Embed Size (px)

Citation preview

1

The pan-European Distributor

Brammer plc

Agenda• Financials• About Brammer• Growth

– Market Segmentation– Key Accounts– Insites™– Product Range Extension– Strategy

• The Future• Questions

2

3

Half Year Results6m to 30th June 2011• Turnover up £45.2m, up 19.7%. At constant currency,

turnover increased £42.0m (18.8%). There were no acquisitions

• Profit before tax up £4.6m from £9.7m to £14.3m*• New banking facilities for €100m in place to 2016• Interest covered 13.45x (June 2010 8.4x)• Net debt to EBITDA ratio 1.27x (June 2010 1.56x)• Net borrowings compared to H1 2010 is up £0.4m to

£40.6m after absorbing £4.7m adverse currency impact

* before amortisation of acquired intangibles

4

Half Year Results6m to 30th June 2011

• Turnover higher by 19.7%• Profit before tax of £14.3m – up 47%*• Basic eps up from 6.4p* to 10.0p (up 56%)• Dividend: 2.7p per share up from 2.1p (up

28.6%)

* all stated before amortisation of acquired intangibles

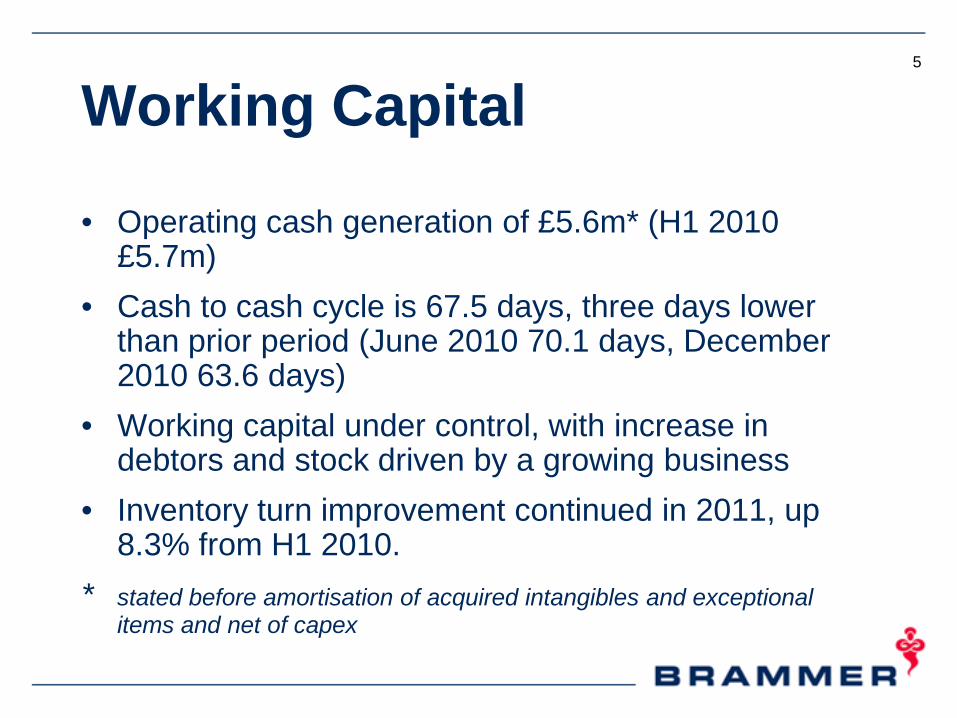

5

Working Capital

• Operating cash generation of £5.6m* (H1 2010 £5.7m)

• Cash to cash cycle is 67.5 days, three days lower than prior period (June 2010 70.1 days, December 2010 63.6 days)

• Working capital under control, with increase in debtors and stock driven by a growing business

• Inventory turn improvement continued in 2011, up 8.3% from H1 2010.

* stated before amortisation of acquired intangibles and exceptional items and net of capex

6

Half Year Results6m to 30th June 2011

7

Half Year Results6m to 30th June 2011

8

Half Year Results: Ratios6m to 30th June 2011

* Segmental assets including goodwill less liabilities, before current & deferred tax, dividends, cash, loans, deferred consideration & pension liability

** Underlying operating profit as a percentage of operating capital as defined in * but excluding goodwill & acquired intangibles

*** Underlying operating profit as a percentage of operating capital as defined in *

9

Half Year Results:6m to 30th June 2011

£m H12009 2010 2011

Underlying operating profit - as reported* 8.8 11.0 15.4

Excluding effect of Bonus - 2.3 3.8Share option related charges (0.1) - 1.7

Adjusted operating profit 8.7 13.3 20.9

Return on sales (adjusted) 4.0% 5.8% 7.6%

*stated pre amortisation and exceptionals items

10

Cash Flow6m to 30th June 2011

11

Working Capitalat 30th June - Actual Rates

12

Working Capitalat 30th June 2011

Cash to cash cycle

13

Balance Sheetat 30th June – Actual Rates

14

Half Year Results: RatiosSegments: 6m to 30th June 2011

£m UK DE FR ES Blux Eeu Other Fx Total

Turnover 79.6 58.9 42.6 22.4 24.8 28.7 9.0 9.2 275.2

Turnover growth/(decline) (SPWD) 16.5% 21.9% 15.4% 14.4% 14.6% 26.0% 16.1% 18.1%

Underlying operating profit 4.2 3.6 1.9 1.8 1.5 2.0 0.0 0.4 15.4

Return on sales 5.3% 6.1% 4.5% 8.0% 6.0% 7.0% 0.0% 5.6%

Return on sales H1 2010 4.2% 5.2% 4.2% 7.5% 5.0% 5.2% 1.2% 4.8%

Capital employed * 15.1 15.2 9.1 5.0 11.4 16.7 12.6 5.3 90.4

Return on capital employed 55.6% 47.4% 41.8% 72.0% 26.3% 24.0% 0.0% 34.2%

Return on capital employed H1 2010

40.0% 31.9% 36.0% 65.2% 19.5% 15.2% 1.8% 27.8%

* Segmental assets excluding goodwill and acquired intangibles less liabilities, before exceptional provisions, current & deferred tax, dividends, cash, loans, deferred consideration & pension liability

15

Exchange Rates

Jun-11 Dec-10 Jun-10

Average € 1.146 € 1.165 € 1.153

Closing € 1.107 € 1.167 € 1.221

16

Brammer plc

2011

17

Brammer plc

The European Leader in Mechanical MRO Supplies

and Services

Agenda• Financials

• About Brammer• Growth

– Market Segmentation– Key Accounts– Insites™– Product Range Extension– Strategy

• The Future• Questions

18

About Brammer• European market leader – <3%

market share

• Focused product range in mechanical MRO components - a €25 billion market• Bearings• Mechanical Power Transmission• Fluid Power• Tools and General Maintenance• Added value services

19

About Brammer• Leading the process of consolidation

in a highly fragmented market

• Diverse customer base of over 100,000 customers

• Customer risk is low

• Top 10 customers in any one country typically account for less than 10% of sales

• Largest European customer of our main strategic suppliers

20

• 2,559 people

About Brammer21

• 2,559 people• Over 300 locations

About Brammer22

• 2,559 people• Over 300 locations• In 15 countries

across Europe

About Brammer23

• 2,559 people• Over 300 locations• In 15 countries

across Europe• With over 4,300,000

products from the world’s leading suppliers

About Brammer24

• 2,559 people• Over 300 locations• In 15 countries

across Europe• With over 4,300,000

products from the world’s leading suppliers

• Working in your industry

About Brammer25

Brammer – Our Strategy

Growth Capability Costs SynergiesCountry organic growth

People Development

Supplier Rationalisation

Business Best Practice

Key Accounts Business Skills Development European Buying Systems

Integration

Insites

Distributed Learning Programme Development

IT and Other Cost Reductions

Brand Development

Product range extension

Internal Communications and Involvement

Capital Employed Management

Supplier Relationship Management

Geographical development

26

Growth ObjectiveThe Market Opportunity

Bearings2.0bn

Seals0.5bn

MPT 5.0bn

Tools and Gen. Maintenance

10.0bn

Fluid Power10.0bn

27

28

Growth

Market Segmentation

Market SegmentationCurrent Segments

• Food & Drink• Pulp, Paper & Packaging• Construction & Aggregates• Utilities• Recycling• Automotive• Refining• Metals

29

Market Segmentation• H1 2011 continued focus on

implementing material over the last 7 years

• Training programme developed including online and face-to-face learning

• Building on success

• Customer testimonials leading to segment leadership

30

Market Segmentation• Sales to targeted segments have

continued to deliver strong growth

• Food & Drink grew by £8.8 million, or 35.9%, to £33.3 million

– UK up by 60.3% to £15.1 million– DE up by 29.4% to £2.6 million– NL up by 57.8% to £1 million– ES up by 21.2% to £3.6 million

• Automotive grew by 46.2% to £24.7 million

• Metals grew by 33.6% to £33.4 million

31

32

Growth

Key Accounts

33

Key Accounts Sales Performance 2011

YTD June 2011 Total

Multi-Site Status Scope Year variance TotalYTD 2010 € Value 32.580.107YTD 2011 € Value 43.729.003

YTD 2010 € Value 36.757.092YTD 2011 € Value 42.726.367

YTD 2010 € Value 9.050.058YTD 2011 € Value 11.538.562

YTD 2010 € Value 20.158.715YTD 2011 € Value 24.373.326

YTD Total 2010 € Value 98.545.972YTD Total 2011 € Value 122.367.258

Tier 4

Tier 3

Tier 2

Tier 1

National ContractNational Group

No Contract Part EU Group

EU Contract 34,2%Part EU Group

16,2%

20,9%

27,5%

24,2%

National Contract Part EU Group

Brammer

Key Accounts• 6 new contracts won

– Beckton & Dickinson– Delphi– Georgia-Pacific– Johnson Controls– Rockwool– Whirlpool

• 24.2% growth overall • 2,279 documented customer cost savings

yielding €23m (£19.2m) for our customers• “turbo boost” contract implementation to

achieve Brammer guaranteed savings a continuing theme

34

Reference List of Pan-European Supply Agreements

35

Key Accounts

• New Key Account Toolkit implemented– Latest best practice gathered

to update toolkit– Processes and tools defined

in a procedures manual -mandatory approach developed

36

Key Accounts– Particular emphasis on those

tools and processes which will accelerate contract implementation – “turbo boosting”

– Regular review and consistent approach across Europe

37

Key Accounts• Continued focus on key sectors

of expertise

– Food & Drink up 20.3% to €30.3 million

– Automotive up 42.7% to €21 million

– FMCG up 46% to €4.7 million– Chemical up 7.6% to €3.6 million– Packaging up 29.1% to €6.6

million

38

39

Growth

Insites™

What is an Insite™?Definition• A self contained Brammer

office on a customer’s site• Provided by the customer• With a direct link to the

Brammer ERP systems and stock

• With agreed menu of services

40

Definition of Insites™ Full Time• One or more BRAMMER

personnel working within their own clearly established workspaces

• Minimum of 4 hours a day, 5 days a week

• Services provided can be a combination of:

– Creation of stock profile– Purchasing management– Technical advice– Sales visits– Delivery services

41

Definition of Insites™ Part time• One or more BRAMMER

personnel working within their own clearly established workspaces

• Minimum of 3 hours a day, 2 days a week

• Services provided can be a combination of:

– Any of the activities offered by a full-time Insite– Creation of stock profile– Purchasing management– Technical advice– Sales visits– Delivery services

42

Insites™

• Insite™ Development– 22 new Insites™ (11 FT/11 PT)

16 Full-Time53 Part-Time(47 closed due to factory closures)

– 244 Insites™ across the Group94 Full-Time150 Part-Time

– Increase of 28.4% to £43.2 million

43

44

Growth

Product Range Extension

BearingsLinear MotionSealsBelts and PulleysChains and SprocketsHealth and SafetyTools and MaintenanceGearboxesMotorsFluid Power

Mechanical Power Transmission –Chains & Sprockets

Seals

Tools &Maintenance

Product Range ExtensionHealth andSafety

Gearboxes

Linear Motion -Industrial AutomationMotors

BearingsFluid Power

Mechanical Power Transmission -Belts & Pulleys

45

Product Range Extension• New product range introduction

continues on the continent

• At constant rates Bearings are up 16.5%, Non-bearings are up 20%

• Continued focus on Fluid Power and Tools & Maintenance throughout continental Europe

• New European Product Group Manager – Fluid Power

• New European Product Group Manager - Tools & Maintenance

46

Product Range Extension• Catalogue supporting Tools and General

Maintenance and Fluid Power launched in France, Spain, Germany & Austria

– Mechanical Power Transmission up 12.1% to £37.1 million

– Fluid Power up 24.8% to £44.6 million

– Tools & General Maintenance up 28.3% to £17.6 million

• Huge opportunity for further growth through cross-selling

– 0.7% market share in Tools and General Maintenance

– 1% share in Fluid Power compared with 10% share in Bearings.

47

Product range Extension• Cross-selling continuing

to benefit base business

• Overall first half growth of 19.7%

– 24.2% in Key Accounts– 15.6% growth in base

business

48

Product Range Extension• Base business growth

of 15.6% driven by

– 21.2% growth in Fluid Power

– 22.1% growth in Tools & General Maintenance

– 25.2% growth in Fasteners and Standard Parts

49

50

Growth

Strategy

The results of our Growth Strategy

Sales per Working Day - Growth

% 2007 2008 Q1-09 Q2-09 Q3-09 Q4-09 Q1-10 Q2-10 Q3-10 Q4-10 Q1-11 Q2-11 YTD-11

UK 12.5% 8.3% 3.4% -1.8% -3.6% 0.9% 5.4% 6.1% 11.7% 9.0% 15.6% 17.4% 16.5%

Germany 17.4% 8.1% -22.9% -37.9% -35.1% -26.3% -6.5% 18.1% 24.5% 22.7% 22.8% 21.1% 21.9%

France 8.6% 9.4% -14.7% -21.8% -15.8% -4.9% 4.1% 14.9% 13.2% 12.7% 12.8% 18.0% 15.4%

Spain 6.7% 8.3% -24.7% -24.7% -26.9% -10.8% 0.3% 14.0% 9.4% 15.1% 14.6% 14.2% 14.4%

Netherlands 18.5% 11.4% -12.8% -23.2% -13.8% -16.1% 3.5% 13.8% 8.5% 15.7% 16.9% 19.5% 18.2%

Poland - - 9.3% 0.7% 7.5% -0.7% -1.2% 27.7% 24.9% 27.4% 32.9% 17.8% 24.6%

Total 20.3% 12.0% -10.8% -21.7% -19.8% -11.4% -0.1% 14.3% 18.0% 15.7% 17.8% 18.3% 18.1%

51

Acquired Businesses

• No new businesses acquired in 2011• Selective bolt-ons being considered• No new territories planned at this stage• We would look to fund acquisitive

growth by free cash flow

52

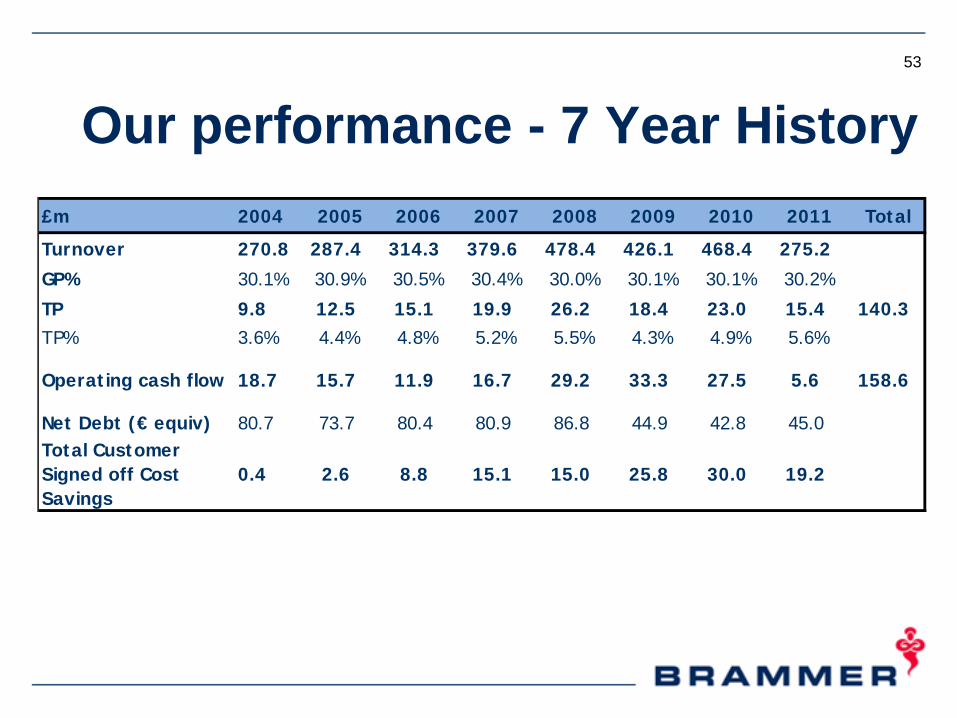

Our performance - 7 Year History

£m 2004 2005 2006 2007 2008 2009 2010 2011 Total

Turnover 270.8 287.4 314.3 379.6 478.4 426.1 468.4 275.2

GP% 30.1% 30.9% 30.5% 30.4% 30.0% 30.1% 30.1% 30.2%

TP 9.8 12.5 15.1 19.9 26.2 18.4 23.0 15.4 140.3TP% 3.6% 4.4% 4.8% 5.2% 5.5% 4.3% 4.9% 5.6%

Operating cash flow 18.7 15.7 11.9 16.7 29.2 33.3 27.5 5.6 158.6

Net Debt (€ equiv) 80.7 73.7 80.4 80.9 86.8 44.9 42.8 45.0Total Customer Signed off Cost Savings

0.4 2.6 8.8 15.1 15.0 25.8 30.0 19.2

53

SPWD Overview

25 consecutive months of growth

54

55

Growth

The Future

The Future• 25 months of sequential growth

• Market share gains evident, driven by Key Accounts, Insites™, and Product Range Extension

• June YTD sales up 19.7%. Good growth continues in July

• Gross margins holding steady (for 8th year)

56

The Future

• Good cash flow, driven by continued improved working capital ratios

• Bank facilities secure through to 2016

• Significant reduction in cost base maintained

57

The Future

• Continued improvement in working capital management, particularly inventory

• Providing the ability to take advantage of growth opportunities

• To drive further consolidation in a fragmented market

58

59

2011

Brammer plc

Visit us online: www.brammer.biz

60