Embed Size (px)

Citation preview

BEING ENTREPRENEURIAL

New York State Small Business Development Center

and the

The CIL Management Center of the Western New York Independent Living Project, Inc.

A B U S I N E S S G U I D E F O R C I L S

ACKNOWLEDGEMENTS

This document is a joint project of the RRTC, WNYILP, NIDRR, NYSSBDC and the authors include the following individuals and institutions:

King, James L., NYS SBDC, SUNY Central AdministrationBrigham, William, NYS SBDC, SUNY AlbanyHefka, Michael, NYS SBDC, SUNY BuffaloMcCartney, Susan, NYS SBDC, SUNY BuffaloMorley, Thomas, NYS SBDC, Mercy CollegeNowicki, Raymond, CPA, Nowicki & Associates, Buffalo, NYThomason, Cindi, NYS SBDC, SUNY Buffalo

The Rehabilitation Research & Training Center on Independent Living Management is a member of The Family of Agencies of The Western New York Independent Living Project Inc.

This is a publication of the Rehabilitation Research & Training Center on Independent LivingManagement which is funded by the National Institute on Disability and Rehabilitation Research of the US Department of Education under grant number H133B000002. The opinions contained in this publication are those of the grantee and do not necessarily reflect those of the Department of Education

© 2004 by the New York State Small Business Development Center, Albany, NY. All rights reserved.© 2004, Rehabilitation Research and Training Center on Independent Living Management (RRTC-ILM), All rights reserved.

Permission is given for duplication or reproduction either mechanically or electronically of any portionof this manual, providing that the following credit is given: Reproduced by permission from materialsdeveloped by the Rehabilitation Research and Training Center on Independent Living Management(RRTC-ILM) and the NYS SBDC.

The NYS SBDC is partially funded by the US Small Business Administration. The support given by theSBA through such funding does not constitute an express or implied endorsement of the co-sponsor orparticipant’s opinions, products or services.

1

Table of Contents

BEING ENTREPRENEURIAL

Quick Start Guide . . . . . . . . . . . 3

Preface – A New Way . . . . . . . . 5

Introduction. . . . . . . . . . . . . . . . 9

Social Entrepreneurship? . . . 10

Background of the Project. . . 13

Is An Entrepreneurial Venture For Your CIL? . . . . . . 14

Strategic Planning and For-Profit Ventures – Is It For Your CIL? . . . . . . . . . . . . . 15

How To Integrate the VentureInto Your CIL Mission . . . . . . . 17

Tax Considerations: An Overview . . . . . . . . . . . . . . 24

Basic Business Considerations . . . . . . . . . . . . 24

Tax Considerations . . . . . . . . . 26

Prohibition Against Private Inurement (personal benefit): . . . . . . . 26

Lobbying Activities . . . . . . . 26

Quid Pro Quo Contributions . . . . . . . . . . . 27

Unrelated Business Income Tax (UBIT) . . . . . . . 27

Business Structure and Legal Form . . . . . . . . . . . . . 28

The CIL "Controlling" A Not-For-Profit (NFP) . . . 29

The CIL with a For-Profit C-CorporationSubsidiary . . . . . . . . . . . . . . 29

The CIL With an S-Corporation Subsidiary . . . . . . . . . . . . . . 30

The CIL as a Partner in aPartnership (including limitedpartnerships) . . . . . . . . . . . 30

Financial Statement and Disclosure Considerations 30

The Business Plan: The CIL’s Primary BusinessCommunication. . . . . . . . . . . . 31

Why Does a CIL Need aStrategic Business Plan?. . . . 31

Strategic Business Plan –Executive Summary . . . . . . . . 33

Business Description. . . . . 35

Market Analysis . . . . . . . . . 35

Product or Service Analysis . . . . . . . . . . . . . . . . 38

Competition . . . . . . . . . . . . 39

Marketing Strategy . . . . . . 40

Operations . . . . . . . . . . . . . 43

Management. . . . . . . . . . . . 45

Finances . . . . . . . . . . . . . . . 46

Supporting Information . . . 48

Timing . . . . . . . . . . . . . . . . . 49

Exhibits/Appendices. . . . . . 49

Wrapping up the Business Plan. . . . . . . . . . . 49

Summary. . . . . . . . . . . . . . . 50

Sample Balance Sheet . . . 51

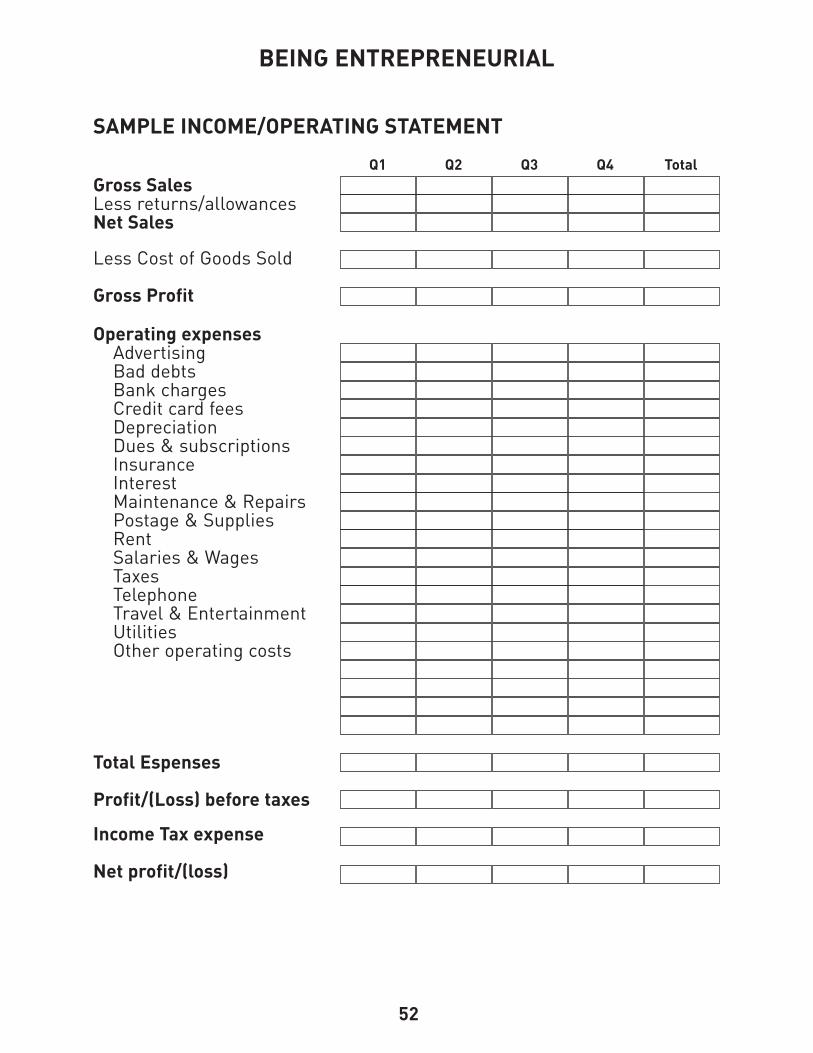

Sample Income/Operating Statement . . . . . . . . . . . . . . 52

Sample Cash Flow . . . . . . . 53

The CIL and SBDC Partnership In Action . . . . . . . 54

Case Study #1 – The Southwestern Center for Independent Living(SWCIL) - Minnesota . . . . . 55

Case Study #2 – Community Resources for Independence (CRI) CIL -Pennsylvania. . . . . . . . . . . . 57

Case Study #3 – The Lynchburg Area Centerfor Independent Living(LACIL) – Virginia . . . . . . . . 59

Case Study #4 – Independent Living Center of Hudson Valley (ILCHV) –New York . . . . . . . . . . . . . . . 61

Appendix A . . . . . . . . . . . . . . . 63

3

A BUSINESS GUIDE FOR CILS

Is entrepreneurship for your CIL?There are no guarantees inbusiness. There is no way toeliminate the risks associatedwith starting a small business.But, you can improve yourchances of success with goodplanning, preparation, andinsight. Start by evaluating yourstrengths and weaknesses.Consider each of the followingquestions:

Is your team together?It will be entirely up to your CILto develop projects, organizetime, and follow through ondetails.

How well do you get along with different stakeholders? Businesses need to developworking relationships with avariety of stakeholders, includ-ing boards, customers, vendors,staff, bankers, and other pro-fessionals (such as lawyers,accountants or consultants).

Can your CIL deal with ademanding client, an unreliablevendor, or a cranky receptionistif business interests demand it?

Can you make decisions? Business operations requiredecisions constantly and oftenquickly, independently, andunder pressure.

Do you have the physical and emotional stamina to run a business? Business operations can beexciting, hard work. Can busi-ness requirements specify theworkdays every week?

Can you plan and organize? Research indicates that poorplanning is responsible for mostbusiness failures. Good organi-zation of financials, inventory,schedules, and production canavoid many pitfalls.

Quick Start Guide

BEING ENTREPRENEURIAL

4

Is the commitment strongenough? Running a business can weardown individuals and organiza-tions. Some business teamsburn out quickly from having tocarry all the responsibility forthe success of the business.Strong motivation and commit-ment help the organization survive slowdowns and periodsof frustration.

How will a business affect your CIL?The first years of businessstart-up will be hard on theorganization. It is important forteam members to know what to expect. The team must beable to trust that the commit-ment will bring success. Theremay be financial strain until the business hits breakeven andbecomes profitable. This couldtake months or even years. Canthe parent CIL adjust to a drainon assets and some additionalrisk in the short-term, with the potential for long-term success?

5

PREFACE – A NEW WAY

A new way…Can a CIL operate in the for-profit world? An analysis ofalternatives, mission, culturesand history, can profits furtherCILs work?

The collaboration between theNew York State Small BusinessDevelopment Center (NYSSBDC) and centers for inde-pendent living (CILs) began in2001 with two training eventsdesigned to introduce not-for-profit centers for independentliving to the concept of businessplanning. The NYS SBDC andthe Rehabilitation Research &Training Center on IndependentLiving Management (RRTC-ILM), a member of the WesternNew York Independent LivingProject, Inc. family of agencies,established a relationship toprovide training and businessassistance to CILs interested indeveloping for profit ventures.Following these training events,three CILs were selected toreceive in-depth assistance tostructure and develop a for-profit venture within their CILs.This manual describes projects

in Erie, Pennsylvania,Lynchburg, Virginia, andMarshall, Minnesota that suc-ceeded with the help of repre-sentatives from the NYS SBDC,their local SBDC, and the RRTC-ILM. The outcomes of thesecase studies, along with thegeneral qualitative evaluationsfrom the training and advise-ment services, measure thesuccess of this collaboration.

A few years ago, a friendreferred a CIL director to mewho wanted to discuss businessopportunities. I did not knowwhat CIL stood for at the time.But, in the world of acronymsoup known as government thatwas not unusual. That was myintroduction to Douglas Usiak,Executive Director of theWestern New York IndependentLiving Project, Inc. (a CIL) andthe development of a series ofprojects that had me workingand experiencing tremendoushighs and extreme disappoint-ments.

Doug gave me a quick introduc-tion to the work of CILs. . Myfirst impression was that of abunch of well-intentioned peo-ple who see the world as it

A BUSINESS GUIDE FOR CILS

BEING ENTREPRENEURIAL

6

‘ought to be’ rather than thesometimes harsh reality of public sector programs andfunding. The key thing thatcaught my interest was thatthese people were not sittingand complaining. They werelooking for new, innovative, andeven untried ways of developingresources to ensure that theirwork would not be interruptedbecause of public funding losses.

I am the New York StateDirector of the Small BusinessDevelopment Center. We are ahigher education-based (StateUniversity of New York) busi-ness advisement, training andresearch organization. Lastyear, we advised 20,000+ entre-preneurs, about evenly dividedbetween start-ups and existingsmall business owners. Wetrained another 22,000+ entre-preneurs at 452 training eventsthroughout New York State. Ourresearch is usually for a specificbusiness. But we get involvedwith any topic that affects thesmall business sector. Lastyear, the small business ownerswe advised, invested $282 mil-lion in their businesses affect-ing 13,142 jobs.

Doug Usiak and I agreed thatthe SBDC would become one ofthe partners of the Rehabilita-tion and Research and TrainingCenter on Independent LivingManagement, a member of theWestern NY Independent LivingProject, Inc. family of agencies).The SBDC project included con-ducting two training events,wherein CILs would be intro-duced to the for-profit busi-ness-planning model. We wouldtest the model’s application toCILs. We would observe thecompatibility of profit decision-making and operations with CIL culture.

The training events weredesigned to advance CIL man-agers’ understanding of imple-menting and successfully oper-ating a for-profit venture withina CIL. While for-profit endeav-ors may be viewed as a majordeparture from the mission andorganizational culture of CILs,they are a valuable alternative ifCIL services are to be main-tained and expanded in today’schallenging environment.

Two training events were held(August, 2001 in Buffalo, NY andJanuary, 2002 in Las Vegas,

7

NV). From those participating,two or three CILs were selectedfor in-depth development of astrategic business plan tostructure a for-profit venturewithin the CIL. The outcomes ofthese case studies, along withgeneral qualitative evaluationsfrom the training and advise-ment services, serve as meas-ures for this section of the proj-ect. Outcomes are being evalu-ated based on contributions ofthe subsidiary to the parent CILorganization and based on theobjectives of that CIL. (Casestudies of the specific effortsare included in this workbook)

Some of the project’s anticipatedoutcomes included:

• Measurement of financial contributions

• Revisions to CIL operating procedures

• Broadened vision for the CIL organization

• Greater and improved community interaction

• More pro-active internal governance of the CIL

• Greater public exposureand enhanced image forthe CIL, and

• Management revisions to apply the business modelto CIL operations.

After the training events, inter-ested CILs were provided with a questionnaire to solicit theirconceptual business proposals.Interviews were conducted toassess the receptivity andpotential impact of SBDCexpertise. A selection teamcomposed of RRTC-ILM andSBDC staff ranked each propos-al and selected four viable candidates. We culled this listfurther, approving three CILsfor this project.

The training sessions encour-aged questions and identifiedvarious concerns that had to beconsidered before a CIL pro-ceeded to launch a for-profitbusiness. These questions wereanswered through longer-termconsulting engagements or inone-to-one meetings with busi-ness mentors from the SBDCs.While the NYS/SBDC is the leadSBDC in each project, the geo-graphic dispersion of the partic-ipating CILs necessitated theinclusion of local SBDC staff for localized services. At eachparticipating CIL, a resource

A BUSINESS GUIDE FOR CILS

BEING ENTREPRENEURIAL

8

team coordinator fromNYS/SBDC conducted needsassessments, proposed a service plan to identify neededassistance, and acted as theliaison between the CIL, localSBDC services and research /technical expertise.

As participating CILs enteredthe consulting phase of the pro-gram, outcomes for the projectwere based upon identifiedobjectives. While growth infinancial viability was anticipat-ed, additional organizationalobjectives that had substantialimpact upon the participatingCIL were pre-identified. Thethree CILs selected to partici-pate in this project were locatedin Pennsylvania, Virginia andMinnesota. The selection com-mittee estimated the probabilityof success for each project andsummarized perceived obsta-cles and outcomes.

The projects are summarizedbelow. They are described inmore detail in the Case Studysection of this workbook.

Pennsylvania was the site of anurban real estate deal to pur-chase the building that the CIL

leased, establishing the CIL as a tenant/owner, developing theCIL as a facility manager andsubletting extra space to othertenants. Initial data indicatedthat the building, in relativelygood shape, would spin off rev-enues sufficient to eliminate theCIL’s rent and encourage facilityexpansion, reduce the CIL’scosts, thereby lowering over-head. At the outset, this projectwas viewed as a guaranteedsuccess, with minimal risk,substantial fiscal return, butlimited application to the fur-therance of the CIL’s mission.

Virginia was the site of a com-munity-based project to providecomputer technical expertiseand support. While market dataindicated customer needs andbusiness viability, the CILlacked unique skills or specialadvantages that could securethe business model or provide acomparable advantage to theCIL over time. Due to the gener-ic nature of the business con-cept, this project had greaterrisk and lowered expectation ofsuccess. The contributions tothe CIL’s mission were per-ceived as initially limited but

9

with greater potential as thebusiness matured.

Minnesota was the site of aproject that was fairly remotebut was viewed as ideally com-patible with the CIL mission.This project focuses on pre-fab-ricated ramp constructiondesigned to meet ADA codes.The business had limited com-petition, significant competitiveadvantage, and excellent mar-ket potential and commercialviability. The project was pre-identified as the project with thegreatest long-term potentialwhile directly contributing to itsCIL’s mission.

INTRODUCTION

This workbook is intended toassist CILs in evaluating theirpotential to develop and operatea for-profit entity for the benefitof their not-for-profit (NFP) CIL.The idea of being entrepreneur-ial has great appeal for manyorganizations for a wide varietyof reasons. These may rangefrom financial independence, togetting rich, to being in charge,or to better meet the mission of

the CIL during a period ofdeclining or stagnant support.

This project gathered numerouspeople together to contributetheir ideas, share expertise andexplore the unique obstaclesconfronted by CILs across thenation. Each participating CILagreed to undergo a significanteffort to analyze a particularbusiness concept for a profit-making venture and share thatexperience. The experiences ofparticipating CILs have beenincorporated in this workbookto further the understandingand value of this project. Forthat willingness and commit-ment, we thank each personand organization that attendedone of the three workshops wepresented, as well as the fiveCILs that choose to more fullyparticipate by pursuing or start-ing a business.

CILs going entrepreneurial per-formed just like the small busi-ness sector. Some CIL projectsnever launched (died duringdiscussion). Others started, butdid not attain success. Othersachieved their objectives andattained success.

A BUSINESS GUIDE FOR CILS

BEING ENTREPRENEURIAL

10

It is our hope that this work-book will stimulate your CIL’sthinking and help to avoid mostof the pitfalls that result inadded risk, business problemsand failures. Applying soundfor-profit business techniquesto the operations of a CIL canyield significant benefits, even ifa separate for-profit venture isnot launched or operated by theCIL. Whatever your CIL decides,good luck.

SOCIAL ENTREPRENEURSHIP?

An entrepreneurial venture by aCIL (a not-for-profit organiza-tion) may support the CIL’s mis-sion or simply advance priorityservices through added finan-cial support. It is important todetermine the CIL’s motivationfor pursuing a business venture,and define success in advancefor the endeavor. The idea of‘social entrepreneurship’ com-bines the passion of a socialservice mission with business-like discipline, innovation, anddetermination to achieve theefficiency associated with theprivate sector.

CIL entities going entrepreneurialblur the public/private sectorboundaries. Social entrepre-neurship includes social pur-pose business ventures, for-profit community businessesthat meet a social need, andhybrid organizations, which mixnot-for-profit and for-profit ele-ments (e.g. a homeless shelterstarting a business to trainemployees for a major hotel inhospitality skills). For CIL man-agement, the willingness toadopt, embrace, harness anddirect business attributes to theCIL can develop new models ofservice delivery, and mecha-nisms to evaluate existing serv-ices. It can become an agent ofchange within the social servicemission.

What is entrepreneurship?Entrepreneurship is the drivingforce behind the processes thatcreate economic activity. PeterDrucker said, "entrepreneursmay not cause change, but arethe opportunists who capitalizeon change (consumer prefer-ences, technology, style, opinion, etc.)."

11

It is important to understandthe opportunities that changeprovides for CILs. Will a busi-ness change a CIL or provide aresponse to changes that aretaking place in the market-place? What change must yourCIL understand?

Every business does not repre-sent entrepreneurship. Theopening of a franchise locationusually does not have the inno-vation and change elements ofentrepreneurship. For CILs,innovation and change mayoccur in the CIL rather than inthe business venture.Resourcefulness distinguishesentrepreneurial managementfrom administrative manage-ment. Entrepreneurial manage-ment pursues opportunitieswith less regard to neededresources, presuming additionalresources can be obtained if theopportunity has a sound busi-ness justification.

Understanding these differ-ences is important for CILs.Usually CILs are administrative-ly managed. An entrepreneurialCIL reconciles divergent man-agement styles and focuses

upon the positive contributionsof each style for longer-termsuccess. While not mutuallyexclusive, administrative andentrepreneurial managementstyles must co-exist if CILs areto prosper. Each managementstyle can benefit from the otherstyle for survival. Agreementwithin the CIL Board, manage-ment and staff, to pursuechange brought about by entre-preneurship will change theCIL’s organizational culture.

CILs have a social purpose andmission that are integral toongoing success. Mission-relat-ed impact is a critical measureof the evaluation for CILs whenexploring entrepreneurship.Ideally, profits can be justifiedbecause of the added support tothe CIL’s mission. The profits, oravoided costs, can have positiveimpacts upon the CIL in termsof quantity and quality of servic-es and improved lifestyles ofconsumers.

A CIL’s evaluation of an entre-preneurial activity includesunderstanding of the marketand the marketplace for theopportunity of success. CIL’s

A BUSINESS GUIDE FOR CILS

BEING ENTREPRENEURIAL

12

usual organizational mentalitydistributes resources. It doesnot sell them for value as abusiness. CIL support is mostoften driven by community needand social commitment, not bydemand. The ‘market factors’within CILs are not disciplinedcompared to business markets.

Public benefit organizations,such as CILs, seek to identifyneeds and improve or enhancethe lives of clients and servicerecipients. In business, thefocus on needs is defined bychoice and characterized bypreference. This notion of needpreference is central to entre-preneurial success.

The challenge for CILs is simi-lar to entrepreneurs - the pur-suit of a goal (business idea orservice mission), but not beyonda point considered reasonable.CILs should set specific goalsand attain buy-in from theentire organization if realisticexpectations of results are to be attained.

Businesses can be successfulby making small, incrementalinnovations or changes to exist-ing products or services.

Success does not requirewholesale or dramatic change.A small change can producestriking results. The strategicplan should be readily under-stood and garner the requiredcooperation and support withinthe organization to be successful.

Entrepreneurs are typicallycharacterized by scarce capital,which does not limit theirefforts. This is often due to theparticipation of others. If CILsare to be entrepreneurial, thenthe critical characteristics tolook for include: collaboration,organizational involvement andparticipation. It is often neces-sary to bring others into thebusiness venture to addressstrategic requirements. Forexample, if the CIL has produc-tion capability but lacks a distri-bution network, perhaps anoth-er organization is needed tomarket the product.

The CIL should understand thestrengths and weaknesses ofthe organization and anticipatechange. The level of change,innovation, and opportunity mayforce the CIL to re-examinebasic operations, test assump-tions, challenge ideas, share

13

information and draw on thecollective experience, skills andknowledge. Entrepreneurs pur-sue resources (from others) anduse them to effect change. If aCIL is committed to providingservices in the future, no matterwhat the level of public support,then an entrepreneurial attitudeshould be explored.

This workbook provides CILmanagement with questions toask when considering a changeto enhance their CIL’s stability.Most people are content withdoing the same thing, whetherin the public or private sector.Change brings risk about theunknown. Acceptance of riskcan be difficult for organizationsand individuals. The key tobeing entrepreneurial is theability to evaluate risk, plan forcontingencies and refine theunknown into an expectedfuture outcome. This process isknown as strategic planning andis the focus of this workbook.

BACKGROUND OF THE PROJECT

The business advisors providingexpertise to CIL entrepreneurs

answered many of the samequestions raised by entrepre-neurs in the private sector. Itwas recognized that, if the levelof risk could be overcome, theopportunity to advance the mis-sion of the CIL by structuring afor-profit unit would benefit theconsumers and the community.The question of accepting riskinitially started out as a second-ary consideration, because abasic and incorrect assumptionwas made - that project partici-pants were pre-committed toentrepreneurial development.Risk proved to be the criticalquestion for every CIL in theproject.

The participating CILs werescreened from a large pool ofapplicants who were aware ofthe changes effecting publicbenefit corporations. They wereselected to represent a cross-section of the entrepreneurialprocess. This assumed commit-ment by CILs (management,staff and Board) was anticipatedafter internal questioning, butwas soon recognized as nothaving been committed to priorto training. The unexpected lackof commitment to accept risk

A BUSINESS GUIDE FOR CILS

BEING ENTREPRENEURIAL

14

was an error. Training wasenhanced with each event withgreater inclusion of risk man-agement with the CILs. Boardmembers were more activelyincluded to help build internalsupport for the entrepreneurialactivity. The management andBoard of Directors for mostCILs were not in full agreementon the advisability of operatinga for-profit venture within theCIL. This conflict was consis-tently the most serious obstacleconfronted by the CILs who par-ticipated in this project.

IS AN ENTREPRENEURIALVENTURE FOR YOUR CIL?

A discussion format was used ineach of the three multiple daytraining events offered to inter-ested CIL managers and Boardmembers. This introduction tothe project selection processstimulated discussion. Itbecame apparent that many ofthe CIL participants had eitherkey management or key Boardmembers that perceived entre-preneurship as an opportunity.But few CILs had both team

groups with a consistent vision.These differences stimulateddiscussion. However, the incon-sistency created obstacles thatdetracted from enthusiasm forentrepreneurial change.Ultimately, a written agreementof CIL management and CILBoard to pursue entrepreneur-ial activities became a keydeterminant in the criteria forthe project’s success.

The following summary is thestarting point for a CIL interest-ed in creating a wider base ofsupport for combining for-profitactivities. Discussions on theseand related topics may be foundthroughout this workbook.Abraham Lincoln is creditedwith properly stressing the needfor planning and preparation.When asked how he would dealwith cutting down a very largetree that was estimated to takesix hours, Mr. Lincoln statedthat first, he would spend fivehours sharpening his axe. Wehope you will sharpen your mis-sion and plan for profits.

15

STRATEGIC PLANNING ANDFOR-PROFIT VENTURES – IS IT FOR YOUR CIL?

Each discussion is meant tofocus on an actual venture. Thatventure may come from a vari-ety of sources, such as CILmanagement, the Board ofDirectors, community needs ora single staff member. Thefocus should be on the stake-holder commitment and analy-sis of a specific definable ven-ture. The actual selection of theventure is less important thanthe understanding of the impactthe venture will have on the CIL:what risks are associated with aventure and how the decisionmakers view the resultingchanges to the CIL. The positionof the CIL’s key stakeholderswill be made clear through thecommitment process. Revisionsto the proposed venture may beincluded over time to deal withspecific concerns.

Exercise: Take a few minutesand look at your CIL’s MissionStatement. Discuss whether theMission Statement encourages oreven allows you to be entrepre-neurial. If not, decide what revi-

sions are necessary to have anentrepreneurial activity conformto the Mission Statement andprepare those revisions for for-mal adoption by the Board ofDirectors.

The feasibility of the venture istied to the motivation for thedecision. For a CIL, motivationsrange from cost containment toprofit incentives to support themission, to combinations ofmission support, added servic-es, to cost containment. (Costcontainment is the reduction ofCIL expenses, allowing savingsto be reprogrammed).

An example of cost containmentwould be: a CIL purchasing thebuilding where the CIL is rent-ing space. Rising rental costsincrease the total CIL operatingexpenses. The entrepreneurialoption might be to purchase thebuilding, helping to fix or stabi-lize these rental costs through amortgaged purchase. An addedbenefit would be the potentialincome of subletting unusedbuilding space to other organi-zations or small businesses.

A BUSINESS GUIDE FOR CILS

BEING ENTREPRENEURIAL

16

Exercise: Can you list the advan-tages of owning the building aswell as the risks of ownership?Where do you think the greatestobstacles would come from ifyour CIL tried to buy its building?Note: This situation will bereviewed in a case study later inthis workbook.

The ideal CIL for-profit venturemight be one that supports themission of the CIL, while con-tributing to the services orneeds of the CIL consumercommunity. CIL consumers relyupon goods and services fromthe business community.Occasionally, required con-sumer goods or services are notreadily available, or not avail-able at an acceptable cost,means of delivery orproduct/service feature. Thisnon-availability represents anopportunity for the CIL torespond to that need through abusiness venture.

By owning the business venture,a CIL determines the price (maychoose to limit profits in favor ofresponding to social needs) andimproves access to goods or

services. For-profit ventureshave incentives through taxesand accounting practices thatmay financially reward the CIL.These incentives are discussedin greater detail in the financialsection and tax appendix of thisworkbook.

The business plan is the start-ing point for most successfulbusiness ventures. Failing toplan for the success of the busi-ness is to plan to fail. Any CILthat is thinking about starting afor-profit venture is, by defini-tion, an innovator and undertak-ing additional risk. The businessplan is critical to controlling thelevel of risk associated with astart-up business venture.

Reference – see Case Study #3for some additional informationon risk tolerance in the CIL environment, assessment and the role of management and theBoard in the planning process.

The initial task for the entrepre-neurial CIL is to undertake anenvironmental review (political,financial, stakeholder and cus-tomer) of the influences that

17

may impact the venture. Thepolitical review sensitizes theCIL’s planning group to the criti-cism of unfair competitioncharges by any existing busi-ness in the same sector or mar-ket area. This concern can bedealt with through careful defi-nition of the customer targetmarket and clear explanation ofCIL business objectives, asthose objectives relate to theCIL’s mission. The establish-ment of a for-profit venture alsodeals with the unfair competi-tion charge against not-for-profits by creating a level play-ing field (financially and throughtaxes) with businesses in theprivate sector.

Staying within the CIL’s missionand balancing the needs of theCIL service community helphandle stakeholder concernsand customer justification. It isimportant to confront early crit-icism with full disclosure of theCIL venture and deal with anyexpressed concerns beforecommitments are finalized. Thiswill reduce the political risksbefore your CIL has madeinvestments in the venture.

HOW TO INTEGRATE THE VENTURE INTO YOUR CIL MISSION

The entrepreneurial approachallows the CIL’s advocates toanticipate the changes that takeplace to be successful. Ventureideas always begin with a mar-ket analysis within the CIL geo-graphic area and the identifica-tion of unmet or partially metneeds, ideally where the CILmay have a competitive advan-tage. Being able to draw adirect link between fulfilling theCIL mission and the operationof a for-profit venture providesthe justification for the venturewithin the CIL. In trying to iden-tify a for-profit business to pur-sue, the fundamental objectiveof increasing CIL support bymaking a profit can be refinedby the objectives of the CIL andmeeting the overall CIL mission.

As the starting point, is recom-mended that CIL staff andBoard attend a brainstormingevent to solicit input. This eventshould be a facilitated, inclusivemeeting, starting with basicquestions about the CIL’s futureand encouraging open discus-

A BUSINESS GUIDE FOR CILS

BEING ENTREPRENEURIAL

18

sion. The following series ofstarter questions might be posedto stimulate the discussion:

• Is the CIL accomplishingeverything in its mission?Or, should more be done?

• Can the CIL expect regularincreases in support, atleast large enough to meetincreasing costs?

• What attributes of anentrepreneur do the staffand Board possess?

• Is there a historical background in the CIL orstakeholders that createsknowledge within a sectoror class of business?

• Why is a for-profit venturenecessary? (By answeringthis question, your primeobjective comes into focus.)

• Within the marketplace,what specific consumer orcommunity needs are notbeing met? If the CIL were tofulfill those needs, can it bedone at acceptable levels of:

- Price?- Service?- Perception?- Risk?

• The impact of earningmoney with a businessventure may impact thetraditional CIL supporters.How will the change in theCIL be perceived, and bywhom?

• What drives the selectedmarket for the businessventure? Are there goodsor services that the CILcan offer that better meetthe needs of the community,supporters, fundingsources, consumers andcustomers?

• Are there regulatory concerns? Does the CILpropose to meet:

- Safety standards?- Labor standards?- Wage rules?- Liability questions?

• What new and existingresources and assistanceproviders can be calledupon?

- Federal, State, public, traditional and innova- tive sources?

- Can the existing business community be supportive?

19

- Other sources - governmental and private sector?

• Can the CIL’s targetedservice recipients be bene-fited by the venture?

• Does the CIL intend toremain in the business for-ever? Is an exit strategyappropriate so that a suc-cessful venture might besold off as an ongoingbusiness after the venturehas been established?

The business plan will recog-nize the objectives of the CILand anticipate the business lifecycle. Planning is actuallyorganizing change, which doesnot end with the successfullaunch and operation of thebusiness. The CIL real strategymay be to force improved oraccessible goods or servicesfrom the private sector bydemonstrating the need andviability, intending to divest thebusiness as soon as possibleand simply recoup any invest-ment. This is an exit strategy forthe business. Launching a ven-ture and planning to divest anongoing venture at a significant

profit can create a CIL reserveventure capital fund for the CIL’sfuture innovation.

Reference – See Case Study #1for additional information on inte-gration of the business idea withthe role, environment and mis-sion of the CIL and working to fitthe pieces together throughoutthe planning and implementationprocess.

Every business goes throughthe highest risk period of start-up, when the business conceptis still being proven. Sales arelow or non-existent; no rev-enues (cash) are being generat-ed to cover expenses. Unlessanticipated, this negative cash-flow situation causes tremen-dous concern among manage-ment. Detailed sales projectionsand careful attention to market-ing allows for early adjustmentsto the plan to attain targetedprojections.

As start-up proceeds success-fully, the business enters agrowth stage. Sales increase(dramatically or gradually) andmay cause similar cash flow

A BUSINESS GUIDE FOR CILS

BEING ENTREPRENEURIAL

20

problems as those experiencedduring start-up, but for very dif-ferent reasons. During growth,increasing sales require addi-tional working capital to fundsupplies and added expenses,(e.g. the timing delays of billingand collections, work inprogress, etc.). Although profits,on paper at least, are growing,the cash requirements of thebusiness may continue tonecessitate that funds areinvested in the business. Short-term borrowing is oftenrequired. As the business pro-ceeds through the growth stage,the short-term borrowingrequirements may not lessen.Ongoing growth may requireexpansion, where additionalterm borrowing matches the lifeof the expansion. Following thegrowth stage, businesses entera mature phase.

The mature business is markedby very predictable sales withonly slight growth correspon-ding to inflation or marketshare growth. During this peri-od, cash flow (income afterexpenses plus non-cash expen-ditures) significantly outpacescash expenditures and the high-

est level of surplus cash isachieved. This is usually theperiod of highest value for theventure. It may be planned totrigger an exit strategy to sellthe business at its ongoing ven-ture value, often significantlymore than the fair market valueof assets. By revising the busi-ness operation, the period oftime associated with the maturestage can be lengthened to gen-erate larger profits for extendedperiods.

Finally, businesses enter thedecline stage, where sales tendto lag behind inflation or actual-ly decline. And managementtends to cut expenses andinvestment as the only way tomaintain cash-flow margins. Atthis point, either the businesswill necessarily evolve toward anew market or cease opera-tions. The photographic industryis going through the declinestage brought on by digitaltechnology. Technological obso-lescence has become anincreasing threat to many busi-nesses in every sector. Thistechnology risk is anotherthreat that is often overlookedby smaller businesses.

21

At each stage, the business planprovides the blueprint or yard-stick by which managementevaluates progress. Early identi-fication of problems can bemade to allow for correctiveaction before the situationbecomes critical. If the businessis off-track, what should bedone? The question to ask iswhether the business is aheador behind projections.Obviously, the response varieswidely. But either condition canspell disaster. It is advisable toanticipate how external eventswill impact your business. For a CIL, public sector fundingchanges have an impact onevery program. In the businesssector, external forces can disrupt the business operationeven more. Anticipating the disruptions allows for planningthat responds to, and furtherreduces, the risk.

The entrepreneurial CIL shouldbuild a consensus amongstakeholders and focus thebusiness planning on an actualbusiness and the resources,commitments and risks associ-ated. The following chapterswill help to introduce key fac-tors involved in the planningprocess that every CIL shouldconsider. It is hoped that thereader will use this informationto successfully analyze the decisions necessary to beentrepreneurial as a CIL.

Reference – See Case Study #4 for additional information oncoordinating the business ideawith the role and resources of theCIL and doing so in the context of a quantified look at the marketplace.

A BUSINESS GUIDE FOR CILS

BEING ENTREPRENEURIAL

22

Exercise: One early step that can prove helpful is to see your (or yourCIL’s) profile as an entrepreneur and small businessperson. The follow-ing exercise was developed by the US Small Business Administration to help gauge an individual’s entrepreneurial strengths. Working withyour Board and management, think about why you would like to start abusiness and what traits you can identify that you think will help you tobe successful in business? Remember this is simply a tool. It is fun totake and fun to interpret, but keep it in perspective.

For each question, circle the Yes, Maybe or No answer that bestdescribes you and/or your CIL. You must answer ALL questions forthe test to be accurate.

Y M N I am persistent.

Y M N When I'm interested in a project, I need less sleep.

Y M N When there's something I want, I keep my goal clearly in mind.

Y M N I examine mistakes and I learn from them.

Y M N I keep New Year's resolutions.

Y M N I have a strong personal need to succeed.

Y M N I have new and different ideas.

Y M N I am adaptable.

Y M N I am curious.

Y M N I am intuitive.

Y M N If something can't be done, I find a way.

Y M N I see problems as challenges.

Y M N I take chances.

Y M N I'll gamble on a good idea, even if it isn't a sure thing.

Y M N To learn something new, I explore unfamiliar subjects.

23

A BUSINESS GUIDE FOR CILS

Y M N I can recover from emotional setbacks.

Y M N I feel sure of myself.

Y M N I'm a positive person.

Y M N I experiment with new ways to do things.

Y M N I'm willing to undergo sacrifices to gain possible long-term rewards.

Y M N I usually do things my own way.

Y M N I tend to rebel against authority.

Y M N I often enjoy being alone.

Y M N I like to be in control.

Y M N I have a reputation for being stubborn.

Count all of your Y answers and multiply time 3. Count your Manswers and multiply times 2. Add the two numbers together foryour score.

If you scored between 60 and 75, start that business plan – you havethe earmarks of an entrepreneur. If you scored between 48 and 59,you have potential but need to push somewhat. You may want toimprove some skills in weaker areas. This can be accomplished byhiring someone with these skills. If you scored between 37 and 47,you may not want to start a business alone. Look for a businesspartner who can compliment you in the areas where you need somehelp. If you scored below 37, entrepreneurship may not be for you.You will probably be happier and more successful working for some-one else. However, only you can make that decision.

Remember, this is only an exercise based on characteristics foundin many entrepreneurs. It is by no means fool proof, but it should befun and a good starting point as you evaluate your feelings aboutpursuing a business idea.

BEING ENTREPRENEURIAL

24

TAX CONSIDERATIONS: AN OVERVIEW

Note: This material is not to bedeemed wholly comprehensive or authoritative. The reader isadvised to consult with appropri-ate legal and tax counsel beforepursuing a particular course ofaction.

This section helps the entrepre-neurial CIL gain an understand-ing of the tax regulatory envi-ronment in which they are plan-ning a for-profit venture. Thissection covers broad issues oftaxation, structure, and conflictsor opportunities when the not-for-profit develops for-profitventures. It is intended to pro-vide awareness of areas inwhich CILs may need to do fur-ther research, to provide ques-tions that should be asked ingoing forward, and, to helpunderstand the implications andsignificance of a for-profit ven-ture in a non-profit environment.

Additionally, this section isintended to demonstrate thecomplex nature of the issuesand the importance of seekingqualified professional advice. Itis important to note that many

topics of taxation and account-ing in for-profit and not-for-profit ventures are subject tointerpretation and may varyfrom situation to situation. Wecannot state strongly enoughthe importance of professionaladvice.

Listed below are summaryareas and questions of generalconcern and interest to a non-profit looking at a for-profit ven-ture. Please refer to Appendix Afor more detailed informationand reference sources.

BASIC BUSINESS CONSIDERATIONS

A CIL evaluating a for-profitbusiness is searching for anopportunity that promotes theCIL’s primary mission byenhancing resources, servicesor access for its consumers. Wemust remain mindful that a CILis in an environment that placesmission fulfillment above finan-cial benefit and that a for-profitventure may conflict with thisnon-profit mission. It is impor-tant to review what the implica-tions may be for the organiza-tion with the Board, stakehold-

25

ers, supporters and staff andassess preparedness to dealwith these challenges.

Many not-for-profit organiza-tions have learned that self-reliance is a means of long-term survival, especially asmore organizations compete forlimited public funding. Toremain in sync with their pri-mary mission, some not-for-profits have developed assetsand skills that are both mis-sion-related and valuable in themarketplace. Other not-for-profits have chosen unrelatedventures for more purely com-mercial opportunities, opting topursue the mission throughenhanced resources. It isimportant to structure whichev-er for-profit opportunity is cho-sen in such a way as to notinterfere with the not-for-profitstatus of the CIL.

Throughout the evaluation andplanning process, a major con-sideration to keep in mind isthat the rules at the federal andstate level that demand strictadherence to primary organiza-tional purpose over personalenrichment. This requires aclear separation between for-

profit and not-for-profit activi-ties. The separation must bereal and the activities on bothfronts must be reasonable intheir respective context.

The CIL should consider thereporting, filing and disclosurerequirements of the non-profitentity because these may com-plicate the ability to maintainconfidentiality of trade secrets,know-how and similar competi-tive information. Clear separa-tion of activities and roles canminimize this challenge.

CILs should be aware that dis-closure of information couldlead to incorrect public percep-tions, which may raise addition-al questions. For example, "Was‘public’ money used to begin thefor-profit venture?" Is the publicbenefit entity ‘competing’ withprivate sector suppliers with theassistance of tax dollars?"

Exercise: Set a meeting with key leaders of your CIL to discussaccess to qualified professionalassistance, the for-profit oppor-tunity in terms of community per-ception, which will the for-profitbe competing with, and, develop a list of the short- and long-term

A BUSINESS GUIDE FOR CILS

BEING ENTREPRENEURIAL

26

pros and cons to determine howthe benefits will outweigh therisks.

TAX CONSIDERATIONS

The following section identifiessome of the basic conceptsneeded to frame your questionsabout the tax-related restric-tions and examples appropriatefor CILs. These items are cov-ered in greater detail in IRSPublication 598 which also cov-ers he Unrelated BusinessIncome Tax (UBIT).

PROHIBITION AGAINST PRIVATE INUREMENT (PERSONAL BENEFIT):

The prohibition against privateinurement means that the per-son(s) who created or control atax-exempt organization,including its members, employ-ees, and other insiders, may notacquire any of its funds orassets, except when:

• They are paid "reasonablecompensation," or relatedexpenses, for services rendered; or

• They pay an amount equalto the "fair market value"of any of the organization’sassets they may receive.

LOBBYING ACTIVITIES

A for-profit organization mayexpend significant resourceslobbying various levels of gov-ernment to achieve preferences.Unfortunately, the not-for-profitis governed by IRC Sec. 501 (c)(3) which prohibits lobbyingactivities and can result in theimposition of an excise tax ifnot-for-profit funds are expend-ed for lobbying purposes.During planning, ascertain iflobbying or advocacy by the CILwill be an essential componentof your for-profit success.

Not-for-profit organizations areallowed to provide educationalinformation and respond to gov-ernmental inquiries without vio-lating the law. If CIL manage-ment has questions in this area,they are encouraged to seekclarification from legal counsel.Serious violations can result inloss of the CIL’s 501(c) (3) tax-exempt status, termination ofcertain officers or directors, ora variety of other sanctions.

27

QUID PRO QUO CONTRIBUTIONS

In business, there are limita-tions on business-relatedexpenses, such as meals andentertainment expenditures,sporting events and other formsof market or client develop-ment. The for-profit can spendlarger sums of money treatinggifts as taxable income to therecipient, and adding the grossamount of the benefit(s) to taxwithholdings. However, there isno requirement of public disclo-sure. A CIL may entertain bene-factors, but there are con-straints dealing with excessiveentertainment and mandatorydisclosures.

A business can only deductactual gifts in under $25 unlessthe recipient reports the excessas taxable income, but there isno public disclosure.Conversely, a CIL must disclosethe value of any benefits, otherthan incidentals, which arereceived by contributors inexchange for donations. This isan example where scrutiny anddisclosure requirements arehigher for the CIL and may

adversely impact businessopportunities, while furtheringthe need for accurate CILrecord keeping.

UNRELATED BUSINESSINCOME TAX (UBIT)

UBIT is applicable to a non-profit entity that has earnedincome unrelated to its primarypurpose. IRC Sec. 513 (a)defines an unrelated trade orbusiness as any trade or busi-ness not substantially related tothe exercise or performance ofthe organization’s exempt sta-tus. When a CIL has an incomeopportunity, it may not auto-matically need to set up a for-profit organization. When a newbusiness develops, it may besmall enough to handle withinthe CIL without serious tax-related consequences to thenot-for-profit structure. Thismight correspond to the earlystages of a business ventureand provide a try and see win-dow for exploring a businessopportunity. This is an area ofwide interpretation and profes-sional advice should be securedbefore proceeding. Additionally,the IRS website at

A BUSINESS GUIDE FOR CILS

BEING ENTREPRENEURIAL

28

http://www.irs.ustreas.gov/businfo/eo/unrel.html offers somediscussion on the definition anddetermination of the UBIT.

The concept of UBIT should notbe automatically viewed as animpossible hurdle for the CIL,which is seeking to protect itstax-exempt status and enhanceeconomic viability. However, theofficers and board membersshould be cognizant of thepotential problems and addressthe issues as part of the overallbusiness plan.

BUSINESS STRUCTURE AND LEGAL FORM

Based upon these decision-making tools, the CIL mustdetermine the most favorablelegal structure in which to growand manage the for-profit business.

Typically, a CIL could start abusiness as the equivalent of asole-proprietorship if the devel-opment of a profitable conceptarises from the normal activi-ties and services provided bythe CIL. This approach does notoffer the goal of having the

for-profit business operating as a separate legal entity. As asole proprietorship, the CIL isexposed to all of the risks andtax implications associated withthe new business. While con-venient, this approach is notgenerally recommendedbecause of the risk to the CIL.

One of the significant elementsof selecting a business struc-ture is risk management.Though many of the specificrisks of the new activity can beaddressed by proper insurancecoverage, the development ofmanagerial controls, systems,and accounting can addressoperational exposure areas. Inmany cases, it is advisable forthe new business to be segre-gated from the CIL for legal lia-bility. This can be done througha limited liability company(LLC), which limits the riskexposure of the CIL. This willnot protect the CIL from tax andUBIT rules, private inurementor general disclosure. It doesprovide a ‘corporate-like’ pro-tection.

There are several forms of busi-ness that may make sense inany situation. This is an area

29

that requires professionaladvice to assure the correctchoice.

THE CIL "CONTROLLING" A NOT-FOR-PROFIT (NFP)

If the business is an acceptableactivity, the CIL may isolate theactivity within another newlyformed entity within the lead orparent not-for-profit, providingoversight through an element ofcommon leadership. However,the Boards of Directors shouldnot be identical, nor should thesenior management.

Exercise: Spend some time withthe current leadership of the CILto discuss and identify skills andtalents among existing leadershipthat may be useful to a for-profitentity. Seek to identify key man-agers and board members thatmay be sought to augment one or the other (but not both).

Reference – See Case Study #1for additional information on howthe skills and resource base thatis currently available can providea good jumping-off point for thebusiness idea.

THE CIL WITH A FOR-PROFIT C-CORPORATION SUBSIDIARY

In situations where a CIL ownsa controlling interest in a for-profit corporation, care shouldbe taken during start-up thatthe for-profit is not simply analter ego of the CIL, and shouldbe combined for the purpose ofdetermining the entity’s tax-exempt status. Barring fraudu-lent or sham transactions,where the parent is not involvedin day-to-day activities of thefor-profit, or where the officersand Boards of Directors are notidentical, the IRS will respectthe separate identities.

It is important to have good sys-tems in place to properly allo-cate joint costs, such as in ashared space facility, or to havean appropriate interest rate setfor loans from the parent to thefor-profit subsidiary, or to setpricing or rates (like rent) at fairmarket values.

Exercise: Many CILs administergrants and similar incomestreams with fairly complexaccounting systems in place.Meet with your internal andexternal accounting professionals

A BUSINESS GUIDE FOR CILS

BEING ENTREPRENEURIAL

30

to determine if the existing sys-tems can handle the requisiteseparation. Determine any new or enhanced accounting softwareor systems that may be requiredto meet IRS regulations.

THE CIL WITH AN S-CORPORATION SUBSIDIARY

A CIL may elect to utilize an S-corporation as the for-profitentity. Though generally seen as a bad idea (earnings of theS-Corporation, which are attrib-utable to a tax-exempt organi-zation, are automatically treatedas UBIT income), you shouldconsult professional advisorsbefore making this determina-tion.

THE CIL AS A PARTNER IN APARTNERSHIP (INCLUDINGLIMITED PARTNERSHIPS)

The IRS takes a negative posi-tion on partnerships where anot-for-profit is a significant ormanaging partner. One keyexception occurs in cases wherethe not-for-profit’s role wasstrictly passive and not contrary

to the not-for-profit’s primaryobjective, as might be the casein an arms-length investmentpartnership.

FINANCIAL STATEMENT ANDDISCLOSURE CONSIDERATIONS

The American Institute ofCertified Public Accountants(AICPA), the FinancialAccounting Standards Board(FASB) as well as several othersources promulgate the rulesby which books and records arekept. When a CIL reports infor-mation in financial statements,the information must meet cer-tain standards to be useful toreaders and meet regulatoryrequirements.

A CIL involved in a for-profitactivity needs to understand therequirements and limits of dis-closure and reporting in orderto present accurate informationand proper disclosure while notdivulging trade secret informa-tion, such as marketing or pro-duction costs. Professionaladvice is a key element of yourdecision making process.

31

THE BUSINESS PLAN: THECIL’S PRIMARY BUSINESS COMMUNICATION

The CIL must develop thestrategic business plan – theroad map for the business. CILstakeholders should be assistedin evaluating the business ideaor concept, asked to define cus-tomer characteristics, help for-mulate a marketing strategy,evaluate operations and beginto project basic financial andperformance data for the ven-ture. The process of goingthrough these steps is impor-tant for the successful launch ofa business, and it may be theonly way for a CIL to ensure keystakeholder buy-in as supportof the business.

WHY DOES A CIL NEED ASTRATEGIC BUSINESS PLAN?

A good business plan encour-ages research that allow theCIL to draw conclusions andplan in response to those con-clusions, helping fix mistakesbefore they happen to the busi-ness. It helps to identify thestrategies and implementationtactics that are most likely tosucceed in the CIL’s venture,

select products, services andmarkets that can be accessedand supported, and gives allmembers of the organizationthe information necessary tomove toward a common goaland success. If a CIL stakehold-er wants to advance the missionof the CIL through a businesssubsidiary, the CIL must be pre-pared to manage and organize abusiness effectively. The busi-ness plan is the best way todevelop the venture at reducedacceptable risk, set targetedgoals and measure progress.

A good strategic business planfocuses on markets for a prod-uct or service, anticipates futureneeds, monitors progress and isproactive - not reactive - inmanaging resources.

A good strategic business planprovides a valuable manage-ment tool which integrates allfacets of the operation -whether profit or non-profit.

A good strategic business plandefines where you are, antici-pates where you are going, andhow you are going to get there,encouraging everyone in theorganization to work together.

A BUSINESS GUIDE FOR CILS

BEING ENTREPRENEURIAL

32

Reference – See Case Study #1for additional information on howthe CIL anticipated the impact ofspace availability on the futurebusiness operation – and plannedthe solution!

If you have never prepared abusiness plan before, this work-book will help you. The ques-tions, outlines, exercises andsamples presented cover how togather information and assem-ble the plan.

The next step is to share thedata across the organizationand focus upon the outcomesneeded or desired. The processof planning allows key CILstakeholders to analyze thestrengths and weaknesses ofthe business idea, identify mar-ket opportunities, anticipatemarket changes and detail theactions required to reach goals,while allowing the CIL to drawon the expertise and strengthsof stakeholders through a par-ticipatory process of knowl-edgeable buy-in.

The first step to a good plan isto develop a Summary. This

short, one page document,takes the broad view of theissues and invites contributionsfrom all levels of the CIL. Bysimplifying the planningprocess, it enables the team toquickly make an assessment ofthe business concept.

Exercise: Develop a simpledescription of the business ideaand key outcomes. For example,the CIL wants to purchase thebuilding currently being rented.

The purposes are to:

a) Reduce cash outlay currentlyused for rent through offset withrental revenue,

b) Create an equity resource toimprove long-term financial sta-bility of the CIL, and,

c) Provide a more flexible realestate environment that will allowfor programmatic expansionand/or contraction in response toclient needs and business activity.

Then, review this statement withkey leaders of the CIL, as thisstatement will essentiallybecome the overall strategy andgoal statement of the project.

33

The next step is to develop thedetails, incorporating feedbackfrom the more extensive plan.The plan is eventually going tobe a complete statement of thebusiness operation and almostlook like a book. Each chapterof the book is a specific plan initself - the marketing plan,sales plan, finance plan, opera-tions plan, and the underlyingdata to support each strategy,tactic and business action.

STRATEGIC BUSINESS PLAN –EXECUTIVE SUMMARY

The one page ExecutiveSummary is an overview of thebusiness. It is a brief descrip-tion that sets the vision, theimplementation and the out-come into one easy to under-stand statement. After readingthe Executive Summary, thereader should understand whatthe CIL wants to do, how theCIL will do it and how the CILwill define success.

While the Executive Summarycan be written last (after com-pleting the nine key areas iden-tified below and after complet-ing the financial projections), it

is preferable earlier in theprocess. The summary high-lights the key ideas of the plan,the measurement of success,competitive advantages andlinks all of the facets of the ideato help the reader understandthe plan without significantexplanation from individualsassociated with the CIL.Approach the Summary as astatement of the business, iden-tify issues or opportunities, andtry NOT to spend more than anhour writing them down. Thisinitial Summary is only meantto communicate the preliminaryvision. The details will beworked out over time.

Take action, share the Summarywith key CIL stakeholders, andinvite their reaction and involve-ment in the Business PlanDevelopment Team (or whatevercatch phrase you prefer). Ifstakeholders do not respond,reach out to them and press fora response. Remember that anegative response early is muchbetter than later on, after theTeam has committed resourcesto the detailed plan. This earlybuy-in through participation ispresented as critical to CIL suc-cess in entrepreneurial activities.

A BUSINESS GUIDE FOR CILS

BEING ENTREPRENEURIAL

34

Exercise: After you have com-pleted the preliminary work oneach section, try to summarizeeach section in one or two sen-tences. Establish the flowbetween sentences or strategies,demonstrating the connections.Try to establish the overall logicand reason of the plan. For example:

"The CIL will establish a whollyowned subsidiary LLC to pur-chase the 30,000 square footbuilding housing 12,000 squarefeet of CIL offices and programspace. The key objectives of thiseffort will be to reduce rentalcost, build equity and increasefacility flexibility."

"There is strong demand fromarea professional services firmsfor small offices with parking andtransit access. We plan to provideconventional rentals and ‘sharedservices’ space, utilizing existingCIL office systems such as voiceand data communications. Thereis a shortage of this type of spaceand service offering in the areawith most facilities showing bet-ter than 95% occupancy."

"Marketing and sales will be han-dled by a new Facilities Manager.

We will develop market aware-ness through close contacts withour stakeholder community andsmall firms offering services toour client base, which is currentlymore than 35 service providers inthe legal, therapeutic and supplysectors. As a single facility, thenew Facility Manager will overseeday-to-day operations includingbuild-out, usage, utility billing,signage, etc. The new positionwill report to the CIL ExecutiveDirector, to the CIL FinanceDirector for fiscal oversight andto the CIL Board for periodicreporting."

"The purchase price of the build-ing is $1,250,000, and an addi-tional $250,000 for first yearoperations and build-out of rentalspace, for a total of $1,500,000.Key factors in our financial planare a $125,000 cash contribution,15 year commercial financing at6%, rental charges at $12 perfoot (the current local marketsupports $13-$15/foot) and a75% first year occupancy of the18,000 square feet we do not nowoccupy. This will produce rentalrevenues of $13,000 per month inthe first year, and, at 85% occu-pancy in the second year produc-

35

ing slightly over $15,000 permonth. Allowing for an $11,600monthly mortgage payment andoperating costs of $5,000 permonth, we should close the yearat a net monthly cash loss of lessthan $2,000 – an $8,000 improve-ment over our current rentalexpense. When we achieve 90%occupancy in year 3, we moveinto a positive monthly cash flowof $1,500. In addition, we will besaving $120,000 in annual rentalexpense."

"This plan details the resources,usage and integration of the pur-chase of the building, the impacton cash flow and the benefits toour CIL. Essentially, this plantakes our CIL from an annualexpense of $120,000 to an annualgain of $138,000. This is a signifi-cant resource improvement thatwill be used to further the mis-sion of the CIL and the services to consumers."

BUSINESS DESCRIPTION

The Business Description is a short statement of what thebusiness is and what it does. In a concise manner, describethe business.

Example: The CIL Real EstateLLC is a corporation establishedto acquire and operate the officebuilding at 123 Main St.,Smithville, NY. Up to 40% of thefacility will be occupied by theCIL, up to 25% will be structured,rented and operated as a ‘sharedservices’ office facility offeringvoice, data and systems accessfor tenants, and, the remaining35% will be structured as rentaloffice space targeted to profes-sional service firms with marketinterests among the client baseof the CIL. The overall aim of theReal Estate LLC is to reduce theoperating expense of the CIL,build long-term equity and sup-port the services of the CILthrough contribution of profit andexpense reduction.

MARKET ANALYSIS

The Market Analysis describeswho the customers are. Howmany customers are out there?What are the characteristics interms of size/age, location orcommon traits? How can theybe identified (e.g., by industry,by size, etc.)? Is the product orservice available from othersources? How big is the mar-

A BUSINESS GUIDE FOR CILS

BEING ENTREPRENEURIAL

36

ket? How much is spent by cus-tomers? What are the past, cur-rent and future market trends?Is the market segmented (bro-ken down by characteristics likecolor or material)? Is the mar-ket a commodity (everything isseen as the same)? Is it cus-tomized and unique? What isthe geographic area of the mar-ket? What part of the entiremarket will the business target?

1) Market Size - Present figuresand factual information on thesize of the market for yourproduct or service. Obtainingnumbers may seem difficult,but the effort will be worth it.Programs like the SmallBusiness Development Centercan help you find sources ofinformation and, in some cases,conduct original marketresearch. Be sure to includeinformation on the following:

a) How much is being spent onthe product or service (by allcustomers)? Or, if the product isnew, how much is being spent onalternative products or services?

b) Is the market expanding orcontracting? At what rate?

c) How is the market changing?Define the characteristics thatare changing?

d) Where will the market be infive years? How much will cus-tomers be spending? Will popu-lation or age projections showan impact on the future of themarket?

2) Market Profile - Describe theexisting or potential customersfor your product or service.Expand on the information inthe Business Description sec-tion. This expanded detailshould include:

a) Who will buy? If customersare individuals, what are theircharacteristics such as; age,income level, education, familystatus, etc. (customer demo-graphics)? How many cus-tomers are there? If customersare businesses, what kind ofbusinesses? What do they havein common? What size(s) arethey? Are products branded orprivate label, etc?

b) Where are customers? Arethey located in a particularregion or area? Describe thecharacteristics of the region as

37

it may relate to your products,e.g., if your business makeswinter coats, your customersare principally in colder regions.

c) Why will the product or serv-ice be purchased? Expand onthe customer need that theproduct or service meets andwhy the customer will selectyour product over a competitivechoice. Will your product bettermeet a feature or benefit need?For example, with athleticfootwear, Velcro brand closuresare a feature. But if the sneak-ers make you jump higher andrun faster, that is a benefit. Theperception of a benefit can beas important in the marketplaceas an actual benefit.

d) When will the product orservice be purchased? Is it sea-sonal and, if so, what is the sea-sonal aspect? Does it tie in withother products or events? Isthere a limited timeframe forthe product?

e) What is the customer expec-tation for the product or servicein terms of price, quality, serv-ice, delivery, packaging, etc.?

Reference – See Case Studies#1 and #2 for additional informa-tion on how the market data wasdeveloped, how additional costeffective resources were broughtin and how the data are used tosupport the decisions in theBusiness Plan.

Exercise: Review some numbersfor the potential customers ofyour product or service. Remember,this is the time to be as quantita-tive as possible.

Smithville, NY, has seen robustgrowth in recent years in demandfor office space. According to theReal Estate Reference Co. annualsummary of office space statis-tics, Smithville has grown from650,000 square feet of primeoffice space to more than1,000,000 square feet over thelast 5 years. Rental rates havekept pace with this growth inavailable space, rising from anaverage of $9/sq. ft. to $14/sq. ft.over the same period. A signifi-cant component of this growthhas been in ‘shared services’ -space that is rented ready to use,equipped with phone systems,computer networks and datacommunications, access to

A BUSINESS GUIDE FOR CILS

BEING ENTREPRENEURIAL

38

conference rooms, a receptionarea and similar attributes. Thistype of space has been extremelypopular among professional serv-ices firms seeking access to larg-er facilities than might otherwisebe cost effective. Long-termgrowth prospects are attractive,with Ollie’s Office Space Monthlyquoting industry experts asexpecting 7% - 10% annualgrowth in this segment over thenext 10 years.

The market for small to mediumsized office space (1,500 – 3,500sq. ft.) has shown excellent sta-bility, with moderate growth overthe last 10 years in the Smithvillearea. The new number of leasesreported by Lisa’s Leasing Statshas shown consistent, moderategrowth, averaging 5% annually,over a 15 year period with fluctu-ations of less than 2 percentagepoints a year.

This space is frequently rented tolarger service providers in themedical, legal and technicalareas. According to statisticsfrom the NYS Dept of Labor, thenumber of service providers inthese segments continues togrow. It is anticipated that thisgrowth will continue on a long-

term basis. The growth shows adirect relationship to the aging ofthe population – a trend that theUS Dept of Commerce indicateswill be continuing for the next 33years. Given the natural linkbetween these medical providersand our client base, we will tar-get the 173 medical practices,with more than 3 physicians,located within 75 miles ofSmithville as our market of rentalcustomers. Add to this marketsize estimate the average 3 newsimilar medical practices beguneach year, and a sustainablemarket for space is projected.

PRODUCT OR SERVICE ANALYSIS

This is where you must presentevidence to prove (and to con-vince the reader) that there is aneed for the product or service– and that there is sufficientdemand to support the businessproposed. It is not enough to believe in the product orservice, it must be shown.This section must:

First, identify the need for the product or service,

39

Second, show how the product or service meets thatneed, and

Third, show how to sell theproduct or service at a profit.

Exercise: Working with the keyproponents of the businessidea: Describe what the productor service is and why customerswill purchase it. What are thefeatures or benefits of the prod-uct or service that are betterthan the competition (e.g., bet-ter quality, cheaper, faster, andsofter)? What need does theproduct meet for customers?How does the product or servicesatisfy demand? Is the productprotected by a patent or otherexclusive contract? What makesthe product unique – is it brandedor private label?

COMPETITION

Identify the companies that pro-vide a similar or an alternativeproduct or service. Be sure notto overlook competition fromoutside the area. Describethese competitors in terms ofimportance, size, location, tar-

get market, distribution or othercharacteristics. This sectionworks well as a chart.

Remember: A good place tostart this research is the localyellow pages in the telephonedirectory and/or industry cata-logs. Describe all identifiablestrengths and weaknesses,such as competitor #1 has alarge dedicated sales force, #2has no local service site, etc. Donot forget to evaluate how thecompetition operates:

• What is done right andwhat is done wrong?

• What appears to be thecompetitor’s strategies inmarkets, sales and opera-tions?

• Is there a competitiveweakness that your busi-ness can improve upon andexploit?

• Is the market large enoughfor an additional businessor will an existing businessbe forced out of the market?

• Can a new business sur-vive long enough to effec-tively compete?

A BUSINESS GUIDE FOR CILS

BEING ENTREPRENEURIAL

40

Describe the companies andproducts that are the competi-tion. Do not forget to includeimports if they are a factor inthe market. Remember, evennew products have some type ofcompetition. For example, if thebusiness will be selling cashregisters, a look at personalcomputers would be appropri-ate as competition as a similarpoint-of-sale data processingequipment.

Exercise: Work with the leadersand managers of the product toidentify the direct and indirectcompetition. Include the followingand limit detailed analysis to thetop 5 or 6 competitors:

How many companies will becompeting against the business?Where are the businesses locat-ed? How long have they been inbusiness? How does the competi-tion distribute the product orservice? What is the respectivemarket share? What are thestrengths and weaknesses inmarketing, operations andfinance, of competitors? And whatare their strategies? How doesyour product compare in terms of price, quality, service, design,delivery or other features? Do you

intend to take market share awayfrom the competition or will yoube creating a new, niche market?

Some of this information mayseem difficult to obtain, but getas much reliable data as possi-ble so you know the competi-tion. Start research with readilyavailable tools, like the tele-phone book yellow pages, cata-logues, sales literature, indus-trial and commercial directo-ries, libraries, trade associa-tions, etc. This section is oftenset up as a chart or table/matrixlisting the same categories foreach competitor and highlight-ing the weaknesses or missedopportunities.

MARKETING STRATEGY

This section describes how toreach customers and salesgoals. Think of why customerswill choose your business overthe competition. Identify anddescribe how to get sales by answering the followingquestions:

How will specific markets bereached through advertisingor promotion?

41

How will you price the productor service?

How will the product or serv-ice be distributed?

For example, will sales bethrough retailers, by direct mail,sales representatives, regionaldistributors, and sales people?How will promotion be handled– a brochure or data sheet,radio/television, etc.? Whereand when will advertising takeplace? How much will be spenton advertising? Will you have a market niche that can be targeted at less cost? How will service policies affect marketing?

This is the section where youintegrate and assess the mar-ket, the competition, your capa-bilities and how to set the prod-uct or service apart from theothers. The following are impor-tant elements to consider whendeveloping the strategy: trendsin the market, competitivestrengths and weaknesses,voids in the market, marketniches, technology, lower costs(production or sale), advertising,public relations, promotions,quality, and service.

Reference – See Case Study #4for additional information on theimportance of looking beyondyour assumptions at additionalmarket areas using numericmodels and quantitative measures.

Be sure to address each of thefollowing areas:

Product Features - Review thefeatures of the product thatmeet the needs or demands ofthe marketplace. Discuss howthose needs are met. Describerelated features and design ele-ments such as: How the productwill be packaged in terms offunction and promotion. Doesthe package need to preserve,protect or display the product(or all three)? Is shipping a con-cern? Are there environmentalconcerns or concerns by theretailer or final seller of theproduct? How will the labelaffect the product?

In addition to promotional infor-mation, are there regulatoryconcerns for label content (e.g.,ingredient lists, nutritional data,warnings, directions, UPCcodes, UL listing, ISO 9000,etc.)? How will you register and

A BUSINESS GUIDE FOR CILS

BEING ENTREPRENEURIAL

42

use trademarks and identifyingimages? Discuss the plan todevelop, establish and protectthe image. Remember: if it isunprotected and can be used byanybody entering the market.What is the investment worth?

Warranty terms are sometimesa critical purchasing decisionpoint. What will the warrantyterms be, why, and, what doesthe market expect? Service maybe another significant purchas-ing decision point. What will theservice policy be and how will itimpact the business?

Pricing - Price can be the keyelement in a marketing strategyand must be carefully thoughtout. Several price developmenttheories exist that may apply.Consider the following: How willthe price relate to the cost ofthe product? How will pricerelate to the cost of marketingand promotional efforts? Is dis-counting required in the mar-ketplace? How will the pricecompare to competitive prod-ucts? Is the difference worth it?How will the price relate towhat the market is able andwilling to pay? Products target-

ed for price sensitive or low-endmarkets cannot succeed at ahigh price. How will the pricingstrategy enable the objectives tobe achieved? How does pricerelate to the distributionmethodology? Is multi-tier pric-ing required? What will theimpact of retailer/distributormarkups be? Will these add-ons make the product tooexpensive?

Distribution - Describe howyour product gets from you tothe customer and how thatrelates to marketing methods.Consider the following: Whatare the available methods fordistribution (e.g., direct salesforce, distributors, retailers,mail order) for similar prod-ucts? What are the methodsused by your competition? Willyour method be different? Why?Can this differentiate your prod-uct? If you use a direct salesforce, how large will it be? Whatwill sales representative growthrate be? How will salespeoplebe compensated? And, whatexpenses will you incur beyondsalaries? If you use dealers ordistributors, how many do youneed? Where will they be? How

43

will you determine these factors(e.g., geographically, demo-graphically, logistically)? Andhow will you hire them?Describe, in reasonable detail,how the distribution method willsupport your strategy and reachyour objectives.