Embed Size (px)

Citation preview

Barnes Group Page 1

Barnes Group Equity and Valuation Analysis Victor Hemmati [email protected]

Michael Randell [email protected]

Travis Monk [email protected]

Taylor Pettigrew [email protected]

Barnes Group Page 2

Table of Contents

Executive Summary .......................................................................................... 6

Industry Analysis .......................................................................................... 6

Accounting Analysis ....................................................................................... 7

Financial Analysis, Forecasting Financials, and Cost of Capital Estimations .................... 8

Business and Industry Analysis ............................................................................ 10

Business Overview........................................................................................ 10

Industry Overview ........................................................................................ 12

Five Forces Model ........................................................................................... 14

Rivalry Among Existing Firms ........................................................................... 15

Concentration .......................................................................................... 17

Degree of differentiation and Switching Costs ................................................... 19

Economies of Scale .................................................................................... 22

Exit barriers ............................................................................................ 23

Excess capacity ........................................................................................ 24

Industry Growth ....................................................................................... 26

Threats of New Entrants ................................................................................ 29

First mover advantage ................................................................................ 29

Distribution access and relationships .............................................................. 31

Legal Barriers .......................................................................................... 33

Threat of Substitute Products .......................................................................... 34

Bargaining Power of Customers ........................................................................ 36

Bargaining Power of Suppliers ......................................................................... 37

Key Success Factors ........................................................................................ 39

Cost Leadership .......................................................................................... 40

Economies of Scale and Efficient Production ..................................................... 40

Tight cost control systems: capability ............................................................ 41

Differentiation ............................................................................................ 42

Superior quality ........................................................................................ 43

Superior Customer service ........................................................................... 43

Barnes Group Page 3

Firm Competitive Advantages .......................................................................... 44

Tight cost control systems ........................................................................... 44

Superior customer service ........................................................................... 45

Accounting Analysis ......................................................................................... 45

Key Accounting Policies ................................................................................. 46

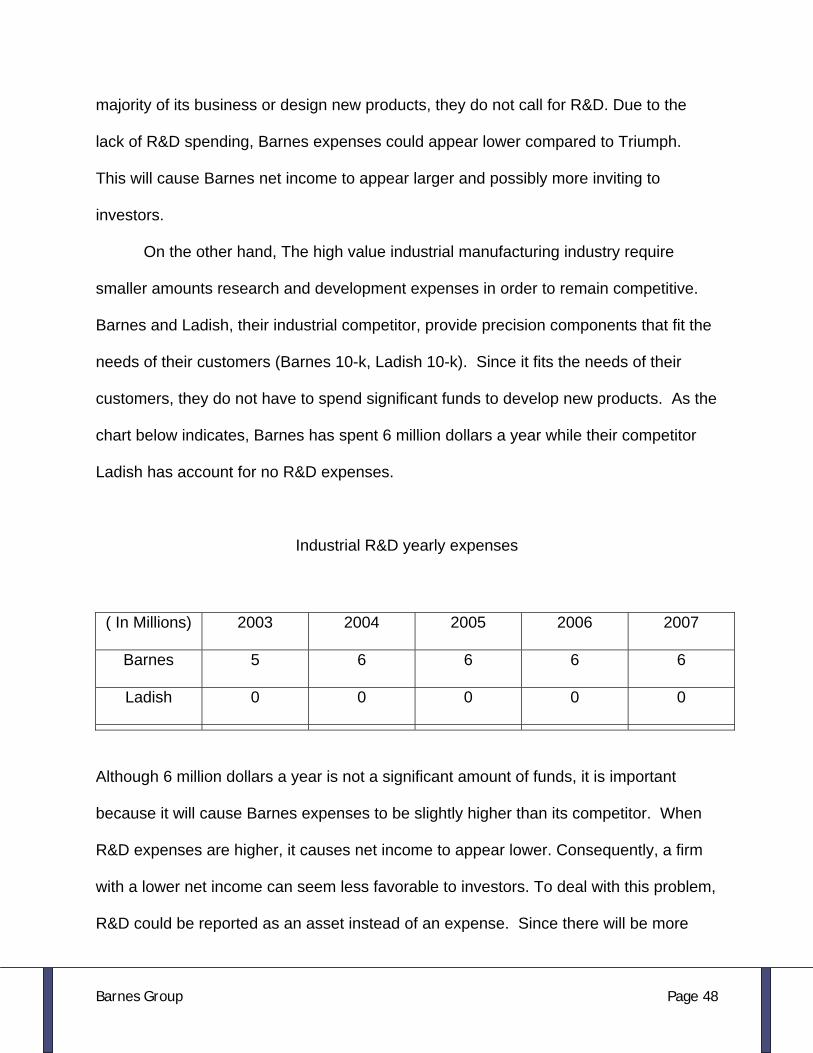

Research and Development .......................................................................... 47

Currency ................................................................................................ 49

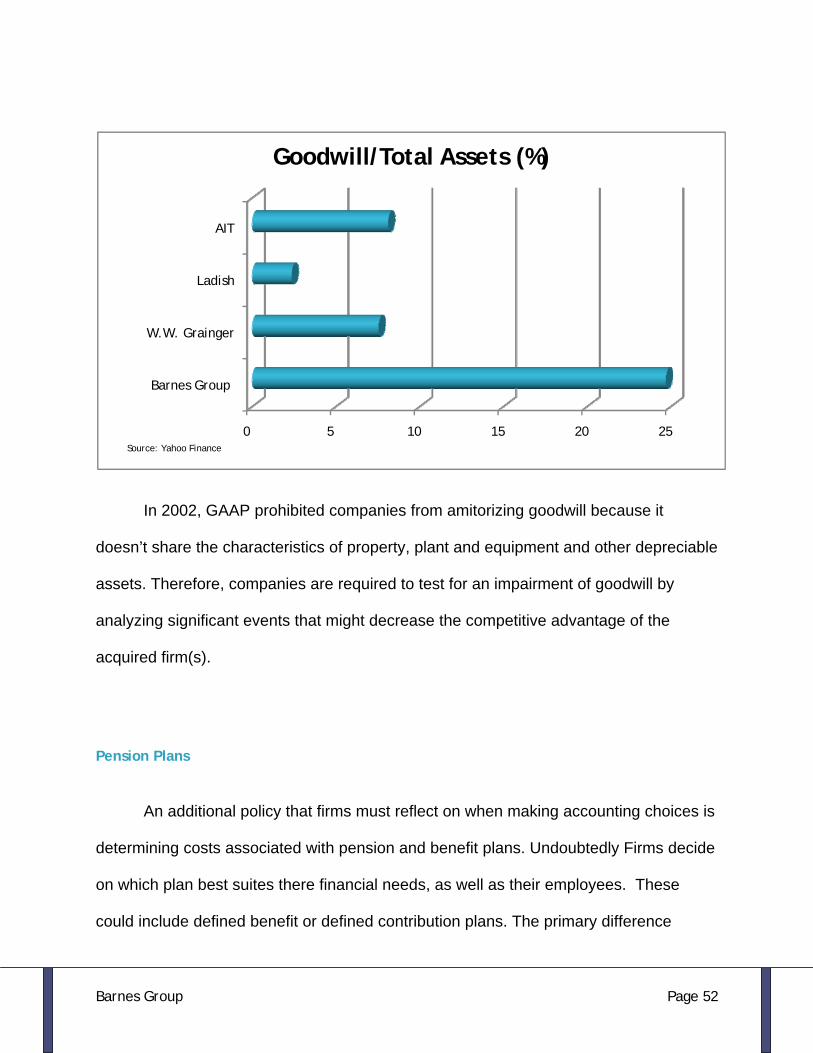

Goodwill ................................................................................................ 49

Pension Plans ........................................................................................... 52

Currency ................................................................................................ 53

Revenue Sharing Programs ........................................................................... 54

Flexibility in Accounting ................................................................................ 55

Research and Development .......................................................................... 55

Currency ................................................................................................ 56

Goodwill ................................................................................................ 57

Pension Plans ........................................................................................... 57

Revenue sharing programs ........................................................................... 58

Evaluate Actual Accounting Strategy ................................................................. 59

Research and Development .......................................................................... 59

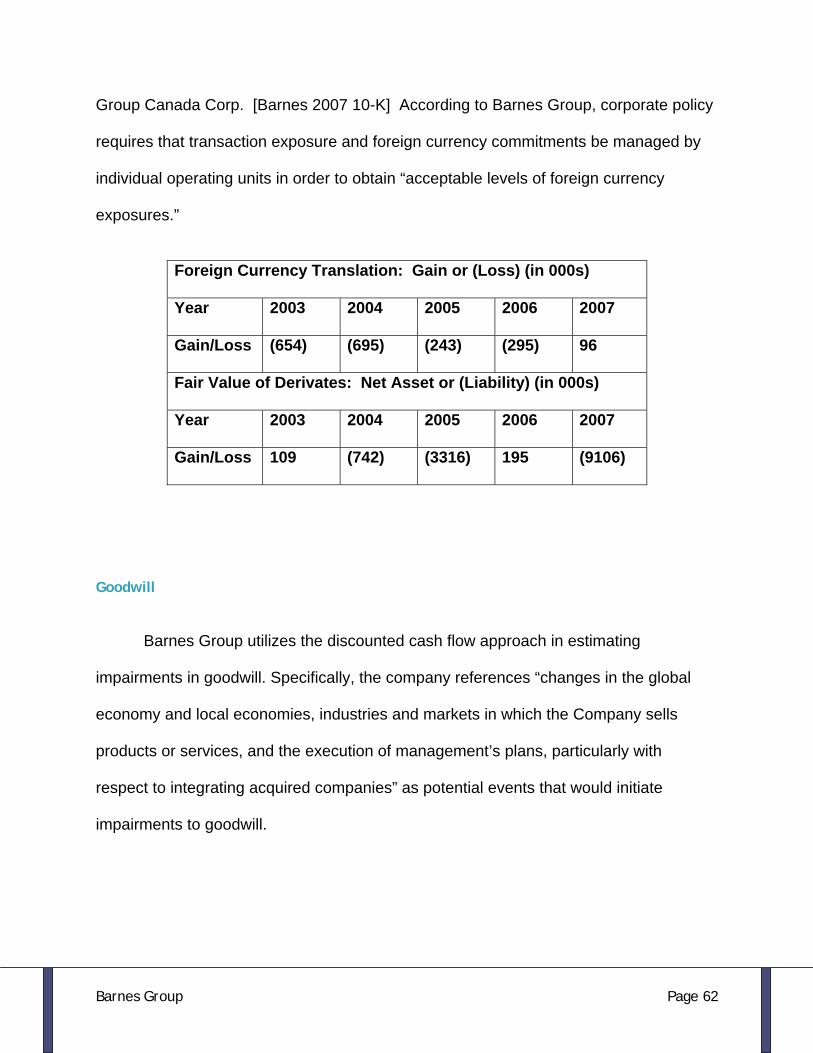

Currency ................................................................................................ 60

Goodwill ................................................................................................ 62

Revenue sharing programs ........................................................................... 63

Disclosures ................................................................................................ 64

Research and Development .......................................................................... 64

Currency ................................................................................................ 65

Goodwill ................................................................................................ 65

Pension Plans ........................................................................................... 66

Revenue Sharing Programs ........................................................................... 66

Quantitative Analysis ................................................................................... 67

Sales Manipulation Diagnostics ...................................................................... 68

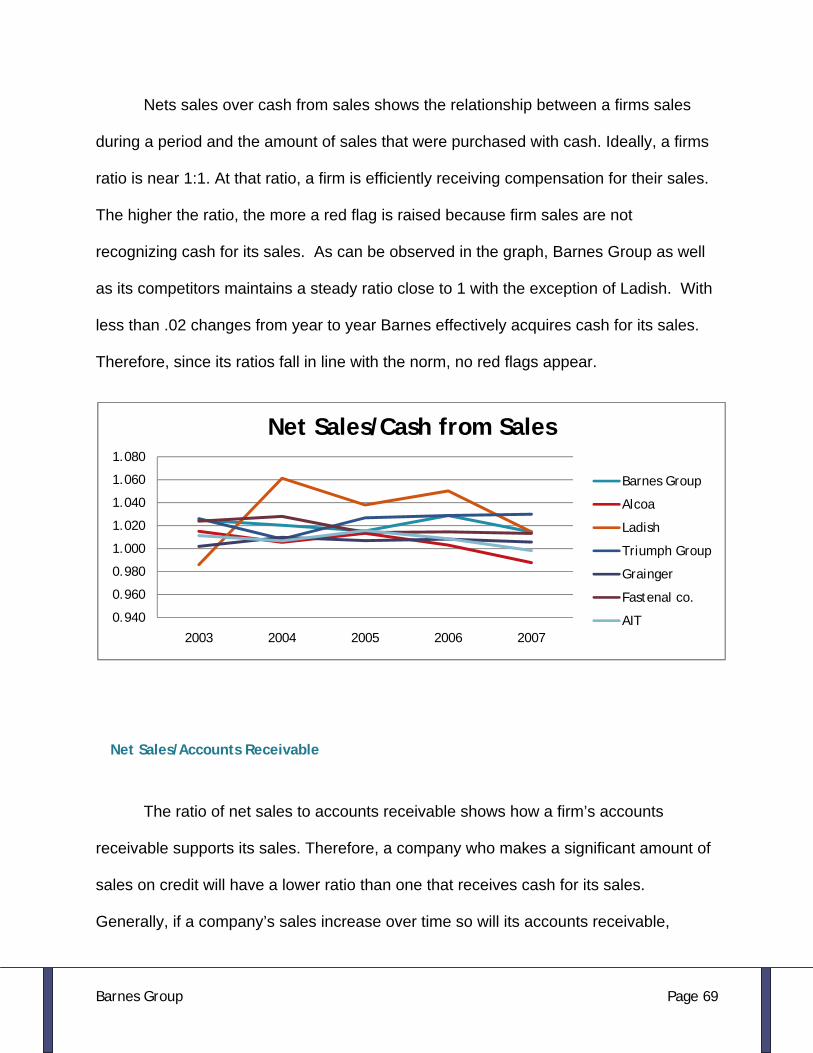

Net Sales/Cash from Sales ........................................................................ 68

Net Sales/Accounts Receivable ................................................................. 69

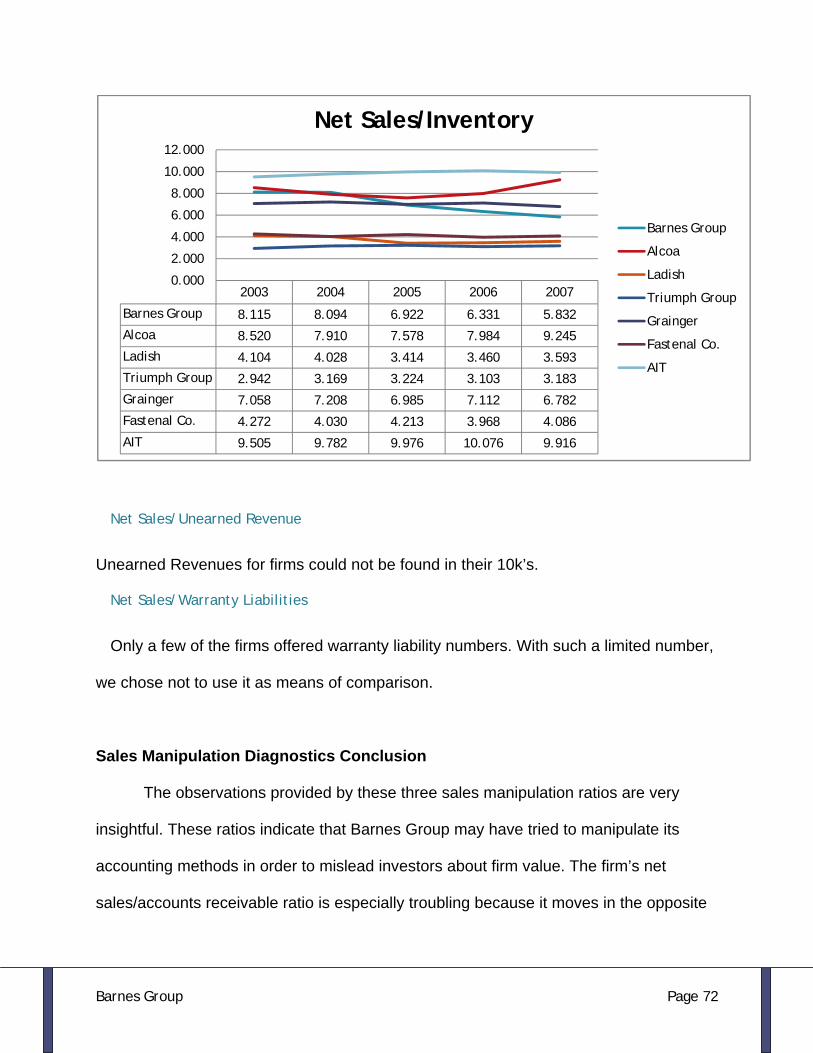

Net Sales/Inventory ............................................................................... 70

Barnes Group Page 4

Net Sales/Unearned Revenue ..................................................................... 72

Net Sales/Warranty Liabilities .................................................................... 72

Expense Manipulation Diagnostics .................................................................. 73

Asset/Turnover ..................................................................................... 73

CFFO/OI .............................................................................................. 74

CFFO/NOA ........................................................................................... 75

Total Accruals/Change in Sales................................................................... 76

Financial Analysis, Forecast Financials, and Cost of Capital Estimation ........................... 78

Financial Analysis ........................................................................................ 79

Liquidity Ratio Analysis ............................................................................... 79

Current Ratio ....................................................................................... 80

Quick Asset Ratio .................................................................................. 81

Working Capital Turnover ........................................................................ 82

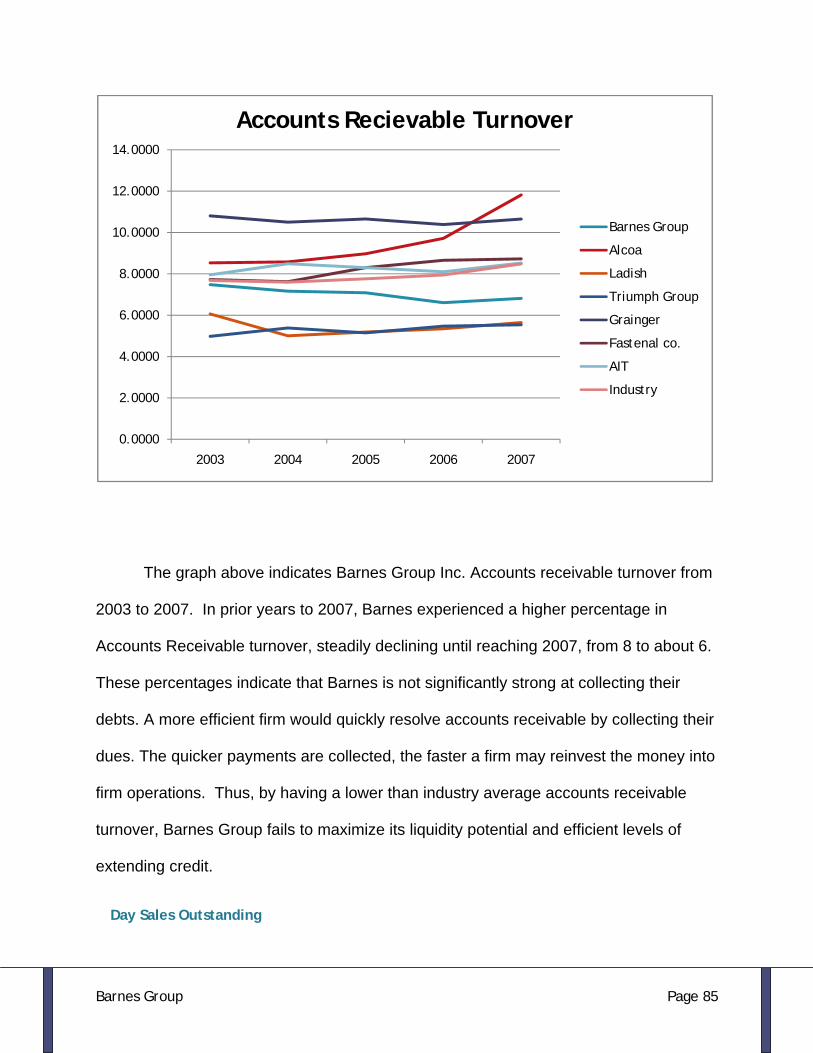

Accounts Receivable Turnover ................................................................. 84

Day Sales Outstanding ............................................................................ 85

Inventory Turnover ............................................................................... 87

Days Supply Inventory ............................................................................ 89

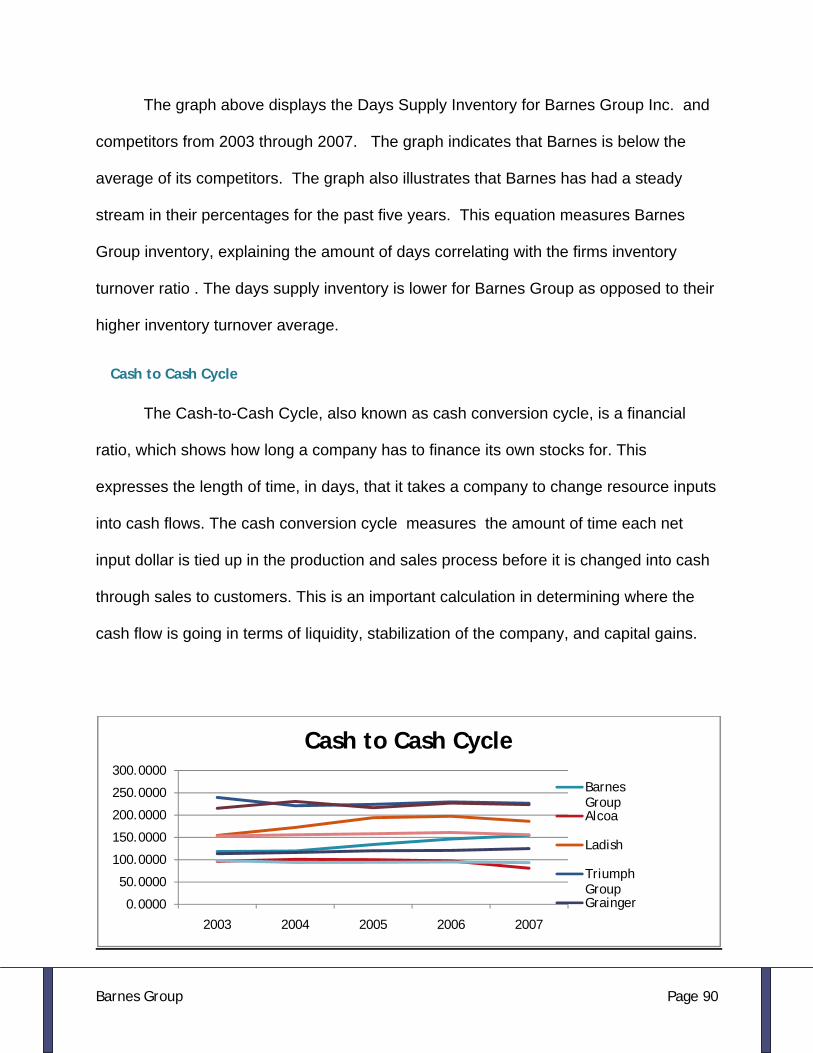

Cash to Cash Cycle................................................................................. 90

Profitability Ratio Analysis ........................................................................... 91

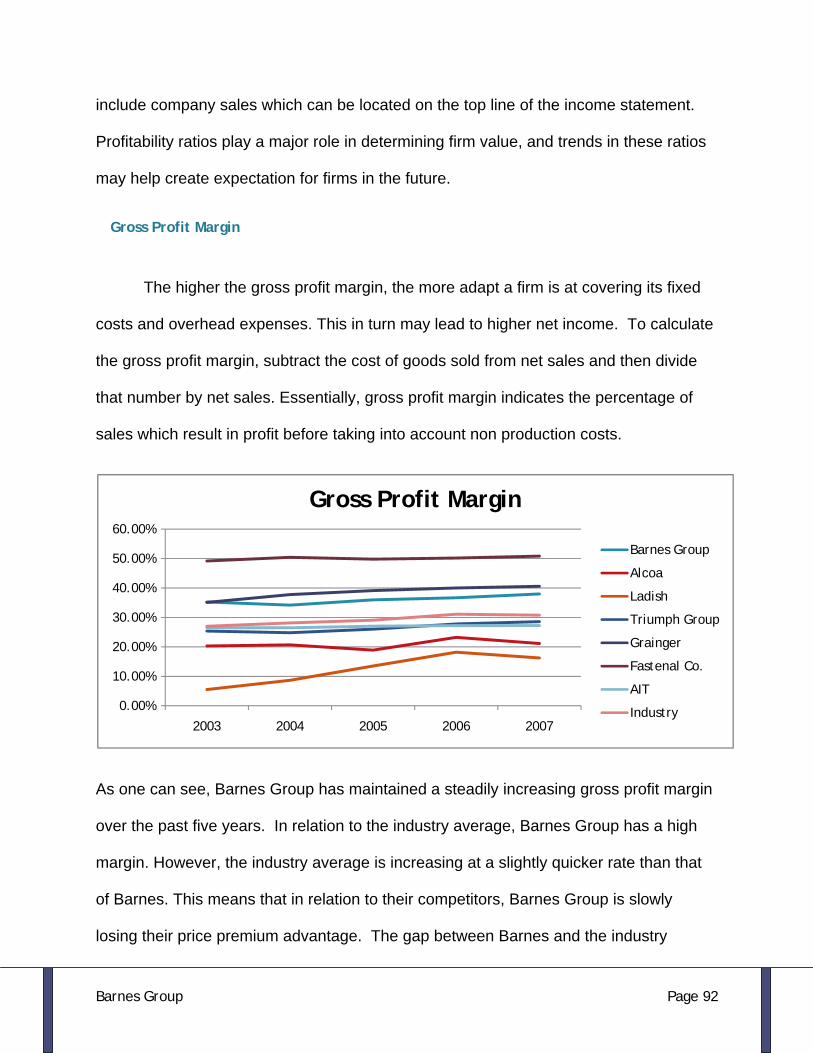

Gross Profit Margin ................................................................................ 92

Operating Expense Ratio ......................................................................... 93

Operating Profit Margin .......................................................................... 94

Net Profit Margin ................................................................................... 95

Asset Turnover ..................................................................................... 96

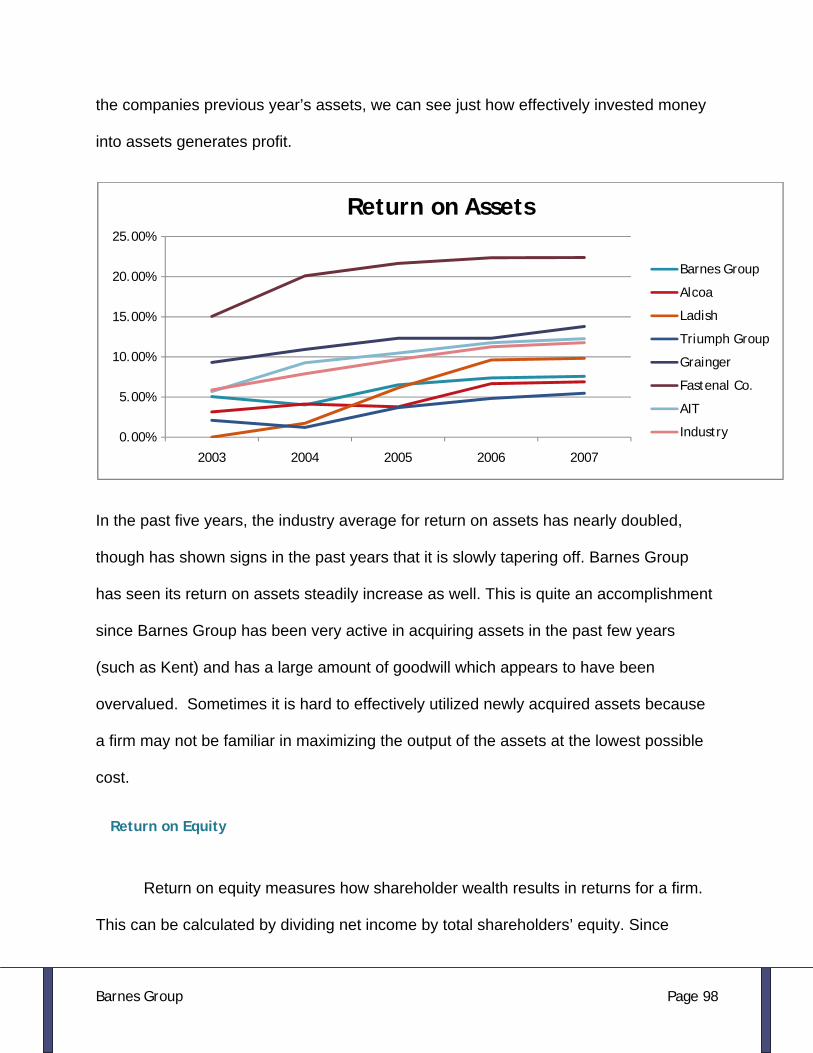

Return on Assets ................................................................................... 97

Return on Equity ................................................................................... 98

Firm Growth Rate Ratios ............................................................................. 99

Internal Growth Rate ........................................................................... 100

Sustainable Growth Rate ....................................................................... 101

Capital Structure ratios ............................................................................ 103

Debt to equity ratio .............................................................................. 103

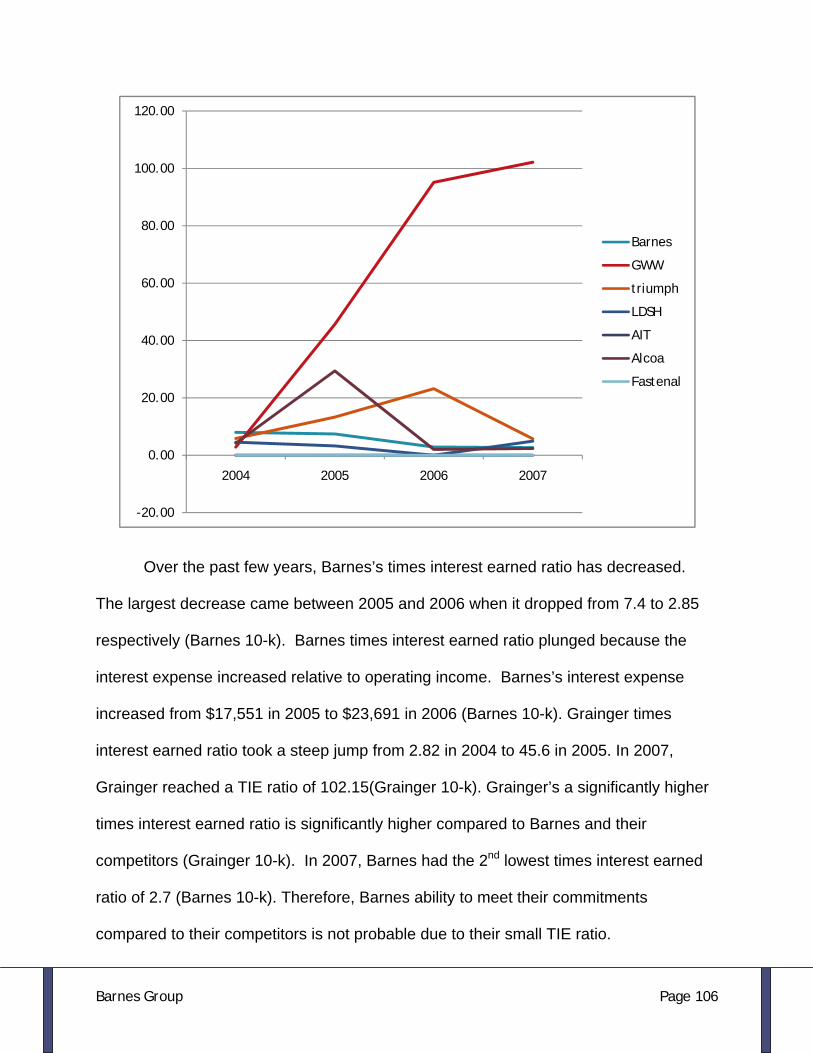

Times interest Earned ........................................................................... 105

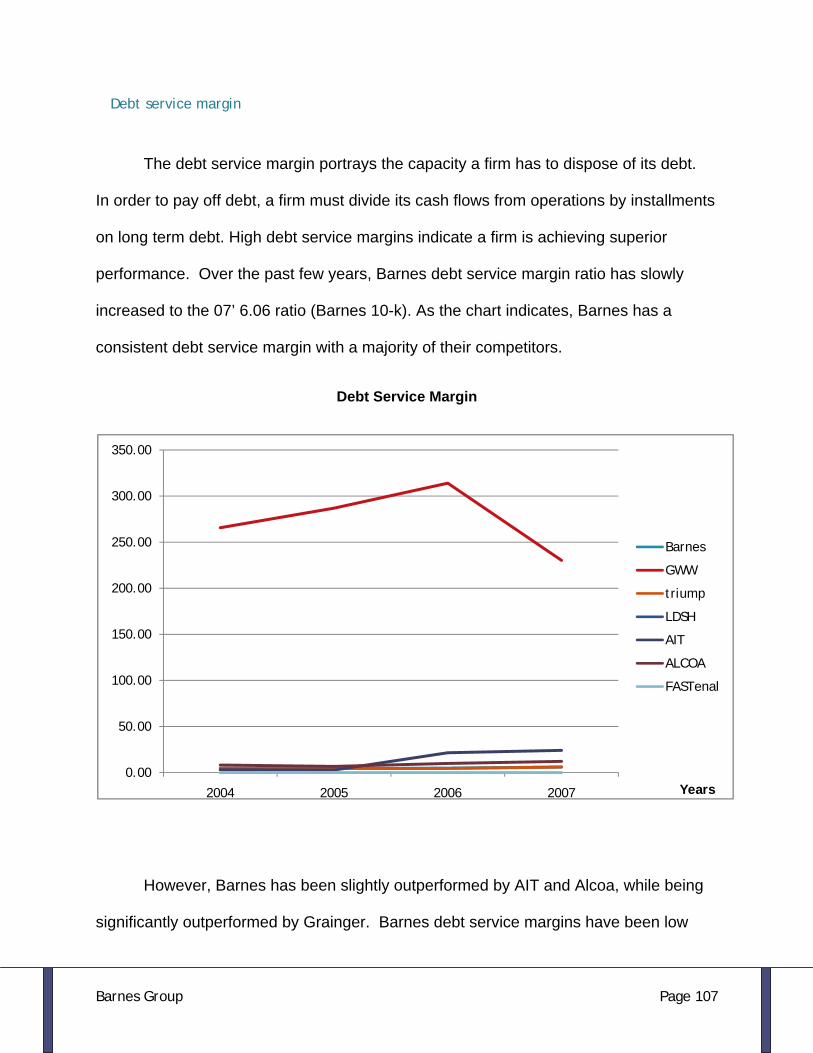

Debt service margin .............................................................................. 107

Barnes Group Page 5

Cost of Capital .......................................................................................... 108

Weighted average cost of debt ................................................................... 108

Altman Z-score ....................................................................................... 109

Cost of Equity ........................................................................................ 112

Weighted Average Cost of Capital (WACC) ...................................................... 114

Forecasting .............................................................................................. 115

Balance Sheet ........................................................................................ 116

Income Statement ................................................................................... 117

Statement of Cash-Flows ........................................................................... 117

Sales Growth ......................................................................................... 118

Profitability .......................................................................................... 120

Method of Comparables ............................................................................... 121

Price/Earnings Trailing ............................................................................. 122

Price/Book ............................................................................................ 123

Price to Earnings Growth ........................................................................... 124

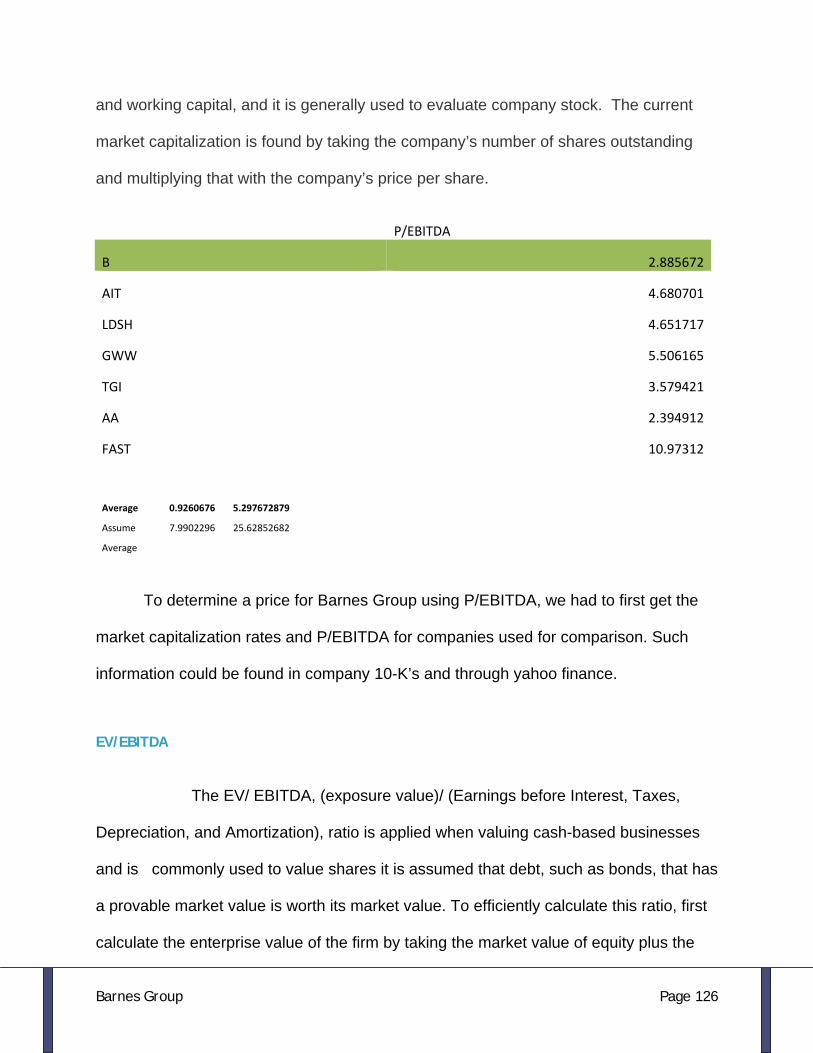

Price over EBITDA ................................................................................... 125

EV/EBITDA ............................................................................................ 126

Price to Free Cash Flows ........................................................................... 127

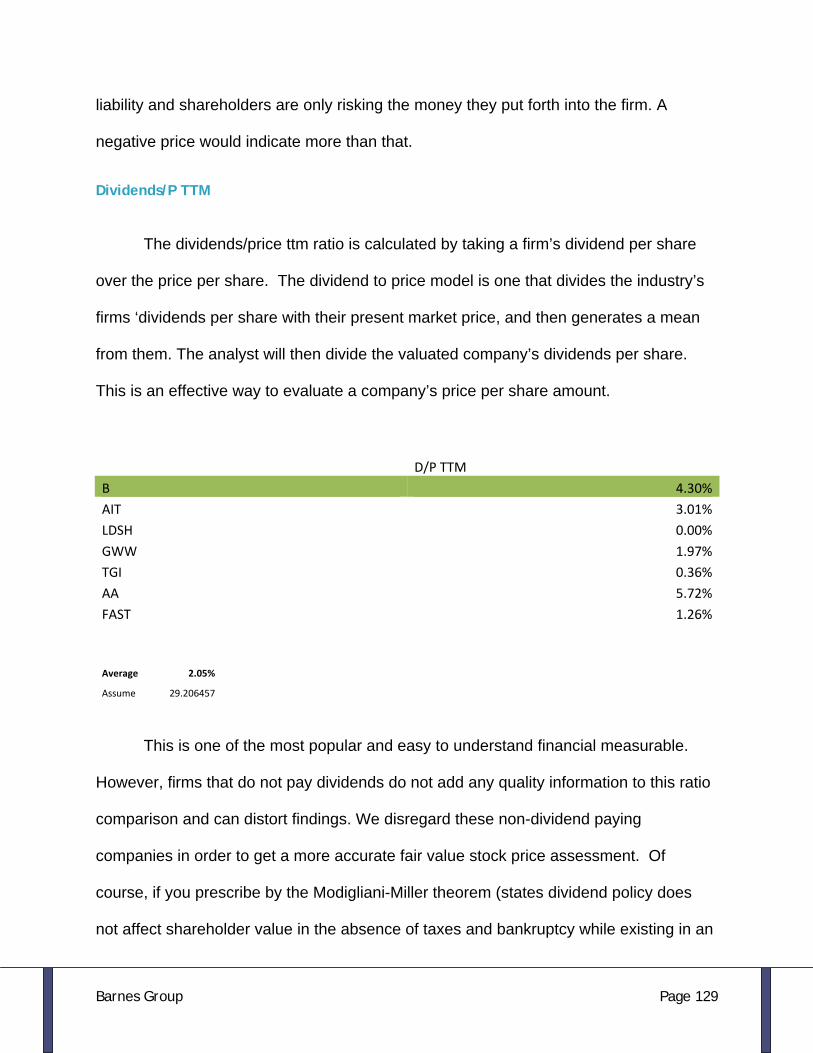

Dividends/P TTM .................................................................................... 129

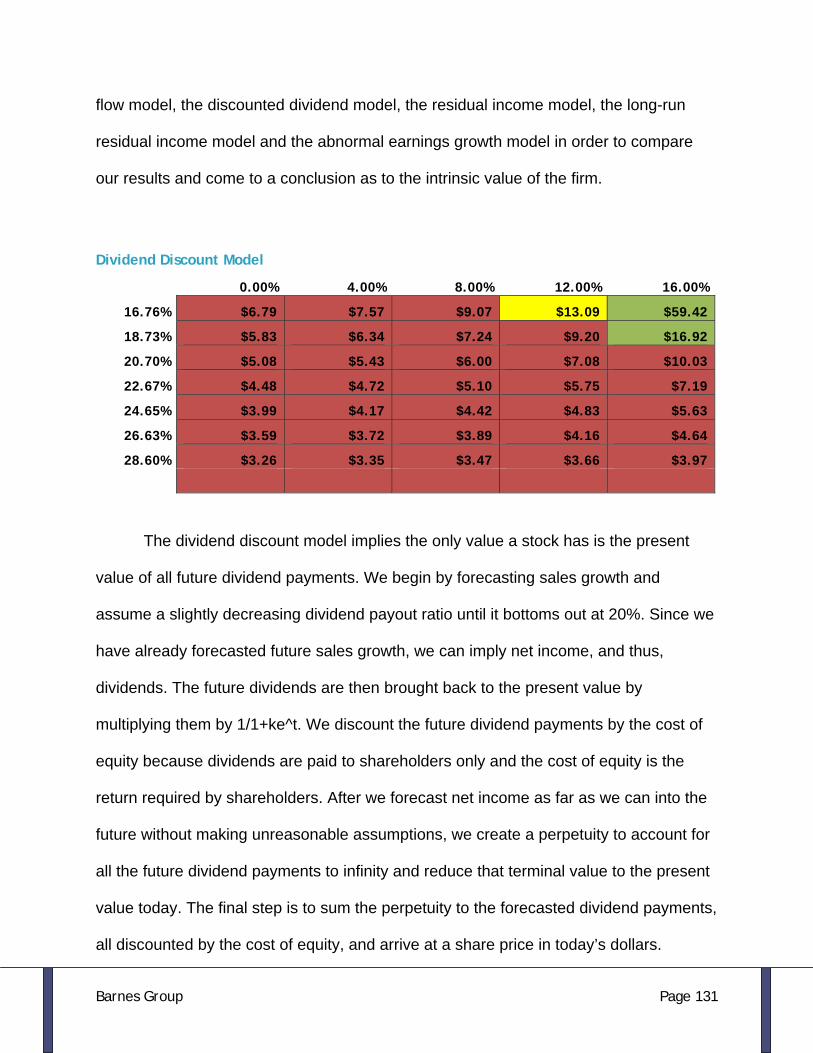

Intrinsic Valuation Models ............................................................................ 130

Dividend Discount Model ........................................................................... 131

Free cash flow model ............................................................................... 132

Residual income model ............................................................................. 133

Recommendation ....................................................................................... 134

Appendices ................................................................................................. 134

Sales Manipulation Diagnostics Tables .............................................................. 134

Expense Manipulation Diagnostics Tables .......................................................... 135

Liquidity Tables ........................................................................................ 136

Profitability Ratio Tables ............................................................................. 138

Growth Rates/Z-Score Tables ........................................................................ 140

Capital Structure Ratio Tables ....................................................................... 141

Barnes Group Page 6

Executive Summary

Industry Analysis

Barnes Group Inc., founded in 1857, has become a diversified leader in

engineering and manufacturing precision metal components and an industrial distributor

of maintenance, repair, operating and production supplies. Today, Barnes Group

consists of three segments - Barnes Aerospace, Barnes Distribution and Barnes

Industrial - in more than 65 locations throughout the world with nearly 6,500 dedicated

employees working towards its success (Barnes Group Inc.)

Barnes Group Inc. has six main competitors within their three segmented

industries: Alcoa Aerospace, Ladish, Triumph Group, Grainger, Fastenal Co., and

Lawson Products. Alcoa Aerospace, Ladish, and Triumph Group all compete in the

aerospace/industrial segment industry with Barnes group while Grainger, Fastenal Co.

and Lawson Products contend with the distribution segment of Barnes’ industry. These

firms manufacture similar products, which challenges Barnes Group to continually press

upon its competitive advantages in order to maintain and even gain market share.

When inspecting Barnes Group Inc. Aerospace/Industrial segment, their

competition is relatively high, yet not as stern as the distribution segment because

products in the aerospace segment in particular are precision machined and fabricated

components for original equipment manufacturer (OEM) turbine, airframe and industrial

gas turbine builders. This means that competitors are creating close, but not quite

indistinguishable products. Thus, competition has its limit. The distribution segment, on

the other hand, has an extremely high level of competition among existing rival firms.

Barnes Group Page 7

The model below explains the analysis of the five forces model which gives an idea of

the level of competition in each segment of Barnes’ Industries:

Barnes Aerospace/Industrial Competitive Force Degree of Competition Rivalry Among Existing Firms High Threat of New Entrants High Threat of Substitute Products Low Bargaining Power of Customers Low Bargaining Power of Suppliers High

Barnes Distribution Competitive Force Degree of Competition Rivalry Among Existing Firms High Threat of New Entrants High Threat of Substitute Products High Bargaining Power of Customers High Bargaining Power of Suppliers Low

Accounting Analysis

Annual 10K reports provided by firms allow us to compare firms based on their

financial statements. These financial reports offer keen insight into the productivity of a

given company. It’s imperative that an analyst be able to establish correlations between

a firm’s key success factors and their core accounting policies. Furthermore, identifying

the level of disclosure presented in these accounting methods helps present red flag

possibilities. Ideally, companies would disclose all of their financial information in a

constant manner from period to period. However, they often find ways to manipulate

their statements in order to appease corporate agendas and only disclose SEC required

Barnes Group Page 8

information. With this in mind, shareholders must be extra cautious when observing

financial statements as they much too often do not tell the whole story.

Barnes Group appears to take its financial disclosing responsibility to investors

seriously. Irregularities in financial information do not exist, and the impact of

acquisitions and goodwill can be directly linked to other aspects of the balance sheet in

the same year. The company expenses its research and development costs; however,

these costs are minimal in relation to competitors which makes it easier to validate the

firm’s worth . Although goodwill is high, its appears to be credible and not overstated.

Firms will often impair goodwill to overstate their assets. A red flag that does arise

comes in methods of the firm’s “participation” fees which are recorded as a long-lived

intangible asset. The manipulation of the amortization of this intangible asset, the

forecasted sales revenue, and the expected life of the project allows managers to

“massage” the revenue process and allows significant flexibility in future reporting.

Thus, Barnes Group go beyond the SEC’s minimum GAAP standards. While a

few disclosure issues do present themselves (valuing RSP contracts), an investor can

feel assured they are gaining a quality understanding of the firm’s financial situation.

Currency financial data, which is particularly important to global companies such as

Barnes Group, can be easily obtained in the 10K. That being said, we would like Barnes

Group to address some of their unclear disclosing practices.

Financial Analysis, Forecasting Financials, and Cost of Capital Estimations

Barnes Group Page 9

By formulating ratios from information provide in a firm’s 10K reports, we may

gain a better understanding of the firm’s financial position. Specifically, a good grasp

on the firm’s liquidity and profitability may be gained. Capital structure especially

can have a large impact on profit. Once we gain an understanding of these ratios, we

can forecast out future financial statement data. Additionally, with this financial

information we can calculate our WACC, or weighted average cost of capital. Those

who make decisions for a company often look to WACC to decide if a new project is

feasible. To be worthwhile, the return on a project must be higher than WACC.

Otherwise the firm will not be able to meet its obligations to bondholders and

shareholders.

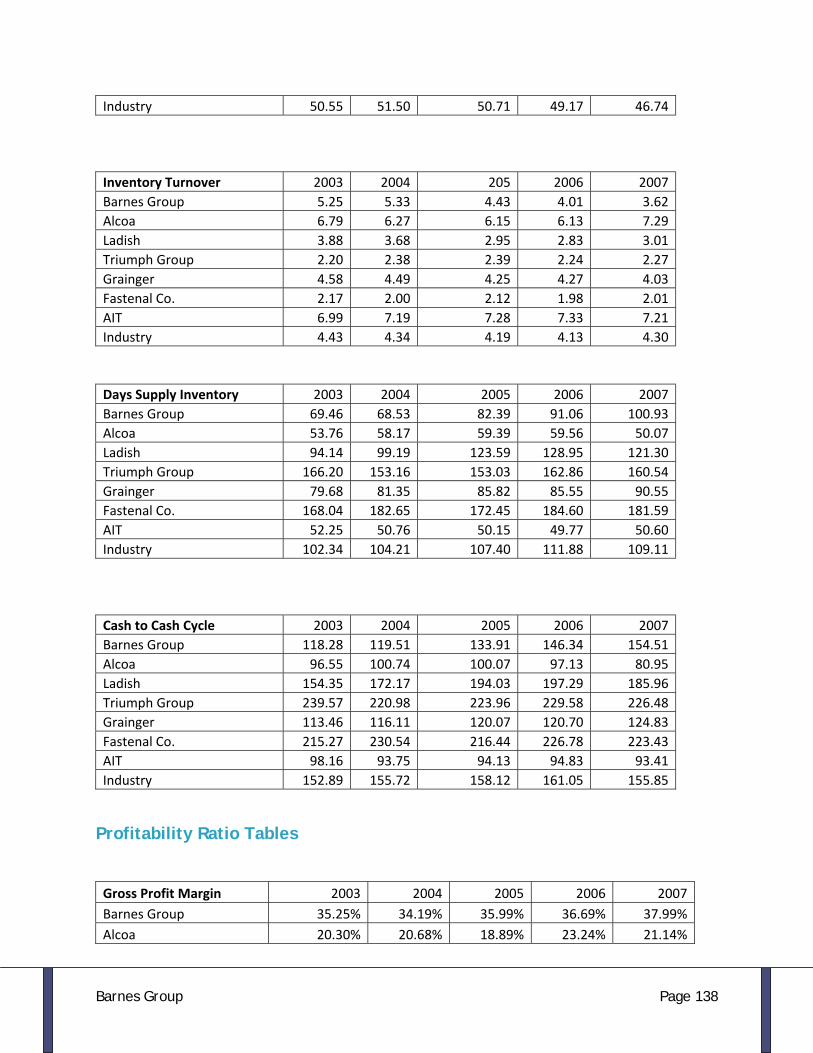

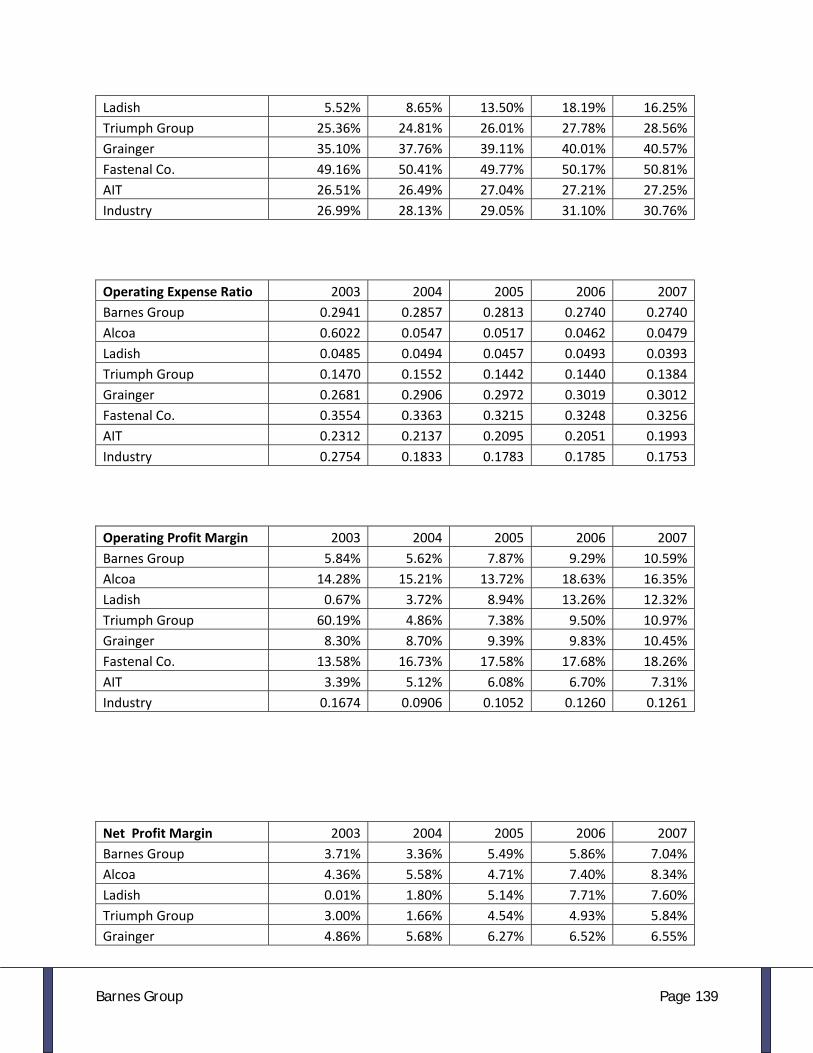

Financial Ratios for Barnes Group reveal several alarming trends. From 2003-

2007 the company has remained well below the industry average in terms of liquidity.

These could be detrimental in a scenario in which a large debt obligations must be

quickly met. One explanation for this is the firm’s poor pursuit of their credit sales.

In comparison to similar firms, Barnes does not collect on payments as efficiently.

However, it should be noticed (as several ratios indicate) that Barnes Group slowly is

making process in managing their inventories which indicates they adequately sell the

products they manufacture in a relatively short time span.

Barnes Group Page 10

Business and Industry Analysis

Business Overview

Barnes group Inc. is a highly productive and successful corporation founded in

the year 1857 by Wallace Barnes in Bristol Connecticut. Barnes Group Inc has an

extensive background of creating innovative and technological developments in

Aerospace, manufacturing, and distribution. What began as a mere local metal parts

shop in Bristol, Connecticut, has progressed to become a primary leader in

manufacturing and engineering precision metal components. Barnes group also strives

as an industrial distributor of a wide range of maintenance, repair, operating and

production supplies.

Barnes Group is segmented into three main business categories, two of which

are primarily intertwined in productivity: the Distribution division, and the

Industrial/Aerospace Division. These segments have more than 6,500 employees, and

are branched out to more the than 65 different locations around the globe. With these

competitive forces in their favor, Barnes Group Inc. was one of the leading producers in

each of its industries.

The Barnes Aerospace Division is the more recent division, which specializes in

precision engineered components for original equipment manufacturer (OEM) turbines.

OEM accounts for 67% of this segment. The corporation also provides jet engine

component overhaul and repairs services for a large portion of the world’s military

applications and commercial airlines. These are considered aftermarket products and

Barnes Group Page 11

account for 33% of the aerospace segment. Although Barnes’s aerospace division

accounts for only 29% of the firm’s total revenue, the segment produces 45% of the

firms total profit. The products and services accounted for $91.2 million in net sales in

2007, and have increased to $112.3 million in net sales in 2008. Barnes Group’s

Aerospace division includes a variety of core competencies. The High Temperature

Alloy dept. specializes in precision machining, numerous types of gear designs, and

advanced fabrications. The Engineering sector identifies new product introduction,

concurrent design, and cost reduction.

The Barnes Industrial Division is an industrial components manufacturer of a

large range of highly integrated set of engineered products for an assorted customer

base. These custom solutions include precision forming, nitrogen gas based products,

retention rings, engineered stampings and springs, injected molded plastic-on-metal

components, and custom assemblies (Barnes group inc.) These products are designed

to gather all customer necessities in applications including general industrial, medical

devices, consumer home products, and transportation. This segment accounts for 35%

of the revenue and 41% of the profit of the firm. The Industrial division accounts for 130

million dollars in net sales in 2007 and has increased 135.6 million in net sales for the

2008 year, making their industrial division one of the top industrial manufacturers

worldwide.

The Distribution Division of Barnes Group is a full service distributor of repair,

maintenance, and production supplies. There are acknowledged as a market leader in

the vendor-managed inventory throughout parts of Europe and North America. The

industry provides an assortment of high-volume class-c distribution replacement parts.

Barnes Group Page 12

These class-c parts are essentially less than 25 dollars per item and make up 50% of

the firms distribution. Also, this division consists of 30% of medium volume, class-b

parts. These products range from 25 dollars to 200 dollars per item. Lastly, 20% of

Barnes distribution is involved in low volume, class-a products. Class-a items price

above 200 dollars an item. With nearly 2,000 sales employees, the distribution segment

of Barnes Group Inc. is seemingly set to increase higher and higher in productivity. This

segment accounts for 36% of the firm’s revenue. Sales accounted for approximately

139.8 million dollars in 2007, and have undoubtedly increased to 141 million for 2008.

Although distribution accounts for a large amount of the firms sales, it only produces

14% of the firm’s profit. This flexible service approach makes the Barnes Distribution

segment the optimum provider for maintenance, repair, operating and production

(MROP) needs.

Industry Overview

The precision industrial manufacturing, aerospace and industrial distribution

industries have changed dramatically over the last decade as a result in advances in

computer and information technology. As a result, the activities that drive value for a

competitive firm are more complex and require greater consideration of customer needs

than ever before. As cost reduction and consolidation impacted the industrial distribution

industry, firms evaluated ways to drive value for their customers by assuming core

business activities taking what was once an adversarial relationship and transforming it

into a collaborative one.

Barnes Group Page 13

Industrial distribution firms are now expected to develop and manage inventory

systems and schedules that work within a framework defined by their customers. They

must act as business partners, not just affiliated businesses. The integration of

enterprise resource planning systems has enabled customers to search for the best

possible price among distributors, driving their profit margins lower, while

simultaneously integrating distributors and allowing them to fulfill additional functions

and add value where they once were not present, creating an entirely new business

model. This new symbiotic relationship has defined the recent history of the industrial

distribution industry while allowing customers to focus on what drives value for their

particular firm.

In the precision industrial manufacturing industries as well as the aerospace

industries, computer aided design and advanced modeling algorithms have enabled all

firms to innovate their manufacturing process to obtain a competitive advantage beyond

simple economies of scale. The commoditization of software tools like computer aided

design software (CAD) have shaken the large firms in the industry by allowing smaller

firms to incorporate complex and extensive design functions while also designing

complementary manufacturing processes. No longer do the largest firms have a

monopoly on creative talent simply because they have the resources to foster it.

In conclusion, the extensive uses of information technology and computer

software has allowed businesses to open their doors enabling their suppliers to be

partners while emphasizing innovation as the core competency that drives value in any

firm. As always, the firms which show the most dynamic ability to welcome these forces

Barnes Group Page 14

of creativity will be the ones who develop competitive advantages and define the

business environment to come.

Five Forces Model

Firm members of any industry seek profit; this simple fact sits at the core

foundation of business. The five-forces model offers a dynamic approach to analyzing

an industry’s market structure. Such data aids in recognizing industry classification and

identifying key firm profitability factors. Who, what, and how are all topics evaluated and

answered by the model. The five-forces model can be separated into two parts:

actual/potential competition and the bargaining power of buyers/sellers. Competition

may be further divided into three categories which include rivalry among existing firms,

threat of new entrants, and threat of substitute products. Each of these three categories

presents its own unique challenges to a firm. They essentially dictate the level of

competition in a given industry and affect how a firm may price its products. A firm who

maintains a high degree of competition with existing firms must be price conscious.

Furthermore, the higher the threat of new industry entrants and substitute products the

more competitive prices and margins must be. Substitute products are sometimes

unexpected and adverse effects on firm profit. As mentioned previous, the rest of the

model deals with bargaining power. A perfect firm would hold power over both suppliers

and customers; however, such a scenario fails to exist due to market competition. Two

aspects compromise bargaining power. They are price sensitivity and relative

bargaining power. Price sensitivity stems from a customer’s window of cost at which

they are willing to purchase a product. Narrowly missing a customer’s maximum price

Barnes Group Page 15

expectancy can spell bad news for a firm. Relative bargaining power associates the

buyer’s ability to dictate costs. Suppliers lose bargaining power as more firms enter the

industry and offer buyers alternate means of acquiring a product. Seller’s meanwhile,

may build on relationships and innovation to distinguish themselves from competitors.

A conclusion from the five-forces model places an industry’s competition level among

three possibilities: high competition (cost competitive), mixed competition (elements of

both and high and low competition) and low competition (specialization). Thus, the

model measures the factors contributing to an industry’s or individual firm’s profitability.

Barnes Aerospace/Industrial Competitive Force Degree of Competition Rivalry Among Existing Firms High Threat of New Entrants High Threat of Substitute Products Low Bargaining Power of Customers Low Bargaining Power of Suppliers High

Barnes Distribution Competitive Force Degree of Competition Rivalry Among Existing Firms High Threat of New Entrants High Threat of Substitute Products High Bargaining Power of Customers High Bargaining Power of Suppliers Low

Rivalry Among Existing Firms

Within any industry, there exist only a finite amount of consumer expenditures.

With this in mind, firms must compete against one another in order to enjoy profit. Price

Barnes Group Page 16

as well as product differentiation serve as the two main sources to drive firm

competition.

Distribution (low value):

Within the industry of maintenance, repair, operations and process distribution,

competition is very intense. The vast majority of products offered through Barnes

Distribution are sold by direct competitors, necessitating low product differentiation and

high competition on cost. The ability for Barnes to compete on non-price dimensions will

depend on the success of their customer services which reduce procurement costs,

such as their Vendor Managed Inventory System (VMI). Vendor Managed Inventory

systems are a product of increased input costs causing many companies to strive for

improved efficiency. A successful VMI system depends largely on cooperation and

shared risk between the suppliers (distributors) and the customers. Many firms within

the distribution industry record sales and receive payment when a product is used, not

when it is restocked.

Aerospace and Industrial (high value):

According to the Aerospace Industries Association, the sales growth of airplanes

has been rising steadily since 2003 at around 8% per year. Also the Industrial industry

has revealed growth in the need for precision industrial components. Precision

industrial components have been rising in tandem with the related products they

complement. Due to the broad nature of the products under the umbrella precision

industrial manufacturing, one can expect the demand for the industry to track durable

goods orders.

Barnes Group Page 17

Durable goods orders roughly track the patterns of investment spending by

businesses, and since a large segment of our industry is designing valves for chemical

and petroleum processing, the costs of the related commodities would be an additional

factor affecting current and potential industry growth.

The increases in fuel prices as well as the need for more complex pipeline and

refining production have spurred an increased need for precision manufactured

industrial components. Similarly, increases in raw material costs, namely mined

resources, undoubtedly increases the amount of investment spending justified to bring

these raw materials to market.

Concentration

The number and relatives sizes of the firms in an industry dictate the industry’s

concentration. Concentration charts provide us a good picture of a firm’s market share.

Having a higher concentration ratio allows a large firm to more actively dictate the price

movements of products, while firms with low ratios must follow the lead of their

competition. Being able to set the market’s prices for products allows a firm to focus on

other aspects of their business while the smaller companies are kept busy trying to

compete on prices. Highly concentrated markets are harder to enter into, sometimes as

a result of big firm collaboration. On the other hand, fragmented industries can’t afford

to overprice products. In an industry composed of many small market share companies,

cost-price strategies play a prominent role in competition which in turn lead to lower

profits for everyone.

Barnes Group Page 18

Distribution (low value):

The number of Firms in an industry and their relative sizes influence the potential

and overall profitability of the industry as a whole. Within the Distribution of industrial

goods industry, there are many firms offering non-unique products and vary widely in

size. Each distributor is rather large in size, facilitating discounts on large purchases,

but aims to offer a special appeal to a specific type of firm while remaining applicable to

most firms in general. Some firms specialize in an inexpensive cost-structure of product

offerings, while other firms pride themselves on the number of products they sell. In

addition, some distribution companies market themselves as an “alternative to industrial

distributors,” facilitating a more personal relationship with customers. In order to

differentiate their sources of value, many distributors attempt to share the risk of

inventory storage and accumulation by in effect “storing” the goods at the end-users

location. By engaging in a shared risk type relationship, the distributor hope to offer the

customer increased service while increasing the switching costs associated with using

another distributor.

Aerospace and Industrial (high value):

Concentration in the aerospace industry is relatively high. However, firms like

Barnes and specialize in manufacturing and repairing turbine engine components and

applications of “original equipment manufacturers (OEM’s)” and the military (Barnes

10k). This “job-shop” nature dictates less of a need for economies of scale in the

aerospace industry. In the industrial manufacturing industry, concentration is more

direct, or head-to-head due to the higher demand for general application products.

Barnes Group Page 19

Degree of differentiation and Switching Costs

A firm may gain advantage over their competition through differentiation.

Differentiation refers to the likeness correlation between competing firms’ products.

Without differentiation, firms would have to compete on price alone. For example, two

products that are similar in appearance, how they conduct, and what they produce

would be classified as having a low level of differentiation between one another. The

higher the level of differentiation, the fewer firms must focus on price as a means of

competition. Therefore, differentiation can have a major impact on a firm’s profitability.

Appearance, features, quality, and build materials are all factors which may differentiate

a product

Switching costs can be observed from two different viewpoints, one of the

company and one of the consumers. The costs of a firm to discontinue its company

direction and begin to compete in a different industry are its switching costs. Low

switching costs would indicate a firm could use its resources to produce in another

industry at a relatively low expenditure, while high switching cost make it much harder

for firms to leave an industry. Switching industries could destroy a firm with high

switching costs. However, high switching cost industries do have one advantage for

established companies; they don’t have to constantly engage in price wars with

competing firms. Consequently, low switching costs allow firms to enter and leave the

industry as they please with little penalty for doing so. Switching costs for the consumer

relates to the affinity of customers switching from one firm to another in a given industry.

Low switching costs mean consumers will more readily be willing to change to a

competing product. In this case, firms will be more prices competitive

Barnes Group Page 20

Distribution (low value):

In past decade, the emergence of more usable, cheaper and efficient inventory

tracking systems and information technology has initiated retailers to push the activity of

procurement to the distributor itself. This is done by utilizing a Vendor Managed

Inventory system or VMI. In one scenario, the retailer will use an Electronic Data

Interchange (EDI) to signal to the distributor that inventory is in need or restocking.

Carefully balancing the incentives of the distributor with the needs of the firm are

essential in creating such a symbiotic relationship. As stated previously, the distributor

often offers the retailer repurchasing agreements in the event the inventory is

overstocked, or offers an option not to pay for the inventory until it is sold.

These relationships dissuade customers from looking elsewhere because the

procurement process is associated with the distributor. Simply put, the purchasing

decision is really on which distributor to use, not which product to buy from which

distributor. Achieving sustainable customer relationships in which each party commits

resources and shares risk increase the switching costs within the industry. The amount

of differentiation on the basis of activities being assumed by the distributor will only

serve to increase the switching costs associated with different distributors and drive the

purchasing decision further up corporate ladder.

Within the industry, this type of differentiation is the only non-price dimension of

their service. Many of the products sold by distributors can be found elsewhere and

there are multiple brands of exactly the same product. In order to establish a

competitive advantage, distributors must find an appeal beyond product scope.

Barnes Group Page 21

Aerospace and Industrial (high value):

In the precision manufacturing industry as well as the aerospace industry, the

importance for firm differentiation, and associated switching costs, depend on the

application of the associated components. For instance, in designing red valves and

compression springs, firms tend not to differentiate much on design and tend to

specialize in different processes and capacity. However, in the business of taking a

design from concept to manufacturing, fewer firms compete on heavily research-

dependent, full service manufacturers. In this scenario, firms vary widely on the service

they can offer customers and the value they add.

Customers of industrial component manufactures primarily consist of durable

goods manufactures for industries such as transportation and farm equipment.

Routinely, industrial component manufactures work directly with these customers to

customize a solution to their specific needs and incorporate their competencies into the

project of their customer (Barnes 10-k). Since these firms service the various needs of

their customers, niche specializations are needed of industrial firms to set them apart.

This distinction increases the associated switching costs because certain firms are more

able to cater to the customers than others making direct comparisons of competitors

difficult. Switching from one type of supplier to another that has different competencies,

capacities and priorities is not conducive to this high-value added industry. Therefore,

differentiation exists and switching costs are moderate.

Barnes Group Page 22

Economies of Scale

Quickly glancing over a review of Fortune 500 companies proves a company’s

size often positively correlates with its success. In most industries, large profits result

from large operations. The longer a firm resides in an industry, the more it learns the

nuances of the business. Assuming it grows as it endures these experience, the firm

gains an advantage of new entrants to the industry. Firms in high R&D industries

understand how to finance such costs while remembering it is imperative keep up with

the technology and advances of the industry. Those firms who are new to the industry

may not have the knowledge nor financial capabilities to fund such operations.

Distribution (low value):

The distribution industry in general is very imitable and therefore not a learning

industry. Although such extensive delivery operations require a logistical competency,

this is by no means an industry that precludes newcomers on the basis of learning the

best practices. Many distributors obtain distinction by having walk-in stores and others

are present on the internet or through call centers exclusively. Large economies of scale

are requisite to achieving low variable costs and competing on cost, however, this

presents the problem of overcapacity and high fixed costs that can bring this cyclical

industry down when economic growth is sluggish.

Aerospace and Industrial (high value):

In our aerospace industry, economies of scale is not a high priority due to oem’s

and rsp’s. They allow Barnes Group to produce after-market precision component parts

Barnes Group Page 23

that do not require large scale property plant, and equipment. As a result, Barnes Group

has only acquired one aerospace property since 1999.

Exit barriers

From time to time, firms make the decision to leave an industry. These decisions

are not without cost. The costs and regulations associate with leaving an industry are

known as exit barriers. Exit barriers may prevent a firm from exiting an industry.

Liquidation presents a huge obstacle for firms who offer specialized products. Often,

these products are hard to liquidate quickly. Losing fair value on these specialized

products as well as the extensive R&D into such product field deter firms from exiting an

industry

Distribution (low value):

The exit barriers associated with the distribution industry and relatively low due to

the liquidity of the assets involved and the competitive price dimensions of the products.

The assets which are illiquid include the brand names/image, enduring customer

relationships and logistical frameworks however these are highly irrelevant in the event

of a firm exiting the industry as they have been proven inefficient to begin with. The

fixed assets include trucking operations, warehouses, administrative offices and real

estate. Although a few exceptions exist, distributors as a whole do not produce the

products they sell. In the event of a firm exiting the industry, there would relatively few

industrial machines that have very specific uses and therefore, hard to sell in a

secondary or used market.

Barnes Group Page 24

Aerospace and Industrial (high value):

Contrary to the distribution industry, exit barriers are high for both precision

industrial manufacturing and aerospace industries. These industries have “illiquid”

assets and their competencies aren’t easily transferable to alternative industries. As a

result, aerospace and industrials have more liberty in the selection of products that will

increase need, and therefore, be more able to change to the direction of the industry

than distribution companies. Furthermore, due to the specialization of products and

regulations implemented by both these high value industries, exiting these industries

could end up being costly.

Excess capacity

Excess capacity occurs when the supply of goods and services within an industry

is larger than the demand. To rid themselves of surplus goods, firms cut prices in

hopes that consumers will purchase more of the product. In periods of long surplus,

prices may dip to unexpectedly low prices. In order to prevent excess capacity, firms

must carefully monitor expected sales forecasts and inventory levels. By maintaining a

healthy infrastructure, they can then maximize profit on supply/demand opportunities

Distribution (low value):

The distribution industry has high fixed costs, however, not high fixed costs

relative to sales. Due to the breadth/scope of product offerings, demand is dependent

on the state of the economy. When demand is low, there is competitive pressure to sell

products at discounts in order to utilize capacity. In a unique situation where commodity

and input prices are rising, either adding to or causing an economic downturn, the effect

Barnes Group Page 25

on the industry can be two-fold. First, cutting prices when demand is decreasing is

destructive in its own; however, doing so when the cost of the goods being sold is rising

adds another painful dimension to the distributors. Therefore, one can expect the higher

the fixed costs such as phone-center style sales teams and brick-and-mortar retail

distribution, the higher the loss in the event of sluggish demand. Firms best poised to

“weather the storm” are the ones with low fixed costs and limited physical presence.

Aerospace and Industrial (high value):

Excess capacity is more relevant to industrial manufacturing companies than to

the aerospace industry as a whole because of the similarity in the products designed

and the higher fixed to variable costs. However, both the aerospace and industrial

industries have high product life cycles due to the high costs of their customer’s

products. Within the Aerospace industry, excess capacity is more a product of aircraft

replacement cycles than economic expansions and contractions in general. Within the

business of aftermarket parts and overhaul services, backlogs are highly common.

Several companies have exclusive rights to provide aftermarket parts, overhaul and

repair services which enables them to vary turn-around rather than pricing in order to

manage demand.

Although aerospace companies have historically estimated these cycles with

high precision, significant events have caused unexpected drops in the demand for

aerospace components. The terrorist attacks of 2001 caused a severe drop in air-travel

as well as numerous cancellations of new aircraft orders.

Barnes Group Page 26

Industry Growth

Industry growth rates allow us to market competition. In a high-growth market,

new consumers are readily available to firms who wish to advance their market share.

Firms must effectively entice these new consumers to try their product. Competition

among firms in this market is much less strenuous than one which has a slow or stale

growth rate. When industry growth rates are low, the only means of market share

growth is to take consumers away from competing firms. Aggressive pricing campaigns

often ensue in low growth rate markets

Distribution (low value):

Determining the growth rate of an industry reveals the causation behind

increased profits, profit margins and market share. When industries are growing rapidly,

firms don’t have to take market share away from rivals in order to grow their profits. In

the case of the industrial supply industry, the growth is predictable and sustained. The

need for industrial, office and construction products closely monitor the growth of the

world economy. As new businesses emerge and populations increase, so does the

need for such products. Obtaining a large presence is considered an advantage,

however, firms within the industry can expect to grow their top line without having to

steal market share from rivals. Granted specialty distributors indeed do exist; many of

the products sold through the major distributors are very general and are not dependent

on one industry in particular.

Aerospace and Industrial (high value):

Barnes Group Page 27

Growth in the shipments of new civil and military aircraft has been consistently

increasing since the beginning of 2004. As well as increased orders, profits as a

percentage of sales, as of the third quarter of 2007, “increased slightly from 6.7

percent to 8.3 percent, which is slightly above the industry average for all

manufacturing corporations (AIA).” Consequently, demand for aerospace components

can be proxied through measuring the growth in the need for civilian travel as well as

the need for military aircraft. In 2005, the “Annual Review of Civil Aviation 2005”

reported that for the first time, scheduled airlines had transported in excess of two

billion passengers worldwide

(http://pdf.aiaa.org/preview/CDReadyMATIO07_1768/PV2007_7809.pdf).

Based on this survey by the Aerospace Industries Association, the average

growth rate of the industry was 5.19% over the last 10 years. It is important to note

the effect of the terrorist attacks of 9/11 (September 11th, 2001) on civilian air

travel, and commercial airlines and its effect on industry growth in the previously

mentioned time period. Even though profit margins have improved slightly in the

short term, prices have grown at an rate of only 1.32%

(www.bts.gov/.../html/air_travel_price_index.html)

since 1995.

Conclusion

We feel the growth in air-travel will directly contribute to the growth in

aerospace sales. Although it is generally thought that rapid sales growth directly

correlates to higher profit-margins, we believe profit margins will remain relatively

Barnes Group Page 28

constant in the industry because of the stagnant prices of air-travel and the

consistent and estimable growth expected in the future.

18.57%

5.69%

-8.02%

5.95%

-8.08% -8.81%

8.63%

12.62%

7.48%

12.82%

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Aerospace Aircraft Industry Growth

Barnes Group Page 29

Threats of New Entrants

Successful markets will always entertain new prospective firms. When an

industry is experiencing large profits, everyone wants a piece of the pie. The ability for

firms to enter new markets, however, is not always easy. Established firms in the

industry will often go to great lengths to aggressively price products so that new firms

can’t compete. Factors which must be contemplated include economies of scale, first

mover advantage, access to channels of distribution and relationships, and legal

barriers. Only after analyzing these factors should a firm makes decision on whether to

enter a market.

First mover advantage

History has shown that the first firms to enter a market enjoy a competitive

advantage over those who follow suit into the industry. This is known as the first mover

advantage. These firms get to set standards for the industry. They are able to build

close relationships with suppliers and acquire resources for production without having to

compete with other firms. When there are only a small limited number of suppliers and

resources, firms who have the first mover advantage possess and distinct advantage in

the industry. Patents and brand name prominence often result from the first move

advantage. Customer loyalty built during the initial industry phases can last a lifetime.

Today, many firms whose product quality levels have dipped still enjoy modest profit

due to name recognition.

Distribution (low value):

Barnes Group Page 30

First mover advantage can be best described as the advantage achieved by the

initial firms entering the business as they have the opportunity to establish best

practices and customer/supplier relationships. In the case of the distribution industry,

there are moderate advantages associated with this effect. First off, buyers who engage

in the Vendor Managed Inventory model and more likely to have higher switching costs

and be less likely to shift the important responsibility/activity of procurement to an

unproven partner. Mistakes in inventory delivery of critical components can cause

severe economic harm to the customers involved, so a trusting relationship with the

distributor is necessary for a successful firm. However, due to the non-specific and

existence of substitute products, it is difficult for firm to compete on non-price

dimensions. This opens the door for new entrants and erodes most any advantage

associated with the first movers in an industry.

Aerospace and Industrial (high value):

The business of maintenance, overhaul and repair services for aircraft engines

has high first-mover advantage, while similar services for generalized components do

not. It is often the case that a single aerospace company will offer the support services

for an entire engine family through exclusive relationships with the engine

manufacturers. For Example, Barnes Group offers support for most every jet-turbine

engine General Electric produces. Similarly, Triumph Group offers support for various

Pratt & Whitney, Honeywell, and Garret engines.

Barnes Group Page 31

Opposed to the engine overhaul services mentioned above, more generalized

components like engine casings, heat exchangers and air seals can be provided by a

variety of different firms, thus necessitating no first mover advantage.

We would characterize the first mover advantage as moderate for the aerospace

MRO industry as a whole.

Distribution access and relationships

As firms grow, their business becomes more complex in terms of managing daily

operations. Customers, suppliers, distributors and must all be consistently monitored.

Establishing close relationships with suppliers help keep product cost as low as possible

while continually upgrading distribution practices enhances the growth of a firm. These

relationships and expansionary methods directly influence a firm’s competitiveness in

an industry.

Distribution (low value):

Limited or restricted access to mechanisms to get a product to the customer (not

distributor in the firm sense) can serve as severe barriers to entry. In the distribution (in

the firm sense) industry, there are very few barriers to entry in achieving access to

channels of distribution because of the intense competition in the trucking and

transportation industries and the ease of obtaining the assets to bring products to

market. However, in developing economies, multinational corporations routinely have

difficulty establishing a competitive position without partnering with an existing firm. Due

Barnes Group Page 32

to the high amount of international sales to most large distributors, this could restrict

future competition.

The costs of delayed or failed delivery of products (inventory) can cause extreme

economic harm to the customer if the items are essential business items. This risk

places importance on the continued track-record of an existing firm or partner and

places significant pressure on firms to regularly deliver on their word. The reliability of

this continuing relationship is paramount to the success of any distribution firm.

Several firms within the industry actually create a portion of the products they sell in

hopes of achieving a brand name differentiation. This exclusive access to these

products creates barriers in the input side of the relationship and access aspect of the

business. Several large industrial distributors strive to obtain an exclusive agreement

with suppliers, or achieve exclusivity through outright acquisitions. If the products that

are exclusively offered through a single distributor are unique, significant barriers to

entry and exist for that niche of the industrial distribution industry.

Aerospace and Industrial (high value):

Within the Aerospace MRO industry, access to channels of distribution is

moderately restrictive. Commercial airlines, Original Equipment Manufacturers and

independent service companies compete for hanger space while commercial airlines

often have their own service stations. In addition, the Federal Aviation Administration

requires repairers of engines to have a certified repair station. Achieving hangar space

near large air-traffic “hubs” is a significant barrier in gaining access to reparable aircraft.

Barnes Group Page 33

Legal Barriers

Legal barriers may pose challenges to firms hoping to enter an industry. Patents, fees,

and regulations are all examples of legal ramifications for any given industry entrant.

Many of these documents request extensive background information. Examples of

legal documents include licenses, regulations, and contracts. The more legal barriers

there are the less likely start-up companies will venture into an industry.

Distribution (low value):

Legal barriers can shield currently competing firms from potential competition in

the event of legal protections that ensure an inefficient market, or protections that

ensure intellectual property rights. There are few legal barriers to new entrants in the

industrial distribution industry that prove to be material. Interstate commerce and

taxation are a few that arise, however none of which are significant enough to dissuade

potential competitors. The availability of GSA contracts (General Services

Administration) is essential to obtaining U.S. Government clientele. Many large

distributors possess such a contract, however, emerging distributors do not, inhibiting

them from competing on future government purchases.

Aerospace and Industrial (high value):

Several legal barriers preclude entrance into the aerospace MRO industry.

Obtaining FAA licenses for repair stations is timely and required for any repairer of

Barnes Group Page 34

critical aircraft components (mostly turbine engines). In addition, some OEM

manufacturers require similar certification prior to repairing their products

Threat of Substitute Products

Substitute products are those that are viewed as alternatives to a given product.

They serve a similar purpose and may be interchanged buy purchasing customers.

Substitute products can cause consumers to use less of a good or to not purchase it all

due to having an alternative that is of a higher quality or offered at a lower price

Distribution (low value):

Substitute products can take a variety of forms depending on the industry being

discussed and these forces work to decrease the profit margin of the affected firms. In

the distribution industry, the major threat of substitutes arises from forward integration

on behalf of the buyers and direct sales by the manufacturers of the products. The term

“disintermediation” is widely cited in trade publications as an inevitability that will negate

the activities of a distributor. The advances in information technologies have created

concerns about the future of the industry and the need to store large amounts of

inventory in anticipation of customers’ needs. Although much consolidation has taken

place within the industrial distribution industry, many see these developments as

constructive and a force that drives sales instead of suppresses them.

Due to the general and non-specific nature of many of the goods offered through

distribution businesses, the suppliers to the distributor lack the bargaining power to

Barnes Group Page 35

make the customer come directly to them. In exception of large bulk orders, many firms

depend on industrial distributors to bring them input goods at the lowest costs. Some

distributors specialize in common parts sold in small amounts and others specialize in

higher value added goods. The differing appeals in both cost structure of product

offerings, and the accessibility albeit brick-and-mortar physical locations or online

presence only, characterize the needs of the many customers and the specialization of

the industrial distributor firms themselves.

Aerospace and Industrial (high value):

The threat of substitute products in the aerospace industry comes primarily from

products that fulfill similar functions rather than similar forms. Substitutes to air-travel

include public transportation, railroads and automobile transportation. In addition,

several factors such as flight delays, increasing fees and tighter security contribute to

declines in the appeal of civilian air-travel. Corporations have been increasingly finding

ways to converse over long distances without a physical presence. Therefore, we would

say there are many substitutes available. The American Consumer Satisfaction Index

conducts a consumer sentiment survey over time of the airline industry as a whole.

Since 1995, the index has declined significantly and many critics attribute the decline to

the previously mentioned factors. Nevertheless, there exists no substitute for trans-

Atlantic flights, as well as no substitute that can achieve a lower travel time.

Another significant factor affecting substitute travel methods are oil prices.

Although all methods of transportation utilize oil as their primary fuel source, air-travel is

Barnes Group Page 36

disproportionally affected by increases in oil prices. Airplanes are the least efficient form

of travel as far as usage of oil.

Bargaining Power of Customers

Distribution (low value):

The relative bargaining power of the buyers in an industry influences the potential

profitability of the industry as a whole. If individual firms are easily imitable and their

competencies highly general, they most likely lack the power to bargain with their

suppliers. The firms in the distribution industry must be large enough achieve

economies of scale for their logistical needs and to obtain discounts on large purchases

of high volume items. Due to the large scope of product offerings, this characterization

is inherently limited.

In high value added goods such as hydraulics and specialty machines, suppliers

have significantly more power than in low value added goods such as fasteners and

abrasives. This is evident in the profit margins of the different firms within the industry,

as they tend to specialize in different goods.

The large number of industrial distributors and the lack of significant non-price

dimensions to compete on allow for many distributors of similar size, decreasing their

power to bargain with suppliers as a whole.

Aerospace and Industrial (high value):

Barnes Group Page 37

The bargaining power of customers is strong in the aerospace MRO industry.

“Original equipment manufacturers…have significant pricing leverage over suppliers

and may be able to achieve price reductions over time (Barnes 2007 10k).” There exist

a high number of aerospace firms that produce fabricated metal components. OEMs

have been recently using aggressive auction strategies to reduce the prices they pay to

their suppliers (Aerospace customers).

Several aircraft manufacturers, most notably Boeing, have been employing

virtual supplier portals. These online networks enable suppliers to bid against each

other for production contracts based upon the desired specifications, quantities and

deadlines. This environment puts significant emphasis on price and forces suppliers to

cut costs in order to compete.

Bargaining Power of Suppliers

Demand from customers largely dictates the bargaining power of a supplier. For instance,

Distribution (low value):

As stated earlier, the relative bargaining power of an industry is paramount in

understanding the current and potential profitability of that industry. In the circumstance

of general, non-specific products such as abrasives, epoxies, fasteners, and cleaners,

the bargaining power tends to rest with the distributors as their large size and customer

relationships trump the need for that one brand of product. However, certain products

Barnes Group Page 38

that are unique and require research and development as well as patent protection,

such as power-tools, cutting machines and hydraulics, tip the scales in the opposing

direction and enable the suppliers to better bargain with the distributors.

Aerospace and Industrial (high value)

The inputs required for metal fabrication in the aerospace industry are largely

commodities, and allow for little negotiation on price dimensions. Furthermore, the high-

grade steel, aluminum and titanium and other special metals used in aerospace

components are periodically offered through a “limited number of primary

suppliers.”(Barnes 10k, 2007) Suppliers of raw materials have significant leverage

because of the large number of buyers and the significance of the raw material to the

end product.

0

50

100

150

200

250

Dec

-98

Jun-

99

Dec

-99

Jun-

00

Dec

-00

Jun-

01

Dec

-01

Jun-

02

Dec

-02

Jun-

03

Dec

-03

Jun-

04

Dec

-04

Jun-

05

Dec

-05

Jun-

06

Dec

-06

Jun-

07

Dec

-07

Jun-

08

Inde

x

Date

Metal Index

2005 = 100

•Copper•Alluminum•Iron Ore•Tin •Nickle •Zinc•Lead•Uranium

Barnes Group Page 39

Key Success Factors

The type of business strategy a firm takes is crucial when trying to add value to a

firm. The two types of strategies firms can undertake are cost leadership and

differentiation. In order for firms wanting to acquire a competitive edge in low value

industries, they must follow the cost leadership strategy. Also, for a firm to obtain a

competitive advantage over high value industries, they must follow the strategy of

differentiation. Although high value industries, such as aerospace and industrials, and

low value industries, such as distribution, follow their respective strategies, they tend to

use competitive advantages from both strategies.

56

58

60

62

64

66

68

70

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

ACSI Airlines

ACSI Airlines

Linear (ACSI Airlines)

Barnes Group Page 40

Cost Leadership

The products distributed in this low value industry are not unique, and its

competitors carry substantially similar products. Firms in this distribution industry must

stress a heavily priced competitive industry. In order to keep the price of products and

cost of distribution in this industry low, achieving superior performance is crucial to the

survival of the firm. Cost leadership might be the best way to achieve superior

performance for low value distribution firms. A few characteristics help to attain superior

performance are economies of scale and scope, tight cost control systems, and limited

investment in Research and Development. Although these characteristics are vital to

firms desiring to achieve superior performance in a low value distributing industry, some

of the cost leadership strategies are enforced by high value industries, such as

aerospace and industrial.

Economies of Scale and Efficient Production

It is important for firms in a low value distribution industry to become highly

efficient in order to mass distribute their products at low costs. Expansion is the

essential method for acquiring additional resources needed to distribute their products

at low costs. The low value distribution industry consists of Barnes competitors

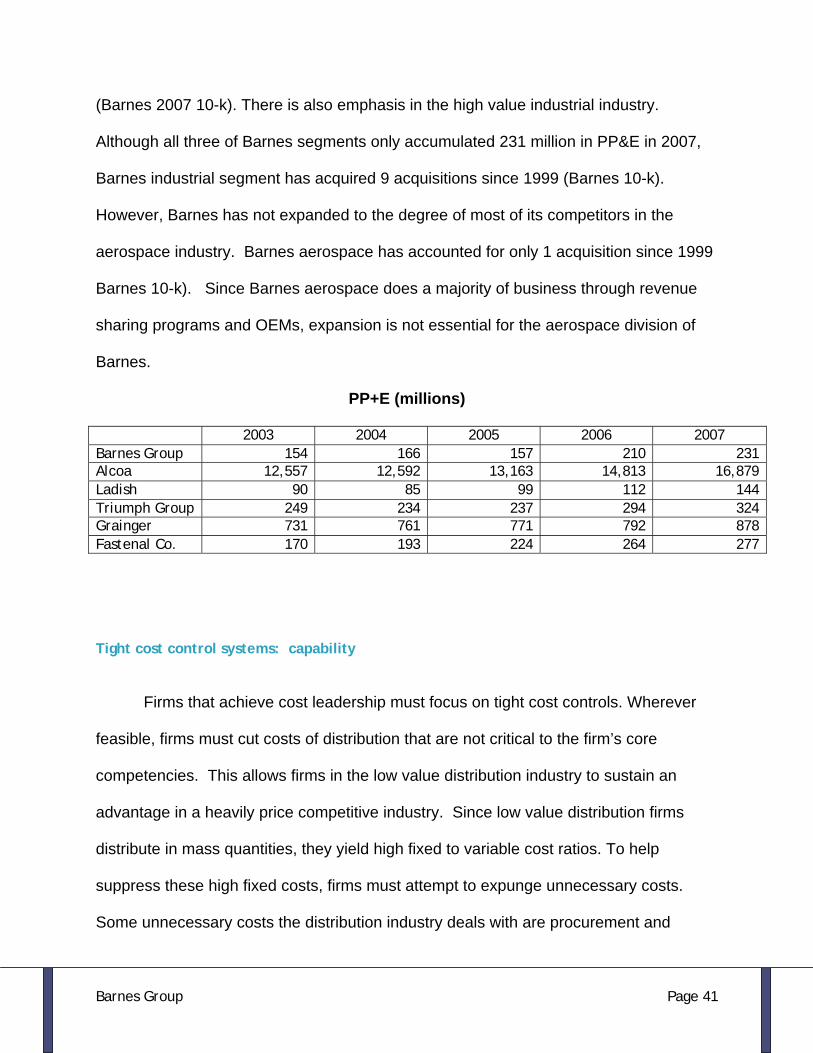

Grainger, Alcoa and Fastenal. According to the table below, Barnes distribution

competitors realize the important of expansion. Alcoa spent close to seventeen billion

last year on PP&E (Alcoa 2007 10-k). Also, Barnes distribution has obtained 5

acquisitions since 1999. Furthermore, Barnes distribution operates in 40 countries

Barnes Group Page 41

(Barnes 2007 10-k). There is also emphasis in the high value industrial industry.

Although all three of Barnes segments only accumulated 231 million in PP&E in 2007,

Barnes industrial segment has acquired 9 acquisitions since 1999 (Barnes 10-k).

However, Barnes has not expanded to the degree of most of its competitors in the

aerospace industry. Barnes aerospace has accounted for only 1 acquisition since 1999

Barnes 10-k). Since Barnes aerospace does a majority of business through revenue

sharing programs and OEMs, expansion is not essential for the aerospace division of

Barnes.

PP+E (millions)

Tight cost control systems: capability

Firms that achieve cost leadership must focus on tight cost controls. Wherever

feasible, firms must cut costs of distribution that are not critical to the firm’s core

competencies. This allows firms in the low value distribution industry to sustain an

advantage in a heavily price competitive industry. Since low value distribution firms

distribute in mass quantities, they yield high fixed to variable cost ratios. To help

suppress these high fixed costs, firms must attempt to expunge unnecessary costs.

Some unnecessary costs the distribution industry deals with are procurement and

2003 2004 2005 2006 2007 Barnes Group 154 166 157 210 231 Alcoa 12,557 12,592 13,163 14,813 16,879 Ladish 90 85 99 112 144 Triumph Group 249 234 237 294 324 Grainger 731 761 771 792 878 Fastenal Co. 170 193 224 264 277

Barnes Group Page 42

transaction costs. Barnes VDI system helps to reduce these costs in a productive and

timeliness manner (Barnes 10-k). Other costs the distribution industry must diminish are

R&D and brand advertising. Firms in the distribution industry do not spend capital on

R&D because the products they distribute are similar and sold in high volumes.

However, Barnes has acquired brand names, such as Kent, Kar and Bowmans in order

to offer quality, brand name parts (Barnes 10-k).

Conclusion

Barnes distribution stresses a tight cost control system in order to keep fixed

costs down. Since Barnes distribution uses a vendor management inventory system

they can try to suppress unnecessary costs more efficiently. Expanding your business

is beneficial for distribution firms that use vendor management technology. However,

firms in the distribution industry all acquire superior brand names in order to supply their

customers with a higher quality product. This accumulates large, unnecessary costs.

Differentiation

The aerospace and industrial industries choose to enforce a differentiation

strategy. This strategy is more concerned with how to differentiate their products from

their competitors than acquiring low cost. Aerospace and industrial industries follow the

differentiation strategy for superior quality/variety and reliable customer service (Barnes

10-k). Although firms in the distribution industry compete on cost leadership, they also

use the differentiation strategy to provide reliable customer service. These key

Barnes Group Page 43

performance indicators help firms in industrial and aerospace industries adjust to the

specific needs of their customers.

Superior quality

Superior quality is a key performance indicator for Barnes aerospace and

industrial industries. They produce components for OEMs and individual customer

needs. This commitment to quality ensures customers will maintain their relationship.

Superior Customer service

Superior customer service is a high priority for firms, like Barnes and Triumph, to

supply precision components for OEM’s. Contracts with these customers provide

overhaul and repair service on these precision engine components once completed

(Barnes + Triumph 10-k). Once they have finished producing their client’s products,

superior customer service will be critical in order to maintain “long standing customer

relationships.” The aerospace firms provide overhaul/ repair services on their precision

components as well (Barnes 10-k and Triumph 10-k). Without providing superior

customer service, aerospace firms that provide overhaul and repair services would have

a hard time finding potential customers. Furthermore, the industrial industry also

competes on superior customer service. They are similar to aerospace industry in that

they provide precision parts that fit a customer’s specifications (Barnes 10-k). High

costs of products in these aerospace and industrial industries make it hard to persuade

Barnes Group Page 44

potential future customers to take a risk doing business with a precision component

supplier.

The distribution industry also relies on superior customer service. Since the

products in this industry are not unique, distributing firms provide automated systems to

assist customers in picking “reliable service options” (Barnes 2007 10-k and Grainger

10-k).

Conclusion

Aerospace, industrial and distribution industries all require superior customer

service because of the highly competitive nature of these industries. Aerospace and

industrial industries enforce it in order to offer unique and customized products. The

distribution industry requires it in order to improve productivity while reducing their

customers costs.

Firm Competitive Advantages

After exploring the high and low value industry success factors and analyzed the

firm’s competitive strategies, we have concluded that Barnes implements a cost

leadership strategy for the low value distribution industry. On the contrary, Barnes high

value aerospace and industrials tends to favor the differentiation strategy. However,

both high and low value industries use some of the tools of the opposing strategy.

Tight cost control systems

Barnes Group Page 45

Barnes distribution industry relies heavily on tight cost control systems. The

vendor managed inventory system gives Barnes a competitive advantage because it

allows them to operate with a “well-diversified customer base” and wide variety of

replacement parts.(Barnes 10-k). Since the distribution industry is based in over forty

countries, the automated VMI system will help increase profitability of their customers

while cutting costs of production.

Superior customer service

Barnes aerospace industry has acquired a competitive advantage because they

provide revenue sharing programs with their OEM customer, General Electric. This

gives Barnes “exclusive rights to supply aftermarket parts for the life of the program”

(Barnes 10-k). These aftermarket parts require “overhaul and repair services.” Also,

since Barnes has rights for the life of the program, continuing to provide superior

customer service will allow Barnes to keep their exclusive manufacturing rights with

General Electric.

Accounting Analysis

Accounting analysis is applied in order to find out how accurately a firm’s

accounting practices “capture its underlying business reality.” (Palepu & Healy) A firm’s

accounting policies, estimates, and degree of accounting flexibility can lead to

distortions in a firms accounting statements. Accounting analysis attempts to identify

these distortions and then “undo” them by adjusting a firm’s accounting numbers using

Barnes Group Page 46