Embed Size (px)

Citation preview

ICIC

I S

ecurit

ies –

Retail E

quit

y R

esearch

MO

ME

NT

UM

PIC

K

• The IT index continues to move within the leading

quadrant highlighting the continuance of relative

outperformance of IT stocks. The decline within the

quadrant suggests profit booking in IT stocks. However,

the bias in IT stocks remains positive

• BSE consumer goods has seen a pick-up in relative

momentum and moved into the leading quadrant from

the improving quadrant implying that consumer stocks

have started a fresh up move after recent consolidation

• BSE Bankex and BSE Auto have moved higher within

the lagging quadrant indicating a pick-up in relative

momentum and are likely to see stock specific action in

the above sector in the coming month

Sectors likely to outperform on Relative Strength Model Relative Rotation Graph

Our May edition of Monthly Technical Outlook highlighted a

possibility of correction in May while reiterating that such a

correction would create an incremental buying opportunity

for investors. Ongoing corrective phase amid global volatility

and higher crude prices have resulted in a sizeable price

correction in the broader markets helping stocks to work off

excesses built in the previous rally.

Contrary to well known adage of “Sell in May and go away”,

empirical evidence in Indian equities favours buying in May.

In the last two decades, 75% of the time, buying in May, has

generated positive returns over the next six months for

investors as calculated from May lows. In the current

context, we expect the Nifty to consolidate above the strong

support of 10400 and eventually head towards 10930.

Hence, we reiterate our stance and recommend investors

with a medium term horizon utilise volatility, to build

portfolio in quality stocks.

Technical Outlook.. NSE Nifty Weekly Bar Chart

Source: Bloomberg, ICICI Direct Research

Month

ly T

echn

ical

Outlo

ok

May 31, 2018 ICICI Securities Ltd. | Retail Equity Research 1

Nifty:Pendulum to swing towards 10930…

Domestic Indices

Research Analyst

Dharmesh Shah

Nitin Kunte, CMT

Pabitro Mukherjee

Ninad Tamhanekar, CMT

Vinayak Parmar

% from 1-month

Indices 200 DMA % chg

Sensex 34949 4.1 -0.7

CNX Nifty 10614 2.5 -0.8

CNX Mid Cap 18975 -2.7 -6.1

CNX Small Cap 7907 -4.7 -5.3

CNX IT 13558 12.2 -3.3

BSE Auto 24568 -1.7 -5.0

CNX Pharma 8321 -9.1 -8.1

CNX FMCG 28658 7.6 0.1

BSE Banking 29411 3.5 2.8

BSE Oil & Gas 14352 -7.2 -1.2

BSE Metal 13638 -4.4 -4.3

BSE Capital Goods 19071 2.5 -3.1

BSE Power 2133 -5.6 -4.5

BSE Realty 2257 -3.5 -7.3

BSE PSU 7857 -9.2 -0.1

* Closing Price of May 30, 2018

Close

ICIC

I S

ecurit

ies –

Retail E

quit

y R

esearch

MO

ME

NT

UM

PIC

K

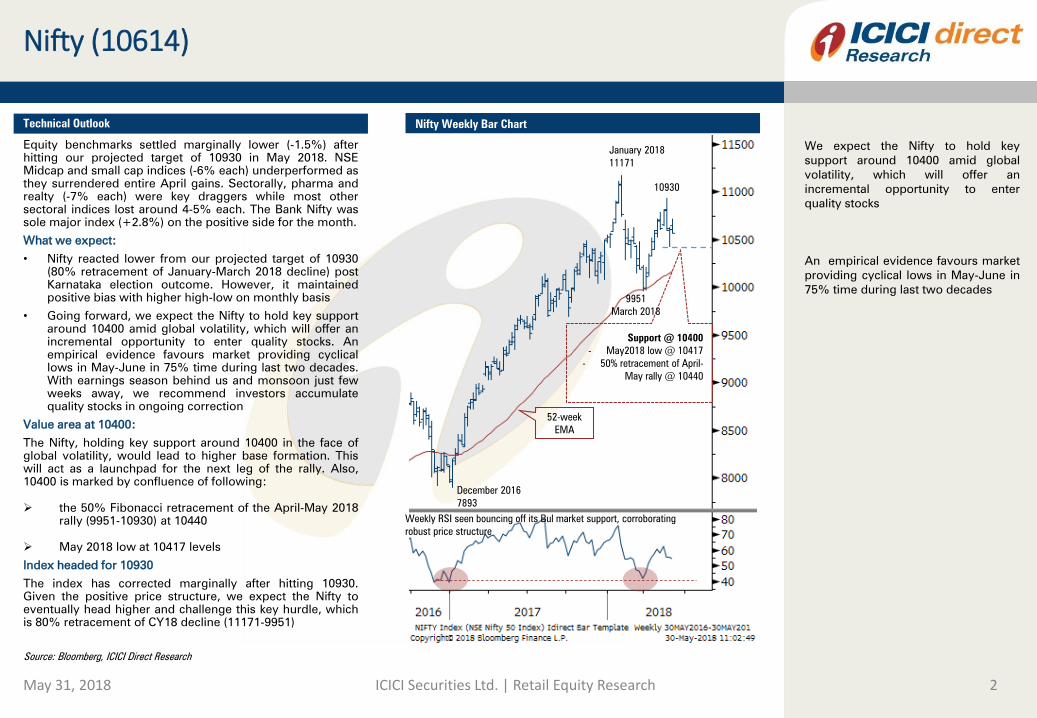

Nifty (10614)

Equity benchmarks settled marginally lower (-1.5%) after

hitting our projected target of 10930 in May 2018. NSE

Midcap and small cap indices (-6% each) underperformed as

they surrendered entire April gains. Sectorally, pharma and

realty (-7% each) were key draggers while most other

sectoral indices lost around 4-5% each. The Bank Nifty was

sole major index (+2.8%) on the positive side for the month.

What we expect:

• Nifty reacted lower from our projected target of 10930

(80% retracement of January-March 2018 decline) post

Karnataka election outcome. However, it maintained

positive bias with higher high-low on monthly basis

• Going forward, we expect the Nifty to hold key support

around 10400 amid global volatility, which will offer an

incremental opportunity to enter quality stocks. An

empirical evidence favours market providing cyclical

lows in May-June in 75% time during last two decades.

With earnings season behind us and monsoon just few

weeks away, we recommend investors accumulate

quality stocks in ongoing correction

Value area at 10400:

The Nifty, holding key support around 10400 in the face of

global volatility, would lead to higher base formation. This

will act as a launchpad for the next leg of the rally. Also,

10400 is marked by confluence of following:

the 50% Fibonacci retracement of the April-May 2018

rally (9951-10930) at 10440

May 2018 low at 10417 levels

Index headed for 10930

The index has corrected marginally after hitting 10930.

Given the positive price structure, we expect the Nifty to

eventually head higher and challenge this key hurdle, which

is 80% retracement of CY18 decline (11171-9951)

May 31, 2018 ICICI Securities Ltd. | Retail Equity Research 2

Technical Outlook Nifty – Weekly Bar Chart

Source: Bloomberg, ICICI Direct Research

January 2018

11171

9951

March 2018

December 2016

7893

52-week

EMA

Weekly RSI seen bouncing off its Bul market support, corroborating

robust price structure

Support @ 10400

- May2018 low @ 10417

- 50% retracement of April-

May rally @ 10440

Nifty Weekly Bar Chart

10930

We expect the Nifty to hold key

support around 10400 amid global

volatility, which will offer an

incremental opportunity to enter

quality stocks

An empirical evidence favours market

providing cyclical lows in May-June in

75% time during last two decades

ICIC

I S

ecurit

ies –

Retail E

quit

y R

esearch

MO

ME

NT

UM

PIC

K

Seasonality favours Bulls…

May 31, 2018 ICICI Securities Ltd. | Retail Equity Research 3

May has typically provided cyclical lows for index..

There is an old adage in overseas markets, “Sell in May and

go away”. This is based on the assumption that stocks

typically underperform during the May-October period.

We have closely examined the performance of NSE Nifty

index over the past 20 years to verify, if this adage holds

true in the Indian context. Empirical evidence suggest that in

fact May has offered a decent buying opportunity for

investors as 75% of the time year-end returns as calculated

from May lows has been positive

The adjacent table lists May lows every year for the Nifty and

year-end returns as calculated from May lows.

To conclude, seasonality clearly favours buying in May.

Investors would therefore be better off utilising volatility

around Karnataka elections and fear of rising interest rates

by RBI, as incremental buying opportunity to ride the

structural uptrend.

Seasonality favours buying in May…

Source: Bloomberg, ICICI Direct Research

Table showing year-end returns of Nifty from May lows every year

CY Lows in May Return till Year-end

2017 9270 13.59

2016 7678 6.6

2015 7997 -0.64

2014 6638 24.77

2013 5910 6.67

2012 4789 23.3

2011 5328 -13.21

2010 4786 28.17

2009 3478 49.54

2008 4802 -38.38

2007 3981 54.18

2006 2896 36.95

2005 1898 49.42

2004 1292 60.99

2003 931 67.02

2002 1020 7.16

2001 1096 -3.38

2000 1201 5.16

1999 968 52.89

1998 1038 -14.84

ICIC

I S

ecurit

ies –

Retail E

quit

y R

esearch

MO

ME

NT

UM

PIC

K

Bank Nifty (26210): Index moving in rising channel highlighting continuance of positive bias

The Bank Nifty gained for a second consecutive month and

ended up more than 3%. The PSU bank index snapped a five

months decline and ended up more than 4% during the

previous month whereas the private bank index ended higher

for a second consecutive month and closed higher by more

than 3%. Positive global market and normal monsoon forecasts

led to the positive sentiments in the market.

The monthly price action formed a second consecutive bull

candle with a higher high and higher low in the monthly time

frame signaling continuance of the positive bias. The entire up

move since March 2018 low (23605) is well channelled

highlighting sustained demand at elevated levels. The index

during the corrective decline of mid May 2018 has rebounded

from the lower band of the rising channel highlighting positive

bias and a higher base formation in the index. In the coming

month, we expect the index to maintain positive bias and head

towards 27000 as it is the confluence of the recent high of mid

May 2018 (26972) and the trend line resistance joining highs of

January 2018 (27652) and May 2018 (26972) around 26900.

The overall bias in the index remains positive. Any corrective

decline from current level is likely to form a higher base and can

be used to accumulate fresh long position. We have revised the

short-term support level higher towards 25500-25700 as it is the

confluence of following:

the lower band of the rising channel containing the entire up

move since march 2018 low of 23605

the 50 days EMA placed around 25600, which has acted as

support during the recent up move since March 2018

38.2% retracement of the entire up move since March 2018

(23605-26972) at 25680

Among oscillators, the weekly 14 period’s RSI remain in strong

uptrend and has been sustaining above its nine period’s average

thus supports the continuation of the positive bias in the index

in the coming month.

May 31, 2018 ICICI Securities Ltd. | Retail Equity Research 4

Technical Outlook Bank Nifty Weekly Bar Chart

Source: Bloomberg, ICICI Direct Research

Index continue to form higher peak and higher trough and is

seen moving in a rising channel thus supports the positive bias

in the coming month

Weekly 14 period’s RSI remains in uptrend and has been

sustaining above its nine period’s average

27652

23605

25622

26972

Major support revised

higher towards @

25600-25800 being

confluence of:

- 38.2% retracement

of previous up move

- The lower band of

the rising channel

ICIC

I S

ecurit

ies –

Retail E

quit

y R

esearch

MO

ME

NT

UM

PIC

K

Sectoral merry-go-round…

• The IT index continues to move within the leading quadrant

highlighting the continuance of relative outperformance of IT

stocks. The decline within the quadrant suggests profit

booking in IT stocks but the bias in IT stocks remain positive

• BSE consumer goods have seen a pick-up in relative

momentum and moved into the leading quadrant from the

improving quadrant implying that the consumer stocks has

started a fresh up move after recent consolidation

• The Capital Goods index is poised at the neutral line implying

an in line performance with the benchmarks. Capital goods

stocks likely to perform at par with the benchmark indices

• BSE Bankex and BSE Auto has moved higher within the

lagging quadrant indicating a pick-up in relative momentum

and are likely to see stock specific action in the above sector

in the coming month

• BSE healthcare index is seen moving in a range signalling

sock specific action to continue in the coming month

• BSE Power index is moving within the lagging quadrant and

has failed to move into improving quadrant as was expected

in last edition signalling continuation of the consolidation in

the power stocks

• Oil & gas and PSU indices have been hovering in the lagging

quadrant suggesting loss of relative momentum and implying

further consolidation in these sectors

• Metal and realty indices have lost further ground after slipping

into the lagging quadrant as it continues to see deceleration

in relative price and momentum suggesting further

consolidation indicating relative underperformance in the

near term

May 31, 2018 ICICI Securities Ltd. | Retail Equity Research 5

Sectoral Rotation Relative Rotation Graph

Source: Bloomberg, ICICI Direct Research

In this section, we focus on the relative

performance of the BSE sectoral indices.

The adjacent scatter chart highlights the

relative performance of the 11 major

sectors of the BSE relative to the Sensex

with the y-axis plotting the relative price

momentum in the past 12 months and the

x-axis plotting the relative price. The chart

is then subdivided into four quadrants

Leadership quadrant: Top right is

“Leadership” quadrant, which represents a

sector that has strengthened in relative

price and momentum vis-à-vis the Sensex.

Weakening quadrant: Bottom right is the

“Weakening” quadrant where the relative

price of a sector has started to deteriorate

and momentum has started to slow.

Lagging quadrant: Bottom left is the

“Lagging” quadrant where the relative

price of a sector has become negative

with momentum suggesting

underperformance vis-à-vis the

benchmark.

Improving quadrant: Top left is the

“Improving” quadrant where the relative

price trend of the sector has started to rise

with momentum.

In summary, if a sector appears in the top

right quadrant, it indicates the sector is

trending higher and outperforming the

benchmarks. If a sector appears on the

bottom left it indicates it is trending lower.

Sectors appearing on the bottom right

indicate they are underperforming the

benchmark while if they appear in the top

left it suggests an improving price

momentum.

Notes

ICIC

I S

ecurit

ies –

Retail E

quit

y R

esearch

MO

ME

NT

UM

PIC

K

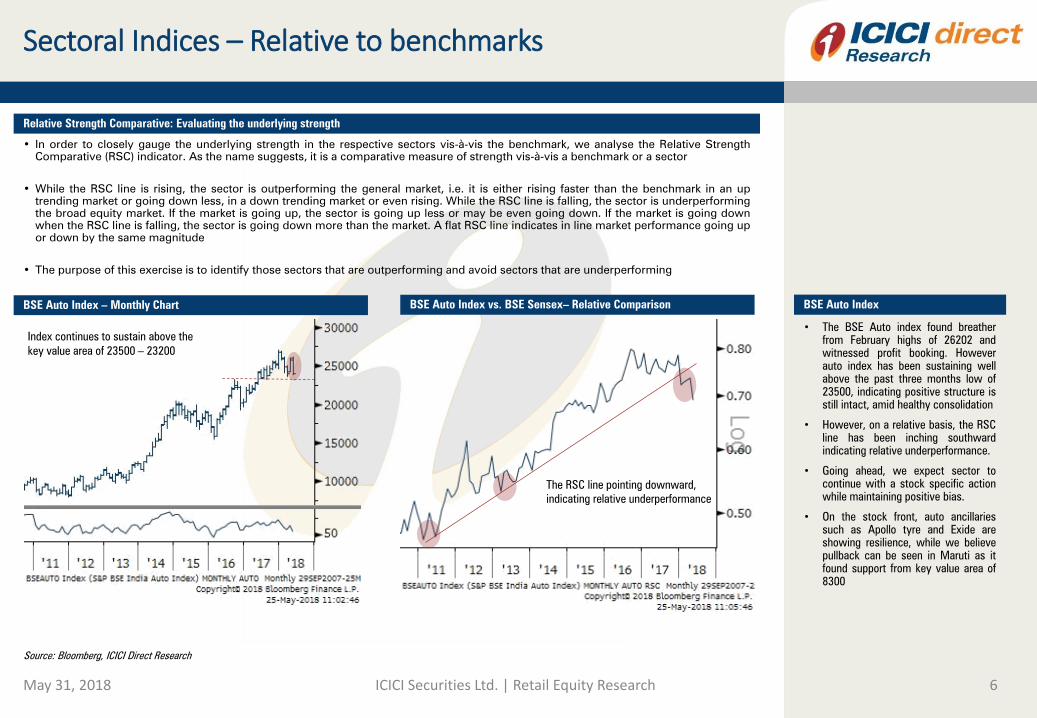

Sectoral Indices – Relative to benchmarks

May 31, 2018 ICICI Securities Ltd. | Retail Equity Research 6

• In order to closely gauge the underlying strength in the respective sectors vis-à-vis the benchmark, we analyse the Relative Strength

Comparative (RSC) indicator. As the name suggests, it is a comparative measure of strength vis-à-vis a benchmark or a sector

• While the RSC line is rising, the sector is outperforming the general market, i.e. it is either rising faster than the benchmark in an up

trending market or going down less, in a down trending market or even rising. While the RSC line is falling, the sector is underperforming

the broad equity market. If the market is going up, the sector is going up less or may be even going down. If the market is going down

when the RSC line is falling, the sector is going down more than the market. A flat RSC line indicates in line market performance going up

or down by the same magnitude

• The purpose of this exercise is to identify those sectors that are outperforming and avoid sectors that are underperforming

Relative Strength Comparative: Evaluating the underlying strength

BSE Auto Index – Monthly Chart

• The BSE Auto index found breather

from February highs of 26202 and

witnessed profit booking. However

auto index has been sustaining well

above the past three months low of

23500, indicating positive structure is

still intact, amid healthy consolidation

• However, on a relative basis, the RSC

line has been inching southward

indicating relative underperformance.

• Going ahead, we expect sector to

continue with a stock specific action

while maintaining positive bias.

• On the stock front, auto ancillaries

such as Apollo tyre and Exide are

showing resilience, while we believe

pullback can be seen in Maruti as it

found support from key value area of

8300

BSE Auto Index vs. BSE Sensex– Relative Comparison

Source: Bloomberg, ICICI Direct Research

BSE Auto Index

The RSC line pointing downward,

indicating relative underperformance

Index continues to sustain above the

key value area of 23500 – 23200

ICIC

I S

ecurit

ies –

Retail E

quit

y R

esearch

MO

ME

NT

UM

PIC

K

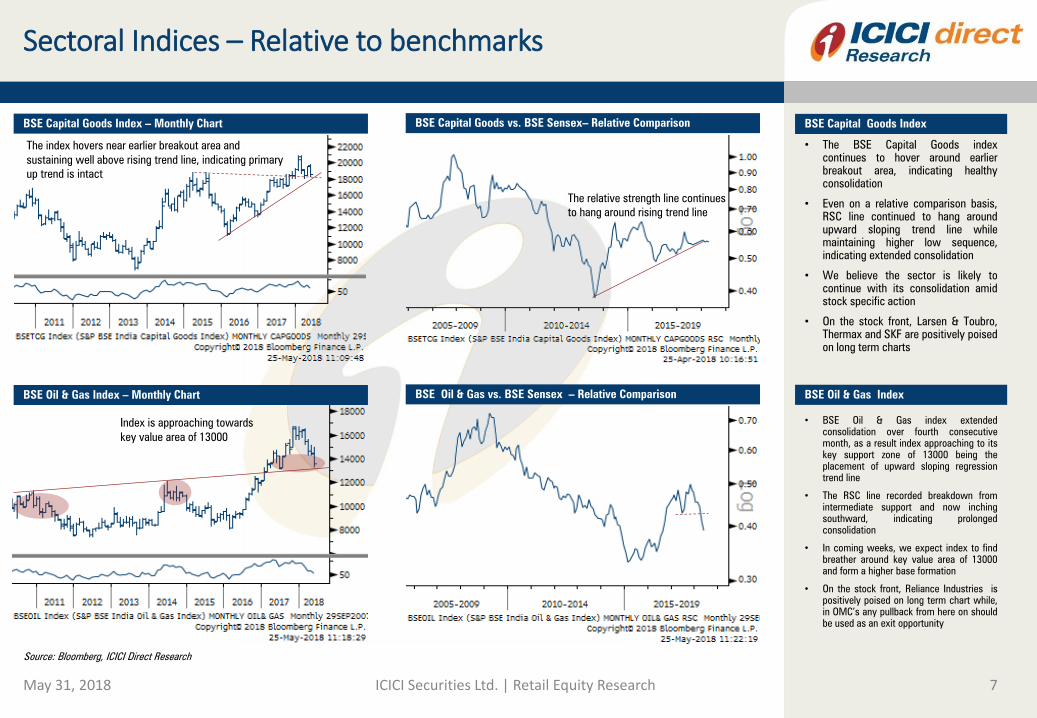

Sectoral Indices – Relative to benchmarks

May 31, 2018 ICICI Securities Ltd. | Retail Equity Research 7

BSE Oil & Gas Index – Monthly Chart BSE Oil & Gas vs. BSE Sensex – Relative Comparison

BSE Capital Goods Index – Monthly Chart BSE Capital Goods vs. BSE Sensex– Relative Comparison

• The BSE Capital Goods index

continues to hover around earlier

breakout area, indicating healthy

consolidation

• Even on a relative comparison basis,

RSC line continued to hang around

upward sloping trend line while

maintaining higher low sequence,

indicating extended consolidation

• We believe the sector is likely to

continue with its consolidation amid

stock specific action

• On the stock front, Larsen & Toubro,

Thermax and SKF are positively poised

on long term charts

• BSE Oil & Gas index extended

consolidation over fourth consecutive

month, as a result index approaching to its

key support zone of 13000 being the

placement of upward sloping regression

trend line

• The RSC line recorded breakdown from

intermediate support and now inching

southward, indicating prolonged

consolidation

• In coming weeks, we expect index to find

breather around key value area of 13000

and form a higher base formation

• On the stock front, Reliance Industries is

positively poised on long term chart while,

in OMC’s any pullback from here on should

be used as an exit opportunity

BSE Capital Goods Index

BSE Oil & Gas Index

Source: Bloomberg, ICICI Direct Research

The index hovers near earlier breakout area and

sustaining well above rising trend line, indicating primary

up trend is intact

The relative strength line continues

to hang around rising trend line

Index is approaching towards

key value area of 13000

ICIC

I S

ecurit

ies –

Retail E

quit

y R

esearch

MO

ME

NT

UM

PIC

K

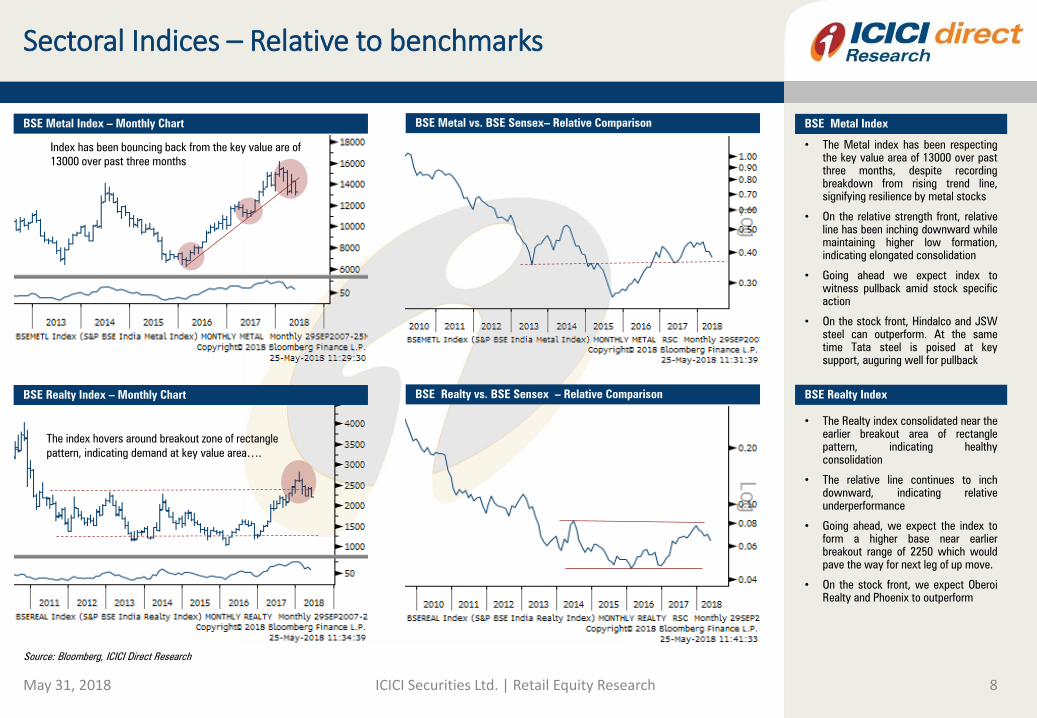

Sectoral Indices – Relative to benchmarks

May 31, 2018 ICICI Securities Ltd. | Retail Equity Research 8

BSE Realty Index – Monthly Chart BSE Realty vs. BSE Sensex – Relative Comparison

BSE Metal Index – Monthly Chart BSE Metal vs. BSE Sensex– Relative Comparison

• The Metal index has been respecting

the key value area of 13000 over past

three months, despite recording

breakdown from rising trend line,

signifying resilience by metal stocks

• On the relative strength front, relative

line has been inching downward while

maintaining higher low formation,

indicating elongated consolidation

• Going ahead we expect index to

witness pullback amid stock specific

action

• On the stock front, Hindalco and JSW

steel can outperform. At the same

time Tata steel is poised at key

support, auguring well for pullback

• The Realty index consolidated near the

earlier breakout area of rectangle

pattern, indicating healthy

consolidation

• The relative line continues to inch

downward, indicating relative

underperformance

• Going ahead, we expect the index to

form a higher base near earlier

breakout range of 2250 which would

pave the way for next leg of up move.

• On the stock front, we expect Oberoi

Realty and Phoenix to outperform

BSE Metal Index

BSE Realty Index

Source: Bloomberg, ICICI Direct Research

Index has been bouncing back from the key value are of

13000 over past three months

The index hovers around breakout zone of rectangle

pattern, indicating demand at key value area….

ICIC

I S

ecurit

ies –

Retail E

quit

y R

esearch

MO

ME

NT

UM

PIC

K

Sectoral Indices – Relative to benchmarks

May 31, 2018 ICICI Securities Ltd. | Retail Equity Research 9

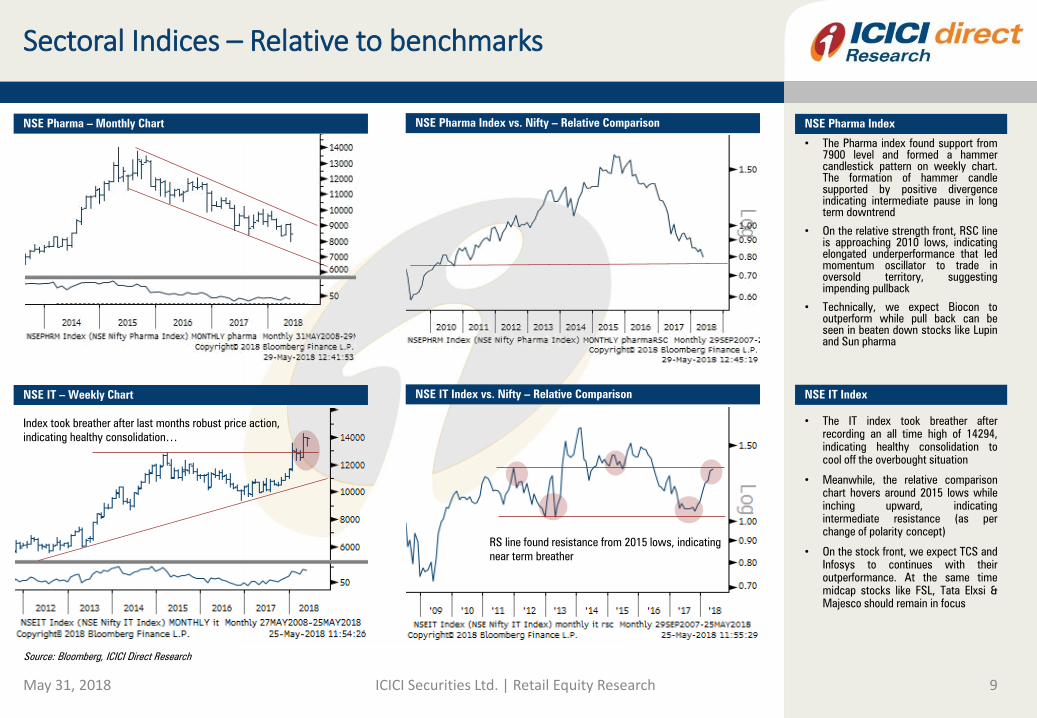

NSE IT – Weekly Chart NSE IT Index vs. Nifty – Relative Comparison

NSE Pharma – Monthly Chart NSE Pharma Index vs. Nifty – Relative Comparison

• The Pharma index found support from

7900 level and formed a hammer

candlestick pattern on weekly chart.

The formation of hammer candle

supported by positive divergence

indicating intermediate pause in long

term downtrend

• On the relative strength front, RSC line

is approaching 2010 lows, indicating

elongated underperformance that led

momentum oscillator to trade in

oversold territory, suggesting

impending pullback

• Technically, we expect Biocon to

outperform while pull back can be

seen in beaten down stocks like Lupin

and Sun pharma

• The IT index took breather after

recording an all time high of 14294,

indicating healthy consolidation to

cool off the overbought situation

• Meanwhile, the relative comparison

chart hovers around 2015 lows while

inching upward, indicating

intermediate resistance (as per

change of polarity concept)

• On the stock front, we expect TCS and

Infosys to continues with their

outperformance. At the same time

midcap stocks like FSL, Tata Elxsi &

Majesco should remain in focus

NSE Pharma Index

NSE IT Index

Source: Bloomberg, ICICI Direct Research

Index took breather after last months robust price action,

indicating healthy consolidation…

RS line found resistance from 2015 lows, indicating

near term breather

ICIC

I S

ecurit

ies –

Retail E

quit

y R

esearch

MO

ME

NT

UM

PIC

K

Sectoral Indices – Relative to benchmarks

May 31, 2018 ICICI Securities Ltd. | Retail Equity Research 10

NSE FMCG – Weekly Chart NSE FMCG Index vs. Nifty – Relative Comparison

• The FMCG witnessed range bound

activity post 10% rally over last month

and recorded an all time high of 29134

• On the relative strength front, RSC line

continues to inch upward, indicating

outperformance by FMCG stocks

• Going ahead, we expect index to enter

into healthy consolidation and

gradually pave the way for next leg of

up move

• On the stock front, we expect Colgate-

Palmolive, Hindustan Unilever and

Dabur to outshine the FMCG pack. At

the same time, Jyothy Laboratories

and ITC are positively poised on long

term chart

NSE FMCG Index

Source: Bloomberg, ICICI Direct Research

Index recorded an all time high, indicating

outperformance

ICIC

I S

ecurit

ies –

Retail E

quit

y R

esearch

MO

ME

NT

UM

PIC

K

Forthcoming Economic Event Calendar

May 31, 2018 ICICI Securities Ltd. | Retail Equity Research 11

Source: Bloomberg, ICICI Direct Research

Date Event Date Event

US China

1-Jun Change in Nonfarm Payrolls 1-Jun Caixin China PMI Mfg

5-Jun Markit US Services/Composite PMI 5-Jun Caixin China PMI Composite

7-Jun Initial Jobless Claims 10-Jun New Yuan Loans CNY

13-Jun FOMC Rate Decision (Upper/lower Bound) 14-Jun Retail Sales YTD YoY

14-Jun Retail Sales Advance MoM 14-Jun Industrial Production YoY

15-Jun Industrial Production MoM 15-Jun New Home Prices MoM

21-Jun Initial Jobless Claims 27-Jun Industrial Profits YoY

25-Jun New Home Sales MoM 30-Jun Non-manufacturing PMI

28-Jun GDP Annualized QoQ 30-Jun Manufacturing PMI

28-Jun PCE Deflator MoM 30-Jun Composite PMI

India UK

1-Jun Nikkei India PMI Mfg 1-Jun Markit UK PMI Manufacturing SA

5-Jun Nikkei India PMI Services 4-Jun Markit/CIPS UK Construction PMI

5-Jun Nikkei India PMI Composite 11-Jun Industrial Production MoM

6-Jun RBI Repurchase Rate/Reverse repo/CRR 13-Jun CPI/RPI MoM/YoY

12-Jun CPI/Industrial Production YoY 21-Jun Bank of England Bank Rate

14-Jun Wholesale Prices YoY 29-Jun GDP QoQ

29-Jun Fiscal Deficit INR Crore 29-Jun Lloyds Business Barometer

ICIC

I S

ecurit

ies –

Retail E

quit

y R

esearch

MO

ME

NT

UM

PIC

K

Pankaj Pandey Head – Research [email protected]

ICICI Direct Research Desk,

ICICI Securities Limited,

1st Floor, Akruti Trade Centre,

Road No 7, MIDC,

Andheri (East)

Mumbai – 400 093

May 31, 2018 ICICI Securities Ltd. | Retail Equity Research 12

ICIC

I S

ecurit

ies –

Retail E

quit

y R

esearch

MO

ME

NT

UM

PIC

K

We /I, Dharmesh Shah, Nitin Kunte, Ninad Tamhanekar, Pabitro Mukherjee, Vinayak Parmar Research Analysts, authors and the names subscribed to this report, hereby certify that all of the views expressed in this research report accurately reflect our views about the

subject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this report.

Terms & conditions and other disclosures:

ICICI Securities Limited (ICICI Securities) is a full-service, integrated investment banking and is, inter alia, engaged in the business of stock brokering and distribution of financial products. ICICI Securities Limited is a SEBI registered Research Analyst with SEBI

Registration Number – INH000000990.ICICI Securities is a wholly-owned subsidiary of ICICI Bank which is India’s largest private sector bank and has its various subsidiaries engaged in businesses of housing finance, asset management, life insurance, general

insurance, venture capital fund management, etc. (“associates”), the details in respect of which are available on www.icicibank.com

ICICI Securities is one of the leading merchant bankers/ underwriters of securities and participate in virtually all securities trading markets in India. We and our associates might have investment banking and other business relationship with a significant percentage of

companies covered by our Investment Research Department. ICICI Securities generally prohibits its analysts, persons reporting to analysts and their relatives from maintaining a financial interest in the securities or derivatives of any companies that the analysts cover.

The information and opinions in this section have been prepared by ICICI Securities and are subject to change without any notice. The report and information contained herein is strictly confidential and meant solely for the selected recipient and may not be altered in

any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written consent of ICICI Securities. While we would endeavour to update the information herein on reasonable basis, ICICI

Securities is under no obligation to update or keep the information current. Also, there may be regulatory, compliance or other reasons that may prevent ICICI Securities from doing so. Non-rated securities indicate that rating on a particular security has been

suspended temporarily and such suspension is in compliance with applicable regulations and/or ICICI Securities policies, in circumstances where ICICI Securities might be acting in an advisory capacity to this company, or in certain other circumstances.

The research recommendations are based on information obtained from public sources and sources believed to be reliable, but no independent verification has been made nor is its accuracy or completeness guaranteed. These research recommendations and

information herein is solely for informational purpose and shall not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial instruments. ICICI Securities will not treat recipients as customers by

virtue of their receiving these recommendations. Nothing in this section constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific circumstances. The securities discussed and

opinions expressed herein may not be suitable for all investors, who must make their own investment decisions, based on their own investment objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of

independent judgment by any recipient. The recipient should independently evaluate the investment risks. The value and return on investment may vary because of changes in interest rates, foreign exchange rates or any other reason. ICICI Securities accepts no

liabilities whatsoever for any loss or damage of any kind arising out of the use of these recommendations. Past performance is not necessarily a guide to future performance. Investors are advised to see Risk Disclosure Document to understand the risks associated

before investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and may be subject to change without notice.

ICICI Securities or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other assignment in the past twelve months.

ICICI Securities or its associates might have received any compensation from the companies mentioned herein during the period preceding twelve months from the date of these recommendations for services in respect of managing or co-managing public offerings,

corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction.

ICICI Securities or its associates might have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the companies mentioned herein in the past twelve months.

ICICI Securities encourages independence in research report preparation and strives to minimize conflict in preparation of research report. ICICI Securities or its associates or its Analysts did not receive any compensation or other benefits from the companies

mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither ICICI Securities nor Research Analysts and their relatives have any material conflict of interest at the time of publication of this reports.

It is confirmed that Dharmesh Shah, Nitin Kunte, Ninad Tamhanekar, Pabitro Mukherjee and Vinayak Parmar, Research Analysts giving these recommendations have not received any compensation from the companies mentioned herein in the preceding twelve

months.

Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions

ICICI Securities or its subsidiaries collectively or Research Analysts or their relatives do not own 1% or more of the equity securities of the company/companies mentioned herein as of the last day of the month preceding the publication of these research

recommendations.

Since Associates (ICICI group companies) of ICICI Securities are engaged in various financial service businesses, they might have financial interests or beneficial ownership in various companies including the subject company/companies mentioned herein.

It is confirmed that Research Analysts do not serve as an officer, director or employee or advisory board member of the companies mentioned herein.

ICICI Securities may have issued other reports that are inconsistent with and reach different conclusion from the information presented herein.

Neither the Research Analysts nor ICICI Securities have been engaged in market making activity for the companies mentioned herein.

We submit that no material disciplinary action has been taken on ICICI Securities by any Regulatory Authority impacting Equity Research Analysis activities.

This report or recommendations are not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be

contrary to law, regulation or which would subject ICICI Securities and affiliates to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to certain category of

investors. Persons in whose possession this document may come are required to inform themselves of and to observe such restriction

May 31, 2018 ICICI Securities Ltd. | Retail Equity Research 13

Disclaimer