Embed Size (px)

Citation preview

Lesson Plan 2.1 – Double-Entry Accounting Copyright @ Texas Education Agency, 2011. All rights reserved.

ACCOUNTING I

Lesson Plan 2.1 – Double-Entry Accounting Course Title – Accounting I

Session Title – Double-Entry Accounting

Lesson Purpose – Introduce students to the double-entry accounting system.

Behavioral Objectives

Prepare a chart of accounts.

Define double-entry accounting.

Use T-accounts to analyze transactions into debit and credit parts.

Understand changes to owner’s equity.

Classify accounts with 100% accuracy.

Discuss the most used accounting assumptions.

Preparation

OLD TEKS Correlations This lesson, as published, correlates to the following TEKS. Any changes/alterations to the activities may result in the elimination of any or all of the TEKS listed.

120.42.C: 1.c. demonstrate the effects of

transactions on the accounting equation, for example, T accounts

7.a. follow oral and written

instructions;

7.b. develop time management skills

by setting priorities for completing work as scheduled

2010 TEKS Correlations This lesson, as published, correlates to the following TEKS. Any changes/alterations to the activities may result in the elimination of any or all of the TEKS listed.

130.166.c: 3.a. classify, record, and summarize financial data; 3.c.demonstrate the effects of transactions on the accounting equation; 3.d. prepare a chart of accounts; 3.e. use T accounts;

TAKS Correlation:

WRITING

Objective 5: The student will produce a piece of writing that demonstrates a command of the conventions of spelling, punctuation, grammar, usage, and sentence structure.

Objective 6: The student will demonstrate the ability to revise and proofread to improve the clarity and effectiveness of a piece of writing.

MATH

Objective 10: The student will demonstrate an understanding of the

Lesson Plan 2.1 – Double-Entry Accounting Copyright @ Texas Education Agency, 2011. All rights reserved.

ACCOUNTING I

mathematical processes and tools used in problem solving.

Materials, Equipment and Resources: Textbook

Internet

Construction Paper

Markers

Multimedia presentation software

Accounting Software

Teaching Strategies: Demonstration

Discussion

Presentations

Observation

Graded Assignments

Learner Preparation:

Have your students read at least two articles on double-entry accounting. Ask them to type a one-page explanation telling why it is called double-entry accounting. Include a brief explanation of the history of double-entry accounting. Include resources in proper format.

Ask for a volunteer to read their paper. Ask for students to share any other facts they learned that were not included. Reinforce by writing a few of these on a white board or projector.

Lesson Content:

Introduce students to the double-entry accounting system. Review students on classifying accounts and the accounting equation. In this lesson, students take a look at the expanded accounting equation and its relationship to the balance sheet. Finally, students use each piece to learn to analyze transactions using “T” accounts and look at the effects of these transactions on owner’s equity.

Assessment: Observation

Verbal Checking for Understanding

Graded Assignments

Additional Resources:

Textbooks: Guerrieri, Donald J., Haber, Hoyt, Turner. Glencoe Accounting Real-World

Applications and Connections. Glencoe McGraw-Hill 2000. ISBN/ISSN 0-02-815004-X.

Ross, Kenton, Gilbertson, Lehman, and Hanson. Century 21 Accounting Multicolumn Journal Anniversary Edition, 1st Year Course. South-Western Educational and Professional Publishing, 2003. ISBN/ISSN: 0-538-43524-0

Lesson Plan 2.1 – Double-Entry Accounting Copyright @ Texas Education Agency, 2011. All rights reserved.

ACCOUNTING I

Ross, Kenton, Gilbertson, Lehman, and Hanson. Century 21 General Journal Accounting Anniversary Edition, 7th Edition. South-Western Educational and Professional Publishing, 2003. ISBN/ISSN: 0-538-43529-1.

Multimedia: “T” Accounts. PowerPoint presentation. South-Western Publishing, Thomson

Learning, 2003. http://www.swcollege.com/acct/heintz/heintz_17e/ppt/03.ppt

Activity 2.1.1 – What Effects Owner’s Equity Copyright © Texas Education Agency, 2011. All rights reserved. ACCOUNTING I

Activity 2.1.1 – What Effects Owner’s Equity Course Title – Accounting I

Lesson Title – Double-Entry Accounting

Activity Purpose – Learn what type of transactions effect owner’s equity and

how.

OLD TEKS Correlations: This lesson, as published, correlates to the following TEKS. Any changes/alterations to the activities may result in the elimination of any or all of the TEKS listed.

120.42.C: 1.c. demonstrate the effects of

transactions on the accounting equation, for example, T accounts

2010 TEKS Correlations: This lesson, as published, correlates to the following TEKS. Any changes/alterations to the activities may result in the elimination of any or all of the TEKS listed.

130.166.C: 3.a. classify, record, and summarize

financial data; 3.c. demonstrate the effects of

transactions on the accounting equation;

3. e. use T accounts

TAKS Correlation:

MATH

Objective 10: The student will demonstrate an understanding of the mathematical processes and tools used in problem solving.

Materials, Equipment and Resources: Textbook

Teaching Strategies: Demonstration

Discussion

Observation

Activity Outline:

Ask students to define owner’s equity, revenue, expenses, and withdrawals.

Review the definition of owner’s equity. Ask the question “What type of transactions do you think affect a person’s investment in a business and how?” Lead students into a discussion about what type of revenue a person has for a service business and what type of expenses. Give specific businesses as examples. Explain why and when an owner might place more money in their capital account as an investment. Explain drawing and what it does to owner’s

Activity 2.1.1 – What Effects Owner’s Equity Copyright © Texas Education Agency, 2011. All rights reserved. ACCOUNTING I

equity.

Place the following transactions on the white board or projector and ask students to consider what they do to owner’s equity.

1. Paid cash for office building rent for this month 2. Received cash from the owner as an investment in the business 3. Paid cash to the owner for personal use 4. Paid cash to Myron’s Office Supplies to buy supplies 5. Paid cash for repairs to the company automobile 6. Received cash from a client

Place a reminder on the projector to review what affects owner’s equity and how: Increases (Investments and Revenue); Decreases (Withdrawals and Expenses).

Have students break into teams of 4. With their partner within the team, have them write 6 transactions. Make the transactions different from the examples and ones that demonstrate all four types of effects. Ask the partners within their team to solve the transactions by telling whether it was an increase or decrease to owner’s equity.

Assessment:

Observation

Verbal Checking for Understanding

Team and Partner Participation

Activity 2.1.2 – Temporary and Permanent Accounts Copyright © Texas Education Agency, 2011. All rights reserved.

ACCOUNTING I

Activity 2.1.2 –Temporary and Permanent Accounts Course Title – Accounting I

Lesson Title – Double-Entry Accounting

Activity Purpose - Gain a general knowledge of what constitutes temporary

or permanent accounts.

OLD TEKS Correlations: This lesson, as published, correlates to the following TEKS. Any changes/alterations to the activities may result in the elimination of any or all of the TEKS listed.

120.42.C: 1.c. demonstrate the effects of

transactions on the accounting equation, for example, T accounts

2010 TEKS Correlations: This lesson, as published, correlates to the following TEKS. Any changes/alterations to the activities may result in the elimination of any or all of the TEKS listed.

130.166.C: 3.a. classify, record, and summarize

financial data; 3.c. demonstrate the effects of

transactions on the accounting equation

3. e. use T accounts

TAKS Correlation:

N/A

Materials, Equipment and Resources: Textbook

Teaching Strategies: Discussion

Observation

Presentation

Activity Outline:

Ask students to define and add to their terms on index cards:

Fiscal Period

Temporary accounts

Permanent accounts

Nominal accounts

Real accounts

Income Summary

Using publisher or online resource, view online or create a Temporary and

Activity 2.1.2 – Temporary and Permanent Accounts Copyright © Texas Education Agency, 2011. All rights reserved.

ACCOUNTING I

Permanent Account presentation, briefly explain temporary accounts and permanent accounts. Reinforce the definitions. Explain why these accounts have to be “refueled” each month. You can use an odometer as an example. When you start the trip (or in a business’ case a fiscal period) the odometer needs to be at zero; otherwise, you don’t know how far you traveled on that trip.

Assessment:

Observation

Activity 2.1.3 – Expanded Accounting Equation Copyright © Texas Education Agency, 2011. All rights reserved. And Balance Sheet

ACCOUNTING I

Activity 2.1.3 – Expanded Accounting Equation and Balance Sheet

Course Title – Accounting I

Lesson Title – Double-Entry Accounting

Activity Purpose - Gain skill in balancing an expanded accounting equation.

OLD TEKS Correlations: This lesson, as published, correlates to the following TEKS. Any changes/alterations to the activities may result in the elimination of any or all of the TEKS listed.

120.42.C: 1.c. demonstrate the effects of

transactions on the accounting equation, for example, T accounts

2010 TEKS Correlations: This lesson, as published, correlates to the following TEKS. Any changes/alterations to the activities may result in the elimination of any or all of the TEKS listed.

130.166.C: 3.a. classify, record, and summarize

financial data; 3.c. demonstrate the effects of

transactions on the accounting equation

3. e. use T accounts

TAKS Correlation:

MATH

Objective 10: The student will demonstrate an understanding of the mathematical processed and tools used in problem solving.

Materials, Equipment and Resources: Textbook

Worksheet

Teaching Strategies: Discussion

Observation

Verbal Checking for Understanding

Activity Outline:

Write the accounting equation on the white board, spreading it out across the board. Underneath each classification ask your students to give some account names that fit in that classification. Explain that this is considered the expanded accounting equation. Draw a line down the middle beneath the equals sign.

Activity 2.1.3 – Expanded Accounting Equation Copyright © Texas Education Agency, 2011. All rights reserved. And Balance Sheet

ACCOUNTING I

Explain that in accounting we have a left and a right side that must be equal. Emphasize the left and right side idea and its relationship to the balance sheet. We demonstrate this equality in what we call a balance sheet. This is a report that shows the equation is equal.

Ask your students to complete the following worksheet either manually or copy it to a file for them to do on the computer:

Activity 2.1.3 – Expanded Accounting Equation Copyright © Texas Education Agency, 2011. All rights reserved. And Balance Sheet

ACCOUNTING I

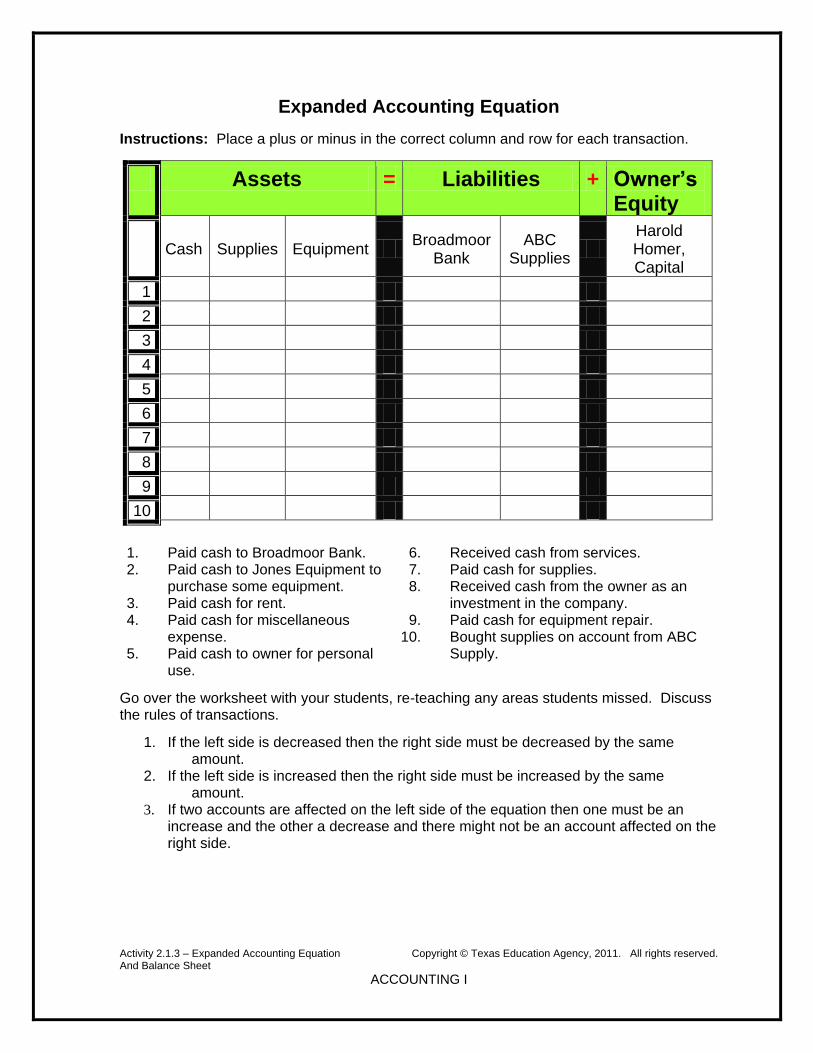

Expanded Accounting Equation

Instructions: Place a plus or minus in the correct column and row for each transaction.

Assets = Liabilities + Owner’s Equity

Cash Supplies Equipment

Broadmoor Bank

ABC Supplies

Harold Homer, Capital

1

2

3

4

5

6

7

8

9

10

1. Paid cash to Broadmoor Bank. 2. Paid cash to Jones Equipment to

purchase some equipment. 3. Paid cash for rent. 4. Paid cash for miscellaneous

expense. 5. Paid cash to owner for personal

use.

6. Received cash from services. 7. Paid cash for supplies. 8. Received cash from the owner as an

investment in the company. 9. Paid cash for equipment repair.

10. Bought supplies on account from ABC Supply.

Go over the worksheet with your students, re-teaching any areas students missed. Discuss the rules of transactions.

1. If the left side is decreased then the right side must be decreased by the same amount.

2. If the left side is increased then the right side must be increased by the same amount.

3. If two accounts are affected on the left side of the equation then one must be an increase and the other a decrease and there might not be an account affected on the right side.

Activity 2.1.3 – Expanded Accounting Equation and Balance Sheet ©Texas Education Agency/UNT

ACCOUNTING I

Expanded Accounting Equation

Instructions: Place a minus or plus sign and the amount on the transaction number line. On the Balance line, calculate the new balance for each account.

Assets = Liabilities + Owner’s Equity

Cash Supplies Equipment

Broadmoor Bank

ABC Supplies

Harold Homer, Capital

Beginning Balance

$4,500 $300 $14,000 $8,800 $225 Find the capital.

1

Balance

2

Balance

3

Balance

4

Balance

5

Balance

6

Balance

7

Balance

8

Balance

9

Balance

10

Ending Balance

1. Paid cash to Broadmoor Bank, $500.00

2. Paid cash to Jones Equipment to purchase some equipment, $1,200.

3. Paid cash for rent, $1,000.

4. Paid cash for miscellaneous expense, $25.00.

5. Paid cash to owner for personal use, $2,500.00.

6. Received cash from services, $4,000.00.

7. Paid cash for supplies, $125.00.

8. Received cash from the owner as an investment in the company, $14,000.00.

9. Paid cash for equipment repair, $250.00.

10. Bought supplies on account from ABC Supply, $75.00.

Activity 2.1.3 – Expanded Accounting Equation and Balance Sheet ©Texas Education Agency/UNT

ACCOUNTING I

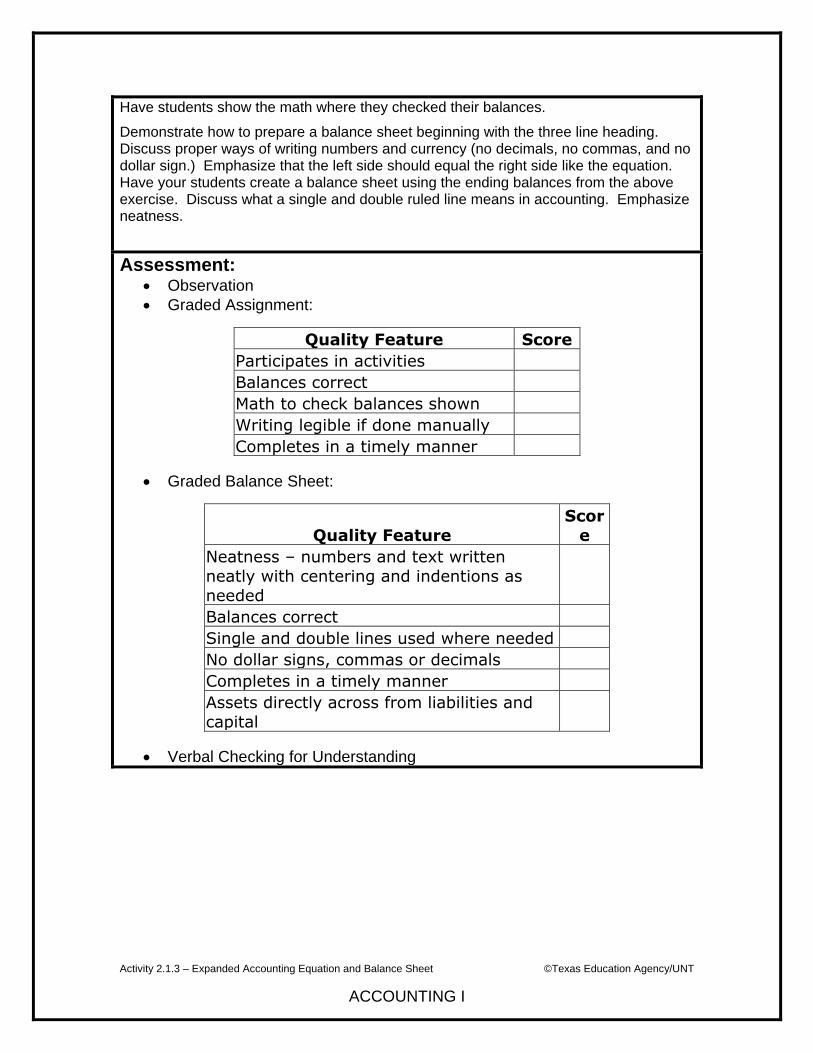

Have students show the math where they checked their balances.

Demonstrate how to prepare a balance sheet beginning with the three line heading. Discuss proper ways of writing numbers and currency (no decimals, no commas, and no dollar sign.) Emphasize that the left side should equal the right side like the equation. Have your students create a balance sheet using the ending balances from the above exercise. Discuss what a single and double ruled line means in accounting. Emphasize neatness.

Assessment: Observation

Graded Assignment:

Quality Feature Score

Participates in activities

Balances correct

Math to check balances shown

Writing legible if done manually

Completes in a timely manner

Graded Balance Sheet:

Quality Feature Scor

e

Neatness – numbers and text written neatly with centering and indentions as

needed

Balances correct

Single and double lines used where needed

No dollar signs, commas or decimals

Completes in a timely manner

Assets directly across from liabilities and capital

Verbal Checking for Understanding

Activity 2.1.4 – Normal Balance Side and “T” Accounts Copyright © Texas Education Agency, 2011. All rights reserved.

ACCOUNTING I

Activity 2.1.4 – Normal Balance Side and “T” Accounts Course Title – Accounting I

Lesson Title – Double-Entry Accounting

Activity Purpose - Identify accounts with a normal debit balance side and

those with a normal credit balance side, and introduce “T” accounts.

OLD TEKS Correlations: This lesson, as published, correlates to the following TEKS. Any changes/alterations to the activities may result in the elimination of any or all of the TEKS listed.

120.42.C: 1.b. – apply basic accounting

concepts and terminology;

1.c. – demonstrate the effects of

transactions on the accounting equation, for example, T accounts

2010 TEKS Correlations This lesson, as published, correlates to the following TEKS. Any changes/alterations to the activities may result in the elimination of any or all of the TEKS listed.

130.166.c: 3.c.demonstrate the effects of

transactions on the accounting equation;

3.e. use T accounts

TAKS Correlation: N/A

Materials, Equipment and Resources: Textbook

Construction Paper

Markers

Pencils

Teaching Strategies: Discussion

Observation

Verbal Checking for Understanding

Activity 2.1.4 – Normal Balance Side and “T” Accounts Copyright © Texas Education Agency, 2011. All rights reserved.

ACCOUNTING I

Activity Outline: Using a Normal Balance Side presentation, explain the normal balance side of accounts and the use of “T” accounts. Emphasize the relationship between the accounting equation and its normal balance side.

Ask your students to use a marker to draw a line down the middle of a piece of construction paper. Have your students trace their left hand and right hand on the piece of construction paper with a pencil. Ask them what types of accounts have a normal left side balance. Ask them to draw some pictures or write some account names on the left side of the construction paper with a marker. Try to think of at least 5 examples. Then ask them to do the same for the right side. Have your students take the online quiz for normal balance side to check for understanding before taking the assessment below. http://webhome.crk.umn.edu/~lhuus/nrmfrm.htm.

Assessment: Observation

Quiz on Normal Balance Side and “T” Accounts

2.1.4 – Quiz on Normal Balance Side and “T” Accounts Copyright © Texas Education Agency, 2011. All rights reserved.

ACCOUNTING I

Quiz on Normal Balance Side and “T” Accounts

1. What is the accounting equation, written in the form used most often?

2. What is a “T” account used for and why? 3. If the left side is the debit side, what is the right side called?

4. What type or classification of accounts normally has a debit

balance? 5. What type or classification of accounts normally has a credit

balance? 6. How do you decrease an asset account? 7. How do you decrease a liability account? 8. Explain why the owner’s equity account is decreased with a

debit.

2.1.4 – Quiz on Normal Balance Side and “T” Accounts Copyright © Texas Education Agency, 2011. All rights reserved.

ACCOUNTING I

KEY

Quiz on Normal Balance Side and “T” Accounts

1. What is the accounting equation, written in the form used most often?

Assets = Liabilities + Capital 2. What is a “T” account used for and why? To assist in analyzing an account, because it shows the left and right

side so clearly. 3. If the left side is the debit side, what is the right side called? Credit side 4. What type or classification of accounts normally has a debit

balance? Asset 5. What type or classification of accounts normally has a credit

balance? Liabilities and Owner’s Equity (Capital) 6. How do you decrease an asset account? Credit the account 7. How do you decrease a liability account? Debit the account 8. Explain why the owner’s equity account is decreased with a debit.

The owner’s equity account is on the right side of the accounting equation and therefore has a normal balance side of credit. It has to be decreased by doing the opposite which is to debit the account.

Activity 2.1.5 – Classifying Accounts (Review) Copyright © Texas Education Agency, 2011. All rights reserved.

ACCOUNTING I

Activity 2.1.5 – Classifying Accounts (Review) Course Title – Accounting I

Lesson Title – Double-Entry Accounting

Activity Purpose - Learn how to classify accounts with 100% accuracy.

.

OLD TEKS Correlations: This lesson, as published, correlates to the following TEKS. Any changes/alterations to the activities may result in the elimination of any or all of the TEKS listed.

120.42.C: 1.b. – apply basic accounting

concepts and terminology;

1.c. – demonstrate the effects of

transactions on the accounting equation, for example, T accounts

2010 TEKS Correlations This lesson, as published, correlates to the following TEKS. Any changes/alterations to the activities may result in the elimination of any or all of the TEKS listed.

130.166.C: 3.a. classify, record, and summarize

financial data;

3.c.demonstrate the effects of

transactions on the accounting equation;

3.e. use T accounts

TAKS Correlation:

WRITING

Objective 6: The student will demonstrate the ability to revise and proofread to improve the clarity and effectiveness of a piece of writing.

Materials, Equipment and Resources: Textbook

Internet

Teaching Strategies: Review

Discussion

Verbal Drills

Activity 2.1.5 – Classifying Accounts (Review) Copyright © Texas Education Agency, 2011. All rights reserved.

ACCOUNTING I

Activity Outline:

Spend several times a week drilling on classifying accounts until almost all students can classify accounts with 100% accuracy.

Have your students use index cards and drill with a partner.

Have your students number 1-20 on their page and classify as many accounts as they can as you call them out. You could also create a presentation displaying various account names and descriptions. You can have this running as they enter the room.

Assessment:

Verbal Response

Observation

Activity 2.1.6 – Numbering Account s Copyright © Texas Education Agency, 2011. All rights reserved.

ACCOUNTING I

Activity 2.1.6 – Numbering Accounts Course Title – Accounting I

Lesson Title – Double-Entry Accounting

Activity Purpose - Learn how to number accounts on a chart of accounts.

OLD TEKS Correlations: This lesson, as published, correlates to the following TEKS. Any changes/alterations to the activities may result in the elimination of any or all of the TEKS listed.

120.42.C: 1.d. prepare a chart of accounts

2010 TEKS Correlations: This lesson, as published, correlates to the following TEKS. Any changes/alterations to the activities may result in the elimination of any or all of the TEKS listed.

130.166.C: 3.c.demonstrate the effects of

transactions on the accounting equation;

3.d. prepare a chart of accounts

TAKS Correlation:

WRITING

Objective 6: The student will demonstrate the ability to revise and proofread to improve the clarity and effectiveness of a piece of writing.

Materials, Equipment and Resources: Textbook

Teaching Strategies: Review

Discussion

Verbal Drills

Activity 2.1.6 – Numbering Account s Copyright © Texas Education Agency, 2011. All rights reserved.

ACCOUNTING I

Activity Outline:

Discuss the need for numbering accounts and the need to keep an updated chart of accounts. Explain that unless an account is on the chart of accounts, it can not be used in the accounting system for that business.

Explain the numbering system used to keep the accounts separated and whether it should be a 3-digit or 4-digit system.

Ask your students to put their index cards from Activity 1 in the order in which they would appear on a chart of accounts. Check the order and review why they are in that order. For instance, assets in order of the most easily liquidated liabilities in alphabetical order and then the capital. Ask students what number should begin all assets, all liabilities and the capital account.

Have them number the accounts on the index card. Check for accuracy.

Assessment:

Verbal Response

Observation

Activity 2.1.7 – Preparing a Chart of Accounts Copyright © Texas Education Agency, 2011. All rights reserved.

ACCOUNTING I

Activity 2.1.7 – Preparing a Chart of Accounts Course Title – Accounting I

Lesson Title – Double-Entry Accounting

Activity Purpose - Learn how to create a manual and computerized chart of

accounts.

OLD TEKS Correlations: This lesson, as published, correlates to the following TEKS. Any changes/alterations to the activities may result in the elimination of any or all of the TEKS listed.

120.42.C: 1.d. prepare a chart of accounts

2010 TEKS Correlations: This lesson, as published, correlates to the following TEKS. Any changes/alterations to the activities may result in the elimination of any or all of the TEKS listed.

130.166.C: 3.c.demonstrate the effects of

transactions on the accounting equation;

3.d. prepare a chart of accounts

TAKS Correlation:

WRITING

Objective 6: The student will demonstrate the ability to revise and proofread to improve the clarity and effectiveness of a piece of writing.

Materials, Equipment and Resources: Textbook

Accounting Software

Teaching Strategies: Review

Demonstration

Observation

Graded Assignments

Activity Outline: Review definitions of assets, liabilities and owner’s equity and the accounting equation. Have students read an explanation from one of the web pages about a chart of accounts. Lead a class discussion on the importance of a chart of accounts and why only accounts on the chart of accounts can be used in the financial process.

Give your students this scenario: Jill Johnson, a sole proprietor, has decided to open a small

hair salon in your area. She lists on the left side of a sheet of paper that she owns these items: Cash, Supplies, Equipment and

Activity 2.1.7 – Preparing a Chart of Accounts Copyright © Texas Education Agency, 2011. All rights reserved.

ACCOUNTING I

Furniture. On the right side she lists that she owes for supplies from Landberg Office Supply and the equipment she purchased was a loan from Bloomer Bank.

Have your students create a proper account on a sheet of paper and list the accounts in the chart of account with an account number. Don’t forget to include the owner’s equity account.

Instruct your students on how to use the available software to enter a chart of accounts. Have your students enter the same chart of accounts as the one they used for the manual chart.

Assessment:

Observation

Graded Assignment

Quality Feature Score

Correct title on chart of accounts

Accounts numbered correctly

Account names accurate with no spelling errors

Writing legible

Computerized chart of accounts: correct title, no errors and numbered correctly

Activity 2.1.8 – Using “T” Accounts Copyright © Texas Education Agency, 2011. All rights reserved.

ACCOUNTING I

Activity 2.1.8 - Using “T” Accounts Course Title – Accounting

Lesson Title – Double-Entry Accounting

Activity Purpose - Use “T’ accounts to analyze transactions into debits and

credits.

OLD TEKS Correlations: This lesson, as published, correlates to the following TEKS. Any changes/alterations to the activities may result in the elimination of any or all of the TEKS listed.

120.42.C: 1.b. Apply basic accounting concepts

and terminology;

1.c. Demonstrate the effects of

transactions on the accounting equation, for example, T accounts.

2010 TEKS Correlations: This lesson, as published, correlates to the following TEKS. Any changes/alterations to the activities may result in the elimination of any or all of the TEKS listed.

130.166.C: 3.a. classify, record, and summarize

financial data;

3.c. demonstrate the effects of

transactions on the accounting equation;

3.e. use T accounts.

TAKS Correlation:

WRITING

Objective 6: The student will demonstrate the ability to revise and proofread to improve the clarity and effectiveness of a piece of writing.

Materials, Equipment and Resources: Textbook

Teaching Strategies: Demonstration

Observation

Practice

Activity Outline:

Draw “T” accounts on a sheet of paper for these accounts: Cash, Supplies, Prepaid Insurance, Equipment, Boomer’s Office Supply, Bank of America, Tina Taylor, Capital, Tina Taylor, Drawing, Income Summary, Fees Earned, Advertising Expense, Miscellaneous Expense, Rent Expense and Utilities Expense.

Have students analyze the transactions below. Remind them they always have

Activity 2.1.8 – Using “T” Accounts Copyright © Texas Education Agency, 2011. All rights reserved.

ACCOUNTING I

debits that equal credits. So if they have a $300 debit to cash, they must also have a $300 credit somewhere. Left side must stay in balance to the right side. Continue to emphasize this.

Ask students to use these steps to analyze the transactions:

1. Paid cash for Supplies, $50.00. 2. Wrote a check for Insurance. $498.00. 3. Received cash for Fees Earned, $230.00. 4. Paid cash for Advertising, $125.00. 5. Paid cash to owner for personal use, $2,000.00. 6. Received cash from owner as an investment in the company,

$14,000.00. 7. Donated cash to the Walk America campaign, $225.00. 8. Charged supplies on the Boomer’s Office Supplies account, $221.00. 9. Paid cash for rent, $1,000.00.

Example for the first transaction?

a. What two accounts are affected? Cash and Supplies b. What type of account is supplies? Asset c. Do you have more or less supplies? More d. How do you increase supplies? Debit e. What type of account is cash? Asset f. Do you have more or less cash? Less g. How do you decrease an Asset? Credit

Assessment:

Observation

Verbal Checking for Understanding

2.1.8 – Quiz on Classifying Accounts Copyright © Texas Education Agency, 2011. All rights reserved.

ACCOUNTING I

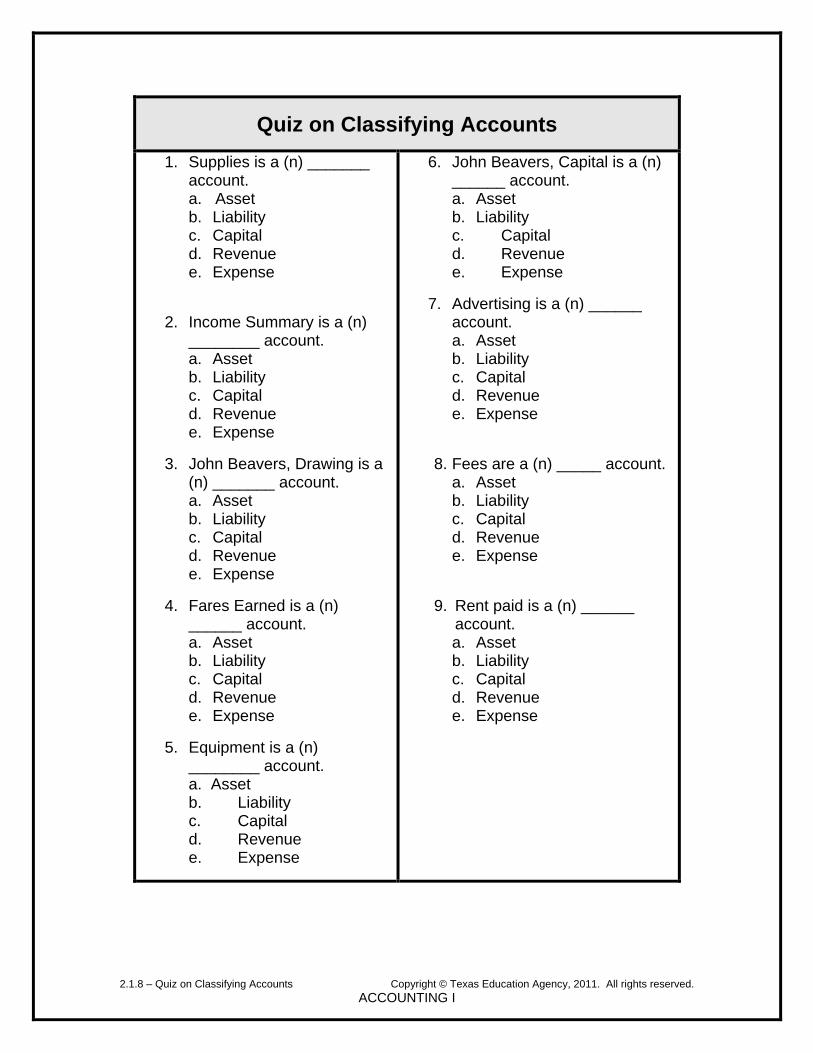

Quiz on Classifying Accounts

1. Supplies is a (n) _______ account. a. Asset b. Liability c. Capital d. Revenue e. Expense

2. Income Summary is a (n) ________ account. a. Asset b. Liability c. Capital d. Revenue e. Expense

3. John Beavers, Drawing is a (n) _______ account. a. Asset b. Liability c. Capital d. Revenue e. Expense

4. Fares Earned is a (n) ______ account. a. Asset b. Liability c. Capital d. Revenue e. Expense

5. Equipment is a (n) ________ account. a. Asset b. Liability c. Capital d. Revenue e. Expense

6. John Beavers, Capital is a (n) ______ account. a. Asset b. Liability c. Capital d. Revenue e. Expense

7. Advertising is a (n) ______ account. a. Asset b. Liability c. Capital d. Revenue e. Expense

8. Fees are a (n) _____ account.

a. Asset b. Liability c. Capital d. Revenue e. Expense

9. Rent paid is a (n) ______

account. a. Asset b. Liability c. Capital d. Revenue e. Expense

2.1.8 – Quiz on Classifying Accounts Copyright © Texas Education Agency, 2011. All rights reserved.

ACCOUNTING I

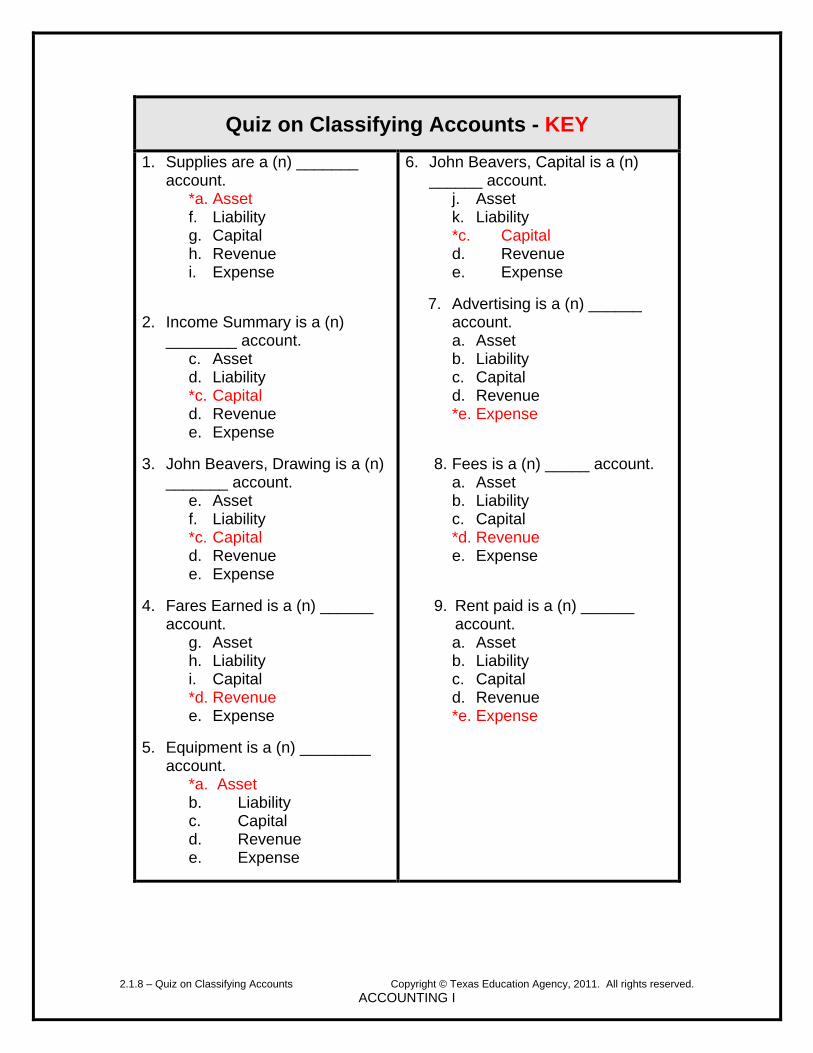

Quiz on Classifying Accounts - KEY

1. Supplies are a (n) _______ account.

*a. Asset f. Liability g. Capital h. Revenue i. Expense

2. Income Summary is a (n) ________ account.

c. Asset d. Liability *c. Capital d. Revenue e. Expense

3. John Beavers, Drawing is a (n) _______ account.

e. Asset f. Liability *c. Capital d. Revenue e. Expense

4. Fares Earned is a (n) ______ account.

g. Asset h. Liability i. Capital *d. Revenue e. Expense

5. Equipment is a (n) ________ account.

*a. Asset b. Liability c. Capital d. Revenue e. Expense

6. John Beavers, Capital is a (n) ______ account.

j. Asset k. Liability *c. Capital d. Revenue e. Expense

7. Advertising is a (n) ______ account. a. Asset b. Liability c. Capital d. Revenue *e. Expense

8. Fees is a (n) _____ account.

a. Asset b. Liability c. Capital *d. Revenue e. Expense

9. Rent paid is a (n) ______

account. a. Asset b. Liability c. Capital d. Revenue *e. Expense

Activity 2.1.9 - Accounting Assumptions Copyright © Texas Education Agency, 2011. All rights reserved.

ACCOUNTING I

Activity 2.1.9 – Accounting Assumptions Course Title – Accounting

Lesson Title – Double-Entry Accounting

Activity Purpose – Demonstrate basic knowledge in the most used

accounting assumptions.

OLD TEKS Correlations: This lesson, as published, correlates to the following TEKS. Any changes/alterations to the activities may result in the elimination of any or all of the TEKS listed.

120.42.C.1.b. Apply basic

accounting concepts and terminology;

7.a. follow oral and written

instructions;

7.b. develop time management skills

by setting priorities for completing work as scheduled;

7.c. make decisions using

appropriate accounting concepts;

7.e. perform accounting procedures

using manual and automated methods.

2010 TEKS Correlations: This lesson, as published, correlates to the following TEKS. Any changes/alterations to the activities may result in the elimination of any or all of the TEKS listed.

130.166.c 1.a. describe the purpose of

accounting and financial reporting

TAKS Correlation:

WRITING

Objective 6: The student will demonstrate the ability to revise and proofread to improve the clarity and effectiveness of a piece of writing MATH Objective 10: The student will demonstrate an understanding of the mathematical processes and tools used in problem solving.

Materials, Equipment and Resources: Textbook

Internet

Teaching Strategies: Demonstration

Observation

Activity 2.1.9 - Accounting Assumptions Copyright © Texas Education Agency, 2011. All rights reserved.

ACCOUNTING I

Activity Outline:

Have students look up these accounting assumptions to discuss in class:

1. Accounting Period Cycle 2. Adequate Disclosure 3. Business Entity 4. Consistent Reporting 5. Going Concern 6. Historical Cost 7. Matching Expenses with Revenue 8. Materiality 9. Objective Evidence

10. Realization of Revenue 11. Unit of Measurement

Ask students to keep their list of assumptions in their notebook because they will review them often.

Assessment:

Observation

![1 session 3 [plan]](https://img.pdfslide.net/doc/110x75/55a628b31a28abd5138b4622/1-session-3-plan.jpg)