Embed Size (px)

Citation preview

BETH ISRAEL DEACONESS MEDICAL CENTER, INC.

AND AFFILIATES

Consolidated Financial Statements

and Other Financial Information

September 30, 2011 and 2010

(With Independent Auditors’ Report Thereon)

BETH ISRAEL DEACONESS MEDICAL CENTER, INC.

AND AFFILIATES

Consolidated Financial Statements

and Other Financial Information

September 30, 2011 and 2010

Table of Contents

Page(s)

Independent Auditors’ Report 1

Consolidated Balance Sheets 2

Consolidated Statements of Operations 3

Consolidated Statements of Changes in Net Assets 4

Consolidated Statements of Cash Flows 5

Notes to Consolidated Financial Statements 6 – 35

Other Financial Information

Independent Auditors’ Report on Other Financial Information 36

Consolidating Balance Sheets 37 – 40

Consolidating Statements of Operations 41 – 42

Independent Auditors’ Report

Board of Directors

Beth Israel Deaconess Medical Center, Inc. and Affiliates:

We have audited the accompanying consolidated balance sheets of Beth Israel Deaconess Medical Center,

Inc. and Affiliates (the Medical Center) as of September 30, 2011 and 2010 and the related consolidated

statements of operations, changes in net assets, and cash flows for the years then ended. These consolidated

financial statements are the responsibility of the Medical Center’s management. Our responsibility is to

express an opinion on these consolidated financial statements based on our audits.

We conducted our audits in accordance with auditing standards generally accepted in the United States of

America. Those standards require that we plan and perform the audit to obtain reasonable assurance about

whether the financial statements are free of material misstatement. An audit includes consideration of

internal control over financial reporting as a basis for designing audit procedures that are appropriate in the

circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Medical

Center’s internal control over financial reporting. Accordingly, we express no such opinion. An audit also

includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial

statements, assessing the accounting principles used and significant estimates made by management, as

well as evaluating the overall financial statement presentation. We believe that our audits provide a

reasonable basis for our opinion.

In our opinion, the consolidated financial statements referred to above present fairly, in all material

respects, the financial position of Beth Israel Deaconess Medical Center, Inc. and Affiliates as of

September 30, 2011 and 2010 and the results of their operations, changes in their net assets, and their cash

flows for the years then ended, in conformity with U.S. generally accepted accounting principles.

January 9, 2012

KPMG LLP Two Financial Center 60 South Street Boston, MA 02111

KPMG LLP is a Delaware limited liability partnership, the U.S. member firm of KPMG International Cooperative (“KPMG International”), a Swiss entity.

BETH ISRAEL DEACONESS MEDICAL CENTER, INC.AND AFFILIATES

Consolidated Balance Sheets

September 30, 2011 and 2010

(In thousands)

Assets 2011 2010

Current assets:Cash and cash equivalents $ 189,005 176,940 Investments 461,180 452,167 Patient accounts receivable, net of allowance for doubtful

accounts of $22,439 in 2011 and $21,341 in 2010 182,931 169,123 Other current assets 66,967 66,108

Total current assets 900,083 864,338

Assets limited or restricted as to use:Held by trustees under debt and other agreements 25,825 28,046 Held for specific purposes and endowments 162,254 177,603

188,079 205,649

Long-term investments 23,905 18,760 Property and equipment, net 550,885 560,833 Debt issuance costs, net 3,453 4,058 Other assets 1,685 1,686

Total assets $ 1,668,090 1,655,324

Liabilities and Net Assets

Current liabilities:Current portion of long-term debt $ 21,265 20,392 Accounts payable and accrued expenses 180,864 186,395 Estimated settlements with third-party payors 57,532 44,929

Total current liabilities 259,661 251,716

Long-term debt, net of current portion 424,582 444,788 Professional liability 18,090 17,004 Employee benefit plans liabilities 141,153 122,935 Deferred gain on sale of real estate 19,153 20,207 Other liabilities 18,105 19,053

Total liabilities 880,744 875,703

Net assets:Unrestricted 625,092 602,018 Temporarily restricted 112,536 129,098 Permanently restricted 49,718 48,505

Total net assets 787,346 779,621 Total liabilities and net assets $ 1,668,090 1,655,324

See accompanying notes to consolidated financial statements.

2

BETH ISRAEL DEACONESS MEDICAL CENTER, INC.AND AFFILIATES

Consolidated Statements of Operations

Years ended September 30, 2011 and 2010

(In thousands)

2011 2010

Operating revenue:Net patient service revenue $ 1,461,503 1,429,999 Research revenue 241,882 222,399 Contributions 9,118 6,947 Other revenue 99,753 101,633

1,812,256 1,760,978

Operating expenses:Salaries and benefits 1,027,311 993,603 Supplies and other expenses 589,072 557,543 Uncompensated care 53,518 58,567 Depreciation 78,578 78,594 Interest 22,572 23,611

1,771,051 1,711,918

Income from operations 41,205 49,060

Nonoperating gains (losses):Loss on extinguishment of debt (2,131) — Net realized gains on sales of investment securities 11,591 7,426 Unrealized change in equity interests in limited partnerships (3,713) 19,464

Nonoperating gains, net 5,747 26,890

Excess of revenue over expenses 46,952 75,950

Change in net unrealized gains and losses on investments (8,495) 3,597 Net assets released from restrictions used for purchase of property

and equipment 4,612 4,552 Change in funded status of employee benefit plans, other than net

periodic benefit cost (19,995) (17,744) Increase in unrestricted net assets $ 23,074 66,355

See accompanying notes to consolidated financial statements.

3

BETH ISRAEL DEACONESS MEDICAL CENTER, INC.AND AFFILIATES

Consolidated Statements of Changes in Net Assets

Years ended September 30, 2011 and 2010

(In thousands)

Temporarily PermanentlyUnrestricted restricted restricted Total

Net assets at September 30, 2009 $ 535,663 119,411 46,395 701,469

Excess of revenue over expenses 75,950 — — 75,950 Restricted contributions, net — 7,435 2,110 9,545 Restricted investment income and gains — 13,749 — 13,749 Change in net unrealized gains and losses

on unrestricted investments 3,597 — — 3,597 Net assets released from restrictions used

for operations — (6,945) — (6,945) Net assets released from restrictions used

for purchase of property and equipment 4,552 (4,552) — — Change in funded status of employee

benefit plans, other than net periodicbenefit cost (17,744) — — (17,744)

66,355 9,687 2,110 78,152

Net assets at September 30, 2010 602,018 129,098 48,505 779,621

Excess of revenue over expenses 46,952 — — 46,952 Restricted contributions, net — (2,140) 1,213 (927) Restricted investment income and gains — 549 — 549 Change in net unrealized gains and losses

on unrestricted investments (8,495) — — (8,495) Net assets released from restrictions used

for operations — (10,359) — (10,359) Net assets released from restrictions used

for purchase of property and equipment 4,612 (4,612) — — Change in funded status of employee

benefit plans, other than net periodicbenefit cost (19,995) — — (19,995)

23,074 (16,562) 1,213 7,725 Net assets at September 30, 2011 $ 625,092 112,536 49,718 787,346

See accompanying notes to consolidated financial statements.

4

BETH ISRAEL DEACONESS MEDICAL CENTER, INC.AND AFFILIATES

Consolidated Statements of Cash Flows

Years ended September 30, 2011 and 2010

(In thousands)

2011 2010

Cash flows from operating activities:Change in net assets $ 7,725 78,152 Adjustments to reconcile change in net assets to net cash

provided by operating activities:Change in funded status of employee benefit plans, other

than net periodic benefit cost 18,218 16,974 Depreciation 78,578 78,594 Amortization (1,520) (1,287) Net gains on investments (230) (45,161) Restricted contributions (5,404) (9,545) Loss on early extinguishment of debt 2,131 — Increase (decrease) in cash resulting from changes in:

Patient accounts receivable (13,808) 5,395 Other current assets (859) 1,364 Accounts payable and accrued expenses (9,215) (1,238) Estimated settlements with third-party payors 12,603 17,852 Other assets and liabilities 138 148

Net cash provided by operating activities 88,357 141,248

Cash flows from investing activities:Purchase of property and equipment (65,403) (62,359) Net sales (purchases) of investments and assets whose use is

limited or restricted 3,642 (47,820)

Net cash used in investing activities (61,761) (110,179)

Cash flows from financing activities:Payments on long-term debt (126,195) (19,713) Proceeds from new borrowing 106,690 — Payment of debt issuance costs (430) — Restricted contributions 5,404 9,545

Net cash used in financing activities (14,531) (10,168)

Net increase in cash and cash equivalents 12,065 20,901

Cash and cash equivalents at beginning of year 176,940 156,039 Cash and cash equivalents at end of year $ 189,005 176,940

See accompanying notes to consolidated financial statements.

5

BETH ISRAEL DEACONESS MEDICAL CENTER, INC.

AND AFFILIATES

Notes to Consolidated Financial Statements

September 30, 2011 and 2010

(In thousands)

6 (Continued)

(1) Organization and Mission

The accompanying consolidated financial statements include the accounts of Beth Israel Deaconess

Medical Center, Inc. and its subsidiaries, Medical Care of Boston Management Corporation, d/b/a The

Affiliated Physicians Group of Beth Israel Deaconess Medical Center (APG), and Beth Israel Deaconess

Hospital – Needham, Inc. (Needham), and its controlled affiliates, Harvard Medical Faculty Physicians at

Beth Israel Deaconess Medical Center, Inc. (HMFP), and Cardiovascular Management Associates, Inc.

(CVMA), (collectively, the Medical Center). Intercompany balances and transactions are eliminated in

consolidation. Beth Israel Deaconess Medical Center, Inc. (BIDMC) is an affiliate of CareGroup, Inc.

(CareGroup), its sole corporate member.

CareGroup is a regional healthcare delivery system comprised of teaching and community hospitals,

physician groups, and other caregivers. It is committed to personalized, patient-centered care, and

excellence in medical education and research. CareGroup serves the health needs of patients and

communities extending from north and south of Boston to the western suburbs beyond the Route 495 belt,

and is comprised of:

Four hospitals – BIDMC, Needham, Mount Auburn Hospital, and New England Baptist Hospital;

A committed medical staff offering community-based primary care and a wide range of specialty

services; and

A broad spectrum of comprehensive health services ranging from wellness programs to home care.

The CareGroup Obligated Group consists of CareGroup and certain of its subsidiaries and affiliates as

follows: BIDMC and its subsidiaries (APG and Needham), Mount Auburn Hospital and its subsidiary

(Mount Auburn Professional Services) and New England Baptist Hospital.

In September 2011, the Medical Center entered into an affiliation agreement with Milton Hospital, Inc.

(Milton) and its affiliates. Under the affiliation agreement, effective January 1, 2012, the Medical Center

became the sole corporate member of Milton and its Foundation.

(2) Summary of Significant Accounting Policies

(a) Basis of Presentation

The accompanying consolidated financial statements have been prepared in accordance with

U.S. generally accepted accounting principles and include the accounts of the Medical Center and its

affiliates. Intercompany balances and transactions are eliminated in consolidation.

The preparation of financial statements in conformity with U.S. generally accepted accounting

principles requires management to make estimates and assumptions that affect the amounts reported

in the financial statements and accompanying notes. Actual results could differ from those estimates.

The Medical Center considers events or transactions that occur after the consolidated balance sheet

date, but before the consolidated financial statements are issued, to provide additional evidence

BETH ISRAEL DEACONESS MEDICAL CENTER, INC.

AND AFFILIATES

Notes to Consolidated Financial Statements

September 30, 2011 and 2010

(In thousands)

7 (Continued)

relative to certain estimates or to identify matters that require additional disclosure. These

consolidated financial statements were issued on January 9, 2012 and subsequent events have been

evaluated through that date.

(b) Cash and Cash Equivalents

Cash and cash equivalents include investments in highly liquid debt instruments with a maturity of

three months or less when purchased, excluding amounts whose use is limited by internal

designation or other arrangements under trust agreements or by donors.

(c) Inventories

Inventories, consisting primarily of drugs and supplies, are stated at the lower of cost (first-in

first-out) or market.

(d) Investments and Assets Limited or Restricted as to Use

Investments and assets limited or restricted as to use primarily include assets restricted by donors,

assets set aside by the board and assets held by trustees under long-term debt and other agreements.

Internally designated assets may, at the board’s discretion, subsequently be used for other purposes.

Internally designated assets are classified as current assets because such amounts are available to

meet the Medical Center’s cash requirements.

(e) Investments and Investment Income

Investments are reported at fair value. Fair value is the price that would be received to sell an asset or

paid to transfer a liability in an orderly transaction between market participants at the measurement

date. See note 4 for a discussion of fair value measurements.

Investment income or loss (including realized gains and losses on investments, interest, and

dividends) and unrealized changes in equity interests in limited partnerships are included in the

excess of revenue over expenses unless the income is restricted by donor or law. Unrealized gains

and losses on marketable investments are excluded from the excess of revenue over expenses.

Periodically, the Medical Center reviews investments where the market value is substantially below

cost, and in cases where the decline is considered to be ―other than temporary,‖ an adjustment is

recorded as a realized loss and a new cost basis is established.

Certain investments are included in investment pools managed by CareGroup. Pooled investment

income and gains and losses are allocated to participating funds based upon the Medical Center’s

respective shares of the pool.

(f) Uncompensated Care and Provision for Bad Debts

The Medical Center provides care without charge or at amounts less than its established rates to

patients who meet certain criteria under its charity care policy.

BETH ISRAEL DEACONESS MEDICAL CENTER, INC.

AND AFFILIATES

Notes to Consolidated Financial Statements

September 30, 2011 and 2010

(In thousands)

8 (Continued)

The Medical Center grants credit without collateral to patients, most of whom are local residents and

are insured under third-party arrangements. Additions to the allowance for doubtful accounts are

made by means of the provision for bad debts. Accounts written off as uncollectible are deducted

from the allowance and subsequent recoveries are added. The amount of the provision for bad debts

is based upon management’s assessment of historical and expected net collections, business and

economic conditions, trends in federal and state governmental health care coverage and other

collection indicators.

(g) Property and Equipment

Property and equipment are stated at cost less accumulated depreciation. Depreciation is computed

using the straight-line method over the estimated useful lives of depreciable assets, which range from

three to forty years. Equipment under capitalized leases is stated at the present value of minimum

lease payments and is amortized using the straight-line method over the shorter period of the lease

term or the estimated useful life of the equipment. Such amortization is included with depreciation

expense.

Gifts of long-lived assets such as land, buildings, or equipment are reported as unrestricted support

(unless explicit donor stipulations specify how the donated assets must be used) and are excluded

from the excess of revenue over expenses. Gifts of long-lived assets with explicit restrictions that

specify how the assets are to be used, and gifts of cash or other assets that must be used to acquire

long-lived assets, are reported as restricted support. Absent explicit donor stipulations about how

long these long-lived assets must be maintained, expiration of donor restrictions are reported when

the donated or acquired long-lived assets are placed in service.

(h) Asset Retirement Obligations

The fair value of a liability for legal obligations associated with asset retirements is recognized in the

period in which it is incurred if a reasonable estimate of the fair value of the obligation can be made.

When a liability is initially recorded, the cost of the asset retirement obligation is capitalized by

increasing the carrying amount of the related long-lived asset. Over time, the liability is accreted to

its present value each period and the capitalized cost associated with the retirement is depreciated

over the useful life of the related asset. Upon settlement of the obligation, any difference between the

actual cost to settle the asset retirement obligation and the liability recorded is recognized as a gain

or loss in the consolidated statements of operations.

(i) Long-Lived Assets

Long-lived assets such as property plant and equipment are reviewed for impairment whenever

events or changes in circumstances indicate that the carrying amount of an asset may not be

recoverable. If circumstances require a long-lived asset be treated for possible impairment, the

Medical Center first compares undiscounted cash flows expected to be generated by an asset to the

carrying value of the asset. If the carrying value of the long-lived asset is not recoverable on an

undiscounted cash flow basis, an impairment is recognized to the extent that the carrying amount

exceeds its fair value. Fair value is determined through various valuation techniques including

BETH ISRAEL DEACONESS MEDICAL CENTER, INC.

AND AFFILIATES

Notes to Consolidated Financial Statements

September 30, 2011 and 2010

(In thousands)

9 (Continued)

discounted cash flow models, quoted market values and third-party independent appraisals, as

considered necessary.

(j) Self-Insurance

The Medical Center is self-insured for certain health insurance and workers’ compensation benefit

programs. Estimated losses and claims are accrued as incurred.

(k) Temporarily and Permanently Restricted Net Assets

Temporarily restricted net assets are those whose use by the Medical Center has been limited by

donors to a specific time period or purpose. Permanently restricted net assets have been restricted by

donors to be maintained by the Medical Center in perpetuity.

The Medical Center has interpreted state law as requiring realized and unrealized gains of

permanently restricted net assets to be retained in a temporarily restricted net asset classification

until appropriated by the board and expended. State law allows the board to appropriate so much of

the net appreciation of permanently restricted net assets as is prudent considering the Medical

Center’s long-and short-term needs, present and anticipated financial requirements, expected total

return on its investments, price level trends, and general economic conditions. Annually, the board

appropriates an amount based upon a 5% spending policy.

(l) Excess of Revenue over Expenses

The consolidated statements of operations include the excess of revenue over expenses from

operating and nonoperating activities. Operating revenues consist of those items attributable to the

care of patients, including contributions and investment income on unrestricted investments, which

are utilized to provide charity and other operational support. Peripheral activities, including realized

gains or losses on sales of securities and unrealized changes in equity interests in limited

partnerships, are reported as nonoperating gains.

Changes in unrestricted net assets, which are excluded from the excess of revenue over expenses

consistent with industry practice, include changes in unrealized gains or losses on marketable

investments, contributions of long-lived assets (including assets acquired using contributions which

by donor restriction were to be used for the purposes of acquiring such assets), transfers to or from

affiliates, and changes in the funded status of employee benefit plans, other than net periodic benefit

cost.

(m) Revenue Recognition

The Medical Center has entered into payment agreements with Medicare, Blue Cross, Medicaid, and

various commercial insurance carriers, health maintenance organizations, and preferred provider

organizations. The basis for payment under these agreements varies, and includes prospectively

determined rates per discharge or per visit, discounts from established charges, capitated rates, cost

(subject to limits), fee screens and prospectively determined daily rates.

BETH ISRAEL DEACONESS MEDICAL CENTER, INC.

AND AFFILIATES

Notes to Consolidated Financial Statements

September 30, 2011 and 2010

(In thousands)

10 (Continued)

Net patient service revenue is reported at the estimated net realizable amounts from patients,

third-party payors and others for services rendered, including estimated retroactive adjustments

under reimbursement agreements with third-party payors. Under the terms of various agreements,

regulations, and statutes, certain elements of third-party reimbursement are subject to negotiation,

audit, and/or final determination by the third-party payors. As a result, there is at least a reasonable

possibility that the recorded estimates will change by a material amount in the near term. Variances

between preliminary estimates of net patient service revenue and final third-party settlements are

included in net patient service revenue in the year in which the settlement or change in estimate

occurs. Changes in prior year estimated settlements with third party payors increased the excess of

revenue over expenses by approximately $2,721 in 2011 and $1,075 in 2010.

(n) Donations

Unconditional promises to give cash and other assets to the Medical Center are reported at fair value

at the date the promise is received. Conditional promises to give and indications of intentions to give

are reported at fair value at the date the gift is received or the conditional promise becomes

unconditional.

The gifts are reported as either temporarily or permanently restricted support if they are received

with donor stipulations that limit the use of the donated assets. When a donor restriction expires, that

is, when a stipulated time restriction ends or purpose restriction is accomplished, temporarily

restricted net assets are reclassified as unrestricted net assets and recorded as net assets released from

restrictions (which are included with other revenue or as direct additions to net assets if for capital).

(o) Debt Issuance Costs

Debt issuance costs and original issue discounts are amortized over the period the related obligation

is outstanding, generally using the interest method.

(p) Research Grants and Contracts

Revenue related to research grants and contracts is recognized as the related costs are incurred.

Indirect costs relating to certain government grants and contracts are reimbursed at fixed rates

negotiated with the government agencies. Amounts received in advance of incurring the related

expenditures are recorded as unexpended research grants and are included with accounts payable and

accrued expenses.

(q) Professional Liability

The Medical Center insures its professional liability risks on a claims-made basis in cooperation with

several other Harvard-affiliated healthcare organizations through a captive insurance company, of

which CareGroup holds a 10% ownership interest. The Medical Center maintains a program of

self-insurance to cover professional liability claims incurred but not reported to the captive insurance

company at year end. The estimated amount of accrued unasserted claims has been determined by

consulting actuaries on a discounted basis using an interest rate of 2.0% in 2011 and 2.5% in 2010.

BETH ISRAEL DEACONESS MEDICAL CENTER, INC.

AND AFFILIATES

Notes to Consolidated Financial Statements

September 30, 2011 and 2010

(In thousands)

11 (Continued)

(r) Income Tax Status

BIDMC, APG, Needham, CVMA and HMFP have been determined by the Internal Revenue Service

to be organizations described in Internal Revenue Code (the Code) Section 501(c)(3) and, therefore,

are exempt from federal income taxes on related income pursuant to Section 501(a) of the Code.

The Medical Center recognizes the effect of income tax positions only if those positions are more

likely than not of being sustained. Recognized income tax positions are measured at the largest

amount of benefit that is greater than fifty percent likely to be realized upon settlement. Changes in

recognition in measurement are reflected in the period in which the change in judgment occurs. The

Medical Center did not recognize the effect of any income tax positions in either 2011 or 2010.

(s) Fair Value of Financial Instruments

The carrying amount of cash and cash equivalents, patient accounts receivable, accounts payable and

accrued expenses approximate fair value because of the short maturity of these instruments.

Long-term debt instruments are carried at cost, which approximates fair value. Fair values are

estimated based on quoted market prices for the same or similar issues. Utilizing available market

pricing information provided by a third party, the Medical Center’s estimated fair value of long-term

debt as of September 30, 2011 is approximately $462,776.

(t) Recently Issued Accounting Pronouncements

In July 2011, the Financial Accounting Standards Board (FASB) issued Accounting Standards

Update (ASU) No. 2011-07, Health Care Entities (Topic 954): Presentation and Disclosure of

Patient Service Revenue, Provision for Bad Debts, and the Allowance for Doubtful Accounts for

Certain Health Care Entities (ASU 2011-07), which requires certain health care entities to change

the presentation of their statement of operations by reclassifying the provision for bad debts

associated with patient service revenue from an operating expense to a deduction from patient

service revenue (net of contractual allowances and discounts). Additionally, those health care entities

are required to provide enhanced disclosure about their policies for recognizing revenue and

assessing bad debts. The amendments also require disclosures of patient service revenue (net of

contractual allowances and discounts) as well as qualitative and quantitative information about

changes in the allowance for doubtful accounts. ASU 2011-07 is effective for the Medical Center’s

fiscal year beginning October 1, 2012, and the change in presentation is not expected to significantly

impact the Medical Center’s financial position, results of operations or cash flows.

In August 2010, the FASB issued ASU No. 2010-23, Health Care Entities (Topic 954): Measuring

Charity Care for Disclosure (ASU 2010-23), which standardizes cost as a basis for charity care

disclosures and specifies the elements of cost to be used in charity care disclosures. ASU 2010-23 is

effective for the Medical Center’s fiscal year beginning October 1, 2011 and is not expected to

significantly impact the Medical Center’s financial position, results of operations or cash flows

although additional disclosures may be required.

BETH ISRAEL DEACONESS MEDICAL CENTER, INC.

AND AFFILIATES

Notes to Consolidated Financial Statements

September 30, 2011 and 2010

(In thousands)

12 (Continued)

Also in August 2010, the FASB issued ASU No. 2010-24, Health Care Entities (Topic 954):

Presentation of Insurance Claims and Related Insurance Recoveries (ASU 2010-24), which

eliminates the practice of netting claim liabilities with expected related insurance recoveries for

balance sheet presentation. Claim liabilities are to be determined with no regard for recoveries and

presented gross. Expected recoveries are presented separately. ASU 2010-24 is effective for the

Medical Center’s fiscal year beginning October 1, 2011 and is not expected to significantly impact

the Medical Center’s financial position, results of operations or cash flows.

(u) Reclassifications

Certain amounts in the 2010 consolidated financial statements have been reclassified to conform to

the 2011 presentation.

(3) Community Service and Uncompensated Care

(a) Community Benefits

The Medical Center works in collaboration with residents of its service areas and with

community-based organizations to identify the healthcare needs of the community and to develop

strategies to improve the health status of community members. The Medical Center’s community

benefits program is focused particularly on underserved populations, and is designed to ensure that

the Medical Center is a welcoming and culturally competent organization for all patients and

employees.

The Medical Center works most closely with its seven affiliated community health centers to

conduct community health needs assessments and to develop appropriate interventions. The

priorities of the Medical Center’s community benefits program are to increase access to

community-based primary care and specialty services, to increase access to Medical Center specialty

services, and to reduce racial and ethnic disparities in the health status of underserved populations.

The Medical Center provides an annual report describing its community benefit activities to the

Massachusetts Attorney General’s office. The report summarizes progress made during the past year

as well as objectives and initiatives for the upcoming year. The Medical Center’s most recent report

for 2010 includes descriptions of community services and programs provided by the Medical Center

at a cost of approximately $12,844 (in addition to the cost of charity care provided). The Medical

Center is in the process of compiling its annual report for 2011.

(b) Charity Care

The Medical Center provides care without charge or at amounts less than its established rates to

patients who meet certain criteria under its charity care policy. Because the Medical Center does not

pursue collection of amounts determined to qualify as charity care, they are not reported as revenue

except to the extent reimbursed by the Massachusetts Health Safety Net Trust (Health Safety Net

Trust).

BETH ISRAEL DEACONESS MEDICAL CENTER, INC.

AND AFFILIATES

Notes to Consolidated Financial Statements

September 30, 2011 and 2010

(In thousands)

13 (Continued)

The Medical Center also makes payments to the Health Safety Net Trust to support the delivery of

charity care to patients throughout Massachusetts. These payments are reported as a component of

uncompensated care expense in the consolidated statements of operations.

The Medical Center’s net cost of charity care, including care for emergent services provided to

nonpaying patients and including payments to and receipts from the Health Safety Net Trust, was

$16,641 in 2011 and $12,656 in 2010 as follows:

2011 2010

Charity care, at cost $ 18,957 16,353 Payments to Health Safety Net Trust 8,992 9,278 Payments from Health Safety Net Trust (11,308) (12,975)

Net charity care $ 16,641 12,656

(c) Other Uncompensated Care

The Medical Center also provides care to patients who participate in other programs designed to

support low-income families, including particularly the Medicaid program, which is jointly funded

by federal and state governments. The Massachusetts Health Reform Law provided an initiative for

expansion of Medicaid coverage to greater populations and for enrollment of uninsured patients in

other insurance programs.

Payments from Medicaid and other programs which insure low-income populations do not cover the

cost of services provided. In aggregate, the cost of care provided by the Medical Center for such

services exceeded reimbursement by $24,794 and $22,999 in 2011 and 2010, respectively.

The Medical Center also provides care to patients who participate in the Medicare program, the

federally sponsored health insurance program for elderly or disabled patients. Because payments to

hospitals have not kept pace with inflation in recent years, payments to the Medical Center for those

services also do not cover the costs of services provided. In aggregate, the cost of care provided by

the Medical Center for such services exceeded reimbursement by $6,073 and $4,047 in 2011 and

2010, respectively.

(d) Bad Debts

In addition to charity care and shortfalls in providing services to patients insured under state and

federal programs, the Medical Center also incurs losses related to self-pay patients who fail to make

payments for services or insured patients who fail to pay coinsurance or deductibles for which they

are responsible under insurance contracts. Bad debt expense is included in uncompensated care

expense in the consolidated financial statements, and includes the provision for accounts anticipated

to be uncollectible. The estimated cost of providing such services was approximately $5,221 and

$5,348 in 2011 and 2010, respectively.

BETH ISRAEL DEACONESS MEDICAL CENTER, INC.

AND AFFILIATES

Notes to Consolidated Financial Statements

September 30, 2011 and 2010

(In thousands)

14 (Continued)

(4) Investments and Assets Limited or Restricted as to Use

The Medical Center invests in various investment securities. Investment securities are exposed to various

risks such as interest rate, market and credit risks. Due to the level of risk associated with certain

investment securities, it is at least reasonably possible that changes in the values of investment securities

will occur in the near term and that such changes could materially affect the amounts reported in the

consolidated financial statements.

Fair value represents the price that would be received upon the sale of an asset or paid upon the transfer of

a liability in an orderly transaction between market participants as of the measurement date. Financial

instruments that are measured and reported at fair value are classified and disclosed in one of the following

categories:

Level 1 – quoted prices (unadjusted) in active markets that are accessible at the measurement date

for assets or liabilities. Level 1 includes debt and equity securities that trade in an active exchange

market, as well as U.S. Treasury securities;

Level 2 – observable prices that are based on inputs not quoted in active markets, but corroborated

by market data. This category generally includes certain U.S. governmental and agency

mortgage-backed debt securities, corporate debt securities, and some alternative investments; and

Level 3 – unobservable inputs are used when little or no market data is available. Significant

professional judgment is used in determining the fair value assigned to such assets or liabilities. This

category includes financial instruments whose value is determined using pricing models, discounted

cash flow methodologies or similar techniques, as well as instruments for which the determination of

fair value requires significant management judgment or estimation. Investments that are included in

this category generally include limited partnerships, private equity, real estate funds, and hedge

funds.

Following is a description of the valuation methodologies used for assets at fair value:

Cash and cash equivalents: Money market funds are valued at the net asset value (NAV) reported by the

financial institution.

Equities: Valued at the closing price reported on an active market on which the individual securities are

traded.

Private equities, credit related, and real assets: The estimation of fair value of investments in investment

companies for which investment does not have a readily determinable value is made using the NAV per

share or its equivalent as a practical expedient.

The Medical Center owns interests in alternative investment funds rather than in the securities underlying

each fund and, therefore, it is generally required to consider such investments as Level 2 or 3 for purposes

of applying ASC 820-10, Fair Value Measurements, even though the underlying securities may not be

difficult to value or may be readily marketable. The Medical Center has applied the provisions of

BETH ISRAEL DEACONESS MEDICAL CENTER, INC.

AND AFFILIATES

Notes to Consolidated Financial Statements

September 30, 2011 and 2010

(In thousands)

15 (Continued)

Accounting Standards Update 2009-12, Investments in Certain Entities that Calculate Net Asset Value per

Share (or its Equivalent), for its alternative investments. This standard allows for the estimation of the fair

value of investments in investment companies for which the investment does not have a readily

determinable value using NAV per share or its equivalent as a practical expedient. The Medical Center has

utilized the NAV reported by each of the underlying funds as a practical expedient to estimate the value of

the investment. Also, because the Medical Center uses NAV as a practical expedient to estimate fair value,

the level in the fair value hierarchy in which each fund’s fair value measurement is classified is based

primarily on the Medical Center’s ability to redeem its interest in the fund at or near the date of the

consolidated balance sheet. Accordingly, the inputs or methodology used for valuing or classifying

investments for financial reporting purposes are not necessarily an indication of the risk associated with

investing in those investments or a reflection on the liquidity of each fund’s underlying assets and

liabilities.

Fixed income: The accounts invest principally in fixed income instruments and debt instruments. Account

investments are primarily valued using market quotations or prices obtained from independent pricing

sources which may employ various pricing methods to value the investments including matrix pricing.

The preceding methods may produce a fair value calculation that may not be indicative of net realizable

value or reflective of future fair values. Furthermore, although the Medical Center believes its valuation

methods are appropriate and consistent with other market participants, the use of different methodologies

or assumptions to determine the fair value of certain financial instruments could result in a different fair

value measurement at the reporting date.

The following table sets forth the Medical Center’s consolidated financial assets that were accounted for at

fair value on a recurring basis as of September 30, 2011. Investments are classified in their entirety based

on the lowest level of input that is significant to the fair value measurement and include related strategy,

liquidity, and funding commitments:

Redemption Days

Level 1 Level 2 Level 3 Total frequency notice

Investments:

Domestic equities $ 45,821 23,891 — 69,712 Daily – Quarterly 1 – 60Global equities — 64,452 19,713 84,165 Daily – Illiquid 1 – 30 and N/APrivate equity and venture capital — — 15,022 15,022 Illiquid N/AAbsolute return and hedged equity — 34,948 120,609 155,557 Quarterly – Illiquid 30 and N/A

Credit related — — 70,476 70,476 Annually – Illiquid N/AReal assets — — 31,121 31,121 Quarterly – Illiquid 360 and N/AFixed income 5,436 18,440 18,010 41,886 Daily – Illiquid 1 – 360

Cash and cash equivalents 199,315 — — 199,315 Daily 1Other equity securities — 2,075 — 2,075 Monthly 30

Total $ 250,572 143,806 274,951 669,329

BETH ISRAEL DEACONESS MEDICAL CENTER, INC.

AND AFFILIATES

Notes to Consolidated Financial Statements

September 30, 2011 and 2010

(In thousands)

16 (Continued)

Global equities of $84,165 noted in the table above are comprised of the following strategies: 28%

Developed Markets, 38% Global Value, 15% Emerging Markets (actively managed), 13% Emerging

Markets (fund of funds) and 6% Emerging/Frontier Market Small Cap.

Absolute return and hedged equity of $155,557 noted in the table above are comprised of the following

strategies: 55% Event Driven, 14% Global Long-Short, 9% Relative Value and 22% Open Mandate.

The following table presents additional information about the changes in Level 3 assets measured at fair

value for the year ended September 30, 2011:

Fair value measurements using significant unobservable inputsNet Changes in Transfers

Beginning purchases Net realized net unrealized into (out of) Endingbalance (sales) gains (losses) gains (losses) Level 3 balance

Global equities $ 526 23,603 (505) (3,911) — 19,713 Private equity and venture capital 11,114 2,069 700 1,139 — 15,022 Absolute return and hedged equity 93,575 24,264 265 (868) 3,373 120,609 Credit related 77,798 (3,053) (1,186) (3,083) — 70,476 Real assets 31,204 (1,102) 1,614 (595) — 31,121 Fixed income 14,121 3,546 — 343 — 18,010

Total $ 228,338 49,327 888 (6,975) 3,373 274,951

The following table describes the redemption frequency or liquidity of investments as of September 30,

2011:

Greater than

Weekly/ one year

Daily monthly Quarterly Annually and illiquid Total

Domestic equities $ 45,821 1,654 22,237 — — 69,712

Global equities 9,278 40,866 14,308 — 19,713 84,165 Private equity and venture capital — — — — 15,022 15,022 Absolute return and hedged equity — — 11,097 97,347 47,113 155,557 Credit related — — — 31,750 38,726 70,476

Real assets — — 5,142 — 25,979 31,121 Fixed income 23,879 — 4,137 — 13,870 41,886 Cash and cash equivalents 199,315 — — — — 199,315

Other equity securities — 2,075 — — — 2,075

Total $ 278,293 44,595 56,921 129,097 160,423 669,329

BETH ISRAEL DEACONESS MEDICAL CENTER, INC.

AND AFFILIATES

Notes to Consolidated Financial Statements

September 30, 2011 and 2010

(In thousands)

17 (Continued)

The following table sets forth the Medical Center’s consolidated financial assets that were accounted for at

fair value on a recurring basis as of September 30, 2010. Investments are classified in their entirety based

on the lowest level of input that is significant to the fair value measurement and include related strategy,

liquidity, and funding commitments:

Redemption Days

Level 1 Level 2 Level 3 Total frequency notice

Investments:

Domestic equities $ 14,186 44,967 — 59,153 Daily – Quarterly 1 – 60Global equities — 80,397 526 80,923 Daily – Illiquid 1 – 30 and N/APrivate equity and venture capital — — 11,114 11,114 Illiquid N/AAbsolute return and hedged equity — 63,218 93,575 156,793 Daily – Illiquid 30 and N/A

Credit related — — 77,798 77,798 Annually – Illiquid N/AReal assets — — 31,204 31,204 Quarterly – Illiquid 360 and N/AFixed income 6,128 19,208 14,121 39,457 Daily – Illiquid 1 – 360

Cash and cash equivalents 204,676 — — 204,676 Daily 1Other equity securities — 2,100 — 2,100 Monthly 30

Total $ 224,990 209,890 228,338 663,218

Global equities of $80,923 noted in the table above are comprised of the following strategies: 28%

Developed Markets, 34% Global Value, 12% Emerging Markets (actively managed), and 26% Emerging

Markets (fund of funds).

Absolute return and hedged equity of $156,793 noted in the table above are comprised of the following

strategies: 51% Event Driven, 19% Global Long-Short, 7% Relative Value and 23% Open Mandate.

The following table presents additional information about the changes in Level 3 assets measured at fair

value for the year ended September 30, 2010:

Fair value measurements using significant unobservable inputs

Net Changes in

Beginning purchases Net realized net unrealized Ending

balance (sales) gains (losses) gains (losses) balance

Global equities $ 2,389 (882) 238 (1,219) 526

Private equity and venture capital 8,982 1,275 (542) 1,399 11,114

Absolute return and hedged equity 76,195 12,289 1,364 3,727 93,575

Credit related 75,352 3,257 (1,088) 277 77,798

Real assets 28,720 825 (283) 1,942 31,204

Fixed income 13,925 — — 196 14,121

Total $ 205,563 16,764 (311) 6,322 228,338

BETH ISRAEL DEACONESS MEDICAL CENTER, INC.

AND AFFILIATES

Notes to Consolidated Financial Statements

September 30, 2011 and 2010

(In thousands)

18 (Continued)

The following table describes the redemption frequency or liquidity of investments as of September 30,

2010:

Greater than

Weekly/ one year

Daily monthly Quarterly Annually and illiquid Total

Domestic equities $ 27,781 3,719 27,653 — — 59,153

Global equities 13,762 53,317 13,318 — 526 80,923 Private equity and venture capital — — — — 11,114 11,114 Absolute return and hedged equity 369 — 51,170 60,939 44,315 156,793 Credit related — — — 29,366 48,432 77,798

Real assets — — 5,586 — 25,618 31,204 Fixed income 101 25,234 4,965 — 9,157 39,457 Cash and cash equivalents 204,676 — — — — 204,676

Other equity securities — 2,100 — — — 2,100

Total $ 246,689 84,370 102,692 90,305 139,162 663,218

Commitments

Private equity and venture capital, credit related, and real asset investments are generally made through

limited partnerships. Under the terms of these agreements, the Medical Center is obligated to remit

additional funding periodically as capital or liquidity calls are exercised by the manager. These

partnerships have a limited existence, generally up to ten years, At September 30, 2011 the Medical Center

projects that the commitments to these partnerships will be exercised by the managers as follows:

Private equityand venture Credit

Fiscal year capital related Real assets Total

2012 – 2021 $ 12,101 21,496 13,740 47,337

BETH ISRAEL DEACONESS MEDICAL CENTER, INC.

AND AFFILIATES

Notes to Consolidated Financial Statements

September 30, 2011 and 2010

(In thousands)

19 (Continued)

Investment income and gains (losses) on unrestricted investments and assets limited or restricted as to use

consisted of the following:

Year ended September 302011 2010

Unrestricted:Excess of revenue over expenses:

Dividends and income $ 298 925 Net realized gains on sales of investment

securities 11,591 7,426 Unrealized change in equity interests in limited

partnerships (3,713) 19,464

8,176 27,815

Change in net unrealized gains on investments (8,495) 3,597

(319) 31,412

Temporarily restricted:Dividends and income (139) (288) Net gains on investments (realized and unrealized) 688 14,037

549 13,749

$ 230 45,161

(5) Contributions Receivable

Contributions receivable, which are included within assets limited or restricted as to use in the consolidated

balance sheets, consisted of the following:

September 302011 2010

Due in less than one year $ 1,308 1,128 Due in one to five years 7,675 21,094 Due in more than five years 400 2,200

9,383 24,422

Less:Discount to present value at rates ranging

from 0.50% to 5.00% (1,298) (2,664) Allowance for uncollectible amounts (4,250) (8,400)

$ 3,835 13,358

BETH ISRAEL DEACONESS MEDICAL CENTER, INC.

AND AFFILIATES

Notes to Consolidated Financial Statements

September 30, 2011 and 2010

(In thousands)

20 (Continued)

(6) Property and Equipment

Property and equipment consisted of the following:

September 302011 2010

Land $ 26,086 25,520 Buildings and improvements 849,920 836,470 Equipment 1,118,763 1,068,067 Construction in progress 12,378 10,082

2,007,147 1,940,139

Less accumulated depreciation, net of disposals (1,456,262) (1,379,306)

$ 550,885 560,833

(7) Long-Term Debt

Long-term debt consisted of the following:

September 302011 2010

Fixed-rate debt:Massachusetts Health and Educational Facilities

Authority (MHEFA) Revenue Bonds:CareGroup Issue, Series A $ 49,275 161,975 CareGroup Issue, Series B 43,258 43,258 CareGroup Issue, Series E 237,990 250,400 Beth Israel Hospital Issue, Series H 4,735 5,820

Massachusetts Development FinanceAgency Revenue Bonds:

CareGroup Issue, Series F 106,690 — Net unamortized original issue premiums 3,899 3,727

445,847 465,180

Less current portion (21,265) (20,392)

$ 424,582 444,788

As defined in note 1, the Medical Center is a member of the CareGroup Obligated Group. Members of the

Obligated Group are jointly and severally liable for amounts outstanding under the CareGroup Series

Revenue Bonds, which aggregated $626,450 at September 30, 2011. The Obligated Group is required to

maintain a minimum number of days cash on hand, a minimum debt service coverage ratio, a maximum

BETH ISRAEL DEACONESS MEDICAL CENTER, INC.

AND AFFILIATES

Notes to Consolidated Financial Statements

September 30, 2011 and 2010

(In thousands)

21 (Continued)

debt capitalization ratio and comply with certain other covenants as specified in the Master Trust

Indenture. In addition, the Revenue Bonds are collateralized by a lien on gross receipts from each member

of the Obligated Group and a mortgage on certain property of each hospital in the Obligated Group. The

Medical Center is also obligated under MHEFA Series H Revenue Bonds.

In September 2011, the Obligated Group refunded a portion of its Series A Bonds, including $105,803 of

the $155,078 Series A Bonds held by the Medical Center. The refunding was completed through the

issuance of CareGroup Series F Bonds, of which $106,690 is held by the Medical Center. As a result of the

refinancing, the Medical Center recorded a loss on the early extinguishment of debt of $2,131.

Under the terms of the CareGroup Series B Bonds, the Medical Center has the option of recycling each

annual principal payment into a new loan with a separate payment schedule, but with terms identical to the

original debt. The Medical Center has historically elected to recycle these principal payments on an annual

basis. The Medical Center intends to continue to recycle its principal payments and, therefore, has

classified all of its Series B debt as long-term.

The Medical Center’s revenue bonds bear interest, mature and are redeemable prior to maturity as follows:

Issue Interest rate Maturity Redemption terms

CareGroup:Series A Fixed 5.0% 2025 Currently at 100%Series B Fixed 4.5% to 5.4% 2028 Beginning in 2018 at 100%Series E Fixed 4.0% to 5.4% 2038 Beginning in 2018 at 100%Series F Fixed 2.1% to 3.1% 2022 Currently with conditions

Beth Israel Hospital:Series H Fixed 4.0% to 4.5% 2015 Not optionally redeemable

Scheduled principal repayments and sinking fund requirements on long-term debt for the next five years

are as follows:

2012 $ 21,265 2013 22,075 2014 23,060 2015 23,975 2016 23,870

Interest paid on all outstanding debt amounted to $24,436 and $24,323 for 2011 and 2010, respectively.

(8) Assets Held by Trustees

Assets held by trustees include amounts held in trust under the requirements of various debt and other

agreements. The terms of the Revenue Bonds require the establishment of certain reserve funds which are

BETH ISRAEL DEACONESS MEDICAL CENTER, INC.

AND AFFILIATES

Notes to Consolidated Financial Statements

September 30, 2011 and 2010

(In thousands)

22 (Continued)

held by trustees. These funds, principally comprised of cash, cash equivalents, and government securities,

are carried at fair market value and are as follows:

September 302011 2010

Debt agreements:Construction fund $ — 1,651 Debt service reserve funds 19,509 20,060 Debt service funds 6,316 6,335

$ 25,825 28,046

(9) Leases

The Medical Center leases office and research space under various operating leases. Minimum lease

payments under these noncancelable operating leases at September 30, 2011 were as follows:

Year ending September 30:2012 $ 39,849 2013 37,226 2014 34,868 2015 32,546 2016 32,311 Thereafter 206,113

$ 382,913

The Medical Center has entered into agreements to sublease portions of its leased space, which will

provide income of approximately $6,500 per year from 2012 through 2018. Rent expense amounted to

approximately $43,364 and $42,866 for the years ended September 30, 2011 and 2010, respectively.

In connection with one of its leases, the Medical Center has secured an irrevocable letter of credit in an

amount equal to six months of the base rent, or $9,314.

(10) Employee Benefit Plans

(a) Pension Benefits

The Medical Center participates in a noncontributory defined benefit pension plan and defined

contribution plans covering substantially all of its employees.

Defined Benefit Plan

The Beth Israel Deaconess Medical Center Pension Plan (the Plan) covers employees of the Medical

Center, CareGroup, and certain other of its subsidiaries. The Medical Center recognizes the funded

BETH ISRAEL DEACONESS MEDICAL CENTER, INC.

AND AFFILIATES

Notes to Consolidated Financial Statements

September 30, 2011 and 2010

(In thousands)

23 (Continued)

status, the difference between the fair value of the plan assets and the projected benefit obligation, of

its defined benefit pension plan as an asset or liability in its consolidated balance sheet and

recognizes the change in that funded status in the year in which the change occurred through changes

in unrestricted net assets.

The measurement date used to determine pension assets and obligations was September 30.

The following table sets forth the Plan’s funded status and amounts recognized in the consolidated

balance sheets:

September 302011 2010

Change in benefit obligation:Benefit obligation at beginning of year $ 442,480 400,229 Service cost 18,158 15,513 Interest cost 20,496 21,327 Benefits paid (14,613) (14,585) Plan amendments — (18,034) Actuarial (gain) loss (342) 38,030

Benefit obligation at end of year $ 466,179 442,480

September 302011 2010

Change in plan assets:Fair value of plan assets at beginning of year $ 330,129 303,969 Actual return on plan assets 1,040 24,745 Employer contributions 18,000 16,000 Benefits paid (14,613) (14,585)

Fair value of plan assets at end of year $ 334,556 330,129

Funded status:Net pension liability at end of year $ (131,623) (112,351)

The accumulated benefit obligation for the defined benefit pension plan was $408,367 and $385,899

at September 30, 2011 and 2010, respectively.

BETH ISRAEL DEACONESS MEDICAL CENTER, INC.

AND AFFILIATES

Notes to Consolidated Financial Statements

September 30, 2011 and 2010

(In thousands)

24 (Continued)

Amounts not yet reflected in net periodic pension expense and included in the change in unrestricted

net assets are as follows:

September 302011 2010

Net actuarial loss $ (156,111) (139,058) Prior service credit 17,758 21,121

$ (138,353) (117,937)

The estimated amount that will be amortized from unrestricted net assets into net periodic pension

expense in 2012 is $8,375.

Net periodic pension expense is comprised of the components listed below:

Year ended September 302011 2010

Service cost for benefits earned during the year $ 18,158 15,513 Interest cost on projected benefit obligation 20,496 21,327 Expected return on plan assets (27,701) (24,991) Amortization of net actuarial loss 9,268 5,957 Net amortization (3,363) (1,914)

Net periodic pension expense $ 16,858 15,892

The following assumptions were used to determine net periodic pension expense and benefit

obligation:

2011 2010

Weighted average discount rate (pension cost) 4.75% 5.55%Weighted average discount rate (benefit obligation) 4.75 4.75Rate of increase in future compensation 4.50 4.50Expected long-term rate of return on plan assets 8.00 8.50

The methodology for selecting the discount rate for the Plan is to match the plan’s cash flow to that

of a yield curve that provides the equivalent yield on zero-coupon corporate bonds for each maturity

based on the expected duration of the benefit payments for the Plan as of the annual measurement

date, subject to change each year.

The Plan’s overall investment objective is to provide a long-term return that is expected to meet

future benefit payment requirements. A long-term horizon has been adopted in establishing

BETH ISRAEL DEACONESS MEDICAL CENTER, INC.

AND AFFILIATES

Notes to Consolidated Financial Statements

September 30, 2011 and 2010

(In thousands)

25 (Continued)

investment policy such that the likelihood and duration of investment losses are carefully weighed

against the long-term potential for appreciation of assets. The Plan’s investment policy requires

investments to be diversified across individual securities, industries, market capitalization, and

valuation characteristics. In addition, various techniques are utilized to monitor, measure, and

manage risk.

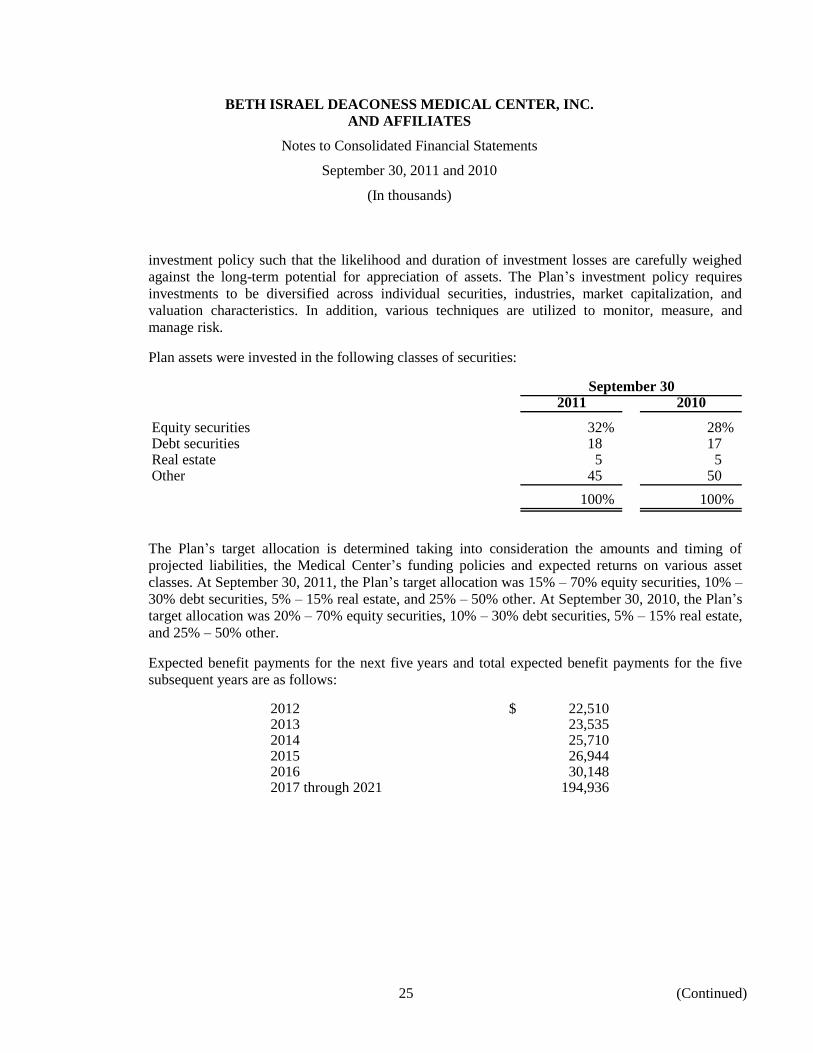

Plan assets were invested in the following classes of securities:

September 302011 2010

Equity securities 32% 28%Debt securities 18 17Real estate 5 5Other 45 50

100% 100%

The Plan’s target allocation is determined taking into consideration the amounts and timing of

projected liabilities, the Medical Center’s funding policies and expected returns on various asset

classes. At September 30, 2011, the Plan’s target allocation was 15% – 70% equity securities, 10% –

30% debt securities, 5% – 15% real estate, and 25% – 50% other. At September 30, 2010, the Plan’s

target allocation was 20% – 70% equity securities, 10% – 30% debt securities, 5% – 15% real estate,

and 25% – 50% other.

Expected benefit payments for the next five years and total expected benefit payments for the five

subsequent years are as follows:

2012 $ 22,510 2013 23,535 2014 25,710 2015 26,944 2016 30,148 2017 through 2021 194,936

BETH ISRAEL DEACONESS MEDICAL CENTER, INC.

AND AFFILIATES

Notes to Consolidated Financial Statements

September 30, 2011 and 2010

(In thousands)

26 (Continued)

Defined Benefit Plan Fair Value Measurements

The following is a summary of the Plan’s investments as of September 30, 2011 at fair value, using

the hierarchy of values described in note 4:

Level 1 Level 2 Level 3 Total

Investments:Domestic equities $ 28,284 16,044 — 44,328 Global equities — 43,420 3,087 46,507 Private equity and

venture capital — — 15,219 15,219 Absolute return and

hedged equity — 26,407 80,403 106,810 Credit related — — 42,999 42,999 Real assets — — 15,938 15,938 Cash and cash equivalents 62,755 — — 62,755

Total $ 91,039 85,871 157,646 334,556

Global equities of $46,507 noted in the table above are comprised of the following strategies: 31%

Developed Markets, 31% Global Value, 5% Emerging Markets (actively managed), 26% Emerging

Markets (fund of funds) and Emerging/Frontier markets small cap 7%.

Absolute return and hedged equity of $106,810 noted in the table above are comprised of the

following strategies: 57% Event Driven, 13% Global Long-Short, 8% Relative Value, and 22% Open

Mandate.

The following table presents additional information about the changes in Level 3 assets measured at

fair value for the year ended September 30, 2011:

Fair value measurements using significant unobservable inputs

Net Changes in Transfers

Beginning purchases Net realized net unrealized into (out of) Ending

balance (sales) gains (losses) gains (losses) Level 3 balance

Global equities $ 638 3,199 (737) (13) — 3,087 Private equity and

venture capital 10,778 1,504 1,144 1,793 — 15,219 Absolute return and —

hedged equity 72,796 4,074 4,289 (4,616) 3,860 80,403

Credit related 47,669 (3,640) 1,304 (2,334) — 42,999 Real assets 13,673 1,529 502 234 — 15,938

Total $ 145,554 6,666 6,502 (4,936) 3,860 157,646

BETH ISRAEL DEACONESS MEDICAL CENTER, INC.

AND AFFILIATES

Notes to Consolidated Financial Statements

September 30, 2011 and 2010

(In thousands)

27 (Continued)

The following is a summary of the Plan’s investments as of September 30, 2010 at fair value, using

the hierarchy of values described in note 4:

Level 1 Level 2 Level 3 Total

Investments:Domestic equities $ 6,547 29,646 — 36,193 Global equities — 46,762 638 47,400 Private equity and

venture capital — — 10,778 10,778 Absolute return and

hedged equity — 47,030 72,796 119,826 Credit related — — 47,669 47,669 Real assets — — 13,673 13,673 Cash and cash equivalents 54,590 — — 54,590

Total $ 61,137 123,438 145,554 330,129

Global equities of $47,400 noted in the table above are comprised of the following strategies: 24%

Developed Markets, 32% Global Value, 13% Emerging Markets (actively managed), and 31%

Emerging Markets (fund of funds).

Absolute return and hedged equity of $119,826 noted in the table above are comprised of the

following strategies: 53% Event Driven, 20% Global Long-Short, 6% Relative Value and 21% Open

Mandate.

The following table presents additional information about the changes in Level 3 assets measured at

fair value for the year ended September 30, 2010:

Fair value measurements using significant unobservable inputs

Net Changes in

Beginning purchases Net realized net unrealized Ending

balance (sales) gains (losses) gains (losses) balance

Global equities $ 2,711 (968) 248 (1,353) 638

Private equity and

venture capital 8,783 929 (311) 1,377 10,778

Absolute return and

hedged equity 57,002 7,797 994 7,003 72,796

Credit related 46,362 (4,258) 720 4,845 47,669

Real assets 12,978 1,375 (973) 293 13,673

Total $ 127,836 4,875 678 12,165 145,554

BETH ISRAEL DEACONESS MEDICAL CENTER, INC.

AND AFFILIATES

Notes to Consolidated Financial Statements

September 30, 2011 and 2010

(In thousands)

28 (Continued)

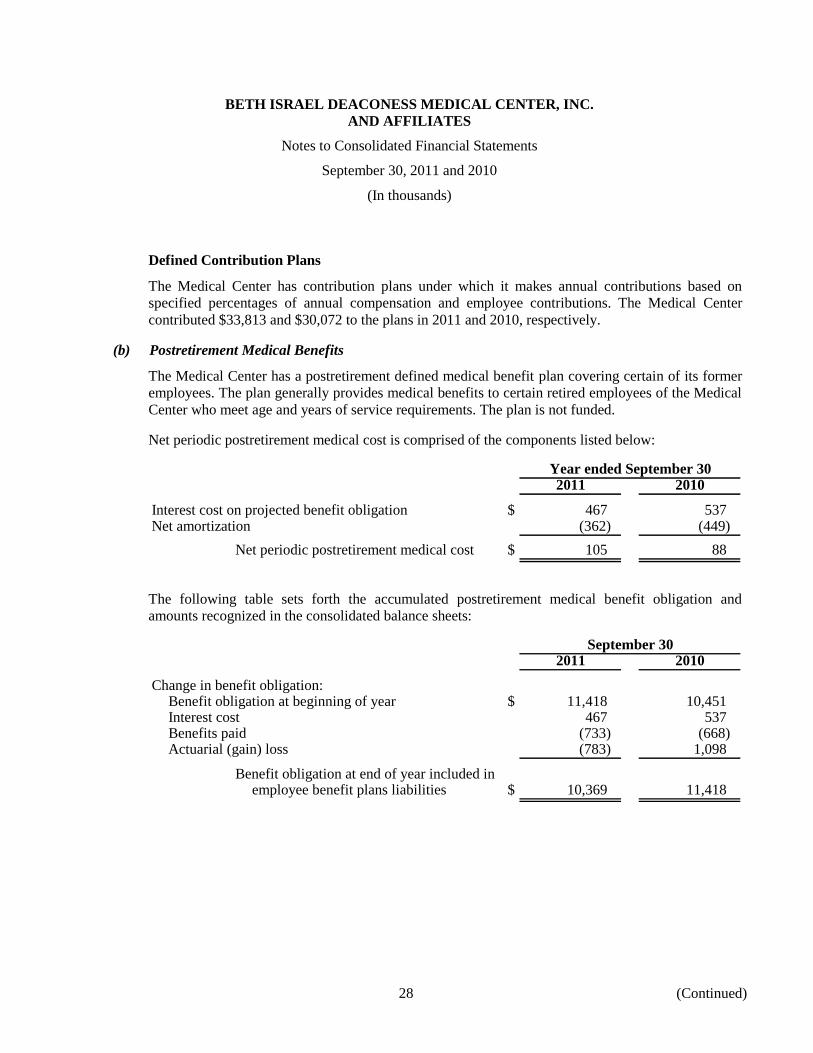

Defined Contribution Plans

The Medical Center has contribution plans under which it makes annual contributions based on

specified percentages of annual compensation and employee contributions. The Medical Center

contributed $33,813 and $30,072 to the plans in 2011 and 2010, respectively.

(b) Postretirement Medical Benefits

The Medical Center has a postretirement defined medical benefit plan covering certain of its former

employees. The plan generally provides medical benefits to certain retired employees of the Medical

Center who meet age and years of service requirements. The plan is not funded.

Net periodic postretirement medical cost is comprised of the components listed below:

Year ended September 302011 2010

Interest cost on projected benefit obligation $ 467 537 Net amortization (362) (449)

Net periodic postretirement medical cost $ 105 88

The following table sets forth the accumulated postretirement medical benefit obligation and

amounts recognized in the consolidated balance sheets:

September 302011 2010

Change in benefit obligation:Benefit obligation at beginning of year $ 11,418 10,451 Interest cost 467 537 Benefits paid (733) (668) Actuarial (gain) loss (783) 1,098

Benefit obligation at end of year included inemployee benefit plans liabilities $ 10,369 11,418

BETH ISRAEL DEACONESS MEDICAL CENTER, INC.

AND AFFILIATES

Notes to Consolidated Financial Statements

September 30, 2011 and 2010

(In thousands)

29 (Continued)

Amounts not yet reflected in net periodic postretirement medical benefit cost and included in the

change in unrestricted net assets are as follow:

Year ended September 302011 2010

Prior service credit $ 1,279 1,728 Net actuarial loss (1,060) (1,930)

$ 219 (202)

In determining the accumulated postretirement medical benefit obligation, the Medical Center used a

discount rate of 4.4% and 4.2% in 2011 and 2010, respectively, and an assumed healthcare cost trend

rate of 8.5%, trending down to 5% in 2018 and thereafter. Increasing the assumed healthcare cost

trend rates by one percentage point in each year would increase the accumulated postretirement

medical benefit obligation as of September 30, 2011 by $1,020 and the net periodic postretirement

medical benefit cost for the year then ended by $44.

(11) Temporarily and Permanently Restricted Net Assets

Temporarily restricted net assets consisted of the following:

September 302011 2010

Donor restricted for research and other $ 68,867 83,653 Accumulated net realized and unrealized gains on permanently

restricted donations subject to spending policy 43,669 45,445

$ 112,536 129,098

Permanently restricted net assets consisted of the following:Donor restricted for research and other $ 49,718 48,505

(12) Endowment

The Medical Center’s endowment consists of approximately nine hundred individual funds established for

a variety of purposes. Net assets associated with endowment funds are classified and reported based on the

existence or absence of donor-imposed restrictions.

(a) Relevant Law

The Massachusetts Uniform Prudent Management of Institutional Funds Act (UPMIFA) permits the

governing board to exercise its discretion in determining the appropriate level of expenditures from a

donor-restricted endowment fund in accordance with a set of guidelines about what constitutes

prudent spending. UPMIFA permits the Medical Center to appropriate for expenditure or accumulate

BETH ISRAEL DEACONESS MEDICAL CENTER, INC.

AND AFFILIATES

Notes to Consolidated Financial Statements

September 30, 2011 and 2010

(In thousands)

30 (Continued)

so much of an endowment fund as the Medical Center determines to be prudent for the uses, benefits,

purposes and duration for which the endowment fund is established. Seven criteria are to be used to

guide the Medical Center in its yearly expenditure decisions: 1) duration and preservation of the

endowment fund; 2) the purposes of the Medical Center and the endowment fund; 3) general

economic conditions; 4) effect of inflation or deflation; 5) the expected total return from income and

the appreciation of investments; 6) other resources of the Medical Center and 7) the investment

policy of the Medical Center.

Although UPMIFA offers short-term spending flexibility, the explicit consideration of the

preservation of funds among factors for prudent spending suggests that a donor-restricted

endowment fund is still perpetual in nature. Under UPMIFA, the Board is permitted to determine and

continue a prudent payout amount, even if the market value of the fund is below historic dollar value.

There is an expectation that, over time, the permanently restricted amount will remain intact. This

perspective is aligned with the accounting standards definition that permanently restricted funds are

those that must be held in perpetuity even though the historic-dollar-value may be dipped into on a

temporary basis.

In accordance with appropriate accounting standards, the Medical Center classifies as permanently

restricted net assets (a) the original value of gifts donated to the permanent endowment, (b) the

original value of subsequent gifts to the permanent endowment, and (c) accumulations to the

permanent endowment made in accordance with the direction of the applicable donor gift instrument

at the time the accumulation is added to the fund. The remaining portion of the donor-restricted

endowment fund that is not classified as permanently restricted net assets is classified as temporarily

restricted net assets until appropriated for spending by the Board of Directors.

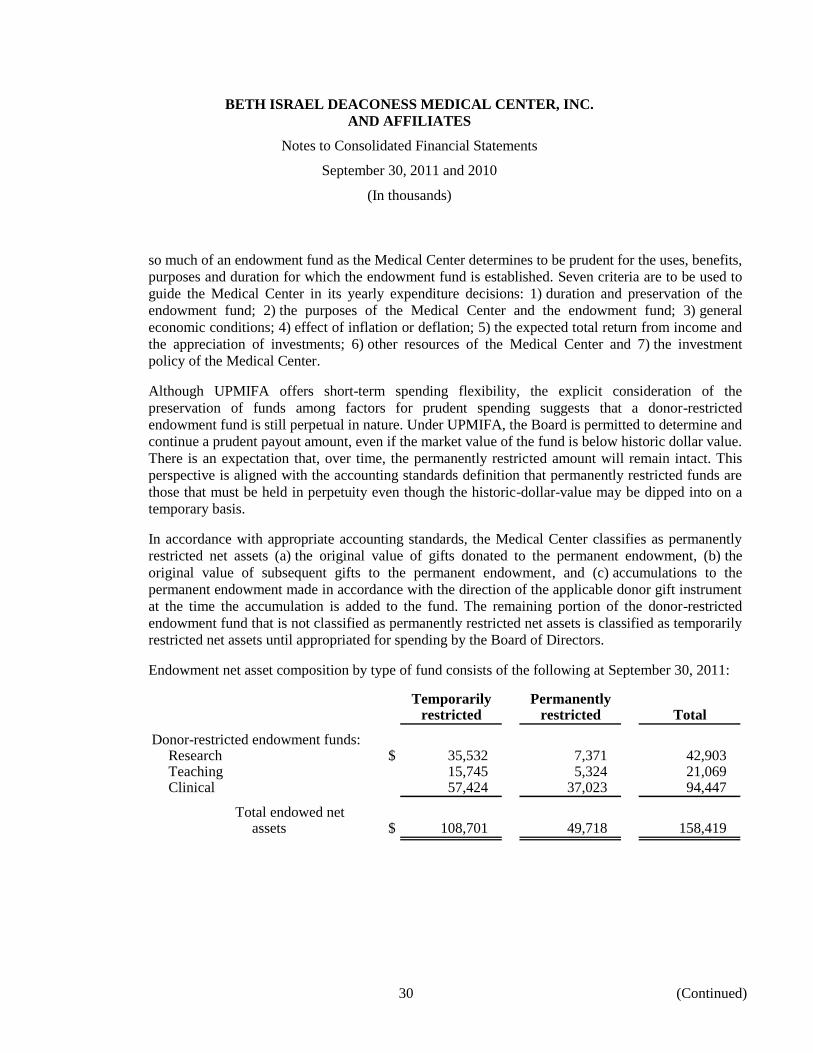

Endowment net asset composition by type of fund consists of the following at September 30, 2011:

Temporarily Permanentlyrestricted restricted Total

Donor-restricted endowment funds:Research $ 35,532 7,371 42,903 Teaching 15,745 5,324 21,069 Clinical 57,424 37,023 94,447

Total endowed netassets $ 108,701 49,718 158,419

BETH ISRAEL DEACONESS MEDICAL CENTER, INC.

AND AFFILIATES

Notes to Consolidated Financial Statements

September 30, 2011 and 2010

(In thousands)

31 (Continued)

Changes in endowment net assets for the year ended September 30, 2011 are as follows:

Temporarily Permanentlyrestricted restricted Total

Endowment net assets,September 30, 2010 $ 115,740 48,505 164,245

Investment return:Investment income, net 549 — 549

Total investment return 549 — 549

Contributions 7,383 1,213 8,596 Appropriation of endowment

assets for expenditure (14,971) — (14,971)

Endowment net assets,September 30, 2011 $ 108,701 49,718 158,419

Endowment net asset composition by type of fund consists of the following at September 30, 2010:

Temporarily Permanentlyrestricted restricted Total

Donor-restricted endowment funds:Research $ 37,549 7,124 44,673 Teaching 16,006 4,949 20,955 Clinical 62,185 36,432 98,617

Total endowed netassets $ 115,740 48,505 164,245

BETH ISRAEL DEACONESS MEDICAL CENTER, INC.

AND AFFILIATES

Notes to Consolidated Financial Statements

September 30, 2011 and 2010

(In thousands)

32 (Continued)

Changes in endowment net assets for the year ended September 30, 2010 are as follows:

Temporarily Permanentlyrestricted restricted Total

Endowment net assets,September 30, 2009 $ 107,143 46,395 153,538

Investment return:Investment income, net 13,749 — 13,749

Total investment return 13,749 — 13,749

Contributions 6,345 2,110 8,455 Appropriation of endowment

assets for expenditure (11,497) — (11,497)

Endowment net assets,September 30, 2010 $ 115,740 48,505 164,245

(b) Funds with Deficiencies

From time to time, the fair value of assets associated with individual donor-restricted endowment

funds may fall below their original contributed value. There were no such deficiencies as of

September 30, 2011 or 2010.

(c) Return Objectives and Risk Parameters

The Medical Center has adopted investment and spending policies for endowment assets that attempt

to provide a predictable stream of funding to programs supported by its endowment while seeking to

maintain the purchasing power of the endowment assets. Endowment assets include those assets of

donor-restricted funds that the Medical Center must hold in perpetuity or for a donor-specified

period. The primary investment objective of the management of the endowment fund is to maintain

and grow the fund’s real value by generating average annual real returns that meet or exceed the

spending rate, after inflation, management fees and administrative costs. Consistent with this goal,

the Board of Directors and the Investment Committee intend that the endowment fund be managed

with an intention to maximize total returns consistent with prudent levels of risk and reduce portfolio

risk through asset allocation and diversification.

(d) Strategies Employed for Achieving Objectives

To satisfy its long-term rate-of-return objectives, the Medical Center relies on a total return strategy

in which investment returns are achieved through both capital appreciation (realized and unrealized)

and current yield (interest and dividends). The asset allocation policy is designed to attempt to

achieve diversity among capital markets and within capital markets, by investment discipline and

management style. The investment portfolio is designed in light of the endowment’s needs for

liquidity, preservation of purchasing power and risk tolerances. There is no limitation on the types of

BETH ISRAEL DEACONESS MEDICAL CENTER, INC.

AND AFFILIATES

Notes to Consolidated Financial Statements

September 30, 2011 and 2010

(In thousands)

33 (Continued)

investments in which the endowment fund may be invested, and it is intended that the investment

managers have the broadest flexibility as to the selection of investments for the endowment fund.

The Medical Center targets a diversified asset allocation that places emphasis on investments in

domestic and international equities, fixed income, real assets, private equity, and hedge funds

strategies to achieve its long-term return objectives within prudent risk constraints.

(e) Spending Policy and How the Investment Objectives Relate to Spending Policy

Under the Medical Center’s current long-term investment spending policy, which is within the

guidelines specified under state law, 5% of the average of the fair value of qualifying long-term

investments applied to a three-year moving average with a one-year lag is appropriated. This

amounted to $1,336 and $983 for the years ending September 30, 2011 and 2010, respectively.

In establishing these policies, the Medical Center considered the expected return on its endowment

and its programming needs. Accordingly, the Medical Center expects the current spending policy to

allow its endowment to maintain its purchasing power and to provide a predictable and stable source

of revenue to the annual operating budget. Additional real growth will be provided through new gifts

or excess investment return.

(13) Concentrations of Credit Risk

The Medical Center grants credit without collateral to its patients, many of whom are local residents and

are insured under third-party payor agreements. Management estimates that patient accounts receivable,

net of contractual allowances, were comprised as follows:

September 302011 2010

Medicare 26% 27%Medicaid 13 10Blue Cross 20 20Commercial insurance and managed care 28 31Patient 7 6Other 6 6

100% 100%

The Medical Center maintains its cash accounts at various financial institutions. Accounts at certain

financial institutions are insured up to $250 per depositor by the Federal Deposit Insurance Corporation

(FDIC). At September 30, 2011, the Medical Center had cash balances of $100,746 in excess of insured

limits at such institutions.

BETH ISRAEL DEACONESS MEDICAL CENTER, INC.

AND AFFILIATES

Notes to Consolidated Financial Statements

September 30, 2011 and 2010

(In thousands)

34 (Continued)

The Medical Center has not experienced any losses in such amounts and evaluates the creditworthiness of

the financial institutions with which it conducts business. Management believes the Medical Center is not

exposed to any significant credit risk with respect to its cash balances.

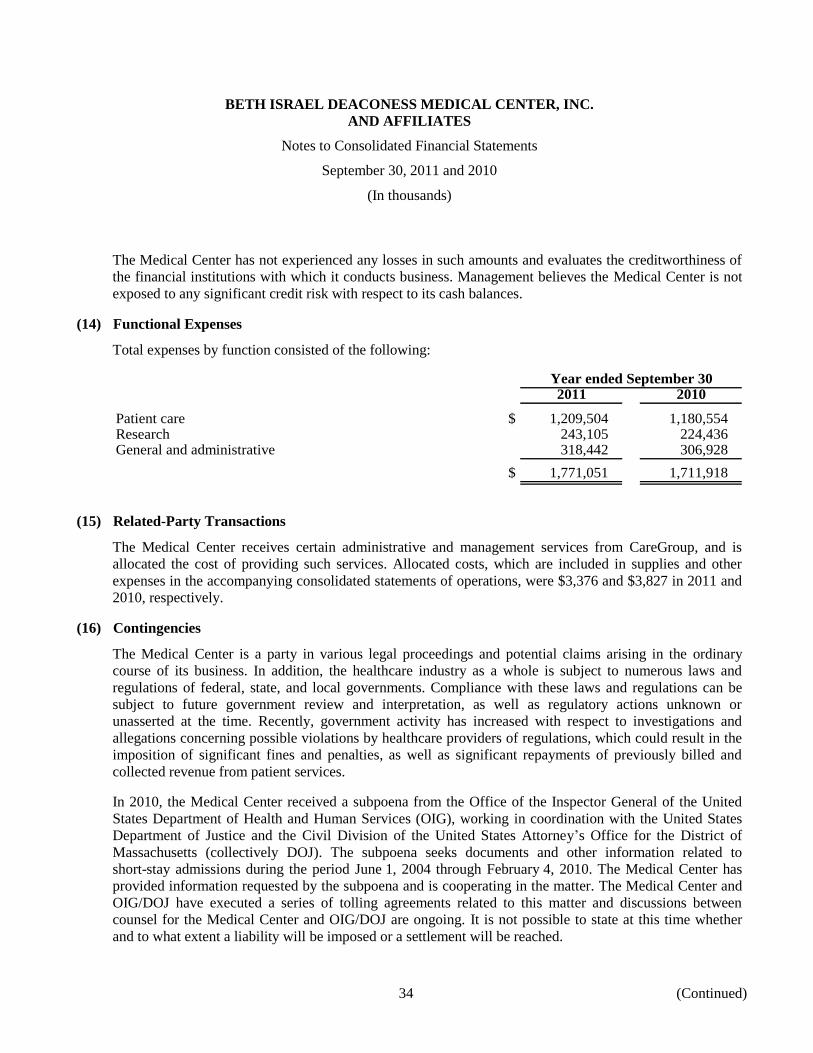

(14) Functional Expenses

Total expenses by function consisted of the following:

Year ended September 302011 2010

Patient care $ 1,209,504 1,180,554 Research 243,105 224,436 General and administrative 318,442 306,928

$ 1,771,051 1,711,918

(15) Related-Party Transactions

The Medical Center receives certain administrative and management services from CareGroup, and is

allocated the cost of providing such services. Allocated costs, which are included in supplies and other

expenses in the accompanying consolidated statements of operations, were $3,376 and $3,827 in 2011 and

2010, respectively.