Embed Size (px)

Citation preview

Copyright Gold Coast Schools1

Chapter 9

Broker

Basic Business Appraisal

Copyright Gold Coast Schools2

2

Learning Objectives

Describe the characteristics of the legal entities a business appraiser may encounter

List at least 5 reasons for a business appraisal

List the 5 steps in the business appraisal process

Describe at least 3 specific problem areas in a financial statement that may distort the firm's true economic value

Copyright Gold Coast Schools3

3

Learning Objectives

Explain the differences between cash basis accounting and accrual basis accounting;

Calculate the important financial ratios

List and describe the 4 approaches to estimating business value

Copyright Gold Coast Schools4

4

Similarities to a Real Estate Appraisal

Estimate market value

Differences

Appraiser must be able

– To read

– Understand

– Interpret financial statements

– inventory valuation

It may be necessary to be able to value intangible assets such as goodwill, licenses and franchises

Copyright Gold Coast Schools5

5

Business Appraisal Definitions

Going concern - value of a business as an

ongoing enterprise

Liquidation value - consistent with a forced or

hurried sale of the business assets

Copyright Gold Coast Schools6

6

Reasons for a Business Appraisal

Contemplated sale or purchase of a business

Allocation of value to specific assets

E.G. The sale of part of the business

Financial reporting purposes

Buy-sell agreements

Liquidation of the business

Divorce

Copyright Gold Coast Schools7

7

Reasons for a Business Appraisal

Estates and inheritance tax

Beneficiary of the estate gift receives the

gift free of tax

Tax is paid by the estate

Basis of property received is the fair market

value at the time of death

Condemnation proceedings

Determination of insurable value

Copyright Gold Coast Schools8

8

Business Appraisal Process

Define the assignment

Establish the date of the appraisal

Collect the data

Analyze the data

Prepare the final estimate

Prepare the appraisal report

Copyright Gold Coast Schools9

Report Includes

Summary and conclusions

Purpose of appraisal

Definition of value estimated

Insurance, cost, market, etc.

Description of subject business

Appraisal effective date

Description of appraisal process

Summary of facts derived from data

Statement of conclusions

Assumptions and limiting conditions

Supporting data, maps, financial statements and other

exhibits

Copyright Gold Coast Schools10

10

Financial Statements

Balance sheet

Statement of financial position at a point in

time

Income statement

Gives the results of operations over an

accounting period

Copyright Gold Coast Schools11

11

Problems with Accounting Principles

Estimates are necessary

Assets are reported at cost

Book value is original cost less depreciation

– Excluding land

Appraisers should restate value to market

value

Valuation accounts do not reflect value

Assets or liabilities may be missing

Copyright Gold Coast Schools12

12

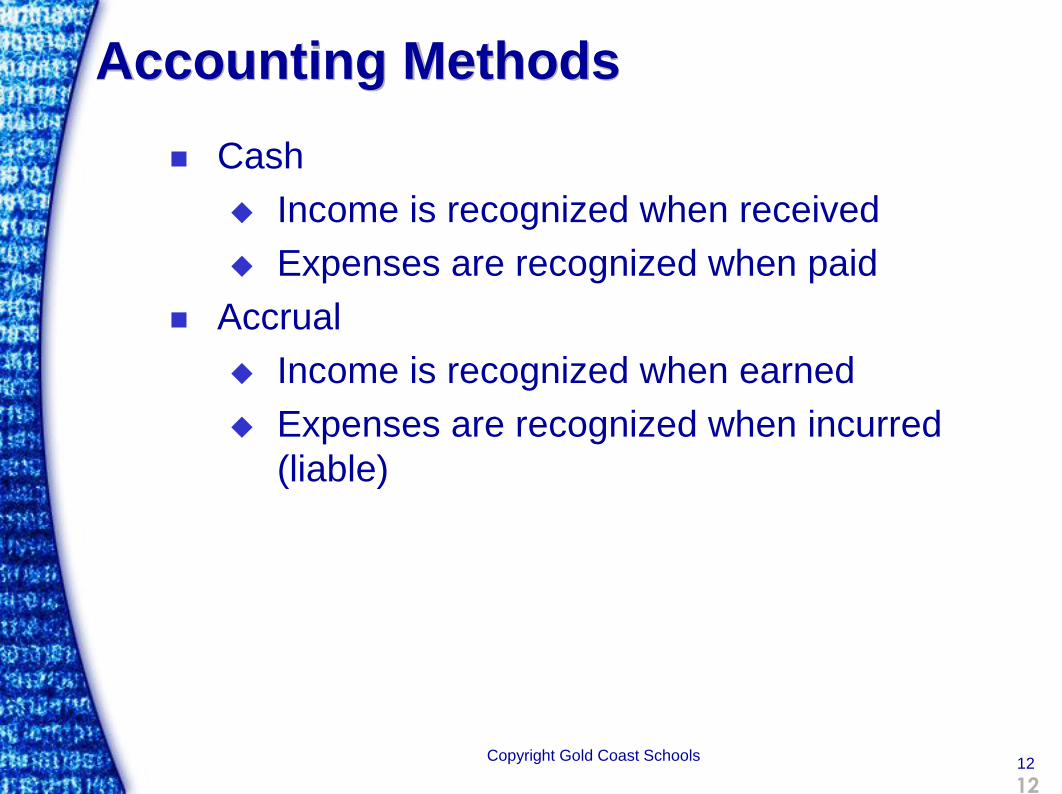

Accounting Methods

Cash

Income is recognized when received

Expenses are recognized when paid

Accrual

Income is recognized when earned

Expenses are recognized when incurred

(liable)

Copyright Gold Coast Schools13

13

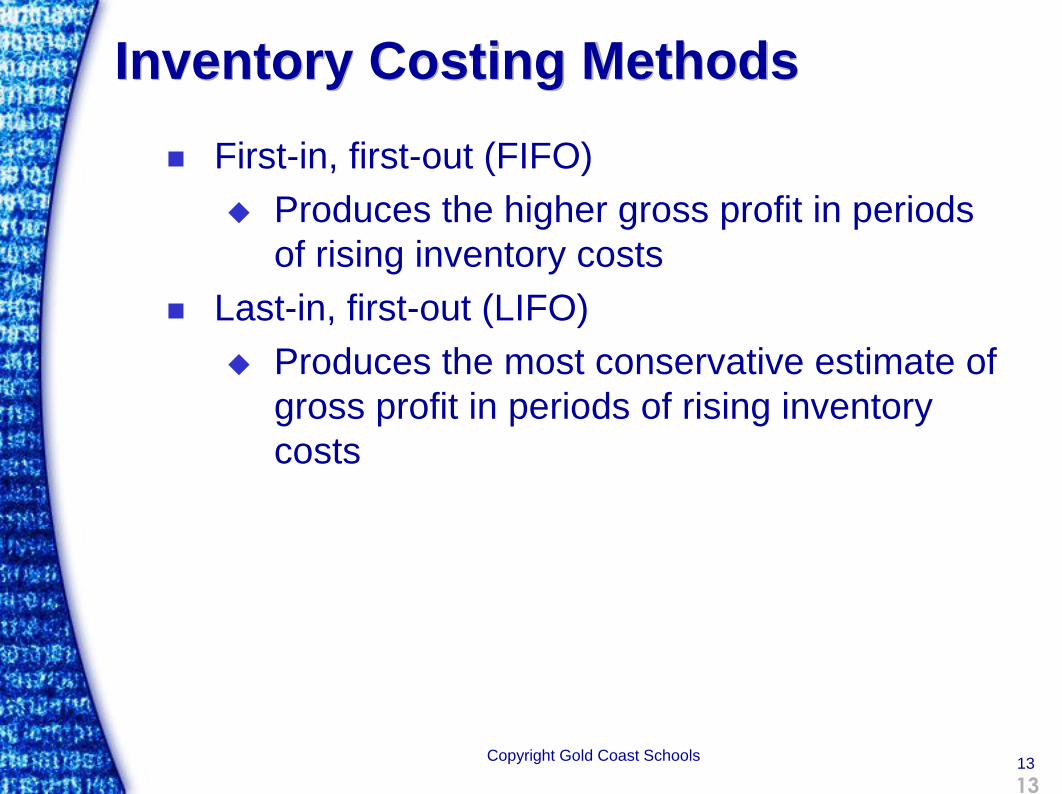

Inventory Costing Methods

First-in, first-out (FIFO)

Produces the higher gross profit in periods

of rising inventory costs

Last-in, first-out (LIFO)

Produces the most conservative estimate of

gross profit in periods of rising inventory

costs

Copyright Gold Coast Schools14

14

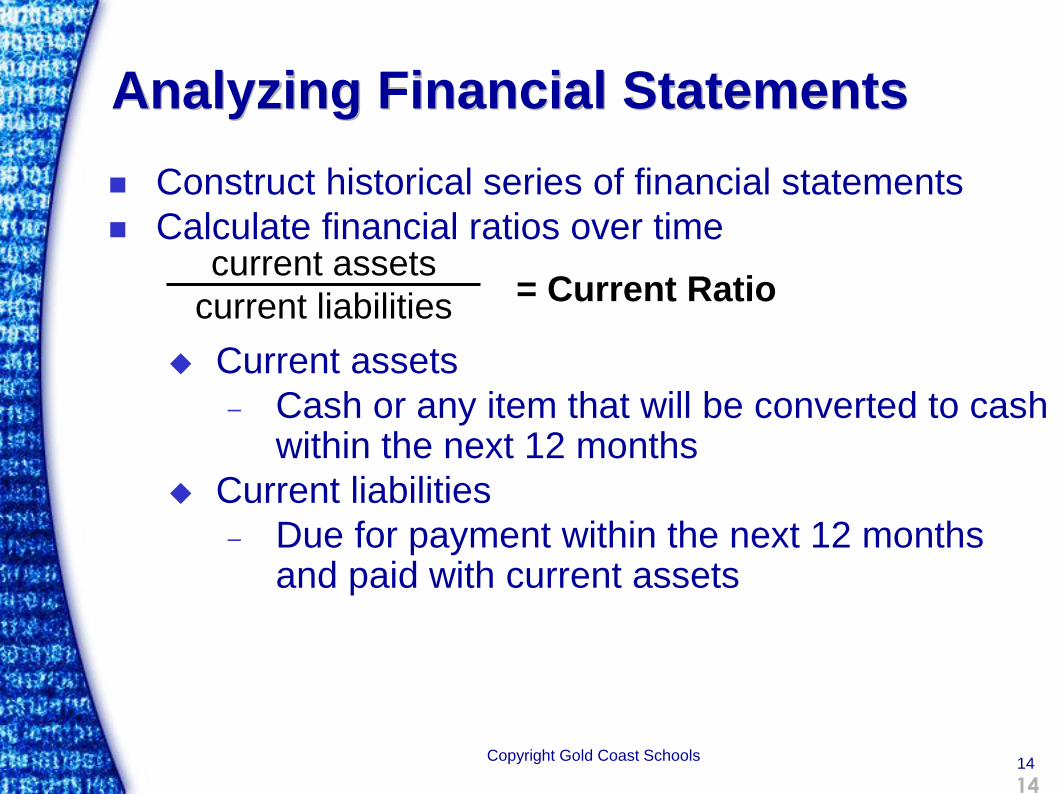

Analyzing Financial Statements

Construct historical series of financial statements

Calculate financial ratios over time

Current assets

– Cash or any item that will be converted to cash within the next 12 months

Current liabilities

– Due for payment within the next 12 months and paid with current assets

= Current Ratiocurrent assets

current liabilities

Copyright Gold Coast Schools15

15

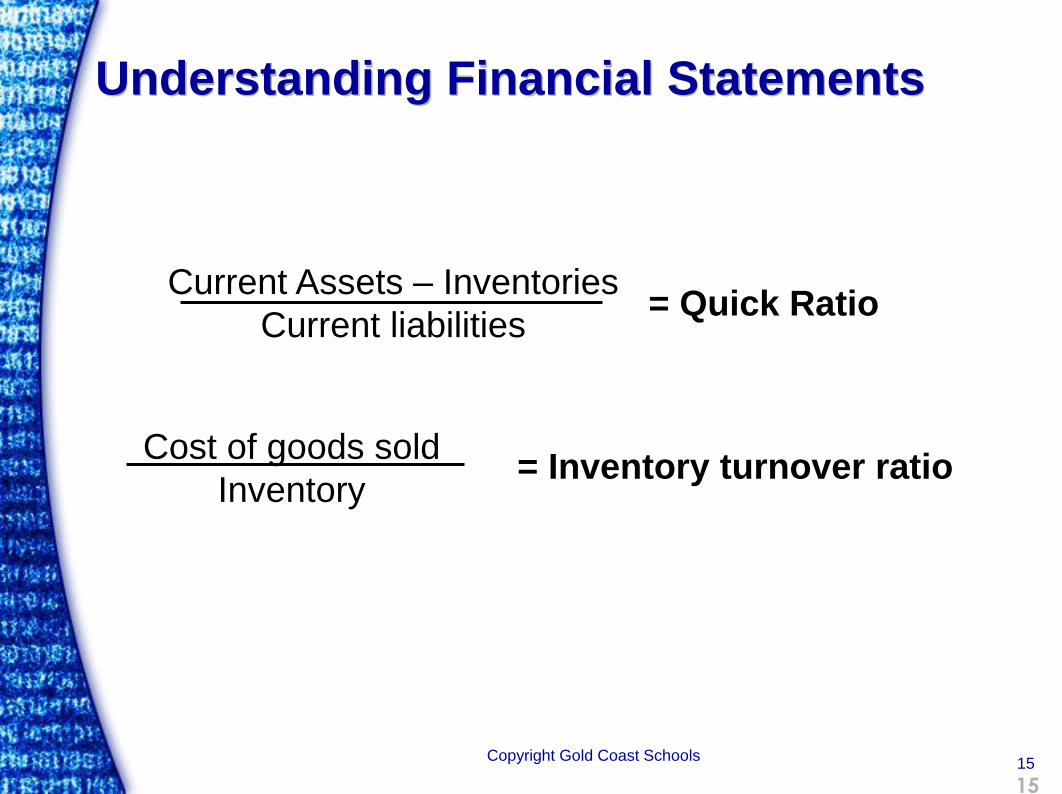

Understanding Financial Statements

= Inventory turnover ratioCost of goods sold

Inventory

= Quick RatioCurrent Assets – Inventories

Current liabilities

Copyright Gold Coast Schools16

16

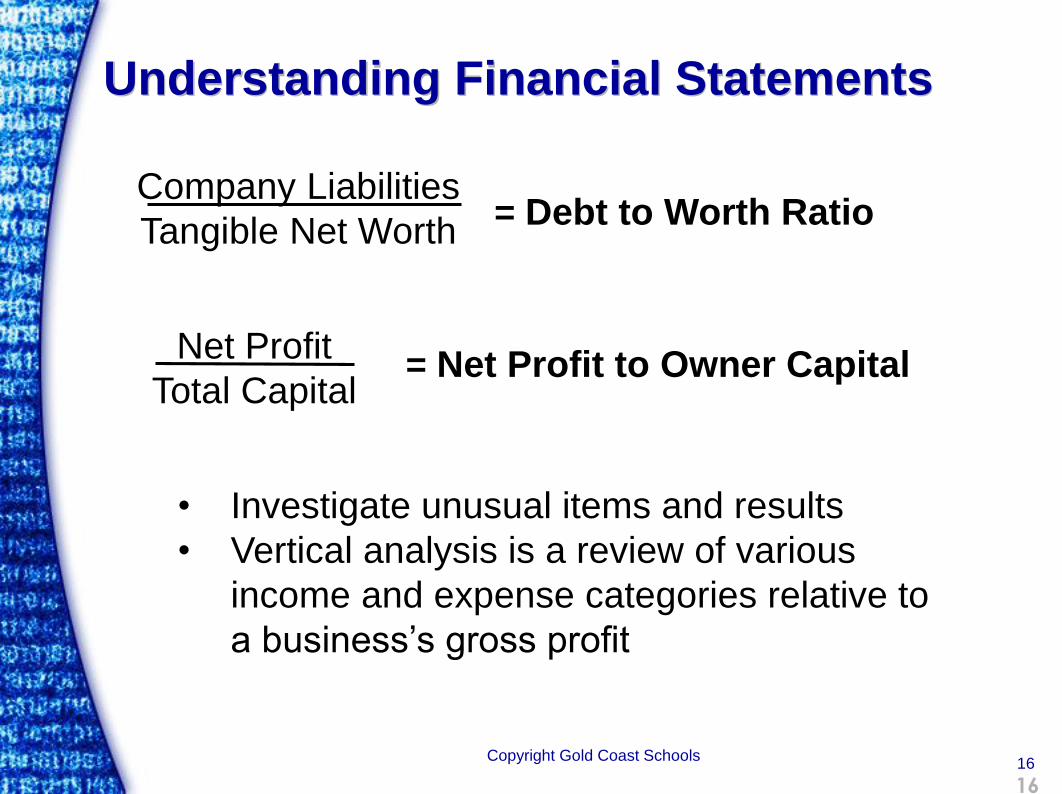

Understanding Financial Statements

= Debt to Worth RatioCompany Liabilities

Tangible Net Worth

= Net Profit to Owner CapitalNet Profit

Total Capital

• Investigate unusual items and results

• Vertical analysis is a review of various

income and expense categories relative to

a business’s gross profit

Copyright Gold Coast Schools17

17

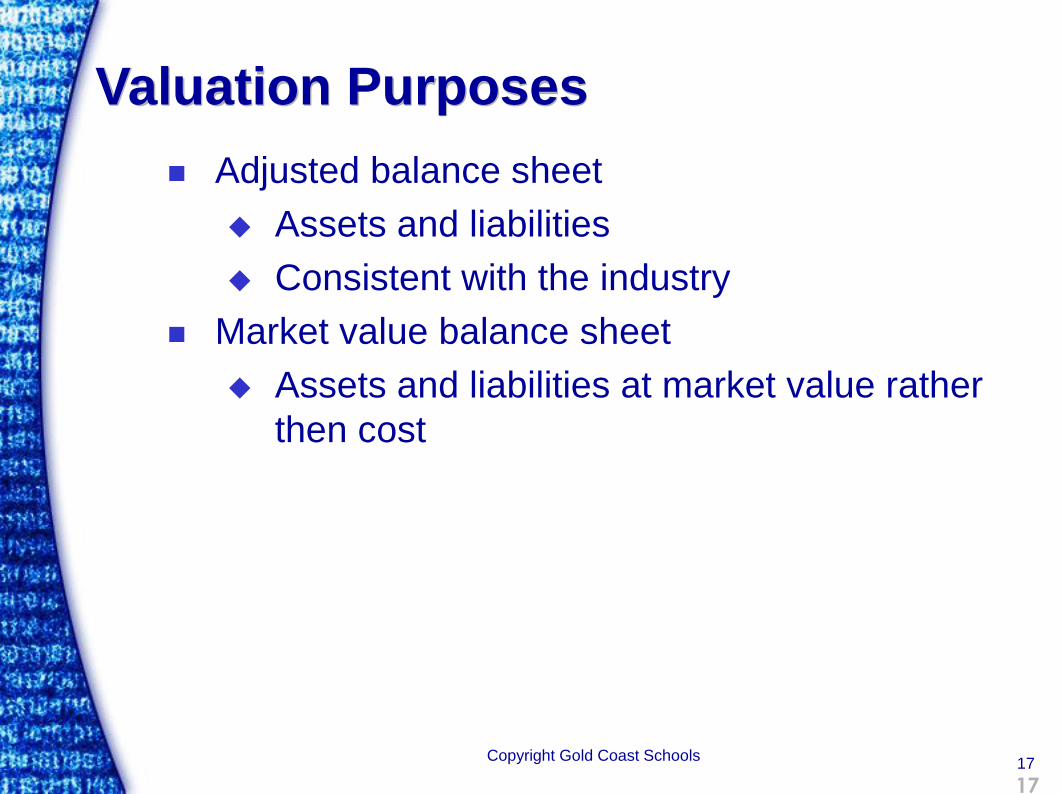

Valuation Purposes

Adjusted balance sheet

Assets and liabilities

Consistent with the industry

Market value balance sheet

Assets and liabilities at market value rather

then cost

Copyright Gold Coast Schools18

18

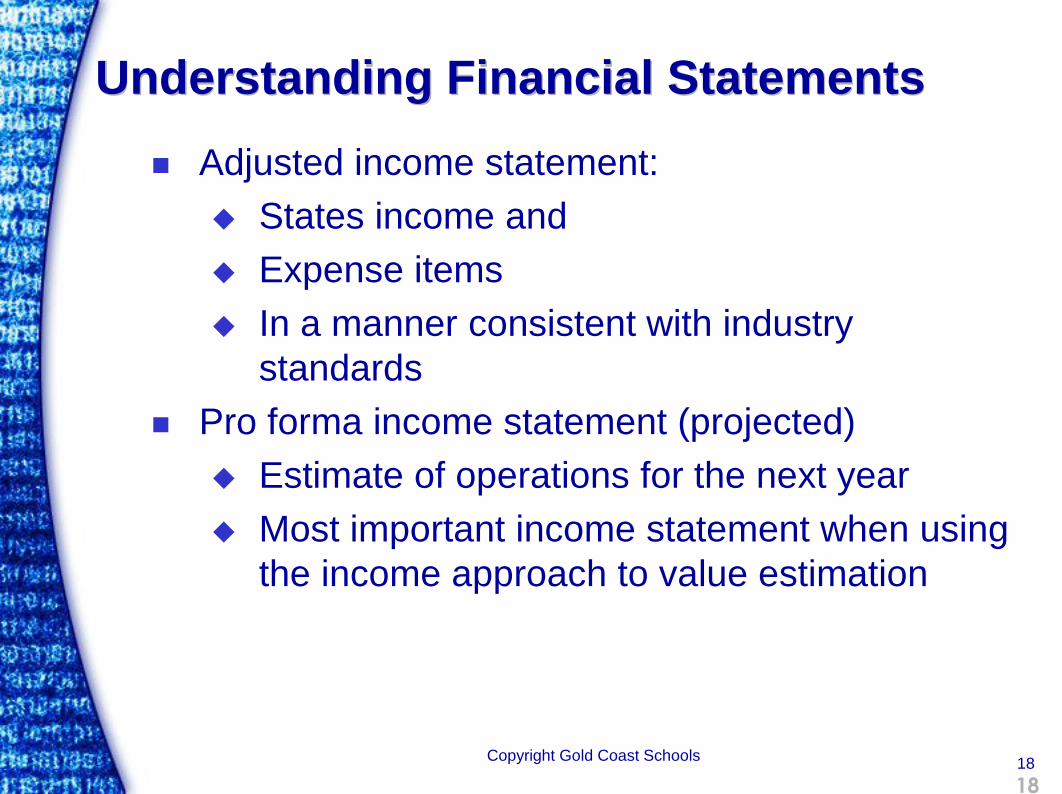

Understanding Financial Statements

Adjusted income statement:

States income and

Expense items

In a manner consistent with industry

standards

Pro forma income statement (projected)

Estimate of operations for the next year

Most important income statement when using

the income approach to value estimation

Copyright Gold Coast Schools19

19

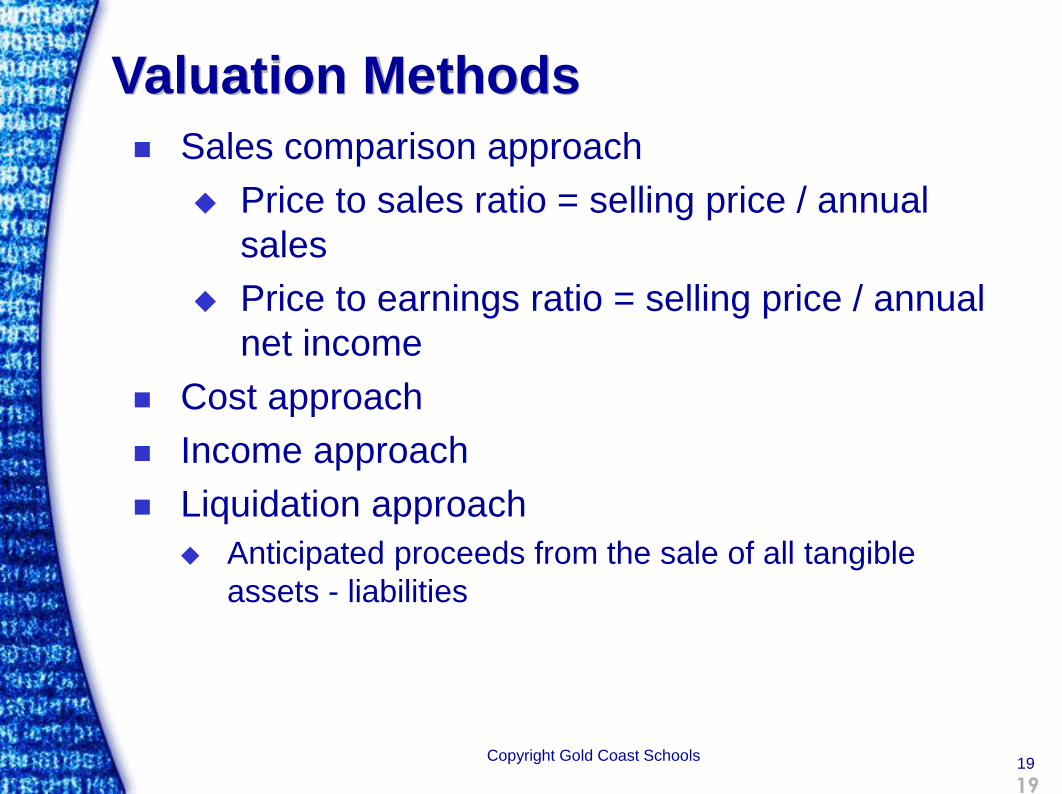

Valuation Methods

Sales comparison approach

Price to sales ratio = selling price / annual

sales

Price to earnings ratio = selling price / annual

net income

Cost approach

Income approach

Liquidation approach

Anticipated proceeds from the sale of all tangible

assets - liabilities

Copyright Gold Coast Schools20

20

Valuation of Intangible Assets

Goodwill

Business

Personal

Separable intangible assets

Franchises

Licenses

Copyrights

Leasehold benefits

Trademarks

Copyright Gold Coast Schools21

21

Methods of Valuation

Estimate the value

Tangible assets

Intangible assets

Business

Personal goodwill

Techniques

Excess profits approach

Market residual approach