Embed Size (px)

Citation preview

True Up for FY 2013-14

Madhya Pradesh Audyogik Kendra Vikas Nigam (Indore) Ltd. 1

BEFORE THE MADHYA PRADESH ELECTRICITY REGULATORY COMMISSION

BHOPAL

CASE NO:

Filing of the Petition for True Up of FY 2013-14 under the MPERC (Terms and Conditions

for determination of tariff for supply and wheeling of electricity and methods and

principles for fixation of charges) Regulations, 2012 along with other guidelines and

directions issued by the MPERC from time to time AND under Part VII (Section 61 to

Section 64) of the Electricity Act, 2003 read with the relevant Guidelines.

Filed by:-

MADHYA PRADESH AUDYOGIK KENDRA VIKAS NIGAM (INDORE) LTD

3/54, Press Complex, Free Press House, Indore (Madhya Pradesh)

True Up for FY 2013-14

Madhya Pradesh Audyogik Kendra Vikas Nigam (Indore) Ltd. 2

BEFORE THE MADHYA PRADESH ELECTRICITY REGULATORY COMMISSION

BHOPAL

Filing No:

Case No:

IN THE MATTER OF Filing of the Petition for True Up of FY 2013-14 under the MPERC

(Terms and Conditions for determination of tariff for supply and

wheeling of electricity and methods and principles for fixation of

charges) Regulations, 2012 along with other guidelines and

directions issued by the MPERC from time to time AND under Part

VII (Section 61 to Section 64) of the Electricity Act, 2003 read with

the relevant Guidelines

AND

IN THE MATTER OF Madhya Pradesh Audhogik Vikas Nigam (Indore) Ltd.

3/54, Press Complex, Free Press House, Indore (M.P.)

PETITIONER

THE PETITIONER ABOVE NAMED RESPECTFULLY SUBMITS

True Up for FY 2013-14

Madhya Pradesh Audyogik Kendra Vikas Nigam (Indore) Ltd. 3

TABLE OF CONTENTS

1. Executive Summary .................................................................................................. 6

1.1. Preamble ........................................................................................................... 6

1.2. True Up of FY 2013-14 ...................................................................................... 7

2. Introduction ........................................................................................................... 10

2.1. Preamble ......................................................................................................... 10

2.2. Introduction .................................................................................................... 10

2.3. Submission to the Hon’ble Commission ......................................................... 11

3. True Up for FY 2013-14 .......................................................................................... 13

3.1. Preamble ......................................................................................................... 13

3.2. Principles for True Up for FY 2013-14 ............................................................. 13

3.3. Category wise Sales ......................................................................................... 14

3.4. Distribution Losses .......................................................................................... 14

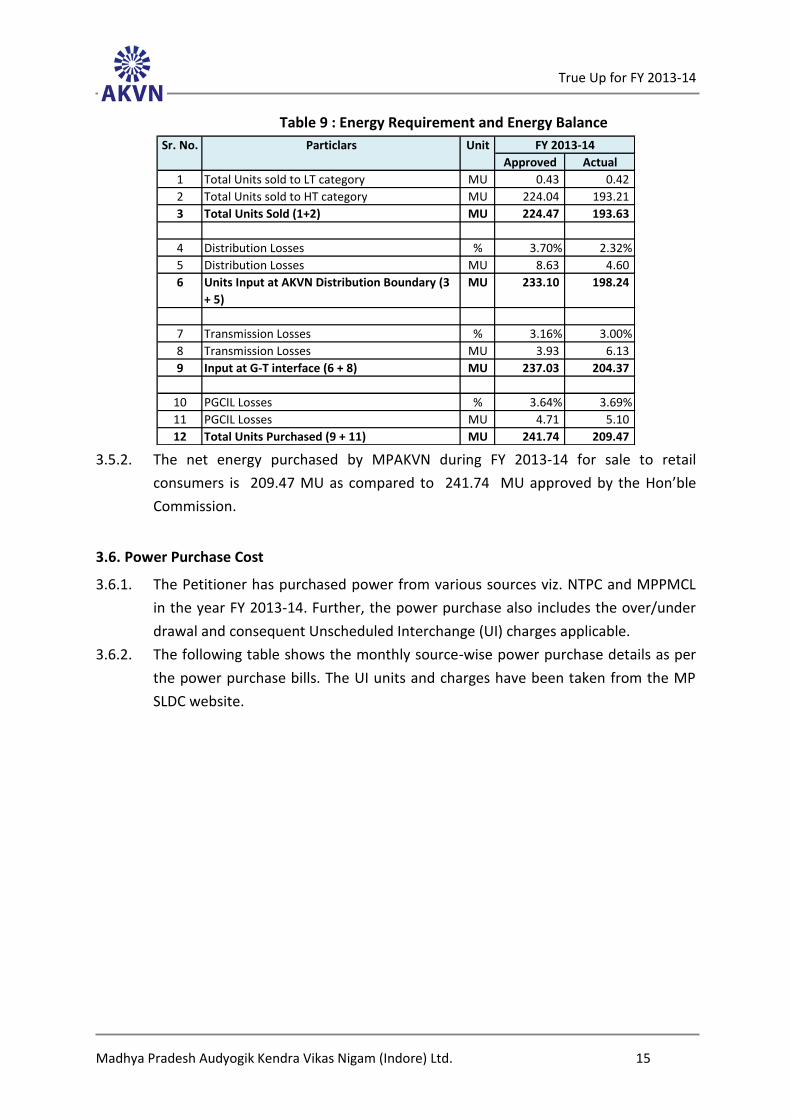

3.5. Energy Requirement and Energy Balance....................................................... 14

3.6. Power Purchase Cost ...................................................................................... 15

3.7. Transmission Charges ..................................................................................... 17

3.8. Capitalisation .................................................................................................. 17

3.9. Funding of Capital Expenditure ...................................................................... 18

3.10. Aggregate Revenue Requirements for FY 2013-14 ........................................ 18

3.11. Operation & Maintenance Expenses .............................................................. 19

3.12. Depreciation .................................................................................................... 23

3.13. Interest & Financial Charges ........................................................................... 24

3.14. Interest on Working Capital ............................................................................ 25

3.15. Lease Rent ....................................................................................................... 25

3.16. Return on equity ............................................................................................. 28

3.17. Other Income .................................................................................................. 28

3.18. Income Tax ...................................................................................................... 28

3.19. Aggregate Revenue Requirement for FY 2013-14 .......................................... 29

3.20. Revenue for FY 2013-14 .................................................................................. 30

3.21. Revenue Gap / (Surplus) for FY 2013-14 ........................................................ 30

4. Prayer ..................................................................................................................... 31

True Up for FY 2013-14

Madhya Pradesh Audyogik Kendra Vikas Nigam (Indore) Ltd. 4

Annexure 1: Letter of CAG ....................................................................................................... 32

Annexure 2: Letter of GoMP regarding lease rent .................................................................. 33

Annexure 3: Tariff Filing Formats............................................................................................. 35

True Up for FY 2013-14

Madhya Pradesh Audyogik Kendra Vikas Nigam (Indore) Ltd. 5

LIST OF TABLES

Table 1 : Category-wise Sales (MU) ........................................................................................... 7

Table 2 : Distribution Losses ...................................................................................................... 7

Table 3 : Power Purchase Cost for FY 2013-14 ......................................................................... 8

Table 4 : Capitalization for FY 2013-14 (Rs. Crore) .................................................................... 8

Table 5 : Aggregate Revenue Requirement for FY 2013-14 (Rs. Crore) .................................... 9

Table 6 : Revenue Gap/ (Surplus) for FY 2013-14 (Rs. Crore) .................................................... 9

Table 7 : Category-wise Sales (MU) ......................................................................................... 14

Table 8 : Distribution Losses .................................................................................................... 14

Table 9 : Energy Requirement and Energy Balance ................................................................. 15

Table 10 : Summary of source-wise Power Purchase Quantum and Cost for FY 2013-14 ..... 16

Table 11 : Power Purchase Cost for FY 2013-14 ..................................................................... 17

Table 12 : Transmission Charges for FY 2013-14 (Rs. Crore) .................................................. 17

Table 13 : Capitalization for FY 2013-14 (Rs. Crore) ................................................................ 18

Table 14 : Funding of Capitalisation (Rs. Crore) ...................................................................... 18

Table 15 : Employee Cost for FY 2013-14 (Rs. Crore) .............................................................. 19

Table 16 : Repair & Maintenance Cost for FY 2013-14 (Rs. Crore) .......................................... 22

Table 17 : Administration & General Expenses for FY 2013-14 (Rs. Crore) ............................. 22

Table 18 : O&M Expenses for FY 2013-14 (Rs. Crore) ............................................................. 23

Table 19 : Depreciation for FY 2013-14 (Rs. Crore) ................................................................. 23

Table 20 : Net Depreciation for FY 2013-14 (Rs. Crore) .......................................................... 23

Table 21 : Interest & Financial Charges for FY 2013-14 (Rs. Crore) ......................................... 24

Table 22 : Interest on Consumer Security Deposit for FY 2013-14 (Rs. Crore) ....................... 24

Table 23 : Interest on Working Capital for FY 2013-14 (Rs. Crore) ......................................... 25

Table 24 : Lease Rent for FY 2013-14 (Rs. Crore) ..................................................................... 26

Table 25 : Return on Equity for FY 2013-14 (Rs. Crore) ........................................................... 28

Table 26 : Other Income for FY 2013-14 (Rs. Crore) ................................................................ 28

Table 27 : Income Tax for FY 2013-14 (Rs. Crore) .................................................................... 29

Table 28 : Aggregate Revenue Requirement for FY 2013-14 (Rs. Crore) ................................ 30

Table 29 : Revenue Gap/ (Surplus) for FY 2013-14 (Rs. Crore) ................................................ 30

True Up for FY 2013-14

Madhya Pradesh Audyogik Kendra Vikas Nigam (Indore) Ltd. 6

1. Executive Summary

1.1. Preamble

1.1.1. Madhya Pradesh Audyogik Kendra Vikas Nigam (Indore) Ltd., (hereinafter referred

as the ‘Petitioner’, MPAKVN, ‘the Company’ or ‘the Licensee’), is a Company

incorporated under the Companies Act, 1956(Now Companies Act, 2013) having its

registered office at 3/54, Press Complex, Free Press House, Indore. The Petitioner is

a deemed distribution licensee under the fifth Proviso to Section 14 of the

Electricity Act, 2003. The area of supply of the Petitioner is SEZ Indore (Pithampur)

within the State of Madhya Pradesh (‘MP’).

1.1.2. The Government of Madhya Pradesh (‘GoMP’ or ‘State Government’), has passed

the Special Economic Zone Policy in August 2003. The Indore Special Economic

Zone (Special Provisions), Act 2003 was also enacted in the year 2003. This Act has

been passed by the Madhya Pradesh Vidhan Sabha on dated 28th March 2003

(Madhya Pradesh Act No 23 of 2003), The Indore Special Economic Zone (Special

Provisions), Act 2003 an Act to provide for the development, operation,

maintenance and administration of Indore Special Economic Zone.

1.1.3. It is submitted that licensee MPAKVN (I) Ltd. is the wholly owned undertaking of

Government of Madhya Pradesh and working for the Industrial Promotion &

Development in the State. MPAKVN (I) Ltd has three subsidiary Companies viz.

SEZ Indore Ltd (Specially formed for the operation, development, maintenance

and administration of SEZ for which MPAKVN (I) Ltd is a Deemed Distribution

Licensee),

Crystal IT Park Indore Ltd. and

Pithampur Auto Cluster Ltd.

1.1.4. In the backdrop of the above facts and circumstances, the present application is

being submitted by the Petitioner (MPAKVN Indore Ltd.) under Section 61 and

Section 62 (1) (d) of the Electricity Act 2003 for True up for ARR of FY 2013-14

under the MPERC (Terms and Conditions for determination of tariff for supply and

wheeling of electricity and methods and principles for fixation of charges)

Regulations, 2012 hereinafter referred as “Tariff Regulations, 2012”.

1.1.5. The present application is being submitted by the Petitioner under Section 61 and

Section 62 (1) (d) of the Electricity Act 2003 for True up for ARR of FY 2013-14

under the tariff principles laid down in the Tariff Regulations, 2012 for approval by

the Hon’ble Commission.

True Up for FY 2013-14

Madhya Pradesh Audyogik Kendra Vikas Nigam (Indore) Ltd. 7

1.2. True Up of FY 2013-14

1.2.1. The actual ARR for FY 2013-14 is based on audited accounts of FY 2013-14 and the

principles adopted by the Hon’ble Commission in its previous Orders on various

ARR elements. The actual expenses have been compared against those approved

for FY 2013-14 in the Tariff Order dated 10th September, 2013 under Petition No.

38/2013.

1.2.2. The actual Energy Sales and those approved by the Hon’ble Commission in its Order

approving the ARR for FY 2013-14 are compared for True up purposes. The

following table shows the energy sales for FY 2013-14.

Table 1 : Category-wise Sales (MU)

Approved Actual

LT Consumer Categories

Non Domestic - 0.04

Public Water Works and Street Light 0.21 0.28

Industrial 0.22 0.10

Total LT Sale 0.43 0.42

HT Consumer Categories

Industrial 224.04 193.21

Non Industrial - -

Total HT Sale 224.04 193.21

Total LT+HT Sale 224.47 193.63

FY 2013-14Consumer Category

1.2.3. In FY 2013-14, the actual distribution losses were 2.32% as against the approved

level of 3.70%. The table below highlights the comparison of actual distribution

losses against that approved by the Hon’ble Commission vide its Tariff Order.

Table 2 : Distribution Losses

Particulars FY 2013-14

(Approved)

FY 2013-14

(Actual)

Distribution Losses 3.70% 2.32% 1.2.4. For FY 2013-14 the Petitioner had proposed the procurement of power from

sources such as NTPC and MPPKVVCL. The comparison of the approved and the

actual cost of power purchase for FY 2013-14 is given in the table below. The

reasons for variation in the power purchase cost as claimed in this Petition as

compared to the audited annual accounts have been elaborated in the subsequent

chapters.

True Up for FY 2013-14

Madhya Pradesh Audyogik Kendra Vikas Nigam (Indore) Ltd. 8

Table 3 : Power Purchase Cost for FY 2013-14

Units

(MU)

Cost

(Rs. Crore)

Units

(MU)

Cost

(Rs. Crore)

NTPC 129.13 26.18 138.12 29.36

MPPKVVCL 112.61 63.02 56.45 30.85

MPPMCL - - - -

Unscheduled Interchange - - 14.89 6.12

Power Purchase 241.74 89.20 209.47 66.32

Particular FY 2013-14 (Approved) FY 2013-14 (Actual)

1.2.5. The actual capitalization of MPAKVN during the FY 2013-14 is Rs. 3.08 Crore out of

which the capitalisation from consumer contribution is Rs. 0.17 Crore. The actual

capitalisation is higher than that approved by the Hon’ble Commission at Rs. 1.25

Crore in the Tariff Order dated 10th September, 2013. The following table shows

the capitalisation for FY 2013-14.

Table 4 : Capitalization for FY 2013-14 (Rs. Crore)

Particulars FY 2013-14

(Actual)

Furniture and Fixture -

Computers -

Buildings 0.06

Plant and Macinery 3.02

Total 3.08 1.2.6. The True up of Aggregate Revenue Requirement of MPAKVN for FY 2013-14 as

against the values approved by the Hon’ble Commission is summarised in the table

below. The element wise details are provided in subsequent chapters of the

Petition.

True Up for FY 2013-14

Madhya Pradesh Audyogik Kendra Vikas Nigam (Indore) Ltd. 9

Table 5 : Aggregate Revenue Requirement for FY 2013-14 (Rs. Crore)

Approved Actual

1 Purchase of Power 89.20 66.32

2 Inter-State Transmission Charges 2.78 4.71

3 Intra-State Transmission (MP Transco) Charges 2.80 4.41

4 SLDC Charges 0.01 0.04

5 Employee Expenses 3.60

6 R&M Expenses 4.32

7 A&G Expenses 2.50

8 MPERC and MPPMCL Fees & Other 0.01 0.01

9 Depreciation 0.39 0.62

10 Interest & Finance Charges 1.33 1.90

11 Interest on Working Capital - -

12 Lease Rent - 4.64

13 Income Tax 0.14 -

14 Sub Total (1 to 13) 100.94 93.09

14 Return on Equity 0.42 0.62

15 Total Expenditure (13 + 14) 101.36 93.71

16 Less: Other Income 0.02 0.43

17 Aggregate Revenue Requirement (15 - 17) 101.34 93.28

Sr. No. Particulars FY 2013-14

4.28

1.2.7. This Aggregate Revenue Requirement is compared against the actual Income of Rs.

87.48 Crore under the head Revenue from Sale of Power. Accordingly, total

Revenue Gap of MPAKVN for FY 2013-14 is as depicted in the table below:

Table 6 : Revenue Gap/ (Surplus) for FY 2013-14 (Rs. Crore)

Sr. No. Particulars FY 2013-14

(Actual)

1 Aggregate Revenue Requirement 93.28

2 Revenue from Sale of Power 87.48

3 Revenu Gap/(Surplus) (1-2) 5.80 1.2.8. The Hon’ble Commission is requested to approve above mentioned revenue gap

and allow recovery of the same while determination of the retail tariff for FY 2018-

19.

True Up for FY 2013-14

Madhya Pradesh Audyogik Kendra Vikas Nigam (Indore) Ltd. 10

2. Introduction

2.1. Preamble

2.1.1. This section presents the background and reasons for filing this Petition.

2.2. Introduction

2.2.1. Madhya Pradesh Audyogik Kendra Vikas Nigam (Indore) Ltd., (hereinafter referred

as the ‘MPAKVN’ or ‘Petitioner’ or ‘the Company’ or ‘the Licensee’), is a Company

incorporated under the Companies Act, 1956 (which has now been superseded by

the Companies Act, 2013) having its registered office at 3/54, Press Complex, Free

Press House, Indore. The Petitioner is a deemed distribution licensee under the

fifth Proviso to Section 14 of the Electricity Act, 2003. The area of supply of the

Petitioner is SEZ Indore (Pithampur) within the State of Madhya Pradesh (‘MP’).

2.2.2. The Government of Madhya Pradesh (‘GoMP’ or ‘State Government’), has passed

the Special Economic Zone Policy in August 2003. The Indore Special Economic

Zone (Special Provisions), Act 2003 was also enacted in the year 2003. This Act has

been passed by the Madhya Pradesh Vidhan Sabha on dated 28th March, 2003

(Madhya Pradesh Act No 23 of 2003) and was enacted to provide for the

development, operation, maintenance and administration of Indore Special

Economic Zone.

2.2.3. The Madhya Pradesh Electricity Regulatory Commission (hereinafter referred to as

“MPERC” or “the Hon’ble Commission”), an independent statutory body

constituted by Government of Madhya Pradesh vide Gazette Notification dated

20th August, 1998 under Electricity Regulatory Commission’s Act, 1998.

Subsequently after the M.P. Vidyut Sudhar Adhiniyam, 2000 came into effect from

03rd July, 2001, the State Regulatory Commission was deemed to have been

constituted under State Act. The Electricity Act 2003 (No. 36 of 2003) enacted by

parliament has come into force w.e.f. 10th June, 2003 and the Commission is now

deemed to have been constituted and functioning under the provisions of

Electricity Act 2003.

2.2.4. The Hon’ble Commission has issued the MPERC (Terms and Conditions for

determination of tariff for supply and wheeling of electricity and methods and

principles for fixation of charges) Regulations, 2012 (hereinafter referred as “Tariff

Regulations, 2012”) which were effective from 1st April, 2013 and up to 31st March,

2016.

2.2.5. The present application is being submitted by the Petitioner under Section 61 and

Section 62 (1) (d) of the Electricity Act 2003 for True up for ARR of FY 2013-14

True Up for FY 2013-14

Madhya Pradesh Audyogik Kendra Vikas Nigam (Indore) Ltd. 11

under tariff principles laid down in the Tariff Regulations, 2012 for approval by the

Hon’ble Commission.

2.2.6. It is submitted that the MPAKVN has prepared separate Accounts for the power

business of the SEZ for FY 2013-14 on the basis of rational allocation of Revenue,

Expenses, and Assets & Liabilities between power & other business and shall

continue preparing separate Accounts for subsequent years as directed by the

Hon’ble Commission.

2.2.7. While filing the present True up and ARR under the prevailing Regulations,

MPAKVN has endeavoured to comply with the various applicable legal and

regulatory directions and stipulations including the directions of the Hon’ble

Commission in the Business Rules of the Commission, the Guidelines, previous ARR

of Discoms and Tariff Orders and the Regulations.

2.2.8. Based on the information available, the Petitioner has made sincere efforts to

comply with the Regulations of the Hon’ble Commission and discharge its

obligations to the best of its capabilities. However, if any further material

information becomes available in the near future, the applicant craves leave of the

Hon’ble Commission to file such additional information and consequently amend/

revise the application.

2.2.9. Shri D.L. Goyal, Joint Director (Planning) of MPAKVN has been authorized to

execute and file all the documents on behalf of the Petitioner in this regard.

Accordingly, the current filing is signed and verified by, and backed by the affidavit

of Shri D.L. Goyal.

2.3. Submission to the Hon’ble Commission

2.3.1. The Petitioner had filed the Petition in Case No. 38/2013 on 12 July, 2013. Vide

letter dated 16 August, 2013, the Hon’ble Commission directed the Petitioner to

substantiate the claims made in the Petition on various items of ARR. Meanwhile,

the petitioner was also directed to invite comments / suggestions / objections from

the stakeholders through a public notice which was published on 8 August, 2013.

The Hon’ble Commission held the motion hearing on 24 August, 2013 and admitted

the Petition vide order dated 26 August, 2013.

2.3.2. The Commission observed that the Petitioner submitted abstracts of the Balance

Sheet and Profit and Loss Account of MPAKVN (I) Ltd., Indore for FY 2011-12 and FY

2012-13, for its power business of SEZ at Pithampur, certified by Chartered

Accountant. These abstracts of Balance Sheet and Profit and Loss Account of power

business have been carved out from the annual accounts of MPAKVN (I) Ltd. on

pro-rata basis making certain assumptions for each item of expense related to the

power business. It further observed that the petitioner could not submit actual

True Up for FY 2013-14

Madhya Pradesh Audyogik Kendra Vikas Nigam (Indore) Ltd. 12

expenses incurred in the power business. Thus, in the Tariff Order the Commission

admitted the ARR of MPAKVN (I) Ltd. and determined the tariff provisionally for FY

2013-14.

2.3.3. MPAKVN hereby submits the Petition under Section 62 of the Electricity Act, 2003

for True-up of FY 2013-14 as per Tariff Regulations, 2012 and based on the audited

annual accounts for FY 2013-14 for the power business of MPAKVN.

True Up for FY 2013-14

Madhya Pradesh Audyogik Kendra Vikas Nigam (Indore) Ltd. 13

3. True Up for FY 2013-14

3.1. Preamble

3.1.1. This section outlines the actual performance of MPAKVN for FY 2013-14. The True

Up for FY 2013-14 has been prepared in line with the provisions of the Tariff

Regulations, 2012. It is submitted that the main Annual Accounts of MPAKVN are

audited by the CAG for FY 2013-14. As per the directions from the Hon’ble

Commission, MPAKVN requested the CAG to audit the Annual Accounts of the

power business of MPAKVN for FY 2010-11 to FY 2014-15. However, vide letter

dated 16 February, 2017, the CAG has stated that it has already conducted

supplementary audit of MPAKVN (I) Ltd., under Section 143(6) of the Companies

Act, 2013 up to the year 2015-16 and audited accounts had already been adopted

in the AGM of the Company. In the absence of any enabling provisions in the

Companies Act, the separate accounts of power business activity of the MPAKVN

for FY 2010-11 to FY 2014-15 cannot be audited/certified by the Statutory auditors/

the CAG. A copy of the said letter is attached at Annexure – 1. Accordingly, the

expenses for FY 2013-14 presented for True-Up are based on the Annual Accounts

duly audited by the Chartered Accountant for the power business of MPAKVN in

compliance with the directive issued by the Hon’ble Commission and other

principles specified in the Tariff Regulations, 2012. The ARR so arrived for the

purpose of true up has been compared with the ARR for FY 2013-14 approved by

the Hon’ble Commission vide Tariff Order dated 10th September, 2013.

3.2. Principles for True Up for FY 2013-14

3.2.1. As per Tariff Regulations, 2012, the Hon’ble Commission shall undertake the True

Up of the licensee for FY 2013-14 based on the comparison of the actual

performance of the past year with the approved estimates for such year.

3.2.2. In line with the provisions of Tariff Regulations, 2012, MPAKVN has filed this

Petition for True Up for the FY 2013-14. Information provided in the True Up for FY

2013-14 is based on the audited actual performance and considering the principles

adopted by the Hon’ble Commission in its previous Orders. The actual performance

has been compared with the ARR approved as per the Tariff Order dated 10th

September, 2013.

3.2.3. Accordingly, the details of the elements of the revised Aggregate Revenue

Requirement, the actual revenue earned during the year and the consequent

revenue gap for FY 2013-14 is discussed in the subsequent paragraphs of this

chapter.

True Up for FY 2013-14

Madhya Pradesh Audyogik Kendra Vikas Nigam (Indore) Ltd. 14

3.3. Category wise Sales

3.3.1. The following table shows the category-wise sales approved by the Hon’ble

Commission and actually recorded for FY 2013-14.

Table 7 : Category-wise Sales (MU)

Approved Actual

LT Consumer Categories

Non Domestic - 0.04

Public Water Works and Street Light 0.21 0.28

Industrial 0.22 0.10

Total LT Sale 0.43 0.42

HT Consumer Categories

Industrial 224.04 193.21

Non Industrial - -

Total HT Sale 224.04 193.21

Total LT+HT Sale 224.47 193.63

FY 2013-14Consumer Category

3.3.2. As can be seen from the table, the actual energy sales for both LT and HT

categories are lower as compared to that approved by the Hon’ble Commission in

its Tariff Order for FY 2013-14. Accordingly, MPAKVN requests the Hon’ble

Commission to approve the actual sales for FY 2013-14.

3.4. Distribution Losses

3.4.1. In FY 2013-14, the actual distribution losses were 2.32% as against the approved

level of 3.70% The table below highlights the comparison of actual distribution

losses against that approved by the Hon’ble Commission vide its Tariff Order.

Table 8 : Distribution Losses

Particulars FY 2013-14

(Approved)

FY 2013-14

(Actual)

Distribution Losses 3.70% 2.32%

3.5. Energy Requirement and Energy Balance

3.5.1. The energy balance based on the actual sales during the year and the distribution

losses for FY 2013-14 is given below:

True Up for FY 2013-14

Madhya Pradesh Audyogik Kendra Vikas Nigam (Indore) Ltd. 15

Table 9 : Energy Requirement and Energy Balance

Approved Actual

1 Total Units sold to LT category MU 0.43 0.42

2 Total Units sold to HT category MU 224.04 193.21

3 Total Units Sold (1+2) MU 224.47 193.63

4 Distribution Losses % 3.70% 2.32%

5 Distribution Losses MU 8.63 4.60

6 Units Input at AKVN Distribution Boundary (3

+ 5)

MU 233.10 198.24

7 Transmission Losses % 3.16% 3.00%

8 Transmission Losses MU 3.93 6.13

9 Input at G-T interface (6 + 8) MU 237.03 204.37

10 PGCIL Losses % 3.64% 3.69%

11 PGCIL Losses MU 4.71 5.10

12 Total Units Purchased (9 + 11) MU 241.74 209.47

Sr. No. Particlars Unit FY 2013-14

3.5.2. The net energy purchased by MPAKVN during FY 2013-14 for sale to retail

consumers is 209.47 MU as compared to 241.74 MU approved by the Hon’ble

Commission.

3.6. Power Purchase Cost

3.6.1. The Petitioner has purchased power from various sources viz. NTPC and MPPMCL

in the year FY 2013-14. Further, the power purchase also includes the over/under

drawal and consequent Unscheduled Interchange (UI) charges applicable.

3.6.2. The following table shows the monthly source-wise power purchase details as per

the power purchase bills. The UI units and charges have been taken from the MP

SLDC website.

True Up for FY 2013-14

Madhya Pradesh Audyogik Kendra Vikas Nigam (Indore) Ltd. 16

Table 10 : Summary of source-wise Power Purchase Quantum and Cost for FY 2013-14

MU Amount

(Rs. Crore)

MU Amount

(Rs. Crore)

MU Amount

(Rs. Crore)

MU Amount

(Rs. Crore)

MU Amount

(Rs. Crore)

April 11.00 2.17 4.53 2.47 - - 0.52 1.32 16.05 5.95

May 11.54 2.79 4.38 2.38 - - 0.61 0.22 16.52 5.39

June 9.94 2.23 4.81 2.56 - - 1.83 0.43 16.57 5.23

July 10.21 2.20 4.82 2.62 - - 2.12 0.52 17.14 5.33

August 9.29 1.86 4.99 2.72 - - 3.28 0.80 17.56 5.38

September 10.30 1.99 5.05 2.72 - - 2.46 0.75 17.81 5.46

October 11.52 3.07 4.91 2.66 - - 1.22 0.96 17.65 6.69

November 11.85 2.70 4.61 2.54 - - (0.52) (0.03) 15.93 5.22

December 12.02 2.83 4.47 2.46 - - 0.60 0.28 17.09 5.57

January 12.09 2.68 4.70 2.59 - - 0.49 0.16 17.29 5.43

February 10.70 2.28 4.60 2.56 - - 0.67 0.23 15.98 5.06

March 11.73 2.56 4.58 2.56 - - 1.63 0.49 17.93 5.61

Adjustment as

per REA

account

5.93 5.93 -

Total 138.12 29.36 56.45 30.85 - - 14.89 6.12 209.47 66.32

Particulars FY 2013-14

NTPC MPPKVVCL MPPMCL UI Total

3.6.3. It is submitted that there is some variation in the power purchase cost as claimed

in the True up Petition and as considered in the annual accounts on account of

various reasons as follows:

The amount of Rs. 4.32 Crore as per the O&M agreement with MPPKVVCL is

considered under the power purchase cost in the annual accounts for FY 2013-

14 which is claimed separately under the R&M expense head of the O&M

expenses in the present Petition.

A power purchase bill of NTPC amounting to Rs. 1.76 Crore for FY 2012-13 was

considered in the audited accounts of FY 2013-14 as it was paid during FY 2013-

14. However, since it is claimed in the Petition for FY 2012-13, it is not claimed

in the present Petition.

Payment of Rs. 6.21 Crore towards UI charges for over/under drawal of power

was made in FY 2013-14 was considered in the audited accounts of FY 2013-14,

however, the same is claimed in the present Petition as it is lump sum payment

towards UI charges and not actual cost of UI for FY 2013-14.

The actual cost of Rs. 6.12 Crore towards UI charges for over/under drawal of

power in FY 2013-14 is not considered in the annual accounts, however, the

same is claimed in the present Petition.

Moreover, MPAKVN is entitled to the gross power purchase cost considering

accrual basis of accounting however, in the audited annual accounts, the cost

towards power purchase has been considered on actual payment basis which is

net of all rebates/incentives/penalties etc. and hence a lower value of power

purchase cost is recorded in the annual accounts.

3.6.4. The comparison of the approved and the actual cost of power purchase for FY

2013-14 is given in the table below:

True Up for FY 2013-14

Madhya Pradesh Audyogik Kendra Vikas Nigam (Indore) Ltd. 17

Table 11 : Power Purchase Cost for FY 2013-14

Units

(MU)

Cost

(Rs. Crore)

Units

(MU)

Cost

(Rs. Crore)

NTPC 129.13 26.18 138.12 29.36

MPPKVVCL 112.61 63.02 56.45 30.85

MPPMCL - - - -

Unscheduled Interchange - - 14.89 6.12

Power Purchase 241.74 89.20 209.47 66.32

Particular FY 2013-14 (Approved) FY 2013-14 (Actual)

3.7. Transmission Charges

3.7.1. The Petitioner has submitted the PGCIL charges (for inter-state power purchase),

MPPTCL charges (for intra-state power purchase) and SLDC charges based on the

audited accounts for FY 2013-14 wherein the Transmission Charges have been

considered under the head of total Power Purchase Cost and are not available

separately.

3.7.2. The comparison of the approved and the actual transmission cost is as given in the

table below:

Table 12 : Transmission Charges for FY 2013-14 (Rs. Crore)

Particulars FY 2013-14

(Approved)

FY 2013-14

(Actual)

Intra-State Transmission Charges 2.78 4.41

Inter-State Transmission Charges 2.80 4.71

SLDC Charges 0.01 0.04

Total Transmission Charges 5.59 9.17 3.7.3. MPAKVN is entitled to the gross transmission charges considering accrual basis of

accounting however, in the audited annual accounts, the cost towards transmission

charges has been considered on actual payment basis which is net of all

rebates/incentives/penalties etc. and hence a lower value of transmission charges

is recorded in the annual accounts.

3.7.4. MPAKVN requests the Commission to approve the actual inter-state and intra-state

transmission charges & SLDC charges for FY 2013-14.

3.8. Capitalisation

3.8.1. The actual capitalization of MPAKVN during the FY 2013-14 is Rs. 3.08 Crore out of

which Rs. 0.17 Crore is through consumer contribution. The Hon’ble Commission

had approved capitalization of Rs. 1.25 Crore in the Tariff Order dated 10th

September, 2013.

3.8.2. The asset head wise capitalization in FY 2013-14 is as shown below.

True Up for FY 2013-14

Madhya Pradesh Audyogik Kendra Vikas Nigam (Indore) Ltd. 18

Table 13 : Capitalization for FY 2013-14 (Rs. Crore)

Particulars FY 2013-14

(Actual)

Furniture and Fixture -

Computers -

Buildings 0.06

Plant and Macinery 3.02

Total 3.08

3.9. Funding of Capital Expenditure

3.9.1. The funding of above mentioned Capital Expenditure is done through various

sources which are mainly categorised under four headings namely: (i) Consumer

Contribution; (ii) Grants; (iii) Equity; and (iv) Debt. The detailed breakup of funding

of capitalisation which took place during FY 2013-14 is mentioned in the table

below.

Table 14 : Funding of Capitalisation (Rs. Crore)

Approved Actual

Total Capitalization 1.25 3.08

Consumer Contribution - 0.17

Grants - -

Balance Capitalisation for the Year 1.25 2.90

Debt 0.87 2.03

Equity 0.37 0.87

Particulars FY 2013-14

3.9.2. It is submitted that the entire funding of the assets (other than those funded

through consumer contribution and grants) capitalised during FY 2013-14 is

through equity. However, in view of the provisions of the Tariff Regulation, 2012,

the quantum of equity has been restricted at 30% of the total funding requirement

and the remaining quantum is treated as normative debt. This is in line with the

provisions of the Tariff Regulations, 2012 and also in line with the approach

adopted by the Hon’ble Commission in the past.

3.9.3. The details pertaining to the interest charges on the normative debt funding and

the Return on the Equity has been discussed in subsequent paragraphs of the

Petition.

3.10. Aggregate Revenue Requirements for FY 2013-14

3.10.1. The ARR of MPAKVN for the FY 2013-14 has been determined in accordance with

the provisions of the Tariff Regulations, 2012 and also considers the cost elements

(both equity and normative debt components) emanating from the Capital Cost of

the Capitalised Expenditure considered in FY 2013-14.

True Up for FY 2013-14

Madhya Pradesh Audyogik Kendra Vikas Nigam (Indore) Ltd. 19

3.10.2. The net ARR of MPAKVN has been computed after netting off non-Tariff income for

the gross ARR mentioned previously.

3.10.3. The subsequent paragraphs outline the details of all the elements of the ARR of

MPAKVN.

3.11. Operation & Maintenance Expenses

3.11.1. The Hon’ble Commission in the Tariff Order for FY 2013-14 had approved the

consolidated O&M expenses of Rs. 4.28 Crore.

3.11.2. Operations and Maintenance (O&M) Expenses of MPAKVN consists of the following

elements:

Employee Expenses

Repairs and Maintenance Costs

Administrative and General Expenses

MPERC Expenses

Employee Cost

3.11.3. Employees of various department of MPAKVN like planning, commercial, technical,

legal, financial & accounts, administrative etc. are involved in activity of power

business. Actual employee expense for FY 2013-14 is Rs. 3.60 Crore which also

includes DA and terminal benefits. The summary of the actual employee expenses

for FY 2013-14 is given in the table below:

Table 15 : Employee Cost for FY 2013-14 (Rs. Crore)

Particulars FY 2013-14

(Actual)

Employee Cost excluding DA,

arrears, terminal benefits and

incentives

1.76

Arrears -

DA 0.90

Terminal Benefits 0.94

Incentive -

Total Employee Cost 3.60

Repair & Maintenance Cost

3.11.4. In the Tariff Order for FY 2013-14, the Hon’ble Commission had noted that the

petitioner had filed O&M expenses as per the Regulations and has also filed the

expenses as per the agreement signed with MPPKVVCL, Indore dated 26 March,

2013 and sought approval of these expenses over and above the regular O&M

expenses. Under this agreement, the MPPKVVCL has to undertake all activities

related to Repairs & Maintenance and also to provide consultancy services in

True Up for FY 2013-14

Madhya Pradesh Audyogik Kendra Vikas Nigam (Indore) Ltd. 20

various techno-commercial matters relating to the distribution and supply of

electricity in the SEZ area. The Hon’ble Commission in view of the difficulties faced

by the petitioner in the past related to its power business, had considered the

contract between the petitioner and MPPKVVCL, Indore in the interest of the

consumers and also due to the fact that MPPKVVCL is a State owned Distribution

Licensee and has expertise in operation and maintenance of power distribution

system.

3.11.5. The actual R&M expenses based on the audited accounts for FY 2013-14 is Rs. 4.32

Crore which also includes the additional O&M expenses approved vide agreement

between MPAKVN and MPPKVVCL dated 26 March, 2013 as well as the other

routine maintenance expenses not covered under the scope of the agreement.

3.11.6. Further, it is submitted that MPAKVN is an SEZ whose area of operation is limited

and cost of activities carried out for providing power supply gets apportioned over

a smaller area, consumer base and asset base as compared to other State Discoms

which have a wide area of operation and thus have the benefit of economies of

scale which is not available to MPAKVN. Hence, it would not be appropriate to link

the R&M expenses with the Gross Fixed Asset of the SEZ area.

3.11.7. It is also submitted that MPAKVN has been consistently providing power with

higher reliability throughout the year to the industrial units of the SEZ which

requires a robust R&M mechanism and which entails substantial cost. Accordingly,

it is submitted that the R&M expenses actually incurred and paid by MPAKVN be

approved as a part of True up of ARR. State Electricity Regulatory Commissions in

other States have also approved additional charges such as Reliability Charges for

uninterrupted / reliable supply of power. The Maharashtra Electricity Regulatory

Commission has approved Reliability Charges to be levied by the State Discom

MSEDCL from the consumers of Pune vide its Order in Case No. 5 of 2008. The

relevant extracts are reproduced below:

“3. MSEDCL, in its Petition, prayed as under:

“The Commission may accord

1. Approval of appointment of the Tata Power Co. Ltd. as Additional Supply Agency;

2. Approval and regularisation of power purchase from them for a period from 4th

April 2008 upto 30th June 2008 and;

3. Approval of Reliability Charge to be recovered from consumers of Pune Circles

of Ganeshkhind and Rasta Peth, for mitigating load shedding in Pune Circles.”

True Up for FY 2013-14

Madhya Pradesh Audyogik Kendra Vikas Nigam (Indore) Ltd. 21

35. Having heard the parties and after considering the material placed on record,

the Commission is of the view as under:

…..

c) Since most of the consumers who attended the hearing, supported MSEDCL’s

proposal to procure additional power from TPC to mitigate load shedding in Pune

Urban Circles, the Commission accords its acceptance to MSEDCL’s proposal for

additional power purchase to mitigate load shedding in Pune Urban Circles, and

has determined the Reliability Charges in this Order.”

3.11.8. It is further submitted that the MPAKVN has entered into the O&M agreement with

MPPKVVCL which is a Government owned entity and the Hon’ble Commission also

has considered such agreement and associated cost to be prudent in its Tariff

Order for FY 2013-14 dated 10 September, 2013 vide Petition No. 38/2013. The

relevant extract of the Order is reproduced below:

“2.47 The Commission noticed that the petitioner has filed O&M expenses as per

the Regulations and has also filed the expenses as per the agreement signed with

MPPKVVCL, Indore dated March 26, 2013. The petitioner has requested that the

expenses in accordance with the agreement executed by them with MPPKVVCL be

allowed. MPPKVVCL has to undertake all activities related to O&M expenses and

also to provide consultancy services in various techno-commercial matters relating

to the distribution and supply of electricity in the SEZ area. The Commission is of

the view that looking at the difficulties faced by the petitioner in the past related

to its power business, it would be prudent to consider the contract between the

petitioner and MPPKVVCL, Indore in the interest of the consumers. MPPKVVCL is a

State owned Distribution Licensee and has expertise in operation and

maintenance of power distribution system.”

3.11.9. It is important to note that although the term used in the agreement is O&M

however, the scope of work under the agreement is related to R&M activities only

and hence expenses incurred under the agreement should be considered as a part

of R&M expenses only and not the O&M expenses.

3.11.10. It is also submitted that all components of the O&M expenses viz. Employee

expenses, A&G expenses and R&M expenses have been actually incurred by

MPAKVN in the course of supply of power to the consumers of SEZ and the Hon’ble

Commission may undertake an independent third party audit of such O&M

expenses of MPAKVN, if deemed fit, for approval as a part of True up of ARR.

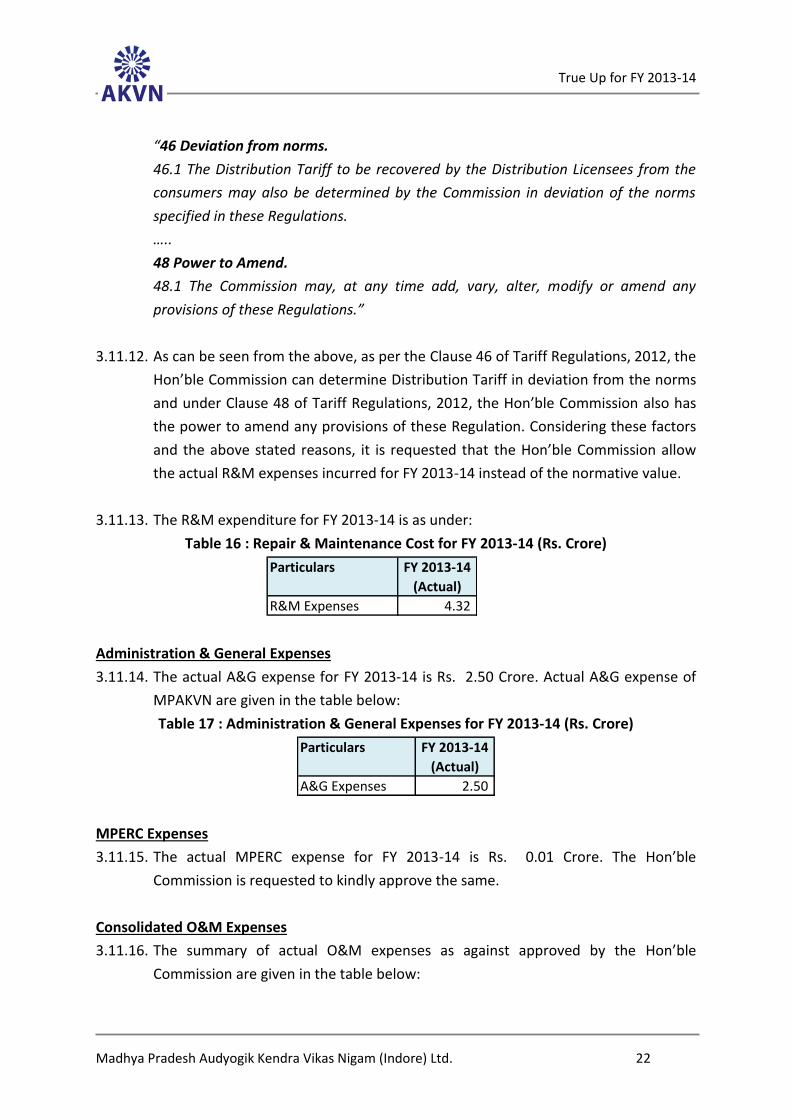

3.11.11. The Regulation 46 and 48 of the Tariff Regulations, 2012 reads as under:

True Up for FY 2013-14

Madhya Pradesh Audyogik Kendra Vikas Nigam (Indore) Ltd. 22

“46 Deviation from norms.

46.1 The Distribution Tariff to be recovered by the Distribution Licensees from the

consumers may also be determined by the Commission in deviation of the norms

specified in these Regulations.

…..

48 Power to Amend.

48.1 The Commission may, at any time add, vary, alter, modify or amend any

provisions of these Regulations.”

3.11.12. As can be seen from the above, as per the Clause 46 of Tariff Regulations, 2012, the

Hon’ble Commission can determine Distribution Tariff in deviation from the norms

and under Clause 48 of Tariff Regulations, 2012, the Hon’ble Commission also has

the power to amend any provisions of these Regulation. Considering these factors

and the above stated reasons, it is requested that the Hon’ble Commission allow

the actual R&M expenses incurred for FY 2013-14 instead of the normative value.

3.11.13. The R&M expenditure for FY 2013-14 is as under:

Table 16 : Repair & Maintenance Cost for FY 2013-14 (Rs. Crore)

Particulars FY 2013-14

(Actual)

R&M Expenses 4.32

Administration & General Expenses

3.11.14. The actual A&G expense for FY 2013-14 is Rs. 2.50 Crore. Actual A&G expense of

MPAKVN are given in the table below:

Table 17 : Administration & General Expenses for FY 2013-14 (Rs. Crore)

Particulars FY 2013-14

(Actual)

A&G Expenses 2.50

MPERC Expenses

3.11.15. The actual MPERC expense for FY 2013-14 is Rs. 0.01 Crore. The Hon’ble

Commission is requested to kindly approve the same.

Consolidated O&M Expenses

3.11.16. The summary of actual O&M expenses as against approved by the Hon’ble

Commission are given in the table below:

True Up for FY 2013-14

Madhya Pradesh Audyogik Kendra Vikas Nigam (Indore) Ltd. 23

Table 18 : O&M Expenses for FY 2013-14 (Rs. Crore)

Approved Actual

Employee Expenses 3.60

Repair & Maintenance Expenses 4.32

Administrative & General Expenses 2.50

MPERC Fees 0.01 0.01

Operation & Maintenance Expenses 4.29 10.43

Particulars FY 2013-14

4.28

3.11.17. The Hon’ble Commission is requested to approve actual O&M expenses incurred by

MPAKVN for FY 2013-14.

3.12. Depreciation

3.12.1. The rate of depreciation as specified in the Tariff Regulations, 2012 have been

considered for the computation of depreciation. The actual and approved

depreciation for FY 2013-14 is as shown below:

Table 19 : Depreciation for FY 2013-14 (Rs. Crore)

Approved Actual

Opening Gross Fixed Asset 11.94 12.74

Addition during the year 1.25 3.08

Deduction during the year 0.00 0.00

Closing Gross Fixed Asset 13.19 15.81

Depreciation 0.63 0.70

Depreciation Rate 5.00% 4.87%

Particulars FY 2013-14

3.12.2. MPAKVN has reduced the amortization of the assets capitalized from the consumer

contribution & grant. Accordingly, net depreciation on GFA for FY 2013-14 after

reducing amortization on consumer contribution is shown in the table below:

Table 20 : Net Depreciation for FY 2013-14 (Rs. Crore)

Approved Actual

Depreciation 0.63 0.70

Less: Consumer contribution

amortized

0.24 0.07

Net Depreciation 0.39 0.62

Particulars FY 2013-14

3.12.3. The Hon’ble Commission is requested to approve depreciation expenses incurred

by MPAKVN for FY 2013-14.

True Up for FY 2013-14

Madhya Pradesh Audyogik Kendra Vikas Nigam (Indore) Ltd. 24

3.13. Interest & Financial Charges

3.13.1. For assessing interest charges on loans in FY 2013-14, the opening balance of Loans

has been considered as the normative closing loan balance for FY 2012-13. The loan

addition in FY 2013-14 is considered at Rs. 2.03 Crore based on the actual

capitalisation during the year as discussed in paragraph 3.9 above.

3.13.2. In line with the approach adopted by the Hon’ble Commission in its Tariff Order

dated 10th September, 2013 and as prescribed by Tariff Regulations, 2012

repayment during the year has been considered equal to depreciation charged for

the financial year.

3.13.3. MPAKVN does not have actual loans and hence in line with Hon’ble Commission’s

methodology, since the True up of State Discoms for FY 2013-14 has not been

carried out, the last available weighted average rate of interest of the West Discom

of 9.48% as approved by the Hon’ble Commission in its True up Order for FY 2012-

13 for the State Discoms dated 17th March, 2016 is considered.

3.13.4. The Interest & Financial charges for FY 2013-14 computed by MPAKVN against

approved by the Hon’ble Commission is as shown below:

Table 21 : Interest & Financial Charges for FY 2013-14 (Rs. Crore)

Approved Actual

Debt Associated with GFA as on the beginning of the

year (Net of consumer contribution)

4.01 6.39

Addition to net debt 0.59 2.03

Repayment during the year 0.39 0.62

Total debt associated with GFA at the end of the

year

4.21 7.80

Weighted average interest rate of State Discoms 9.48% 9.48%

Interest on project loans(normative) 0.39 0.67

Particulars FY 2013-14

3.13.5. The interest paid on consumer security deposit in line with the provisions of the

Tariff Regulations, 2012 is given in table below:

Table 22 : Interest on Consumer Security Deposit for FY 2013-14 (Rs. Crore)

Approved Actual

Consumer Security Deposit 11.09 10.95

Interest amount claimed 0.94 1.23

Particulars FY 2013-14

3.13.6. Based on the above, the Hon’ble Commission is requested to approve total interest

& finance charges of Rs. 1.90 Crore for FY 2013-14.

True Up for FY 2013-14

Madhya Pradesh Audyogik Kendra Vikas Nigam (Indore) Ltd. 25

3.14. Interest on Working Capital

3.14.1. The interest on working capital has been calculated on the basis of normative

parameters as provided in the Tariff Regulations, 2012.

3.14.2. The rate of interest considered is the SBI Base Rate as on 1 April 2013 plus 3.5% as

provided in Tariff Regulations, 2012. The interest on working capital for FY 2013-14

incurred by MPAKVN as against that approved by the Hon’ble Commission is as

shown below:

Table 23 : Interest on Working Capital for FY 2013-14 (Rs. Crore)

Approved Actual

For Wheeling Activity

1/6th of annual requirement of inventory for

previous year

0.02 0.02

1/12th of O&M Expenses 0.37 0.87

2 months of Receivables from Wheeling

charges

- -

Total Working Capital 0.39 0.89

Rate of Interest 13.20% 13.20%

Interest on Working Capital 0.05 0.12

For Retail Supply Activity

1/6th Annual requirement of Inventory for

previous year

- 0.00

2 months of Receivables of average biling 16.89 14.65

1/12th of O&M Expenses - 0.87

Minus: 1/12th of Power Purchase expenses7.43 6.29

Minus: Consumer Security Deposit 11.09 11.19

Total Working Capital (1.63) (1.95)

Rate of Interest 13.20% 13.20%

Interest on Working Capital (0.21) (0.26)

Total Interest on Working Capital - -

Particulars FY 2013-14

3.15. Lease Rent

3.15.1. MPAKVN is the SEZ developer who is responsible for providing various services to

the business units who setup their factories in the SEZ premises. As a deemed

licensee, MPAKVN also supplies power to the occupants of the SEZ. For this

purpose, MPAKVN (SEZ Developer) has provided land to power business of

MPAKVN for setting up its infrastructure necessary for providing power to the

industrial units. Against this land which has been allocated to the power business,

MPAKVN is charging lease rent for the area allocated to the power business which

True Up for FY 2013-14

Madhya Pradesh Audyogik Kendra Vikas Nigam (Indore) Ltd. 26

is a separate business unit within the company and is a distribution licensee

recognised by the Hon’ble Commission. The lease rent applicable for the land

allocated for establishing various assets is shown below in the table:

Table 24 : Lease Rent for FY 2013-14 (Rs. Crore)

Lease Rent 4.64

FY 2013-14Particulars

3.15.2. It is humbly submitted that lease rent is legitimate expense and should be

permitted to be recovered as an expense through the ARR. The lease rent is being

charged by MPAKVN as it is an opportunity cost lost for MPAKVN SEZ business as

they could have leased out this land to some other industry and received lease rent

against it.

3.15.3. Further, as a distribution licensee, in normal course of action MPAKVN would have

purchased this land for establishment of its power distribution infrastructure. The

cost incurred for purchase of land gets capitalized and the Hon’ble Commission

allows depreciation, interest on loan and return on equity chargeable on account of

this cost as part of ARR. Accordingly, this expenditure, in the form of either lease

rent or depreciation, interest on loan and return on equity chargeable on the

capital cost incurred by MPAKVN, is inevitable.

3.15.4. MPAKVN has sought lease rent in its review petition 86 of 2012 and the Hon’ble

Commission in its Order dated 21st December, 2012 has disallowed lease rent

sighting reason of non-payment. The relevant part of the same is reproduced here

below for reference.

“ii. Land Premium and Lease rent charges:

…….

The Commission considered the matter and observed that in the instant case

since no actual payments are being made to the SEZ on account of land

premium or lease rent such notional expense cannot be charged to the

consumers. The claim made by the petitioner in this regard is not

sustainable.”

3.15.5. The Tariff Regulations, 2012 also provide for lease rent charges as an expenditure

to be approved as a part of ARR of a distribution licensee. The relevant Regulation

is reproduced below:

“33.1 Lease charges for assets taken on lease by Distribution Licensee shall be

considered as per lease agreement provided the charges are considered reasonable

by the Commission.”

True Up for FY 2013-14

Madhya Pradesh Audyogik Kendra Vikas Nigam (Indore) Ltd. 27

3.15.6. The Hon’ble Commission in its Tariff Order for FY 2017-18 dated 7 April, 2017 vide

Petition No. 72/2016 had observed the following regarding lease rent:

“2.67 After examining the submissions regarding lease rent by the Petitioners, the

Commission finds the claim un-reasonable as the Petitioner being a deemed

licensee under the Provisions of the Electricity Act, 2003, is obligated to supply

power to the consumers under its own license area therefore the Commission has

not admitted the lease rent of Rs. 2.19 Crore claimed by the Petitioner.”

3.15.7. As can be seen from the above, the Hon’ble Commission has observed that

MPAKVN being a deemed distribution licensee, it is obligated to supply power in its

license area. However, it is submitted that the Government of Madhya Pradesh

vide letter dated 31 March, 2017 has clarified that any revenue received by

MPAKVN towards any land premium, lease rental etc. is the revenue of the

Government of Madhya Pradesh. Accordingly, it is submitted that lease rent is not

a part of revenue of either power business or non-power business of the SEZ i.e.

MPAKVN and hence, the lease rent expense should be considered as a legitimate

expense and approved as a part of True up of ARR. The aforementioned letter is

attached as Annexure-2.

3.15.8. There have been instances in other states wherein the Commission has allowed this

expenditure pertaining to lease rental as a pass through in the tariff over and above

the other expenses.

3.15.9. A precedence in this matter can be seen in case of approval of the Truing-up of FY

2013-14 and FY 2014-15, Provisional Truing-up of FY 2015-16, and Projection of

ARR for the 3rd Control Period FY 2016-17 to FY 2019-20 for the transmission

licensee MEGPTCL in Maharashtra by the Hon’ble MERC in Case no. 50 of 2016. In

the said case, the land for Akola-II Sub-station was initially to be purchased and

handed over by MSETCL to MEGPTCL, however, later on based on management

decision, the land was leased out to MEGPTCL. Accordingly, while the total capital

cost of land in the overall capital cost was reduced, the corresponding increase in

the lease rental for the same was factored as additional Operation and

Maintenance (O&M) expenses in the ARR for the Control Period. Considering the

facts of the case, the Hon’ble Commission had approved the least rent for Akola II

Sub-station over and above the normative O&M expenses of MEGPTCL prescribed

in the MYT Regulations.

3.15.10. In view of the above, the Hon’ble Commission is humbly requested to allow lease

rent charged to MPAKVN to the power business as a legitimate expenditure as part

of the ARR.

True Up for FY 2013-14

Madhya Pradesh Audyogik Kendra Vikas Nigam (Indore) Ltd. 28

3.16. Return on equity

3.16.1. As per the Tariff Regulations, 2012, a return @ 16% on the equity base is

considered as reasonable and allowed by the Hon’ble Commission. Accordingly,

MPAKVN has computed the Return on Equity considering a rate of return at 16%.

3.16.2. The Opening Equity for FY 2013-14 is considered as the closing normative equity for

FY 2012-13. Accordingly, the return on equity for FY 2013-14 is as shown below:

Table 25 : Return on Equity for FY 2013-14 (Rs. Crore)

Approved Actual

Equity associated with GFA as on the

beginning of the year

2.35 3.44

30% of addition to net GFA considered as

funded through equity

0.25 0.87

Total equity associated with GFA at the end

of the year

2.61 4.31

Average equity associated with GFA at the

end of the year

2.48 3.88

Return on equity @ 16% 0.42 0.62

Particulars FY 2013-14

3.17. Other Income

3.17.1. The actual other Income of MPAKVN for FY 2013-14 is Rs. 0.4309 Crore. Element

wise detail of the same is as given in table below:

Table 26 : Other Income for FY 2013-14 (Rs. Crore)

Particulars FY 2013-14

(Actual)

Miscellaneous Income 0.0292

Interest Received on Deposit with MPSEB 0.4014

Shutdown Charges 0.0004

Surcharge Received on Power Bill -

Power Application Processing Fees -

Total Other Income 0.4309

3.18. Income Tax

3.18.1. The Appellate Tribunal for Electricity in its Judgment in Appeal No. 71 of 2013

dated 30 October, 2014 had ruled the following regarding the income tax for FY

2010-11 to FY 2012-13:

“38. We find that the Appellant had claimed income tax for FY 2010-11 as per the

balance sheet but for FY 2011-12 and 2012-13 no supporting details were furnished.

The State Commission felt that the amount claimed by the Appellant was very high

True Up for FY 2013-14

Madhya Pradesh Audyogik Kendra Vikas Nigam (Indore) Ltd. 29

when compared to the profit earned from the power business. In the absence of the

requisite information, the State Commission has admitted the income tax based on

admitted cost of return on equity at applicable income tax rates. The State

Commission has, however, submitted that the claim of the Appellant for income

tax shall be duly considered at the time of true-up based on the duly audited

financial statements of its power business.”

3.18.2. Accordingly, for FY 2013-14 also, it is submitted that MPAKVN has now prepared

separate accounts for power business which are audited. The Income tax in the

audited annual accounts has been actually paid and the same is apportioned in the

ratio income earned by the power and non-power business. Accordingly, an Income

Tax of Rs. Crore has been claimed in the present Petition as shown in the following

table:

Table 27 : Income Tax for FY 2013-14 (Rs. Crore)

Approved Actual

Income Tax 0.14 -

Particulars FY 2013-14

3.19. Aggregate Revenue Requirement for FY 2013-14

3.19.1. Based on above, the Aggregate Revenue Requirement of MPAKVN for FY 2013-14

as against the values approved by the Hon’ble Commission is summarised in the

table below.

True Up for FY 2013-14

Madhya Pradesh Audyogik Kendra Vikas Nigam (Indore) Ltd. 30

Table 28 : Aggregate Revenue Requirement for FY 2013-14 (Rs. Crore)

Approved Actual

1 Purchase of Power 89.20 66.32

2 Inter-State Transmission Charges 2.78 4.71

3 Intra-State Transmission (MP Transco) Charges 2.80 4.41

4 SLDC Charges 0.01 0.04

5 Employee Expenses 3.60

6 R&M Expenses 4.32

7 A&G Expenses 2.50

8 MPERC and MPPMCL Fees & Other 0.01 0.01

9 Depreciation 0.39 0.62

10 Interest & Finance Charges 1.33 1.90

11 Interest on Working Capital - -

12 Lease Rent - 4.64

13 Income Tax 0.14 -

14 Sub Total (1 to 13) 100.94 93.09

14 Return on Equity 0.42 0.62

15 Total Expenditure (13 + 14) 101.36 93.71

16 Less: Other Income 0.02 0.43

17 Aggregate Revenue Requirement (15 - 17) 101.34 93.28

Sr. No. Particulars FY 2013-14

4.28

3.20. Revenue for FY 2013-14

3.20.1. During the FY 2013-14, MPAKVN’s actual revenue from sale of power was Rs. 87.48

Crore.

3.21. Revenue Gap / (Surplus) for FY 2013-14

3.21.1. The Aggregate Revenue Requirement for FY 2013-14 works out to Rs. 93.28 Crore

and the revenue from sale of power recovered during the same period is Rs. 87.48

Crore. Accordingly, the revenue gap for FY 2013-14 works out to Rs 5.80 Crore as

given in the Table below:

Table 29 : Revenue Gap/ (Surplus) for FY 2013-14 (Rs. Crore)

Sr. No. Particulars FY 2013-14

(Actual)

1 Aggregate Revenue Requirement 93.28

2 Revenue from Sale of Power 87.48

3 Revenu Gap/(Surplus) (1-2) 5.80 3.21.2. The Hon’ble Commission is requested to approve above mentioned revenue gap

and allow recovery of the same while determination of the retail tariff for FY 2018-

19.

True Up for FY 2013-14

Madhya Pradesh Audyogik Kendra Vikas Nigam (Indore) Ltd. 31

4. Prayer

MPAKVN Indore Ltd. respectfully prays to the Hon’ble Commission as under:

1. To admit this petition seeking True up for FY 2013-14.

2. To approve Aggregate Revenue Requirement (ARR) and Revenue Gap for FY 2013-14

as per the provisions of the Tariff Regulations, 2012.

3. To allow recovery of the Revenue Gap of FY 2013-14 while determining the retail

tariff for FY 2018-19.

4. To allow recovery of lease rent charges for the use of land for the substation and line

and premium for the substation land.

5. To grant any other relief as the Hon’ble Commission may consider appropriate.

6. To condone any inadvertent omissions, errors, short comings and permit the

Petitioner to add/change/modify/alter this filing and make further submissions as

may be required at a future date; and

7. To pass any other Order as the Hon’ble Commission may deem fit and appropriate

under the circumstances of the case and in the interest of justice.

Place: Indore

Date: _________, 2017 Signature of the Petitioner

True Up for FY 2013-14

Madhya Pradesh Audyogik Kendra Vikas Nigam (Indore) Ltd. 32

Annexure 1: Letter of CAG

True Up for FY 2013-14

Madhya Pradesh Audyogik Kendra Vikas Nigam (Indore) Ltd. 33

Annexure 2: Letter of GoMP regarding lease rent

True Up for FY 2013-14

Madhya Pradesh Audyogik Kendra Vikas Nigam (Indore) Ltd. 34

True Up for FY 2013-14

Madhya Pradesh Audyogik Kendra Vikas Nigam (Indore) Ltd. 35

Annexure 3: Tariff Filing Formats