Embed Size (px)

Citation preview

Bellringer

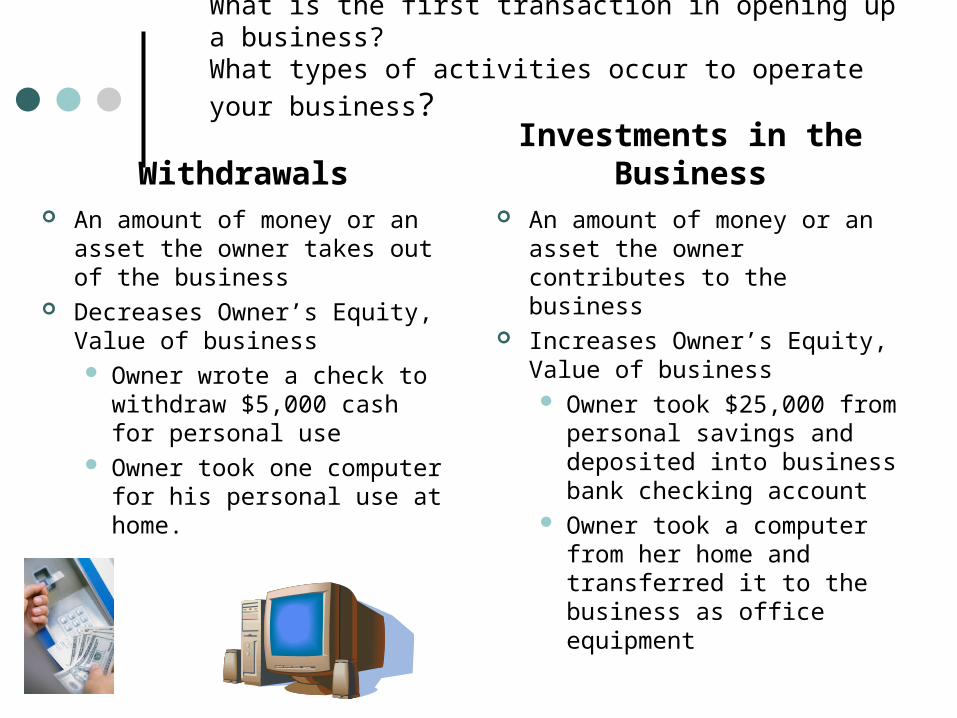

What is the first transaction in opening up a business?

Why do people start a business? What types of activities occur to

operate your business? How do businesses survive or stay in

business? Write down on a piece of paper…

Essential Questions

Why do revenue, expenses, and owner’s withdrawals affect owner’s equity?

How are they a part of the accounting equation?

How do you analyze transactions that relate to revenues, expenses and withdrawals?

Enduring Understanding

Revenues and Expenses and withdrawals are temporary accounts. They start each new accounting period with -0- balances.

Students will be able to:

Describe the purposes of the revenue, expense and drawing accounts and illustrate their effects on owner’s equity.

Compare and Contrast Temporary and Permanent accounts.

Explain the double-entry system of accounting and apply debit and credit rules when analyzing business transactions.

Why do people start a business?What types of activities occur to operate your business?

Revenue income earned from the sale of goodsIncreases owner’s equity, the value of

your business

What types of activities occur to operate your business?How do business’ survive or stay in business?

Expenses cost of products or services used to

operate a businessDecreases owner’s equity, the value

of your business

What is the first transaction in opening up a business?

What types of activities occur to operate your business?

WithdrawalsInvestments in the

Business An amount of money or an

asset the owner contributes to the business

Increases Owner’s Equity, Value of business Owner took $25,000 from

personal savings and deposited into business bank checking account

Owner took a computer from her home and transferred it to the business as office equipment

An amount of money or an asset the owner takes out of the business

Decreases Owner’s Equity, Value of business Owner wrote a check to

withdraw $5,000 cash for personal use

Owner took one computer for his personal use at home.

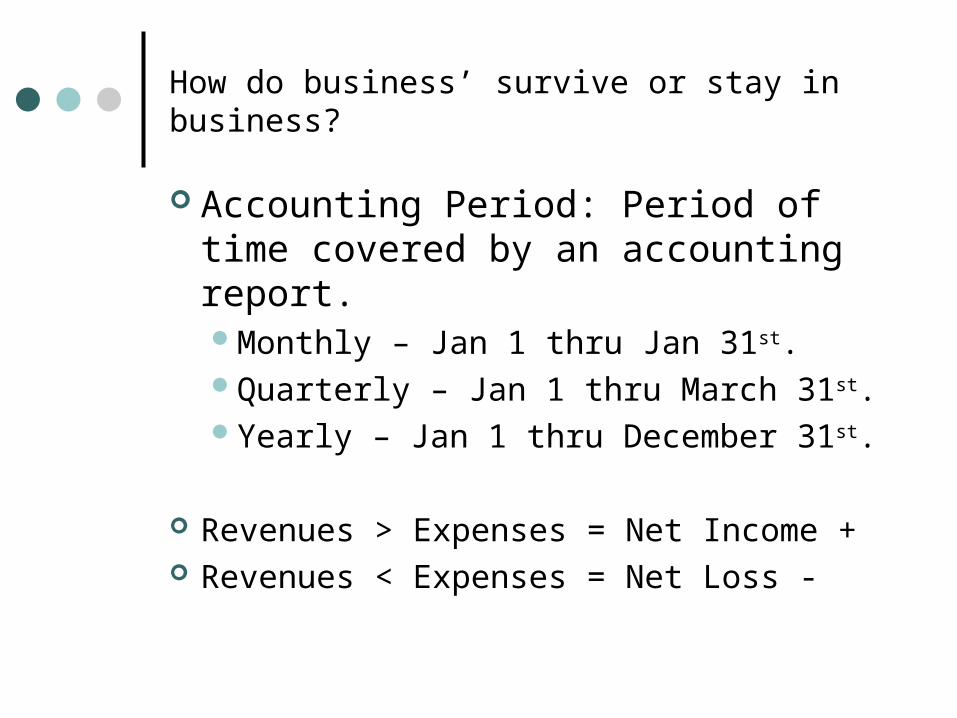

How do business’ survive or stay in business?

Accounting Period: Period of time covered by an accounting report.Monthly – Jan 1 thru Jan 31st.Quarterly – Jan 1 thru March 31st.Yearly – Jan 1 thru December 31st.

Revenues > Expenses = Net Income + Revenues < Expenses = Net Loss -

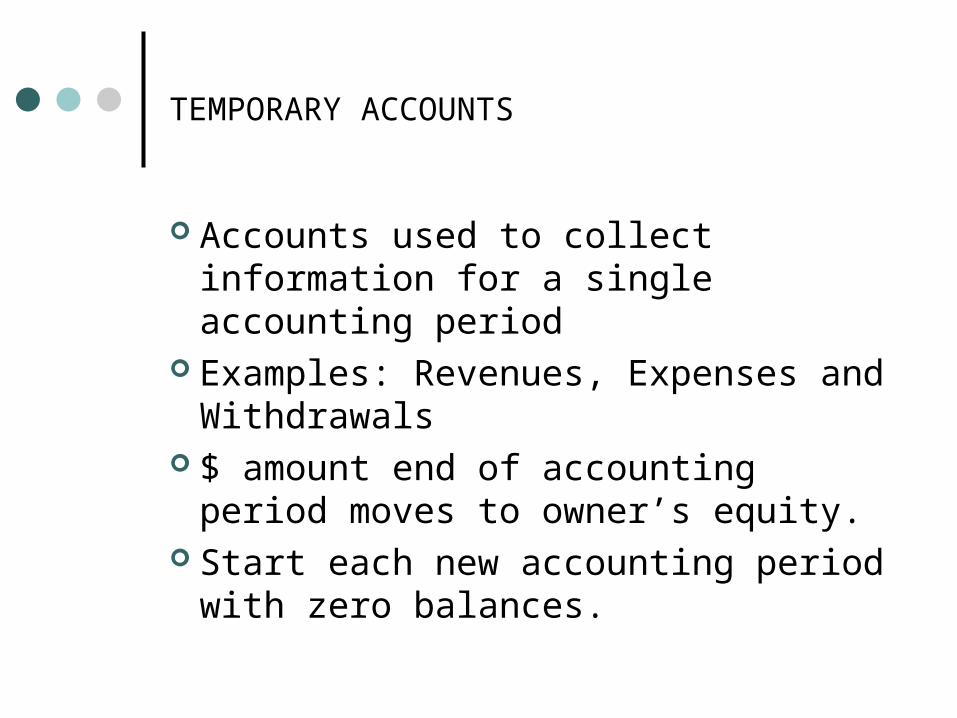

TEMPORARY ACCOUNTS

Accounts used to collect information for a single accounting period

Examples: Revenues, Expenses and Withdrawals

$ amount end of accounting period moves to owner’s equity.

Start each new accounting period with zero balances.

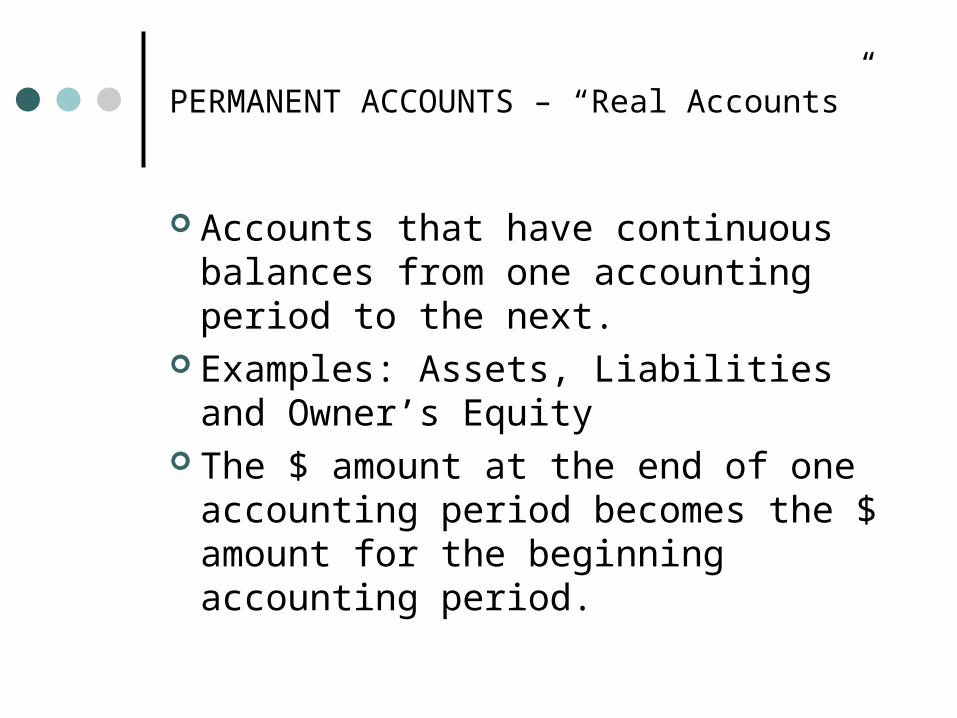

PERMANENT ACCOUNTS – “Real Accounts”

Accounts that have continuous balances from one accounting period to the next.

Examples: Assets, Liabilities and Owner’s Equity

The $ amount at the end of one accounting period becomes the $ amount for the beginning accounting period.

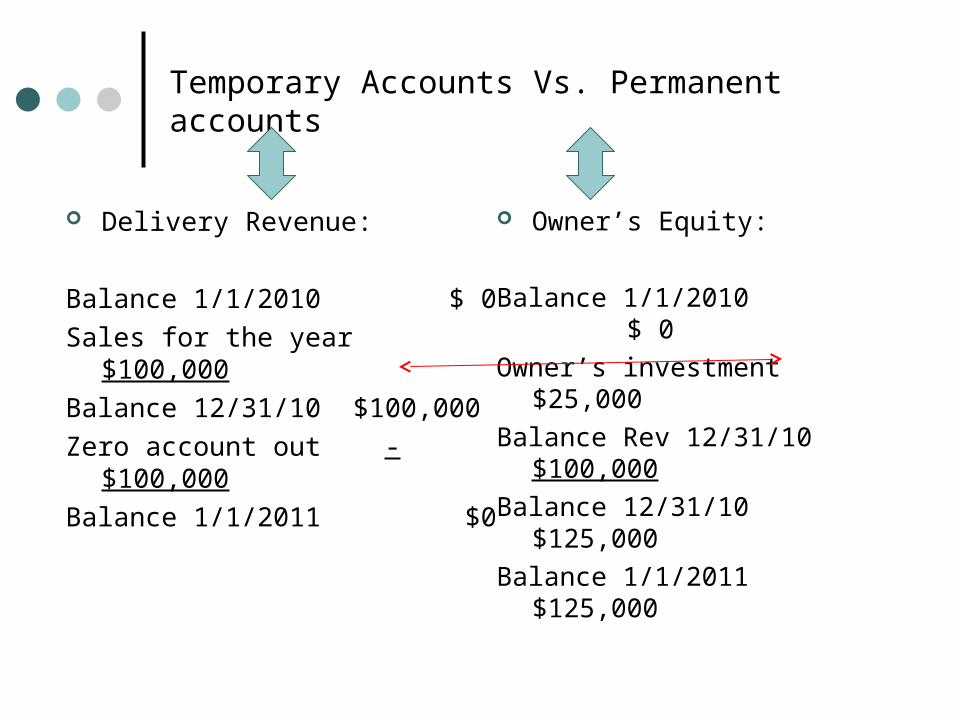

Temporary Accounts Vs. Permanent accounts

Delivery Revenue:

Balance 1/1/2010 $ 0

Sales for the year $100,000

Balance 12/31/10 $100,000

Zero account out -$100,000

Balance 1/1/2011 $0

Owner’s Equity:

Balance 1/1/2010 $ 0

Owner’s investment $25,000

Balance Rev 12/31/10 $100,000

Balance 12/31/10 $125,000

Balance 1/1/2011 $125,000

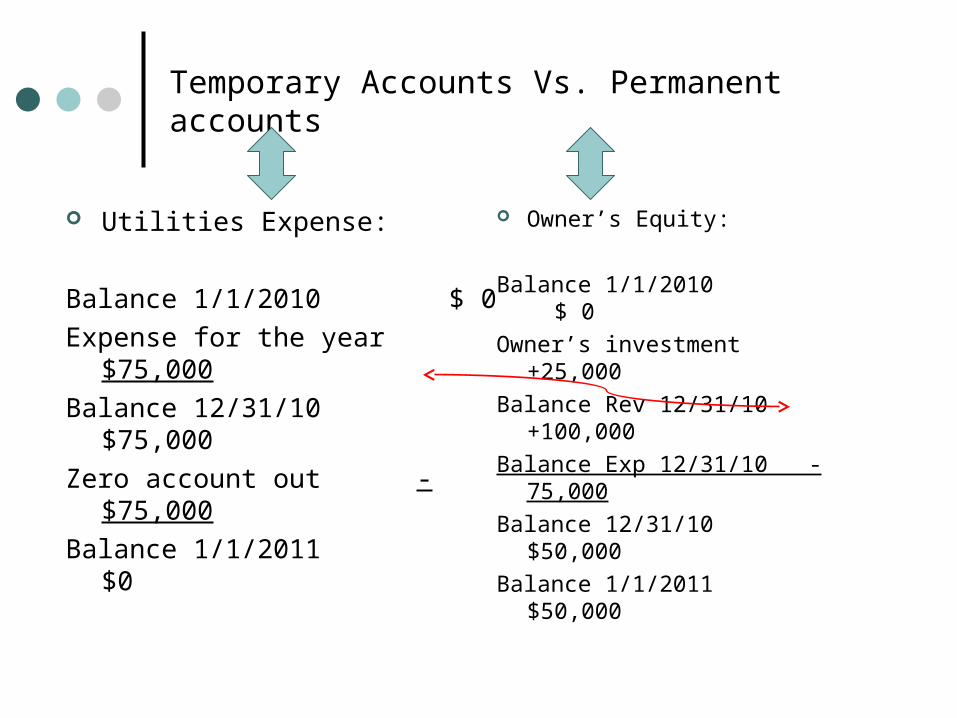

Temporary Accounts Vs. Permanent accounts

Utilities Expense:

Balance 1/1/2010 $ 0

Expense for the year $75,000

Balance 12/31/10 $75,000

Zero account out -$75,000

Balance 1/1/2011 $0

Owner’s Equity:

Balance 1/1/2010 $ 0

Owner’s investment +25,000

Balance Rev 12/31/10 +100,000

Balance Exp 12/31/10 - 75,000

Balance 12/31/10 $50,000

Balance 1/1/2011 $50,000

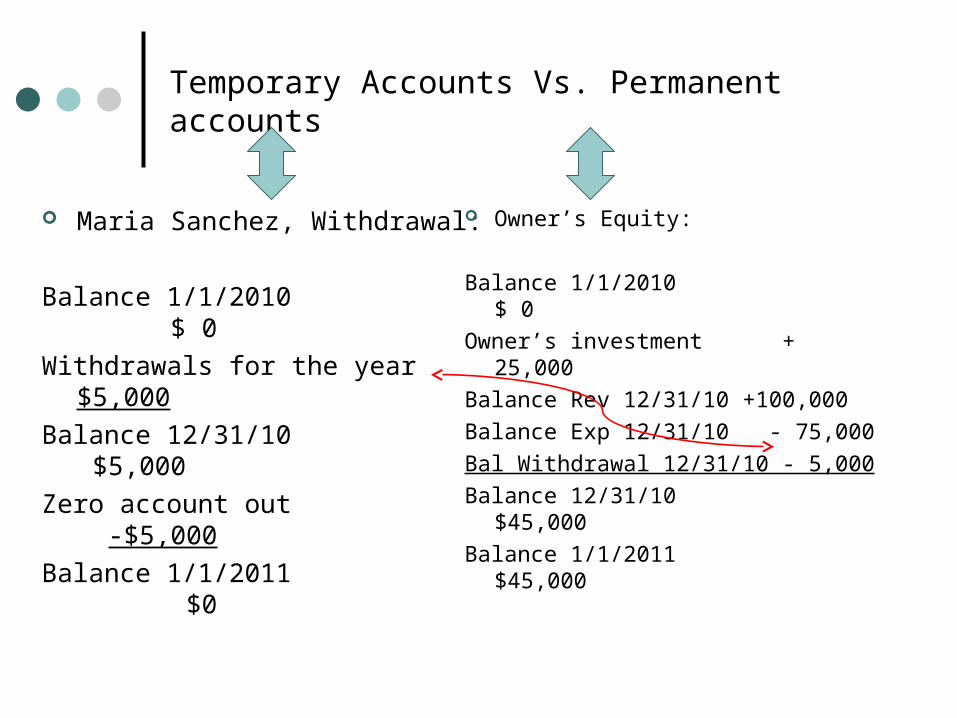

Temporary Accounts Vs. Permanent accounts

Maria Sanchez, Withdrawal:

Balance 1/1/2010 $ 0

Withdrawals for the year $5,000

Balance 12/31/10 $5,000

Zero account out -$5,000

Balance 1/1/2011 $0

Owner’s Equity:

Balance 1/1/2010 $ 0

Owner’s investment + 25,000

Balance Rev 12/31/10 +100,000

Balance Exp 12/31/10 - 75,000

Bal Withdrawal 12/31/10 - 5,000

Balance 12/31/10 $45,000

Balance 1/1/2011 $45,000

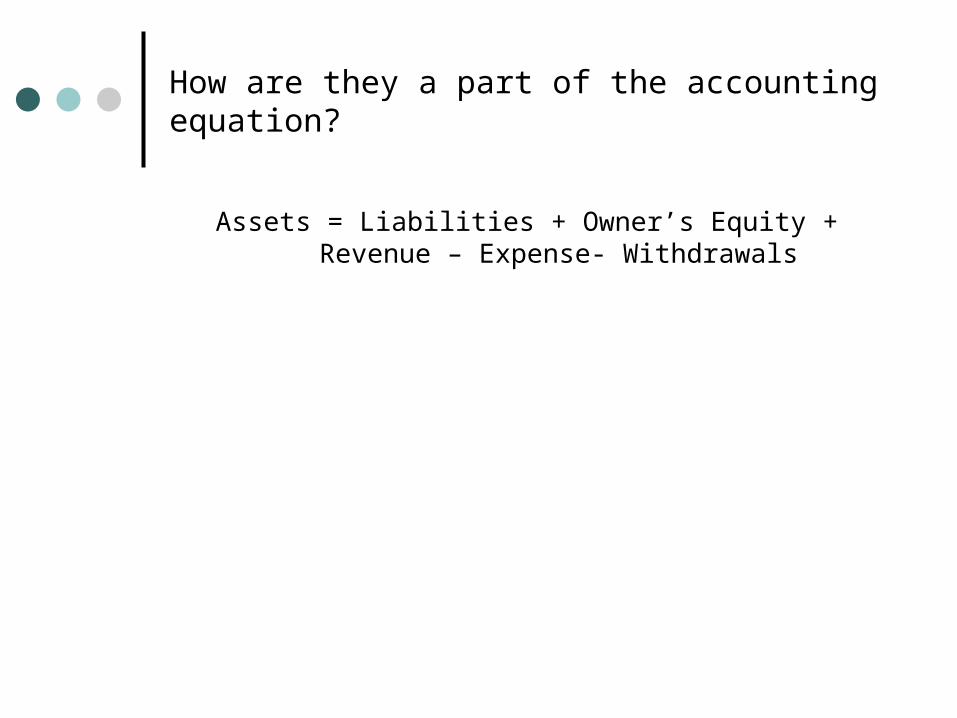

How are they a part of the accounting equation?

Assets = Liabilities + Owner’s Equity + Revenue – Expense- Withdrawals

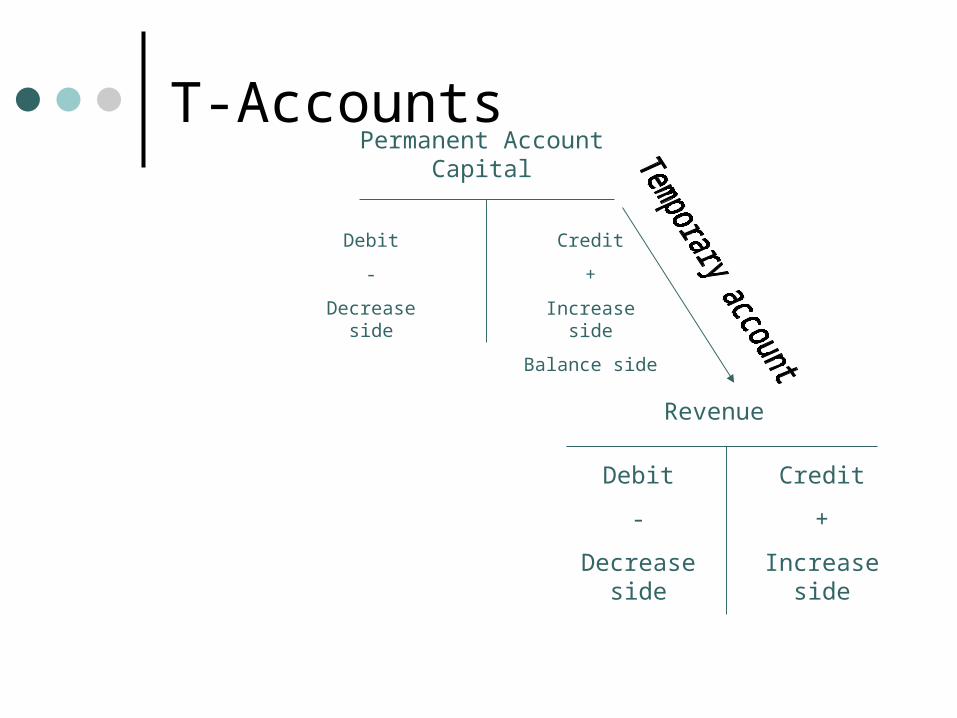

T-AccountsPermanent Account

Capital

Debit

-

Decrease side

Credit

+

Increase side

Balance side

Revenue

Debit

-

Decrease side

Credit

+

Increase side

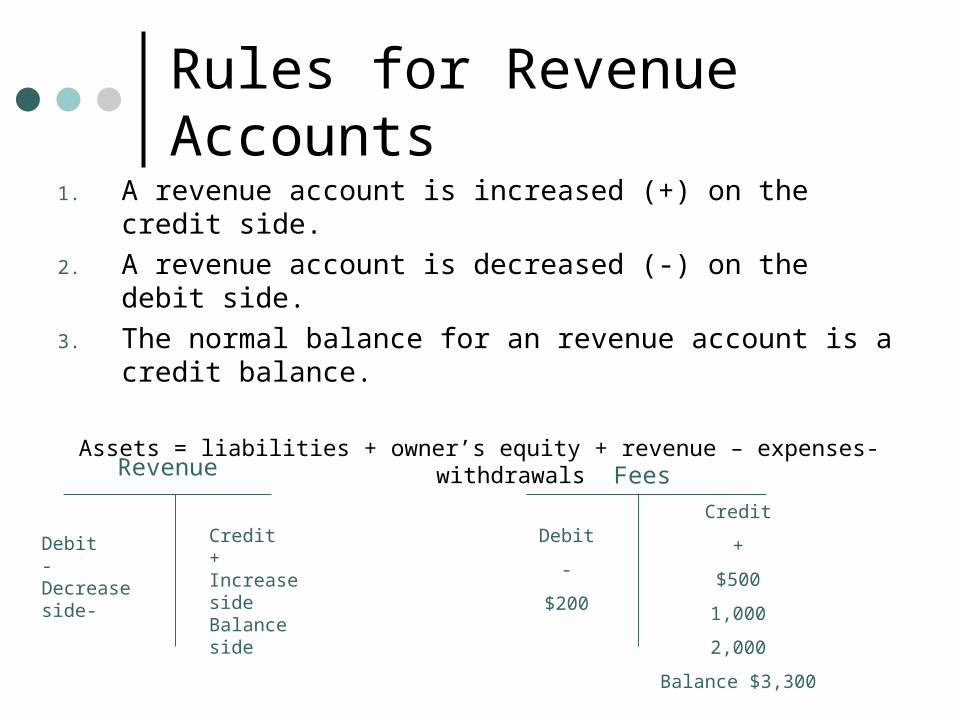

Rules for Revenue Accounts

1. A revenue account is increased (+) on the credit side.

2. A revenue account is decreased (-) on the debit side.

3. The normal balance for an revenue account is a credit balance.

Assets = liabilities + owner’s equity + revenue – expenses- withdrawals

Revenue

Debit-Decrease side-

Credit+Increase sideBalance side

Fees

Debit

-

$200

Credit

+

$500

1,000

2,000

Balance $3,300

REMEMBER

The normal balance side of any account is the same as the side used to increase that account.

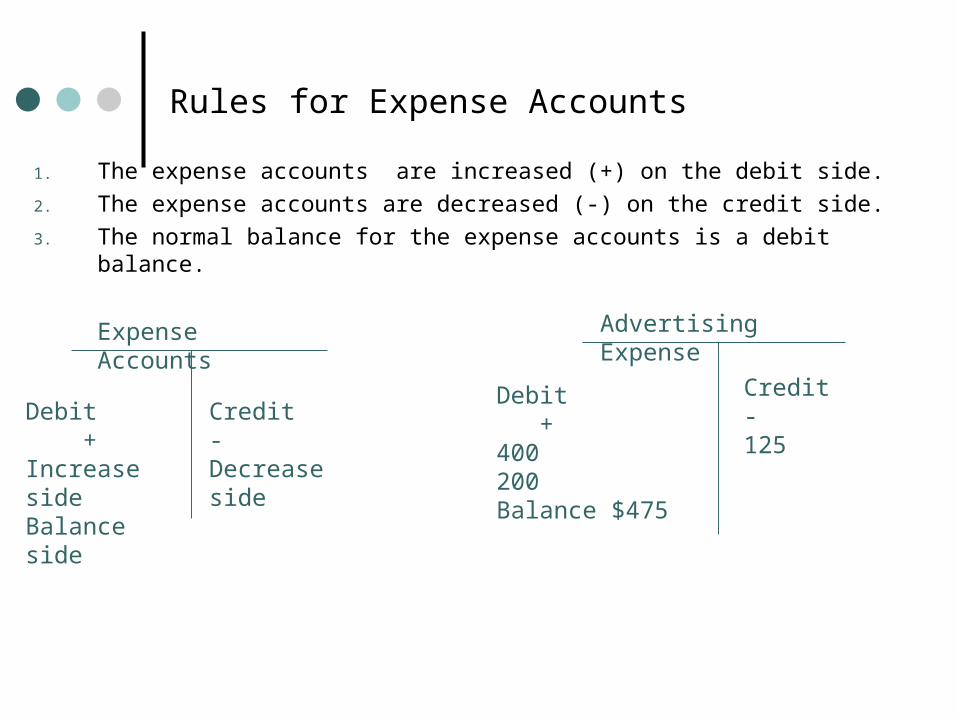

Rules for Expense Accounts

1. The expense accounts are increased (+) on the debit side.

2. The expense accounts are decreased (-) on the credit side.

3. The normal balance for the expense accounts is a debit balance.

Expense Accounts

Debit +Increase sideBalance side

Credit-Decrease side

Advertising Expense

Debit +400200Balance $475

Credit-125

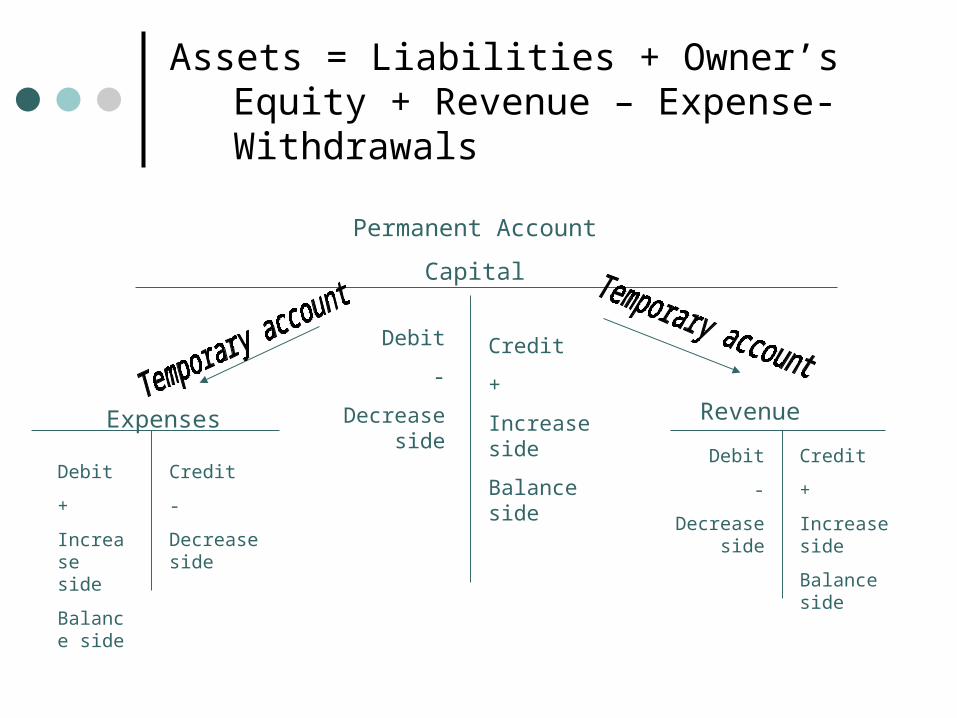

Assets = Liabilities + Owner’s Equity + Revenue – Expense- Withdrawals

Permanent Account

Capital

Debit

-

Decrease side

Credit

+

Increase side

Balance side

Expenses Revenue

Debit

+

Increase side

Balance side

Credit

-

Decrease side

Debit

-

Decrease side

Credit

+

Increase side

Balance side

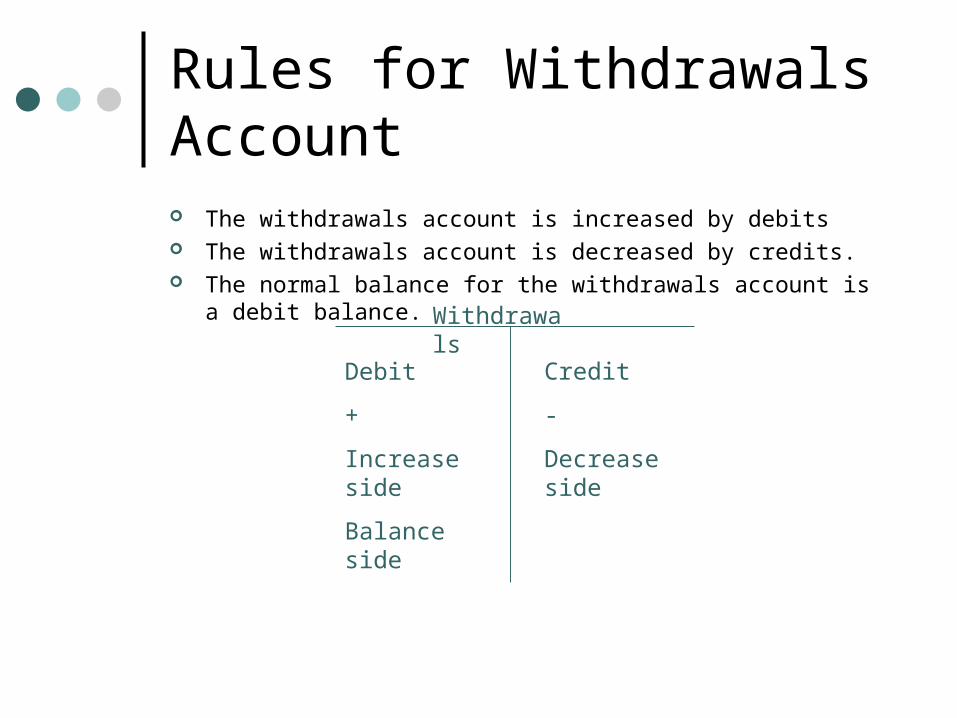

Rules for Withdrawals Account The withdrawals account is increased by debits The withdrawals account is decreased by credits. The normal balance for the withdrawals account is a debit balance.

Withdrawals

Debit

+

Increase side

Balance side

Credit

-

Decrease side

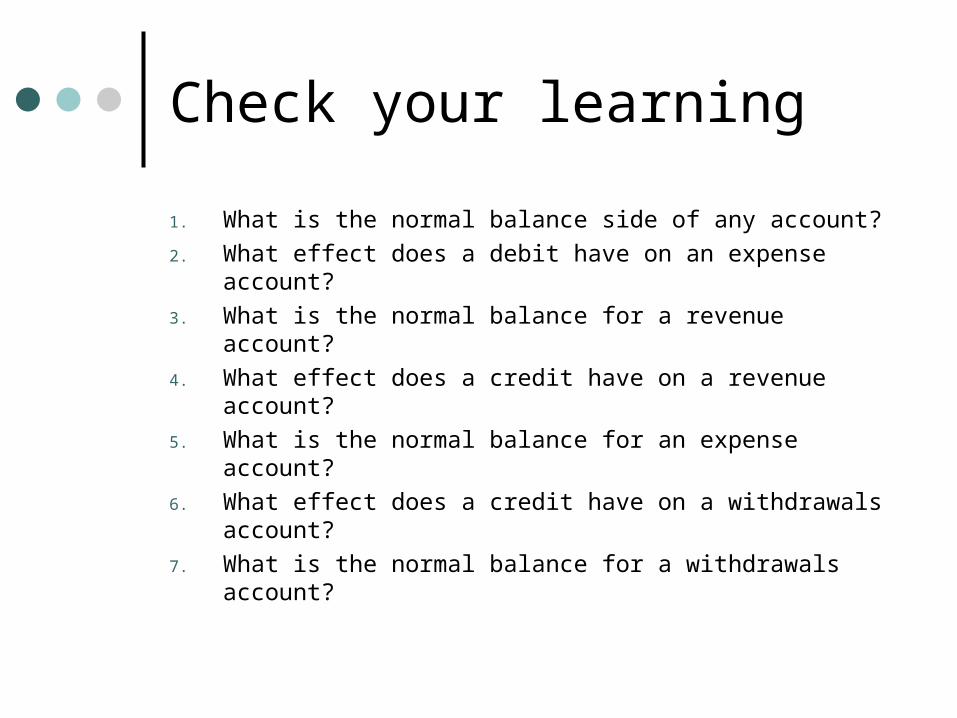

Check your learning

1. What is the normal balance side of any account?

2. What effect does a debit have on an expense account?

3. What is the normal balance for a revenue account?

4. What effect does a credit have on a revenue account?

5. What is the normal balance for an expense account?

6. What effect does a credit have on a withdrawals account?

7. What is the normal balance for a withdrawals account?

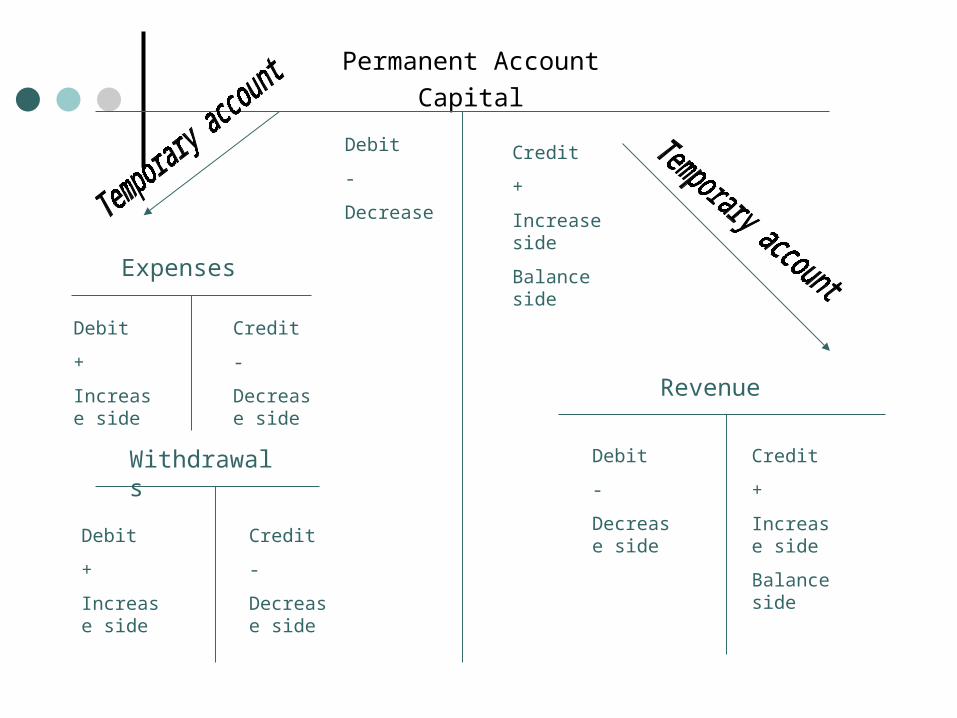

Permanent Account

Capital

Debit

-

Decrease

Expenses

Withdrawals

Debit

+

Increase side

Credit

-

Decrease side

Debit

+

Increase side

Credit

-

Decrease side

Credit

+

Increase side

Balance side

Revenue

Credit

+

Increase side

Balance side

Debit

-

Decrease side

Remember

Expenses decrease owner’s capital. As a result, increases in expenses are recorded as debits and the normal balance of an expense account is a debit balance.

Amounts taken out of the business decrease owner’s capital. Therefore, increases in the withdrawals account are recorded as debits.

Testing for the Equality of Debits and Credits

Make a list of the account titles used by the business.

Opposite each account title, list the final or current balance of the account. Use two columns, one for debit balances and one for credit.

Add each amount column.