-

8/12/2019 Binomial Option Chance

1/20

A Synthesis of Binomial OptionPricing iVIodels for

LognormaiiyDistributed Assets

Don M Chance

The fmance literature has revealed no fewer than Ialternative

versions of the binomial option pricingmod el for options on

lognorm aiiy distribute d assets.These models are derived under a

variety ofassumptions and in some cases require informationthat is

ordinarily unnece ssary to value options. T hispaper provides a

review and synthesis of thesemodels, showing their commonalities

and differencesand demonstrating how 1 diverse models all

producethe samere sultin the limit. Some of the models

admitarbitrage with a finite number of time steps and somefail to

capture the correct volatility. T his paper alsoexamines the

convergence properties of each m odeland finds that none exhibit

consistently superiorperformance overthe others. Finally, it

demonstrateshow a general model that accepts any arbitrage-freerisk

neutral probability will reproduce the Black-Scholes-Merton model

in the limit.

Option pricing theory has become one of the mostpowerful tools

in economics and finance. The celebratedBlack-Scholes-Merton model

not only led to a NobelPrize but completely redefined the financial

industry.Its sister model, the binomial or two-state model, hasalso

attracted much attention and acclaim., both for itsability to

illustrate the essential ideas behind optionpricing theory with a

minimum of mathematics and tovalue many complex options.Don M.

Chance is a Professor of Finance at Louisiana StateUniversity in

Balon Rouge. LA 70803.The author thanks Jim HilHard Boh Brooks,

Tung-Hsiao Yang.To m Arnold Adam Schwartz, and an anonymous referee

forhetpful comments. A document containing detailed proofs

andsupporting results is available on the Journal's web site or

canbe obtained by emaiiing the author.

The origins of the binomial model are somewhatunclear . Options

folklore has i t that around 1975William Sharpe, latert win a Nobel

Prize for his seminalwork on the Capital Asset Pricing Model,

suggestedto Mark Rubinstein that option valuation should befeasible

under the assumption that the underlyingstock price can change to

one of only two possibleoutcomes. Sharpe subsequently developed the

ideain the first edition of his textbook.^ Perhaps the best-known

and most widely cited original paper on themodel is Cox, R oss, and

Rubinstein {1979), but almosts imul t aneous ly , Rend leman and

Bar t t e r ( 1979)presented the same model in a sl ightly

differentmanner.

Over the years, there has been an extensive bodyof research

design ed to improv e tbe model.^ In theliterature the model has

appeared in a variety of forms.Anyone at tempt ing to understand

the model canbecome bewildered by the array of formulas that

allpurport to accomplish the desired result of showinghow to value

an option and hedge an option position.These formulas have many

similarities but notable

Not s urprisingly , this story do es not appear form ally in

theoptions literature but is related by Mark Rubinstein inRiskBooks

(2003, p. 581).See Sharpe, Alexander, and Bailey (1998) for the c

urrentedition of this book.See . for example, Boyle (1988), Om berg

(1988). Tian (19 93).Figlewski and Gao (1999), Baule and Wilkens

(2004) (fortrinomials). He (1990) (for multiple state variables),

andRogers and Stapleton (1998). Breen (1991). Broadie andDetemple

(1997). and Joshi (2007) (for American optionpricing). See also

Widdicks, Andricopoulos, Newton, and Duck(2002). Walsh (2003),

Johnson, Pawlukicwicz, and Mehta(1997) for various other

modifications, and Leisen and Reimer(1996) for a study of the m

odel s convergence.

-

8/12/2019 Binomial Option Chance

2/20

CH NCE SYNTHESIS OF BINOMI L OPTION PRICING MODELS

39differences. Ano ther source of confusion is that someprese n ta

t io ns use oppo s i t e no ta t ion .* But m orefundamentally, the

obvious question is how so manydifferent candidates for the inputs

of the binomialmodel can exist and how each can technically

becorrect.

The objective of this paper is to synthesize thedifferent

approaches within a body of uniform notationand provide a coherent

treatment of each model. Eachmodel is presented with i ts distinct

assumptions.Detailed derivations are om itted but are available in

asupplemental docum ent on the journal website or fromthe

author.Some would contend that it is wasteful to study amodel that,

for European options, in the limit equalsthe Black-Scholes-Me rton

model. Use of the binomialmodel, they would argue, serves only a

pedagogicalpurpose. But it is difficult to consider the

binomialmodel as a method for deriving the values of morecomplex

options without knowing how well it worksfor the one scenario in

which the true continuous limitis known. An unequivocal b enchmark

is rare in finance.For options on lognormally distributed assets,

theliterature contains n o less than 11 distinct versions ofthe

binomial m odel. Some of the models are improp erlyspecified and

can lead to arbitrage profits for a finitenumber of time steps,

while some do not capture theexogenous volatility. Several models

focus first onfitting the binomial model to the physical

process,rather than the risk neutral process, thereby requiringthat

the expected return on the stock be known, anunnecessary

requirement in arbitrage-free pricing. Ishow that the translation

from the physical to the riskneutral process has produced some

misleading results.The paper also provides an examinat ion of

theconvergence properties of each model and concludeswith a

demonstration that an y risk neutral probability(other than one or

zero) will correctly price an optionin the limit.My focus is

exclusively on models for pricingoptions on lognormally distributed

assets and not oninterest rates. Hence, these models can be used

foroptions on stocks, indices, currencies, and possiblycom mo

dities. Cash flows are ignored on the underlying,but these can be

easily added. The paper begins witha brief overview of the model

that serves to establishthe notation and terminology.*In some

versions, the mean arithmetic return is a while themean log return

is fi. In others the opposite notation is used.Although there is no

notational standard in the optionsliterature, the inconsistent use

of these symbols is a significantcost to comparing the models.

I. Basic Review of the Bino mial M odelThe continuously

compounded risk-free rate perannum isr .Consider a risky asset

priced atS that canmove up to state '+ fora value ofu or down to

state - for a valueof dS.Let there be a call option expiring

in one period with exercise price X. The value of theoption in

one period isc_ if the + state occu rs and c.if the - state

occurs.A. Deriving the Binomial Model

Now construct a portfolio consisting ofA units ofthe asset and B

dollars invested in the risk-free asset.This portfolio rep licates

the call option if its outcome sare the same in both states, that

is,

The unknowns areB and A. Rearranging to isolateB setting the

results equal to each other, and solvingfor Bgives

S u-dSince both values,c and c^, are know n, I substitutefor A

in either equation and solve for B. Then, given

knowledge of A,S an d B I obtainc exp( r)

as the value of the option, andK =

(1 )

2)as the risk-neutral probability, sometimes referred toas the

pseudo-probabili ty or equivalent martingaleprobability, with h as

the period length or time toexpiration, T divided by the number of

binomial timeperio ds. A'. Extension to the multiperiod ca se

followsand leads to the same result that the option value at anode,

given the option values at the next possible twonodes, is given by

Equation (I).B. Spe cif icat ion of the Binom ialParameters

At times I will need to work with raw or discretereturns and at

others times, I will work w ith continuou sor log returns. Let the

concept of return refer to the

-

8/12/2019 Binomial Option Chance

3/20

40 JOURNAL OF APPLIED FINANCE SPRING/SUMMER 2008future price

dividedbythe current price, or technicallyone

plustherateofreturn.Let theexpected priceoneperiod later beE(S^)and

theexpected raw returnbeE S^)fS. The true probability

ofanupmoveisq.Thus,the per-period expectedrawreturnis

3)The per-period expectedlogreturnis

4 )The varianceoftherawreturnis

5)The varianceofth elogreturnis

5 ^Vl \J. s.6 )

These parameters describe the actual probabili tydis t r ibut

ion of the stock return, or the physicalprocess. Option valuation

requires transformation ofthe phys ical process to the risk neutral

process .Typically,theuser kno ws the v olatility of the log

returnas given by the physical process, a value thatmayhave been

estimated using historical dataorobtainedas an implied volatility.

In any case, 1assume thatvolati l i ty is exogenous and constant,

as is usuallyassumed in continuous-time option pricing.II .Fitting

the inomial Model

In early research on the binomial model, severalpaper s examined

f i t t i ng a binomia l model to acontinuous-time process,andeach

provide d differentprescriptionson how to doso. Before exam ining

thesemodels , I will review the basic concepts from

thecontinuous-time models that are needed to fit thebinomial

model.A. Basic Continuous Time Conceptsforthe Binomial Model

The results in this section are from the Black-Scholes-Merton

model.Itstartsbyproposing thatthelog return is normally distributed

with mean and

variance(f.Given that \Q S^JS) - \n{S^J -stochastic process is

proposed as ^),the

whereand o^ are the annuaiized expected returnandvariance,

respectively,asgivenbyE[d\n S)] ^fu tandVr[d\n{S)] a^di,anddW^is

aWeiner p rocess.Examine now the raw return,dSJS^.LettingG,-

ln(5^),then S ^ e^ Needed are the part ial der iv at ives ,dSJdG^ =

e^ s and d^SJG^ =e^'- Applying I t 'sLemmatoS.obtains

Noting that dG ^= ^dt + adW^,then dG^ =cf^dt.Substituting these

resultsand the partial derivativesobtainsdS .

Define aas theexpected valueofth erawreturnsothatdS . (8 )

an da = /i +tr=/2. The exp ectatio n odSJS, is E[dSJS}^ adtand

Var[/5/5J- a^dt. tisevident that the m odelassumesnodifference

inthe volatilities of theraw andlogarithmic processesin continuous

time. This resultisthe standard assumption and derives from the

factthat It's Lemmaisusedtotransform the logprocesstothe raw

process. Technically, the variance of theraw processis

Var\ 9)which is adapted to continuous time from Aitchisonand

Brown (1957). The difference in the variancedefined ascrdtand

inEquation(9)liesin the fact thatthe stochastic process fordSJS^is

an approximation.This subtle discrepancy is thesource of someof

thedifferences, however small,in the various binomialmodels. 'One

final resultisneeded.The expected valueof 5' E q u a t i o n (9) is

der ived in Aitchison and B r o w n ( 1 9 5 7 ) byt a k i n g the

mo me n t - g e n e r a t i n g f u n c t i o n for the l o g n o r

m a ldistr ibution. Thedifference in using Equation(9) in

comparisontoCTs quite small over most reasonable ranges of volali l

i tyand expected return. For example, with a 10 expeeted return,3 0

volati l i ty, and one day as a rough approximat ion of dt,the

difference in instantaneous vola t i l i ty is only .000005.

-

8/12/2019 Binomial Option Chance

4/20

CHANCE A SYNTHESIS OF BINOMIAL OPTION PRICING MODELS 41at the

horizon Tis given as*

B. Fitting the Binomiai Model to aContinuous-Time Process

Several ofthe papers on the binomial model proceedto fit the

model to the continuous-time process byfinding the binomial

parameters ,d,an d q that forcethe binomial model mean and variance

to equal thecontinuous-time model mean and variance. Thus, inthis

approach the binomial model is fit to the physicalprocess. These

parameters are then used as thoughthey apply to the risk neutral

process when valuingthe option. As shown shortly, this is a

dangerous step.

The binomial equations for the physical process are

model to the equations for the physical process is atbest

unnecessary and at worst, misleading. Recall that

(10) the Btack-Sch oles-Me rton model requires know ledgeofthe

stock price, exercise price, risk-free rate, time toexpiration, and

log volatility but not the expectedreturn. Fit t ing the binomial

model to the physicalprocess is unnecessary and adds the

requirement thatthe expected return be known, thereby eliminating

themain advantage of arbitrage-free option pricing

overpreference-based pricing.

As is evident from basic option pricing theory,

thearbitrage-free and correct price ofthe option is derivedfrom

knowledge ofthe volatility with the conditionthat the expected

return equals the risk-free rate. Itfollows that correct

specification ofthe binomial modelshould require only that these

two conditions be met.Le tn be the risk neutral probab ility. The

correct m eanspecification is

and(U) KU +{\-n) =e . (14)

This expression is then turned around to isolateK :

oru-d

(12)

( 3 )depending on whether one is fitting the log varianceor raw

variance. The volatility defined in the Black-Scholes-Merton model

is the log volatility so the logvolatility specification would seem

more appropriate.But because the var iance of the raw return i

sdeterministically related to the variance ofthe logreturn, fitting

the model to the variance of the rawreturn will still give the

appropriate values ofwandd

To convert the physical process to the risk-neutralproce ss, a

small transformation is needed. The meanraw return a is set to the

risk-free rater .Alternatively,the mean log return \i is set to r -

0^/2. But fitting th e*For proof see the appendix in Jarrow and

Tumbull (2000, p.112 ) .'One would, however, need to exercise some

care. Assume thatthe user knows ihe log variatice. Then the raw

variance can bederive d IVoni the right-ha nd side of Equa tion

(9), which thenbecomes the right-hand side of Equation (13). If the

user knowst he l og va r i a nc e , t he n i l be c ome s i he r i

gh t - ha nd s i de o fEquation (12). If the user has empirically

estimated the rawand log variances, the former can be used as (he

right-handside of Equation (13) and the latter can be used as the

right-hand side of Equation (12)- But then Equations (12) and

(13)might lead to different values of u and d. because the

empiricalrand log stochastic processes are unlikely to conform

preciselyto the forms specified by theory.*See Jarrow and Turnbull

(2000) for an explanation of thist r a n s f o r m a t i o n .

K (15)Either Equation 14)or (15) is a necessary condition

toguarantee the absence of arbitrage.' ' Surprisingly, notall

binomial option pricing mod els satisfy Equation (14).Note that

this condition is equivalent to, under riskneutrality, forcing the

binomial expected raw return.not the expected log return, to equal

the continuousrisk-free rate. In other words, the correct value of

nshouid come by specifying Equation (14), not

, (16)which comes from adapting Equation (1 1) to the

riskneutral measure and setting the log expected return to its risk

neutral analog ,r - cfll. Surprisingly, many ofthe binomial m odels

in the literature use this im properspecification.'

The no-arbitrage condition is a necessary but notsufficient

condition for the binomial model to yield the

' 'The proof is widely known. One simply retaxes this

constraintwhereu pon a self-financed portfolio of long stock-sh ort

bond(or vice versa as appropriate) always generates posit ive

valueeven in the worst outcome. It will follow that there exists

ameasure, like n, such that ;ni + (1 - n d = e'^'', which is

Equation( 1 4 ) .' A c o r r e c t l oga r i t h mi c s pe c i f i

c a t i on o f t he no - a r b i t r a g econdition would involve

taking the log of Equation (14). Ifthis modified version of

Equation (14) were solved, the modelwould be correc t . 1 found no

ins tan ces in the l i te ra ture inwhich this alternative approach

is used.

-

8/12/2019 Binomial Option Chance

5/20

42 JOURNAL OF APPLIED FINANCE SPRING SUMMER 2008

correct option price. The model m ust also be calibratedto the

correct volatility. This constraint is met by usingthe risk-neutral

analog of Equation (5),(17)

or Equation (6),/)f7r \-7:) =CT h. 18)

Either condition will suffice because both providethe correct

raw or log volatility.C. Convergence of the Binomial Modelto the

Black Scholes Merton Model

Threeofthe mo st wide ly cited versionsofthebinomial model. Cox,

Ross, and Rubinstein (1979);Rendleman and Bartter (1979); and

Jarrow and Rudd(1983), provide proofs that their models converge

tothe BSM model when A>oo.Recall that each m odel

ischaracterized by formulas for w,d and the probab ility.Hsia

(1983) has providedaproof that dem onstratesthat convergence can be

shown under less restrictiveassum ption s. For risk n eutral prob

ability T, Hs ia's(1983) proof shows that the binomial model co

nvergesto the BSM model ifNK-> co as A'^->oo.To meet

thisrequirement,0< ;r < 1 is all that is necessary."

Thisresult may seem surprising for it suggests that the riskneutral

probability can be setatany arbitrary valuesuch as 0.1 or 0.8, In

the literature som e versions ofthe binomial mo del constrain the

risk neutral proba bilityto /2 and as shown later, all versions of

the model haverisk neutral probabilities that converge to V2. But

Hsia's(1983) proof shows that an y probability other thanzero or

one will lead to convergence. This interestingresult is examined

later.D. Alterna tive B inom ial Models

1 now examine the 11 binomial models that haveappeared in the

literature.1 . Cox Ross Rubinstein

Cox , Ross, and Rubinstein (1979 ), henceforth C RR.is arguably

the seminal article on the model. Their

"The o ther requi rements not noted byHsia (19 83) a re tha tt h

e c h o i c e of w,d, and n must force the b inom ial modelv o l a

t i l i t y to e q u a l thet r u e v o l a t i l i t y a n d th e

me a n mu s tguarantee no arb i t rage .

Equations (2) and (3) (p. 234) show the option value asg iven

bymy Eq uat ion (1) wi th the r isk neu tralprobability specified

as my Equation (2). CRR thenproceed to examine how their formula

behaves when A^-^OO(their p.246-251).They do this by choosing , dan

d qso that their mode con verg es in the limit to theexpected value

and variance of the physical process.Thus, they solve for u d,an

dqusing the p hysicalprocess , my Equat ions (11) and (12) . Note

thatEquations (11) and (12) constituteasystem of twoequa t ions and

th ree unknowns . CRR proposeasolution while implicitly imposinga

necessary thirdcondition, ud 1, an assum ption frequently found

inthe literature. Upon obtaining their solution, they thenassume

the limiting condition that /r ^ 0. This conditionis necessary so

that the correct variance is recovered,though the mean is recovered

for any A . The ir solutionsare;

u e a=ewith physical probability

^

-

8/12/2019 Binomial Option Chance

6/20

CHANCE A SYNTHESIS OF BINOMIAL OPTION PRICING MODELS 43f i t the

binomial model to the physical process,simultaneously deriving the

physical probabilityq,andthen substitute the arbitrage-free formula

for n as q.Had they imposed the arbitrage-free condition

directlyinto the solution, they would have obtained

differentformulas, as we will see inanother model.2.

Rendleman-Bartterand Jarrow-Rudd-Turnbull

Because of their sim ilarities,discussion of the Rendleman-Bar t

t e r (RB) approach i scombined with discussion ofthe Jarrow-Rudd

(JR) approach and later appendedwi th the Ja r row-Turnbu l l ( JT

) approach . Theseapproac hes also fit the binomial m odel to the

phy sicalprocess. The RB approach specifies the log mean andlog

variance E quations (11) and (12), and solves thesetwo equations to

obtain:

The so-called binomial modelis really a family of modelsthat,

under surprisingly mildconditions, all converge in thelimit to the

Black-Schules-Merton model.

u = e \\-q , d = eBecause these formulas do not specify the

value of

q, they are too genera to be of use. In risk neu tralizingthe

model, RB assume that/ J-r- 2 0)

but again, these formulas are consistent only with aprobability

of Yiand risk ne utrality as specified byfu^ r-d^/2. Simply

converting the mean is not sufficientto ensure risk neutrality for

a finite number of timesteps.'**"A close look al JR shows ihat q is

clearly the physicalprobability. On page 187, they constrain q to

equal the riskneutral probability, with iheir symbol tor the latter

being ^.Bui this constraint is noi upheld in subsequent pages

whereuponthey rely on convergence in ihe limit to guarantee the

desiredresult that arbitrage is prevented and BSM is obtained.

Thispoint has been recognized in a slightly different manner

byNawalkha and Chambers (1995, p. 608).

-

8/12/2019 Binomial Option Chance

7/20

44 JOURNAL OF APPLIED FINANCE SPRING SUMMER 2008

A number of years later,JTderive thesame modelbul make a much

clearer d is t inct ion betweenthephysical and risk neutral

processes. They fix7i at itsarbitrage-free value andshow fortheirup

anddownparameters that

7 -du-d (21)Like CRR, the correct specification of K ensures

thattheir model does not admit arbitrage. But, because

theirsolutions foruanddwere obtainedbyspecifyingthelog mean, these

solutions are nottechnically correctfor fmite N. The mean

constraint ismet, so there mustbe an error somew here, which ha s

to be in the variance.Thus, their model does not recover

thevariance forfinite A' using therisk neutral pro babilities.

Itreturnsthe co r r ec t va r i ance e i the r when thep h y s i c

a lprobability isusedor in the limit with the risk

neutralprobability converging toVi.

For future reference, this model will becalledtheRBJRT modeland

referred only to thelast ve rsionofthe model inwhich the no-arb

itrage co nstraintisapplied toobtain K.I have shown that

itdoesnotrecover thecorrect v olatility for finite

A^.NowIwillconside r a model that fits a binomial tree to the

physicalprocess but does prevent arbitrage and recoversthecorrect

volatility.

3. hrissChriss's model (1996) specifies the rawmeanand

log varianceofthe physical process. The formerisgiven

byqu+{\-q)d=-e \ (22)

an d thelatterby Equation (12). He then assumes thatq =Y2.The

solutionsareM =2e ^*- 2eHlThe risk-neutralized analogs are found

by

substitutingrfor a:

=2^ri,.: d= (23)

Note that because Chriss' mean specification is theraw mean,

transformation to risk neutrality bya=rcorrectly returns the

no-arbitrage condition. Equation(15).Thus,forthe Chriss m odel,K= n

=ViforallN.an d the model correctly preserves the

no-arbitragecondition andrecovers thevolatility for anynumber

of time steps.4 . Trigeorgis

The Trigeorgis 1991 )model transforms the originalprocess

intoalog process. That is, letX In5 andspecify the binomial process

as thechange in A ,orAA .Thesolutions for the physical

processare

Note thatif/i^-0,the Trigeorgis model isthe sam eas the CRR mod

el. Trigeorgis then risk neutralizes themodelbyassum ing thatfi r-

cH/2. The resu ltsare

J(rh^r-a/2fh , -Jah+{r-a/2fhu= e , d=e > Trige orgis' risk

neutral probability comes simply fromsubstitutionof r - d llfor

inthe formula for q..thereby obtaining

-a I2)h.7X - + 2Of course this is therisk neutral proxy

probability

and isnot given bythe no-a rb i t r age cond i t ion

.Therefore,itis not arbitrage -free for fmite A^, thoughitdoes

recover the correct volat i l i ty . In thel imi t ,Tr igeorg i s '

s r i sk neu t r a l p roxy p robab i l i t y ,;r*,converges to

Aand the arbitrage -free risk neutralprobability, K ,converges

toVz, so the Trigeorgis modelis arbitrage-free inthe limit.

5. Wi lmott i ndW ilmott2Wilmott (1998) derives twobinomial

models.He

specifies the raw mean and raw variance of the physicalprocess .

Equat ions (22) and (17). His first mo del,referred to here as Wil

1, assum esud =.The solutionsfor the physical processare

2 eMM_4The physical probabilityqisfound easily from themean

condition.

u-dRisk neutralizing themodel isdone by simply

-

8/12/2019 Binomial Option Chance

8/20

CHANCE A SYNTHESIS OF BINOMIAL OPTION PRICING M ODELS

48substitutingrfor a;

-rH=-\e2\1/-r.=-{e ' +2 \

e^

{r-ta-\h\

J

\ -A\e ^ ,and d)d1.This resu lt for C RR is well-known.'** It

arises w hen h >(CT//-)\which is likely to occur with low

volatility, highinterest rates, and a long time to expiration.

Sufficientlylow volatility is unlikely to apply when modeling

stockprices, but exchange rate volatility isoften less than0 .1 .

Thus, long-term foreign exchange options wherethe interest rate is

high canh a v e a r isk neutralprobabili ty greater than on e. For

RBJRT,theriskneutral probability can exceed one if/i 4. For very

low volatility, asin the foreign exchange market, the time step

wouldhave to beextrem ely large. Thus , it would takeexceptionally

large volatility and a very small num berof time steps relative to

the option maturity for the riskneutral probability to exceed one

for the RBJRT model.Of course, if the risk neutral probability

exceeds one,a model could still correctly value the option. But,as'

^See, forexample . Carp enter (1998) ,' See, forexample . Chr iss

(1996,p.239) ,' 'For example , ii r = , 1 ,CT= ,05.and7 = 5, In

that case,wewould requireN>2 0 ,

-

8/12/2019 Binomial Option Chance

11/20

48 JOURNAL OF APPLIED FINANCE SPRING SUMMER 2008

A An Init ial Look at Convergencereviously noted, the CRR and

RBJRT models use theuan d d formulas from the physical process,

which isderived by constraining the log mean, not the rawmea n. It

is the raw mean that guarantees no arb itrage.

For the other two desirable conditions that the upfactor ex

ceeds one and

If the correct mean and volatility arecaptured, any binomial

probabil i tyother than zero or one will producethe

Black-Schules-Merton price in thelimit.

the down factor is lessthan one , on ly theRBJRT

methodologypermits an up factorthat can be less thano n e . I n t e

r e s t i n g l y ,seven of the e levenmodels permit a downfactor

greater than one. Only the models of Trigeorgis,Wil 1, and the JK

YAB MD model have no anomalies.

These anomalies are interesting but usually occuronly with

extreme values of the inputs and/or a smallnumber of time steps

relative to the option maturity.They can usually be avoided when

actually pricing anoption. The greatest risk they pose is probably

whenthe model is used for illustrative purposes.

III Model ComparisonsTable I illustrates an exam ple for valuing

a call option

in which the asset is priced at 100, the exerc ise price is100,

and the volatility is 30%.^ The continuous risk-free rate is 5% and

the option expires in one year. In allcases, I use the probability

:Tor ;r* as specified by th eauthors of the respective models. I

show the valuesfor 1 ,5,1 0,2 0,3 0,5 0,7 5 and 100 time steps. The

correctvalue, as given by the Black-Scholes-M erton formula,is

14.23.At 50 times steps all of the prices are within0.06. At 100

time steps, all ofth e prices are within 0.03.

To further investigate the question of which m odelsperform

best, I vary the inputs by letting the volatilitybe 0.10,0.30, and

0.50; the time to expiration be 0.25,1.0, and 4.0; and the

moneyness be 10% out-of-the-money, at-the-money, and 10%

in-the-money. Theseinputs comprise 27 unique combinations. I

examineseveral characterist ics of the convergence of thesemodels

to the Black-Scholes-Merton value.

^ The choices of stock price and exer cise price are

notparticularly important as long as moneyness is

consistent.Standard European options, indeed most options, have

valuesthat are linearly homogeneous with respect to the stock

priceand exercise price. Thus, after choosing a stock price

andexercise price, we could use a scale factor to change to

anyother stock price and exercise price, and we would obtain

anoption price that differs only by the scale factor.

Let b N)be the value com puted for a given binom ialmodel with

A'^time steps and BSM be the true Black-Schoies-Merton value.

Binomial models are commonly

descr ibed as convergingin a pattern referred to as odd-even .

That is, whenthe number of time stepsis odd (even), the binomialpr

ice tends to be above(below) the true price. Wewill call this

phenomenonthe odd-even property.Interestingly, my num erical

analyses show that the odd-even phenomenon neveroccurs for any

model with out-of-the-money options.For at-the-money options, the

odd-even phenomenona lway s occu r s for t he JK YA BM Dl mode l

andoccasionally for other models. Odd-even convergencenever occurs

for any inputs for JKY RB 2, JKYABM C2,and JKYABMD2c. Thus, the

odd-even property is nota consistent phenomenon across models.

Next, I examine whether a model exhibits m onotonieconvergence,

dened as

where |e{AO| = IM ^ - BSM |. That is, successive errorsare smal

ler . Only the Tr igeorgis model exhibi tsmonotonie convergence and

it does so for only one ofthe 27 combinations of inputs examined.

Becausemonotonie convergence is virtually non-existent, weexamine a

slight variation. Suppose each alternate erroris smaller than the

previous one, a phenomenon wecall alternating monotonie

convergence, defined as

{N)\2.As i t happens , however , a l t e rna t ing mono ton

ieconvergence never occurs.

I then attempt to identify at which step a model isdeemed to

have acceptably converged. For a givent ime step , I com pute the

average of the cur ren tcomputed price and the previous computed

price. Ithen identify the time step at which this average priceis

within 0.01 ofthe BSM price with the added criterionthat the

difference must remain less than 0.01 throughstep 100. The results

are presented in Tables II, III,and IV. One consistent result in

all three tables is thatthe RBJRT and Chriss models produce the

same results.Further examination shows that tbe values of uan d

lare not precisely equal for both models for all values

-

8/12/2019 Binomial Option Chance

12/20

CHANCE A SYNTHESIS OFBINOMIAL OPTION PRICING MODELS 9Table I

Some Num erical Exam ples ^ iThe tabie contains the binomial option

value for various time steps N) for a call option with stock price

of 100, exercise priceof 100, volatility of 0.30, risk-free rate

of0.05, and time to expiration of one year for each of the 11

binomial models. The riskneutral probability is/j orp* as specified

by tbe authors of the models. Tbe Black-Scholes-Merton option value

is 14.23.

151020305075100

CRR16 9614 7913 9414 0814 1314 1714 2714 20

RBJRTn oo14 7914 0014 1314 1714 2014 2714 22

ChrJss17 0014 7914 0014 1314 1714 2014 2714 22

Trigeorgis16 9714 7913 9414 0914 1314 1714 2714 20

Win17 7914 9314 0014 1214 1614 1914 2814 21

Wil217 7814 9214 0514 1514 1914 2114 2714 23

JKYABMD116 6914 7413 9214 0714 1314 1714 2614 20

JKYRB217 1714 6914 3914 3614 3314 2914 2514 24

JKYABMC217 2414 7014 4014 3614 3314 2914 251424

JKYABMD2C16 1514 5114 3114 3214 3014 2714 2414 23

JKYABMD316 6514 7313 9714 1114 1614 1914 2614 22

Table II Convergence Time Step for Binom ial Models by

MoneynessTbe table sbow s the average time step A at which converg

ence is achieved w here the error is defined asHb N) b{N ))/2 -

BSM]where b N) is the value computed by the given binomial model

for time step /V, BSM is tbe cotrect value of the option ascomputed

by the Black-Seboles-Merton model, and convergence is defined as an

error of less than 0.01 for all remaining timesteps tbrough 100.

The ex ercise price is 100, the risk-fi ee rate 0.05 , the

volatilities are is 0.10, 0.30, and 0.5 0, and the times

toexpiration are 0.25 , 1.0, and 4.0. Out-of-the-m oney options

bave a stock price 10% lower tban the exercise price, and

in-the-money options have a stock price 10% higher tban tbe

exercise price. These parameters combine to create nine options for

eacbmone yness class. A maxim um of 100 time steps is used. For

mode ls tbat did not converge by the 100 'time step, a value of

100is inserted.Model Moneyness S/100)

Out-of-the-MoneyCRR 66.86RBJRT 55.57Chriss 55.57Trigeorgis

62.57Will 66.93Wil2 66.64JKYABMDl 59.20JKYRB2 61.67JKYABMC2

61.92JKYABMD2C 61.92JKYABMD3 63.47

At-the-Money40 2554 3054 3031 9148 0859 8550 5160 3960 4763 5556

88

In-the-Money54 2955 0255 0263 6669 0855 066 3 2 457 3458 5863

1763 93

-

8/12/2019 Binomial Option Chance

13/20

5 JOURNALOFAPPLIED FINANCE SPRING/SUMMER 2008Table III.

Convergence Time Step for Binomial M odeis by Time to ExpirationThe

table shows the average time stqj A'at which convergence is

achieved where the error is defined as\ b N) +b NA)y2 - BSM|where

b{N) is the value computed by the given binomial model for time

step N, BSM is the correct value of the option ascomputed by the

Black-Scholes-Merton model, and convergence is defined as an error

of less than 0.01 for all remaining timesteps through 100. The exe

rcise price is 100, the risk-free rate 0.05, the volatilities are

is 0.1 0,0 .30 , and 0.50, and the money nessis 10%

out-of-the-money, at-the-money, and 10% in-thc-money. The times to

expiration are shown in the columns. Theseparameters combine to

create nine options for each time to expiration. A maximum of 100

time steps is used. For models that didnot converge by the 100 '

time step, a value of 100 is inserted.

Model Time to Expiration 7^0 25 1 00 4 00

CRR 33.33 54.33 87.89RBJRT 43.33 67.78 79.00Chriss 43.33 67.78

79.00Trigeorgis 33.78 53.33 84.67Will 38.33 72.33 93.33Wil2 48.44

76.67 82.56JKY AB MD l 33.67 53.78 99.22JKY RB2 51.44 74.44

81.44JKYA BMC 2 53.22 74.78 81.44JKYABM D2C 46.78 61.22 ..

100.00JKYA BMD 3 43.44 61.44 97.44

Table IV. Convergence Time Step for B inom ial Models by

VolatilityThe table shows the averag e time step A'at which

converge nce is achieved w here the error is defined as\{b{N)+h N-

))/2 - BSMwhere (AO is the value com puted by the given binomial

model for time step A , BSM is the correct value of the option

ascomputed by the Black-Scholes-Merton model, and convergence is

defmed as an error of less than 0.01 for all remaining timesteps

through 100. The exercise price is 100, the risk-free rate 0.05,

the times to expiration are 0.25, 1.00, and 4.00. and themoneyness

is 10% out-of-the-money. at-the-money, and 10% in-the-money. The

volatilities are shown in the columns. Theseparam eters co mbine to

create nine options for each time to expiration. A maximum of 100

time steps is used. For models that didnot converge by the 100 '

time step, a value of 100 is inserted.

Model Volat i l i ty CT)0 ^ 3 0 0 5 0

CRR 40.22 61.89 73.44RBJRT 25.78 68.89 95.44Chriss 25.78 68.89

95.44Trigeorg is 38.00 62.33 71.44Will 40.11 74.67 89.22Wit2 29.78

80.11 97.78JKYABMD 42.78 63.22 80.67JK:YRB2 27.33 82.22 97.78JKYAB

MC2 27.33 82.44 99.67JKYAB MD 2e 45.33 67.78 94.78JKYA BM D3 48.33

60.22 93.78

-

8/12/2019 Binomial Option Chance

14/20

CH NCE SYNTHESIS OF BINOMI L OPTION PRICING MODELS 51of N but

they are very close and become essentiallyequal for fairly small

values ofN.

Table II illustrates that forat- the-money options,the

Trigeorgis model performs best followed by CRRand Wil1.The wo rst

model is JKYA BM D2c, followedby JKYABMC2 andJ K Y R B 2 . For in -

the -moneyoptions, the best model isCR R, followedbyChriss-RBJRT

with W il2 very close behind. Th e worst is Wil1,followed by

JKYABMD3 and Trigeorgis. Forout-of-t h e - m o n e y o p t i o n s

, thebest are R B J R T - C h r i s s .followed by JKYAB MD 1. The

worst is Wil1,followedby CRR and Wil2.

Table IIIshows that convergen ce isalways fasterwitha shorter

time toexpiration, This result shouldnot be surprising. W ith a

fixed num ber of time steps,ashorter timetoexpiration mean s that

the time stepiss m a l l e r . For the m e d i u m m a t u r i t y

, the f as t es tconvergence is achieved by theTrigeorgis mod el,f

o l lowed by J K Y A B M D I andC R R . The wor s tperformance is

by Wil2, followed by JKYAB MC 2 andJ K Y R B 2 . For the s h o r t

e s t m a t u r i t y , the b e s tperformance is by CRR, followed

by JKYAB MD 1 andT r i g e o r g i s ; and the w o r s t p e r f o

r m a n c e is byJKYABMC2, followed by JKYRB2 and Wil2. For

thelongest maturity, the best performance is byRBJRT-Chriss,

followed by JKYRB2 and JKYABMC2 (tied).The worst performance is by

JKYABMD2c, followedby JKYABMDI andJKYA BMD 3.

TableIV shows that convergenceisalways slowerwith higher

volatility. For the lowest volatility,thefastest models are

RBJRT-Chriss (tied), followed byJKYRB2 and JKYABMC2 (tied). The

slowest modelisJ K Y A B M D 3 , f o l l o w e d by J K Y A B M D 2

c andJKYABMDI. For medium volatility, the fastest modelis JKYABMD3,

followed by CRR and Trigeorgis; andthe slowest is JKYABMC2,

followed by JKYRB2 andWil2. For the highest volatility, the fastest

models areTrigeorgis, followed by CRR and JKYA BM DI; whilethe

slowest is JKYABMC2, followed by JKYRB2 andWiI2(tied).

Itisdifficult todraw con clusions about whicharethe fastest and

slow est mo dels. Each model finishes inth e top orbottom four at

least once. Althoughthetestsare notindependent,we can gain some

insightby assigninga simple ranking (1=best, 11=worst)and tally the

performance acrossallnine g roupings.CRR has the best performance

with the lowest overallscore of36 ,while Trigeorgis isat37, and

RBJRT andChriss areat38. The highest scores and, thus,

worstperformance are JKYABMC2 at71.5,followed by Wil2at 69.5 and

JKYABMD2cat67.5 . These rankings areuseful and could suggest that

CRR, Trigeorgis, RBJRT,

and Chriss mightbethe bestset of models, but theyare not

sufficient to declareadefinitive winner.

Whether a model conv erges acce ptably can bedefmed by whether

the error is within a tolerance for agiven time step.Icalculate the

error for the 100''' timestep. These results also reveal

noconsistent winneramong the models. Most model values are within

fourcentsofthe true value on the lOO time step, and thedifferences

are largest with long maturity and/or highvolatility, consistent

with myprevio us finding thatshort maturity and low volatility

options are the fastestto pr ice .B A More Formal Look at

Convergence

One p rob lem wi th ana lyz ing the c o n v e r g e n c

eproperties o f a model is that it is difficult to

definitivelyidentify when convergence occurs. Visual observationand

rules about differences being less thana specifiedvalue are useful

but arbitrary.It ispossible, however,touse a more m athematically

precise definit ionofconvergence. Leisen and Reimer 1996) (LR)

provide adetailed analysis ofthe convergence ofthe CRR andR B J R T

m o d e l s u s i n g the n o t i o n of order ofconvergence.

Amodel co nverges more rapidlytheh i g h e r the o r d e r of c o n

v e r g e n c e . T h e r e f o r e ,determining the order of

convergence of these modelsavoids the subjectivity ofthe previous

analysis.

Convergence of a binomial model is defined to occurwith orderp

ifthere existsaconstantksuch that

Visual examination o fthe errors on a log-Iog graph canreveal

theorderofconvergence. LRfurther show ,however, that a better

measure of convergence can bederived using the difference between

the momentsofthe binomial and continuous-time distributions.

Thesemoments are defined as follows:

p N):=7r\nu u-\f+{\-K)\nd{d-\f.The moment s m^(A^)and m^(A ' ) a

r e obv ious ly

related to thesecond andthird mo men ts. The thirdterm is

referred to as a pseudo-moment . Let p .)represent theorder of

convergence of the a b o v emoments and the pseudo-moment. LR show

thattbeorder of convergence ofthe binomial seriesis

-

8/12/2019 Binomial Option Chance

15/20

52 JOURNAL OF APPLIED FINANCE SPRING/SUMMER 2008

max[lmn (p{m {N)),p{m {N )),p{p{N)))-l].In other words, the

order of convergence is theminimum of the orders of convergence of

the twomoments and the pseudo-moment minus one with anoverall

minimum order of convergence of one. Theyshow that the order of

convergence can be derivedmathematically and they do so for the

three modelsthey examine. These proofs, however, are quite

detailedand cumbersome and, as they note, visual inspectionof these

momen ts with a graph is equally effective.

I examine the order of convergence using themoments and

pseudo-moments of each of the elevenmodels. Because of the

excessive space required, Ipresent the results only for the Chriss

model. Figures1, 2, and 3 illustrate various characteristics of

theconvergence of the Chriss model for the previouslyused inputs .

Because the LR er ror analysis usescomm on logs, I show only the

time steps starting with10,

Figure 1 is the option price graphe d against thenumbe r of time

steps, with the BSM value representedby the horizontal line. The

converg ence is oscillatory,exhibiting the odd-even pattern

previously noted.^Figure 2 shows the absolute value of the error,

whichexhibits a wavy p attern. The solid line was created

byproposing values for k and p such that the error boundalways lies

above the absolute value of the error. Thevalue of k is not

particularly important, but the valueof p indicates the order of

convergence. Here, p = 1.A value of p = 2 would force the bound

below the w avyerror line. Thus, the order of convergence is

clearlyone. Figure3shows the moments and pseudo-mom entsas def ined

by L iesen and Re imer (1996) . Thep s e u d o - m o m e n t s p (

A / ) a n d m^{N) a r e a l m o s tindistinguishable- The heavy

solid line is the simpleftinction \fN where p is the order of

convergence ofthe moments and pseudo-moments. In this case, p =

2provides the best fit. Therefore, following Theorem Iof Leisen and

R eimer (1996 ), the order of convergenceis one, confirming my

direct exam ination of the error.These graphs were generated for

all of the modelsand all have an order of convergence of one. In

thelimit all models produce the correct option value, butof course

limit analysis m akeTV essentially infinite. Asshown earlier ,

seven of the eleven models admitarbitrage with finite A^, but these

opportunities vanishin the limit. Also, the values of ;rand K *

converge to V2in the limit. These results suggest that a model

that^ As previously noted, ihe Ch riss model does not exhibit

thisproperty for every case.

correc tly p reve nts a rbitrag e for all A and sets the

riskneutral probability ;rat Vi fora ny A might be superior.That

model is the Chriss model. And yet, there is noevidence that the

Chriss model consistently performsbest for finite N.

C Why the Models ConvergeI have shown that all the models

converge, but it is

not clear why. As Hsia s (1983) proof s how s, therequ i r ement

fo r convergence i s no t pa r t i cu la r lydemanding, but clearly

one cannot arbitrarily chooseformulas for w, d , and n.

As noted, it is possible to prove that all of theformulas for

either ;ror ;r*converge toViin the lim it. Iwill exam ine why this

result oc curs. F ocusing on ;r, Idivide the models into four

categories: 1 )models thata s s u m e TC = V2 ( C h r i s s , W i l

2, J K Y A B M D 3 ) ;2 ) mode l s tha t assume ud = e- ( J K Y R B

2 ,JKYABMC2, JKYABMD2C); 3) models that assumeud = e^ - ^^*

(RBJRT); and 4) models that assumeud - 1 (CRR, T r igeorg i s , W i

l l , JKYA BMD l) .^^For 1), there is no need to examine the l

imitingcondition. For 2), 3) and 4), general convergenc e isshown

in the aforementioned supporting document.

Thus, all of the models either have ;ror n* convergeto Vi. The

other requirements are that the models returnthe correct mean and

volatility in the limit. I will look athow they achieve this

result. Re-classify the modelsaccording to their assumptions about

the mean. Group(a) includes all models that correctly use the

arbitrage-free specification of the raw mean. Equation (14) (CRR

,RBJRT, Chriss, Will , Wil2, JKYABMC2). Group (b)includes all

models that correctly use the raw meanspecification but use \+rh

instead of e (JK YA BM Dl,JKYABMD2C, and JKYABMD3). Group (c)

includesthe models that specify the log mean, Equation

(16)(Trigeorgis and JKYRB2). Obviously Group (a) willcorrectly

converge to the proper mea n. Grou p (b) willdo so as well, because

e is well approximated by 1 +rh in the l imit . Group (c) uses the

specification[Equation 16)],Tt \nu+ 1 -K *)\nd=ir - a^/2)h.Usingthe

approximation Inw = M - 1 and like wise for d, wehave^Mt is

important to understand why RBJRT is classified in thismanner and

not in any other group, RB and JR obtain theirsolut ions by se t t

ing the physical probabi l i ty q to / i . Theirsolution derives

from using the mean of the log process, andthus, is not

arbitrage-free. JT then impose the arbitrage-freecond i t i on and

, hence , co r r ec t l y u se n for the r isk neut r a lprobabili

ty, but this constraint cannot lead to their formulasfor H and d.

Their formulas can be obtained only by imposinga third condition,

which can be inferred to be the one statedhe re .

-

8/12/2019 Binomial Option Chance

16/20

CH NCE SYNTHESIS OF BINOMI L OPTION PRICING MODELS 63Figure 1.

Convergence ofthe Chriss Modei tothe Black Schoies Merton

iVIodeiThis figure showsthe option price obtainedbytheChrissmodel

againsttheBlaek-Sc holes-Me rton model indicatedbythe solid

line)fortime steps 10 to 100. The stoek priceistOO,the exercise

priceis 100, the risk-free rateis0.05, the timetoexpirationisone

year,andthe volatilityis0.30.

14,60

1 19 28 37 46 55 64 73 82 91 100ikneStqe 10-100)

Figure 2. Absoiute Value of the ConvergenceError for the Chriss

Modeiand its Order Bound FunctionThis figure shows the absolute

value ofthe errorforthe optionprice obtainedby the Chriss model

against the Black-Scholes-Merton modelfortime steps 10to100. The

stoek prieis 100,the exercise priceis 100, the risk-free

rateis0.05,thetimetoexpirationisoneyear,and thevolatility is0.30.

Becausetheerror boundislinear in logs,alog-log scale is used. The

upperbound is the dark shaded line based on an order of

eonvergeneeof one.

Figure 3. Absolute Vaiue of the Moments andPseudo moments for

the Chriss Modeiand its Order Bound FunctionThis figure shows the

absolute value ofthe error for the secondand third mom ents and the

pseudo-mom ent as defined by Leisenand Reimerfor the option price

obtainedbythe Chriss modeiagainsttheBlaek-Seholes-Merton modelfor

time steps 10to100.The stoek prieis100, the exercise prieis100, the

risk-free rateis0.05,thetimetoexpiration

isoneyear,andthevolatilityis0.30. Becausetheerror

boundislinearinlogs,alog-log scaleisused. The upper boundis the

dark shaded linebased on an order of eonvergen ee of 2,which is

consistent withorder of convergence ofth e model ofone.

1.0000

10 100

m\

-\ ={r-(j /2)h

This specification isextremely closetothatofGroup b), differing

onlyby thevariance termon the RHS,which goestozeroin thelimit.

The next stepis toconsiderthevolatility. Let Group(a) consist of

models that correctly specify the logvolatility (CRR, RBJRT,

Trigeorgis, JKYRB2, Chriss);(b) consist ofmodels that correctly

specify the rawvolatility (Wil 1, Wil2, and JKYABMC2); and (c)

consistof models that use an approximation of the rawvolatility,

7-A^e-^' '(e ' ' ' - 1) (JKYABMDl,JKYABMD2C, and JKYABMD3). Group

(a) willobviously returnthecorrect logvolatility,andGroup(b) will

return the correct rawvolatility. Eitherspecification suffices

because constraining the onevolatility automatically constrains the

other. Group(c)

-

8/12/2019 Binomial Option Chance

17/20

54 JOURNAL OF APPLIED FINANCE SPRING SUMMER 2006can be shown to

be based on an accep tab leapproximation by using the Taylor series

for theexponential function and assuming / = 0 for all k ofpower2or

more.

Hence, all of the models work because in the limitthey al have a

binomial probability of'/2, and they allreturn the risk-free rate

as the mean and the correctvolatility in the limit. Thus, any model

with thesecharacteristics will work. As shown in the next

section,however, the constraints are not nearly that severe.

IV A General Binom ial FormulaAs previously noted, Hsia's (1983)

proof of the

convergence of the binomial model to the Black-Scholes-Merton

model shows that any probability isacceptable provided that u and d

return the correctmean and volatility. This result suggests that

any valueof the r i sk neu t r a l p robab i l i t y wou ld l ead

toconvergence if the correct mean and volatility areupheld. We now

p ropose a general binomial m odel witharbitrary n that prohibits

arbitrage and recovers thecorrect volatility for all N. Let the

mean and variancebe specified as follows:

Of course, these are Equations (14) and (18). Themean equation

guarantees no arbitrage profits for allN. Now assume that Kis know

n but its valu e is leftunspecified. Solving forw and /gives

While yet one more binomial formula i s notnecessary, this model

shows that binomial optionpricing is a remarkably flexible

procedure that makesonly minimum demands on its user and the choice

ofprobability is not one of them.

V ConclusionThis paper synthesizes the research on binomial

models for European options. It shows that the modelis not a

single modei but a family of interpretations ofa d i sc r e t e - t

im e p roces s tha t con verg es to thecontinuous Brownian motion

process in the limit andaccurately prices options. That there are

no less than11 such members of this family may seem surprising.The

fact that they all perform equally in the limit, eventhough some

admit arbitrage for a finite number oftime steps, is a testament to

the extremely generalnature of the Black-Scholes-Merton model and i

tsmodest requirements. It would seem that a preferablebinomial

modei should prohibit arbitrage for a finitenumber of time steps

and recover the correct volatility,and some models fail to meet

these requirements. Butperhaps most interesting of the results

shown here isthat given H sia's elegantproof the choice of the

actualrisk neutral probability is meaningless in the limit,though

clearly a risk neutral probability of Aassuresthe fastest

convergence.*

M =Tie

neand, of course.

udFor the special case where n^ Vi the equations areequivalent

to those of Chriss.These equations tell us that we can arbitrarily

set n

to an y value between 0 and 1 and be assured that themodel will

converge to the BSM value. This result isobserved in Figure 4. Note

that while convergenceappears much smoother and faster with K- Vi

th eresults are not much different for pro bab ilities of %andy 4.

ForA'^^ 100, a prob ability of gives an optionvalue of 14.27, while

a probability ofy4gives an optionvalue of 14.15.The correct BSM

value is 14.23."

' ^A get ie ra l formula of th is lype even meat i s tha t ext

remeprobabilities, say 0.01 and 0.99, would also correctly price

theoption in the l imit . I tested these extrem e value s, how ever

,a nd I he r e s u l t s a r c no t i mpr e s s i ve . Fo r e xa

mpl e , w i t h aprob ability of 0.01 I obtain an option value of

13.93. while aproba bili ty of 0.99 gives an option value of 13.01

after 100time steps. Convergenc e is extremeiy erratic and the

order ofconv ergen ce i s d i f f icul t to de ter min e . No neth

eless , in thelimit , the correct option value is obtained.

-

8/12/2019 Binomial Option Chance

18/20

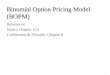

CHANCE A SYNTHESIS OF BINOMIAL OPTION PRICING MODELS 85Figure 4

Convergence of a General BinomialModel that Prohibits Arbitrage

andAllows any Probability between Zero and OneThese figures show

the value of the option computed from ageneral binomial model that

assures the ahsence of arbitrage,recovery of the correct log

volatility, and in which the prob-ability can be arbitrarily ch

osen as indicated. Tlie stock price is100, the exercise price is

100. the risk-free rate is 0.05, thevolatility is 0.30, and the

option expires in one year. Thehorizontal line is the BSM value of

14.23.

Number of Time Steps (N )

21 41 61 8 101 121 141

7C= 3 41817 -

1 21 41 61 81 m i 121 141Number of Time Steps (N )

ReferencesAitchison. J. and j . A . C . Brown, 1957. The

LognormalDistribution, Cambridge, UK, Cambridge University

Press.Avellaneda, M. and P. Laurence, 1999, Quantitative Modelingof

Derivative Securities: From Theory lo Practice, Boca

Raton. FL, CRC Press.Baule, R. and M. Wilkens. 2004. Lean Trees

- A GeneralApproach for Improving Performance of Lattice Modelsfor

Option Pricing, Review of erivativesResearch 1(No.1, January).

53-72.Black, F. and M. Scholes, 1973, The Pricing of Options

andCorporate Liabilities, Journal of Political Economy 81(No. 3,

May), 637-654.Boyle. P.P.. 1988, A Lattice Framework for Option P

ricingwith Two State Variables. Journal of Financial

andQuantitative Analysis 23 (No. 1, March), 1-12.Breen. R.. 1991.

The Accelerated Binomial Option PricingModel, Journal

ofFinancialand Quantilative Analysis 26(No. 2, June),

153-164.Broadie. M. and J. Detemple, 1997, Recent Advances

inNumerical Methods for Pricing Derivative Securiti es, inL.C.G.

Rogers and D. Talay, Ed., Numerical Methods inFinance, Cambridge,

UK, Cambridge University Press.Ca rpenter , J.N., 1998, The

Exercise and Valuation ofExecutive Stock Options, Journal of

Financial Economics48 (No- 2, May), 127-158.Chriss, N.. 1996,

Black-Scholes andBeyond Option PricingModels, New York. NY.

McGraw-Hill.Cox. J.C., S.A. Ross, and M. Rubinstein, 1979. Option

Pricing:A Simplified Approach, Journal ofFinancialEconomics 7(No.

3, September), 229-263.Figlewski, S. and B. Gao. 1999. The Adaptive

Mesh Model: ANew Approach to Efficient Option Pricing, Journal

ofFinancial Economics 53 (No. 3, September), 313-351.He, H., 1990,

Convergence from D iscrete- to Continuous-Time Contingent Claims

Prices, The Review of FinancialStudies 3 (No. 4, Winter).

523-546.Hsia, C-C, 1983, On Binomial Option Pricing, Journal

ofFinancial Research 6 (No, 1, Spring), 41-46.Jabbour, G.M., M.V.

Kramin. and S.D. Young. 2001 , Two-State Option Pricing: Binomial

Models Revisited. Journalof Futures Markets 21 (No. IK November),

987-1001.Jarrow, R.A. and A. Rudd, 1983,Option Pricing,

Homewood,IL, Richard Irwin.Jarrow, R. and S. Tumbull, 2000,

erivativeSecurities, 2Cincinnati, OH, Southwestern College

Publishing. Ed.,

Johnson, R.S., J.E. Pawiukiewiez, and J. Mehta, 1997, Binomial

Option Pricing with Skewed Asset Retur ns,Review ofQuantitative

Finance and Accounting(No. July),8 9 - 1 0 1 .

-

8/12/2019 Binomial Option Chance

19/20

JOURNAL OF APPLIED FINANCE SPRING SUMMER 2008Joshi, M.S., 2007.

The Convergence of Binomial Treesfor Pricing the American Put,

University of MelbourneWorking Paper.Leisen, D.P.J. and M. Reimer.

1996, Binom ial Models forOption Valuation - Examining and

ImprovingConvergence. Applied Mathematical Finance 3 (No.

4,December). 319-346.Merton, R.C., 1973, Theory of Rational Option

Pricing,Beil Journal of Economics and Management Science 4(No. 1,

Spring), 141-183.Nawalkha, S.K. and DR , Cham bers. 1995, The

BinomialModel and Risk Neulrality: Some Important Details,The

Financial Review 30 (No. 3, August), 605-615.Omberg, E., 1988.

Efficient Discrete Time Jump ProcessModels in Option Pricing.

Journal of Financial andQuantitative Analysis 23 {No. 2. June),

161-174.Rendleman, R.J.. Jr. and B.J. Bartter. 1979, Two

StateOption Pricing. The Journal of Finance 34 {No. 5.December).

109-1110.Roge rs, L.C.G. and E.J. Stapleton. 1998, Fast

AccurateBinomial Pricing. Finance and Stochastics 2 {No.

1,November), 3-17.

Rubinstein, M., 2003, AH in All. It's been a Good Life, in

P.Field Ed.. Modern Risk Management: A History London,UK. Risk

Books, 581-586.Sharpe, W.F., G.J. Alexander, and J.V. Bailey, 1998,

Investments6 - Ed., Englewood Clifs. NJ. Prentice Hall.Tian, Y.,

1993, A Modified Lattice Approach to Option

Pricing, The Journal of Futures Markets 13 {No. 5, Aug

ust),563-577.Trigeorgis. L., 1991. A Log-Transformed Binomial

NumericalAnalysis Method for Valuing Complex

Multi-OptionInvestments , Journal of Financial and

QuantitativeAnalysis 26 {No. 3, September), 309-326.Walsh. J.B..

2003, The Rate of Convergence ofth e BinomialTree Scheme, Finance

and Stochastics 7 (No. 3, July),337-361.Widdicks. M., A.D.

Andricopoulos, D.P. Newton, and P.W.Duck, 2002. On the Enhanced

Convergence of StandardLattice Methods for Option Pricing, The

Journal ofFutures Markets 22 (No. 4, April). 315-338.Wilmott, P.,

1998, Derivatives: The Theory and Practice ofFinancialEngineering.,

West Sussex. UK. Wiley.

-

8/12/2019 Binomial Option Chance

20/20