Embed Size (px)

Citation preview

3

Why Spin-Off? Spin-Offs are a source of significant market outperformance

for investors. Spin-Offs often result in a higher aggregate value for the

constituent pieces. Studies conducted by a range of researchers, from Penn

State to McKinsey have documented that spin-offs, on average, outperform market indexes.

4

Spin-Offs Outperform S&P 500 (10 YTD)

-100.00%

-50.00%

0.00%

50.00%

100.00%

150.00%

200.00%

250.00%

BNSPIN Index CSD US Equity SPX Index

10Y Total Return 12/29/2006-7/29/2016:Bloomberg Spin Index: 192.36%Guggenheim Spin-Off ETF: 88.20%S&P 500: 88.13%

5

Spin-Offs Outperform S&P 500 (YTD)

-20.00%

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

BNSPIN Index CSD US Equity SPX Index

YTD Total Return 12/31/2015-9/20/2016:Bloomberg Spin Index: 13.35%Guggenheim Spin-Off ETF: 9.73%S&P 500: 6.37%

6

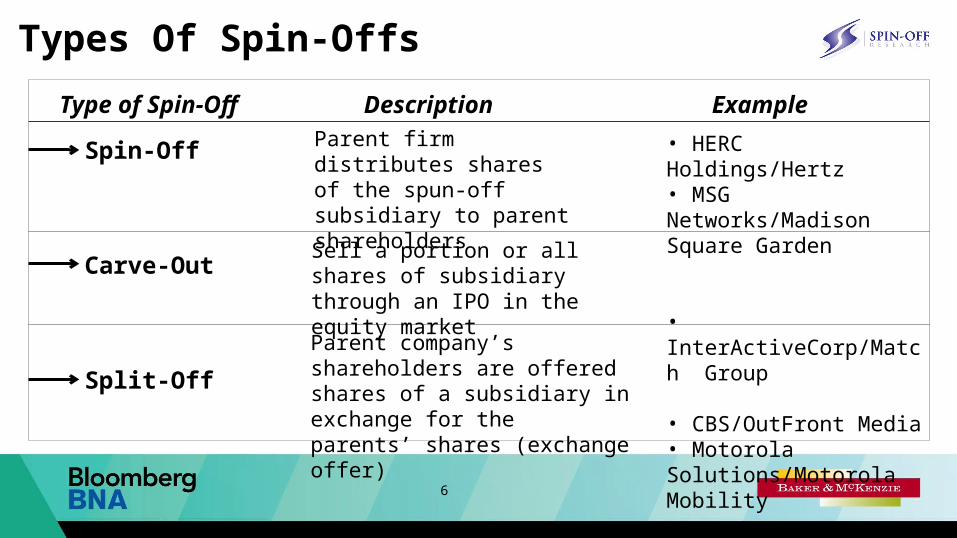

Types Of Spin-OffsType of Spin-Off

Spin-Off

Carve-Out

Split-Off

Description ExampleParent firm distributes shares of the spun-off subsidiary to parent shareholders

• HERC Holdings/Hertz• MSG Networks/Madison Square Garden

• InterActiveCorp/Match Group

• CBS/OutFront Media• Motorola Solutions/Motorola Mobility

Sell a portion or all shares of subsidiary through an IPO in the equity market

Parent company’s shareholders are offered shares of a subsidiary in exchange for the parents’ shares (exchange offer)

7

Spin-Off A parent distributes the stock of a subsidiary in the form of a dividend Following the distribution, the stockholders hold stock of the parent and

the stock of the company that was spun-off Two independent companies exist where before there was only one A spin-off effectively removes the parent from management and control of

the subsidiary Pure spins are tax efficient

8

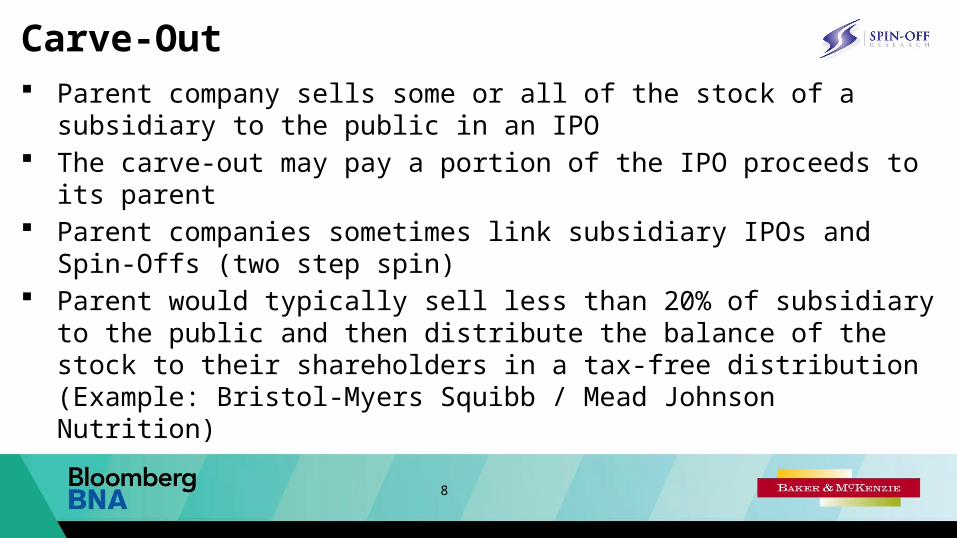

Carve-Out Parent company sells some or all of the stock of a subsidiary to the public

in an IPO The carve-out may pay a portion of the IPO proceeds to its parent Parent companies sometimes link subsidiary IPOs and Spin-Offs (two

step spin) Parent would typically sell less than 20% of subsidiary to the public and

then distribute the balance of the stock to their shareholders in a tax-free distribution (Example: Bristol-Myers Squibb / Mead Johnson Nutrition)

9

Equity Carve-OutsParent sells Equity in the New Firm to the Public (IPO) and creates a New Publicly Traded Entity.

Parent65%Carve-Out in

an IPO10%

Subsidiary25%

Parent65%

Subsidiary35%

• A carve-out brings cash into the firm, whereas a pure spin-off does not• Carve-outs disperse assets and ownership in the assets to non-owners of the original firm• Carve-outs are often an intermediate step before a full spin-off

10

Split-Offs In a split-off, the investor must decide between the new company and the parent. Holders of the parent company stock must choose to continue owning stock in the

parent or, instead, exchange some or all of the parent stock for stock in the spin-off.

The parent offers its existing shareholders stock in the subsidiary in exchange for shares in the parent company.

If the parent distributes 80% of the subsidiary stock, the split is tax-free. What’s more, in an effort to induce enough shareholders to swap stock, investors are offered shares in the subsidiary that are worth more than the shares being returned to the parent company. This offered “premium” explains why split-offs are often oversubscribed.

11

Selected Split-Off Transactions

Parent/Sub DateSize

($mm)

% of Parent Shares

Repurchased

Initial

Prem.Closing

Prem.

Over Sub.

Factor

Sub as % of Parent

Market

AT&T / AWE 5/21/01 $7.8 B 10% 7% 1% .87x 22%

Sara Lee / Coach 4/4/01 $998 M 5% 12.90% 6.90% 2.1x 6%

General Motors / Hughes Electronics 5/19/00 $8.27 B 14% 17.70% 10.10% 3.9x 70%

DuPont / Conoco 8/6/99 $11.7 B 13% 17.90% 3.30% 2.4x 20%

Lockheed Martin / Martin Marietta 10/18/96 $906 M 4% 17.50% 5.20% 5.4x 6%

Eli Lilly / Guidant 9/18/95 $1.55 B 6% 13.10% 8.80% 2.9x 9%

12

Drivers for Spin-Offs Lack of synergy De-conglomeration Focus in core business Legal / regulatory Undervalued assets Monetize value of

subsidiary

De-leverage balance sheet Riskiness of the subsidiary Avoid a takeover Tax avoidance Conflicts of interest

13

Successful Spins Easier for the markets to recognize underlying value Pursue compelling business opportunities Greater freedom to pursue new ventures, streamline production, and pare

overhead Accountability and direct incentives (stock & options) Eliminates competitive disadvantages Greater access to capital Increase corporate focus for the spin-off and parent

14

Shift from Conglomeration to Pure Play Era of conglomerate (1960s - 1980s)

- Firms diversify holdings to “smooth” earnings- Market rewards empire building

Conglomerates fall out of favor- Focus on cost- Difficult to value all businesses in diversified companies- Market discounts conglomerate stocks

Rise of the Pure Play (1990s - Current)- Market rewards firms that concentrate on core business- Competitive landscape pressures management to improve operating efficiency and clarify strategic decision making

15

Number of Completed Spin-Offs by Year19

8519

8619

8719

8819

8919

9019

9119

9219

9319

9419

9519

9619

9719

9819

9920

0020

0120

0220

0320

0420

0520

0620

0720

0820

0920

1020

1120

1220

1320

1420

1520

16

0

10

20

30

40

50

60

70

19

27

21

34

27 27

18

23

33

2831

41

36

44

66 66

3941

21

35

2731

34

29

20 20

27

37 37

60

40 39

2016 Estimated Total

16

2016 Completed Spin-Offs (20 YTD)

Key: SP = Spin-Off CO = Carve-Out SPLIT = Split-Off

Announce Spin-Off TaxParent Symbol Spin-Off Symbol Date Date Exempt Ratio

1 Fiat Chrysler FCAU Ferrari N.V. RACE 10/29/2014 1/3/2016 Y 1:102 W.R. Grace GRA GCP Applied Technologies GCP 2/5/2015 2/3/2016 Y 1:13 Manitowoc MTW Manitowoc Foodservices MFS 1/29/2015 3/4/2016 Y 1:14 Integer Holdings ITGR Nuvectra NVTR 4/30/2015 3/14/2016 Y 1:35 Armstrong World Industries AWI Armstrong Flooring AFI 2/23/2015 4/1/2016 Y 1:26 MGM Resorts MGM MGM Growth Properties MGP 10/29/2015 4/20/2016 CO7 Community Health Systems CYH Quorum Health QHC 8/3/2015 4/29/2016 Y 1:48 Gaming & Leisure Prop GLPI Pinnacle Entertainment PNK 7/21/2015 4/28/2016 N 1:19 WestRock WRK Ingevity NGVT 1/8/2015 5/15/2016 Y 1:6

10 Starwood Hotels & Resorts HOT Vistana/Merger: Interval Leisure Group IILG 2/10/2015 5/12/2016 Y 1:111 Philips PHG Philips Lighting N.V. LIGHT 6/30/2014 5/27/2016 CO12 IDT Corp IDT Zedge ZDGE 8/29/2013 6/1/2016 Y 1:313 Brookfield Asset Management BAM Brookfield Business Partners BBU 10/7/2015 6/20/2016 N 1:5014 HERC Holdings HRI Hertz Rental Car Holding Co HTZ 3/18/2014 6/30/2016 Y 1:515 Danaher DHR Fortive Corporation FTV 5/13/2015 7/2/2016 Y 1:216 Liberty Ventures LVNTA CommerceHub CHUBA/B 11/25/2015 7/22/2016 Y .1/0.2:117 Emergent BioSolutions EBS Aptevo Therapeutics APVO 8/6/2015 8/1/2016 Y 1:218 E.ON SE EONGY Uniper SE UN01 11/30/2014 9/12/2016 Y 1:1019 Noble NE Noble Midstream Partners LP NBLX 10/28/2014 9/15/2016 CO20 Ashland ASH Valvoline VLV 9/22/2015 9/23/2016 CO

17

Q4-2016 Expected Spin-Offs (est. 19)Announce Spin-Off Tax

Parent Symbol Spin-Off Symbol Date Date Exempt Ratio1 Air Products & Chemicals APD Versum Materials "VSM" 9/16/2015 10/1/2016 Y 1:12 Honeywell HON AdvanSix "ASIX" 5/12/2016 10/1/2016 Y 1:253 RR Donnelley RRD Financial Communications Services "LKSD" 8/4/2015 10/1/2016 Y 1:84 RR Donnelley RRD Publishing & Retail Centric Print Services "DFIN" 8/4/2015 10/1/2016 Y 1:85 Johnson Controls JCI Adient "ADNT" 7/24/2015 10/28/2016 N 1:106 Yum! Brands YUM Yum! China 10/20/2015 10/31/2016 Y SP7 CBS Corp. CBS CBS Radio 3/15/2016 Oct-16 CO8 Alcoa (Arconic) AA ("ARNC") Alcoa "AA" 9/28/2015 Oct-16 Y SP9 Liberty Ventures LVNTA Liberty Expedia "LEXEA/B" 11/25/2015 Oct-16 Y SPLIT

10 ConAgra CAG Lamb Weston "LW" 11/18/2015 Fall-16 Y SP15 Cousins Properties CUZ Parkway "PKY" 4/29/2016 Q4-16 Y 1:116 IDT Corp IDT SpinCo 8/27/2015 Q4-16 Y SP17 HCP Inc. HCP Quality Care Properties "QCP" 5/9/2016 Q4-16 N SP18 Overseas Shipholding Group OSG OSG International "OIN" 3/1/2016 Q4-16 N SP11 Hilton Worldwide HLT Hilton Grand Vacations "HGV" 2/26/2016 Dec-16 Y SP12 Hilton Worldwide HLT Hilton Park Hotels & Resorts "PK" 12/16/2015 Dec-16 Y SP13 Xerox XRX Conduent 1/29/2016 Dec-16 Y SP14 Varian Medical Systems VAR Varex Imaging Company "VREX" 10/23/2016 Dec-16 Y SP19 SUPERVALU SVU Save-A-Lot 7/28/2015 Dec-16/Jan-17 N SP

Key: SP = Spin-Off CO = Carve-Out SPLIT = Split-Off

18

Joe Cornell, CFA Spin-Off Advisors, LLCPublishers of Spin-Off Research

spinoffresearch.com/trial

1327 W. Washington Blvd., Suite 4G, Chicago IL, 60607 | [email protected] | 312-939-8900

To get a copy of our research: