Embed Size (px)

Citation preview

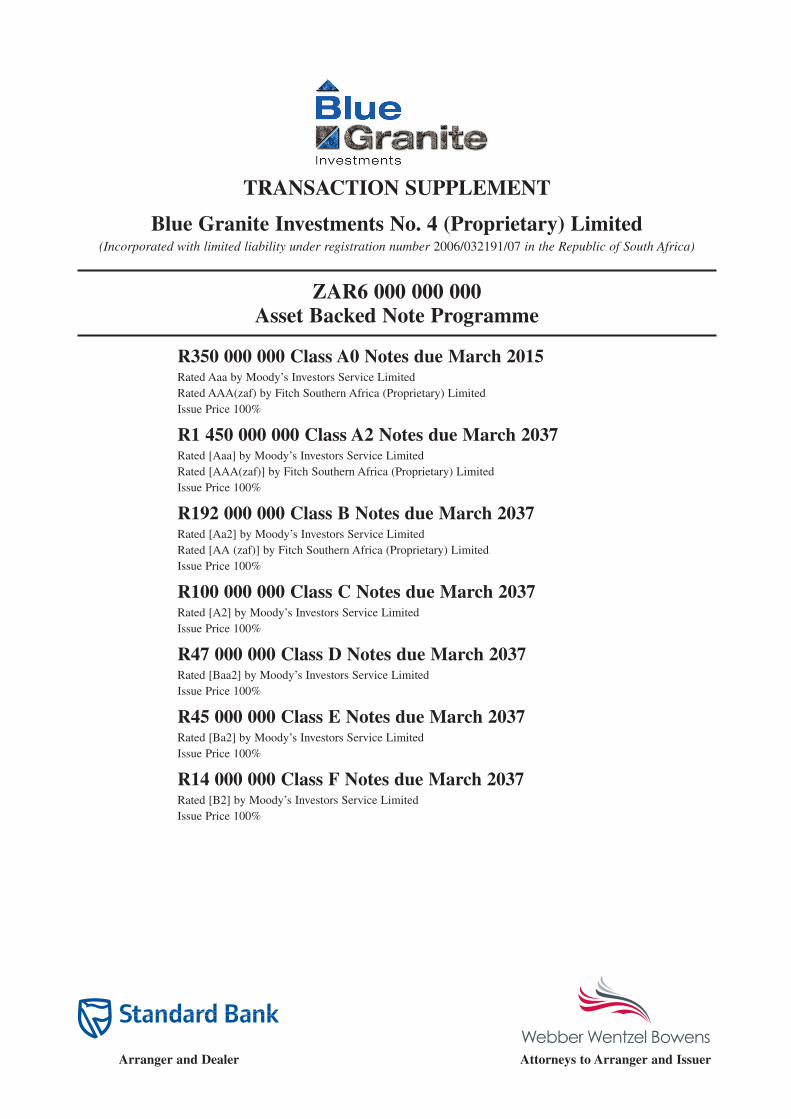

TRANSACTION SUPPLEMENT

Blue Granite Investments No. 4 (Proprietary) Limited(Incorporated with limited liability under registration number 2006/032191/07 in the Republic of South Africa)

ZAR6 000 000 000Asset Backed Note Programme

R350 000 000 Class A0 Notes due March 2015Rated Aaa by Moody’s Investors Service LimitedRated AAA(zaf) by Fitch Southern Africa (Proprietary) LimitedIssue Price 100%

R1 450 000 000 Class A2 Notes due March 2037Rated [Aaa] by Moody’s Investors Service LimitedRated [AAA(zaf)] by Fitch Southern Africa (Proprietary) LimitedIssue Price 100%

R192 000 000 Class B Notes due March 2037Rated [Aa2] by Moody’s Investors Service LimitedRated [AA (zaf)] by Fitch Southern Africa (Proprietary) LimitedIssue Price 100%

R100 000 000 Class C Notes due March 2037Rated [A2] by Moody’s Investors Service LimitedIssue Price 100%

R47 000 000 Class D Notes due March 2037Rated [Baa2] by Moody’s Investors Service LimitedIssue Price 100%

R45 000 000 Class E Notes due March 2037Rated [Ba2] by Moody’s Investors Service LimitedIssue Price 100%

R14 000 000 Class F Notes due March 2037Rated [B2] by Moody’s Investors Service LimitedIssue Price 100%

Arranger and Dealer Attorneys to Arranger and Issuer

This document constitutes the Transaction Supplement, relating to the Issuer described in this Transaction Supplement.

By executing this Transaction Supplement the Issuer binds itself to the terms and conditions of the Master Programmeand, accordingly, this Transaction Supplement must be read in conjunction with the Programme Memorandum issued byBlue Granite Investments No. 1 (Proprietary) Limited dated 28 October 2005. To the extent that there is any conflict orinconsistency between the contents of this Transaction Supplement and the Programme Memorandum, the provisions ofthis Transaction Supplement shall prevail.

In addition to disclosing information about the Issuer and the Issuer Programme, this Transaction Supplement mayspecify other terms and conditions of Notes (which replace, modify or supplement the Terms and Conditions), in whichevent such other terms and conditions shall, to the extent so specified in this Transaction Supplement, or to the extentinconsistent with the Terms and Conditions, replace, modify or supplement the Terms and Conditions.

Any capitalised terms not defined in this Transaction Supplement shall have the meanings ascribed to them in the sectionof the Programme Memorandum headed “Glossary of Definitions”. References in this Transaction Supplement to theTerms and Conditions are to the section of the Programme Memorandum headed “Terms and Conditions of the Notes”.A reference to any Condition in this Transaction Supplement is to that Condition of the Terms and Conditions.

Arranger and Dealer

The Standard Bank of South Africa Limited

The date of this Transaction Supplement is 6 March 2007

1

TABLE OF CONTENTS

Page

GENERAL DESCRIPTION OF THE ISSUER PROGRAMME 3

TRANSACTION PARTIES 5

TRANSACTION DOCUMENTS 6

THE ISSUER 7

THE SECURITY SPV 8

THE ORIGINATOR AND THE ORIGINATOR’S CREDIT OPERATIONS 9

THE HOME LOAN POOL 16

THE SERVICER, THE SERVICING AGREEMENT AND SERVICER UNDERTAKING AGREEMENT 19

THE ADMINISTRATOR AND THE ADMINISTRATION AGREEMENT 20

STRUCTURAL FEATURES 21

PRIORITY OF PAYMENTS 26

THE SALE AGREEMENT 29

SUBSCRIPTION AND SALE 32

TRANSACTION SPECIFIC DEFINITIONS 34

ADDITIONAL/AMENDED TERMS AND CONDITIONS 47

GENERAL INFORMATION 48

CORPORATE INFORMATION 50

Appendix 1: ASSET POOL STRATIFICATION 52

Appendix 2: AUDITORS’ REPORT 58

Appendix 3: ESTIMATED AVERAGE LIVES OF THE NOTES 59

2

3

GENERAL DESCRIPTION OF THE ISSUER PROGRAMME

A general description of the Issuer Programme is set out below. The general description does not purport to be completeand is taken from, and is qualified by, the remainder of this Transaction Supplement and, in relation to any particularTranche of Notes, the Applicable Pricing Supplement.

A brief overview of the Issuer Programme is as follows:

Issuer Programme Steps:

1. SBSA carries on the business of, amongst other things, originating Home Loans against the security of IndemnityBonds registered in SBSA’s favour over the Property by the relevant Borrower.

2. SBSA, as Seller, will sell Participating Assets to a newly created, insolvency remote Issuer on the Initial EffectiveDate. During the Revolving Period, the Issuer may acquire Additional Assets from the Seller on the terms set out inthe Sale Agreement.

3. The Borrower Indemnities and Indemnity Bonds held by SBSA pertaining to Participating Assets sold to the Issuerwill be transferred by SBSA to the Guarantee Entity. The Guarantee Entity will, in respect of each ParticipatingAsset transferred, issue to the Issuer a limited recourse Guarantee Entity Guarantee, guaranteeing the obligations ofthe relevant Borrower to the Issuer.

4. The Issuer will fund the purchase of Participating Assets on the Initial Effective Date using the funds raised throughthe issuance of the Notes on the Initial Issue Date and, if applicable, the funds raised through the Subsequent Issue.The Initial Effective Date will be determined in accordance with the provisions of the Sale Agreement and will bea date no later than 30 days after the Initial Issue Date. The funds raised by the Issuer on the Initial Issue Date willbe invested in Permitted Investments until the Initial Effective Date. The Subsequent Issue will be subject to thewritten consent of the Security SPV and the Rating Agency not advising the Issuer that such Subsequent Issue willcause the downgrading of the Notes in issue or result in the Notes in issue being placed on negative watch. The Issuermay issue further Notes to fund the acquisition of Additional Assets.

Borrower Indemnity and first ranking (and ifapplicable, lower ranking)Indemnity Bond over theBorrower’s Property

Sale ofParticipating

Assets

Limited Recourse

Guarantee

Participating Assets(Payments) Notes Issue

Proceeds

ExcessSpread andServicingFee

SubordinatedLoans

Security Cessionand Indemnity

SBSASecurity

SPV

Borrower

Blue GraniteInvestments No. 4

(Proprietary)Limited

Investors

SBSASubordinated

Lenders

GuaranteeEntity

Assignment

Limited RecourseGuarantee

5. SBSA, as Servicer to the Issuer, will administer, manage and service on behalf of the Issuer the Participating Assetssold and transferred to the Issuer. Pending registration of the transfer of Indemnity Bonds in relation to ParticipatingAssets sold to the Issuer, the Servicer will furthermore provide the Servicer Indemnity Undertaking, in terms ofwhich the Servicer undertakes, on request by the Issuer, to pay over all amounts collected from the Borrower interms of the Borrower Indemnity and the Indemnity Bond. Upon registration of transfer of an Indemnity Bond tothe Guarantee Entity, the rights and obligations of SBSA under the relevant Borrower Indemnity and the IndemnityBond and of the Servicer under the Servicer Indemnity Undertaking in relation to that Borrower Indemnity andIndemnity Bond will be transferred to the Guarantee Entity, and such rights and obligations under the ServicerUndertaking Agreement will be replaced by the Guarantee Entity Guarantee issued by the Guarantee Entity in favourof the Issuer with effect from the Transfer Date.

6. SBSA, as Administrator to the Issuer, will provide financial administration services to the Issuer, includingadministering the Priority of Payments.

7. SBSA, as the Derivative Counterparty, will enter into Derivative Contracts with the Issuer to hedge all of the Issuer’sinterest rate risk exposure arising from any mismatch between the basis of the interest earned on the PerformingAssets and that payable on the Notes.

8. SBSA and any member of the Standard Bank Group, as Subordinated Lenders, will advance Subordinated Loans tothe Issuer to provide part of the initial funding for the Issuer on the Initial Issue Date.

9. On the Initial Issue Date and from time to time thereafter, the Issuer will pay an amount into the Cash Reserve, suchthat the Cash Reserve shall be funded at 2.75% of the greater of the aggregate of the Principal Balances of theParticipating Assets of the Issuer, or the Outstanding Principal Amount of the Notes in issue, from time to time.

10. On the Initial Issue Date and thereafter, the Issuer will pay an amount into the Redraw Reserve, such that the RedrawReserve shall be funded at 2.25% of the greater of the aggregate of the Principal Balances of the Participating Assetsof the Issuer, or the Outstanding Principal Amount of the Notes in issue, from time to time.

11. Additional credit enhancement is provided for the Notes by the Issuer trapping cash in the Arrears Reserve in termsof the Priority of Payments, if certain delinquency levels are triggered.

12. SBSA, as Preference Shareholder, will be entitled to receive dividends in respect of the Preference Shares, subjectto the Priority of Payments.

13. The Security SPV has been incorporated for the purpose of holding and realising security for the benefit of SecuredCreditors, including Noteholders, subject to the Priority of Payments.

14. The Security SPV will furnish a limited recourse Guarantee to the Noteholders and other Secured Creditors. TheIssuer will indemnify the Security SPV in respect of claims made under the Guarantee. As security for suchIndemnity, the Issuer will cede and pledge the assets of the Issuer to the Security SPV.

4

TRANSACTION PARTIES

Programme Wide

Owner Trustee Maitland Trust Limited

Security SPV Owner Trustee Maitland Trust Limited

Arranger SBSA

Administrator SBSA, acting through its Corporate and Investment Banking Division

Servicer SBSA, acting through its Home Loans Division

Transaction Wide

Originator SBSA

Seller SBSA, acting through its Home Loans Division

Issuer Blue Granite Investments No. 4 (Proprietary) Limited, registration number2006/032191/07

Security SPV Blue Granite No. 4 Security SPV (Proprietary) Limited, registration number2006/034129/07

Dealer SBSA

Subordinated Lenders SBSA and any member of the Standard Bank Group

Preference Shareholder SBSA

Calculation Agent SBSA

Transfer Agent Computershare Investor Services 2004 (Proprietary) Limited

Settlement Agent SBSA

Account Bank SBSA

GIC Provider SBSA

Guarantee Entity SB Guarantee Company (Proprietary) Limited, registration number 2006/021576/07

Guarantee Entity Servicer SBSA

Guarantee Entity Administrator SBSA

Derivative Counterparty SBSA

Rating Agencies Fitch and Moody’s

Such parties may be replaced in accordance with the provisions of the Transaction Documents.

5

TRANSACTION DOCUMENTS

Programme Wide

1. Programme Memorandum dated 28 October 2005, incorporating the Terms and Conditions of the Notes

2. Trust deed of the Owner Trust

3. Trust deed of the Security SPV Owner Trust

Transaction Wide

4. Memorandum and articles of association of the Issuer

5. Memorandum and articles of association of the Security SPV

6. Trust Deed of the Guarantee Entity Owner Trust

7. Memorandum and articles of association of the Guarantee Entity

8. This Transaction Supplement dated 6 March 2007

9. Common Terms Agreement dated on or about 5 March 2007

10. Sale Agreement dated on or about 5 March 2007

11. Servicing Agreement dated on or about 5 March 2007

12. Servicer Undertaking Agreement dated on or about 5 March 2007

13. Common Terms Guarantee Agreement dated on or about 5 March 2007

14. Guarantee Entity Servicing Agreement dated on or about 5 March 2007

15. Guarantee Entity Administration Agreement dated 14 November 2006

16. Assignment Agreement dated on or about 5 March 2007

17. Administration Agreement (including appointment of Administrator as Calculation Agent) dated on or about5 March 2007

18. Owner Trust Suretyship dated on or about 5 March 2007

19. Pledge and Cession dated on or about 5 March 2007

20. Security Cession dated on or about 5 March 2007

21. Guarantee dated on or about 5 March 2007

22. Indemnity dated on or about 5 March 2007

23. Bank Agreement dated on or about 5 March 2007

24. Preference Share Subscription Agreement dated on or about 5 March 2007

25. Transfer Agent Agreement dated on or about 5 March 2007

26. Subordinated Loan Agreement (First Loss) dated on or about 5 March 2007

27. Subordinated Loan Agreement (Second Loss) dated on or about 5 March 2007

28. Safe Custody Agreement dated on or about 5 March 2007

29. Derivative Contracts dated on or about 5 March 2007

30. Guaranteed Investment Contract dated on or about 5 March 2007

31. Programme Agreement dated on or about 5 March 2007

32. Guarantee Entity Guarantees in respect of each Participating Asset

33. Note Subscription Agreements from time to time

34. Applicable Pricing Supplements from time to time

6

THE ISSUER

1. INTRODUCTION

The Issuer was incorporated and registered in South Africa on 17 October 2006 under Registration number2006/032191/07 under the Companies Act as a private company with limited liability. The authorised share capitalof the Issuer is ZAR1 001.00 divided into 1000 ordinary par value shares of ZAR1.00 each and 100 cumulativeredeemable preference shares of ZAR0.01 each. The issued ordinary share capital of the Issuer comprises onehundred and twenty ordinary shares with a par value of ZAR1.00, held by the Owner Trust and the issued preferenceshare capital of the Issuer comprises of one Preference Share with a par value of ZAR0.01 held by the PreferenceShareholder. The Issuer has no subsidiaries.

2. DIRECTORS

The Directors of the Issuer are Francois Johan Schindehutte, Paul Werner Behrens and Edwin Marcus Letty, onlyone of whom is nominated by SBSA. The board of directors of the Issuer is accordingly independent of SBSA ascontemplated in paragraph 4(2)(m) of the Securitisation Regulations.

3. REGISTERED OFFICE

The registered office of the Issuer is situated at Standard Bank Centre, 9th Floor, Reception 3, 5 Simmonds Street,Johannesburg, 2001.

4. AUDITOR

The current auditors of the Issuer are KPMG Inc. and PricewaterhouseCoopers Inc.

5. ACTIVITIES

The activities of the Issuer will be restricted by the Transaction Documents and will be limited to the issue of Notes,the purchase of Participating Assets meeting the Eligibility Criteria, the exercise of related rights and powers andother activities referred to in the Transaction Documents or reasonably incidental to such activities.

As at the date of this Transaction Supplement, save as disclosed herein, the Issuer has no loan capital outstandingor created but unissued, no term loans outstanding and no other borrowings or indebtedness in the nature ofborrowing nor any contingent liabilities or guarantees.

7

THE SECURITY SPV

1. INTRODUCTION

The Security SPV was incorporated and registered in South Africa on 31 October 2006, under Registration number2006/034129/07 under the Companies Act as a private company with limited liability. The authorised share capitalof the Security SPV is ZAR1 000.00 divided into 1000 ordinary par value shares of ZAR1.00 each. The issued sharecapital of the Security SPV comprises one hundred and twenty ordinary shares with a par value of ZAR1.00, heldby the Security SPV Owner Trust. The Security SPV has no subsidiaries.

2. DIRECTORS

The Directors of the Security SPV are Paul Werner Behrens and Edwin Marcus Letty.

3. REGISTERED OFFICE

The registered office of the Security SPV is situated at c/o Maitland Trust Limited, 1st Floor, 32 Fricker Road, IllovoBoulevard, Johannesburg, 2196.

4. AUDITOR

The current auditors of the Security SPV are KPMG Inc. and PricewaterhouseCoopers Inc.

5. ACTIVITIES

The activities of the Security SPV are described in the section of the Programme Memorandum headed “Security”and restricted in terms of its memorandum and articles of association.

8

THE ORIGINATOR AND THE ORIGINATOR’S CREDIT OPERATIONS

This section should be read in conjunction with, and is qualified in its entirety by, the detailed information containedelsewhere in this Transaction Supplement and the Programme Memorandum and in particular, the section of theProgramme Memorandum headed “The Originator and the Originator’s Credit Operations”.

GROUP FINANCIAL HIGHLIGHTS

The financial highlights are set out below.

June Change June December2006 % 2005 2005

Standard Bank Group

Earnings

Headline earnings Rm 4 869 18 4 126 9 013Profit attributable to ordinary shareholders Rm 5 121 27 4 036 8 981

Other indicators

Headline EPS cents 359,0 18 304,8 666,0Fully diluted headline EPS cents 353,0 18 300,4 654,5EPS cents 377,9 27 298,1 663,6Fully diluted EPS cents 371,3 26 293,8 652,2Dividend cover times 2,5 2,5 2,5Total dividends per share cents 144,0 18 122,0 267,0Net asset value per share cents 3 231 22 2 644 2 830Ordinary shareholders’ funds Rm 43 907 23 35 794 38 270ROE % 24,2 23,7 25,2Capital adequacy % 14,7 15,0 14,2Number of ordinary shares– weighted average thousands 1 356 202 1 353 703 1 353 382– fully diluted weighted average thousands 1 379 172 1 373 708 1 377 085Number of employees 40 601 40 514 40 245

Banking activities

Earnings

Headline earnings Rm 4 539 18 3 850 8 393Profit attributable to ordinary shareholders Rm 4 671 20 3 877 8 479

Balance sheet

Total assets Rm 755 112 34 564 891 601 738Loans and advances (net of credit Rm 415 585 38 301 546 342 870impairments)Deposit and current accounts Rm 498 994 33 374 063 412 309

Other indicators 24,4 24,2 25,6

ROE % 2,75 2,92 2,97Net interest margin times 54,2 55,0 54,4Non-interest revenue to total income % 1 300 >100 638 1 207Credit impairment charges Rm 0,70 0,45 0,40Credit loss ratio % 54,2 56,4 56,0Cost-to-income ratio %Effective tax rate (including indirect taxation) % 25,3 25,6 26,1Number of employees 36 524 1 36 113 36 131

9

10

GROUP BUSINESS UNITS

The Standard Bank Group key business units report as follows:

Personal andBusiness Banking

Vehicle andAsset Finance

Global markets Liberty Life

Mortgage lendingBanking and trade finance

Stanlib

Card products

Transactional products

Bancassurance

Investmentbanking

Corporate andInvestment Banking

Standard Bank Group

Investment Managementand Life Insurance

The business units are briefly described below.

Personal and Business banking

This includes banking and other financial services to individual customers and small to medium-sized enterprisesthroughout South Africa and in the rest of Africa.

June 2006 June 2005

External net advances (Rm) 229 966 180 238Headline earnings (Rm) 2 086 1 683Headline earnings growth (%) 24 26ROE (%) 28,9 27,3Cost-to-income ratio (%) 57,2 60,3Credit loss ratio (%) 1,02 0,85Headline earnings contribution (%) 43 41

The major product areas within Personal and Business banking are represented as follows:

Total income Headline earningsJune June December June June December2006 Change 2005 2005 2006 Change 2005 2005Rm % Rm Rm Rm % Rm Rm

Mortgage lending 1 379 18 1 171 2 425 501 14 440 793Instalment sales and finance leases 811 18 685 1 458 95 4 91 307Card products 1 471 38 1 066 2 363 172 16 148 402Transactional products 5 746 14 5 033 10 588 1 040 20 870 2 025Bancassurance 681 49 457 1 163 278 >100 134 463

Personal and Business Banking 10 088 20 8 412 17 997 2 086 24 1 683 3 990

Corporate and Investment Banking

This includes commercial and investment banking services to larger corporates, financial institutions and internationalcounterparties, focused on emerging markets through South Africa, 16 other African countries and 21 countries outsideAfrica.

June 2006 June 2005

External net advances (Rm) 179 469 115 040Headline earnings (Rm) 2 210 1 896Headline earnings growth (%) 17 7ROE (%) 27,9 25,5Cost-to-income ratio (%) 52,7 54,2Credit loss ratio (%) 0,26 (0,16)Headline earnings contribution (%) 45 46

The major product areas within Corporate and Investment Banking are represented as follows:

Total income Headline earningsJune June December June June December2006 Change 2005 2005 2006 Change 2005 2005Rm % Rm Rm Rm % Rm Rm

Global markets 2 653 25 2 129 4 428 816 11 735 1 417Banking and trade finance 2 333 12 2 077 4 433 742 6 700 1 560Investment banking 1 083 36 795 1 859 652 41 461 1 073

Corporate and Investment Banking 6 069 21 5 001 10 720 2 210 17 1 896 4 050

11

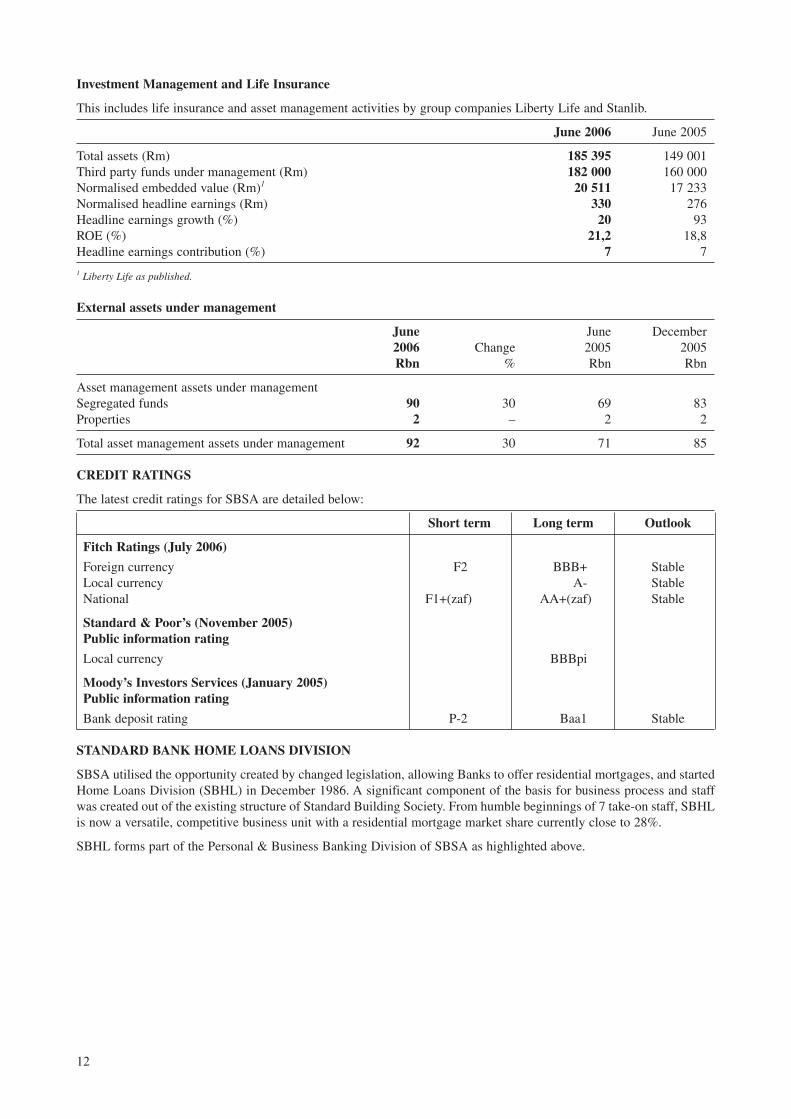

Investment Management and Life Insurance

This includes life insurance and asset management activities by group companies Liberty Life and Stanlib.

June 2006 June 2005

Total assets (Rm) 185 395 149 001Third party funds under management (Rm) 182 000 160 000Normalised embedded value (Rm)1 20 511 17 233Normalised headline earnings (Rm) 330 276Headline earnings growth (%) 20 93ROE (%) 21,2 18,8Headline earnings contribution (%) 7 7

1 Liberty Life as published.

External assets under management

June June December2006 Change 2005 2005Rbn % Rbn Rbn

Asset management assets under managementSegregated funds 90 30 69 83Properties 2 – 2 2

Total asset management assets under management 92 30 71 85

CREDIT RATINGS

The latest credit ratings for SBSA are detailed below:

Short term Long term Outlook

Fitch Ratings (July 2006)

Foreign currency F2 BBB+ StableLocal currency A- StableNational F1+(zaf) AA+(zaf) Stable

Standard & Poor’s (November 2005) Public information rating

Local currency BBBpi

Moody’s Investors Services (January 2005) Public information rating

Bank deposit rating P-2 Baa1 Stable

STANDARD BANK HOME LOANS DIVISION

SBSA utilised the opportunity created by changed legislation, allowing Banks to offer residential mortgages, and startedHome Loans Division (SBHL) in December 1986. A significant component of the basis for business process and staffwas created out of the existing structure of Standard Building Society. From humble beginnings of 7 take-on staff, SBHLis now a versatile, competitive business unit with a residential mortgage market share currently close to 28%.

SBHL forms part of the Personal & Business Banking Division of SBSA as highlighted above.

12

The SBHL organogram reflects the business unit’s structure, below

Note:

(i) Shaahien Mottiar has a direct reporting line into the centralised Credit function headed by the Global Head, Personal& Business Banking Credit.

(ii) Francois Schindehutte has a direct reporting line into the centralised Finance function headed by the Director,Personal & Business Banking Finance.

(iii) James Cullen has a direct reporting line into the centralised processing function headed by the Director, Personaland Business Banking Integrated Processing.

Origination and Customer Interaction: Products, Acquisition and Operations:

Products

Home Loans Product and Low Income Housing units deliver development and management services. Product diversityis required to cover a wide range of customer profiles and income ranges based on the country’s social demographics, inthe following key categories/segments:

• Affinity & Mass;

• Private;

• Affordable Housing; and

• Fully Guaranteed (pension-backed) Lending.

Acquisition

SBSA follows a multi-channel strategy that involves partnerships on internal and external fronts, as follows:

Internal:

• Branch network;

• Private Bank and Priority Suites;

• Internet;

• Call centre;

• Home Loans mobile consultants; and

• Business banking.

13

Shaahien Mottiar

Head, Credit (i)

Staff Comp: 69

FrancoisSchindehutte

Director,Finance (ii)

Staff Comp: 18

JohnRivers-Moore

Director, SalesSupport

Staff Comp: 4

Dennis Lupambo

Director

Shaheen Adam

Director, Product

Staff Comp: 10

Rob Pellizzer

Head, LegalCompliance andOperational Risk

Staff Comp: 2

Linda Sing

Director,AffordableHousing

Staff Comp: 103

Jenny Price

Head, CustomerRetention

Staff Comp: 77

Trevor Biggs

Head, BusinessDelivery

Enablement

Staff Comp: 14

James Cullen

Director,Operations (iii)

Staff Comp: 1 153

Leon Barnard

Director

Home Loans

External:

• Corporate partnerships;

• Mortgage originators;

• Estate agencies; and

• Developers.

Operations

Application processing and customer management involves five provincial home loans offices. The new loans team isresponsible for application, processing and granting; the assessors are responsible for property valuation and theregistration team is responsible for the legal fulfilment process.

Once application information has been validated it is input into credit application scorecards. The scorecard decisionoutcome is an approval, decline or referral to the credit granting team to make the final grant decision. A credit qualityassurance team validate key data inputs on a sample (±20%) of monthly grants. Results of the monthly assuranceassessments are distributed to key credit and operations staff for further action.

Provincial operations are supported by the retention unit; securities and cancellations; client services departments andthe customer contact centre. Further business management and support involves SBHL finance, SBHL credit,compliance and risk, legal and various other centralised service teams.

Home Loans Credit

Governance and Structure

Credit risk is managed in a governance structure supported by clearly defined mandates and delegated authorities. TheGroup Credit Committee delegates authority to the African Credit Committee for the approval of credit proposals. ThePersonal and Business Banking Credit department is responsible for the credit operations within the Personal andBusiness Banking Division of the group and is managed and mandated by the Personal and Business Banking CreditCommittee. Credit decision making is independent of other business areas.

Underwriting

The underwriting team consists of four provincial processing units in Johannesburg, Pretoria, Cape Town and Durban.These processing units cover all business origination processes and effectively assess loan applications where a manualcredit assessment is required. Credit scoring and policy rules are applied against all applications and each applicant inthe case of multiple (joint) applicants. Governance committees and processes ensure the effective evaluation of, andchanges to credit policies.

Application scorecards were first introduced in mid-1997 to support the entire underwriting process. The scorecarddevelopment team has used expertise from Experian/Scorex although most development is now done in-house withguidance from international scorecard consultants. The Experian Strategy Manager software application is used insupport of bespoke Personal & Business Banking Credit software and systems, managing both application andbehavioural scorecards. Internal and external data is used in the scoring process. Ongoing and regular reviews ofscorecards are conducted using analytical methods. Cut-offs are adjusted depending on SBSA’s risk appetite.

A dual credit bureau strategy is utilised. The outcome of the process is ‘a credit score’ associated with a predeterminedrisk profile including the probability of default. Credit scores are categorised by risk-bands which are then used todetermine interest-rate pricing and terms and conditions extended to the applicant. Acceptance or rejection of theapplication offered to the customer is largely driven by scorecard outcomes.

Credit policies and procedures supplement the scorecard and enhance the business’ ability to best manage exceptions oroutliers, commonly known as ‘refers’. The granting area that assesses the refers is staffed by qualified and experiencedpersonnel of appropriate seniority with appropriate mandates. This ensures that all referred applications found tocontravene policy rules or supported by compelling circumstances i.e. marginal affordability, are comprehensivelyreviewed. Acceptance rates and the relative performance of referred applications are monitored, maintaining establishedparameters.

Collections

The Home Loan Collections Department is centralised in Johannesburg. The primary objective of the arrearsmanagement process is to rehabilitate arrear accounts. An account is deemed to be in arrears if any payment or portionsthereof have not been made in a timely manner.

14

Accounts are differentiated into two broad categories in the collections process depending on their arrears status.These are:

• Pre-Legal or Pre-Non-Performing Loans (NPL), including collectors; and

• Legal or Non-Performing Loans (NPL), including deceased estates and insolvencies.

Accounts in pre-legal/pre-NPL are those which are one instalment or more in arrears and have not yet been placed in theforeclosure process. Deceased estates and insolvencies will move directly to Legal/NPL as soon as they have beenidentified as such.

It should be noted that accounts could be in the pre-legal process after 90-days in arrears as a result of transfer beingawaited for the sale of the related property. In most of these instances a property guarantee will be held.

Legal or NPL accounts are those on which the foreclosure process has been initiated. Once accounts have been flaggedas legal/NPL, interest income is suspended and specific debt provisions are raised against these accounts according tothe agreed policy. Most legal/NPL accounts are outsourced to SBSA’s panel of attorneys as part of the debt collectionprocess.

Differentiated collection strategies are used to ensure an effective and efficient process. The risk determines thecollection procedure to be followed with respect to each account including the type of contact (phone call, physical calls,letters, SMS, etc) as well as frequency of contact. There is a dedicated credit call centre located in Johannesburg.

SBHL was the first area in credit to implement an automated collections system (CACS). The CACS was implementedin November 2005 and is performing to expectations.

Systems

All aspects of SBHL business are operated through systems that are continually reviewed and updated to supportbusiness requirements. These systems are integrated into SBSA’s branch network and third party originators. Thisfacilitates the comprehensive management of origination, customer management, legal, credit and retention processes.

15

THE HOME LOAN POOL

This section should be read in conjunction with, and is qualified in its entirety by, the detailed information containedelsewhere in this Transaction Supplement and the Programme Memorandum and in particular the loan pool informationdisclosed under Appendix I of this Transaction Supplement.

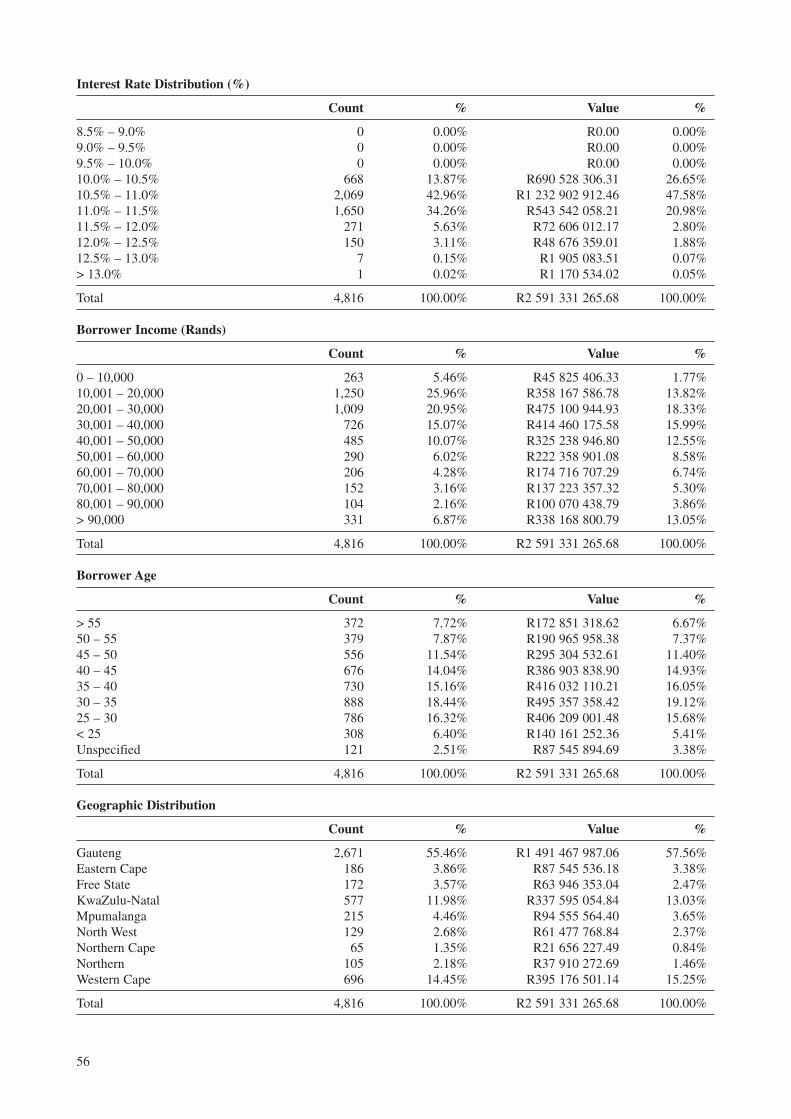

1. HOME LOAN POOL

1.1 The Home Loans included in this transaction were originated by SBSA directly through its network ofbranches or indirectly through third party originators since 10 March 2006 (selected by the date on which theIndemnity Bond was registered). The loan pool is a subset that was randomly selected from of all loans thatwere originated and complied with the Eligibility Criteria. All loans that were included in the loan pool havebeen evaluated and approved in terms of SBSA’s standard credit procedures applicable to residential mortgageloans at the time they were granted. The majority of property valuations are performed by valuers employedby SBSA or, in some cases, by accredited independent valuers.

1.2 All Home Loans are amortising and the Borrower is required to repay the loan in equal instalments over theterm of the loan. The loans generally bear a variable interest rate, and when that rate changes, the instalmentwill be recalculated to ensure that the loan is amortised over the remaining term of that loan. Where the loansare linked to a variable rate, this will be SBSA’s Prime Rate as determined from time to time. Historically allthe major banks have charged similar prime rates. However, SBSA is not obliged to change its rate when otherbanks do or to charge a similar rate.

1.3 Some Home Loans are subject to a fixed rate of interest (or the rate may be capped) for part of the term ofsuch loans. The remainder of the Home Loans are typically granted at a variable rate that is a concession toSBSA’s Prime Rate (i.e. on a Prime minus basis). The magnitude of the concession (discount) is determinedby SBSA when the loan is granted and reflects, to some extent, the creditworthiness of the Borrower. In termsof the Eligibility Criteria, the minimum interest rate payable on each loan is the Prime Rate less 2.2% (or, inthe case of a fixed rate loan, the net yield paid by the Hedge Counterparty). The Home Loans comprising therelevant Asset Pool (as defined in the Sale Agreement) at the Initial Effective Date will not be subject tointerest rates which are capped or fixed.

1.4 All of the Home Loans included in the Initial Asset Pool are Guaranteed Home Loans.

2. HISTORICAL DATA

2.1 The tables in Appendix 1 set out statistical information representative of the characteristics of the portfolio ofHome Loans on the Cut-Off Date, being 13 January 2007. The aggregate balance of the portfolio of HomeLoans on the Cut-Off Date is R4 627 214 381.40. In the event that the Subsequent Issue does not take place,the portfolio of Home Loans sold to the Issuer on the Initial Effective Date, shall comprise an initial pool ofHome Loans to the value of at least R2 114 225 000.00. The information is derived from information suppliedby the Seller, which reflects the position as at the Cut-Off Date. The characteristics of the Initial Asset Poolas at the Initial Effective Date may differ from those set out in the tables as a result of, inter alia, Repaymentsand Prepayments of Home Loans prior to the Initial Effective Date.

2.2 At the Cut-Off Date, 78.05% (78.56% in the event that the Subsequent Issue does not take place) of Borrowersunder the entire pool of Home Loans were not self-employed, the remainder being self-employed. Informationin respect of employment and use of the Property is derived from information supplied to the Seller by theBorrowers which cannot be independently verified.

3. ELIGIBILITY CRITERIA

On origination of each Participating Asset from time to time, the Seller’s standard credit approval policies andprocedures will have been applied. The general criteria that each Participating Asset must satisfy in order to qualifyfor acquisition by the Issuer, include, inter alia, the following, all as at the Effective Date:

16

Programme Wide

3.1 each Home Loan Agreement:

3.1.1 constitutes legal, valid and binding obligations of the Borrower under such Home Loan Agreement,enforceable against such Borrower in accordance with the terms of such Home Loan Agreement;

3.1.2 is in full force and effect and, at the date such Home Loan Agreement was entered into, each party tosuch Home Loan Agreement had the capacity and authority to execute such Home Loan Agreement;

3.1.3 is entered into with a Borrower who may only be a natural person, company, close corporation or atrust;

3.1.4 is one in respect of which:

3.1.4.1 there are no facts or circumstances which give rise to any right of rescission, set-off,counterclaim or defence, to the obligations of the Borrower;

3.1.4.2 neither the operation of any of the terms of the Home Loan Agreement nor the exercise of anyright under the Home Loan Agreement will render such Home Loan Agreementunenforceable in whole or in part or subject to any right of rescission, set-off, counterclaimor defence;

3.1.4.3 no such right of rescission, set-off, counterclaim or defence has been asserted with respect tosuch Home Loan Agreement;

3.1.4.4 the Seller has no knowledge of any challenge, dispute or claim by or against the Borrowerunder or affecting such Home Loan Agreement or of the liquidation or insolvency of theapplicable Borrower;

3.1.4.5 neither the Seller nor the Borrower is (nor would with the giving of notice or lapse of time orthe satisfaction of any other condition or any combination thereof be) in breach of, or indefault under, its obligations arising under such Home Loan Agreement;

3.1.4.6 no amounts due with respect to such Home Loan Agreement shall be reduced or impaired, asa result of:

3.1.4.6.1 any action or inaction by the Seller in respect of periods prior to the Effective Date;or

3.1.4.6.2 any claim by any Borrower against the Seller in respect of periods prior to theEffective Date;

3.1.5 is capable of being assigned without the prior consent of, or notice to, the Borrower;

3.1.6 is not subject to any option, right of first refusal, pre-emptive right or other agreement giving anyperson a right (whether exercisable now or in the future and whether contingent or not) to call for thesale and transfer to them or any third party of such Home Loan Agreement, and each such Home LoanAgreement is free and capable of being assigned;

3.1.7 the Properties subject thereto are not subject to any Encumbrance, save as expressly contemplated inany Transaction Document;

3.1.8 has not been ceded, assigned, transferred, made-over, sold and/or discounted by the Seller to any thirdparty, bank, discount house, finance house and/or factoring house;

3.1.9 is upon terms and conditions substantially and materially the same as those disclosed in writing to theIssuer;

3.1.10 is Rand denominated;

3.1.11 has been concluded with a Borrower who is a citizen of South Africa;

3.1.12 was originated by or on behalf of the Seller in the ordinary course of the Seller’s business, applyingthe Seller’s standard credit approval policies and procedures at the time when the relevant Home LoanAgreement was concluded;

17

3.1.13 has not been amended or modified, except in writing, and copies of all such amendments andmodifications are attached to the relevant Home Loan Agreement;

3.1.14 can be segregated and is a separately identifiable agreement on the system of the Servicer at any timeafter the Effective Date;

3.1.15 is capable of cession and assignment to the Issuer free of any Encumbrances in terms of a legal, validand binding Sale Agreement;

3.2 each Borrower has executed a Borrower Indemnity in favour of the Seller, its successors in title or assigns andeach such Borrower Indemnity requires the Borrower to secure its obligations under the Borrower Indemnityby a first ranking Indemnity Bond or such other lower ranking bond, provided that all mortgage bondsregistered against the title deeds of the Property are registered in favour of the Seller, its successors in title orassigns and the registration of such first ranking Indemnity Bond or other lower ranking bond, if applicablehas taken place;

3.3 each document in respect of Related BG4 Security:

3.3.1 is a legal, valid and binding obligation of the provider of such security, enforceable against suchprovider in accordance with the terms of such document;

3.3.2 is in full force and effect and each party to such document had capacity and authority to execute suchdocument;

3.3.3 is capable of being assigned without the prior consent of, or notice to, the provider of such security;

3.3.4 has not been amended or modified, except in writing, and copies of all such amendments andmodifications are attached to the relevant Home Loan Agreement; and

3.3.5 can be segregated and is a separately identifiable agreement on the system of the Servicer at any timeafter the Effective Date.

Transaction Specific

3.4 each Home Loan:

3.4.1 provides that payments under such agreement are not subject to deduction or withholding;

3.4.2 complies with all requirements of any Applicable Laws;

3.4.3 has a maximum LTV Ratio (“LTV Ratio Maximum”) of not more than 100% in relation to thecommitted loan balance provided that if the Arrears Reserve Threshold is greater than 0.8%, theMaximum LTV Ratio is not more than 80% in relation to the committed loan balance. If the ArrearsReserve Threshold reduces to below 0.8%, the LTV Ratio Maximum shall again not be more than100% in relation to the committed loan balance;

3.4.4 has an ITI Ratio of less than 30%;

3.4.5 has a maximum term of 25 years from the date of the first advance of funds to a Borrower in terms ofthe relevant Home Loan Agreement;

3.4.6 is Fully Performing as at the date of purchase thereof by the Issuer;

3.4.7 is not more than 0.5 months in arrears;

3.4.8 is repayable in equal instalments over the term of the Home Loan;

3.4.9 is a loan agreement secured directly or indirectly by, at least, a first ranking Indemnity Bond over animmovable property;

3.4.10 requires the Borrower, or the relevant body corporate on behalf of the Borrower, to take out andmaintain homeowners’ insurance;

3.4.11 is a loan agreement not secured by a dwelling or building under construction;

3.4.12 has a minimum interest rate yield (or in the case of a fixed rate loan, the net yield paid by the DerivativeCounterparty) of the Prime Rate less 2.2%; and

3.4.13 has a maximum loan amount of R3 500 000.

18

THE SERVICER, THE SERVICING AGREEMENT AND SERVICER UNDERTAKINGAGREEMENT

This section should be read in conjunction with, and is qualified in its entirety by, the detailed information containedelsewhere in this Transaction Supplement and the Programme Memorandum and in particular the section of theProgramme Memorandum headed “The Servicer and the Servicing Agreement”.

The Issuer will appoint SBSA as the Servicer in terms of the Servicing Agreement. The Servicer is required to administerthe Participating Assets as the agent of the Issuer in accordance with the terms of the Servicing Agreement as readtogether with the Master Servicing Agreement.

The description of the Servicer’s duties contained in the Programme Memorandum applies to the Servicer’s duties interms of this Transaction provided that, in addition to such duties:

• in terms of the Servicing Agreement, the Servicer undertakes to advise and assist the Issuer in relation to all such stepswhich need to be taken in order to procure that the Issuer complies with all Applicable Laws, including, whereapplicable, the National Credit Act, No 34 of 2005; and

• in terms of the Servicer Undertaking Agreement, pending registration of the transfer of the Indemnity Bonds to theGuarantee Entity in relation to Participating Assets sold to the Issuer, the Servicer will provide the Servicer IndemnityUndertaking in terms of which the Servicer undertakes, on request by the Issuer in terms of the Servicer UndertakingAgreement, to pay over all amounts collected from the Borrower in terms of the Borrower Indemnity and/or theIndemnity Bond. Upon registration of transfer of an Indemnity Bond to the Guarantee Entity, the rights andobligations of SBSA under the relevant Borrower Indemnity and the Indemnity Bond and of the Servicer under theServicer Undertaking Agreement in relation to that Indemnity Bond will be transferred to the Guarantee Entity, andsuch rights and obligations under the Servicer Undertaking Agreement will be replaced by the Guarantee EntityGuarantee, issued by the Guarantee Entity in favour of the Issuer with effect from the Transfer Date.

The Servicing Agreement provides for the manner in which the Servicer will collect all monies from Borrowers due tothe Issuer, on the Issuer’s behalf. Monies collected will be transferred from the Collections Account to the TransactionAccount on the 5th Business Day of the month following the month during which the amounts were collected by theServicer, unless an Enforcement Notice has been delivered to the Issuer, the Servicer no longer has the Required CreditRating and/or upon the occurrence of an Event of Default by the Servicer under the Servicing Agreement, in which eventmonies collected will be transferred to the Transaction Account on a daily basis.

SBSA is entitled to charge a Servicing Fee (exclusive of VAT) for its services under the Servicing Agreement payableon each Payment Date in accordance with the Priority of Payments. For so long as SBSA is the Servicer, the ServicingFee payable to SBSA in accordance with the Priority of Payments will be capped at the Servicing Fee Cap.

The appointment of SBSA may be terminated by the Issuer (with the consent of the Security SPV) on the happening ofcertain events of default, insolvency on the part of SBSA or pursuant to a breach by the Servicer of its obligations. TheServicer is entitled to resign on not less than 12 months’ written notice.

SBSA has disaster recovery systems and back up arrangements in place. In the event of a “disaster” (for these purposes,any event which disrupts on-line availability for more than 48 consecutive hours), SBSA’s software will be loaded onone or more computers in a secure offsite location. The completion of recovery is to take place within 48 hours.

The Servicer is not under any obligation to fund payments owed in respect of the Securitisation Scheme, absorb lossesincurred in respect of the Participating Assets transferred to the Issuer or otherwise to recompense investors for lossesincurred in respect of the Securitisation Scheme.

On each Determination Date the Servicer is entitled, but not obliged, to pay into the Transaction Account an amount (a “Servicer Advance”) equal to any instalments owing under a Participating Asset but unpaid prior to suchDetermination Date, but only if the Servicer confirms in writing that, in its reasonable opinion, the failure of theBorrower to make timeous payment of the instalment is for non credit-related reasons and is not due to a lack of fundsor an invalid refusal on the part of the Borrower to make that payment. The Issuer shall reimburse the Servicer Advancetogether with market related interest which has accrued on such Servicer Advance (from the date of the Servicer Advanceto the date of reimbursement) forthwith upon, but only to the extent that, such late instalments are paid by or on behalfof the relevant Borrower to the Issuer. Such amounts shall be paid as an Excluded Item from available funds in theTransaction Account. The obligations of the Servicer in regard to the advance of Servicer Advances do not significantlyextend beyond the salient features disclosed in this Transaction Supplement and the Servicer will not support theSecuritisation Scheme beyond such obligations within the meaning of the Securitisation Regulations.

19

THE ADMINISTRATOR AND THE ADMINISTRATION AGREEMENT

This section should be read in conjunction with, and is qualified in its entirety by, the detailed information containedelsewhere in this Transaction Supplement and the Programme Memorandum and in particular the section of theProgramme Memorandum headed “The Administrator and the Administration Agreement”.

The Issuer will appoint SBSA as the Administrator and as its agent, to advise the Issuer in relation to the managementof the Issuer Programme and to exercise the Issuer’s respective rights, powers and duties under the TransactionDocuments, upon the terms and conditions of the Administration Agreement.

SBSA is entitled to charge an Administrator Fee (exclusive of VAT) for its services under the Administration Agreementpayable on each Payment Date in accordance with the Priority of Payments.

The appointment of SBSA as Administrator may be terminated by the Issuer (with the consent of the Security SPV) onthe happening of certain events of default, insolvency on the part of SBSA or pursuant to a breach by the Administratorof its obligations. The Administrator is entitled to resign on not less than 12 months’ written notice.

20

STRUCTURAL FEATURES

1. CASH MANAGEMENT

Cash is managed in the manner set out below.

1.1 Account Bank

In the event that the Account Bank ceases to hold the Required Credit Rating, a replacement Account Bankwill be appointed in accordance with the provisions of the Bank Agreement.

1.2 Transaction Account

All amounts due to the Issuer (other than amounts referred to in 1.3 below) will be paid directly on receiptthereof into the Transaction Account. Certain cash reserves of the Issuer if established, will be held in theTransaction Account. Prior to the delivery of an Enforcement Notice, the Administrator and the Servicer willhave joint signing authority in respect of the Transaction Account. After the delivery of an EnforcementNotice, the Security SPV will have sole signing authority in respect of the Transaction Account.

1.3 Collections Account

The Servicer undertakes to procure that amounts paid by or on behalf of Borrowers in respect of theParticipating Assets sold to the Issuer and paid for or to the account of the Issuer will be paid into theCollections Account and transferred, together with any interest earned, to the Transaction Account on the5th Business Day of the month following the month during which the amounts were collected by the Servicer,unless an Enforcement Notice has been delivered to the Issuer, the Servicer no longer has the Required CreditRating and/or upon the occurrence of an Event of Default by the Servicer under the Servicing Agreement, inwhich event monies collected will be transferred to the Transaction Account on a daily basis.

1.4 Other payments

The Servicer shall procure that all amounts received by the Servicer under the Participating Assets which havenot specifically been provided for under 1.2 and 1.3 above and which are attributable to the ParticipatingAssets sold to the Issuer shall be paid into the Transaction Account on a daily basis. Where such amounts arenot immediately identifiable as being attributable to such Participating Assets, the amounts (together with anyinterest earned) shall be paid into the Transaction Account immediately upon their being identified as beingattributable to such Participating Assets.

1.5 Permitted Investments

The Administrator may, on behalf of the Issuer and on the instructions of the Servicer, invest cash from timeto time standing to the credit of the Issuer’s Bank Accounts in Permitted Investments, provided that for so longas the GIC Provider has the Required Credit Rating all cash from time to time standing to the credit of theIssuer’s Bank Accounts will be invested with the GIC Provider. The proceeds from the Initial Issue of Notesshall be invested in Permitted Investments until the Initial Effective Date on which date such proceeds shallbe applied to purchase the eligible Participating Assets.

2. CASH RESERVE

On any Payment Date, the Issuer will be required to pay an amount into the Cash Reserve, in terms of the Priorityof Payments, up to the Cash Reserve Required Amount. The Cash Reserve will be available to meet certain seniorfees and expenses and interest on the most senior Notes as more fully specified in the Pre-Enforcement Priority ofPayments (which is summarised in the section headed “Priority of Payments”) and set out in more detail in theAdministration Agreement, on any Payment Date, in the event of a shortfall in available funds for that purpose interms of the Priority of Payments. On each Payment Transfer Date, interest accrued on the Cash Reserve balance upto the Payment Date, will be paid to the Transaction Account. In the event of the delivery of an Enforcement Notice,all monies in the Cash Reserve will be applied in accordance with the Post-Enforcement Priority of Payments.

3. ARREARS RESERVES

3.1 The Issuer will be obliged to pay an amount into the Arrears Reserve up to the Arrears Reserve RequiredAmount on each Payment Date immediately succeeding the relevant Determination Date pursuant to therelevant provisions of the Pre-Enforcement Priority of Payments. The Arrears Reserve will be funded out ofexcess spread and not out of Principal Collections.

21

3.2 If at any time the amount standing to the credit of the Arrears Reserve exceeds the Arrears Reserve RequiredAmount, the amount of such excess shall be paid to the Transaction Account. If an Enforcement Notice isdelivered, all monies in the Arrears Reserve will be applied in accordance with the Post-Enforcement Priorityof Payments. On each Payment Transfer Date, interest accrued on the Arrears Reserve balance up to thePayment Date, will be paid into the Transaction Account.

4. PURCHASE RESERVE

On any Payment Date during the Revolving Period, the Issuer will be required to pay Principal Collections notapplied, in terms of the Pre-Enforcement Priority of Payments, to meet certain senior fees and expenses, the paymentof capital and interest on the most senior Notes and the funding of Further Advances, as more fully specified in thePre-Enforcement Priority of Payments, (which is summarised in the section headed “Priority of Payments”) and setout in more detail in the Administration Agreement, into the Purchase Reserve in terms of the Priority of Payments.Funds in the Purchase Reserve may be used during each Interest Period (i) to fund Redraws; (ii) to fund theacquisition of Additional Assets during the Revolving Period or the advance of Further Advances, during theRevolving Period and (iii) to meet certain senior fees and expenses, the payment of capital and interest on the mostsenior Notes in the Pre-Enforcement Priority of Payments, on any Payment Date, in the event of a shortfall inavailable funds for that purpose in terms of the Priority of Payments. Any amounts in excess of R10 000 000standing to the credit of the Purchase Reserve for two consecutive Payment Dates shall be added to the RedemptionAmount and applied in redeeming the Notes. On each Payment Transfer Date, interest accrued on the PurchaseReserve balance from the Determination Date up to the Payment Date, will be paid to the general funds in theTransaction Account. In the event of the delivery of an Enforcement Notice, all monies in the Purchase Reserve willbe applied in accordance with the Post-Enforcement Priority of Payments.

5. REDRAW RESERVE

On any Payment Date, the Issuer will be required to pay an amount into the Redraw Reserve, in terms of the Priorityof Payments, up to the Redraw Reserve Required Amount. The Redraw Reserve will be available to (i) fund Redrawsand (ii) meet certain senior fees and expenses, the payment of capital and interest on the most senior Notes and thefunding of Redraws, as more fully specified in the Pre-Enforcement Priority of Payments, (which is summarised inthe section headed “Priority of Payments”) and set out in more detail in the Administration Agreement) in the Pre-Enforcement Priority of Payments, on any Payment Date, in the event of a shortfall in available funds for thatpurpose in terms of the Priority of Payments. On each Payment Transfer Date, interest accrued on the RedrawReserve balance up to the Payment Date, will be paid to the Transaction Account. In the event of the delivery of anEnforcement Notice, all monies in the Redraw Reserve will be applied in accordance with the Post-EnforcementPriority of Payments.

6. INTEREST DEFERRAL EVENT

In the event of the occurrence of an Interest Deferral Event on any Class of Notes, interest will not accrue nor bepaid on the amount of the deferred interest in respect of such Class of Notes.

7. SUBORDINATED LOAN AGREEMENTS

7.1 SBSA and any member of the Standard Bank Group will be appointed as Subordinated Lenders in terms ofthe Subordinated Loan Agreements. The advances in terms of the Subordinated Loan Agreements shall beused to provide part of the initial funding for the Issuer on the Initial Issue Date.

7.2 The Subordinated Loans will be in the following amounts:

7.2.1 Subordinated Loan No. 1: R9 000 000; and

7.2.2 Subordinated Loan No. 2: R18 500 000.

7.3 The Subordinated Loans will be repaid as and when cash is available to make such repayment in accordancewith, and to the extent permitted by, the Priority of Payments, with the final repayment date being the FinalMaturity Date of the last Tranche of Notes in issue.

7.4 There is no recourse to the Subordinated Lenders, as lenders under the Subordinated Loan Agreements,beyond the fixed contractual obligations provided for in such agreements.

22

7.5 The Subordinated Lenders will bear a first-loss interest in the Issuer through Subordinated Loan No. 1 and asecond-loss interest in the Issuer through Subordinated Loan No. 2, respectively.

8. REDRAWS AND FURTHER ADVANCES

8.1 Redraws

8.1.1 The Issuer may advance Redraws to Borrowers on any date (whether in terms of a Redraw Facility oras otherwise agreed between the Home Loan Lender and the Borrower), subject to the satisfaction ofcertain conditions, including that the Borrower is not then in unremedied default of any of suchBorrower’s obligations in terms of the Home Loan Agreement and that the Redraw will be repaidwithin the original duration of the Home Loan Agreement, unless rescheduled by agreement betweenthe Home Loan Lender and the Borrower.

8.1.2 The Issuer, is entitled in its discretion, to cancel the Access Bond facility. The Issuer may exercise thisdiscretion to cancel the facility if, inter alia, the Issuer has insufficient funds available to fund suchRedraws and a Redraw Notification Trigger Event has occurred.

8.1.3 Upon the occurrence of a Redraw Notification Trigger Event, the Servicer on behalf of the Issuer shallbe obliged to notify Borrowers of any action which the Issuer intends to take in respect of the Redrawobligations as provided for in the Servicing Agreement (including, but not limited to, terminating therelevant Redraw Facility in accordance with its terms).

8.2 Further Advances

8.2.1 The Issuer may, in its discretion, advance Further Advances to Borrowers on any given day inaccordance with the provisions of the relevant Home Loan Agreements, provided that the conditionsset out in the Servicing Agreement are met. Such conditions include, inter alia, that:

8.2.1.1 the Revolving Period is continuing and no Stop Purchase Event has occurred;

8.2.1.2 the Issuer has funds available to make such Further Advance;

8.2.1.3 following the making of the Further Advance, the Portfolio Covenants are met;

8.2.1.4 each relevant Further Advance, together with the balance outstanding under the relevantHome Loan Agreement immediately prior to the making of such Further Advance, does notexceed the capital amount secured by the relevant Indemnity Bond(s);

8.2.1.5 each relevant Further Advance, together with the balance outstanding under the existingHome Loan Agreement (with the Borrower in respect of whom such Further Advance ismade) immediately prior to the making of such Further Advance, satisfies the EligibilityCriteria, assessed as if such Further Advance had been acquired by the Issuer; and

8.2.1.6 in respect of each Further Advance, the Home Loan Agreement with the relevant Borrower isamended, in accordance with the provisions of such Home Loan Agreement, to reflect theamended capital amount which, for the avoidance of doubt, does not exceed the capitalamount secured by the relevant Indemnity Bond(s), as the case may be, in respect of therelevant Property (excluding any amount identified as an additional sum in the relevantIndemnity Bond(s)).

9. ADDITIONAL ASSETS

9.1 The Issuer may, during the Revolving Period, acquire Additional Assets from the Seller on the terms of theSale Agreement using monies available for this purpose in accordance with the Pre-Enforcement Priority ofPayments.

9.2 Each sale and transfer of Additional Assets is subject to the satisfaction of the criteria set out in the SaleAgreement including, inter alia, the following: (i) the Additional Asset is an Eligible Asset; and (ii) as aconsequence of giving effect to the sale and transfer of such Additional Asset, the Portfolio Covenants aresatisfied.

9.3 The Issuer may acquire Eligible Assets originated by or on behalf of SBSA subject to the Issuer entering intosuitable Derivative Contracts with Derivative Counterparties so as to ensure that no interest rate basismismatch will exist between the Notes in issue and the Participating Assets. The purchase of such loans isfurther subject to, inter alia, (i) the relevant provisions of the Sale Agreement being applicable to such sale,thereby constituting a legal, valid, binding and enforceable agreement; and (ii) the Participating Assetscomplying with the Eligibility Criteria.

23

10. PRINCIPAL DEFICIENCY LEDGER

10.1 A Principal Deficiency Ledger will be established to record the Principal Deficiency (if any) on eachDetermination Date, calculated by deducting the Assets expected to exist (after having made all payments inaccordance with the Priority of Payments) as at the close of business on the immediately succeeding InterestPayment Date from the Liabilities expected to exist (after having made all payments in accordance with thePriority of Payments) as at the close of business on the immediately succeeding Interest Payment Date,

where “Liabilities” means:

10.1.1 the aggregate Outstanding Principal Amount of the Notes on the last day of the immediately precedingCollection Period; less

10.1.2 the amount allocated in the Pre-Enforcement Priority of Payments for the redemption of the Notes onthe immediately succeeding Interest Payment Date;

and “Assets” means:

10.1.3 the aggregate outstanding Principal Balances of the Participating Assets sold to the Issuer on the lastday of the immediately preceding Collection Period, excluding any Non-Performing Loans, providedthat, for the purpose of this 10.1.3 and notwithstanding the definitions set out in the section headed“Transaction Specific Definitions”, “Non-Performing Loans” means Participating Assets of the Issuerin respect of which there are arrears of an amount greater than 6 instalments; provided further that forthe purpose of this definition: (i) a Borrower shall not be deemed to be in arrears if the obligations ofthe Borrower under the Home Loan Agreement are guaranteed by a financial institution; and (ii) for aslong as Participating Assets are under rehabilitation in accordance with the Servicer’s standard policiesand procedures, such Participating Assets shall not be regarded as “Non-Performing” for the purposeof this 10.1.3; plus

10.1.4 the amount allocated in the Pre-Enforcement Priority of Payments to advance Redraws and advanceFurther Advances and purchase Additional Assets on the immediately succeeding Interest PaymentDate; plus

10.1.5 the aggregate principal amount of Redraws and Further Advances advanced since the previousCollection Period and expected to be made up to the immediately succeeding Interest Payment Date;plus

10.1.6 the aggregate of the credit balances, if any, in each of the:

10.1.6.1 Cash Reserve;

10.1.6.2 Arrears Reserve;

10.1.6.3 Purchase Reserve; and

10.1.6.4 Redraw Reserve,

provided that the Principal Deficiency shall never be less than zero.

11. REVOLVING PERIOD

11.1 The Revolving Period comprises the period commencing on (and including) the Initial Effective Date andending on the occurrence of a Stop Purchase Event or upon the first Business Day following the expiry of3 years commencing from the Initial Effective Date, whichever occurs first, unless the Issuer elects to shortenthe Revolving Period by giving 5 Business Days’ notice to the Security SPV, the Noteholders and the Servicerin which case the Revolving Period will end on the date on which such notice expires.

11.2 During the Revolving Period, if the amount allocated for the purchase of Additional Assets or the advance ofFurther Advances is not fully utilised due to insufficient Eligible Assets offered to the Issuer for purchase orinsufficient Further Advances advanced by the Issuer then such unutilised cash shall be paid into the PurchaseReserve. Any amounts in excess of R10 000 000 standing to the credit of the Purchase Reserve for twoconsecutive Payment Dates shall be added to the Redemption Amount and applied in redeeming the Notes.

12. GUARANTEED HOME LOANS

12.1 All Participating Assets sold to the Issuer will be Guaranteed Home Loans.

12.2 Upon the purchase of a Guaranteed Home Loan, only the Home Loan is transferred to the Issuer in terms ofthe provisions of the Sale Agreement. The Issuer’s rights against the Borrower on default under the HomeLoan Agreement are secured initially, pending the Transfer Date, in terms of the Servicer Undertaking

24

Agreement, and with effect from the Transfer Date by a Guarantee Entity Guarantee issued by the GuaranteeEntity in favour of the Issuer. The Borrower indemnifies the Seller (and/or its successor-in-title) in terms ofthe Borrower Indemnity against, amongst other things, any claims by the Issuer under the ServicerUndertaking Agreement and the Guarantee Entity Guarantee, as the case may be. As security for theBorrower’s obligations under the Borrower Indemnity, the Borrower registers an Indemnity Bond in favour ofthe Seller. With effect from the Transfer Date, the rights and obligations of SBSA under the correspondingBorrower Indemnity and Indemnity Bond and of the Servicer under the Servicer Undertaking Agreementapplicable to the relevant Participating Asset will be assigned to the Guarantee Entity, and such rights andobligations under the Servicer Undertaking Agreement are replaced by those under the Guarantee EntityGuarantee issued by the Guarantee Entity in favour of the Issuer in terms of the Common Terms GuaranteeAgreement. If the registration of transfer of the relevant Indemnity Bond does not take place:

12.2.1 in respect of Indemnity bonds relating to the Home Loans comprising the Initial Asset Pool within aperiod of 6 months from the Initial Effective Date;

12.2.2 in respect of Indemnity Bond relating to a Warranty Replacement Asset, Replacement Asset orAdditional Asset as the case may be, within a period of 6 months from the corresponding Sale Date ordate of replacement of such Warranty Replacement Asset, Replacement Asset or Additional Asset asthe case may be; or

12.2.3 in respect of any particular Indemnity Bond, such later period as the case may be agreed in writingbetween the parties to the Assignment Agreement and the Rating Agency, if applicable

the Assignment Agreement provides that there will be no assignment of the relevant Indemnity Bond andBorrower Indemnity and SBSA will continue to be the holder of the rights and obligations under the relevantIndemnity Bond and Borrower Indemnity.

12.3 The Servicer Undertaking Agreement and the Guarantee Entity Guarantee is limited to the amounts theServicer or the Guarantee Entity, as the case may be, is able to recover from the Borrower under the BorrowerIndemnity and the Indemnity Bond. The Guarantee Entity Guarantee also provides that, if requested by theIssuer or upon the happening of certain events, the Guarantee Entity shall transfer all Borrower Indemnitiesand Indemnity Bonds to the Issuer’s nominee.

12.4 In terms of the Guarantee Entity Servicing Agreement and the Guarantee Entity Administration Agreement,the Guarantee Entity appoints SBSA to render certain services related to the servicing and administration ofthe Guarantee Entity’s rights and obligations under the Common Terms Guarantee Agreement including,amongst other things, enforcing the Guarantee Entity’s rights under the relevant Borrower Indemnity and/orthe Indemnity Bond.

13. HEDGING

13.1 Home Loans held by the Issuer may yield income in accordance with a fixed rate of interest whilst a Series ofNotes may pay a floating rate of interest, or vice versa, resulting in interest rate mismatches.

13.2 The Issuer may also be exposed to basis risk in that the reset dates of the interest rates payable in respect ofits assets may be different to the reset dates of the interest payable in respect of the Notes.

13.3 In order to hedge against, amongst others, interest rate mismatches and basis risk, the Issuer will enter intoone or more hedging agreements from time to time with a Derivative Counterparty (with the Required CreditRating, if applicable) to ensure that such risks are appropriately hedged.

14. NATIONAL CREDIT ACT, 34 of 2005 (“NCA”)

In terms of the relevant provisions of the NCA (which takes effect on 1 June 2007, unless a later date is promulgatedsubsequently), the Home Loan Agreements and Related BG4 Security comprising Participating Assets sold to theIssuer will need to be reviewed on or before 1 June 2007 to ensure that the provisions contained in such Home LoanAgreements and/or Related BG4 Security comply with the requirements of the NCA. In terms of the ServicingAgreement, the Servicer has undertaken to take all such steps as may be reasonably necessary to ensure that suchHome Loan Agreements and Related BG4 Security comply with the NCA on or before 1 June 2007 (or such laterdate as may be promulgated in terms of the NCA). In addition, the NCA requires any entity granting credit, such asthe Seller and upon assignment of the Home Loan Agreements to the Issuer, the Issuer, to be registered with theNational Credit Regulator.

25

26

PRIORITY OF PAYMENTS

1. PRE-ENFORCEMENT PRIORITY OF PAYMENTS

1.1 On each Payment Date, monies standing to the credit of the Transaction Account as of the immediatelypreceding Determination Date and, to the extent that such monies are insufficient, all monies standing to thecredit of the Cash Reserve, the Arrears Reserves, the Redraw Reserve and the Purchase Reserve as of theimmediately preceding Determination Date (save that such monies shall only be applied to meet the relevantexpenses set out in the Administration Agreement), shall after making payment of or providing for amountsowing in respect of the Excluded Items, until enforcement of the Security for the Notes, be transferred fromthe Transaction Account and the Cash Reserve, the Arrears Reserves, the Redraw Reserve and the PurchaseReserve in accordance with the procedures provided for in the Administration Agreement. Such monies shallbe applied on each Payment Date in the detailed order set out in Appendix 2 to the Administration Agreement,an abridged and simplified version of which is set out below:

1.1.1 to pay or provide for (in the order set out in Appendix 2 to the Administration Agreement) seniorexpenses such as Taxes and any statutory fees, costs and expenses due and payable by the Issuer inorder to preserve the corporate existence of the Issuer; the remuneration due and payable to theSecurity SPV and/or the Security SPV Owner Trustee and to the Owner Trustee; all fees, costs,charges, liabilities and expenses (inclusive of VAT, if any) due and payable by the Issuer to third partiesand incurred without breach by the Issuer of its obligations under the Transaction Documents and notprovided for payment elsewhere and the Servicing Fee up to the Servicing Fee Cap;

1.1.2 to pay pari passu and pro rata all amounts due and payable in respect of the Class A Notes other thanin respect of principal and any net settlement amounts and Derivative Termination Amounts due andpayable to any Derivative Counterparty in accordance with the Derivative Contracts (but excluding anyDerivative Termination Amounts where the Derivative Counterparty is in default);

1.1.3 to pay or provide for in descending order of rank all amounts due and payable in respect of the Class Bto Class F Notes other than in respect of principal on such Notes, subject to an Interest Deferral Eventnot occurring;

1.1.4 subject to an Interest Deferral Event not occurring, to credit pari pasu and pro rata each of the ArrearsReserves up to the relevant portion of the Arrears Reserve Required Amount. In the event that anInterest Deferral Event occurs in respect of a Class of Notes, the Arrears Reserve in respect of suchClass of Notes will not be credited;

1.1.5 while the Class A Notes remain outstanding:

1.1.5.1 to credit the Cash Reserve up to the Cash Reserve Required Amount;

1.1.5.2 to credit the Redraw Reserve up to the Redraw Reserve Required Amount;

1.1.5.3 to fund the advance by the Issuer of Redraws up to an amount equal to the PotentialRedemption Amount less the amounts specified in the Priority of Payments;

1.1.5.4 during the Revolving Period only:

1.1.5.4.1 to fund the advance by the Issuer of Further Advances up to an amount equal to thePotential Redemption Amount less the amounts specified in the Pre-EnforcementPriority of Payments;

1.1.5.4.2 to fund the purchase by the Issuer of Additional Assets or to set aside cash for suchfunding;

1.1.5.4.3 to credit Principal Collections received and not applied in items 1.1.1 to 1.1.5.4.2above to the Purchase Reserve;

27

1.1.5.5 to redeem, in descending order of rank as to Class, the Notes equal to the greater of zero andthe difference between the Potential Redemption Amount and the sum of the amountsspecified in the Priority of Payments. Within a particular Class of Notes (and to the extentapplicable) the Notes in that particular Class will also be redeemed sequentially indescending order of rank. By way of example, the Class A Notes will be redeemedsequentially in descending order of rank so that the Class A0 Notes will be redeemed in fulland thereafter the Class A1 Notes and thereafter the Class A2 Notes and so forth;

1.1.6 if there are no Class A Notes outstanding, 1.4.4, 1.1.5.1 and 1.1.5.2 are repeated in respect of theremaining Classes of Notes in descending order of rank and the remaining Notes are redeemed indescending order of rank as set out in 1.1.5.5, provided that an amount to be applied in redeeming theClass B Notes up to an amount equal to the Principal Deficiency on such Payment Date will beallocated before the Cash Reserve and the Redraw Reserve are credited;

1.1.7 similarly, if there are no Class A and Class B Notes outstanding (and thereafter no Class C, Class DNotes and Class E Notes outstanding, respectively), 1.1.4, 1.1.5.1 and 1.1.5.2 are repeated in respectof the remaining Classes of Notes in descending order of rank and the remaining Notes are redeemedin descending order of rank as set out in 1.1.5.5, provided that an amount to be applied in redeemingin descending order of rank the remaining Notes up to an amount equal to the Principal Deficiency onsuch Interest Payment Date will be allocated before the Cash Reserve and the Redraw Reserve arecredited;

1.1.8 if a Class B Interest Deferral Event occurs on such Interest Payment Date, to pay all amounts due andpayable in respect of Class B Notes other than in respect of principal on the Class B Notes;

1.1.9 if a Class B Interest Deferral Event occurs on such Interest Payment Date, to credit the Arrears Reserve Bup to the relevant proportion of the Arrears Reserve Required Amount;

1.1.10 if an Interest Deferral Event occurs on such Interest Payment Date in respect of the Class C, to pay indescending order of rank all amounts due in respect of the Class C Notes other than in respect ofprincipal on such Notes;

1.1.11 if a Class D Interest Deferral Event occurs on such Interest Payment Date, to pay pari passu andpro rata:

1.1.11.1 all amounts due and payable in respect of the Class D Notes other than in respect of principalon the Class D Notes; and

1.1.11.2 in the event that a substitute Servicer assumes the role of Servicer, the SubordinatedServicing Fee due and payable to the substitute Servicer on such Interest Payment Date, ifany (inclusive of VAT);

1.1.12 to pay or provide for any capital amounts due and payable to the Subordinated Lender in accordancewith the provisions of the Subordinated Loan Agreements, provided that the Notes have beenredeemed in full;

1.1.13 to pay or provide for the Derivative Termination Amounts due and payable to any DerivativeCounterparty under the Derivative Contracts where the Derivative Counterparty is in Default;

1.1.14 provided that the Issuer has not exercised the Early Redemption Option to pay or provide for anyamounts, other than capital, due and payable to the Subordinated Lender in accordance with theprovisions of the Subordinated Loan Agreements in descending order of rank;

1.1.15 to pay or to provide for the dividend due and payable to the Preference Shareholder; and

1.1.16 while any amounts (whether actual or contingent) are outstanding to Secured Creditors, the surplus, ifany, to be invested in Permitted Investments and, only once all the obligations (whether contingent orotherwise) to Secured Creditors have been discharged in full, to pay the surplus, if any, to the ordinaryshareholders of the Issuer.

28

2. POST-ENFORCEMENT PRIORITY OF PAYMENTS

2.1 After the Security SPV has given notice to the Issuer pursuant to an Event of Default, declaring the Notes tobe due and payable, no Additional Assets may be purchased and no Further Advances or Redraws may beadvanced. The available funds in the Transaction Account on each Payment Date (including monies in theCash Reserve, the Arrears Reserves, the Redraw Reserve and the Purchase Reserve) will be applied on eachPayment Date in the order set out in Appendix 2 to the Administration Agreement, an abridged and simplifiedversion of which is set out below:

2.1.1 to pay or provide for senior expenses referred to in 1.1.1 above;

2.1.2 to pay or provide for any net settlement amounts and Derivative Termination Amounts due and payableto any Derivative Counterparty in accordance with the Derivative Contracts (but excluding anyDerivative Termination Amounts where the Derivative Counterparty is in default);

2.1.3 to pay or provide for interest, principal and all other amounts due and payable in respect of each of theClass A0 notes;

2.1.4 to pay or provide for interest, principal and all other amounts due and payable in respect of each of theClass A1 Notes;