Embed Size (px)

Citation preview

Alexandre Elias / 05-14-2014Alexandre Elias / 05-14-2014

Breakout SessionBreakout SessionBringing Renewable Elastomers to MarketBringing Renewable Elastomers to Market

BRASKEM’S EVOLUTION TIMELINEA 12 years old company that started locally and have expanded nationally and internationally

2 2

Inauguration of Brazil’s first petrochemical complex

19781979

Investments by Odebrecht in the

sector

Start of industry integration

19902002

Creation of Braskem

Acquisition of Grupo Ipiranga assets. Launch of Green

Polyethylene

20072008

Inauguration of first

greenfield plant

Announcement of project in partnership with Idesa in Mexico

20092010

Acquisition of Quattor, consolidating the

industry in Brazil. Acquisition of Sunoco’s

polypropylene assets, marking the first plants

outside Brazil.

Inauguration of green ethylene

plant

Acquisition of Dow’spolypropylene assets

20112012

Inauguration of two new plants.

Construction begins on Mexico

project

2013

Acquisition of Solvay’sAssets in Argentina

3 3

REACHING THE CURRENT STRUCTURE SIZE

*December 2012/2013

36INDUSTRIAL UNITS

TEAM MEMBERS8096

INVESTED ININNOVATION

92US$

MM

22GROSS REVENUE OF

USS$ BI

CLIENTSIN OVER

70COUNTRIES

EXPORT REVENUE OF

8,1NET REVENUE OF

US$19BI

EBITDA OF

US$2,2BI

BIUS$

BAHIABRAZIL

1 CRACKER4 PE1 PP1 PVC1 CHLOR-ALKALI

ALAGOASBRAZIL

2 PVC1 CHLOR-ALKALI

SAO PAULOBRAZIL

2 PE2 PP1 CRACKER

RIO DE JANEIROBRAZIL

1 CRACKER 1 PE 1 PP

RIO GRANDE DO SULBRAZIL

2 CRACKER5 PE 2 PP

BRAZIL (KTA)BASIC: 3,752PE: 3,025PP: 1,975PVC: 710

USA (KTA)PP: 1,425

EUROPE (KTA)PP: 545

INDUSTRIAL PRESENCE

PROJECTS

4 4

36 INDUSTRIAL UNITS WORLDWIDE

PENNSYLVANIAUNITED STATES

1 PP

WEST VIRGINIAUNITED STATES

1 PP

NORTH RHINE-WESTPHALIAGERMANY

1 PP

SAXONY-ANHALTGERMANY

1 PP

TEXASUNITED STATES

3 PP

PROJECTS IN CONSTRUCTION

WITH INTERNATIONAL INDUSTRIAL FOOTPRINT

BRAZIL

SALVADORSAO PAULORIO DE JANEIROPORTO ALEGRE

UNITED STATES

PHILADELPHIAHOUSTON

LATIN AMERICA

VENEZUELACARACASPERULIMACHILESANTIAGO

ASIA

Serving the markets of SINGAPORE, CHINA, INDIA, INDONESIA, SOUTH KOREA AND JAPAN

5 5

AND INTERCONTINENTAL COMMERCIAL PRESENCE

ARGENTINABUENOS AIRESCOLOMBIABOGOTAMEXICOMEXICO CITY

EUROPE

GERMANYFRANKFURTNETHERLANDSROTTERDAMAUSTRIAVIENNA

OFFICES AND COUNTRIES

COMMERCIAL MEMBERS

SPAINENGLANDPOLANDITALY

BRASKEM’S GROWTH IS STRUCTURED AROUND THREE MAIN DRIVERS:

GROWTH IN THE BRAZILIAN MARKET

6 6

INTERNATIONAL EXPANSION FOCUSED

ON THE AMERICAS

RENEWABLE CHEMISTRY

WORKING ON STRATEGIC EXPANSION

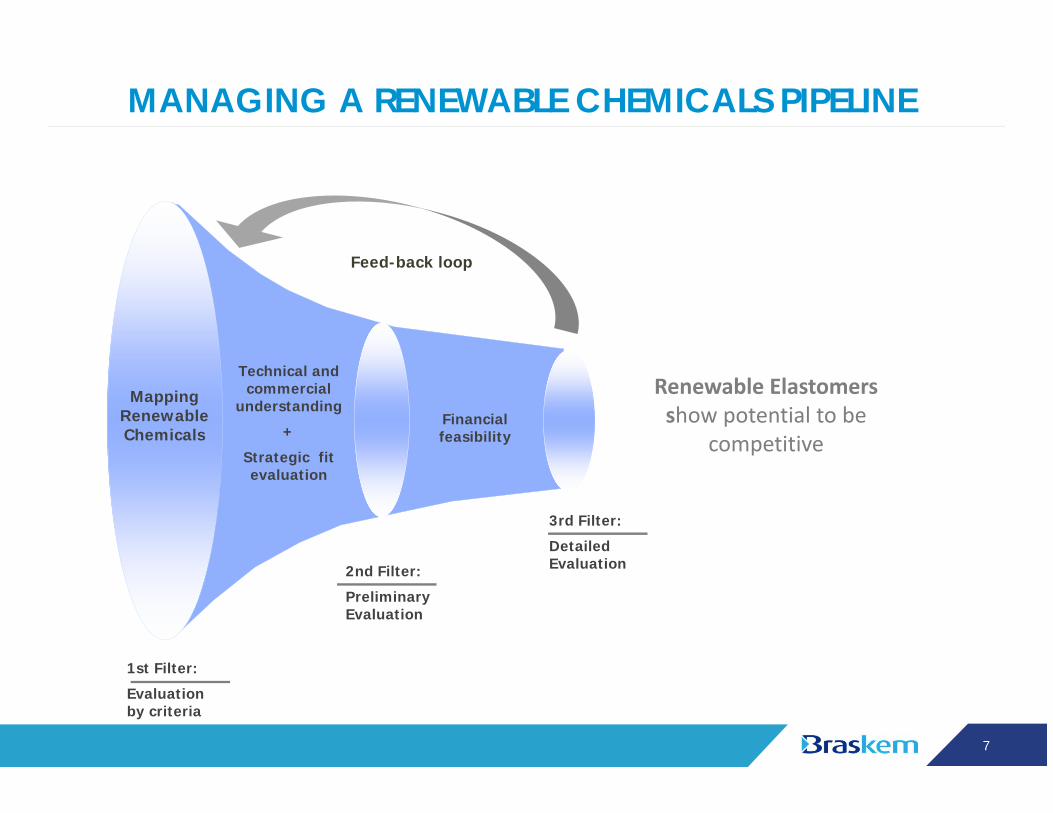

MANAGING A RENEWABLE CHEMICALS PIPELINE

7 7

Technical and commercial

understanding

+

Strategic fit evaluation

Mapping Renewable Chemicals

1st Filter:

Evaluation by criteria

2nd Filter:

Preliminary Evaluation

Feed-back loop

3rd Filter:

Detailed Evaluation

Financial feasibility

Renewable Elastomers show potential to be

competitive

88Note: Sources: CEH 2012 Natural Rubber – SRI consulting

World Natural and synthetic rubber consumption (MM tons)

CAGAR (a.a.) 1981 to 2004 2004 to 20113,8%1,4%

1,0%0,9%

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

5

15

10

0

4

76

3

12

89

11121314 Synthetic Rubber

Natural Rubber

Elastomers demand is over 20 MM tons and synthetic rubber accounts for 70%

99

Most representative sorts of synthetic rubber produced have the tire industry as main destination

Synthetic rubber is mainly represented by butadiene derivatives

Note: Sources: CEH 2012 Natural Rubber – SRI consulting

PolybutadieneApplications: About 70% tire

Industry

Capacity: 3,7 MM (2011)

Main Producers: China and USA

11%

13%

18%

5%

3%3%

47%

Other

South America

Southeast Asia

West Europe

Cis & Baltic States

North América

Northeast Asia

Styrene ButadieneMain Applications

• EPM: Insulator for high‐voltage cables Nitrile: Hoses, seals and gaskets

(mainly for automobiles)• Polyisoprene: Tires, Mechanical Goods,

Footwear• PClR: Mechanical rubber and

automotive components

Capacity: 3,3 MM (2011)

Other Syntetic Ruber

9%

11%

6%

8%

18%

48%

Other

West Europe

South America

Cis & Baltic States

Norht America

Northeast Asia

Main Producers: China and USA

Capacity: 6,0 MM (2011)

Applications: About 70 ~ 75% destined to tire industry

NITRILE

RUBB

ER

1,2

0,5

0,10,2

0,30,1

ETHY

LENE

PROPYLENE

RUBB

ER

1,3

0,4

0,5

0,4

0,1

0,4

0,0

0,2

0,20,1

0,6

POLYISOPR

ENE

0,1

0,30,10,0

POLYCH

LORO

PREN

ERU

BBER

(neo

pren

e)

0,0

Cent East Europe

Other North America

Southeast Asia

West Europe

Northeast Asia

1010

Almost half of butadiene consumption is represented by tire industries applications

And elastomers are the larger butadiene demand driver

Butadiene Global Demand (2011) MM tons

1,4(13%)

0,6(6%)

1,0(9%)

1,2(12%) 0,2

(2%)0,5(5%)

2,8(27%)

2,8(27%)

OtherAdiponitrile (HMDA)

Styrene‐Butadiene LatexesABSPolychloroprene (PCR)

Nitrile (NBR)Styrene‐Butadiene (SBR)Polybutadiene (PBR)

Source: CEH ‐ Butadiene (2011); PERP ‐ Isoprene/Bioisoprene (2012)

Total Global Market Demand: 10,5 MM tons

Tire Industry Influence:

~ 70% of Polybutadieneand Styrene-butadiene production goes to tire industry (~46% of total

butadiene production)

Elastomers Other

Approximately 60% of total’s budatiene

consumption goes to elastomers applications

1111

Necessity to search for alternative ways to produce butadiene

It is forecasted a shortage on butadiene chain

19

55 52 53 51 50 50 49 47 47 46 45

29 29 30 32 32 34 35 35 35 36

19191817181819191919

27

2013E20122011201020092008200720062005 2015E2014E

OthersNaphthaEthane

21

149

62

Gas OilNaphtan‐ButanePropaneEthane

Butadiene average content from steam cracking using different feedstock (kg Butadiene content / 100 kg Ethylene)Butadiene is currently

almost entirely produced as a by‐product of ethylene steam cracking of naphtha or gas oil feedstock, the

cheapest process

A switch to lighter feedstock has

reduced the amount of butadiene available from

ethylene cracking

Source: CMAI; SRI PEP Report 35E ON‐PURPOSE BUTADIENE PRODUCTION

Probable Butadiene Shortage

Feedstock distribution for Ethylene World Production (in %)

1212

In the last ten years the ratio of crude oil to natural gas prices has expanded almost four times

Caused by the evolution of US gas and oil prices trends

0

10

20

30

40

50

60

70

80

90

100

950

2

4

6

8

10

12

14

16

18

08070605040302010099989796 11YTD

1009

1 Assume 5.8 MMTBTU per barrel crude oil

SOURCE: IHS

Henry Hub natural gas, $/MMBTU

WTI crude oil, $/Bbl

06

1.7

05

1.1

02

1.8

1.0

04

1.2

0301

1.1

00

1.2 1.4

3.1

10

4.0

11YTD

09

2.7

08

1.9

0799

1.4

98

1.2

97

1.4

96

1.4

95

1.9

$/Bbl $/MMBTURatio of crude oil (in MMBTU equivalents1) to natural gas price

US oil and gas prices

1313

Butadiene forecast indicates that the demand will growhigher ( 3p.p.) than historic average...

SOURCE: IHS

3.8 MM t

CAGR 1%CAGR 4%

Region Demand 2012(million t)

CAGR2012‐2020

Northeast Asia 4.9 4%

North America 1.8 1%

Brazil 0.3 4%

West Europe 1.8 0,4%

Others 1.4 8%

Source: IHS Chemical, analysis Braskem

Represents, on average, 45% of world demand

• The world recession during2008‐2009 resulted in adowntrend growth for thebutadiene demand: this factpushed down the last 5 yearsaverage.

• There’s a growth expectationfor the car industry, speciallyin China and India,consequently for butadieneas well.

• These two facts togetherbring an indication that thebutadiene demand will grow3 p.p more than the past.

1414

Due to switch to lighter feedstocks, the butadiene production through Naphta cracker will stay lower than demand...

Resulting in a probable pressure on butadiene supply

Source: CMAI, analysis Braskem*Considering only actual production

12

1

2019

13

11

1

2018

13

11

1

2017

12

11

1

2016

9

9

1

2007

10

9

1

2008

10

10

1

2011

10

10

1

2010

10

9

1

2009

9

8

1

‐1MM tonsShortage of Butadiene

2020

1312

2014

11

1010

2015

10 111

2013

10

11

11

1

2012

Butadiene Demand

Butadiene Extraction(Naphta Cracker)

On Purpose Production*

Butadiene World Production x Demand (in Million tons per year)

Forecast

Butadiene Extraction Production CAGR 2013 – 2022 = 3%

Butadiene DemandCAGR 2013 – 2022 = 4%

Butadiene on‐purpose productionneeds to grow 9% CAGR 2013 –2022 to supply outpace demand

1515

Renewable Butadiene positive potentials

A sustainable portfolio of products

Developing a Sustainable Portfolio

Cost Competitive

Lower production cost through a fermentation route

Social Impact

Agricultural industry growth and social development

Renewable Source

Produced from sugar

1616

Genomatica

Differentiated technology platform Strong patents portfolio on C4 products Proven scale up capacity (1,3 BDO process)

Thank YouThank You