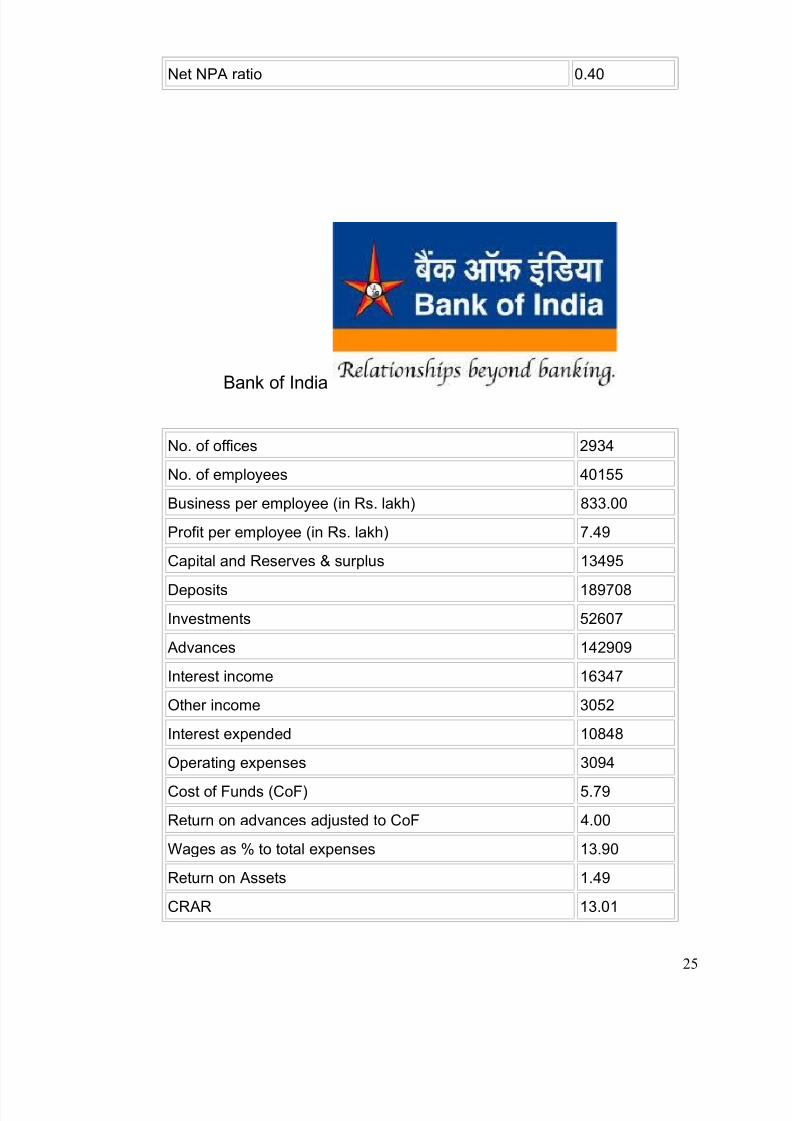

Bank of India

No. of offices 2934

No. of employees 40155

Business per employee (in Rs. lakh) 833.00

Profit per employee (in Rs. lakh) 7.49

Capital and Reserves & surplus 13495

Deposits 189708

Investments 52607

Advances 142909

Interest income 16347

Other income 3052

Interest expended 10848

Operating expenses 3094

Cost of Funds (CoF) 5.79

Return on advances adjusted to CoF 4.00

Wages as % to total expenses 13.90

Return on Assets 1.49

CRAR 13.01

25

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 26/59

Net NPA ratio 0.44

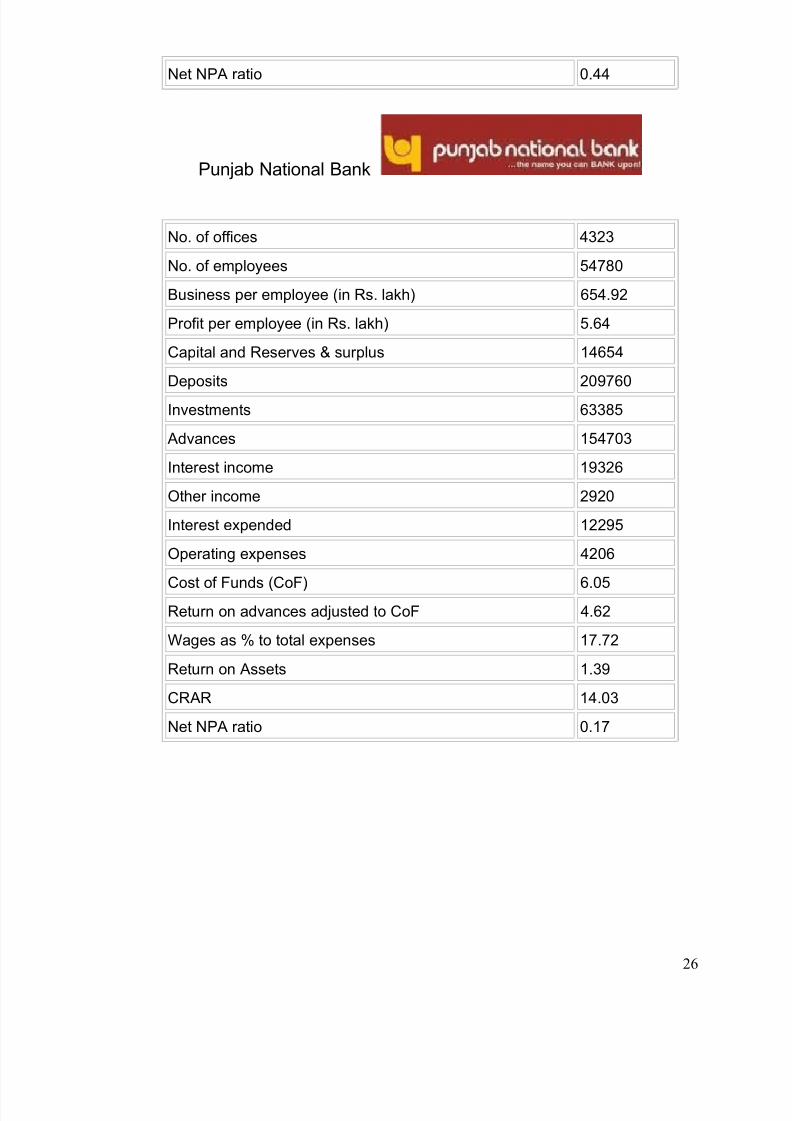

Punjab National Bank

No. of offices 4323

No. of employees 54780

Business per employee (in Rs. lakh) 654.92

Profit per employee (in Rs. lakh) 5.64

Capital and Reserves & surplus 14654

Deposits 209760

Investments 63385

Advances 154703

Interest income 19326

Other income 2920

Interest expended 12295

Operating expenses 4206

Cost of Funds (CoF) 6.05Return on advances adjusted to CoF 4.62

Wages as % to total expenses 17.72

Return on Assets 1.39

CRAR 14.03

Net NPA ratio 0.17

26

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 27/59

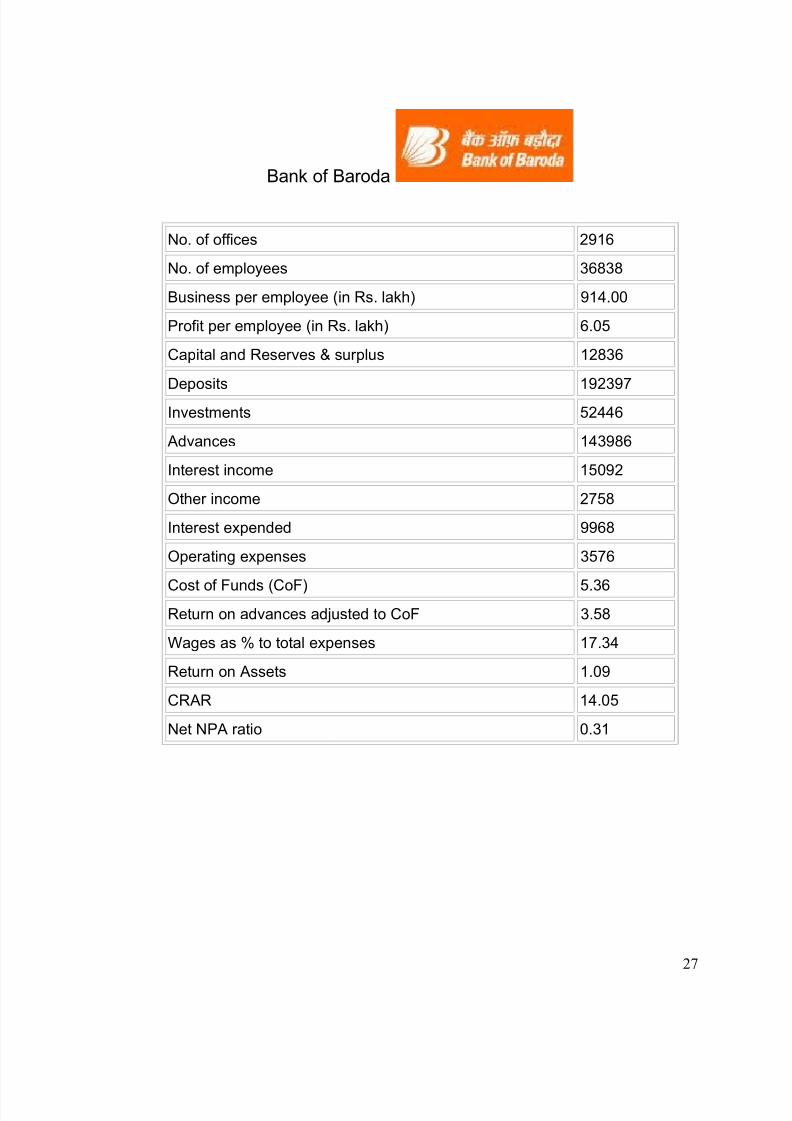

Bank of Baroda

No. of offices 2916

No. of employees 36838

Business per employee (in Rs. lakh) 914.00

Profit per employee (in Rs. lakh) 6.05

Capital and Reserves & surplus 12836

Deposits 192397

Investments 52446

Advances 143986

Interest income 15092

Other income 2758

Interest expended 9968

Operating expenses 3576

Cost of Funds (CoF) 5.36Return on advances adjusted to CoF 3.58

Wages as % to total expenses 17.34

Return on Assets 1.09

CRAR 14.05

Net NPA ratio 0.31

27

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 28/59

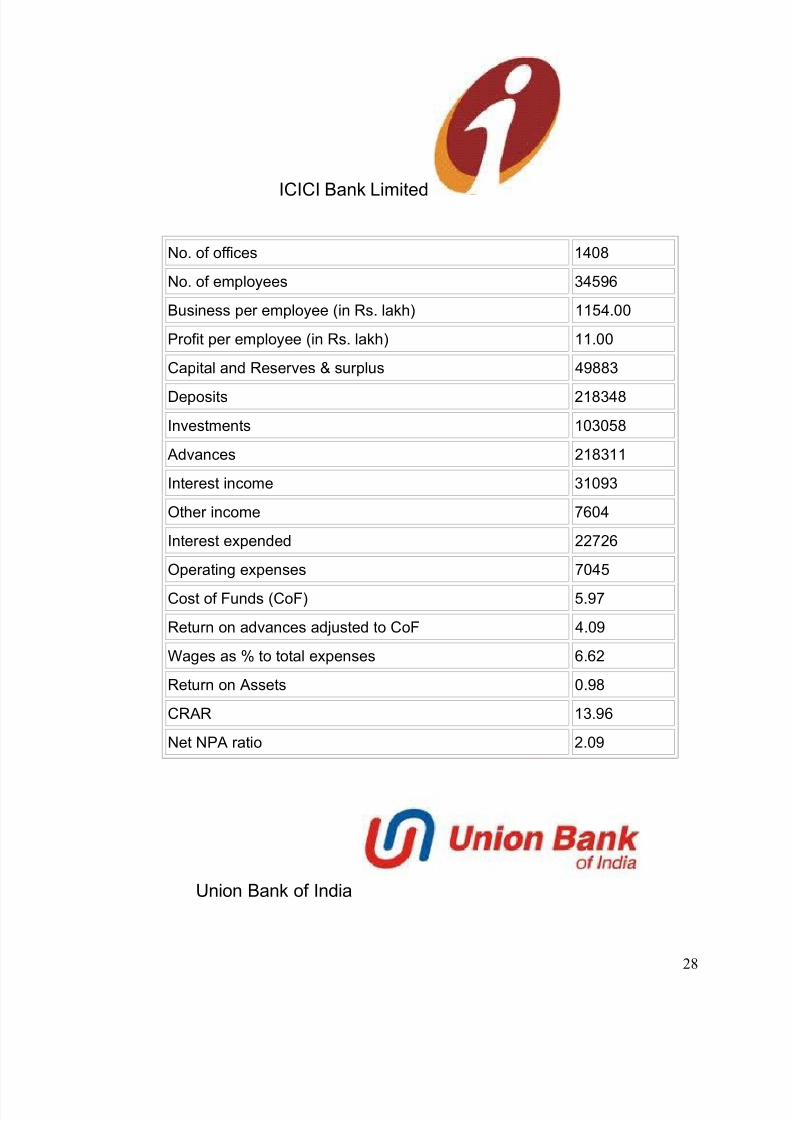

ICICI Bank Limited

No. of offices 1408

No. of employees 34596

Business per employee (in Rs. lakh) 1154.00

Profit per employee (in Rs. lakh) 11.00

Capital and Reserves & surplus 49883

Deposits 218348

Investments 103058

Advances 218311

Interest income 31093

Other income 7604

Interest expended 22726

Operating expenses 7045

Cost of Funds (CoF) 5.97

Return on advances adjusted to CoF 4.09

Wages as % to total expenses 6.62

Return on Assets 0.98

CRAR 13.96

Net NPA ratio 2.09

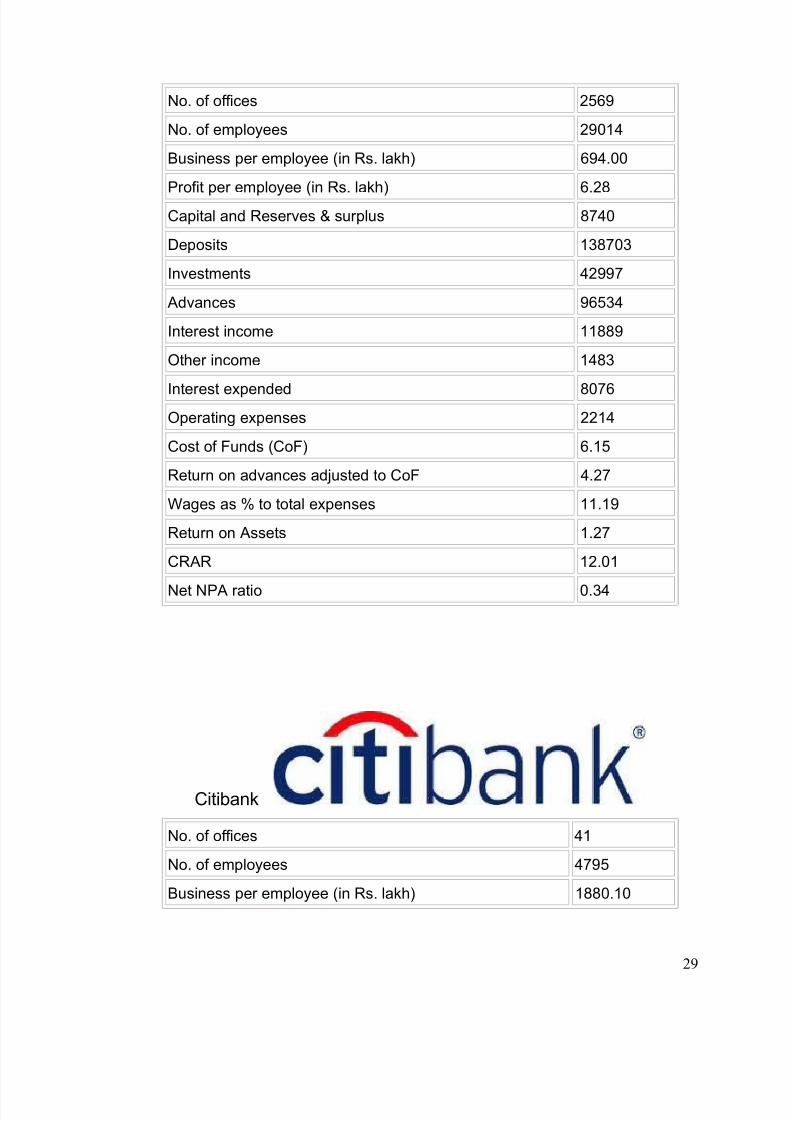

Union Bank of India

28

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 29/59

No. of offices 2569

No. of employees 29014

Business per employee (in Rs. lakh) 694.00

Profit per employee (in Rs. lakh) 6.28

Capital and Reserves & surplus 8740

Deposits 138703

Investments 42997

Advances 96534

Interest income 11889

Other income 1483

Interest expended 8076Operating expenses 2214

Cost of Funds (CoF) 6.15

Return on advances adjusted to CoF 4.27

Wages as % to total expenses 11.19

Return on Assets 1.27

CRAR 12.01

Net NPA ratio 0.34

Citibank

No. of offices 41

No. of employees 4795

Business per employee (in Rs. lakh) 1880.10

29

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 30/59

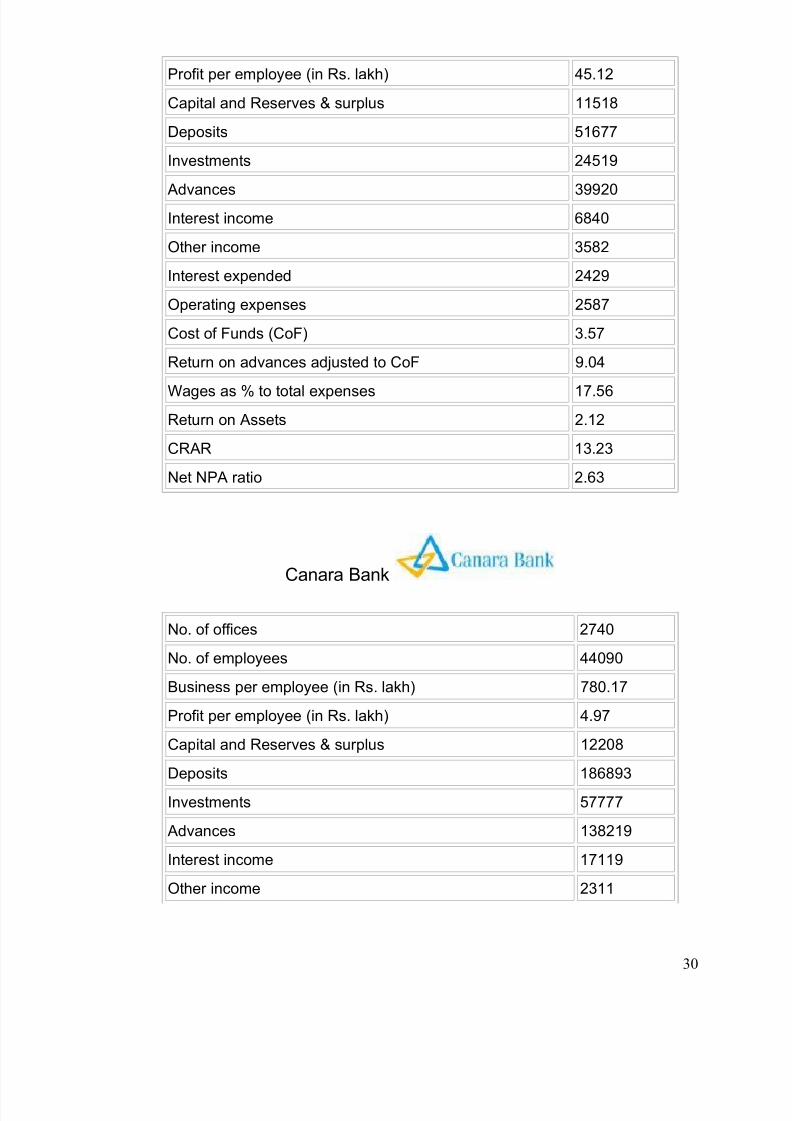

Profit per employee (in Rs. lakh) 45.12

Capital and Reserves & surplus 11518

Deposits 51677

Investments 24519

Advances 39920Interest income 6840

Other income 3582

Interest expended 2429

Operating expenses 2587

Cost of Funds (CoF) 3.57

Return on advances adjusted to CoF 9.04

Wages as % to total expenses 17.56

Return on Assets 2.12

CRAR 13.23

Net NPA ratio 2.63

Canara Bank

No. of offices 2740

No. of employees 44090

Business per employee (in Rs. lakh) 780.17

Profit per employee (in Rs. lakh) 4.97

Capital and Reserves & surplus 12208

Deposits 186893

Investments 57777

Advances 138219

Interest income 17119

Other income 2311

30

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 31/59

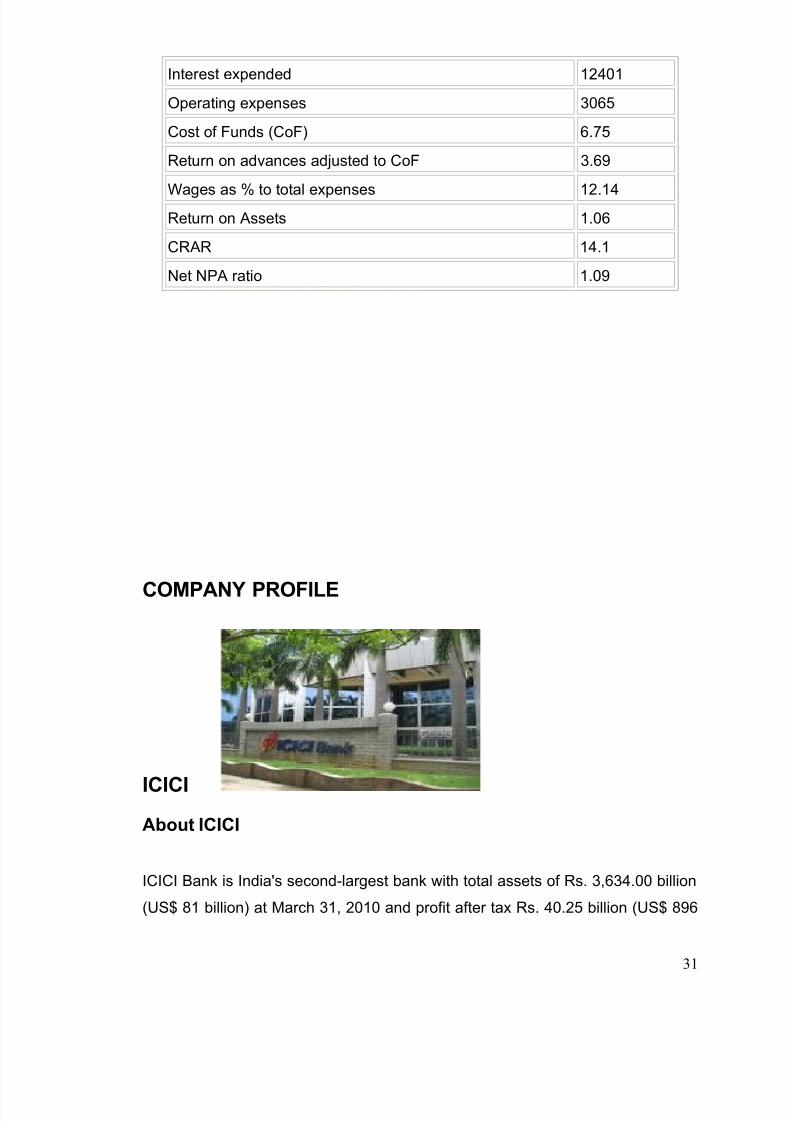

Interest expended 12401

Operating expenses 3065

Cost of Funds (CoF) 6.75

Return on advances adjusted to CoF 3.69

Wages as % to total expenses 12.14Return on Assets 1.06

CRAR 14.1

Net NPA ratio 1.09

COMPANY PROFILE

ICICI

About ICICI

ICICI Bank is India's second-largest bank with total assets of Rs. 3,634.00 billion

(US$ 81 billion) at March 31, 2010 and profit after tax Rs. 40.25 billion (US$ 896

31

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 32/59

million) for the year ended March 31, 2010. The Bank has a network of 2,035

branches and about 5,518 ATMs in India and presence in 18 countries. ICICI

Bank offers a wide range of banking products and financial services to corporate

and retail customers through a variety of delivery channels and through its

specialized subsidiaries in the areas of investment banking, life and non-life

insurance, venture capital and asset management. The Bank currently has

subsidiaries in the United Kingdom, Russia and Canada, branches in United

States, Singapore, Bahrain, Hong Kong, Sri Lanka, Qatar and Dubai International

Finance Centre and representative offices in United Arab Emirates, China, South

Africa, Bangladesh, Thailand, Malaysia and Indonesia. Our UK subsidiary has

established branches in Belgium and Germany

History

In 1955, The Industrial Credit and Investment Corporation of India Limited (ICICI)

was incorporated at the initiative of World Bank, the Government of India and

representatives of Indian industry, with the objective of creating a development

financial institution for providing medium-term and long-term project financing to

Indian businesses. In 1994, ICICI established Banking Corporation as a banking

subsidiary. Formerly known as Industrial Credit and Investment Corporation of India, ICICI Banking Corporation was later renamed as 'ICICI Bank Limited'.

ICICI founded a separate legal entity, ICICI Bank, to undertake normal banking

operations - taking deposits, credit cards, car loans etc. In 2001, ICICI acquired

Bank of Madura (est. 1943). Bank of Madura was a Chettiar bank, and had

acquired Chettinad Mercantile Bank (est. 1933) and Illanji Bank (established

1904) in the 1960s. In 2002, The Boards of Directors of ICICI and ICICI Bank

approved the reverse merger of ICICI, ICICI Personal Financial Services Limited

and ICICI Capital Services Limited, into ICICI Bank. After receiving all necessary

regulatory approvals, ICICI integrated the group's financing and banking

operations, both wholesale and retail, into a single entity. At the same time, ICICI

started its international expansion by opening representative offices in New York

32

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 33/59

and London. In India, ICICI Bank bought the Shimla and Darjeeling branches that

Standard Chartered Bank had inherited when it acquired Grindlays Bank.

In 2003, ICICI opened subsidiaries in Canada and the United Kingdom (UK), and

in the UK it established an alliance with Lloyds TSB. It also opened an Offshore

Banking Unit (OBU) in Singapore and representative offices in Dubai andShanghai. In 2004, ICICI opened a representative office in Bangladesh to tap the

extensive trade between that country, India and South Africa. In 2005, ICICI

acquired Investitsionno-Kreditny Bank (IKB), a Russia bank with about US$4mn

in assets, head office in Balabanovo in the Kaluga region, and with a branch in

Moscow. ICICI renamed the bank ICICI Bank Eurasia. Also, ICICI established a

branch in Dubai International Financial Centre and in Hong Kong. In 2006, ICICI

Bank UK opened a branch in Antwerp, in Belgium. ICICI opened representative

offices in Bangkok, Jakarta, and Kuala Lumpur . In 2007, ICICI amalgamated

Sangli Bank, which was headquartered in Sangli, in Maharashtra State, and

which had 158 branches in Maharashtra and another 31 in Karnataka State.

Sangli Bank had been founded in 1916 and was particularly strong in rural areas.

With respect to the international sphere, ICICI also received permission from the

government of Qatar to open a branch in Doha. Also, ICICI Bank Eurasia opened

a second branch, this time in St. Petersburg. In 2008, The US Federal Reserve

permitted ICICI to convert its representative office in New York into a branch.

ICICI also established a branch in Frankfurt. In 2009, ICICI made huge changes

in its organization like elimination of loss making department and retrenching

outsourced staff or renegotiate their charges in consequent to the recession. In

addition to this, ICICI adopted a massive approach aims for cost control and cost

cutting. In consequent of it, compensation to staff was not increased and no

bonus declared for 2008-09.

On 23 May ICICI Bank announced merger with Bank of Rajasthan with it through

share-swap in a non-cash deal that values the Bank of Rajasthan at about Rs

3,000 crore. Each 118 shares of Bank of Rajasthan will be converted into 25

shares of ICICI. It is said that this merger will also expand ICICI Bank's branch

network by 25%.

33

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 34/59

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 35/59

• Family Banking

Loans

ICICI Bank offers following loan facilities:

• Home Loans

• Loan Against Property

• Personal Loans

• Car Loans

• Two Wheeler Loans

• Commercial Vehicle Loans

• Loans Against Securities

• Loan Against Gold Ornaments

• Pre-approved Loans

Cards

ICICI Bank is India's largest issuer of credit cards. It also offers other types of

cards. The various cards offered by ICICI bank are as below:

• Consumer Cards

• Credit Cards

• Travel Cards

• Debit Cards

• Commercial Cards

• Corporate Cards

• Prepaid Cards

•

Purchase Cards• Distribution Cards

• Business Cards

• Merchant Services

35

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 36/59

Investments

ICICI Bank facilitates a range of investment products including:

• ICICI Bank Tax Saving Bonds

•

Mutual Funds• Government of India Bonds

• Initial Public Offers (IPO) by Corporate

• Foreign Exchange Services

• ICICI Bank Pure Gold

• Senior Citizens Savings Scheme, 2004

Insurance

ICICI Bank offers various types of insurance. Customers can choose from the

following:

• Home Insurance

• Health Insurance

• Health Advantage Plus

• Family Floater

• Personal Accident

• Travel Insurance

• Individual Overseas Travel Insurance

• Student Medical Insurance

• Motor Insurance

• Car Insurance

• Two Wheeler Insurance

• Life Insurance

• ICICI Pru LifeTime Gold

• ICICI Pru LifeState RP

NRI Services

36

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 37/59

following services are offered to the NRIs:

• Money Transfer

• Bank Accounts

• Investments

•

Home Loans• Insurance

• Loans Against FD

SWOT Analysis of ICICI

STRENGHTS:

1) Online Services: ICICI Bank provides online services of all its banking

facilities. It also provides D-Mart account facilities on-line, so a person can

access his account from anywhere he is .D-Mart is a dematerialized account

opened by a salaried person for purchase & sale of shares of different

companies.

37

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 38/59

2) Advanced Infrastructure: Branches of ICICI Bank are well equipped with

advanced technology to provide the customers with taster banking services. All

the computerized machines are located in suitable manner & are very useful to

the customers & staff of the bank.

3) Friendly Staff : The staff of ICICI Bank in all branches is very friendly & helpsthe customers in all cases. They provide faster services along with bonding &

personal relationship with the customers.

4) 12hrs.Banking services: Compared to other bank ICICI bank

provides long hrs. Of services i.e. 8-8 services to the customers. This

service is one of its kinds & is very helpful for the customers who are

in urgent need of money.

5) Other Facilities to the Customers & Employees: ICICI Bank also

provides other facilities like drinking water facilities, proper sitting

arrangements to the customers. And there are also proper Ventilation

& sanitary facilities for the employees of the bank.

6) Late night ATM services: ICICI bank provides late night ATM

services to the customers. The ATM centers of ICICI bank works

even after 11:00pm. At night in certain branches.

Weakness:

1) High Bank Service Charges: ICICI bank charges highly to

customers for the services provided by them when compared to

other bank & that is why it is only in the reach of higher class of

society.

2) Less Credit Period: ICICI bank provides credit facilities but only

upto limited period. Even when the credit period is not over it

sends reminder letters to the customers which may annoy them.

OPPORTUNITIES:

38

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 39/59

1) Bank–Insurance services: The bank should also provide

insurance services. That means the bank can have a tie-up with an

insurance company. The bank will advertise & promote the different

policies introduced by the insurance company & convince their

customers to buy insurance policies.

2) Increase in percentage of Returns on increase: The bank should

provide higher returns on deposits in comparison of the present

situation. These will also upto large extent help the bank earn profits &

popularity.

3) Recruit professionally guided students: Bank & Insurance is a

special non-aid course where the students specialize in the

functioning & services of the bank & also are knowledge about

various tax policies. The bank can recruit these students through tie-

ups with colleges. Such students will surely prove as an asset to the

bank.

4) Associate with social cause: The bank can also associate itself

with social causes like providing relief aid patients, funding towards

natural calamities. But this falls in the 4th quadrant so the bank should

neglect it.

THREATS

1) Competition: ICICI Bank is facing tight competition locally as well

as internationally. Bank like CITI Bank, HSBC, ABM, Standered

Chartered, HDFC also provide equivalent facilities like ICICI do and

also ICICI do not have consistency in its international operation.

2) Net Services: ICICI Bank provides all kind of services on-line.

There can be easy access to the e-mail ids of the customers through

wrong people. The confidential information of the customers can be

leaked easily through the e-mail ids.

39

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 40/59

3) Decentralized Management: Each branch manager is given the

authority of taking decisions in their respective branches. The

decisions made by different managers are diverse and any one

wrong decision can laid to heavy losses to the bank.

4) No Proper Facilities To Uneducated customers: ICICI Bankprovides all services through electronic computerized machines. This

creates problems to the less educated people. But this threat falls in

the 4th quadrant so it’s negligible. The company can avoid this threat.

The Bank is actively involved since 1973 in non-profit activity called Community

Services Banking. All the branches and administrative offices throughout the

country sponsor and participate in large number of welfare activities and social

causes. Their business is more than banking because they touch the lives of

people anywhere in many ways.

Their commitment to nation-building is complete & comprehensive.

History

The roots of the State Bank of India rest in the first decade of 19th century, when

the Bank of Calcutta, later renamed the Bank of Bengal, was established on 2

June 1806. The Bank of Bengal and two other Presidency banks, namely, the

Bank of Bombay (incorporated on 15 April 1840) and the Bank of Madras

(incorporated on 1 July 1843). All three Presidency banks were incorporated as

joint stock companies, and were the result of the royal charters. These three

banks received the exclusive right to issue paper currency in 1861 with the Paper

Currency Act, a right they retained until the formation of the Reserve Bank of

India. The Presidency banks amalgamated on 27 January 1921, and the

40

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 41/59

reorganized banking entity took as its name Imperial Bank of India. The Imperial

Bank of India continued to remain a joint stock company.

Pursuant to the provisions of the State Bank of India Act (1955), the Reserve

Bank of India, which is India's central bank, acquired a controlling interest in the

Imperial Bank of India. On 30 April 1955 the Imperial Bank of India became theState Bank of India. The Govt. of India recently acquired the Reserve Bank of

India's stake in SBI so as to remove any conflict of interest because the RBI is

the country's banking regulatory authority.

In 1959 the Government passed the State Bank of India (Subsidiary Banks) Act,

enabling the State Bank of India to take over eight former State-associated banks

as its subsidiaries. On 13 September 2008, State Bank of Saurashtra, one of its

Associate Banks, merged with State Bank of India.

SBI has acquired local banks in rescues. For instance, in 1985, it acquired Bank

of Cochin in Kerala, which had 120 branches. SBI was the acquirer as its affiliate,

State Bank of Travancore, already had an extensive network in Kerala.

Associate banks

SBI has five associate banks that with SBI constitute the State Bank Group. All

use the same logo of a blue keyhole and all the associates use the "State Bank

of" name followed by the regional headquarters' name. Originally, the then seven

banks that became the associate banks belonged to princely states until the

government nationalized them between October, 1959 and May, 1960. In tune

with the first Five Year Plan, emphasizing the development of rural India, the

government integrated these banks into State Bank of India to expand its rural

outreach. There has been a proposal to merge all the associate banks into SBI tocreate a "mega bank" and streamline operations.

The first step towards unification occurred on 13 August 2008 when State Bank

of Saurashtra merged with SBI, reducing the number of state banks from seven

to six. Then on 19 June 2009 the SBI board approved the merger of its

41

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 42/59

subsidiary, State Bank of Indore, with itself. SBI holds 98.3% in State Bank of

Indore. (Individuals who held the shares prior to its takeover by the government

hold the balance of 1.77 %.)

The acquisition of State Bank of Indore added 470 branches to SBI's existing

network of 12,448 and over 21,000 ATMs. Also, following the acquisition, SBI'stotal assets will inch very close to the Rs 10-lakh crore mark. Total assets of SBI

and the State Bank of Indore stood at Rs 998,119 crore as on March 2009. The

process of merging of State Bank of Indore was completed by April 2010, and the

SBI Indore Branches started functioning as SBI branches on 26 August 2010.

SBI's still surviving associate banks are:

•

State Bank of Bikaner & Jaipur • State Bank of Hyderabad

• State Bank of Mysore

• State Bank of Patiala

• State Bank of Travancore

Group companies

• SBI Capital Markets Ltd

• SBI Mutual Fund (A Trust)

• SBI Factors and Commercial Services Ltd

• SBI DFHI Ltd

• SBI Cards and Payment Services Pvt Ltd

• SBI Life Insurance Company Limited - Bancassurance (Life Insurance)

• SBI Funds Management Pvt Ltd• SBI Canada

International presence

42

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 43/59

The bank has 131 overseas offices spread over 32 countries as on 31st Dec

2009. It has branches of the parent in Colombo, Dhaka, Frankfurt, Hong Kong,

Johannesburg, London and environs, Los Angeles, Male in the Maldives,

Muscat, New York, Osaka, Sydney, and Tokyo. It has offshore banking units in

the Bahamas, Bahrain, and Singapore, and representative offices in Bhutan and

Cape Town.

SBI operates several foreign subsidiaries or affiliates. In 1990 it established an

offshore bank, State Bank of India (Mauritius).

In 1982, the bank established a subsidiary, State Bank of India (California), which

now has eight branches - seven branches in the state of California and one in

Washington DC that it opened on 23 November 2009. The seven branches in

California are located in Los Angeles, Artesia, San Jose, Canoga Park, Fresno,

San Diego and Bakersfield.

The Canadian subsidiary, State Bank of India (Canada) too dates to 1982. It has

seven branches, four in the greater Toronto area and three in British Columbia.

In Nigeria SBI operates as INMB Bank. This bank began in 1981 as the Indo-

Nigerian Merchant Bank and received permission in 2002 to commence retail

banking. It now has five branches in Nigeria.

In Nepal, SBI owns 50% of Nepal SBI Bank, which has branches throughout the

country. In Moscow SBI owns 60% of Commercial Bank of India, with Canara

Bank owning the rest. In Indonesia it owns 76% of PT Bank Indo Monex.

State Bank of India already has a branch in Shanghai and plans to open one up

in Tianjin.

Corporate details

This site provides comprehensive information on state bank of India, the premier

nationalized Indian bank. State bank of India is actively involved since 1973 in

non profit activity called community services banking. State bank of India is

43

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 44/59

India’s largest bank amongst all public and private sector banks operating in

India. State bank of India owns and operates the following subsidiaries and joint

venture:

• State bank of India credit card

• State bank of India online

• State bank of India USA

• State bank of India services

• State bank of India mutual funds

• State bank of India branch

• State bank of India NRI account

Banking subsidiaries

• State bank of Bikaner and Jaipur

• State bank of Hyderabad

• State bank of Indore

• State bank of Mysore

• State bank of Patiala

• State bank of Saurashtra

• State bank of Travancore

Foreign subsidiaries:

• State bank of India international (Mauritius) Ltb

• State bank of India ( California)

•

State bank of India ( Canada)• INMD bank ltd, Lagos

Non banking subsidiaries

• SBI Capital Market Ltb

44

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 45/59

• SBI Funds Management Pvt Ltb

• SBI DFHI Ltb

• SBI Factors and Commercial Services Pvt Ltb

• SBI Cards and Payments Services Pvt Ltb

The main activities of SBI are:

• Personal banking

• NRI services

• Agriculture

• International

• Corporate

• SME

• Domestic treasury

State bank of India offers following services to its customers:

• Domestic treasury

• SBI Vishwa Yatra Foreign Travel Card

• Broking services

• International banking

• E- Pay

• E-Rail

• RBIEFT

• Safe deposit lockers

• Gift cheque

• MICR codes

• Foreign Inward Remittances

SWOT Analysis

Strengths

45

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 46/59

• Brand name

• Market Leader

• Wide Distribution Network

• Government Owned

• DiversifiedPortfolio

Weaknesses

• Minor hindrances

• Hierarchical management

• Lags modernization

Opportunities

• Merger of associate banks with SBI

• Opportunities for public sector banks

• New Branches and ATM's

• Expansion on Foreign soil

Threats

• Advent of MNC banks

• CRM

• Private banks venturing into the rural

• Employee Strike

46

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 47/59

RESEARCH METHODOLOGY

Research methodology is a systematic way, which consists of series of action

steps, necessary to effectively carry out research and the desired sequencing to

these steps. The marketing research is a process of involves a no. of inter

related activities, which overlap and do rigidly follow a particular sequence. It

consists of the following steps:

• Formulating the objective of the study

• Designing the methods of data collection

• Selecting the sample plan

• Collecting the data

• Processing and analyzing the data

• Reporting the findings

Research objective

• To study whether the customers are satisfied with their services among

ICICI bank and SBI bank

• To know about the customer preferences among ICICI bank and SBI

bank

47

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 48/59

• To give suggestions to improve the services

Data analysis

Processing and analysis the collected data:

Once questionnaire have been received, the next task is to aggregate the

data in a meaningful manner. A number of tables are preparing to bring out

the main characteristics of the data. The researcher should have a well

thought out framework for processing and analyzing data, and this should be

done prior to the collection. It includes the following activities:

Editing: the first task in data processing is the editing. Editing is the process

of examining errors and omissions in the collected data and making

necessary corrections in the same.

Coding: coding is the procedure of classifying the answer to a question into

a meaningful categories. Coding is necessary to carry out the subsequent

operations of tabulating and analyzing data. If coding is not done, it will not be

possible to reduce a large number of heterogeneous responses into a

meaningful categories with the result that the analysis of data would be weak

and ineffective, and without proper focus.

Tabulation: tabulation comprises of the data into different categories and

counting the number of cases that belong to each category. The simplest way

to tabulate is to count the number of responses to one question. This is also

called universal tabulation. The analysis based on just one variable is

obviously meager. Where two or more variables are involved in tabulation, it

is called bivariate or multivariate tabulation.

SAMPLING DESIGN

Target population

48

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 49/59

The target population in this research refers to the bank customers who are

having an account in SBI bank and ICICI bank due to them convenience in

collecting the data. The respondents can be any gender, any income level, any

occupation and any education level.

Sources of data

Primary data:

• Questionnaire

Secondary data:

• Books

• Website

Data collection method

• Communication approach was basically structured questioning that is

personal interview with the aid of printed questionnaires.

49

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 50/59

Data analysis

Appropriate comparative analysis will be adopted. The data will be tabulatedand analyzed.

Limitations of study

• The study is limited to particular branch of SBI and ICICI bank

• Since the time is less the sample of certain no. of people has been

taken which is a small portion of the country.

50

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 51/59

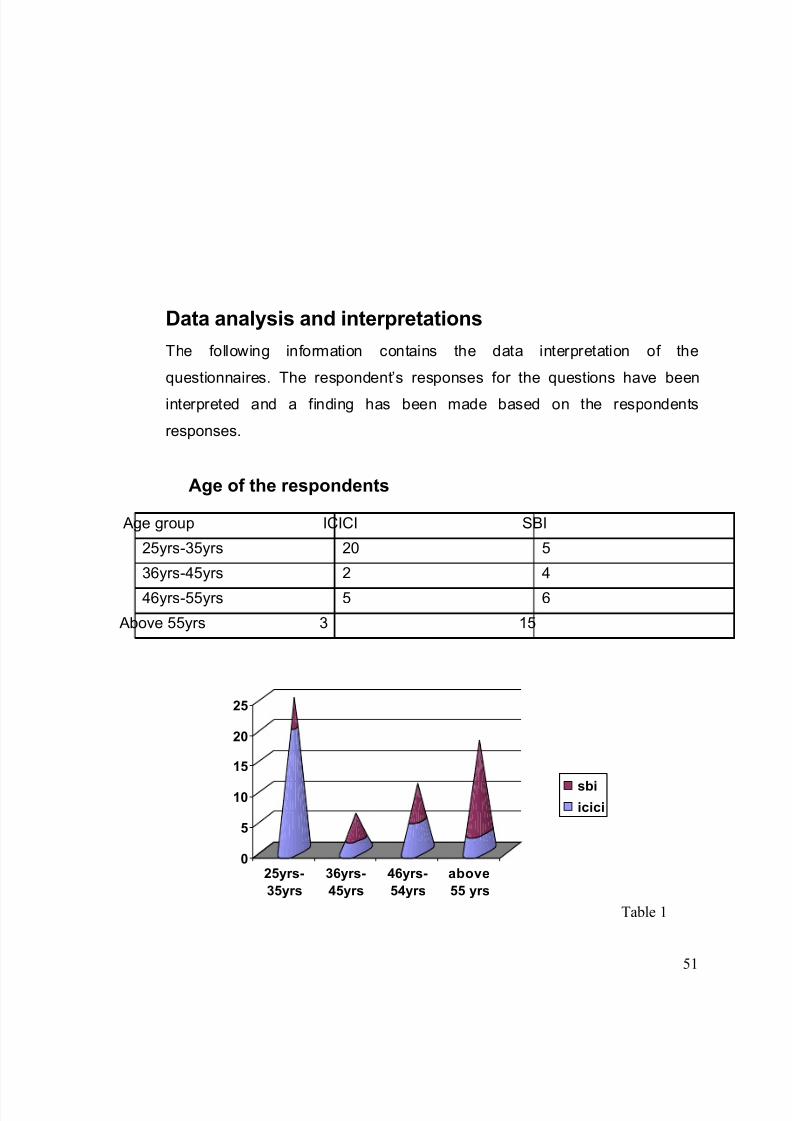

Data analysis and interpretations

The following information contains the data interpretation of the

questionnaires. The respondent’s responses for the questions have been

interpreted and a finding has been made based on the respondents

responses.

Age of the respondents

Age group ICICI SBI

25yrs-35yrs 20 5

36yrs-45yrs 2 4

46yrs-55yrs 5 6

Above 55yrs 3 15

0

5

10

15

20

25

25yrs-

35yrs

36yrs-

45yrs

46yrs-

54yrs

above

55 yrs

sbi

icici

Table 1

51

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 52/59

Interpretation

From the above table we can draw the conclusion that people belonging to the

age group of 55 yrs above trust more on SBI as compare to ICICI and ICICI is

more popular in the age group of 25yrs-35yrs.

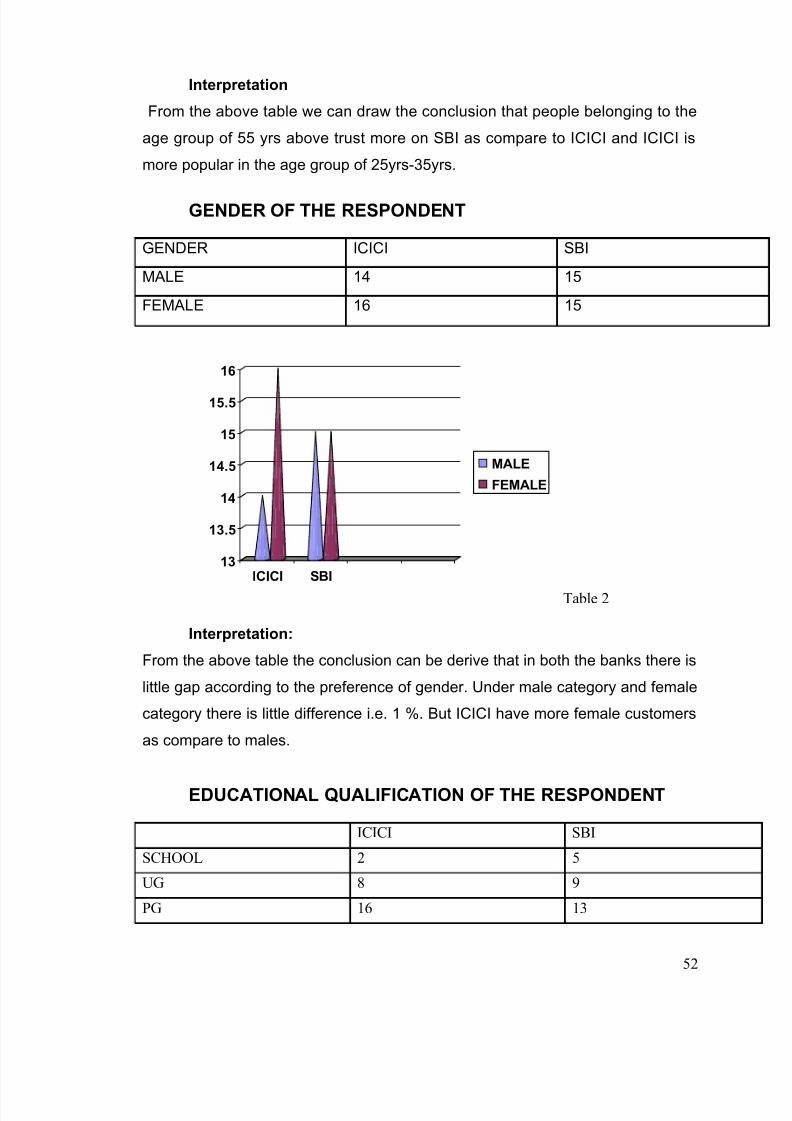

GENDER OF THE RESPONDENT

GENDER ICICI SBI

MALE 14 15

FEMALE 16 15

13

13.5

14

14.5

15

15.5

16

ICICI SBI

MALE

FEMALE

Table 2

Interpretation:

From the above table the conclusion can be derive that in both the banks there is

little gap according to the preference of gender. Under male category and female

category there is little difference i.e. 1 %. But ICICI have more female customers

as compare to males.

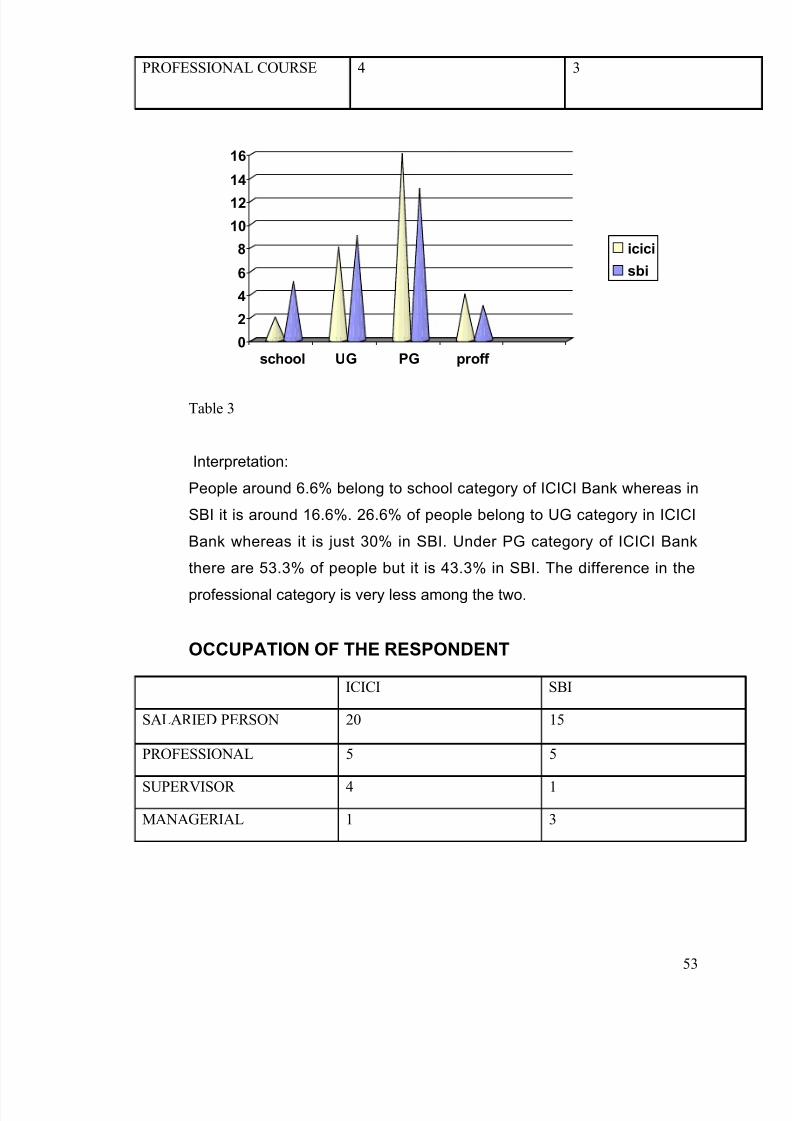

EDUCATIONAL QUALIFICATION OF THE RESPONDENT

ICICI SBI

SCHOOL 2 5

UG 8 9

PG 16 13

52

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 53/59

PROFESSIONAL COURSE 4 3

0

2

4

6

8

10

12

14

16

school UG PG proff

icici

sbi

Table 3

Interpretation:

People around 6.6% belong to school category of ICICI Bank whereas in

SBI it is around 16.6%. 26.6% of people belong to UG category in ICICI

Bank whereas it is just 30% in SBI. Under PG category of ICICI Bank

there are 53.3% of people but it is 43.3% in SBI. The difference in the

professional category is very less among the two.

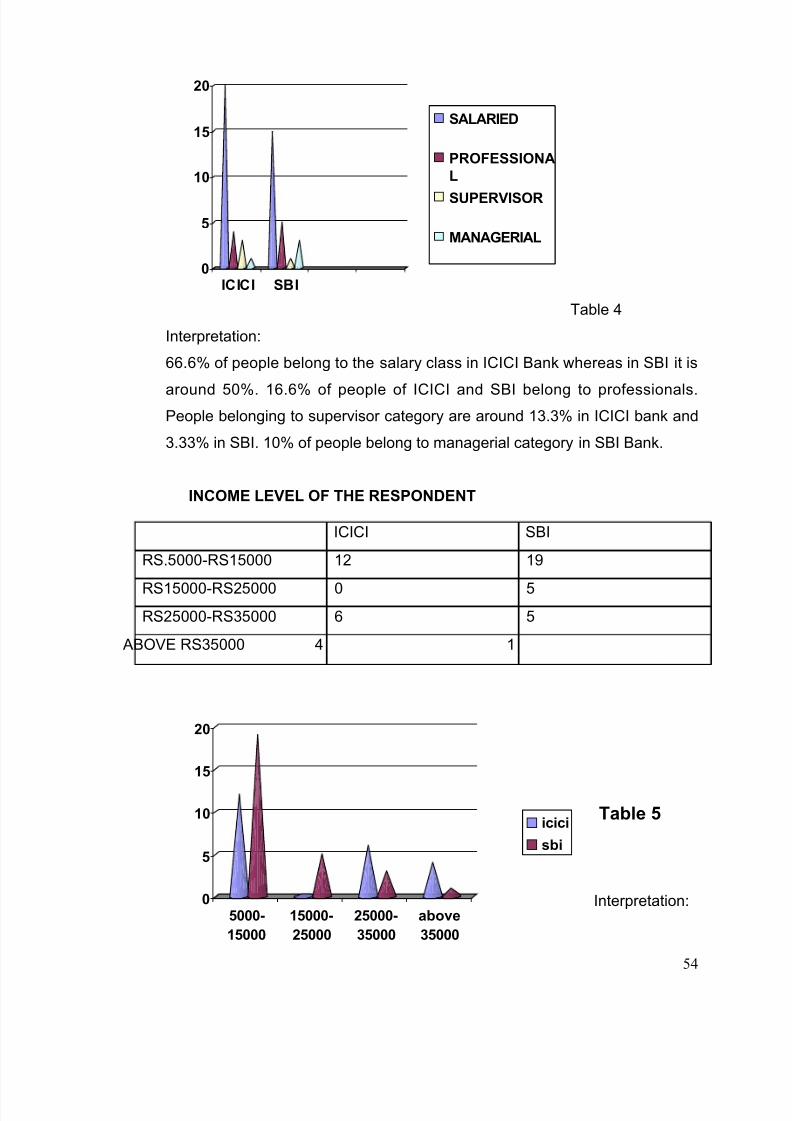

OCCUPATION OF THE RESPONDENT

ICICI SBI

SALARIED PERSON 20 15

PROFESSIONAL 5 5

SUPERVISOR 4 1

MANAGERIAL 1 3

53

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 54/59

0

5

10

15

20

ICICI SBI

SALARIED

PROFESSIONA

L

SUPERVISOR

MANAGERIAL

Table 4

Interpretation:

66.6% of people belong to the salary class in ICICI Bank whereas in SBI it is

around 50%. 16.6% of people of ICICI and SBI belong to professionals.People belonging to supervisor category are around 13.3% in ICICI bank and

3.33% in SBI. 10% of people belong to managerial category in SBI Bank.

INCOME LEVEL OF THE RESPONDENT

ICICI SBI

RS.5000-RS15000 12 19

RS15000-RS25000 0 5

RS25000-RS35000 6 5

ABOVE RS35000 4 1

Table 5

Interpretation:

54

0

5

10

15

20

5000-

15000

15000-

25000

25000-

35000

above

35000

icici

sbi

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 55/59

According to the income level of respondents 40% of people from ICICI Bank

belong to the category of Rs.5000-Rs 15000. But people in SBI have a higher

percentage as compare to ICICI Bank. There is no one under the category of Rs

15000-Rs25000 in ICICI Bank but there are around 16.6% of people under this

category in SBI. People are more in percentage in ICICI Bank as compare to SBI

under the category of Rs25000-Rs 35000.

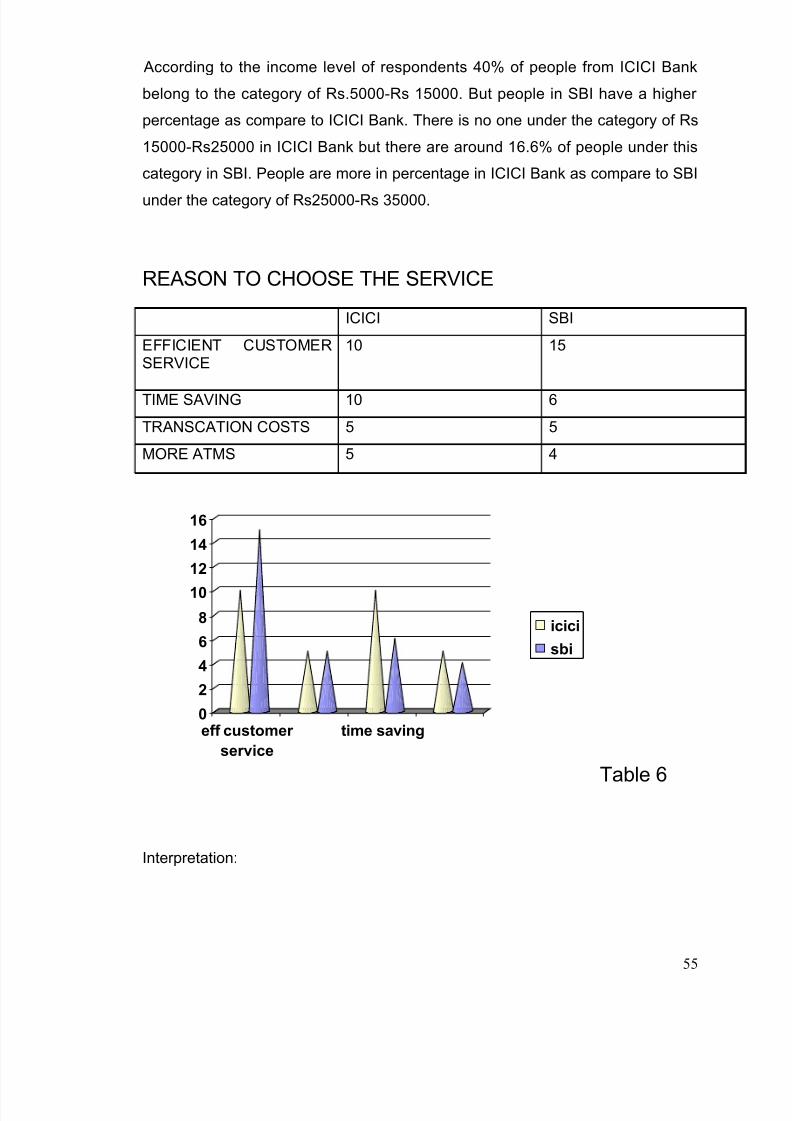

REASON TO CHOOSE THE SERVICE

ICICI SBI

EFFICIENT CUSTOMERSERVICE

10 15

TIME SAVING 10 6

TRANSCATION COSTS 5 5

MORE ATMS 5 4

0

2

4

6

8

10

12

14

16

eff customer

service

time saving

icici

sbi

Table 6

Interpretation:

55

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 56/59

Under the category of efficient customer service category 33.3% of people

belong to ICICI and 50% belong to SBI. Time saving percentage is more in ICICI

as compare to SBI. Transactional cost is same for the two.

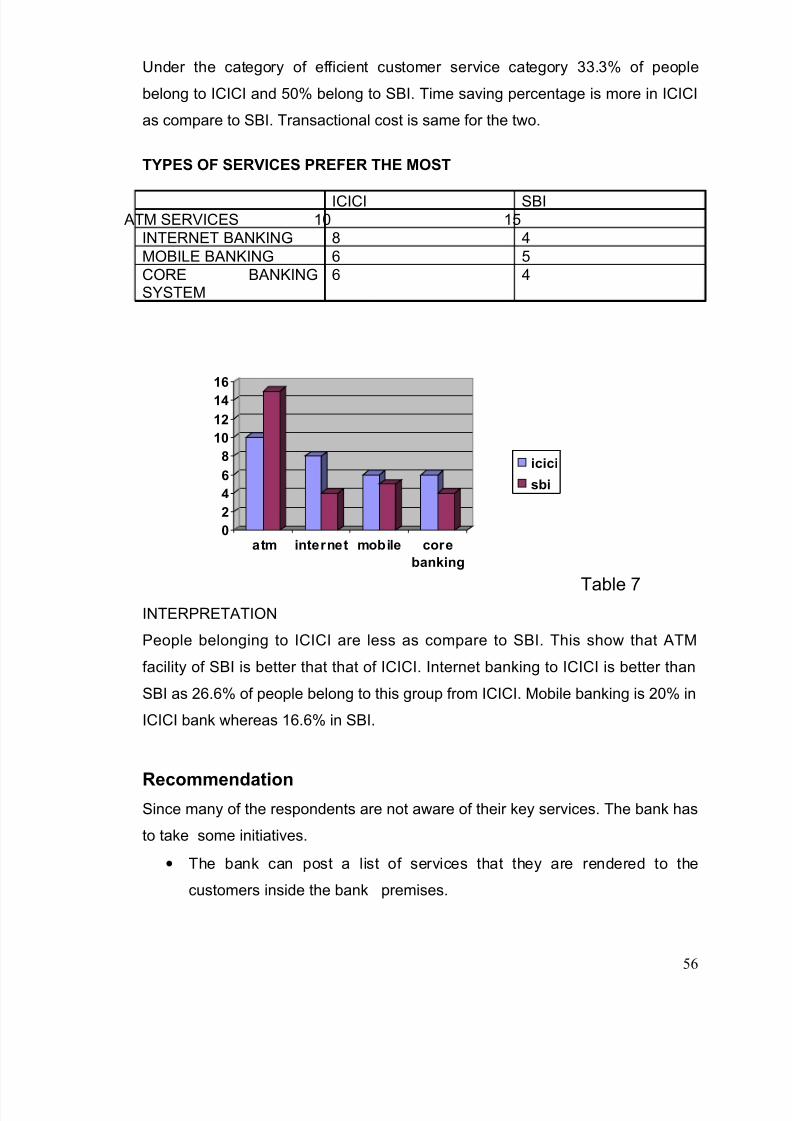

TYPES OF SERVICES PREFER THE MOST

ICICI SBI ATM SERVICES 10 15INTERNET BANKING 8 4MOBILE BANKING 6 5CORE BANKINGSYSTEM

6 4

0

2

4

6

8

10

12

14

16

atm internet mobile core

banking

icici

sbi

Table 7INTERPRETATION

People belonging to ICICI are less as compare to SBI. This show that ATM

facility of SBI is better that that of ICICI. Internet banking to ICICI is better than

SBI as 26.6% of people belong to this group from ICICI. Mobile banking is 20% in

ICICI bank whereas 16.6% in SBI.

RecommendationSince many of the respondents are not aware of their key services. The bank has

to take some initiatives.

• The bank can post a list of services that they are rendered to the

customers inside the bank premises.

56

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 57/59

• And they can post demo of all these services in their bank website.

• They can concentrate more on the respondents are falling under the age

group 25yrs – 35yrs.

• The SBI bank can concentrate on customer complaints handling.

• The bank can also send a post to there customers by informing there

services and how to proceed with that.

Conclusion

From the above calculations and result analysis I can conclude that:

• Table 1 show that ICICI is more popular under the age group of 25yrs-

35yrs but SBI is popular under the age group of above 55 yrs.

• Table 2 shows that ICICI is more popular in female category but SBI is

same in both i.e. male and female.

• Table 3 shows that people with education up to PG are more in both ICICI

and SBI.

• Table 4 give the conclusion that salary class and supervisor class prefer

ICICI more as compare to SBI. It has equal preference with the

professionals but managerial level people prefer more to SBI.

• Table 5 shows that income level of Rs.15000-Rs.25000 gives no

preference no ICICI and income level above Rs.35000 gives less

preference to SBI as compare to ICICI.

• Table 6 shows that the most popular reason for choosing ICICI and SBI is

its efficient customer handling ad time saving but among these two the

preference is more on ICICI.

• Table 7 shows that among all the services provided by the banks the

preference is more on ICICI.

Bibliography

Website

57

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 58/59

• www.icicibank.com

• www.statebankofindia.com

Book:

• Indian Institute of Banking and finance, Banking Products and Services

Questionnaire

Personal details

1. Name:

2. Age:

a) 25yrs- 35 yrs b) 36 yrs - 45yrs

c) 46 – 55 yrs d) above 55 yrs

3. Gender:

a) Male b) Female

4. Educational Qualification:

a) Illiterate b) School

c) UG d) PGe) Professional Course f) Others

5. Occupation:

a) House wife b) Students c) Salaried person

d) Business man e) Professionals f) Supervisor

58

8/2/2019 BANKS1 (1)

http://slidepdf.com/reader/full/banks1-1 59/59

g) Managerial h) pensioner

6.Incomelevel:

a) Rs.5, 000 – Rs.15, 000 b) Rs.15, 001-Rs.25, 000

c) Rs.25, 001- Rs.35, 000 d) Rs.35, 001-Rs.45, 000

e) Above Rs. 45,000

7. In which bank do you have an account?

a) ICICI bank b) SBI bank

8. What is the reason to choose the services of the bank?

a) Efficient customer service b) efficient complaints handling

c) Time saving d) transaction costs e) technology

9. What type of services do you prefer the most?

a) ATM service b) Internet Banking c) Mobile Banking

d) Core banking system