-

1

Does the OECD Convention affect bribery? Investment

Liberalization and Corruption in Vietnam

Nathan M. Jensen

Associate Professor Washington University in St. Louis

CB 1062 St. Louis, MO 63130 Phone: 314-935-5857

Fax: 314-935-5856 Email: [email protected]

Edmund J. Maleksy Associate Professor

Duke University Department of Political Science

140 Science Dr., Rm 208 Gross Hall, Box 90204

Durham, NC 27708 (919) 660-4300 [email protected]

Acknowledgements: We would link to thank US-AID and the Vietnam

Chamber of Commerce and Industry for the generous use of the

data.

-

2

Abstract: Scholars have long debated the role of home country

attributes on the propensity of firms to bribe government officials

in host countries. Unfortunately, research in this area has been

hampered by the fact that reporting bias in corruption is

correlated with the variable of interest, leading to incorrect

estimations of effects. For instance, the OECD Anti-Bribery

Convention criminalizes bribery for a large number of developed and

middle income countries. While this may reduce bribery, it also

reduces willingness to report. In this paper, we examine the

effectiveness of the convention on the propensity of firms to pay

bribes in Vietnam using a survey experiment to reduce

under-reporting in briber propensity. We find that the foreign

firms from OECD convention signatories are slightly more likely to

pay bribes than firms from non-signatory countries and are just as

likely to enter into sectors that are more prone to bribery.

-

3

INTRODUCTION

The control of corruption dates back at least as far as the

Egyptian pharaoh Horemhebs

(1342-1314 BC) edict making bribery a capital offense and the

urging of Christians to avoid

engaging in corruption in Exodus (Exodus 23: 1-3, 68).1 After

centuries of laws on bribery,

societies are still attempting to constrain the bribery of

citizens and firms.

In the management literature, scholars have attempted to both

understand what drives

corruption and how corruption affects the investments and

operations of firms (Beets 2005). In

this paper, we contribute to this literature through an

examination a very specific form of bribery

and a single set of solutions to constrain the bribery behavior

of firms. Our study focuses on how

foreign firms use bribes to enter into restricted markets in a

single country, and how international

laws shape this bribery behavior. While narrowing this study

does limit our ability to speak to

other forms of corruption, our main advantage is in the precise

measurement of corruption and a

relatively unique institutional environment that allows us to

observe the opening of sectors over

time and how this affects the bribery behavior of firms.

To address the complex measurement issues in studying the

bribery behavior of firms, we

take advantage of a novel strategy for measuring corruption.

Utilizing the Unmatched Count

Technique (UCT), or list question from an original firm level

survey in Vietnam, we can both

directly measure corruption and shield respondents from the

dangers of admitting to the process

directly. This technique randomly assigns respondents into two

groups. One group is given a list

of non-sensitive questions and is asked to identify the number

of activities that the respondents

firm engaged in. The second group, in addition to the

non-sensitive questions, receives an extra

sensitive question. In our context, non-sensitive questions

include infrequent activities that

firms could engage in during registration. Our sensitive

question is on the use of bribery at the

time of registration. Respondents only answer the number of

activities they engaged in, not any 1 See Martin (1999)

-

4

specific activities. A simple comparison between the treatment

and control groups provides

insights on the overall level of corruption.

This innovation of using a List question to address illegal or

unethical behavior has been

underutilized in management scholarship. Activities as seemingly

inconsequential, like self-

reports of whether or not a person votes in US elections, can be

inaccurately reported due to

social desirability effects and List questions have been

utilized to show the extent of this

misreporting (Holbrook and Krosnick 2010). Numerous activities

by firms, managers, and

employees share these similar characteristics, where

observational data on these sensitive acts are

rare and surveys behavior often require admissions of guilt.

Scholars in political science have

recently used List questions to uncover the selling of votes

during elections (Corstange 2009;

Gonzalez-Ocantos et al. 2012), immigration views (Janus 2010),

bias against women running for

political office (Streb et al. 2008), and racial prejudice

(Sniderman et al. 1992; Kuklinski et al.

1997). We use this research design to address an important

question in businesswhat causes

bribery behavior by firms?

Building on the work of Kaufman et al. (2000) and Kolstad and

Sreide (2009), we

acknowledge that bribery is not simply a tax on firms. Firms can

strategically use bribery enter

markets in search of rents (Ades and Di Tella 1999; Bliss and Di

Tella 1997; Djankov et al 2002).

Indeed, Malesky et al. (2013) show that firms are much more

likely to bribe when entering high

rent sectors.

To gain leverage on how rent-generating restrictions on entry

provide avenues for

corruption, we field our survey in Vietnam, a country that has

undergone tremendous

liberalization of investment laws in recent years. Through a

serious of domestic reforms, along

with reforms associated with signing of a bilateral trade

agreement with the United States in 2000

and entry into the World Trade Organization in 2006, Vietnam has

considerable variation in the

sectors that are open to FDI and heterogeneity in the timing of

these reforms.

-

5

This research design strategy allows us to examine both bribery

in restricted and non-

restricted sectors, but also to examine the differences in

behavior between signatories of the

OECD convention and non-signatories. Building on previous

research we test whether bribery by

firms from OECD convention signatory countries should be

substantially less frequent than firms

from non-signatory countries. We selected the OCED convention

for two reasons. First, it is

highly visible, global policy attempt to reduce corruption and

improve business environments for

foreign investors. More importantly, however, it is key example

of how reporting biases may be

correlated directly with the variable of interest, scholars are

attempting to study. Because the

OECD convention criminalizes bribery for investors from

signatory country, it not only reduces

the willingness to bribe; it reduces the willingness to answer

honestly in surveys regarding

engagement in the activity an extreme example of social

desirability bias (Couts and Jann

2011).

After employing a survey experiment to address the error,

empirical results suggest that

the OECD convention is ineffective in reducing bribery, and does

not deter firms from entering

into restricted sectors. We find that firms from OECD

signatories are marginally more likely to

engage in bribery. In a series of more exploratory tests, we do

show that domestic political

factors, namely democratic institutions, can shape bribery

behavior and that we observe massive

variation in bribery by home countries. Thus our results do

suggest that country of origin matters,

and this is most likely in the enforcement of bribery laws, not

which countries sign onto anti-

bribery conventions.

Our paper is organized as follows. In the next section we

provide a brief overview of

research in international business on the causes and

consequences of corruption. In the third

section we discuss how investment liberalization in Vietnam

allows us to test the OECD

convention affects bribery and firm entry into sectors ripe for

corruption. In the fourth and fifth

section we document our data and methodology for measuring

corruption and present our results.

-

6

LITERATURE REVIEW AND THEORY

Beginning with the seminal work of Hymer (1976), management

scholars have

highlighted the unique barriers for foreign firms operating

overseas. While this research

originally referred to the broad costs of doing business abroad,

a more recent wave of research

has focused on the liability of foreignness (Zaheer 1995; Zaheer

and Mosakowski 1997; Zaheer

2002; Miller and Eden 2006). This stream of research has

identified additional social costs for

foreign investors operating outside of their home country. This

can range from backlashes

against foreign products to discriminatory treatment of foreign

firms relative to domestic firms by

government officials (Shimp and Sharma 1987; Peterson and

Jolibert 1995).

Firms can use a number of strategies to overcome these barriers

(Luo et al. 2002)

including the use of illicit payments to enter markets, keep out

competitors, or to sway

government decisions on procurement contracts. The liability of

foreignness research points to

how foreign firms are more likely to use illicit payments

(corruption) than domestic firms as a

means of overcoming these barriers to foreignness.

Thus, corruption can distort firms decisions ranging from

reducing investment (Mauro

1995; Wei 2000; Habib and Zurawicki 2002; and Cuervo-Cazurr

2008) to shaping firm entry

strategies (Henisz 2000; Smarzynska and Wei 2000; Rodriguez et

al 2005).2 Unfortunately,

many of these studies are open to the criticism of reverse

causality, where the entry of foreign

firms can affect corruption. For example, Robertson and Watson

(2004) find that countries with

more rapid increases in FDI are associated with bigger increases

in corruption.

This caveat on reverse causation aside, great strides have been

made in examining how

home country laws influence the activities of firms. The use of

corruption as a strategy for firms

to complete with domestic firms, while plausible on the surface,

has a number of shortcomings. 2 Brouthers et al (2008) finds that

corruption has a bigger impact on resource seeking FDI relative

to market seeking FDI.

-

7

First, domestic firms can also use these same corruption

strategies to bribe officials, and their

better access to these officials can actually reduce the

monetary cost of bribery. Second, most

relevant for this study, foreign firms can be highly constrained

in their ability to provide bribes.

These constraints are often a function of the home country

environment, and thus country

of origin studies focus on how domestic laws affect the foreign

operations of home country firms.

For example, Kwok and Tadesse (2006) articulate that foreign

investment from specific source

countries can reduce corruption through home government use of

regulation to reduce corruption

in foreign affiliates.3 Similar points have been made by

Sandholtz and Koetzle (2000) and

Gerring and Thacker (2005).

In this paper we focus specifically on how international

agreements on corruption,

specifically the OECD Convention on Combating Bribery of Foreign

Public Officials in

International Business Transactions affects the propensity for

firms to bribe (Pacini et al 2002).4

This convention, created in 1997, criminalized the bribery of

public officials for business

transactions.

The empirical evidence is mixed regarding the effectiveness of

laws against bribery in

home countries on bribery behavior of their firms abroad. Hines

(1995) finds that the US Foreign

Corrupt Practices Act had a major negative impact on US business

while Graham (1984) finds

that the act had no impact on US market share in corrupt

countries. Cuervo-Cazurr (2008) finds

that the OECD convention leads to less FDI into highly corrupt

countries for signatories. DSouza

(2012) finds that signatories to the OECD convention decrease

their exports to highly corrupt

countries. Spencer and Gomez (2011) find mixed evidence for home

country effects and the 3 They also argue that firms can build

reputations for not providing bribes and the employees of

foreign firms can lead to the diffusion of best practices as

they leave the foreign firms for

domestic firms.

4 See Argandoa (2007) for work on the UN Convention Against

Corruption.

-

8

OECD Convention on corruption. Kim and Barone (1981) survey

members of the Academy of

International Business on the US Foreign Corrupt Practices Act,

finding that this act both has a

very limited effect on bribery, and put US firms at a

competitive disadvantage.

We build on this literature, although we note that many of the

studies of corruption

suffered from limitations on the measurement of corruption.

First, the use of perceptions of

corruption rather than actual incidence of corruption has been

widely criticized (Treisman 2007;

Olken 2009). Second, there is considerably evidence that firms

are reluctant to share information

on their direct payments to politicians for fear of legal or

political reprisals (Jensen et al 2010).

Importantly for our research goals, there is reason to believe

that firms from signatory

countries to the OECD Anti-Bribery Convention will actually be

more reluctant to reveal their

experience with bribery, as they face domestic, criminal

repercussions for the revelation that their

non-signatory peers do not. If this is true, the measurement

error in traditional measures will be

associated systematically with a variable measuring whether a

home country has signed the

Convention, directly biasing in favor of research designs trying

to measure its effectiveness.

To mitigate these concerns, scholars have been increasingly

turning to alternative ways to

measure corruption. Some use clever proxies for corruption, such

as Fisman and Miguels (2007)

study of unpaid parking tickets by diplomats in New York City.

One of the most direct measures

of firm corruption comes from Jeong and Weiners (2012) study of

bribery for procurement under

the Iraq Oil for Food Program.

In a similar vein, we focus on a single recipient of FDI,

although our study comes with a

number of additional advantages that we document in the next

section. Specifically, Vietnams

signing of a bilateral trade agreement with the United States in

2000 and accession into the WTO

in 2006 led to a series of reforms that vary across sectors in

their implementation over time.

Using original survey of actual incidence of bribery, we

document how the country of origin of

investors shapes bribery behavior.

-

9

While the focus of our project is on how the country of origin

affects the propensity to

pay bribes, we take seriously the firm level studies of bribery

(Svensson 2003; Clarke and Xu

2004; Martin et al 2007; Lee et al 2010; Jeong and Weiner 2012).

Through our process of

randomization and through the use of a randomized survey

experiment, a within country design,

and sector fix effects, we can mitigate concerns that our study

is being affected by unobserved

industry or country factors driving corruption. More

importantly, we directly model a key finding

in the bribery literature on the role of available rents in

shaping bribery decision.

We build on previous research on how the availability of rents

shapes bribery behavior

(Bliss and Di Tella 1997; Ades and Di Tella 1999; Djankov et al

2002). Malesky et al (2013)

showed that sectors in Vietnam that restricted entry to foreign

firms, described in the next section,

have much higher levels of industry concentration and

profitability. Restricted (or Group A)

sectors, those where investors need special permission to enter,

had 2.4% greater industrial

concentration and 13% higher profit margins. Malesky et al.

(2013) theorize that these sectors

provide rents for firms and allow the gatekeepers of these

sectors to demand bribers for firms to

enter. Indeed, they find that 39.4% of foreign firms provided

bribes to enter these sectors. What

remained unanswered by the authors, however, is why only a

minority of firms paid bribes, and if

the need to pay bribes drove some entrants away.

To answer these questions, we first provide more details on

foreign investment in

Vietnam and discuss the liberalization process. We argue that

this setting gives us tremendous

leverage in examining the propensity of firms of different

country origins to provide bribes, and

whether or not these firms choose to enter into Vietnam in the

first place.

INVESTMENT LIBERALIZATION IN VIETNAM AND THE OECD CONVENTION

Vietnam has emerged as one of the most successful developing

countries in attracting FDI across

a number of sectors. While domestic liberalization in the 1980s

and 1990s attracted large

-

10

numbers of investors, Vietnams entry into the WTO entry in 2006

has been the highpoint of FDI

attraction. Post-WTO entry FDI inflows totaled a staggering 10%

of GDP (World Bank 2010).

Despite Vietnams success in attracting FDI and the massive

liberalization over the past

decade, Vietnam remains a difficult environment for

multinational corporations. This is

somewhat attributable to Vietnams complex FDI policies. Vietnams

1987 Foreign Investment

Law, the first major reform that attracted FDI, lead to a

partial liberalization of many sectors.

These sectors, known as Group A projects, are formally open to

entry by foreign firms, but

only after special approval from the Prime Ministers office. In

the 1990s the licensing of FDI

projects was decentralized to the provinces, yet the requirement

for a special license remained

(Malesky 2008). These special requirements covered over thirty

different economic sectors,

ranging from insurance, transportation (air, land and sea), real

estate, telecommunications, legal

and accounting, and the motion picture industry. We provide

details on these sector restrictions

in the Appendix C.

Many of these restrictions were scheduled supposed to have been

lifted by Vietnams

entry into the WTO in 2007, although our own data collection

finds that plenty of restrictions

remain in place, because domestic laws implementing the WTO

agreements have not yet been

written. More importantly, the variation across sectors on the

ability of foreign firms to enter and

the different timing of these restrictions makes Vietnam an

excellent case for us to examine

bribery by foreign firms during entry. Most important for our

design, many of these liberalization

decisions were made either in accordance of signing a

preferential trade agreement with the

United States in 2000 and liberalizations associated with WTO

entry. In short, despite lobbying

by many domestic firms, Vietnam acquiesced in numerous cases

through the lifting of

restrictions, opening sectors to foreign investment without

special approval.

Equally important for our research design is that foreign

investors, with the approval

from the Prime Ministers office, did enter into all of these

sectors, even during the periods with

-

11

restricted entry. Thus government officials served as

gatekeepers for FDI entry, but some foreign

firms succeeded in gaining entry to almost every conditional

sector.

As noted in the previous section, Malesky et al. (2013) show

that not only do these

sectors have higher levels of industry concentration and vastly

higher profitability, but they are

also associated with a higher propensity to pay bribes. Our main

contribution in this paper is

exploring how companies from different source countries respond

to the availability of rents in a

given sector. While previous work shows that firms are more

likely to bribe to gain entry into

these sectors, in this paper, we examine how the OECD

anti-bribery convention shapes this

propensity of firms to bribe during registration.

While many countries have passed laws against bribery, including

the high profile US

Foreign Corrupt Practices Act, a major OECD initiative has been

successful in criminalizing

bribery for a large number of countries. The OECD Convention on

Combating Bribery of

Foreign Officials in International Business Transactions began

as an ad hoc working group in

1989, culminating in the passage of the convention in 1997 and

officially coming into force in

February 1999. Countries have joined and ratified this

convention at different dates, and new

signatories (including Colombia in 2013) have continued to join

the Convention. The key

principle of this convention is the passage of local laws

criminalization of bribery. The OECD

does not directly enforce these laws, but they both monitor

anti-bribery legislation and

enforcement of anti-bribery laws of signatory countries.5

While many advanced industrialized countries have joined the

convention, the major

investors in Vietnam consist of both firms from signatory and

non-signatory countries. While we

cannot evaluate the counterfactual of what investors would have

entered in Vietnam in the

absence of either corruption or the convention, we can explore

the sectoral allocation of bribers 5 For individual country

monitoring reports see: http://www.oecd.org/daf/anti-

bribery/countryreportsontheimplementationoftheoecdanti-briberyconvention.htm

-

12

and investments by firms from governments that are party to the

OECD convention and those that

are not.

Our first hypothesis builds on our previous discussion of the

OECD convention deterring

bribery.

Hypothesis 1: Firms from signatories of the OECD convention are

less likely to bribe.

The substantive focus of this paper is on the OECD convention

and how this international

agreement, binding governments to pass anti-corruption reforms

on their outward investments. A

secondary contribution of this paper is to examine an

alternative framework through which

institutions can shape corruption behavior of home government

investors. We specifically focus

on how the level of democracy in home governments reduces the

propensity of firms to pay

bribes.

How do democratic institutions shape bribery behavior? Empirical

studies of corruption

find some evidence that democratic institutions reduce bribery

domestically. This can occur

through a number of mechanisms. For example, Sandholtz and

Koetzle (2000) argue that

democratic norms and institutions both reduce corruption, by

institutionalizing openness and

equality. Gerring and Thacker (2005) find that democracy has a

significant impact on business

corruption in a home government. Treisman (2007) finds similar

patterns in studies of corruption

perceptions, but there is little relationship between democratic

institutions and reported corruption

acts.

While this literature on the domestic politics of corruption is

too vast for us to review in

its entirety here, central to our paper is that many of the same

theoretical mechanism linking

democracy and less corruption in a home country could translate

into lower levels of corruption

in the overseas investment of firms from democratic governments.

Democratic systems, often

with free and fair presses and political competition leading to

information revelation about

incumbent leaders and to specifically pass laws to crack down on

corruption. As these

-

13

democratically elected leaders in the home country do not

directly benefit from the international

bribery of foreign officials, they have greater incentives to

reduce corruption that harms their

electoral prospects and does not directly line their pockets.

This leads to our second hypotheses:

Hypothesis 2: Firms from democratic countries are less likely to

bribe.

This first two hypothesis examines all foreign investment in

Vietnam, while our data

shows that the propensity to bribe is substantially higher in

restricted sectors, because the

protected market guarantees monopoly rents for those fortunate

to receive a license to enter. We

hypothesize, therefore, that the impact of the OECD convention

and democratic institutions in the

home should be especially apparent in these sectors. This leads

to our third and fourth

hypothesis.

Hypothesis 3: Firms from signatories of the OECD convention are

less likely to bribe in

restricted sectors.

Hypothesis 4: Firms from democratic countries are less likely to

bribe in restricted

sectors.

Finally, the lower propensity to bribe by firms from convention

signatory countries and

democratic home countries puts these firms at a comparative

disadvantage in competing to enter

restricted sectors. We argue that we should see less entry into

restricted sectors by firms from

countries that joined the OECD convention or are from democratic

home countries.

Hypothesis 5: Firms from signatories of the OECD convention are

less likely to enter in

restricted sectors.

Hypothesis 6: Firms from democratic countries are less likely to

enter in restricted

sectors.

-

14

Our comparison between signatories of the OECD convention and

countries with

democratic institutions clearly isnt exhaustive of the home

country factors that can shape bribery

behavior abroad. For example, levels of corruption in a home

country can be a predictor of

bribery behavior abroad (Cuervo-Cazurra 2006; Fisman and Miguel

2007).6 Our focus is to

examine how formal institutions, one international and one

domestic, shape bribery behavior in

Vietnam through the use of a List question.

DATA AND METHODS

In this section we provide a clear application of this novel

measurement of corruption by drawing

on three waves of the Vietnam Provincial Competitiveness Index

(PCI) survey.7 This survey

paints a relatively comprehensive picture of domestic and

foreign firms in Vietnams 63

provinces with high response rates of 30% for domestic firms and

25% for foreign firms.8

Malesky et al (2013) document that this survey is representative

of the population of firms in

Vietnam. Most important for this study, of the 10,437 active

foreign firms, 46% of these firms

(4,821) are in our sample.

Foreign investment in Vietnam is largely dominated by firms from

East Asia. The five

largest investors include Taiwan (23.2%), South Korea (20.2%),

Japan (18.3%), China (7.2%),

and Singapore (4.2%). Our sample also includes 370 investors

from the EU, 112 investors from

the US, and 40 from Australia. While this concentration of

investment from East Asia may seem

like a liability for this study, two of the top five countries

(Japan and South Korea) are both 6 Habib and Zurawicki (2002) test

how the differences in the levels of corruption between host

and home government affect FDI.

7 For methodological details and background on the survey can be

found at www.pcivietnam.org.

8 See White and Luo (2006) for a discussion of response rates in

firm level surveys.

-

15

signatories of the OECD anti-bribery convention, while the

remaining three are not. Thus our

study provides the added benefit of a large number of investors

from the same region along with

considerable variation in signatories to the OECD

Convention.

The fact that the OECD convention criminalizes corruption, and

thus firms must avoid

openly admitting engaging in corruption, adds to an already long

list of concerns about the

measurement of corruption. For example, there has been serious

criticism leveled at perception-

based studies of corruption. Both Triesman (2007) and Olken

(2009) find very little correlation

between perceptions of bribery and the actual incidences of

bribery. One conjecture, forwarded

by Triesman, is that perceptions of corruption may be formed by

our beliefs of what causes

corruption, not on actual evidence of corruption. For example,

many scholars and practitioners

believe that natural resource dependent economies suffer from

greater levels of corruption.

Experts asked about their perception of corruption in a country

may use their knowledge of the

abundance (or scarcity) of natural resources to judge corruption

in the country. Similar

perception biases affect the ability to evaluate the OECD

Convention or democracy. Respondents

associate these attributes with less corruption and thus

evaluate them more highly when asked to

rank their corruption status.

This would be especially problematic in our study since

individuals knowledgeable of

investment in Vietnam know that foreign investment is dominated

by East Asian firms. These

firms often have reputations for high propensities for

corruption. Expert surveys indicating high

levels of corruption by foreign firms in Vietnam could be due to

detailed knowledge of

corruption, or simply hunches based on the composition of

investment.

Our approach directly asks respondents about their experience

with corruption, while

shielding them from incriminating themselves or being subject to

reprisal for answering sensitive

questions about corruption, thereby reducing downward bias in

corruption associated with the

OECD convention. We designed the PCI survey to include a

question that utilizes the

-

16

Unmatched Count Technique (UCT), which is also know as the list

question (Ahart and Sackett

2004; Coutts and Jann 2011).

List questions have been shown to be easy for respondents to

understand and outperform

other techniques in their ability to elicit sensitive answers

from respondents (Coutts and Jann

2011). This is done through allowing respondents the ability to

plausibly deny answering yes to

the sensitive questions. As noted earlier, this technique has

been applied to a number of

substantive questions in political science. In our context, a

respondent can admit to bribery

without fear that this information can be used against the

manager or firm.

This is accomplished by separating respondents, in our case

firms, into two groups that

through randomization are equal in terms of all observable

characteristics. One group, that we

call our control group receives a list of non-sensitive items

and is asked to indicate how many

of these items the respondent has engaged in. In our survey, we

ask firms about their experience

with registration. Respondents are instructed to indicate the

total number of activities that they

engaged in, but to not indicate the individual activities.

Respondents answer 0, 1, 2, or 3.

The other half of our sample, our treatment group, receives the

same list, but with one

additional sensitive question. In our survey, this is question 3

below. Respondents are given the

same instructions. Provide us a number, but do not indicate any

of the individual activities that

the firm or manager engaged in. Respondents answer 0, 1, 2, 3,

or 4.

Notice that the treatment group has one additional item than the

control group, which is

the crux of the experiment. If all of the respondents in the

treatment group provided bribes, we

would expect that the mean response of the treatment group to be

one point higher than that of the

control group. Conversely, if no firms paid bribes, the means

for the control and treatment group

should be the same.

-

17

UCT Question 1: Please take a look at the following list of

common activities that firms engage in to expedite the steps needed

to receive their investment license/registration certificate. How

many of the activities did you engage in when fulfilling any of the

business registration activities listed previously?

1. Followed procedures for business license on website. 2. Hired

a local consulting/law firm to obtain the license the firm for

you.9 3. Paid informal charge to expedite procedures (Only

Available on Form B of the

Survey)10 4. Looked for a domestic partner who was already

registered

This question was included on the 2010, 2011, and 2012 PCI

surveys that were mailed

out to firms in both English and Vietnamese. In Appendix A we

show that there is excellent

balance across the control and treatment groups, mitigating

concerns that differences between the

groups is attributable to differences in the sub-samples.

Another concern is that if these activities

are too frequent (everyone is answering at the maximum) or too

rare (most responses are zero),

respondent answers on the sensitive question are not shielded.

Luckily our survey indicates that

most firms answer one or two items, and few are near the floor

or the ceiling.11

One final concern is that while our survey includes three years,

some of the firms

registered prior to our first survey in 2010. While the majority

of our firms have registered within

the past five years (53% of foreign firms and 63% of domestic

firms), a small number of firms

registered as long as 15 years prior to the fielding of our

survey. Can we expect that these 9 This item is added, as firms can

avoid direct culpability for bribes by hiring a facilitator. By

including this as nonsensitive item, we seek to only capture

direct experience and conservatively

estimate a lower bound on bribe frequency. Because FIEs are more

likely to hire facilitators, they

have a slightly higher share of total activities in both control

and treatment averages, but there is

no bias in bribery estimates, which are the differences in means

between control and treatment

within a group.

10 Note informal charges (chi phi khong chinh thuc) is the

common Vietnamese and English term

to describe this type of bribery.

11 See Malesky et al (2013) for details.

-

18

managers remember bribes that took place so long ago? Are these

managers even still employed

with the firm?

Our survey construction mitigates these concerns, and any

measurement error is unlikely

to be biased. First, we include a clear and simple factual

question on whether or not a firm paid a

bribe at the point of registration, not details on the amount of

the bribe. This requires very limited

recall from managers. Second, including additional noise

(limited ability to recall for firms that

registered many years ago) should increase standard errors but

not bias results. As noted, we

have considerable over time variation in the sectors that are

restricted and unrestricted. While

this does include some noise into our data, this only makes our

job of finding significant

differences between the control and treatment group more

difficult.

Results To examine the impact of the OECD convention on bribery

behavior we utilize a two-stage non-

linear least squares (NLS) estimation model developed by Imai

(2011). This method uses a set of

covariates to model non-sensitive responses in the control group

and then uses this model to

estimate response for the treatment group. The Imai process

involves fitting a model to describe

the control group, then using the estimated coefficients to

predict new values for the treated

group, as described below.

( ) ( ) , :: response variable (total number of activities),:

treatment variable (received survey with sensitive item),: matrix

of covariates,

( ) : model for non-sensitive item

i i i i i

i

i

i

i

Y f X T X whereYTXf X

= + +

s (negative binomal regression),( ) : model for sensitive items

(non-linear least squares).ig X

We fit the ( )if X model to the control group via negative

binomial estimation (to

account for count nature of the data and the over-dispersion

caused by zero answers) in the first

stage. From this we obtain relationship between the response on

the nonsensitive questions and

-

19

each independent variable ( ). Then we fit the ( )ig X model in

the second stage using non-

linear least squares (NLS). Then after subtracting ( )if X from

we have a measure for the

relationship between participating in the sensitive behavior and

each independent variable ( ).12

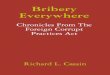

[Insert Figure 1 here]

In Figure 1 we present the predicted bribery in the control

group relative to the treatment

group, using a simple difference-in-means between the number of

activities completed.

Treatment firms engaged in 1.562 activities, while the control

group 1.355 activities. As the

figure shows, these means are significantly different,

indicating the success of the experiment.

Subracting the treatment from control averages, we find that on

average, 20.7% of foreign firms,

whose home country can be correctly identified, engaged in

bribery when entering the Vietnam

market.

While uncovering bribery by foreign firms is interesting, our

key test is how OECD

signatories fare relative to non-signatories. In Table 1, we

provide our breakdown of bribery by

different categories of investors. In the first four rows, we

present the raw data from our List

experiment for OECD non-signatories, while the bottom panel

presents data from signatories

countries. Of interest to most readers is the difference between

the control and treatment groups,

which is presented in the final column of Table 1. For instance,

we find that for non-OECD

signatories, the pattern is as expected. These countries with

weak bribery standards do engage in

bribery, and that this bribe activity increases in order to gain

access to restricted sectors. Firms

on average bribe 11.6% of the time to enter into an unrestricted

sector and 21.3% of the time to

enter into a restricted sector.

12 Standard errors are calculated using bootstrapping with 1,000

replications.

iY

-

20

Our results, while tentative, are more perplexing for the OECD

signatories. First, these

signatory countries are more likely to bribe entering into

unrestricted sectors relative to non-

signatory countries. We observe 25.8% of firms bribing to enter

into unrestricted sectors.

Surprisingly, this figure drops to a still large 18.6% of the

time in restricted sectors.

[Insert Table 2 here]

The results in Table 1 are tentative, since we are simply

presenting a broad comparison

across groups. In Table 2, we present a similar comparison, this

time focusing on how domestic

political institutions shape bribery. We specifically focus on

democratic institutions, where we

use the Cheibub et al. (2010) dichotomous measure of democracy.

Our most striking finding is

that while democratic and non-democratic home countries have

firms that engage in relatively

similar levels of bribery in non-restricted sectors (17.2% and

19.9%), the difference is extremely

large in the restricted sectors. While firms from democratic

home countries are found to bribe in

11.8% of the cases of investments in restricted sectors, this

number skyrockets to over 40% for

similar investment from non-democratic home governments. This

finding on democratic

governments illustrates the importance of home countries in

affecting bribery behavior. In this

paper, however, we are interested in the specific effect of the

OECD convention on bribery

behavior.

Our descriptive data are suggestive of the ineffectiveness of

the OECD bribery

convention, yet we are leaning heavily on the representativeness

of the comparisons between

groups. Are we so sure that firms on non-signatory countries are

investing in the same sectors or

type of operations? Thus these results are prone to suffer from

omitted variable bias that can be

mitigated through multivariate regression.

[Insert Table 3 here]

In Table 3 we present our results using the List methodology

from Blaire and Imai (2011)

outlined above. Note that our sample size is halved as it is a

two-stage model, where we first

estimate the number of non-sensitive items in the control group,

then use those estimates to

-

21

calculate bribery in the treatment group on the second stage.

Thus, our n only reflects the

observations in the treatment group.13 In Model 1, we present a

model with no controls, showing

that our results correctly recover the difference-in-means

estimate presented in Figure 1. We find

that 20.7% of firms pay bribes in our sample. Models 2-5 focus

on OECD signatories as the main

independent variable, coded 1 for signatories and 0 otherwise.

As a comparison, in Models 6-10

we examine how democratic institutions affects bribe

propensity.

In Model 2 we first include our dummy variable for OECD

signatories and Model 3

includes a dummy variable for restricted sectors. Model 4

includes the interaction of OECD

signatories and restrictions. Model 5 includes a number of

control variables.

Our results provide strong evidence that the OECD convention has

not been effective in

reducing bribes. In fact, we find signatories are slightly more

likely to bribe than non-signatories

once we correct for the reporting biases in perception surveys,

although the result is shy of

standard diagnostic of statistical significance. We find that

restrictions have no substantive

impact on bribery in this context, and equally important the

interaction (OECD signatories

investing in restricted sectors) is not significant. Once

controls for size and age of firm are added,

the impact of the OECD convention is indistinguishable from zero

in restricted or unrestricted

sectors.

Our results in Models 6-9 do find some weak evidence for

political institutions shaping

bribery behavior. In the fully specified model, we find that

firms are more likely to bribe to enter

into restricted sectors, and that this propensity is lower for

investors from democratic home

countries. Model 10, includes both our OECD signatory dummy

variable and our democracy

dummy variable. Again, we find no evidence that OECD signatories

are less likely to bribe,

13 To preserve space we only present the bribery results,

although they will be made available with our replication

materials.

-

22

although we do find that democratic governments do reduce

bribery, specifically when firms are

entering into restricted sectors.

[Insert Table 4 here]

Our empirical results point to the ineffectiveness of the OECD

convention, and point to

some positive impact of democratic institutions on reducing

bribery. Yet, our models largely

include country-level and firm level factors, ignoring the

potential sectoral factors that can shape

bribery behavior. In Table 4 we include dummy variables for

4-digit ISIC codes. Our results are

quite similar to the previous table. When comparing firms within

narrowly-defined industrial and

service sectors, we find that signatories of the OECD convention

are about 8% more likely to

provide bribes when registering their business overall, but this

effect is not conditioned by

whether the sector is restricted. Once sector effects are

introduced, we find that the democracy

result disappears. This indicates that the effect of democracy

from Table 3 is driven by selection

of firms from democracies into less corrupt industries.

This clue propels our final test. While we have focused on the

actual bribery behavior of

firms, an alternative way to examine the effectiveness of the

OECD Convention is to examine

how this convention shapes entry into restricted sectors. Again,

the sectors that are only

selectively open to foreign investment are those where firms

should be the most willing to

provide bribes, and government officials can use their power as

gatekeepers to extract bribers.

Firms that can not engage in bribery as a strategy to enter into

this markets are a major

disadvantage and thus we should see less entry into this sectors

by signatories of the OECD

convention. For comparison we also include test of how FDI from

democratic governments

enters into restricted sectors.

[Insert Table 5 here]

In Table 5 we present probit models of entry decisions. Marginal

probabilities of entry

are presented with standard errors (clustered at the province

level) in parentheses. In all four of

our models, we find that signatories of the OECD convention are

no more or less likely to enter

-

23

into this restricted sectors. In contrast, we do find evidence

that firms from democratic countries

are 5% less likely to enter into these restricted sectors.

Although the magnitude is modest, it does

indicate selection away from corrupt industries based on home

country status.

In summary, we find zero evidence that the OECD convention

reduces bribery behavior

or deters firms entering into sectors that are more prone to

bribery. This finding may come as a

surprise to some readers, where the OECD has legislative a

serious initiative aimed at reducing

bribery. Why isnt this effective?

We can not provide any definitive answer to this question, but

we can provide a bit of

descriptive data. In Figure 2 we present the variation of

bribery by home country for all countries

with at least 20 observations in our dataset. Two important

patterns are obvious. First, there is

tremendous variation in bribery by home country, with Indian,

Malaysian, and South Korean

firms most likely to pay bribers in our sample. Yet these

patterns do not clearly track map into

the OECD signatories, where signatory countries such as South

Korea, Australia, and France have

firm that have a high propensity to pay bribers.

Thus the simple conjecture is that the domestic laws, such the

US Foreign Corrupt

Practices Act, or the mechanisms for enforcement of the OECD

Convention are much more likely

to shape bribery behavior than simply signing the OECD

Convention.

CONCLUSION

In this paper we engage the large and growing literature on the

determinants of bribery in

business transactions. Using Vietnam as an ideal empirical case

study of liberalization, we utilize

unique survey data that directly measures corruption without

forcing managers to incriminate

themselves for illegal activities. Using this methodology we

find that roughly 20% of foreign

investments in Vietnam engaged in bribery to obtain a business

license.

We harness this data to answer a substantive question: how has

the OECD Convention on

Bribery of Foreign Public Officials in International Business

Transactions affected both bribery

-

24

by firms from signatory countries in Vietnam, and has it

deterred firms from signatory countries

into entering into sectors most prone to have firms engage in

bribery. Unfortunately, our results

point to the ineffectiveness of the convention on both counts.

We actually find that OECD

convention signatories are more likely to engage in bribes and

that there is no deterring effect of

the OECD convention on firms entering into highly corrupt

sectors.

This is not to say that home country institutions and policies

dont matter for outward

investors. On the contrary, we find that home country

institutions, specifically the level of

democracy, shapes bribery behavior. Countries with more

democratic institutions both have

firms that are slightly less likely to bribe, and are less

likely to enter into sectors that largely

require bribes to enter.

Thus our results do not find that international agreements

affecting can not be effective in

combating corruption. Rather, we see that the passage and

enforcement of anti-corruption laws

are largely within the realm of domestic politics and thus home

countries institutions are key to

both combating bribery and to giving international agreements to

teeth to enforce best practices of

ethical business behavior.

Our research also helps open avenues for new questions and

rigorous tests in

management. Our use of a LIST experiment allows us to have the

advantages of both obtaining

direct information on illegal or unethical activities, while at

the same time shielding respondents

from any repercussions from answering honestly. The applications

of this technique are vast,

where anything from employees admitting to shirking to

discrimination in the workplace are all

candidates for this approach.

We also believe there is at least one other advantage of this

technique. Existing

management research harnessing the power of surveys has

literally decades of results. We see

List questions as compliments to these studies and any

differences between surveys of managers

or outside experts can be contrasted with results from results

from List questions. These

-

25

differences not only tell us something about systematic

measurement error, they also provide

insights as to when individuals are unwilling to provide honest

answers.

One clear example directly related to corruption, is what

affects whether firms are willing

to provide answers about corrupt behavior. Jensen et al (2010)

find substantial non-response bias

to corruption questions in firm-level survey questions. They

find that managers are less likely to

answer questions on corruption or more likely to indicate low

levels of corruption in countries

with more authoritarian political institutions and lowers levels

of press freedom. These results

are suggestive of the type of political environments where firms

fear reprisals from politicians. A

List question allows for a more direct test, where under the

shield of anonymity, do we observe

substantially higher levels of reported corruption? This ability

to examine the conditions under

which employees, managers, and owners are willing to express

opinions may open avenues for

exploring new questions in management research.

-

26

References

Ades, Alberto, and Rafael Di Tella. 1999. Rents, Competition,

and Corruption. American

Economic Review 89 (4): 982993.

Ahart, Allison M., and Paul R. Sackett. 2004. A New Method of

Examining Relationships

between Individual Difference Measures and Sensitive Behavior

Criteria: Evaluating the

Unmatched Count Technique. Organizational Research Methods 7

(1): 101114.

Argandoa, Antonio. 2007. The United Nations Convention Against

Corruption and its Impact

on International Companies. Journal of Business Ethics 74:

481-496.

Bliss, Christopher and Rafeal Di Tella. 1997. Does Competition

Kill Corruption? The

Journal of Political Economy 101 (5): 10011023.

Beets SD. 2005. Understanding the demand-side issues of

international corruption. Journal of

Business Ethics 57(1): 6581.

Brouthers, Lance Elipt, Yan Gao, and Jason Patrick McNicol.

2008. Corruption and Market

Attractiveness on Difference Types of FDI. Strategic Management

Journal 29: 673-680.

Coutts, Elizabeth, and Ben Jann. 2011. Sensitive Questions in

Online Surveys: Experimental

Results for the Randomized Response Technique (RRT) and the

Unmatched Count

Technique (UCT). Sociological Methods & Research 40

(1):169-193

Cuervo-Cazurr 2008 A. 2008. The effectiveness of laws against

bribery abroad. Journal of

International Business Studies 39(4): 634651.

Clarke, George, and Lixin Xu. 2004. Privatization, competition,

and corruption: how

characteristics of bribe takers and payers affect bribes to

utilities. Journal of Public

Economics Vol. 88 (9-10): 20672097

Corstange, D. 2009. Sensitive questions, truthful answers?

Modeling the list experiment with

LISTIT. Political Analysis 17(1): 4563.

DSouza, Anna. 2012. The OECD Anti-Bribery Convention: Changing

the Currents of Trade.

Journal of Development Economics 97: 73-87.

-

27

Djankov, Simeon, Rafael La Porta, Florencio Lopez-De-Silanes and

Andrei Shleifer, 2002.

The Regulation of Entry. The Quarterly Journal of Economics

117(1): 1-37

Fisman, Raymond and Edward Miguel. 2007. Corruption, Norms, and

Legal Enforcement:

Evidence from Diplomatic Parking Tickets. Journal of Political

Economy 115 (6) 1020-

1048.

General Statistical Office (GSO). 2012. Socio-Economic

Statistical Data. Available at

http://www.gso.gov.vn/

Glynn, Adam N. 2010. What Can We Learn with Statistical Truth

Serum? Design and Analysis of

the List Experiment. Working Paper, Harvard University Institute

for Quantitative Social

Science.

Gonzalez-Ocantos, Ezequiel, Chad Kiewiet de Jong, Carloes

Melndez, Javier Osorio, and David

W. Nickerson. 2012. Vote Buying and Social Desireability Bias:

Experimental Evidence

from Nicaragua. American Journal of Political Science 56 (1):

202-217.

Graham, John L. 1984. The Foreign Corrupt Practices Act: A New

Perspective. Journal of

International Business Studies 15 (3): 107-121.

Habib M. and L. Zurawicki. 2002. Corruption and Foreign Direct

Investment. Journal of

International Business Review 10 (6): 687-700.

Hines, James Roger, 1995. Forbidden payment: foreign bribery and

American business

after 1977. NBER Working Paper W5266.

Holbrook, A. L. and Krosnick, J. A. 2010. Social desirability

bias in voter turnout reports: Tests

using the item count technique. Public Opinion Quarterly 74, 1,

37-67.

Hymer, Stephan H. 1976. The International Operations of National

Firms: A Study of

Direct Foreign Investment. Cambridge, MA: MIT Press.

Imai, Kosuke. 2011. Multivariate Regression Analysis for the

Item Count Technique.

Journal of the American Statistical Association 106 (494):

407416.

Janus, A. L. 2010. The influence of social desirability

pressures on expressed immigration

-

28

attitudes. Social Science Quarterly 91, 4, 928-946.

Jensen, Nathan M., Quan Li, and Aminur Rahman. 2010.

Understanding Corruption Using

Cross-National Firm-Level Surveys. Journal of International

Business Studies 41 (9):

14811504.

Kaufmann, Daniel, Hellman, Joel S., Jones, Geraint and

Schankerman, Mark A. 2000.

Measuring Governance, Corruption, and State Capture: How Firms

and Bureaucrats

Shape the Business Environment in Transition Economies. World

Bank Policy Research

Working Paper No. 2312.

Kolstad, Ivar and Tina Sreide. 2009. Corruption in natural

resource management:

Implications for policy makers. Resources Policy 34 (4):

214-226.

Kim, S and S. Barone. 1981. Is the Foreign Corrupt Practices Act

of 1977 a success or failure?

Journal of International Business Studies 12 (3): 123-126.

Kuklinski, J. H., M. D. Cobb, and M. Gilens. 1997. Racial

attitudes and the New South.

Journal of Politics 59:32349.

Kwok, Chuck, and Soloman Tadesse. 2006. The FIE as an Agent of

Change for Host-

Country Institutions: FDI and Corruption. William Davidson

Institution Working Paper

Number 882, September.

Jeong, Yujin and Robert J. Weiner. 2012. Who Bribes? Evidence

from the United Nations

Oil for Food Program. Strategic Management Journal 33:

1363-1383.

Lee, Seung-Hyu. Kyeungrae Oh and Lorraine Eden. 2010. Why Do

Firms Bribe? Insights

from Residual Control Theory into Firms Exposure and

Vulnerability to Corruption.

Management International Review 50: 775-796.

Luo, Yadong, Oded Shenkar, and Mee-Kau Nyaw. 2002. Mitigating

the liability of

Foreignness: Defensive versus Offensive Approaches. Journal of

International

Management 8 (3): 283-300.

Malesky, Edmund. 2008. Straight Ahead on Red: How Foreign Direct

Investment

-

29

Empowers Subnational Leaders. Journal of Politics 70 (1):

97119.

Maleksy, Edmund J., Dimitar Gueorguiev,, and Nathan M. Jensen.

2013. Monopoly Money:

Foreign Investment and Bribery in Vietnam, a Survey Experiment.

Working Paper.

Martin K, Cullen J, Johnson J, Parboteeah K. 2007. Deciding to

bribe: a cross-level analysis

of firm and home country influences on bribery activity. Academy

of Management

Journal 50 (6): 14011422.

Mauro, P. 1995. Corruption and Growth. Quarterly Journal of

Economics, CX, 681-712.

Miller, Stewart and Lorraine Eden. 2006. Local Density and

Foreign Subsidiary

Performance. Academy of Management Journal 49 (2): 341-355.

Olken, Benjamin. 2009. Corruption Perceptions vs. Corruption

Reality. Journal of Public

Economics 93 (7-8): 950-964.

Pacini, Carl, Judyth A. Swingen, and Hudson Rogers. 2002. The

Role of the OECD and

EU Conventions in Combating Bribery of Foreign Public Officials.

Journal of Business

Ethics 37: 385-405.

Peterson, Robert A., and Alain J. P. Jolibert. 1995. A

Meta-Analysis of Country-Of-Origin

Effects. Journal of International Business Studies 26 (4):

883-900.

Robertson, Christopher J. and Andrew Watson. 2004. Corruption

and Change: The Impact

of Foreign Direct Investment. Strategic Management Journal 25:

385-396.

Rodriguez P, Uhlenbruck K, Eden L. 2005. Government corruption

and the entry strategies of

multinationals. Academy of Management Review 30(2): 383396.

Sandholtz, Wayne, and Mark Gray. 2003. International Integration

and National

Corruption. International Organization 57(4): 761800.

Shimp, Terence A., and Subhash Sharma. 1987. Consumer

Ethnocentrism: Construction and

Validation of the CETSCALE. Review of Marketing Research. 24

(3): 280-89.

Spencer JW and Gomez C. 2011. MNEs and corruption: the impact of

national institutions and

subsidiary strategy. Strategic Management Journal 32(3):

280300.

-

30

Smarzynska, Beata K. and Shang-Jin Wei. 2000. Corruption and the

Composition of

Foreign Direct Investment: Firm-Level Evidence. NBER Working

Paper 7969.

Sniderman, P. M., P. E. Tetlock, and T. Piazza. 1992. Codebook

for the 1991 National Race and

Politics Survey. Survey Research Center, Berkeley,

California.

http://sda.berkeley.edu/D3/Natlrace/Doc/nrac.htm.

Streb, M. J., Burrell, B., Frederick, B., and Genovese, M. A.

2008. Social desirability effects and

support for a female American president. Public Opinion

Quarterly 72, 1, 76-89.

Svensson, Jakob. 2003. Who Must Pay Bribes and How Much?

Evidence from a Cross

Section of Firms. Quarterly Journal of Economics 118 (1):

207230.

Tanzi, Vito, and Hamid Davoodi. 1997. Corruption, Public

Investment, and Growth. IMF

Working Paper 97/139, Washington DC.

Tanzi, Vito. 1998. Corruption around the World: Causes,

Consequences, Scope, and Cures. IMF

Staff Papers 45 (4). Washington DC.

Tresiman, Daniel. 2000. The Causes of Corruption: A Cross

National Study. Journal of

Public Economics 73(3): 399-457.

Treisman, Daniel. 2007. What we have learned about the causes of

corruption from ten

years of cross-national empirical research? Annual Review of

Political Science. 10: 211

44.

Uhlenbruck K, Rodriguez P, Doh J, Eden L. 2006. The impact of

corruption on entry

strategy: evidence from telecommunication projects in emerging

economies.

Organization Science 17(3): 402414.

Wei, Shang-Jin. 2000. How Taxing is Corruption on International

Investors? Economics and

Statistics 82 (1): 1-11.

White, Glenn D., and Amy Luo. 2006. Business Survey Response

RatesCan They be

Improved. American Statistical Association Section on Research

Methods.

World Bank. 2010. World Development Indicators. Available at

-

31

http://data.worldbank.org/(accessed on Feb. 4, 2011).

Zaheer, S. 1995. Overcoming the liability of foreignness.

Academy of Management Journal 38:

341-63.

Zaheer, S. 2002. The Liability of Foreignness, Redux: A

Commentary. Journal of International

Management 8(3): 351-358.

Zaheer, S. and E. Mosakowski. 1997. The dynamics of the

liability of foreignness: A global

study of survival in financial services. Strategic Management

Journal 18: 439-64.

-

32

Figure 1: Bribe Share of Firms

1.562

1.355

20.7% Bribe

11.

051.

11.

151.

21.

251.

31.

351.

41.

451.

51.

551.

61.

651.

7

Num

ber o

f Act

iviti

es d

urin

g R

egis

tratio

n

95% CI Treatment Mean

95% CI Control Mean

95% CI for Bribe Frequency

-

33

Figure 2: Share of Firms Paying Bribes at Entry (By Foreign

Firm)

Note: Analysis limited to countries with 20 or more

responses.

0 5 10 15 20 25 30 35 40 45 50 55 60 65 70 75 80 85 90 95

100

Canada

Netherlands

Thailand

Hong Kong

Taiwan

United States

Japan

Singapore

Germany

United Kingdom

China

France

Australia

South Korea

Malaysia

India

OECD Member

Non-Member

-

34

Table 1: Calculation of Firms Paying Bribes at Entry (By OECD

Convention and Restricted Sector) OECD Restricted Treatment Mean SE

Low High Bribe No No No 1.35 0.04 1.27 1.43 11.6% No No Yes 1.46

0.04 1.38 1.55 No Yes No 1.36 0.11 1.15 1.58 21.3% No Yes Yes 1.58

0.09 1.39 1.76 Yes No No 1.39 0.04 1.31 1.46 24.9% Yes No Yes 1.64

0.04 1.56 1.72 Yes Yes No 1.37 0.08 1.20 1.53

20.2% Yes Yes Yes 1.57 0.10 1.37 1.77

-

35

Table 2: Calculation of Firms Paying Bribes at Entry (By Regime

Type and Restricted Sector) Democracy Restricted Treatment Mean SE

Low High Bribe

No No No 1.35 0.07 1.23 1.48 17.2% No No Yes 1.53 0.07 1.39 1.66

No No No 1.14 0.14 0.86 1.41 40.5% No Yes Yes 1.54 0.16 1.23 1.85

Yes No No 1.37 0.03 1.31 1.43 19.9% Yes No Yes 1.57 0.03 1.50 1.63

Yes No No 1.44 0.08 1.29 1.59

11.8% Yes Yes Yes 1.55 0.08 1.40 1.70

-

36

Table 3: Correlates of Corruption during Business Entry

Bivariate Restrict Interaction Full Bivariate Restrict

Interaction Full(1) (2) (3) (4) (5) (6)_ (7) (8) (9) (10)OECD

Signatory 0.084 0.111 0.133** 0.041 0.027(0.067) (0.091) (0.058)

(0.059) (0.034)Democracy=1 -0.057 -0.035 0.027 0.031 0.010(0.040)

(0.053) (0.071) (0.060) (0.078)Restricted Sector 0.028 0.097 0.062

-0.017 0.232*** 0.196*** 0.188(0.091) (0.077) (0.079) (0.157)

(0.079) (0.065) (0.134)OECD*Restrict -0.144 0.003 0.149

0.149(0.091) (0.161) (0.135) (0.135)Democracy*Restrict -0.314***

-0.204* -0.304**(0.066) (0.115) (0.146)Capital Size at

Establishment -0.008 -0.013 -0.013(0.024) (0.021) (0.023)Time

-0.067*** -0.068** -0.065**(0.025) (0.034) (0.030)Time Squared

0.003*** 0.003* 0.003**(0.001) (0.002) (0.001)Constant 0.207***

0.161*** 0.128 0.116 0.451** 0.252*** 0.224** 0.172* 0.477**

0.452***(0.034) (0.055) (0.106) (0.096) (0.220) (0.058) (0.110)

(0.092) (0.193) (0.161)SurveyWave FE No No No No Yes No No No Yes

YesObservations 1,454 1,454 1,337 1,337 1,074 1,431 1,316 1,316

1,057 1,057rmse 0.994 0.993 0.996 0.996 0.955 0.994 0.999 0.999

0.956 0.956ll -2054 -2052 -1891 -1890 -1470 -2021 -1864 -1864 -1447

-1446

Combined

Note: These results are derived from a two-stage model. In the

first stage, the number of nonsensitive activities is regressed on

the covariates for the control group using a negative binomial

specification. The predicted number of nonsensitive activities is

then subtracted from the total number of registration activities

for the treatment group. The difference becomes the dependent

variable in the second stage, which is analyzed using a Non-Linear

Least Squares (NL) specification in this model. Note that the

number of observations (N) is the number of respondents in the

treatment group. As Model 1 shows, the process correctly delivers

the difference-in-means estimator for the whole sample and by year,

indicating that the two-stage procedures yields unbiased estimates.

Because the dependent variable is an estimate, standard errors are

calculated are through bootstrapping procedure with 1000

repetitions . Errors are clustered at the province level, which is

the main interface for business registration. ( *** p

-

37

Table 4: Correlates of Corruption During Business Entry (with

4-Digit Sector Dummies)

Direct Interaction Direct Interaction(3) (4) (7) (8) (10)OECD

Signatory 0.081* 0.082 0.068(0.047) (0.053) (0.056)Democracy=1

0.025 0.058 0.014(0.087) (0.091) (0.100)Restricted Sector 0.049

0.160 0.166(0.244) (0.340) (0.343)OECD*Restrict -0.058

-0.273(0.136) (0.235)Democracy*Restrict -0.195 0.110(0.228)

(0.125)Capital Size at Establishment -0.027 -0.028 -0.032* -0.033*

-0.032*(0.018) (0.018) (0.017) (0.017) (0.018)Time -0.052**

-0.053** -0.054** -0.053** -0.049*(0.023) (0.023) (0.025) (0.024)

(0.024)Time Squared 0.002* 0.002* 0.002* 0.002* 0.002(0.001)

(0.001) (0.001) (0.001) (0.001)Constant 0.475*** 0.475*** 0.524***

0.494*** 0.455***(0.169) (0.166) (0.165) (0.158) (0.161)SurveyWave

FE Yes Yes Yes Yes YesSector FE Yes Yes Yes Yes YesObservations

1,074 1,074 1,057 1,057 1,057rmse 0.950 0.951 0.952 0.952 0.951ll

-1431 -1429 -1409 -1409 -1407Note: These results are derived from a

two-stage model. In the first stage, the number of nonsensitive

activities is regressed on the covariates for the control group

using OLS. The predicted number of nonsensitive activities is then

subtracted from the total number of registration activities for the

treatment group. The difference becomes the dependent variable in

the second stage, which is analyzed using OLD. Note that the number

of observations (N) is the number of respondents in the treatment

group. Because the dependent variable is an estimate, standard

errors are calculated are through bootstrapping procedure with 1000

repetitions . Errors are clustered at the province level, which is

the main interface for business registration. ( *** p

-

38

Table 5: Determinants of Entry into Restrict Sector (Marginal

Probability) Restrict=1 (1) (2) (3) (4) OECD -0.002 -0.003 0.015

0.018 (0.031) (0.031) (0.028) (0.017) Democracy -0.051* -0.049**

(0.029) (0.019) Labor at establishment -0.022** (0.010) Capital at

establishment 0.014* (0.008) Optimism 0.005 (0.009) Survey Wave FE

No Yes Yes Yes Observations 2,980 2,980 2,937 1,917 pbar 0.163

0.163 0.162 0.151 Pseudo R-Squared 0.000143 0.00146 0.00350 0.0203

ll -1324 -1322 -1295 -796.3 Robust standard errors in parentheses;

*** p

-

39

Appendix A: Balance Test for Foreign Invested Enterprises

Treated Control Treated Control p-value t-statSectors

(Services=1, Manf & other=0) 0.252 0.260 0.434 0.439 0.505

-0.667Province Attributes

GDP 117276 118411 127688 132351 0.769 -0.294Population (10,000)

2837.5 2890.0 2384.5 2429.8 0.462 -0.736Paved Roads (%) 0.770 0.761

0.172 0.174 0.067 1.832Telephones Per Capita (%) 0.278 0.277 0.081

0.080 0.535 0.620Industrial Zone* 0.498 0.476 0.500 0.500 0.151

1.436Region [nominal] 3.970 4.013 2.353 2.331 0.538 -0.616National

Level City* 0.380 0.385 0.486 0.487 0.749 -0.320Distance to

Hanoi/HCMC (km) 79.7 87.6 163.3 170.9 0.110 -1.598

Firm AttributesYear Registered 2004 2003 4.601 4.746 0.003

2.941Time to Register (days) 49 61 82 211 0.059 -1.889Employment

[1-8] 3.748 3.746 1.629 1.662 0.962 0.047Equity [1-8] 4.724 4.696

1.767 1.873 0.652 0.451Joint Venture* 0.103 0.110 0.305 0.313 0.468

-0.725Fully Owned* 0.813 0.814 0.390 0.389 0.977 -0.028Land Rights*

2.275 2.272 0.525 0.538 0.879 0.153

Business BurdenBribe Size [1-8] 6.665 6.714 1.285 1.210 0.270

-1.103Bureaucracy Rent Burden [1-4] 2.812 2.764 0.677 0.625 0.022

2.294Bureaucracy Time Burden [1-6] 4.820 4.794 1.202 1.173 0.525

0.635Document Burden* 0.234 0.312 0.424 0.463 0.000 -5.161Annual

Inspections 2.297 2.533 2.988 2.718 0.010 -2.569Performance

(y-on-y) -56.390 -41.885 63.356 59.823 0.000 -5.879

GovernanceWeighted PCI [0-100] 60.221 59.997 4.145 4.169 0.069

1.820Service Provision [1-5] 3.365 3.512 1.105 0.966 0.000

-4.038Proactiveness [0-10] 4.722 4.768 1.460 1.460 0.293

-1.051Informal Charges [0-10] 6.835 6.718 0.918 0.885 0.000

4.389Transparency [0-10] 6.125 6.121 0.528 0.533 0.807 0.244*binary

variable

(N = 4,821) Mean Std. Deviation

-

40

Appendix B: Country of Origin of Investors

Home Country ID OECD DemocracyFirms in restricted sectors

NArgentina 1 1 1 1Australia 2 1 1 35.1% 40Austria 3 1 1 33.3%

3Belgium 4 1 1 28.6% 8Brunei Darussalam 5 0 0 0.0% 6Cambodia 6 0 0

0.0% 2Canada 7 1 1 27.3% 13China 8 0 0 14.2% 221Cuba 9 0 0 0.0%

1Cyprus 10 0 1 0.0% 1Czech Republic 11 1 1 66.7% 4Denmark 12 1 1

21.1% 20Finland 13 1 1 1France 14 1 1 20.8% 80Germany 15 1 1 15.0%

42Hong Kong 16 0 0 23.9% 97Hungary 17 1 1 0.0% 1India 18 0 1 35.7%

14Indonesia 19 0 1 33.3% 7Ireland 20 1 1 0.0% 1Israel 21 0 1 50.0%

5Italy 22 1 1 44.4% 10Japan 23 1 1 16.5% 620Korea (Democratic

Peoples Rep.) 24 0 0 20.0% 16Laos 26 0 0 66.7% 4Macau 27 0 0 20.0%

5Malaysia 28 0 0 19.3% 93Monaco 29 0 1 0.0% 1Netherlands 30 1 1

32.0% 26New Zealand 31 1 1 0.0% 2Nigeria 32 0 0 0.0% 1Norway 33 1 1

33.3% 7Panama 34 0 1 100.0% 1Philippines 35 0 1 50.0% 10Poland 36 1

1 50.0% 2Romania 37 0 1 0.0% 1Russian Federation 38 1 0 40.0%

6Samoa 39 0 0 0.0% 1Singapore 40 0 0 23.6% 154Slovakia (Slovak

Rep.) 41 1 1 0.0% 1South Africa 42 1 1 1South Korea 43 1 1 10.4%

649Spain 44 1 1 2Sri Lanka 45 0 0 0.0% 1Swaziland 46 0 0 0.0%

2Sweden 47 1 1 0.0% 6Switzerland 48 1 1 40.0% 10Taiwan 49 0 1 13.0%

769Thailand 50 0 1 16.9% 89Turkey 51 1 1 0.0% 1Ukraine 52 0 1 0.0%

2United Kingdom 53 1 1 27.7% 51United States 54 1 1 19.2% 112

-

41

Appendix C: Investment Restrictions by Sector

Catching aquaculture R R R OPEN OPENLogging and silviculture R R

R R RExtraction of crude and gas R R R R RMining coal and ignite RA

RA RA RA RAMining of metal ores RA RA RA RA RAMining and quarrying

clay, stone RA RA RA RA RAManufacture of sugar and alcohol R R R R

RManufacture of tobacco R R R R RPublishing and Journalism RA RA RA

RA RAManufacture of chemicals R R R R OPENManufacture of

pharmaceuticals R R R R RManufacture of cement R R OPEN OPEN

OPENManufacture of refined petroleum R R R R RProduction of

electricity R R R R RInfrastructure construction R R R OPEN

OPENLand transport and railways R R R R RSea and inland water

transport R R R R OPENAir transport R R R R RTransport and travel

activities R R R R RPost and telecomm R R R R RTourism R R R R

OPENFinancial intermediation (banks) R R R R RInsurance and pension

funding R R R OPEN OPENAuxiliary financial activities R R R OPEN

OPENReal Estate RA RA RA RA RAResearch and development R R R OPEN

OPENLegal, accounting, and auditing R R R R RPublic security and

defense RA RA RA RA RAHigher Education RA RA RA RA RAHealth

services R R R R OPENSewage and refuse disposal R R R R RMotion

picture, TV, entertainment R R R R RR=Restricted to Foreign

Investors, RA= Restricted to all Investors, OPEN= Open to all

InvestorsUSBTA = United States Bilateral Trade AgreementISIC =

International Standard Industrial Classification WTO = World Trade

OrganizationSource: Authors' coding referencing various years of

Vietnamese Foreign Investment Law available at

Restricted sectors As of 1996

Post-2009 (WTO phase-in)Pre-2000

2000-2005 (USBTA era)

2005-2007 (Common

investment law)

2007-2009 (WTO era)

JensenMaleksy_Country of Origin_Working Paper_Aug

29_2013.pdfJensenMaleksy_Country of Origin_Working Paper_Aug

29_2013.2JensenMaleksy_Country of Origin_Working Paper_Aug

29_2013.3