Embed Size (px)

DESCRIPTION

Â

Citation preview

POLICY GUIDE 2013

1 Connecting you to opportunity

PRIORITY AREAS:

PRIORITY AREAS: .......................................................................................................................... 1 SKILLS ............................................................................................................................................. 2

Summary .............................................................................................................................. 2 The Skills Show ..................................................................................................................... 4 Apprenticeships 1000 in 100 Campaign ..................................................................................... 4 Birmingham Baccalaureate ...................................................................................................... 5 The Youth Contract ................................................................................................................ 6 Young Talent for Business: Birmingham Jobs Fund ..................................................................... 6 Chamber Council Employability Campaign ................................................................................. 7

ECONOMY ...................................................................................................................................... 8

Summary .............................................................................................................................. 8 Export Markets ...................................................................................................................... 9 Employment .........................................................................................................................10 Access to Finance ..................................................................................................................10 Business Rates .....................................................................................................................11 Enterprise Zones ...................................................................................................................13 Regulation ............................................................................................................................14

TRANSPORT ................................................................................................................................. 16

Summary .............................................................................................................................16 HS2 .....................................................................................................................................17 Regional Airports...................................................................................................................19 Roads ..................................................................................................................................20 Regional Rail Network ............................................................................................................22 Transport Governance Review ................................................................................................23

LOCAL AND REGIONAL GOVERNMENT .................................................................................... 24

Police and Crime Commissioners .............................................................................................25 Birmingham Business Advisory Group ......................................................................................26 LEP .....................................................................................................................................27

EQUALITY AND DIVERSITY ......................................................................................................... 29

Women in Business ...............................................................................................................30 Shared Parental Leave and Pay ...............................................................................................31

OTHER .......................................................................................................................................... 33

EU .......................................................................................................................................33

2 Connecting you to opportunity

SKILLS

Summary

Background: Skills are the lifeblood of any economy and are vital to the economic development of our

city. Skills levels, however, vary enormously across the Greater Birmingham area.

Unemployment levels remain relatively high despite the significant number of frequently

high-level jobs being advertised in the region (10,000+ in Birmingham in April 2013 alone).

In particular, Birmingham has a high proportion of residents with no qualifications and

relatively low attainment of level 4 (degree equivalent) qualifications. This is reflected in the

city‘s highly worrying employment rate, which stands at just 57.0 per cent, compared with

70.6 per cent for the UK. Consequently, Birmingham‘s employers are forced to rely heavily

on in-commuters to meet skills requirements. Whilst this keeps employment rates higher in

other parts of the GSBLEP and the Black Country it does little to soothe Birmingham‘s own

unemployment problems. Whilst the recession has certainly played a role in the current

situation, extremely high levels of youth unemployment also reflect structural issues which

predate the collapse of the banking system.

In addition, careers advice for school age children and young people is an area of concern.

Following the 2011 Education Act schools are now required to commission their own

careers advice services as opposed to being required to use the centrally commissioned

service, Connexions. This has resulted in patchy and highly variable provision of careers

advice across the sector and concerns that young people are leaving school without

sufficient awareness of the career paths open to them and the skills and qualities needed

to succeed.

While business accepts that it will be necessary to train people to ensure that they have

‗job specific‘ skills the Chamber believes that it is not the responsibility of employers to

provide basic skills, such as literacy and numeracy. Too many employers are unsatisfied

with the literacy, numeracy and communication skills of their staff and job applicants.

In response to these issues Birmingham Chamber‘s Chamber Council has initiated an

Employability Campaign. This campaign aims to improve connections between schools,

young people and businesses, influence Government and decision makers to prioritise the

importance of these links and position the Chamber as ‗youth friendly‘ and diverse in

outlook and scope of activity.

3 Connecting you to opportunity

GBCC Position:

The Chamber believes that more needs to be done to ensure more people leave

school with essential literacy and numeracy skills.

The Chamber believes that schools, academies and colleges should endeavour to

work closely with businesses in order to aid in the provision of careers advice, work

experience and feedback on delivery of the curriculum. Chamber Council is directly

working to provide this connectivity and to make a real difference to young people‘s

lives through their Employability Campaign.

The Chamber supports apprenticeships as a positive means of up skilling our

nation‘s young people. The Chamber supports schemes aimed at making recruiting

and retaining apprentices easier for businesses.

The Birmingham Baccalaureate must reflect employer needs and requirements and

align with the national agenda to ensure its credibility and value to young people and

its recognition by schools as worthwhile and viable. In particular, we would support it

being accredited.

GBCC Activities:

Chamber Council is designing and delivering an Employability Campaign aiming to

provide connectivity between schools and businesses.

The Chamber is a member of the Birmingham Employment & Skills Board, which

directly informs the GBSLEP‘s skills and employment strategy.

The Chamber took a lead role in boosting engagement and recruiting businesses to

offer ‗Have-A-Go‘ sessions at The Skills Show 2012.

4 Connecting you to opportunity

The Skills Show

Background:

The Skills Show UK offers Birmingham a game-changing opportunity to tackle the city‘s

long-term skills shortages. It plays host to a range of skills competitions, awards and

activities. It is going to be hosted annually at the NEC between 2012 and 2014. The next

event will take place at the NEC, 14th-16th November 2013 and will consist of the best of

the nation‘s young talent performing at the WorldSkills UK Competitions, Have a Go at new

skills opportunities with local businesses, access to up to the minute careers advice and

access to Apprenticeships and real job opportunities from employers. Outside of the

exhibition, the Skills Show co-ordinates ‗Have-a-Go‘ sessions. These involve young people

taking part in work related activities and tasks organised by local businesses and learning

more about the world of work and career opportunities open to them.

GBCC Position:

The Skills Show UK is a highly positive initiative. The Chamber supports it and would

encourage businesses to get involved and offer ‗Have-a-go‘ sessions.

There is an important opportunity for the City Council, LEP and business to highlight

the show both is terms of its strategic objectives and direct economic benefits to the

area. The opportunities are endless.

However, its success depends upon our collective ability to align all partners behind

the initiative and to ensure ‗action on the ground‘ to deliver. This is challenging given

the fractured nature of the skills agenda and the number of different and competing

initiatives at play.

Apprenticeships 1000 in 100 Campaign

Background:

As part of the Chamber‘s skills agenda we have taken a lead role in promoting

Apprenticeships to businesses in the area. Under current Government policy employers of

16 to 24 year old Apprentices can apply for an Apprenticeship Grant, Apprentices can gain

key skills qualifications as part of the scheme and they will receive a National

Apprenticeship Certificate on completion of their Apprenticeship.

5 Connecting you to opportunity

Earlier this year Birmingham City Council and the National Apprenticeship Service

launched the ‗1000 in 100‘ campaign designed to create 1000 new apprentices in Greater

Birmingham between May and August 2013.

GBCC Position:

Despite the vast potential of apprenticeship schemes, uptake of apprentices

amongst businesses with fewer than 200 employees remains disproportionally low.

To counter this, the Chamber is supporting the Birmingham City Council & National

Apprenticeship Service ‗1000 in 100‘ campaign designed to create 1000 new

apprentices in Greater Birmingham between May and August 2013.

The Chamber is supporting Birmingham City Council‘s pledge to get 3000 young

people off Job Seekers Allowance and into work over the next year. Likewise we

work closely with local authorities and colleges across the full GBSLEP to support

their employability work with young people.

Birmingham Baccalaureate

Background:

In September 2013, Birmingham City Council will launch the Birmingham Baccalaureate.

The BBac is a central part of the Council‘s efforts to increase the employability of young

people and to foster closer working relationships between schools and employers.

GBCC Position:

We must ensure that the Birmingham Baccalaureate reflects employer needs and

requirements. It must align with the national agenda to ensure it is credible and

valuable to young people as well as being recognised by schools as worthwhile and

viable.

In particular, we would support the BBac being accredited.

6 Connecting you to opportunity

The Youth Contract

Background:

In response to the challenge of youth unemployment, the Government launched a £1billion

Youth Contract to help young unemployed people into work in April 2012. The Youth

Contract‘s offer of voluntary work experience, sector-based work academies,

Apprenticeships and wage incentives for employers hiring young people is the right short-

term prescription to help young people into work.

GBCC Position:

The Youth Contract‘s offer of voluntary work experience, sector-based work

academies, Apprenticeships and wage incentives for employers hiring young people

is the right short-term prescription to help young people into work.

The Government has learnt the lessons of the past by striving for a standard national

package that is easy for employers to understand and to access.

Unfortunately, despite their desire to help young people, too few employers know

about the Youth Contract and its opportunities.

The Government should show its willingness to invest in young people by extending

its regional marketing campaign pilot to the rest of the country.

Young Talent for Business: Birmingham Jobs Fund

Background:

In order to tackle Birmingham‘s high levels of youth unemployment, a Youth Employment

Multi-Agency Team (MAT) has been established to place young people into jobs, training

and other employment-related activities. In addition to championing the 1000 in 100

campaign, the MAT is responsible for establishing and operating the Birmingham Jobs

Fund wage incentive and ensuring its alignment with partner incentives such as National

Apprenticeship Service‘s AGE Grant and the Department for Work and Pensions‘ Wage

Incentive. These incentives have been introduced to make it as easy- and affordable as

possible- for Birmingham‘s employers to offer paid roles to young people.

GBCC Position:

The Birmingham Jobs Fund is a £2 million scheme designed to part-fund young

people‘s salaries in new roles across Birmingham. The Chamber is an advocate of

7 Connecting you to opportunity

the scheme which will help to up-skill and up-knowledge a significant number of local

young people by helping local businesses to utilise their abilities.

We support the Council in its innovative approach to incentivising local employers to

hiring young people through matching different funding streams across NAS and

DWP funding streams.

The Chamber is supporting a number of measures to assist young people into

finding work via our own Birmingham Chamber Training programmes and through

supporting critical events such as jobs and skills fair across our Chambers.

Chamber Council Employability Campaign

Background:

Businesses have long been vocal about wanting to play a greater role in the education

system and ‗give something back‘ to the workforce of tomorrow. In May 2013 Chamber

Council were asked to select an area they wanted to make a positive impact in and devise

a campaign. The result was the GBCC Chamber Council Employability Campaign. The

campaign aims to improve members‘ awareness of the importance of developing young

people‘s employability skills, promote business engagement with youth groups, schools,

colleges and universities, see a substantial increase in Chamber-led activity with young

people, influence Government and decision-makers to prioritise the importance of young

people-business engagement and to position the Chamber as ‗youth-friendly‘ and diverse

in outlook and scope of activity. This campaign will be launched in autumn 2013, to

coincide with the new school year.

GBCC Position:

The Chamber believes that schools, academies and colleges should endeavour to

work closely with businesses in order to aid in the provision of careers advice, work

experience and feedback on delivery of the curriculum.

Providing young people with the skills, knowledge and experience necessary to

compete in current and future jobs markets should be a high priority for educational

establishments.

Chamber Council is directly working to provide this connectivity and to make a real

difference to young people‘s lives through their Employability Campaign.

8 Connecting you to opportunity

ECONOMY

Summary

Background:

Having narrowly missed a double-dip recession at the beginning of 2012, economic

indicators are beginning to hint at signs of stability. Revised GDP figures for Q2 2013

showed growth of 0.7%. The Quarterly Economic Survey (QES) carried out GBBC

However, this stabilization is set against the backdrop of wider economic shifts such as the

Eurozone crisis. Improving business confidence against this will be crucial in generating

growth from the private sector. Access to finance is still a major issue for smaller firms;

lending growth rates to SMEs have been negative since 2009. SMEs account for almost

half of private sector employment and stunted growth can contribute to higher

unemployment making access to finance a major issue.

GBCC Position:

While controlling the budget deficit is a legitimate concern, more needs to be done

both on the supply and demand side to stimulate and rebalance the economy.

The Chamber support supply side efforts by the government to stimulate private

sector growth (such as the reduction in employers National Insurance contributions).

Short and long term economic stimulus in the form of major infrastructure projects

such as HS2 will provide the engine of growth needed by the West Midlands and

wider national economy.

Major capital spending projects have the potential to generate both technology and

skills which offer positive effects to the economy in the long term beyond the

immediate impact of the spending.

GBCC supports a rebalancing of government expenditure from current spending to

wealth-producing capital expenditure.

GBCC supports exporting as a national strategy to stimulate growth in the private

sector and help improve the nation‘s balance of payments. As such, both EU and

non-EU export markets should be promoted as viable export strategies for

businesses.

GBCC support the Business Bank for consolidation of SME funding streams and

clearer signposting.

GBCC Activities:

9 Connecting you to opportunity

GBCC produces the Quarterly Economic Survey, analysing the economic activities

of organisations based in the LEP area.

GBCC continues to work closely with the GBS LEP on its approach to economic

strategy.

Export Markets

Background:

Export markets in the West Midlands have grown significantly in the past decade, with the

total value of exports doubling from around £3bn in Q1 2009 to over £6bn in Q1 2013. A

significant proportion of these exports are machinery and transport, and this is a testament

to the renaissance the West Midlands is currently experiencing in advanced manufacturing

and automotive production. The continued success of firms such as Jaguar Land Rover is

a prime example of this.

The GBCC promotes an export strategy to both the EU and non-EU emerging markets.

The burgeoning middle class in China will be a crucial growth market for Midlands firms.

Birmingham Airport will have a role to play in the cultivation of links to emerging markets by

improving transport connectivity. However, while the value of exports is rising, the actual

number of firms exporting is proportionality lower. More support needs to be provided to

companies who may not realise their product is suitable for exporting.

The GBCC is home to a range of international trade services, from UKTI and Europe

Direct, to the issuing of export documentation. A recent international trade survey indicated

that users of UKTI were generally very satisfied with the level of service.

GBCC Position:

The Chamber believes that more needs to be done to support firms seeking to

export. We believe that the Chamber can play a key role in this.

The GBCC supports the findings of the West Midlands Economic Forum (Exports,

Economics, and Connectivity, 2013) that better air connectivity, i.e. point-to-point

airport connections, can lead to stronger regional export growth.

As such, the Chamber supports the expansion of Birmingham Airport‘s runway and

its ability to deliver direct flights to emerging markets as a means of boosting

exports.

10 Connecting you to opportunity

Employment

Background:

Unemployment affects Birmingham and the West Midlands disproportionately compared to

other UK regions. In June 2013, ONS statistics showed that the WM had an unemployment

rate of 9.4 per cent, second only to the North East. Unemployment began to grow rapidly in

the West Midlands during the latter half of the 2000s. Like other industrial cities, the

economy underwent reorientation – a shift towards the service sector, in the 1970s and

1980s. Many manufacturing jobs were relocated to lesser developed countries where the

cost of labour was cheaper. However, despite the high level of unemployment, the volume

of apprenticeships has risen significantly both at the national and regional level.

GBCC Activities

GBCC is focusing on forging links between business and schools to ensure that

students are exposed to key skills which are in high demand among businesses (see

SKILLS section of this document).

GBCC is working with the National Apprenticeship Service to promote

apprenticeships to both businesses and students.

Access to Finance

Background:

Access to finance is a consistently major concern for SMEs. Following the financial crisis of

2007-8, paralysis in the banking sector has affected borrowers across many sectors of

society – from businesses to mortgage borrowers. Despite the highly developed nature of

the UK‘s financial markets many SMEs (firms with 0-249 employees) are still unable to

obtain the finance they need.

This is not a new phenomenon. The Macmillan Report of 1931 indicated that small

businesses seeking finance of up to £250,000 (approx. £7million at present prices) faced

11 Connecting you to opportunity

discrimination. The report concluded that banks were failing industry, especially when

compared to the USA and Germany, and highlighted the divergence in interests between

the two groups. Bank depositors favoured high interest rates and a high level of liquidity,

whereas borrowers, i.e. industry, favoured low-interest rates and a guarantee that loans

would not be recalled quickly.

More recently, HM Treasury estimated that sums between £250,000 and £2million were

difficult to access. This market failure is even more significant when we consider that

SMEs account for around 99% of all private sector businesses in the UK and almost half of

all private sector turnover. Since 2009, lending growth to SMEs has been negative.

Lack of funding is both a demand and supply side problem. On the demand side, around

one third of SMEs do not look for external finance. Uncertainty of the economic climate

(e.g. the Eurozone crisis) could be causing a lack of demand. However, on the supply side,

loan rejection rates are far higher in the UK than in France and Germany. A BIS report

found 34% of SMEs applying for a loan were unsuccessful.

Private SME funding is effectively controlled by an oligopoly of the big five banks, making

up 90% of the SME banking market share. This is even higher than the 75% market share

the five banks have in the personal loan market. One of the key problems in getting

effective finance to SMEs is lack of awareness on the part of businesses. BIS has stated

that ―current awareness amongst SMEs of Government support… is relatively low and

knowledge about how to access the finance programmes is even lower‖. The Heseltine

Review likewise made a similar point on the complexity of business support currently

available.

GBCC Position:

The GBCC, like the British Chambers of Commerce, has supported the introduction

of a ―British Business Bank‖ that would provide finance for those unable to access it

through traditional banks, without crowding out or infringing on private sector

banking activity.

The Business Bank as proposed by Vince Cable in September 2012 can fulfil this

function.

However, questions need to be raised on the functionality of the bank. E.g. whether

the bank would have a regional or sectoral focus.

Business Rates

12 Connecting you to opportunity

Background: Business Rates are taxes levied on non-domestic properties such as businesses and warehouses. It is calculated by multiplying the rateable value of a property by a multiplier set by government. Different types of property have a different rateable value (e.g. Retail zones, storage, staff rooms). The multiplier is currently 45.8p. This means that for every £1 of the rateable value of their property, businesses must pay 45.8p in business rates. Click here for more information. There are several business rates relief schemes available, notably the small business rate relief and charitable rate relief. Click here for more information on business rate relief. Business rates go towards paying for local services. As of April this year (2013) local authorities are able to retain just under 50% of the value of business rates collected in their area. The remainder is sent to central government where it is pooled and redistributed to local authorities as a ―top-up‖ fund based on a set formula. Business rates have been a contentious issue amongst businesses for some time. They can represent a significant financial burden. Despite the recession, they have continued to rise annually in line with inflation. Business rates are usually reviewed every five years. The Government recently postponed the next business rates review until 2017. Some of the key recommendations of the Grimsey Review, which examined the future of the British High Street, are to reintroduce the 2015 business rates revaluation, freeze business rates from 2014 and introduce annual revaluations from 2017. GBCC Position:

The Government should be looking at measures to bring down business rates; heavily taxing inputs, like property, drags down business profitability.

Unless a business‘s premises are the size of a double garage, or if a firm is building speculatively over the next two years, there‘s little relief on offer.

The Chamber is currently working with a private sector partner to develop a product around business rate support relief.

Whilst we welcome the increased discretion and flexibility allowing local authorities to retain just under 50% of business rates provides, we believe that more needs to be done to ensure that revenue from business rates is spent in ways that are best for local businesses.

The Greater Birmingham Chambers of Commerce supports the principals of the recommendations made on business rates in the Grimsey Review.

We need increased consultation and communication between local authorities and businesses in our city to make sure business rates help pay for business needs.

13 Connecting you to opportunity

Enterprise Zones

Background:

Enterprise Zones (EZs) were first introduced in 1979 by the Conservative Government as a

means of granting areas relief from local rates and freedom from normal planning

regulations. In 2012, the Coalition Government announced 24 new EZs across the country.

As with the original EZs, businesses in the area will see business rate discounts over a

number of years up to a value of £275,000 and ―radically simplified‖ planning processes.

LEPs were given the responsibility of allocate EZs in their region. The GBS LEP chose Birmingham City Centre as its EZ location. Within this, there are 26 sites across the city which focus on four key industries; business and financial services, ICT sector, creative industries, and digital media. They are clustered into seven areas; the Westside, Snow Hill District, Eastside, Southern Gateway, Digbeth Creative Cluster, Birmingham Science Park Aston and the Jewelry Quarter.

In the Black Country, the EZ comprises of i54 Wolverhampton North, which focuses on

high-technology, and Darlaston, which focuses on environmental technologies.

Studies of the original EZs in the 1980s have suggested that wealth was largely

transferred. Merry Hill, in Brierley Hill, is seen as an example of wealth transfer, where

retail businesses simply moved from surrounding towns such as Dudley to the EZ.

However, the Docklands development in Canary Wharf, London is widely seen as a

success, going from 9,000 jobs pre-EZ to around 90,000 presently.

GBCC Position:

GBCC supports Enterprise Zones and any initiatives that can be put in place to

make Birmingham a more competitive, business friendly environment.

Business Zones, and the benefits they offer to businesses, need to be publicised to

capitalise on this initiative as much as possible.

14 Connecting you to opportunity

Regulation

GBCC members consistently cite regulation as a very significant barrier to business growth. In May 2013, the members of the GBCC identified regulation and associated red tape as the second largest barrier to growth and one of their top priorities for the Chamber‘s advocacy and campaign work. National surveys reconfirm the importance business places on regulation. A British Chambers of Commerce survey demonstrated that 62% of businesses see regulation as a key issue, presenting a burden that around 50% of businesses view as increasing. Smaller businesses appear to be disproportionately affected, with the Forum for Private Business calculating that they incur an estimate of £9.3 billion of internal costs a year. A survey conducted by the Federation of Small Business revealed that 33% of SMEs felt that regulation is the greatest barrier to business success. Regulation originates at both the European and national level- with much implementation led by local authorities and other agencies. This ranges from national regulators such as the HMRC, Gambling Commission and HSE to local councils charged with regulating aspects of business including trading standards, environmental health and licensing. A UK wide survey of 2000 businesses indicated that 80% of businesses felt that local councils have an important role to providing regulatory advice but 48% felt that councils do not currently have enough understanding of their business communities to enable them to regulate effectively. Throughout the downturn, we have seen businesses increasingly emphasise the impact of regulation on the bottom line- and more than this, their ability to grow and create jobs. Regulation is now seen by our members as a more significant barrier to growth than access to finance, the absence of wider business support and the skills shortage.

GBCC Position GBCC recognises the need for proportionate regulation, but it must be well targeted, risk-based and business friendly. Via the British Chambers of Commerce, we continue to campaign for better European regulation decision-making and for the end of the damaging practice of ‗gold-plating‘ of EU legislation when transposed into British law. Locally, we recognise our members‘ very real concerns around the sheer scale of regulation affecting their business and the need for a level playing field in terms of its application by different regulators/regulatory areas. We very much support the primary authority initiative and support all measures which harmonise and simplify regulation and its impact on business. Additionally, we also believe that a better quality of regulation could be understood as part of business support and play a very real role in terms of assisting local firms to grow. In part, this is because local regulators – unlike all other business-associated bodies- come

15 Connecting you to opportunity

into contact with more or less all local businesses and as such, have the opportunity to assist all businesses across their patch to grow and develop. We recognise, however, that to realise this opportunity huge shifts will have to occur in terms of local authorities‘ mind-sets as well as across local businesses and Government. We believe the new Regulators‘ Code is a step in the right direction and endorse the Government‘s position with regards to the ‗one regulation in, one regulation out‘ rule. GBCC Activities

The Chamber was the key private sector architect of the GBSLEP and through our close links to the LEP, we ensured that the original GBSLEP proposal to government highlighted the need for better regulation as an early priority. The Chamber then led discussions with the then Local Better Regulation Office to secure funding for the GBSLEP to become a pathfinder for the UK‘s new better regulation approach via LEPs.

The Chamber has worked hard to keep better regulation at the forefront of the LEP‘s business agenda as well as in separate dialogue with our LEP‘s local authorities and regulators. This has led to the LEP‘s 2013 Growth Strategy and Birmingham City Council‘s 2013 Leader Statement explicitly prioritising the importance of developing and implementing better regulation.

The GBSLEP-BRDO initiatives to date have been well-received by local businesses but we have much to do to expand the scheme to impact upon our key sectors and businesses more widely.

In September 2013, the Chamber assumed responsibility for the secretariat for the GBSLEP Regulation Steering and Delivery Groups. These groups will lead the GBSLEP‘s better regulation initiative- Better Business for All.

Via the BCC, we continue to lobby for better and less regulation at the national and European level including in terms of ending the practice of ‗goldplating‘ incoming European legislation.

16 Connecting you to opportunity

TRANSPORT

Summary

Background:

Top-quality transport systems form the backbone of economic development. Strong

transport infrastructure can increase both business activity and connectivity of a city, as

well as its desirability to residents and potential investors. Birmingham‘s central location in

the UK means that it is at the heart of the nation‘s logistics network and this provides a

very strong comparative advantage. Improvement of the regional, national, and

international transport networks will be a decisive factor in the city‘s ability to access new

markets.

Congestion and passenger capacity is increasingly an issue which the region needs to find

long term solutions for. Figures released by the Association of Train Operating Companies

in March 2013 show that the growth of passenger commuting in the region is among the

highest in the country. At the international level, greater air connectivity to emerging

markets will be crucial for exports and Foreign Direct Investment (FDI) in the region.

GBCC Position:

GBCC advocates an integrated strategy to alleviate future capacity problems and

unlock the economic potential of the region.

GBCC supports a comprehensive governance review (in line with the conditions set

in the Local Transport Act 2008) in order to better align transport bodies and provide

a stronger voice for business concerns.

The West Coast Main Line is currently the busiest trunk railway line in Europe, and

as such, viable alternatives need to be developed to create built-in contingency

GBCC supports the construction of a high speed rail link from London-Birmingham

(eventually connecting Birmingham to the North).

Additionally, substantial investment in the regional rail network will alleviate

passenger demand and allow for efficient integration in to the HS2 network.

GBCC supports the expansion of the Midland Metro line as a form of light rail

connecting destinations within the city centre.

17 Connecting you to opportunity

GBCC Activities:

GBCC has campaigned for a regional airport strategy and has supported

Birmingham Airport in its response to the Davies Commission.

GBCC has actively campaigned for the HS2 network.

The Chamber has expressed concern at the lack of rail investment for the West

Midlands in Network Rail‘s Strategic Business Plan.

The Chamber continues to host the Greater Birmingham & Solihull Business

Transport Group, which has representation from all the key transport stakeholders in

the region.

GBCC will continue to lobby to secure more funding for transport investment

The Chamber also supports diversification of parts of the transport network and has

supported initiatives such as Birmingham City Council‘s Cycle Revolution campaign.

HS2

Background:

High Speed 2 (HS2) is a planned rail line which aims to link London to Birmingham and

ultimately the North of the UK. The construction of HS2 is split into 2 phases:

Phase 1 will link London to Birmingham and is due to be completed by 2026;

Phase 2 will link Birmingham to the North West and Yorkshire by 2032.

In a survey conducted by GBCC in September 2013, over 70% of businesses believe that

the project would have a positive economic impact on the West Midlands. GBCC supports

the establishment of a new north-south railway primarily for capacity and economic

reasons.

Capacity

Demand for rail travel continues to grow rapidly and estimates show that by the 2020s, the

West Coast Main Line will be full. DfT passenger figures show that in 2011, during the

morning peak, an average of 5,000 passenger were standing on arrival into Birmingham,

and 4,000 passengers were standing on arrival into London Euston. The ORR has also

18 Connecting you to opportunity

reported growth of 14% in WM rail journeys over the previous year and both Birmingham

and Coventry are in the top four UK cities for rail growth.

Economic benefits

In September 2013, KPMG released a report on the regional economic impacts of HS2,

and estimated that the project could generate between £1.5 billion and £3.1 billion per

annum for the West Midlands. Centro have also stated that the Y-network (connecting

Birmingham to Manchester in the West and Leeds in the East) could generate over 50,000

additional jobs. Nationally, the project could generate £15 billion per annum, with £5billion

in tax receipts to government.

The HS2 terminus in Birmingham city centre has the potential to completely transform the

surrounding area and further regenerate the Eastside area of the city. High speed lines

have had regenerative effects on cities across the world. In France, Lyon and Lille saw

major office, retail, housing, and hotel developments following the construction of the TGV.

In the UK, HS1 (connecting London to Europe) helped cause major redevelopment in the

King‘s Cross, Stratford, and Ebbsfleet areas, which is expected to generate 15,000 homes

and 70,000 new jobs.

Opposition to the scheme

Several reports have been critical of the economic case for HS2. In May 2013, the National

Audit Office (NAO) stated that the project had a £3.3 million funding gap, while the Major

Projects Authority (MPA) gave HS2 an ―amber/red‖ rating. However, the reports

themselves have attracted criticism. Both the Department for Transport (DfT) and the

British Chambers of Commerce have argued that the NAO report is based on obsolete

data from 2011. The DfT also stated that the MPA rating is actually a view from June 2012,

and that once risks outside the direct control of the HS2 project team are removed, the

rating is in fact amber, meaning that successful delivery is feasible if key concerns are

addressed.

Other reports have argued that the cost of the line could be better spent elsewhere, such

as on high speed internet and while the Chamber would agree that more investment needs

to be channelled into ultra-fast broadband, this is not a sufficient alternative to HS2. A

recent survey conducted by the Birmingham Chamber showed that 37% businesses

believed that the internet/remote access had not had an impact on their travel, while 41%

said it had decreased their level of travel only slightly. Alternatives to HS2 have been

assessed and they confirm they will not deliver HS2‘s objectives.

19 Connecting you to opportunity

GBCC Position:

HS2 is needed to bring the UK‘s transport infrastructure into the 21st Century,

connect the great cities of England, boost regional economies and provide the extra

capacity required to keep our rail network running.

GBCC will work with the HS2 Growth Task Force to ensure that the region receives

the maximum economic benefit from the project and benefits businesses.

GBCC will lobby for further projects to enhance the ease of access and ease of use

of HS2 facilities in the region.

GBCC endeavours to make its members aware of HS2 procurement opportunities.

Regional Airports

Background:

In 2012 the economist Howard Davies was commissioned to chair the Airports

Commission, which is tasked with examining the UK‘s airport capacity and how this

demand can be met. As a part of this, airports have been requested to submit discussion

papers to make their case. GBCC fully endorsed Birmingham Airport‘s (BHX) response to

the commission, and continues to provide support to ensure that BHX is seen as the

region‘s hub airport.

Studies by the West Midlands Economic Forum have shown a correlation between

increased air connectivity and increased export capacity. Heathrow and Gatwick currently

host around 1,800 direct flights per year to China, compared with 36,000 to the USA. With

enhanced air connectivity, Birmingham Airport can exploit this market. The extension of the

existing runway at BHX, which is currently under construction, will be a crucial element to

this strategy. An extended runway will enable direct connections to long-haul destinations

such as China, and will put BHX on an even footing with Manchester and Heathrow in

terms of long-haul destinations.

GBCC Position:

GBCC has supported BHX in its submission to the Davies Commission and co-

signed joint responses along with the Black Country LEP, GBS LEP, and Black

Country Chamber of Commerce.

20 Connecting you to opportunity

The Chamber believes that broader air connectivity from Birmingham Airport will be

crucial in helping to open up international trade and FDI for Birmingham and the

wider West Midlands.

GBCC has supported the runway extension and successfully campaigned for the re-

routing of the A45 in order to facilitate the development.

GBCC has formally support the ―Fair Tax on Flying‖ campaign which seeks to

reduce the rate of Air Passenger Duty (APD). APD in the UK is among the highest in

the world, and this can have impeding effect on air connectivity.

Roads

Background:

Whilst all forms of transport infrastructure are crucial to a functioning, developed economy,

road travel remains the most popular form of transport in the UK. The ONS National

Transport Survey 2011, the most recent version available, suggests that approximately

64% of all trips British citizens make are made as either the driver or passenger of a road

vehicle.

There are currently numerous policies in place relating to road traffic and road

improvements. In his 2011 Autumn Statement Chancellor George Osborne outlined many

of the UK Government‘s growth initiatives, which included the pinch-point programme.

Pinch Points are traffic congestion points, intersections or short lengths of road at which a

traffic bottlenecks exist, slowing down the broader network. They cause a build-up of traffic

and travel delays at these spots and on the wider road network. The pinch-point

programme, delivered by the Highways Agency, aims to target these hot-spots across the

country and implement small scale improvements.

Managed motorways are motorways that use active traffic management techniques to

improve capacity. This involves activities such as variable speed limits and running the

hard shoulder at peak times. Birmingham‘s M42 and M6 both have managed motorway

initiatives in place at various sections and junctions.

The M6 Toll, also called the Birmingham North Relief Road, connects M6 Junction 4 at the

NEC to M6 Junction 11A at Wolverhampton with 27 miles of six-lane motorway. The

weekday cash cost is £5.50 for a car and £11.00 for an HGV. Designed to alleviate

21 Connecting you to opportunity

congestion on the busiest section of the M6, the toll road was first opened in 2003. The toll

road was a public-private finance initiative and is currently operated by Midland

Expressway, a subsidiary of the Australian Macquire Group. Since opening traffic volume

on the road has been below the level forecasted. In 2012 the Macquire Group wrote

£150million off the value of Midlands Expressway in response to the decreased flow of

traffic and reduced revenues.

GBCC Position:

The road network is still the overwhelming preference for travel among workers and

businesses.

GBCC supports the government‘s pinch-point programme to identify small—scale

improvements in sections of the road network to alleviate congestion. Motorway

widening where possible should also be viewed as an option to alleviate traffic in the

long-term.

GBCC supports the expansion of managed motorways, namely the management of

motorways (such as variable speed limits) based on effective use of data and traffic

patterns.

GBCC supports the exploration of alternatives to the current M6 toll arrangement,

which has seen a fall in usage in recent years, to ensure that the impact on

congestion is efficiently managed, while acknowledging the interests of investors.

22 Connecting you to opportunity

Regional Rail Network

Background:

Strengthening the regional rail network must be a crucial part of long term transport

infrastructure development. This is particularly true of the need to integrate regional rail

with HS2. Passenger commuting to and from Birmingham in the West Midlands has more

than doubled in the last five years. In this time overall passenger growth in Birmingham

and Coventry has risen by 22 per cent and 30 per cent respectively, with the latter being

the highest increase in the country.

The Chamber has expressed concern over the lack of planned investment for the Midlands

contained in the Network Rail Strategic Business Plan (SBP) for operational period 5

(OP5), 2014-19. Under the current SPB, by 2019 we could expect to see a potential seat

shortfall of 7,650 seats during the peak 3 hours, with a shortfall of 3,460 during the top

peak hour alone. The SBP also raises questions over the equitable distribution of

resources. Under SBP plans an additional 89% of seats will be delivered to Manchester

during the 3 hour AM peak time, compared to less than 10% for Birmingham.

On 16th July 2012, the coalition government announced the overhead electrification of the

Chase Line between Rugeley Trent Valley and Walsall, with work scheduled to take place

between 2014 and 2019. It is estimated to cost around £30m, as part of a £9.4bn package

of investment in the railways in England and Wales. The electrification would improve

journey times and allow the Birmingham to Liverpool Lime Street service to run via Walsall.

The line is a fast growing key commuter route to Birmingham and the conurbation, and

now generates nearly 600,000 passenger journeys a year in the district. In 2012 alone an

additional 91,000 passengers used the rail service, with increases in use of between 13

per cent and 29 per cent at Cannock, Hednesford and Rugeley Town. In May 2013 it was

announced that all electrification of the line would be postponed until 2019.

The Whitacre Link is a proposed scheme to reopen a disused section of railway which

passes close to the proposed HS2 station at Birmingham Curzon Street. The railway has

been disused since 1917. The scheme would open up a wide range of opportunities to

provide direct rail services from HS2 to towns and cities across the West Midlands. The old

Walsall-Stourbridge line, also known as the South Staffordshire line, currently only

operates limited services between Round Oak Steel Terminal in Brierly Hill and

Stourbridge Junction. In 2011 plans were announced for re-opening the line using Tram

Trains (connecting it to the Midlands Metro) and freight services. These plans remain at

23 Connecting you to opportunity

proposal stage subject to securing adequate funding to cover the estimated £268million

cost.

GBCC Position:

The Network Rail SBP should be reviewed and additional investment allocated to Midlands rail infrastructure.

With the vast increase in traffic in recent years, electrification of the Chase Line between Rugeley Trent Valley and Walsall is essential for wider regional growth.

The Chamber supports the proposal to re-open the Whitacre line between Birmingham Airport and Hampton-in-Arden. The new route would improve access to Birmingham Airport for passengers traveling from the north.

Together with the potential reopening of the Walsall-Stourbridge line, the Whitacre

Link could form the beginnings of a Western Orbital railway line which links the Black

Country, South Staffs, and south Derbyshire to Birmingham Airport. An infrastructure

development of this nature would provide the long term benefits associated with

improved connectivity as well as short term economic stimulus.

Transport Governance Review

Background:

In March 2013 the West Midlands Metropolitan District Leaders Group announced their

intention to hold a Transport Governance Review. The West Midlands consists of seven

Metropolitan Districts (the City of Birmingham, the City of Coventry, and the City of

Wolverhampton, as well as Dudley, Sandwell, Solihull, and Walsall). Each of these districts

holds their own transport planning powers and funding. West Midlands Metropolitan District

Leaders Group has proposed converting the Integrated Transport Authority (the

governance body for CENTRO) into a Joint Committee, to consist of the 7 leaders of the

Metropolitan Districts. They argue that this new structure will ensure greater co-ordination

and co-operation in the creation, and unified and effective implementation of, cross-

regional transport strategies.

GBCC Position:

GBCC supports the proposal to hold a Transport Governance Review.

GBCC would like to see greater co-operation and consultation with business groups,

including the Business Transport Group, established by GBCC.

24 Connecting you to opportunity

LOCAL AND REGIONAL GOVERNMENT

Summary

Background:

There are several political/quasi political bodies influencing the policy agenda in the West

Midlands. The newly installed Police and Crime Commissioner leads on policing and

community safety, the Greater Birmingham and Solihull LEP leads on skills, employment,

transport and growth agendas and the Birmingham Business Advisory Group seeks to

influence Birmingham City Council and create a united voice for business.

GBCC Position:

The elected Police and Crime Commissioner must recognise the impact of crime on

businesses and work with them to reduce levels of business crime, fear of crime and

build a positive relationship between the business community and the police.

The Birmingham Business Advisory Group represents a great opportunity to create a

shared agenda for businesses in the city and influence local and regional policy.

The Chamber supports the LEP and favours further devolution of power and

resources to the regions, provided governance structures are strengthened

accordingly.

GBCC Activities:

In September 2012 the Chamber launched the GBCC Police and Crime

Commissioner Manifesto based on members‘ views.

The Chamber organises quarterly BBAG Meetings.

The Chamber supports LEP activities by facilitating business engagement and

stands ready to play a leading role in terms of design and delivery of the GBSLEP‘s

business support agenda particularly in terms of business advice and support

signposting.

25 Connecting you to opportunity

Police and Crime Commissioners

Background:

On the 15th November 2012 the first ever Police and Crime Commissioner Elections took

place. Excluding the London Metropolitan area, where PCC powers are held by the

Mayor‘s office, every police force across the UK now has their own democratically elected

PCC, who wields significant influence over the policing priorities, and budget, of their

region‘s police force. PCC‘s are required to produce a Police and Crime Plan shortly after

gaining office detailing their strategy for their region‘s police force and budget. The West

Midlands Police and Crime Commissioner is currently Labour‘s Bob Jones and the next

elections will take place in May 2016. Police and Crime Commissioners have their actions

and budgets scrutinised by a Police and Crime Panel made up of between 10 and 18 local

councillors and 2 independent members. The West Midlands PCP is made up of twelve

local councilors from Birmingham, Coventry, Dudley, Sandwell, Solihull, Walsall and

Wolverhampton, and two co-opted independent members.

GBCC believes that businesses are often the forgotten victims of crime but, with business

crime in the UK costing approximately £8000 per business per year, these criminal acts

represent a major issue to our economy and society. Businesses are also impacted

financially by changes to policing priorities. Many Chamber members either currently

provide supplies and services to the police force or could do in the future. Some, such as

social enterprises, are heavily reliant on Community Safety Grants for their continuing

activities.

GBCC Position:

In September 2012 GBCC published research into Business Views on Police and Crime

Commissioner Priorities and an associated Manifesto. We launched this research at a

PCC candidates hustings hosted at the Chamber. From this research we developed

several key recommendations including:

We believe that tackling crimes against business should be a priority. Levels of

business crime, and perceived levels of crime, can have a negative impact on

business location and investment decisions. Reducing crime and fear of crime

against the business community can help encourage economic growth in the city.

We believe that the PCC should commit to strengthening and raising awareness of

community safety initiatives. In order to achieve this we recommend that in the first

26 Connecting you to opportunity

instance a central online resource is created which lists the location, information on

and the contact details of said initiatives in the West Midlands policing area.

The elected Police and Crime Commissioner should work to improve the relationship

between businesses and the police force.

The Police and Crime Panel should include a representative of the business

community as one of their independent members. Business organisations across the

west Midlands must raise awareness of the role and encourage their members to

apply. Given that the independent PCP members for this term have already been

selected, this is a recommendation for the next time selection opens in 2016.

Birmingham Business Advisory Group

Background:

In Birmingham there are a lot of organisations that represent business and/or present

views on the economic and business agenda. As well as the Chamber of Commerce there

are; the Local Enterprise Partnership (LEP), Marketing Birmingham, the city Council,

Birmingham Future, ten Business Improvement Districts and various other private and

public sector organisations. This can lead to conflicting messages on what the business

community want from the city leadership.

In early 2013 Birmingham Chamber Chief Executive Jerry Blackett was invited to join the

Leader‘s Advisory Board (LAB). The LAB features representatives from across the public,

private and third sectors and aims to advise Sir Albert Bore, leader of the Birmingham City

Council, on key issues affecting the city. Jerry‘s role is to represent Birmingham

businesses. In order to facilitate this he established the Birmingham Business Advisory

Group (BBAG). Representatives from the major business organisations across

Birmingham are invited to attend (GBCC, IOD, FSB, MAS, EEF, CBI, BCC, Business

Improvement Districts and Birmingham Future) and the BBAG meets quarterly to raise

issues affecting Birmingham‘s business community and share information on opportunities

with the rest of the group. This information is the communicated to Sir Albert Bore and the

Leaders Advisory Group. One strand of BBAG activity is to develop a shared agenda for

business organisations in the city: a key set of aims, objectives and concerns that can

provide a clear message on the views of businesses in the city region.

27 Connecting you to opportunity

GBCC Position:

The Chamber believes that business organisations in Birmingham must work

together to deliver a shared message in favour of the City and its economic

interests.

The BBAG represents an excellent environment through which its partners can work

together to articulate the Birmingham agenda.

The City Leadership has the opportunity to play a significant role in creating this

‗shared agenda‘ now which should not be missed.

For our part, the Chamber will continue to be the lead body that coordinates and

aligns the work of other business membership organisations behind a common,

shared agenda.

LEP

Background:

The Greater Birmingham and Solihull LEP (GBSLEP) was co-founded in November 2010

by the Chamber and Greater Birmingham‘s local authorities. The GBSLEP is a partnership

between local authorities and the private sector, led by business, charged with providing

the vision, knowledge and strategic leadership to drive sustainable private sector growth

and job creation. The GBSLEP covers the local authority areas of Birmingham,

Bromsgrove, Cannock Chase, East Staffordshire, Lichfield, Redditch, Solihull, Tamworth

and Wyre Forest.

During the founding of the GBSLEP, the Chamber was instrumental in ensuring the

GBSLEP included the southern Staffordshire local authority areas reflecting the wishes of

local businesses. The Chamber also defined the business agenda of the GBSLEP and in

particular, its early policy priorities around critical areas such as better regulation, the

development of infrastructure and securing a strong settlement from the Regional Growth

Fund (RGF).

The Chamber continues to support the GBSLEP. As such, the Chamber is the only private

sector representative on the LEP‘s Executive Steering and Officer Steering Groups as well

strong contributors to a number of working groups including the Employment & Skills

Board. The Chamber provides the secretariat to the Greater Birmingham Business

Transport Group, which advises the LEP on transport and infrastructure requirements.

28 Connecting you to opportunity

Most recently, the Chamber enjoyed a fruitful dialogue with the GBSLEP regarding the

LEP‘s economic strategy. The LEP‘s Strategy for Growth is highly reflective of our

members‘ priorities and the Chamber‘s submission. The Chamber also responded to the

LEP‘s Greater Birmingham Project, which sought to provide a blue print for the

implementation of Lord Heseltine‘s No Stone Unturned report. The Chamber‘s Growing

Businesses and Jobs report was recognised by Lord Heseltine as ‗ground-breaking‘ and

outlined how the Chamber could boost competitiveness and productivity through the

development of a funded signposting and growth boosting service.

GBCC Position:

The GBSLEP is well-respected by national government and in coordination with a

reinvigorated Birmingham City Council, leaves our region well-positioned to benefit

from national Government policy such as the Heseltine single shared pot.

The Chamber is in favour of increased devolution to the regions and welcomes the

growing investment in the resources and capacity of the GBSLEP to play this role.

We note, however, that this should be complemented by improved local and regional

governance in the form of the creation of a Combined Authority across the LEP and

Black Country areas and the introduction of a regional mayor.

LEPs remain the Government‘s preferred vehicle for economic development and are

likely to be retained in some form post-2015 regardless of the outcome of the next

General Election.

The Chamber will continue support the GBSLEP‘s agenda including in terms of

facilitating its business engagement with our membership and the wider business

community.

The Chamber stands ready to play a leading role in terms of designing and delivery

of the GBSLEP‘s business support agenda particularly in terms of business advice

and support signposting.

29 Connecting you to opportunity

EQUALITY AND DIVERSITY

Summary

Background:

Equality, in particular gender equality, in UK businesses has been a hot topic this year.

Data has been released that shows efforts to increase the proportion of women on boards

in top companies are slowing. The EU has been debating quotas for women in non-

executive positions on boards and the Government has announced plans to introduce

shared parental leave. The need for encouraging diversity and to understand the impact of

forthcoming/potential equality legislation on businesses has rarely been greater. As a

consequence GBCC has been looking into the Equality and Diversity agenda focusing, so

far, on Women in Business and Shared Parental Leave and Pay.

GBCC Position:

Diversity is good for business.

More needs to be done to improve and promote diversity at senior levels. Business

lead change is preferred to legislative/government intervention.

Shared Parental Leave and Pay is a fantastic idea in principal but the details of

some of the proposals are giving cause for concern.

GBCC Activities:

GBCC is working on a Diversity How-To Toolkit for businesses offering simple,

straightforward advice on how to design and implement low cost initiatives aimed at

improving the diversity of their workforce.

GBCC supports the idea of Shared Parental Leave but is keeping abreast of any

updates to the proposals to ensure that concerns regarding how the administration

of shared parental leave will work are heard.

National Activities:

The British Chamber of Commerce recently published their Business is Good for

Equality booklet in partnership with the Government Equalities Office. This

document details issues discussed in various Business is Good for Equality

workshops such as recruitment, Think, Act, Report and disability. It also features

some short best-practice ideas and case studies.

30 Connecting you to opportunity

Women in Business

Background:

Numerous studies have shown having an equal balance of women at all levels of seniority

is good for businesses. Evidence suggests that companies with strong female

representation at top management level perform better than their less equal counterparts

and that gender diverse boards positively impact on performance.

The UK as a whole does not have the best track record with ensuring equal representation

of women at senior levels. In 2008 it was estimated that at current rates of change it would

be over 70 years before FTSE 100 firms would have gender balanced boardrooms.

Currently, women make up 17.3% of boards in FTSE 100 firms, 40% of department heads

and 24% of chief executives and managing directors across the UK. Recent research

revealed that, in 2012, women made up just 8.2% of boards in West Midlands listed

companies. Equal pay in the UK also remains an issue, with women earning on average

20.2% less than men.

There is no doubting the on-going trend of ‗blockage‘ in the talent pipeline preventing equal

numbers of women from reaching the most senior positions. National studies have cited

the various reasons for this including; additional family and childcare responsibilities,

difficulty advancing after returning to work after having children, a lack of professional

networks or sponsors at senior levels, potential unhelpful attitudes from individuals and

groups of both genders and weaknesses within recruitment and talent identification

practices.

Between February and March 2013 the Greater Birmingham Chambers of Commerce

undertook research into members‘ views on key gender equality policies. One of the key

findings of The Women in Business: The Greater Birmingham Picture report was that,

whilst 86% of respondents believed that at least one additional measure should be put in

place in their organisation to promote equality, 78% identified at least one barrier

preventing their organisation from tackling gender inequality. Top amongst the barriers

identified were financial costs of implementing change and a lack of awareness of what the

root causes of inequality are. Consequently the Greater Birmingham Chambers of

Commerce is seeking to create a ‗Women in Business: Diversity Toolkit‘ offering simple,

straightforward advice on low cost ways of promoting diversity such as mentoring schemes

31 Connecting you to opportunity

and understanding and tackling unconscious bias. This toolkit will be launched at an event

in October.

The Women in Business report also revealed that, whilst 64% of businesses believed that

more should be done to increase the proportion of women on boards the majority, 56%

were opposed to quotas. 63% of businesses surveyed believed that improvements in

equality should be business led. Only 19% identified government legislation as their

preferred way forward.

GBCC Position:

Having a diverse workforce at all levels of seniority is good for business.

Women make up approximately half of the workforce but only significantly smaller

proportions of senior positions. More needs to be done to challenge this.

Businesses are not in favour of legislative intervention such as quotas and instead

favour business lead change.

More needs to be done to raise awareness of low cost measures businesses can put

in place to have a positive impact on diversity and equality in their workforce.

Shared Parental Leave and Pay

Background:

Currently all mothers meeting certain employment criteria qualify for up to 52 weeks

maternity leave and 39 weeks maternity pay. The first 6 weeks of maternity pay are paid at

90% of average weekly earnings (before tax) and the remaining 33 weeks at the statutory

minimum £136.78 a week or 90% of average weekly earnings (whichever is lower) for the

next 33 weeks.

Between February and May 2013 the Department for Business, Innovation and Skills held

a consultation into plans for Shared Parental Leave and Pay. The consultation is now

closed and the feedback will be used to review proposals before they are implemented in

2015. Under the plans for Shared Parental Leave and Pay as they currently stand parents

will be able to split maternity leave. Mothers will be required to take the first two weeks

leave after birth but thereafter they will be able to transfer untaken leave and pay to their

32 Connecting you to opportunity

partners giving couples up to 50 weeks total leave to split between them. Partners will be

able to take parental leave at the same time if they choose, provided that their plans are

approved by their employers. This will be an opt-in system. Parents who do not request

access to shared parental leave will continue to be able to access traditional maternity and

paternity arrangements. Parents can request sections of flexible leave whenever they like

provided they give a minimum of 8 weeks‘ notice and gain the approval of their employer.

Parents will be responsible for agreeing plans with their employers separately – the

employers will not be required to liaise with each other. If an employee is unable to agree

plans with their employer, the employer can insist that the employee take their entire

entitlement of leave in one solid block.

One of the key findings of the GBCC Women in Business: The Greater Birmingham Picture

report was that many businesses had concerns over the impact the shared parental leave

and pay will have on businesses. As a result GBCC held a focus group and created a

consultation response to the proposal.

GBCC Position:

In principal GBCC entirely support the idea of Shared Parental Leave and Pay.

Ensuring that both parents are able to maintain strong links to both the workplace

and family is highly important.

However, the administration of Shared Parental Leave and Pay as the proposals

stand will be far too complex. The system lacks structure in a way that is likely to be

onerous for both new parents and employers. It is highly important that BIS clarify

their proposals and provide a system that is easy to understand and supports

parents and employers through the process at every step. Without the support of

both employers and parents these potentially game changing proposals will fail to

make the desired positive impact.

Furthermore, more needs to be done to raise awareness of the existence of

alternative parental leave options (such as paternity leave) to encourage greater

uptake. Until all of these schemes become common knowledge uptake will remain

low.

33 Connecting you to opportunity

OTHER

EU

Background:

At present the Coalition Government is seeking to open up negotiations to re-define the

UK‘s relationship with the EU. If successful, and if the Conservatives are still in

government, they aim to hold a referendum in 2017. Some backbenchers, particularly

Conservatives, are unhappy with progress on this agenda. No Bill outlining the referendum

was introduced in the Queen‘s speech in May 2013, which caused a back-bench rebellion

as Euro-sceptics unsuccessfully attempted to get an amendment including it through the

Commons. In short debate on this topic is highly contentious and divisive. Generally, those

for withdrawing from the EU see it as unnecessarily invasive, interfering in policy areas that

it should not, limiting the sovereignty of the UK in a highly detrimental way and risking the

economies of its members through continuing problems with the Euro. Those for

maintaining the relationship view the benefits as outweighing the negatives and cite the

economic benefits gained from the free market and trade negotiations, believe isolating

Britain from the EU would dramatically reduce the UK‘s international influence and power

and feel that, since the UK would continue to be influenced by EU regulation even if it did

withdraw (thanks to close economic and social links with the area) it is better to have a

strong voice in Europe than no voice. The third perspective falls between these two views,

believing that the UK should renegotiate its relationship with the EU to take advantage of

mutually beneficial trade, diplomatic and policing agreements, but limit Brussels‘ influence

over decision making in the UK.

Issues with EU regulations have been a recurring theme in Chamber surveys for some

time.

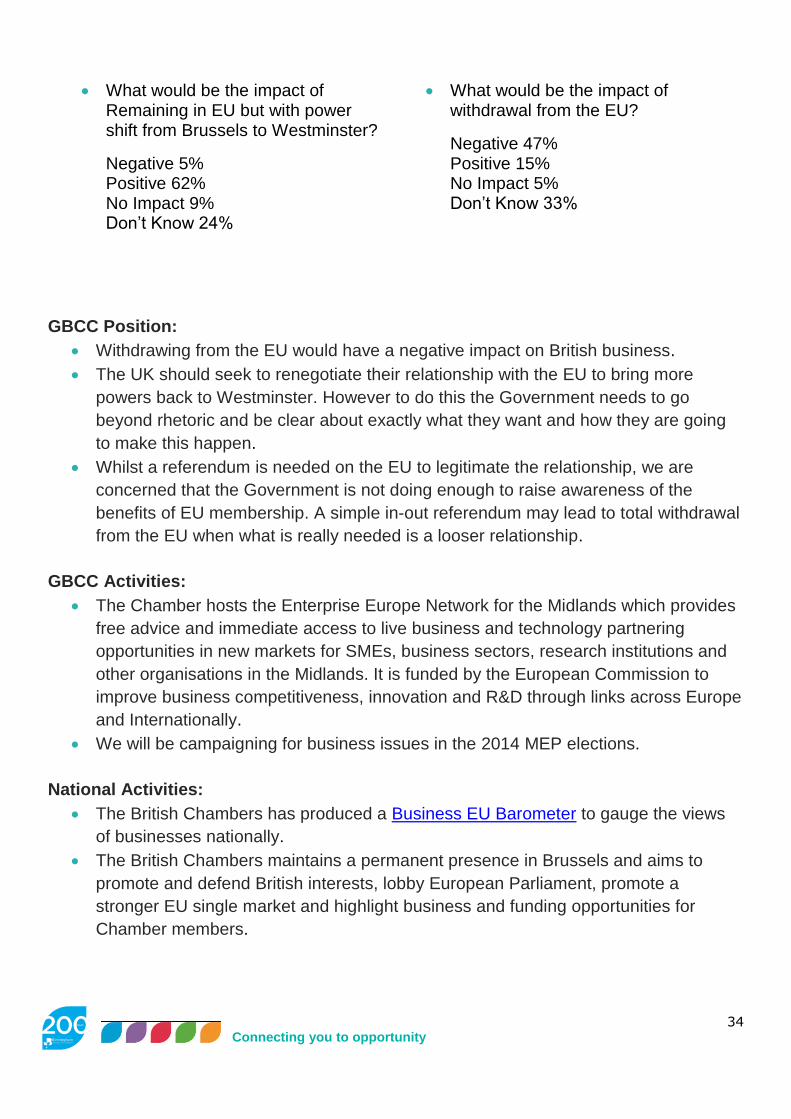

In the Quarterly Economic Survey for Q1 2013 the Chamber asked Birmingham and

Solihull businesses their views which revealed that, whilst members do not support total

withdrawal from the EU, they do favour a renegotiating a power shift from Brussels to

Westminster:

34 Connecting you to opportunity

GBCC Position:

Withdrawing from the EU would have a negative impact on British business.

The UK should seek to renegotiate their relationship with the EU to bring more

powers back to Westminster. However to do this the Government needs to go

beyond rhetoric and be clear about exactly what they want and how they are going

to make this happen.

Whilst a referendum is needed on the EU to legitimate the relationship, we are

concerned that the Government is not doing enough to raise awareness of the

benefits of EU membership. A simple in-out referendum may lead to total withdrawal

from the EU when what is really needed is a looser relationship.

GBCC Activities:

The Chamber hosts the Enterprise Europe Network for the Midlands which provides

free advice and immediate access to live business and technology partnering

opportunities in new markets for SMEs, business sectors, research institutions and

other organisations in the Midlands. It is funded by the European Commission to

improve business competitiveness, innovation and R&D through links across Europe

and Internationally.

We will be campaigning for business issues in the 2014 MEP elections.

National Activities:

The British Chambers has produced a Business EU Barometer to gauge the views

of businesses nationally.

The British Chambers maintains a permanent presence in Brussels and aims to

promote and defend British interests, lobby European Parliament, promote a

stronger EU single market and highlight business and funding opportunities for

Chamber members.

What would be the impact of Remaining in EU but with power shift from Brussels to Westminster?

Negative 5% Positive 62% No Impact 9% Don‘t Know 24%

What would be the impact of withdrawal from the EU?

Negative 47% Positive 15% No Impact 5% Don‘t Know 33%

35 Connecting you to opportunity