Embed Size (px)

Citation preview

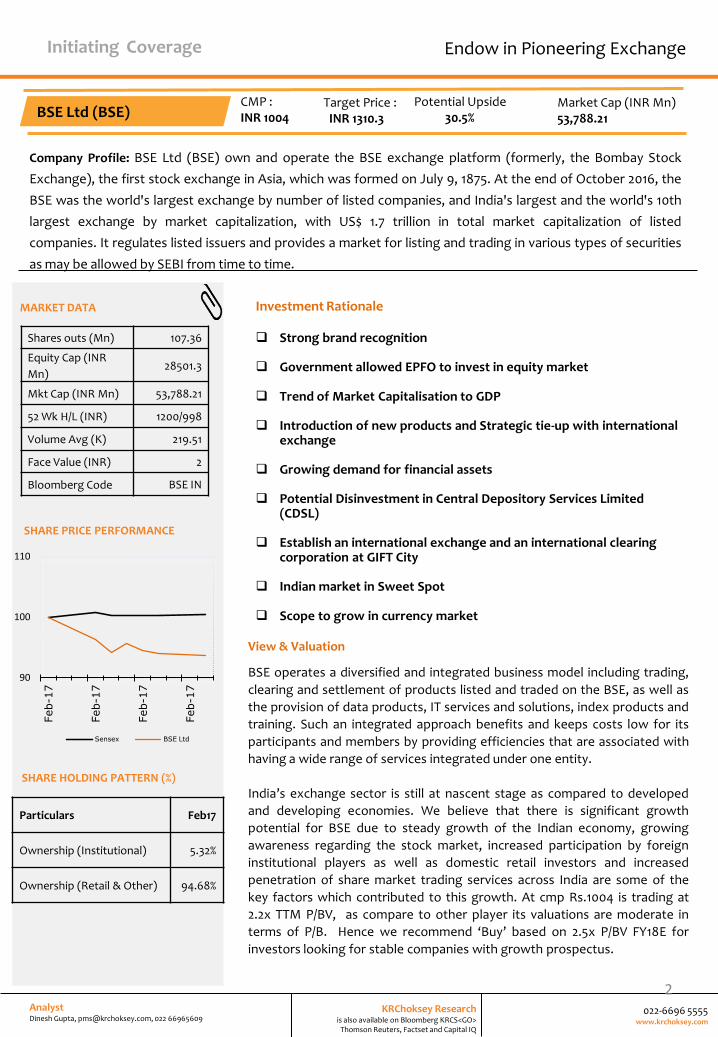

BSE Ltd (BSE)

15th February, 2017

Endow in Pioneering Exchange

Company Profile: BSE Ltd (BSE) own and operate the BSE exchange platform (formerly, the Bombay Stock

Exchange), the first stock exchange in Asia, which was formed on July 9, 1875. At the end of October 2016, the

BSE was the world's largest exchange by number of listed companies, and India's largest and the world's 10th

largest exchange by market capitalization, with US$ 1.7 trillion in total market capitalization of listed

companies. It regulates listed issuers and provides a market for listing and trading in various types of securities

as may be allowed by SEBI from time to time.

Target Price : INR 1310.3

Potential Upside 30.5%

CMP : INR 1004

Market Cap (INR Mn) 53,788.21

022-6696 5555 www.krchoksey.com

KRChoksey Research is also available on Bloomberg KRCS<GO>

Thomson Reuters, Factset and Capital IQ

Analyst Dinesh Gupta, [email protected], 022 66965609

Shares outs (Mn) 107.36

Equity Cap (INR

Mn) 28501.3

Mkt Cap (INR Mn) 53,788.21

52 Wk H/L (INR) 1200/998

Volume Avg (K) 219.51

Face Value (INR) 2

Bloomberg Code BSE IN

MARKET DATA

SHARE PRICE PERFORMANCE

SHARE HOLDING PATTERN (%)

BSE Ltd (BSE)

Investment Rationale Strong brand recognition

Government allowed EPFO to invest in equity market

Trend of Market Capitalisation to GDP

Introduction of new products and Strategic tie-up with international

exchange

Growing demand for financial assets

Potential Disinvestment in Central Depository Services Limited (CDSL)

Establish an international exchange and an international clearing corporation at GIFT City

Indian market in Sweet Spot

Scope to grow in currency market

View & Valuation

BSE operates a diversified and integrated business model including trading,

clearing and settlement of products listed and traded on the BSE, as well as

the provision of data products, IT services and solutions, index products and

training. Such an integrated approach benefits and keeps costs low for its

participants and members by providing efficiencies that are associated with

having a wide range of services integrated under one entity.

India’s exchange sector is still at nascent stage as compared to developed

and developing economies. We believe that there is significant growth

potential for BSE due to steady growth of the Indian economy, growing

awareness regarding the stock market, increased participation by foreign

institutional players as well as domestic retail investors and increased

penetration of share market trading services across India are some of the

key factors which contributed to this growth. At cmp Rs.1004 is trading at

2.2x TTM P/BV, as compare to other player its valuations are moderate in

terms of P/B. Hence we recommend ‘Buy’ based on 2.5x P/BV FY18E for

investors looking for stable companies with growth prospectus.

2

90

100

110

Feb-1

7

Feb-1

7

Feb-1

7

Feb-1

7

Sensex BSE Ltd

Particulars Feb17

Ownership (Institutional) 5.32%

Ownership (Retail & Other) 94.68%

Endow in Pioneering Exchange Initiating Coverage

Source – BSE RHP, KRChoskey PMS research

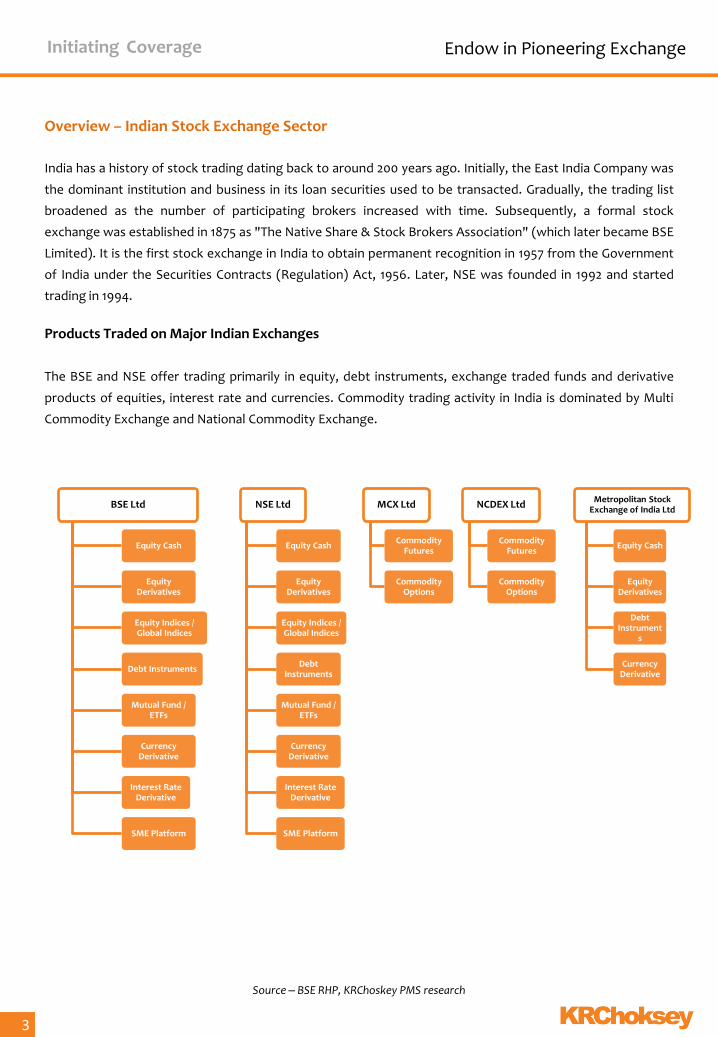

Overview – Indian Stock Exchange Sector

India has a history of stock trading dating back to around 200 years ago. Initially, the East India Company was

the dominant institution and business in its loan securities used to be transacted. Gradually, the trading list

broadened as the number of participating brokers increased with time. Subsequently, a formal stock

exchange was established in 1875 as "The Native Share & Stock Brokers Association" (which later became BSE

Limited). It is the first stock exchange in India to obtain permanent recognition in 1957 from the Government

of India under the Securities Contracts (Regulation) Act, 1956. Later, NSE was founded in 1992 and started

trading in 1994.

Products Traded on Major Indian Exchanges

The BSE and NSE offer trading primarily in equity, debt instruments, exchange traded funds and derivative

products of equities, interest rate and currencies. Commodity trading activity in India is dominated by Multi

Commodity Exchange and National Commodity Exchange.

BSE Ltd

Equity Cash

Equity Derivatives

Equity Indices / Global Indices

Debt Instruments

Mutual Fund / ETFs

Currency Derivative

Interest Rate Derivative

SME Platform

NSE Ltd

Equity Cash

Equity Derivatives

Equity Indices / Global Indices

Debt Instruments

Mutual Fund / ETFs

Currency Derivative

Interest Rate Derivative

SME Platform

MCX Ltd

Commodity Futures

Commodity Options

NCDEX Ltd

Commodity Futures

Commodity Options

Metropolitan Stock Exchange of India Ltd

Equity Cash

Equity Derivatives

Debt Instrument

s

Currency Derivative

3

Initiating Coverage Endow in Pioneering Exchange

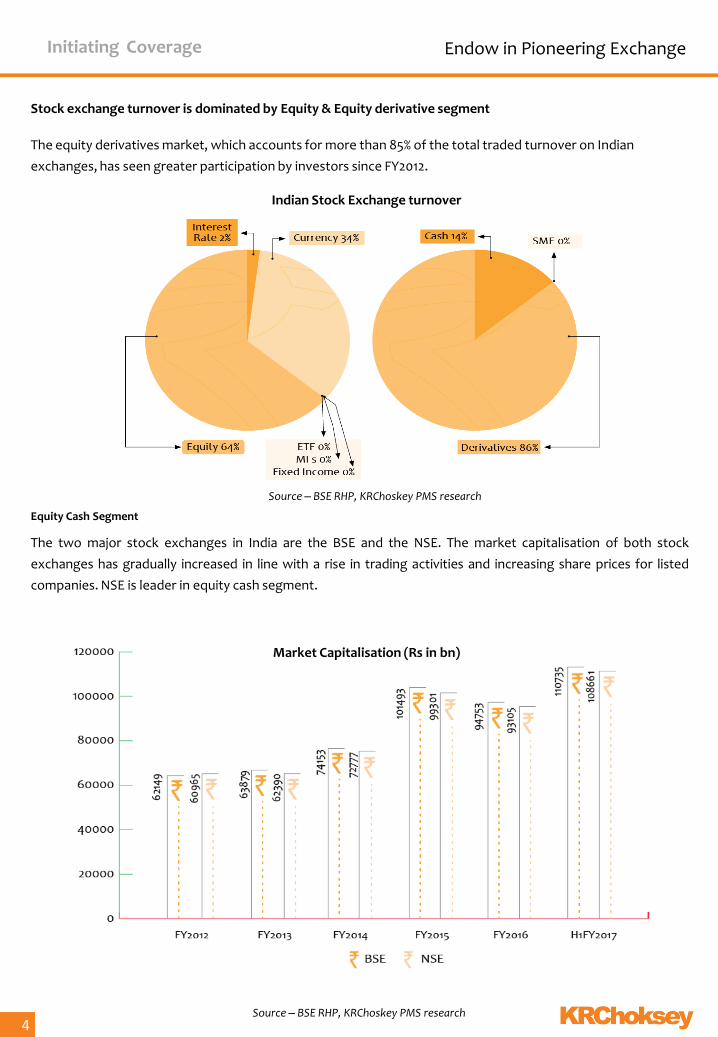

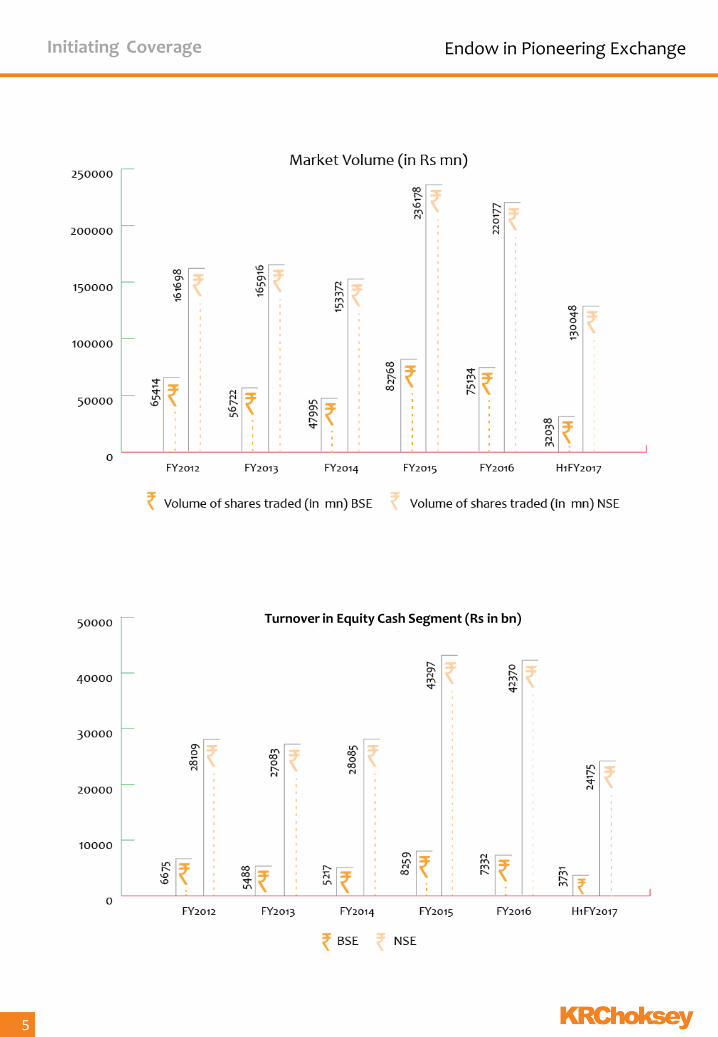

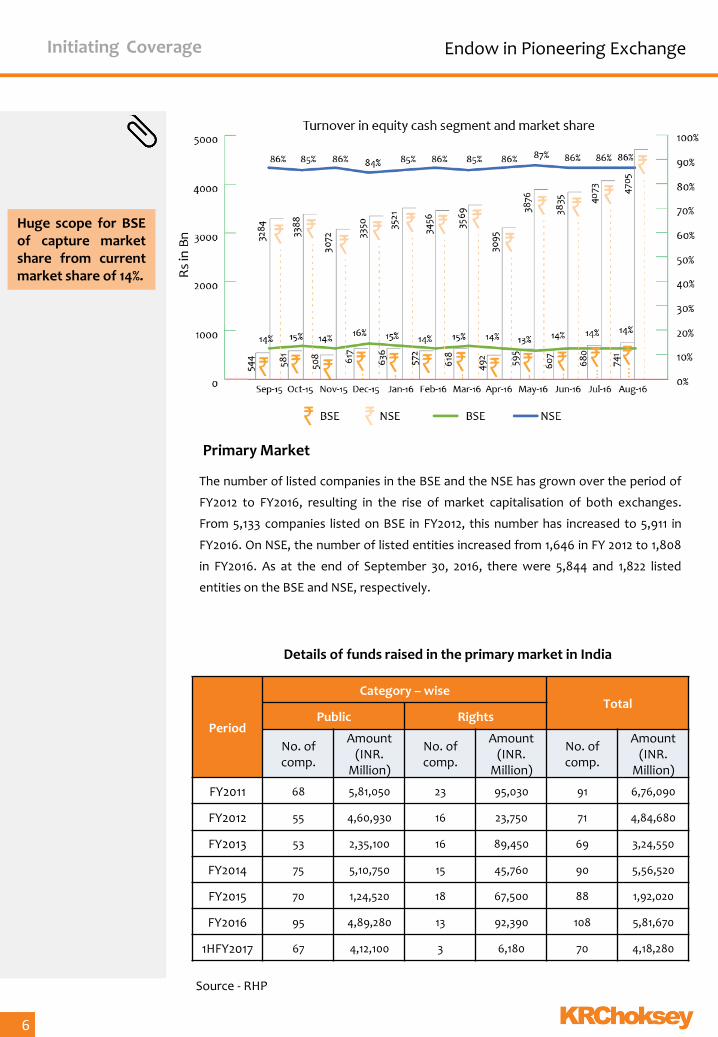

Stock exchange turnover is dominated by Equity & Equity derivative segment

The equity derivatives market, which accounts for more than 85% of the total traded turnover on Indian

exchanges, has seen greater participation by investors since FY2012.

Equity Cash Segment

The two major stock exchanges in India are the BSE and the NSE. The market capitalisation of both stock

exchanges has gradually increased in line with a rise in trading activities and increasing share prices for listed

companies. NSE is leader in equity cash segment.

Source – BSE RHP, KRChoskey PMS research 4

Market Capitalisation (Rs in bn)

Initiating Coverage Endow in Pioneering Exchange

Indian Stock Exchange turnover

Source – BSE RHP, KRChoskey PMS research

5

Turnover in Equity Cash Segment (Rs in bn)

Initiating Coverage Endow in Pioneering Exchange

Investment Rationale

The number of listed companies in the BSE and the NSE has grown over the period of

FY2012 to FY2016, resulting in the rise of market capitalisation of both exchanges.

From 5,133 companies listed on BSE in FY2012, this number has increased to 5,911 in

FY2016. On NSE, the number of listed entities increased from 1,646 in FY 2012 to 1,808

in FY2016. As at the end of September 30, 2016, there were 5,844 and 1,822 listed

entities on the BSE and NSE, respectively.

Source - RHP

Period

Category – wise Total

Public Rights

No. of comp.

Amount (INR.

Million)

No. of comp.

Amount (INR.

Million)

No. of comp.

Amount (INR.

Million)

FY2011 68 5,81,050 23 95,030 91 6,76,090

FY2012 55 4,60,930 16 23,750 71 4,84,680

FY2013 53 2,35,100 16 89,450 69 3,24,550

FY2014 75 5,10,750 15 45,760 90 5,56,520

FY2015 70 1,24,520 18 67,500 88 1,92,020

FY2016 95 4,89,280 13 92,390 108 5,81,670

1HFY2017 67 4,12,100 3 6,180 70 4,18,280

Details of funds raised in the primary market in India

6

Primary Market

Huge scope for BSE of capture market share from current market share of 14%.

Initiating Coverage Endow in Pioneering Exchange

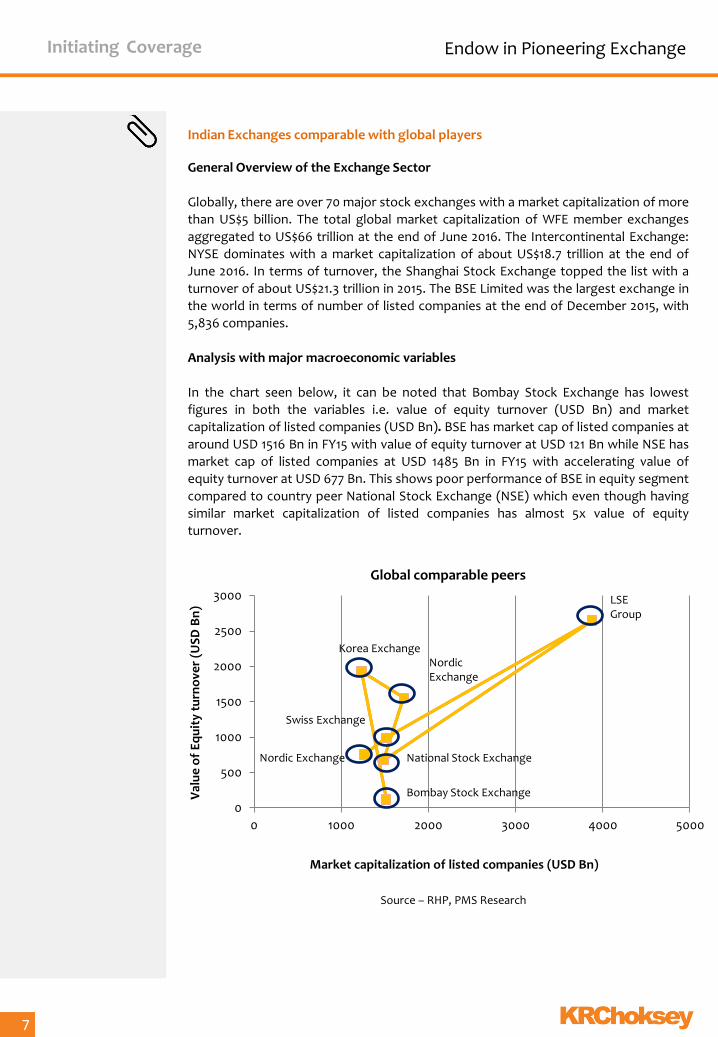

Indian Exchanges comparable with global players General Overview of the Exchange Sector

Globally, there are over 70 major stock exchanges with a market capitalization of more

than US$5 billion. The total global market capitalization of WFE member exchanges

aggregated to US$66 trillion at the end of June 2016. The Intercontinental Exchange:

NYSE dominates with a market capitalization of about US$18.7 trillion at the end of

June 2016. In terms of turnover, the Shanghai Stock Exchange topped the list with a

turnover of about US$21.3 trillion in 2015. The BSE Limited was the largest exchange in

the world in terms of number of listed companies at the end of December 2015, with

5,836 companies.

Analysis with major macroeconomic variables

In the chart seen below, it can be noted that Bombay Stock Exchange has lowest

figures in both the variables i.e. value of equity turnover (USD Bn) and market

capitalization of listed companies (USD Bn). BSE has market cap of listed companies at

around USD 1516 Bn in FY15 with value of equity turnover at USD 121 Bn while NSE has

market cap of listed companies at USD 1485 Bn in FY15 with accelerating value of

equity turnover at USD 677 Bn. This shows poor performance of BSE in equity segment

compared to country peer National Stock Exchange (NSE) which even though having

similar market capitalization of listed companies has almost 5x value of equity

turnover.

Investment Rationale

7

0

500

1000

1500

2000

2500

3000

0 1000 2000 3000 4000 5000

Val

ue

of

Eq

uit

y tu

rno

ver

(US

D B

n)

Market capitalization of listed companies (USD Bn)

Global comparable peers

LSE Group

National Stock Exchange Nordic Exchange

Bombay Stock Exchange

Swiss Exchange

Nordic Exchange

Korea Exchange

Source – RHP, PMS Research

Initiating Coverage Endow in Pioneering Exchange

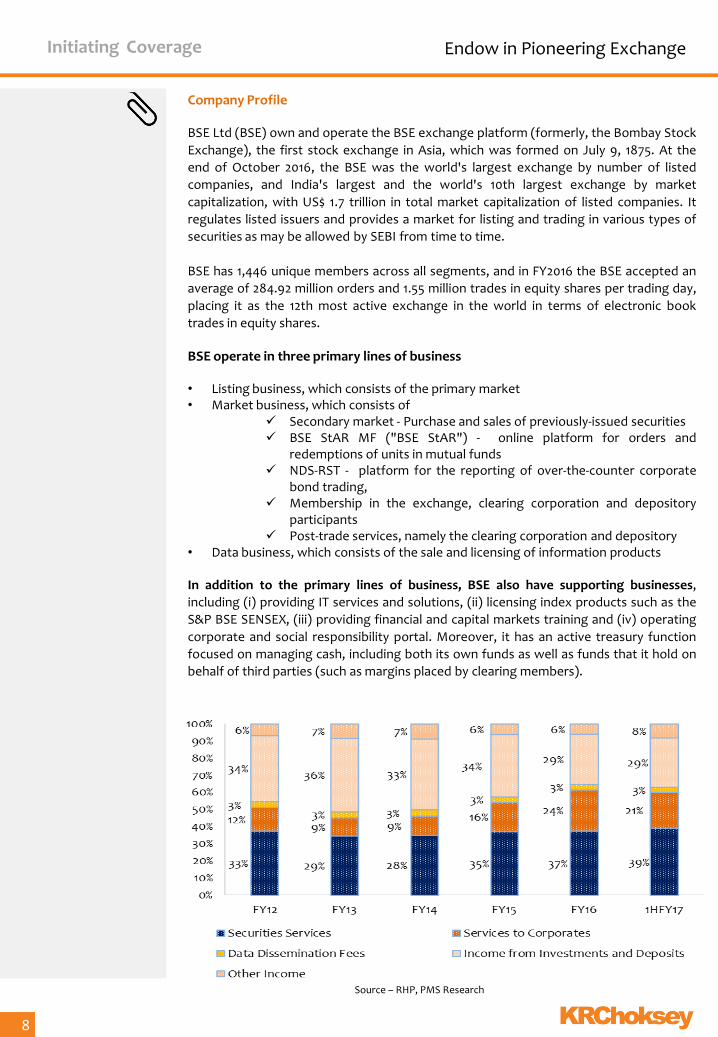

Company Profile BSE Ltd (BSE) own and operate the BSE exchange platform (formerly, the Bombay Stock

Exchange), the first stock exchange in Asia, which was formed on July 9, 1875. At the

end of October 2016, the BSE was the world's largest exchange by number of listed

companies, and India's largest and the world's 10th largest exchange by market

capitalization, with US$ 1.7 trillion in total market capitalization of listed companies. It

regulates listed issuers and provides a market for listing and trading in various types of

securities as may be allowed by SEBI from time to time.

BSE has 1,446 unique members across all segments, and in FY2016 the BSE accepted an

average of 284.92 million orders and 1.55 million trades in equity shares per trading day,

placing it as the 12th most active exchange in the world in terms of electronic book

trades in equity shares.

BSE operate in three primary lines of business • Listing business, which consists of the primary market • Market business, which consists of

Secondary market - Purchase and sales of previously-issued securities BSE StAR MF ("BSE StAR") - online platform for orders and

redemptions of units in mutual funds NDS-RST - platform for the reporting of over-the-counter corporate

bond trading, Membership in the exchange, clearing corporation and depository

participants Post-trade services, namely the clearing corporation and depository

• Data business, which consists of the sale and licensing of information products

In addition to the primary lines of business, BSE also have supporting businesses,

including (i) providing IT services and solutions, (ii) licensing index products such as the

S&P BSE SENSEX, (iii) providing financial and capital markets training and (iv) operating

corporate and social responsibility portal. Moreover, it has an active treasury function

focused on managing cash, including both its own funds as well as funds that it hold on

behalf of third parties (such as margins placed by clearing members).

Source – RHP, PMS Research

Investment Rationale

8

Initiating Coverage Endow in Pioneering Exchange

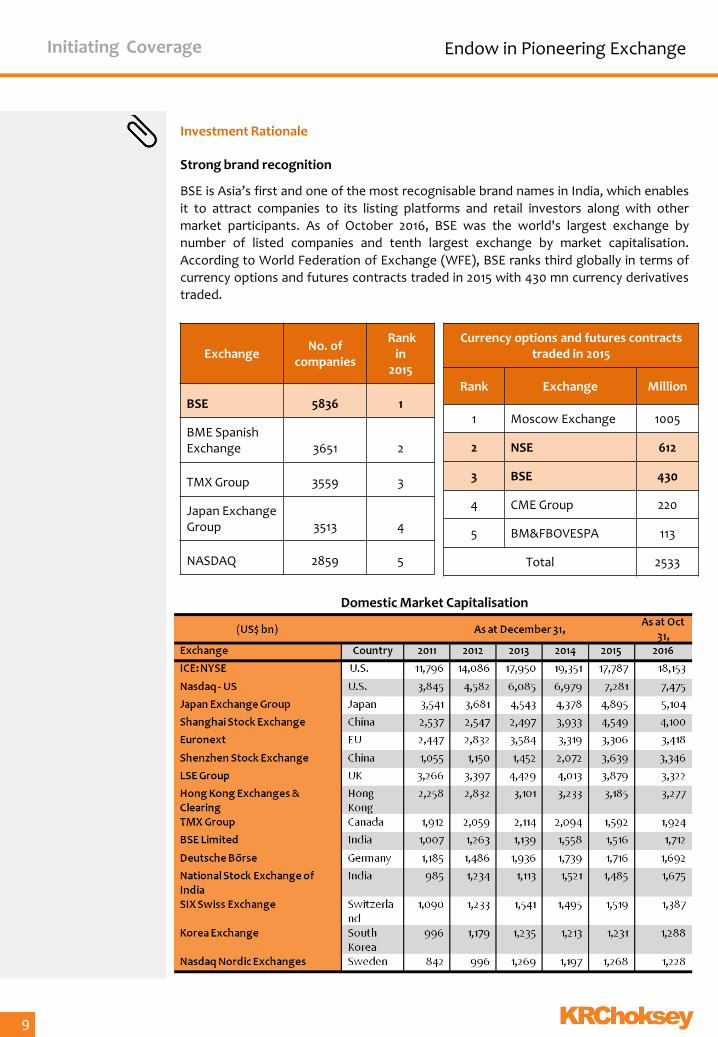

Investment Rationale Strong brand recognition

BSE is Asia’s first and one of the most recognisable brand names in India, which enables

it to attract companies to its listing platforms and retail investors along with other

market participants. As of October 2016, BSE was the world's largest exchange by

number of listed companies and tenth largest exchange by market capitalisation.

According to World Federation of Exchange (WFE), BSE ranks third globally in terms of

currency options and futures contracts traded in 2015 with 430 mn currency derivatives

traded.

Investment Rationale

9

Exchange No. of

companies

Rank in

2015

BSE 5836 1

BME Spanish Exchange 3651 2

TMX Group 3559 3

Japan Exchange Group 3513 4

NASDAQ 2859 5

Currency options and futures contracts traded in 2015

Rank Exchange Million

1 Moscow Exchange 1005

2 NSE 612

3 BSE 430

4 CME Group 220

5 BM&FBOVESPA 113

Total 2533

Domestic Market Capitalisation

Initiating Coverage Endow in Pioneering Exchange

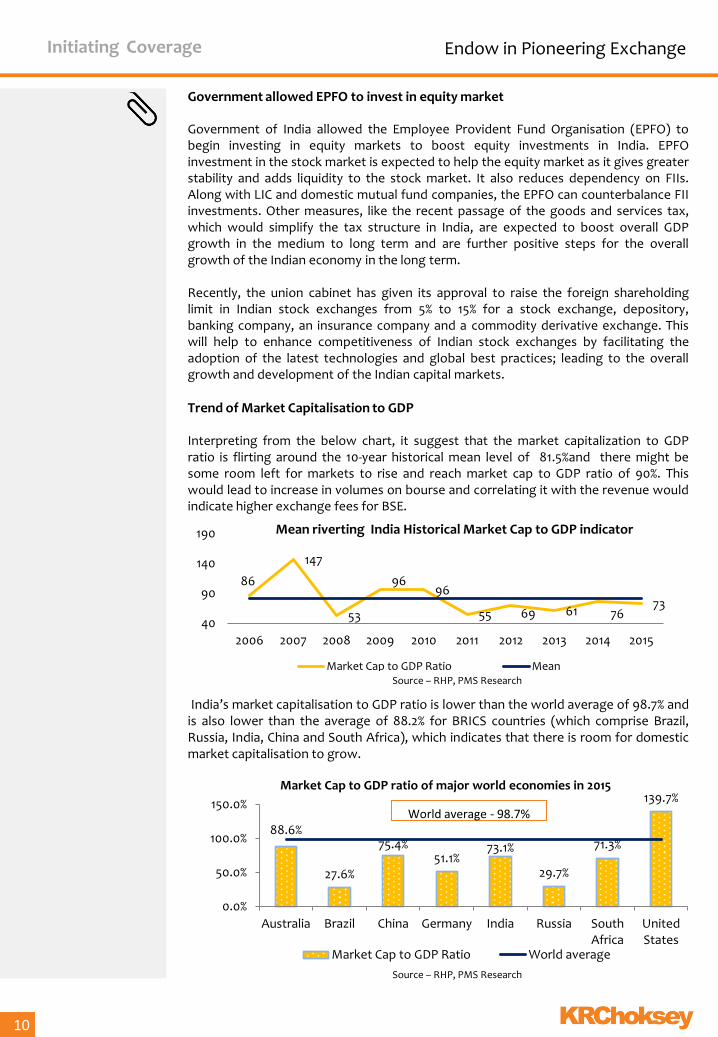

Government allowed EPFO to invest in equity market Government of India allowed the Employee Provident Fund Organisation (EPFO) to begin investing in equity markets to boost equity investments in India. EPFO investment in the stock market is expected to help the equity market as it gives greater stability and adds liquidity to the stock market. It also reduces dependency on FIIs. Along with LIC and domestic mutual fund companies, the EPFO can counterbalance FII investments. Other measures, like the recent passage of the goods and services tax, which would simplify the tax structure in India, are expected to boost overall GDP growth in the medium to long term and are further positive steps for the overall growth of the Indian economy in the long term. Recently, the union cabinet has given its approval to raise the foreign shareholding limit in Indian stock exchanges from 5% to 15% for a stock exchange, depository, banking company, an insurance company and a commodity derivative exchange. This will help to enhance competitiveness of Indian stock exchanges by facilitating the adoption of the latest technologies and global best practices; leading to the overall growth and development of the Indian capital markets. Trend of Market Capitalisation to GDP Interpreting from the below chart, it suggest that the market capitalization to GDP ratio is flirting around the 10-year historical mean level of 81.5%and there might be some room left for markets to rise and reach market cap to GDP ratio of 90%. This would lead to increase in volumes on bourse and correlating it with the revenue would indicate higher exchange fees for BSE.

Source – RHP, PMS Research

Investment Rationale

10

86

147

53

96 96

55 69 61 76 73

40

90

140

190

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Mean riverting India Historical Market Cap to GDP indicator

Market Cap to GDP Ratio Mean

88.6%

27.6%

75.4% 51.1%

73.1%

29.7%

71.3%

139.7%

0.0%

50.0%

100.0%

150.0%

Australia Brazil China Germany India Russia South Africa

United States

Market Cap to GDP ratio of major world economies in 2015

Market Cap to GDP Ratio World average

World average - 98.7%

India’s market capitalisation to GDP ratio is lower than the world average of 98.7% and is also lower than the average of 88.2% for BRICS countries (which comprise Brazil, Russia, India, China and South Africa), which indicates that there is room for domestic market capitalisation to grow.

Source – RHP, PMS Research

Initiating Coverage Endow in Pioneering Exchange

Introduction of new products and Strategic tie-up with international exchange BSE continually strive to diversify its product and service offerings to serve investors'

needs by developing new products and bringing new types of financial instruments.

Even though stock exchanges in India have seen business growth in the past, there

are product gaps which exist in certain segments. There is room to introduce

innovative derivative products like weather derivatives, energy derivatives and credit

derivatives, which are currently traded in major exchanges worldwide. The availability

of such new products would bring additional business volumes on the exchanges.

BSE is expanding its overseas presence through strategic alliances. It entered into

strategic partnership with S&P Dow Jones Indices LLC (USA) to grow its index

business by licensing its index products. Further, BSE has signed agreement with

Deutsche Börse to sell and market BSE market data and information to global clients.

It is also a member of BRICS Exchanges Alliance, whereby leading exchanges in the

member counties (Brazil, Russia, India, China & South Africa) cross-list futures

products based on the flagship indices of each of the other exchanges.

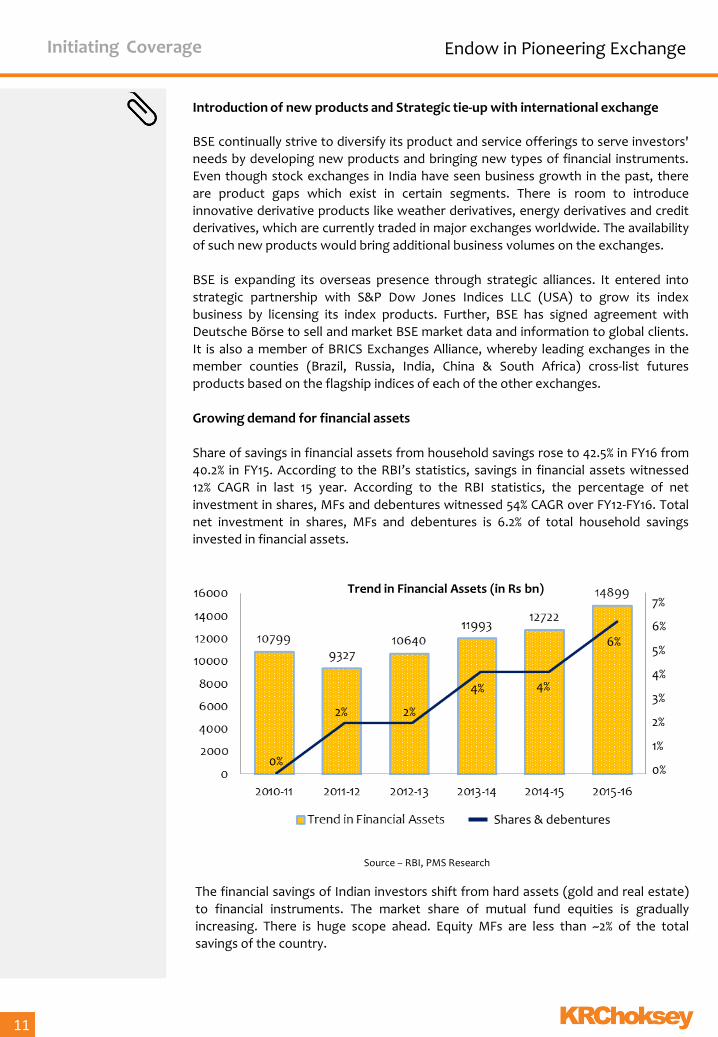

Growing demand for financial assets Share of savings in financial assets from household savings rose to 42.5% in FY16 from

40.2% in FY15. According to the RBI’s statistics, savings in financial assets witnessed

12% CAGR in last 15 year. According to the RBI statistics, the percentage of net

investment in shares, MFs and debentures witnessed 54% CAGR over FY12-FY16. Total

net investment in shares, MFs and debentures is 6.2% of total household savings

invested in financial assets.

Source – RBI, PMS Research

The financial savings of Indian investors shift from hard assets (gold and real estate)

to financial instruments. The market share of mutual fund equities is gradually

increasing. There is huge scope ahead. Equity MFs are less than ~2% of the total

savings of the country.

Investment Rationale

11

Shares & debentures

7%

6%

5%

4%

3%

2%

1%

0% 0%

2% 2%

4% 4%

6%

Trend in Financial Assets (in Rs bn)

Initiating Coverage Endow in Pioneering Exchange

Potential Disinvestment in Central Depository Services Limited (CDSL) BSE has divested a 4.15% stake in CDSL to LIC at Rs 78.93 per share aggregating to Rs.

342.3 mn valuing it Rs 8248.1 mn, currently hold 54.2% stake in CDSL. Pursuant to

Indian law, effective April 1, 2017 stock exchanges will be prohibited from holding

more than a 24.0% stake in depositories, as a result of which BSE is required to divest

26.05% of stake in CDSL. The disinvestment of stake in CDSL will significantly impact

revenue.

Establish an international exchange and an international clearing corporation at GIFT City BSE to investing about ~Rs 500 crore in the international exchange over the next

three years, International exchange in GIFT City (Ahmadabad) may turn into major

success due to first-mover advantage. Establishing this exchange will increase BSE’s

brand's profile and also provide with additional sources of revenue. BSE intends to

offer across equity and index derivatives, currency derivatives and commodities in

foreign currency. It will also offer interest rate futures, fixed income securities and

provide an electronic trading platform.

The exchange will be a beneficiary of several tax sops, including exemptions from

stamp duty, service tax, dividend distribution tax, as well as commodity and securities

transaction tax (STT). STT is one of the biggest sore points for investors participating

in derivatives trading and the new exchange will eliminate that. A lot of Indian traders

dealing in equity derivatives from Singapore and Dubai may be tempted to set up

desks here. At present, sellers of options contracts have to pay an STT of 0.05 per

cent on the premium value. In addition, STT on buying options that get exercised is

0.125 per cent of the entire contract value. For futures contracts, sellers have to pay

an STT of 0.01 per cent.

Indian market in Sweet Spot

India is in sweet spot and one of the preferred global investment destinations given

its macro-economic stability, long-term growth prospects and ongoing economic and

social reforms. With India's GDP growing at a rate of 7% to 8% in the current financial

year, India is one of the fastest growing economies in the world compared to the

relatively muted growth of other major global economies. We expect the growth of

the Indian economy to attract foreign investments in coming years. Global events

such as Brexit are also expected to attract new investors to India given slower growth

in the European continent. Given the rise in the Indian capital markets, 269 new

Foreign Portfolio Investors ("FPIs") registered with SEBI in April 2016.

Investment Rationale

12

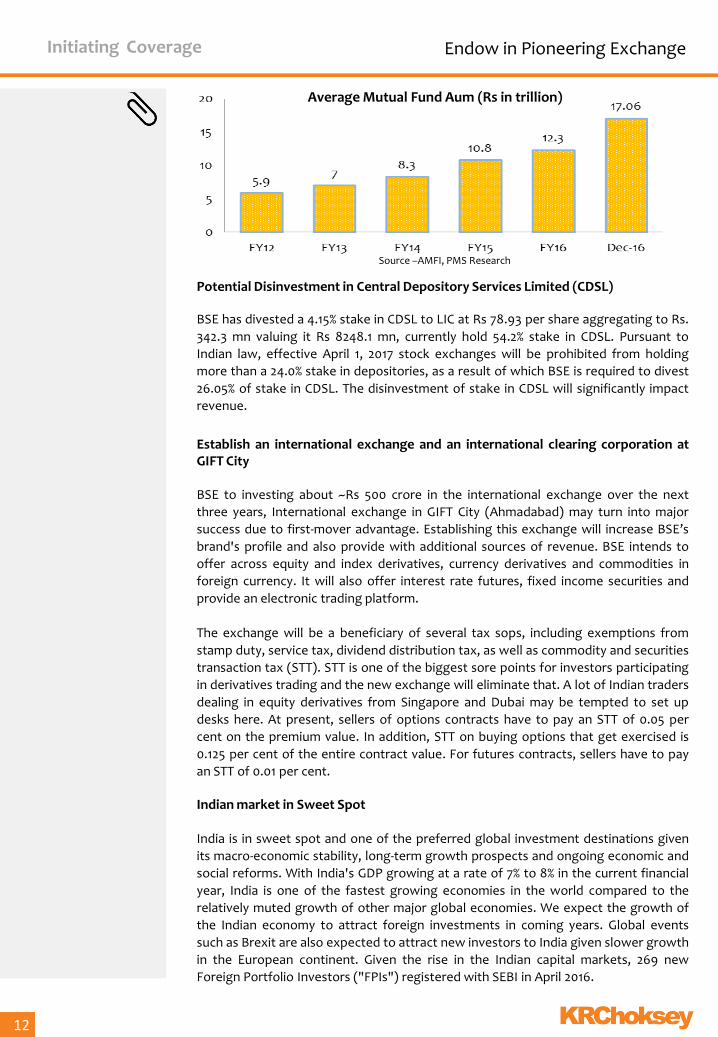

Source –AMFI, PMS Research

Average Mutual Fund Aum (Rs in trillion)

Initiating Coverage Endow in Pioneering Exchange

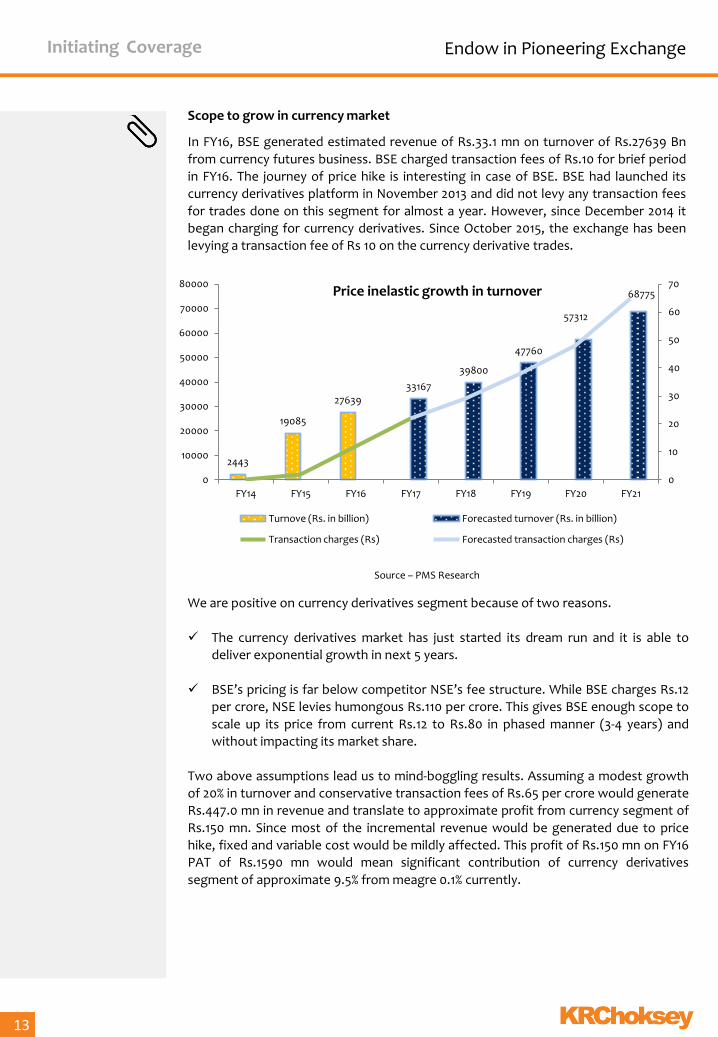

Scope to grow in currency market

In FY16, BSE generated estimated revenue of Rs.33.1 mn on turnover of Rs.27639 Bn

from currency futures business. BSE charged transaction fees of Rs.10 for brief period

in FY16. The journey of price hike is interesting in case of BSE. BSE had launched its

currency derivatives platform in November 2013 and did not levy any transaction fees

for trades done on this segment for almost a year. However, since December 2014 it

began charging for currency derivatives. Since October 2015, the exchange has been

levying a transaction fee of Rs 10 on the currency derivative trades.

Source – PMS Research

We are positive on currency derivatives segment because of two reasons.

The currency derivatives market has just started its dream run and it is able to

deliver exponential growth in next 5 years.

BSE’s pricing is far below competitor NSE’s fee structure. While BSE charges Rs.12

per crore, NSE levies humongous Rs.110 per crore. This gives BSE enough scope to

scale up its price from current Rs.12 to Rs.80 in phased manner (3-4 years) and

without impacting its market share.

Two above assumptions lead us to mind-boggling results. Assuming a modest growth

of 20% in turnover and conservative transaction fees of Rs.65 per crore would generate

Rs.447.0 mn in revenue and translate to approximate profit from currency segment of

Rs.150 mn. Since most of the incremental revenue would be generated due to price

hike, fixed and variable cost would be mildly affected. This profit of Rs.150 mn on FY16

PAT of Rs.1590 mn would mean significant contribution of currency derivatives

segment of approximate 9.5% from meagre 0.1% currently.

Investment Rationale

13

2443

19085

27639

33167

39800

47760

57312

68775

0

10

20

30

40

50

60

70

0

10000

20000

30000

40000

50000

60000

70000

80000

FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21

Turnove (Rs. in billion) Forecasted turnover (Rs. in billion)

Transaction charges (Rs) Forecasted transaction charges (Rs)

Price inelastic growth in turnover

Initiating Coverage Endow in Pioneering Exchange

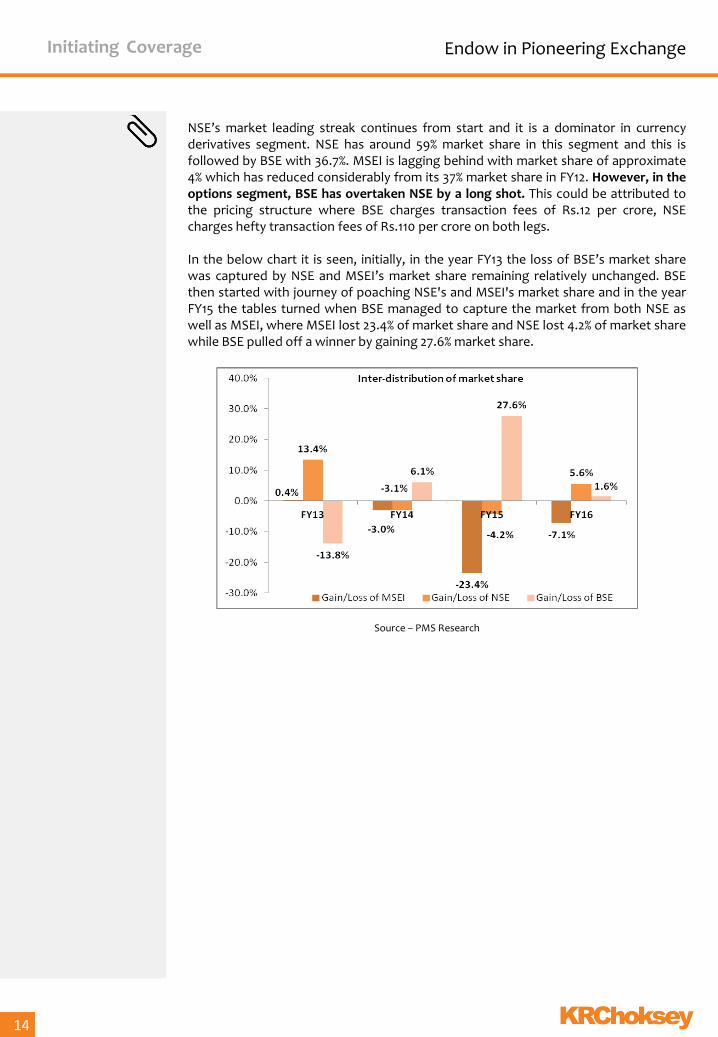

NSE’s market leading streak continues from start and it is a dominator in currency derivatives segment. NSE has around 59% market share in this segment and this is followed by BSE with 36.7%. MSEI is lagging behind with market share of approximate 4% which has reduced considerably from its 37% market share in FY12. However, in the options segment, BSE has overtaken NSE by a long shot. This could be attributed to the pricing structure where BSE charges transaction fees of Rs.12 per crore, NSE charges hefty transaction fees of Rs.110 per crore on both legs. In the below chart it is seen, initially, in the year FY13 the loss of BSE’s market share was captured by NSE and MSEI’s market share remaining relatively unchanged. BSE then started with journey of poaching NSE's and MSEI's market share and in the year FY15 the tables turned when BSE managed to capture the market from both NSE as well as MSEI, where MSEI lost 23.4% of market share and NSE lost 4.2% of market share while BSE pulled off a winner by gaining 27.6% market share.

Investment Rationale

14

Initiating Coverage Endow in Pioneering Exchange

Source – PMS Research

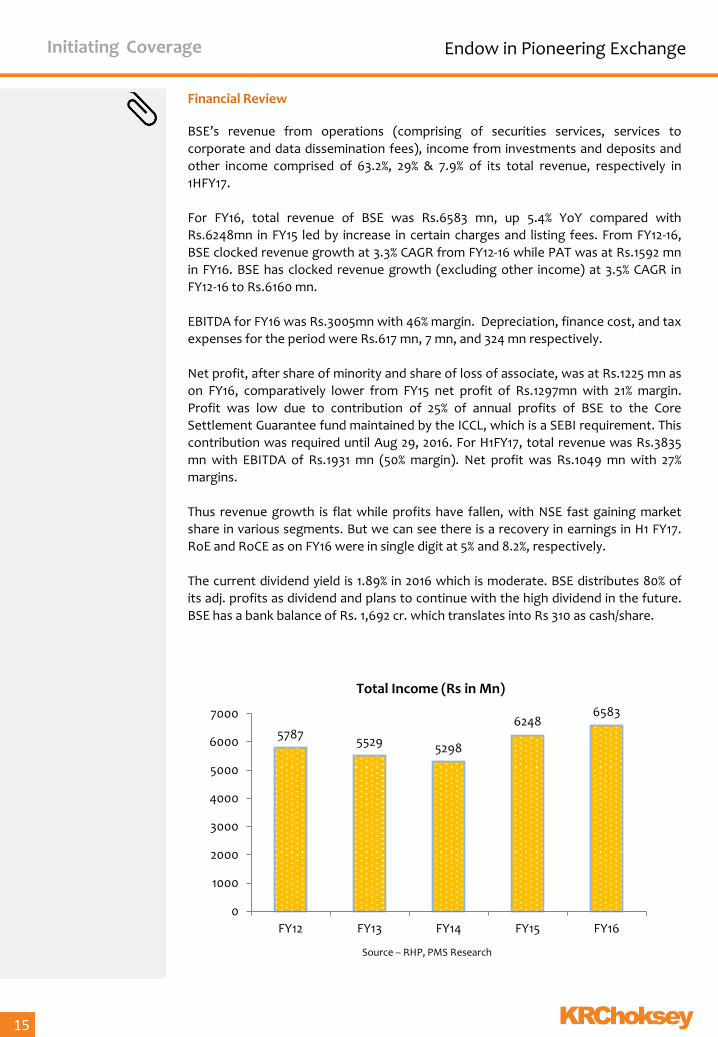

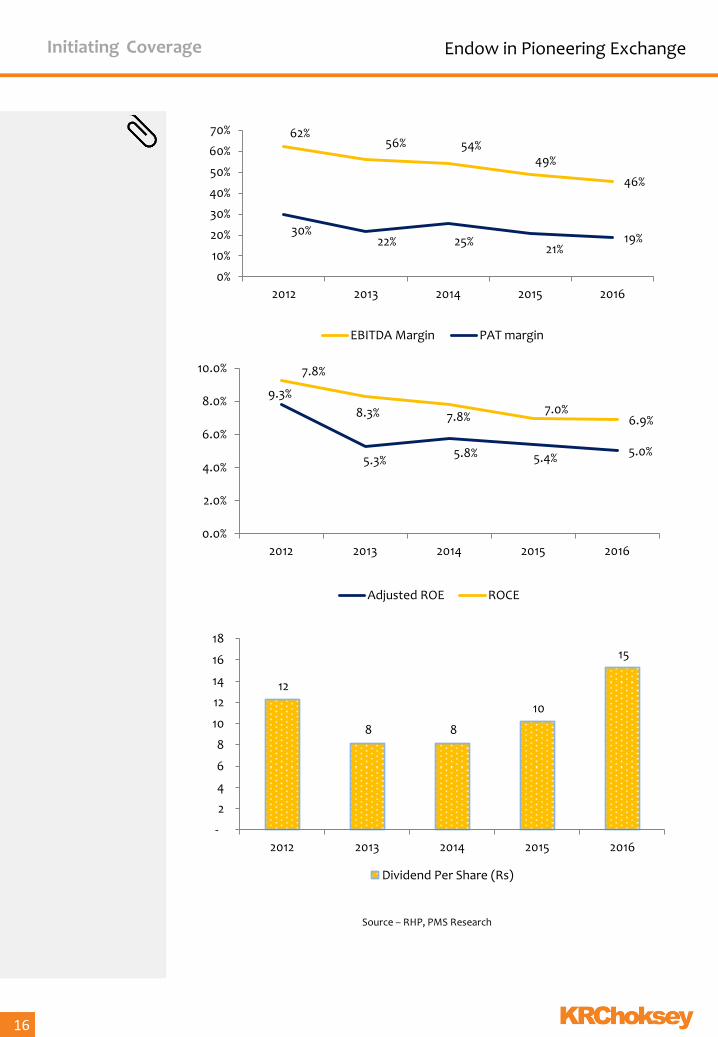

Financial Review BSE’s revenue from operations (comprising of securities services, services to

corporate and data dissemination fees), income from investments and deposits and

other income comprised of 63.2%, 29% & 7.9% of its total revenue, respectively in

1HFY17.

For FY16, total revenue of BSE was Rs.6583 mn, up 5.4% YoY compared with

Rs.6248mn in FY15 led by increase in certain charges and listing fees. From FY12-16,

BSE clocked revenue growth at 3.3% CAGR from FY12-16 while PAT was at Rs.1592 mn

in FY16. BSE has clocked revenue growth (excluding other income) at 3.5% CAGR in

FY12-16 to Rs.6160 mn.

EBITDA for FY16 was Rs.3005mn with 46% margin. Depreciation, finance cost, and tax

expenses for the period were Rs.617 mn, 7 mn, and 324 mn respectively.

Net profit, after share of minority and share of loss of associate, was at Rs.1225 mn as

on FY16, comparatively lower from FY15 net profit of Rs.1297mn with 21% margin.

Profit was low due to contribution of 25% of annual profits of BSE to the Core

Settlement Guarantee fund maintained by the ICCL, which is a SEBI requirement. This

contribution was required until Aug 29, 2016. For H1FY17, total revenue was Rs.3835

mn with EBITDA of Rs.1931 mn (50% margin). Net profit was Rs.1049 mn with 27%

margins.

Thus revenue growth is flat while profits have fallen, with NSE fast gaining market

share in various segments. But we can see there is a recovery in earnings in H1 FY17.

RoE and RoCE as on FY16 were in single digit at 5% and 8.2%, respectively.

The current dividend yield is 1.89% in 2016 which is moderate. BSE distributes 80% of

its adj. profits as dividend and plans to continue with the high dividend in the future.

BSE has a bank balance of Rs. 1,692 cr. which translates into Rs 310 as cash/share.

Investment Rationale

15

5787 5529 5298

6248 6583

0

1000

2000

3000

4000

5000

6000

7000

FY12 FY13 FY14 FY15 FY16

Total Income (Rs in Mn)

Source – RHP, PMS Research

Initiating Coverage Endow in Pioneering Exchange

Investment Rationale

16

12

8 8

10

15

-

2

4

6

8

10

12

14

16

18

2012 2013 2014 2015 2016

Dividend Per Share (Rs)

Source – RHP, PMS Research

62% 56% 54%

49%

46%

30% 22% 25%

21% 19%

0%

10%

20%

30%

40%

50%

60%

70%

2012 2013 2014 2015 2016

EBITDA Margin PAT margin

7.8%

5.3% 5.8% 5.4% 5.0%

9.3%

8.3% 7.8% 7.0%

6.9%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

2012 2013 2014 2015 2016

Adjusted ROE ROCE

Initiating Coverage Endow in Pioneering Exchange

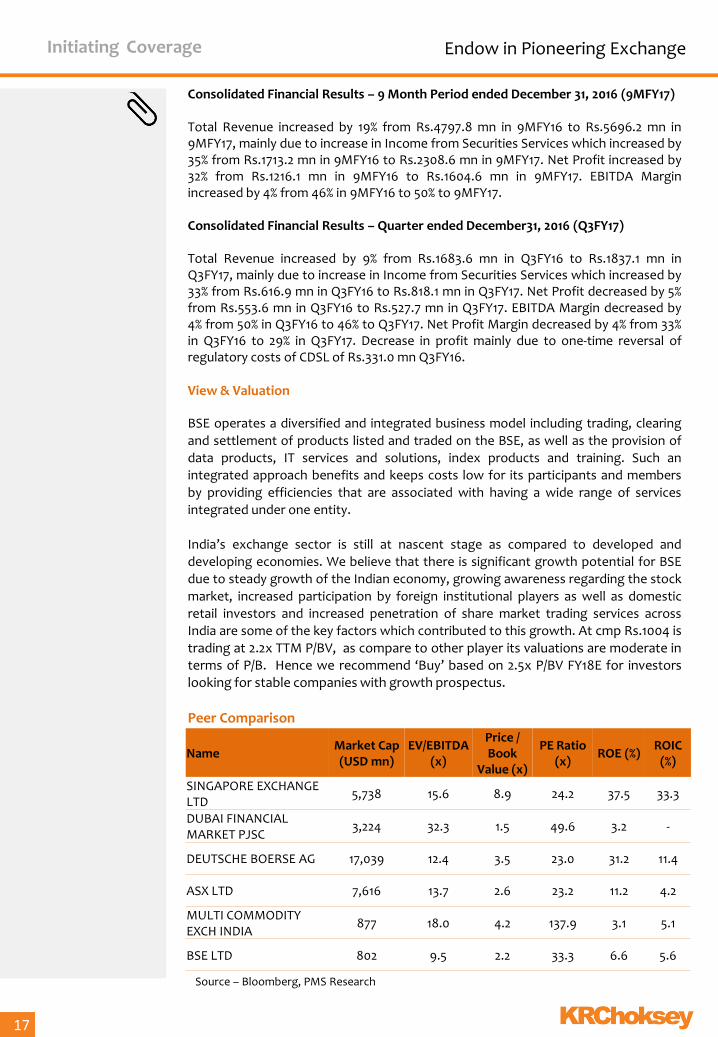

Consolidated Financial Results – 9 Month Period ended December 31, 2016 (9MFY17) Total Revenue increased by 19% from Rs.4797.8 mn in 9MFY16 to Rs.5696.2 mn in 9MFY17, mainly due to increase in Income from Securities Services which increased by 35% from Rs.1713.2 mn in 9MFY16 to Rs.2308.6 mn in 9MFY17. Net Profit increased by 32% from Rs.1216.1 mn in 9MFY16 to Rs.1604.6 mn in 9MFY17. EBITDA Margin increased by 4% from 46% in 9MFY16 to 50% to 9MFY17. Consolidated Financial Results – Quarter ended December31, 2016 (Q3FY17) Total Revenue increased by 9% from Rs.1683.6 mn in Q3FY16 to Rs.1837.1 mn in Q3FY17, mainly due to increase in Income from Securities Services which increased by 33% from Rs.616.9 mn in Q3FY16 to Rs.818.1 mn in Q3FY17. Net Profit decreased by 5% from Rs.553.6 mn in Q3FY16 to Rs.527.7 mn in Q3FY17. EBITDA Margin decreased by 4% from 50% in Q3FY16 to 46% to Q3FY17. Net Profit Margin decreased by 4% from 33% in Q3FY16 to 29% in Q3FY17. Decrease in profit mainly due to one-time reversal of regulatory costs of CDSL of Rs.331.0 mn Q3FY16. View & Valuation BSE operates a diversified and integrated business model including trading, clearing

and settlement of products listed and traded on the BSE, as well as the provision of

data products, IT services and solutions, index products and training. Such an

integrated approach benefits and keeps costs low for its participants and members

by providing efficiencies that are associated with having a wide range of services

integrated under one entity.

India’s exchange sector is still at nascent stage as compared to developed and

developing economies. We believe that there is significant growth potential for BSE

due to steady growth of the Indian economy, growing awareness regarding the stock

market, increased participation by foreign institutional players as well as domestic

retail investors and increased penetration of share market trading services across

India are some of the key factors which contributed to this growth. At cmp Rs.1004 is trading at 2.2x TTM P/BV, as compare to other player its valuations are moderate in terms of P/B. Hence we recommend ‘Buy’ based on 2.5x P/BV FY18E for investors looking for stable companies with growth prospectus.

Peer Comparison

Investment Rationale

17

Name Market Cap (USD mn)

EV/EBITDA (x)

Price / Book

Value (x)

PE Ratio (x)

ROE (%) ROIC

(%)

SINGAPORE EXCHANGE LTD

5,738 15.6 8.9 24.2 37.5 33.3

DUBAI FINANCIAL MARKET PJSC

3,224 32.3 1.5 49.6 3.2 -

DEUTSCHE BOERSE AG 17,039 12.4 3.5 23.0 31.2 11.4

ASX LTD 7,616 13.7 2.6 23.2 11.2 4.2

MULTI COMMODITY EXCH INDIA

877 18.0 4.2 137.9 3.1 5.1

BSE LTD 802 9.5 2.2 33.3 6.6 5.6

Source – Bloomberg, PMS Research

Initiating Coverage Endow in Pioneering Exchange

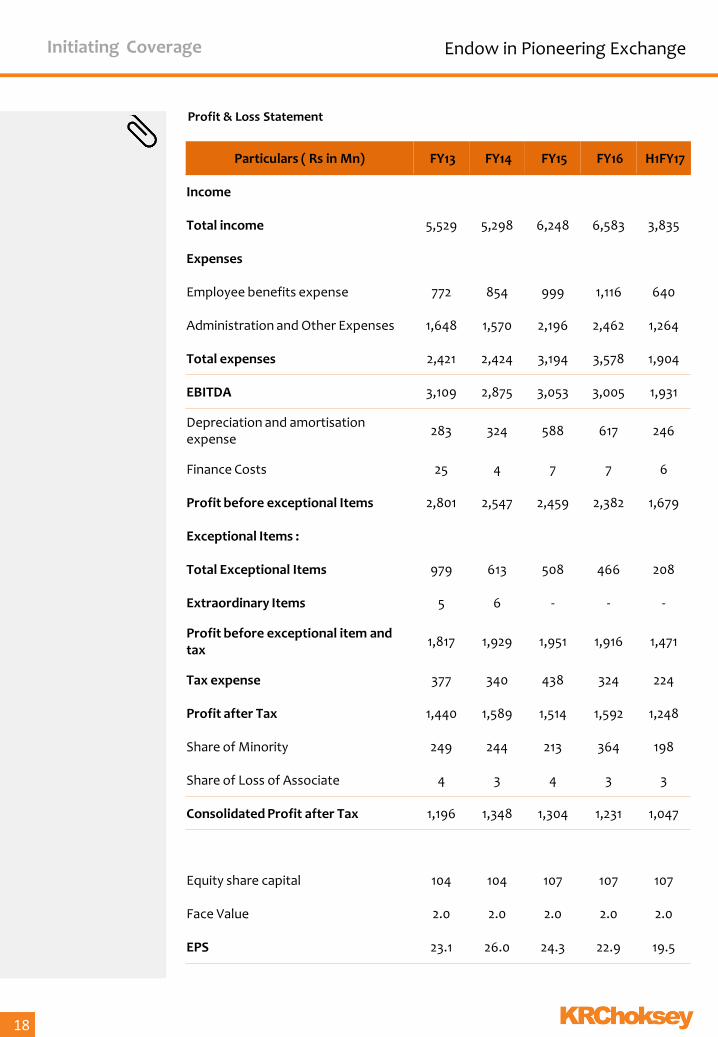

Profit & Loss Statement

Investment Rationale

18

Particulars ( Rs in Mn) FY13 FY14 FY15 FY16 H1FY17

Income

Total income 5,529 5,298 6,248 6,583 3,835

Expenses

Employee benefits expense 772 854 999 1,116 640

Administration and Other Expenses 1,648 1,570 2,196 2,462 1,264

Total expenses 2,421 2,424 3,194 3,578 1,904

EBITDA 3,109 2,875 3,053 3,005 1,931

Depreciation and amortisation expense

283 324 588 617 246

Finance Costs 25 4 7 7 6

Profit before exceptional Items 2,801 2,547 2,459 2,382 1,679

Exceptional Items :

Total Exceptional Items 979 613 508 466 208

Extraordinary Items 5 6 - - -

Profit before exceptional item and tax

1,817 1,929 1,951 1,916 1,471

Tax expense 377 340 438 324 224

Profit after Tax 1,440 1,589 1,514 1,592 1,248

Share of Minority 249 244 213 364 198

Share of Loss of Associate 4 3 4 3 3

Consolidated Profit after Tax 1,196 1,348 1,304 1,231 1,047

Equity share capital 104 104 107 107 107

Face Value 2.0 2.0 2.0 2.0 2.0

EPS 23.1 26.0 24.3 22.9 19.5

Initiating Coverage Endow in Pioneering Exchange

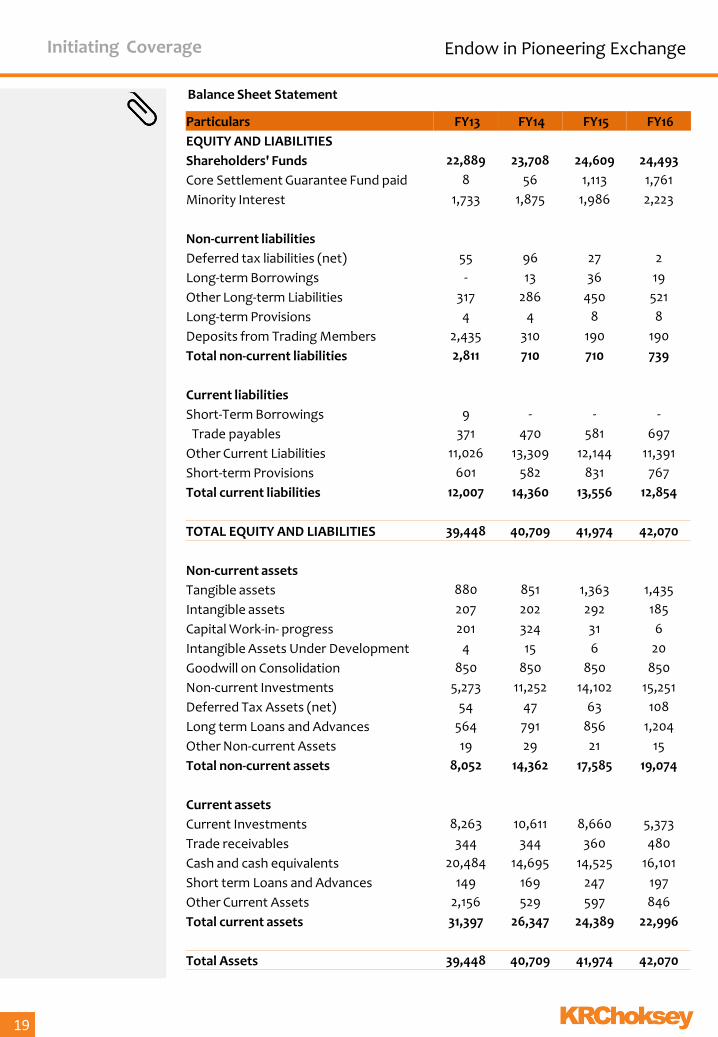

Investment Rationale

19

Balance Sheet Statement

Particulars FY13 FY14 FY15 FY16

EQUITY AND LIABILITIES

Shareholders' Funds 22,889 23,708 24,609 24,493

Core Settlement Guarantee Fund paid 8 56 1,113 1,761

Minority Interest 1,733 1,875 1,986 2,223

Non-current liabilities

Deferred tax liabilities (net) 55 96 27 2

Long-term Borrowings - 13 36 19

Other Long-term Liabilities 317 286 450 521

Long-term Provisions 4 4 8 8

Deposits from Trading Members 2,435 310 190 190

Total non-current liabilities 2,811 710 710 739

Current liabilities

Short-Term Borrowings 9 - - -

Trade payables 371 470 581 697

Other Current Liabilities 11,026 13,309 12,144 11,391

Short-term Provisions 601 582 831 767

Total current liabilities 12,007 14,360 13,556 12,854

TOTAL EQUITY AND LIABILITIES 39,448 40,709 41,974 42,070

Non-current assets

Tangible assets 880 851 1,363 1,435

Intangible assets 207 202 292 185

Capital Work-in- progress 201 324 31 6

Intangible Assets Under Development 4 15 6 20

Goodwill on Consolidation 850 850 850 850

Non-current Investments 5,273 11,252 14,102 15,251

Deferred Tax Assets (net) 54 47 63 108

Long term Loans and Advances 564 791 856 1,204

Other Non-current Assets 19 29 21 15

Total non-current assets 8,052 14,362 17,585 19,074

Current assets

Current Investments 8,263 10,611 8,660 5,373

Trade receivables 344 344 360 480

Cash and cash equivalents 20,484 14,695 14,525 16,101

Short term Loans and Advances 149 169 247 197

Other Current Assets 2,156 529 597 846

Total current assets 31,397 26,347 24,389 22,996

Total Assets 39,448 40,709 41,974 42,070

Initiating Coverage Endow in Pioneering Exchange

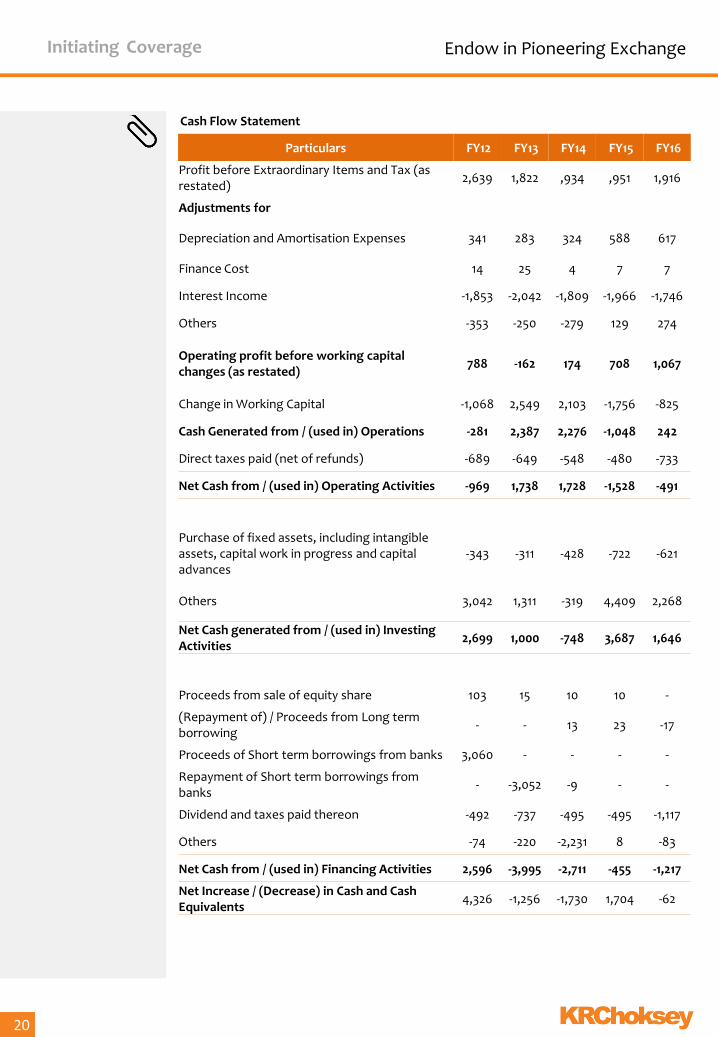

Cash Flow Statement

Investment Rationale

20

Particulars FY12 FY13 FY14 FY15 FY16

Profit before Extraordinary Items and Tax (as restated)

2,639 1,822 ,934 ,951 1,916

Adjustments for

Depreciation and Amortisation Expenses 341 283 324 588 617

Finance Cost 14 25 4 7 7

Interest Income -1,853 -2,042 -1,809 -1,966 -1,746

Others -353 -250 -279 129 274

Operating profit before working capital changes (as restated)

788 -162 174 708 1,067

Change in Working Capital -1,068 2,549 2,103 -1,756 -825

Cash Generated from / (used in) Operations -281 2,387 2,276 -1,048 242

Direct taxes paid (net of refunds) -689 -649 -548 -480 -733

Net Cash from / (used in) Operating Activities -969 1,738 1,728 -1,528 -491

Purchase of fixed assets, including intangible assets, capital work in progress and capital advances

-343 -311 -428 -722 -621

Others 3,042 1,311 -319 4,409 2,268

Net Cash generated from / (used in) Investing Activities

2,699 1,000 -748 3,687 1,646

Proceeds from sale of equity share 103 15 10 10 -

(Repayment of) / Proceeds from Long term borrowing

- - 13 23 -17

Proceeds of Short term borrowings from banks 3,060 - - - -

Repayment of Short term borrowings from banks

- -3,052 -9 - -

Dividend and taxes paid thereon -492 -737 -495 -495 -1,117

Others -74 -220 -2,231 8 -83

Net Cash from / (used in) Financing Activities 2,596 -3,995 -2,711 -455 -1,217

Net Increase / (Decrease) in Cash and Cash Equivalents

4,326 -1,256 -1,730 1,704 -62

Initiating Coverage Endow in Pioneering Exchange

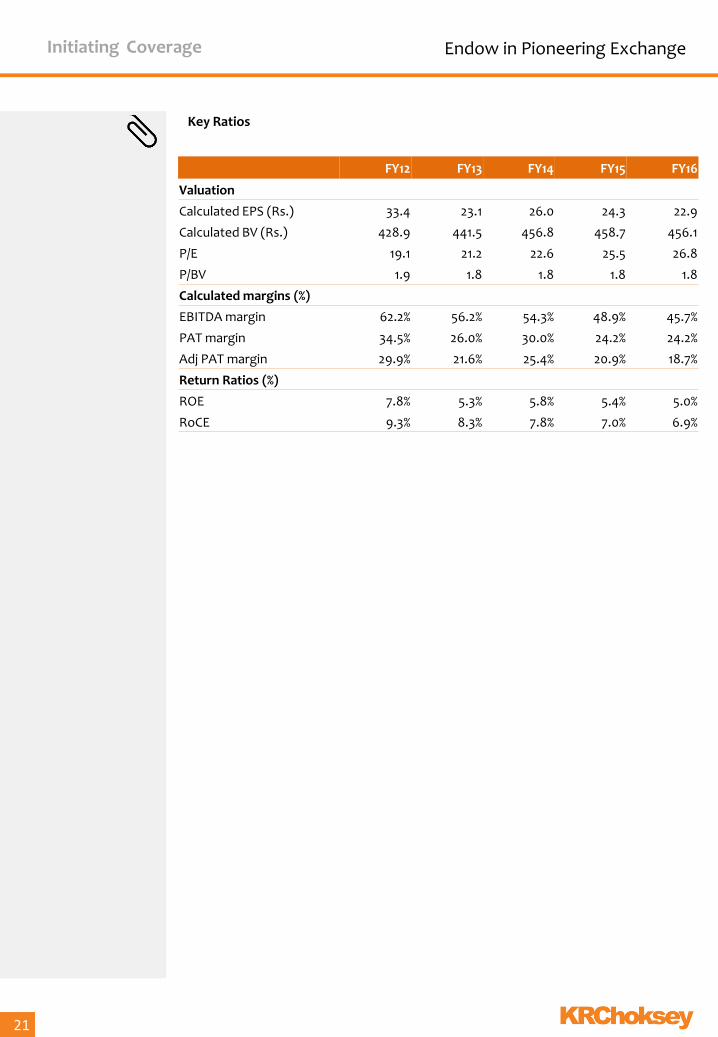

Investment Rationale

21

Key Ratios

FY12 FY13 FY14 FY15 FY16

Valuation

Calculated EPS (Rs.) 33.4 23.1 26.0 24.3 22.9

Calculated BV (Rs.) 428.9 441.5 456.8 458.7 456.1

P/E 19.1 21.2 22.6 25.5 26.8

P/BV 1.9 1.8 1.8 1.8 1.8

Calculated margins (%)

EBITDA margin 62.2% 56.2% 54.3% 48.9% 45.7%

PAT margin 34.5% 26.0% 30.0% 24.2% 24.2%

Adj PAT margin 29.9% 21.6% 25.4% 20.9% 18.7%

Return Ratios (%)

ROE 7.8% 5.3% 5.8% 5.4% 5.0%

RoCE 9.3% 8.3% 7.8% 7.0% 6.9%

Initiating Coverage Endow in Pioneering Exchange

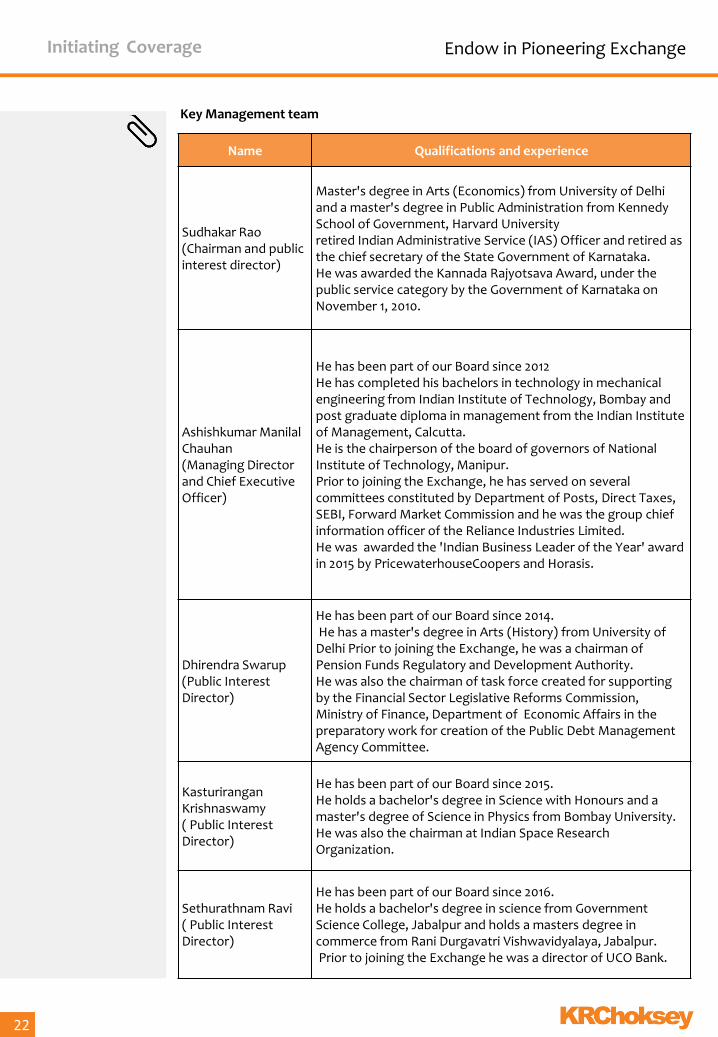

Name Qualifications and experience

Sudhakar Rao (Chairman and public interest director)

Master's degree in Arts (Economics) from University of Delhi and a master's degree in Public Administration from Kennedy School of Government, Harvard University retired Indian Administrative Service (IAS) Officer and retired as the chief secretary of the State Government of Karnataka. He was awarded the Kannada Rajyotsava Award, under the public service category by the Government of Karnataka on November 1, 2010.

Ashishkumar Manilal Chauhan (Managing Director and Chief Executive Officer)

He has been part of our Board since 2012 He has completed his bachelors in technology in mechanical engineering from Indian Institute of Technology, Bombay and post graduate diploma in management from the Indian Institute of Management, Calcutta. He is the chairperson of the board of governors of National Institute of Technology, Manipur. Prior to joining the Exchange, he has served on several committees constituted by Department of Posts, Direct Taxes, SEBI, Forward Market Commission and he was the group chief information officer of the Reliance Industries Limited. He was awarded the 'Indian Business Leader of the Year' award in 2015 by PricewaterhouseCoopers and Horasis.

Dhirendra Swarup (Public Interest Director)

He has been part of our Board since 2014. He has a master's degree in Arts (History) from University of Delhi Prior to joining the Exchange, he was a chairman of Pension Funds Regulatory and Development Authority. He was also the chairman of task force created for supporting by the Financial Sector Legislative Reforms Commission, Ministry of Finance, Department of Economic Affairs in the preparatory work for creation of the Public Debt Management Agency Committee.

Kasturirangan Krishnaswamy ( Public Interest Director)

He has been part of our Board since 2015. He holds a bachelor's degree in Science with Honours and a master's degree of Science in Physics from Bombay University. He was also the chairman at Indian Space Research Organization.

Sethurathnam Ravi ( Public Interest Director)

He has been part of our Board since 2016. He holds a bachelor's degree in science from Government Science College, Jabalpur and holds a masters degree in commerce from Rani Durgavatri Vishwavidyalaya, Jabalpur. Prior to joining the Exchange he was a director of UCO Bank.

Key Management team

Investment Rationale

22

Initiating Coverage Endow in Pioneering Exchange

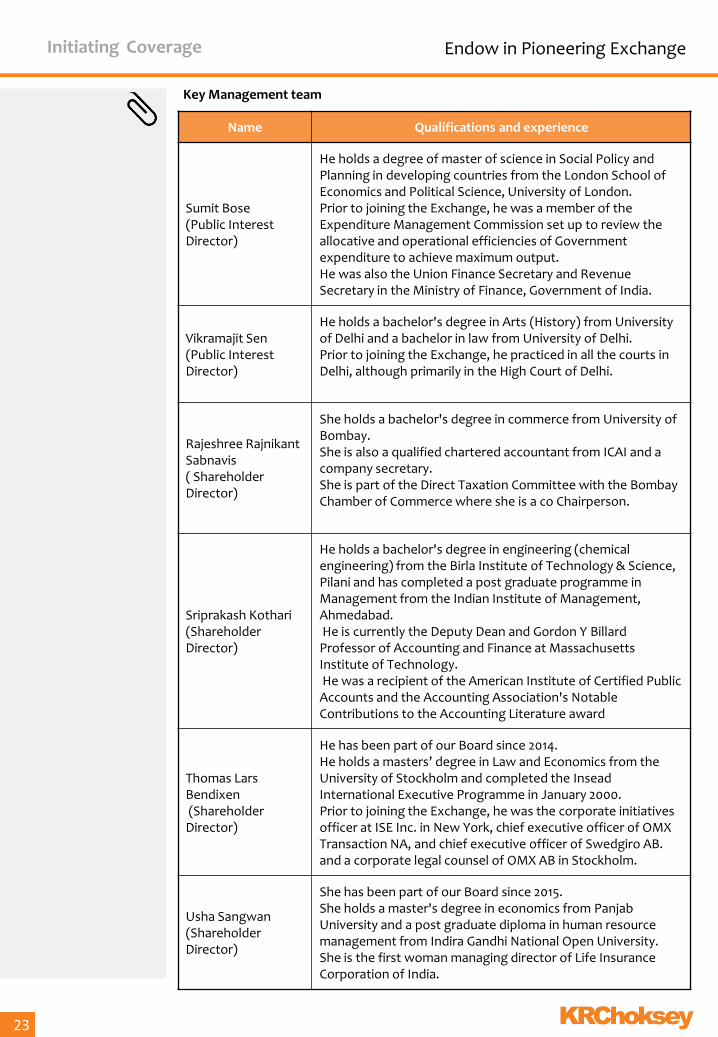

Name Qualifications and experience

Sumit Bose (Public Interest Director)

He holds a degree of master of science in Social Policy and Planning in developing countries from the London School of Economics and Political Science, University of London. Prior to joining the Exchange, he was a member of the Expenditure Management Commission set up to review the allocative and operational efficiencies of Government expenditure to achieve maximum output. He was also the Union Finance Secretary and Revenue Secretary in the Ministry of Finance, Government of India.

Vikramajit Sen (Public Interest Director)

He holds a bachelor's degree in Arts (History) from University of Delhi and a bachelor in law from University of Delhi. Prior to joining the Exchange, he practiced in all the courts in Delhi, although primarily in the High Court of Delhi.

Rajeshree Rajnikant Sabnavis ( Shareholder Director)

She holds a bachelor's degree in commerce from University of Bombay. She is also a qualified chartered accountant from ICAI and a company secretary. She is part of the Direct Taxation Committee with the Bombay Chamber of Commerce where she is a co Chairperson.

Sriprakash Kothari (Shareholder Director)

He holds a bachelor's degree in engineering (chemical engineering) from the Birla Institute of Technology & Science, Pilani and has completed a post graduate programme in Management from the Indian Institute of Management, Ahmedabad. He is currently the Deputy Dean and Gordon Y Billard Professor of Accounting and Finance at Massachusetts Institute of Technology. He was a recipient of the American Institute of Certified Public Accounts and the Accounting Association's Notable Contributions to the Accounting Literature award

Thomas Lars Bendixen (Shareholder Director)

He has been part of our Board since 2014. He holds a masters’ degree in Law and Economics from the University of Stockholm and completed the Insead International Executive Programme in January 2000. Prior to joining the Exchange, he was the corporate initiatives officer at ISE Inc. in New York, chief executive officer of OMX Transaction NA, and chief executive officer of Swedgiro AB. and a corporate legal counsel of OMX AB in Stockholm.

Usha Sangwan (Shareholder Director)

She has been part of our Board since 2015. She holds a master's degree in economics from Panjab University and a post graduate diploma in human resource management from Indira Gandhi National Open University. She is the first woman managing director of Life Insurance Corporation of India.

Key Management team

Investment Rationale

23

Initiating Coverage Endow in Pioneering Exchange

Sr No.

Name of Subsidiary Holder Holding

(%)

Paid-up Share Capital (Rs in

mn)

1 Central Depository Services Limited

(CDSL) BSE 54.2% 1045

2 Indian Clearing Corporation Limited

(ICCL) BSE 100.0% 3540

3 Marketplace Technologies Private

Limited (Marketplace Technologies) BSE 100.0% 20

4 CDSL Ventures Limited (CDSL

Ventures) CDSL 100.0% 45

5 CDSL Insurance Repository Limited

(CDSL Insurance) CDSL 51.0% 300

Subsidiary

Investment Rationale

24

Initiating Coverage Endow in Pioneering Exchange

Disclaimer

022-6696 5555 www.krchoksey.com

KRChoksey Research is also available on Bloomberg KRCS<GO>

Thomson Reuters, Factset and Capital IQ

Analyst Dinesh Gupta, [email protected], 022 66965609

25

We, Dinesh Gupta (B.com, M.Sc), research analyst, author and the name subscribed to this report, hereby certify that all of the views expressed in this research report accurately reflect my views about the subject issuer(s) or securities. I also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this report. Terms & Conditions and other disclosures: KRChoksey Shares and Securities Pvt. Ltd (hereinafter referred to as KRCSSPL) is a registered member of National Stock Exchange of India Limited, Bombay Stock Exchange Limited and MCX Stock Exchange Limited. KRCSSPL is a registered Research Entity vide SEBI Registration No. INH000001295 under SEBI (Research Analyst) Regulations, 2014. We submit that no material disciplinary action has been taken on KRCSSPL and its associates (Group Companies) by any Regulatory Authority impacting Equity Research Analysis activities. KRCSSPL prohibits its analysts, persons reporting to analysts and their relatives from maintaining a financial interest in the securities or derivatives of any companies that the analyst covers. The information and opinions in this report have been prepared by KRCSSPL and are subject to change without any notice. The report and information contained herein is strictly confidential and meant solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written consent of KRCSSPL. While we would endeavor to update the information herein on a reasonable basis, KRCSSPL is not under any obligation to update the information. Also, there may be regulatory, compliance or other reasons that may prevent KRCSSPL from doing so. Non-rated securities indicate that rating on a particular security has been suspended temporarily and such suspension is in compliance with applicable regulations and/or KRCSSPL policies, in circumstances where KRCSSPL might be acting in an advisory capacity to this company, or in certain other circumstances. This report is based on information obtained from public sources and sources believed to be reliable, but no independent verification has been made nor is its accuracy or completeness guaranteed. This report and information herein is solely for informational purpose and shall not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial instruments. Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. KRCSSPL will not treat recipients as customers by virtue of their receiving this report. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. The recipient should independently evaluate the investment risks. The value and return on investment may vary because of changes in interest rates, foreign exchange rates or any other reason. KRCSSPL accepts no liabilities whatsoever for any loss or damage of any kind arising out of the use of this report. Past performance is not necessarily a guide to future performance. Investors are advised to see Risk Disclosure Document to understand the risks associated before investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and may be subject to change without notice. Our employees in sales and marketing team, dealers and other professionals may provide oral or written market commentary or trading strategies that reflect opinions that are contrary to the opinions expressed herein, .In reviewing these materials, you should be aware that any or all of the foregoing, among other things, may give rise to real or potential conflicts of interest.

ANALYST CERTIFICATION:

022-6696 5555 www.krchoksey.com

KRChoksey Research is also available on Bloomberg KRCS<GO>

Thomson Reuters, Factset and Capital IQ

Analyst Dinesh Gupta, [email protected], 022 66965609

Disclaimer

26

Associates (Group Companies) of KRCSSPL might have received any commission/compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services in respect of brokerage services or specific transaction or for products and services other than brokerage services. KRCSSPL or its Associates (Group Companies) have not managed or co-managed public offering of securities for the subject company in the past twelve months KRCSSPL encourages the practice of giving independent opinion in research report preparation by the analyst and thus strives to minimize the conflict in preparation of research report. KRCSSPL or its analysts did not receive any compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither KRCSSPL nor Research Analysts have any material conflict of interest at the time of publication of this report. It is confirmed that, Dinesh Gupta (B.com, M.Sc), research analyst, of this report have not received any compensation from the companies mentioned in the report in the preceding twelve months. Compensation of our Research Analysts is not based on any specific brokerage service transactions. KRCSSPL or its associates (Group Companies) collectively or its research analyst do not hold any financial interest/beneficial ownership of more than 1% (at the end of the month immediately preceding the date of publication of the research report) in the company covered by Analyst, and has not been engaged in market making activity of the company covered by research analyst. Since associates (Group Companies) of KRCSSPL are engaged in various financial service businesses, they might have financial interests or beneficial ownership in various companies including the subject company/companies mentioned in this report. It is confirmed that, Dinesh Gupta (B.com, M.Sc), research analyst, do not serve as an officer, director or employee of the companies mentioned in the report. This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject KRCSSPL and affiliates to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such restriction.

Please send your feedback to [email protected] Visit us at www.krchoksey.com

Kisan Ratilal Choksey Shares and Securities Pvt. Ltd

Registered Office: 1102, Stock Exchange Tower, Dalal Street, Fort, Mumbai – 400 001.

Phone: 91-22-6633 5000; Fax: 91-22-6633 8060. Corporate Office:

ABHISHEK, 5th Floor, Link Road, Andheri (W), Mumbai – 400 053. Phone: 91-22-6696 5555; Fax: 91-22-6691 9576.

![CHALLAN-DEC.pdf n/epfopaymentbilldeskresponse.htm Pay EPFO Exit 15-Jan-2016 [01:52 PM IST] State Bank Co ect state Bank MOPS Pay EPFO > Pay EPFO You are here: Pay EPFO Cancel Pending](https://img.pdfslide.net/doc/110x75/5aefb4e07f8b9ac2468d2bba/challan-decpdf-nepfopaymentbilldeskresponsehtm-pay-epfo-exit-15-jan-2016-0152.jpg)