Embed Size (px)

Citation preview

Number 39

Market Performance Sector Returns Top 5 TradedBRVM 10 BRVM Comp XOF Volume % Market

Close 273,9 268,0 Industrie 1,8% SNTS 2 545 014 415 25,3%1 month gain/loss 1,5 3,3 Services Publics 0,6% ONTBF 1 610 389 940 20,5%MTD change 0,5% 1,2% Finance -‐0,7% SGBC 1 168 517 400 9,3%YTD change 2,4% 3,8% Transport 14,4% UNXC 655 312 770 7,3%

Agriculture 0,0% FTSC 601 650 400 4,7%Distribution 8,5%

Total 11 695 591 907 100%

BRVM MONTHLY NEWSLETTER

Sunday, May 31, 2015

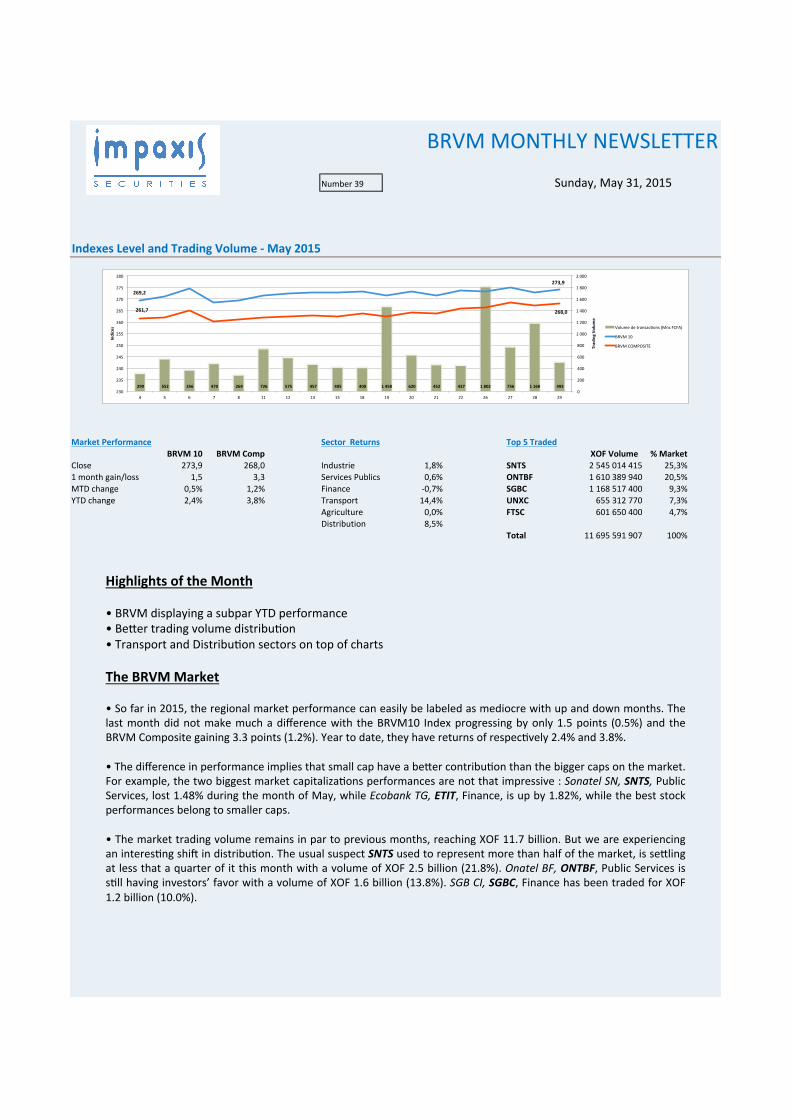

Indexes Level and Trading Volume -‐ May 2015

Highlights of the Month • BRVM displaying a subpar YTD performance • BeXer trading volume distribuYon • Transport and DistribuYon sectors on top of charts The BRVM Market • So far in 2015, the regional market performance can easily be labeled as mediocre with up and down months. The last month did not make much a difference with the BRVM10 Index progressing by only 1.5 points (0.5%) and the BRVM Composite gaining 3.3 points (1.2%). Year to date, they have returns of respecYvely 2.4% and 3.8%. • The difference in performance implies that small cap have a beXer contribuYon than the bigger caps on the market. For example, the two biggest market capitalizaYons performances are not that impressive : Sonatel SN, SNTS, Public Services, lost 1.48% during the month of May, while Ecobank TG, ETIT, Finance, is up by 1.82%, while the best stock performances belong to smaller caps. • The market trading volume remains in par to previous months, reaching XOF 11.7 billion. But we are experiencing an interesYng shid in distribuYon. The usual suspect SNTS used to represent more than half of the market, is seXling at less that a quarter of it this month with a volume of XOF 2.5 billion (21.8%). Onatel BF, ONTBF, Public Services is sYll having investors’ favor with a volume of XOF 1.6 billion (13.8%). SGB CI, SGBC, Finance has been traded for XOF 1.2 billion (10.0%).

299 552 356 470 269 726 575 457 405 400 1 458 620 452 437 1 802 756 1 168 493

269,2

273,9

261,7 268,0

0

200

400

600

800

1 000

1 200

1 400

1 600

1 800

2 000

230

235

240

245

250

255

260

265

270

275

280

4 5 6 7 8 11 12 13 15 18 19 20 21 22 26 27 28 29

Trad

ing Vo

lume

Indices Volume de transacYons (Mns FCFA)

BRVM 10

BRVM COMPOSITE

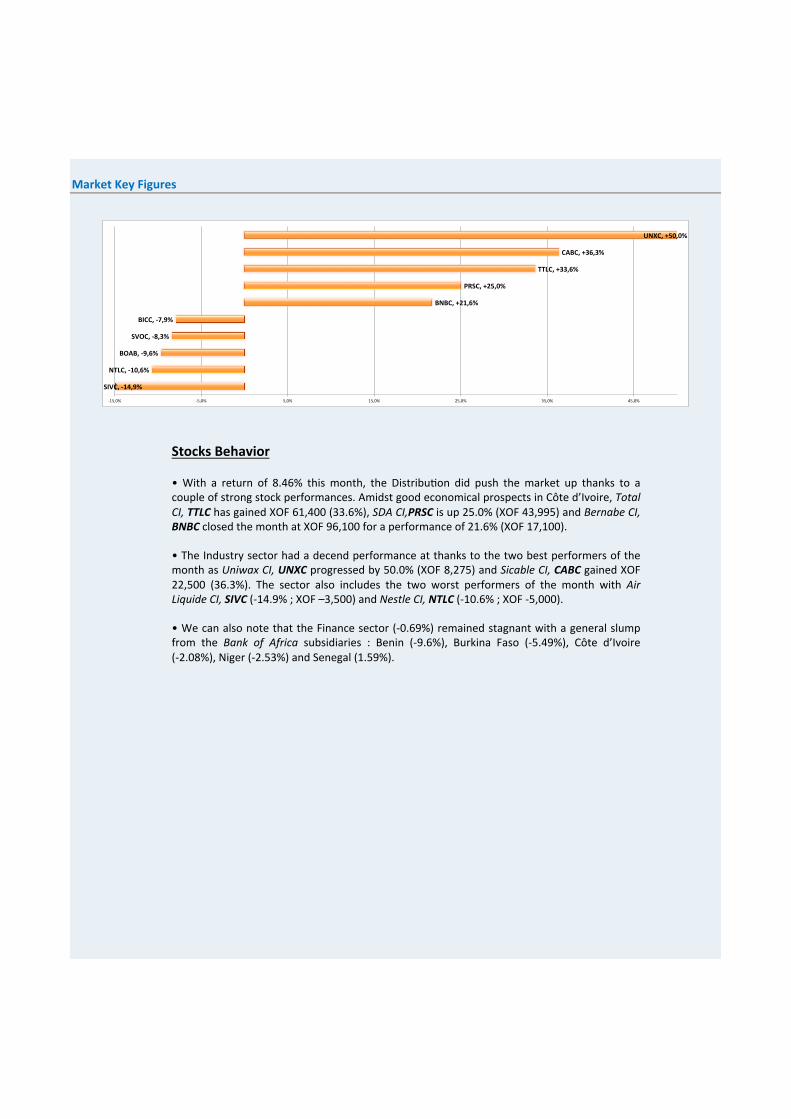

Market Key Figures

Stocks Behavior • With a return of 8.46% this month, the DistribuYon did push the market up thanks to a couple of strong stock performances. Amidst good economical prospects in Côte d’Ivoire, Total CI, TTLC has gained XOF 61,400 (33.6%), SDA CI,PRSC is up 25.0% (XOF 43,995) and Bernabe CI, BNBC closed the month at XOF 96,100 for a performance of 21.6% (XOF 17,100). • The Industry sector had a decend performance at thanks to the two best performers of the month as Uniwax CI, UNXC progressed by 50.0% (XOF 8,275) and Sicable CI, CABC gained XOF 22,500 (36.3%). The sector also includes the two worst performers of the month with Air Liquide CI, SIVC (-‐14.9% ; XOF –3,500) and Nestle CI, NTLC (-‐10.6% ; XOF -‐5,000). • We can also note that the Finance sector (-‐0.69%) remained stagnant with a general slump from the Bank of Africa subsidiaries : Benin (-‐9.6%), Burkina Faso (-‐5.49%), Côte d’Ivoire (-‐2.08%), Niger (-‐2.53%) and Senegal (1.59%).

SIVC, -‐14,9%

NTLC, -‐10,6%

BOAB, -‐9,6%

SVOC, -‐8,3%

BICC, -‐7,9%

BNBC, +21,6%

PRSC, +25,0%

TTLC, +33,6%

CABC, +36,3%

UNXC, +50,0%

-‐15,0% -‐5,0% 5,0% 15,0% 25,0% 35,0% 45,0%

WAEMU NEWS • Is Côte d’Ivoire headed for a new record in cocoa producYon? The country which last season registered the best crop of brown gold in its history with a producYon of 1.74 million tons could sYll surpass that. “I know we had an iniYal forecast of producing 1.6 million tons, but at present we expect to be at the same level as last year”, a member of the Ivorian Ministry of Finance who requested anonymity told Reuters. The country had already received 1,347,944 tons at its ports by end of April and could increase the price of the product in the next agricultural season if good sales conYnue. Thus, farmers could earn XOF 900 per kilogram of beans against 850 francs currently. If the trend conYnues, this Ivorian success would take place in a context where its neighbor and rival cocoa producer Ghana would encounter difficulYes with its producYon. The country has revised its forecast harvest and expects to produce about 700,000 tons, 20% less than expected. These grim prospects seem to confirm the risk of a global cocoa producYon deficit. It remains to be seen whether with this new record, Côte d’Ivoire may somewhat offset the low Ghanaian producYon. At this rate, Côte d’Ivoire could soon surpass 2 million tons, a level of producYon that could be unfavorable to the country according to Jean-‐Marc Anga, execuYve director of the InternaYonal Cocoa OrganisaYon (ICCO). source: Agence Ecofin

• Canadian company Enerdynamic Hybrid Technologies (EHT) announced it was awarded a USD 500,000 contract to build 87 Micro-‐UYlity systems in Senegal. EHT will supply up to 2 KilowaXs of power for each installaYon including baXery storage that will be deployed on the roodops of exisYng housing units which require an independent power source. “EHT provides a superior Micro-‐UYlity soluYon that we can deploy across our housing projects in Africa and regions where off-‐grid energy soluYons are most needed. We look forward to growing our business relaYonship with EHT across Africa and North America” said Roman Eder, President of the German firm IQ Engineering, the project sponsor. The construcYon of these mini-‐grids is expected to begin within two months and to be completed in the fourth quarter of 2015. EHT will be paid on commercial terms with 50% payable on delivery of equipment to Senegal and 50% on the compleYon of construcYon. source: Agence Ecofin

• Côte d’Ivoire could raise its palm oil producYon from 400,000 tonnes to 600,000 tonnes within the next 5 years, according to Alexis Kemanhon, director of the extension and renewal fund for the development of palm oil culYvaYon. This producYon increase should be done under the “3rd palm tree plan” implementaYon framework. Today, Côte d’Ivoire is the 2nd largest African palm oil producer (1.8 million tons / year) ader Nigeria and has been able to reach this level thanks to two palm oil plans executed between 1962 to 1983 and 1985 to 1990. These iniYaYves have led to the creaYon of 150,000 hectares of plantaYons. The palm oil industry employs 2 million people and generates revenues of around one billion dollars. Côte d’Ivoire aims to go further. “The 3rd palm plan aims to increase producYon by over 50% to fight against poverty in rural areas, improve and diversify smallholder income and create new development hubs in areas with high potenYal,” Alexis told Kemanhon Xinhua. source: Agence Ecofin

• Air Côte d’Ivoire has announced an investment of USD 200 million over the next two years. This amount will be used to acquire three Airbus A319 that will enable the company to establish itself regionally. Loukou Laurent, CEO of Air Côte d’Ivoire, told Reuters: “We want to consolidate our posiYon and establish ourselves in West and Central Africa over the next two years.”. The investment announcement comes ader Air Côte d’Ivoire commiXed earlier this month to acquiring two Q400 aircrads from the Canadian company Bombardier Inc. Air Côte d’Ivoire, which is owned at 65% by the Ivorian government, 20% by Air France and 15% naYonal investor Goldenrod, expects to see its turnover reach XOF 70 billion this year and XOF 100 billion in 2016. source: Agence Ecofin

• The remarks were made by Mr Emmanuel Nnadozie, the execuYve secretary of Africa Capacity Development FoundaYon, at the 50th anniversary celebraYon of the African Development Bank (AfDB) in Abidjan-‐ Ivory Coast. Speaking at the bank’s annual meeYngs which started on Monday and end today in Abidjan-‐ Ivory Coast, Mr Nnadozie, said if African countries strengthened their tax collecYon capaciYes, as much as USD 500 million can be mobilised. Mr Nnadozie said instead of looking to raise financing for development from outside their countries, African countries should locally raise their resources through the stock market, and sovereign bond market. Bank governors, finance and economy ministers are among the delegates who have will review the bank’s 2014 operaYons and its 2015 development funding poruolio. They will highlight challenges facing Africa in key areas such as climate change, infrastructure, private sector and governance. source: Daily Monitor, Uganda

Contact: yakhoub.niang@impaxis-‐securities.com

Limite de Responsabilité: Les informations contenues dans le présent rapport ont été compilées par Impaxis Securities à partir de sources considérées comme fiables, mais aucune représentation ou garantie, expresse ou implicite, n’est faite par Impaxis Securities ou toute autre personne quant à son exactitude, exhaustivité ou exactitude. Toutes les opinions et les estimations contenues dans le présent rapport relèvent du jugement d’Impaxis Securities, jugement à la date du présent rapport, et sont sujettes à modification sans préavis et sont fournies de bonne foi mais sans responsabilité légale. Ce rapport ne constitue pas une offre de vente ni de sollicitation d'une offre d'achat de valeurs mobilières, ou à faire des investissements. Les performances passées ne préjugent pas des performances futures, les rendements futurs ne sont pas garantis, et une perte du capital initial peut se produire. Aucun élément contenu dans ce document ne peut être reproduit ou copié par n’importe quel moyen, sans le consentement préalable d’Impaxis Securities. Veuillez contacter Impaxis Securities en cas de questions.

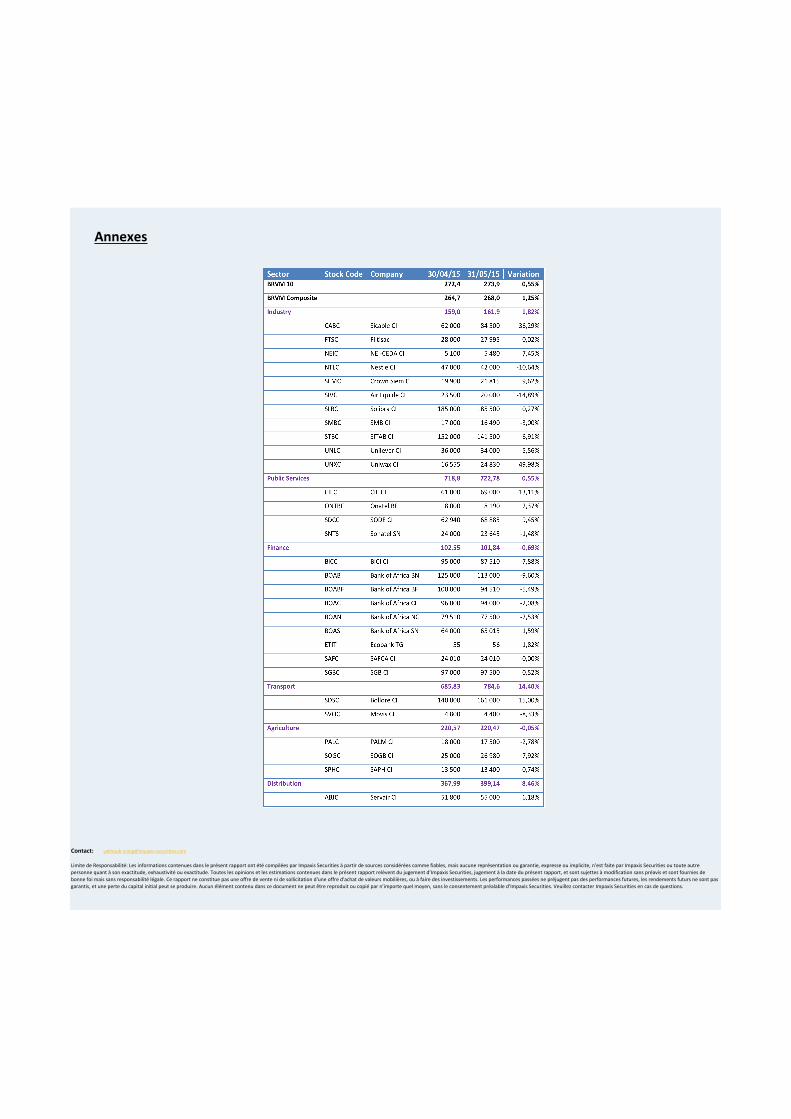

Annexes