Embed Size (px)

Citation preview

Benchmarking Your Portfolio

January 13, 2011By: David Witthohn, CFA, CIPM, Director

2

Why Benchmark Your Portfolio?

3

What is the Purpose of Benchmarking?

Why wear a watch? Why have a speedometer?

• Establish a Standard – Minutes, Speed or Return • Measure Progress – Next Break, Destination or Goals & Objectives• Set Limits – Time, Speed or Risk

4

Isn’t It Just All About Performance?

Would you buy a U.S. Treasury Bond with a yield of 4.27%?

It’s about performance and risk

Risk/Return Tradeoff

5

Portfolio Objectives

● Preserving principal

• Providing sufficient liquidity to meet cash flow demands

• Achieving a market rate of return

6

Benchmark used to Achieve Portfolio Objectives

A good benchmark can be used to measure all of the following:

●Safety – How much credit risk is in the portfolio? How much interest rate risk? How long is the portfolio’s average maturity?

•Liquidity - Can the assets be sold? Are there sufficient funds available to meet cash demands?

•Return – What is a market rate of return? Is the portfolio under invested?

7

Performance Measurement

8

Measuring Return

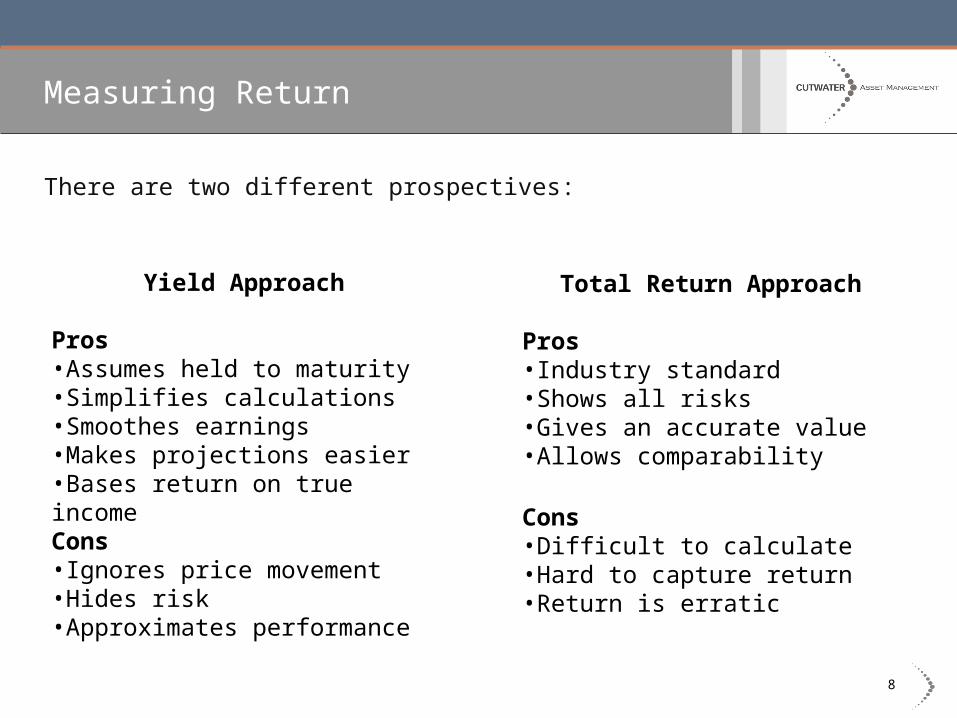

There are two different prospectives:

Yield Approach

Pros•Assumes held to maturity•Simplifies calculations•Smoothes earnings•Makes projections easier•Bases return on true incomeCons•Ignores price movement•Hides risk•Approximates performance

Total Return Approach

Pros•Industry standard•Shows all risks•Gives an accurate value•Allows comparability

Cons•Difficult to calculate•Hard to capture return•Return is erratic

9

Yield Approach – Yield to Maturity (YTM)

Assumptions:

● Looks only at the income from the bond

● Yield-to-Maturity (purchase yield)

● Reinvestment of interest at the YTM

● Security held to maturity with no optionality (non-callable)

● Annualized for comparison purposes

● Approximation of true yield

10

Yield to Maturity

11

Yield to Call

Yield-to-Call and Yield-to-Worst

● Adjusts the yield based on a call date

● Uses the market price as an indication of which securities will be called

12

Yield to Call

13

Amortized Cost

Amortized Cost Method

Return = (Interest +/- Accretion/Amortization +/- Realized Gain/loss)

Average Daily Historical Cost

● Annualize: divide by # of days in the period and then multiple by 365

● Captures sales and purchases, maturities, and called securities

● Calculates actual reinvestment rate

● Calculates return for period – not just a point in time

14

Total Return – Industry Standard

Total return performance combines both income and change in price.

Total Return = Value End – Value Start Value Start

●Doesn’t allow for cash flows for the period (no additions or subtractions)

●Assumes you will sell the security today using the current price

●Changing prices varies return from period-to-period

●Global Investment Performance Standards (GIPS) – These are client returns adjusted for any cash flows

15

Total Return vs. Yield to Maturity (YTM)

6.35%

4.39%

-1.26% -1.73%

1.07%0.84%

-0.45% -0.47% -0.67% -0.31% -0.56% -1.08%

1.80%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

7%

No

v-0

8

De

c-0

8

Ja

n-0

9

Fe

b-0

9

Ma

r-09

Ap

r-09

Ma

y-09

Ju

n-0

9

Ju

l-09

Au

g-0

9

Se

p-0

9

Oc

t-09

No

v-0

9

To

tal R

etu

rn

Months

Total ReturnTreasury Note - 4 5/8 %, Dated 6/30/07

YTM 1.55%

16

Total Return – Price vs. Income

Total Return – 5.52% Income Return – 5.51% Price Return - .01%

17

Benchmark Selection

When you select an Index as your benchmark ideally want it to reflect what you are doing in the portfolio. Here are some issues that you might not have thought about:

•Indexes don’t include transaction costs

•Indexes are passive

•Indexes have no transactions

18

Benchmark Selection

The transaction issue can be reduced by splitting the portfolio into liquid funds and core funds.

19

● Provide money market-like liquidity with incremental returns to traditional Rule 2a-7 funds

● Capture money market return

● Manage liquidity and credit risks

● Reinvest cash flows timely (critical to achieving competitive return profile)

● Capture best duration risk-adjusted returns with the “Core” portfolio

● Allocate to government and high quality sectors, ensuring liquidity if needed

Liquidity Portfolio

1 to 3 Years

Traditional Portfolio Structure

20

Selecting a Benchmark For Your Core Portfolio

21

There are three main drivers of portfolio performance for core funds. Generally these are short-term high quality portfolios:

Duration Effect – duration of portfolio

Sector Effect – allocation of portfolio

Selection Effect – securities in portfolio

Drivers of Performance

22

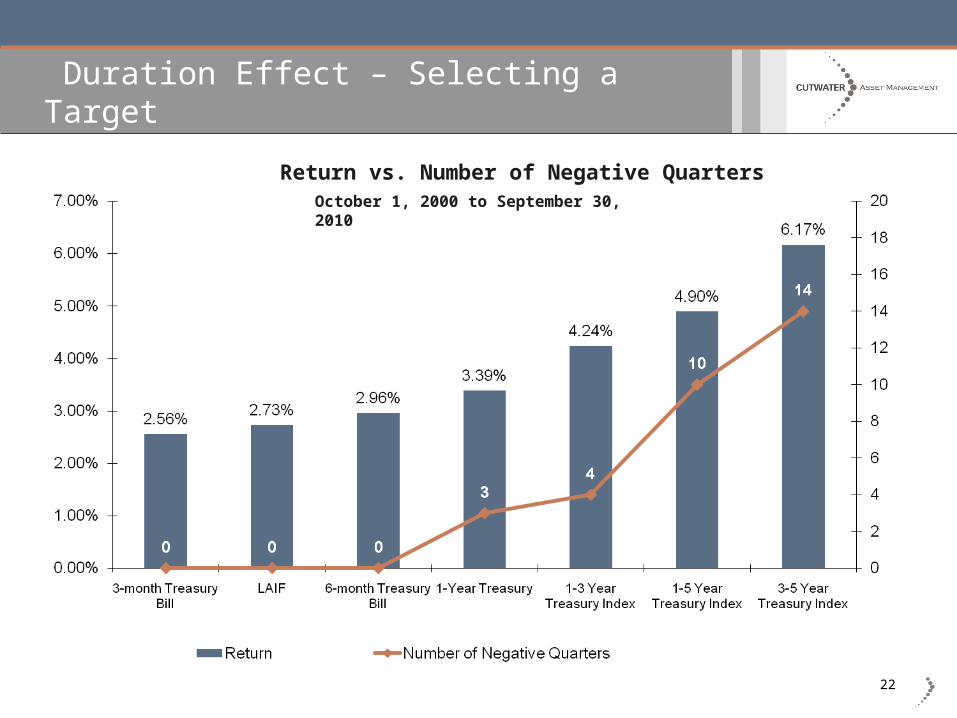

Duration Effect – Selecting a Target

Return vs. Number of Negative QuartersOctober 1, 2000 to September 30, 2010

23

Duration Effect - Risk/Return Tradeoff

24

Cutwater adjusts target duration based on current market conditions. We favor a low-risk approach, using an asymmetrical range to limit market risk. When rates are at the upper end of the band, a duration that is 10% above target is appropriate. When rates are low, a target duration as low as 50% of the target limits market risk.

Source: Bloomberg

Duration Management

25

Amortized Cost – Evaluating Market Risk

Report Date: 12/31/07Wtd. Avg. Wtd. Avg. Weighted

Issuer / Maturity Call Acquisition % ofDays to Days to YTM Maturity Maturity Average Security Coupon Date Date Cost PortfolioFinal Call (Purchase Y) to Final Call Yield

FHLB 3.100% 01/08/08 1,000,000.00 8 3.100% 0.86 0.86 0.334%FHLMC 4.890% 02/01/08 429,959.00 32 5.000% 1.48 1.48 0.232%FHLB-Called 4.570% 04/29/08 01/29/08 359,507.00 120 29 5.000% 4.65 1.12 0.194%FHLB 5.000% 06/27/08 125,000.00 179 5.000% 2.41 2.41 0.067%FNMA 3.250% 08/15/08 371,528.00 228 3.000% 9.13 9.13 0.120%FHLB-Called 4.600% 08/22/08 02/05/08 374,415.00 235 4.850% 9.49 9.49 0.196%FHLB 4.010% 09/17/08 03/17/08 347,995.00 261 4.860% 9.79 9.79 0.182%FHLB 4.570% 10/17/08 349,839.00 291 4.630% 10.98 10.98 0.175%FHLB 4.100% 11/26/08 02/26/08 348,218.00 331 4.700% 12.43 12.43 0.176%FNMA 4.550% 12/01/08 06/01/08 431,669.00 336 153 4.900% 15.64 7.12 0.228%FHLB-Called 5.000% 01/02/09 01/02/08 430,461.00 368 2 4.880% 17.08 0.09 0.227%FNMA-Called 4.100% 02/13/09 02/04/08 399,827.00 410 35 4.850% 17.68 1.51 0.209%FHLB 4.000% 02/23/09 02/04/08 357,265.00 420 35 4.700% 16.18 1.35 0.181%FHLB-Called 4.660% 04/13/09 01/16/08 369,290.00 469 16 4.810% 18.68 0.64 0.192%FFCB-Called 4.300% 06/09/09 01/25/08 303,205.00 526 25 4.730% 17.20 0.82 0.155%FHLB-Called 4.550% 07/14/09 01/28/08 209,365.00 561 28 4.760% 12.67 0.63 0.107%FHLB-Called 4.520% 08/26/09 01/28/08 119,538.00 604 28 4.770% 7.79 0.36 0.061%FHLMC-Called 4.500% 08/10/09 01/10/08 349,962.00 588 10 5.150% 22.19 0.38 0.194%FHLMC-Called 4.500% 08/10/09 01/10/08 159,982.00 588 10 5.150% 10.14 0.17 0.089%FHLB 4.280% 09/08/09 03/08/08 198,486.00 617 68 4.760% 13.21 1.46 0.102%FNMA-Called 4.500% 09/30/09 01/22/08 443,103.00 639 22 4.760% 30.53 1.05 0.227%FHLMC-Called 4.130% 10/09/09 01/30/08 291,661.00 648 30 4.800% 20.38 0.94 0.151%FFCB-Called 4.500% 11/13/09 02/01/08 1,404,513.00 683 32 4.320% 103.44 4.85 0.654%FFCB-Called 4.300% 11/18/09 02/01/08 98,985.00 688 32 4.880% 7.34 0.34 0.052%

Totals 9,273,773.00$ 391.37 79.41 4.507%

26

Amortized Cost – Evaluating Market Risk

27

Sector Effect – Asset Allocation

It may be difficult to find a standard benchmark that completely matches your asset allocation. Here is an example:

28

Sector Effect – Asset Allocation

It may be difficult to find a standard benchmark that completely matches your asset allocation. Here is an example:

29

Custom Benchmark

XYZ City Benchmark

Treasury 1-3 Year 10%Agency 1-3 Year 80%Corporate A+ 1-3 Year 10%

Blended Benchmark 100%

30

How to Communicate Using Benchmarks

31

Communicating Performance Using Benchmarks

In communication it is helpful to show not only performance of the portfolio but also a measure of risk for the portfolio, like standard deviation or weighted average maturity

32

Benchmarking Summary

■ Benchmarks gauge portfolio return and portfolio risk

■ Portfolio return is linked to portfolio safety and portfolio liquidity

■ Performance can be measured by just income or by total return

■ Cash flow analysis splits the portfolio into Liquidity and Core portions

■ There are three primary drivers of portfolio performance

■ Duration is the primary driver of performance

■ Risk measurement is just as important as performance

■ Variation from the benchmark means active management