Embed Size (px)

Citation preview

A Tale of Two Crises: The Political Economy of East Asian Finance

in the 1990s and 2000s

Barbara Stallings International Studies Assn

March 2011

Agenda

Introduction Literature and hypotheses Financial policy changes after 1997 Outcomes of policy changes Korea case study China case study Conclusions

Introduction

Crises of 1990s and 2000s were both crucial for East Asia, but their origins and consequences were different

Why no financial crises in EA in 2000s, when finance was main source of crises there in 1990s and elsewhere today?

Two-part study: regional economic analysis and country political economy analysis

Literature and Hypotheses (1)

The 1997 crisis stimulated a new theoretical literature on financial crisis

Previous view: crises caused by loose macroeconomic policy or banking panics that spread

Neither fit the situation in EA in 1990s

New approaches came in two versions

Literature and Hypotheses (2)

Internal explanations for crises

-- Macroeconomic policy errors (over-investment, fixed exchange rates)

-- Financial sector weaknesses (poor regulation and supervision, lack of transparency, imprudent lending)

-- Political improprieties (“crony capitalism,” moral hazard)

Literature and Hypotheses (3)

External explanations for crises

-- Internal issues had existed for a long time without hindering success in EA

-- Real changes were external, following liberalization of capital account

-- Resulting large capital inflows and “sudden stops” led to crisis

Literature and Hypotheses (4)

Hypothesis 1: East Asia suffered both internal and external problems in 1990s; policy changes corrected problems, thus avoiding financial crises in 2008-09

Hypothesis 2: Policy changes came about in different ways in different countries, depending on whether they suffered crises in 1990s or not

Changes after 1997 Crisis (1)

Banking sector

-- Eliminate NPLs from balance sheets

-- Recapitalize banks, sometimes nationalizing them in the process

-- Privatization (or re-privatization) of banks, sometimes to foreign capital

-- Improvement of regulation/supervision

Changes after 1997 Crisis (2)

Capital markets

-- Main focus: promoting bond markets to provide alternative source of finance

-- Various economic reforms were important: financial liberalization, opening capital account, pension reform

-- Institutional reforms: better regulation and supervision, corporate governance

Outcomes of Changes (1)

Asset type 1990 1995 2003 2007

Bank claims 67 87 103 93

Bonds outstanding 30 31 60 61

Stock market 49 95 90 123

Total 146 213 253 277

East Asia: Composition of Domestic Financial Sector, 1990-2007 (% GDP)

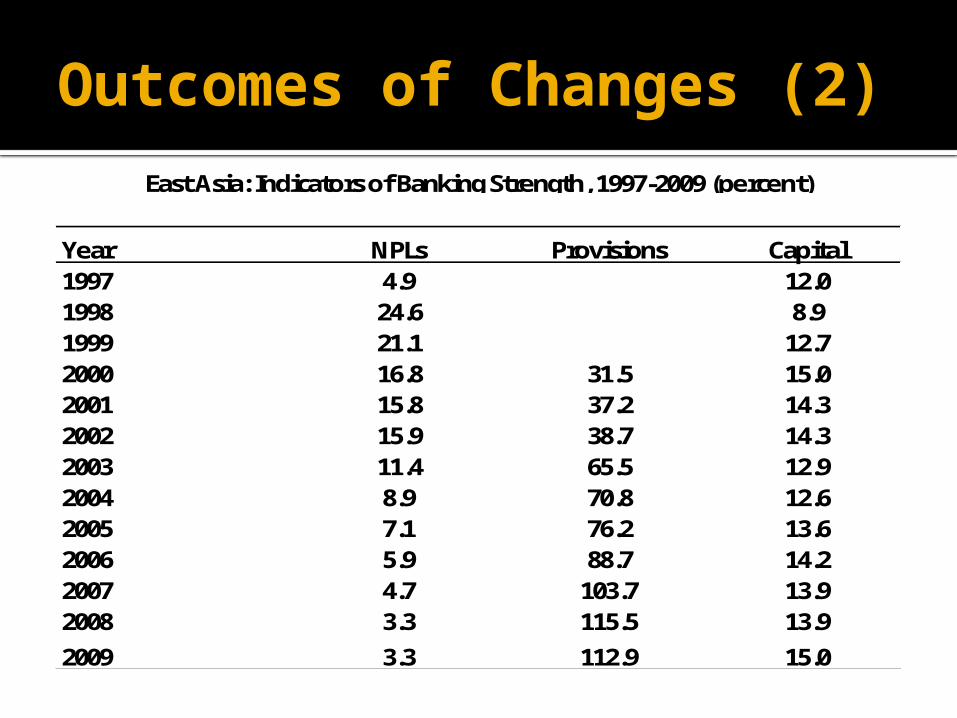

Outcomes of Changes (2)

Year NPLs Provisions Capital1997 4.9 12.01998 24.6 8.91999 21.1 12.72000 16.8 31.5 15.02001 15.8 37.2 14.32002 15.9 38.7 14.32003 11.4 65.5 12.92004 8.9 70.8 12.62005 7.1 76.2 13.62006 5.9 88.7 14.22007 4.7 103.7 13.92008 3.3 115.5 13.9

2009 3.3 112.9 15.0

East Asia: Indicators of Banking Strength, 1997-2009 (percent)

Consequences of Current Crisis

East Asian economies slowed, but recovered quickly through stimulus

Feedback of economic crisis to financial sector? Still early, but some indicators

-- No bank failures

-- Indicators deteriorated, but still strong

-- Stimulus may lead to more NPLs in the future

Korea – 1997 Crisis

Korea’s 1997 crisis resulted from a poorly executed financial liberalization, which led to heavy borrowing, especially short-term

Cutoff of access to international financial markets triggered crisis

Government requested IMF loan in Dec. 1997; it was large but not large enough and poorly designed

Korea – Reforms (1)

After crisis, many banks were closed or taken over by the government and later reprivatized

An asset management company (KAMCO) purchased most NPLs

Regulation and supervision were consolidated; forward-looking approach was adopted

Korea – Reforms (2)

Deposit insurance limits were made clear to avoid moral hazard, and corporate governance and transparency were strengthened

Complete foreign ownership was permitted

Capital markets were a lower priority; similar reforms introduced

Outcomes (1)

Indicators of banking sector strength rose substantially

Both banks and capital markets increased finance to Korean economy, in part as result of policy changes

Economy was hit hard by fall in trade and withdrawal of international finance in 2008, but no crisis like 1997

Outcomes (2)

Year NPLs Provisions Capital1997 5.81998 7.6 8.21999 11.3 10.82000 8.9 10.52001 3.3 10.82002 2.4 10.52003 2.6 84.0 11.12004 1.9 104.5 12.12005 1.2 131.4 13.02006 0.8 175.2 12.82007 0.7 205.2 12.32008 1.1 146.3 12.3

2009 1.5 125.2 14.2

Korea: Banking Strength Indicators, 1997-2009 (percent)

Korea – Reform Process (1)

Several approaches

1) Domination by foreign actors

-- IMF imposed macroeconomic and structural reforms (especially financial opening) on an unwilling Korean government

-- US government was partner, perhaps acting on behalf of US firms

Korea – Reform Process (2)

2) Domination by domestic actors

-- Democratization was key factor, which changed the relative power of political actors in Korea

-- This weakened the executive and led to “western style” reforms

-- IMF as scapegoat, not main actor

Korea – Reform Process (3)

3) Interaction of foreign and domestic actors-- Role of political leadership (President Kim Dae-Jung) in mediating domestic and external pressures-- Kim persuaded labor to accept reforms-- Foreign actors played specific roles: pressed for recognition of NPLs, financial institution reforms, corporate reforms

China – No Crisis in 1997

China escaped crisis in 1997 because financial sector was still largely closed; no international borrowing binge as in other East Asian countries

Growth slowed, which was met with stimulus but no devaluation

Saw neighbors’ crisis as a call for reform in China itself

China Reforms (1)

Reforms moved in similar direction as Korea’s, but did not go as far

AMCs were created to clean up problem loans in major banks

Major banks were recapitalized several times

Improved regulation/supervision (CBRC)

China Reforms (2)

Increased role of foreign capital-- Foreign banks purchased small shares of several Chinese banks

-- IPOs in Hong Kong by largest state-owned banks

-- “Strategic investors”

-- But significant barriers remain for foreign ownership

Outcomes (1)

Like Korea, banking strength indicators in China rose significantly

China’s banks became increasingly oriented toward the corporate sector, although bond markets used mainly by government

Stimulus funneled through banks was key to quick recovery in China in 2009

Outcomes (2)

Year NPLs Provisions Capital2000 22.4 4.7 13.52001 29.8 5.2 12.32002 25.5 5.3 11.22003 20.4 19.7 -5.92004 13.2 14.2 -4.72005 8.6 24.8 2.52006 7.1 34.3 4.92007 6.2 39.2 8.42008 2.4 116.4 12.0

2009 1.6 155.0 10.0

China: Banking Strength Indicators, 2000-2009 (percent)

China – Reform Process (1)

Dominance by domestic actors is usually assumed by China scholars

CCP as ultimate source of decisions Political leadership seen as important,

especially role of Premier Zhu Rongji, but several variants re financial reform

-- Zhu pursuing ideological agenda

-- Zhu fighting for political survival

China – Process (2)

New literature suggests that external forces are also important in Chinese policy making

-- International structural constraints

-- Internalization of international norms Case study of international role –

explaining WTO accession, which is important for financial sector

Conclusions (1)

Support found for both hypotheses about political economy of finance in East Asia

Region did not have financial crises in 2008-09 (as opposed to serious economic problems) because of strengthening of financial sector after 1997 crisis

Different processes of policy change in crisis and non-crisis countries in 1997

Conclusions (2)

Despite support for the two hypotheses, there are some interesting caveats

Problems were created, as well as resolved, in cleaning up banks

Government role seems to have increased because of crisis

Both foreign and domestic actors can play a significant role; interaction is important