Embed Size (px)

Citation preview

8/8/2019 Beets 1999

http://slidepdf.com/reader/full/beets-1999 1/18

© 1999 American Accounting AssociationAccounting HorizonsVol. 13 No. 2Jun e 1999

pp.129-145

Corporate Environmental Reports:The N eed for Standards and

an Environmental Assurance Service

S. Douglas Beets and Christopher C. Souther

S. Douglas Beets is an Associate Professor at Wake Forest Universityand Christopher C. Souther is a Staff A ccountant with KPMG PeatMarwick in Charlotte, North C arolina.

SYNOPSIS: Many companies are becoming more responsive to investors' con-cerns about the en vironment by voluntarily com piling an d issuing periodic environ-me ntal reports that are essentially indepen dent of the annual finan cial reports. Be-

cause of an absence of environmental reporting standards, however, these reportsdiffer significantly thereby confou nding co mp arability. Additionally, the credibility ofthese rep orts is being ques tioned , as they are typically not verified by inde pende nt

third parties. As m any public accounting firms are currently attempting to dev elopadditional assurance services to offer existing and potential clients, verification ofenvironme ntal reports may be an appropriate application of accounting firms' at-testation skills and their desire to expand the client relationship. Such verificationengagements may also be beneficial for corporations, investors, regulators and,

ultimately, the environment. Guidance and criteria for environmental verificationservices are scant, however, and the accounting profession m ay benefit from ex-peditious development of such standards so that public accountants are empow-ered to offer a need ed assurance service and com pete effectively with other co n-sulting firm s.

INTRODUCTION

As societal concern for the environment grows, many compeuiies are becoming moreresponsive to investor demands for information regarding corporate environmental re-sponsibility. Several corporations have disclosed such information to the investing pub-lic in the form of periodic environmental reports that are issued separately from theann ual financial report. Because of the absence of environmental reporting sta nd ards,however, these reports differ significantly from compziny to company, confounding com-parability. Furth er, the information in many of these environmental repo rts lacks cred-ibility, as it is not independently verified by outside partie s. The increasing prevalence

Submitted: June 1998

8/8/2019 Beets 1999

http://slidepdf.com/reader/full/beets-1999 2/18

130 Accounting Horizons/June 1999

of these reports, consequently, may create a new niche for those pubUc accounting firmsthat develop expertise in environmental reporting and verification.

CURRENT TRENDS IN CORPORATE ENVIRONMENTAL REPORTING

Environmental issues are an overwhelming concern for many corporations. Theoverall known environm ental liability in the United States is currently estimated to bebetween 2 and 5 percent of the gross national product. Environmental cleanup costsunder the Comprehensive Environmental Response, Compensation and Liability Act of1980, or "Superfund," are approximately $500 billion and will take 40 to 50 years tocomplete (Chadwick et al. 1993). Related penalties are also on the rise; the federalgovernment, for example, now prosecutes ind ividuals such as corporate officers for en-vironmental offenses even if they did not personally commit the violation of the law(McMahon 1995). The U.S. Sentencing Commission is currently devising sentencing

guidelines re lated to environmental crimes that will further increase existing pena lties(Uzumeri and Tabor 1997).Because of investor concern about corporate environmental issues, the Securities

and Exchange Commission (SEC) has, in recent years, increased environm ental disclo-sure requirements of public companies. In 1994, SEC Commissioner Richard Robertsacknowledged th at heightened public awareness of environmental m atte rs has resultedin:

increased pressure to bear on the SEC to ensure that publicly-held companies aredisclosing in a fair, full, and timely mann er th e presen t and potential environm entalcosts of an economically material na ture. My view is tha t the company owes this to

the investing public. {Risk Management 1994, 15).In Jun e 1993, the SEC issued Staff Accounting Bulletin 92 (SAB 92) which d ictatesincreased and more prominent disclosure of existing and potential environmental li-abilities (Risk Management 1994), and SEC Commissioner Roberts threatened that somecompanies would be "drawn and quEirtered" by the SEC's enforcement division for in-consistencies and lack of disclosure related to published corporate environmental infor-mation (Kreuze et al. 1996). One year la ter, however, more than one third of U.S. publiccompanies did not plan to mention existing and potential environm ental liabilities intheir annual report as required by SAB 92 (Environment T oday 1993; Journal of Ac-countancy 1994). These companies could face possible sanctions from the SEC for inad-

equate disclosvires and may lose thei r registration or be forced to pay fines of up to halfa m illion dollars for each violation (Kreuze et al. 1996).

Partiadly because of the SEC's concern about environmental disclosures, the Ac-coimting S tandards Executive Com mittee of the American Ins titute of Certified PublicAccountants (AICPA) issued Statement of Position 96-1 in October 1996. This state-men t was intended to provide clarification to public accountants and their clients re-garding adequate disclosure of environm ental rem ediation liabilities.

Compzinies are also experiencing increased disclosure pressure from the Environ-mental Protection Agency (EPA). In early 1998, the EPA began requiring additionalInterne t disclosures of companies in five arge industries: oil, steel, me tals, automobiles

and paper. Using an In ternet pollution profile designed by the EPA, the affected corpo-rations m ust rep ort the number of plan t inspections in the past two years, noncompli-

8/8/2019 Beets 1999

http://slidepdf.com/reader/full/beets-1999 3/18

Corporate Environmental Reports: The Need for Standards and an Environmental Assurance S ervice 13 1

based on the toxicity of the chemicals released , the ratio of pollution re leases to produc-tion, the racial and income profiles of those living within three miles of each p lan t, andinformation from the Toxic Release Inventory {St. Louis Post-Dispatch 1997). The re-

sultant "Envirofacts Warehouse" on the Internet (www.epa.gov/enviro/) includes envi-ronmental data about thousands of corporate industrial sites.In the first half of this decade, the EPA began penalizing companies for environ-

mental violations th at were disclosed in the information released to stakeholders. InMarch 1996, however, the EPA decided to reduce or eliminate penalties for responsiblecompanies tha t perform periodic internal aud its, correct the problems discovered andvoluntarily report the infonnation. N onetheless, the EPA refuses to tre at a company'sinternal environmental audit as privileged business information and reserves the righ tto assess penalties on all violations found through these self-examinations (Shanoff1995).

In addition to government agencies, investors and o ther stakeholders are demand-ing more disclosure of company environm ental information because of the ir intere st inenvironmental issues and their concern about the magnitude of related costs and li-abilities (Mastrandonas and Strife 1992). In response, many corporations, includingalmost half of the F ortune 500, are now compiling £ind issuing periodic environm entalreports th at are voluntary and essentially independent of the traditional annua l finan-cial repo rt {CFO 1996).

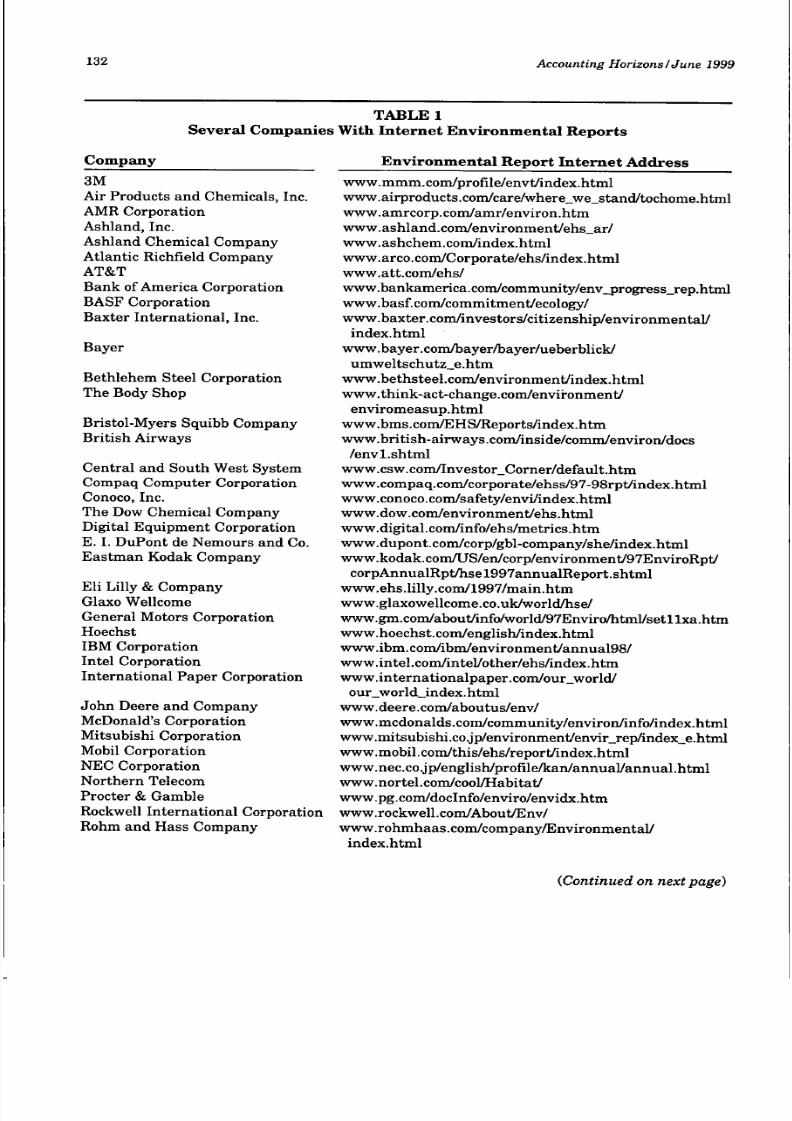

Many companies are now displaying their corporate environmental reports on theirInternet sites; table 1 lists several corporations and the In terne t address for their peri-odic environmental reports. Most of these corporations also issue these reports in ahard-copy, published form similar in appearance to the traditional annual financialreport. A review of these online or printed environmental reports reveals extreme di-versity in format and data provided, but tj^jical inclusions are report scope, corporateenvironmental values and comm itment, tangible goals and performance rela ted to thosegoals, environmental management systems, legal compliance, enforcement actions £tndliabilities, industry-specific environmental issues, the company's environmental per-formance as depicted by the media, financial data related to environmental issues andthird par ty audits or reviews (Mastrandonas and Strife 1992).

While there may be some similarities in content, current periodic environmental re-ports are very different with no common format and varying amounts of data and informa-tion. Some of these reports are short, perfunctory and contain little quantifiable data while

others are very detailed and lengthy with num erous charts, graphs and tables related tospecific pollutants, abatement expenditures, tons of waste, etc. An innovative example of adetailed environmental report is that of Hoescht Company whose environmental report ispresented on a CD-ROM in multiple languages including background music and videoclips. The relevant time period also differs among these reports; some are prepared annu-ally, others biannually, and still others have been prepared with no indication about thetiming of future reports. Some corporate environmental reports address not only environ-mental matters but report on health and safety issues as well; the verification reportsincluded in appendices A and B, for example, relate to examinations of corporate environ-ment, health, and safety reports and programs.

These several trends indicate an increased emphasis on corporate environmentalcommunications by all stakeholders, including the investing public and regulatory bod-

8/8/2019 Beets 1999

http://slidepdf.com/reader/full/beets-1999 4/18

132 Accounting Horizons / June 1999

TABLE 1

Se v e r a l C o m pa n ie s W i t h In t e r ne t Env ir o nm e nt a l R e po r t s

C o m pa ny3MAir Products and Chemicals, Inc.AMR CorporationAshland, Inc.Ashland Chemical CompanyAtlantic Richfield CompanyAT&TBa nk of Am erica Co rporation

BASF CorporationBaxter International, Inc.

Bayer

Bethlehem Steel CorporationThe Body Shop

Bristol-Myers Squibb CompanyBritish Airways

Central and South West SystemCompaq Computer Corporation

Conoco, Inc.The Dow Chemical CompanyDigital Equipment CorporationE. I . DuP ont de Nemours and Co.Eastman Kodak Company

Eli Lilly & CompanyGlaxo Wellcome

General Motors CorporationHoechstIBM Corporation

Intel CorporationInternational Paper Corporation

John Deere and Company

McDonald's CorporationMitsubishi CorporationMobil CorporationNEC CorporationNorthern TelecomProcter & Gamble

Rockwell International Corporation

Rohm and Hass Company

Environmental Report Internet Addresswww.mmm.com/profile/envt/index.html

ww w.airproducts.com/car e/where_we_stand/tochome.htmlwww. am rcorp. com/am r/envir on. htmwww.ashland.com/environment/ehs_ar/www.ashchem.com/index.htmlwww.arco.com/Corporate/ehs/index.htmlwww.att.com/ehs/

www .bankamerica.com/communi ty/env_progress_rep.htmlwww.basf.com/commitment/ecology/www.baxter.com/investors/citizenship/environmental/

index.htmlwww.bayer.com/bayer/bayer/ueberblick/

umweltschutz_e.htmwww.bethsteel.com/environment/index.html

www.think-act-change.com/envii-onment/enviromeasup.html

www.bms.com/EHS/Reports/index.htm

www.bri tish-airways.com/inside/comm/environ/docs/envl . sh tml

www.csw.com/Investor_Corner/default.htmwww.compaq.com/corporate/ehss/97-98rpt/index.htmlwww.conoco.com/safety/envi/index.htmlwww.dow.com/environment/ehs.htmlwww. digital. com/info/ehs/metr ics. h tmwww.dupont.com/corp/gbl-company/she/index.htmlwww.kodak.com/US/en/corp/environment/97EnviroRpt/

corpAnnualRpt/hsel997annualReport .shtmlwww.ehs.lilly.com/1997/main.htmwww.glaxowellcome.co.uk/world/hse/www.gm.com/about/info/world/97Enviro/html/setllxa.htmwww.hoechst.com/english/index.htmlwww.ibm.com/ibm/environment/annual98/

www.intel.com/intel/other/ehs/index.htmwww.internationalpaper.com/our_world/

our_world_index. htm lwww. deere. com/aboutus/env/

www.mcdonalds.com/community/environ/info/index.htmlwww.mitsubishi.co.jp/environment/envir_rep/index_e.htmlwww.mobil. com/this/ehs/report/index.htmlww w.nec.co.jp/english/profile/kan/annual/annual.htmlwww. nor tel. com/cool/Habitat/www.pg.com/doclnfo/enviro/envidx.htmwww.rockwell.com/About/Env/

www.rohmhaas.com/company/Environmental/index.html

8/8/2019 Beets 1999

http://slidepdf.com/reader/full/beets-1999 5/18

8/8/2019 Beets 1999

http://slidepdf.com/reader/full/beets-1999 6/18

134 Accounting Horizons/June 1999

companies by environmentally concerned inv estors . Studies of investor preferencesand behavior have indicated th at m any investors are concerned about environmen-tal issues and would be more likely to invest in companies that have favorable

environmental records (The Accountant 1998; Deutsch 1998; Investors Chronicle1998; Krumsiek 1998).Some corporations may defend the sta tus quo of minimal standards related to envi-

ronmental reporting and verification, arguing that economic forces will reward envi-ronmentally oriented companies if the market ascribes value to their efforts. Otherscontend, however, that unregulated economic forces may resu lt in a healthy economybut not necessarily a healthy environment; i.e., an economic mark et without environ-mental standards does not efficiently lead to environm ental protection (Greer and Bruno1996).

Unfortunately, while the need for external verification of environmental reports

may be warranted , major challenges exist: an absence of standard s related to environ-mental reporting, an absence of standards related to environmental verification en-gagements, and a scarcity of public accounteints who are qualified to perform such aservice. In 1996, the Global Environmental M anagement In itiative (GEMI), an organi-zation of large environmentally proactive businesses, published the resu lts of a study of

environmental reports and their perceived value . This study involved a series of inter-views of environmentalists, investors, media, regulators and corporations. These par-ties consistently indicated tha t third-par ty a ttestatio n of environmental reports is cur-rently of little value because of the lack of guidelines and standards related to the re-ports and their verification. Those interviewed suggested that the needed standards

should cover scope, limitations and content of third-party verification and state ments ,as well as eventual integration into the accepted accounting attestation scheme (Envi-ronmental Management Today 1996).

The accounting profession in the United States may learn m uch about addressingthese challenges from environmental verification practices in Europe. In 1993, the Eu-ropean Council of the European Union adopted the Eco-Management and Audit Scheme(EMAS), a regulatory plan intended to promote improvement in the environmentalperfonnance of industrisil companies. In addition to msiny specific standsirds, EMASrequires companies to prepare publicly available environm ental reports which m ust bevalidated by a qualified third party, that is , an accredited EMAS verifier (Environmen-

ta l Management Today 1996). Because of the specific standards and external verifica-tion, the environmental reports prepared u nder EMAS are likely to be more useful Eindreliable than their unregulated, unverified counterparts in the United States.

Although EMAS has been in effect for a relatively short period of time, there issome evidence of its success and acceptance by the European business community. Thenum ber of applications for accreditation as EMAS verifiers has steadily increased, indi-cating that accounting and consulting firms may be considering EMAS verification tobe a potentially profitable type of engagement. Additionally, all EMAS registered siteswere surveyed in 1996, regarding their perceived value of EMAS. Without exception,all responden ts ascribed vedue to EMAS and indicated th at , given the choice, they would

go through the process again (EMAS Help Desk Inte rne t Site 1998).While external verification of environm ental p rograms and reports is not currentlyrequired in the U.S., many corporations voluntarily elect to undergo external environ-

8/8/2019 Beets 1999

http://slidepdf.com/reader/full/beets-1999 7/18

Corporate Environmental Reports: The Need for Standards and an Environmental Assurance Service 135

those examinations public (Aeppel 1993). One of the primary reasons for this lack ofdisclosure is the absence of environmental reporting standards. While corporate offi-cials may vsilue an external verification of the environmental report for internal pur-

poses, they may be reluctant to make the verifier's report public because the lack ofstandards confounds stakeholder analysis and comparisons. {Environmental Manage-ment Today 1996).

Other companies, however, believe th at sharing the environmental verification re-port builds tru st with the public (Aeppel 1993). Four such public reports a re included inthe appendices: appendix A displays the environm ental verification reports of two U.S.corporations, DuPont and WMX Technologies; appendix B shows the reports of twoother companies, British Petroleum and Northern Telecom, that are headquarteredoutside the U.S. A review of these four reports reveals the diversity resu lting from anabsence of environmental reporting and verification standards. Two of these were pre-

pared by Big 5 public accounting firms while the other two were prepared by consultingfirms, one of which is oriented specifically tow ard environm ental consulting.These voluntary efforts to compile corporate environmental reports, have them in-

dependently verified, and publish both the environmental report and the related verifi-cation report may exemplify what Elliot (1994a, 115) referred to as an accountabilityobligation. Such obligations m ay originally be voluntary but la ter thought by society tobe so clear and compelling th at they should be uniformly performed and, perhaps, writ-ten into law (Elliot 1994a).

One of the likely concerns of corporate officials regarding environmental reportverification is the related increase in professional fees. These added costs, however,

could be partially mzinaged by £in adequate and efficient internal audit system. Manycompanies that currently issue periodic environmental reports have significant inter-nal audit functions, and the environmented work of these internal audit departmentscould be evaluated and used by the external verifiers. As in the case of financ ial state-ment a udits, the more the external verifiers can rely on the work of intern al auditors ,the lower a company's costs related to environmental verification. Additional profes-sional fees may also be offset by the positive public relations that may accrue fromissuing a verified environmental report; that is, "being green" may have a positive im-pact on revenues and stock prices.

In addition to concern regarding increased professional fees, company officials maybe hesita nt to provide additional environmental disclosures tha t could result in litiga-tion and more public and government scrutiny if environmental disclosures are inaccu-rate or incorrectly in terpreted . Adverse public sentiment and regu latory reaction couldalso result if a corporate environmental report discloses detrimental environmentaleffects that were not previously known or understood.

With regard to the challenge of developing useful environm ental reporting and veri-fication standard s, progress is being made by various organizations. In addition to theGEMI mentioned previously, bodies such as the Internationa l S tandards Organization(ISO), the Coalition for Environmentally Responsible Economics, and the Council onEconomic Priorities have estab lished useful principles and stemdards, although partici-pation in such programs is voluntary and, consequently, does not have the regulatoryimpact of EMAS. An exEimple of an industry environmental initiative is the Respon-sible Care Program of the Chemical Manufacturers Association.

8/8/2019 Beets 1999

http://slidepdf.com/reader/full/beets-1999 8/18

136 Accounting Horizons/June 1999

implement and monitor an environmental management system. The ISO 14000 stan-dards also provide an objective way to verify company environmental performance re-ports {The CPA Journal 1997).

For external verification of environmental reports to become viable in th e UnitedState s, reporting and verification standards s imilar to those of the EMAS and ISO mustbe developed and uniformly adopted by companies th at publish the se reports. One pos-sible source of such sta nd ard s is the EPA. Following the exeunple of Securities Acts of1933 and 1934, the U.S. Congress could enact legislation that would require verifiedenvironm ental sta tem ents of corporations sind establish the EPA as an oversight agencyto see tha t the private sector developed, enacted and enforced the necessary standards.Environmentalists may argue that this analogy is apt. Just as Congress in the 1930swas reacting to a problem arising, in part, from unaudited corporate financial state-me nts, current lawm akers may attribute a degree of environmental problems to inad-

equate independent verification of corporate environmental information. Under thispossible model, a priva te, independen t organization, similar to th e F inancial Account-ing Standards Board, would develop environmental reporting s tand ards while anotherprivate group, similar to the Auditing Standards Board of the AICPA would promul-gate environmental verification stan dards . Another possibility would be the EPA 's adop-tion and enforcement of stand ard s similar to those of ISO 14000 or the EMAS.

The Necessity of Environm ental Reporting StandardsWidely recognized or mandated environmental reporting standards would enable

corporations to define th eir responsibilities and be able to deliver useful reports which

would, in turn, help corporate managem ent assess the environm ental considerations oftheir operations. Such criteria-based reports would also empower corporate manage-ment to compare their environmental efforts to those of the ir com petitors. Curren tly,environmentally proactive compjinies have difficulty distinguishing themselves fromother companies because of the lack of environmental reporting standards. PolaroidCorporation, for example, has attempted, in recent years, to publicly disclose usefulenvironmental data about the company but has been stymied in their efforts by theabsence of reporting criteria. Polaroid's diirector of health, safety and environment statedthat, without recognized standards, environmental information can always be chcd-lenged as inaccu rate or incomplete (Aeppel 1993).

Environmental reporting standards would also benefit investors and other stake-holders by making the reports more consistent and comparable. Because of the extremediversity and lack of comparability among existing periodic environm ental repo rts, in-vestors may have difficulty using these reports to determ ine which compainies are moreenvironmentally oriented. Currently, corporate env ironmental reports can disclose asmuch or as little information as corporations prefer in whatever format they prefer.Many corporate officials, such as those at Bristol-Myers Squibb and Polaroid Corpora-tion, have expressed concern about public confusion resultin g from the lack of stand arddefinitions in environmental reporting (Aeppel 1993; Environmental Management To-day 1996). The term "water usage ," for example, can be defined differently from com-

pany to company and indu stry to indus try {Environmental Management Today 1996).While some corporations genuinely wa nt to be environmentally friendly and share

8/8/2019 Beets 1999

http://slidepdf.com/reader/full/beets-1999 9/18

Corporate Environmental Reports: The Need for Standards and an Environmental Assurance Service 137

enhance public relations (Aeppel 1993). Corporations may be especially tempted to pub-lish few tangible deta ils about their environm ental efforts if the ir com petitors' environ-mental programs and efforts a re more subs tantive than th eir own.

The Necessity of Environmental Verification StandardsIn addition to environmental reporting standards, the accounting profession

needs to study and consider several related issues to develop adequate guidelinesfor extern al env ironm ental verification. The reports in appendices A and B illus-tr at e the diversity that s tem s from a lack of verification sta nd ards . In reviewingthese four verification reports, one may wonder what is being verified. The tworeports in appendix A discuss the verifiers' examination of environm ental m anage-ment systems but do not comment specifically on the corporate environmental re-ports in which the verifiers' reports are included. The two reports in appendix B,

on the other hand, specifically verify the corporations' periodic environmental re-ports. A consequent issue that must be addressed in promulgating environmentalverification standards is the scope of a verification engagement. To what extent,for example, should the verifier examine the corporation's environmental systems,or should the verification enga gem ent be confined to dete rm ining t he credibility ofinformation published in the periodic environmental report?

As discussed previously, another critical issue that must be addressed by the verifi-cation process is the adequacy of reported environmental liabilities disclosed in boththe financial statem ents and environmental reports. Verifiers must a ssess the client'sdisclosure of environmental contingencies, liabilities and the related risks.

Other considerations of an external environmental verifier include disclosures ofcontaminated asse ts and hazardous waste, the effectiveness of interned controls relatedto environmental issues, and client adherence to applicable environmental laws andregulations, as well as SEC rules regarding environmental issues (Dittenhofer 1995).The SEC, for example, curren tly m andates that public corporations file a report if pol-lution expenditures are having a material effect on earnings (Williams and Phillips1994). While these issues will have to be addressed by the verifier, the re w ill doubtlessbemany other company-specific and industry-specific environmental concerns that willrequire consideration d uring a verification engagement.

The Necessity of Environmental E xpertise in Public A ccountingAnother major challenge to external verification of environmental reports is the

scarcity of requisite environm ental verification expertise in the public accounting pro-fession. Public accountants may be interested in developing a new assurance or attes ta-tion service related to corporate environmental reports, but th eir qualifications to pro-vide such services may be questioned. This problem m ay be partially addressed by arecent cooperative effort by the Environm ental Auditing Roundtable and th e Ins tituteof Inte rna l A uditors (IIA). In 1997, these two groups created th e Board of Environmen-tal Auditor Certifications (BEAC), an independent, nonprofit organization intended toprovide certification of environmental auditors. A public accountant who wishes to at-tain the BEAC 14000 PLUS certification must successfully complete an examinationand have appropriate education and environmental auditing experience. The IIA iscurren tly offering comprehensive courses to train individuals in environmental audit-

8/8/2019 Beets 1999

http://slidepdf.com/reader/full/beets-1999 10/18

138 Accounting Horizons/June 1999

A NEW NICHE FOR PUBLIC ACCOUNTANTS

The role of public accountan ts in society is rapidly evolving with the emergence ofmany assurance services that expand the profession into dimensions of client service

which have not been previously offered by accounting firms. In addition to promoting awide variety of professional service possibilities, the Internet site of the AICPA indi-cates that environmental matters may result in assurance opportunities for AICPAmem bers, and Elliot and Pallais (1997,59) similarly suggest th at infonnation related toair and water quality, environmental restrictions and environmental effects are appro-pr iate assurance services for professional accountants to offer com panies. They also list"annual environmental report" in a list of assurance services possibilities (Elliot andPallais 1997).

The credibility of corporate environm ental information is critical as it may be influ-encing investing decisions, and many in the accounting, business and environmental

communities believe that public accountants should and will have a role in attesting tothese disclosures (Cheney 1995; Environmental Management Today 1996; Sylph 1992).If accounting firms acquire the related expertise, they can address this concern as theyhave historically with regard to a company's financial infonnation. By providing assur-ance on environmental reports , public accoimtants may foster investor reliance on thesereports and develop a new and potentially profitable service to offer existing and pro-spective clients.

Because of accounting firms' historical and traditional services, however, some com-panies and investors may be skeptical of the competence of public accountants in pro-viding assurance services that require specialized knowledge and skills that are not

typically associated with accounting firms (Burgess 1995). Robert K. Elliot (1994b, 80),Vice Chair of the AICPA, explained:

A question also might be raised on the grounds of the CPA's competence. However,the re is no reason CPA firms, convinced of the ra nge of availab le op portu nities, can-not an d will not seek an d employ th e rele van t portfolio of skills to fulfill such a broad errole. If the opportunities are attractive, competence will be achieved.

The BEAC 14000 PLUS certification th at is curren tly being offered by the IIA is anexample of efforts by accountamts to enhance their skills regau-ding environmental at-testation. In the interes t of expanding the array of assurance services offered by publicaccountants and enhancing their competence in providing those services, the AICPA

may develop a program similar to that of the IIA.An accounting firm that is interested in entering the environmental verification

marke t may develop a cooperative arrangement with an environmental consulting firm.Such an arrangement could mitigate concerns regarding the environmental compe-tence of the accounting firm in such engagements and relieve, to some extent, theaccountant's responsibility to acquire the needed expertise. In such a partnership, anenvironmental consulting firm would presumably bring environmental expertise to therelationship, while the accounting firm would add experience re lated to interna l con-trols, evidence gathering and repo rting. The British Petroleum report in appendix B isan example of a collaborative verification effort between a public accounting firm, Ern st

& Young, Eind an environmental consulting firm. Environmental Resources Manage-ment Limited.

8/8/2019 Beets 1999

http://slidepdf.com/reader/full/beets-1999 11/18

Corporate Environmental Reports: The Need for Standards and an Environmental Assurance Service 139

synergy, however, afforded by a corporation contracting one accounting firm to provideassurance on both the environmental rep ort and the financial statem ents would likelyresult in lower total professional fees for those services, as well as an expanded rela-

tionship between the firm and client. This suggestion of an expansion of the publicaccountant-client relationship is consistent with the similar concepts of business audits(Drucker 1992) and multidimensional attestatio n (Uzumeri and Tabor 1997) wherebypublic accountants atte st to a wide variety of corporate infonnation beyond the histori-cal financial statements. Obviously, for public accounting firms that are qualified toprovide these services, verification of environmental reports may also develop as anexpansion service to offer po tential clients whose curren t fineincial sta tem ent aud itorshave not acquired the necessary skills.

A public accountant's examination of a corporate environmental report is currentlyconsidered an attestation engagement subject to the AICPA S tatements on Staindards for

Attestation Engagements. With this type of engagement, the practitioner makes state-ments regarding the conformity of management assertions with applicable criteria. Asdiscussed previously, however, the continuing issue for environmental report verificationis the definition of the applicable criteria or standard s. Until such criteria a re developed,the value of attestation on environmental reports and disclosures is questionable.

Because of the lack of widely accepted criter ia for corporate environm ental reports ,the attestation stand ards currently place public accountants at a competitive disadvain-tage with consulting firms that are not bound by such standards. Environmental con-sulting firms can essentially perform whatever procedures they consider necessary whenengaged to verify corporate environmental information and create whatever reports

they deem appropriate. The resulting varied reports, such as those in the appendices,not only confuse stakeholders and investors but re tard requests for them. Understand-ably, members of the accounting profession have been critical of the verification effortsconducted by consulting firms (Environmental Management Today 1996). At present,public accounting firms th at a re interested in providing environm ental verification ser-vices find themselves in a difficult position. They mu st acqu ire the necessary expertise,build a client base of companies th at are interested in the service, and perform environ-mental verification w ithin the para m eters of the attes tation stan dards th at provide nospecific guidance w ith regard to environm ental assurance. This process must be accom-plished while competing with environmen tal consulting firms that are not restricted by

such standards.If the AICPA, however, acts quickly in establishing s tand ards for an environmentalassurance service, the attes tation stan dards can provide a framework whereby the pro-fession may simultaneously create a demeind for environmental verification and grantitself an exclusive market advantage in providing those services. Environmental verifi-cation may be developed as an assuran ce service analogous to WebTrust, an assuranceservice offered exclusively by AICPA mem bers. When a corporation th at is interested indirect marketing through the World Wide Web contracts with an AICPA member toprovide the W ebTrust service, the member performs specific procedures recommendedby the AICPA in examining the security and controls related to the company's web site.If the results are satisfactory, the AICPA member grants the company the right todisplay the AICPA WebTrust seal on their web site for a limited period of time. Thisseal provides consumers with a degree of assurance tha t they can safely conduct In ternet

8/8/2019 Beets 1999

http://slidepdf.com/reader/full/beets-1999 12/18

140 Accounting Horizons/June 1999

In a similar fashion, th e AICPA could develop an environmental a ssurance serviceth at would result in a "green seal" tha t companies could display on their web site andpublished periodic environmental report. This seal would signify that an AICPA mem-

ber had conducted certain procedures related to the environmental performance sinddisclosures of a company and was satisfied that criteria had been met. To obtain theseal, companies would have to contract with an AICPA member who provided the AICPAenvironmental assurance service.

This arrangem ent could prove advantageous to many stakeholders. Because of thestanda rds and requirements imposed by such a service, corporations would benefit fromthe credibility that third-party verification would add to their environmental disclo-sures. As mentioned previously, such verification would undoubtedly result in increasedexpenses related to professional fees, but the se costs may be offset by resulting positivepublicity regarding the company's environmental efforts. Investors and the general public

would similarly benefit from an AICPA green seal because it would enable them toquickly and easily determine which companies are environmentally oriented withoutinvestor knowledge of environmental jargon or analysis of convoluted verification re-ports such as those in the appendices. AICPA members would benefit from having anadditional well-defined assurance service to offer companies, and demand for this ser-vice could grow quickly as companies and investors act to take advan tage of the ben-efits mentioned above. Additionally, such an assurance service would be controlled bythe AICPA, as is the W ebTrust designation discussed previously. As a consequence, theAICPA environmental assurance service would be offered exclusively by AICPA mem-bers, and consulting firms th at are not m embers of the AICPA could no t offer the ser-

vice. Fina lly, a very positive eventual outcome of an AICPA -sanctioned environm entalassurance service may be greater corporate stew ardship of the environment, as compa-nies amend their practices in an effort to achieve the green seal designation.

From a regulatory perspective, development of an environmental assurance servicemay also m itigate th e likelihood of additional government involvement regard ing cor-porate environmental disclosures. The EPA, SEC and stat e and local governments m aybe content w ith a corporation's environm ental disclosures if the resu lts of an environ-mental assurance engagement are satisfactory.

Considering the m arketing aspects of a green seal designation, expeditious AICPAdevelopment of this assuramce service could be an appropriate and timely reaction to

three m arket trends . First, many public accounting firms are currently attemp ting tofind appropriate extensions of their ex isting attes tation skills and expand the ir assur-ance service offerings. Second, many investors wemt credible, verified information aboutcorporate environm ental efforts. T hird, corporations th at are willing to provide moreenvironmental data are often frustrated by the current lack of standards and criteriafor environmental reporting.

While the m arke t for environmental assurance seems promising, however, the ac-counting profession's "window of opportunity" may be limited, as many consulting firmsare also interested in providing this service. Delays by the accounting profession inaddressing environmental verification issues will allow other consulting firm s to de-

velop the needed expertise and client base before many public accountants enter thism arke t. Groups or organizations of consulting firms m ay develop the ir own green seal

8/8/2019 Beets 1999

http://slidepdf.com/reader/full/beets-1999 13/18

Corporate Environmental Reports: The Need for Standards and an Environmental Assurance S ervice 14 1

environmental reports from regulatory authorities. In the interests of environmentalprotection and g reate r private sector enviro nm ental accountability, the EPA m ay beginrequiring e xtern al verification of corporate environm ental information; an action th at

the agency has already prescribed for some individual companies in the past (Aeppel1993). Os tensibly , th e SEC , acting in th e int ere sts of th e investin g public, could furth erimprove the quality of information being delivered to present and potential stockhold-ers by req uirin g verification of corporate environm ental reports.

CONCLUSIONIn an era of increased environ me ntal aw aren ess and busines s scrutiny, corporate

environmental reports may be having an appreciable effect on investment decisions.External verification of this information would lend substantial credibility to this newtren d in corporate com munications and w ould benefit th e investing public by providing

assura nce on a relatively new form of disclosure in an increasingly complex inv estm entm arke tplace . For such benefits to accrue, however, the accounting profession m us t beproactive in promulgating environmental reporting and verification standards and de-veloping an environmental assurance service.

In one corporation's recent en viron m ental re port, th e Chief Executive Officer stated :

Why are we issuing this report? Because it's important that you know what (ourcompany) is doing to protect...the environment. We think we are acting responsiblyin these a reas. Now you have the facts to make your own judgment.

W hat ass uran ce do stockholders and potential investors have th at this repor t gives theneeded facts to m ake such a judgm ent? Is the information contained in this re port

accurate and reliable? If this report h ad been verified by a public accoun tant thro ughan env ironm ental a ssura nce service, the stak ehold ers would certainly be bette r able todraw conclusions about the company's environmentad efforts.

APPENDIX ATwo Examples of Environmental Verification Reports of Companies

Based in the United States

Example 1:Third-Party Evaluation of DuPont's Safety, Health and Environment (SHE) Audit ProgramsEnvironm ental Resources Management, Inc. (ERM) conducted an evaluation of DuPont's Envi-ronm ental, Safety, Occupational Health and Process Safety Audit Programs managed by Corpo-rate Safety, Health and Environment Excellence Center and implemented by the Company'sStrategic Business Units. ERM evaluated the elements and performance of the Programs inorder to render an independent opinion about their effectiveness in achieving improved SHEperformance throughout the Company. The assessment was conducted between May and No-vember 1996 and included a review of Program documentation, interviews with Program Man-agers and staff, selected interviews of site represen tatives who have been subject to the aud itsand observation of nine audits.

The Programs were evaluated against (1) audit program criteria developed by the U.S. Environ-mental P rotection Agency in its 1986 and 1995 Environm ental Auditing Policy Statements, bythe 1993 U.S. Department of Justice Draft Corporate Sentencing Guidelines for Environmental

8/8/2019 Beets 1999

http://slidepdf.com/reader/full/beets-1999 14/18

142 Accounting Horizons/June 1999

policy as principally articulated in its SHE Audit Program Stand ard, and (3) generally acceptedaudit practices existing in comparable companies.

ERM reviewed the scope and elements of the Programs, the procedures utilized, the resources

applied to implement the Programs and the degree and quality of management commitment.Based on the information m ade available to ERM by DuPont, ERM has concluded th at DuPont'sPrograms are generally consistent with and, in some cases, exceed expectations of the estab-lished criteria. In our opinion, the Programs provide competent, reliable and objective informa-tion to management about the status of the Company's SHE compliance programs and perfor-mance. Further, DuPont's management is responsive in correcting deficiencies when they areidentified by the Programs.

As shown in Figure 1, a number of the Program's elements, such as the written aud it proceduresand qua lity assurance, a re quite advanced when compared to practices in other companies. Twoelements, including auditor independence and verification of the resolution of corrective actions,were identified during the ERM evaluation as areas still needing improvement. Managementhas been informed of these issues and is currently taking steps to respond to them.

Environmental Resources Management, Inc.

Example 2:

To the M anagement ofWMX Technologies, Inc.

We have reviewed the appropriateness and quality of the environmental, health, and safetymanagement systems in place during 1996 at WMX Technologies, Inc. and its principal operat-ing sub sidiaries.

Our review included an assessm ent of policies and procedures, organization, tra inin g program s,

regulatory and management reporting systems, risk assessment and risk management pro-grams, regulatory surveillance systems, audit programs and corrective action systems, andother environmental, health and safety manag ement programs and systems in place through-out the Company. In conducting our review, we examined selected documents and interview edkey employees at the corporate and operating subsidiary levels, as well as at select operatingfacilities. We conducted our review rel5dng upon our judgm ent based on our extensive consult-ing experience in this area as well as our familiarity with similar programs established bymany other corporations.

In our opinion, WMX Technologies, Inc.'s corporate, subsidiary, and facility environmental man-agement systems place it among the leaders of industry as a whole with regard to environm entalmanagement.

In our opinion, while WMX Technologies, Inc.'s corporate, subsidiary and facility managem entsystems for health and safety are less matu re and not as comprehensively implemented as thosefor environment, they are generally consistent with good practice found in in dustry worldwide.

Arthur D. Little, Inc.December 1996

8/8/2019 Beets 1999

http://slidepdf.com/reader/full/beets-1999 15/18

Corporate Environmental Reports: The Need for Standards and an Environmental Assurance Service 14 3

APPENDIX BTwo Examp les of Environmental Verification Reports of Compan ies

Based Outside the United States

Exam ple 1:Ernst & Young Report on Health, Safety and Environment (HSE> Facts 1996

To: The Board of Directors of the British Petroleum Company p.l.c.

We have carried out a review of the da ta and state me nts in HSE Facts 1996, the pre paration ofwhich is the respon sibility of the d irectors. Our objective was to form an in depe nden t view on thestatements made, and the processes by which the data was collected and collated. We wereassiste d by En viron me ntal Resources M anag em ent L imited in respect of data collation processes.

This report has been prepared in accordance with the recomm endations issued by the Europ eanFederation of Accountants (FEE) "Expert Statem ents on Env ironmen tal Repo rts."

Basis of our reviewIn accordance with your instructions, our review comprised the following:

1. Discussions with a selection of HSE executives throughout BP and a review of documentsincluding Board and HSE Audit Committee minutes for 1996 to ensure that all significantHSE events have been considered for inclusion

2. A review of documents provided to us by management, and obtained in the public domain, toensure that statements made are consistent with underlying information

3. A review of th e meth ods used for data collection a nd collation at BP's head office, an d a t theexploration regional office in Aberdeen, U K, Alliance oil refinery in New O rlean s, USA, a ndWingles chemicals manufacturing site, France , to gain an u nde rstand ing of data estimationand measurement methods used.

RecommendationsWe recommend:

1. Improvements to data collection processes at sites, with focus on consistent application ofmeasurement and estimation protocols to improve data accuracy, reliability and relevancefurther

2. A systema tic review of the ex tent of externally re porte d da ta in relation to all significant H SEissues

3. Implementation of the audit protocol, developed during this year's review, across BP's sites.

Conclusions

On the basis of th e review described above, we are pleased to find BP is continuing to enhan ce it scollection an d repo rting of corporate enviro nm ental performance da ta as evidenced by a year-on-year improvement in the processes used to collect data in terms of its clarity and consistency ofdefinitions. We believe th at th e statem ents made are suppo rted by underlying information andthat the reported data has been properly collated from the data provided by BP's operations.

Ern st & Young

London9 May 1997

Example 2:

AUDITORS' REPOR T

To the readers of the Progress Report on Environment, Health and Safety of Northern TelecomLimited:

8/8/2019 Beets 1999

http://slidepdf.com/reader/full/beets-1999 16/18

144 Accounting Horizons / June 1999

man agem ent of the C orporation. We have been engaged to review th e process used by manag e-men t in preparing this Report and evaluate wh ether the meas urem ents of environm ental, healthand safety performance are compiled on a reasonable basis and are fairly presented.

We have examined the Corporation's environment, health and safety policies as set out hereinand reviewed the approach used by man agem ent to me asure progress toward conformance w iththese policies. Our review included interviews with management and staff and, on a test basis,analysis of data collected; review of environment, health and safety audit reports; observationsof performance an d exam ination of relevant docum entation.

Based on the above procedures, in our opinion, ma nage me nt h as ado pted a reasonable approachto assessing the Corporation's environmental, health and safety performance for the year endedDecember 31, 1996, which is appropriately described in the Report, and the measurements ofenvironmental, health and safety perfonnance are fairly represented in all material respects.

Deloitte & ToucheToronto, CanadaMarch 4,1997

REFERENCES

Accountant, The. 1998. Going green . (April): 14.Aeppel, T. 1993. Firms reveal more details of environmental efforts but still don't tell all. Wall

Street Journal (December 13): B l.Burg ess, D. O. 1995. More on assura nce services. The C PA Journal (December): 10.CFO. 1996. A new disclosure environment. (February): 12.Chadwick, B., R. W. Rouse, and J. Surm a. 1993. Perspectives on env ironmen tal accounting. The

CPA Journal (January) : 18-24.Cheney, G. 1995. It's not easy being green but top com panies are try ing. Management Accounting

(December): 58-59.CPA Journal, The. 1997. New board of environmental auditor certifications (BEAC) to provide

BEAC 14000 PLUS certification. (October): 9.Demery, P. 1996. Is it time to tackle environmental issues? The Practical Accountant (Novem-

ber): 76-80 .Deutsch, C. H. 1998. For Wall Street, increasing evidence that green begets green. New York

Times (July 19): 7.Dittenhofer, M. 1995. Environ mental accounting an d au diting. Man agerial Auditing Journal

10(8): 4 0 - 5 1 .Drucker, P. F. 1992. Post-Capitalist Society. New York, NY: H arp er Collins.Eco-Management and Audit Scheme (EMAS). 1998. Help Desk Internet Site: <URL:http://

www.emas.lu>.Elliot, R. K. 1994a. Confronting the future: Choices for the attest function. Accoure^mg Horizons

(September): 10 6-124.. 1994b. The future of aud its. Journal of Accountancy (September): 74-82., and D. M. Pallais. 1997. First: Know your ma rket . Journal ofAccountancy (July): 56-63 .

Environmental Management Today. 1996. There's no rus h to verify corporate EHS rep orts. (March/

April) 1: 12-13.Environment Today. 1993. Survey un covers E-disclosure is sue s. (December): 27.Greer, J., and K. Bruno. 1996. Greenwa sh: The Reality Behind Corporate Environm entalism.

Fairfax, VA: Third World Network and APEX Pres s.

Investors Chronicle. 1998. Survey-ethical investm ent: Pensions w ith p rinciples. (July 17): 44.

Journal of Accountancy. 1994. M any comp anies fail to disclose environ me ntal liabilities. (July):12.

8/8/2019 Beets 1999

http://slidepdf.com/reader/full/beets-1999 17/18

Corporate Environmental RepoHs: The Need for Standards and an Environmental Assurance Service 14 5

Krumsiek, B. J. 1998. The emergence of a new era in m ut ua l fund inve sting: Socially respo nsibleinve sting comes of age. Journal of Investing (Winter): 84-99 .

Mastrandonas, A., and P. T. Strife. 1992. Corporate environmental communications: Lessonsfrom investors. Columbia Journal of World Business (Fall/Winter): 234-240 .

McMahon, M. S. 1995. The growing role of accountants in environmental compliance. The OhioCPA Journal (April): 21 -25 .

Risk Management. 1994. Corporations pressed for SEC d isclosure. (July): 15.Shanoff, B. 1995. EPA sets corporate audit policy. World Wastes (June): 78.Sylph, J. M. 1992. Apocalypse no! CA Magazine (January) : 24-29.St. Louis Post-Dispatch, The. 1997. A new weapon to expose polluters. (Au gust 14): B6.Uzumeri, M. V., and R. H. Tabor. 1997. Emerging management metastandards: Opportunities

for expanded attest services. Accounting Horizons (March): 54-66 .Williams, G., and T. J. Phillips, Jr. 1994. Cleaning up our act: Accounting for environmental

liabilities. Management Accounting {FehTuary): 30-33.

8/8/2019 Beets 1999

http://slidepdf.com/reader/full/beets-1999 18/18