Embed Size (px)

Citation preview

7/27/2019 Bridging the Pioneer Gap The Role of Accelerators in Launching High Impact Enterprises .pdf

http://slidepdf.com/reader/full/bridging-the-pioneer-gap-the-role-of-accelerators-in-launching-high-impact 1/33

Bridging the “Pioneer Gap”:The Role of Accelerators in Launching High-Impact Enterprises

A report by the Aspen Network of Development Entrepreneurs and Village Capital

With the support of:

Ross BairdLily BowlesSaurabh Lall

7/27/2019 Bridging the Pioneer Gap The Role of Accelerators in Launching High Impact Enterprises .pdf

http://slidepdf.com/reader/full/bridging-the-pioneer-gap-the-role-of-accelerators-in-launching-high-impact 2/33

The Aspen Network of Development Entrepreneurs (ANDE)The Aspen Network o Development Entrepreneurs (ANDE) is a global

network o organizations that propel entrepreneurship in emerging markets. ANDE members provide critical nancial, educational, and busi-ness support services to small and growing businesses (SGBs) based onthe conviction that SGBs will create jobs, stimulate long-term economicgrowth, and produce environmental and social benets. Ultimately, we believe that SGBS can help lit countries out o poverty. ANDE is part o the Aspen Institute, an educational and policy studies organization. Formore inormation please visit www.aspeninstitute.org/ande.

Village Capital Village Capital sources, trains, and invests in impactul seed-stage enter-prises worldwide. Inspired by the “village bank” model in micronance,

Village Capital programs leverage the power o peer support to provideopportunity to entrepreneurs that change the world. Our investment pro-cess democratizes entrepreneurship by putting unding decisions into the hands o entrepreneurs themselves. Since 2009, Village Capital has servedover 300 ventures on ve continents building disruptive innovations inagriculture, education, energy, environmental sustainability, nancialservices, and health. For more inormation, please visit www.vilcap.com.

Report released June 2013

Cover photo by TechnoServe

7/27/2019 Bridging the Pioneer Gap The Role of Accelerators in Launching High Impact Enterprises .pdf

http://slidepdf.com/reader/full/bridging-the-pioneer-gap-the-role-of-accelerators-in-launching-high-impact 3/33

Table of ContentsExecutive Summary

I. Introduction

II. Backgrounda. Incubators and Accelerators in Traditional Business Sectorsb. Incubators and Accelerators in the Impact Investing Sector

III. Data and Methodology

IV. The Landscape of Impact-Focused Acceleratorsa. Geographic Scopeb. Organizational Structurec. Funding Sources

V. Enterprise Pipeline and Selectiona. Sector and Impact Objectivesb. Enterprise Stage of Developmentc. Enterprise Recruitment and Selection

VI. Services and Benetsa. Duration and Frequency of Programb. Services Providedc. Post-Program Support

VII. Accelerator Networksa. Types of Formal Partnershipsb. Partnerships with Impact Investors

VIII. Metrics and Evaluationa. Financial and Social Performance Data Collectionb. Accelerator Graduate Performance

IX. Measuring Accelerator Performance: First Steps

X. Conclusions and Next StepsXI. Recommendations

Acknowledgments

AppendicesList of Surveyed AcceleratorsList of Surveyed Investors

References

7/27/2019 Bridging the Pioneer Gap The Role of Accelerators in Launching High Impact Enterprises .pdf

http://slidepdf.com/reader/full/bridging-the-pioneer-gap-the-role-of-accelerators-in-launching-high-impact 4/33

Executive SummaryOver the past several years, researchers and practitioners have increasingly highlighted a consistent gap in capital and support between social enterprises and impact investors, a gap which incubatorsand accelerators can play a critical role in bridging. These organizations support early-stage socialenterprises by providing them with a range o services, such as business development support, mentoring,inrastructure, as well as access to networks o investors, oundations, and corporations. This report represents the rst quantitative assessment o the impact accelerator landscape, with data rom 52organizations globally, collected by ANDE and Village Capital between November 2012 and February 2013.

We present ndings in 6 key areas:

• TheLandscapeofAccelerators: While nearly 75% o all accelerators in our sample rely on somelevel o philanthropic support, about one-third are structured as or-prots, suggesting that they expect to develop sustainable revenue streams in the uture. Currently, over 50% o all unding oraccelerators is rom philanthropy.

• EnterprisePipelineandSelection:Employment, economic development, health, clean energy,and agriculture are the most common impact areas that accelerators ocus on. These acceleratorstypically spend 1-2 months recruiting each cohort, but are not as selective as traditional business

accelerators.• ServicesandBenets:The majority o accelerators provide the same set o core services –

mentorship, access to investors, networks o partners, and business skills development. About 50%also provide direct unding to the enterprises.

• AcceleratorNetworks: Accelerators also seek to develop ormal partnerships with a range o dierent types o organizations, including impact investors, commercial investors, oundations,governments, and universities. However, many impact investors preer to maintain inormalrelationships with accelerators, though they do not commit any capital to the accelerator’s operationsor its enterprises.

• MetricsandEvaluation: While the majority o accelerators collect nancial data, almost one-third do not collect any social perormance data. Additionally, 23% o the accelerators in our sampledid not collect data on the status o their graduate enterprises, making it dicult to assess their

perormance.

• MeasuringAcceleratorPerformance: We ound that selectivity and partnerships with in-country commercial investors are associated with higher accelerator perormance. However, we did not ndany relationship between accelerator perormance and the level o philanthropic unding.

This report is the rst step o our broader initiative to strengthen incubators and accelerators in the impact investing ecosystem. We believe our research will provide signicant value or the enterprises, investors,and unders that support accelerator services, in addition to the accelerators themselves. Our work willprovide answers to critical questions that will allow entrepreneurial rms to make more educated decisionsabout whether to join an incubator, and i so, which one. It will inorm accelerator managers about best-in-class practices and provide mechanisms to improve their perormance. Finally, oundations, investors

and development institutions will be able to assess the impact o their investments and identiy strategies toscale or replicate successul incubator models.

7/27/2019 Bridging the Pioneer Gap The Role of Accelerators in Launching High Impact Enterprises .pdf

http://slidepdf.com/reader/full/bridging-the-pioneer-gap-the-role-of-accelerators-in-launching-high-impact 5/332

I. Introduction

Bridging the “Pioneer Gap”

Despite an age o unprecedented global wealth, billions o people worldwide live in

poverty. Over the past decade, however, governments, the nonprot sector, and the business world have proactively explored the ability o small and growing businesses(SGBs) to reduce poverty, particularly in emerging markets. The promise o market- based solutions to social problems has generated much excitement about “impact investing”—an investment strategy seeking positive social/environmental returns beyond nancial. According to a 2013 JPMorgan/GIIN study, a total o $17 billion isexpected to be deployed into socially benecial sectors in 2012-2013.1 However, thiscapital is not yet reaching many o the innovative SGBs that can contribute to poverty alleviation through the jobs they create, and the products and services they provide. While social enterprises continue to emerge (Village Capital alone has seen over 5,000applications rom impact-ocused entrepreneurs worldwide over the last three years.),many innovative companies in their early stages have ound diculty in getting o theground. They are still not able to access and take advantage o this new fow o capital orother support and resources they need to succeed.

A 2012 report rom Monitor-Deloitte and the Acumen Fund highlights this paradox-“The Pioneer Gap: While thousands o early-stage innovators seeking impact launchcompanies worldwide, very ew are able to build the teams, nd the customer base, orraise the investment necessary to scale.”2 The “Pioneer Gap” specically reers to the burden shouldered by enterprises that are pioneering new business models or socialchange. Monitor-Deloitte and Acumen identiy our stages that these rms typically progress through, rom the blueprint stage, to validation, preparation, and nally, scale.The “Pioneer Gap” occurs between the early stages in an enterprise’s growth, when it isnot considered investable by many impact investors.

The “Pioneer Gap” hypothesis is supported by additional research on this sector. In anindustry survey conducted in 2012 by Village Capital, o over 300 sel-described “impactinvestment” unds, ewer than 10 invested at less than $250,000/company.3 Additionallya Monitor-Deloitte study o Arican impact investors ound that only 6 o 84 invested at the early stage.4

Impact investors cite “lack o appropriate capital across the spectrum” and “lack o investable enterprises” as the top two barriers to deploying more impact investment,suggesting that the bottleneck o (a) not enough quality companies in the early stageand (b) not enough eective support to produce later-stage investable companies isthwarting the growth o this sector.

The Role of Accelerators

Over the past several years, actors in the impact investing sector have developed agrowing recognition that early-stage support—specically, in the orm o businessincubators and accelerators—is a key intervention to addressing the “Pioneer Gap.”Business incubators and accelerators support early-stage entrepreneurs by providing them with: (a) business development support (e.g. consulting, technology assistance);(b) inrastructure support (e.g. access to oce space, shared back-oce services);(c) network support (e.g. access to potential customers, investors, mentors), and (d)nancial support (in the orm o grants/investments). This study surveys 52 impact-ocused accelerators worldwide, to better understand their characteristics, operations,and perormance.

ncubator or Accelerator?n traditional businessectors, “incubators” andaccelerators” generally focusn different stages of enterpriseevelopment - incubatorsypically serve earlier stagenterprises (pre-customers and

re-revenue), while acceleratorsupport enterprises withxisting customers and revenue.owever, we have found that

hese differences are lessistinct for the impact investingector. For the purposes of thisaper, we will use the termaccelerator” to describe anrganization that provides someubset of the support outlined

n this report, at any stage ofevelopment.

7/27/2019 Bridging the Pioneer Gap The Role of Accelerators in Launching High Impact Enterprises .pdf

http://slidepdf.com/reader/full/bridging-the-pioneer-gap-the-role-of-accelerators-in-launching-high-impact 6/333

This research is particularly timely. Over the past ve years, the number o accelerators has grown signicantly—73% o accelerators surveyed are ewer than ve years o age. While the role o accelerators in entrepreneurship has been studied to some extent—and we will review the existing literature in the next section—studies are largely limited toaccelerators ocused on technology companies in developed markets (U.S. and Europe). Very little research exists on accelerator activity in emerging markets, and almost noneon the role o accelerators ocused on impact investment. With over 40 impact ocusedaccelerators ounded in the last hal-decade, an accurate assessment o what accelerators

are doing and where is necessary—so that we can eventually understand how acceleratorsare doing in addressing market-based solutions to poverty.

ANDE and Village Capital believe there is a pressing need or a more holistic, evidence- based approach to leverage the potential o incubators and accelerators, and tounderstand what makes them successul. This report “Bridging the Pioneer Gap,” buildson an earlier piece o research conducted by Village Capital, and represents the rst data-driven analysis o the social enterprise accelerator landscape. Through a comprehensivesurvey o accelerators’ pipeline, services, networks, and outcomes, we expect ndings to be relevant to accelerators, impact investors, philanthropists, entrepreneurs, and the broadereld o SGB development.

ocial Entrepreneurship or

mpact Investment?veral terms over the pastrty years have been used toscribe market-based solutionssocial problems: “socialtrepreneurship”, popularizedBill Drayton, the founder ofhoka; “impact investing”,

oneered by the Rockefellerundation and the Global Impactvesting Network, Base of theramid businesses, coined byahalad & Hart, and severalhers (e.g. “Triple-bottom-linevesting, Inclusive Business.”)ven that accelerators arepically both enterprise andvestor facing, for this report,e will use “impact investing” &ocial enterprise” to encompass

l business activity that seeksuse markets to address socialoblems, as well as investmentrategies that proactively seekcial/environmental returns indition to nancial returns.

7/27/2019 Bridging the Pioneer Gap The Role of Accelerators in Launching High Impact Enterprises .pdf

http://slidepdf.com/reader/full/bridging-the-pioneer-gap-the-role-of-accelerators-in-launching-high-impact 7/334

II. Backgrounda. Incubators and Accelerators in Traditional Business Sectors

The study o social-impact ocused incubators and accelerators is in its inancy. However, the collectedresearch on business incubators and accelerators in developed markets provides a basis or guidance in thisstudy.

The critical ocus o researchers, prominently Vanderstraeten, McMullen, and Sherman, stress that any accelerator has a relatively high nancial cost or unders (as a percentage o unds deployed, compared totraditional venture capital) and time-cost or participants; as a result, they stress the upront importance o perormance evaluation or accelerators, yet recognize that measuring perormance is oten challenging.5

Lalkaka states that the perormance o a business incubator should be measured by “the survival and growtho the businesses it incubates.” However, there is little consensus among researchers on the best measuresor enterprise growth.6 Various studies suggest growth in sales, employees, cash fow, and assets as measureso success. Vanderstraeten and Matthyssens review the literature on incubators and accelerators, andsuggest the ollowing two measures o perormance: (1) Number o companies which have had an IPO or were acquisition targets, (2) Number o companies which have not had an IPO or been acquired, but are stillactive.

There is some consensus on the key actors that lead to accelerator success:

• OrganizationalResources:Some research suggests that ‘resource dependency’, or the unding structure or accelerators can have an impact on their perormance. Chandra and Fealey suggest that over-reliance on philanthropic support can have a negative relationship with acceleratorperormance.7

• Selection: A number o studies conrm that enterprise selection has a critical relationship withaccelerator perormance, and a rigorous selection process enables incubators and accelerators toevaluate key enterprise characteristics. Screening best practices include evaluating managerial,product, and nancial characteristics, as well as market dynamics. 8

• Qualityof(andAccessto)Services:The same researchers suggest that access to proessionalmanagement services, as well as other supporting resources (administrative support, accounting,marketing, legal support), are considered important—yet the quality of services and period of

engagement have a stronger relationship with the success o an accelerator.9

• Networks:Haanasalo and Eckham argue that the most important actor or incubator success isorganized networking, with the most critical service being a strong network o experts, potentialinvestors, and business contacts.10

Yet to date, conclusive evidence on accelerator perormance is mixed in traditional business sectors. BothFerguson and Lösten suggest that startup companies with accelerator intervention have a higher survivalrate11 and rate o sales growth12, compared to similar startup companies without exposure to an accelerator.

Conversely, Amezcua studied a nationally representative sample o rms in the US and ound that in act,incubated rms ail 10% sooner than their non-incubated counterparts. Incubated enterprises demonstrateshort-term employment and sales growth, but ail sooner, suggesting that the protective environment o anincubator may actually inhibit the rms rom developing resilient routines and competencies13. In this same vein, in his study o business incubators in Europe, Ratinho ound that there is oten a mismatch between theservices that incubators oer and the needs o participating enterprises14.

Underscoring all these ndings are the relative paucity o signicant research conducted on acceleratorinputs and enterprise outcomes—necessitating an exploration o the “impact investing”/”socialentrepreneurship” landscape.

7/27/2019 Bridging the Pioneer Gap The Role of Accelerators in Launching High Impact Enterprises .pdf

http://slidepdf.com/reader/full/bridging-the-pioneer-gap-the-role-of-accelerators-in-launching-high-impact 8/335

b. Incubators and Accelerators in the Impact Investing Sector

According to our ndings, the number o accelerators serving impact enterprises has grown rapidly in thelast ve years (over 70% o the accelerators surveyed were ounded in 2008 or later). Despite this strong growth, limited research and data-driven analysis o accelerators’ role in the impact investment ecosystemexists. This report is a rst step towards generating a greater understanding o accelerators in the impact investment sector, and is part o a broader strategy to analyze, evaluate, benchmark, and strengthenaccelerators. This report is not intended to be a comprehensive evaluation o impact accelerators, but rather

an initial assessment o the landscape o these organizations.

We have divided this report into six sections:

• TheLandscapeofAccelerators: We present an overview o the data collected rom 52 incubatorsand accelerators between November 2012 – February 2013, ocusing on key descriptors such asorganizational structure, nances, geographic scope, and human capital. This overview presents a valuable landscape o a growing group o accelerators proactively seeking impact beyond nancialreturns.

• EnterprisePipelineandSelection: We discuss key impact areas, the stage o the enterprises they support, and their recruitment and selection processes.

•

ServicesandBenets:In this section, we examine the various services that accelerators provide totheir enterprises, the duration o their programs, and the requency o the mentoring sessions. Wealso study post-program support that accelerators provide.

• AcceleratorNetworks: We review the various kinds o ormal partnerships that acceleratorstypically seek, with impact investors, commercial investors, oundations, governments, anduniversities. We also present ndings rom our survey o investors, about their connections withaccelerators.

• MetricsandEvaluation: We discuss accelerators’ eorts to collect nancial and socialperormance data rom their enterprises, and identiy gaps in current practices.

• MeasuringAcceleratorPerformance : In this section, we examine which actors (in terms o organizational age, structure, selection, services, and networks) are associated with improved

accelerator perormance, drawing rom the literature on traditional incubators and accelerators. We do not suggest any potential causality through this analysis, but expect the ndings to provideguidance to more rigorous evaluations o social enterprise accelerator perormance in the uture.

Based on our ndings, we highlight common conclusions and trends that we hope can help unders,investors, and enterprises better leverage accelerators to drive enterprise impact and growth. We conclude by providing a series o recommendations or these various groups.

7/27/2019 Bridging the Pioneer Gap The Role of Accelerators in Launching High Impact Enterprises .pdf

http://slidepdf.com/reader/full/bridging-the-pioneer-gap-the-role-of-accelerators-in-launching-high-impact 9/336

III. Data and Methodology Village Capital launched the rst phase o this project in Spring 2012, gathering initial data romaccelerators in the impact investment sector, and joined ANDE in Summer 2012 to integrate initial ndingsinto a broader research strategy on accelerators. In October 2012, Village Capital and ANDE sharedndings rom an initial survey o 25 accelerators at SOCAP, and other conerences, in the report “Bridging the Gap: The Role o Accelerators in Impact Investing”.

Based on the eedback rom various stakeholders, including impact investors, accelerators, oundations,and academics, Village Capital and ANDE revised the survey in October 2012, sending it to 50 additionalaccelerators identied through our networks in mid-November 2012. The 25 original respondents alsoreceived a supplemental survey to enable comparable data points rom the rst research report. In January 2013, we identied a urther 122 incubators and accelerators through F6S, a website that serves as a bulletin board or upcoming incubator and accelerator programs or startups. We asked all accelerators surveyedupront or “impact objectives beyond nancial returns,” and allowed accelerators to state that they “have noimpact objective beyond nancial returns”, in order to enable a comparison o impact-ocused acceleratorsto non-impact ocused programs.

Initial eedback rom the rst report also ocused on investors: given 98% o accelerators surveyed listed“access to investors” as a primary benet o the program, industry eedback suggested that an appropriate

study o the accelerator landscape should also ocus on investors’ engagement with accelerators. Wesurveyed 60 impact investors on dierent variables surrounding their relationship with accelerators.

Ater signicant ollow-up via e-mail and phone rom December 2012-February 2013, we closed the surveysin mid-February 2013, with a nal response rate o 33% (65 out o 197 accelerators). Additionally, wereceived a 60% response rate or the investor survey (36 out o 60 investors surveyed).

We dropped 7 incomplete responses due to insucient data, leaving us with 58 complete responses.However, only 6 accelerator respondents identied themselves as having “no impact objectives beyondnancial returns”, which was not a sucient sample or a reasonable comparison between impact-ocusedand non-impact ocused accelerators. We dropped these 6 observations, and have ocused on examining the52 social impact-ocused accelerators in this study.

In our ndings, we provide descriptive statistics on key aspects o accelerator characteristics andperormance, and also conduct some preliminary analysis o the actors that may contribute to betterperormance. We used t-tests to compare accelerators’ perormance in dierent categories related toorganizational structure and unding, selection, services, and networks. Given the relatively small samplesize, and the act that all the data are sel-reported, we are cautious about making strong inerences at thisstage.

However, we suggest that these ndings will be helpul in pointing the way or urther, more rigorousanalysis o incubator and accelerator perormance. We are currently developing a more extensive analysison this topic by building a longitudinal dataset o social enterprises—both accelerator and non-acceleratorgraduates—to nd relationships between accelerator interventions and enterprise perormance, as well as

an evaluative ramework to assess accelerator perormance.

7/27/2019 Bridging the Pioneer Gap The Role of Accelerators in Launching High Impact Enterprises .pdf

http://slidepdf.com/reader/full/bridging-the-pioneer-gap-the-role-of-accelerators-in-launching-high-impact 10/33

IV. The Landscape of Impact-FocusedAccelerators

a. Geographic Scope

O the 52 accelerators surveyed, 27% are open to enterprises across the globe (e.g. the Unreasonable

Institute and the Global Social Benet Incubator are open to ventures worldwide) ; 31% operate are open to ventures rom specic regions (e.g., GrowthArica is open to ventures rom East Arica; Agora Partnershipsis open to ventures across Central America and Mexico), 35% operate nationally (e.g. Artemisia is open to ventures in Brazil; New Ventures-Mexico is pan-Mexico), and 8% operate in specic cities (e.g. the SEHubocuses on Singapore-based ventures). The majority o accelerator operations in this study are Arica-ocused.

8%

35%

31%

27%

0% 5% 10% 15% 20% 25% 30% 35% 40%

City

National

Regional

Global

Figure 1: Geographic Scope

n=52

0%

4%

6%

8%

23%

25%

30%

30%

42%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45%

Caribbean

Oceania

Middle East

Central America/Mexico

North America

South America

Europe

Asia

Africa

Figure 2: Geographic Focus

n=52

7/27/2019 Bridging the Pioneer Gap The Role of Accelerators in Launching High Impact Enterprises .pdf

http://slidepdf.com/reader/full/bridging-the-pioneer-gap-the-role-of-accelerators-in-launching-high-impact 11/338

b. Organizational Structure

As a baseline analysis o accelerators, we rst analyzed organizations’ ounding, structure,and sources o unding. As mentioned beore, accelerators are relatively new—72% were ounded in the last ve years, though the oldest in our sample was ounded in1996. Perhaps counter-intuitively, impact-ocused accelerators seem more ocused ondeveloping revenue streams beyond philanthropic support than traditional businessaccelerators: while research on incubators and accelerators in traditional businesssectors suggest that the majority are structured as non-prots15, interestingly, 38% o theaccelerators in our sample are set up as or-prots, 44% as nonprots, and 17% as hybrids.

c. Funding Sources

Accelerators appear to have sucient resources to operate—but are by no means sel-sustaining. In act, 57% o the respondents stated their nancial condition as “operating smoothly”, while 16% report operating with a surplus. Only about a quarter o therespondents said they were “strapped or cash”.1 Accelerators’ current sources o revenueinclude, in order (with detail on each below): (1) Philanthropic capital; (2) Program Fees(3) Consulting Contracts; (4) Return rom Successul Investment; and (5) Investment Closing Fees.

PhilanthropicCapital, 53.5%

Consultingcontracts, 13%

Entrepreneurfees, 17%

Return fromsuccessful

investments,8%

InvestmentClosing Fees,

7%

Figure 3: Accelerator Budgets by Funding Source

n=50

PhilanthropyEven though almost two-thirds o the accelerators we surveyed report being struc-tured as or-prots or hybrids, 74% o all accelerators rely on philanthropic support or their operations, and 54% o the total amount o capital currently used by accel-erators is rom philanthropic sources. This nding suggests that while many ac-

celerators expect to develop revenue streams in the uture, the majority o them arealso likely to rely on grants to support some portion o operations or the oreseeableuture.

Entrepreneur fees About one-third o the accelerators surveyed charge participants ees, while an addi-tional 17% plan to have ees in the uture. On average, accelerators charge $1,300 perenterprise, ranging rom $120 to $5,000 (excluding 3 outliers that charge $10,000 ormore).

1 We received 37 responses or this question (71% o the sample).

Human Capital

With the growing awarenessf accelerators’ valuable role impact investment, these

rganizations are attractinggnicant human capital and

esources to their operations.n average, accelerators

mploy about 11 staff members8 full-time and 3 part-timemployees).* Older acceleratorshose that were foundedefore 2008), are considerablyarger, with an average of 27mployees, compared to youngerccelerators (that have aboutemployees), suggesting thatccelerators have the potentialo scale. As newer acceleratorsecome more established andtrengthen their operations,

e expect them to develop theesources to attract and retaintrong talent.

We excluded a large accelerator

with 280 employees for this estimate.

included, accelerators in the

ample would have an average of 17

mployees.

7/27/2019 Bridging the Pioneer Gap The Role of Accelerators in Launching High Impact Enterprises .pdf

http://slidepdf.com/reader/full/bridging-the-pioneer-gap-the-role-of-accelerators-in-launching-high-impact 12/339

Consulting contractsThe second-highest source o accelerator budget is revenue rom consulting contracts. Accelerators have a unique position o high exposure to a large volume o enterprises, and are able to monetize theirexpertise in two ways: (a) research on knowledge and insights gained rom enterprise exposure, and(b) direct business development assistance provided to entrepreneur graduates.

Returns from InvestmentReturns rom investments represent a small overall percentage o revenue (8.2%), though nearly hal the accelerators surveyed report taking some equity in the enterprises that go through their programs.

This is airly unsurprising given that the sample o accelerators is relatively young, and liquidity eventsrom impact investments are rare, and can take several years to materialize.

“Success Fees” From Investment98% o accelerators promote access to investors as a valuable service o the program, and many mon-etize this service through charging “success ees” or investments brokered. While this remains thelowest budget line-item o all accelerator budgets, nearly 7.5% o all accelerator budgets are unded by

success ees.

7/27/2019 Bridging the Pioneer Gap The Role of Accelerators in Launching High Impact Enterprises .pdf

http://slidepdf.com/reader/full/bridging-the-pioneer-gap-the-role-of-accelerators-in-launching-high-impact 13/331

V. Enterprise Pipeline and Selectiona. Sector and Impact Objectives

20% o accelerators ocus on entrepreneurs rom one particular sector, 40% work with entrepreneurs romseveral specic sectors, and 40% o accelerators are not sector-specic. As certain sectors continue to grow, we expect to see more specialization among accelerators.

We ocused our study specically on incubators and accelerators that claim to have at least one impact objective beyond nancial returns. Based on our sample, the types o impact objectives can be broadly categorized under two categories: “Employment” and “Products and Services or the Underserved”. Themajority o accelerators surveyed (56%) ocus on employment generation and income and productivity growth (46%), aiming to stimulate socio-economic development by supporting SGBs. However, asignicant proportion also ocuses on supporting enterprises working in health (35%), clean energy (35%),and agriculture (33%). This nding is consistent with previous data that suggest these three sectors are thelargest and astest growing in impact investing (ANDE, 2012).

0%

6%

6%

8%

13%

19%21%

25%

25%

25%

29%

33%

33%

35%

35%

46%

56%

0% 10% 20% 30% 40% 50% 60%

No Impact Objectives

Conflict Resolution

Generate Funds for Charitable Giving

Disease-Specific Prevention & Mitigation

Affordable Housing

Food SecurityAll Impact Objectives

Clean Water

Capacity-Building

Equality & Empowerment

Financial Services

Community Development

Agricultural Productivity

Clean Energy

Health Improvement

Income/Productivity Growth

Employment Generation

Figure 4: Impact Objectives

n=52

b. Enterprise Stage of Development

The accelerators surveyed work with enterprises in a range o developmental stages, ranging rom theidea stage to the growth stage (Figure 5). To ocus on specic areas where accelerators have intervenedin ventures, we clearly dened our areas o enterprise development and identied the percentage o accelerators that sel-reported working with ventures in each stage (some accelerators reported multiplestages):

• Ideastage (40% o accelerators): The proverbial “idea on paper”; ventures at this stage do not yet have a working prototype, good/service/product, or customer.

• Prototypestage(75% o accelerators): the most common stage or accelerators, “prototype stage”is a phase where accelerators have a working “minimum viable” model o their good or service, but do not yet have revenue.

7/27/2019 Bridging the Pioneer Gap The Role of Accelerators in Launching High Impact Enterprises .pdf

http://slidepdf.com/reader/full/bridging-the-pioneer-gap-the-role-of-accelerators-in-launching-high-impact 14/331

• Post-revenuestage (65% o accelerators): Ventures have customers and typically unctioning revenue models; however, their business model is not yet at scale, and they are not yet cash-fow positive, and they typically have not raised signicant nancing outside “riends and amily.”

• Growthstage(23% o accelerators): Ventures are operating business models at scale; they typically are cash/fow positive and/or have raised signicant outside venture nancing.

O particular note is a less-clear distinction between incubators and accelerators in the social enterprisespace than in traditional business sectors, where these roles are more clearly dened. Social-enterpriseocused accelerators tend to work across a airly wide spectrum o enterprise development stages, perhaps

refecting the relatively limited pipeline o rms.

Figure 5: Enterprise Development Stages

Idea StagePrototype

Stage

Post-Revenue

Stage

GrowthStage

Figure 6: Enterprise Stage of Development

23%

65%

75%

40%

0% 10% 20% 30% 40% 50% 60% 70% 80%

Growth Stage

Post-Revenue Stage

Prototype Stage

Idea Stage

n=52

c. Enterprise Recruitment and Selection

The 52 surveyed accelerators have worked with a total o 20,216 entrepreneurs in their history. Acceleratorsdevote a signicant amount o resources upront to the recruitment and selection process. While 7% o accelerators spend less than a month on recruitment activities, 33% spend between three months and one year on recruitment. Most commonly, 60% o the accelerators surveyed spend between one and three months

recruiting each new cohort.

Accelerators recruit entrepreneurs through a host o dierent channels. The most common sources cited by accelerators include:

1) Reerrals rom entrepreneurs aliated with the accelerator,

2) Impact investors (individuals and investment unds),

3) Commercial investors (individuals and investment unds that do not sel-identiy as impact

investors,4) Entrepreneurial associations (ellowships, scholarships) in the social impact space,

5) Entrepreneurial associations that do not identiy with social entrepreneurship or impact investing,

6) Universities,

7) Industry associations ocused on specic sectors,

8) Sector-specic conerences (e.g., agriculture, education),

9) Social entrepreneurship or impact investing conerences,

10) Inbound requests rom program marketing eorts and social media,

11) Outbound direct, “cold-call” recruitment (e.g., nding and contacting entrepreneurs on the web,Facebook, LinkedIn)

7/27/2019 Bridging the Pioneer Gap The Role of Accelerators in Launching High Impact Enterprises .pdf

http://slidepdf.com/reader/full/bridging-the-pioneer-gap-the-role-of-accelerators-in-launching-high-impact 15/331

But not all sources are equally helpul. In order, accelerators ranked the ollowing sources as most helpul:

1) Reerrals rom entrepreneurs aliated with the accelerator (“helpul” by over 50% o theorganizations surveyed)

2) Inbound requests rom program marketing eorts (30%);

3) Reerrals rom entrepreneurial associations (19%);

4) Reerrals rom upstream impact investors (15%).

Interestingly, social entrepreneurship and impact investing conerences were listed as the least helpul.This nding is somewhat surprising, considering the prevalence o conerences in the sector that promotethemselves as a means o identiying entrepreneurs. However, it may also be the case that social enterpriseconerences typically eature more successul and mature enterprises, making them a less useul source o early stage companies that might apply to participate in accelerators.

Based on our sample, accelerators in the impact investment sector appear to be less competitive interms o selection—with an average acceptance rate o almost 21%--than accelerators in the traditional business sector, which accept about 5% o applicants.16 The exact reasons or the lack o selectivity areunclear, though it is possible that there is simply a much smaller pipeline o socially oriented enterprises. Additionally, it is possible that, due to the high percentage o accelerators earning revenue romentrepreneur ees, investment returns, and success ees, accelerator managers may admit enterprisesmore readily in order to bring in more revenue. Philanthropic support may also be linked to the numbero entrepreneurs supported, which would also encourage accelerators to accept a greater percentage o applicants. But selectivity matters: in Section IV we compare accelerators that accept 10% or ewer o theirapplicants, to less selective accelerators, on the basis o key perormance characteristics.

Technology and “Invention-Based” Enterprises

While accelerators do not necessarily need to be focused on technology/invention, we studied thedegree to which accelerators were actively focused on “invention-based enterprises” (which wedene as enterprises that have a core technology that was invented/created by the founding team,who owns or seeks to own core intellectual property on the invention).

25% of accelerators surveyed focus exclusively on working with enterprises that have technologyand/or an invention at the center of their enterprises, while another 41% have an active focus ontechnology (but still work with non-technology or invention-focused entrepreneurs). Only 31% haveno active focus on tech innovations, and only one accelerator had no technology-based companiesin its program.

2%

26%

31%

41%

No technology-based companies inprograms

No active focus on technologyinnovations

100% focused on technology innovations(do not work with non-tech companies)

Active focus on technology, but still workwith entrepreneurs without tech

innovations

0% 5% 10% 15% 20% 25% 30% 35% 40% 45%

Figure 7: Focus on Technology and Innovation

n=51

7/27/2019 Bridging the Pioneer Gap The Role of Accelerators in Launching High Impact Enterprises .pdf

http://slidepdf.com/reader/full/bridging-the-pioneer-gap-the-role-of-accelerators-in-launching-high-impact 16/331

VI. Services and Benetsa. Program Duration & Frequency

The average duration o surveyed accelerator programs is six months.2 The requency o meetings during this time period varies widely, ranging rom every day (26%) to once a month (14%), with many dierent meeting requencies in between (Figure 8).

Every day,23%

More than twotimes perweek, 17%

Twice a week,11%

Once a week,15%

More thantwice a month,

13%

Twice amonth, 6%

Once a month,15%

Figure 8: Frequency of Program Sessions

n=47

b. Program Services & Benefts

83% o accelerators describe their support approach as “high-touch”. In this case, social impact-ocusedaccelerators appear to be similar to the majority o incubators and accelerators in traditional businesssectors that provide “high-touch”, highly tailored services to a small group o enterprises.

Almost all surveyed programs provide the ollowing benets: mentorship rom experts (100%), accessto potential investors (98%), network o partners and customers (97%), and business skills development (97%). The majority o programs provide direct unding (54%), while a minority provides technology training and assistance (33%).

2 We excluded two outliers that have 60- and 84-month engagement periods. I we include those organizations, the averageduration would be over nine months.

33%

54%

97%

97%

98%

100%

0% 20% 40% 60% 80% 100%

Technology Assistance

Direct Funding

Business SkillsDevelopment

Network of Partners &Customers

Access to PotentialInvestors

Mentorship from Experts

Figure 9: Accelerator Services and Benefits

n=52

7/27/2019 Bridging the Pioneer Gap The Role of Accelerators in Launching High Impact Enterprises .pdf

http://slidepdf.com/reader/full/bridging-the-pioneer-gap-the-role-of-accelerators-in-launching-high-impact 17/331

Other sel-identied benets o accelerators include: media exposure, brand recognition, access to aco-working space, reerrals to vetted talent and human capital, exposure to relevant and timely R&D,and membership in an extensive alumni network consisting o other like-minded entrepreneurs, serviceproviders, and investors.

However, the existing literature reinorces that just because a service is provided, it does not necessarily mean that the service is o high-quality. We expect to dive deeper into this issue through the next phaseo our research strategy by collecting enterprise-level data rom ventures who have participated inaccelerators, and comparable enterprises that have not received accelerator support.

c. Post-Program Support

The majority o accelerators (66%) oer post-program support to all o their graduates at no cost. 28%percent o accelerators provide post-program services or ree on a case-to-case basis, while 4% provideservices on a case-to-case basis or a ee. (2% do not provide post-program support at all due to a lack o bandwidth or resources.)

O the accelerators that do provide post-program services to their entrepreneurs, 21% o accelerators oerservices between one and six months ater an entrepreneur graduates rom their program, and 9% oersupport between six to eight months. The majority (70%) oer services beyond nine months, and may

extend as long as the entrepreneurs’ ventures exist.

The types o post-program services oered to entrepreneurs include: public relations opportunities,connections with investors, board participation, HR/recruitment support, regional meet-ups, alumninetworking, and online communities listing unding and promotion opportunities).

7/27/2019 Bridging the Pioneer Gap The Role of Accelerators in Launching High Impact Enterprises .pdf

http://slidepdf.com/reader/full/bridging-the-pioneer-gap-the-role-of-accelerators-in-launching-high-impact 18/33

7/27/2019 Bridging the Pioneer Gap The Role of Accelerators in Launching High Impact Enterprises .pdf

http://slidepdf.com/reader/full/bridging-the-pioneer-gap-the-role-of-accelerators-in-launching-high-impact 19/331

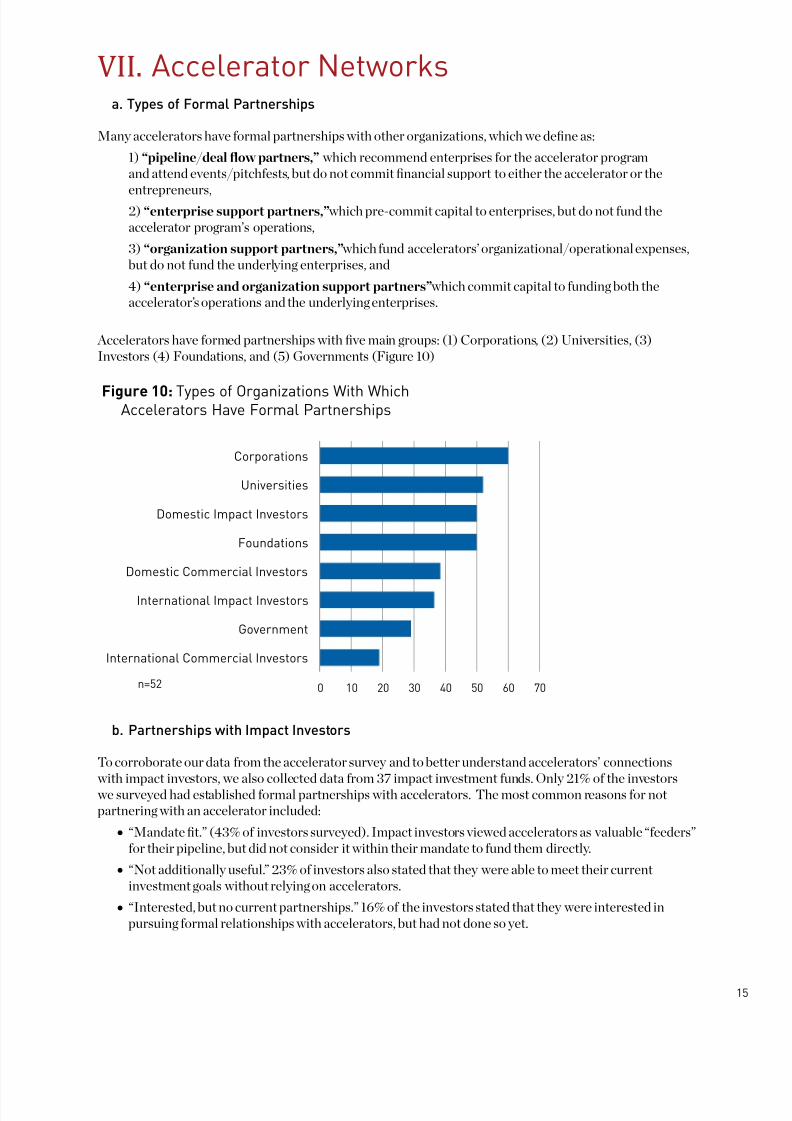

FormalPartnership

21%

No FormalPartnership

79%

Figure 11: Impact Investors that have a FormalPartnership with an Accelerator

n=37

Despite the lack o ormal partnerships and unding rom impact investors, 60% o theinvestors in our sample did report having inormal partnerships with accelerators. Wedene an inormal partnership as one in which an investor “regularly communicates

with accelerator sta, attends events, or stays otherwise inormed, with a primary goal o obtaining deal fow, but does not und the accelerator directly.”

The range o accelerator/investor engagement is wide across the board. Some acceleratorsare in sync with impact investors: 32% o investors report that up to 20% o theirportolio was sourced rom accelerators. Yet a plurality o impact investors do not rely onaccelerators or “deal fow”- 47% o investors report that 0% o their current portolio wassourced rom accelerators.

Investors withInformal

Partnershipswith

Accelerators60%

Investors withno Informal

Partnershipswith

Accelerators40%

Figure 12: Impact Investors with InformalPartnerships with Accelerators

n=34

Our ndings underscore the critical need or philanthropic support or acceleratorsin the near term, but also raise important questions about aligning the services that accelerators provide with the needs o impact investors. Many impact investors do not lookto accelerators or deal fow, and the majority do not contribute to accelerators’ budgets inany ormalized and consistent way. We suggest that accelerators need to more accurately calculate the specic value that they add or investors in terms o lower searching and duediligence costs, and design their pipeline and curriculum in collaboration with experiencedinvestors. ANDE is pursuing additional research on developing a ramework to analyze the value created by accelerators (described in Section X).

o-Working Spaces

any accelerators’ work isade nancially viable due toerating out of free or affordable-working spaces. In fact,% of accelerators surveyedaintain a formal partnershipth a university, organization,co-working space (e.g. the

ub) to lessen the cost of theirerations.

7/27/2019 Bridging the Pioneer Gap The Role of Accelerators in Launching High Impact Enterprises .pdf

http://slidepdf.com/reader/full/bridging-the-pioneer-gap-the-role-of-accelerators-in-launching-high-impact 20/331

VIII. Metrics & EvaluationBased on our analysis, metrics and evaluation is a key target area or improvement or impact-ocused accelerators. Most notably, a signicant proportion o organizations that we surveyeddo not track nancial or social perormance data on an ongoing basis, making it dicult to assessperormance and establish benchmarks or the sector.

a. Financial and Social Performance Data Collection

We asked accelerators to report on the status o their graduate enterprises. While the majority o accelerators (96%) never collect nancial data rom enterprises, 23% do not track the status o their graduate enterprises, which makes it dicult to evaluate their perormance. We noticed theollowing gaps in accelerator data analysis:

• Lackofanydatacollection:O the accelerators we surveyed, 4% do not collect any nancial perormance data rom their enterprises, while 20% do not collect any social orenvironmental perormance data (Figure 13 & 14). We nd this discrepancy surprising,given the impact-oriented ocus o these accelerators. Potential interventions to improvethe impact-oriented data collection with accelerators could be support or the introduction

o standardized reporting rameworks (such as IRIS and GIIRS) also used by investors andcapital providers in the sector.

• Datatrackingventureperformanceovertime: Additionally, 14% o the respondentsonly collect nancial data at a single point in time (e.g. at the beginning or end o theirprogram), and 15% only collect social and environmental data (n = 48) at a single point (Figure 15). This makes it dicult to assess whether there is any change in the social ornancial perormance o the enterprises that go through these programs.

• Accelerator-drivendatacollectionmandates.Finally, 28% o respondents considerreporting by their program participants to be “optional”3. The majority o the acceleratorsthat do require reporting expect enterprises to provide data or at least one year ater theend o their programs, and about one-third require reporting as long as the enterprise is inoperation.

• Datacollectionmethodologies.The primary method o collecting data also varies widely, with 64% o accelerators collecting data through in-person interviews or during site visits,52% via phone, and 50% via email or online mechanisms. The variety o methods used indata collection also aects how reliable and unbiased the data are.

3 43 accelerators responded to this question (83%).

7/27/2019 Bridging the Pioneer Gap The Role of Accelerators in Launching High Impact Enterprises .pdf

http://slidepdf.com/reader/full/bridging-the-pioneer-gap-the-role-of-accelerators-in-launching-high-impact 21/331

b. Accelerator Graduate Performance

About 77% o the accelerators in our sample track the status o their graduate enterprises, though theirdata collection methodologies are varied and incomplete. We analyzed the perormance o venturesthat graduated rom the accelerators that do collect data (n=40). 31% o the enterprises are reported to be protable and/or have received major investment, another 46% are still in operation but are not yet protable and/or have not yet received major investment, and about 10% o the enterprises are no longeroperating. There is no data available on 13% o the enterprises, even or the accelerators that do track theirenterprises.

Never (with noplans to)

2%

Never (butplan to in the

future)2%

Only once(e.g., at theend of our

acceleratorprogram)

14%Annually

37%

Quarterly33%

Monthly12%

Figure 13: Financial Performance Data CollectionFrequency

n=49

Never (with noplans to)

18%

Never (butplan to in the

future)

10%Only once

(e.g., at theend of our

acceleratorprogram)

15%

Annually27%

Quarterly

18%

Monthly12%

Figure 14: Frequency of Social & EnvironmentalPerformance Data Collection

n=48

As long asenterprise

staysoperational

33%

2-5 years23%

Over 1 year(but lessthan 2)

12%

7-12 months2%

1-6 months2%

Reporting isoptional28%

Figure 15: Data Reporting Period

n=49

7/27/2019 Bridging the Pioneer Gap The Role of Accelerators in Launching High Impact Enterprises .pdf

http://slidepdf.com/reader/full/bridging-the-pioneer-gap-the-role-of-accelerators-in-launching-high-impact 22/331

IX. Measuring Accelerator Performance:First Steps

Based on research on incubators and accelerators in developed markets, we analyzed among the samplesize o this study 4 key actors that typically aect accelerator success: OrganizationalFundingSources,Selectivity,Services,andNetworks. Additionally, we also analyzed the variable o AcceleratorYearsinOperation to compare older accelerators (those that have been in operation or over 5 years) to younger

accelerators. We used the ollowing two (sel-reported) variables as measures o accelerator success,consistent with the literature on incubators and accelerators17. We conducted independent sample t-tests tocompare average perormance measures across dierent categories or these actors.4

• EnterpriseSuccessRate:Percentage o graduate enterprises operating at a protable level, and/or having raised major investment ($500,000 or more)

• EnterpriseSurvivalRate:Percentage o graduate enterprises that “are operating at a protablelevel, and/or have raised major investment ($500,000 or more) OR “Are still operating, but are not yet protable and/or have not yet raised necessary investment” (i.e., inclusive o previous category)

Accelerator Years in Operation While there are many accelerator characteristics that can infuence their perormance, on average, we

hypothesized that older, more established accelerators would perorm better, given their experience andtrack record. As mentioned previously, 72% o accelerators are relatively young (under 5 years old). Theresearch seems to suggest some validity to our hypothesis: older accelerators do perorm better in termso their enterprise success rates, with an average o 46%, compared to only 25% or younger accelerators,a dierence that is statistically signicant at the 5% level. However, we do not observe any statistically signicant dierences in terms o survival rates, with older accelerators achieving an 80% survival rate,compared to a 76% survival rate or younger programs. A more thorough study would investigate whetherthe discrepancy in results is due to graduates o older accelerators having more time to develop successul business models—the enterprise-level study we are proposing as a ollow-up to this initial study can morethoroughly investigate this hypothesis.

Table 1: Comparing Accelerators by Age

Accelerators foundedbefore 2008 (n = 11)

Accelerators foundedafter 2008 (n = 29)

Avg. Enterprise Success Rate 46% 25%

Avg. Enterprise Survival Rate 80% 76%

Organizational Funding SourcesIn our sample, we ound that about two-thirds o respondents relied primarily on grants or their operations(dened as over 50% o annual revenue). However, we did not nd any signicant dierences in this study in the enterprise success rate or the enterprise survival rate. On average, grant reliant accelerators had anaverage enterprise success rate o 29%, and a survival rate o 74%, while those that were not, had a success

rate o 35%, and a success rate o 82%.

Table 2: Comparing Organizational Funding Sources

Majority PhilanthropicSupport (n = 27)

Majority Non-Philan-thropic Support (n = 13)

Avg. Enterprise Success Rate 29% 35%

Avg. Enterprise Survival Rate 74% 82%

4 The Independent Sample t-test is used to compare averages or two groups o cases (e.g. or-prot/non-prot), to see i any dierences are statistically signicant. A result may be signicant at the 10%, 5% or 1% level, which means that you are 90%,95%, or 99% sure o a dierence between the means in this sample, respectively. We provide sample means or various catego-ries, along with sample sizes in parentheses.

7/27/2019 Bridging the Pioneer Gap The Role of Accelerators in Launching High Impact Enterprises .pdf

http://slidepdf.com/reader/full/bridging-the-pioneer-gap-the-role-of-accelerators-in-launching-high-impact 23/332

Selectivity We ound that, consistent with general theory on incubators, selectivity is a key characteristic o successulincubators/accelerators in the social-enterprise sector. In traditional incubator literature, a 5% acceptancerate is considered a characteristic o a good program. Incubators in the social enterprise space are stillrelatively new, so we dened accelerators that accept 10% or ewer o their applicants as “Selective”, and therest as “Non-selective”.

We were only able to gather data points rom 34 accelerators or this part o the analysis, so it is dicult to draw denitive inerences at this stage. However, in conducting t-tests across selective and non-

selective accelerators, we ound that selective accelerators do appear to perorm better, with an averageenterprise success rate o 39% and an average enterprise survival rate o 91%. In comparison, non-selectiveaccelerators have an average enterprise success rate o 24% and a survival rate o 69%. The dierencesare weakly signicant (at the 10%) level. However, we believe more research is needed to understand why social enterprise incubators in general are not as selective, and the extent to which selectivity actors intoaccelerator perormance. By encouraging more accelerators to collect data rom their graduate enterprises,as well as developing a longitudinal dataset o enterprises, we hope to examine this issue in more detail.

Table 3: Comparing Selective and Non-Selective Accelerators

Selective (n = 21) Non-Selective (n = 13)

Avg. Enterprise Success Rate 39% 23%

Avg. Enterprise Survival Rate 91% 69%

Services We received data rom 52 accelerators globally. We ound that the majority o accelerators provided thesame core services: (1) Business skills training, (2) Mentoring, (3) Network o partners/customers, and (4) Access to potential investors. The only area o dierentiation was whether or not an accelerator provideddirect unding to its enterprises as part o its program.

39 accelerators responded to the question on provision o direct unding. Surprisingly, we ound that accelerators that do not provide direct unding appear to have higher enterprise survival rates, though theresults were not statistically signicant. On average, accelerators that did not provide any direct unding hadenterprise survival rates o 84%, compared to those that did (71%).

Table 4: Comparing Accelerators that Provide Direct Funding to those that do not

No Direct Funding(n = 17)

Direct Funding (n = 22)

Avg. Enterprise Survival Rate 84% 71%

Networks and Partnerships As discussed previously, accelerators partner with a wide range o organizations, including investors (bothcommercial and impact-ocused), oundations, universities, corporations, and governments. We ound no

apparent dierences between accelerators that partnered with the ollowing types o organizations, andthose that did not:

• International Impact Investors

• Domestic Impact Investors

• International Commercial Investors

• Foundations

• Universities

• Governments

7/27/2019 Bridging the Pioneer Gap The Role of Accelerators in Launching High Impact Enterprises .pdf

http://slidepdf.com/reader/full/bridging-the-pioneer-gap-the-role-of-accelerators-in-launching-high-impact 24/332

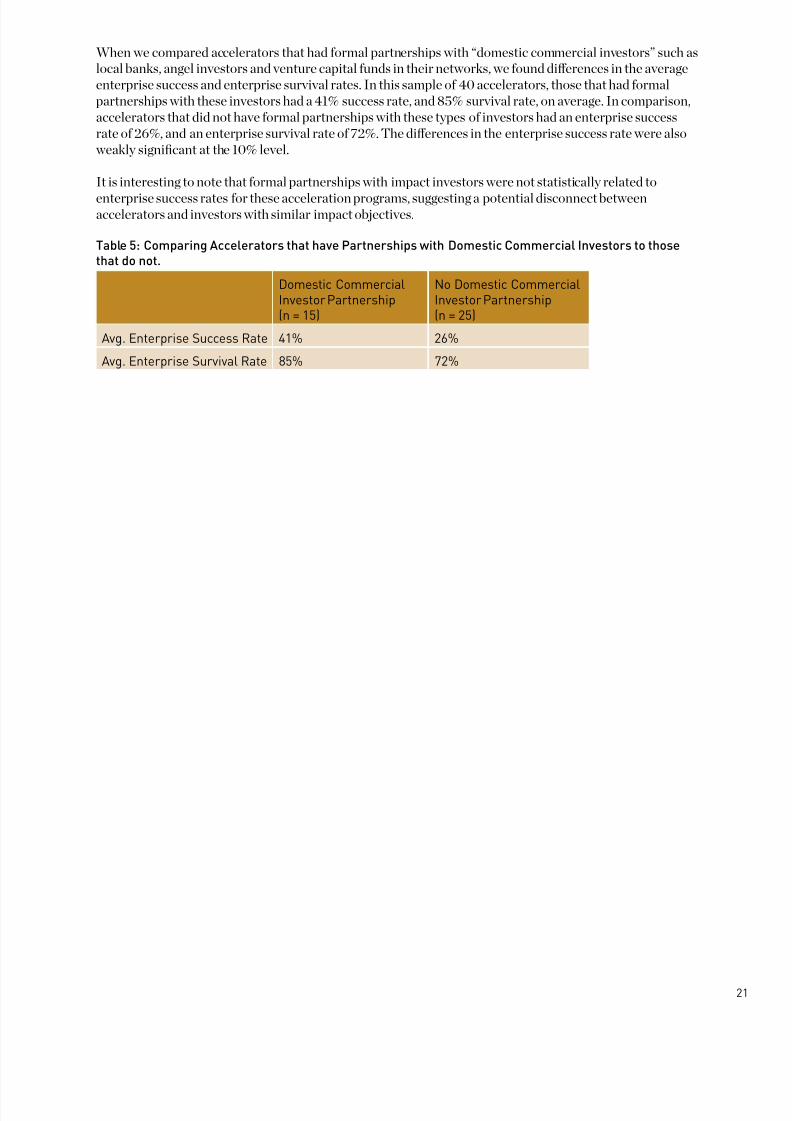

When we compared accelerators that had ormal partnerships with “domestic commercial investors” such aslocal banks, angel investors and venture capital unds in their networks, we ound dierences in the averageenterprise success and enterprise survival rates. In this sample o 40 accelerators, those that had ormalpartnerships with these investors had a 41% success rate, and 85% survival rate, on average. In comparison,accelerators that did not have ormal partnerships with these types o investors had an enterprise successrate o 26%, and an enterprise survival rate o 72%. The dierences in the enterprise success rate were also weakly signicant at the 10% level.

It is interesting to note that ormal partnerships with impact investors were not statistically related to

enterprise success rates or these acceleration programs, suggesting a potential disconnect betweenaccelerators and investors with similar impact objectives.

Table 5: Comparing Accelerators that have Partnerships with Domestic Commercial Investors to thosethat do not.

Domestic CommercialInvestor Partnership(n = 15)

No Domestic CommercialInvestor Partnership(n = 25)

Avg. Enterprise Success Rate 41% 26%

Avg. Enterprise Survival Rate 85% 72%

7/27/2019 Bridging the Pioneer Gap The Role of Accelerators in Launching High Impact Enterprises .pdf

http://slidepdf.com/reader/full/bridging-the-pioneer-gap-the-role-of-accelerators-in-launching-high-impact 25/332

X. Conclusions and Next StepsThe number o incubators and accelerators providing tailored support to social enterprises continues togrow. In many countries, these incubators and accelerators are the rst entry point or social enterprises intoa broader ecosystem and impact investing community that can help them grow at a key stage o development,creating the opportunity or organizations to play a critical role in bridging the “pioneer gap.”

This study identied several key variables that are related to the success and ailure o accelerators, as well

as several key gaps that may be holding back accelerator success. We have outlined key ndings below, anddeveloped recommendations in light o these ndings.

Partnership with in-country commercial investors matter

For many impact accelerator graduates, the next step in nancing may not be impact investors (in an Emory- Village Capital study in 2012, ewer than 10 impact investors made investments o less than $250,000per enterprise). However, traditional commercial investors—banks, angel networks, and strategically aligned corporations who nd a particular interest in the impact objective o the accelerator. The ormo partnership that generated the greatest dierence between enterprise success rates was the “domesticcommercial investor”: local investors who were able to provide unding to ventures, but did not necessarily sel-identiy as “impact investors.”

Two relevant an examples: Nigeria’s Wennovation Hub, which has partnered with Google-Arica in agoal to enable all ventures to use Google products to build their businesses, and Nairobi’s m:Lab, which has partnered with Nokia and Samsung to help mobile-based entrepreneurs addressing the poor developproducts. In our own experience, Village Capital is launching a program with the Pearson AordableLearning Fund in India to source, accelerate, and invest in education interventions that support the base-o-the-pyramid.

Selectivity matters

It stands to reason that the accelerators that select the best ventures are likely to have the best results. Thecollected research on traditional business accelerators suggests that programs with a lower acceptance

rate and more rigorous selection process had a higher degree o success in graduate ventures. Acceleratorscast a wide net in recruiting ventures, knowing that most startups ail. Our research is consistent with the broader literature on the topic, and shows that impact accelerators with a lower percent acceptance rate have a higher proportion o successul graduates. This nding provides two actionable steps or accelerators:(1) over-resource recruiting, so accelerators are not required, or business model reasons, to accept sub-standard ventures; (2) ocus on the quality, not the quantity o entrepreneurs served, and develop rigorousselection processes.

Further research would explore the cumulative impact o more selective accelerators, as some acceleratorprograms operate a “high-volume, light-touch” model that, they believe, may lead to less selective cohorts, a higher ailure rate, but more ultimate impact per dollar invested due to a high volume o graduate ventures.

Philanthropy is currently necessary for accelerators to survive (and is not statistically related toenterprise success).

Three out o our accelerators rely on philanthropy to survive, and 54% o all accelerator budgets are undedthrough grants. This nding suggests the ollowing: (1) impact accelerator business models are not yet proven to the degree where they can develop sustainable revenue streams, and accelerators currently requiregrants to ll the gaps they are seeking to address; and (2) most accelerators are providing resource leverageon philanthropy, complementing grants with sources o earned-revenue. We believe that philanthropy willplay a critical role in supporting impact-ocused accelerators in the immediate uture. However, donors canalso encourage accelerators to explore new revenue streams that will allow them to become less reliant ongrants, but not compromise their social mission.

7/27/2019 Bridging the Pioneer Gap The Role of Accelerators in Launching High Impact Enterprises .pdf

http://slidepdf.com/reader/full/bridging-the-pioneer-gap-the-role-of-accelerators-in-launching-high-impact 26/332

Most impact investors are looking to accelerators for investment opportunities, but are not

fnding them.

While 60% o impact investors say they have an inormal sourcing partnership with accelerators, 47%say they have sourced “zero” portolio companies directly rom an accelerator. This disconnect refects amore undamental challenge that accelerators ace, balancing the business development needs o socialentrepreneurs on the one hand, while also trying to meet the specic criteria o impact investors. Investorscite “lack o t with our investment criteria” as a primary reason why they do not invest in acceleratorgraduates, suggesting that accelerators could do a better job proactively engaging with investors in theselection process to develop cohorts that are more ready or ollow-on investment.

Accelerators might face a “free rider” problem.

At the same time, while the majority o impact investors look to accelerators as a sourcing mechanism,only 20% help accelerators und their operations. The primary reason or non-involvement is “MandateFit”—investors do not view it as their role in the ecosystem to support accelerators. In the long run, as cash-strapped accelerator programs try to und their operations, they may see a “ree-rider problem” that causesmis-alignment between accelerators and investors. Accelerators, investors and donors need to nd a unding model that covers the cost o quality business acceleration or entrepreneurs, maintains the impact ocus,and also generates a reasonable value proposition or all parties.

We have very little systematic data on how accelerators are performing—and manyaccelerators themselves are not even collecting data.

These ndings are rom a sample o 52 accelerators worldwide; however, we need much more data onincubator and accelerator eectiveness to assess the quality o services provided as well as the importanceo selection and networks. While relatively small or statistical analysis, our sample accelerators is relatively large given the stage and size o the impact investing sector so ar. We believe that that expanding this dataset will allow more rened, multivariate analysis o key accelerator success actors. We suggest as ollow-ups:

• In order to better assess accelerator perormance, we need more and better longitudinal data on theenterprises that receive support, as well as the enterprises that apply, but do not receive support. Village Capital and ANDE are currently working with Social Enterprise at Goizueta (Emory University) to develop a longitudinal database o enterprise perormance, in collaboration withseveral key partners. This project will address the ollowing:

o How do entrepreneurs that participate in accelerator programs perorm dierently thanothers?

o Are there dierences in measurable impact between general/global accelerator programsand those that ocus on specic sectors or regions?

o What specic program design choices (related to participant selection, services providedand network development) are associated with more positive accelerator impacts?

Over the longer term, this database will allow more longitudinal analysis o how various interventions canaect social enterprises at dierent stages o their development.

In addition, the majority o accelerators that did not collect data cited a lack o time/resources or datacollection. Most accelerators are start-ups themselves, and we recommend that philanthropists or investors who support accelerators also provide support or data collection/assessment.

Finally, ANDE is also collaborating with I-Dev International to develop a common ramework to quantiy the value created by incubators and accelerators or investors and enterprises. I-Dev is evaluating and benchmarking 6-8 impact incubators and accelerators, identied through the ANDE-Village Capital survey,and using this ramework to compare the perormance o “accelerated” vs. “un-accelerated” SGBs that havereceived investment. Through this analysis, we hope to quantiy the monetary value created or SGBs as well as investors by comparing costs associated with deal sourcing, due diligence, investment cycle, advisory services, and probability o exits.

7/27/2019 Bridging the Pioneer Gap The Role of Accelerators in Launching High Impact Enterprises .pdf

http://slidepdf.com/reader/full/bridging-the-pioneer-gap-the-role-of-accelerators-in-launching-high-impact 27/332

We believe this broad, multi-pronged initiative will provide signicant value or the enterprises, incubators,and unders that support accelerator services. Our work will provide answers to critical questions that will allow entrepreneurial rms to make more educated decisions about whether to join an incubator andi so which one. It will inorm accelerator managers about best-in-class practices and provide mechanismsto improve their perormance. Finally, oundations, investors and development institutions will be ableto assess the impact o their investments and identiy strategies to scale or replicate successul incubatormodels.

7/27/2019 Bridging the Pioneer Gap The Role of Accelerators in Launching High Impact Enterprises .pdf

http://slidepdf.com/reader/full/bridging-the-pioneer-gap-the-role-of-accelerators-in-launching-high-impact 28/332

XI. RecommendationsFollowing on this research, we recommend several action items or various players in this ecosystem: (1)Incubators and Accelerators, (2) Impact Investors, (3) Foundations, and (4) Academics.

For Incubators and Accelerators

• Invest in platorms and systems to encourage and enable quality data collection rom theenterprises you support,

• Collect data rom all enterprises that apply to your programs, even the ones that are not acceptedor do not receive services, to more comprehensively assess perormance against a control group.Simple data collection processes can be built into your application orm.

• Collect data rom participating enterprises or at least ve years post-graduation to track progressand growth over the medium to long-term. The impact o accelerator support can take several yearsto materialize.

• Partner with academic institutions and industry associations to develop stronger data collectionsystems.

• Strengthen your processes or searching and sourcing ventures or your programs. Being in aposition to select the top ventures—without compromising quality—matters.

• Develop more rigorous, multi-stage, selection processes, drawing rom best practices in other

sectors. Engage other ecosystem members, such as investors, oundations, and technical expertsin the selection process, so that you are building a cohort that aligns with the needs o upstreamnancers .

• Build networks with the local nancial sector, in particular domestic commercial investors, whomay be able to directly support a plurality or majority o your graduates more readily than impact investors.

• Enterprises do not need investment alone, but also, access to markets. Build networks withcorporate supply chains, both domestic, and international.

• Explore other revenue streams such as investment closing ees and direct investment.

For Impact Investors

•

Leverage the networks and reach o incubators and accelerators, and work in collaboration withthem to strengthen your pipeline and explore potential areas or improved alignment in theiractivities.

• Build ormal partnerships with accelerators that are closely aligned with your investment strategy and that have strong perormance records.

• Invest in accelerators, either with time or money. Accelerators will be more inclined to deliver youthe deal fow you’re asking or—as a customer—i you help them do the work they are trying to do.

For Foundations

• Support the development and continuation o best practices among successul accelerators andincubators by contributing to their operations, development o perormance management systems,and dissemination o their results.

• Emphasize quality o services over quantity o entrepreneurs served when supporting incubatorand accelerator grantees.

• Build stronger networks between investors and incubators to enhance ecosystem eciency.

• Provide support or accelerators to track enterprise perormance.

For Academics

• Focus on developing methodologies to better assess incubator and accelerator perormance.

• Conduct empirical research on key success actors or incubators and accelerators, including ananalysis o the quality o services, the relevance o the selection process, and the eects o strong partnerships and networks.

7/27/2019 Bridging the Pioneer Gap The Role of Accelerators in Launching High Impact Enterprises .pdf

http://slidepdf.com/reader/full/bridging-the-pioneer-gap-the-role-of-accelerators-in-launching-high-impact 29/332

Appendices

ListofSurveyedAccelerators

Organization Name (in alphabetical order)

1) Agora Partnerships*

2) Angels Initiatives

3) Artemisia*

4) Betaspring

5) Global Accelerator Network

6) Bethnal Green Ventures

7) BiD Network*

8) Capital Innovators

9) Dasra*

10) Eleven Accelerator Venture Fund11) Endeavor*

12) Endeavor Global*

13) FATE Foundation*

14) Fledge

15) Global Catalyst Initiative*

16) Global Social Benet Incubator*

17) good.bee

18) Groundwork Labs

19) GrowLab

20) GrowthAfrica / The GrowthHub*

21) Hired by Society

22) HUB Vienna Incubation

23) iAccelerator, Centre for Innovation Incubation and Entrepreneurship, IIM-Ahmedabad

24) Impact Amplier*

25) Incubate

26) Intellecap (Intellectual Capital Advisory Services Pvt Ltd)*

27) Invest2Innovate*

28) Investment Ready Program

29) iStarter

30) LGT Venture Philanthropy Foundation*

31) m:lab East Africa

32) Mara Foundation

33) Mozilla WebFWD

34) National Collegiate Inventors and Innovators Alliance

35) NESsT*

7/27/2019 Bridging the Pioneer Gap The Role of Accelerators in Launching High Impact Enterprises .pdf

http://slidepdf.com/reader/full/bridging-the-pioneer-gap-the-role-of-accelerators-in-launching-high-impact 30/332

36) New Ventures India*

37) NewME Accelerator

38) Nxtp Labs

39) Panzanzee

40) Sinapis Group

41) StarCube

42) Startup Farm

43) Startupbusiness

44) StartupYard

45) SURF Incubator

46) Tree Labs

47) UnLtd India

48) Unreasonable Institute

49) Village Capital*

50) Wennovation Hub

51) Villgro*

52) Z80 Labs Technology Incubator *ANDE Members

7/27/2019 Bridging the Pioneer Gap The Role of Accelerators in Launching High Impact Enterprises .pdf

http://slidepdf.com/reader/full/bridging-the-pioneer-gap-the-role-of-accelerators-in-launching-high-impact 31/332

ListofSurveyedInvestors

Organization Name (in alphabetical order)

1) Accion Venture Lab*

2) Adobe Capital

3) Anavo

4) Angel Ventures Mexico

5) Annona Sustainable Investments BV

6) Bamboo Finance*

7) Creas

8) EcoEnterprises Fund*

9) eVA Fund

10) Ferd Social Entrepreneurs

11) Good Capital

12) Gray Ghost Ventures*

13) GroFin *14) Injaro Agricultural Capital Holdings

15) Insitor Management

16) Inversor Fund *

17) Invested Development

18) Jacana Partners *

19) LGT Venture Philanthropy*

20) Lundin Foundation*

21) ManoCap

22) Oasis500 (Oasis Ventures 1)

23) Oikocredit USA

24) Peery Foundation

25) PhiTrust Partenaires

26) Pomona Impact

27) Renewal2 Investment Fund

28) RSF Social Finance

29) Small Enterprise Assistance Fund (SEAF) *

30) SITAWI - Finance for Good31) Social Venture Fund

32) TBL Mirror Fund

33) Unitus Impact *

34) Unitus Seed Fund

35) Vox Capital *

36) Voxtra *

37) Willow Impact Investors*

*ANDE Members

7/27/2019 Bridging the Pioneer Gap The Role of Accelerators in Launching High Impact Enterprises .pdf

http://slidepdf.com/reader/full/bridging-the-pioneer-gap-the-role-of-accelerators-in-launching-high-impact 32/332

References

1 Saltuk, Y., Bouri, A., Mudaliar, A. & Pease, M. (2013) Perspectives on Progress: The Impact Investor Survey, J. P. Morgan and GIIN

2 Koh, H., Karamchandani, A., & Katz, R. (2012). “From Blueprint to Scale: The Case or Philanthropy in Impact Investing” The MonitorInstitute & Acumen Fund.

3 Baird, R., Hedinger H., Seekins C. (2012). Bridging the Gap: The Role o Accelerators in Impact Investing. Village Capital

4 Kubzansky, M., Cooper, A. and Barbary V. (2011) Promise and Progress, Market Based Solutions to Poverty in Arica, Monitor Group

5 Vanderstraeten, J., & Matthyssens, P. (2010). Measuring the perormance o business incubators: A critical analysis o eectiveness approachesand perormance measurement systems. In ICSB conerence, Cincinnati, US, June, published in conerence proceedings-USB, ISBN (pp. 978-0)Sherman, H., & Chappell, D. S. (1998). Methodological challenges in evaluating business incubator outcomes. Economic Development Quarterly, 12(4), 313-321.McMullan, E., Chrisman, J. J., & Vesper, K. (2001). Some problems in using subjective measures o eectiveness to evaluate entrepreneurialassistance programs. Entrepreneurship Theory and Practice, 26(1), 37-54.

6 Lalkaka, R., & Bishop, J. (1996). Business incubators in economic development: an initial assessment in industrializing countries. UnitedNations Development Programme.

7 Chandra, A., & Fealey, T. (2009). Business incubation in the United States, China and Brazil: a comparison o role o government, incubatorunding and nancial services. International Journal o Entrepreneurship, 13(13), 67-86.

8 Khalid, F. A., Gilbert, D., Huq, A., & Melaka, U. T. M. (2012). INVESTIGATING THE UNDERLYING COMPONENTS IN BUSINESSINCUBATION PROCESS IN MAL AYSIAN ICT INCUBATORS. congurations, 1(1). Aerts, K., Matthyssens, P., & Vandenbempt, K. (2007). Critical role and screening practices o European businessincubators. Technovation, 27(5), 254-267.Lumpkin, J. R., & Ireland, R. D. (1988). Screening practices o new business incubators: the evaluation o critical success actors. AmericanJournal o Small Business, 12(4), 59-81. Aerts, K., Matthyssens, P., & Vandenbempt, K. (2007). Critical role and screening practices o European businessincubators. Technovation, 27(5), 254-267.

9 Ibid.

10 Haapasalo, H., & Ekholm, T. (2004). A prole o European incubators: a ramework or commercialising innovations. International Journal oEntrepreneurship and Innovation Management, 4(2), 248-270.

11 Ferguson, R., & Olosson, C. (2004). Science parks and the development o NTBFs—location, survival and growth. The journal o technology transer, 29(1), 5-17.

12 Lösten, H., & Lindelö, P. (2002). Science Parks and the growth o new technology-based rms—academic-industry links, innovation andmarkets.Research Policy, 31(6), 859-876.

13 Amezcua, A. S. (2010). Boon or Boondoggle? Business Incubation as Entrepreneurship Policy.

14 de Oliveira, R. A., & Filipe, T. (2011). Are they helping? An examination o business incubators’ impact on tenant rms. University o Twente.