Embed Size (px)

Citation preview

Basic Accounting and Financial Audit Concepts

Presenter: Nick Kolitsos, CPA August 27, 2014

2

Opening Remarks

ModeratorR. Kinney PoynterExecutive Director

NASACT

SpeakerNick Kolitsos, CPA

Senior AuditorOffice of the State Auditor (CA)

3

Intentionally Blank

Objective To provide audit staff a basic understanding of

key accounting concepts to aid in the execution of performance audit or review objectives.

Intended for staff with little or no accounting background that perform various types of audits.

4

Topics covered:

Basic accounting terms (focus will be on governmental accounting)

Financial statement overview Budgetary/Legal vs Generally Accepted

Accounting Principles Case examples

5

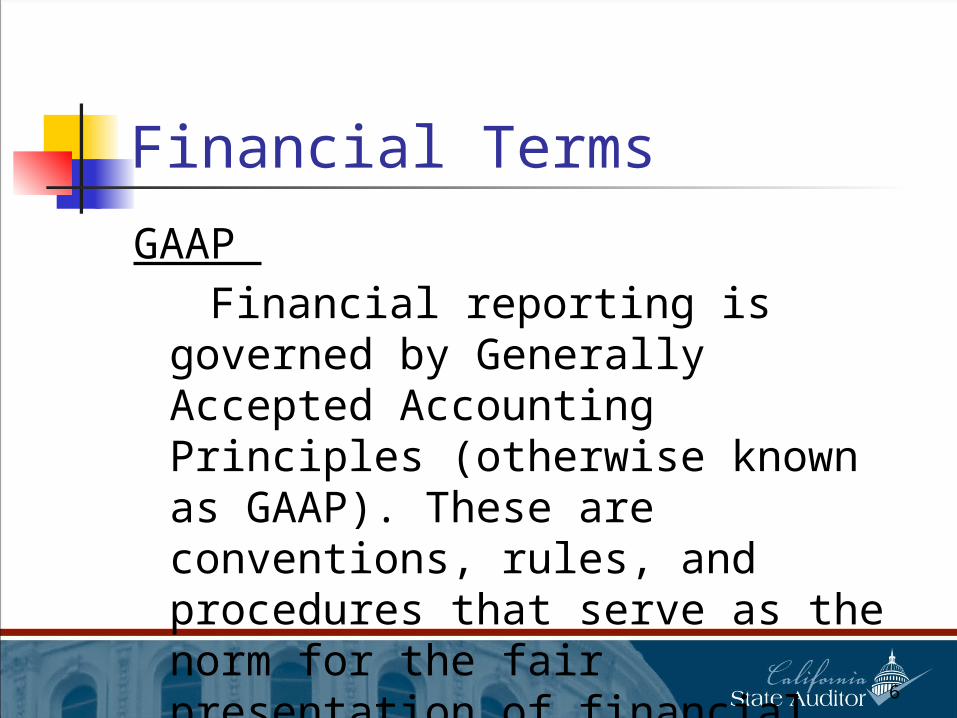

Financial Terms

GAAP Financial reporting is governed by

Generally Accepted Accounting Principles (otherwise known as GAAP). These are conventions, rules, and procedures that serve as the norm for the fair presentation of financial statements.

6

Financial Terms

Basic Financial StatementsBalance Sheet: Financial statement that lists types and

dollar amounts of assets, liabilities, and their difference at a specific date, such as June 30, 2012.

Income Statement: Financial statement that subtracts expenses from revenues for a specified period of time, such as fiscal year.

Statement of Cash Flows: Financial statement that lists cash inflows (receipts) and cash outflows (payments) during a period; arranged by operating, investing, and financing activities.

7

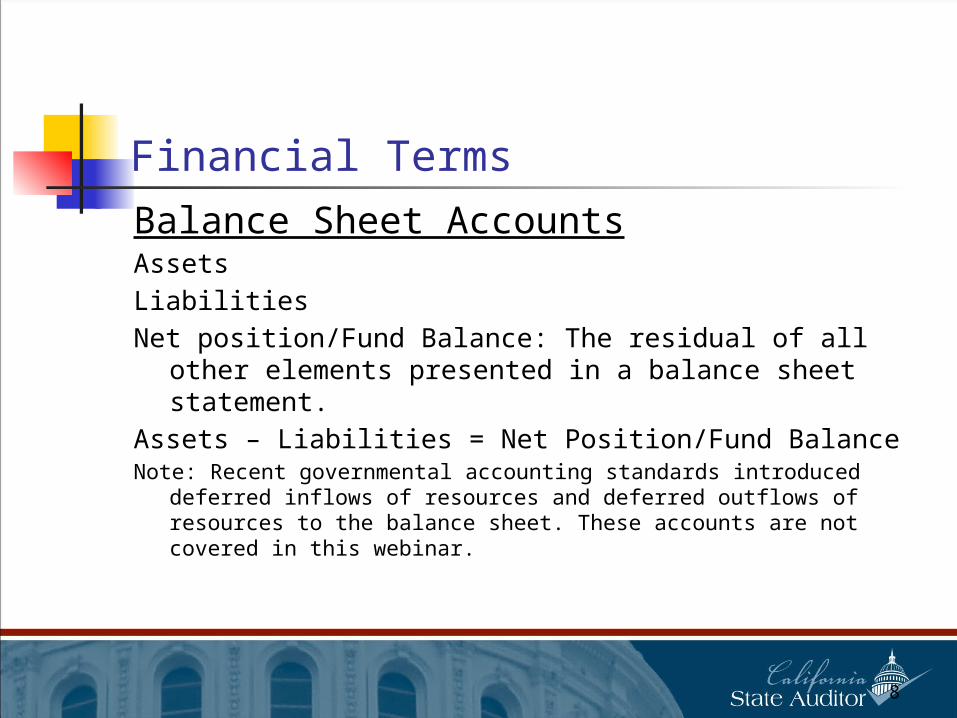

Financial Terms

Balance Sheet AccountsAssetsLiabilitiesNet position/Fund Balance: The residual of all other

elements presented in a balance sheet statement. Assets – Liabilities = Net Position/Fund BalanceNote: Recent governmental accounting standards introduced deferred

inflows of resources and deferred outflows of resources to the balance sheet. These accounts are not covered in this webinar.

8

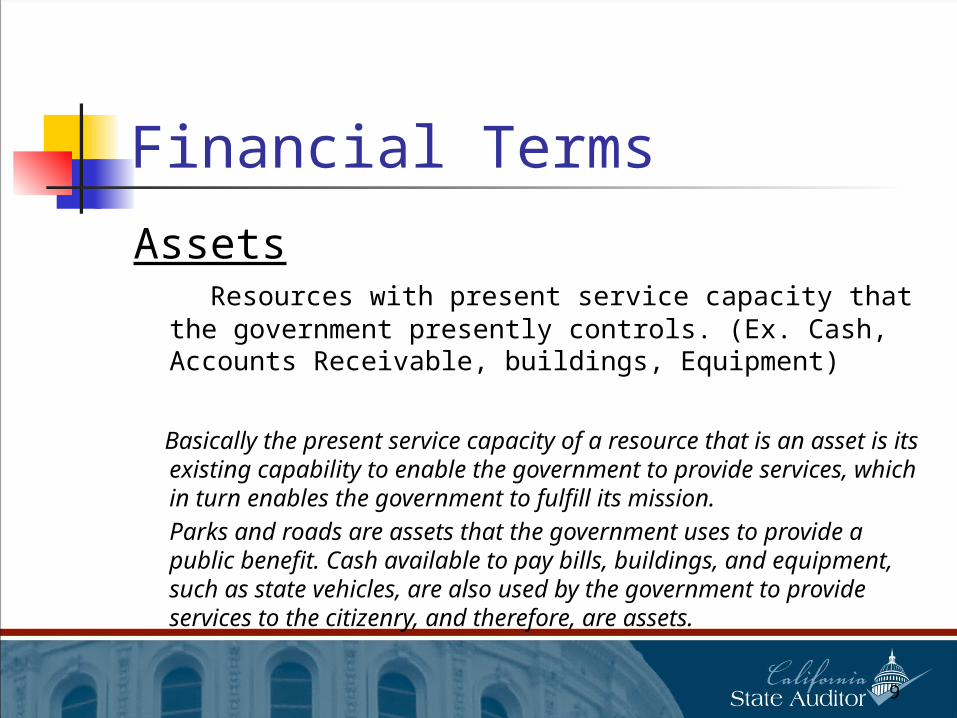

Financial Terms

Assets Resources with present service capacity that the

government presently controls. (Ex. Cash, Accounts Receivable, buildings, Equipment)

Basically the present service capacity of a resource that is an asset is its existing capability to enable the government to provide services, which in turn enables the government to fulfill its mission. Parks and roads are assets that the government uses to provide a public benefit. Cash available to pay bills, buildings, and equipment, such as state vehicles, are also used by the government to provide services to the citizenry, and therefore, are assets.

9

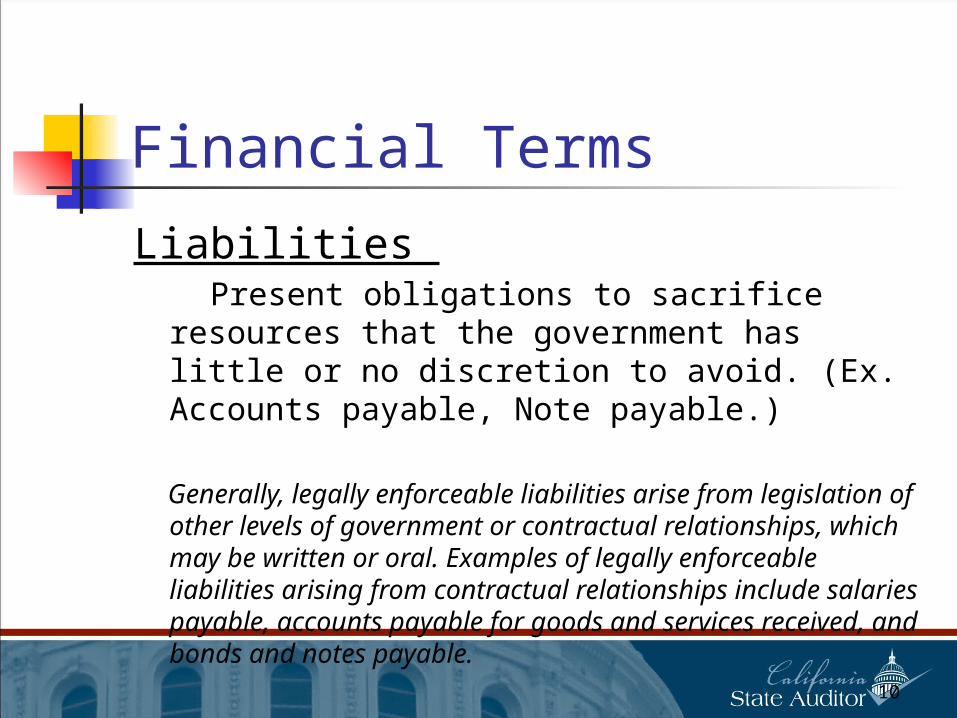

Financial Terms

Liabilities Present obligations to sacrifice resources that

the government has little or no discretion to avoid. (Ex. Accounts payable, Note payable.)

Generally, legally enforceable liabilities arise from legislation of other levels of government or contractual relationships, which may be written or oral. Examples of legally enforceable liabilities arising from contractual relationships include salaries payable, accounts payable for goods and services received, and bonds and notes payable.

10

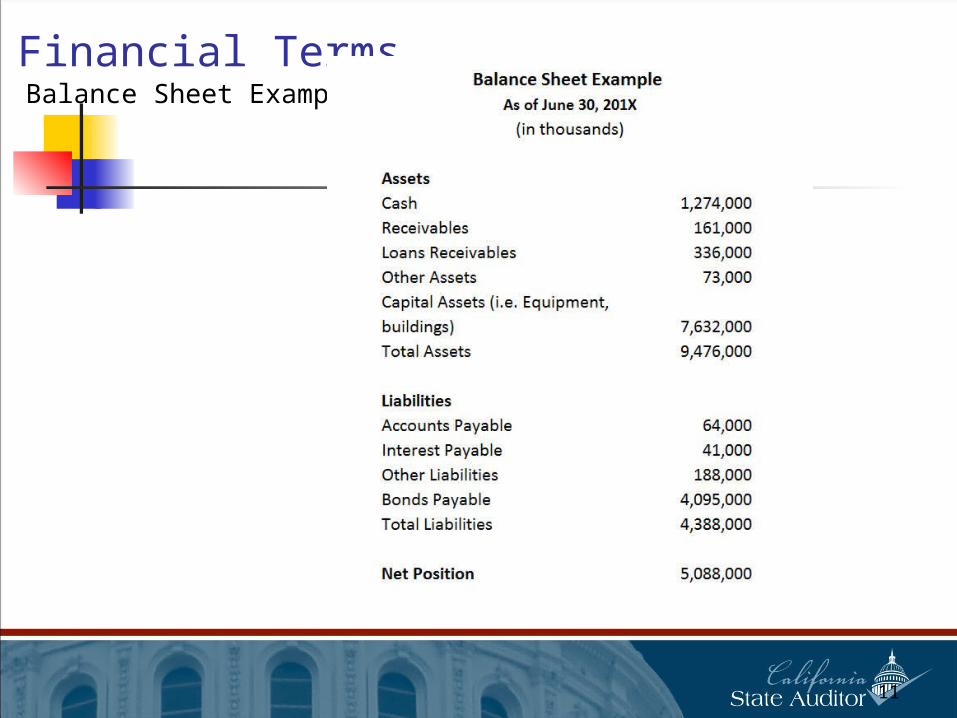

Financial Terms Balance Sheet Example

11

Financial Terms

Income Statement Accounts Revenues: Resources claimed by the government to the

extent that the resource is earned and collected or available (modified accrual) (ex. Taxes and fees)

Expenses/Expenditures: Transactions that reduce economic resources. Generally, recognized when a liability is incurred.

Beginning Balance + Revenues - Expenditures = Ending

balance (Should equal respective fund balance/net position on balance sheet.)

12

Financial Terms Income Statement

Example

13

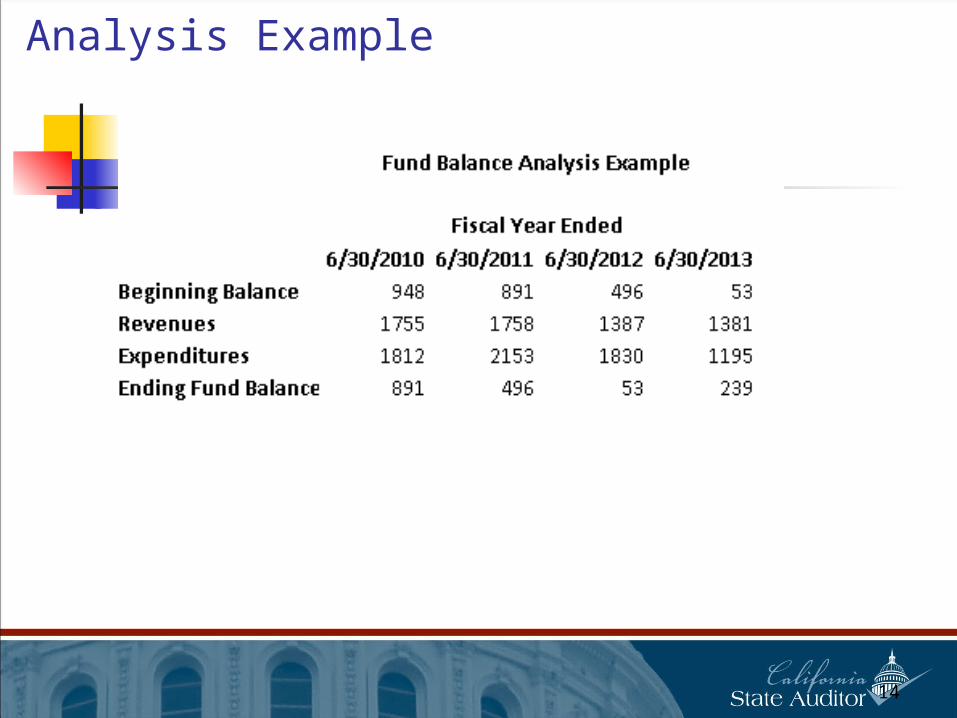

Analysis Example

14

Analysis Example

15

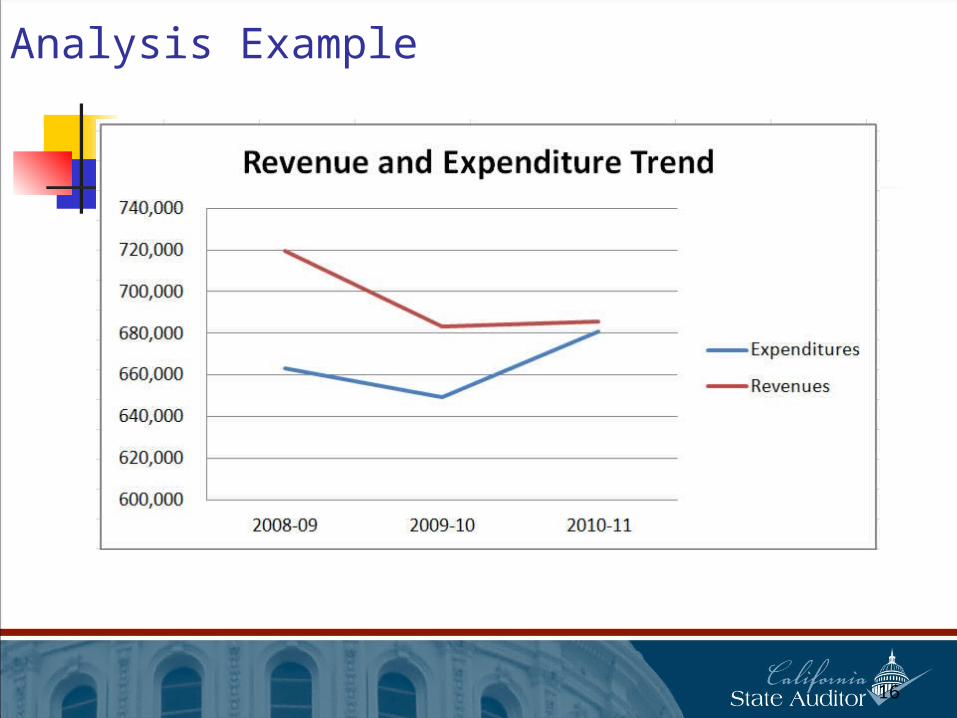

Analysis Example

16

Analysis Example

17

18

Intentionally Blank

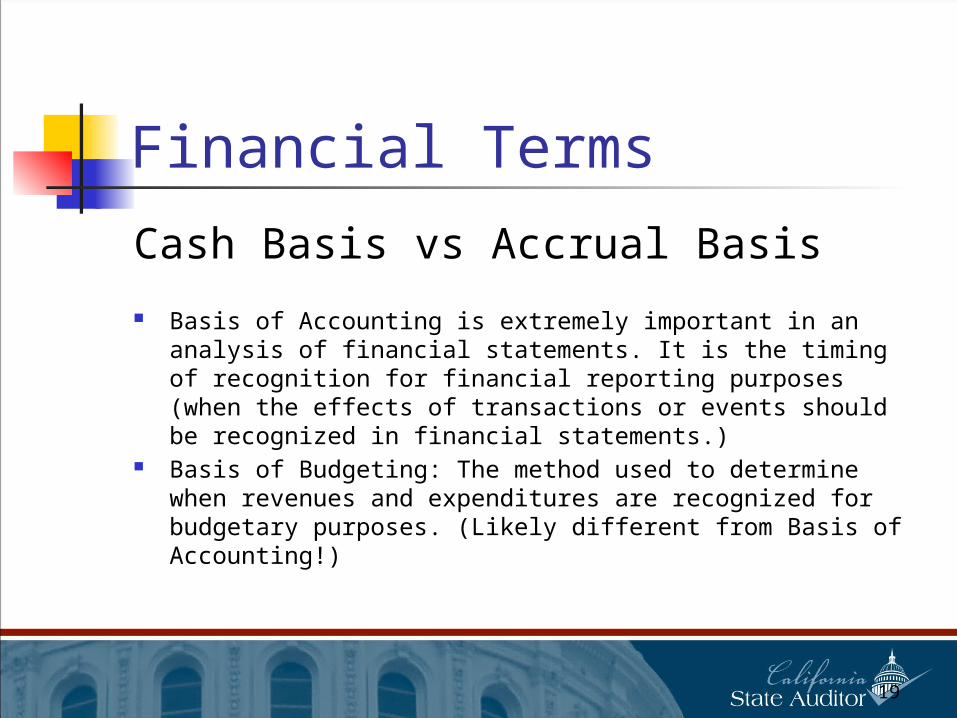

Financial Terms

Cash Basis vs Accrual Basis

Basis of Accounting is extremely important in an analysis of financial statements. It is the timing of recognition for financial reporting purposes (when the effects of transactions or events should be recognized in financial statements.)

Basis of Budgeting: The method used to determine when revenues and expenditures are recognized for budgetary purposes. (Likely different from Basis of Accounting!)

19

Financial Terms

Basis of Accounting (revenue) Cash – Earned and collected during a period. Accrual – Earned and collected; or earned but

may or may not be collectable soon enough to pay liabilities.

Modified Accrual – Same as accrual, but must be collectable soon enough after the current period to pay liabilities of the current period. (State generally uses modified accrual.)

20

Financial Terms

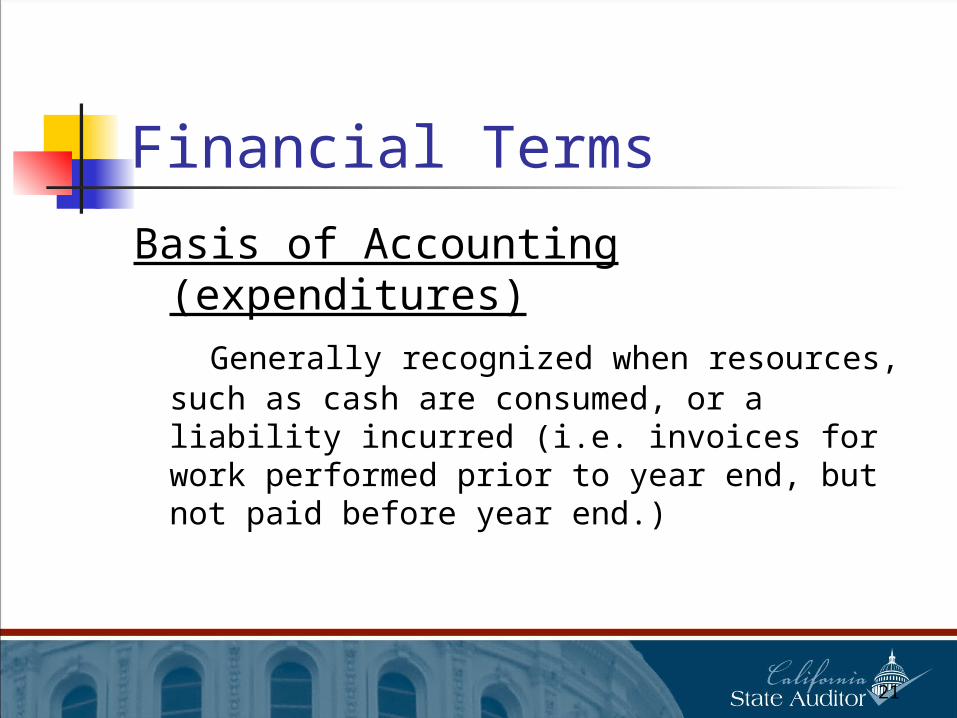

Basis of Accounting (expenditures) Generally recognized when resources, such as

cash are consumed, or a liability incurred (i.e. invoices for work performed prior to year end, but not paid before year end.)

21

Financial Terms Double entry accounting: Accounting system in

which each transaction affects at least two accounts and has at least one debit and one credit.

Debit: an entry that increase asset and expenditure accounts and decreases liability and revenue accounts.

Credit: an entry that increases liability and revenue accounts and decreases asset and expenditure accounts.

22

Financial Terms

Journal Entry ExampleEntry for an unpaid $100 electric bill at year end:

Credit: Accounts Payable (Liability) $100Debit: Expense $100

After it is paid: Credit: Cash (Asset) $100Debit: Accounts Payable (Liability) $100

23

Financial Terms

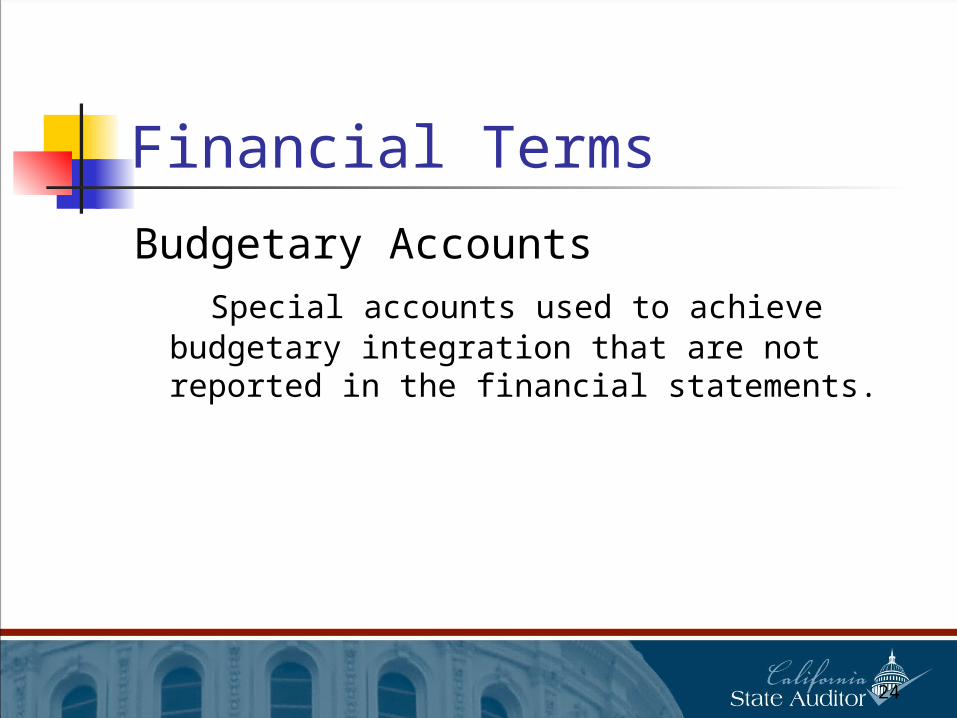

Budgetary Accounts Special accounts used to achieve budgetary

integration that are not reported in the financial statements.

24

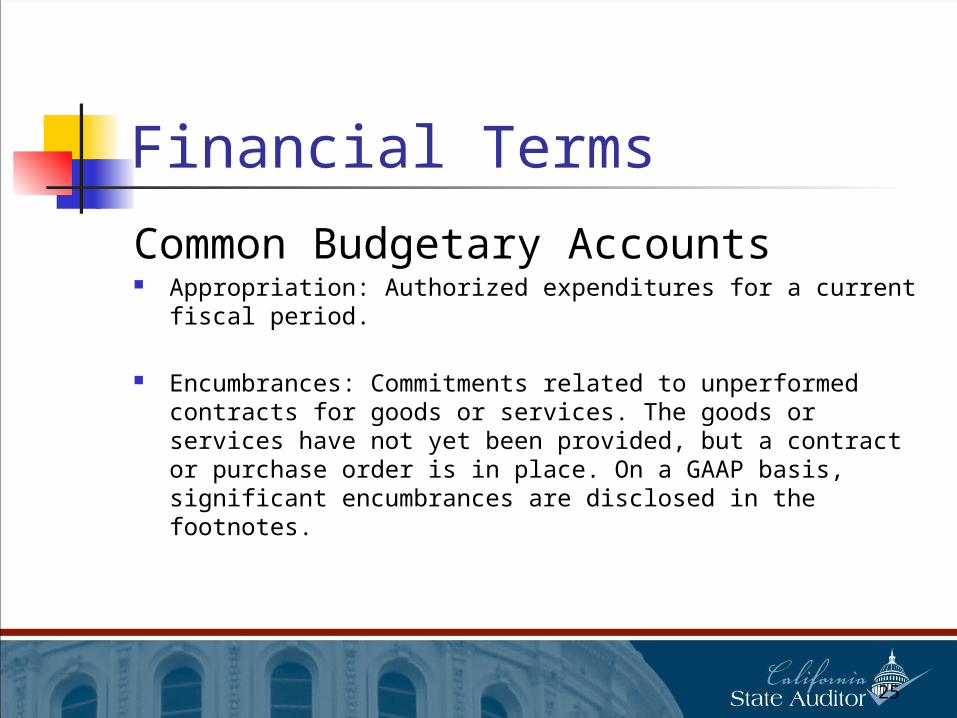

Financial Terms

Common Budgetary Accounts Appropriation: Authorized expenditures for a current fiscal

period.

Encumbrances: Commitments related to unperformed contracts for goods or services. The goods or services have not yet been provided, but a contract or purchase order is in place. On a GAAP basis, significant encumbrances are disclosed in the footnotes.

25

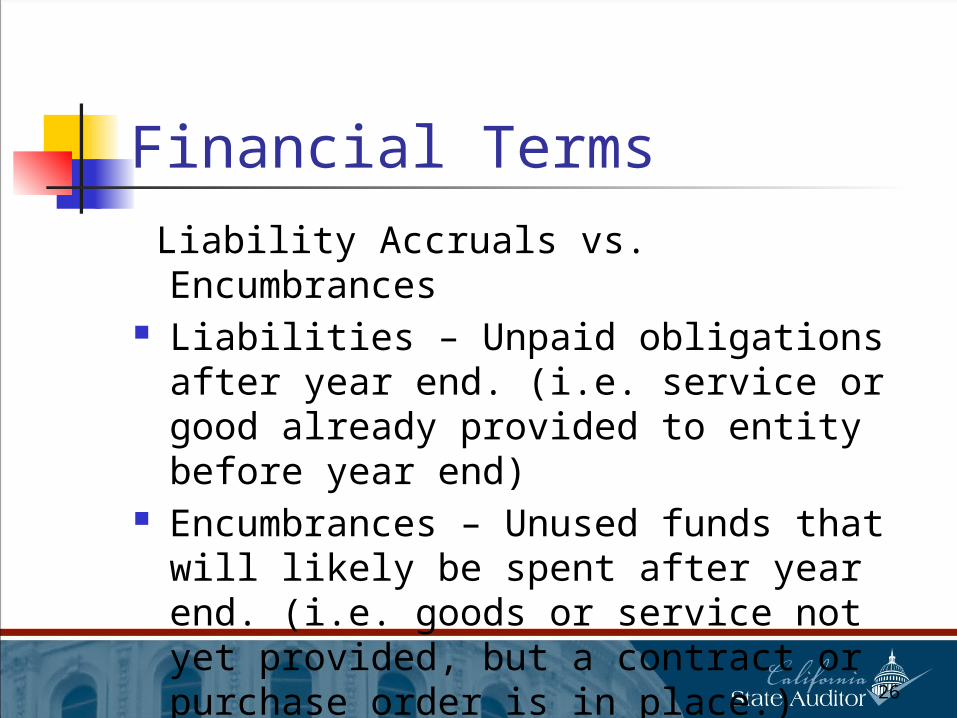

Financial Terms

Liability Accruals vs. Encumbrances Liabilities – Unpaid obligations after

year end. (i.e. service or good already provided to entity before year end)

Encumbrances – Unused funds that will likely be spent after year end. (i.e. goods or service not yet provided, but a contract or purchase order is in place.)

26

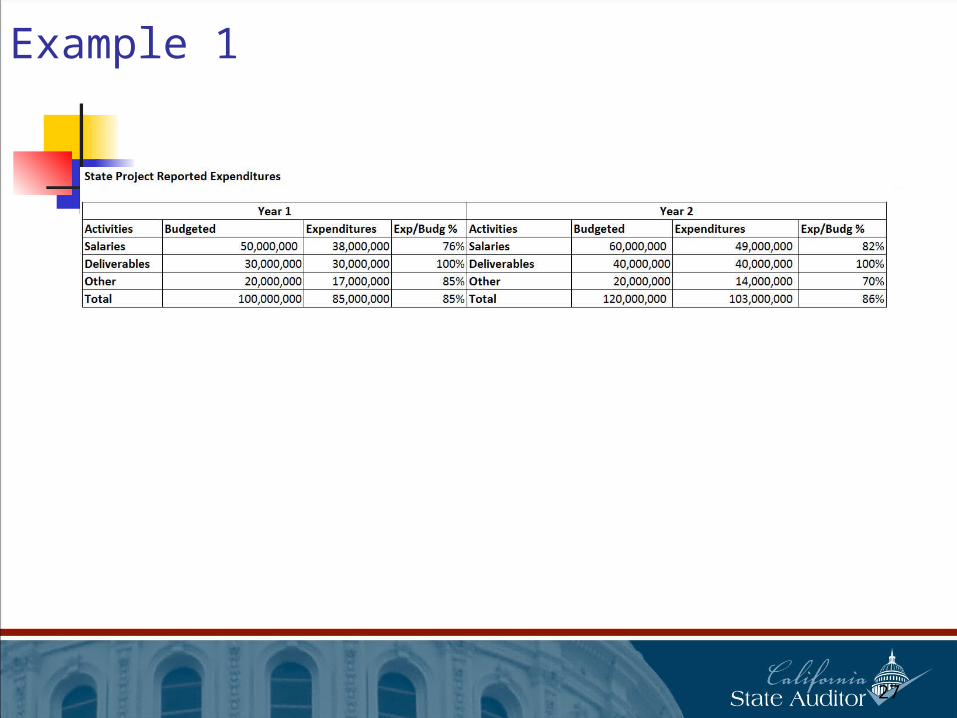

Example 1

27

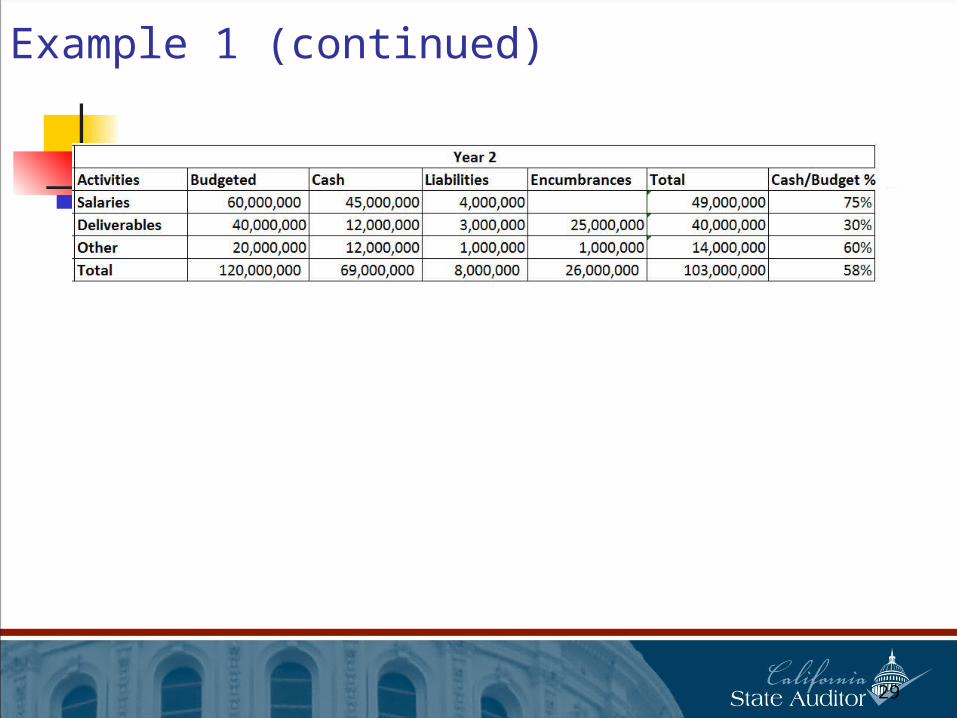

Example 1 (continued)

28

Example 1 (continued)

29

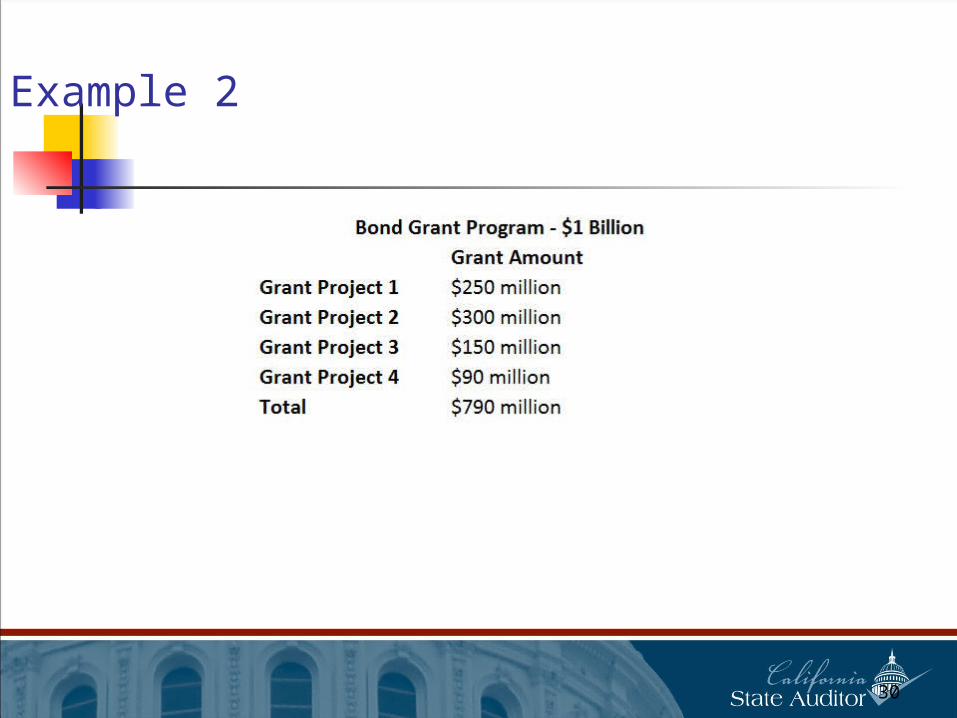

Example 2

30

Example 2 (continued)

31

Financial Statements and Audits/Reviews

Audited financial statements can provide valuable information to assist us in audits or reviews.

32

Financial Statements and Performance AuditsComponents of financial statements (governmental entity) Transmittal Letter: Preparer of statement introduces financial

statements (Not audited, not to be confused with audit opinion). Opinion Starts Management Discussion & Analysis (MD&A): Preparer describes and

analyzes its financial position, and provides an overview of its activities. (No opinion expressed, but limited procedures applied)

Financial Statements: Balance Sheet, income statement, and statement of cash flows. (Audited)

Footnotes: Additional information that is essential to a full understanding of the data in the financial statements. (audited)

Required supplementary information (RSI): Additional information that follows the footnotes, such as funding progress of pensions, reconciliation of budgetary to GAAP, and information on infrastructure. (No opinion expressed, but limited procedures applied)

33

Financial Statements and Performance Audits

Audit Opinion Definitions Unqualified: Financial statements are fairly

presented on a material basis. Qualified: Financial statements are fairly

presented with exceptions. Explanatory paragraph is included to describe these deviations.

Adverse: Financial statements are not fairly presented as a whole.

Disclaimer: Auditor could not perform work to issue an opinion.

34

Financial Statements and Performance Audits

Breakdown of financial statements Government-wide financial statements: Broad

overview of the government’s finances, and provides both long term and short term financial information. (Audited)

Fund Financials: Financial information by fund—a grouping of related accounts that is used to maintain control over resources that have been segregated for specific activities or objectives.

35

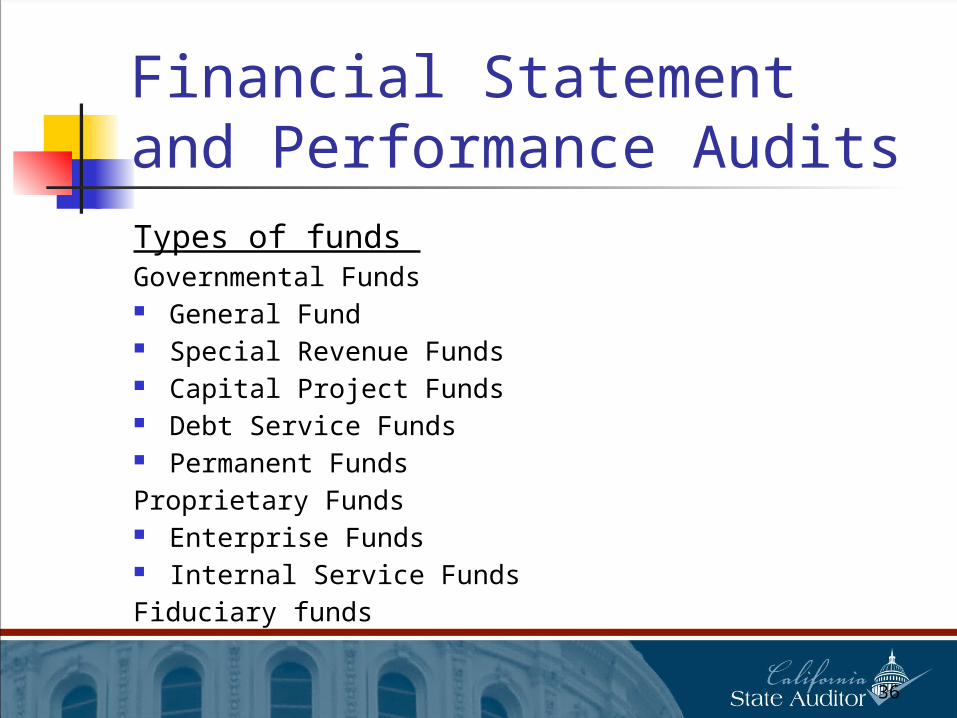

Financial Statement and Performance AuditsTypes of funds Governmental Funds General Fund Special Revenue Funds Capital Project Funds Debt Service Funds Permanent Funds Proprietary Funds Enterprise Funds Internal Service FundsFiduciary funds

36

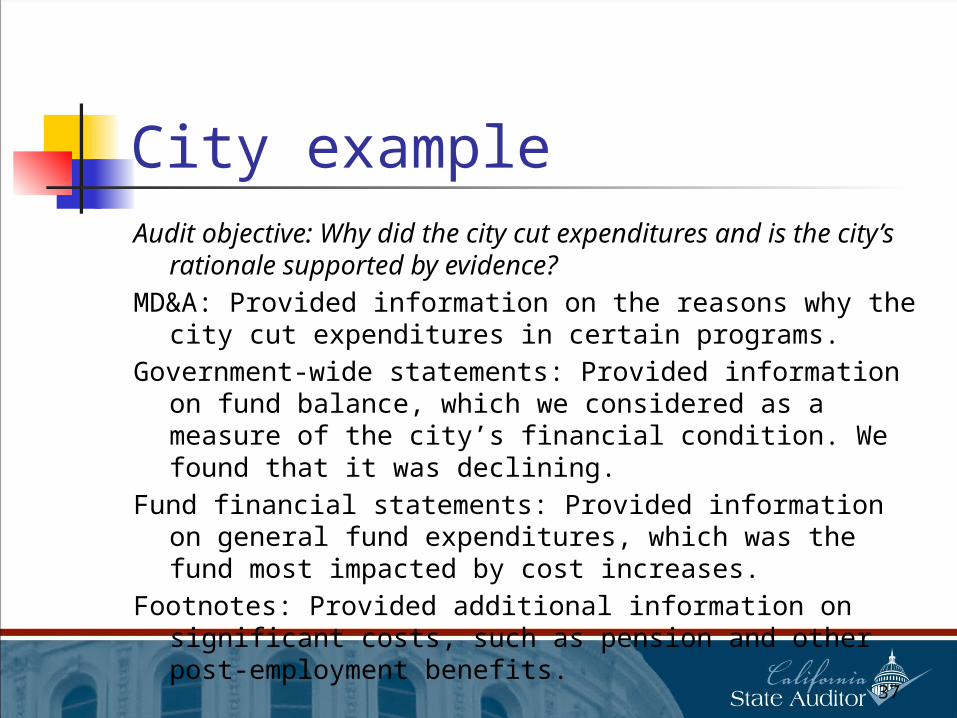

City example Audit objective: Why did the city cut expenditures and is

the city’s rationale supported by evidence? MD&A: Provided information on the reasons why the city

cut expenditures in certain programs.Government-wide statements: Provided information on

fund balance, which we considered as a measure of the city’s financial condition. We found that it was declining.

Fund financial statements: Provided information on general fund expenditures, which was the fund most impacted by cost increases.

Footnotes: Provided additional information on significant costs, such as pension and other post-employment benefits.

37

38

Questions?

ModeratorR. Kinney PoynterExecutive Director

NASACT

SpeakerNick Kolitsos, CPA

Senior AuditorOffice of the State Auditor (CA)

39

Intentionally Blank

References

Stephan J. Gauthier (2012) Governmental Accounting, Auditing, and Financial Reporting; Chicago, IL; Governmental Finance Officers Association of United States and Canada

Eric S. Berman (2013) 2014 Governmental GAAP Guide For State and Local Governments; Chicago, IL; CCH Incorporated.

Various Governmental Accounting Standards Board

pronouncements.

40