Embed Size (px)

Citation preview

CONFIDENTIAL

FOR INTERNAL USE WITHIN CLIENT COMPANY ONLY

BRAZIL – WORLD-LEADING

PRODUCER AND EXPORTER

OF PULP AND PAPER

AN OVERVIEW OF THE BRAZILIAN PULP AND PAPER INDUSTRY

São Paulo, Brazil

February 2016

BUSINESS SWEDEN 27 JUNE, 2016 2

BRAZILIAN INDUSTRY IS THE WORLD’S 4TH

LARGEST IN

PULP PRODUCTION, AND 9TH

IN PAPER PRODUCTION

SOURCE: IBGE, IBÁ

1,1% of Brazil’s GDP

BRL 61bn in 2014

Exports grew 12,6% in 2014

Pulp and paper industrial GDP is growing above

Brazil’s GDP

Brazil has a forest productivity higher than Sweden,

US and China

High forest

productivity

Developed

industry

World-leading

producer and

exporter

BRAZILIAN EUCALYPTUS HAS A SHORT ROTATION PERIOD OF 7 YEARS

BUSINESS SWEDEN 27 JUNE, 2016 3

BRAZIL IS A LEADING PRODUCER OF PULP AND PAPER

WITH A HIGH FOREST PRODUCTIVITY

SOURCE: IBÁ

Rank Country Production (MT*)

1 United States 57,42

2 China 18,88

3 Canada 17,29

4 Brazil 16,46

5 Sweden 11,50

Rank Country Production (MT*)

1 China 106,61

2 United States 72,88

3 Japan 25,12

4 Germany 22,10

5 Sweden 11,49

9 Brazil 10,40

TO SUPPLY A PULP PLANT OF 1,5 MT/YEAR CAPACITY, SWEDEN WOULD NEED A 720 000 HA FOREST WHILE BRAZIL WOULD NEED 140 000 HA

70

35

30

30

41

25

25

22

20

18,8

18

15

6

5,5

0 10 20 30 40 50 60 70

Brazil

Uruguay

Indonesia

Australia

Chile

New Zealand

South Africa

US

Finland

Sweden

Currently

Potential

(m³/ha.year)

FOREST PRODUCTIVITY WORLDWIDE (HARDWOOD) PULP PRODUCTION RANK

PAPER PRODUCTION RANK

* MILLION TONS

BUSINESS SWEDEN 27 JUNE, 2016 4

BRAZILIAN MANUFACTURERS ARE LEADERS WITHIN

THE GLOBAL PULP INDUSTRY

SOURCE: PÖYRY 2014, VALOR, COMPANIES’ WEBSITES

COMPANY PULP PRODUCTION CAPACITY (Million Tons/Year)

0 2 4 6 8

Fibria

RGE/ APRIL

Eldorado

Suzano

Arauco

CMPC

Stora Enso

APP/ Sinar Mas

UPM

Cenibra

ENCE

Klabin

International Paper

Altri

Marubeni

Mitsubishi Braziliancompanies

Other

FIBRIA, SUZANO AND KLABIN ARE THE LARGEST PULP AND PAPER COMPANIES IN BRAZIL CONTROLLING 65% OF THE MARKET

FIBRIA

Net Revenue: 7 084

Forest Base: 969 thousand hectares

Headquarter: São Paulo

Focus: Eucalyptus Pulp

SUZANO

Net Revenue: 7 265 MBRL

Forest Base: 897 thousand hectares

Headquarter: Bahia

Focus: Eucalyptus Pulp

KLABIN

Net Revenue: 4 894 MBRL

Forest Base: 450 thousand hectares

Headquarter: São Paulo

Focus: Paper and Cardboard

LARGEST BRAZILIAN PLAYERS IN REVENUE

17 MILLION TONS OF PULP WERE PRODUCED IN 2014, OF WHICH 86% IS HARDWOOD

BUSINESS SWEDEN 27 JUNE, 2016 5

BRAZILIAN PULP PRODUCTION GREW 37% FROM 2007-14

SOURCE: IBÁ

0

1500

3000

4500

6000

7500

9000

10500

12000

13500

15000

16500

2007 2008 2009 2010 2011 2012 2013 2014

Pulp Paper

EXPORTS ARE STIMULATING THE PRODUCTION OF PULP, WHILE PAPER SUPPLIES MOSTLY THE DOMESTIC MARKET

PULP AND PAPER PRODUCTION (THOUSAND TONS)

86%

11% 3%

Hardwood

Softwood

High yield pulp*

52%

25%

11%

7%

1% 4%

Packaging and Wrapping

Printing and Writing

Tissue

Cardboard

Newsprint

Others

PULP PRODUCTION BY TYPE, 2014

PAPER PRODUCTION BY TYPE, 2014

* VERY HIGH YIELD (>95%). USED IN PRINTING PAPER

THIS ACCOUNTS FOR 10 MILLION TONS OF PULP

BUSINESS SWEDEN 27 JUNE, 2016 6

BRAZIL EXPORTS 64% OF ALL PULP PRODUCTION

SOURCE: IBÁ

BRAZILIAN CURRENCY DEVALUATION WILL CONTINUE TO BOOST PULP EXPORTS IN 2016

0

2000

4000

6000

8000

10000

12000

2007 2008 2009 2010 2011 2012 2013 2014

Exports

Imports

Balance

0

500

1000

1500

2000

2500

2007 2008 2009 2010 2011 2012 2013 2014

Exports

Imports*

Balance

31%

22% 19%

5%

23%

Europe

China

United States

Argentina

Others

Pulp

Pulp

Pulp, paper, wood panels

Paper

Pulp, paper, wood panels

EXPORTS DESTINATION AND MAIN PRODUCT,

2014

PULP BALANCE OF TRADE (THOUSAND TONS)

PAPER BALANCE OF TRADE (THOUSAND TONS)

* PAPER IMPORTS INCLUDE MAINLY: COATED PAPER OR PAPERBOARD

(PRINTED, COLORED, DECORATED), NEWSPRINT AND PRINTING PAPERS.

PINUS REPRESENTS 22%

BUSINESS SWEDEN 27 JUNE, 2016 7

EUCALYPTUS REPRESENTS 72% OF PLANTED AREA

SOURCE: ABRACELPA, IBÁ

FORESTRY INDUSTRY IS LOCATED IN SOUTHERN STATES SUCH AS SÃO PAULO, PARANÁ AND SANTA CATARINA

Pará

Santa Catarina

Tocantins

Bahia

Rio Grande

do Sul

Paraná

Mato Grosso

do Sul São

Paulo

Espírito

Santo

Rio de

Janeiro

Minas

Gerais

Mato Grosso

Rondônia

Acre

Amazonas

Roraima Amapá

Maranhão

Piauí

Sergipe

Ceará

Alagoas

Pernambuco

Goiás

Paraíba

Rio Grande

do Norte

Brasília

Pinus planted area

Eucalyptus planted area

Forestry industrial area

LEGEND

State Eucalyptus Pinus Others Total

Minas Gerais 1 400 232 39 674 5 313 1 445 219

São Paulo 976 186 123 996 90 147 1 190 329

Paraná 224 089 673 769 16 255 914 113

Mato Grosso 803 699 7 135 23 000 833 834

Bahia 630 808 6 499 34 000 671 307

Santa Catarina 112 944 541 162 6 645 660 751

Rio Grande do Sul 309 125 184 585 103 592 597 302

Others 1 101 570 12 177 309 569 1 423 316

Total 5 558 653 1 588 997 588 521 7 736 171

PLANTED AREA (ha) AND DESTINATION SEGMENT

34%

27%

15%

10%

7%

4% 3% Pulp and paper

Wood in natura (small producers)

Steel industry and charcoal

Timber Investment Management Organizations(TIMO's)*Wood panels and laminate floor

Furniture and other sawn products

Other

* MANAGEMENT GROUP THAT AIDS INSTITUTIONAL

INVESTORS IN MANAGING THEIR TIMBERLAND INVESTMENTS

MAIN CHALLENGES FOR THE PULP AND PAPER INDUSTRY

BUSINESS SWEDEN 27 JUNE, 2016 8

YET, BRAZILIAN PULP AND PAPER INDUSTRY FACES

CHALLENGES REGARDING COST-EFFICIENCY

SOURCE: IBÁ

Key take-

away 2

Key take-

away 3

Key take-

away 1

* LAND ACQUISITION IS RESTRICTED ACCORDING TO LAW 6.634/79

EXPENSIVE ENERGY, POOR INFRASTRUCTURE AND CONFUSING REGULATION ARE PROBLEMS SHARED BY MOST INDUSTRIES IN BRAZIL

Resources

Infrastructure

Costs

Key take-

away 3 Regulation

Both foreign companies and Brazilian companies with a majority share of foreign capital are limited on

the land area they may acquire*

Companies need special approval from INCRA, a public entity responsible for acquisition of land

Brazilian forestry sector experienced a higher increase of costs (7,9%) compared to rest of Brazilian

economy (6,4%) in 2014. Reasons involve energy and infrastructure high costs, besides a gap between

labor productivity and salary increase

Increase of energy cost and lack of water. Companies want to invest in efficient technology and reuse

67% of the energy used by industrial plants is produced within the sector. Main source is black liquor (70%)

Brazil presents low investments on infrastructure when compared to average global spending on

infrastructure, which generates increase in the production cost

BUSINESS SWEDEN 27 JUNE, 2016 9

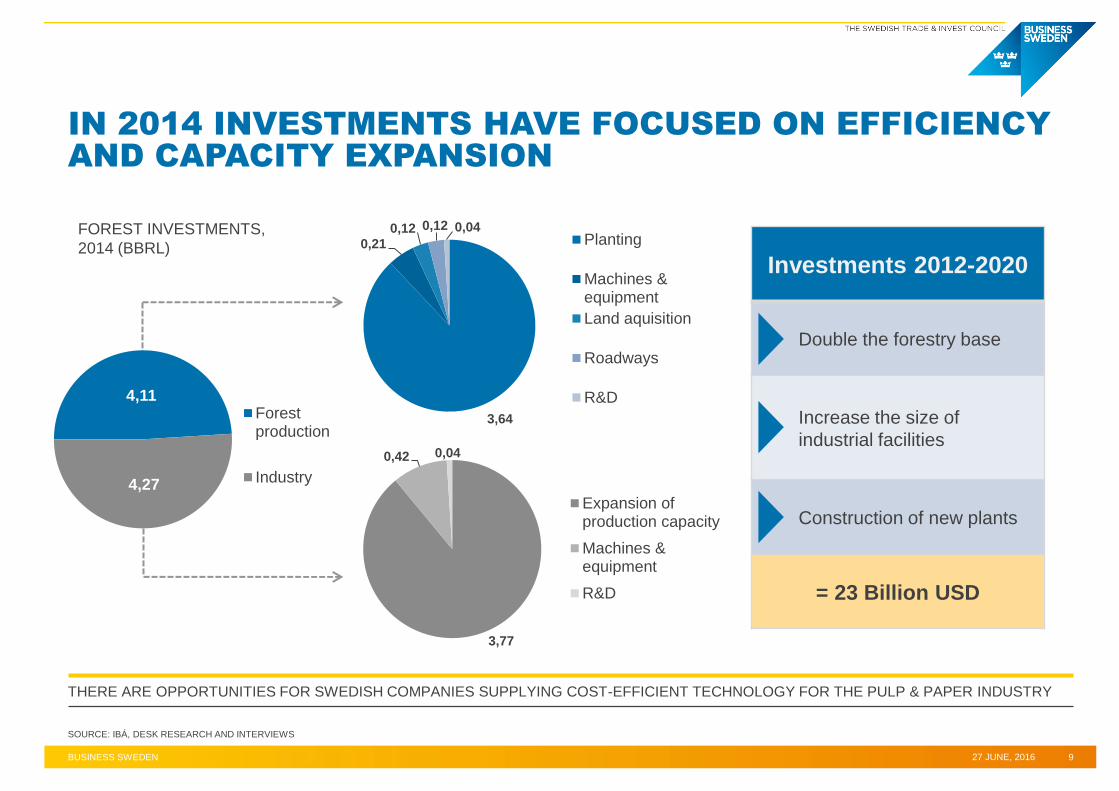

IN 2014 INVESTMENTS HAVE FOCUSED ON EFFICIENCY

AND CAPACITY EXPANSION

SOURCE: IBÁ, DESK RESEARCH AND INTERVIEWS

3,64

0,21 0,12 0,12 0,04

Planting

Machines &equipment

Land aquisition

Roadways

R&D

3,77

0,42 0,04

Expansion ofproduction capacity

Machines &equipment

R&D

THERE ARE OPPORTUNITIES FOR SWEDISH COMPANIES SUPPLYING COST-EFFICIENT TECHNOLOGY FOR THE PULP & PAPER INDUSTRY

FOREST INVESTMENTS,

2014 (BBRL)

4,11

4,27

Forestproduction

Industry

Investments 2012-2020

Double the forestry base

Increase the size of

industrial facilities

Construction of new plants

= 23 Billion USD

BUSINESS SWEDEN 27 JUNE, 2016 10

THE PULP AND PAPER INDUSTRY OFFERS GREAT

OPPORTUNITIES FOR SWEDISH COMPANIES IN BRAZIL

Which

opportunities

make Brazil

interesting?

What

challenges

should companies

be ready to face?

Difficult and excessively bureaucratic regulations

Complex tax system

High import tariffs, besides other taxes

Economic slowdown may

affect investments

Poor infrastructure for roads,

energy, ports and airports,

and high energy cost

Increase of costs (inflation)

High investments focused on capacity expansion

Investments grew 8% in 2013, against other sectors

Investments in energy efficiency and reuse

Large production of pulp and paper, and large market

Advantages: climate and land availability

Recent growth of exports, mainly of pulp

Devaluated currency is stimulating exports

Investments

Players

Market

Demand

Business in Brazil

Market

Recent economic slowdown

Lower commodities price on international market

LARGE AND GROWING PULP AND PAPER COMPANIES IN BRAZIL HAVE AN INCREASING DEMAND FOR TECHNOLOGY

Large producers,

capable of investing

Brazilian players among

the most productive in

the world

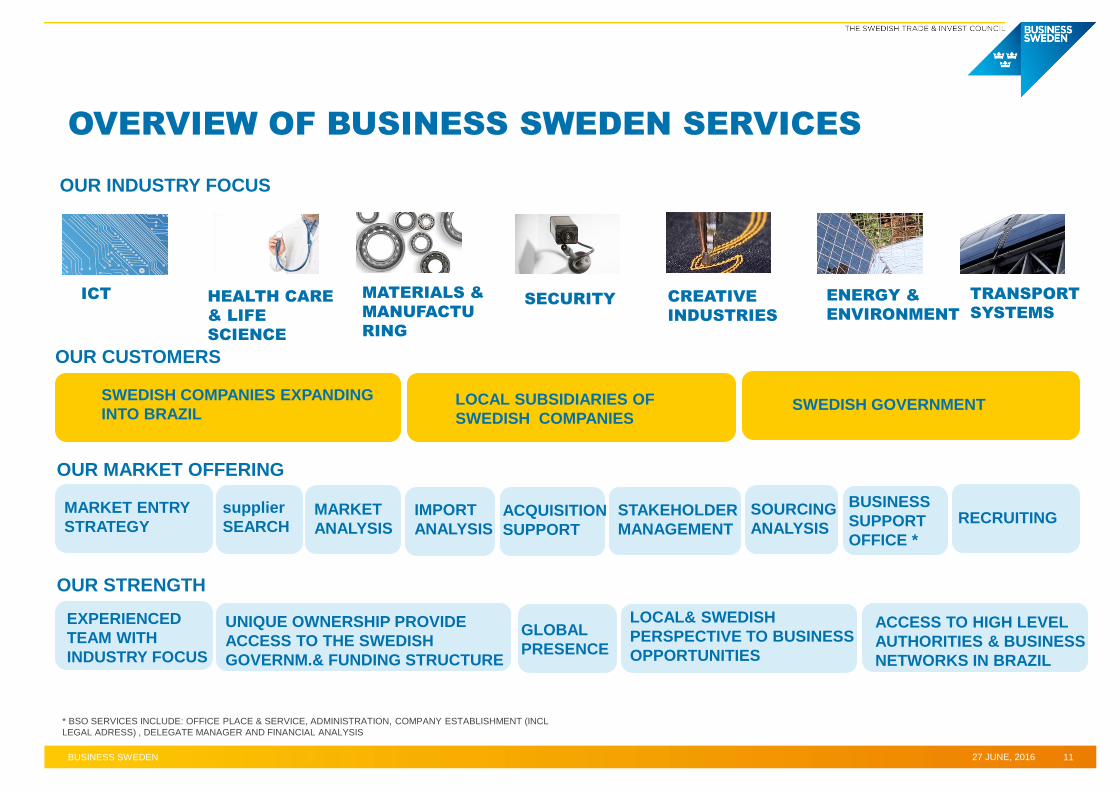

OVERVIEW OF BUSINESS SWEDEN SERVICES

* BSO SERVICES INCLUDE: OFFICE PLACE & SERVICE, ADMINISTRATION, COMPANY ESTABLISHMENT (INCL

LEGAL ADRESS) , DELEGATE MANAGER AND FINANCIAL ANALYSIS

27 JUNE, 2016 BUSINESS SWEDEN 11

ICT

OUR INDUSTRY FOCUS

HEALTH CARE

& LIFE

SCIENCE

MATERIALS &

MANUFACTU

RING

SECURITY CREATIVE

INDUSTRIES

ENERGY &

ENVIRONMENT

TRANSPORT

SYSTEMS

OUR CUSTOMERS

SWEDISH COMPANIES EXPANDING

INTO BRAZIL LOCAL SUBSIDIARIES OF

SWEDISH COMPANIES SWEDISH GOVERNMENT

OUR MARKET OFFERING

MARKET ENTRY

STRATEGY

OUR STRENGTH

supplier

SEARCH STAKEHOLDER

MANAGEMENT

IMPORT

ANALYSIS

SOURCING

ANALYSIS ACQUISITION

SUPPORT

MARKET

ANALYSIS

BUSINESS

SUPPORT

OFFICE *

RECRUITING

EXPERIENCED

TEAM WITH

INDUSTRY FOCUS

UNIQUE OWNERSHIP PROVIDE

ACCESS TO THE SWEDISH

GOVERNM.& FUNDING STRUCTURE

GLOBAL

PRESENCE

LOCAL& SWEDISH

PERSPECTIVE TO BUSINESS

OPPORTUNITIES

ACCESS TO HIGH LEVEL

AUTHORITIES & BUSINESS

NETWORKS IN BRAZIL

CONTACT US

BUSINESS SWEDEN IN BRAZIL

Rua Joaquim Floriano, 466 – cj 1908 – Ed. Office

BR 04534-002 – São Paulo - Brazil

Phone: +55 11 2137 4400

Fax: +55 11 2137 4425