Embed Size (px)

Citation preview

Board of Regents

Mandatory Student Fees

Greater guidance and stronger manage-ment controls are needed to improve accountability and transparency related to mandatory student fees

What We Found In fiscal year 2009, the USG collected approximately $239.2 million in mandatory student fees. In the current fiscal year, USG students are required to pay mandatory fees ranging from $194 - $855 per semester depending on the college or university they attend. We found that the Board of Regents’ (BOR) student fee policies allow significant discretion on the part of each USG institution regarding the use of student fee revenues. As such, they provide little assurance that fees are used in a manner that benefits the entire student body to the greatest extent possible even though all students are required to pay these fees.

In addition, we found that BOR and individual institutions need to improve their management controls over mandatory student fees to ensure greater transparency and accountability. These problems are detailed below.

While BOR policies require that all mandatory student fees be approved by BOR and have student input, we identified eight fees that failed to be approved by either BOR or by student fee advisory committees. USG institutions annually submit information about the fees they charge to BOR for its approval; however, the information is self-reported and BOR staff do not independently verify that all fees charged by an institution have been included. Consequently, BOR does not have a process to ensure that all fees assessed by each USG institution are reported and have gone through

Performance Audit 09-05 May 2010

Why we did this review The purpose of this audit was to present the information requested by the Senate Appropriations Committee. The Committee requested that we review mandatory student fees charged by all USG institutions to identify the amount collected from students for each fee, to determine how the fees are used and if the use of funds is consistent with statutory and policy constraints, and to determine if internal controls exist to appropriate-ly account for and monitor the use of these funds.

Who we are The Performance Audit Operations Division was established in 1971 to conduct in-depth reviews of state programs. The purpose of these reviews is to determine if programs are meeting their goals and objectives; provide measurements of program results and effectiveness; identify other means of meeting goals; evaluate the efficiency of resource allocation; and assess compliance with laws and regulations.

Website: www.audits.state.ga.us Phone: 404-657-5220

Fax: 404-656-7535

the appropriate approval process.

We also found that the information submitted by USG institutions to BOR in their annual fee requests is not always sufficient for members of the Board to make informed decisions regarding the appropriateness of current fee rates or the necessity for fee rate increases. Our review of the annual fee requests found that the revenue, expenditure, and fund balance data submitted by several institutions was incomplete, inaccurate, or inconsistent. While BOR staff review the information submitted by USG institutions, they do not compare data submitted to other sources (e.g., data contained in the financial data system). In addition, BOR staff do not use the information to generate multi-year trends that would reveal fee surpluses over time, or obtain explanations from many USG institutions for the planned use of, or necessity for, persistent and significant revenue surpluses and fund balances. Such analyses could potentially assist Board members during their annual review and approval of fees.

We identified four mandatory fees whose revenues were either not being used for or are not planned to be used for their originally approved purpose. BOR policies require that the establishment of new mandatory fees and increases to existing fees be presented to student fee advisory committees and be approved by BOR. Institutions are also required to present to the advisory committees and to BOR the purpose and intended use of these new fees and fee increases. However, BOR policies do not require institutions to obtain approval to use fee revenues in a manner that is significantly different than the purpose for which the fee was originally approved.

In general, we found that most of the fee expenditures we reviewed appeared to be appropriate and properly documented; however, at three of the seven USG institutions, we found expenditures that were either not appropriate or not properly documented. These transactions involved the use of student activity fees to fund ineligible programs, to provide improperly reconciled cash advances to faculty members, or to fund excessive/unnecessary travel for faculty, staff members, and students.

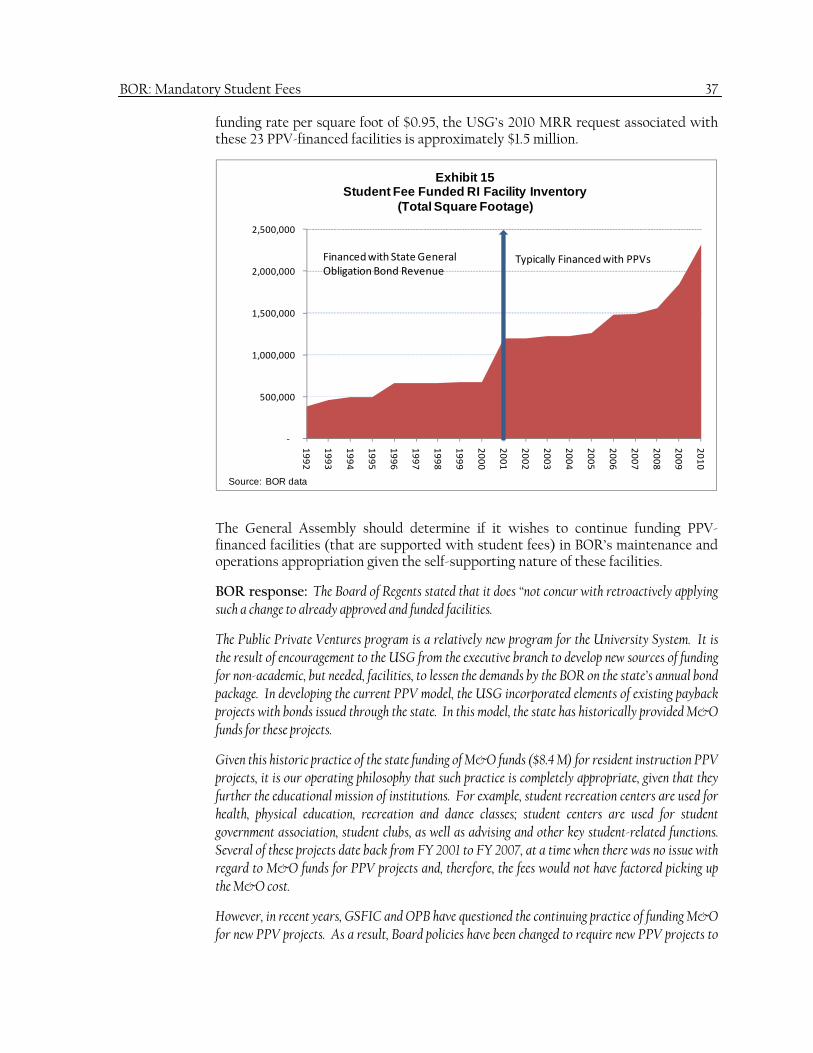

During this review, we identified several issues related to the use of student fees to support the construction or renovation of USG facilities through public-private ventures. Over the past 10 years, the USG has increasingly used public private venture (PPV) financing (supported by student fee revenues) to acquire and construct facilities. While BOR policies require all new building, major renovations, and rehabilitations, using funds from any source, including PPVs, to be approved by BOR, it appears that two facilities constructed by Georgia Gwinnett College (GGC) were not appropriately authorized and approved. In addition, we found that although the General Assembly cannot limit the acquisition and construction of facilities financed through PPVs, BOR includes these facilities in the maintenance and operations component of its annual funding formula request for state appropriations even though such facilities are considered to be “self-supporting” using student fee revenues. The fiscal year 2010 budget request associated with the USG’s 23 mandatory student fee supported and PPV-financed facilities is over $11.3 million.

BOR’s Response: The Board of Regents stated that it “takes very seriously its fiduciary responsibility with regard to ensuring accountability and transparency, including all matters related to mandatory fees. The Board of Regents is committed to using the results of the State Auditor’s Mandatory Student Fee performance audit to review and revise, where necessary, internal controls related to this important facet of the University System of Georgia’s operations.”

BOR: Mandatory Student Fees i

Table of Contents

Purpose of the Audit 1

Background 1

University System of Georgia 1 Financial Information 4 Comparison with Other States 8

Findings and Recommendations 11

BOR Policies and Oversight To ensure greater accountability and transparency, BOR should provide greater guidance to USG institutions regarding mandatory student fees. 11

BOR should implement a periodic review process to ensure that all mandatory student fees assessed by USG institutions have been appropriately approved. 12

BOR should ensure that prior-year fee revenue surplus and fund balance information received from USG institutions is complete, accurate, and consistent. 15

To ensure that members of BOR have sufficient information to determine if fee increases are necessary, they should be provided with better data regarding annual fee surpluses and the planned uses for fund balances when considering annual fee rate requests. 19

BOR should develop a policy that requires USG institutions to seek input from the appropriate student fee advisory committee and approval from BOR if an institution substantially changes the use of an existing fee. 23

Questionable Transactions

In general, the mandatory student fee expenditures that were reviewed appeared to be appropriate and properly documented; however, at three institutions we found expenditures that were either not appropriate or not properly documented. 25

Both student activity fee revenue and state appropriations were used to fund travel expenses that were wasteful and abusive at the University of West Georgia. 27

Student activity fee revenue was used to fund abusive, wasteful, and potentially fraudulent travel expenses at Fort Valley State University. 30

BOR: Mandatory Student Fees ii

Public/Private Ventures The acquisition and rehabilitation of two large facilities at Georgia Gwinnett College, costing approximately $14 million, that were financed through public-private ventures do not appear to have been appropriately authorized by BOR. 33

Although the construction or renovation of USG facilities financed through public- private ventures and supported with student fee revenue are not approved by the General Assembly, the USG obtains state appropriations to operate and maintain these facilities. 35

Appendices 39

Appendix A: Objectives, Scope, and Methodology 39 Appendix B: FY 2010 Mandatory Student Fees Charged by USG Institutions 40 Appendix C: National Comparison of Tuition and Fee Rates 41

BOR: Mandatory Student Fees 1

Purpose of the Audit Our review of mandatory student fees charged by institutions of the University System of Georgia (USG), which is governed by the Board of Regents (BOR), was conducted at the request of the Senate Appropriations Committee. Per the Committee’s request, our review included the following:

an assessment of the student fees collected by BOR institutions; determining the amount schools collect from students and how the funds are used; determining if the use of funds is consistent with any statutory or policy constraints; determining if internal controls exist to appropriately account for and monitor the

use of these funds; and comparing student fees in Georgia to fees assessed by state schools in other

comparable southern states.

Details about our objectives, scope, and methodology related to this report are included in Appendix A.

This report has been discussed with appropriate personnel representing the Board of Regents. A draft copy was provided for their review, and they were invited to provide a written response, including any areas in which they plan to take corrective action. Pertinent responses have been included in this report as appropriate.

Background

University System of Georgia Under the Constitution and laws of the state of Georgia, the Board of Regents (BOR) of the University System of Georgia (USG) was created to govern, control and manage a system of public institutions providing quality higher education for the benefit of Georgia citizens. BOR oversees 35 colleges and universities, including four research universities, two regional universities, 13 state universities, eight state colleges, and eight two-year colleges. The names and location of each of these institutions are shown in Exhibit 1 on the following page. Higher Education Funding USG institutions are funded through multiple revenue sources including state appropriations, tuition, grants, donations, mandatory student fees, and elective fees such as housing and meal plans. Annual appropriation levels are determined by a formula whereby approximately 75% of the USG operating cost is funded with state appropriations and 25% is funded by student tuition and fees. While the General Assembly appropriates state funds to the USG, BOR determines the amount of state funds to be allocated to each institution. In addition, BOR establishes the tuition rates for each type of institution and approves mandatory fee rates requested by individual institutions.

BOR: Mandatory Student Fees 2

Mandatory Student Fees According to BOR policy, a “mandatory fee” is defined as any fee or special charge that is required to be paid by all full-time, undergraduate students at an institution or by all undergraduate students in a specific degree program. There are many types of mandatory student fees, including, but not limited to, fees for intercollegiate athletics, student activities, student health services, parking, transportation, and facilities development. Mandatory fees are distinguished from “elective” fees such as housing and laboratory fees which are associated with goods, services, or specific academic courses that students “elect” to purchase. While the amount of state appropriations available to the USG is determined by the General Assembly and tuition rates are determined by the Board of Regents, each USG institution is authorized to charge different types of mandatory student fees at rates associated with their unique needs, with the approval of BOR. For example, all USG institutions charge an Activity Fee (ranging from $33 to $150 per semester);

BOR: Mandatory Student Fees 3

whereas only three institutions charge an International Fee (ranging from $5 to $14 per semester). As shown in Exhibit 2 below, the total mandatory student fee rates charged by each institution range from a low of $194 to a high of $855 per semester. Appendix B lists all mandatory student fees and the amounts at each USG institution.

Exhibit 2 Total Mandatory Student Fee Rates

Charged by USG Institutions FY 2010

Type of Institution Total Mandatory Fee Rates Per Semester

Research University $556-$830

Regional University $822-$855

State University $455-$793

4-Year College $194-$540

2-Year College $217-$387

Source: BOR data BOR Policies for Mandatory Student Fees The mandatory student fee approval process is shown in Exhibit 3. Annually, each USG institution follows this process in developing proposed fee requests and fee budgets. In accordance with BOR policy, institutions must have a mandatory student fee committee, of which 50% or more of the members should be students appointed by the Student Government Association (SGA). This committee is charged with reviewing and voting on the student fee request. It should be noted, however, that each institution’s president and BOR may approve fee requests without the approval of the fee committees. BOR policies also require mandatory student fee revenue to be budgeted and administered with the advice and counsel of an advisory committee composed of at least fifty percent (50%) students. An exception to both of these policies has been granted for the general purpose “institutional” fees that have been instituted system-wide by BOR. Once the annual fee requests are reviewed at the institutional level, USG institutions are required by BOR policy to submit mandatory student fee request packages to the BOR Office of Fiscal Affairs. These packages are submitted in December. Fee request packages are required to include the following information:

1. actual and projected revenues and expenditures for each mandatory fee, 2. statement of needs and purpose for any new and increased mandatory fees, 3. fund balances for each mandatory fee, and 4. forms signed by mandatory student fee committee members (50% of which

must be students) indicating their approval or denial of fee requests.

BOR: Mandatory Student Fees 4

Once the institutions’ fee requests are received by BOR, analysts in the Office of Fiscal Affairs review and make recommendations to the Chancellor and to the Board of Regents as to whether the fee request should be approved, denied, or modified. BOR votes on fee requests at its April meeting. BOR policies allow institutions to waive mandatory fees for students who are enrolled for fewer than six credit hours. Alternatively, institutions may prorate mandatory fees on a per credit hour basis for students taking less than 12 credit hours. Institutions may also elect to reduce Board-approved mandatory fees for students enrolled in summer courses. BOR policies also allow institutions to waive mandatory fees, excluding technology fees, for:

students who reside or study at another institution,

students who enroll in practicum experiences or internships located at least 50 miles from the institution,

students enrolled in distance learning courses or programs who are not also enrolled in on-campus courses nor residing on campus,

students enrolled at off- campus centers, and

U.S. military reserve and Georgia National Guard Combat Veterans.

Financial Information

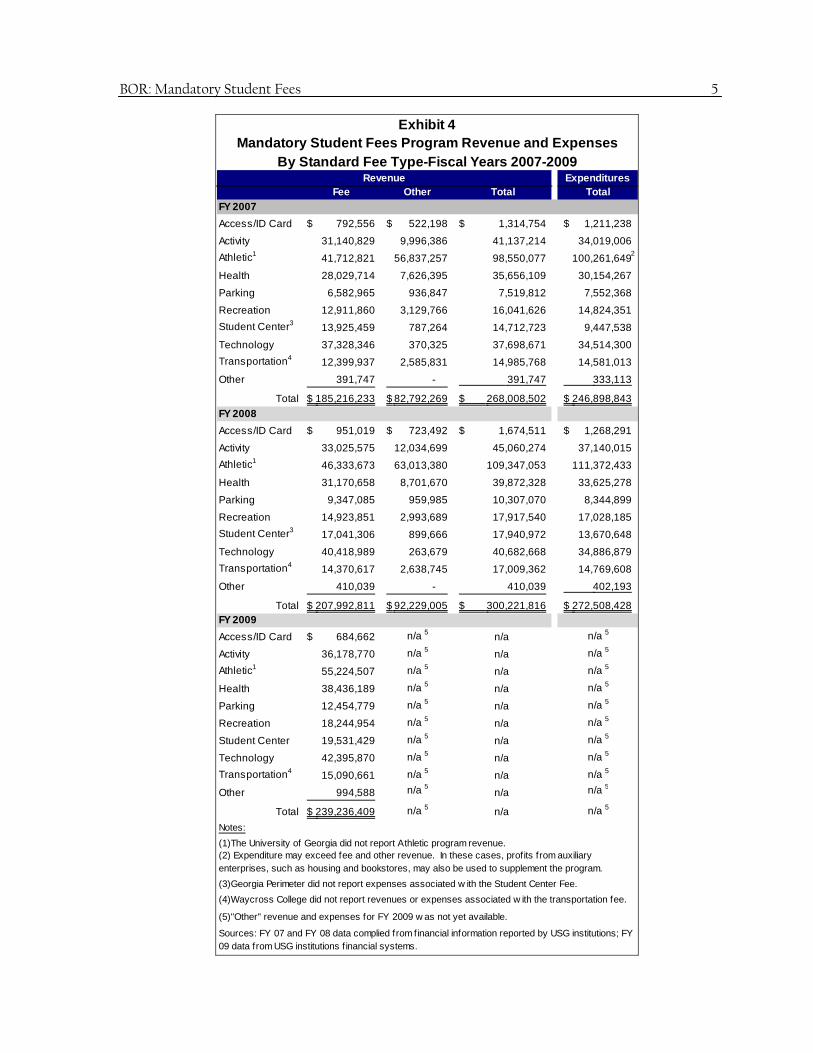

Mandatory student fees generate significant amounts of revenue across the USG. As shown in Exhibit 4, from fiscal year 2007 to fiscal year 2009, mandatory student fee revenues grew from approximately $185.2 to $239.2 million. Mandatory student fee revenues support a variety of programs at the state’s public colleges and universities. As shown in the Exhibit, these programs are also supported with “other revenue” related to the direct use of a program (e.g., parking fines). With the exception of revenue generated by the recently implemented general purpose institutional fees, USG institutions may retain unexpended revenues for these programs from year to year. As a result, programs funded with mandatory student fees can accumulate fund balances which are available for use in future years.

BOR: Mandatory Student Fees 5

ExpendituresFee Other Total Total

FY 2007

Access/ID Card 792,556$ 522,198$ 1,314,754$ 1,211,238$

Activity 31,140,829 9,996,386 41,137,214 34,019,006

Athletic1 41,712,821 56,837,257 98,550,077 100,261,649

Health 28,029,714 7,626,395 35,656,109 30,154,267

Parking 6,582,965 936,847 7,519,812 7,552,368

Recreation 12,911,860 3,129,766 16,041,626 14,824,351

Student Center3 13,925,459 787,264 14,712,723 9,447,538

Technology 37,328,346 370,325 37,698,671 34,514,300

Transportation4 12,399,937 2,585,831 14,985,768 14,581,013

Other 391,747 - 391,747 333,113

Total 185,216,233$ 82,792,269$ 268,008,502$ 246,898,843$

FY 2008

Access/ID Card 951,019$ 723,492$ 1,674,511$ 1,268,291$

Activity 33,025,575 12,034,699 45,060,274 37,140,015

Athletic1 46,333,673 63,013,380 109,347,053 111,372,433

Health 31,170,658 8,701,670 39,872,328 33,625,278

Parking 9,347,085 959,985 10,307,070 8,344,899

Recreation 14,923,851 2,993,689 17,917,540 17,028,185

Student Center3 17,041,306 899,666 17,940,972 13,670,648

Technology 40,418,989 263,679 40,682,668 34,886,879

Transportation4 14,370,617 2,638,745 17,009,362 14,769,608

Other 410,039 - 410,039 402,193

Total 207,992,811$ 92,229,005$ 300,221,816$ 272,508,428$ FY 2009

Access/ID Card 684,662$ n/a 5 n/a n/a 5

Activity 36,178,770 n/a 5 n/a n/a 5

Athletic1 55,224,507 n/a 5 n/a n/a 5

Health 38,436,189 n/a 5 n/a n/a 5

Parking 12,454,779 n/a 5 n/a n/a 5

Recreation 18,244,954 n/a 5 n/a n/a 5

Student Center 19,531,429 n/a 5 n/a n/a 5

Technology 42,395,870 n/a 5 n/a n/a 5

Transportation4 15,090,661 n/a 5 n/a n/a 5

Other 994,588 n/a 5 n/a n/a 5

Total 239,236,409$ n/a 5 n/a n/a 5

Notes:

(1)The University of Georgia did not report Athletic program revenue.

(3)Georgia Perimeter did not report expenses associated w ith the Student Center Fee.

(4)Waycross College did not report revenues or expenses associated w ith the transportation fee.

(5)"Other" revenue and expenses for FY 2009 w as not yet available.

Sources: FY 07 and FY 08 data complied from financial information reported by USG institutions; FY 09 data from USG institutions f inancial systems.

Exhibit 4Mandatory Student Fees Program Revenue and Expenses

By Standard Fee Type-Fiscal Years 2007-2009Revenue

(2) Expenditure may exceed fee and other revenue. In these cases, profits from auxiliary enterprises, such as housing and bookstores, may also be used to supplement the program.

2

BOR: Mandatory Student Fees 6

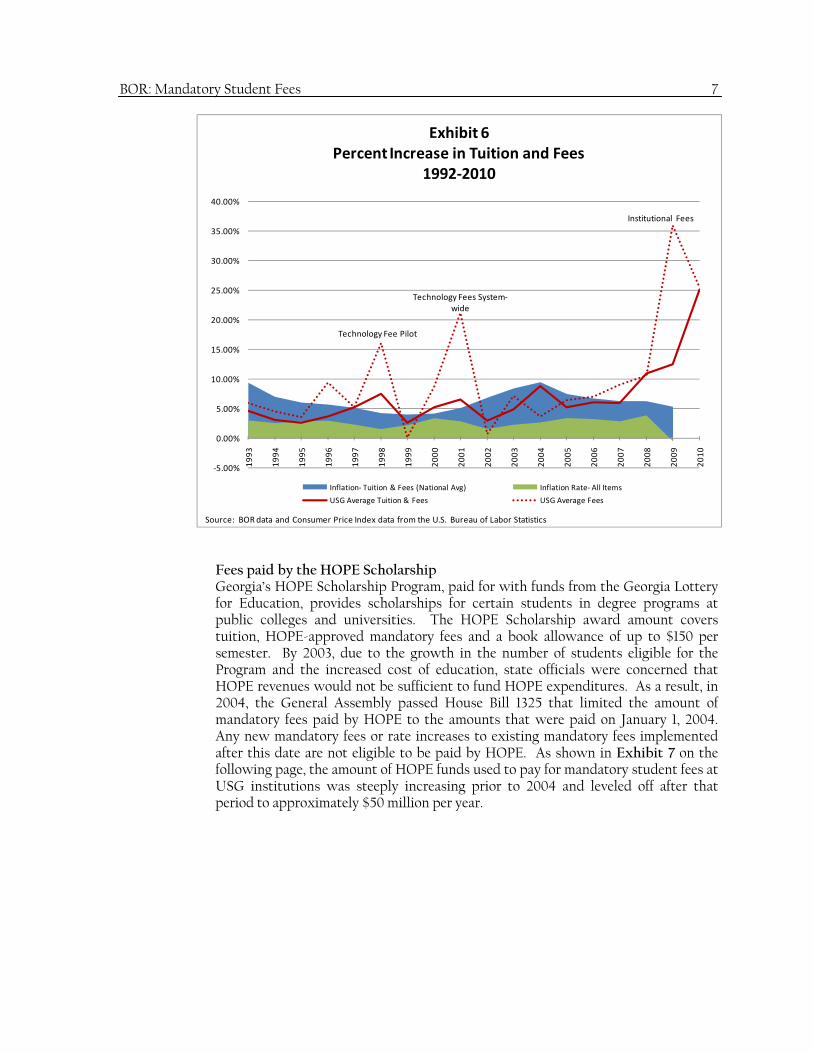

Tuition and Mandatory Fee Rate Trends As shown in Exhibit 5 below, the cost of higher education (tuition and mandatory student fees) in Georgia has substantially increased each year since 1992, from an average of $705 to $2,278 per semester. In addition, the proportion of these costs attributable to mandatory student fees has also increased (from an average of 13.4% in 1992 to 21.9% in 2010).

$0

$500

$1,000

$1,500

$2,000

$2,500

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Exhibit 5USG Average Student Costs per Semester

1992‐2010

Average Resident Tuition Average Mandatory Fees

Source: BORdata

As shown in Exhibit 6, nationally, the average cost for college tuition and fees has increased at higher rates than general inflation. The average increase in tuition and fees at USG institutions mirrored national trends until 2008 when the average USG institution rate significantly increased by 11% over the previous year. Much of this increase was due to a large tuition increase. Again, in 2009, the average USG student costs increased another 12%. This increase was due to the implementation of system-wide “institutional” mandatory fees to fund general operating costs as a result of cuts in state appropriations.

BOR: Mandatory Student Fees 7

Technology Fee Pilot

Technology Fees System‐wide

Institutional Fees

‐5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Exhibit 6Percent Increase in Tuition and Fees

1992‐2010

Inflation‐ Tuition & Fees (National Avg) Inflation Rate‐ All Items

USG Average Tuition & Fees USG Average Fees

Source: BOR data and Consumer Price Index data from the U.S. Bureau of Labor Statistics Fees paid by the HOPE Scholarship Georgia’s HOPE Scholarship Program, paid for with funds from the Georgia Lottery for Education, provides scholarships for certain students in degree programs at public colleges and universities. The HOPE Scholarship award amount covers tuition, HOPE-approved mandatory fees and a book allowance of up to $150 per semester. By 2003, due to the growth in the number of students eligible for the Program and the increased cost of education, state officials were concerned that HOPE revenues would not be sufficient to fund HOPE expenditures. As a result, in 2004, the General Assembly passed House Bill 1325 that limited the amount of mandatory fees paid by HOPE to the amounts that were paid on January 1, 2004. Any new mandatory fees or rate increases to existing mandatory fees implemented after this date are not eligible to be paid by HOPE. As shown in Exhibit 7 on the following page, the amount of HOPE funds used to pay for mandatory student fees at USG institutions was steeply increasing prior to 2004 and leveled off after that period to approximately $50 million per year.

BOR: Mandatory Student Fees 8

$‐

$10,000,000

$20,000,000

$30,000,000

$40,000,000

$50,000,000

$60,000,000

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

HOPE Funds

Exhibit 7HOPE Funded Fees at USG Institutions

1998‐2008

Rate increases after 2004 not HOPE eligible

Source: Georgia Student Finance Commission (GSFC)

Comparison with Other States Mandatory student fees are also common in public higher education institutions in other states. According to a 2006 study conducted by the State Higher Education Executive Officers Association (SHEEO)1, states have differing philosophies regarding the general purpose and function of mandatory student fees. For example, some states mainly assess mandatory student fees to make up for tuition limitations; whereas, other states require that mandatory student fees be used only for specific purposes. Georgia has recently adopted both philosophies. While most mandatory student fees are approved for specific purposes such as intercollegiate athletics or health, for fiscal years 2009-2012 USG institutions have been directed by BOR to assess general purpose mandatory fees to partially replace reductions in state appropriations. Limits and Controls on Mandatory Fees USG institutions can establish new mandatory student fees and increase fee amounts with the approval of BOR. State law does not place any restrictions on the maximum amount of fees that can be assessed, annual fee increases, or how the fee revenue may be expended. As discussed below, a small number of states have implemented legislative controls over student fees. It should be noted that some of these states lack a central governing authority, like BOR, to provide oversight and guidance for their institutions of higher education which may explain the higher levels of legislative involvement. Limits on Fees: According to the 2006 SHEEO study, only one state (California) requires approval from the Governor for certain mandatory fees and seven states 1 Boatman, Angela and L’Orange, Hans, “State Tuition, Fees, and Financial Assistance Policies for Public Colleges and Universities,” State Higher Education Executive Officers, November 2006.

BOR: Mandatory Student Fees 9

require legislative approval. In Texas, state law defines specific types of fees that may be charged by public

colleges and universities and requires that mandatory student services fees be approved by each institution’s governing board. State law limits the total amount of “compulsory” fees charged to $250 per semester and limits increases when fees are more than $150 unless such increases are approved in a student vote or by a majority vote of the student government. In addition, state law limits rates for particular types of fees such as student union fees, medical services fees, and international education fees and prohibits compulsory parking and parking facilities fees.

In Florida, state law also limits fee amounts, where the sum of activity, health, and athletic fees is not to exceed 40% of tuition. Florida state law also prohibits universities from increasing the combined sum of these fees more than 5% per year unless specifically authorized in law or in the General Appropriations Act.

In Oklahoma, increases to tuition and fees are statutorily capped by a formula based upon other states’ and peer institutions’ rates.

Controls on Fee Usage: Some states have implemented legislative controls to ensure accountability over the use and expenditure of student fees. In Texas, state law establishes the purpose of each fee type and how the fee may

be used. For example, the statute states that the recreational sports fee “may be used only for financing, constructing, operating, maintaining, and improving recreational sports facilities and programs.”

In Tennessee, state law requires institutions to publish financial disclosure statements that provide information on the amount of student activity fee revenue received and expended and any remaining balances.

In Virginia, state law requires institutions to publish annual reports that show the amount of student activity fee revenue and the names of organizations receiving student activity funds.

Mandatory Fees Charged in Other States As shown in Exhibit 8 on the following page, the types of mandatory student fees levied by USG institutions are similar to those fees levied by public colleges and universities in other southern states. At least one institution in each of the seven states we reviewed charge athletic and student facility fees. Other common fees charged include activity, health, and transportation fees. Some institutions also charge a “consolidated” mandatory fee which can be used for a variety of purposes.

BOR: Mandatory Student Fees 10

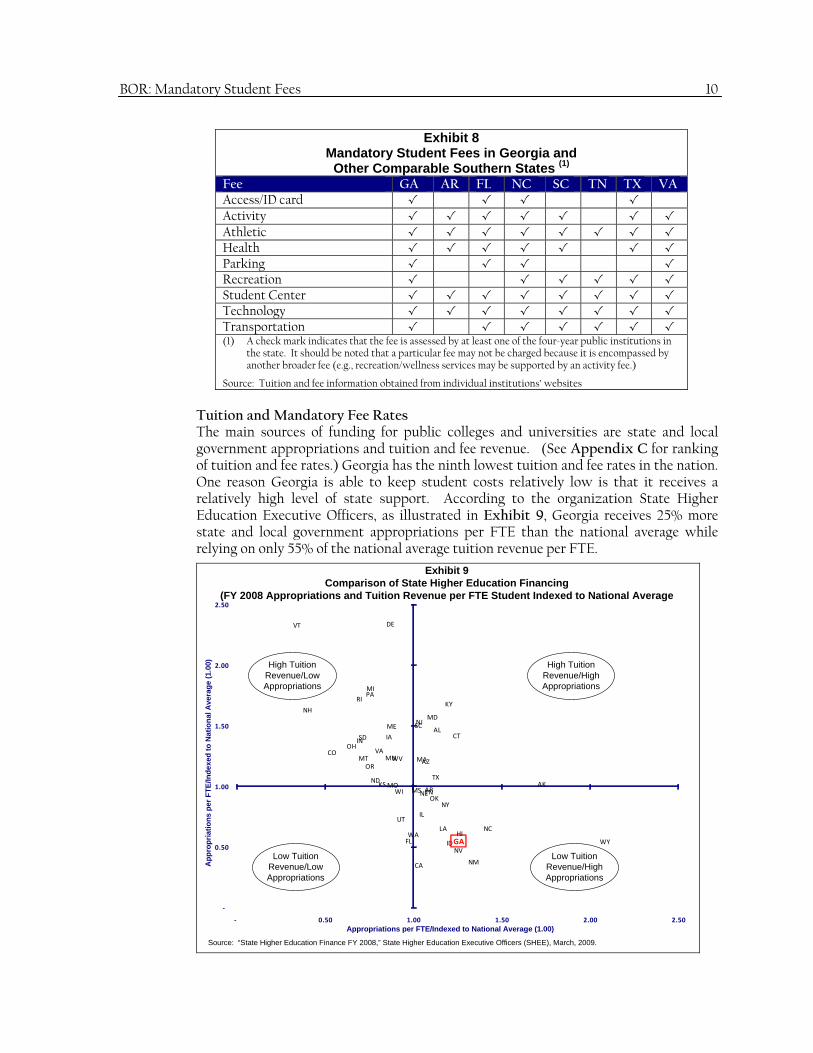

Exhibit 8 Mandatory Student Fees in Georgia and

Other Comparable Southern States (1) Fee GA AR FL NC SC TN TX VA Access/ID card √ √ √ √ Activity √ √ √ √ √ √ √ Athletic √ √ √ √ √ √ √ √ Health √ √ √ √ √ √ √ Parking √ √ √ √ Recreation √ √ √ √ √ √ Student Center √ √ √ √ √ √ √ √ Technology √ √ √ √ √ √ √ √ Transportation √ √ √ √ √ √ √ (1) A check mark indicates that the fee is assessed by at least one of the four-year public institutions in

the state. It should be noted that a particular fee may not be charged because it is encompassed by another broader fee (e.g., recreation/wellness services may be supported by an activity fee.)

Source: Tuition and fee information obtained from individual institutions’ websites

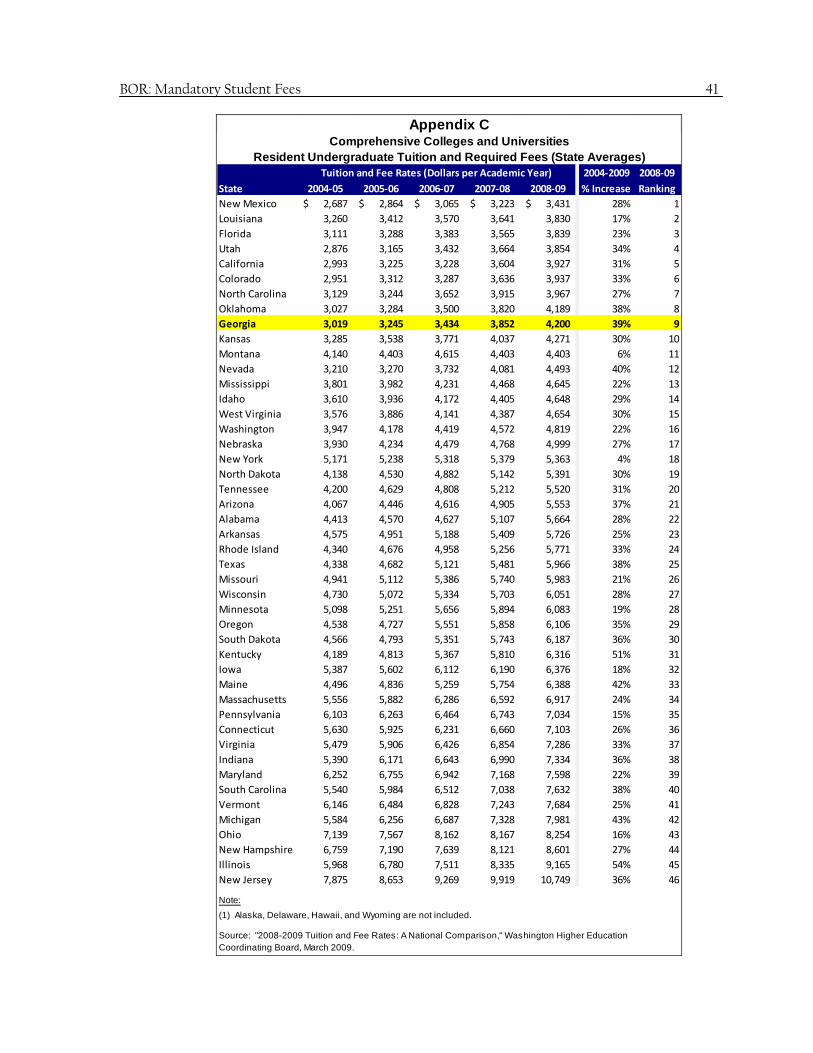

Tuition and Mandatory Fee Rates The main sources of funding for public colleges and universities are state and local government appropriations and tuition and fee revenue. (See Appendix C for ranking of tuition and fee rates.) Georgia has the ninth lowest tuition and fee rates in the nation. One reason Georgia is able to keep student costs relatively low is that it receives a relatively high level of state support. According to the organization State Higher Education Executive Officers, as illustrated in Exhibit 9, Georgia receives 25% more state and local government appropriations per FTE than the national average while relying on only 55% of the national average tuition revenue per FTE.

VT

NH

COOH

RI

INSD

MT

MI

OR

PA

ND

VA

KS

IA

DE

MN

ME

MO

WV

WI

UT

FLWA

SC

MS

NJ

CA

IL

MA

NE

AZ

ARTN

MD

OK

TX

AL

LA

NY

KY

ID

CT

NVGAHI

NM

NC

AK

WY

‐

0.50

1.00

1.50

2.00

2.50

‐ 0.50 1.00 1.50 2.00 2.50

Low Tuition Revenue/High Appropriations

Low Tuition Revenue/Low Appropriations

High Tuition Revenue/Low Appropriations

Appropriations per FTE/Indexed to National Average (1.00)

Ap

pro

pri

atio

ns

per

FT

E/In

dex

ed t

o N

atio

nal

Ave

rag

e (1

.00)

Source: “State Higher Education Finance FY 2008,” State Higher Education Executive Officers (SHEE), March, 2009.

Exhibit 9Comparison of State Higher Education Financing

(FY 2008 Appropriations and Tuition Revenue per FTE Student Indexed to National Average

High Tuition Revenue/High Appropriations

BOR: Mandatory Student Fees 11

Findings and Recommendations

BOR Policies and Oversight

To ensure greater accountability and transparency, BOR should provide greater guidance to USG institutions regarding mandatory student fees.

At the beginning of our review, BOR policies regarding mandatory student fees were primarily administrative and procedural in nature – setting forth requirements for establishing, budgeting, and expending student fees according to the approved business procedures of each institution. During our review, BOR policy was updated to also indicate that “mandatory student fees shall be used exclusively to support the institutions’ mission to enrich the educational, institutional and cultural experience of students.” While the updated policy attempts to set an overall direction for student fees, it still does not provide enough direction or guidance to help ensure that decisions regarding the allocation and expenditure of mandatory student fees are focused in a manner that benefits the entire student body of each institution to the greatest extent possible given the fact that all students are required to pay the fees. In the absence of more specific guidance from BOR, USG institutions have been made responsible for ensuring the appropriate stewardship of mandatory student fees collected by their respective institutions. However, we found that the extent to which institutions establish and expend mandatory student fees in a manner that benefits the broadest number of students varies significantly. Based on our review, the following areas could benefit from clearer guidance from the Board regarding its philosophy of mandatory student fees:

Whether mandatory student fees should be used for professional salaries, training, and travel,

Whether mandatory student fees should be used for student scholarships,

Involvement of the fee advisory committee (which includes student representatives) in amending student activity fee budgets,

Whether costs associated with construction or improvement of facilities, paid for with mandatory student fees, should be borne by students who will likely graduate before the facility is ready for use, and

Whether fees should be continued and used for another purpose after their original purpose for being established has been fulfilled (e.g., facilities whose debt service has been retired).

While some differences in the use of fees is expected given the varying sizes and missions of the state’s 35 institutions, additional guidance could be helpful to both students and institutions in determining whether fees are used to reflect the broadest variety of student interests. To increase accountability and transparency related to student fees, BOR should provide more specific guidance regarding the appropriate uses of mandatory student fees. In addition, as discussed in the remaining findings of this report, both BOR and USG institutions should improve the management controls related to mandatory student fees.

Accountability promotes good stewardship of funds and is intended to prevent fraud, waste, and abuse.

Transparency provides accurate and user-friendly information regarding these fees to the BOR, institution administration, and students.

BOR: Mandatory Student Fees 12

BOR’s Response: The Board of Regents stated that while the recommendation for consistency in the use of mandatory fees is reasonable in theory, it is somewhat impractical to implement given the unique characteristics of the 35 USG institutions. However, regarding our suggestions for additional guidance, the Board of Regents did state that it will follow up with the Student Advisory Council to determine whether there is an interest in students being involved in the budget amendment process. In addition, the Board of Regents stated that it would propose a policy change that would require institutions to obtain authorization from the Board of Regents to repurpose a fee that is no longer needed for its original purpose. The Board of Regents did not agree with the recommendation to develop a consistent policy regarding whether the costs associated with construction or improvement of facilities should be borne by students who will likely graduate before the facility is ready for use. The Board of Regents stated that this “question goes to the heart of a philosophical debate or difference of opinion: are fees paid by the individual to be judged solely on whether they are a private benefit, or are they based upon the greater public good? The Board of Regents, USG presidents and students have historically believed-and agreed-that such fees are designed for the greater public good.”

BOR should implement a periodic review process to ensure that all mandatory student fees assessed by USG institutions have been appropriately approved.

Although BOR policies require that all mandatory student fees be approved by BOR and have student input, we identified eight fees that failed to be approved by either BOR or by student fee advisory committees. Although USG institutions annually submit proposals to BOR to create new mandatory fees and to increase the rates for existing mandatory fees, the information is self-reported and BOR staff do not verify its accuracy or completeness. Consequently, BOR does not have a process to ensure that all fees assessed by each USG institution are reported and have been appropriately approved. In order to identify fees that were being charged to students but not approved by BOR, we compared the list of mandatory fees approved by BOR to information regarding tuition and fees on the 35 institutions’ web sites. Since all fees may not be listed or clearly explained on the web site, we may not have identified all fees that are being charged that have not been appropriately approved. Our comparison revealed the following eight fees that had not been appropriately approved.

Columbus State University mandatory course fees: Beginning spring 2009, Columbus State University began assessing a $12 per semester hour fee on courses that are part of the general education core curriculum and many other undergraduate courses. While BOR policies allow institutions to charge “other elective fees and special charges” without approval of BOR, this mandatory course fee does not have the characteristics generally associated with elective fees and special charges. Elective fees and special charges are defined as fees and charges which are paid selectively by students and are associated with specific programs of study or courses, fines, and services such as housing. The course fees established by Columbus State University were charged for all core courses, regardless of program of study or unique costs (e.g., laboratory costs). Therefore, this fee has the characteristics of a mandatory student fee. The revenue from this fee was allocated to the respective colleges for each course. For example, revenue

BOR: Mandatory Student Fees 13

obtained from core courses in the College of Science were distributed to the College of Science. The revenue was used to cover general operating expenses such as faculty development or part-time faculty salaries.

After being informed by the audit team of this fee, BOR staff instructed leadership at Columbus State University to cease these fees and to reimburse students the amount of such fees already paid. These reimbursements were made June 2009 and totaled approximately $300,000.

Darton College Identification (ID) Card Fee: In fall 2008, Darton College implemented a $10 mandatory ID card fee for all students. This fee was not presented to or approved by the College’s fee advisory committee or BOR. Upon being informed by the audit team of this fee, BOR required Darton College to present a proposal for the fee to its fee advisory committee and to seek approval for the fee from BOR. The fee was approved by BOR to be effective fall 2009.

Georgia Southwestern State University Postal Fee: Since at least 2003, Georgia Southwestern State University has charged an $8 mandatory postal fee each semester to students enrolled in more than 5 credit hours. It is currently charged to students enrolled in more than 3 credit hours. This fee has not been presented to or approved by BOR. In fact, it is apparent that the University had not presented financial information concerning this fee to BOR until their fiscal year 2010 fee request. Although this request included financial information concerning the fee, the fee has still not been formally approved by members of the Board.

North Georgia College and State University Yearbook Fee: For at least the past two years, North Georgia College and State University has charged a $12 mandatory yearbook fee. This fee has not been presented to or approved by BOR.

Parking fees at Gainesville College and South Georgia College: Two colleges were identified to be charging unapproved parking fees to all students, regardless of whether or not they have vehicles. At Gainesville College, a $20 “auto” fee that has not been presented to or approved by BOR is automatically charged to all students. This fee is in addition to a BOR- approved $35 parking deck fee. South Georgia College charges all students a $10 per semester parking fee that has not been reviewed or approved by BOR. This fee is waived for students without vehicles upon request.

Mandatory meal plans at Kennesaw State University and Georgia Gwinnett College: At Georgia Gwinnett College, effective fall 2008, all students enrolled in at least 7 credit hours were required to purchase meal plans (through meal debit cards) worth at least $200 each semester. In addition, students enrolled in less than 7 credit hours were required to purchase meal plans worth at least $100 each semester. Balances remaining on individual debit cards at the end of the academic year do not carry forward and are retained by the food services contractor. This minimum meal plan

BOR: Mandatory Student Fees 14

requirement has not been presented to the student fee advisory committee or to BOR for approval. In addition, effective fall 2009, Kennesaw State University (KSU) implemented mandatory meal plans for all full-time students. While this plan has been approved by KSU’s student government association, it was not submitted to BOR for approval. KSU’s plan requires all full-time students to purchase meal plans each semester ranging from $120 for full-time commuter non-freshman to $928 for residential freshman. BOR staff stated that the meal fees do not meet the definition of “mandatory student fees” because students directly “receive an equivalent cash value” from the plans. As a result, BOR approval and student input was not necessary. While students may receive such value for these plans, there is no exclusion in BOR policy related to mandatory student fees for such occurrences. BOR policy simply defines mandatory fees as fees paid by all students, with exemptions allowed for part-time students. In addition, food service fees, which are not subject to student fee committee and BOR approval requirements, are defined as fees paid by students who choose an institutional food service plan. Since these plans are mandatory for students and do not meet the definition of a food service fee, these plans should be considered mandatory student fees under current BOR policy. In response to this issue, BOR changed its policy in January 2010 to require BOR approval “for any fee or charge that is mandatory for all full-time undergraduate students or all undergraduate students in a specific degree program.”

Based on BOR’s new policy requiring BOR approval for any fee or charge that is mandatory for all full-time undergraduate students or all undergraduate students in a specific degree program, several other types of fees or charges that are currently in place at USG institutions may now be required to be reviewed and approved by BOR. For example, the Medical College of Georgia requires all students to purchase insurance from their contractor (Pearson and Pearson) at a minimum semester rate of $551. Students may apply to Pearson and Pearson to have this requirement waived if they provide the company with proof of acceptable insurance. This mandatory program has not been reviewed by or approved in the annual BOR student fee process. This is likely because it does not have the traditional characteristics of a mandatory fee-it is a required insurance program. However, since all students are required to pay the fee unless they obtain a waiver, it may now be subject to BOR’s new student fee policy.

In order to ensure that all mandatory student fees have been appropriately approved, BOR staff should develop a process to independently compare all fees actually being charged to those that have been approved by BOR.

BOR’s Response: The Board of Regents stated that it concurs “with this recommendation and will work with the institutions to develop templates to provide additional information to assist the Board of Regents with its review of mandatory student fees assessed by USG institutions. Under Board Policy, institutions can charge only those mandatory fees as approved by the Board of Regents each year. Additionally, in January 2010, three gaps in the policy have been filled to address the following provisions: (1) any charge/fee to all full-time students must be approved by the Board

BOR: Mandatory Student Fees 15

(7.3.2.2); (2) any fee that is required of all undergraduate students in a particular program of study must be approved by the Board (7.3.2.2); (3) course fees approved by the President can be used only for miscellaneous materials costs associated with the specific course (7.3.2.2). In addition to tightening the policies and clarifying what fees are submitted to the Board for approval, beginning May 2010, we will institute two additional steps to make sure that institutions do not charge any mandatory fees that have not been approved by the Board:

1. Once the Board approves the mandatory fees for each institution in April/May each year, the President of each institution will confirm in June each year the list of mandatory fees to be charged for the new academic year.

2. The budget analyst in the Office of Fiscal Affairs will verify mandatory fees listed on the institution’s website each fall.”

BOR should ensure that prior-year fee revenue surplus and fund balance information received from USG institutions is complete, accurate, and consistent.

Annually, each USG institution submits mandatory student fee requests to BOR.2 BOR requires that annual fee requests include prior-year mandatory student fee revenue, expenditures, and fund balances. BOR staff reviews this information and members of the BOR approve or deny the fee requests. Our review of annual fee requests found that the data submitted by several institutions was incomplete, inaccurate, or inconsistent. In addition, while BOR staff review the information submitted by USG institutions, they do not compare data submitted to other sources (e.g., data maintained in their financial data system) or perform analyses to detect such problems. Examples of the problems we identified are discussed below.

Incomplete- A review of the fiscal years 2008-2010 annual fee requests submitted by USG institutions to BOR revealed that institutions often fail to report required financial information.

The fee requests rarely include explanations for the purpose and/or planned use of fund balances.

Several institutions failed to report the fund balances for all of their fees. For example, Georgia Perimeter College did not report fund balance information for any of their fees in its fiscal years 2008 and 2009 fee requests; Armstrong Atlantic State University failed to report any fee fund balances in its fiscal years 2009 and 2010 fee requests; and, the University of Georgia and Kennesaw State University have not reported the technology fee fund balance for the past three fiscal years.

Georgia Institute of Technology failed to report revenues, expenditures, and fund balance information for its recreation center fee in its fiscal years 2008,

2 All institutions are required to submit information about all of their fees to BOR each year for review and approval in its “annual fee requests.” This information includes new fees as well as fees that the institution wishes to continue or increase.

BOR: Mandatory Student Fees 16

2009 and 2010 fee requests. In addition, this university also failed to report revenues and expenditures for its student activity fee in its fiscal years 2008 and 2010 requests.

Georgia Perimeter College failed to report revenue, expenditure, and fund balance information for any of its fees in its fiscal year 2009 fee request. In addition, the College continued to exclude revenue and expenditure information for its student support/center fee in the fiscal year 2010 fee request.

Inaccurate- A comparison of revenue, expenditure, and fund balance information reported in the annual fee requests with similar financial information obtained during the audit revealed the following instances in which inaccurate data was reported in the fee requests.

In its 2010 annual fee request, Georgia State University reported significantly lower fund balances in its fee request for three fees than shown in financial reports provided by the institution in response to audit requests and in information maintained in their financial system. As shown in Exhibit 10, the fund balances reported by the institution in its annual fee request were several million dollars lower than the fund balances reported on annual financial reports and recorded in the financial system.

Exhibit 10 Comparison of Reported and Actual FY 2008 Fund Balances

(Georgia State University) Fee Reported Fund Balance

(2010 Fee Request) Actual

Fund Balance Health $ 704,490 $ 5,594,804Activity $ 582,581 $ 4,998,926

Technology $ 274,562 $ 3,069,564

Source: BOR data, USG institution financial data

In its annual fee requests, Georgia Southern University has consistently understated the potential revenue from the recreation facility fee and recreation center expansion fee. As shown below, the University provided revenue estimates lower than actual revenue received in prior years even though the previous fee rate was either the same or lower.

o For fiscal year 2008, the University requested a $6 increase in recreation fees (from a total of $134 per semester to $140 per semester). The request stated that the increase was needed to allow the newly expanded recreation facility to be fully staffed and to pay all operational expenses. The request included projected fiscal year 2008 revenues of $3.9 million without the increase (at the $134 rate) even though in fiscal year 2006, $3.9 million in revenue generated with a lower fee rate of $128. The University was not anticipating a decline in enrollment.

o For fiscal year 2010, the University requested a $2 increase in recreation fees (from a total of $140 per semester to $142 per

BOR: Mandatory Student Fees 17

semester). In the request, the University stated that the increase was needed to cover increases in operating costs and that without the increase spending “would likely result in a deficit during fiscal year 2010.” To justify this increase, the University projected that recreation fee revenue would total $4.4 million without a fee increase; however, the actual fiscal year 2008 revenue from the fee at the same rate was over $4.8 million. In addition the fiscal year 2009 recreation fee revenue was over $5.1 million. The revenue projection for fiscal year 2010 appears to be unreasonably low; thus, the fee rate increase request does not appear to provide valid data.

In its 2010 annual fee request, Columbus State University reported significantly higher expenditures for the transportation fee than was subsequently reported by the University in response to audit questions. The University reported fiscal year 2007 expenditures to be $152,015 but subsequently reported to auditors that the expenditures were only $32,618, accounting for only 12% of fee revenue.

Inconsistent- In the annual fee request, each USG institution is required to identify revenues and expenditures for each fee type. Three of the 35 USG institutions include the prior-year reserves or fund balance as available revenue. BOR should require USG institutions to submit data that is consistent from institution to institution to facilitate analysis.

Fund Balances After we compiled revenue, expenditure, and fund balance information for each fee and USG institution and presented this information to BOR staff, they requested that each institution provide them with explanations for annual revenues that significantly exceed expenditures and the planned uses of significant fund balances. While the institutions subsequently provided explanations for surpluses and fund balances, it is apparent that this information had not routinely been provided to BOR during the annual fee request process. As shown in the examples below, many of the explanations provided by USG institutions failed to identify the exact amount of the fund balances that would be used for the various plans mentioned or the timeframe within which the funds would be spent. It also appears that some of these balances have been accumulating without specific plans that identify the desired amount of fund balance it would like to achieve and the intended use of the resulting balance.

At Georgia Southern University, the recreation center fee fund balance has grown to over $5.3 million over the past four years. In response to a BOR inquiry prompted by this audit, the University stated that $3 million of the fund balance is committed to a capital renovation project for another facility. The recreation center expansion fee was established in fiscal year 2005 to specifically fund the construction and operating cost of a new/expanded recreation center. It is not evident that the fee was established to also fund an additional capital project. In addition, the University requested fee rate increases over the past three years with the stated purpose of covering increased operating costs. The University stated in the fee rate requests that without the rate increases, its spending would likely result in a deficit. In the fiscal year 2008 request, the University stated

BOR: Mandatory Student Fees 18

that $1 million of the reserve was needed for outdoor lighted fields surrounding the recreation facility and that another $1 million was needed for equipment. No mention is made in this request or any subsequent request of the necessity to increase fees with the purpose of building a fund balance to pay for any other capital improvements.

At Georgia State University, the recreation center fee fund balance has grown to over $10 million. According to the explanation provided to BOR, the University plans to use the reserve for major repairs that are needed on the 10-year old building. However, the amount of the reserve that is needed for this purpose was not provided. In addition, the timeframe within which the reserve funds will be spent was also not provided.

The activity fee fund balance at Georgia State University has grown to almost $5 million. The explanation provided to BOR indicated that the reserves will be used to replace the university’s radio tower and to upgrade the radio station to a digital format. The cost and timeframe of these projects was not provided.

The activity fee fund balance at Georgia Southern University has grown to over $2 million. In response to BOR inquiry resulting from this audit, the university stated that it plans to use the fund balance in fiscal years 2010 and 2011 to fund large-scale student programming such as a spring concert, a lecture series, and other similar activities. It should be noted that such activities are associated with typical operating costs for student activities and that once these funds are expended in fiscal years 2010 and 2011 there will be insufficient funds to continue similar activities in future years. It is a questionable practice to build a fund balance over several years with the intent of spending the funds for higher level operations for only a one or two year period.

BOR should ensure that institutions provide complete, accurate, and consistent information in the annual fee rate requests. Without such information, there is no assurance that the fee rates are set at reasonable levels or that fee increases are necessary.

BOR response: The Board of Regents stated that it “concurs with this recommendation and will develop further processes that ensure that reported fund balances are complete, accurate and consistent, as well as provide institutions with the opportunity to explain circumstances that may clarify the presence of a fund balance variation from pro-forma and/or five-year business plan projections.”

The Board of Regents did “not agree that the fund balances were inaccurate simply because they were inconsistently stated across institutions. There are two interpretations of what a fund balance represents: (1) total fund balance and (2) available fund balance. Institutions often report the available fund balance, which is the most relevant amount for analysis, so as not to mislead the reader into believing that there are more available funds than actually exists.” However, the Board of Regents stated that it is modifying the fee requests to be consistent across institutions.

BOR: Mandatory Student Fees 19

Audit Response: We did not intend to imply that fund balances were inaccurate simply because they were inconsistent. We noted instances where the amount of the fund balances were inaccurately reported to BOR. A separate issue was that fund balance data reported to BOR was not consistently defined from institution to institution.

To ensure that members of BOR have sufficient information to determine if fee increases are necessary, they should be provided with better data regarding annual fee surpluses and the planned uses for fund balances when considering annual fee rate requests.

As discussed in the previous finding, USG institutions are required to submit student fee revenue, expenditures, and fund balance information each year to BOR for review. This data, however, is not used by BOR staff to generate multi-year trends that would reveal fee surpluses over time. In addition, BOR staff do not obtain explanations from many USG institutions regarding the planned use of or necessity for persistent and significant revenue surpluses and fund balances. As a result, it unlikely the members of the Board are provided with information needed to make fully informed decisions regarding fee requests.

Our review and analysis of fee revenues revealed that the majority of mandatory fee revenue generated across the USG is expended within the year the fees were collected. As shown in Exhibit 11, on average, at least 80% of fees are expended for most fee categories in fiscal years 2007 and 2008.

Fee Type FY 2007 FY 2008

Access/ID Card 101% 90%

Student Activity 90% 88%

Athletic 99% 99%

Health 81% 80%

Parking 96% 68%

Recreation 97% 85%

Student Center/Facility 69% 79%

Technology 94% 89%

Transportation 97% 87%

Other 84% 108%

Exhibit 11Average % of Fee Revenue Expended

Source: BOR data

While it is difficult to determine whether the level of expenditure or a given fund balance is appropriate without an explanation of their intended use, analyses that identify trends and fund balances are important to making decisions about whether

BOR: Mandatory Student Fees 20

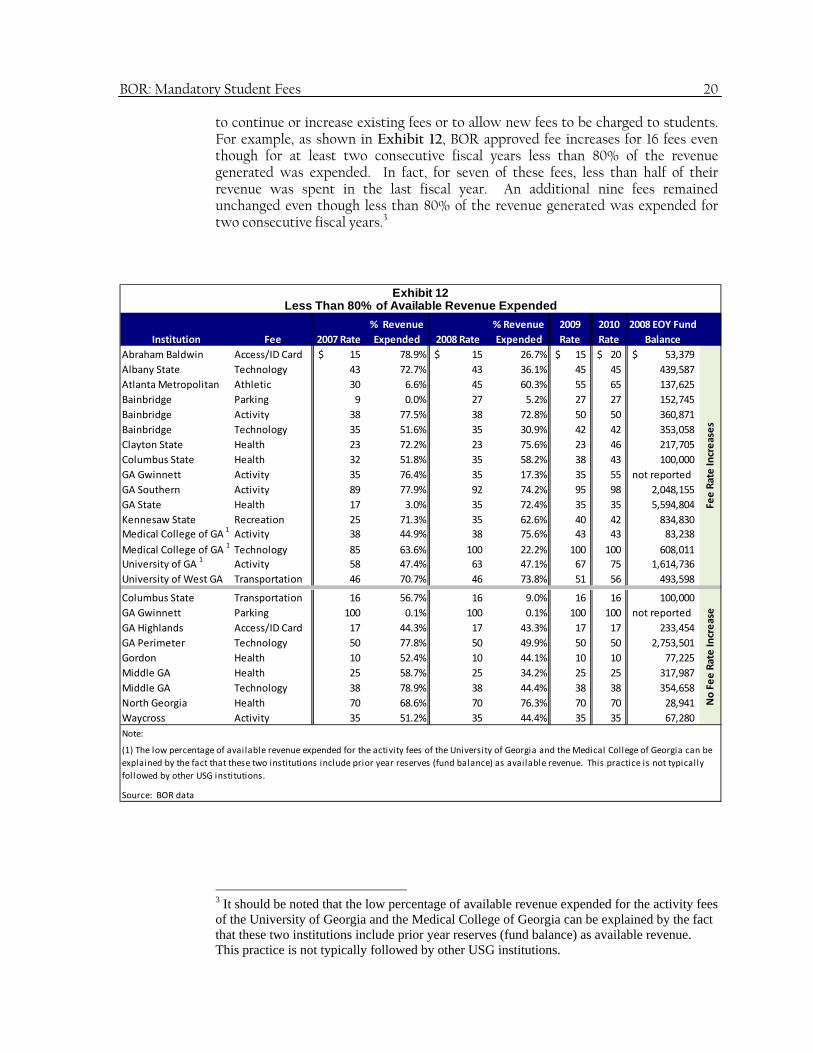

to continue or increase existing fees or to allow new fees to be charged to students. For example, as shown in Exhibit 12, BOR approved fee increases for 16 fees even though for at least two consecutive fiscal years less than 80% of the revenue generated was expended. In fact, for seven of these fees, less than half of their revenue was spent in the last fiscal year. An additional nine fees remained unchanged even though less than 80% of the revenue generated was expended for two consecutive fiscal years.3

Institution Fee 2007 Rate

% Revenue

Expended 2008 Rate

% Revenue

Expended

2009

Rate

2010

Rate

2008 EOY Fund

Balance

Abraham Baldwin Access/ID Card 15$ 78.9% 15$ 26.7% 15$ 20$ 53,379$

Albany State Technology 43 72.7% 43 36.1% 45 45 439,587

Atlanta Metropolitan Athletic 30 6.6% 45 60.3% 55 65 137,625

Bainbridge Parking 9 0.0% 27 5.2% 27 27 152,745

Bainbridge Activity 38 77.5% 38 72.8% 50 50 360,871

Bainbridge Technology 35 51.6% 35 30.9% 42 42 353,058

Clayton State Health 23 72.2% 23 75.6% 23 46 217,705

Columbus State Health 32 51.8% 35 58.2% 38 43 100,000

GA Gwinnett Activity 35 76.4% 35 17.3% 35 55 not reported

GA Southern Activity 89 77.9% 92 74.2% 95 98 2,048,155

GA State Health 17 3.0% 35 72.4% 35 35 5,594,804

Kennesaw State Recreation 25 71.3% 35 62.6% 40 42 834,830

Medical College of GA 1Activity 38 44.9% 38 75.6% 43 43 83,238

Medical College of GA 1Technology 85 63.6% 100 22.2% 100 100 608,011

University of GA 1

Activity 58 47.4% 63 47.1% 67 75 1,614,736

University of West GA Transportation 46 70.7% 46 73.8% 51 56 493,598

Columbus State Transportation 16 56.7% 16 9.0% 16 16 100,000

GA Gwinnett Parking 100 0.1% 100 0.1% 100 100 not reported

GA Highlands Access/ID Card 17 44.3% 17 43.3% 17 17 233,454

GA Perimeter Technology 50 77.8% 50 49.9% 50 50 2,753,501

Gordon Health 10 52.4% 10 44.1% 10 10 77,225

Middle GA Health 25 58.7% 25 34.2% 25 25 317,987

Middle GA Technology 38 78.9% 38 44.4% 38 38 354,658

North Georgia Health 70 68.6% 70 76.3% 70 70 28,941

Waycross Activity 35 51.2% 35 44.4% 35 35 67,280

Note:

Source: BOR data

(1) The low percentage of available revenue expended for the activity fees of the University of Georgia and the Medical College of Georgia can be

explained by the fact that these two institutions include prior year reserves (fund balance) as available revenue. This practice is not typically

followed by other USG institutions.

No Fee Rate Increase

Fee Rate Increases

Exhibit 12Less Than 80% of Available Revenue Expended

3 It should be noted that the low percentage of available revenue expended for the activity fees of the University of Georgia and the Medical College of Georgia can be explained by the fact that these two institutions include prior year reserves (fund balance) as available revenue. This practice is not typically followed by other USG institutions.

BOR: Mandatory Student Fees 21

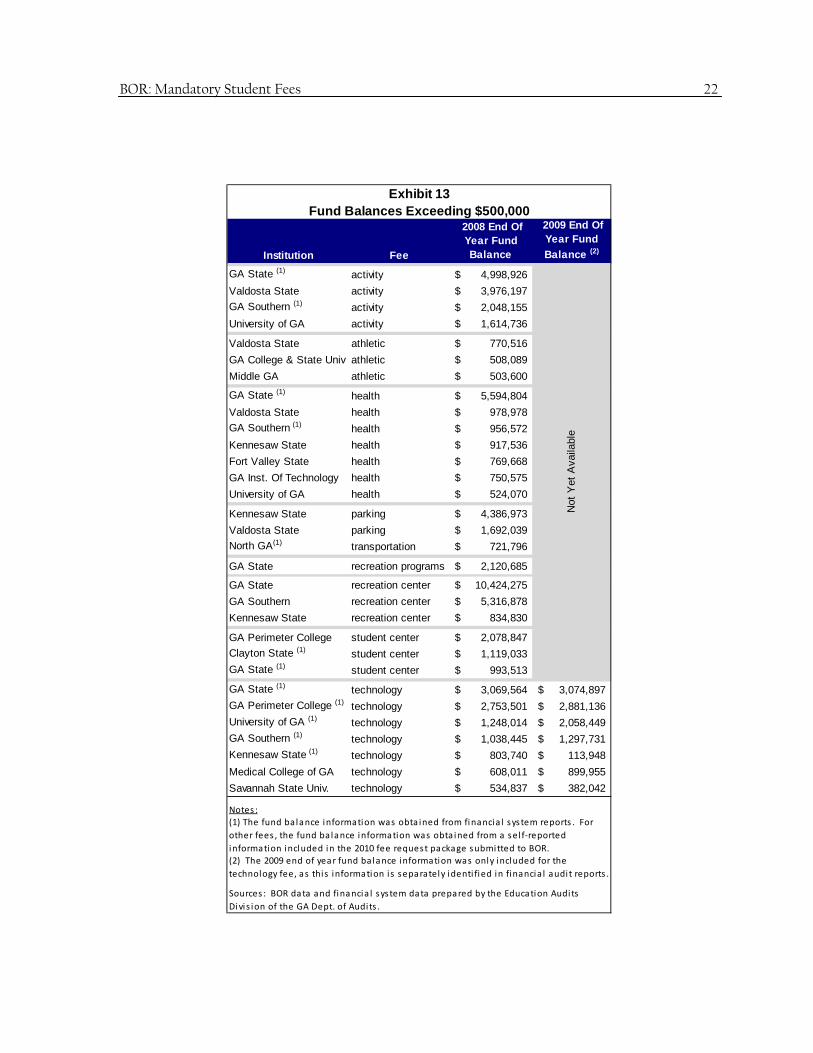

In addition to analyzing the annual expenditure of fee revenues, we conducted an analysis of fund balances to identify the highest balances. As shown in Exhibit 13 on page 22, we identified 31 fees that had more than $500,000 in reserves at the end of fiscal year 2008. In some cases, these fund balances may be necessary to make future debt service payments on facilities that are supported by mandatory student fees. Institutions may also be accumulating large fund balances to fund future capital improvements. (However, the planned use and the timeframe within which these funds will be used are not typically included in the annual fee request packages submitted by USG institutions to BOR.) It should be noted, however, that some of these fund balances are associated with fees that do not support capital improvements. For example, activity fees at Georgia Southern University and at Georgia State University and the recreation programming fee at Georgia State University are not associated with debt service obligations or capital improvement projects.

BOR staff should develop additional analyses related to mandatory student fees to help determine if fee rates are reasonable. These analyses should include a review of the percentage of revenues actually expended. In addition, the necessity of fund balances should be reviewed. During the annual fee rate review and approval process, BOR members should be provided with the results of such analyses.

BOR response: The Board of Regents agrees with this recommendation. “The Board of Regents should have all of the necessary information to determine if a fee increase request from an institution is to be approved. This includes (1) the planned use of the fee; (2) the projected revenues and expenditures; (3) student support; and (4) funds available on hand to support the planned use. In the interest of transparency, supplemental information will be provided to the Board beginning May 2010 on all of these elements.

Beginning with the FY 2012 fee cycle, the analysis of the institutional fee requests will include a comparison of the actual fund balance with the projected fund balance and the corresponding needs and priorities. Where actual fund balances exceed institutional projections, institutions will be asked to substantiate the need for a fee increase in light of the additional funds on hand at the institution.”

BOR: Mandatory Student Fees 22

Institution Fee

2008 End Of Year Fund Balance

2009 End Of Year Fund

Balance (2)

GA State (1) activity 4,998,926$

Valdosta State activity 3,976,197$

GA Southern (1) activity 2,048,155$

University of GA activity 1,614,736$

Valdosta State athletic 770,516$

GA College & State Univ athletic 508,089$

Middle GA athletic 503,600$

GA State (1) health 5,594,804$

Valdosta State health 978,978$

GA Southern (1) health 956,572$

Kennesaw State health 917,536$

Fort Valley State health 769,668$

GA Inst. Of Technology health 750,575$

University of GA health 524,070$

Kennesaw State parking 4,386,973$

Valdosta State parking 1,692,039$

North GA(1) transportation 721,796$

GA State recreation programs 2,120,685$

GA State recreation center 10,424,275$

GA Southern recreation center 5,316,878$

Kennesaw State recreation center 834,830$

GA Perimeter College student center 2,078,847$

Clayton State (1) student center 1,119,033$

GA State (1) student center 993,513$

GA State (1) technology 3,069,564$ 3,074,897$

GA Perimeter College (1) technology 2,753,501$ 2,881,136$

University of GA (1) technology 1,248,014$ 2,058,449$

GA Southern (1) technology 1,038,445$ 1,297,731$

Kennesaw State (1) technology 803,740$ 113,948$

Medical College of GA technology 608,011$ 899,955$

Savannah State Univ. technology 534,837$ 382,042$

Notes :

Sources : BOR data and financia l system data prepared by the Education Audits

Divis ion of the GA Dept. of Audits .

Not

Yet

Ava

ilabl

e

(1) The fund balance information was obta ined from financia l system reports . For

other fees , the fund balance information was obta ined from a sel f‐reported

information included in the 2010 fee request package submitted to BOR.

(2) The 2009 end of year fund balance information was only included for the

technology fee, as this information i s separately identi fied in financia l audit reports .

Exhibit 13Fund Balances Exceeding $500,000

BOR: Mandatory Student Fees 23

BOR should develop a policy that requires USG institutions to seek input from the appropriate student fee advisory committee and approval from BOR if an institution substantially changes the use of an existing fee.

BOR policies require that institutions present the purpose and intended use of any new student fees or fee increases to their respective fee advisory committees and to BOR. Currently, if an institution changes the use of an existing fee, there is no such approval requirement specified in BOR policies. While most mandatory student fees at the seven institutions we reviewed appear to be used for their approved purpose, at four of the seven institutions, some fees were found to either not be used for their approved purpose or that the institution is planning to use the funds in a manner that was significantly different than the stated purpose. Examples of these differing uses are detailed below. University of Georgia Recreation Facility Fee: In 1989, a $33 per quarter ($50 per semester) facility fee was approved through referendum by the student body to support the financing associated with the construction of the Ramsey Center.4 Informational materials distributed to students prior to the referendum earmarked this fee specifically for the Ramsey Center. The scheduled debt retirement date for the Ramsey Center is 2013; therefore, 2013 is the last year that lease/debt service payments will be made for the center. However, the University is not intending to “sunset” the recreation center fee in 2014. Instead, the University is planning to use $2.5 million of the revenue generated by this fee for lease/debt service payments associated with the renovation and expansion of the Tate Student Center. While students and BOR did vote to approve a $25 increase in student fees to fund the renovation and expansion of the Tate Student Center, neither BOR nor the students specifically approved the continuation of the $50 fee associated with the Ramsey Center to be used to help fund the Tate Student Center. According to UGA administrators, students and BOR were aware that the Ramsey Center fee would continue after debt retirement and that its revenue would be used to fund the Tate Student Center expansion. However, there is no evidence that either party was provided with this information or given the option to vote to continue the Ramsey Center fee and to use a portion of this revenue for the new project. Because the original $50 per semester recreation facility fee was approved by referendum for the financing and operations associated with the Ramsey Center, the fee should be reduced in 2014 to reflect only associated operating costs when debt service payments are no longer necessary.

University of West Georgia Transportation Fee: A portion of the transportation fee at the University of West Georgia is used to make debt service payments for parking lots related to the new Greek Village housing project. In fiscal year 2007, the transportation fee was increased by $20 and in fiscal year 2009 another $10 increase was requested (only $5 was approved). A portion of

4 While BOR policy only requires that USG institutions obtain student input regarding new and increased mandatory student fees from mandatory student fee advisory committees, for this fee, the University of Georgia allowed the student body to vote on the implementation of the fee through a referendum.

BOR: Mandatory Student Fees 24

these increases were necessary to enable the University to use $250,000 in 2009 to over $606,000 in 2039 of transportation fee revenue to make annual debt service payments for the project. However, the documentation submitted to BOR requesting approval for these fee increases did not include reference to these debt service payments or to the Greek Village project. Instead, the reason provided was that the increase was necessary to replace reserves, to purchase new buses, and to build funds for a new parking lot-indicating that no debt would be incurred. Since the exact amount of the transportation fee increase that was necessary to generate the revenue for the annual lease payments was not separately identified in the request, it is unlikely that these fees will be set to expire upon retirement of the debt.

Valdosta State University Multi-Use Stadium Fee: VSU planned on constructing its own football stadium instead of continuing to use the local high school stadium which was in need of repairs and renovation. A fee increase of $20 for a “multi-use stadium” was presented to VSU’s mandatory student fee advisory committee and approved by BOR to be effective fall semester 2006. Subsequent to this approval, VSU opted to use revenue generated by this fee to finance the construction of an intercollegiate athletic field house and practice fields. Although BOR approved the rental agreement for the field house in June 2007 with the understanding that revenue from the “multi-purpose stadium” fee would be used for lease payments, there is no evidence that this change was formally presented to or approved by the University’s mandatory fee advisory committee. In fact, the 2010 list of mandatory student fees presented to BOR and tuition and fee information provided to students still identify this fee as a “multi-use stadium” fee.

Georgia Gwinnett College Recreation Programming Fee: A new $60 recreation programming fee was presented to the student fee advisory committee and approved by BOR in April 2009 (for $30) to become effective fall semester 2009. In their presentation to the student fee advisory committee, GGC administrators stated that the fee would be used to provide funding for recreational activities such as outdoor adventure excursions. However, over the next several years, a large amount of the revenue generated by the fee will not be available for recreation programming. Due to lower than anticipated student enrollment, the existing $40 recreation fee (established to fund the acquisition and renovation of the fitness center) will be inadequate to pay for the rental and operating costs of the fitness center. As a result, GGC administrators plan to use revenue from the new $30 recreation programming fee to help cover such costs for the next several years. It is not apparent that the student advisory committees or recreation staff was made aware that these funds would not be immediately available for recreation programming.

In addition to the above examples, administrators at three of the seven institutions we visited stated that they would likely find new uses for mandatory student fees that were no longer needed for debt service payments rather than ending the fees or reducing the fee amount. In fact, a president at one institution stated that in situations where a fee was no longer needed for debt service payments, the fee should continue to be charged and be used for another purpose since students were already used to paying the fee. In order to improve transparency and accountability, BOR should develop a policy

BOR: Mandatory Student Fees 25

that requires USG institutions to seek approval from both the student fee advisory committee and BOR if an institution substantially changes the use of an existing fee. BOR should also consider implementing a policy that requires fees to expire when they are no longer deemed necessary for the purpose for which they were established. If the institution identifies better uses for fee revenue, it should be required to obtain approval for a new fee for such purposes rather than continuing the older obsolete fee. BOR response: The Board of Regents stated that it “will extend the current mandatory student fee process regarding new mandatory fees and mandatory fee increases to include any substantial change in the use of a fee. A policy change to this effect will be presented to the Board for consideration.”

Questionable Transactions

In general, the mandatory student fee expenditures that were reviewed appeared to be appropriate and properly documented; however, at three institutions we found expenditures that were either not appropriate or not properly documented.

BOR policies require that all payments from funds supported by mandatory fees be made according to approved business procedures of the institution. The purpose of these policies is to ensure that student fee expenditures are appropriate and properly documented. We reviewed a sample of student fee expenditures at seven institutions and found that these transactions were generally appropriate and properly documented. However, at three institutions we found transactions that were either not appropriate or not properly documented. These transactions involved the use of student activity fees to fund ineligible programs, to provide improperly reconciled cash advances to faculty members, or to fund excessive/unnecessary travel for faculty, staff members and students. These issues have been reported to each institution and/or BOR and have either been corrected or are under consideration for correction. These transactions are discussed below.

Ineligible Programs/Functions Funded with Student Fee Revenue At Armstrong Atlantic State University (AASU), some programs that are not eligible to receive funding from student activity fees received student activity fee revenue. In addition, also at AASU, the University had utilized technology fee revenue to support administrative functions of the University which are specifically prohibited by BOR guidelines. These situations are detailed below.

At the time of our review, several programs were identified as having mistakenly received student fee revenue. These programs, which have separate revenue sources, include: HOLA (Hispanic student recruiting program funded by a foundation); counseling and career services (funded by state funds); Navigate/orientation (funded by a separate orientation fee); and, a stipend for honor students studying abroad (no other funding source). According to University administrators, expenditures for these programs that exceeded revenue from these other funding sources were covered with student activity fee revenue because all the programs were accounted for in

BOR: Mandatory Student Fees 26

the same student activity fee fund. AASU administrators stated that the programs would be moved out of Fund 13000 (Student Activity Fee Fund).

BOR has disseminated guidelines to USG institutions regarding the appropriate use of technology fee revenue. The guidelines state that “the focus of student technology fees should be on academic or instructional technology and distinctions should be drawn between expenditures for administrative applications or scientific and laboratory equipment, and instructional technology.” The guidelines also clarify that “in almost no cases should technology fee revenues be used for administrative software or software implementation” (such as BANNER or PeopleSoft). However, in fiscal year 2008, AASU spent over $150,000 in student technology fee revenue to pay for expenses related to the renewal and maintenance of the University’s accounting software, PeopleSoft. While AASU does not have a fee allocation committee, its new Chief Information Officer (CIO) has developed preliminary budgets which will no longer use fee revenue to fund administrative items such as PeopleSoft.

Inadequately Reconciled Cash Advances Cash advances from student activity fee revenue routinely provided to a faculty member at Armstrong Atlantic State University and to a faculty member at the University of West Georgia were not sufficiently reconciled to ensure that the funds were appropriately used.

At AASU, one faculty member routinely received $600 in cash to pay for various supplies needed for the production of plays. However, the receipts provided by the faculty member to AASU’s financial office either do not account for the entire $600 advance or are dated as far as a year prior to the “advance.” For example, no receipts were provided to account for two $600 advances and receipts submitted for another two $600 advances only accounted for about half of the advance. AASU administrators stated that these transactions may not have received an adequate level of scrutiny because they were not processed as travel-related expenses. Typically, cash advances are provided to faculty and staff members as “travel” transactions and are “flagged” in the financial system as requiring reconcilement within a specified time period. These transactions were completed as ordinary expense reimbursement and, thus, were not flagged for subsequent reconciliation.