Embed Size (px)

Citation preview

Godfreys Group Limited 1H 2015 Results Presentation

23 February 2015

Tom Krulis Managing Director

Bernie Bicknell

COO/CFO

For

per

sona

l use

onl

y

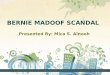

Financial Highlights

Godfreys 2

Total sales increase of 3.5% on previous corresponding period

Reaffirm F15 Prospectus pro forma EBITDA of $22.1 million, and pro forma NPAT

forecast of $12.2 million

Gross Profit improvement of 220bp on corresponding period, and 50bp better

than pro forma forecast despite unfavourable exchange rate movement

Seven new company-owned stores opened (net of four after three franchise store

closures)

Five Franchise stores bought back into company-owned store network

Earnings per share of 10.6 cents on the current Issued Share Capital

On 10 December 2014 the shareholders of the International Cleaning Solutions Group Pty Ltd (ICSG) undertook a capital reconstruction process, through which the Godfreys Group

Limited acquired ICSG. Under the principles of capital reconstruction in accordance with the Australian Accounting Standards, the Half Year Statutory Financial Report includes the

historical financial information of ICSG. Consequently, earning per share of 14.8 in the Half Year Statutory Financial Report represents the blended earning per share for the Issued

Share Capital under ICSG, and the new Issued Share Capital under Godfreys Group Limited.

For

per

sona

l use

onl

y

Gross profit reflects the margin on sales after incorporating direct material costs including hedged foreign exchange gains/losses resulting from procurement of goods from

international suppliers. On 1 July 2014, Godfreys Group Ltd made a decision to implement hedge accounting for foreign exchange hedge contracts, hence realised and

unrealised exchange gains/losses are recognised in costs of sales once the hedged inventory is sold.

CODB includes uplift executive remuneration (including short term incentives and expense in relation to performance rights issued under the new long term incentive plan) and

corporate costs expected to arise in FY15 as a consequence of the company becoming ASX listed.

Profit and Loss (Pro Forma)

Godfreys 3

1H2015 FY15

(A$m) Pro Forma Prospectus

Sales 90.6 185.0

Gross Profit 56.9 115.4

Gross margin 62.8% 62.3%

Other costs of sales 7.4 13.8

Operating gross profit 49.5 101.6

Other income 2.3 4.0

CODB 40.5 83.4

CODB/Sales 44.7% 45.1%

EBITDA 11.3 22.1

EBITDA margin 12.4% 12.0%

Depreciation 1.6 3.8

EBIT 9.7 18.4

EBIT margin 10.7% 9.9%

Interest 0.6 1.0

Profit before tax 9.1 17.4

Tax 2.7 5.1

NPAT 6.4 12.2

Headline Statistics:

Earning per share - basic (cents) 14.8

Earning per share - diluted (cents) 14.3

Stores 210 216

Gross margin improved and ahead of Prospectus

forecast

Other income relates to franchise fee revenue,

and advertising contribution. 1H2015 on track

with forecast

EBITDA margin at 12.4%, ahead of Prospectus

forecast

For

per

sona

l use

onl

y

Profit and Loss – Country segment

Godfreys 4

AUS NZ NZ Consolidated

(A$m) (A$m) (NZ$m) (A$m) (A$m)

Sales 78.7 13.1 11.9 90.6

LFL Sales growth -1.2% -3.4% -1.6%

Gross Profit 49.6 8.0 7.3 56.9

Gross Profit margin 63.0% 60.9% 60.9% 62.8%

Other cost of sales 6.3 1.2 1.1 7.4

Operating gross profit 43.3 6.8 6.2 49.5

Other income 2.1 0.2 0.2 2.3

CODB 35.5 5.5 5.0 40.5

CODB % of Sales 45.1% 42.3% 42.3% 44.7%

EBITDA 9.9 1.5 1.4 11.3

EBITDA margin 12.5% 11.5% 11.5% 12.5%

Depreciation 1.4 0.2 0.2 1.6

EBIT 8.5 1.3 1.2 9.7

EBIT margin 10.8% 10.3% 10.3% 10.7%

LFL results consistent with forecast. Prospectus

forecast growth based on the significant increase

in Sales in 1H2014, and the impact on average

selling prices of introducing a higher share of

Company-branded products in FY2015. The shift

in selling product mix delivers higher profit margin

and lower cost to sell

EBITDA Margin strong at 12.5%. Group EBITDA

margin 50bp ahead of F15 prospectus EBITDA

margin forecast

Gross Profit margin ahead of F15 prospectus

forecast by 50bp

Group EBIT margin at 10.7%

New Zealand benefitted from stronger currency

For

per

sona

l use

onl

y

Trading Performance - Sales

Godfreys 5

Negative LFL sales (1.6%) as forecast, due to changing sales product mix

Overall growth of 3.5%

New Product launches of Hoover Allergy Bagged and Bagless product highly

successful

Store expansion program on track

New Product rollout on track for 1H2015 including the Sauber excellence,

Hoover Allergy bagged, Wertheim W2500, etc…

Strong January trading result

For

per

sona

l use

onl

y

Trading Performance – Gross Margin

Godfreys 6

Group

62.8% blended Gross Margin across Australia and new Zealand

Ahead of forecast Gross Margin percentage and Last Year

Margin has improved despite FX deterioration

New products introduced in first half have improved Margin

Suppliers have assisted with price reductions in many areas, to

offset FX impact

Price increases have been taken, where appropriate

Australia

Gross margin of 63.0%, higher than prior year.

Foreign currency hedging arrangements have been entered into up

until August 2015. Current hedged average rate of:

• US$, 1A$ = 0.85 US$; and

• EUR, of 1A$ = 0.65 EUR

New Zealand

Gross Margin of 60.9%, impacted by products sourced from

Australia

0.57

0.58

0.59

0.6

0.61

0.62

0.63

0.64

57.0%

58.0%

59.0%

60.0%

61.0%

62.0%

63.0%

64.0%

F12 F13 F14 1H2015 F15Forecast

GM (group) GM (AU) GM (NZ)For

per

sona

l use

onl

y

Trading Performance - CODB

Godfreys 7

Group

Pro Forma CODB at 44.7%, 0.4% favorable against Prospectus

forecast

Year-on-year favorable CODB margin, a reduction of 1.2%

compared to the previous corresponding period

Costs reduction benefited from lower cost to sale (Commission

and Interest finance) as a result of the shift in product mix, and

support office costs.

Combination of CPI rental increases offset by rental reductions on

lease renewals

No unexpected costs in first half

0.38

0.39

0.4

0.41

0.42

0.43

0.44

0.45

0.46

0.47

0.48

38.0%

39.0%

40.0%

41.0%

42.0%

43.0%

44.0%

45.0%

46.0%

47.0%

48.0%

F12 F13 F14 1H2015 F15Forecast

CODB (group) CODB (AU) CODB (NZ)For

per

sona

l use

onl

y

Balance Sheet

Godfreys 8

(A$'m) 1H2015 FY2014

Assets

Cash and cash equivalents 1.5 7.4

Trade and other receivables 7.6 5.3

Inventories 34.4 25.2

Total current assets 43.6 37.9

Trade and other receivables 0.4 0.5

Property, plant and equipment 11.8 11.4

Intangible assets 91.2 89.8

Deferred tax assets 5.2 2.7

Total non-current assets 108.7 104.5

Total assets 152.3 142.4

Liabilities

Trade and other payables 23.3 16.4

Interest-bearing loans and borrowings - 6.0

Other current liabilities 7.2 6.8

Total current liabilities 30.5 29.2

Interest-bearing loans and borrowings 20.0 54.4

Other liabilities 4.0 3.3

Total non-current liabilities 24.0 57.7

Total liabilities 54.6 86.9

Net assets 97.7 55.4

Equity

Share capital 109.5 28.0

Capital reconstruction reserves (43.5) 0.1

Retained earnings 31.6 27.3

Total equity 97.7 55.4

Trade Debtors higher than FY14 due to higher

trading volumes with Franchises and a temporary

extended franchisees payment terms. Extended

terms balance now fully paid.

Goodwill increased as a result of Franchise store

buybacks.

Inventory build for January and pre Chinese New

Year in 1H2015. Inventory balance normalised in

March 2015.

New non-current debt facility drawn. All bank

covenants met.

For

per

sona

l use

onl

y

Cash Flow

Godfreys 9

(A$'m) 1H2015 1H2014

Cash Flows From Operating Activities

Receipts from customers 92.2 87.0

Payments to suppliers and employees (83.9) (72.5)

Income taxes (0.4) (0.2)

Net cash provided by operating activities 7.9 14.3

Cash Flows From Investing Activities

Payment for property, plant and equipment (1.9) (1.5)

Acquisition of intangible assets (1.4) (0.1)

Net cash used in investing activities (3.4) (1.5)

Cash Flows From Financing Activities

Proceeds from Issue of equity securities 77.7 -

Proceeds of new debt facility 20.0 -

Payment for the acquisition of shares in ICSG (46.2) -

Repayment of old debt facility (59.4) -

Interest and other costs of finance paid (2.5) (4.1)

Net cash used in financing activities (10.4) (4.1)

Net Increase / (Decrease) In Cash Held (5.9) 8.6

Cash At The Beginning Of The Period 7.4 (0.3)

Cash At The End Of The Period 1.5 8.4

Payments to suppliers include payments for

additional temporary Inventory build for January

and pre-Chinese New Year.

CAPEX spent mainly relates to Store fit out:

New & conversion stores $1.0m

Store Refurbish $0.4m

Other $0.5m

Total $1.9m

Franchise store buybacks $1.1m

Software $0.3m

Total $1.4m

New non-current debt of $20m, Interest paid of

$2.5m relates to old debt facilities.

For

per

sona

l use

onl

y

170 170 175 178 181 185

23 24 26 28 29 31

0

50

100

150

200

250

F11 F12 F13 F14 1H2015 F15 forecastNew Zealand Australia

1H2015 stores movement Seven new stores opened • VIC: Traralgon, Sunbury • WA: Geraldton, Claremont • NSW: Coffs Harbour • TAS: Kingston • NZ: Gisborne

Five conversion to company-owned stores • VIC: Camberwell, Richmond, • NSW: Blacktown • SA: Ridgehaven • QLD: Bundaberg

Three stores closed • WA: North Perth • NSW: Bathurst (store concession) • TAS: Kingston (store concession)

2H2015 planned new stores • VIC: Wangaratta, West Gosford • NSW: Caringbah, Mt Druitt, Dubbo, Bathurst

One conversion to franchise own store in 2H2015 • WA: Whitford City

Retail Store Network

Godfreys 10

193 201 206 210 216 194

NZ

18

11

WA

5

18

NSW

37

11

SA

12

7

VIC

19

23

TAS

6

1

ACT

3

-

128 Company-owned stores

82 Franchised stores

QLD

28

10

NT

-

1

For

per

sona

l use

onl

y

FY2015 Outlook

Godfreys 11

Strong January sets up good Full Year trading result in line with forecast

Additional 6 company stores expected to open in 2H2015

New Product rollout on track (Hoover regal launched in January)

Improve Gross Margin to achieve Prospectus forecast

CODB improvements continue in both cost to sale (finance interest and commission) and support

office

Anticipated to meet Prospectus Profit and Cash targets

Continue with foreign currency hedging strategy to limit exposure to changes in the cost of

internationally sourced inventory

Relocation of the main distribution centre in Victoria to complete in 2H2015.

For

per

sona

l use

onl

y

Appendix: Statutory to Pro Forma reconciliation

Godfreys 12

Half-year ending 26 December 2014$A’m

1H2014 statutory results 90.6 5.9 7.6 4.3 (5.9)

IPO costs - 3.3 3.3 3.3 -

IPO Bonus paid to Management - 1.8 1.8 1.8 -

Proceeds from IPO - - - - (77.7)

Refinancing of borrowings - - - - 39.4

Payment to the owner of ICSG - - - - 46.2

Impact of first time adopting of hedge accounting - (0.8) (0.8) (0.8) -

Tax consolidation adjustment - - - (3.2) -

Underlying Statutory results 90.6 10.3 11.9 5.4 2.0

Public company costs - (0.5) (0.5) (0.5) (0.5)

Incremental executive remuneration - (0.1) (0.1) (0.1) -

Change in interest costs - - - 2.0 2.0

Tax impact of Pro Forma adjustments - - - (0.4) (0.4)

Underlying Pro Forma results 90.6 9.7 11.3 6.4 3.0

Sales EBIT EBITDA NPATNet cash

flow

Half-year ending 27 December 2013$A’m

1H2014 statutory results 87.5 10.5 11.9 6.4 8.6

Forward contracts unrealised gain - (0.8) (0.8) (0.8) -

Tax consolidation adjustment - - - (2.0) -

Underlying Statutory results 87.5 9.7 11.1 3.7 8.6

Public company costs - (0.5) (0.5) (0.5) (0.5)

Incremental executive remuneration - (0.1) (0.1) (0.1) -

Change in interest costs - - - 3.6 3.6

Tax impact of Pro Forma adjustments - - - (0.9) (0.9)

Underlying Pro Forma results 87.5 9.1 10.5 5.7 10.8

Sales EBIT EBITDA NPATNet cash

flow

For

per

sona

l use

onl

y

Questions

Godfreys 13

For

per

sona

l use

onl

y