Embed Size (px)

Citation preview

Before the

MAHARASHTRA ELECTRICITY REGULATORY COMMISSION

World Trade Centre, Centre No.1, 13th

Floor, Cuffe Parade, Mumbai – 400 005

Tel. 22163964/ 65/ 69 Fax 22163976

Email: [email protected]

Website: www.mercindia.org.in/www.merc.gov.in

CASE NO. 158 of 2017

In the matter of

Petition of Nagpur Solid Waste Processing and Management Pvt. Ltd. for determination of

Tariff for sale of electricity from 11.5 MW Municipal Solid Waste based power project to

be commissioned at Nagpur to Distribution Licensees in Maharashtra

Coram

Shri. Anand B. Kulkarni, Chairperson

Shri Deepak Lad, Member

ORDER

Date: 5 February, 2018

M/s Nagpur Solid Waste Processing and Management Pvt. Ltd. (NSWPMPL), 513A,5th

Floor,

Kohinoor City, Kirol Road, Kurla (West), Mumbai has filed a Petition on 7 November, 2017

under Section 62(1)(a) of the Electricity Act (EA), 2003 and Regulations 8.1 and 8.2 of the

Commission‟s (Terms and Conditions for Determination of Renewable Energy Tariff)

Regulations, 2015 („RE Tariff Regulations,2015‟), for determination of Tariff for supply of

electricity from its 11.5 MW capacity Municipal Solid Waste(MSW) based Power Plant at

Bhandewadi, Nagpur to Distribution Licensees in the Maharashtra.

The Commission, in exercise of its powers under Sections 61, 62, and 86 read with Section 181

of the EA, 2003, and all other powers enabling it in this behalf, and after taking into

consideration the submissions made by NSWPMPL, suggestions and objections from the public

and stake-holders and other relevant material, has determined the tariff for the Project of

NSWPMPL at Nagpur as set out in this Order.

MERC Order for determination of Tariff for 11.5 MW MSW project of NSWPMPL

Order- Case No 158 of 2017 Page 2 of 92

Table of Contents

1. BACKGROUD AND BRIEF HISTORY .................................................................................................... 7

1.1. Background ............................................................................................................................ 7

1.2. Admission of the Petition and Public Consultation Process .................................................. 8

1.3. Organization of Order ............................................................................................................ 9

2. CONCESSION AGREEMENT BETWEEN NMC AND CONCESSIONAIRE ................................... 10

2.1. Tendering Process ................................................................................................................ 10

2.2. Salient features of Concession Agreement ........................................................................... 10

2.3. Salient features of the Nagpur MSW Project, as per NSWPMPL ....................................... 13

2.4. Scope of work of MSW Project ........................................................................................... 13

2.5. Existing and New Scientific Landfills.................................................................................. 14

2.6. Role of NMC ........................................................................................................................ 14

2.7. Term and Termination of Agreement:.................................................................................. 15

2.8. Ownership of assets and transfer of Project ......................................................................... 16

2.9. Viability Gap Funding .......................................................................................................... 16

2.10. Bid evaluation report and observations of NEERI and GIPE: ............................................. 16

2.11. Solid Waste Management Rules (SWM) 2016 and its Implications: ................................... 18

2.12. Provisions of Tariff Policy 2016: ......................................................................................... 21

3. PREMISES FOR DETERMINATION OF PROJECT-SPECIFIC TARIFF ....................................... 23

3.1. Regulatory Framework for Tariff Determination ................................................................. 23

3.2. Premise for Development of Tariff Structure: ..................................................................... 24

4. SUGGESTIONS/OBJECTIONS, NSWPMPL’S RESPONSE AND COMMISSION’S RULINGS .... 27

4.1. Maharashtra Energy Development Agency‟s (MEDA) Submission: .................................. 27

4.2. Nagpur Municipal Corporation‟s (NMC) Submission: ........................................................ 29

4.3. Maharashtra State Electricity Distribution Company Limited (MSEDCL)‟s Submission ... 31

5. PARAMETERS OF TARIFF DETEREMINATION .............................................................................. 34

5.1. Background .......................................................................................................................... 34

5.2. Technology of proposed MSW Project ................................................................................ 34

MERC Order for determination of Tariff for 11.5 MW MSW project of NSWPMPL

Order- Case No 158 of 2017 Page 3 of 92

5.3. Calorific Value (CV) of MSW in Nagpur: ........................................................................... 38

5.4. Installed Plant Capacity ........................................................................................................ 41

5.5. Capacity Utilisation Factor ................................................................................................... 42

5.6. Auxiliary Energy Consumption Factor ................................................................................ 44

5.7. Capital Cost .......................................................................................................................... 48

5.8. Viability Gap Funding (VGF) .............................................................................................. 57

5.9. Useful Life of MSW Plant ................................................................................................... 58

5.10. Debt-Equity Ratio ................................................................................................................ 62

5.11. Depreciation ......................................................................................................................... 63

5.12. Operation and Maintenance(O&M) Expenses ..................................................................... 65

5.13. Escalation factor for Annual O&M expenses: ..................................................................... 73

5.14. Periodic Maintenance expenditure: ...................................................................................... 74

5.15. Interest on Term Loan .......................................................................................................... 76

5.16. Interest on Working Capital ................................................................................................. 78

5.17. Return on Equity .................................................................................................................. 79

5.18. Tipping Fee and Other Income ............................................................................................. 80

5.19. Discount Rate ....................................................................................................................... 82

5.20. Status of Statutory Clearances: ............................................................................................ 83

5.21. The summary of various parameters and assumptions ......................................................... 83

5.22. Tariff Rate and Other Conditions ......................................................................................... 86

5.23. Other Commercial aspects: .................................................................................................. 86

6. SUMMARY OF COMMISSION’S DIRECTIVES AND APPLICABILITY OF ORDER .................. 89

Appendix – 1 ..................................................................................................................................................... 90

List of persons at the Technical Validation Session held on 22 November, 2017 ........................................ 90

Appendix – 2 ..................................................................................................................................................... 91

List of persons at the Public Hearing held on 29 December 2017 ................................................................ 91

Annexure-1: Summary of Levellised Tariff ................................................................................................... 92

MERC Order for determination of Tariff for 11.5 MW MSW project of NSWPMPL

Order- Case No 158 of 2017 Page 4 of 92

List of Tables

Table 1: Waste Generation in Nagpur ......................................................................................................................... 11

Table 2: Financial working by GIPE ........................................................................................................................... 18

Table 3: Emission standard for incinerators technologies as per SWM Rules, 2016 .................................................. 21

Table 4: Chemical characteristics of MSW ................................................................................................................. 38

Table 5: Physical characteristics of MSW ................................................................................................................... 39

Table 6: Summary matrix- All sources ........................................................................................................................ 40

Table 7: Summary matrix- Chemical and physical characterization ........................................................................... 40

Table 8: Comparative Capacity Utilization factor of MSW Projects........................................................................... 44

Table 9: Auxiliary Equipment Details submitted by NSWPMPL ............................................................................... 45

Table 10: Comparison of Auxiliary Consumption of various similar projects ............................................................ 46

Table 11: Auxiliary Consumption as considered by Commission ............................................................................... 47

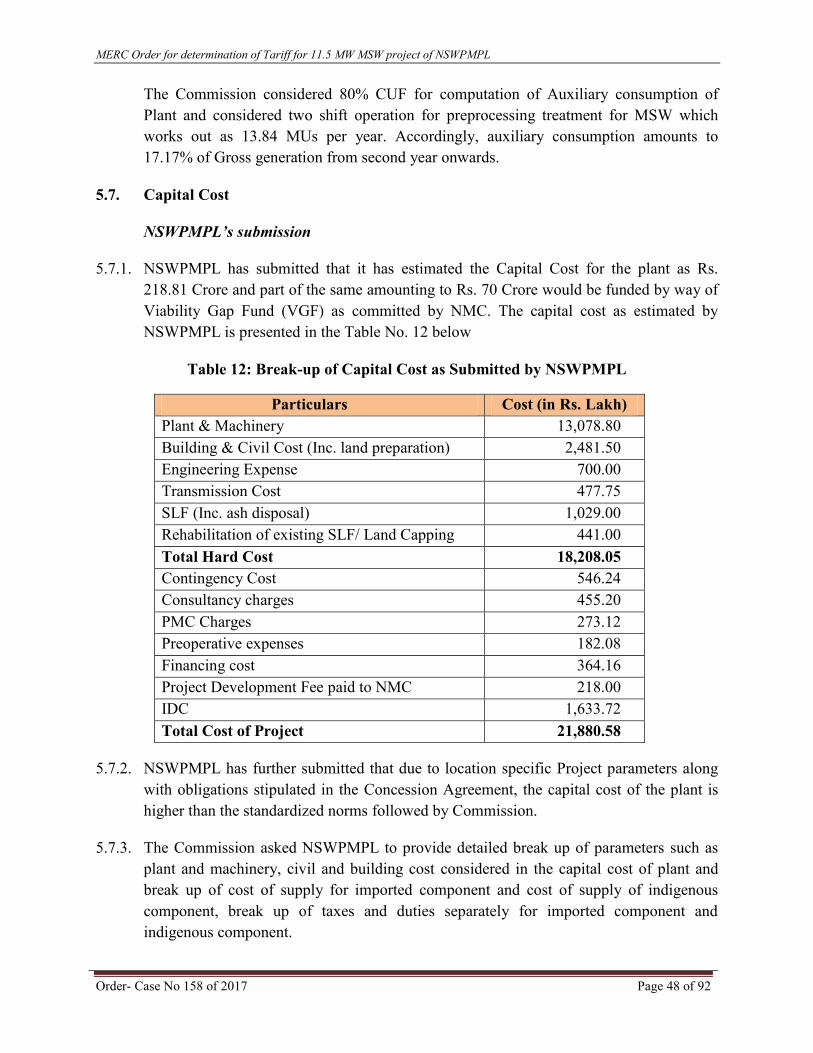

Table 12: Break-up of Capital Cost as Submitted by NSWPMPL .............................................................................. 48

Table 13: Quotation for Plant & Machinery Cost (as per Hitachi-Zosen India Pvt. Ltd.) .................................. 49

Table 14: Details of Quotations received for Civil work of MSW Plant ............................................................... 50

Table 15: Comparative Capital Cost of MSW Projects ............................................................................................... 53

Table 16: Comparison of Soft Cost and Hard Cost of MSW Projects ......................................................................... 56

Table 17: Capital Cost of MSW Projects considered by the Commission ................................................................... 56

Table 18: Comparative Useful life of MSW Projects .................................................................................................. 60

Table 19: O&M Expenses for the plant as estimated of the by NSWPMPL ............................................................... 65

Table 20: O&M Expenses for pre-processing facility as estimated of the by NSWPMPL .................................. 66

Table 21: Summary of O&M expenses proposed by NSWPMPL (Year 1 to 7) ......................................................... 66

Table 22: Summary of O&M expenses proposed by NSWPMPL (Year 8 to 13) ....................................................... 67

Table 23: Detailed Break up of O&M expenses as submitted by NSWPMPL ............................................................ 67

Table 24: Category wise break-up of Employees as submitted by NSWPMPL ................................................... 68

Table 25: Detailed break up of A&G expense as submitted by NSWPMPL ........................................................ 69

Table 26: Detailed Break up of O&M expenses as submitted by NSWMPMPL ................................................. 71

Table 27: Annual inflation escalation for computation of Capex ................................................................................ 75

Table 28: Monthly 1 Year MCLR declared by SBI ..................................................................................................... 77

Table 29: Computation of Revenue from tipping fees ................................................................................................. 81

Table 30: Status of Statutory Clearances ..................................................................................................................... 83

Table 31: Summary of Project Specific Parameters .................................................................................................... 84

MERC Order for determination of Tariff for 11.5 MW MSW project of NSWPMPL

Order- Case No 158 of 2017 Page 5 of 92

Abbreviations

APTEL Appellate Tribunal for Electricity

BOOT Build Own Operate and transfer

CEA Central Electricity Authority

CER Certified Emission Reduction

CERC Central Electricity Regulatory Commission

CDM Clean Development Mechanism

CoD Commercial date of Operation

CPCB Central Pollution Control Board

CSS Cross subsidy Surcharge

DBFOT Design Build Finance Operate and Transfer

DPR Detail Project Report

EA 2003 Electricity Act 2003

EIA Environmental Impact Assessment

EIL Essel Infra Projects Limited

EPA Energy Purchase Agreement

EPC Engineering, Procurement and Construction

FD Forced Draft

GCV Gross Calorific Value

GIPE Gokhale Institute of Politics & Economics

GoM Government of Maharashtra

ID Induced Draft

IDC Interest During Construction

IRR Internal Rate of Return

HV High Voltage

kVA Kilo Volt Ampere

kW Kilo Watt

kWh Kilo Watt Hour

MERC Order for determination of Tariff for 11.5 MW MSW project of NSWPMPL

Order- Case No 158 of 2017 Page 6 of 92

LDO Light Diesel Oil

MEDA Maharashtra Energy Development Agency

MERC Maharashtra Electricity Regulatory Commission

MoD Merit Order Despatch

MNRE Ministry of New and Renewable Energy

MoEF Ministry of Environment & Forest and climate change

MSEDCL Maharashtra State Electricity Distribution Company Limited

MSETCL Maharashtra State Electricity Transmission Company Limited

MSW Municipal Solid Waste

MU Million Unit

MW Mega Watt

NCV Net Calorific Value

NEERI National Environmental Engineering Research Institute

NMC Nagpur Municipal Corporation

NSWPMPL Nagpur Solid Waste Processing and Management Pvt. Ltd.

O&M Operation and Maintenance

OEM Original Equipment Manufacturer

PLF Plant Load Factor

PPP Public Private Partnership

RDF Refuse-Derived Fuel

RE Renewable Energy

RPO Renewable Purchase Obligation

SERC State Electricity Regulatory Commission

SLF Sanitary land filling

SPV Special Purpose Vehicle

TPD Metric Tons per Day

WTE Waste to Energy

MERC Order for determination of Tariff for 11.5 MW MSW project of NSWPMPL

Order- Case No 158 of 2017 Page 7 of 92

1. BACKGROUD AND BRIEF HISTORY

1.1. Background

1.1.1. Nagpur is one of largest city in the state of Maharashtra having 4.73% of the total urban

population of the state. Nagpur is being developed as a Smart City under Smart City

Mission of Government of India. As per Nagpur Municipal Corporation (NMC), the city

is currently generating an average of 1100-1200 TPD of waste, with an average

generation of 444 grams per capita per day.

1.1.2. For effective treatment of MSW in the Nagpur City, NMC had invited Expression of

Interest (EoI) published dated 29 November, 2014. Further, Request for Proposal (RfP)

was invited on 19 January, 2015 for selection of bidder for construction, operation and

maintenance of Municipal Solid Waste Management (MSWM) facility on Design, Build,

Finance, Operate and Transfer (DBFOT) basis for treating the MSW. Consortium of M/s

Essel Infraprojects Ltd. and M/s Hitachi Zosen India Pvt. Ltd., was selected vide

competitive bidding process and Letter of Award (LoA) was issued to Consortium by

NMC dated 4 January, 2017

1.1.3. Consortium has promoted and incorporated M/s Nagpur Solid Waste Processing &

Management Pvt. Ltd. (NSWPMPL) as Special Purpose Vehicle (SPV) for execution of

the solid waste processing plant at Nagpur. A Concession Agreement was signed between

NSWPMPL and NMC on 4 May, 2017 for design, construction and operation of MSW

processing facility at Bhandewadi, Nagpur for capacity of 800 MT per day including Pre-

processing of MSW in line with the provisions of the Solid Waste Management (SWM)

Rules, 2016 during the Concession Agreement Period.

1.1.4. NSWPMPL has proposed Hitachi Zosen‟s incineration technology for managing waste

processing and generating electricity from the processed waste. The Installed capacity of

the proposed Waste to Energy power plant is 11.5 MW.

1.1.5. Accordingly, NSWPMPL has filed the Petition under Sections 62(1) (a) and 86(1) (e) of

the EA, 2003 and Regulations 8.1 and 8.2 of RE Tariff Regulations, 2015 for

determination of Tariff for sale of electricity generated from its 11.5 MW MSW-based

Power Plant.

1.1.6. The prayers of NSWPMPL are as follows:

1. Take the accompanying Tariff Petition for approval of power purchase from the

11.50 MW pre-processed MSW based WtE plant of NSWPMPL on record and treat it

as complete;

MERC Order for determination of Tariff for 11.5 MW MSW project of NSWPMPL

Order- Case No 158 of 2017 Page 8 of 92

2. Approve the levellised tariff of Rs. 7.80/kWh in accordance with the tariff structure

adopted by the Hon‟ble CERC;

3. Grant exemption from Merit Order Dispatch Principles for the Project.

4. Direct DISCOMs to consider the benefit of zero contract demand charges.

5. Direct the DISCOMs to consider energy which may be drawn during shut down or

start up after the CoD of the Project be set off against the energy injected into the

grid by the Project

6. Grant waiver on Cross Subsidy Surcharge on sale of power from the Project in case

of sale of power directly to third party.

7. Condone any inadvertent omissions/ errors/ shortcomings and permit the Petitioner

to add/ change/ modify/ alter portion(s) of this filing and make further submissions as

may be required at a later stage; and

8. Pass such an order as the Hon'ble Commission deems fit and proper as per the facts

and circumstances of the case.

1.1.7. This Order relates to NSWPMPL‟s Petition for determination of Tariff for supply of

electricity from its 11.5 MW capacity MSW-based Power Project at Bhandewadi, Nagpur

to Distribution Licensees in Maharashtra.

1.2. Admission of the Petition and Public Consultation Process

1.2.1. NSWPMPL has filed a Petition on 7 November, 2017 under Sections 62(1) (a) and 86(1)

(e) of the EA, 2003 and Regulations 8.1 and 8.2 of the RE Tariff Regulations, 2015 for

determination of Tariff for sale of electricity generated from its 11.5 MW MSW-based

Power Plant.

1.2.2. Preliminary data gaps were forwarded to NSWPMPL on 13, 22, 27 November,2017 and

11 December,2017, to which NSWPMPL submitted replies vide letter dated 21, 25

November, 2017 and 25 December,2017.

1.2.3. A Technical Validation Session (TVS) was held on 22 November, 2017. During TVS,

NSWPMPL made a presentation on the salient features of the Petition. The Commission

directed NSWPMPL to implead NMC as Party and serve the copy of the Petition to NMC

as well as to other Distribution Licensees in the state. TVS minutes were forwarded to

NSWPMPL on 29 November, 2017.List of person attended the TVS is at Appendix – 1

1.2.4. The Commission highlighted the data gaps in the Petition, and asked NSWPMPL to

comply with all data gaps within a week. Along with reply to data gaps, NSWPMPL

submitted a revised petition on 28 November, 2017. The Commission admitted the

MERC Order for determination of Tariff for 11.5 MW MSW project of NSWPMPL

Order- Case No 158 of 2017 Page 9 of 92

revised Petition on 30 November, 2017 in accordance with Section 64 of the EA, 2003,

and directed NSWPMPL to publish its Petition in an abridged form by 7 December,2017,

and to reply expeditiously to all suggestions and objections received from the public on

its Petition.

1.2.5. NSWPMPL published the Public Notice in the daily English Newspapers viz. Times of

India and Indian Express and Marathi Newspapers viz. Loksatta and Maharashtra Times

in all editions all over Maharashtra on 5 December, 2017 inviting public

suggestions/objections and intimating the date of Public Hearing. Copies of the Petition

and its Executive Summary were made available at NSWPMPL‟s offices and on its

website in downloadable format. The Public Notice and Executive Summary of the

Petition were also made available on the websites of the Commission

(www.mercindia.org.in, www.merc.gov.in) in downloadable format.

1.2.6. A Public Hearing was held on 29 December, 2017 at the Office of the Commission, 13th

Floor, Centre No. 1, World Trade Centre, Cuffe Parade, Colaba, Mumbai. The list of

persons at the Public Hearing is at Appendix-2.

1.2.7. The Commission has ensured that the due process was contemplated under the law to

ensure transparency and public participation was followed at every stage and adequate

opportunity was given to all concerned to file their say.

1.3. Organization of Order

1.3.1. This Order is organized in the following 7 Sections:

Section 1 provides a brief history and sets out the quasi-judicial regulatory process

undertaken by the Commission. A list of abbreviations with their expanded forms is

included.

Section 2 describes the salient features of the Concession Agreement between NMC and

the Concessionaire.

Section 3 details the Tariff philosophy underlying the tariff determination.

Section 4 covers objection summary and rulings thereof.

Section 5 comprises the submissions with respect to performance parameters and

financial parameters, the Commission's analysis, and the methodology adopted to

determine the tariff and other parameters.

Section 6 summarizes the directives and rulings of the Commission.

Section 7 addresses the applicability of this Tariff Order.

MERC Order for determination of Tariff for 11.5 MW MSW project of NSWPMPL

Order- Case No 158 of 2017 Page 10 of 92

2. CONCESSION AGREEMENT BETWEEN NMC AND CONCESSIONAIRE

2.1. Tendering Process

2.1.1. NMC had issued RfP document for selection of developers on DBFOT basis (copy of

which is shared by NSWPMPL as part of this Petition), wherein it stipulated eligibility

criteria for shortlisting the potential bidders. The eligibility criteria included the past

experience in commissioning a MSW processing facility of minimum 200 MT per day of

MSW in India or elsewhere in last five years and the plant to be operational for 180 days

before bid due date.

2.1.2. The financial requirement of minimum net-worth of Rs. 25 Crore at close of preceding

year was also stipulated as part of bid condition.

2.1.3. The Bid evaluation and selection of successful bidder was on the basis of minimum

technical and financial criteria and the bidder who quoted the lowest tipping fee declared

as the successful bidder.

2.1.4. Accordingly, the Project has been allotted to Consortium of M/s Essel Infraprojects Ltd.

and M/s Hitachi Zosen India Pvt. Ltd on DBFOT basis for construction and operation of

a MSW processing facility for 800 TPD for a period of 15 years. Post completion of the

Concession Agreement period, Concessionaire will have to transfer all the moveable

infrastructure and facilities including vehicles, equipment, workshop offices,

communication arrangement etc. and immovable infrastructure facilities, free of cost to

NMC.

2.2. Salient features of Concession Agreement

2.2.1. Consortium of M/s Essel Infraprojects Ltd. and M/s Hitachi Zosen India Pvt. Ltd

promoted and incorporated NSWPMPL as Special Purpose Vehicle (SPV) for execution

of the waste processing plant at Nagpur.

2.2.2. A Concession Agreement was signed between NSWPMPL and NMC on 4 May, 2017 for

design, construction and operation of MSW processing facility at Bhandewadi, Nagpur

for capacity of 800 MT per day including Pre-processing of MSW in line with the

provisions of the Solid Waste Management (SWM) Rules, 2016 over the period of

Concession Agreement. The Concession Agreement is for a period of 15 years, including

construction period of 2 years.

2.2.3. NMC has agreed to deliver the assured waste quantity of 800 TPD ±20% at the Project

site for processing. NMC has also agreed to pay a tipping fee of Rs. 225 per MT with an

annual escalation of 4.5% till the end of the Concession Period.

MERC Order for determination of Tariff for 11.5 MW MSW project of NSWPMPL

Order- Case No 158 of 2017 Page 11 of 92

2.2.4. The waste generation on a daily basis in Nagpur city is quantified by NMC in a report

covering a span of almost two years from 2015 to 2017. The data is shown in the Table

below:

Table 1: Waste Generation in Nagpur

Year Waste per month (in MT) Average Daily (in MT)

Apr-15 32907 1097

May-15 31103 1003

Jun-15 32785 1093

Jul-15 34164 1102

Aug-15 32330 1043

Sep-15 32255 1075

Oct-15 34785 1122

Nov-15 34986 1166

Dec-15 36448 1176

Jan-16 34738 1121

Feb-16 34443 1188

Mar-16 36080 1164

Apr-16 33970 1132

May-16 36140 1166

Jun-16 36923 1231

Jul-16 37483 1209

Aug-16 35511 1146

Sep-16 33999 1133

Oct-16 36007 1162

Nov-16 35068 1169

Dec-16 35517 1146

Jan-17 36181 1167

Feb-17 34349 1227

Mar-17 36848 1189

2.2.5. The Concessionaire can market and sell or dispose of all the components/ products of

MSW, including but not limited to electricity, recyclables and to further retain and

appropriate any revenues generated from the sale of such products/ end-products.

2.2.6. The Concessionaire shall receive all financial benefits accruing in respect of or on

account of the Project, including Carbon Credits/Certified Emission Reductions (CERs)

under the Clean Development Mechanism (CDM) and share 50% of such fiscal

incentives/ benefits with the NMC as per the provision of the Concession Agreement.

MERC Order for determination of Tariff for 11.5 MW MSW project of NSWPMPL

Order- Case No 158 of 2017 Page 12 of 92

2.2.7. The treatment facility selected for the Project would scientifically process and dispose the

MSW. NSWPMPL is to ensure that not more than 20% of the MSW received at the

processing facility will be sent to a Landfill.

2.2.8. The Concessionaire should transfer the Project facilities to NMC, free of cost at the end

of the Concession Period or on Termination, in accordance with the provisions of the

Agreement.

2.2.9. The Concession Agreement also provided for Condition Precedent for its effectiveness as

under:

Condition Precedent required to be satisfied by the Authority (NMC):

NMC shall hand over the land to the Concessionaire for the development of the

Project and provide clear, vacant and unencumbered possession of the site to the

Concessionaire.

NMC will enter into an Escrow Agreement in accordance with Clause 23 and as per

the schedule 20 of Escrow Agreement.

NMC shall appoint an Independent Engineering/monitoring committee in accordance

with the Article 21.

Some of the major Condition Precedent required to be satisfied by the Concessionaire:

Provide construction and O&M Performance Security to the NMC as specified in the

Addendum.

Provide project development Fee of 1% of the total cost of the project.

Prepare the Environment and social Impact assessment (ESIA) Report through a

competent agency and obtain approval from NMC.

Obtain the EIA approval for the Project from competent authorities.

Procure all applicable permits specified in Schedule-2 unconditionally and if subject

to conditions, all such conditions required to be fulfilled by date specified therein.

Execute the Financing Agreements and deliver to the NMC.

Execute and procure execution of Escrow Agreement

MERC Order for determination of Tariff for 11.5 MW MSW project of NSWPMPL

Order- Case No 158 of 2017 Page 13 of 92

Obtaining consent to establish and operate, based on project requirement from the

Maharashtra Pollution Control Board (MPCB), as per applicable rules and regulations

including SWM Rules, 2016.

2.3. Salient features of the Nagpur MSW Project, as per NSWPMPL

2.3.1. The proposed MSW Project involves use of mass combustion / incineration technology

for WtE conversion.

2.3.2. The Project will receive about 800 TPD of mix waste which will be segregated during

Pre-processing treatment and Project will process approximately 550 TPD of Pre-

processed MSW and produce around 80.59 million units yearly including Auxiliary

Consumption.

2.4. Scope of work of MSW Project

2.4.1. As per clause 2.1 of the Concession Agreement the scope of work is as follows: -

a) Design, construction and operation of MSW processing facility at Bhandewadi,

Nagpur for assured MSW quantity during the Concession Period.

b) The Concessionaire should erect a plant of capacity 800 TPD with presorting waste to

energy per day capable of producing 11.5 MW less auxiliary consumption.

c) Provision and operation of adequate number of suitable vehicles for transport of

MSW within the Municipal Solid Waste Management Facility at Bhandewadi

Nagpur.

d) Performance and fulfillment of all other obligations of the Concessionaire in

accordance with the provisions of Concession Agreement and matters incidental

thereto or necessary for the performance of any or all of the obligations of the

Concessionaire under the Concession Agreement.

e) Rehabilitation and operations and maintenance of existing Scientific Landfill and

disposal of process remnants and Residual Inert matters.

f) Re- Location of waste dumped at proposed land site at Bhandewadi.

g) The scope of work also included any and all other activities that are ancillary to the

above mentioned scope of work.

h) The Concessionaire has to develop and implement the above Project on DBFOT

basis.

MERC Order for determination of Tariff for 11.5 MW MSW project of NSWPMPL

Order- Case No 158 of 2017 Page 14 of 92

2.5. Existing and New Scientific Landfills

2.5.1. The Concessionaire is responsible for rehabilitation and operations and maintenance of

existing Scientific Landfills (SLF). As per the provisions of SWM rules 2016, post-

closure care of landfill site shall be taken for at least fifteen years. Accordingly, the

Concessionaire is required to close the existing SLF as well as to maintain the exiting

SLF post closure the till 15th

year of the Project life.

2.5.2. Further the Concessionaire is also responsible for design, construction and operation of

new SLF along with its post closure maintenance. Accordingly, the Concessionaire has

proposed new SLF consisting of 3 cells. Each cell of new SLF would be used

sequentially up to its storage capacity. Further, the use of the three cells for the new SLF

would be closed at the end of 4th

year, 8th

year and 13th

year from CoD of the proposed

Project respectively. Each of these closure would incur a capital expenditure towards

scientific closure of SLF site at respective years.

2.5.3. All closed SLFs would be maintained for 15 years from the day of their respective

closures.

2.6. Role of NMC

2.6.1. To grant in a timely manner all such approvals, permission and authorization which

Concessionaire may require.

2.6.2. To recommend and forward to the relevant authority/ministry /department any

application of Concessionaire to obtain necessary permissions.

2.6.3. To ensure that the building plans for the Projects Facilities at site are duly and

expeditiously approved by the concerned authority under relevant Acts/ Building by-laws

/other relevant bylaws or regulation

2.6.4. To handover land to the Concessionaire as per the requirement, on a License basis, for

development of the Project Facilities and Land Fill at Bhandewadi, Nagpur

2.6.5. To pay Tipping fee to Concessionaire for processing of MSW on a Monthly basis.

2.6.6. To declare and maintain or cause to declare and maintain, a no development zone around

the landfill site in accordance with applicable laws

MERC Order for determination of Tariff for 11.5 MW MSW project of NSWPMPL

Order- Case No 158 of 2017 Page 15 of 92

2.7. Term and Termination of Agreement:

As per Concession Agreement, the tenure of Concession Period means fifteen (15) years

including construction period of 24 months starting on and from the Appointment Date

and ending on Transfer Date. As defined in the Concession Agreement, “Appointment

Date means the date on which Financial Close is achieved or an earlier date that the

Parties may by mutual consent determine, and shall be deemed to be the date of

commencement of the Concession Period” As defined in the Concession Agreement,

“Transfer date means the date on which this Agreement and the Concession hereunder

expires pursuant to the provisions of this Agreement or is terminated by a Termination

Notice.”

Further, as per the Concession Agreement the agreement may be terminated by either

party on the occurrence of the following Events:

2.7.1. Termination due to failure to achieve financial closure: As per clause 23.2 of

Concession Agreement in case financial closure does not occur, for any reason

whatsoever, the Concession agreement shall be deemed to have been terminated, upon

such termination NMC shall be entitled to encash the bid security.

2.7.2. Termination upon occurrence of any Forces Majeure Event: As per clause 26.8 of

Concession Agreement, if a forced Majeure Event subsists for a period of 180 days or

more with a continuous period of 365 days, either party may in its discretion terminate

the agreement by issuing termination notice to the other party, upon issuance of such

termination notice the agreement shall stand to be terminated.

2.7.3. Termination due to Default Event: In case of occurrence of either Concessionaire (i.e.

NSWPMPL) or Authority (i.e. NMC) event of default i.e. either party may terminate the

agreement by issuing a termination notice in a manner set out under clause 29.2.3 of

Concession Agreement.

2.7.4. Events of Default as per Concession Agreement have been stipulated as follows

1. Concessionaire Event of Default: In case a Concessionaire event of default occurs

(as given in clause 29.1.2) and the Concessionaire fails to cure the default within the

cure period (if cure period not specified a cure period of 30 days), the Concessionaire

shall be deemed to be in default of the agreement.

2. Authority Event of Default: In case an Authority event of default (as given in clause

29.1.3) occurs and NMC (the authority) fails to cure the default within the cure period

of 90 days, NMC shall be deemed to be in default of the agreement.

MERC Order for determination of Tariff for 11.5 MW MSW project of NSWPMPL

Order- Case No 158 of 2017 Page 16 of 92

2.8. Ownership of assets and transfer of Project

2.8.1. As per clause 22 of the Concession Agreement, the ownership of the Project Facilities,

including all improvements made therein by Concessionaire during the Concession

Period that, all the immovable assets including sites and civil structure created for

processing facility shall remain with NMC, while the ownership of all the moveable

assets including equipment and machinery and vehicles shall remain with the

Concessionaire.

2.8.2. Upon completion of the Concession period the Concessionaire shall transfer all the

moveable infrastructure and facilities including vehicles, equipment, workshop offices,

communication arrangement etc. and immovable infrastructure facilities to NMC in

working condition and certified by independent engineer, free of cost.

2.8.3. The Concessionaire shall provide training to NMC‟s staff for taking over the Project

facilities from the Concessionaire for at least 3 months.

2.9. Viability Gap Funding

2.9.1. NMC has committed a Viability Gap Funding (VGF) support amounting to a maximum

of Rs. 70 Crore to NSWPMPL and as per clause 39.1 and 39.2 of the Concession

Agreement the VGF would be released in minimum of two tranches as follows: -

a) First tranche to the extent of a maximum 50% of VGF amount or an amount equal to

Concessionaire‟s equity contribution whichever is less shall be released at a date not

earlier than 30 day of fulfilment of condition precedent to VGF disbursement.

b) The balance 50 % amount shall be release in the second Tranche or progressively in

equal installments subject to equity contribution and achievement of milestones as

well as fulfilment of condition precedent to VGF disbursement.

2.9.2. VGF shall be released by NMC subjected to creation of security by Concessionaire

(NSWPMPL) in favor of NMC on the assets of the Project.

2.10. Bid evaluation report and observations of NEERI and GIPE:

2.10.1. The technical evaluation of bid was carried out by National Environmental Engineering

Research Institute (NEERI) and the financial evaluation by Gokhale Institute of Politics

& Economics (GIPE), Pune.

2.10.2. The key recommendations of NEERI report are as follows:

a) From the environmental point of view MSW management is essential and has to be

taken up on priority basis considering the rapid urbanization and increasing

MERC Order for determination of Tariff for 11.5 MW MSW project of NSWPMPL

Order- Case No 158 of 2017 Page 17 of 92

population. The scientific waste management should have priority over energy

recovery or product recovery.

b) The apprehensions about the incineration are air pollution and the design of basic

incineration equipment, which can be sorted out by selection of the appropriate and

proven design and robust pollution control systems. NMC may go ahead with Hitachi

Zonsen‟s technology subject to strict compliance to environment laws.

c) Hitachi Zosen‟s incinerator has considered the wide range of calorific value of MSW

i.e. from 1100 kcal/kg to 2200 kcal/kg, which is normal Indian MSW scenario with

800 TPD of nominal waste throughout of 1650 kCal/kg. NSWPMPL has designed the

WtE plant to burn waste with the lowest heat value (LHV) which can reasonably be

sent to a waste incineration plant.

d) NSWPMPL has proposed storage of 5 days which appears to be adequate in normal

circumstances.

e) The bidder shall install appropriate segregation system for removal of construction

and demolition (C&D) waste and to maintain caloric value suitable for the plant.

f) The bidder shall maintain the existing RDF, compost and landfill facilities to avoid

any further environmental impact and health problem to people inhabited in and

around the site.

g) The bidder shall install and operate state of art emission control system for

conforming to all Central Pollution Control Board (CPCB) and Maharashtra Pollution

Control Board (MPCB) norms, including dioxins and furans, Compliance to

Environmental norms is the most important.

Key observations of GIPE:

2.10.3. GIPE evaluated financial proposal of MSW processing plant at Nagpur and found that the

EPC cost of Rs. 251.63 Crore for MSW Plant is overestimated which includes soft cost of

16%.

2.10.4. Plant O&M expenses and periodic maintenance cost is also overestimated with escalation

rate of 6.5% p.a. which is higher than CERC norms of 5.72% p.a.

2.10.5. Overestimated cost and O&M expenses results in lower Project IRR (12.62%) and Equity

IRR (14.76%). Further NEERI report has not considered the favorable tax treatment

available for infrastructure Projects. Sales of revenue from electricity has not been

considered in the NEERI report.

MERC Order for determination of Tariff for 11.5 MW MSW project of NSWPMPL

Order- Case No 158 of 2017 Page 18 of 92

2.10.6. The cost of fly ash disposal plant has been considered as Rs. 3.37 Crore. However,

revenue from using the fly ash in the manufacture of bricks has not been estimated over

the Concession period.

GIPE reworked the financial parameters based on the CERC norms and found that the

project IRR and equity IRR of the Project works out to be 17.32% and 26.18%

respectively. GIPE has considered levellised tariff of Rs. 6.82 per kWh as per norms

considered by CERC. Details of financial working of GIPE is provided in the Table

below.

Table 2: Financial working by GIPE

Variable in Decision Sheet

Original

proposal of

EIL

GIPE

working as

per CERC

Guidelines

Financing Cost, IDC & Pre-Operative Exp. (% of EPC) 15.00% 15.00%

Yearly Increase in O&M Expenses 6.50% 5.72%

Interest Rate (p.a.) 12.75% 13.00%

Tipping Fee for Processing of Waste (Rs. per MT) 750.00 750.00

Yearly Increase in Tipping Fee for Processing of Waste 4.50% 0.00%

O&M - Processing 14.00 8.63

Gross MW Generation 11.50 11.50

Auxiliary consumption (%) 16.00% 12.50%

PLF: 1st year 60.00% 60.00%

PLF: 2nd year 80.00% 65.00%

PLF: 3rd year onwards 85.00% 70.00%

Levellised Tariff (in Rs.) 5.86 6.82

Based on above observations, GIPE concluded that the Project is financially viable.

2.11. Solid Waste Management Rules (SWM) 2016 and its Implications:

2.11.1. MoEF had notified the SWM Rules 2016 on 8 April 2016 to lay a framework for

scientific waste management across urban settlements and are applicable beyond

Municipal areas and extend to urban agglomerations, census towns, notified industrial

townships, areas under the control of Indian Railways, airports, airbase, Port and harbor,

defense establishments, special economic zones, State and Central government

organizations, places of pilgrims, religious & historical importance. These Rules

supersede the Municipal Solid Waste Rules, 2000. SWM,2016 Rules explicitly

emphasize on Pre-processing and Post-processing of MSW. These rules have casted the

responsibility of Pre-processing and Post processing on local bodies.

MERC Order for determination of Tariff for 11.5 MW MSW project of NSWPMPL

Order- Case No 158 of 2017 Page 19 of 92

2.11.2. The SWM Rules,2016 lay emphasis on:

Source segregation of waste to channelize the waste to wealth by recovery, reuse

and recycle

Levy of user fees for collection of waste by local bodies.

Waste processing and treatment

Promoting use of compost

Promotion of waste to energy

Revision of parameters and existing standards

Management of waste in hilly areas

Constitution of a Central Monitoring Committee

2.11.3. Clause 9 seeks Distribution Licensees to procure power generated from municipal solid

waste to energy plants.

2.11.4. Clause 10 stipulates facilitation of infrastructure creation for waste to energy plants and

providing appropriate subsidy or incentives for such waste to energy plants as the duties

of MNRE Sources.

2.11.5. Clause 15 specifies the duties and responsibilities of local authorities wherein the local

authorities are responsible for: -

Facilitation construction, operation and maintenance of solid waste processing

facilities (on their own /private participation/other agency) for optimum utilization of

solid waste by adopting suitable technology including waste to energy.

Adhering to the guidelines issued by the Ministry of Urban Development from time

to time and standards prescribed by the Central Pollution Control Board.

Undertaking (on their own/through other agency) construction, operation and

maintenance of sanitary landfill and associated infrastructure.

Stop land filling or dumping of mixed waste soon after the timeline as specified for

setting up and operationalization of sanitary landfill is over.

Allow only the non-usable, non-recyclable, non-biodegradable, non-combustible and

non-reactive inert waste and pre-processing rejects and residues from waste

processing facilities to go to sanitary landfill

2.11.6. Clause 16 stipulates monitoring of environmental standards and adherence to conditions

as specified under the Schedule I and Schedule II of the rules for waste processing and

MERC Order for determination of Tariff for 11.5 MW MSW project of NSWPMPL

Order- Case No 158 of 2017 Page 20 of 92

disposal sites, as one of the duties of State Pollution Control Board or Pollution Control

Committee.

2.11.7. Clause 19 specifies criteria for duties regarding setting-up solid waste processing and

treatment facility.

2.11.8. As per Clause 21, Non-recyclable waste having calorific value of 1500 kCal/kg or more

shall not be disposed of on landfills and shall only be utilised for generating energy either

or through refuse derived fuel or by giving away as feed stock for preparing refuse

derived fuel.

2.11.9. The Schedule I (A) of SWM Rules, 2016 specifies the following condition for site

selection of sanitary Landfills: -

Specifications for Sanitary Landfills

“(A) Criteria for site selection. -

…

(ii) The sanitary landfill site shall be planned, designed and developed with proper

documentation of construction plan as well as a closure planning a phased manner. In

case a new landfill facility is being established adjoining an existing landfill site, the

closure plan of existing landfill should form a part of the proposal of such new

landfill………………………………………………………………………….

2.11.10. Schedule-I (H) of SWM Rules, 2016 specifies the Criteria for post-care of landfill site as

below:

(1) The post-closure care of landfill site shall be conducted for at least fifteen years and

long term monitoring or care plan shall consist of the following, namely: -

(a) Maintaining the integrity and effectiveness of final cover, making repairs and

preventing run-on and run-off from eroding or otherwise damaging the final

cover;

(b) Monitoring leachate collection system in accordance with the requirement;

(c) Monitoring of ground water in and around landfill;

(d) Maintaining and operating the landfill gas collection system to meet the

standards.”

2.11.11. Therefore, as per the above provisions Concessionaire has to undertake the post-closure

care of landfill site for at least fifteen years.

MERC Order for determination of Tariff for 11.5 MW MSW project of NSWPMPL

Order- Case No 158 of 2017 Page 21 of 92

2.11.12. The Schedule 2 (C) of the SWM Rules, 2016 also stipulates various emission standards to

be met by incineration/thermal technologies in Solid Waste treatment/disposal facility as

follows.

Table 3: Emission standard for incinerators technologies as per SWM Rules, 2016

Parameter Emission standards

Values Reference

Particulates 50 mg/Nm3 Standard refers to half hourly average value

HCl 50 mg/Nm3 Standard refers to half hourly average value

SO2 200 mg/Nm3 Standard refers to half hourly average value

CO

100 mg/Nm3 Standard refers to half hourly average value

50 mg/Nm3 Standard refers to daily average value

Total Organic

Carbon 20 mg/Nm3 Standard refers to half hourly average value

HF 4 mg/Nm3 Standard refers to half hourly average value

NOx (NO and NO2

expressed as NO2 ) 400 mg/Nm3 Standard refers to half hourly average value

Total dioxins and

furans

0.1 ng

TEQ/Nm3

Standard refers to 6-8 hours sampling. Please refer

guidelines for 17 concerned congeners for toxic

equivalence values to arrive at total toxic

equivalence.

Cd + Th + their

compounds 0.05 mg/Nm3

Standard refers to sampling time anywhere

between 30 minutes and 8 hours.

Hg and its

compounds 0.05 mg/Nm3

Standard refers to sampling time anywhere

between 30 minutes and 8 hours

Sb + As + Pb + Cr +

Co + Cu + Mn + Ni

+ V + their

compounds

0.5 mg/Nm3 Standard refers to sampling time anywhere

between 30 minutes and 8 hours

Accordingly, the Concessionaire has to meet the above mentioned emission standards.

2.12. Provisions of Tariff Policy 2016:

2.12.1. The Tariff policy 2016 mandates distribution licensees to procure 100 % of the power

produced from Waste to Energy Project, the relevant extracts are reproduced below

“6.4 Renewable sources of energy generation including Co-generation from renewable

energy sources:

…………….

MERC Order for determination of Tariff for 11.5 MW MSW project of NSWPMPL

Order- Case No 158 of 2017 Page 22 of 92

1 (ii) Distribution Licensee(s) shall compulsorily procure 100% power produced from all

the Waste-to-Energy plants in the State, in the ratio of their procurement of power from

all sources including their own, at the tariff determined by the Appropriate Commission

under Section 62 of the Act.”

2.12.2. Further the clause 6.4 (2) of the Tariff policy 2016, stipulates exemption of waste to

energy plant from Competitive bidding based tariff determination. The relevant extract of

the tariff policy 2016 is reproduced below:

“6.4 (2) States shall endeavor to procure power from renewable energy sources through

competitive bidding to keep the tariff low, except from the waste to energy plants”

MERC Order for determination of Tariff for 11.5 MW MSW project of NSWPMPL

Order- Case No 158 of 2017 Page 23 of 92

3. PREMISES FOR DETERMINATION OF PROJECT-SPECIFIC TARIFF

3.1. Regulatory Framework for Tariff Determination

3.1.1. As per Section 62(1) of the EA, 2003, the Appropriate Commission is empowered to

determine the Tariff for supply of electricity by a Generating Company to a Distribution

Licensee, and for transmission and wheeling of electricity. As per Section 61 (h), the

Commission shall be guided, among others, by the aspect of promotion of electricity

generation from renewable sources of energy.

“61. The Appropriate Commission shall, subject to the provisions of this Act, specify the

terms and conditions for the determination of tariff and in doing so, shall be guided by

the following, namely………………………

(h) The promotion of co-generation and generation of electricity from renewable

sources of energy;”

3.1.2. Section 86(1)(e) of the Electricity Act, 2003 stipulates that –

"The State Commission shall discharge following functions, namely

(1)(e) promote cogeneration and generation of electricity from renewable sources of

energy by providing suitable measures for connectivity with grid and sale of electricity to

any person, and also specify, for purchase of electricity from such sources, a percentage

of total consumption of electricity in the area of distribution licensee.”

3.1.3. The Commission has recognized Municipal Solid Waste based Waste-to-Energy Projects

as Renewable Energy Sources. As per Regulation 2(cc) of the RE Tariff Regulations,

2015.

“(cc) „Renewable Energy Sources” means the renewable sources such as Mini, Micro

and Small Hydro, Wind, Solar, Biomass including bagasse, bio-fuel urban or Municipal

Solid Waste and such other sources as are recognized or approved by the MNRE”

3.1.4. Central Electricity Regulatory Commission (CERC) also recognizes these Projects in its

regulations as Renewable Energy Sources. As per Regulation 2(x) of the CERC RE

Tariff Regulations, 2017.

“renewable energy sources” means renewable sources such as small hydro, wind, solar

including its integration with combined cycle, biomass, bio fuel cogeneration, urban or

municipal waste and other such sources as approved by the MNRE;”

MERC Order for determination of Tariff for 11.5 MW MSW project of NSWPMPL

Order- Case No 158 of 2017 Page 24 of 92

3.1.5. Regulation 3.1 of the MERC RE Tariff Regulations, 2015 states that:

“3.1 These Regulations shall apply to those new RE Projects which are commissioned in

the State of Maharashtra for the generation and sale of electricity to Distribution

Licensees in the State, are Eligible Projects for the purposes of these Regulations, and

whose tariff is to be determined by the Commission under the provisions of Section 62

read with Section 86 of EA, 2003:”

3.1.6. As per Regulation 8.1, a Project-specific Tariff shall be determined on case to case basis

in case of MSW-based Power Projects.

“8.1 A Project-specific tariff shall be determined by the Commission on a case-to case

basis for the following types of Projects:

(a) Waste to Energy Projects based on the technologies approved by MNRE such as

Municipal Solid Waste-based Projects;”

3.1.7. Regulation 8.2 provides that the financial norms set out in the Regulations, except for

capital cost and O&M expenses, shall be the ceiling norms while determining the Project-

specific Tariff:

“8.2 The determination of Project-specific tariff for generation of electricity from such

RE sources shall be in accordance with such terms and conditions as may be stipulated

in the relevant Orders of the Commission:

Provided that the financial norms specified in Chapter 2, except with regard to

Capital Cost and O&M expenses, shall be the ceiling norms while determining such

Project-specific tariff.”

3.1.8. The Commission has issued a generic Tariff Order for procurement of power from RE

sources (namely, wind, non-fossil fuel-based co-generation, biomass, small hydro and

solar) for FY 2017-18 in Case No. 33 of 2017, dated 28 April, 2017.

3.1.9. While determining the Project-specific Tariff for this MSW Project, it has considered the

relevant principles and methodology adopted in the RE Tariff Order and subsequent

regulatory developments including amendments to MYT Regulations so as to ensure

consistency and certainty in the regulatory approach.

3.2. Premise for Development of Tariff Structure:

3.2.1. The Commission has analyzed the Detailed Project Report (DPR) and the revised Petition

submitted by NSWPMPL taking into consideration the regulatory framework and the

objective of promoting generation from MSW-based Power Project. The Commission has

MERC Order for determination of Tariff for 11.5 MW MSW project of NSWPMPL

Order- Case No 158 of 2017 Page 25 of 92

also taken into consideration objection/suggestion/ view expressed by stakeholders

through public consultation process and submission thereof. The Tariff has been

determined as per Regulation 9.2 of the RE Tariff Regulations, which reads as follows:

“9.2 A Petition for determination of Project-specific tariff shall be accompanied by

such fee as may be specified in the applicable Regulations of the Commission, and shall

be accompanied by:

(a) Information in Forms 1.1, 1.2, 2.1 and 2.2, as the case may be, appended as

Annexure-A to these Regulations;

(b) A detailed Project report outlining technical and operational details, site-specific

aspects, premises for Capital Cost and financing plan, etc.;

(c) A statement of all applicable terms and conditions and expected expenditure for the

period for which tariff is to be determined;

(d) A statement containing details of any grant, subsidy or incentive received, due or

assumed to be due from the Central Government and/or State Government, which

shall also include the computation of tariff without consideration of such grant,

subsidy or incentive;

(e) Details of financial gain through REC or any other mechanism;

(f) Any other information that the Commission may require the Petitioner to submit.”

3.2.2. Useful Life: Regulation 2.1 (mm) of RE Tariff Regulations, 2015 stipulates as follows

regarding the Useful Life of RE Projects requiring a Project-specific Tariff.

“Provided that the Useful Life of other RE Projects shall be as stipulated by the

Commission while determining the Project specific tariff, taking into consideration the

norms of the Central Commission.”

3.2.3. The CERC RE Regulations, 2017, specifies 20 years as the Useful Life of MSW Projects.

Accordingly, the Commission has taken the Useful Life of the present Project as 20 years

from its CoD. Rationale for considering useful life as 20 years have been elaborated in

subsequent Section.

3.2.4. Levellised Tariff Design: In accordance with Regulations 11.2 and 11.3, the

Commission has determined the levellised tariff for the Project case under consideration.

The relevant provisions are given below:

MERC Order for determination of Tariff for 11.5 MW MSW project of NSWPMPL

Order- Case No 158 of 2017 Page 26 of 92

“11.2 For the purpose of computation of levellised tariff, a discount factor equivalent to

the normative post-tax weighted average cost of capital shall be considered.

11.3 Levelisation shall be carried out for the „Useful Life‟ of the RE Project, while tariff

shall be determined for the period equivalent to the Tariff Period.”

3.2.5. Tariff Period: The Commission has considered a Tariff Period of 13 years from the CoD

for the MSW Project of NSWPMPL.

3.2.6. The assumptions and rationale for input values of Project-specific parameters have been

elaborated in the subsequent Sections of this Tariff Order.

MERC Order for determination of Tariff for 11.5 MW MSW project of NSWPMPL

Order- Case No 158 of 2017 Page 27 of 92

4. SUGGESTIONS/OBJECTIONS, NSWPMPL’S RESPONSE AND COMMISSION’S

RULINGS

4.1. Maharashtra Energy Development Agency’s (MEDA) Submission:

4.1.1. MEDA sought clarification from NSWPMPL, whether NSWPMPL has come up with any

pilot Project based on the same technology in order to prove the technology for Indian

climatic condition and to ascertain the performance parameters for development of large

scale MSW power Project.

4.1.2. MEDA suggested NSWPMPL to compare the parameters such as capital cost, Auxiliary

Consumption, O&M expense, working capital etc., with the parameters as approved by

Commission in its order in Case No 87 of 2015 dated 10 October,2016 in matter of

petition filled by Kolhapur Green Energy for determination of tariff from its 1.8 MW

MSW based power Project, wherein the Commission has determined levellised tariff of

Rs. 5.49/kWh for 20 years. [This was subsequently modified for revision in escalation

factor through Review Order as Rs. 5.94/kWh]

4.1.3. MEDA sought clarification from NSWPMPL if it has already opted for MNRE subsidy,

stating that the MNRE scheme for providing subsidy of 2 Crore/MW (Rs. 10 crore

/Project) was applicable only for setting up of 5 pilot Project based on MSW till 30

September 2017.

4.1.4. MEDA referred to MNRE's Standing Committee Report on power generation from

Municipal Solid waste dated August 2016, and submitted that the tariff for all waste to

energy plants should be declared through the process of Competitive Bidding.

4.1.5. MSW Projects Based on gasification, incineration and pyrolysis technology should

comply with MPCB norms as all these technology comes under combustion

route/thermal process.

4.1.6. MEDA submitted that the GoM RE policy 2015 dated 20th July 2015 only specifies

target of 200 MW for Industrial waste based power Projects, and no targets have been

specified for MSW based Power Projects in the RE policy.

NSWPMPL’s Reply:

4.1.7. NSWPMPL has undertaken detailed technology assessment while selecting the waste

processing technology for the proposed Project. It involved extensive discussions with

prospective vendors, including the site visits to several operational plants globally. For

this a team comprising of 3 members have visited 2 plants in China namely Teda

Environmental processing facility in the City of Dalian and processing facility in Gonzou

in China. NSWPMPL has also visited gasification plants in India and in Germany and has

evaluated existing technologies in „waste to energy‟ concept.

MERC Order for determination of Tariff for 11.5 MW MSW project of NSWPMPL

Order- Case No 158 of 2017 Page 28 of 92

4.1.8. NSWPMPL has thus selected highly proven and dependable technology for processing

the waste and creating sustainable green energy. Hitachi Zosen‟s incineration technology

provides the cleanest and most efficient capability for managing waste processing and

creating sustainable green energy. M/s Hitachi Zosen has more than 833 operating WtE

Projects worldwide. NSWPMPL has therefore decided to move ahead by selecting the

technology partner, Hitachi Zosen which has most successful, existing and commercial

viable Projects. The primary promoter of the Project viz. Essel Infra has also successfully

commissioned and operating waste to energy plant based on mass incineration

technology in Jabalpur. EIL had ventured into the SWM business with focus on creation

of a sustainable ecosystem for future generations. Essel Infraprojects Ltd. is successfully

operating 11.5 MW waste to energy plant in Jabalpur (M.P.) for more than one and half

years on the same technology proposed for this Project.

4.1.9. WtE Projects have nonstandard scope of work, geographically different factors, and city

specific waste characteristics play a big role in definition of the capital expenditure.

These factors make mere comparison of cost parameters completely inappropriate.

Comparison of Kolhapur and Nagpur Project cannot be done as Regulatory framework

allows Project specific capital cost consideration to MSW Projects. Further Nagpur

Project involves rehabilitation of existing waste and its subsequent closure. The existing

waste dumped in the SLF needs to be properly rehabilitated by use of excavators/JCB‟s

to enable proper closure of the same. This also requires design and construction of the

same. Additionally, Nagpur Project also have air cooled condenser which increases the

auxiliary consumption.

4.1.10. As per the discussion with MEDA and as per GoM Comprehensive policy for RE dated

July 20th

, 2015, Municipal Solid Waste based WtE Plants are not included in the list for

subsidy and other incentives. Therefore, in compliance with the policy, NSWPMPL has

not approached MNRE for the financial assistance under any scheme. However, the VGF

for the Project committed by NMC has been used to offset the tariff required.

4.1.11. NMC has followed the process of competitive bidding for selection of selection of

successful bidder for the Nagpur MSW plant. NMC had invited proposal for EoI for

selection of bidders for construction, operation and maintenance of MSWM facility for

treating the MSW on DBFOT basis. Consortium of M/s Essel Infraprojects Ltd. and M/s

Hitachi Zosen India Pvt. Ltd. won the bid in competitive bidding process. The above

process concludes that NMC had followed the recommended procedure for selection of

successful bidder for Nagpur WtE power plant.

4.1.12. NSWPMPL appreciates the concern raised by MEDA regarding compliance with

environmental norms. It would be appropriate to re-iterate that NSWPMPL has chosen a

technology partner which has a successful record of setting up plants with the proposed

technology across the countries having stricter norms for environmental compliance.

MERC Order for determination of Tariff for 11.5 MW MSW project of NSWPMPL

Order- Case No 158 of 2017 Page 29 of 92

NSWPMPL shall ensure that all statutory compliances are in place for successful

execution of the Project.

Commission’s view:

4.1.13. The Commission notes the MEDA‟s concern regarding of selection of appropriate

technology which suits Indian conditions. The technical evaluation report prepared by

NEERI and financial assessment report prepared by GIPE confirms that the said

technology and proposed Project is technically feasible and economically viable. Further

in response to the Commission‟s query during Public Hearing, NSWPMPL has confirmed

that, the support of its Technology Partner M/s Hitachi Zosen India Pvt. Ltd. shall be

available throughout the Concession Period of the Project.

4.1.14. The Commission notes the submission of MEDA and reply submitted by NSWPMPL.

Regarding availability of MNRE or any other subsidy, NSWPMPL has submitted that, it

is not availing any grant or subsidy except VGF of Rs. 70 Crores from NMC which it has

factored in Tariff.

4.1.15. Regulation 24 of RE Tariff Regulations, 2015, specifies the treatment to be provided to

the grant, subsidy or any incentives received by Project Entity. The Commission has

considered the VGF of Rs. 70 Crores to be received to NSWPMPL from NMC while

determining the Tariff.

4.1.16. Accordingly, the Commission rules that, in case any additional subsidy or grant is

received by NSWPMPL other than VGF of Rs. 70 Crores to be received from NMC,

MEDA shall inform the Distribution Licensee(s) regarding any such grant, subsidy or

incentives received by a NSWPMPL and Distribution Licensee(s) shall deduct any such

grant, subsidy or incentives received by a NSWPMPL in subsequent bills raised by

NSWPMPL towards sale of electricity in suitable installments or within such period as

may be stipulated by the Commission.

4.2. Nagpur Municipal Corporation’s (NMC) Submission:

4.2.1. The Commission during TVS, directed NSWPMPL to implead NMC as a Party and serve

the copy of the Petition to NMC. Accordingly, NSWPMPL impleaded as a Party and

served the copy of Petition and minutes of TVS. NMC vide its email dated 28 December,

2017 made its submission on the Petition submitted by NSWPMPL and queries raised by

the Commission during TVS.

4.2.2. NMC submitted that, the dumping yard at Bhandewadi, Nagpur is in existence since

1967. The waste was being dumped in around 55 acres of the reserved land in

unscientific manner. Regarding consideration of 15 year of Concession Period, presently

M/s Hanjer Biotech Energies Pvt. Ltd. is appointed as BOOT operator and processing the

waste of 200 MT/day and the contract is for 15 years. Since the life of existing SFL under

MERC Order for determination of Tariff for 11.5 MW MSW project of NSWPMPL

Order- Case No 158 of 2017 Page 30 of 92

existing contract with Hanjer is envisaged for another 15 years, during finalization of

present tender, NMC decided to consider the bid for 15 years‟ period.

4.2.3. Further, NMC submitted that, after the contract period of 15 years is over, NMC will be

in possession of the waste to energy plant, and shall operate the plant by appointing a

new operator on the basis of tendering. The tipping fee will be also decided based on the

quotes, received through tendering process after 15 years.

4.2.4. NMC also submitted that, the existing plant installed by M/s Hanjer was operating only

on part capacity. In the year 2011-12, due to major fire in the processing unit & the

operator‟s limitations, M/s Hanjer, could not bring the plant to its original capacity. Due

to this there was a PIL in the Hon‟ble Bombay High Court, Nagpur bench & this matter

was further transferred to the Hon‟ble National Green Tribunal (NGT) Western Zone,

Pune being an environmental issue.

4.2.5. National Green Tribunal (NGT) instructed NMC to go for new operator at the earliest.

On this, NMC has carried out tendering process selection of the developer for processing

waste of 800 TPD. Since only one bid was received, NGT directed to get the bid

scrutinized by NEERI and GIPE. NEERI and GIPE has scrutinized the bid submitted by

M/s Essel Infraprojects and submitted its report. The report of NEERI and GIPE was

submitted to NGT and NGT and directed to complete the tendering process. The bid was

negotiated before the Municipal Commissioner of Nagpur and M/s Essel Infraprojects

offered the revised Tipping of Rs. 225 per MT with 4.5% escalation. The same was

submitted before the standing committee for approval. Upon approval, Concession

Agreement was signed with NSWPMPL on 4 May, 2017.

NSWPMPL’s Reply:

4.2.6. NSWPMPL vide its letter dated 1 January, 2018 submitted its reply on the submission

made by the NMC dated 28 December, 2017. NSWPMPL submitted that in view of the

non-operational waste processing units, there have been a series of directives from the

NGT asking NMC to come up with new waste processing facility on urgent basis to

address the environmental concerns. The proposed site is next to the existing dump site,

which avoids the resistance to such projects from citizens. Moreover, the identified site

also makes it possible to include the closure of existing landfill and rehabilitation of the

accumulated waste in the scope of PPP Project developer. Hence, NMC had appropriately

decided to proceed with competitive bidding for 15 years in order to address the issues of

existing dumping site.

4.2.7. Technical evaluation of the bid was done by NEERI, while the financial evaluation was

done by GIPE to finalize the tipping fees and other financial parameters. The integrated

DPR of scientific management and disposal Municipal Solid waste of Nagpur city was

submitted under the Swachh Bharat Mission, which was subsequently approved by high

MERC Order for determination of Tariff for 11.5 MW MSW project of NSWPMPL

Order- Case No 158 of 2017 Page 31 of 92

power committee of GoM on 22 March 2016, along with a provision of viability gap

funding of Rs. 96.22 Crore for various components of the Municipal Solid waste, out of

which Rs. 70 Crore was allocated to WtE Project and the same has been considered for

Tariff determination.

4.2.8. NSWPMPL submitted that the plant will be transferred to NMC free of cost after the end

of 15 years period as provided under the Concession Agreement. NSWPMPL further

submitted that, since identified site is sufficient to absorb the inert and residue from the

procession facility for only about 15 years, NMC shall decide the future strategy for the

proposed Project only after conducting techno-commercial feasibility check. While

conducting the feasibility check NMC shall pay due consideration to the various key

aspects, such as land availability, compliance to environmental norms, growing

population density, technological advancements and the expected increase in the quantum

of MSW from 800 to 1500 TPD by 15 years. Therefore, NMC would need great deal of

clarity to ascertain the future of Project beyond 15 years.

4.2.9. As regards determination of Tipping fee, NSWPMPL submitted that, NMC would be in a

position to determine tipping fee only after finalizing the future of the Project at the end

of 15 Years period as provided under the Concession Agreement.

Commission’s view:

4.2.10. The Commission notes the submission of NMC regarding, competitive process conducted

by NMC for selection of bidder on DBFOT basis. The Commission also notes that,

though NMC has entered in to Concession Agreement with NSWPMPL for 15 years,

NMC has submitted that, Post completion of concession period of 15 years, NMC would

have liberty to operate the Project either themselves or by appointing a new operator on

the basis of tendering.

4.2.11. As regards Tipping Fee, the Commission notes that, NMC has confirmed about providing

Tipping Fee as per the provisions of the Concession Agreement and also NMC has

confirmed about providing VGF of Rs. 70.00 Crore to the NSWPMPL‟s MSW project.

Accordingly, the Commission has considered the VGF and Tipping Fee while

determining the Tariff for said Project.

4.3. Maharashtra State Electricity Distribution Company Limited (MSEDCL)’s

Submission

4.3.1. MSEDCL vide its letter dated 28 December, 2017 sought one week‟s time for submitting

its objections/suggestions on NSWPMPL‟s Petition. MSEDCL vide its letter dated 1

January, 2018 made its submission.

4.3.2. MSEDCL submitted that it purchases RE power only for fulfillment of its Renewable

Purchase Obligations (RPO). MSEDCL would not assume any obligation to enter into

MERC Order for determination of Tariff for 11.5 MW MSW project of NSWPMPL

Order- Case No 158 of 2017 Page 32 of 92

EPA, as it has sufficient power supply and adequate renewable projects in pipeline and

further option of purchasing REC to fulfil their future RPO target.

4.3.3. MSEDCL has submitted its analysis for higher Tariff of Rs. 7.80/kWh proposed by

NSWPMPL. NSWPMPL has proposed a PPA period of 13 years, while other SERC such

as Tamil Nadu, Telangana, Madhya Pradesh and Gujarat and MERC itself (in case of

Kolhapur MSW project) has approved PPA period of 20 Years.

4.3.4. Further, the Capital Cost of Rs. 19.03 Crore/MW proposed by NSWPMPL is higher as

against the Capital Cost approved by the Commission in case of Kolhapur MSW (13.79

Crore/MW) as well as the Capital Cost approved by other States (Tamil Nadu,

Telangana, Madhya Pradesh and Gujarat) for MSW Projects, which remains in range of

14 to 16 Crore/MW. Further, NSWPMPL is also receiving VGF of Rs. 6.09 Crore/MW

which was not available for other MSW Projects.

4.3.5. Further, the O&M cost approved for various MSW Projects in major states remains in the

range of 5 to 7% of Capital Cost, however NSWPMPL has computed O&M expense as

9.38% of capital Cost.

NSWPMPL’s Reply:

4.3.6. NSWPMPL vide its letter dated 4 January, 2018 submitted its reply to the objections/

suggestions submitted by MSEDCL. With regards to MSEDCL‟s submission on Useful

Life of 13 years considered by NSWPMPL, NSWPMPL submitted that, the RE Tariff

Regulations, 2015 does not explicitly define the term „useful life‟ for Waste to Energy

Projects in the state. The Regulations provide that the Commission can stipulate the

Useful Life in its Order after considering the case specific aspects for Waste to energy

Project. NSWPMPL has also submitted that, the O&M expense has highest impact on

Levellised Tariff which increases from 46% (year-2) to 82% (13th

year). This

demonstrates that, the higher Useful Life will further increase the Levellised Tariff on

account of increased O&M.

4.3.7. As regards Capital Cost, NSWPMPL has referred to Regulation 8.2 of RE Tariff

Regulations, 2015 which specifies, Project specific consideration of Capital Cost for the

WtE Projects. WtE Projects have non-standard scope of work, geographically different

factors, and city specific waste characteristics, therefore the approval of the Capital Cost

shall be on the merit of the specific Project under consideration instead of its comparison

with other Projects. In addition, NSWPMPL also has to comply with the norms specified

in the SWM rules 2016 such as mandatory pre-processing facility, compliance to

stringent emission norms etc., which has resulted into additional costs.

4.3.8. As regards O&M expenses, NSWPMPL submitted that the O&M expense as claimed by

NSWPMPL also includes additional O&M expenses towards Pre-processing activity