Embed Size (px)

Citation preview

Berkeley Research Group - Chairman’s Dinner

November 4, 2015

San Francisco, CA

Corporate Governance and Crisis Management:

A General Counsel’s Perspective

Robert E. Bostrom

Senior Vice President, General Counsel & Secretary,

Abercrombie & Fitch

(formerly Executive Vice President, General Counsel &

Secretary, Freddie Mac)

What I would like to do this evening is first, share with you the

conclusions of my review of some of the major corporate

crises since 2000 involving corporate governance breakdowns,

accounting irregularities, earnings restatements, violations of

law, enforcement actions, financial failures, financial markets

disruption, and other events such as those at BP, GM and

Volkswagen. Whether before Sarbanes Oxley, after Sarbanes

Oxley, before Dodd Frank or after Dodd Frank, the reasons

identified in the multiple public reports and investigations are

strikingly similar.

2

My theme here is simple: you cannot legislate away bad

behavior or bad judgment – but you can create sound

governance that involves an ethical culture, independent risk

management, and creates an environment where people do

the right thing – but even then there will be mistakes and

errors in judgment.

Second, I would like to share an inside view of my own

experience at Freddie Mac through the financial crisis of 2008

and the U.S. Government conservatorship and takeover of

Freddie Mac and some lessons I learned about leading and

managing through a major corporate crisis and addressing the

governance issues.

Let me start with a famous quote that I think highlights the

importance of culture and governance.

“When the music stops, in terms of liquidity, things will get

complicated. But as long as the music is playing, you’ve got to

3

get up and dance. We’re still dancing.

The depth of the pools of liquidity is so much larger than it

used to be that a disruptive event now needs to be much

more disruptive than it used to be.

At some point, the disruptive event will be so significant that

instead of liquidity filling in, the liquidity will go the other

way. I don’t think we’re at that point.”

Chuck Prince, the then Citigroup CEO, “Citigroup chief stays

bullish on buy-outs,” Financial Times, July 9, 2007.

Introduction:

> As you know, corporate crises are caused by a variety of

different types of events including:

– Fraud

– Violations of law and compliance

– Excessive risk-taking

– External market or environmental events

4

– Previously acceptable market practices that

retroactively become the subject of enforcement

actions

– Financial markets disruption

– Product failures

– Environmental events

– Corporate governance breakdowns

Pre-Sarbanes Oxley

> By 2000, corporate scandals involving Enron, WorldCom,

and a host of others leading up to the enactment of

Sarbanes-Oxley made it clear that traditional corporate

governance structures, internal controls and risk

management systems did not address the challenges

faced by companies and Boards of Directors.

Post-Sarbanes Oxley

> But, even after the enactment of Sarbanes Oxley, events

subsequent to Sarbanes-Oxley suggest that Sarbanes-

Oxley was not the answer as reports and disclosures of

5

accounting irregularities, earnings restatements,

violations of law, enforcement actions, and corporate

governance breakdowns continued.

> After Sarbanes Oxley, from 2002 through 2005 Freddie

Mac, Fannie Mae, the New York Stock Exchange, a

number of mutual fund complexes, Halliburton, AOL

Time-Warner, Tenet Healthcare, Raytheon, Vivendi,

Parmalat and other companies were the subject of

headlines and went through major corporate crises.

> Investigations and public reports issued in connection

with these events identified the same fundamental

breakdowns of corporate governance.

> The Report of the Special Examination of Freddie Mac,

the Report on Fannie Mae, the Report on Corporate

Governance for the Future of MCI, the NYSE Grasso

Report and the multiple Reports of the Court-Appointed

Examiner in the Enron Bankruptcy, identified problems

6

and proposed recommendations with disturbingly similar

themes.

The problems identified include:

> Inappropriate corporate culture and tone at the top

> Ineffective or absence of compliance and risk

management systems

> Inadequate internal control structure

> Executive compensation programs

> Inadequate disclosure and transparency

> Inadequate Board oversight as a result of a variety of

factors including

> Cronyism

> Lack of relevant subject matter and knowledge

> Inattention to duties and responsibilities

> Not receiving adequate and accurate information

from management to exercise oversight

responsibilities on a timely basis

7

> The key themes which merged were the importance of an

ethical culture, transparency, trust, accountability,

governance, reputation and independence.

> Nonetheless, we were about to enter a new chapter,

even after Sarbanes Oxley.

The Financial Crisis

In 2007 and 2008 we saw the failures of Washington Mutual,

Merrill Lynch, Lehman, Bear Stearns, Wachovia, Country-Wide

Financial, Freddie Mac and Fannie Mae, GM, MF Global and

AIG. Some were arguably market-induced but certainly some

significant breakdowns in corporate governance, and ethical

culture and risk management were major causes as we shall

discuss shortly.

Recent Events

Even after Dodd Frank we have seen major issues and

prosecutions involving trading losses, FOREX bid-rigging,

8

international tax evasion, LIBOR rate manipulation, violations

of Iran sanctions, money laundering, Foreign Corrupt Practices

Act, and more.

> We have seen companies facing major non-financial

created crises:

– BP

– Toyota

– News Corp

– Massey

– Chesapeake Energy

– Siemens

– GM

– Volkswagen

Let’s talk for a minute about the velocity and politicization of

consequences in the current environment

> The consequences flowing from a crisis or headline

event are extremely severe in the current

environment because of:

1. the politicization of headline events,

9

2. the criminalization of corporate events,

3. the extreme and activist reaction of criminal and

regulatory agencies, shareholders and the public,

and

4. the velocity of consequences.

> Historically a headline event could lead to SEC, criminal

and civil actions.

> We are in a new era now. In addition to SEC, civil and

criminal actions, significant headline events lead to:

– Congressional hearings and investigations,

– intervention by the Executive Branch,

– actions by State AGs,

– public vilification,

– political and governmental reactions,

– shareholder reaction,

– customer reaction,

– executive officer dismissals, and more.

10

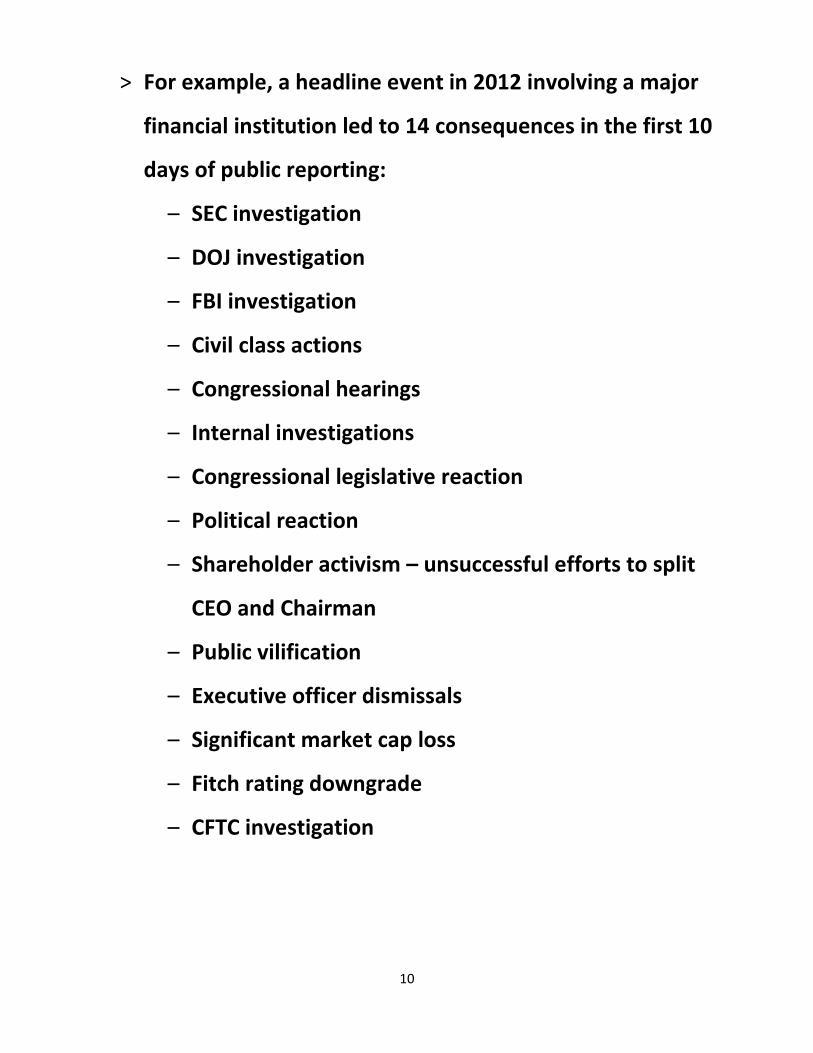

> For example, a headline event in 2012 involving a major

financial institution led to 14 consequences in the first 10

days of public reporting:

– SEC investigation

– DOJ investigation

– FBI investigation

– Civil class actions

– Congressional hearings

– Internal investigations

– Congressional legislative reaction

– Political reaction

– Shareholder activism – unsuccessful efforts to split

CEO and Chairman

– Public vilification

– Executive officer dismissals

– Significant market cap loss

– Fitch rating downgrade

– CFTC investigation

11

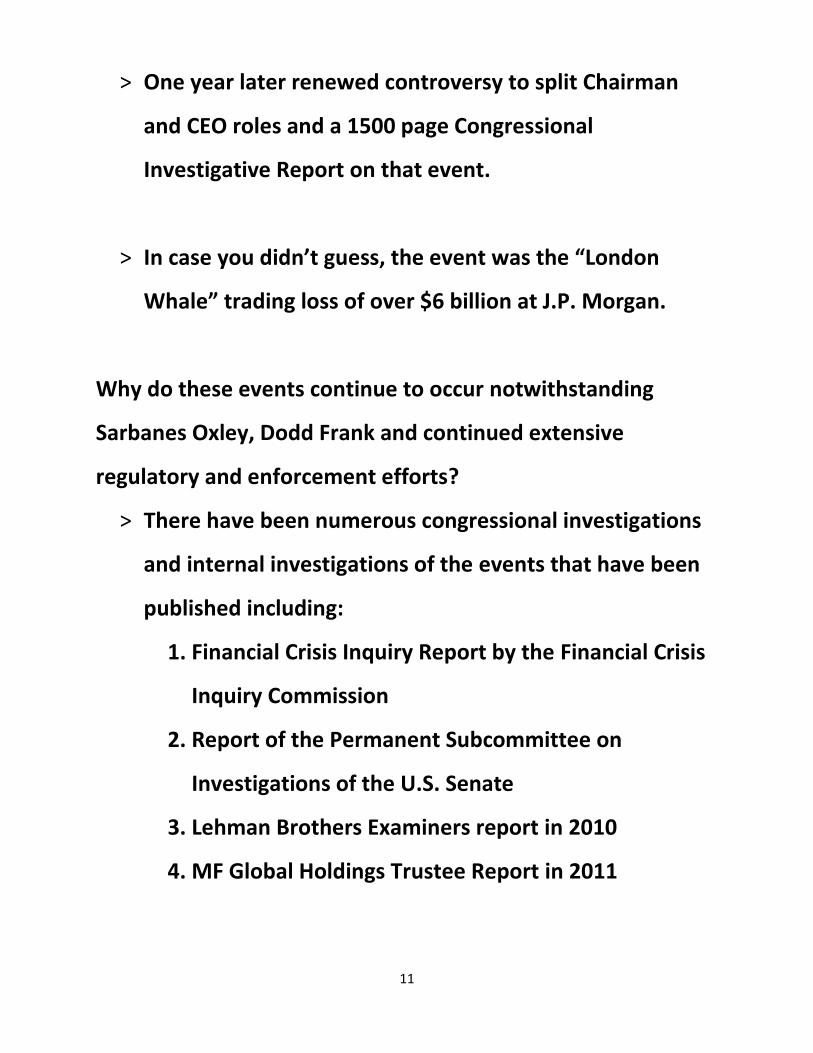

> One year later renewed controversy to split Chairman

and CEO roles and a 1500 page Congressional

Investigative Report on that event.

> In case you didn’t guess, the event was the “London

Whale” trading loss of over $6 billion at J.P. Morgan.

Why do these events continue to occur notwithstanding

Sarbanes Oxley, Dodd Frank and continued extensive

regulatory and enforcement efforts?

> There have been numerous congressional investigations

and internal investigations of the events that have been

published including:

1. Financial Crisis Inquiry Report by the Financial Crisis

Inquiry Commission

2. Report of the Permanent Subcommittee on

Investigations of the U.S. Senate

3. Lehman Brothers Examiners report in 2010

4. MF Global Holdings Trustee Report in 2011

12

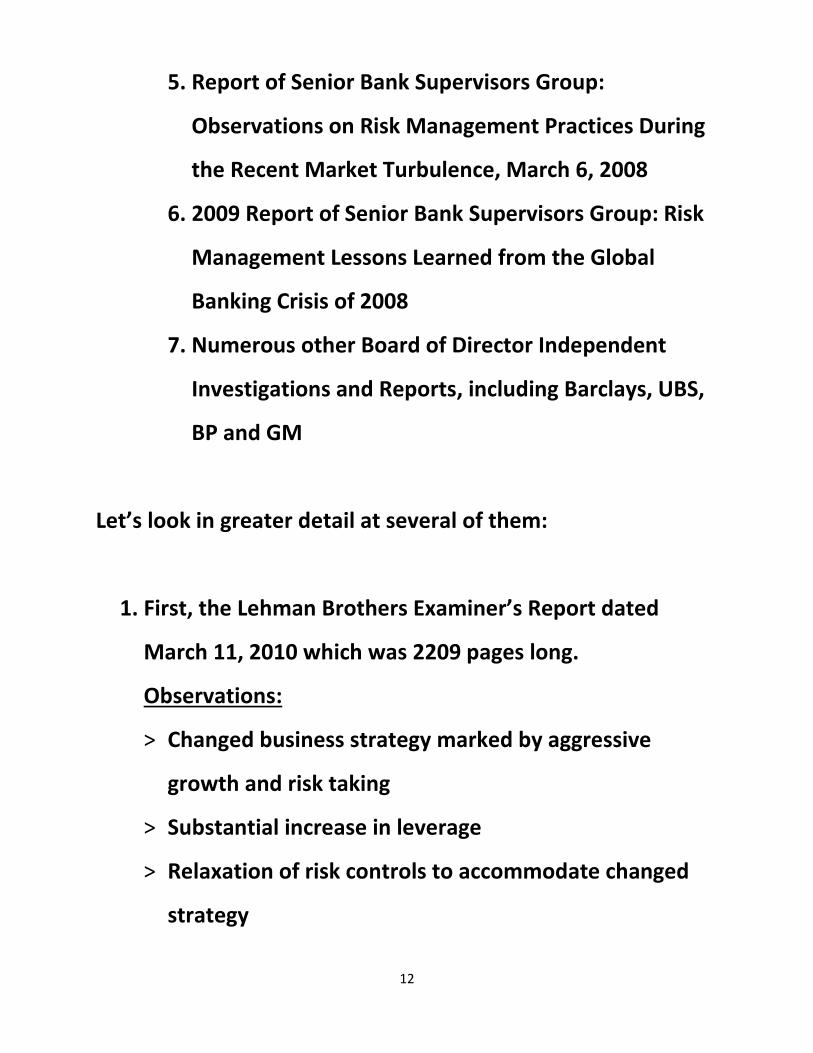

5. Report of Senior Bank Supervisors Group:

Observations on Risk Management Practices During

the Recent Market Turbulence, March 6, 2008

6. 2009 Report of Senior Bank Supervisors Group: Risk

Management Lessons Learned from the Global

Banking Crisis of 2008

7. Numerous other Board of Director Independent

Investigations and Reports, including Barclays, UBS,

BP and GM

Let’s look in greater detail at several of them:

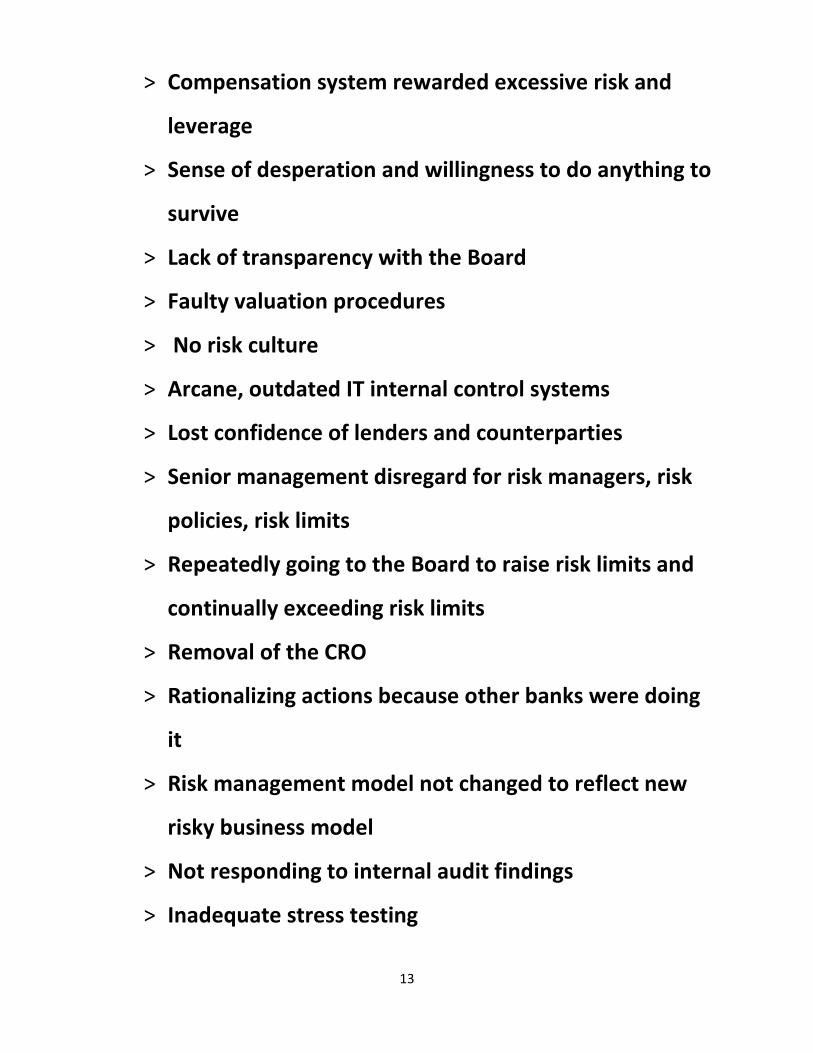

1. First, the Lehman Brothers Examiner’s Report dated

March 11, 2010 which was 2209 pages long.

Observations:

> Changed business strategy marked by aggressive

growth and risk taking

> Substantial increase in leverage

> Relaxation of risk controls to accommodate changed

strategy

13

> Compensation system rewarded excessive risk and

leverage

> Sense of desperation and willingness to do anything to

survive

> Lack of transparency with the Board

> Faulty valuation procedures

> No risk culture

> Arcane, outdated IT internal control systems

> Lost confidence of lenders and counterparties

> Senior management disregard for risk managers, risk

policies, risk limits

> Repeatedly going to the Board to raise risk limits and

continually exceeding risk limits

> Removal of the CRO

> Rationalizing actions because other banks were doing

it

> Risk management model not changed to reflect new

risky business model

> Not responding to internal audit findings

> Inadequate stress testing

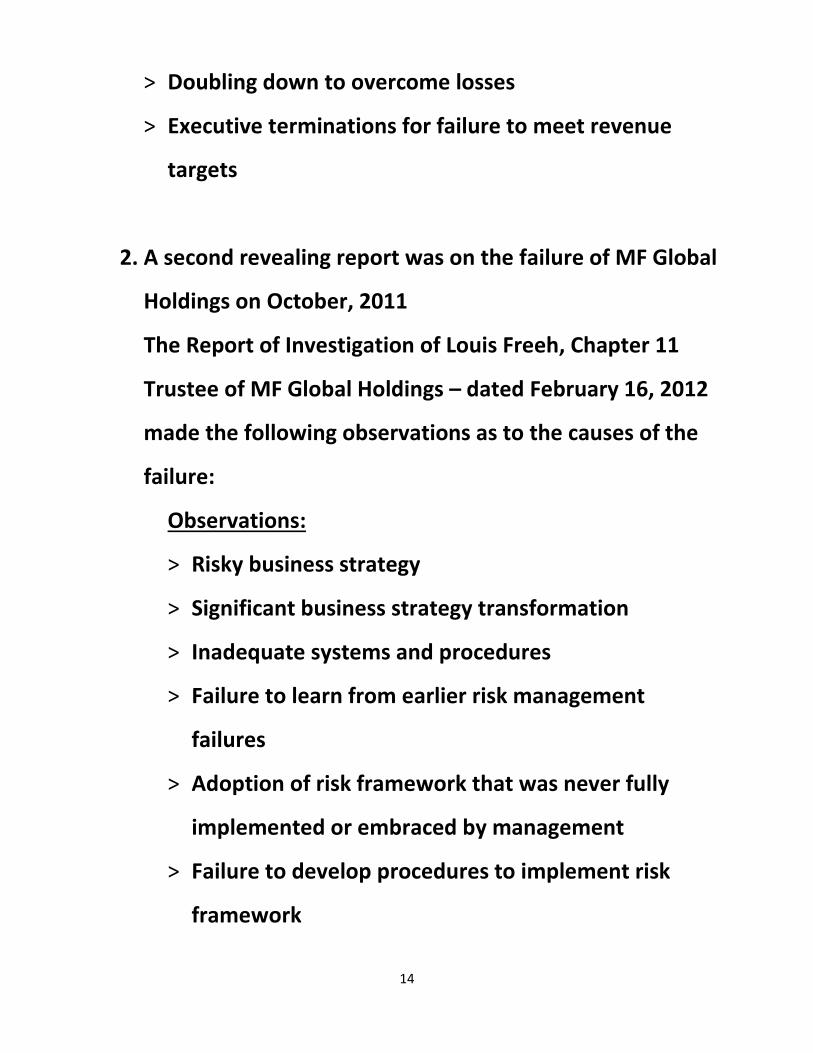

14

> Doubling down to overcome losses

> Executive terminations for failure to meet revenue

targets

2. A second revealing report was on the failure of MF Global

Holdings on October, 2011

The Report of Investigation of Louis Freeh, Chapter 11

Trustee of MF Global Holdings – dated February 16, 2012

made the following observations as to the causes of the

failure:

Observations:

> Risky business strategy

> Significant business strategy transformation

> Inadequate systems and procedures

> Failure to learn from earlier risk management

failures

> Adoption of risk framework that was never fully

implemented or embraced by management

> Failure to develop procedures to implement risk

framework

15

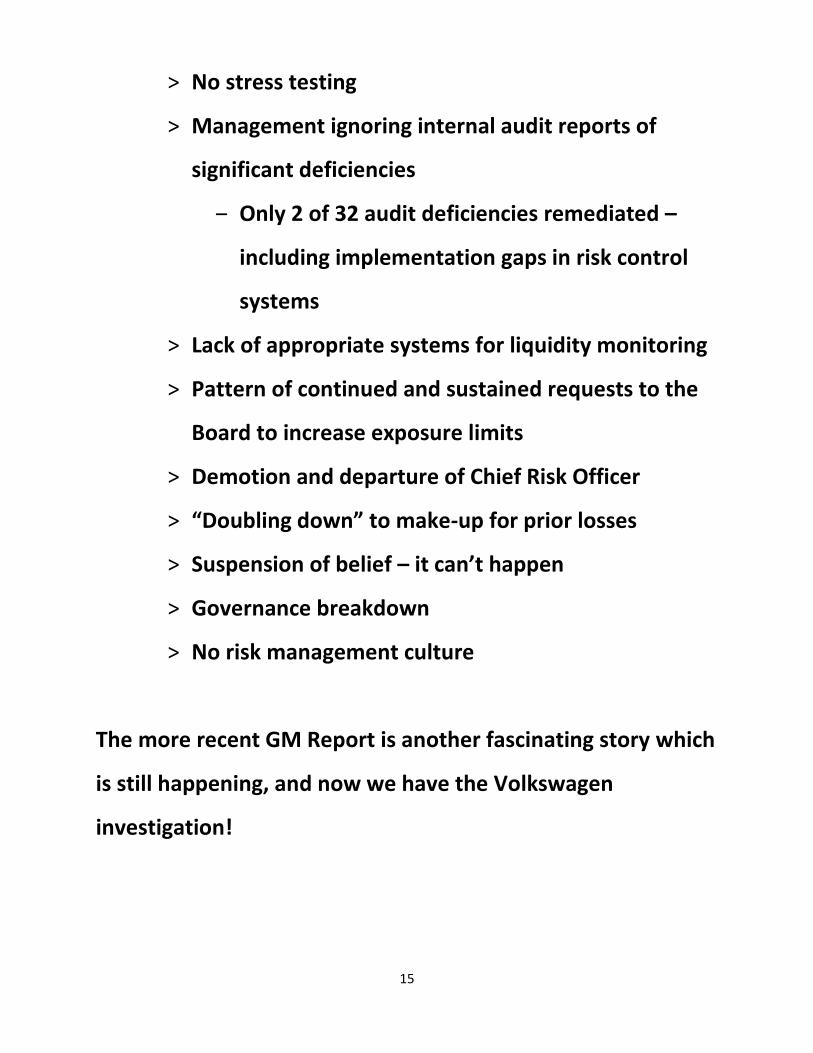

> No stress testing

> Management ignoring internal audit reports of

significant deficiencies

‒ Only 2 of 32 audit deficiencies remediated –

including implementation gaps in risk control

systems

> Lack of appropriate systems for liquidity monitoring

> Pattern of continued and sustained requests to the

Board to increase exposure limits

> Demotion and departure of Chief Risk Officer

> “Doubling down” to make-up for prior losses

> Suspension of belief – it can’t happen

> Governance breakdown

> No risk management culture

The more recent GM Report is another fascinating story which

is still happening, and now we have the Volkswagen

investigation!

16

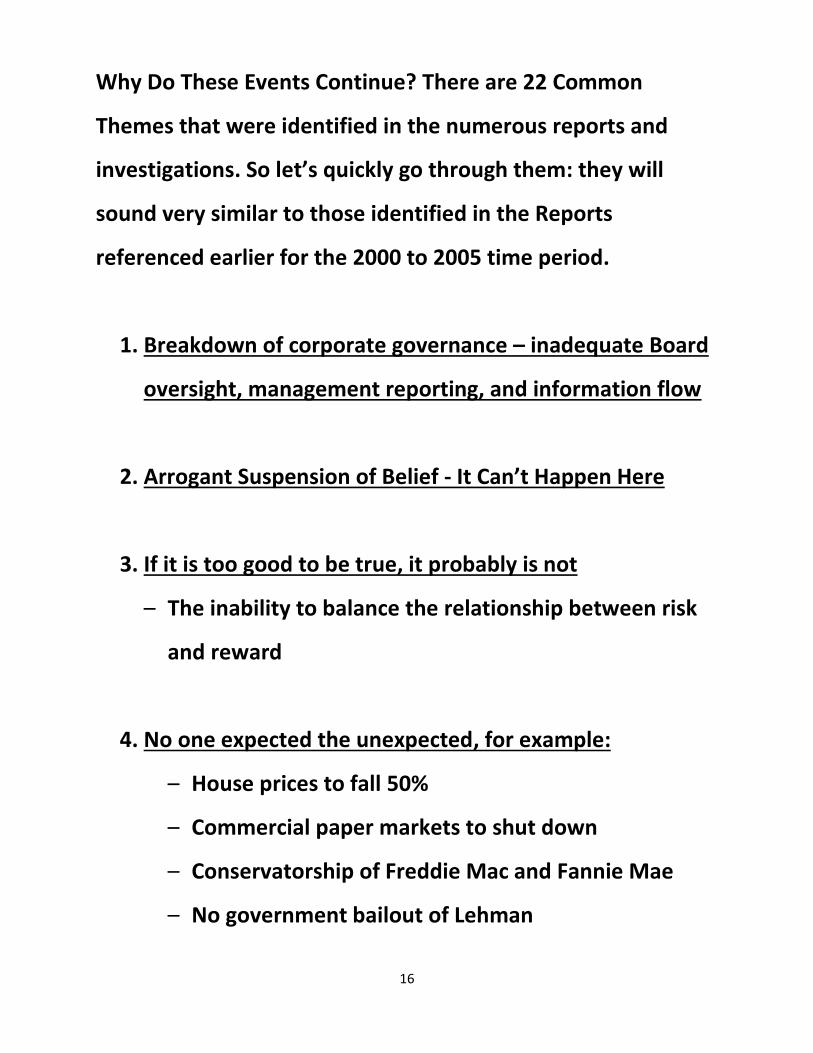

Why Do These Events Continue? There are 22 Common

Themes that were identified in the numerous reports and

investigations. So let’s quickly go through them: they will

sound very similar to those identified in the Reports

referenced earlier for the 2000 to 2005 time period.

1. Breakdown of corporate governance – inadequate Board

oversight, management reporting, and information flow

2. Arrogant Suspension of Belief - It Can’t Happen Here

3. If it is too good to be true, it probably is not

– The inability to balance the relationship between risk

and reward

4. No one expected the unexpected, for example:

– House prices to fall 50%

– Commercial paper markets to shut down

– Conservatorship of Freddie Mac and Fannie Mae

– No government bailout of Lehman

17

– Well-head blowout

– Coal mine explosion

– Ignition switch problem

– Wide-spread manipulation of emissions testing

5. Failure to escalate and report and trying to self-correct

– “Doubling down” to avoid problems

6. As a General Counsel, this is my favorite – “Everyone else

is doing it”….

The arguments that there is:

– Safety in numbers

– Can't all be wrong

– Puts us in a competitive disadvantage with our

competitors

– It is technically legal

7. Absence of an effective Enterprise-Wide Risk

Management System at Board and Management Levels

18

to proactively identify, assess, prioritize and mitigate risk.

8. Absence of a No Risk Culture

> No emphasis on doing the right thing

> Lack of awareness and priority

> Complacency

> Arrogance

> Blind reliance on models

> Lack of accountability

> No escalation

> No clear roles and responsibilities

9. Compensation Systems

> Rewarding the wrong behavior

> Not incentivizing the right behavior

10. Lack of Sensitivity

Individuals lost their sensitivity and awareness of what

can happen. It is imperative to:

> Stay sensitized

19

> Constant “headline training” and awareness

> Stay ever vigilant and mindful

> Be skeptical

> Constantly adjust risk-reward balance and risk

tolerance

> Trust but verify

Inadvertent vs. Advertent Bad Acts

> Inadvertent – good people making bad judgment calls

– A lack of sensitivity and awareness leads to “bad”

decisions or no decisions

– Business “justification” or “rationalization” clouds

judgment – whether excessive risk or violation of

law or both

– Important for formal and informal reminders –

training, tone at the top, risk culture

11. Ignoring Red Flags

Either:

– Not seeing

20

– Not believing what you were seeing, or

– coming up with a business justification

rationalization

12. Regulatory arrogance

> Absence of regulatory and enforcement sensitivity –

regulator is wrong and we are right

13. Long-Standing Market Behavior

> Be aware of, and always self-assess, long-standing

market behavior and activity

– Libor rate setting

– Market-timing cases

– Off-shore tax havens

– Sanctions and money laundering

14. Absence of stress testing

> Absence of a sound stress testing and contingency plan

to identify potential problems and risks, crisis

management plans, and risk-adjusted analysis of

21

business activities based on geography, lines of

business, organization and governance

15. Blind Reliance on Models that Failed

> We must always think critically – be skeptical

> Need to use judgment

16. Absence of thinking forward with hindsight

> How will actions today be viewed with the benefit of

hindsight

17. Accountability

> Acceptance/tolerance of de minimus violations of law

because there is “no harm” and the business or

individual is a key producer or part of management

18. Use of Independent Reviews

> Need to conduct periodic third party assessments

before problems occur to ensure periodic, objective,

22

unbiased assessments of governance and risk

management practices and business practices.

> Learn from mistakes

– Root cause analysis of problems after they occur

and remedial steps to correct

19. Management and Board indifference and tolerance of

Internal Audit findings not being remediated

20. Absence of truly INDEPENDENT internal control

functions

– Legal

– Audit

– Compliance

– Risk

– Internal controls

21. Ineffective internal controls and no ethical culture

23

22. Failure to focus on, identify and manage risk in

significant business transformations

So what’s a General Counsel To Do?

> Be a proactive and persuasive advisor to management

and the Board

> Advise, counsel and persuade for the adoption of

governance standards that ensure independence, ethical

behavior, and an informed independent Board

> Provide constant reminders of these 22 observations

> Make sure that Board is getting complete, accurate,

reliable and timely information

> Be the devil’s advocate – challenge “everybody’s doing

it” justifications

> Educate and emphasize the importance of enterprise risk

management to prevent and mitigate problems

> Motivate and advocate for the fostering and nurturing of

an ethical culture

24

> Develop a crisis management plan and have it in place

before the crisis

> Be a respected and trusted advisor: be the conscience of

the corporation

So now let me turn for a few minutes to an inside view of

leading through a crisis: my experience at Freddie Mac

through the financial crisis and government takeover and

conservatorship and some lessons learned.

First, a little background to set the stage.

> In 2008, Freddie Mac was a Fortune 50, New York Stock

Exchange listed, SEC registrant with 2.5 trillion dollars in

assets, approximately 1.0 trillion dollars of publicly

traded debt and 1.5 trillion dollars of public

securitizations. Freddie Mac had over 650 million shares

of outstanding common stock and 18 series of

outstanding preferred stock.

25

> Freddie Mac was put into conservatorship on September

7, 2008 by the U.S. Treasury and The Federal Housing

Finance Agency. Shareholder capital was wiped out and

it became one of the largest restructurings and

conservatorships in history.

> The U.S. Treasury would contribute 200 billion dollars of

capital to Freddie Mac and Fannie Mae.

> The U.S. Treasury would enter into financing

arrangements to support over 5 trillion dollars of debt

obligations of Fannie Mae and Freddie Mac.

At the time Freddie Mac was

> Regulated by

– Office of Federal Housing Enterprise Oversight (later

the Federal Housing Finance Agency)

– US Department of Housing and Urban Development

– US Securities and Exchange Commission

– New York Stock Exchange

26

– US Treasury

> And governed by

– Federal Statutory Charter

– Virginia Corporation Law

> When I first joined Freddie Mac in early 2006, the

Company was in the aftermath of a $6 billion Financial

Statement Restatement with a massive Consent Order

with OFHEO and a remediation plan to satisfy its terms,

in the midst of a myriad of investigations and litigation,

including the DOJ, the SEC and the FEC, was the focus of

intense Congressional investigations and political

attention, and was a party in a multitude of derivative

suits, ERISA suits and shareholder securities fraud class

actions arising out of the Restatement.

> From 2006 to 2007, in addition to managing and resolving

these investigations and the civil litigation, I helped to

restructure the Board and put in place a new corporate

27

governance structure in the aftermath of the

Restatement.

> Freddie Mac had barely recovered from those challenges

when Freddie Mac and Fannie Mae faced the brunt of an

investigation by New York Attorney General Andrew

Cuomo in 2007and then the ensuing global financial crisis

in 2008.

> Before I knew it, I was unexpectedly sitting across a table

from Hank Paulson, Ben Bernanke and then FHFA

Director Jim Lockhart being informed of a government

takeover and conservatorship options. After 96 hours

with little sleep, 3 Board meetings, advising the Board of

its fiduciary duties and its options at this tense and crisis-

laden moment, Freddie Mac went into conservatorship

on September 7, 2008 and the world as I knew it

changed.

28

> The directors were offered the opportunity to resign.

> Shortly after, the CEO, CFO and CBO left the company,

followed by many other senior executives.

> Government appointed a new Non-executive Chairman

and CEO

Day 1 – September 7, 2008

What is the Conservatorship?

> Most significantly, the conservator has all of the rights,

titles, powers and privileges of the shareholders,

management and directors.

> Conservator is required by statute to preserve and

conserve assets.

> There were pre-existing Statutory Responsibilities under

the Federal Charter.

> The Senior Preferred Stock Purchase Agreement with the

U.S. Treasury had significant covenants and requirements

and granted UST warrants for 79.9% of common stock.

29

> Remaining 20.1% of outstanding common stock

continued to be held by Shareholders with rights and

dividends suspended.

> 18 Series of Preferred Stock continued to be held by

preferred Shareholders but with no rights and dividends

suspended.

> Continued SEC registration and NYSE Listing.

> Subject to Virginia Corporation Law, Federal Charter, the

Federal Conservatorship Statute and the Emergency

Economic Stabilization Act.

Conservatorship

> Because of the sheer size and magnitude of the scope of

government support and the politics of “blame”, the U.S.

government launched immediate investigations.

> Within 3 weeks, Freddie Mac and Fannie Mae were hit

with multiple parallel investigations by the DOJ and the

FBI, the SEC, the FHFA, over time approximately 20

Congressional investigations and inquiries, state

30

attorneys general inquiries, and civil litigation.

> There was a document retention hold put in place. This

lead to millions of documents being maintained.

> FBI agents showing up at employee’s residences at night,

or offices during the day, wanting interviews.

> There were multiple interviews and depositions of 100s

of current and former employees and former directors.

> EVERYONE blamed Freddie Mac and Fannie Mae for the

financial crisis and assumed financial fraud and

misconduct.

> All of this had a huge impact on employees.

> Working closely with the FHFA and the U.S. Treasury, I

helped to guide the prior Board of Directors and

Executive Management of Freddie Mac through the

31

governance for appointment of the Conservator during

the weekend of September 5, 2008.

> After the appointment of the Conservator that weekend,

the ensuing resignations of most of the prior Board of

Directors and the departure of the 3 senior executives, I

advised and supported the creation of a new corporate

governance structure and the appointment of a new

Board of Directors (including 3 directors from the pre-

conservatorship Board) with a new non-executive

Chairman.

> This involved, among other things, negotiations and

developing an appropriate Delegation of Authority from

the FHFA as Conservator to the new Board of Directors

and management, the creation of a Board Committee

structure, and the recruitment, selection and orientation

of new directors. This involved developing roles and

responsibilities for new directors, a non-executive chair,

new CEO, new management team, the Conservator, and

32

the US Treasury.

> For almost three years after conservatorship, I advised

the new Board of Directors and the new management

team of Freddie Mac, on their duties and responsibilities

in conservatorship and the appropriate corporate

governance structure in conservatorship including the

drafting of the Board Committee Charters, advising on

Board and Committee agendas, running the Board and

Committee meetings, policies and procedures, the

legality of corporate actions, determining who had

authority to approve actions and when approvals were

required from FHFA pursuant to the Delegation of

Authority or the US Treasury pursuant to the Senior

Preferred Stock Purchase Agreement.

> This involved balancing the conflicting and oftentimes

competing requirements of the conservatorship statute,

the Emergency Economic Stabilization Act, the statutory

requirements of Freddie Mac’s Federal charter, the safety

33

and soundness requirements of the FHFA as regulator,

directives from the Administration, the Senior Preferred

Stock Purchase Agreement with the US Treasury, Virginia

corporation law, the Federal Securities laws (since

Freddie Mac continues to be an SEC registrant), and the

listing requirements of the New York Stock Exchange

(until voluntary delisting).

> During this period I helped to navigate Freddie Mac

through multiple Congressional investigations,

governmental investigations, internal investigations, and

parallel civil litigation. The impact of these events on the

company was incredible.

> To give you some perspective on these 6 years, when I

joined, I was the 5th General Counsel in 2 years – while I

was GC for almost 6 years I survived:

– 4 CEO’s,

– 4 CFOs,

– CFO termination

34

– government appointed CEO resignation,

– multiple heads of business units and IT,

– the resignation of the COO, and

– a virtually 100% NEW Management Committee.

> It was 5 years of never ending crisis management.

> The stress was indescribable.

> Every day came another unimaginable event. The impact

on employees was catastrophic.

> Our CFO committed suicide. This set off another round of

investigations.

> We had additional multiple key executive departures and

difficulty hiring.

> It was an extremely hostile public, congressional and

political environment.

35

> Multiple internal and external investigations of

allegations of employee misconduct.

> Multiple constant Congressional initiatives to eliminate

Freddie Mac and Fannie Mae.

There were a number of lessons learned and governance

challenges for a general counsel in a major corporate crisis:

1. There are multiple simultaneous challenges involving:

> Your public reputation

> Customers

> Vendors

> Shareholders

> Counter-parties

> Regulators

> Employees

> Media

> The Administration

36

> Congress

2. You need a holistic approach on a variety of fronts to

minimize loss and manage litigation and investigations

including:

> Public Relations

> Government Relations (Congressional)

> Political

> Clearly defined and articulated Board involvement and

role

> Regulators

> Enforcement agencies

> Reputation

> Shareholders

> Management’s role

> Employees (How do you keep them going? Tired,

demoralized, uncertain, scared, angry)

> Customers

> Counter-parties

37

> From a legal perspective – need to be prepared for and

develop a strategy for simultaneous investigations and

actions:

– SEC

– DOJ

– Civil Shareholder suits

– Internal investigations

– Congressional investigations

– Regulatory investigations

– State attorney general actions

3. These events are like an iceberg, you can really only see

the little part sticking out of the water but it is the mass

of ice underneath that can do the most damage.

> When management and Boards think about a crisis

that might result in an investigation or litigation, it is

critical to be prepared to get on top of the issue

quickly. In this environment, a headline grabbing event

-- the tip of the ice berg -- results in simultaneous or

38

rapid sequential civil litigation, governmental

investigations by the SEC, DOJ, primary regulatory

agency, congressional investigations, and actions by

state Attorney Generals.

> The strategies for each are different and require an

integrated, coordinated, holistic response. Managing

conflicting views of multiple legal and public relations

advisors who are myopically focused on their

particular proceeding is a leadership challenge.

4. Significant challenges regarding strategy, production of

documents, consistency of multiple interviews and

depositions:

> Production in one venue was public for all proceedings

> Productions to Congressional Committees would be

posted on the Committee website

39

> Developing a legal representation strategy for the

100’s of employees being interviewed – many of whom

were not officers and not technically entitled to

indemnification

> Massive e-discovery and technology challenges

5. Misinformation or bad information can often times

create more problems than the underlying facts.

> Information disclosure - advertent and inadvertent.

> The impact of these investigations and the facts for the

company and the employees, and management, can be

paralyzing and distracting. The political and public

relations issues are overwhelming.

> Important to proactively monitor social media and

blogs to gather intelligence on what is happening and

40

what messaging is going on, including allegations or

facts that may impact the investigative process.

6. The consequences can go on forever.

> Legal actions started in 2007 and 2008.

> The SEC settled with the 3 individual defendants this

year - 2015.

7. Failure of boards and companies in responding can result

in stakeholders all acting irrationally. Board should have

a plan in place.

> First, a predetermined list of advisors who know the

company, and immediate fact-finding -- a careful,

truthful, deliberate response is necessary no matter

how painful. In particular, independent counsel for the

Board.

41

> Second, conflicts can and will develop between Board

counsel and company counsel – working together and

partnering can be challenging.

> Third, from a governance perspective, the Board

should decide ahead of time what its role will be --

how involved it will be. I believe that in this

environment a Board, or a Board committee, must be

intimately and actively involved with management of

the situation. The communications and information

flow to the Board is critical. There can be no surprises.

8. What is the Board governance during the crisis – who,

how much and how?

> Who?

– Entire Board

– Board Committee

– Special Committee

– Lead Director

– Non-Executive Chair

42

– Chair of Audit Committee

> How

– Updates, Special meetings

– Timely information flow

– Input on key decisions, alternatives, implications

9. A communications plan to all stakeholders and

constituencies including shareholders, employees,

vendors, customers, suppliers, regulators, Congress, the

Administration -- is imperative. There must be confirmed,

fact-based, open and honest communication.

10. The identity of the public company spokesperson should

be determined ahead of time.

– CEO

– Chairman or Lead Director

– Outside PR Firm

– General Counsel

43

11. Always do the right thing – as lawyers you are the

conscience of the corporation.

12. Counsel and advise management and the Board of

Directors with objectivity and understanding – BUT DO

NOT FORGET WHO YOUR CLIENT IS. Your job is NOT to

protect the CEO and executive management.

13. You must maintain credibility, your reputation, and the

trust of others – including management, the Board,

prosecutors, regulators and all employees.

14. Be a role model – you must inspire and lead your

colleagues to work 24/7 for long periods of time under

great stress and potential personal liability.

15. Maintain relentless enthusiasm, dedication,

commitment and professionalism.

44

16. Most importantly, and I cannot emphasize this enough,

say “thank you” – constantly show appreciation and

respect for everyone.

Thank you for the opportunity to share these thoughts with

you this evening.