Embed Size (px)

Citation preview

December, 2015 | Volume 35 – Issue 12

Biotechs are some of our BIGGEST Winners A good number of our superstar recommendations have been in the biotech sector, and I routinely get asked, “How do you find so many huge winners in small biotech companies?” I always answer that it took a number of years to learn how to profitably analyze development-stage biotechs. They are different from the other

stocks we recommend, because most times, they don’t have sales and earnings. Instead, we evaluate the stock’s drug candidates, look at how much cash is on hand and then compare its current price with its 52-week low and high. We take into consideration things

like: how many potential products does the company have, where are they in the FDA approval funnel, does the company have enough cash to survive for a couple of years, and is its price near the 52-week low. That investment strategy has given us several mega winners as you can see from the chart above.

There are several biotech indexes, but the one we like to follow is the NASDAQ Biotechnology ETF (IBB). We prefer the IBB index because most of the biotech stocks we recommend are listed on the NASDAQ exchange. In the last five years, the IBB has made an amazing move from a low of 85 in November, 2010 to a high of 401 in July 2015. The IBB index is volatile, and after hitting that high of 401, it plunged the following month to a low of 284. It’s currently trading around 334.

Just as a bull market can be extremely positive for stocks in a particular sector, a bear market can negatively impact those stocks. Currently the IBB is experiencing a downward trend since July. However, we know it’s only a matter of time before biotechs take off again.

Biotechs are extremely speculative and volatile. Positive results from an FDA study of the company’s drug candidates or the announcement of a licensing agreement with a major pharmaceutical company can cause the biotech to skyrocket. On the other hand, negative news usually causes the stock to plunge, sometimes to the point where it is much undervalued – and that can be a buying opportunity for savvy investors.

NASDAQ Biotechnology ETF – 5 Year Chart

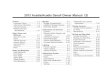

Recommended High Profit

Stock Name Symbol Price Price Percent

Acadia Pharmaceuticals ACAD 1.05 51.99 4851%

Arena Pharmaceuticals ARNA 1.38 13.50 878%

Avigen *AVGN 3.63 89.00 2352%

Dynavax DVAX 0.25 5.34 2036%

Elan Pharmaceuticals *ELN 1.87 29.93 1501%

Horizon Pharma HZNP 2.15 39.49 1737%

IDEC Pharm. *IDPH 5.00 222.00 4340%

Vanda Pharmaceuticals VNDA 0.75 19.25 2467%

CHEAP Investor's Biotech Mega Winners

Bill Mathews

The Cheap Investor Newsletter – December, 2015 2

Hill International, Inc. NYSE Stock Symbol – HIL Price: $3.27

Hill International provides program management, project management, construction management, construction claims, and other consulting services primarily for the buildings, transportation, environmental, energy, and industrial markets worldwide. The Company primarily serves the United States and other national governments, state and local governments, foreign governments, and the private sector customers.

It operates through two segments, Project Management and Construction Claims. The Project Management segment offers program management, project management, construction management, project management oversight, troubled project turnaround, staff augmentation, project labor agreement consulting, commissioning, estimating and cost management, and labor compliance services. This segment manages various phases of the construction process for construction owners, which include cost and budget controls, scheduling, estimating, expediting, inspection, contract administration, and management of contractors, subcontractors, and suppliers.

The Construction Claims segment provides claims consulting, management consulting, litigation support, expert witness testimony, cost/damages assessment, delay/disruption analysis, adjudication, lender advisory, risk management, forensic accounting, fraud investigation, and project neutral services. This segment advises clients for preventing or resolving claims and disputes based upon schedule delays, cost overruns, and other problems on construction projects.

We recommended Hill International in the October 2013 issue at $3.15, and it more than doubled to a high of $7.57 or +140%. Now that the price has fallen back near our original buy level, we decided to review it again.

Hill International reported nice increases in its sales and earnings and is selling near its 52-week low price. Insiders own about 30% of the 51 million shares outstanding, and 76 institutions own 53% of the float. The Company has a fair balance sheet with $32 million ($0.62 per share) in cash, a book value of $3.05 per share and debt of $153 million. Institutions bought 600,000 more shares than they sold for the quarter ended September 30, 2015. The negative factors are the large debt, and the price has been drifting downward.

The Company posted excellent sales and earnings for the third quarter and nine-month periods ended

September 30 as shown below. Buy Recommendation

Third Quarter Nine Months 2015 2014 2015 2014 Total Revenue $178,935,000 $161,491,000 $530,851,000 $471,143,000

Net Income (Loss) Attributable to Hill International

2,948,000 (8,966,000) 8,045,000 (2,139,000)

Net Income per Share 0.06 (0.19) 0.16 (0.05)

Avg. Shares Outstanding 51.1 Million

Total revenue for the third quarter of 2015 was $178.9 million, an increase of 10.8% from the third quarter of 2014. Consulting fee revenue for the third quarter was $158.6 million, an increase of 9.1% from last year's third quarter.

Hill International, Inc.

The Cheap Investor Newsletter – December, 2015 3

Total revenue for the first nine months of 2015 was a record $530.9 million, an increase of 12.7% from the first nine months of 2014. Consulting fee revenue for the first nine months of 2015 was a record $469.5 million, an increase of 9.9% from the first nine months of last year.

“Our net earnings were a big improvement from last year, and would have been even better but for several large one-time expenses and an unusually high effective tax rate,” said David L. Richter, Hill's President and Chief Executive Officer. “Our consulting fee growth in the third quarter was not as high as expected, and that also had a dampening effect on an otherwise strong quarter.”

Based on Hill's financial performance during the first nine months, current market conditions and the backlog amounts described above, the Company is adjusting and narrowing its prior guidance regarding consulting fee revenue growth in 2015. Hill International now expects consulting fees this year to be between $630 million and $640 million, up from $577.1 million in 2014. This guidance reflects approximately 9% to 11% growth in consulting fees for the year. In addition, based upon Hill's financial performance during the first nine months and Hill's current cost optimization program, the Company is narrowing its prior guidance regarding EBITDA (Earnings before Interest, Taxes, Depreciation and Amortization) margin as a percentage of consulting fee revenue in 2015. The Company now expects EBITDA margin this year to be between 8% and 9%, up from 6.6% in 2014.

Hill International is an NYSE-listed, low-priced stock with good increases in its revenues and earnings. If the Company continues its growth trend, the stock has the potential to move at least 50% to 100% over the next couple of years. The stock can be followed daily in some major newspapers. For more information contact: Hill International, Inc., One Commerce Square, 17th Floor, Philadelphia, Pennsylvania 19103 or call 1-215-309-7700. The Website: http://www.hillintl.com

Mattson Technology Inc. NASDAQ Stock Symbol – MTSN Price: $2.52

Mattson Technology designs, manufactures, markets, and supports semiconductor wafer processing equipment for use in fabricating integrated circuits (ICs). The Company is a leading supplier of plasma and rapid thermal processing equipment to the global semiconductor industry. Its dry strip products include the SUPREMA strip system, which is used for production and process development at 20 nanometer technology nodes and beyond by semiconductor companies. The Company’s etch products comprise the paradigmE and Alpine systems that feature a proprietary Faraday-Shielded ICP plasma source combined with etch bias control for production and process development at advanced memory and foundry/logic wafer fabs. Its conventional rapid thermal processing products include the Helios XP for use in IC production based on its dual side wafer heating and differential thermal energy control, and Millisecond Anneal products comprise Millios system for gate anneal and activation process requirements.

Recommended in the July 2014 issue at $2.11, Mattson Technology more than doubled to a high of $5.10 (+122%). With the price near $2.50, the stock is very attractive. The Company has a good balance sheet with about $37 million ($0.50 per share) in cash, a book value of about $1.16 and no debt. Insiders own about 1%

Mattson Technology, Inc.

The Cheap Investor Newsletter – December, 2015 4

of the 75 million shares outstanding, and 103 institutions own 76% of the float. During the quarter ended September 30, 2015, institutions sold about 3 million more shares than they bought. The negative factor is that huge amount of institutional selling. In addition, the price has been in a downward trend, probably due to the semiconductor industry. The semiconductor index has been quite volatile, hitting a high this year around 750, but it is currently trading in the 650 range.

Mattson Technology recently reported nice increases in both revenues and income for the third quarter and

nine-month periods ended September 27 as shown below. Buy Recommendation

Third Quarter Nine Months 2015 2014 2015 2014 Net Revenue $38,894,000 $38,430,000 $140,482,000 $123,657,000

Net Income 2,023,000 537,000 10,909,000 4,918,000

Net Income per Share 0.03 0.01 0.15 0.07

Avg. Shares Outstanding 75.1 Million

“In spite of challenging industry conditions, I am pleased with our ability to achieve top line results at the high end of expectations,” noted Fusen Chen, Mattson Technology's President and Chief Executive Officer. “Further, our flexibility in managing our cost structure to align with changes in industry demand, without sacrificing our focus on our customers' success, enabled us to exceed our own expectations for profitability.”

Gross margin in the third quarter of 2015 was in-line with previously issued guidance at 35%. Net income for the third quarter of 2015 was $2.0 million, or $0.03 per diluted share, and exceeded previously issued guidance and represented the ninth consecutive profitable quarter on a non-GAAP basis.

Mattson Technology is a speculative stock that has been in a downward trend. However, it posted good increasing revenues and earnings compared to a year ago. If Mattson continues its growth, the stock has the potential to move 50 to 100% in the next year or two. The stock can be followed daily through Internet quote services. For more information contact: Mattson Technology Inc., 47131 Bayside Parkway, Fremont, California 94538 or call 1-510-657-5900. The fax number is 1-510-492-5911. The Website: http://www.mattson.com.

Eleven Biotherapeutics, Inc. NASDAQ Stock Symbol – EBIO Price: $2.81

Eleven Biotherapeutics, Inc. is a clinical-stage biopharmaceutical company with a proprietary protein engineering platform, called AMP-Rx, that it applies to the discovery and development of protein therapeutics to treat diseases of the eye. Eleven’s therapeutic approach is based on the role of cytokines in diseases of the eye, its understanding of the structural biology of cytokines and the Company’s ability to rationally design, and engineer proteins to modulate the effects of cytokines. Cytokines are cell signaling molecules found in the body that can have important inflammatory effects.

Its product candidates include EBI-005, a novel interleukin-1 receptor antagonist that was in Phase III clinical program for the treatment of moderate to severe dry eye diseases; and has completed Phase II clinical trial for the treatment of allergic conjunctivitis.

Eleven Biotherapeutics, Inc.

The Cheap Investor Newsletter – December, 2015 5

The Company’s preclinical product candidates are EBI-031, a novel inhibitor of the cytokine interleukin-6 for the treatment of retinal diseases, such as diabetic macular edema; and EBI-028, a novel inhibitor of the cytokine interleukin-17 for the treatment of uveitis, and other diseases of the back of the eye, such as dry age-related macular degeneration.

Eleven Biotherapeutics has a collaboration and license agreement with ThromboGenics N.V. to identify protein or peptide therapeutics that directly modulate any of a specified set of targets in a novel pathway in retinal disease.

Eleven Biotherapeutics was a hot biotech IPO (Initial Public Offering) in February 2014. The IPO sold five million shares at $5.00 per share, and the stock soared to a high of $19.37 a couple weeks later. On May 18, 2015, the stock price plummeted after Eleven Biotherapeutics received negative news from the FDA on its drug candidate in Phase 3 trial. The stock closed at $11.97 on Friday, May 15 and plunged 70% after the announcement on Monday the 18th, closing at $3.69. Since then Eleven Biotherapeutics has focused on the treatment of allergic conjunctivitis with EBI-005 and developing the other drug candidates in its pipeline.

Eleven Biotherapeutics has a decent balance sheet with $47 million ($3.01 per share) in cash, a book value of $1.47 per share and debt of about $15 million. Insiders own about 14% of the 19 million shares outstanding, and 53 institutions own 73% of the float. During the quarter ended September 30, 2015, institutions purchased about 100,000 more shares than they sold. Like most development-stage biotech companies, Eleven Biotherapeutics has little revenues and a large loss. The results for the third quarter and nine-month

periods ended September 30 are shown below. Buy Recommendation

Third Quarter Nine Months 2015 2014 2015 2014 Collaboration Revenue 67,000 539,000 425,000 1,868,000

Net Loss (9,693,000) (10,674,000) (23,123,000) (26,536,000)

Net Loss per Share (0.50) (0.66) (1.23) (1.90)

Avg. Shares Outstanding 19.3 Million

“We made great strides in the advancement of our ophthalmic therapeutics pipeline this quarter. We completed patient enrollment in the first of two planned pivotal Phase 3 clinical trials of isunakinra (EBI-005), for moderate to severe allergic conjunctivitis patients suffering from the late-phase inflammatory response. This Phase 3 study follows completion in 2014 of a Phase 2 clinical trial in which isunakinra showed clinically relevant, statistically significant improvements in multiple endpoints including ocular itching, ocular tearing and nasal symptoms associated with the late phase allergen response,” said Abbie Celniker, Ph.D., President and Chief Executive Officer of Eleven Biotherapeutics. “In addition, we are continuing the preclinical work necessary to advance development of EBI-031 for the treatment of diabetic macular edema and uveitis. We remain on track to report top-line data for the ongoing isunakinra Phase 3 clinical trial in the first quarter of 2016 and to file an IND for EBI-031 in the first half of 2016.”

Eleven Biotherapeutics is speculative because of the negative FDA results on its major drug candidate. However, the Company does have three potential products in various stages of development and FDA trials. In addition, it has $47 million in cash, which would last about 1.5 years at its current burn rate. Eleven Biotherapeutics has only 19 million shares outstanding, which is a small amount; and we think it has the potential to move at least 50% over the next couple of years. If the Company signs a licensing agreement with a major pharmaceutical company or releases positive news about its FDA trials on any of its products, the stock could move considerably higher.

The stock can be followed daily through Internet quote services. For more information contact: Eleven Biotherapeutics, Inc., 215 First Street, Suite 400, Cambridge, Massachusetts 02142 or call 1-617-871-9911. The fax number is 1-617-858-0911. The Website: http://www.elevenbio.com.

The Cheap Investor Newsletter – December, 2015 6

Groupon, Inc. NASDAQ Stock Symbol – GRPN Price: $2.79

Groupon operates online local commerce marketplaces that connect merchants to consumers by offering goods and services at a discount worldwide. It also offers deals on products for which it acts as the merchant of record. The Company offers deals in various categories, including food and drink, events and activities, beauty and spa, health and fitness, home and garden, and automotive; deals on various product lines comprising electronics, sporting goods, jewelry, toys, household items, and apparel; features travel offers comprising hotels, airfare, and package deals; and tools, such as payments and credit card payment processing service, as well as point-of-sale solutions to merchants. It distributes its deals to customers through mobile applications and mobile browsers that enable consumers to browse, purchase, manage, and redeem deals on their mobile devices; Websites; emails that are targeted by location, purchase history, and personal preferences; and search engines and others.

Groupon was a hot IPO (Initial Public Offering) at $20.00 in November 2011. The stock opened at $28.00 and hit a high of $31.14 on opening day. Over the next year, the price plunged to $2.60, and we recommended it in the December 2012 issue at $2.90. Within nine months, the stock soared 340% to a high of $12.76. Recently the stock has fallen to under $3.00, and we wanted to take another look at it.

The Company has a good balance sheet with $964 million ($1.57 per share) in cash, a book value of $0.96 per share and a debt of $256 million. Insiders own 21% of the 644 million shares outstanding, and 234 institutions own 53% of the float. The negative factors include the huge amount of institutional selling causing the price to spiral downward, third quarter revenue is down slightly and the loss is larger.

The Company posted its third quarter and nine-month financial results for the periods ended September 30 as

shown below. Buy Recommendation

Third Quarter Nine Months 2015 2014 2015 2014 Consolidated Revenue $713,595,000 $714,269,000 $2,202,346,000 $2,158,895,000

Net Income (Loss) Attributable to Groupon

(27,615,000) (21,208,000) 67,196,000 (81,878,000)

Net Income per Share (0.04) (0.03) 0.10 (0.12)

Avg. Shares Outstanding 652 Million

“Over the past few years, we’ve repositioned the business for success and strengthened our foundation. On a trailing twelve-month basis, we generated $3.1 billion in revenue, $1.4 billion in gross profit, $283 million in adjusted EBITDA and $228 million in free cash flow,” Eric Lefkofsky, Chairman of the Board of Directors, said.

“We’ve successfully transformed Groupon to support our next stage of growth. The business is stable, the marketplace is scaling, and we are ready to take our next big step. Now is the right time for me to return to my role as Chairman, and let Rich (Williams), who has done a tremendous job over the past four years, lead Groupon during this next stage.”

“We delivered a solid third quarter and one that was largely in line with our expectations,” added Groupon interim CFO Brian Kayman. “Our fourth quarter guidance reflects increased investments in marketing and a tighter focus on margin improvement, both domestically and abroad.”

Groupon’s outlook for the fourth quarter reflects current foreign exchange rates, as well as expected marketing investments in customer acquisition. For the fourth quarter 2015, Groupon expects revenue of between $815 million and $865 million. This guidance anticipates nearly 400 basis points of unfavorable impact on the year-over-year growth rate from changes in foreign exchange rates. Groupon expects Adjusted EBITDA for the fourth quarter 2015 of between $40 million and $60 million, and non-GAAP earnings per share

The Cheap Investor Newsletter – December, 2015 7

of between negative $0.01 and positive $0.01.

Many institutional investors and Wall Street are writing off Groupon, much like they did in 2012. We agree that Groupon is more speculative today than when we recommended it in 2012. However, we think Groupon is undervalued at this low level. With over $3 billion in revenues and almost $1 billion in cash, Groupon has more pros than cons. The Company is restructuring by closing unprofitable international operations, and if that restructuring plan returns Groupon to profitability, the stock should do very well. With its huge revenues and cash, Groupon could be an acquisition target. On the other hand, it has a lot of shares outstanding (644 million), so there is always a chance that the Company will execute a reverse stock split.

The stock can be followed daily through Internet quote services. For more information contact: Groupon, Inc., 600 West Chicago Avenue, Suite 400, Chicago, Illinois 60654 or call 1-312-334-1579. The Website: http://www.groupon.com.

Commercial Vehicle Group, Inc. NASDAQ Stock Symbol – CVGI Price: $3.72

Commercial Vehicle Group designs, engineers, produces, and sells various cab related products and systems in North America, Europe, and the Asia/Pacific regions. The Company provides its products and systems for the commercial vehicle market, including the medium-and heavy-duty truck market; the medium-and heavy-construction vehicle market; and the military, bus, agriculture, specialty transportation, mining, industrial equipment, and off-road recreational markets.

It operates in two segments, the Global Truck and Bus, and the Global Construction and Agriculture. The Global Truck and Bus segment offers seats and seating systems, such as mechanical and air suspension seats, static seats, bus seats, and military seats, as well as seats for medium-and heavy-duty trucks; and aftermarket seats, and parts and components. It also provides trim systems and components for the interior cabs of commercial vehicles comprising vinyl or cloth-covered appliqués, armrests, map pocket compartments, carpets, and sound-reducing insulations; instrument panels; headliners/wall panels; storage systems; floor covering systems; sleeper bunks; grab handles and armrests; privacy curtains; and plastics decorating and finishing products. The Global Construction and Agriculture segment provides electronic wire harness assemblies that function as current carrying devices used to provide electrical interconnections for gauges, lights, control functions, power circuits, powertrain and transmission sensors, emissions systems, and other electronic applications on a commercial vehicle; and panel assemblies and cabinets.

We recommended Commercial Vehicle Group twice – in the June issue at $6.24 (it moved up 21% to $7.50) and last month at $3.82 (it moved up to $4.67 or +22% this month).

The Company recently announced its third quarter and nine month financial results for the periods ended

September 30 as shown below. Update – Buy at Lower Price

Third Quarter Nine Months 2015 2014 2015 2014 Revenues $202,729,000 $213,802,000 $640,649,000 $627,869,000

Net Income 2,554,000 1,162,000 9,351,000 3,393,000

Net Income per Share 0.09 0.04 0.32 0.12

Avg. Shares Outstanding 29.1 Million

Rich Lavin, President and CEO of Commercial Vehicle Group, stated, “As adjusted for foreign currency exchange translation of $4.5 million, our sales in the third quarter declined by $6.6 million, or by 3.1%. Sales in the Global Construction and Agriculture Segment declined by $11.6 million, net of unfavorable foreign

The Cheap Investor Newsletter – December, 2015 8

currency exchange translation of $3.9 million, and reflects the challenging conditions in these end markets. Global Construction and Agriculture are two of our core industries, and we intend to continue to invest in those businesses to take advantage of the long term growth we are confident will develop in the coming years. Conversely, sales in our Global Truck and Bus segment increased by 2.8%, reflecting the continued favorable production volumes in the North American medium- and heavy-duty truck markets. As regards operating income, we were pleased with our overall cost management and pull through on lower sales for the quarter.”

Tim Trenary, Chief Financial Officer of Commercial Vehicle Group, added, “As previously announced, on October 15, 2015, we elected to call for the redemption of $15 million of the $250 million outstanding 7.875% Senior Secured Notes due 2019…This redemption and therefore de-leveraging of our balance sheet is consistent with our capital allocation strategy and will reduce annual cash interest payments by $1.2 million. Adjusted for the anticipated redemption and the semi-annual interest payment we made on October 15, 2015, at September 30, 2015, the Company had liquidity of $122 million.”

Management estimates that 2015 North American Class 8 truck production levels will be in the range of 320,000 – 330,000 units, up from the 297,000 units produced in 2014. 2016 North American Class 8 truck production is expected to remain above the generally accepted annual replacement level. Additionally, Commercial Vehicle Group expects equipment production to remain soft for the remainder of 2015 and into 2016 in the global construction and agriculture end markets it serves.

While the Company’s revenues are down for the third quarter and nine months, net income is up. We like the stock for the longer term, and would consider buying more shares if the stock fell to $3.25 or below. The stock can be followed daily through Internet quote services. For more information contact: Commercial Vehicle Group Inc., 7800 Walton Parkway, New Albany, Ohio 43054 or call 1614-289-5360. The Website: http://www.cvgrp.com.

MeetMe, Inc. NASDAQ Stock Symbol – MEET Price: $2.90

MeetMe® is the leading social network for meeting new people in the US and the public market leader for social discovery. The network makes it easy to discover new people to chat with on mobile devices. With approximately 80% of traffic coming from mobile and more than one million total daily active users, MeetMe is fast becoming the social gathering place for the mobile generation. MeetMe is a leader in mobile monetization with a diverse revenue model comprising advertising, native advertising, virtual currency, and subscription. MeetMe apps are available on iPhone, iPad, and Android in multiple languages, including English, Spanish, Portuguese, French, Italian, German, Chinese (Traditional and Simplified), Russian, Japanese, Dutch, Turkish and Korean.

MeetMe was recommended in the June issue at $1.63, and the stock hit a new 52-week high of $3.07 (+88%). The Company recently reported financial results for the third quarter and nine month periods ended

September 30 as shown below. Update – Do Not Buy

Third Quarter Nine Months 2015 2014 2015 2014 Net Sales $14,308,080 $11,604,724 $37,023,933 $31,795,558

Net Income (Loss) (2,035,621) 52,031 (103,639) (4,809,088)

Net Income (Loss) per Share (0.04) --- --- (0.12)

Avg. Shares Outstanding 45.5 Million

Geoff Cook, Chief Executive Officer of MeetMe, stated, “In the third quarter, we set a new revenue record, reflecting growth in both engagement and ad pricing (or CPMs). Our mobile daily active users increased 19%

The Cheap Investor Newsletter – December, 2015 9

year over year, and our total mobile monthly active users increased 31% year over year. Additionally, our mobile CPMs increased 88% year over year. We believe it is significant to have achieved this level of revenue performance in the third quarter, as the fourth quarter is historically our strongest revenue quarter of the year, due to seasonal trends in CPMs. We are pleased to see the positive CPM momentum experienced in the third quarter continue to date into the fourth quarter.”

“On the product side, by year end, we expect to launch a major revamp of the MeetMe Plus subscription service, as well as additional native advertising partners. Our team is also hard at work at initiatives designed to deliver future user growth, including a significant revamp to our Recommendation Engine and a major new feature designed to facilitate interest-based communities.”

David Clark, Chief Financial Officer of MeetMe, added, “With continued effective management of our mobile advertising inventory, our mobile revenue during the quarter increased 73% year over year. Mobile revenue represented 81% of our total quarterly revenue, the highest percentage in our history and up from 58% in the year ago quarter. Much of that revenue improvement flowed through to adjusted EBITDA, which increased to $5.2 million on a year over year basis, resulting in a 37% adjusted EBITDA margin.”

According to American Banking and Market News, On November 5, “Equities researchers at Roth Capital boosted their third quarter 2016 EPS (Earnings per Share) estimates for MeetMe in a research note issued to investors on Wednesday, according to Zacks. Roth Capital analyst D. Aftahi now forecasts that the firm will earn $0.08 per share for the quarter, up from their prior forecast of $0.07. Roth Capital currently has a “Buy” rating and a $4.25 price target on the stock.

“In other news, CEO Geoffrey Cook sold 180,000 shares of the company's stock in a transaction that occurred on Wednesday, October 28th. The shares were sold at an average price of $2.47, for a total transaction of $444,600.00. Following the transaction, the chief executive officer now directly owns 1,712,093 shares in the company, valued at $4,228,869.71.”

MeetMe had a great move from a low of $1.52 on October 1 to a recent 52-week high of $3.07. Even though we like the stock, we would not buy it at this high price. The stock can be followed daily through Internet quote services. For more information contact: MeetMe, Inc., 100 Union Square Drive, New Hope, Pennsylvania 18938 or call 1-215-862-1162. The Website: http://www.meetmecorp.com.

Iridium Communications, Inc. NASDAQ Stock Symbol – IRDM Price: $7.76

Iridium Communications is the only mobile voice and data satellite communications network that spans the entire globe. It enables connections between people, organizations and assets to and from anywhere in the world, in real time. It offers postpaid mobile voice and data satellite communications services, prepaid mobile voice satellite communications services, broadband data services, and machine-to-machine services for sending and receiving data from fixed and mobile assets in remote locations to a central monitoring station.

The Company also provides inbound connections from the public switched telephone network, subscriber identity module, activation, customer reactivation, and other peripheral services. In addition, it offers voice and data solutions, including personnel tracking devices; asset tracking devices for equipment, vehicles, and aircraft; aircraft and submarine communications applications; specialized communications solutions for high-value individuals; mobile communications and data devices for the military and intelligence community, such as secure satellite handsets, as well as offers voice, netted voice, data, messaging, and paging services; and maintenance services for the Department of Defense’s dedicated gateway.

We recommended Iridium twice. The first time was in the December 2013 issue at $5.87, and it almost

The Cheap Investor Newsletter – December, 2015 10

doubled to $11.36. We recommended the stock again in the October issue at $6.40 and it moved up 35% to a high of $8.64 this month.

Iridium released its third quarter and nine-month financials for the period ended September 30 as shown

below. Update – Buy at Lower Price

Third Quarter Nine Months 2015 2014 2015 2014 Total Revenue $106,034,000 $107,493,000 $304,960,000 $308,046,000

Net Income Attributable to Common Stockholders

25,688,000 16,529,000 64,977,000 43,489,000

Net Income per Share 0.27 0.18 0.68 0.51

Avg. Shares Outstanding 95.3 Million

The Company ended the quarter with 781,000 total billable subscribers, which compares to 726,000 for the year-ago period and is up from 766,000 for the quarter ended June 30, 2015. Total billable subscribers grew 8% year-over-year, driven by growth in machine-to-machine (“M2M”) customers.

“Iridium continues to succeed in a challenging macroeconomic environment,” said Matt Desch, CEO, Iridium. “While our commercial service revenues are being impacted by a strong U.S. dollar and weakness in the energy sector, we are benefitting from strength in government services and continued growth in M2M data services.”

Commenting on Iridium NEXT, Desch said, “We have revised the date of the initial launch of the Iridium NEXT program to reflect an updated delivery schedule from our prime satellite supplier, Thales Alenia Space. In consideration of this timeline, Iridium and launch service provider Kosmotras have now scheduled the deployment of the first two satellites of the Iridium NEXT constellation for April 2016, and we continue to expect the Iridium NEXT constellation to be fully operational by the end of 2017. Insurance for the initial launch has been fully bound, and Iridium has agreed with its lenders on material terms to amend its credit facility to provide additional flexibility in obtaining launch and in-orbit insurance.” Desch continued, “Once deployed, Iridium NEXT will offer advanced satellite services like AireonSM and Iridium CertusSM broadband, which will drive revenue growth in 2018 and beyond.”

For full-year 2015, Iridium continues to expect total service revenue growth between 1% and 3%. Full-year 2015 Operational EBITDA should be approximately $230 million. (OEBITDA for 2014 was $216.5 million). Given the expected 2017 Iridium NEXT system completion, the Company continues to project total service revenue between $420 million and $465 million for the full-year 2018, an increase from $309.4 million for the full-year 2014. OEBITDA margin should be approximately 60% in 2018.

While revenues for the third quarter and nine month periods are down slightly, net income is up. We would buy more shares if Iridium fell to $6.50 or below. The stock can be followed daily through Internet quote services. For more information contact: Iridium Communications Inc., 1750 Tysons Boulevard, Suite 1400, McLean, Virginia 22102 or call 1-703-287-7400. The fax number is 1-703-287-7450. The Website: http://www.iridium.com.

ArQule, Inc. NASDAQ Stock Symbol – ARQL Price: $2.42

ArQule is a biopharmaceutical company engaged in the research and development of targeted therapeutics to treat cancers and rare diseases. Its mission is to discover, develop and commercialize novel small molecule drugs in areas of high unmet need that will dramatically extend and improve the lives of its patients. The Company’s prioritized clinical-stage pipeline consists of four drug candidates, all of which are in targeted,

The Cheap Investor Newsletter – December, 2015 11

biomarker-defined patient populations, making ArQule an early leader in precision medicine.

ArQule’s lead product, in Phase 2 and Phase 3 clinical development, is tivantinib (ARQ 197), an oral, selective inhibitor of the c-MET receptor tyrosine kinase. The Company’s pipeline includes: ARQ 092, designed to inhibit the AKT serine/threonine kinase; ARQ 087, a multi-kinase inhibitor designed to preferentially inhibit the fibroblast growth factor receptor (FGFR) family; and ARQ 761, a Beta lapachone analog being evaluated as a promoter of NQ01-mediated programmed cancer cell necrosis. ArQule’s current discovery efforts are focused on the identification of novel kinase inhibitors, leveraging the Company’s proprietary library of compounds.

Recommended in the February issue at $1.11, ArQule hit a 52-week high this month of $2.63 or +137%. The Company released its financial results for the third quarter and nine-month periods ended September 30 as

shown below. Update – Do Not Buy

Third Quarter Nine Months 2015 2014 2015 2014 Research and Development Revenue $2,653,000 $2,662,000 $8,442,000 $8,239,000

Net Loss (2,354,000) (6,399,000) (10,922,000) (19,879,000)

Net Loss per Share (0.04) (0.10) (0.17) (0.32)

Avg. Shares Outstanding 62.8 Million

“The last few months have been very productive for ArQule from both an operational and pipeline development standpoint,” said Paolo Pucci, Chief Executive Officer of ArQule. “As we are approaching the completion of recruitment for the METIV-HCC trial we have exercised our co-commercialization option with Daiichi Sankyo in the U.S. for tivantinib. We are also making progress with ArQule’s proprietary pipeline, which continues to show promising results in multiple biomarker-driven trials.”

“We continue to show excellent progress in our AKT program with the achievement of the fifth PR in the phase 1b expansion cohort,” said Dr. Brian Schwartz, M.D., Head of Research and Development and Chief Medical Officer at ArQule. “These data validate the preclinical hypothesis underlying the recently published PLOS ONE manuscript. We will be presenting additional data on ARQ 092 and ARQ 751, as well as tivantinib and ARQ 087, at the AACR-NCI-EORTC conference, triple meeting, in Boston this weekend. We are also looking forward to our collaborator, the National Institutes of Health, dosing the first patient with ARQ 092 in Proteus syndrome.”

Highlights in the third quarter include Tivantinib phase 2 data, in hepatocellular carcinoma presented at the International Liver Cancer Association Conference, supports tumor MET status as a prognostic and predictive biomarker. The biomarker-driven phase 3 trial for tivantinib, METIV-HCC, in second line hepatocellular carcinoma (HCC) is expected to complete patient accrual by year end.

The Phase 1 trial for Proteus syndrome with ARQ 092 is open for enrollment. ArQule’s collaborator, the National Institutes of Health, has completed pre-trial preparations and recently opened the site for enrollment. The Phase 2 trial for ARQ 087 in intrahepatic cholangiocarcinoma (iCCA) continues to enroll. Five sites are now open and enrolling in the U.S. for iCCA patients with the FGFR translocation.

For 2015, ArQule expects net use of cash to range between $22 million and $24 million. Revenues are expected to range between $10 million and $11 million. Net loss is expected to range between $13 million and $15 million, and net loss per share is expected to range between ($0.21) and ($0.24). ArQule expects to end 2015 with between $37 million and $39 million in cash, equivalents and marketable securities.

We like ArQule for the longer term, as the Company has several products in FDA trials and a large cash position. Since the stock has more than doubled from our recommendation and hit a new 52-week high this month, investors should consider taking some profits off the table. The stock can be followed daily through Internet quote services. For more information contact: ArQule Inc., One Wall Street, Burlington, Massachusetts 01803 or call 1-781-994-0300. The Website: http://www.arqule.com.

The Cheap Investor Newsletter – December, 2015 12

DISCLAIMER AND DISCLOSURE NOTICE: The Cheap Investor is a monthly subscription-based newsletter, along with its related publications (including, but not limited to special reports, but not including paid for alerts) and other services (the “Newsletter”), is edited by Bill Mathews (the “Editor”) in association with Mathews and Associates, Inc. (“MAI”), and is published by Core Capital Media, LLC (“Core Capital”). The Newsletter presents publicly available data and information concerning publicly traded/quoted companies to our subscribers and potential subscribers. None of Core Capital, the Editor, or MAI, is registered as an investment advisor or broker/dealer. Unless the context otherwise dictates, reference in this disclaimer to “us,” ‘we,” or “our,” refer collectively to Core Capital, the Editor and MAI.

Other than subscription revenues, we receive no compensation with respect to any of the companies detailed in the Newsletter.

As of November 20, 2015, the Editor and MAI own securities of the following companies initially detailed in this edition of the Newsletter (identified with the words “Buy Recommendation” in bold type): 10,000 shares of Groupon.

However, please note that Core Capital, and its respective principals, employees, partners, directors, and officers may from time to time own, buy or sell the securities of a company detailed in the Newsletter. We have implemented a policy restricting our principals, employees, partners, directors and officers from purchasing the securities of any company detailed in the Newsletter less than seven (7) days after the date of the publication of the Newsletter in which such company is detailed and selling the securities of such company until at least thirty (30) days have lapsed from the date of the publication of the Newsletter in which such company is detailed.

For companies that are detailed in the Newsletter in order to update readers regarding the securities of such company (these companies are identified with the word “Update” before the Editor’s recommendation), please refer to the Newsletter in which the Company was initially detailed for additional disclosures. For your convenience the paragraph regarding each updated company will identify the issue in which such company was initially detailed.

We have not made, nor do we make, any claim that we have taken any steps to ensure that the securities of any company detailed in the Newsletter are suitable for any particular investor. In particular, such securities may not be suitable for you and it is recommended that you consult with an independent advisor if you have any concerns or questions regarding such securities. Accordingly, you should not view the information in the Newsletter as constituting investment, legal, accounting or tax advice or a representation that any investment or strategy is suitable or appropriate to your individual circumstances or otherwise constitutes a personal recommendation to you. Information, opinions and estimates referenced in the endorsement reflect a judgment at its original date of publication and are subject to change without notice. You should note also that the price and value of the securities of a company detailed in the Newsletter is as of a date prior to publication and may not reflect the most recent price for such security. The price and value of the securities of a company detailed in the Newsletter can fall as well as rise, and may have a high level of volatility and associated risk.

We do not claim any special expertise or knowledge of the industries in which a detailed company operates. You should conduct your own research and due diligence to independently verify the data, material and other information contained in the Newsletter. You are solely responsible for your own investment decisions.

The opinions and analyses presented in the Newsletter are based on sources and information believed to be reliable, but no representation or warranty, expressed or implied, as to the reliability, accuracy or completeness of any of the data, material and other information presented and we are not responsible for errors or omissions contained in the Newsletter.

The views and opinions expressed in the Newsletters are those of the Editor and do not necessarily reflect the views of Core Capital, MAI, its affiliates, or its employees.

Past performance is no guarantee of future success and you should not assume that the securities of companies detailed in current or future Newsletters will perform better than or even equal to the performance of the securities of companies detailed in prior Newsletters. All stock investments carry some degree of risk. By investing in any of the stocks of the companies detailed in the Newsletter you can and may lose some or all of your investment. Do not invest in any stock if you are not prepared to lose your entire investment.