Embed Size (px)

Citation preview

• ISSUE - I • VOLUME - VII • OCTOBER - 2011

UPDATE

www.bizsolindia.com

UPDATE

THISMONTH

4U

IN THIS ISSUE

We believe in C-2

This Month 4 U C-2

Editorial 1

What's New 2

DEPB out Drawback Enhanced 10

Beyond the Onvious 12

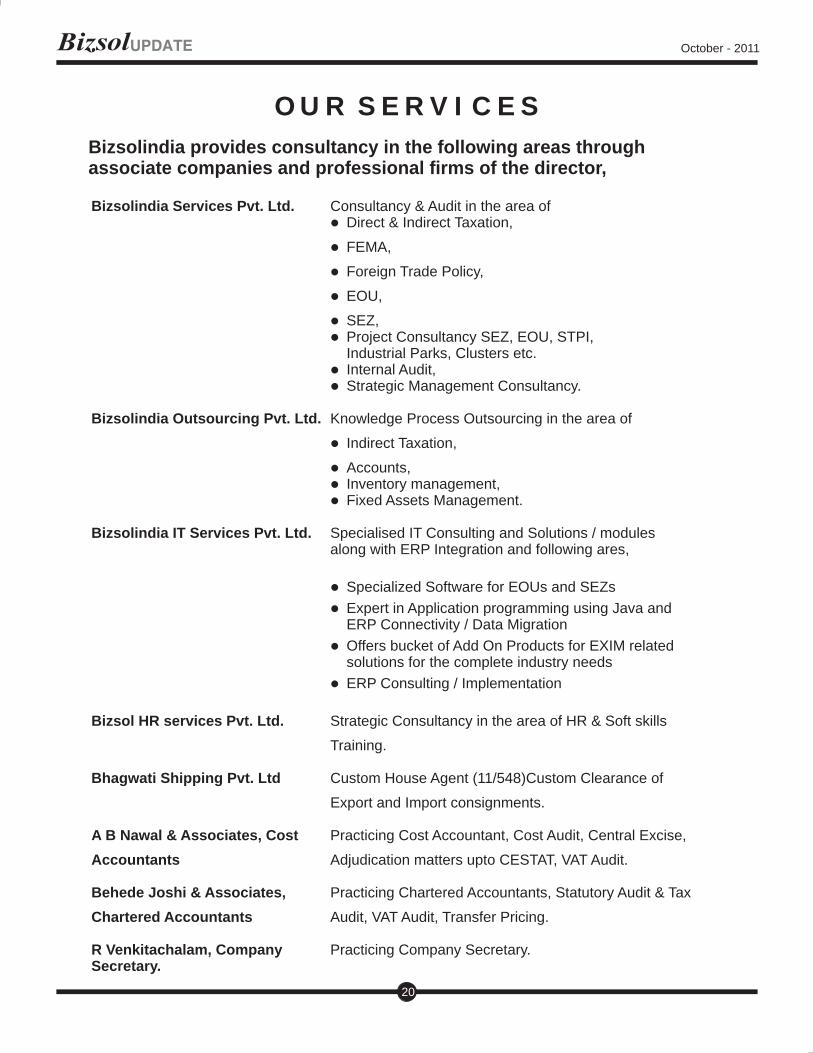

Did you Miss this 19Our Services 20

Photo C-3

Greeting C-4

• For important due dates please turn over

Payments Due Dates

Excise Duties-Sep 2011 05/10/11 Service Tax – Sep 2011 05/10/11 Excise Duties- Sep 2011 By E-Payment 06/10/11 Service Tax -Sep 2011–By E Payment 06/10/11

TDS/TCS- Sep 2011 07/10/11 Provident Fund- Sep 2011 15/10/2011

Central Sales Tax –Sep 2011 Return-cum-Challan 21/10/2011 VAT – Sep 2011 Return 21/10/2011 ESI Contribution 21/10/2011 Professional Tax 31/10/2011

Returns

ER-1 and ER-2 Monthly return for Sep 2011

10/10/11

ER-6- Sep 2011 10/10/11

October - 2011 W E B E L I E V E I N

E D I T O R I A LThere is a classic dilemma that anyone who writes an Editorial faces. Write on a subject about which nothing more is there to write about; but at the same time not writing about it would be tantamount to a kind of abdication of responsibility. While writing this piece I face this dilemma today. L’affaire Anna Hazare and his anti corruption movement is a subject which is bound to be a case study of sorts for business schools and social activists and it deserves a discussion even at the cost of repetition. Malcolm Gladwell in his famous book “The Tipping Point” explains in graphic detail the times of reckoning, however small or insignificant, which lead to earth-shaking events. When Gladwell comes out with a new edition of this famous book he could refer to the huge response to Anna Hazaare’s movement. There is something hugely significant when a diminutive and hitherto relatively unknown man from a village in Maharashtra who did not have any following in any part of the country other than his home state captures the imagination of the entire county and galvanises a movement of this magnitude. If nothing else he proved that a cause is more important than a person when it comes to mass social movements. The scourge of corruption has come to be accepted by the population as something one has to put up with in the absence of any movement to counter it. It was something to be accepted as a way of life with little or no chance of redressal. When Anna launched the movement, people found an anchor especially since Anna himself was not tainted by any scandal nor did he have any political (especially of the electoral variety) ambitions. The population instantly identified itself with the cause and rallied behind the seventy four year old man to whom they bestowed a Gandhian halo. It was almost as if the people were waiting for the moment and Anna’s initiative became the tipping point and snowballed into a mass social movement.Who won and who lost in the faceoff between the Government and Anna will depend on whom you ask. The spin doctors on either side would wax eloquently that their respective side won this battle of attrition. Some would say that it was a ‘win-win’ situation for both. It may be true in this case. How does one define this clichéd phrase ‘win-win’? In a conflict management situation it may not be possible to explain the concept with the gains of both parties, as a gain for one has to be at the cost of other. It is almost impossible to feel that you have gained something when the other party is also celebrating at the same time for the same reason. The best way to decide would be to look at what each party set out to achieve and did not. If you feel that you won but you could have done better and this sense of disappointment is shared by the other party also even while claiming victory you have indeed a win-win solution in hand. Going by this yardstick both the Government and Team Anna left the battle field with a sense of disappointment even while claiming victory. For us the people of this county it was indeed a win all the way in that we have something now to hope for in our fight against corruption.Anna’s movement against corruption was not without its ironies. It was happening at a time when in the middle east the

Arab spring was peaking replete with all the violence associated with it. The Indian middle class joined the movement in droves when it was clear that the entire process was to be non-violent and it evoked a kind of romance associated with the freedom movement with Gandhi caps et al. You may or may not agree with the movement of Anna Hazare, but you must compliment his team for carrying out a protest movement without violence and still claim victory. Credit should go to both parties for showing restraint and it looks as if the concept of non violent protest is in our DNA. On the last day of Anna’s fast the irony of a minister like Vilasrao Deshmukh partaking in the final ritual of the protest fast was not lost on anyone. Acting as a interlocutor of the Government he handed over the final letter from the Prime Minister to Anna Hazare and he also did not miss the photo-op of the historic occasion even as a popular national magazine carried a cover page article on him for the very act against which Anna Hazare hit the streets and took on the might of the State! Another paradox was when Rahul Gandhi stood up to talk on the subject of Anna Hazare’s crusade against corruption - a classic case of saying the right thing at the wrong time. He articulated in favour of creating a constitutional body to deal with corruption with a slew of measures. Besides the fact that he could have articulated them before, his views were at variance with that of the Government, though in my opinion he was more right than all others.Having commented on the outcome of the movement it may be in order to look at the performance of the players. No one seems to have come out of the conflict smelling of roses. It may be natural to overlook the ham-handed way in which the Government handled the entire episode if you are a sympathiser of the cause. But it is extremely disconcerting to think that the Government of yours with all the resources at its command can be so inept in formulating an effective strategic response to Anna Hazare’s movement. It is quite scary that the Government is seen as so clumsy time and time again. Memories of the Government’s handling of Ramdev’s protest are still fresh in our minds. How safe are we with such a Government? Manmohan Singh is proving to be a burden on the country as well as our conscience at the same time.If the Government did not cover itself with glory, the story is no different with Team Anna either. Post 9/11 George Bush famously said “you are either with us or with them”. Anna Hazare appears to have taken a leaf out of the former US President’s strategy book. His implicit slogan was “my way or high way”. Strange that those who express dissent do not brook no dissent! We saw some brilliant performances on the floor of the House in Parliament. It looks as if our representatives in the Parliament come into their own when they were not constrained by their respective party whips. We saw one of the best debating exercises during the impeachment proceedings of Justice Soumitra Sen as well. The quality of debate rose to an entirely different level during the debate on Anna Hazare’s protest episode. We got a glimpse of what the parliamentarian are really capable of. Anna Hazare’s movement is a defining moment in India’s history – both for the means and the end. His protest is bound to become the new benchmark for all protests in future – violent or otherwise. Indian parliamentary democracy is all set to change course. The institution of Parliament which came into being after a non-violent movement, barely managed to survive the assault on it by Anna’s non-violent movement. India got independence from the British and let us hope we get freedom from corruption after this epic struggle.This Editorial is being dedicated to this cause.Thank you.Venkat R Venkitachalam

October - 2011

1

What's New…!!CUSTOM

Anti-dumping duty

Notification

l Anti-dumping duty on Rubber Chemicals imposed earlier if imported from Republic of India under No. 4, 5 & 6 of the Table of Notification No. 133/2008 CUS has been withdrawn. [CUS NTF NO. 93/2011 DATE 20/09/2011]

l Anti-dumping duty on Rubber Chemical PX-13 (6PPD), originating in or exported from, Korea RP (Heading 29, 38) will continue upto 04.05.2013. [CUS NTF NO. 91/2011 DATE 20/09/2011]

l Anti-dumping duty on Para Nitroaniline (29214226) has been imposed when goods are originated or imported from China PR. [CUS NTF NO. 88/2011 DATE 09/09/2011]

l Anti-Dumping Duty on cold rolled flat product of stainless steel falling under chapter 7219 having width of more than 1000 mm has been imposed if imported from China PR, Korea, Japan, South Africa, Thiland, Taiwan and USA. [CUS NTF NO. 86/2011 DATE 06/09/2011.]

l Safeguarding duty on N1, 3-dimethyl butyl-N’phenylenediamine (PX-13 also known as 6 PPD), falling under tariff items 3812, 3810, 2921, 2925, 2934 and 2942 at 30% / 25% as the case may be after reducing anti-dumping duty paid thereon if goods are imported from notified countries. [CUS NTF NO. 83/2011 DATE 30/08/2011.]

l Anti-dumping duty on imports of PVC Flex Films (Chapter 39) originating in or exported from, People’s Republic of China has been continued for a period of five years. [CUS NTF NO. 82/2011 DATE 25/08/2011]

l A n t i - d u m p i n g d u t y o n i m p o r t s o f Polytetrafluoroethylene (PTFE) (390461) originating in or exported from, People’s Republic of China has been continued for a period of five years. [CUS NTF NO. 81/2011 DATE 24/08/2011]

l Anti-dumping duty on imports of 1-Phenyl-3-Methyl-5-Pyrazolone, falling under Chapters 29 and 98 originating in or exported from, People’s

Republic of China has been continued for a period of five years. [CUS NTF NO. 80/2011 DATE 24/08/2011]

l Definitive anti-dumping duty has been imposed on imports of Caustic soda (ITCHS 281511, 281512), originating in or exported from Thailand, Taiwan (Chinese Taipei) and Norway. [CUS NTF NO. 79/2011 DATE 23/08/2011]

l Anti-dumping duty on imports of Sodium Nitrite (28341010) originating in, or exported from, People’s Republic of China has been continued for a period of five years. [CUS NTF NO. 76/2011 DATE 17/08/2011]

l Anti-dumping duty on Pentaerythritol falling under sub-heading 290542 originating in, or exported from Chinese Taipei has been continued upto 27th April, 2013. [CUS NTF NO. 74/2011 DATE 12/08/2011 & CUS NTF NO. 75/2011 DATE 12/08/2011]

l Anti-dumping duty on nylon filament yarn of specification synthetic filament yarn including synthetic monofilament of less than 67 decitex of nylon or other polyamides (Chapter 54) originating in, or exported from, People’s Republic of China, Chinese Taipei, Malaysia, Indonesia, Thailand and People’s Republic of Korea has been continued upto 28th November, 2011. [CUS NTF NO. 73/2011 DATE 09/08/2011]

l Anti-dumping Duty of 0.82 USD / KG has been on Opal Glassware falling under heading 7013, originating in, or exported from, People’s Republic of China and UAE. [CUS NTF NO. 72/2011 DATE 09/08/2011]

l Anti-dumping duty on ‘Partially Oriented Yarn(POY)’, falling under heading 5402 originating in, or exported from, the China PR has been continued upto 10th February 2012. [CUS NTF NO. 71/2011 DATE 09/08/2011]

l Anti-dumping duty on imports of Sodium Formaldehyde Sulphoxylate (ITCHS 28311020) originating in, or exported from, China PR has been extended for a further period of five years pursuant to the final findings of Sunset review investigations conducted by the Directorate General of Anti-dumping and Allied duties. [CUS NTF NO. 70/2011 DATE 05/08/2011]

October - 2011

2

l Silghat in the District of Nagaon, Assam has been notified land frontier of Bangladesh. [CUS NTF NO. 61/2011 (NT) DATE 25/08/2011]

l Mathilakam (Thrissur) in Kerala has been notified as port for Unloading of imported goods and the loading of export goods. [CUS NTF NO. 60/2011 (NT) DATE 24/08/2011]

l Chandigarh has been notified has Customs Port for Unloading of baggage and the loading of baggage and Unloading of imported goods and the loading of export goods related to Ministry of Defense. [CUS NTF NO. 58/2011 (NT) DATE 19/08/2011]

l Tariff Value of Poppy Seeds has been revised USD 2242/MT and Brass Scrap (all grades) to USD 4399 / MT. [CUS NTF NO. 57/2011 (NT) DATE 12/08/2011]

l Customs Tariff (Determination of Origin of Goods under the Comprehensive Economic Partnership Agreement between the Republic of India and Japan) Rules, 2011 has been notified for import of goods at concessional rate of duties from Japan. [CUS NTF NO. 55/2011 (NT) DATE 01/08/2011]

l Prohibition on Import of Acetate tow (5502 00 10) and Filter Rod (56 or any Chapter) for manufacture of Pharmaceutical products of Chapter 30 has been revoked. [CUS NTF NO. 16/2011 (NT) DATE 01/03/2011]

Circulars

l Detail clarification has been issued on new Duty Drawback Rates notified & made applicable w.r.f. 01.10.2011. [CUS CIR NO. 42/2011 DATE 22/09/2011]

Please read detail article on the subject in this Bizsol Update.

l Since export of Onion are permitted with minimum limit of FOB value and being sensitive item at par with Basmati Rice & Wheat, Board instructed to follow the guidelines without deviation and also ask to submit fortnightly report to field formation. [CUS CIR NO. 41/2011 DATE 14/09/2011] & [CUS CIR NO. 43/2011 DATE 23/09/2011]

l To avoid the interest during the time lag between provisional assessment & final assessment, system of making Voluntary payment of duty before final assessment has been introduced without change in clauses of the bond and limiting refund if applicable only after final assessment. [CUS CIR NO. 40/2011 DATE 09/09/2011]

l Since self-assessment has been introduced for import & export consignment and post audit has been introduced, Risk Management Control

Tariff Notification

l Anti-dumping duty on Morpholine originating in or exported from China PR, European Union and the United States of America, for a period of six months (Heading 29) has been imposed. [CUS NTF NO. 91/2011 DATE 20/09/2011]

l Deeper concessions under DFTP scheme for Least Developed Countries (LDCs) has been provided for certain goods when imported from least developed countries. [CUS NTF NO. 90/2011 DATE 16/09/2011]

l Amendments in the notification regarding exemption for Defence Machinery & Equipment has been made so as to extend exemption to para-military Force or Home Ministry. [CUS NTF NO. 89/2011 DATE 12/09/2011]

l Additional number of items have been included in the list for concessional rate of customs duty when manufactured goods are imported from SAARC under SAFTA agreement. [CUS NTF NO. 85/2011 DATE 06/09/2011.]

l Exemption on Basic Customs Duty has been granted on import of Cold rolled sheets of grain- oriented (CRGO) silicon-electrical steel for manufacture of transformers. [CUS NTF NO. 84/2011 DATE 09/09/2011]

l Quantitative restriction has been enhanced from 30,000/- MT to 50,000/- MT for import of Milk Powder falling under ITCHS 0402 10 or 0402 21 00 at concessional rate of duty. [CUS NTF NO. 78/2011 DATE 19/08/2011]

l Exemption of Basic Customs Duty on Coking Coal will be available irrespective of any criteria reflectance & Swelling Index. Accordingly the Notification 21/2002 has been amended. [CUS NTF NO. 77/2011 DATE 17/08/2011]

Non Tariff Notification

l New Duty Drawback Rates has been notified w.e.f. 01.10.2011 and interest provision has been made applicable if claim of duty drawback rate has not been given within one month. [CUS NTF NO. 68/2011 (NT) DATE 22/09/2011]& [CUS NTF NO. 69/2011 (NT) DATE 22/09/2011]

Kindly read Article for more details in this Bizsol Update.

l Explanation has been inserted to clarify resident Public Limited Company for the purpose of section 28EE of Customs Act, 1962 [CUS NTF NO. 67/2011 (NT) DATE 22/09/2011]

l CBEC revises tariff value of poppy seeds and brass scrap (all grades) & palm Oil [CUS NTF NO. 63/2011 (NT) DATE 30/08/2011] & [CUS NTF NO. 65/2011 (NT) DATE 15/08/2011] & [CUS NTF NO. 71/2011 (NT) DATE 30/09/2011]

October - 2011

3

l Customs Department has introduced Authorized Economic Operator (AEO) programme for importer, exporter, logistics provider, Customs House Agents based on decided criteria. AEO is implemented to ensure security in global supply chain in international movement of goods.

Instructions

Provisions of Plastic Waste Management and Handling Rules, 2011 has been made applicable on Export of Pan Masala-Gutkha packed in plastic sachet by 100% EOU. [F.No. 528/69/2011-STO (TU) dated 30.08.2011]

CENTRAL EXCISE

Tariff Notification

l Biscuits which are cleared in packaged form with per kg retail sale price equivalent not exceeding Rs. 100 if consumed with in the factory of manufacturer is exempt from payment of Central excise duty, however this exemption shall not apply to any inputs or intermediate goods other than sugar syrup or cream used in the manufacture of goods mentioned at S. No. 19. of Notification No. 10/1996 CE dated 23.06.1996. [Notification No. 39 /2011 – CE dated 12.09.2011]

Non Tariff Notification

l Now electronic filling of return is mandatory and irrespective of any limit turnover or amount of duty. [ Notification No. 21/2011-CE (N.T) dated 14.09.2011]

l Format of ER-1 & ER-3 return has been revised again amending the format which was amended in July 2011 [Notification No. 20/2011 -CE (N.T. dated 13.09.2011)]

One of the most appreciable amendment to eliminate interface with Central Excise Officers for obtaining acknowledgment and perhaps cases on forthcoming “Janalokpal” will automatically reduce.

Circulars

l Since e-filing of all Central Excise Returns in ACES made mandatory it is requested to all Central Excise Officer to provide all assistance so as to help them in adopting the new procedure. [Circular No. 955/14/2011 -CX dated 15.09.2011]

l Regional Advisory Committee for organized sector and small scale industries will be constituted with the view that to facilitate greater participation of the representatives of the trade

System for import & export clearance needs to be liberalized therefore, Board has directed to achieve the target of clearing the export consignment without any delay at least to reach expectation of 80% of Air Consignment, 70% for sea consignment & 60% for ICD / CFS and target is require to be made within 6 months. [CUS CIR NO. 39/2011 DATE 02/09/2011]

l It has been decided by the Board that the applicants who had already passed the examination held under regulation 9 of CHALR, 1984 but have not been granted license and are seeking qualification in additional subjects shall be allowed to clear the examination by 31.12.2012 irrespective of number of chances to become eligible for grant of CHA license in terms of Regulation 9 of CHALR, 2004. [CUS CIR NO. 38/2011 DATE 24/08/2011]

l AEO certified operators will be entitled to preferential treatment in terms of less Customs examination, relaxed procedural requirements etc. This is subject to the authorized operators maintaining security standards and compliance requirements as detailed in Annexure and informing the AEO Programme Manager within 30 days in case of any significant change in business or business processes. [CUS CIR NO. 37/2011 DATE 23/08/2011]

l It has been re-clarified by the Board that entitlement of bank guarantee exemption to 100% EOUs / EHTP / STP / BTP units should be denied only in cases involving fraud/ collusion/ willful mis-statement/ suppression of facts, whether or not extended period for issue of SCN has been invoked. In simple cases of issue of show cause notices for procedural violation against such units, the entitlement of exemption f rom fu rn i sh ing bank guaran tee to EOU/EHTP/STP/BTP units need not be denied. [CUS CIR NO. 36/2011 DATE 12/08/2011]

l Customs officers have been directed by CBEC to be vigilant and take necessary actions on the importer who are not declaring common name as well as chemical names for proper classification of the goods. This is in view of illegal import of pesticides under various headings of harmonized tariff by declaring their chemical names instead of both common and chemical names by some traders. [CUS CIR NO. 35/2011 DATE 09/08/2011]

l In view of Prohibition by U. S. Department of Agriculture, Animal and Plant Health Inspection Service (USDA - APHIS), it is clarified that air passengers travelling to USA should not carry rice in their baggage. [CUS CIR NO. 34/2011 DATE 03/08/2011]

October - 2011

4

classification or valuation needs to be filed only before Hon’ble Supreme Court. [F. No. 390/ Misc. / 100/2010-JC]

SERVICE TAX

Notification

l Exemption granted on R & D Cess for payment of service tax has been amended considering provisions of Point of Taxation Rules, 2011, and therefore R & D Cess payable is also required to deducted while arriving taxable value and need to be paid within six month. [47/2011-ST, DT. 19/09/2011 ] [46/2011-ST, DT. 19/09/2011]

l Arbitrator / Arbitrator firms have got some relief, exemption from service has been granted when service provided by them in relation to advice, consultancy or assistance in any branch of law in any manner to any other business entity has been exempted. [45/2011-ST, DT. 12/09/2011]

l Exemption from payment of service tax has been extended to authorise person of Sub-broker also in relation to sale or purchase of securities listed on a registered stock exchange. [44/2011-ST, DT. 09/09/2011]

l Now electronic filling of return is mandatory and irrespective of any limit turnover or amount of duty. [Notification No. 43/2011 ST dated 25.08.2011] One of the most appreciable amendments to eliminate interface with Central Excise Officers for obtaining acknowledgment and perhaps cases on forthcoming “Janalokpal” will automatically reduce.

Circulars

l BSNL providing services for ‘Guaranteed Public Telephone operating only for local calls’ is continued to be exempted even after becoming public sector undertaking. [Circular No. 146/15/ 2011 – ST dated 20.09.2011]

l Certificate charges paid for obtaining certificate Origin from Chamber of Commerce or presecribed Agency will get classified under or ‘technical inspection or certification service’, therefore will be entitled for refund under Notification 17/2009-ST dated 7th July, 2009. [Circular No. 145/14/ 2011 – ST dated 19.08.2011]

Instructions

At last the issue of payment under reverse charge, when services are provided by person not resident of India and not having permanent establishment in India and effective date of applicability has been come to end and

and industry and also to raise the quality of deliberations in the forum, the RAC should be constituted at the zonal level and the Chief Commissioner should preside over the RAC meetings. [Circular No. 953/14/2011 -CX dated 12.09.2011]

l Provisions of stuffing of export containers under supervision of Central Excise Officers has been more clarified to avoid different practices at different commissionerate. One time factory stuffing permission is required to be obtained and even the intimation of exports or scheduling of export containers can be done online or through e-mail and sealing / examination is required to be made either by Superintendent or Inspector (not both). Moreover no MOT charges is payable for the export made from registered premises. [Circular No. 952/13/2011-CX dated 08.09.2011]

l Change of designation of officers representing CBEC in the CESTAT

Rank of the officer Present New DesignationDesignation

(i) Chief Commissioner CDR Chief Commissioner (A.R.)

(ii) Commissioner Jt. CDR Commissioner (A.R.)

(iii)a) Addl. Commissioner SDR Addl. Commissioner (A.R.)

b) Joint Commissioner SDR Joint Commissioner (A.R.)

(iv)a) Deputy Commissioner JDR Deputy Commissioner (A.R.)

b) Assistant Commissioner JDR Assistant Commissioner (A.R.)

c) Superintendent JDR Superintendent (A.R.)

d) Appraiser JDR Appraiser (A.R.)

The abbreviation (A.R.) stands for (Authorised Representative).[Circular No. 951/12/2011 -CX dated 26.08.2011]

l Classification of Chlorinated Paraffin waxes (in solid form), the HSN Explanatory Note (B)(a) to Heading 27.12 of CETH clarifies that artificial waxes obtained by the chemical modification of lignite wax or other mineral waxes are classified in Heading 34.04. In the Budget, 2010, the specific sub headings 27122010 covering Chlorinated Paraffin Waxes has been deleted from the tariff. This item is therefore, classifiable under 3404.90 of Central Excise Tariff. [Circular No. 950 /1/2011-CX dated 01.08.2011]

Instructions

The Board has instructed to field formation, not to file appeal with wrong forum, Appeal against Hon’ble CESTAT order w.r.t. dispute on

October - 2011

5

be US$ 400 per Metric Ton F.O.B. [Notification No 68 (RE – 2010)/2009-2014 Dt. 24th August, 2011]

l An exporter can now obtain more than one RC for export of cotton during current cotton year 2010-11 (up to 30th September 2011). [Notification No. 67 (RE-2010)/2009-2014

thDt. 18 August, 2011[

l Minimum Export Price (MEP) of Bangalore Rose Onions and Krishnapuram onions will be US$ 400 per Metric Ton F.O.B. It was US$ 350 per Metric Ton as notified on 16.05.2011. Minimum Export Price (MEP) of onions other than Bangalore Rose Onions and Krishnapuram onions will be US$ 275 per Metric Ton F.O.B. It was US$ 230 per Metric Ton as notified on 15.07.2011. [Notification No 66 (RE – 2010)/ 2009-2014 Dt.: 12th August, 2011]

l Now the import of items under the Exim Codes 6802 10 00, 6802 21 10, 6802 21 20, 6802 21 90, 6802 91 00 and 6802 92 00 of Chapter 68 of ITC(HS) Classifications of Export and Import Items is permitted freely if CIF value is US$ 60 and above per square meter instead of the earlier value of US$ 50 . [Notification No. 65 (RE-2010)/2009-2014 Dt. 4th August, 2011]

l Import policy of rough marble blocks for the year 2011-12 has increased the import quota from 3 lakh MT to 5 lakh MT with a floor price of US$ 325 per Metric Tonne (MT) [Notification No. 64 (RE-2010)/2009-2014 Dt. 4th August, 2011]

l Exporters intending to export cotton [ITC (HS) Codes 5201 and 5203] will apply to the Regional Authority (RA) for grant of Registration Certificate (RC) Subject to Certain conditions:

v Export must be completed within 30 days from the date of issuance of the RC.

v Holders of the RC would require to send two reports to the RA from whom the RC was obtained a) First report immediately on obtaining the Let Export Order (LEO) 2) A Second Consolidatedreport within 35 days of the issue of RC in detail

v Holders of any valid RC that was obtained before 1st August 2011, has the option of getting the RC revalidated or applying afresh under this new dispensation. Thus any RC obtained before 1st August would lose its validity unless revalidated by the RA.

[Notification No. 63 (RE-2010)/2009-2014 thDt. 4 August 2011]

l The cap on export of cotton [ITC (HS) Code 5201 & 5203] has been removed. However,

department accepted number Judgment and applicability will be w.e.f. 18.04.2006. [F. No. 276/8/2009-CX8A dated 26.09.2011]

FOREIGN TRADE POLICY

Notification

l The prohibition on export of onions is withdrawn and export of all varieties of onions is now allowed. [Notification No 75 (RE – 2010)/2009-2014 New Delhi, Dt. : 20th September, 2011]

l Export of cotton [ITC(HS) Codes 5201 & 5203] will continue to be free subject to registration of contracts with DGFT. Performance guarantee (as was given in Notification No. 63 of 04.08.2011) will no longer be required. This will come into effect from 01.10.2011.[Notification No. 74 (RE-2010)/2009-14 New Delhi, Dt. 12th September, 2011].

l The export of all varieties of onions is prohibited with immediate effect till further orders. But, transitional arrangements under para 1.5 of Foreign Trade Policy shall be allowed. [Notification No 73 (RE – 2010)/2009-2014 New Delhi, Dt. 9th September, 2011]

l Export of wheat has been made free. Exports shall be only through Custom EDI ports. [Notification No. 72 (RE-2010)/2009-2014 New Delhi, Dt. 9th September, 2011]

l All varieties of non-Basmati rice have been made free for export out of privately held stocks. Export shall be only through Custom EDI ports. [Notification No 71 (RE – 2010)/2009-2014, New Delhi, Dt. 9th September, 2011.]

l Minimum Export Price (MEP) of all varieties of onions including Bangalore Rose Onions and Krishnapuram Onions will be US$ 475 per Metric Ton F.O.B. It was US$ 300 per Metric Ton for general category onion as notified on 24.08.2011 and US$ 400 per MT F.O.B. for Bangalore Rose Onions and Krishnapuram onions as notified on 12.08.2011. [Notification No 70 (RE – 2010)/2009-2014 New Delhi, Dt. 7th September, 2011.]

l The annual quota for import of marble from Bhutan will now be 5,882 MTs. Previously it was 1847 Mts. [NOTIFICATION No. 69 (RE-2010)/ 2009-14 Dt. 1st September, 2011]

l Minimum Export Price (MEP) of onions other than Bangalore Rose Onions and Krishnapuram onions will be US$ 300 per Metric Ton F.O.B. It was US$ 275 per Metric Ton as notified on 12.08.2011. There is no change in Minimum Export Price (MEP) of Bangalore Rose Onions and Krishnapuram onions and it will continue to

October - 2011

6

No. And e-mail:Tel:0891-2749334, Fax : 0891-2755424, e-mail: [email protected] There is no change in other entries, as they exist at present.

Similarly address of some of the inspection & certification agencies has been changed [Public Notice No. 75/2009-2014 (RE-2010) Dt.30th August, 2011.]

l Earlier only one item at Sl No. 1 in SION C-1579 under Engineering Product Group was allowed for import. Now one more input i.e. Billets of Iron/ Low Carbon Steel for Remelting has been added at Sl No. 2 .There is no change either in description or in the quantity of export item. [Public Notice No. 74 /(RE-2010)2009-2014 Dt.30th August, 2011]

l There has been advancement in the technology i n t h e f i e l d o f m a n u f a c t u r e o f ‘Briefcases/Suitcases/Beauty cases’. Due to advancement in the technology, the Poly Carbonate (PC) is being used in place of ABS/other polymers, to provide higher impact strength. These amendments enable import of required raw materials for exports of ‘Briefcases/Suitcases/Beauty cases’ made up of Poly Carbonate and therefore there is addition of Import item Poly carbonate Moulding powder/Grannules in SION No. H-3 of Plastic Product Group [PUBLIC NOTICE NO. 73/(RE-

rd2010)/2009-2014 Dt. 23 August. 2011].

l Minimum Export Price (MEP) of Sona Masuri, Ponni Samba and Matta varieties of rice is reduced to USD 600 per MT. It was USD 850 per MT as notified on 31.03.2011. [Public Notice No. 72 (RE-2010)/2009-2014, Dt.12th August, 2011]

l SION A-3331 for the export product Ethambutol HCl BP/USP in the Chemicals And Allied Product Group (Product Code:A) deleted. SION for g Ethambutal HCL are available at Sl.No. A-225. [PUBLIC NOTICE NO. 71(RE-2010)2009-2014, Dt. 12th August,2011]

l Over the period, in respect of certain import items pertaining to SION A-2462 and A-2951 under Chemical & Allied Products Group, Improvement in consumption has been observed. Accordingly, quantity allowed for such items has been reduced.

l EIC would also be the authorized agency to issue Certificate of Origin under India-Japan Comprehensive Economic Partnership Agreement with immediate effect. [Public

thNotice No. 70/2009-2014 (RE-2010) Dt. 12 August, 2011]

condition regarding registration of contracts with DGFT would continue to apply. A new procedure of registration is being separately notified for export of Cotton [ITC (HS) Code 5201 & 5203]. In respect of cotton waste including yarn waste and garneted stock [ITC (HS) Code 5202] there is no change even in the procedure to obtain registration [Notification No. 62 (RE-2010)/

nd2009-2014 ,Dt. 2 August 2011]

Public Notices

l Earlier ‘Handloom’ was not included in the expression “Handmade” in the ‘Note’ in Table-2, Sr. No.11 of Appendix 37D. This has been rectified. [Public Notice No. 77 (RE-2010)/ 2009-14 New Delhi, Dt. 05 September, 2011].

l The unit of measurement of Sl No. 4 ( i.e. epoxide resin ) of import list of SION B-149 under electronics product group has been corrected to read as Lbs instead of Kft as Lbs is the standard unit of weight. There is no other change. [Public Notice No. 76 / (RE-2010) 2009-2014 Dt. the 2nd September, 2011].

l Address & Contact Numbers has been changed of Registered Office & Branch Offices of Export Promotion Council for EOU & SEZ unit:

Sl.No. Name of EPC Revised Entries

11 Export Promotion Change of Address of Registered Office/

Council for EOUs Head Office8G, 8th Floor, Hansalaya Bldg.,

& SEZ Units 15 Barakhamba Road, New Delhi-110001

Tel : 23329766-69, Fax No.011-23329770,

e-mail:[email protected],

[email protected], [email protected]

Following changes are incorporated in

the Regional Offices:

i. Chennai – Change in e-mail address New e-mail: [email protected] in place of [email protected]

ii. Cochin- Additional e-mail e-mail: [email protected] iii. Kandla (Gujrat) - Minor changes Premises No. 13-A is added to the postal address and STD Code is changed to 02836.

iv. Mumbai- Change of Address SEEPZ-Special Economic Zone, Office no. 3, 3rd Floor, Business Facilitation Centre, SEEPZ- SEZ Andheri (East), Mumbai-96. Tel: 022-28291343, e-mail: [email protected]

v. Noida (U.P.)-New Phone No. and e-mail address:Tel:0120-2463110; e-mail:[email protected], [email protected]

vi. Visakhapatnam-Change in Phone

October - 2011

7

l In case any unit having only trading turnover has mistakenly applied for import quota by e mail , they should immediately send an e mail to [email protected] with the subject header: “ Withdrawal of application for import of marble”. [Policy Circular No. 37 (RE-2010)/ 2009-2014 Dt. 8th August, 2011].

l Now it has been decided to add the following one new location to 82 existing locations for on-l ine t ransmiss ion o f DES (Advance Authorization), EPCG and DEPB Authorization. i.e. Air Cargo Complex, Cochin.

With effect from 8th August, 2011 It shall be mandatory that DEPB application in respect of shipping bills issued on or after 8.8. 2011 from this port has to be filed in EDI mode. And all authorizations for DES (Advance authorization), EPCG, and DEPB in respect of this port issued on or after 8.8. 2011 by Regional Authorities would be communicated to Customs on-line. [Policy Circular No. 36 (RE-2010)/2009-14 Dt. 5th August, ,2011].

l Representations have been received seeking a clarification on the applicability of condition of shelf life of 60% stipulated under Para 13 of Chapter 1A (General notes regarding Import Policy) of ITC(HS) in case of re-import of edible/food products

The matter has been examined and it has been decided that the condition of 60% shelf life stipulated under para 13 of Chapter 1A (General notes regarding Import Policy) of ITC (HS) is not applicable to re-import for export purpose under para 2.38 of Foreign Trade policy. [Policy Circular No.35 (RE-2010)/2009-2014 Dt. 4th August, 2011].

Most important DEPB scheme is withdrawn stw.e.f. 01 October 2011 and shipping bill for

which Let Export order is granted as on 30.09.2011 will only be eligible for DEPB scheme

MVAT

Notifications / Circular

l Periodicity of returns to be filed every year in respect of each dealer will be decided by the commissioner of sales tax to promote effective compliance and to ensure compatibility with the automated system, which will be displayed on the website of sales Tax Department. [Vide Notification No. VAT 1511 / CR 84 / Taxation -1

thdated 13 September, 2011]

l Benefit of Administrative relief beyond 5 years to dealers remained unregistered can now be

l ICD Merripalem, Guntur District, (AP) is included under para 4.19 of HBP v.1 for availing export promotion benefits. [Public Notice No.69

th(RE-2010)/2009-2014 Dt. 4 August, 2011.]

l DEPB benefit on export of “Cotton” was withdrawn vide Public Notice No. 45 (RE 2010)/2009-14 dated the 31st March, 2011. Exports made on or after 01.10.2010 will now be entitled for DEPB benefit under DEPB entry Sl. No. 22D of the Product Group ‘Miscellaneous’. [PUBLIC NOTICE NO. 68 /2009-2014 (RE 2010) Dt. 4th August, 2011].

l DEPB benefit on export of “Cotton yarn including Melange yarn” was withdrawn vide Public Notice No. 57/2009-14 dated the 21st April, 2010. Now, Export of ‘Cotton yarn including Melange yarn’ appearing at DEPB entry Sl. No. 78 of the Product Group “Textiles”will be entitled for DEPB benefit on exports made on or after 1.4.2011 [PUBLIC NOTICE NO.67 /2009-2014(RE 2010) Dt. 4th August, 2011].

l Quantity permitted for import of Skimmed and Whole Milk Powder under Tariff Rate Quota Scheme is increased from 30,000 MTs to 50,000 MTs, with immediate effect. [PUBLIC NOTICE NO.66 (RE-2010)/2009-2014 Dt. 4th August, 2011]

Circulars

l Regarding Notification No 64 dated 4th August 2011 for import of rough marble blocks for the year 2011-12., It is clarified that only manufacturing turnover of the units in respect of processed marble slabs/tiles will be considered for grant of import quota of marble and no trading turnover will be considered.

l One new location ( i.e. ICD Karur ) has been added to 83 existing locations for on-line transmission of DES (Advance Authorization), EPCG and DEPB Authorization:

DEPB application in respect of shipping bills issued on or after 12.09.2011 from this port has to be filed in EDI mode.

All authorizations for DES (Advance authorization), EPCG, and DEPB in respect of this port issued on or after 12.09.2011 by Regional Authorities would be communicated to Customs on-line. [Policy Circular No. 40 (RE-2010)/2009-14 Dated the, 9th September, 2011]

l The consolidated guidelines on import of precious metal by the nominated agencies and the system of monitoring are issued. [Policy Circular No. 39 (RE-2010)/2009-14 Dt.19th August, 2011].

October - 2011

8

upto 31-12-2012, which were previously not allowed beyond 2 years from the end of Financial years in which tax was deductible at source. [Vide CIrcular No. 6/2011 dated 24/08/2011]

l Detail guideline has been provided w.r.t. TDS on income from salary during the financial year 2011-12. [Circular No. 5/2011, dated 16-8-2011]

COMPANY LAW :

Notifications

l Some modification is made in Form 23AC (for filling Balance Sheet and other documents with the registrar) and Form 23ACA(for filing P&L account and other documents with registrar) [Notification dated 11.08.2011]

Circulars

l Company Law Settlement Scheme, 2011: An opportunity to the defaulting companies to enable them to make their default goods by filing such belated documents and to become regular compliant in future, the scheme is introduced for condoning the delay infilling documents with the Registrar to avoid prosecution & penalty. This scheme shall come into force on 12.08.2011 up to 31.10.2011. [General Circular No. 59 / 2011 dated 05.08.2011]

l The verification and certification of the XBRL documents of financial statement on the e-forms would continue to be done by Authorized Signatory of the Company as well as professional like Chartered Accountant or Company Secretary or Cost Accountant in whole time practice. [General Circular No. 57 / 2011 dated 28.07.2011]

l Simplified procedure likely to be implemented w.e.f. 24.09.2011 for obtaining online approval of Central Government under section 297 of the Companies Act, 1956 where Board’s sanction to be required for certain contracts in which particular Directors are interested. [General Circular No. 52 / 2011 dated 25.07.2011]

l The simplified procedures to be followed by the companies and Registrar of Companies shall be given in the modified e-forms and instruction kit thereto shortly, for rectification of register of charges under section 141 of the Companies Act, 1956.[General Circular No. 51 / 2011 dated 24.07.2011]

given if the claimant dealers proves that the delay was not due to negligence or disregard of the provisions of law but due to bonafide belief that he was not required to obtain the registration. [Circular No. 13T of 2011 dated 30/08/2011].

INCOME TAX

Notifications

l Any amount paid to Mangalore University, Mangalore for research purposes will make the payee entitled to deduction of an amount equal to one and one fourth times of the amount paid u/s 35 (iii). [Vide Notification No. 51/2011 dated 14th September, 2011]

l For deduction u/s 80CCF, Long term Infrastructure Bonds can be issued by IDFC, IFCI, LIC, IIFC, and NBFC’s classified as Infrastructure Finance company by RBI. It should be named as “The Long Term Infrastructure Bonds” and furnishing PAN number to the issuer is mandatory for the subscribers. The minimum tenure of the bond should be 10 years, with minimum lock-in period of 5 years. [Vide Notification No. 50/2011

thdated 9 September, 2011]

l The agreement between India-Taipei Association in Taipei and Taipei Economic and Cultural Center in New Delhi for the avoidance of double taxation and the prevention of fiscal evasion with respect to taxes on income is given

steffect from 1 April, 2012. [Notification No. nd48/2011 dated 2 September, 2011]

l The second protocol for amendment in agreement for avoidance of double taxation and prevention of fiscal evasion between Government of Republic of India and Singapore is given effect to for taxable periods from financial year 2008-09 and subsequent financial

styears. [Notification No. 47/2011 dated 1 September, 2011]

Circulars

l Refund of excess tax deducted at source u/s 195 from the payment to be made to the nonresident shall also be available in the case where tax have been deducted at a higher rate relying upon the provisions of relevant DTAA, while the rate under the Income Tax Act is lower. [Vide CIrcular No. 7/2011 dated 27/09/2011]

l Refund Claims for the TDS paid by the deductor in excess of the amount deducted or deductible pertaining to the period upto March 31, 2009 may be now submitted to the assessing officer

October - 2011

9

DEPB out,

Drawback Enhanced …

The end of DEPB scheme has now really been declared without any extension. Mindset of the exporter was already prepared since the scheme was extended at least more than three times.

Task force for revamping/ reviewing EOU scheme have already submitted their report and Ministry of Commerce & Industry has released the same. Exporters are eagerly waiting for early amendment in Foreign Trade Policy which is due in the month of August 2011 itself. It was thought that the report submitted by the Task Force for revamping/ reviewing of EOU scheme will find the place in the new Foreign Trade Policy.

Meanwhile, since DEPB scheme was not to be extended, Department of Revenue, Ministry of Finance have really tried to give justice to enhance Drawback Schedule which needs to be appreciated.

The following factors has been declaring “All Industry Rate of Duty Drawback for the year 2011-12 which were notified vide Notification No. 68/2011 dated

st22.09.2011 made effective from 1 October 2011.

A. All items covered under DEPB list has been aligned with 4 digit level and corresponding serial number has been given which is available at

B. Drawback Rates has been determined on the basis of certain broad parameters like prevailing price of inputs, Standard Input –output Norms(SION), share of imports in the consumption of inputs, FOB value of export goods and present rate of applicable duties.

C. Incidence of duty on Furnace Oil / HSD have been factored in the Drawback rates.

D. Incidence of service tax paid on taxable services which are used as input services in the manufacturing / processing of export goods have also been factored in the Drawback rates.

There is a major shift from earlier Drawback schedule, earlier drawback restricted in some of the items based on value cap on FOB value of export, now Drawback is also made restrictive as Drawback amount per unit of measurement.

Drawback schedule will have two rates :

i. When Cenvat Benefit has not been availed – These rates include the element of Customs

www.cbec.gov.in

duty on imported Inputs, Excise Duty on indigenous inputs and Service Tax on input services used in manufacturing and processing of export goods. However it doesn’t include service tax on services mentioned in Notification No. 17/2009 ST dated 07.07.2009, therefore exporter can avail the drawback as well as entitled for refund of service tax of the service mentioned in Notification No. 17/2009 ST dated 07.07.2009.

ii. When Cenvat benefit is availed – These rates includes the element of Basic Customs Duty & Education Cess of Customs Duty. However it doesn’t include service tax on services mentioned in Notification No. 17/2009 ST dated 07.07.2009, therefore exporter can avail the drawback as well as entitled for refund of service tax of the service mentioned in Notification No. 17/2009 ST dated 07.07.2009.

In view of above, following aspects need to be considered.

i. If Cenvat benefit is availed export can not take place under the claim of rebate under Rule 19 of Central Excise Rules, 2002.

ii. No Drawback claim can be taken on the goods manufactured by EOU or goods manufactured in warehouse under section 65 of Customs Act, 1962,

iii. No Drawback under All Industry Rate can be taken, when export is made for discharge of export obligation under Advance Authorisation / Duty Free Import Authorisation.

iv. No Drawback will be allowed if export of goods are made under the claim of rebate under Rule 18 of Central Excise Rules, 2002.

v. If Drawback Rate under heading “with availing Cenvat benefit” and under the heading “without availing Cenvat benefit” is the same then the Drawback Rate reflect the element of Basic Customs Duty plus Education Cess on customs and therefore exports can be made under the claim of rebate under Rule 18 or 19 of Central Excise Rules, 2002.

While close comparison of the DEPB schedule with new Drawback Rates, it is noticed that there is a reduction of benefit in the range of 1% to 3 % of FOB

— By CMA A. B. Nawal

October - 2011

10

cases domestic supplier can import duty free items or avail duty drawback, which will reduce procurement cost of inputs. Now new duty drawback rates for most of the items have been increase on the background of end of DEPB scheme.

b. Exporters availing Duty Drawback Benefit:- Generally it is the trend to obtain drawback based on rates prescribed under All Industry Drawback Rates rather than doing the cost benefit analysis under Drawback under Brand Rate application in accordance with Rule 6 / 7 of Customs Central Excise & Service Tax Drawback Rules, 1995. Exporter needs to appreciate that there is a mandatory provision now drawback will be disbursed along with interest if drawback claim is given after one month.

c. Re-export of imported goods:- Drawback under section 74 of Customs Act, 1962, and claimed drawback equivalent to 98% of Customs duty paid if goods are re-exported within 6 months or reduced rate as prescribed in notification issued under section 74 of Customs Act, 1962, subject to following procedure as prescribed under the said notification.

d. Export by EOU/EHTP/STP:- All supplies by manufacturer to EOU are entitled for deemed export benefit under para 8.3 of Foreign Trade Policy which are given below:

i. Duty free import under Advance Authorisation

ii. Entitlement of Duty Free Advance Authorisation

iii. Deemed Export Drawback – now the said benefit has been substantially enhanced due to increase in Drawback Rates.

iv. Refund of Terminal Excise Duty/ Cenvat Credit

EOU can avail benefit under i. or ii. And iv. Or iii. And iv. above simultaneously, thereby reduce the procurement cost. Those EOUs which are planning to convert to Domestic Tariff Area unit in absence of Income Tax benefit under section 10 B under Income Tax Act, needs work out cost benefit analysis before taking decision of debonding /exit from EOU scheme.

To conclude the enhancement of Duty Drawback rate on background of end of DEPB scheme will prove bonanza if proper planning is done, needless to say at most care to be taken while preparing export documentation including ARE-1 / ARE-2 where declaration is printed and whatever is not applicable should be strike out after understanding scheme otherwise substantial benefit will be lost due to wrong declaration.

of exports which will directly impact the profitability & competitiveness of expoters

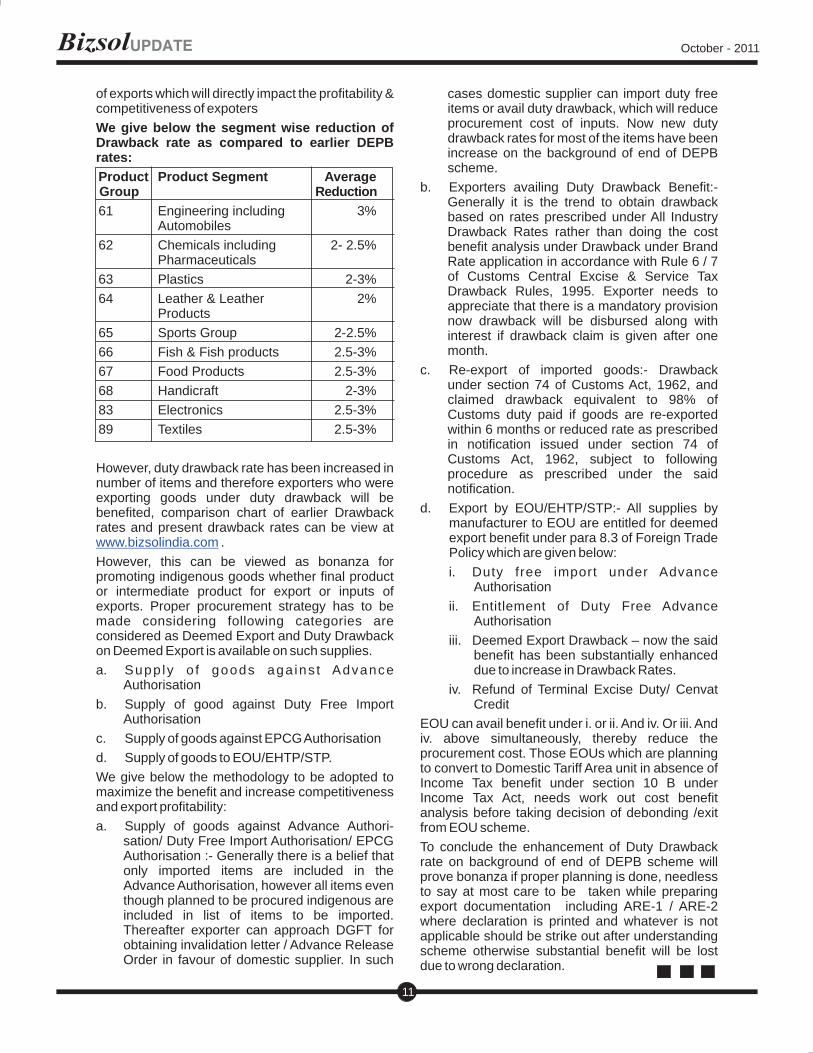

We give below the segment wise reduction of Drawback rate as compared to earlier DEPB rates:

Product Product Segment Average Group Reduction

61 Engineering including 3%Automobiles

62 Chemicals including 2- 2.5%Pharmaceuticals

63 Plastics 2-3%

64 Leather & Leather 2%Products

65 Sports Group 2-2.5%

66 Fish & Fish products 2.5-3%

67 Food Products 2.5-3%

68 Handicraft 2-3%

83 Electronics 2.5-3%

89 Textiles 2.5-3%

However, duty drawback rate has been increased in number of items and therefore exporters who were exporting goods under duty drawback will be benefited, comparison chart of earlier Drawback rates and present drawback rates can be view at

.

However, this can be viewed as bonanza for promoting indigenous goods whether final product or intermediate product for export or inputs of exports. Proper procurement strategy has to be made considering following categories are considered as Deemed Export and Duty Drawback on Deemed Export is available on such supplies.

a. Supp ly o f goods aga ins t Advance Authorisation

b. Supply of good against Duty Free Import Authorisation

c. Supply of goods against EPCG Authorisation

d. Supply of goods to EOU/EHTP/STP.

We give below the methodology to be adopted to maximize the benefit and increase competitiveness and export profitability:

a. Supply of goods against Advance Authori-sation/ Duty Free Import Authorisation/ EPCG Authorisation :- Generally there is a belief that only imported items are included in the Advance Authorisation, however all items even though planned to be procured indigenous are included in list of items to be imported. Thereafter exporter can approach DGFT for obtaining invalidation letter / Advance Release Order in favour of domestic supplier. In such

www.bizsolindia.com

October - 2011

11

CENTRAL EXCISE

Ø Manufacture of dutiable and exempted goods - CENVAT Credit availed on common input was reversed during the same month and further no Cenvat Credit was availed for the subsequent period - Demand under Rule 6(3)(b) of the CENVAT Credit Rules 2004 rightly set aside by the lower authorities - No substantial question of law arises [2011-TIOL-510-HC-P&H-CX]

Ø Reversal of unutilized credit lying in CENVAT A/c after availing exemption benefit under Notification No. 30/04-CE - Whether interest payable on delayed reversal of CENVAT credit - Matter remanded to Tribunal for fresh consideration in light of supreme court decision. [2011-TIOL-509-HC-KAR-CX ]

Ø CESTAT, WZB is burdened with more than 16000 appeals and the hearings are being conducted for the appeals filed in 2003-2004 – since duty involved is less than Rs.1 crore, no ground for listing the matter on priority basis – Revenue application for early hearing rejected. [2011-TIOL-1063-CESTAT-MUM]

Ø In the absence of show-cause notice, the applicant cannot be held to have got a fair opportunity of defending the case - no such opportunity availed by this presence at the hearing - law clearly requires issuance of SCN before conclusion of adjudication proceedings - not open to the department to bypass this legal requirement and find a short-cut method - Revenue appeal dismissed: MUMBAI CESTAT [2011-TIOL-1062-CESTAT-MUM]

Ø Demand of 8% on value of exempted goods confirmed by lower authority for not maintaining separate accounts - Appeal rejected by Appellate Commissioner for non-compliance of order of pre-deposit - Gujarat High Court in Ashima Dyecot case = 2008-TIOL-659-HC-AHM-CX held that reversal of CENVAT Credit amounts to not taking any credit at all - Prima facie case in favour of assessee - Impugned order set aside a n d m a t t e r r e m a n d e d t o A p p e l l a t e Commissioner to decide case on merits without insisting on any pre-deposit [2011-TIOL-807-CESTAT-AHM]

Ø The provisions of section 35F are mandatory. The appellate authority has exercised the discretion and directed the appellant to make deposit of duty demanded but he failed to do so, the appeal is rightly dismissed without entering into the merits of the controversy. [2011-TIOL-571-HC-ALL-CX]

Ø Physician Samples manufactured and cleared to brand owners/buyers on principal to principal basis for a consideration and which are further distributed/delivered by the buyer free of cost to physicians/doctors – Valuation on transaction value is correct [2011-TIOL-1189-CESTAT-MUM]

Ø Manufacturer of excisable goods has to file appeal under the provisions of Central Excise Act, 1944 in respect of CENVAT Credit availed input services – Appeal filed under the provisions of Finance Act, 1994 rightly rejected by the Commissioner (Appeals) – Appeal should have been filed within the time limit prescribed under Section 35 of the Central Excise Act, 1944 – Provisions of Section 85 of the Finance Act, 1994 are not applicable for manufacturers. [2011-TIOL-1250-CESTAT-MAD]

Ø Demand alleging clandestine removal on basis of discrepancy in production figures between balance sheet and RT-12 returns. Revenue’s submission that balance sheet prepared by professional CA on the basis of material furnished by manufacturer to be relied, Hon’ble HC Patna held that no proposition of law that in case of conflict between balance sheet and RT-12 return, balance sheet will prevail, same depends upon facts and circumstances of each case. [2011 (270) ELT 168 (Pat.)]

Ø Excise duty was not paid at the time of clearance to sister unit, with a view that the goods were not excisable to tax but duty was deposited to gain peace and thereafter credit was availed by the assessee. Department denied the Cenvat Credit on the ground that credit is not availed against Invoices issed at the time clearances. Hon’ble HC Kerala held that once the assessee pays duty is entitled to avail credit and utilise the same subsequently, for fault of department the assessee cannot be suffer. [2011 (270) ELT 173 (Ker.)]

October - 2011

12

E.L.T. 351 (Kar.)

Ø Gas purchased and segregated into different grades having different properties on basis of various tests and some treatment and sold at different rates to different customer amounts to manufacture. As the Gas sold is distinct commodity than that of Gas purchased. The concept of marketability needs to be looked into from the point of view of the end consumer who has purchased it and not from the marketability from the point of view of purchaser trading in it. [2011 (271) ELT 321 (SC)]

Ø Rebate claim not be rejected only on the grounds that the original documents are not submitted. Collateral evidences should be accepted as proof of exports and accordingly rebate to be allowed. [2011 (271) ELT 449 (G.O.I)]

Ø Cenvat Credit on inputs like Plates / Bottom of Plates / Roof Plates used for manufacture of Tank used for storage of goods is allowed as the tank is part of the Plant & Machinery. [2011 (271) ELT 360 (Kar. HC)]

Ø After settlement of issue against the assessee by the Larger Bench of Tribunal, demand could not be made against them invoking extended period on the ground of suppression. [2011 (270) ELT 691 (Tri. Ahmd.)]

Ø CESTAT view that the department officer who is Assistant Director (Cost) and member of ICWAI as cost accountant to ascertain value of goods manufactured is not competent based on the reasoning that he not is practice as mentioned in Rectification of Mistake (ROM) application is not justified. [2011 (270) ELT 625 (SC)]

Ø Refund of the accumulated Cenvat Credit of the input service not pertaining to goods exported during the period for which claim is filed, is allowed as no bar is specified in the notification 5/2006 CE (N.T.). Refund of Cenvat Credit of past periods can be granted in subsequent quarters. [2011 (270) E.L.T. 531 (Tri. –Bang.)]

Ø Chiller Plant erected at site is not movable property though the individual parts may be removed and transported. But the plant as a whole can not be transported and hence it can not be called goods and accordingly it can not be liable to excise duty under section 3 of Central Excise Duty. [2011 (270) E.L.T. 541 (Tri. –Mumbai.)]

CUSTOMS

Ø Import of goods without valid IEC number – Revenue’s assertion that such goods are

Ø Condonation of delay in filing appeal by the department can only be admissible when reasonable cause for delay is shown; condonation cannot be admissible when there is lackadaisical approach by the department. [2011(270) E.L.T. 301(Tri-Mumbai)]

Ø After re-registering, Assessee shall be entitled to avail the credit lying in balance at the time of surrender of Central Excise registration, as there is no any provision in law which could deny such benefit to the assessee. Rule 57AG(2) of Central Excise Rules, 1944 nowhere relates to the credit earned from the duty paid on Capital Goods but it essentially restricted to the credit earned from the duty paid on inputs. [2011 (270) E.L.T. 127 (Tri-Del.]

Ø Intention of Legislature behind issuing Notification No. 5/2006-C.E. (N.T.) dated 14.03.2006 was to avoid multiplicity of refund claim. Notification No. 5/2006 C.E. (N.T.) provides that refund claim should not be submitted more than once in any quarter, it does not mean that assessee has to file refund claim quarterly and refund claim could be rejected on that ground. Filing of refund once a year would also avoid multiplicity of claim. [2011 (270) E.L.T. 101 (Tri-Mumbai)]

Ø Assessee held entitled to refund of Cenvat Credit under Rule 5 of Cenvat Credit Rules, 2004, on clearance to 100% EOU, which they were not able to utilize. Matter remanded back to adjudicating authority to verify whether goods cleared to EOU actually exported. [2011 (270) E.L.T. 101 (Tri-Mumbai)].

Ø Manufacturing does not merely means making a new thing, it is sufficient that there is transformation of an article into something else, a different commercial commodity having its distinct character, use and name within the meaning of section 2(f) of Central Excise Act, 1944 read with Note 6 of Section XVI of Central Excise Tariff. Refurbishing also amounted to manufacture.

Assessee has to maintain proper records of receipt /utilization/ inventory on inputs, utilization of credit etc. to claim benefit of credit under Rule 9 of Cenvat Credit Rules, 2004. (2011 (270) E.L.T. 395 (Tri.Del)

Ø As per Notification No. 10/2007 dated 01.03.2007, assessee is entitled to to take credit of duty paid on inputs and are not obliged to reverse it even if Inputs and semi finished goods lying in stock on day prior to when Notification exempting final goods came in to force. The said amendment is prospective in nature. (2011(270)

October - 2011

13

because any such error or mistake can lead to claim and possibility of getting drawback at a rate which actually is not admissible for the item under claim as per law. Wrong and changed declaration/ claims of different heads of schedule of relevant drawback notification cannot be termed as mere “procedural mistakes”. An export made and sale proceeds realized does not give a free hand to any exporter so as to claim any benefit without following the compliance of provisions of relevant Rules/ Regulation. No entry applicable to declared and exported item ‘fishing nets’ in the relevant Drawback Schedule and any after thought/ changed and subsequent claims cannot be legally permitted. BY virtue of Note 10 of Notification No. 49/96-Cus (N.T.) claim is not eligible under All Industry Drawback Rate. (2011 (270)E.L.T. 441 (G.O.I)

Ø If any duty ordered to be refunded under sub- section 2 of Section 27 of the Customs Act, is not refunded within a period of three months from the date of receipt of application, interest shall be payable by the Central Government on the refund claim. The decision of the Apex Court in Sandvik Asia Ltd. [2006 (196) E.L.T. 257 (S.C) distinguished as based on the interpretation of the word ‘any amount’ as appearing in sections 240 and 244 (1A) of the Income Tax Act and in the absence of any specific provision on grant of interest on the belated refund of the interest component it applied the general principles. Therefore, interest shall be available on duty and not on interest. (2011 (270) E.L.T. 314 (Mad.))

Ø Conversion of Shipping Bills are allowed from ‘Zero duty EPCG Scheme’ to ‘Zero duty EPCG and drawback scheme’, there is no reason or provisions to prohibit such availment of the benefit by the assessee. (2011 (270)E.L.T. 426 (Tri- Bang.)

Ø Suspension of CHA license upheld on the ground of manipulation of import documents for evasion of duties. Whether Manipulation carried out by Import or CHA is irrelevant. As the CHA had full knowledge of manipulation and was in possession of original and manipulated documents immediate suspension of the license is warranted. [2011 (271) ELT 321 (Tri-Bangalore)]

Ø Lower price declared in Bill of entry inadvertently based on another invoice of supplier. However correct amount reflected in EPCG licence, Letter of Credit, Bank Guarantee and Bond. Importer was not given opportunity to seek amendment of Bill of Entry. It was inadvertent mistake for which EPCG licence can not be denied. Penalty or fine

‘prohibited goods’ liable for confiscation under s. 111(d) and attract penalty under s. 112 of Customs Act, 1962 – Confiscation of goods and levy of penalty without issue of SCN contravenes provisions of s. 124 ibid – No infirmity in impugned order setting aside confiscation and penalty - Revenue appeal rejected [2011-TIOL-1066-CESTAT-BANG ]

Ø Sec. 114A of Customs Act permits benefit of reduction in penalty subject to assessee paying balance amount of duty determined with interest and 25% penalty within 30 days of communication of the order – No infirmity in Tribunal order allowing such benefit by following High Court decision in Akash Fashion Prints (P) Ltd = 2009-TIOL-125-HC-AHM-CX [2011-TIOL-506-HC-AHM-CUS]

Ø Amendment of shipping bills from EPCG Drawback to EPCG Drawback and Advance Licence Scheme cannot be denied on the ground that the same can only be allowed when the benefit of export promotion scheme has been denied by the DGFT since as per Section 149 of the Customs Act, conversion is possible on the documents in existence at the time of export. [2011-TIOL-1245-CESTAT-MAD]

Ø Import of different types of scrap under Notification No. 83/90-Cus and sent for re-cycling to other units in DTA after mutilation - Unit availed benefit of Notification No. 2/95-CE - When appellant could not produce proof of use of scrap in electric arc furnace, central excise duty demand under sec. 11A justified - Since goods were cleared under a notification after execution of bond with the knowledge of department and in respect of a considerable portion of goods, appellants furnished end use certificate, lenient view to be taken for penalty - Duty demand upheld and penalty set aside. [2011-TIOL-808-CESTAT-AHM]

Ø If there is delay in pre-deposit amount in appeal of overvaluation to claim excess drawback and absence of consignees and condonation of pre-deposit made after 4 years (after long period) of dismissal of appeal for non-payment, then routine condonation of such default for long periods can render the stay orders passed by Tr ibunal and Higher Judic ia l forums meaningless hence, leniency to be shown with lot of circumspection in these cases. Assessee be given chance to argure merits of case, Tribunals powers to restore appeal cannot be restricted. [2011 (270) E.L.T. 84 (Tri-Del.)]

Ø One cannot go changing the drawback claim from one serial number and description to another serial number of (Other) description

October - 2011

14

assessing officer in the order, as well as in the statement of objections filed in these proceedings. In fact, the authorities proceeded on that basis and passed the assessment orders. Whether it is treated as a composite contract, which is indivisible, or as an indivisible contract, it is a contract for rendering service. In that view of the matter, the State is not empowered to levy sales takes under the said legislation for the services rendered by the service provider to the subscriber. [2011-TIOL-518-HC-KAR-ST ]

Ø Commission received by appellant from General Motors through Indian Railways in Indian Rupees – Refund of service tax paid cannot be denied on the ground no foreign exchange was received and thereby conditions of Rule 3(2)(b) of Export of Services Rules, 2005 were not fulfilled: DELHI CESTAT [2011-TIOL-1060-CESTAT-DEL]

Ø Electricity produced in wind mill situated away from the factory transferred to Maharashtra State Electricity Board Power Grid which in turn supplies equivalent quantum to appellant’s factory – Services used for such wind mills are Input Services for manufacturer – Cenvat Credit available: CESTAT [2011-TIOL-1059-CESTAT-MUM]

Ø CESTAT was correct in holding that the respondent is entitled to avail the CENVAT credit on the services provided by Overseas Commission Agents (provided in relation to canvassing and procuring of orders) as input services. [AIT-2011-379-HC]

Ø Clear ing and Forward ing Serv ice - Reimbursement of Expenses - Penalty - Reimbursed expenditure is to be included in taxable value. However, due to the confusion prevailing at the relevant period, penalty stands waived [2011-TIOL-1114-CESTAT-DEL]

Ø Service Tax- Renting of Immovable Property – Constitutional validity upheld : Renting of any property ipso facto would not amount to service for the purpose of service charge. Petition Dismissed : GUJARAT HIGH COURT [2011-TIOL-535-HC-AHM-ST]

Ø Assessee paid tax without abatement as per Circular of DGST - Later Board clarified that assessee is eligible for abatement - Refund with interest to be granted: confusion was created by the redundant circular dated 30.3.2005, which was rectified by the circular dated 27.7.2005. In such a situation, coupled with the bona fides clearly attributable to the assessee, the benefit of the circular dated 27.7.2005 would be

can not be imposed. [2011 (270) E.L.T. 547 (Tri. –Mumbai) ]

Ø Full Bench of SC Ruling since all offences under the Central Excise Act, 1944 and the Customs Act, 1962, are non-cognizable, are such offences bailable?

In view of the provisions of Sections 9 and 9A read with Section 20 of the 1944 Act, offences under the Central Excise Act, 1944, besides being non-cognizable, are also bailable, though not on the logic that all non-cognizable offences are bailable, but in view of the aforesaid provisions of the 1944 Act, which indicate that offences under the said Act are bailable in nature, the offences under the Central Excise Act, 1944, are bailable as in the case of offences under the Central Excise Act, 1944, it is held that offences under Section 135 of the Customs Act, 1962, are bailable and if the person arrested offers bail, he shall be released on bail in accordance with the provisions of sub-Section (3) of Section 104 of the Customs Act, 1962, if not wanted in connection with any other offence-AIT-2011-418-SC

SERVICE TAX

Ø Rule 4(7) of the CENVAT Credit Rules, 2004 - Credit availed before making payment - The gap is only of five days between the date of taking credit and payment of service tax - The lapse is only of technical nature, it is not correct to deny the credit. [2011-TIOL-1091-CESTAT-DEL]

Ø VAT/Service Tax - Artificially Created Light Energy – ACLE, not goods: From the judgments of the Apex Court, it is clear that the essential test to be satisfied before an article is said to be ‘goods’ is the test of marketability. Yet another characteristic, which is recognised, is that the goods should be capable of being delivered- in the case of electricity, electricity is delivered to the customer at his residence, office or industry. ACLE is not seen by the subscriber/consumer. It never comes to the market for it to be bought or sold. It is unknown in the market. It is not capable of abstraction, consumption, delivery by subscriber/customer. Therefore, it does not possess the characteristic of “goods” as understood in law and there is no sale of such goods involved in a telecommunication service.

Covered under Service Tax and not VAT - To levy tax on the same aspect under both the legislation is impermissible: Therefore, it is clear from the recitals in the written contract that it is a service contract, which in fact is admitted by the

October - 2011

15

goods or inputs.

Rent-a-cab service for transport of inputs is activity related to business of assessee thus entitled for cenvat credit.

Mobile phones used by officials for company work is input service on which assessee is allowed to take cenvat credit.

Taking of cenvat credit before payment is made is technical error for which asseseee could not be denied cenvat credit. [2011(270) E.L.T. 225(Tri.-Del.)]

Ø Group Medical Policy and Group Insurance Health Policy is an obligation cast on manufacturer by statue that employer has to obey, such activity is relating to business and is eligible for input tax credit. [2011(270)E.L.T. 156(Kar)]

Ø There is no requirement for co-relation between the Inputs service used and the goods exported for the purpose of granting refund under Rule 5 of Cenvat Credit Rules, 2004. [2011 (271) ELT 436 (Tri-Bang)]

Ø The assets and liabilities of the Subsidiary company (IBP) is taken over by Holding company (IOCL) with retrospective effect. Refund of the service tax paid by the subsidiary company to the holding company prior to amalgamation allowed. [2011 (23) S.T.R. 625 (Tri. –Chennai.)]

Ø The refund of the service tax under notification 41/2007 ST, paid for bringing the empty container for stuffing the goods for export is allowed. [2011 (23) S.T.R. 478 (Tri. – Ahmd.)]

Ø Abatement of 75% of taxable service is available to Consignor and Consignee even if the declaration that “The Goods Transport Agency has not availed the Cenvat Credit of the inputs and Capital Goods used for the provision of such service” is not endorsed on the consignment note provided the consignor or consignee obtains a certificate from the “The Goods Transport Agency” that “WE (GTA) have not availed the Cenvat Credit of the inputs and Capital Goods used for the provision of such service”. [2011 (23) S.T.R. 451 (Pat)]

Ø The sum collected from the sale of SIM Card is includible in the value of Activations Charges to arrive at the value of taxable services provided by telecommunication services to its subscribers as the gross amount received. [2011 (23) S.T.R. 433 (S.C) ]

Ø Cenvat Credit of service tax paid on security

available to the assesse. The substantial questions of law are answered against the Revenue, and in favour of the assessee . It shall be entitled to amount of refund along with interest at the same rate at which the Revenue is entitled to interest for delayed deposit by the assessee , from the dates of deposits of the excess amount till the date of refund: PATNA HIGH COURT [2011-TIOL-569-HC-PATNA-ST]

Ø Non-payment of service tax on Goods Transport Agency service - Penalty - The appellant have proved their bona fide by paying the service tax along with interest on being pointed out by the department - Benefit of Section 80 can be extended to the appellant - Penalties under Section 77 and 78 are set aside [2011-TIOL-810-CESTAT-MAD]

Ø Granting refund under Notification No. 41/2007 ST to exporters on taxable services that he received and used for export does not require verification of registration certificate of the supplier of service

Ø Granting refund to exporters on taxable services that he received and used for export does not require verification of registration certificate of the supplier of service. M/s Indoworth (India) Ltd Vs CCE, Nagpur.

Ø Assessee paid tax without abatement as per Circular of DGST - Later Board clarified that assessee is eligible for abatement - Refund with interest to be granted: confusion was created by the redundant circular dated 30.3.2005, which was rectified by the circular dated 27.7.2005. In such a situation, coupled with the bona fides clearly attributable to the assessee, the benefit of the circular dated 27.7.2005 would be available to the assesse. The substantial questions of law are answered against the Revenue, and in favour of the assessee . It shall be entitled to amount of refund along with interest at the same rate at which the Revenue is entitled to interest for delayed deposit by the assessee , from the dates of deposits of the excess amount till the date of refund: [2011-TIOL-569-HC-PATNA-ST ]

Ø The appellant have proved their bona fide by paying the service tax along with interest on being pointed out by the department - Benefit of Section 80 can be extended to the appellant - Penalties under Section 77 and 78 are set aside. M/s Amman Steel Corporation Vs CCE, Trichy

Ø Inputs used for repairs and maintenance of plant and machinery are allowed as deduction even if they are not covered in the definition of capital

October - 2011

16

display on returnable basis can be allowed without payment of duties as the same is in line with Notification 52/2003-Cus as amended and Foreign Trade Policy. [2011 (271) ELT 425 (Tri-Delhi)]

SEZ

Ø SEZ Unit - Import of different types of scrap under Notification No. 83/90-Cus and sent for re-cycling to other units in DTA after mutilation - Unit availed benefit of Notification No. 2/95-CE - When appellant could not produce proof of use of scrap in electric arc furnace, central excise duty demand under sec. 11A justified - Since goods were cleared under a notification after execution of bond with the knowledge of department and in respect of a considerable portion of goods, appellants furnished end use certificate, lenient view to be taken for penalty - Duty demand upheld and penalty set aside. [2011-TIOL-808-CESTAT-AHM ]

INCOME TAX

Ø Validity of Assessment in case the Search Warrant not in the name of the Assessee: If search as contemplated u/s 132 of the I.T. Act, 1961 is conducted in the premises of a person without any warrant of authorization in the name of the person searched, or on the basis of a warrant of authorization in the name of some other persons, that would be a clear case of non-application of mind of the empowered I.T. authorities and such a search cannot be held to be valid. Therefore a Search conducted u/s 132 in the absence of warrant in the name of the assessee renders it invalid and accordingly as conduct of a valid search is a pre-requisite for issue of notice for making assessment u/s 153A and the assessment under Sec 153A is cannot be said to be valid. [2011-TIOL-527-HC-ORISSA-IT]

Ø Relevant Date for Payment of Tax: Once the authorized agent of the Central Government collects the tax by debiting the bank account of the assessee, the payment of tax to the Central Government would be complete. Delay on the part of the authorized agent to credit that amount to the account of the Central Government, it cannot be said that the payment of tax is not made by the assessee, till the amount of tax is credited to the account of the Central Government. For calculating interest u/s 244A (1)(b) the relevant date is the date of payment of tax and not the date on which the amount of tax

services availed outside the factory are not allowed. [2011 (23) S.T.R. 372 (Chennai)]

Ø Cenvat Credit of the excise duty paid on the Cement and TMT bar used in the construction of warehouse to provide the “Storage and Warehousing Service” is allowed. [2011 (23) S.T.R. 341 (A.P.)]

Ø HC Ruling- Service Tax - service of transportation of employees of a factory to the factory was an ‘input service’ under the ambit of definition of ‘input service’ as given under Rule 2(l) of the Cenvat Credit Rules, 2004 and consequently the credit of service tax paid on such service was allowed to be taken as credit under the said Rules of 2004 - [AIT-2011-420-HC]

Ø HC Ruling-Service Tax-Hindu marriage is not treated or regarded a social function per se. If the dictionary clause is appositely appreciated, there can be no trace of doubt that only when a “pandal or shamiana is used for marriage, it earns the status of “social function” because the service component is involved. It is worth noting, the statute itself postulates that marriage is to be regarded as a social function and full effect has to be given to the same. That apart, the pre-requisite is the use of “pandal or shamiana” and, therefore, the contention raised by the learned counsel that Hindu marriage is not a contract but a sacred institution and hence, no service tax is imposable treating it as a social function has to be repelled. [AIT-2011-419-HC]

EOU

Ø 100% EOU – Manufacture of sodium perborate by procuring indigenous and imported raw materials as well as capital goods duty free – Development Commissioner permitted broad banding and allowed manufacture of hydrogen peroxide – No capital goods procured for production and export of hydrogen peroxide – Demand of duty foregone for not achieving NFE and for non-fulfillment of export obligation – Development Commissioner dropped proposal to levy penalty and granted in principle permission for exiting EOU scheme after failure to achieve NFE and non-fulfillment of export obligation – Prima facie case for full waiver of pre-deposit.

Ø Bank guarantee encashment cannot be deemed to be a voluntary payment of duty, so as to claim immunity from penalty or fine. [2011(270) E.L.T. 280 (Tri.-Mumbai].

Ø Re-Import of finished goods exported by EOU for

October - 2011