Embed Size (px)

Citation preview

BofAML – Global Metals, Mining & Steel ConferenceMay 2017

Victor Gobitz - CEO

Cautionary Statement

This presentation contains certain information that may constitute forward-looking information underapplicable U.S. securities legislation, including but not limited to information about costs applicable tosales, general and administrative expenses; production volumes; current expectations on the timing,extent and success of exploration; development and metallurgical sampling activities, the timing andsuccess of mining operations and the optimization of mine plans. This forward-looking informationentails various risks and uncertainties that are based on current expectations, and actual results maydiffer materially from those contained within said information. These uncertainties and risks include, butare not limited to, the strength of the global economy, the price of commodities; operational, fundingand liquidity risks; the degree to which mineral resource estimates are reflective of actual mineralresources; the degree to which factors which would make a mineral deposit commercially viable arepresent, and other risks and hazards associated with mining operations. Risks and uncertainties aboutthe Company’s business are more fully discussed in the BVN’s form 20-F filed with the Securities andExchange Commission in the U.S. and available at www.sec.gov . Readers are urged to read thesematerials. Buenaventura assumes no obligation to update any forward-looking information or to updatethe reasons why actual results could differ from such information unless required by law.

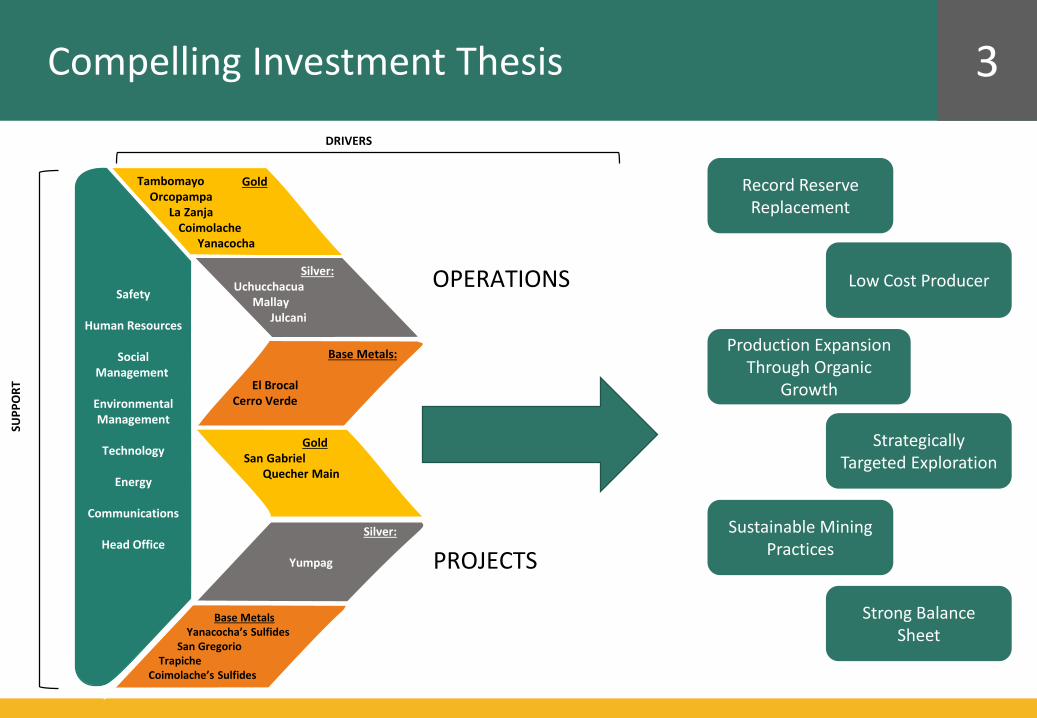

Compelling Investment Thesis 3

Record Reserve Replacement

Low Cost Producer

Production ExpansionThrough Organic

Growth

StrategicallyTargeted Exploration

Sustainable MiningPractices

Strong Balance Sheet

OPERATIONS

PROJECTS

Base Metals:

El Brocal Cerro Verde

Silver:

Yumpag

Base MetalsYanacocha’s Sulfides

San GregorioTrapiche

Coimolache’s Sulfides

SUP

PO

RT

DRIVERS

GoldSan Gabriel

Quecher Main

Safety

Human Resources

SocialManagement

EnvironmentalManagement

Technology

Energy

Communications

Head Office

TambomayoOrcopampa

La Zanja Coimolache

Yanacocha

Silver:Uchucchacua

MallayJulcani

Gold

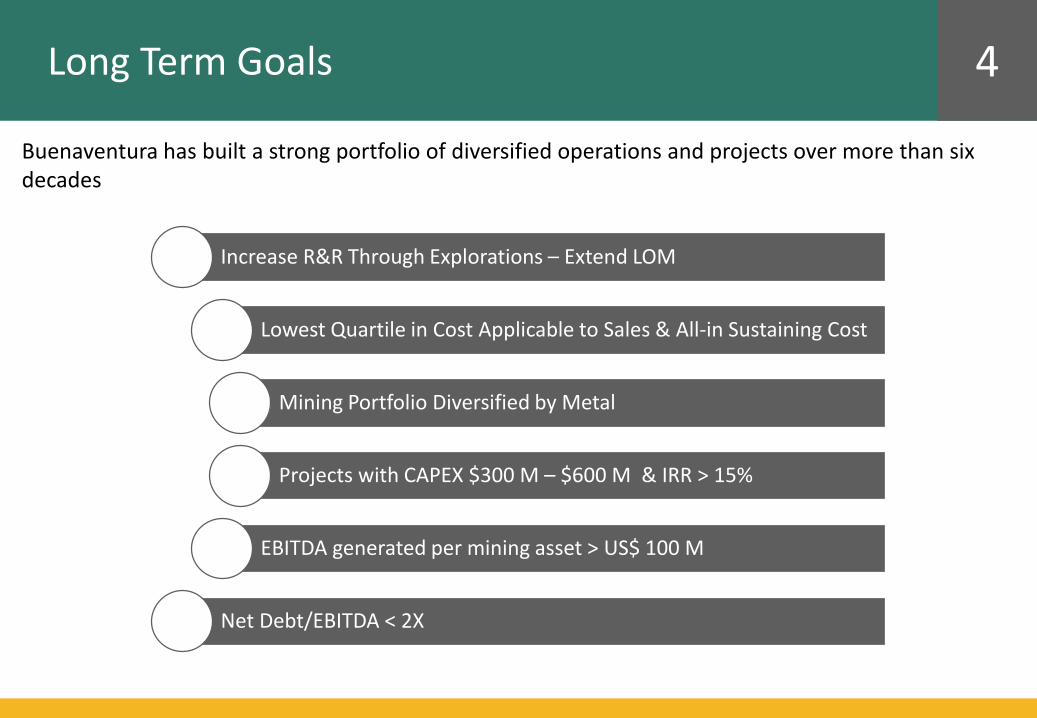

Long Term Goals 4

Increase R&R Through Explorations – Extend LOM

Lowest Quartile in Cost Applicable to Sales & All-in Sustaining Cost

Mining Portfolio Diversified by Metal

Projects with CAPEX $300 M – $600 M & IRR > 15%

EBITDA generated per mining asset > US$ 100 M

Net Debt/EBITDA < 2X

Buenaventura has built a strong portfolio of diversified operations and projects over more than six decades

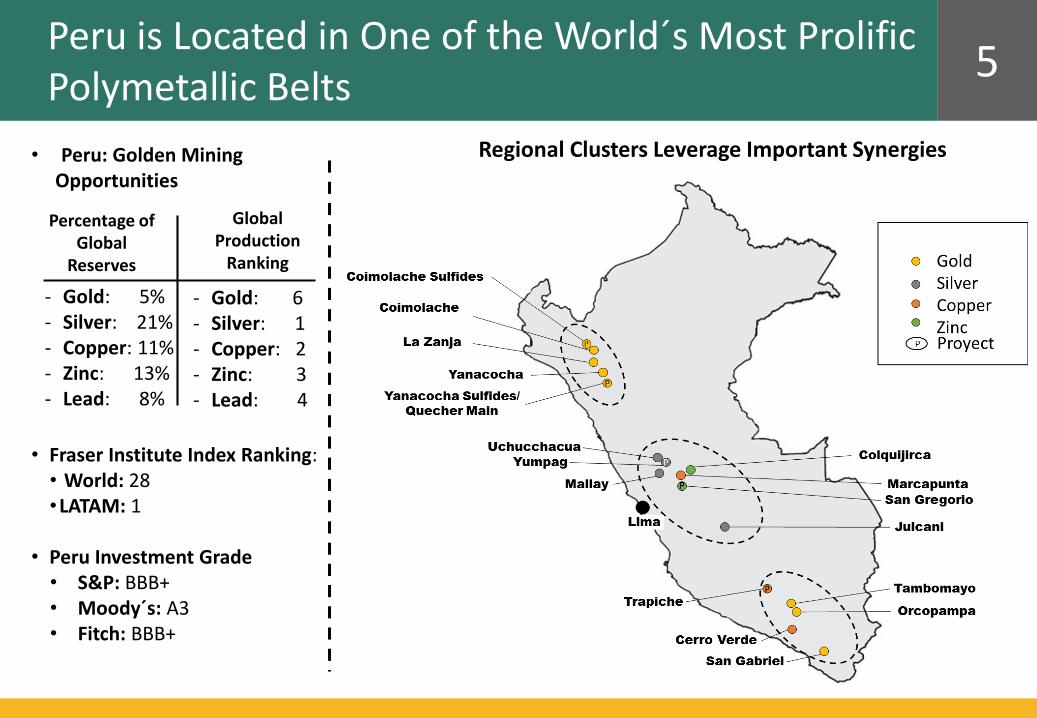

5Peru is Located in One of the World´s Most ProlificPolymetallic Belts

• Fraser Institute Index Ranking:• World: 28•LATAM: 1

• Peru Investment Grade• S&P: BBB+• Moody´s: A3• Fitch: BBB+

Regional Clusters Leverage Important Synergies• Peru: Golden Mining Opportunities

Percentage of Global

Reserves

Global Production

Ranking

‐ Gold: 6‐ Silver: 1‐ Copper: 2‐ Zinc: 3‐ Lead: 4

‐ Gold: 5%‐ Silver: 21%‐ Copper: 11%‐ Zinc: 13%‐ Lead: 8%

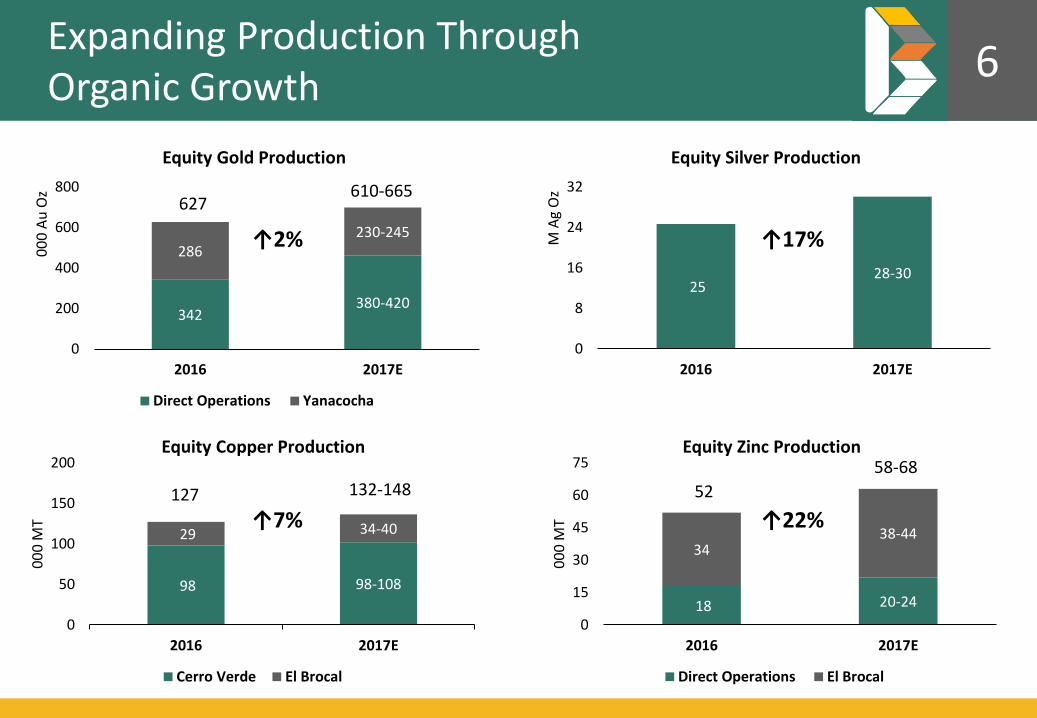

Expanding Production ThroughOrganic Growth

6

342380-420

286230-245

0

200

400

600

800

2016 2017E

00

0 A

u O

z

Equity Gold Production

Direct Operations Yanacocha

25 28-30

0

8

16

24

32

2016 2017E

M A

g O

z

Equity Silver Production

18 20-24

3438-44

0

15

30

45

60

75

2016 2017E

00

0 M

T

Equity Zinc Production

Direct Operations El Brocal

↑2% ↑17%

↑22%

610-665627

52

58-68

98 98-108

29 34-40

0

50

100

150

200

2016 2017E

00

0 M

T

Equity Copper Production

Cerro Verde El Brocal

↑7%

132-148127

Tambomayo: Our Newest Gold Mine 7

• Updated 2017 Productionguidance of 60 – 90K AuOz

• Ramp up has been extended due to a filtering process-related bottleneck

• Full capacity expected by 3Q17

Highlights:

Ownership 100%

Deposit Type Underground

Location Caylloma, Arequipa

Reserves 2.1M MT@ 0.281 OzAu (8.7g), 9.7 OzAg, 2.4% Zn, 1.2% Pb

Resources 0.64M MT@ 0.22 OzAu (6.8g), 9.11 OzAg, 2.2% Zn, 1.2% Pb

336238

141

328597

0

200

400

600

800

2014 2015 2016

00

0 A

uO

z

Reserves & Resources - LOM

Recursos Reservas

(2 years)

(4 years)

(5 years)

Resources Reserves

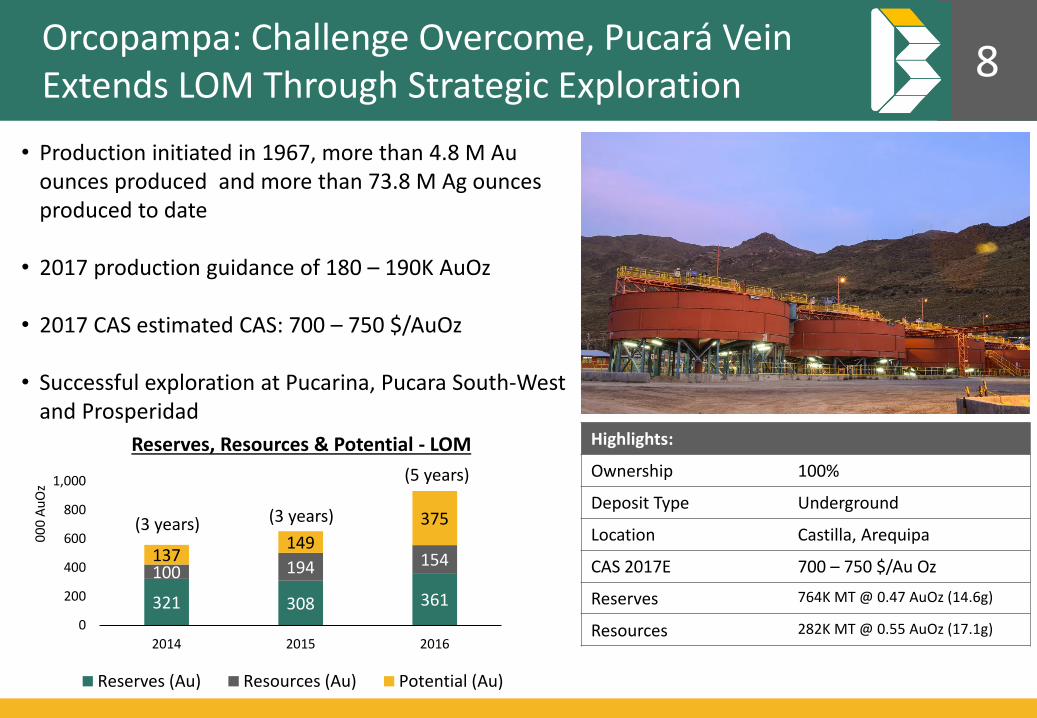

Orcopampa: Challenge Overcome, Pucará VeinExtends LOM Through Strategic Exploration

Highlights:

Ownership 100%

Deposit Type Underground

Location Castilla, Arequipa

CAS 2017E 700 – 750 $/Au Oz

Reserves 764K MT @ 0.47 AuOz (14.6g)

Resources 282K MT @ 0.55 AuOz (17.1g)

• Production initiated in 1967, more than 4.8 M Au ounces produced and more than 73.8 M Ag ouncesproduced to date

• 2017 production guidance of 180 – 190K AuOz

• 2017 CAS estimated CAS: 700 – 750 $/AuOz

• Successful exploration at Pucarina, Pucara South-West and Prosperidad

321 308 361

100 194 154137149

375

0

200

400

600

800

1,000

2014 2015 2016

00

0 A

uO

z

Reserves, Resources & Potential - LOM

Reserves (Au) Resources (Au) Potential (Au)

(3 years) (3 years)

(5 years)

8

9

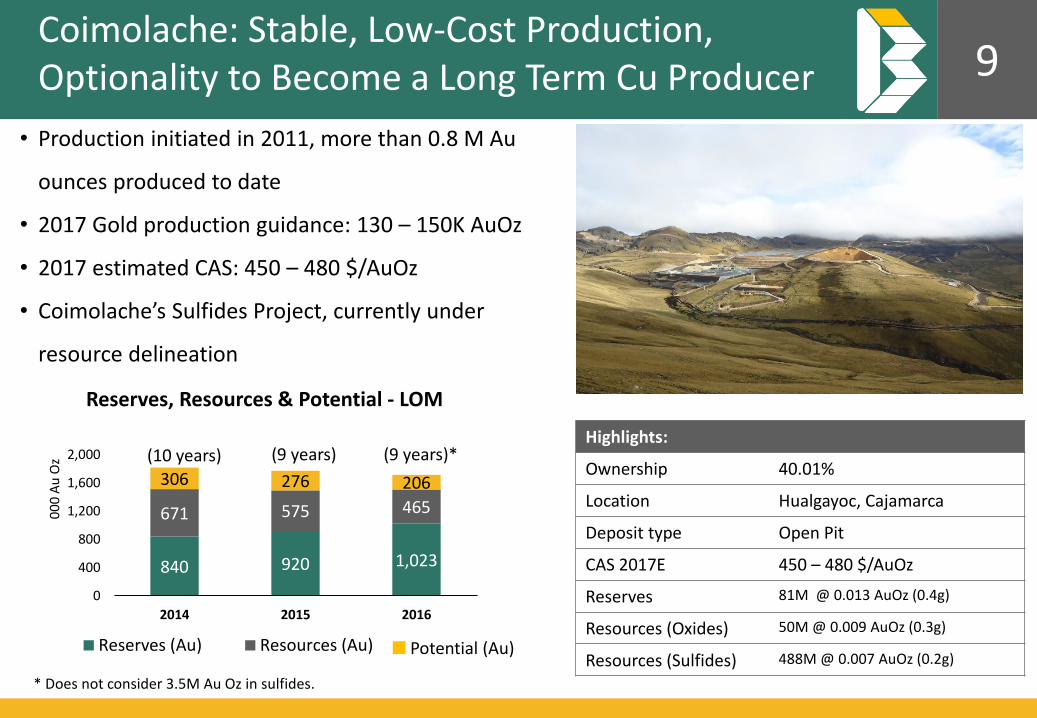

Highlights:

Ownership 40.01%

Location Hualgayoc, Cajamarca

Deposit type Open Pit

CAS 2017E 450 – 480 $/AuOz

Reserves 81M @ 0.013 AuOz (0.4g)

Resources (Oxides) 50M @ 0.009 AuOz (0.3g)

Resources (Sulfides) 488M @ 0.007 AuOz (0.2g)

• Production initiated in 2011, more than 0.8 M Au

ounces produced to date

• 2017 Gold production guidance: 130 – 150K AuOz

• 2017 estimated CAS: 450 – 480 $/AuOz

• Coimolache’s Sulfides Project, currently under

resource delineation

840 920 1,023

671 575 465

306 276 206

0

400

800

1,200

1,600

2,000

2014 2015 2016

00

0 A

u O

z

Reserves, Resources & Potential - LOM

Reserves (Au) Resources (Au)

(10 years) (9 years) (9 years)*

Potential (Au)

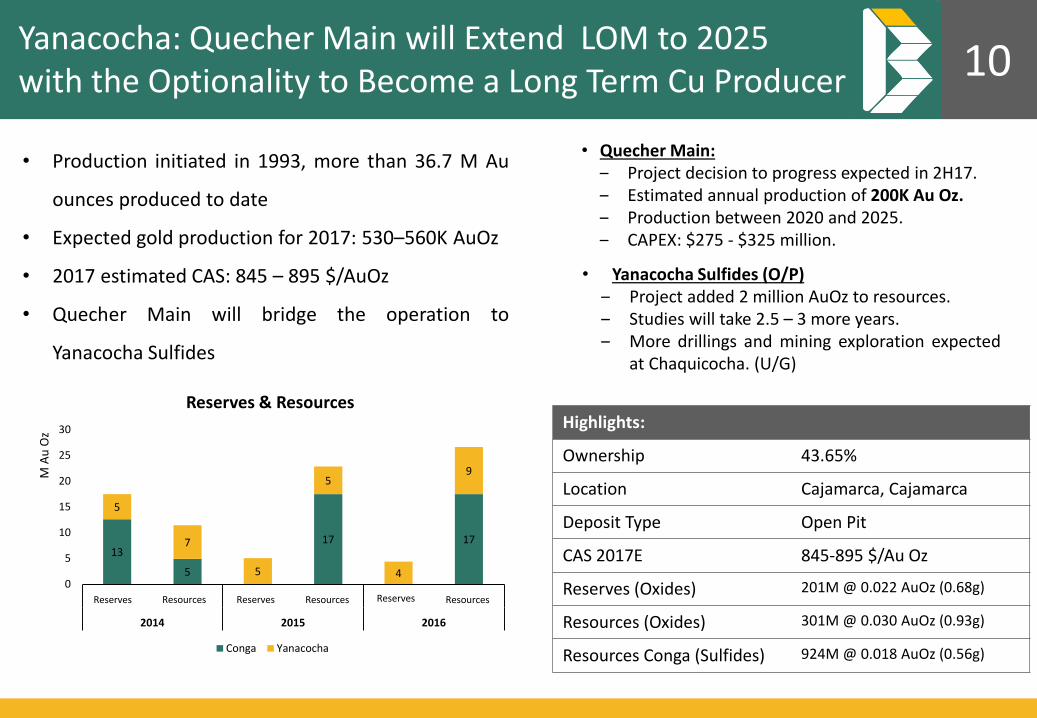

Coimolache: Stable, Low-Cost Production,Optionality to Become a Long Term Cu Producer

* Does not consider 3.5M Au Oz in sulfides.

10

Highlights:

Ownership 43.65%

Location Cajamarca, Cajamarca

Deposit Type Open Pit

CAS 2017E 845-895 $/Au Oz

Reserves (Oxides) 201M @ 0.022 AuOz (0.68g)

Resources (Oxides) 301M @ 0.030 AuOz (0.93g)

Resources Conga (Sulfides) 924M @ 0.018 AuOz (0.56g)

• Production initiated in 1993, more than 36.7 M Au

ounces produced to date

• Expected gold production for 2017: 530–560K AuOz

• 2017 estimated CAS: 845 – 895 $/AuOz

• Quecher Main will bridge the operation to

Yanacocha Sulfides

• Quecher Main:‒ Project decision to progress expected in 2H17.‒ Estimated annual production of 200K Au Oz.‒ Production between 2020 and 2025.‒ CAPEX: $275 - $325 million.

• Yanacocha Sulfides (O/P)‒ Project added 2 million AuOz to resources.‒ Studies will take 2.5 – 3 more years.‒ More drillings and mining exploration expected

at Chaquicocha. (U/G)

13

5

17 17

5

7

5

5

4

9

0

5

10

15

20

25

30

Reservas Recursos Reservas Recursos Reservas Recursos

2014 2015 2016

M A

u O

z

Reserves & Resources

Conga Yanacocha

Reserves Resources Reserves ReservesResources Resources

Yanacocha: Quecher Main will Extend LOM to 2025 with the Optionality to Become a Long Term Cu Producer

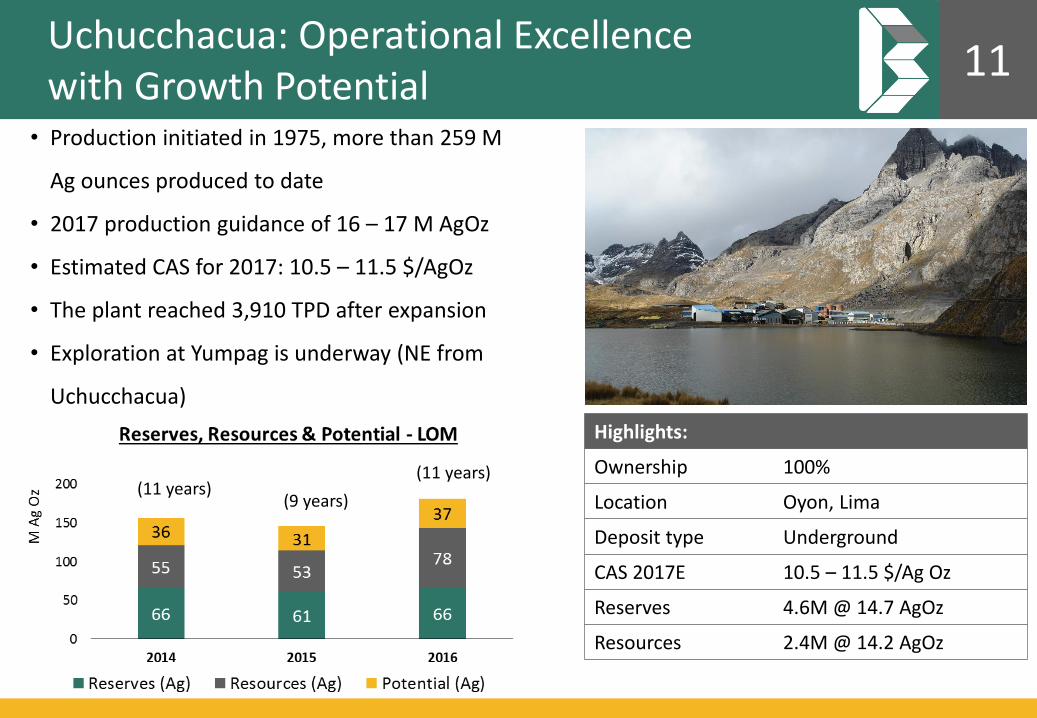

• Production initiated in 1975, more than 259 M

Ag ounces produced to date

• 2017 production guidance of 16 – 17 M AgOz

• Estimated CAS for 2017: 10.5 – 11.5 $/AgOz

• The plant reached 3,910 TPD after expansion

• Exploration at Yumpag is underway (NE from

Uchucchacua)

Uchucchacua: Operational Excellencewith Growth Potential

11

Highlights:

Ownership 100%

Location Oyon, Lima

Deposit type Underground

CAS 2017E 10.5 – 11.5 $/Ag Oz

Reserves 4.6M @ 14.7 AgOz

Resources 2.4M @ 14.2 AgOz

(11 years)(9 years)

(11 years)

12

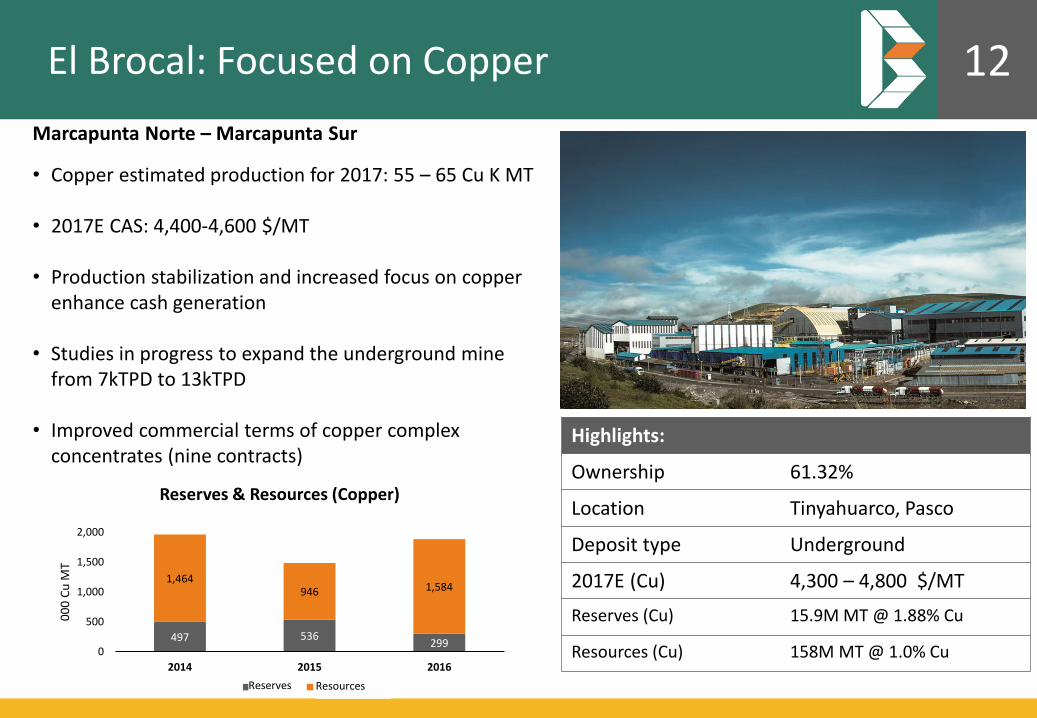

Highlights:

Ownership 61.32%

Location Tinyahuarco, Pasco

Deposit type Underground

2017E (Cu) 4,300 – 4,800 $/MT

Reserves (Cu) 15.9M MT @ 1.88% Cu

Resources (Cu) 158M MT @ 1.0% Cu

Marcapunta Norte – Marcapunta Sur

• Copper estimated production for 2017: 55 – 65 Cu K MT

• 2017E CAS: 4,400-4,600 $/MT

• Production stabilization and increased focus on copperenhance cash generation

• Studies in progress to expand the underground mine from 7kTPD to 13kTPD

• Improved commercial terms of copper complexconcentrates (nine contracts)

497 536299

1,464946 1,584

0

500

1,000

1,500

2,000

2014 2015 2016

00

0 C

u M

T

Reserves & Resources (Copper)

Reservas RecursosReserves Resources

El Brocal: Focused on Copper

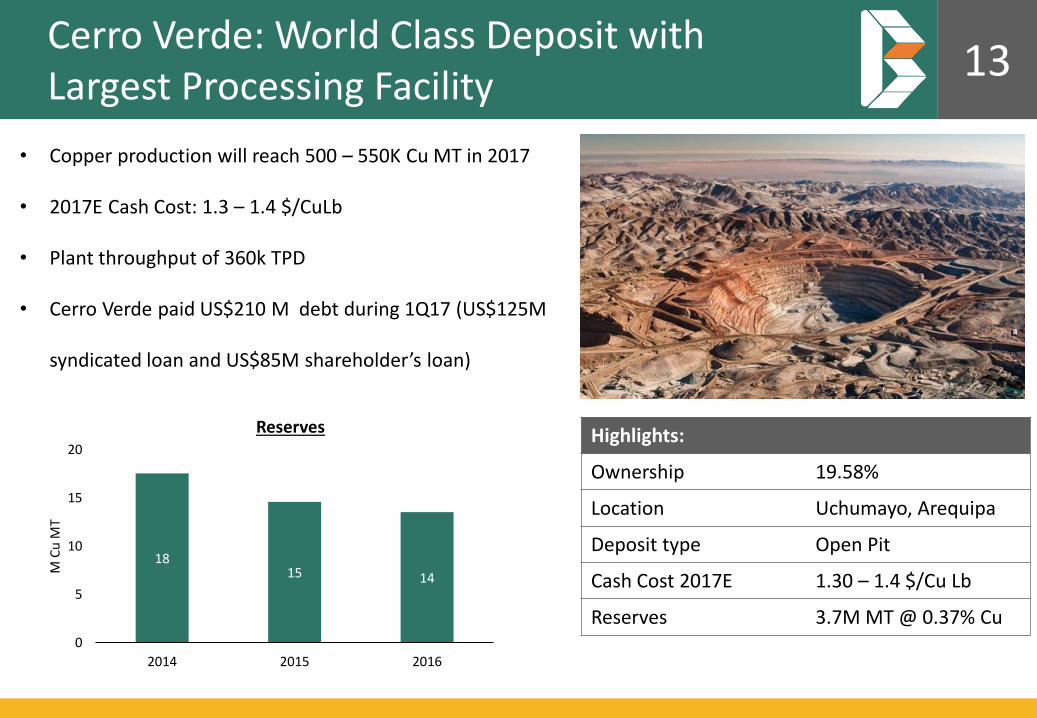

Cerro Verde: World Class Deposit withLargest Processing Facility

13

Highlights:

Ownership 19.58%

Location Uchumayo, Arequipa

Deposit type Open Pit

Cash Cost 2017E 1.30 – 1.4 $/Cu Lb

Reserves 3.7M MT @ 0.37% Cu

• Copper production will reach 500 – 550K Cu MT in 2017

• 2017E Cash Cost: 1.3 – 1.4 $/CuLb

• Plant throughput of 360k TPD

• Cerro Verde paid US$210 M debt during 1Q17 (US$125M

syndicated loan and US$85M shareholder’s loan)

1815 14

0

5

10

15

20

2014 2015 2016

M C

u M

T

Reserves

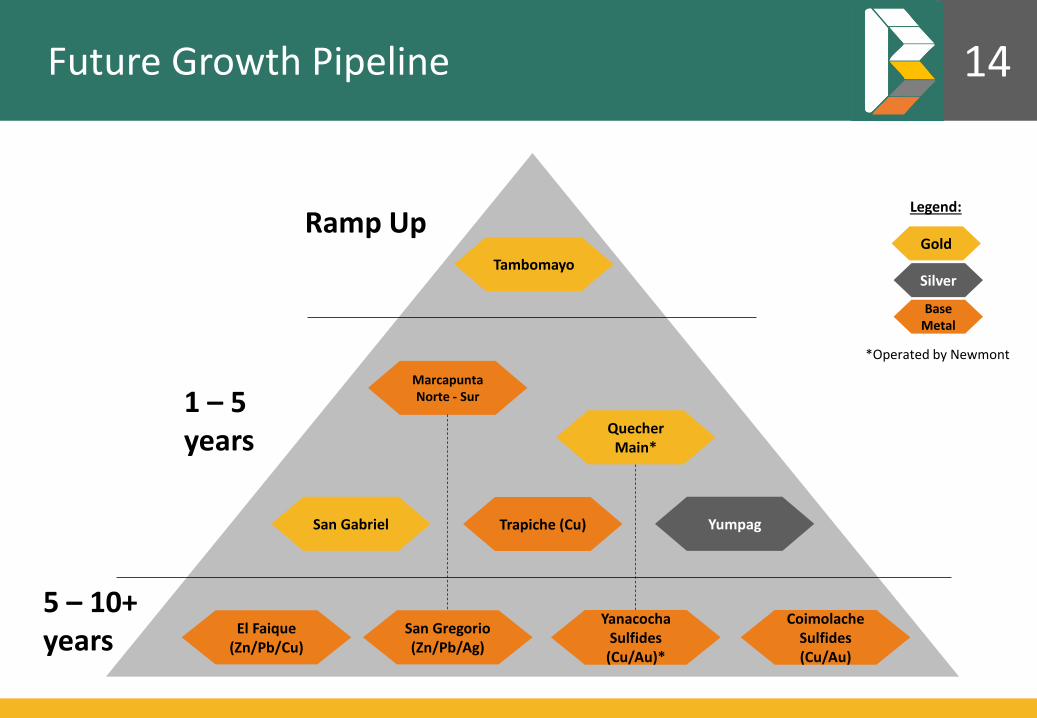

14Future Growth Pipeline

CoimolacheSulfides(Cu/Au)

YanacochaSulfides

(Cu/Au)*

Yumpag

El Faique(Zn/Pb/Cu)

San Gregorio (Zn/Pb/Ag)

San Gabriel Trapiche (Cu)

Tambomayo

Ramp Up

1 – 5years

5 – 10+years

Gold

Silver

Base Metal

*Operated by Newmont

Legend:

Quecher Main*

MarcapuntaNorte - Sur

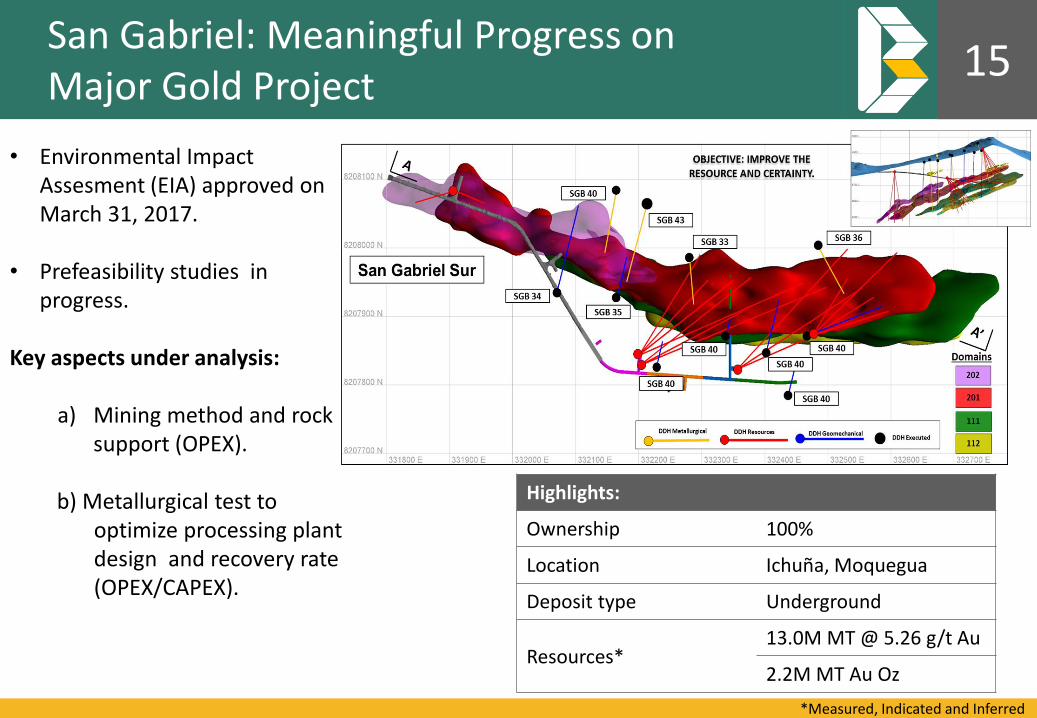

San Gabriel: Meaningful Progress onMajor Gold Project

15

Highlights:

Ownership 100%

Location Ichuña, Moquegua

Deposit type Underground

Resources*13.0M MT @ 5.26 g/t Au

2.2M MT Au Oz

• Environmental ImpactAssesment (EIA) approved onMarch 31, 2017.

• Prefeasibility studies in progress.

Key aspects under analysis:

a) Mining method and rock support (OPEX).

b) Metallurgical test to optimize processing plantdesign and recovery rate(OPEX/CAPEX).

*Measured, Indicated and Inferred

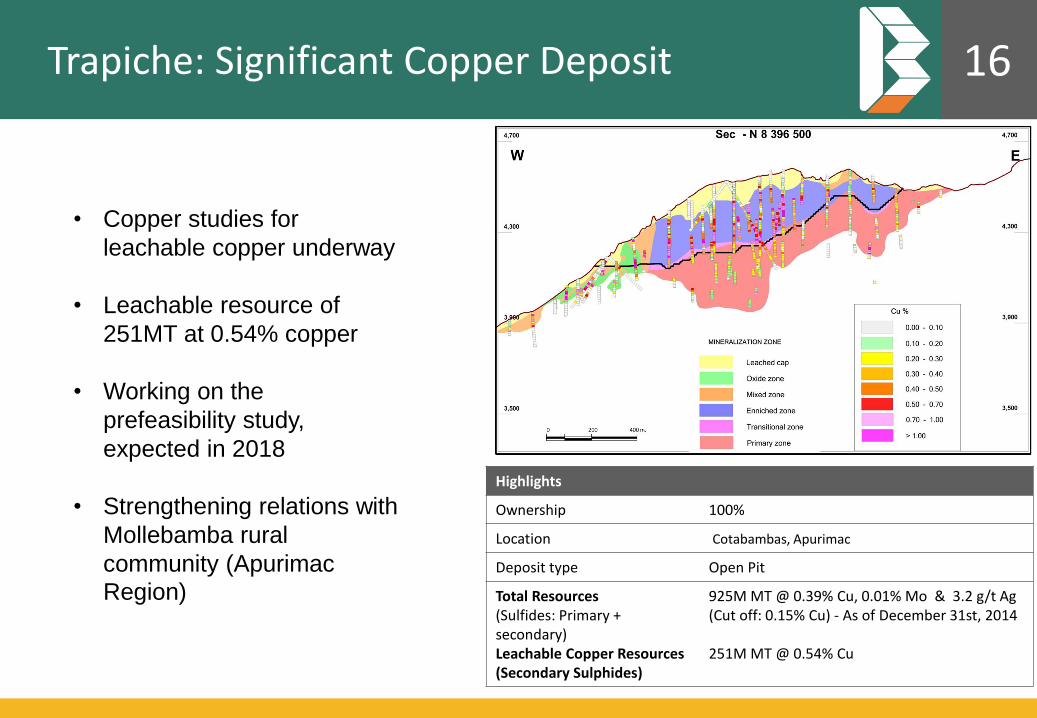

Trapiche: Significant Copper Deposit 16

Highlights

Ownership 100%

Location Cotabambas, Apurimac

Deposit type Open Pit

Total Resources(Sulfides: Primary + secondary)Leachable Copper Resources(Secondary Sulphides)

925M MT @ 0.39% Cu, 0.01% Mo & 3.2 g/t Ag(Cut off: 0.15% Cu) - As of December 31st, 2014

251M MT @ 0.54% Cu

• Copper studies for

leachable copper underway

• Leachable resource of

251MT at 0.54% copper

• Working on the

prefeasibility study,

expected in 2018

• Strengthening relations with

Mollebamba rural

community (Apurimac

Region)

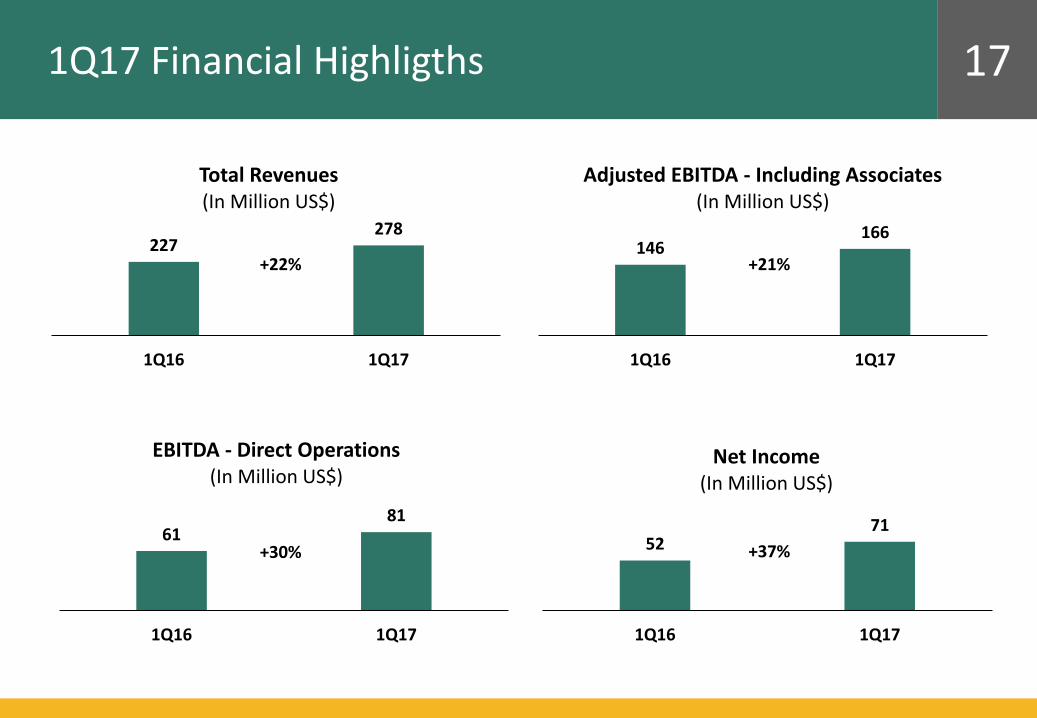

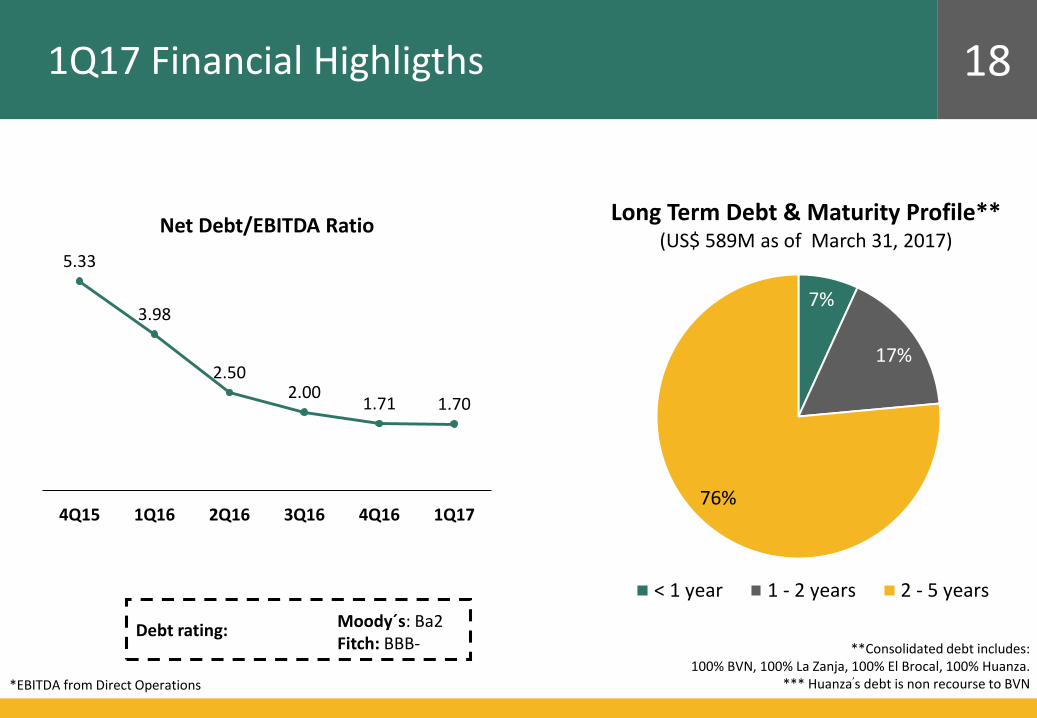

1Q17 Financial Highligths 17

227278

1Q16 1Q17

Total Revenues(In Million US$)

6181

1Q16 1Q17

EBITDA - Direct Operations(In Million US$)

5271

1Q16 1Q17

Net Income(In Million US$)

146166

1Q16 1Q17

Adjusted EBITDA - Including Associates(In Million US$)

+22% +21%

+30% +37%

1Q17 Financial Highligths 18

**Consolidated debt includes:100% BVN, 100% La Zanja, 100% El Brocal, 100% Huanza.

*** Huanza,s debt is non recourse to BVN*EBITDA from Direct Operations

Debt rating: Moody´s: Ba2Fitch: BBB-

5.33

3.98

2.502.00

1.71 1.70

4Q15 1Q16 2Q16 3Q16 4Q16 1Q17

Net Debt/EBITDA Ratio

7%

17%

76%

Long Term Debt & Maturity Profile**(US$ 589M as of March 31, 2017)

< 1 year 1 - 2 years 2 - 5 years

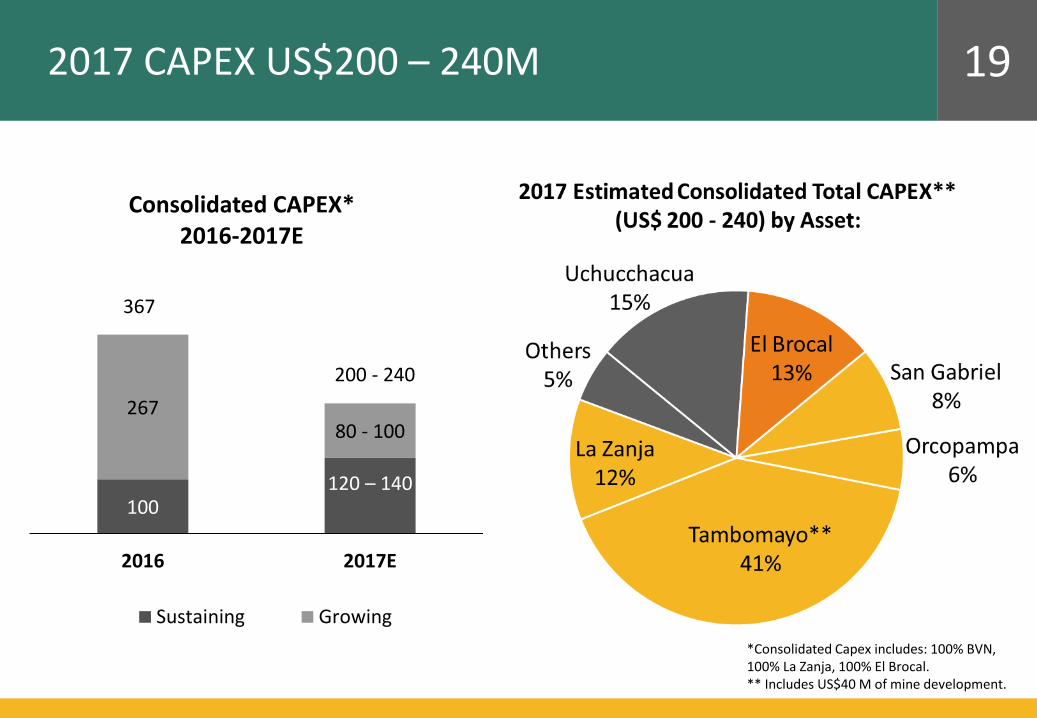

2017 CAPEX US$200 – 240M 19

*Consolidated Capex includes: 100% BVN, 100% La Zanja, 100% El Brocal.** Includes US$40 M of mine development.

100120 – 140

26780 - 100

2016 2017E

Consolidated CAPEX*2016-2017E

Sustaining Growing

367

200 - 240

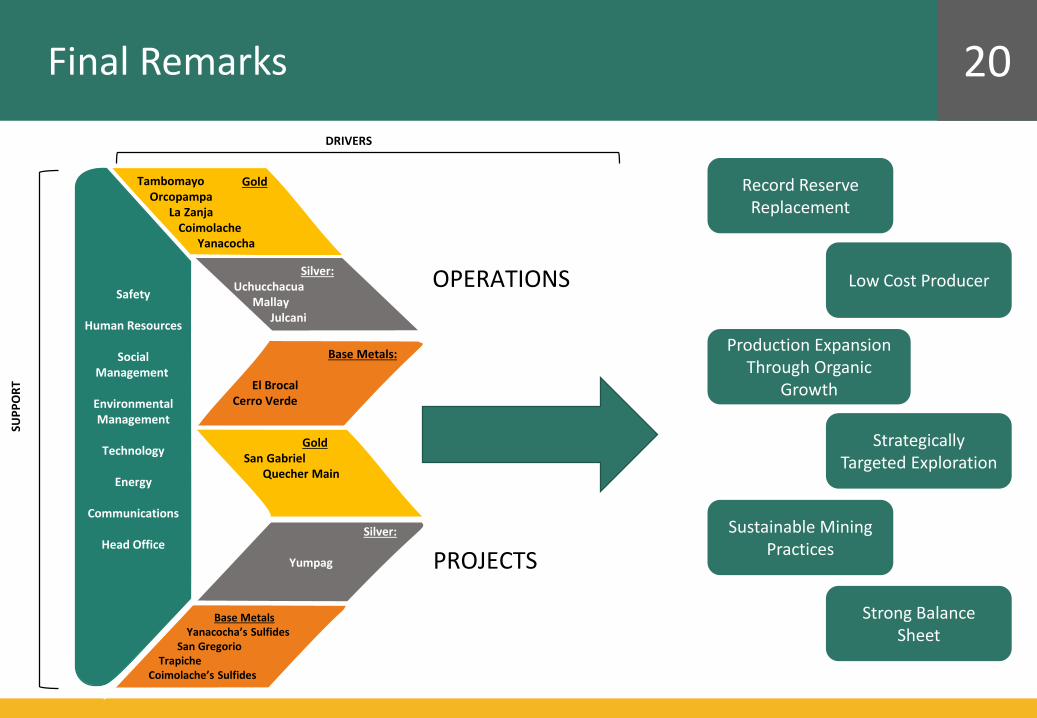

Final Remarks 20

Record Reserve Replacement

Low Cost Producer

Production ExpansionThrough Organic

Growth

StrategicallyTargeted Exploration

Sustainable MiningPractices

Strong Balance Sheet

OPERATIONS

PROJECTS

Base Metals:

El Brocal Cerro Verde

Silver:

Yumpag

Base MetalsYanacocha’s Sulfides

San GregorioTrapiche

Coimolache’s Sulfides

SUP

PO

RT

DRIVERS

GoldSan Gabriel

Quecher Main

Safety

Human Resources

SocialManagement

EnvironmentalManagement

Technology

Energy

Communications

Head Office

TambomayoOrcopampa

La Zanja Coimolache

Yanacocha

Silver:Uchucchacua

MallayJulcani

Gold

BofAML – Global Metals, Mining & Steel ConferenceMay 2017

Victor Gobitz - CEO