-

8/8/2019 BeasleyCh9 v2

1/30

Chapter 9

CapitalStructure

2005 Thomson/South-Western

-

8/8/2019 BeasleyCh9 v2

2/30

2

The Target Capital Structure

Capital Structure: The combination ofdebt and equity used to

finance a firm

Target Capital Structure: The ideal mix

of debt, preferred stock, and commonequity with which the firm

plans tofinance its investments

-

8/8/2019 BeasleyCh9 v2

3/30

3

The Target Capital Structure

Four factors that influence capital structuredecisions:

The firms business risk

The firms tax position Financial flexibility

Managerial attitude

-

8/8/2019 BeasleyCh9 v2

4/30

4

What is Business Risk?

Uncertainty about future operating income

(EBIT).

How well can we predict operating income?

-

8/8/2019 BeasleyCh9 v2

5/30

5

Sales variability

Input price variability

Ability to adjust output prices for changesin input prices

The extent to which costs are fixed:

operating leverage

Factors AffectingBusiness Risk

-

8/8/2019 BeasleyCh9 v2

6/30

6

What is Operating Leverage?

Operating Leverage: Use of fixed operatingcosts rather than

variable costs

If most costs are fixed (i.e., they do not

decline when demand falls) then the firm hashigh DOL (degree of

operating leverage)

-

8/8/2019 BeasleyCh9 v2

7/30

7

What is Financial Risk?

Financial Leverage: The extent to whichfixed-income securities

(debt and preferredstock) are used in a firms capital structure

Financial Risk: Additional risk placed onstockholders as as

result of financialleverage

-

8/8/2019 BeasleyCh9 v2

8/30

8

Business Risk vs. Financial Risk

Business risk depends on business factorssuch as competition,

product liability, andoperating leverage.

Financial risk depends only on type ofsecurities issued: the

more debt, the morefinancial risk.

-

8/8/2019 BeasleyCh9 v2

9/30

9

Determining theOptimal Capital Structure:

Seek to maximize the price of the firmsstock.

Changes in use of debt will cause changes inearnings per share,

and, thus, in the stock

price. Cost of debt varies with capital structure.

Financial leverage increases risk.

-

8/8/2019 BeasleyCh9 v2

10/30

10

EPS Indifference Analysis

EPS Indifference Point:The level of sales at which EPS will

bethe same whether the firm uses debt

or common stock (pure equity)financing.

-

8/8/2019 BeasleyCh9 v2

11/30

11

Probability

Density

0 $2.40 $3.36

50% Debt Financing

Zero Debt Financing

EPS ($)

Probability Distribution ofEPS with Different AmountsofFinancial

Leverage

-

8/8/2019 BeasleyCh9 v2

12/30

12

The Effect of Capital Structureon Stock Prices and the Cost

of CapitalThe optimal capital structure

maximizes the price of a firms stock.

The optimal capital structure alwayscalls for a debt/assets

ratio that islower than the one that maximizesexpected EPS.

-

8/8/2019 BeasleyCh9 v2

13/30

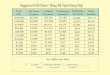

13

Debt/Assets

kd ExpectedEPS

EstimatedBeta

ks = [kRF +

(kM kRF)Fs]

EstimatedPrice

ResultingP/E Ratio

WACC

0% - $2.40 1.50 12.0% $20.00 8.33 12.00%

10 8.0% 2.56 1.55 12.2 20.98 8.20 11.4620 8.3 2.75 1.65 12.6

21.83 7.94 11.08

30 9.0 2.97 1.80 13.2 22.50 7.58 10.86

40 10.0 3.20 2.00 14.0 22.86 7.14 10.80

50 12.0 3.36 2.30 15.2 22.11 6.58 11.20

60 15.0 3.30 2.70 16.8 19.64 5.95 12.12

All earnings paid out as dividends, so EPS = DPS.Assume that kRF

= 6% and kM = 10%. Tax rate = 40%.

WACC = wdkd(1 - T) + wsks

= (D/A) kd(1 - T) + (1 - D/A)ks

At D/A = 40%, WACC = 0.4[(10%)(1-.4)] + 0.6(14%) = 10.80%

Stock Price and Cost of Capital Estimateswith Different

Debt/Assets Ratios

-

8/8/2019 BeasleyCh9 v2

14/30

14

Relationship BetweenCapital Structure and EPSEPS

0

0.5

1

1.5

2

2.5

3

3.5

0 10 20 30 40 50 60

Maximum EPS = $3.36Expected EPS ($)

Debt/Assets (%)

-

8/8/2019 BeasleyCh9 v2

15/30

15

0

5

10

15

20

0 10 20 30 40 50 60

Cost of Equity, ks

Cost ofCapital (%)

Debt/Assets (%)

WACC

Minimum = 10.8%

Relationship BetweenCapital Structure and Cost of CapitalCost of

Capital

-

8/8/2019 BeasleyCh9 v2

16/30

16

18

19

20

21

22

23

24

0 10 20 30 40 50 60

Maximum = $22.86

StockPrice ($)

Debt/Assets (%)

Relationship BetweenCapital Structure and Stock PriceStock

Price

-

8/8/2019 BeasleyCh9 v2

17/30

17

Percentage change in NOI

Percentage change in sales

(EBIT

EBIT

(Sales

Sales

(EBIT

EBIT

(Q

Q

DOL = = =

DOLQ =Q(P - V)

Q(P - V) - FC

DOLS =S - VC

S - VC - F

Gross Profit

EBIT=

Degree of Operating Leverage(DOL)

The percentage change in operating income (EBIT)

associated with a given percentage change in sales.

-

8/8/2019 BeasleyCh9 v2

18/30

18

(EPS

EPS

(EBIT

EBIT

Percentage change in EPSPercentage change in EBIT

EBITEBIT - Int

DFL = = =

Degree ofFinancial Leverage(DFL)

The percentage change in earnings availableto common

stockholders associated with agiven percentage change in EBIT.

This equation assumes the firm has no preferred stock.

-

8/8/2019 BeasleyCh9 v2

19/30

19

S - VC

S - VC - F - IntGross Profit

EBIT - IntDTL = =

Q(P - V)Q(P - V) - F - Int

DTL =

DTL = DOL X DFL

Degree of Total Leverage(DTL)

The percentage change in EPS that results

from a given percentage change in sales.

-

8/8/2019 BeasleyCh9 v2

20/30

20

Liquidity and Capital StructureDifficulties with Analysis

1. We cannot determine exactly how either P/E ratiosor equity

capitalization rates (ks values) are affectedby different degrees

of financial leverage.

2. Managers may be more or less conservative thanthe average

stockholder, so management may set adifferent target capital

structure than the one thatwould maximize the stock price.

3. Managers of large firms have a responsibility toprovide

continuous service and must refrain fromusing leverage to the point

where the firms long-run viability is endangered.

-

8/8/2019 BeasleyCh9 v2

21/30

21

Liquidity and Capital Structure

Financial strength indicator

Times-Interest-Earned (TIE) Ratio

Ratio that measures the firms ability to meet

its annual interest obligationsFormula: divide EBIT (earnings

before interest

and taxes) by interest charges

-

8/8/2019 BeasleyCh9 v2

22/30

22

Capital Structure Theory

Trade-off Theory

Signaling Theory

-

8/8/2019 BeasleyCh9 v2

23/30

23

Trade-Off Theory(Modigliani and Miller)

1. Theory:

1. Interest is tax-deductible expense, therefore less

expensivethan common or preferred stock.

2. So, 100% debt is the preferred capital structure.

2. Theory:

1. Interest rates rise as debt/asset ratio increases2. Tax rates

fall at high debt levels (lowers debt tax shield)

3. Probability of bankruptcy increases as debt/assets

ratioincreases.

-

8/8/2019 BeasleyCh9 v2

24/30

24

Trade-Off Theory (continued)

3. Two levels of debt:

1. Threshold debt level (D/A1) = where bankruptcy costsbecome

material

2. Optimal debt level (D/A2) = where marginal tax

shelterbenefits = marginal bankruptcyrelated costs

3. Between these two debt levels, the firms stock price

rises,but at a decreasing rate

4. So, the optimal debt level = optimal capitalstructure

-

8/8/2019 BeasleyCh9 v2

25/30

25

Trade-Off Theory (cont)

4. Theory and empirical evidence supportthese ideas, but the

points cannot beidentified precisely.

5. Many large, successful firms use much lessdebt than the

theory suggestsleading todevelopment of signaling theory.

-

8/8/2019 BeasleyCh9 v2

26/30

26

Signaling Theory

Symmetric Information Investors and managers have identical

information about the firms prospects.

Asymmetric Information

Managers have better information about theirfirms prospects than

do outside investors.

-

8/8/2019 BeasleyCh9 v2

27/30

27

Signaling Theory

Signal

An action taken by a firms management thatprovides clues to

investors about howmanagement views the firms prospects

Result: Reserve Borrowing CapacityAbility to borrow money at a

reasonable cost when

good investment opportunities arise Firms often use less debt

than optimal to ensure

that they can obtain debt capital later if needed.

-

8/8/2019 BeasleyCh9 v2

28/30

28

Variations in CapitalStructures among Firms

Wide variations in use of financial leverageamong industries and

firms within anindustry TIE (times interest earned ratio) measures

how

safe the debt is: percentage of debt

interest rate on debt

companys profitability

-

8/8/2019 BeasleyCh9 v2

29/30

29

Co try ity otal e t Lo g- erm

e t

hort- erm

e t

United Kingdom 68.3 31.7 N/ N/

United tates 48.4 51.6 26.8 24.8

anada 47.5 52.5 30.2 22.7

Germany 39.7 60.3 15.6 44.7 pain 39.7 60.3 22.1 38.2

rance 38.8 61.2 23.5 37.7Japan 33.7 66.3 23.3 43.0

Italy 23.5 76.5 24.2 52.3

Capital Structure Percentages for Selected CountriesRanked by

Common Equity Ratios, 1995

Capital Structures Around the World

-

8/8/2019 BeasleyCh9 v2

30/30

30

Before Next Class:

1.Review Chapter 9 material

2.Do Chapter 9 homework3.Prepare for Chapter 9 quiz4.Read

Chapter 10