-

8/9/2019 BMI Ghana Telecommunications Report Q3 2013[1]

22145049

1/91

Q3 2013www.businessmonitor.com

GHANA TELECOMMUNICATIONS REPORT

INCLUDES 5-YEAR FORECASTS TO 2017

ISSN 2041-6679Published by:Business Monitor International

-

8/9/2019 BMI Ghana Telecommunications Report Q3 2013[1]

22145049

2/91

Ghana Telecommunications

Report Q3 2013INCLUDES 5-YEAR FORECASTS TO 2017

Part of BMI’s Industry Report & Forecasts Series

Published by: Business Monitor International

Copy deadline: June 2013

Business Monitor International

Senator House

85 Queen Victoria Street

LondonEC4V 4AB

United Kingdom

Tel: +44 (0) 20 7248 0468

Fax: +44 (0) 20 7248 0467

Email: [email protected]

Web: http://www.businessmonitor.com

© 2013 Business Monitor International

All rights reserved.

All information contained in this publication iscopyrighted in

the name of Business Monitor

International, and as such no part of this

publication may be reproduced, repackaged,

redistributed, resold in whole or in any part, or used

in any form or by any means graphic, electronic or

mechanical, including photocopying, recording,

taping, or by information storage or retrieval, or by

any other means, without the express written consent

of the publisher.

DISCLAIMER

All information contained in this publication has been

researched and compiled from sources believed to be accurate and

reliable at the time of publishing. However, in view of the

natural scope for human and/or mechanical error, either at source

or during production, Business Monitor

International accepts no liability whatsoever for any loss

or damage resulting from errors, inaccuracies or omissions

affecting any part of the

publication. All information is provided without warranty, and

Business Monitor International makes no representation of

warranty of any kind as

to the accuracy or completeness of any information hereto

contained.

-

8/9/2019 BMI Ghana Telecommunications Report Q3 2013[1]

22145049

3/91

-

8/9/2019 BMI Ghana Telecommunications Report Q3 2013[1]

22145049

4/91

CONTENTS

BMI Industry View

...............................................................................................................

7

BMI Industry View . .. .. .. .. .. .. .. .. .. .. .. .. ..

.. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. ..

.. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. ..

.. .. .. .. .. .. .. .. .. 7

SWOT

....................................................................................................................................

9

Mobile . .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. ..

.. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. ..

.. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. ..

.. .. .. .. .. .. .. .. .. .. .. .. .. .. 9

SWOT

...................................................................................................................................................

11

Politics

..................................................................................................................................................

13

Economic .. ..

...........................................................................................................................................

15

Business Envir onment

..............................................................................................................................

16

Industry Forecast

..............................................................................................................

18 Mobile . .. .. .. ..

..........................................................................................................................................

18

Table: Telecoms Sector - Mobile - Historical Data & Forecast

... . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . 18

ARPU . .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. ..

.. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. ..

.. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. ..

.. .. .. .. .. .. .. .. .. .. .. .. . 20

Table: Telecoms Sector - ARPU - Historical Data & Forecast

.. .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . 20

Fixed Line

..............................................................................................................................................

21

Table: Telecoms Sector - Fixed Line - Historical Data &

Forecast .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. ..

.. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. ..

.. 21

Broadband .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. ..

.. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. ..

.. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. ..

.. .. .. .. .. .. .. .. .. .. . 22

Table: Telecoms Sector - Internet - Historical Data &

Forecast .. .. . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . 22

Industry Business Environment Overview

......................................................................

25

Sub-Saharan Africa Risk/Reward Ratings .... ........ .........

........ ........ ........ ........ ......... ........ ........

........ ......... ...... 25Table: Sub-Saharan Africa Industry

Risk/Reward Ratings, Q313 .. . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

28

Ghana Risk/Reward Ratings

......................................................................................................................

29

Market Overview

...............................................................................................................

31

Mobile . .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. ..

.. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. ..

.. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. ..

.. .. .. .. .. .. .. .. .. .. .. .. .. 31

Regional Perspective .. .. .. .. .. .. .. .. .. .. .. ..

.. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. ..

.. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. ..

.. .. .. .. .. .. .. 31

Table: Ghana Mobile Market Regional Comparison, 2012 .. ... . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . 32

Key Developments ........ ......... ........ ........ ........

......... ........ ........ ........ ........ ......... ........

........ ........ ......... ...... 32

Market Growth .. .. .. .. .. .. .. .. .. .. .. .. .. .. ..

.. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. ..

.. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. ..

.. .. .. .. .. .. .. .. 33

Table: Ghana Mobile Market ( '000) . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

33

Market Share .. .. .. .. .. .. .. .. .. .. .. .. .. .. ..

.. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. ..

.. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. ..

.. .. .. .. .. .. .. .. .. 35

Usage

..................................................................................................................................................

37

Networks .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. ..

.. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. ..

.. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. ..

.. .. .. .. .. .. .. .. .. .. .. 38

Table: Comparison Of 3G Pricing, May 2013 . . . . . . . . . . .

. . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . .. . .

. . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . .

. . . . . . .. . . . . . . . . . . . . . . . . . . 40

Content

................................................................................................................................................

41

Mobile Operator Data

............................................................................................................................

45

Table: Market Overview . . . . . . . . . . . . . . . . . .

. . .. . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . .

. . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . ..

. . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . .

. . . . . . 45

Table: MTN . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . .. . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . .

. . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . ..

. . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . .

. . . . . . . . . . 45

Table: Vodafone . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . 46

Table: Tigo . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . .. . . . . . . . . . . . . . . . . . . . . .. . . . . . . .

. . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . .

. .. . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . .

. . . . . . . . . . . . 46

Ghana Telecommunications Report Q3 2013

© Business Monitor International Page 4

-

8/9/2019 BMI Ghana Telecommunications Report Q3 2013[1]

22145049

5/91

Table: Airtel . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . 46

Table: Glo . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . 47

Table: Expresso . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . 47

Mobile Content .. .. .. .. .. .. .. .. .. .. .. .. .. ..

.. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. ..

.. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. ..

.. .. .. .. .. .. .. .. .. . 48

Non-Voice Revenue Contribution Head Into Double Digits ..

.. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. ..

.. .. .. .. .. .. .. .. .. .. .. .. .. .. .. 48

Diversity Of Services .. .. .. .. .. .. .. .. .. .. .. ..

.. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. ..

.. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. ..

.. .. .. .. .. .. .. 50

Mobile Crossovers Still In The Mix .. .. .. .. .. .. .. ..

.. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. ..

.. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. ..

.. .. 51

M2M Debuts In Africa .. .. .. .. .. .. .. .. .. .. .. ..

.. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. ..

.. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. ..

.. .. .. .. .. .. 52

Fixed Line

..............................................................................................................................................

53

Table: Ghana Fi xed-Line Market . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . 54

Broadband

.............................................................................................................................................

55

Table: Wireline Developments Table . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

60

Industry Trends And Developments

................................................................................

61

Table: Mobile Market Trends And Developments ..... . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . 62

Table: Value-Added Services Developments . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . 63

Regulatory Development

..................................................................................................

64

Regulatory Overview .. .. .. .. .. .. .. .. .. .. .. .. ..

.. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. ..

.. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. ..

.. .. .. .. .. .. .. 64

Table: Ghana's Regulatory Bodies And Their Responsibilities . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . 64

Regulatory Developments

........................................................................................................................

66

Competitive Landscape

....................................................................................................

69

Table: Key Pla yers - Ghana Telecoms Sec tor . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69

Table: Operators Financial Ind ica tors . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

69

Company Profiles

..............................................................................................................

70

Vodafone Ghana

.....................................................................................................................................

70

MTN Ghana

...........................................................................................................................................

74

Regional Overview

............................................................................................................

78

Regional Overview ... .. .. .. .. .. .. .. .. .. .. .. ..

.. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. ..

.. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. .. ..

.. .. .. .. .. .. .. .. 78

Background

..........................................................................................................................................

79

2012 Achievements ......... ........ ........ ........ .........

........ ........ ........ ......... ........ ........ ........

........ ......... ........ ..... 79

Financial Results

...................................................................................................................................

81

Table: Avanti C ommunications Group Results (GBP '000) . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . 81

Demographic Forecast

.....................................................................................................

82

Table: Ghana's Population By Age Grou p, 1990-2020 ('000) .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . 83

Table: Ghana's Population By Age Group, 1990-2020 (% of

total) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . 84

Table: Ghana's Key Population Ratios, 1990-2020 ...... . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . 85

Table: Ghana's Rural and Urban Population, 1990-2020 .. ... . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . 85

Glossary

............................................................

.................................................................

86

Table: Glossary Of Terms . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . 86

Methodology

......................................................................................................................

88

Table: Key Indicators For Telecommunications Industry Forecasts

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . 88

Telecoms Business Environment Ratings ........ ........

......... ........ ........ ........ ......... ........ ........

........ ........ ......... .. 89

Ghana Telecommunications Report Q3 2013

© Business Monitor International Page 5

-

8/9/2019 BMI Ghana Telecommunications Report Q3 2013[1]

22145049

6/91

Table: Ratings Indicators . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . 90

Table: Weighting Of Indicators . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . 91

Ghana Telecommunications Report Q3 2013

© Business Monitor International Page 6

-

8/9/2019 BMI Ghana Telecommunications Report Q3 2013[1]

22145049

7/91

BMI Industry View

BMI Industry View

BMI View: Although mobile penetration crossed the

100% mark in the end of 2012, the market continued

to show considerable growth in Q113. Increasing mobile

substitution continued to apply downward

pressure on the fixed-line connections, which showed slow

and erratic growth in the first quarter of

2013. Strong uptake of data services in Q113 support our

continued view that increased data usage will

drive growth in the telecoms sector over our forecast period to

2017. Outperformance of this sector will be

underpinned by ongoing investment in the extension of network

coverage to underserved areas, improved

submarine cable connections, which will lower prices, and

increasing availability of affordable 3G-enabled

devices.

Key Data

■ The Ghanaian mobile market grew by 3.3% q-o-q in Q113, up from

2.9% q-o-q in Q412.

■ Mobile ARPU contracted by 3.3% in Q113, reflecting continued

fierce competition as Glo Ghana enters

its second year of operation in the mobile market.

■ The fixed-line market grew by 1% in Q113, maintaining the

overall trend from 2012 of slow positive

subscriptions growth in the fixed-line sector.

Risk/ Reward Ratings

Ghana remains in fifth position on BMI's Risk/Reward ratings

table this quarter, behind Nigeria, South

Africa, Gabon and Angola, despite a five-point increase in its

industry rewards rating, due to increased

connectivity and uptake of data services. Ghana scores above the

regional average in all four of our ratings

categories.

Key Trends And Developments

Ghana's operators continue to invest in improving their networks

and broadband connectivity throughout

the country. MTN Ghana announced plans to invest around US$105mn

upgrading and expanding its

network this year. The subsidiary of MTN Group is

understood to be part of the investment that has been

reserved for a national fibre-optic cable and also for a metro

fibre cable in Kumasi, Ghana to enhance data

services. MTN Ghana will also deploy 3G base stations and roll

out 200 2G sites. Expresso, Ghana's

smallest operator, has announced plans to launch high-speed

broadband services as its link to the African

Coast to Europe (ACE) submarine cable went live in May 2013. It

is the last operator to gain access to a

Ghana Telecommunications Report Q3 2013

© Business Monitor International Page 7

-

8/9/2019 BMI Ghana Telecommunications Report Q3 2013[1]

22145049

8/91

submarine cable, and it will use its improved competitive

position to try and boost its market share, which

was less than 1% in March 2013.

These developments are paralleled by strong growth in the data

sector, according to results on the mobile

data market for Q113 published by the National Communication

Authority (NCA). The data showed

that 34.5% of mobile subscribers also use data services, and

MTN has the lion's share of the market with

65%. The rest of the data market is split between Tigo, with a

14% share; Airtel with 10%; Vodafone with

7%; Glo with 3%; and finally Expresso with a 1% share.

Ghana Telecommunications Report Q3 2013

© Business Monitor International Page 8

-

8/9/2019 BMI Ghana Telecommunications Report Q3 2013[1]

22145049

9/91

SWOT

Mobile

SWOT Analysis

Strengths ■ Relatively strong subscriber growth

continues, despite penetration having surpassed

the 100% mark at the end of 2012.

■ Regulatory regime is widely praised for its licensing

procedure and clarity.

■

Vibrant competition, with six active mobile networks.

■ Sector plays host to several major international players,

including South Africa's MTN,

India's Bharti Airtel, Luxembourg's Millicom and

Vodafone of the UK.

Weaknesses ■ MTN still overly dominant in the market,

with a voice market share of more than 45%

a data market share of 65% at the end of March 2013.

■ The sector continues to suffer from quality of service

issues.

■ Market remains skewered towards lower spending prepaid users;

this contributes to

low levels of ARPU.

■ Although ARPU has appeared fairly steady, and not as low

as some markets in Africa,

it is still low and continues to experience downward pressure as

new operators vie to

gain market share.

■ Price competition among operators in the prepaid sector could

encourage further

growth of the prepaid market leading to lower ARPUs

Opportunities ■

There is considerable scope for expanding networks into

underserved parts of thecountry while, at the same time, improving

the resilience of existing infrastructure.

■ As all operators have now have access to one or more

submarine cables, there are

many more opportunities to offer advanced data services.

■ Ghana has a potentially large market for value-added services

(VAS), if operators can

find the right way to tap it. Recent service launches by MTN,

Airtel and Vodafone have

introduced mobile commerce and payments services to the

country.

Ghana Telecommunications Report Q3 2013

© Business Monitor International Page 9

-

8/9/2019 BMI Ghana Telecommunications Report Q3 2013[1]

22145049

10/91

SWOT Analysis - Continued

Threats ■ The commercial launch of sixth operator

Globacom in April 2012 has increased

downward pressure on mobile ARPU.

■ Although it can be beneficial for subscribers, new

competition increases the

possibility of a price war, which can damage operators in the

long run.

■ The growth of the larger GSM operators could continue to

threaten the survival of

smaller operator Expresso Telecom (Kasapa).

Ghana Telecommunications Report Q3 2013

© Business Monitor International Page 10

-

8/9/2019 BMI Ghana Telecommunications Report Q3 2013[1]

22145049

11/91

SWOT

SWOT Analysis

Strengths ■ Ghana has adopted a universal licensing

scheme, which effectively means that all

those licensed to offer mobile services and mobile

infrastructure can also move into

the fixed-line sector. This is likely to encourage investment,

especially in the fixed-

wireless segment.

■ Limited competition exists in the fixed-line sector, with

Airtel holding some small

fixed-line assets.

■ Competition exists in the internet access sector, where there

are many licensed ISPs,

although only a handful of them are believed to be active.

■ The presence of Vodafone as a major international investor in

the fixed-line market is

a plus. Vodafone has been doubted in the fixed-line sector so it

is making great

efforts to prove itself.

Weaknesses ■ Fixed-line infrastructure is very

limited.

■ Because mobile services have taken off so markedly, growth in

the fixed-line sector

has recently stagnated.

■ Internet usage levels remain relatively low with penetration

estimated at 17.8% at the

end of 2012.

■ Broadband services are still a long way beyond the means of

most ordinary people;

penetration is estimated at just 1.4% at the end of 2012.

■

Ghana Telecom's National Communications Backbone Company has a

monopolyover the provision of national bandwidth.

■ The incumbent's monopoly over fixed network infrastructure

limits the prospects of

investments in fixed next generation access networks.

Opportunities ■ Potential to issue additional licences

for the construction of competing national

infrastructures; this would help to undermine the monopoly of

NCBC and the

potentially harmful effects of having limited competition.

Ghana Telecommunications Report Q3 2013

© Business Monitor International Page 11

-

8/9/2019 BMI Ghana Telecommunications Report Q3 2013[1]

22145049

12/91

SWOT Analysis - Continued

■ The focus of much of the recent fixed-line investment has been

on providing public

services so that more people will start to have access to

communications services

through facilities like phone booths.

■ The award of broadband wireless access (BWA) licences offer

significant

opportunities for expansion for voice and broadband internet

services.

■ New live connections to submarine cables have increased

Ghana's total broadband

capacity to 12.12Tbps; this will bring down prices, which should

in turn help the

growth in the number of broadband subscriptions.

Threats ■ The growth of mobile broadband services could

negatively affect the growth of fixed

broadband services such as ADSL and WiMAX.

■ Short- to medium-term danger that broadband prices may not

fall far enough to make

such services accessible to ordinary Ghanaians.

■ Increased incidence of cable cuts threatens fixed network

expansion to across the

country.

Ghana Telecommunications Report Q3 2013

© Business Monitor International Page 12

-

8/9/2019 BMI Ghana Telecommunications Report Q3 2013[1]

22145049

13/91

Politics

SWOT Analysis

Strengths ■ Ghana is widely regarded as a rapidly

maturing African democracy, with peaceful

elections and transitions of power since the multi-party system

was introduced in

1992.

■ The constitution prevents undue power concentration in any one

ethnic or religious

group.

■ A free media climate has stimulated open and lively

debate and aided the

democratisation process.

■ Relatively strong ethnic cohesion, in large part due to the

tradition of secondary

boarding schools that mix children from all ethnic groups, has

helped keep tensions -

common elsewhere in Africa - at bay.

■ Ghana's participation in many peacekeeping missions across the

continent has

bolstered its image as a pan-African role model.

■ Ghanaians residing abroad are likely to inject a fresh

external dynamic to domestic

politics, after the passage of the Representation of the

People's Amendment Bill,

giving them the right to vote in national elections.

Weaknesses ■ Corruption is still a concern, both in the

private and public arena.

■ The institutional architecture remains relatively weak,

impeding the effective execution

of policy.

■ Intra- and inter-party squabbling is common and is an

impediment to constructive

debate.

Opportunities ■ Oil revenues could be used by the

authorities to redistribute wealth among the

populace.

■ Ghana could strengthen its institutional structures and

accelerate the decentralisation

of power.

Ghana Telecommunications Report Q3 2013

© Business Monitor International Page 13

-

8/9/2019 BMI Ghana Telecommunications Report Q3 2013[1]

22145049

14/91

SWOT Analysis - Continued

■ Greater stimulus for a civil society, with more intense

monitoring of incumbents also

adding to greater transparency.

Threats ■ There could be potential spillover effects

(such as refugee inflows) from neighbouring

Côte d'Ivoire in instability erupts again.

■ Rife poverty and health problems (HIV/AIDS and ongoing

problems such as the

waterborne Guinea worm disease) remain a threat.

■ An inability to close the developmental rift between the

north and the south (urban

and rural areas) could lead to heightened tensions.

Ghana Telecommunications Report Q3 2013

© Business Monitor International Page 14

-

8/9/2019 BMI Ghana Telecommunications Report Q3 2013[1]

22145049

15/91

Economic

SWOT Analysis

Strengths ■ Ghana's natural resource riches are a boon in

times of elevated commodity prices,

and there is scope to ramp up output further.

■ Multilateral debt relief has reduced Ghana's external

liabilities significantly, freeing up

erstwhile debt servicing funds for pro-poor spending and

deepened developmental

efforts.

Weaknesses ■ An overwhelming dependence on the

agricultural sector makes the country vulnerable

to unpredictable weather forces.

■ The large informal sector eludes the government coffers'

official statistics.

■ Ghana's narrow export portfolio, predominantly cocoa, oil and

gold, exposes the

country to the vagaries of the commodity markets.

■ Heavy reliance on donor funds and poor revenue collection

capacity are a strain on

government finances.

Opportunities ■ A more aggressive pursuit of

structural reforms and further consolidation of

macroeconomic stability would help Ghana.

■ Domestic oil production should reduce reliance on oil imports

over the long term.

■ The country's tourism potential could be tapped more

aggressively.

■ Deepening the domestic capital markets - through the issuance

of longer-dated

government bonds, for example - would facilitate private-sector

access to credit.

Threats ■ Excessive government spending in 2012 derailed

the drive towards fiscal

consolidation and led to the accumulation of a costly debt

burden.

■ Any halt in aid inflows or the drying up of remittances

from the Ghanaian Diaspora

would dent the outlook for the economy.

Ghana Telecommunications Report Q3 2013

© Business Monitor International Page 15

-

8/9/2019 BMI Ghana Telecommunications Report Q3 2013[1]

22145049

16/91

Business Environment

SWOT Analysis

Strengths ■ The absence of deep domestic tensions and

political stability in an otherwise volatile

region means that the security risks are comparatively

subdued.

■ The authorities have shown a commitment to offering better

protection of intellectual

property rights.

■ A proactive reform drive, reflecting the pro-business

ethos of the current

administration, has reduced red tape.

■ Ghana is a member of the Economic Community of West African

States, with a

market of some 250mn people.

Weaknesses ■ Corruption remains a problem, as reflected

in Ghana's ranking in Transparency

International's 2012 Corruption Perceptions Index (64th out of

176 countries).

■ While constitutionally independent, the judiciary remains

inefficient, which is reflected

by the interest in alternative dispute resolution avenues.

■ Rudimentary infrastructure, still relatively poor information

and communication

technology penetration, and a fickle energy supply pose

difficulties.

■ Bureaucratic obstacles and red tape still impede business

activity.

■ The labour market is broadly unskilled and relatively

inflexible.

Opportunities ■ Consolidating the independence and

integrity of the judiciary would enhance the

effectiveness of the court system.

■ Shoring up the domestic banking sector further would bring the

broader financial

sector in line with international best practices.

■ Enhancing communications infrastructure would give wider

access to information

technology and accelerate the spread of mobile telephony.

■ Mitigating energy shortages would aid business activity.

Ghana Telecommunications Report Q3 2013

© Business Monitor International Page 16

-

8/9/2019 BMI Ghana Telecommunications Report Q3 2013[1]

22145049

17/91

SWOT Analysis - Continued

Threats ■ There is a risk of tax rises to prop up

government revenue streams given the

perennially weak fiscal position.

■ A resurgence of macroeconomic instability could raise

the cost of borrowing.

Ghana Telecommunications Report Q3 2013

© Business Monitor International Page 17

-

8/9/2019 BMI Ghana Telecommunications Report Q3 2013[1]

22145049

18/91

Industry Forecast

Mobile

Table: Telecoms Sector - Mobile - Historical Data &

Forecast

2010 2011 2012 2013f 2014f 2015f 2016f 2017f

No. of mobile phone subscribers ('000) 17,437 21,166 25,618

28,820 31,299 32,832 33,850 34,730

No. of mobile phone subscribers/100 fixed linesubscribers 6,275

7,434 8,989 10,309 11,252 11,791 12,072 12,325

No. of mobile phone subscribers/100inhabitants 71.5 84.8 100.3

110.3 117.1 120.2 121.3 121.8

No. of 3G phone subscribers ('000) 346 680 1,250 2,063 2,995

4,183 5,448 6,750

3G market as % of entire mobile market 2.0 3.2 4.9 7.2 9.6 12.7

16.1 19.4

f = BMI forecast. Source: BMI

The Ghanaian mobile market grew by 3.3% q-o-q in

Q113, with 844,000 net additions, to reach

26.462mn subscribers, according to regulatory data.

This was a continuation of the impressive growth

recorded in 2011 and 2012, and slightly better than

2.9% q-o-q growth in Q412. The market finished

Q113 with a penetration rate of 101.3%, up from

84.8% in March 2012 and 100.3% last quarter.

Although we expect there is still a fair amount of

growth potential in the Ghanaian market, the pace of

growth has slowed down in the last two quarters

since the market reached the 100% penetration mark.

The market continues to be boosted by promotional

activities, a trend observed throughout 2011 and

2012. BMI notes that the country's operators

adopted this strategy to encourage existing and new

subscribers to register their lines during the mandatory SIM

registration exercise. We expect promotional

activities to continue in 2013 and beyond, largely driven by an

increase in competition in the mobile market

following the launch of commercial voice and data services by

sixth licensee Globacom Ghana in April

Industry Forecast - Mobile

2010-2017

No. of mobile phone subscribers ('000) (LHS)

No. of 3G & 4G phone subscribers ('000) (LHS)No. of mobile

phone subscribers/100 inhabitants (RHS)

2 0 1 0

2 0 1 1

2 0 1 2

2 0 1 3 f

2 0 1 4 f

2 0 1 5 f

2 0 1 6 f

2 0 1 7 f

0

20,000

40,000

100

75

f = BMI forecast. Source: BMI

Ghana Telecommunications Report Q3 2013

© Business Monitor International Page 18

-

8/9/2019 BMI Ghana Telecommunications Report Q3 2013[1]

22145049

19/91

2012, and Expresso's connection to the ACE submarine cable in

May 2013. We expect these developments

to increase downward pressure on mobile tariffs, especially with

the market penetration rate now above the

100% mark.

Our mobile forecast remains unchanged since last quarter and

envisages growth to slow down significantly

in 2013 compared to the two previous years. Our view is based on

the likelihood of inactive SIM

discounting considering that Ghana has fully implemented the

mandatory SIM registration exercise and will

require operators disconnect inactive SIMs on a regular basis.

We expect the number of mobile subscribers

to reach 28.8mn by the end of 2013 and 34.7mn by 2017. We also

forecast the mobile penetration rate to

rise from 100.3% in 2012 to around 122% by 2017.

Ghana's 3G market is becoming increasingly competitive with five

of the country's mobile operators -

MTN, Vodafone, Airtel, Tigo and Expresso - investing

considerable resources to upgrade and expand their

3G networks during 2012. We believe this move is partly driven

by the rising demand for broadband

services, especially over mobile networks, and the arrival of

Globacom, which claims to have built the

country's biggest and fastest mobile data network for its

operations.

We expect the arrival of submarine cables Main One, WACS, GLO-1

and ACE, along with the increasing

availability of low-cost data enabled handsets, to drive the

uptake of 3G services. Although the National

Communications Authority (NCA) published figures stating there

were a total of 8.9mn data subscribers in

Ghana in March 2012, because of differing definitions,

BMI maintains its much more conservative estimate

1.25mn 3G subscribers in 2012 and 2.06mn in 2013. While the NCA

is understood to include basic 2G

mobile data users in its figures, BMI's figures only include

advanced 3G mobile phone users.

Meanwhile, limited fixed broadband infrastructure means more

users are likely to access the internet using

mobile devices and USB-based internet dongles. BMI expects

these factors to boost 3G subscriptions over

the next five years. We have not adjusted our 3G figured this

quarter, maintaining our forecast of around

6.75mn 3G subscribers in 2017, equivalent to 19.4% of the total

mobile subscriber base. We believe 3G

services will play an increasingly important role in the

competitive landscape as operators aim to diversify

revenue away from basic voice and messaging services.

Ghana Telecommunications Report Q3 2013

© Business Monitor International Page 19

-

8/9/2019 BMI Ghana Telecommunications Report Q3 2013[1]

22145049

20/91

ARPU

Table: Telecoms Sector - ARPU - Historical Data &

Forecast

2010 2011 2012 2013f 2014f 2015f 2016f 2017f

Market Average ARPU(GHS) 9 7.6 6.0 5.5 5.3 5.1 5.1 5.1

MTN (GHS) 10.1 9.8 7.8 7.1 6.7 6.4 6.3 6.2

f = BMI forecast. Source: BMI

The BMI ARPU forecast is based on the weightedaverage of

monthly ARPUs published by mobile

operators. In Ghana, MTN Ghana is the only

operator that publishes regular updates of its ARPU

figures. The latest available ARPU figures for Airtel

Ghana and Tigo Ghana relate to December 2009

and December 2010 respectively. Our overall ARPU

forecast is therefore based on actual ARPU data

from MTN and estimates for the other operator

based on their historical ARPU data. There are no

available ARPU figures for Vodafone Ghana,

Globacom and Expresso.

Using the latest data from MTN, BMI calculates

monthly blended ARPU in Ghana's mobile market

was GHS6 at the end of December 2012, from

GHS7.6 at the end of 2011. Competition in Ghana's

mobile market intensified in April 2012 with the launch of

commercial operations by the country's sixth

network operator Globacom. This accelerated ARPU erosion in the

country, which has been driven in the

last few years by price competition and promotional offers.

MTN reported ARPU of US$5.9 in Q113, down slightly from US$6.1

at the end of Q412. MTN's

continuing decline in ARPU levels coincides with our forecast

for 2013. . BMI believes MTN has the

highest ARPU rate in Ghana partly because of its wide range of

value-added services, including mobile

payments. We expect its main rivals to expand their VAS

portfolio to drive revenue growth amid declining

Industry Forecast - ARPU (GHS)

2010-2017

2 0 1 0

2 0 1 1

2 0 1 2

2 0 1 3 f

2 0 1 4 f

2 0 1 5 f

2 0 1 6 f

2 0 1 7 f

0

2.5

5

7.5

10

f = BMI forecast. Source: BMI

Ghana Telecommunications Report Q3 2013

© Business Monitor International Page 20

-

8/9/2019 BMI Ghana Telecommunications Report Q3 2013[1]

22145049

21/91

voice revenue. Although such higher value services could help

stabilise ARPU, we caution that the possible

launch of commercial services by the sixth licence holder

Globacom, poses downside risk to mobile ARPU

growth in Ghana. We expect overall monthly blended ARPU to reach

GHS5.1 by 2015 and to remain

constant between then and 2017.

Fixed Line

Table: Telecoms Sector - Fixed Line - Historical Data &

Forecast

2010 2011 2012 2013f 2014f 2015f 2016f 2017f

No. of main telephone lines ('000) 277.9 284.7 285.0 279.6 278.2

278.4 280.4 281.8

No. of main telephone lines/100

inhabitants 1.1 1.1 1.1 1.1 1.0 1.0 1.0 1.0

f = BMI forecast. Source: BMI

Ghana's fixed-line market grew by 1% q-o-q in

Q113 reaching a total of 287,909 subscribers,

according to data from the National

Communications Authority (NCA). Although this

was slower than the 3.7% q-o-q in Q412, it is in line

with 0.9% y-o-y growth at the end of December

2012 and a good performance in view of continued

downward pressure on fixed-line subscriptions,

especially from fixed-to-mobile substitution. We

retain our view of declining fixed-line connections

over our forecast period, through to 2017, as demand

wanes over strong mobile voice and data uptick and

limited investment in network infrastructure

development.

Ghana's fixed-line penetration was 1.1% at the end

of March 2013, unchanged from December 2012 and

December 2011, when there were 284,981 and 284,721 active

fixed-lines in the country. The market's

growth of just 0.9% in 2012, compared to growth of 2.4% during

2011 and 3.9% in 2010, is in line with our

view that sustained growth is not likely. Meanwhile, subscriber

numbers have continued to fluctuate in the

Industry Forecast - Fixed Line

2010-2017

No. of main telephone lines in service ('000) (LHS)

No. of main telephone lines/100 Inhabitants (RHS)

2 0 1 0

2 0 1 1

2 0 1 2

2 0 1 3 f

2 0 1 4 f

2 0 1 5 f

2 0 1 6 f

2 0 1 7 f

0

100

200

300

0.5

0.75

1

1.25

1.5

f = BMI forecast. Source: BMI

Ghana Telecommunications Report Q3 2013

© Business Monitor International Page 21

-

8/9/2019 BMI Ghana Telecommunications Report Q3 2013[1]

22145049

22/91

first three months of 2013, making it difficult to identify a

growth pattern and forecast future

performance. Despite a small amount of growth in Q113, we

maintain our expectation that the market will

decline in 2013 and largely remain flat over our forecast

period. By 2017 we expect 281,800 subscribers,

equivalent to a penetration rate of around 1.0%.

We once again emphasise that we are cautious when forecasting

the way in which Ghana's fixed-line market

will develop, considering the continued fluctuation in

subscriber figures, for which the regulator and

operators have not provided any explanations. Over the next few

years, we expect the fixed-line sector to

continue to largely remain flat. It should be remembered that

because mobile telephony is becoming a mass

market commodity, there is an increased likelihood that mobile

substitution will become a stronger force for

Ghana's fixed-line market to contend with.

BMI believes the continued growth of Ghana's fixed-line

sector over the next few years will depend on

multiple factors. These include the extent to which

Vodafone Ghana can move forward with more of its

modernisation plan. Continued growth will also depend on whether

the market sees the arrival of new

competition and the deployment of new fixed-wireless

technologies. Meanwhile, we expect operators to

focus on business customers in the future to take advantage of

the growing demand for corporate telecoms

services in Ghana.

Broadband

Table: Telecoms Sector - Internet - Historical Data &

Forecast

2010 2011 2012 2013f 2014f 2015f 2016f 2017f

No. of internet users ('000) 2,032 3,251 4,550 5,556 6,400 7,083

7,713 7,986

No. of internet users/100 inhabitants 8.3 13 17.8 21.3 24.0 25.9

27.6 28.0

No. of broadband internet subscribers ('000) 107 250 350 509 707

908 1,136 1,384

No. of broadband internet subscribers/100inhabitants 0.4 1.0 1.4

1.9 2.6 3.3 4.1 4.9

f = BMI forecast. Source: BMI

Ghana Telecommunications Report Q3 2013

© Business Monitor International Page 22

-

8/9/2019 BMI Ghana Telecommunications Report Q3 2013[1]

22145049

23/91

Ghana's internet sector has significant growth

potential in view of the growing demand for

advanced data services in the country. At the time of

writing, there were no new data available on the

broadband sector. By the end of 2012, the sector had

largely underperformed the mobile sector, with

broadband penetration at just 1.4% compared to

mobile penetration of 100.3%. We have highlighted

some of the factors limiting the sector in our

previous reports, including lack of competition in the

wireline sector and very expensive international

bandwidth. However, Ghana's connections to

international bandwidth on submarine cable systems

have improved drastically since 2011, which we

believe bodes well for the uptake of broadband

services over our forecast period, ending in 2017.

We have not changed our forecast since Q213, and maintain our

expectation that there will be around 5.6mn

regular internet users at the end of 2013, a penetration rate of

21.3%. This is based on the increasing use of

mobile access technologies, and continued intense competition in

the mobile sector as the sixth mobile

licensee Glo Ghana began its second year of business and

Expresso's connection to the African Coast to

Europe (ACE) submarine cable went live in Q213. By the end of

2017, we expect the number of internet

users to have risen to 8mn, or 28% of the population.

Based on our estimates, the broadband sector grew by more than

130% during 2011. We attribute this

growth, albeit from a low base, to increasing competition in the

internet sector. However, the low

broadband penetration rate implies that most of the country's

internet users access the internet using public

sites, including offices, schools and internet cafes.

We believe the prospects exist for strong broadband user growth

over the next few years. In addition to

internet cafés, we expect the imminent arrival of many low cost

smartphones options on the African market

to drive growth of internet access through wireless broadband

networks. Meanwhile, the Ghanaian

government is pushing ahead with a computerisation programme,

which could see around 560,000 laptops

distributed to schools and research institutions by the end of

2013. We also expect this to boost the take-up

Industry Forecast - Internet

2010-2017

No. of internet users ('000) (LHS)

No. of broadband internet subscribers ('000) (LHS)

No. of broadband internet subscribers/100 inhabitants (RHS)

2 0 1 0

2 0 1 1

2 0 1 2

2 0 1 3 f

2 0 1 4 f

2 0 1 5 f

2 0 1 6 f

2 0 1 7 f

0

5,000

10,000

0

2.5

5

7.5

f = BMI forecast. Source: BMI

Ghana Telecommunications Report Q3 2013

© Business Monitor International Page 23

-

8/9/2019 BMI Ghana Telecommunications Report Q3 2013[1]

22145049

24/91

of broadband services in the country. Our revised forecast

envisages broadband subscription of around

1.384mn by 2017, equivalent to a penetration rate of 4.9%.

Our broadband subscriber forecast takes into account the impact

which mobile broadband services are

having on the sector. Meanwhile, the spread of mobile broadband

services is also stimulating a rise in

internet usage levels. Mobile broadband services connect to the

internet wirelessly though a high-speed (3G/

HSPA) network and are accessible from a wide range of devices,

including 3G-enabled mobile phones,

netbooks, smartphones and USB sticks.

We believe operators will continue to promote their mobile

broadband services, coupled with the launch of

several undersea cables extending along the West African

coastline to gradually lower the wholesale and

retail cost of international bandwidth and fuel subscriber

growth for the remainder of our forecast period to

2017.

Ghana Telecommunications Report Q3 2013

© Business Monitor International Page 24

-

8/9/2019 BMI Ghana Telecommunications Report Q3 2013[1]

22145049

25/91

-

8/9/2019 BMI Ghana Telecommunications Report Q3 2013[1]

22145049

26/91

Angola now has the highest industry rewards score

in the region, and, by virtue of an increase to

industry risks, it moves into third place at the

expense of Gabon. Similar to Nigeria, Angola has a

low penetration of about 70%, and our outlook for

the next five years forecasts a CAGR of 22.6%. The

state's influence on the main two operators is still a

concern. However, the reduction of interest stakes

and a desire to expand LTE and broadband to

underserved areas has led BMI to upgrade its

industry risks score by 10 points.

Other countries that saw increases to industry risks

scores include Cameroon (10 points), Kenya (10),

Mauritius (10), Uganda (5) and Tanzania (5). In

Cameroon, this was due to the issuance of a third

mobile network licence to Vietnamese operator

Viettel, breaking the MTN-Orange duopoly. The duopoly has

stunted market growth, through

uncompetitive pricing and limited network coverage, so the

entrance of Viettel will add a new dynamic to

the market. In Kenya, the government has made moves to becoming

a knowledge-based economy,

launching its new ICT master plan in February 2013, the main

goal of which is to connect every Kenyan

citizen to the internet. The plan has had an immediate effect,

starting up the process of digital switchover for

terrestrial television, to be completed before the end of the

year. Smaller increases of five points were seen

in Uganda and Tanzania, the latter of which introduced

regulations aimed at improving the oversight of

mobile payment services. We believe this will instil security

and confidence in the market, as well as define

the boundaries between traditional banking sectors and mobile

payment service providers. Meanwhile, the

Ugandan regulatory authority, UCC, has been active in

encouraging network sharing to reduce costs,

resulting in a partnership for satellite broadband services

between operators Yahsat and TruIT. These

industry risk increases demonstrate the wide-range of options

available to regulators and governments to

improve competition and universal access in the market,

improving the environment for operators and

consumers.

There has been some movement at the bottom of the table, as Mali

has improved its industry rewards score

by 12.5 points, moving it up from 25th to 22nd in our rankings.

This places it ahead of Sudan and South

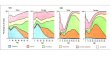

Sub-Saharan Africa ARPU

ARPU (US$), Q313

Souce: BMI

Ghana Telecommunications Report Q3 2013

© Business Monitor International Page 26

-

8/9/2019 BMI Ghana Telecommunications Report Q3 2013[1]

22145049

27/91

Sudan, both of which were unchanged in any category during the

quarter, and Ethiopia, which has increased

its industry rewards score by 2.5 as a result of the changing

forecast periods. Burundi remains rooted to the

bottom of the table, despite low penetration and a competitive

environment. Instead, low income levels, low

urbanisation and limited investment are resulting in slow

growth, and ARPUs of only US$3, one of the

lowest in the region. Mali's 12.5-point improvement allows it to

leapfrog these countries, after a quarter of

strong growth. The licensing of a third mobile operator and new

WiMAX operator in the broadband market

also helps to give the score a significant boost. However, the

ongoing conflict in the northern part of the

country and the uncertainty surrounding the outcome keep the

country risk scores low and prevent Mali

from moving up higher.

Other big gains come from Zimbabwe, with a 10-

point industry risk increase, Mozambique (7.5) and

Senegal (7.5). Proposed legislation from regulator

PORTRAZ to grant converged licences and from the

Reserve Bank of Zimbabwe (RBZ) to facilitate

mobile banking offer upside potential for the

industry, with our forecast predicting an 8.5%

CAGR until 2017. A large boost in ARPU for

Vodacom Mozambique helped improve the

market's score, as does an upcoming auction for

800MHz spectrum. Senegal outperformed

expectations throughout 2012, with Sonatel

reporting impressive annual results, resulting in

significant upgrades to our forecasts.

Tanzania, Sudan, South Sudan and Democratic

Republic of Congo (DRC), where no improvement

to industry risks was recorded, generally show

slowing growth, or have significant downside risks to their

outlooks. For example, the DRC remains the

only country not connected to the West African Cable System,

whereas South Sudan's underdeveloped

industry will continue to hamper its growth prospects. No

changes have been made to country risks or

country rewards scores, indicating that there have been no major

changes to our views. Ongoing instability

in countries such as Mali and South Sudan should ensure that

this does not persist into another quarter and

we would expect to see changes in both directions next

quarter.

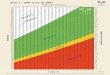

Industry And Country Risk TheDifference-Makers

Country Comparison KPIs, Q313

Source: BMI

Ghana Telecommunications Report Q3 2013

© Business Monitor International Page 27

-

8/9/2019 BMI Ghana Telecommunications Report Q3 2013[1]

22145049

28/91

Table: Sub-Saharan Africa Industry Risk/Reward Ratings, Q313

Industry Rewards

Country Rewards

Industry Risks

Country Risks

TelecomsScore Rank

PreviousRank

Nigeria 52.3 45.6 70.0 65.1 55.2 1 1

South Africa 54.6 51.6 60.0 57.5 55.1 2 2

Angola 55.0 57.3 30.0 68.2 53.8 3 4

Gabon 42.8 73.3 50.0 58.3 53.7 4 3

Ghana 45.0 53.3 70.0 56.5 52.5 5 5

Botswana 38.5 59.3 60.0 71.8 51.8 6 6

Senegal 42.5 50.0 60.0 57.6 49.2 7 8

Cote d'Ivoire 40.0 53.3 60.0 53.4 48.3 8 7

Cameroon 35.0 60.0 50.0 51.1 45.8 9 10

Rwanda 38.0 36.7 70.0 59.2 45.7 10 9

Kenya 37.5 41.7 60.0 53.7 44.3 11 12

Zambia 33.3 40.8 60.0 63.0 43.6 12 11

Mauritius 35.0 38.3 50.0 58.5 41.6 13 17

Uganda 33.3 36.7 55.0 60.8 41.5 14 15

Namibia 33.8 45.3 40.0 57.9 41.2 15 13

Tanzania 28.5 39.3 65.0 56.4 40.8 16 14

Mauritania 35.0 41.4 40.0 45.9 39.0 17 18

Mozambique 30.0 37.8 50.0 52.1 38.2 18 20

Zimbabwe 40.0 39.0 40.0 27.9 37.9 19 22

Democratic Republic of Congo 30.9 32.1 70.0 36.6 37.9 20 16

Malawi 27.0 36.7 60.0 50.7 37.9 21 19

Mali 35.0 39.0 40.0 34.8 36.7 22 25

Ethiopia 35.0 40.3 10.0 51.6 35.1 23 21

Sudan 26.1 43.7 40.0 31.7 33.3 24 23

South Sudan 27.5 47.0 20.0 40.4 33.1 25 24

Burundi 22.5 30.0 60.0 33.5 31.6 26 26

Average 36.7 45.0 51.5 52.1 43.3

Scores are weighted as follows: 'Rewards': 70%, of which

Industry Rewards 65% and Country Rewards 35%; 'Risks':30%, of which

Industry Risks 40% and Country Risks 60%. The 'Rewards' rating

evaluates the size and growth potential of a telecoms market

in any given state, and country's broader

economic/socio-demographic characteristics, which impact the

industry's development; the 'Risks' rating evaluates

industry-specific dangers and those emanating from the state's

political/economic profile. Source: BMI

Ghana Telecommunications Report Q3 2013

© Business Monitor International Page 28

-

8/9/2019 BMI Ghana Telecommunications Report Q3 2013[1]

22145049

29/91

Ghana Risk/Reward Ratings

Ghana remains in fifth position on BMI's Risk/Reward Ratings

table this quarter, despite its aggregate score

jumping to 52.5, up from 50.2 in our previous update. The

country is behind Nigeria, South Africa, Gabon

and Angola on our table, scoring above the regional average in

all four categories of our telecoms ratings.

Ghana's improved score on BMI's Risk/Reward Ratings this quarter

is due to a better score in the industry

rewards category, increasing from a score of 40.0 in the

previous quarter to a 45.0 this quarter. Ghana's

industry rewards has gone up as a result of newly released data

from the regulator showing strong uptake of

data services and a new connection to international bandwidth on

the African Coast to Europe submarine

cable. Both of these developments strengthen our optimistic

forecast for the broadband sector, to 2017,

which is based on the rapid expansion of wireless data networks,

the government's computerisationprogramme and lower cost of

international bandwidth. Moreover, though the country's mobile

penetration

rate has surpassed the 100% mark, its mobile market continues to

record strong subscriber

growth. However, these factors are counterbalanced by the

increasing downward pressure on ARPUs and,

consequently, tightening operating margins.

Ghana's relatively high country rewards score remains unchanged

since our last update, at 53.3, reflecting

its positive economic outlook. The country has a nascent oil and

gas industry, and we expect strong GDP

growth over the next few years. This will increase the rate of

urbanisation and, potentially, boost

employment and income levels in the country. These factors,

according to our country rewards

methodology, have the potential to ease the rollout of next

generation network infrastructure as well as drive

demand for high-value telecoms services.

Ghana's industry risks score remains unchanged from our previous

update. Despite having a relatively

liberalised market, and the presence of competition in it mobile

telephony, fixed-line and internet access

segments, Ghana's wireline telecoms market remains dominated by

the incumbent operator Vodafone

Ghana (formerly Ghana Telecom). Ghana's relatively strong

score in this category reflects the privatised

status of Vodafone Ghana, which has opened the door to private

investment and bodes well for the future

development of the country's infrastructure. However, Vodafone

Ghana continues to have monopoly control

over the provision of national backbone infrastructure; this is

seen by some as a problem which needs to be

overcome in order to ensure the future growth of the internet

sector. In addition to introducing competition

in the provision of national infrastructure, there is a need to

enhance the level of competition at the local

access level, not least through the licensing of new broadband

wireless access (BWA) providers. Recent

developments suggest that progress is being made in this area,

with the issuance of BWA licences.

Meanwhile, the mobile market, in terms of voice and data

services, continues to be dominated by South

Ghana Telecommunications Report Q3 2013

© Business Monitor International Page 29

-

8/9/2019 BMI Ghana Telecommunications Report Q3 2013[1]

22145049

30/91

Africa's MTN. Steps to encourage an increased level of mobile

market competition include the introduction

of mobile number portability and the development of a clearer

regulatory framework on the construction of

telecoms masts.

Ghana's country risks score, at 56.5, reflects our positive view

of the country's political and economic

environment in 2013 and beyond. Ghana successfully held

competitive and keenly contested elections in

December 2012. John Dramani Mahama of the National Democratic

Congress (NDC) emerged victorious

as the people's elected choice. The NDC also obtained a

parliamentary majority in the elections. On the

economic front, we hold a positive outlook on private

consumption growth, anticipating that the rapid

growth of key sectors, including oil and gas, infrastructure and

retail, will generate wealth and consequently

boost consumer spending. Granted, this effect will be unevenly

spread across the country, with pockets of

growth likely to develop around key projects, and the southern

area between Accra, Kumasi and Sekondi-

Takoradi (known as the 'golden triangle') is likely to be

especially prosperous. Furthermore, the high

interest rate environment and relative weakness of the cedi may

dampen demand somewhat. Nevertheless,

we expect strong growth in aggregate private consumption,

forecasting an increase of 8.0% in real terms in

2013 (contributing 5.3 percentage points (pp) to headline

growth), followed by an annual average of 6.5%

over 2014-2017.

Ghana Telecommunications Report Q3 2013

© Business Monitor International Page 30

-

8/9/2019 BMI Ghana Telecommunications Report Q3 2013[1]

22145049

31/91

Market Overview

Mobile

Regional Perspective

Ghana's mobile penetration rate reached 100% for the first time

at the end of December 2012. This gave the

country the seventh highest mobile penetration rate in the

region at the end of that period. Over our forecast

period, through to 2017, the country's mobile market is expected

to record a CAGR of around 4.6%, the

19th highest in the region. The relatively slow growth reflects

increasing market saturation as well as the

likelihood for operators to focus on high-value mobile data

services in the future to offset declining revenue

growth from traditional voice services. Ghana's 3G penetration

and ARPU were in the bottom half of our

regional table in 2012, although there has been a massive surge

in uptake of 3G services over the last year.

Regional Perspective

Mobile Penetration (LHS) And Key Market Indicators, 2013

(RHS)

f = forecast. Source: BMI

Ghana Telecommunications Report Q3 2013

© Business Monitor International Page 31

-

8/9/2019 BMI Ghana Telecommunications Report Q3 2013[1]

22145049

32/91

Table: Ghana Mobile Market Regional Comparison, 2012

GhanaSub-Saharan Africa Rank (Out of 26)

CAGR 2012-2017 (%) 6.3 7.5 15

Mobile penetration (%) 100.3 76.4 7

3G as % of entire market* (%) 4.9 8.4 14

ARPU (US$)* 4.7 7.1 14

*= Out of 21 countries. Source: BMI

Key Developments

■ Expresso announced plans to launch high-speed broadband

services as its link to the Africa Coast toEurope (ACE) submarine

cable went live in May 2013. Expresso Telecom is a partial owner of

the

17,000km-long cable, and will be solely responsible maintenance

of the cable in Ghana and Nigeria and

manage the construction, operation and maintenance of cable

landing stations in Mauritania, Senegal and

Guinea Conakry.

■ In May 2013, the National Communication Authority (NCA)

published results on mobile data market

shares for the first quarter of 2013. The data showed that 34.5%

of mobile subscribers also use data

services, and MTN has the lion's share of the market with 65%.

The rest of the data market is split

between Tigo, with a 14% share; Airtel with 10%; Vodafone with

7%; Glo with 3%; and finally

Expresso with a 1% share.

In March 2013, MTN announced plans to invest around

US$105mn in upgrading and expanding its network

in 2013. The operator is rolling out terrestrial fibre-optic

cable networks across the country to enhance data

services. MTN Ghana also plans to deploy new 3G base stations

and around 200 2G sites.

Ghana Telecommunications Report Q3 2013

© Business Monitor International Page 32

-

8/9/2019 BMI Ghana Telecommunications Report Q3 2013[1]

22145049

33/91

Market Growth

There were 26.462mn mobile subscribers in Ghanaat the end of

March 2013, according to market data

published by the National Communications

Authority (NCA). This was a growth of 3.3% q-o-q

during Q113, and a y-o-y growth rate of 22%. This

brought the country's mobile penetration rate to

101.3% at the end of March 2013. BMI believes the

strong performance over the last year, despite the

introduction of mandatory SIM registration in 2011,

was mainly due to the increase in competition in the

mobile market following the launch of commercial

services by sixth operator Globacom in April 2012.

Although Ghana's mobile penetration rate is high by

regional standards, we expect subscriber growth to

remain strong over our forecast period, through to

2017, considering the low mobile penetration rate in rural areas

where majority of the population live. BMI

notes that some operators are beginning to implement strategies

for rural roll-out to take advantage of the

significant subscriber growth opportunities in underserved

areas. An example of this is the partnership

between Tigo and Ireland-based firm Altobridge to

extend mobile services to underserved areas using the

latter's low-cost solution specifically designed for small

communities of less than 1,500 residents. The

project, which has so far recorded impressive results, is also

supported by the Ghana Investment Fund for

Electronic Communications (GIFEC), an agency of the Ministry of

Communications.

Table: Ghana Mobile Market ('000)

Q112 Q212 Q312 Q412 Q113 Y-o-Y Change

MTN 10,394 10,758 11,270 11,735 12,024 15.7

Net additions 238 364 512 465 289

Market share (%) 48 46 45.3 45.8 45.4

Vodafone 4,524 4,819 5,027 5,259 5,609 24

Net additions 248 295 208 232 350

Market share (%) 20.9 20.6 20.2 20.5 21.2

Ghana Mobile Growth

2010-2013

Source: BMI, NCA, operators

Ghana Telecommunications Report Q3 2013

© Business Monitor International Page 33

-

8/9/2019 BMI Ghana Telecommunications Report Q3 2013[1]

22145049

34/91

Ghana Mobile Market ('000) - Continued

Q112 Q212 Q312 Q412 Q113 Y-o-Y Change

Tigo 3,642 3,553 3,758 3,698 3,676 0.9

Net additions -280 -89 205 -60 -22

Market share (%) 16.8 15.2 15.1 14.4 13.9

Airtel 2,897 3,022 3,041 3,192 3,384 16.8

Net additions 271 125 19 151 192

Market share (%) 13.4 12.9 12.2 12.5 12.8

Glo na 991 1,610 1,568 1,607 100

Net additions na 991 619 -42 39

Market share (%) na 4.2 6.5 6.1 6.1

Expresso 202 227 178 166 162 -19.8

Net additions 16 25 -49 -12 -4

Market share (%) 0.9 1 0.7 0.6 0.6

Total Subscriptions 21,660 23,370 24,884 25,618 26,462 22.2

na = not applicable. Source: BMI, NCA, operators

Ghana Telecommunications Report Q3 2013

© Business Monitor International Page 34

-

8/9/2019 BMI Ghana Telecommunications Report Q3 2013[1]

22145049

35/91

Market Share

MTN continued to be Ghana's largest mobile

operator by subscribers at the end of March 2013,

with a total of 12.024mn subscribers and a market

share of 45.4%. Although the operator had a net gain

of 289,000 subscribers in the quarter, this was

significantly lower than its net gain of 465,000 in

Q412 and lower than Vodafone's net gain of

350,000 subscribers for the same quarter. Despite

showing good subscriber growth throughout 2012,

the operator's market share has been trending down

since Q310, partly because of the commercial launch

of mobile services by the sixth mobile licensee, Glo

Ghana. MTN's market share fell by 2.6pps in the 12

months to March 2013.

MTN's performance in Q412, which gave it a 63.4%

of total net additions that quarter, was remarkable considering

that the regulator had suspended the sale of

new MTN SIM cards in early December because the deteriorating

quality of service provided by the

operator. The ban lasted for the whole of December, including

the busy Christmas period, and was only

lifted in late January 2013. However, it appears the operator's

rivals failed to capitalise on this to boost their

subscriber bases. BMI calculates that the remaining five

mobile operators jointly accounted for the

remaining 36.6% of net additions in Q412.

Vodafone remained in second place in Q113, with a subscriber

base of 5.609mn. The operator recorded net

additions of 350,000 subscribers in Q113, significantly higher

than its average quarterly net additions of

246,000 in 2012. The operator's position appears to be secured

for now as its two closest rivals, Tigo and

Airtel, are not. Tigo, which Vodafone beat to second position in

Q411, recorded net losses for six out of the

seven quarters to Q113, while Airtel's subscriber acquisitions

over the past two years have been largely

inconsistent. Vodafone's market share of 21.2% at the end of

Q113 was up from 20.5% in the previous

quarter.

As mentioned above, Tigo underperformed its rivals over the two

years to December 2012. BMI calculates

that the operator's subscriber base of 3.676mn at the end of

Q113 reflects a decrease of 22,000 from the

previous quarter and 426,000 from a peak base of 4.102mn

recorded at the end of Q211. As a result, the

Market Shares

2010-2013

Source: BMI, NCA, operators

Ghana Telecommunications Report Q3 2013

© Business Monitor International Page 35

-

8/9/2019 BMI Ghana Telecommunications Report Q3 2013[1]

22145049

36/91

operator's market share fell to 13.9% at the end of Q113, from

14.4% in the previous quarter and 16.8% a

year earlier.

For its part, Airtel had 3.384mn subscribers at the end of Q113.

This was a growth of 6% q-o-q and 16.8%

y-o-y, and reflected net additions of 487,000 subscribers during

the 12 months to March 2013. Although

Airtel reported only one quarterly net loss in the two years to

Q113, its subscriber gains have been less

consistent that those of its major rivals, resulting in a fairly

flat market share since the beginning of 2012.

The operator had a market share of 12.8% at the end of Q113, up

from 12.5% in the previous quarter, but

down from 13.4% a year earlier.

The launch of Globacom's (Glo Ghana) operations in Ghana has

significantly increased competition in the

country's mobile market, in line with BMI's expectations. This

is mainly evidenced by investments in

network infrastructure development and, perhaps more worrying

for the five incumbent operators, the re-

emergence of intense price competition. Glo Ghana, owned by

Nigeria-based Globacom Limited, launched

commercial operations in April 2012, almost four years after

winning the country's sixth mobile licence in

mid-2008. BMI had predicted Glo would adopt an aggressive

marketing and pricing strategy to gain a

foothold in the market, considering the significant changes in

the market dynamics between 2008 and 2012,

including the rise in the mobile penetration rate from just

40.1% to more than 85%, the reduction of

interconnection rates and the implementation of mobile number

portability and mandatory SIM registration.

Glo's aggressive marketing strategy involved number reservation

by prospective customers many months