Embed Size (px)

DESCRIPTION

Final Exam by prof Tammy

Citation preview

7/18/2019 BU5540 Exam 3 Summer I 2015(1)

http://slidepdf.com/reader/full/bu5540-exam-3-summer-i-20151 1/10

BU 5540 – Advanced Accounting Name_______________________________

SUNY Old Westbury

Third Exam – Summer I 2015

Prof. Straus

Page

1 of 10

Please answer all questions completely. This Exam is worth 30% of the grade forthe course. You must do your own work; d o n o t w o r k w i t h a n y o n e e l se in t h e

c l as s a n d d o n o t c o n s u l t a n y o n e o u t s i d e t h e c l a ss . You may use your book andnotes, but to other materials.

Submit o n e Excel file with all of your answers. Each part of the test (there are 5

parts, Parts I through V) should be on a separate sheet in the file.

Part I: Multiple Choice (2 points each for a total of 36 points)

1. Dell makes an investment in ATS, a small computer company, by buying 25% of itsstock, and obtains significant influence over ATS’ operations. Dell most likely willaccount for ATS using the:

a) Cost method

b) Fair value method

c) Equity method

d) Consolidation method

2. In preparing a consolidation of a wholly-owned subsidiary, non-controlling interest isrecorded for:

a) the portion of the subsidiary company owned by outside investors

b) the portion of the parent company owned by outside investors

c) the portion of the subsidiary company owned by majority investors

d) non-controlling interest is not recorded

3. In an acquisition, a positive result between the Fair Value of an acquired companyless the Fair Value of its net identifiable assets is:

a) Expensed immediately

b) Recorded as Goodwill

c) Amortized over the remaining life of any assets or liabilities that were

adjusted to fair value

d) Recorded as a Gain on Bargain Purchase

7/18/2019 BU5540 Exam 3 Summer I 2015(1)

http://slidepdf.com/reader/full/bu5540-exam-3-summer-i-20151 2/10

BU 5540 – Advanced Accounting Name_______________________________

SUNY Old Westbury

Third Exam – Summer I 2015

Prof. Straus

Page

2 of 10

4. In a dissolution of a general partnership of partners D, E, and F, partner D has a

negative capital balance of $100,000 after all assets are liquidated and any gain or loss

on sale was recorded, and E and F each have zero balances. The responsibility forcontributing $100,000 of cash to pay the balance owed to creditors falls to:

a) First to D to bring their capital balance to zero, then to E and F if D refuses or

is unable

b) It is D’s sole responsibility

c) The partners have no responsibility to contribute additional funds, as the

creditors made the decision to extend credit

d) D, E and F in order of their joining the partnership

5. Fair value of a company purchased in a partial acquisition can be calculated if oneknows the percentage purchased and the price paid by:

a) Subtracting book value from purchase price

b) Adding book value and purchase price

c) Multiplying price paid by percentage purchased

d) Dividing price paid by percentage purchased

6. Polar Bear Company buys 65% of Seal Corp. for $400,000. Seal’s equity at the timeof acquisition was $180,000. All of Seal’s accounts approximated fair value except that

the fair value of inventory was $850,000, while the book value was $720,000. Theamount of goodwill to be recorded is:

a) $435,385

b) $305,385

c) $130,000

d) $90,000

7. Using the current method of translating financial statements, revenue and expenseaccounts are translated at the:

a) Historical exchange rate

b) Exchange rate on the last day of the period

c) Average exchange rate during the period

d) Weighted average exchange rate during the period

7/18/2019 BU5540 Exam 3 Summer I 2015(1)

http://slidepdf.com/reader/full/bu5540-exam-3-summer-i-20151 3/10

BU 5540 – Advanced Accounting Name_______________________________

SUNY Old Westbury

Third Exam – Summer I 2015

Prof. Straus

Page

3 of 10

8. What is a registration statement as it relates to the SEC:

a) An annual filing made with the SECb) A filing made by a public company to alert the market that a significant

change occurred in its business

c) A required filing before an inside party trades a large amount of stock

d) A document that must be filed before a company can begin an initial offering

of securities to the public

9. What is EDGAR as it relates to the SEC?

a) The enforcement arm of the SECb) An electronic filing system

c) A system the SEC uses to reject incomplete filings

d) The branch of the US government that oversees the SEC

10. Müller Co. is based in New York and sells strawberries to Canada. If Müller sells10,000 cases of strawberries to a company in Quebec in Canadian dollars on December1, 2014 for payment on February 1, 2015, what information is needed to determine theamount of Müller’s foreign currency transaction gain or loss at December 31, 2014?

a) The sales price per caseb) The USD/CAN exchange rate on December 1, 2014

c) The USD/CAN exchange rate on December 31, 2014

d) All of the above

11. Which of the following is filed with the SEC on a regular periodic basis:

a) Form S-1

b) Form S-3

c) Form 10-K

d) Prospectus

7/18/2019 BU5540 Exam 3 Summer I 2015(1)

http://slidepdf.com/reader/full/bu5540-exam-3-summer-i-20151 4/10

BU 5540 – Advanced Accounting Name_______________________________

SUNY Old Westbury

Third Exam – Summer I 2015

Prof. Straus

Page

4 of 10

12. Partners X, Y, and Z has capital balances of $20,000, $40,000, and $60,000 at

January 1, 2014. If the partners share equally in any profit and loss, and the

partnership had profit of $120,000 in 2014, the profit allocated to X, Y and Z was:

a) X: $60,000; Y: $80,000; Z: $100,000

b) X: $80,000; Y: $80,000; Z: $80,000

c) X: $20,000; Y: $40,000; Z: $60,000

d) X: $40,000; Y: $40,000; Z: $40,000

13. A shelf registration is a registration statement ___________

a) That the SEC rejects due to the lapse of a specified period of time

b) That the SEC formally rejects

c) That the filer withdraws before going effective

d) For large companies that allows them to offer securities over a period of time

without getting additional SEC approval

14. A significant difference between accounting for partnerships versus corporations is

that partnerships:

a) Must use the cash basis of accounting

b) Track each partner’s capital accounts, while a corporation just has a one

retained earnings account for all shareholders

c) Are required to recognize expenses earlier than corporationsd) Must defer revenue recognition until cash is collected

15. A Variable Interest Entity (VIE) should be consolidated into Klose Co. if:

a) Klose Co. has the power to direct the most significant economic activities of the

VIE OR has the right to receive benefits or obligation to absorb losses that are

significant to the VIE.

b) Klose Co. has the power to direct the most significant economic activities of the

VIE AND has the right to receive benefits or obligation to absorb losses that are

significant to the VIE.

c) Klose Co. owns more than 20% of the VIE.

d) Klose Co. has significant influence over the VIE.

7/18/2019 BU5540 Exam 3 Summer I 2015(1)

http://slidepdf.com/reader/full/bu5540-exam-3-summer-i-20151 5/10

BU 5540 – Advanced Accounting Name_______________________________

SUNY Old Westbury

Third Exam – Summer I 2015

Prof. Straus

Page

5 of 10

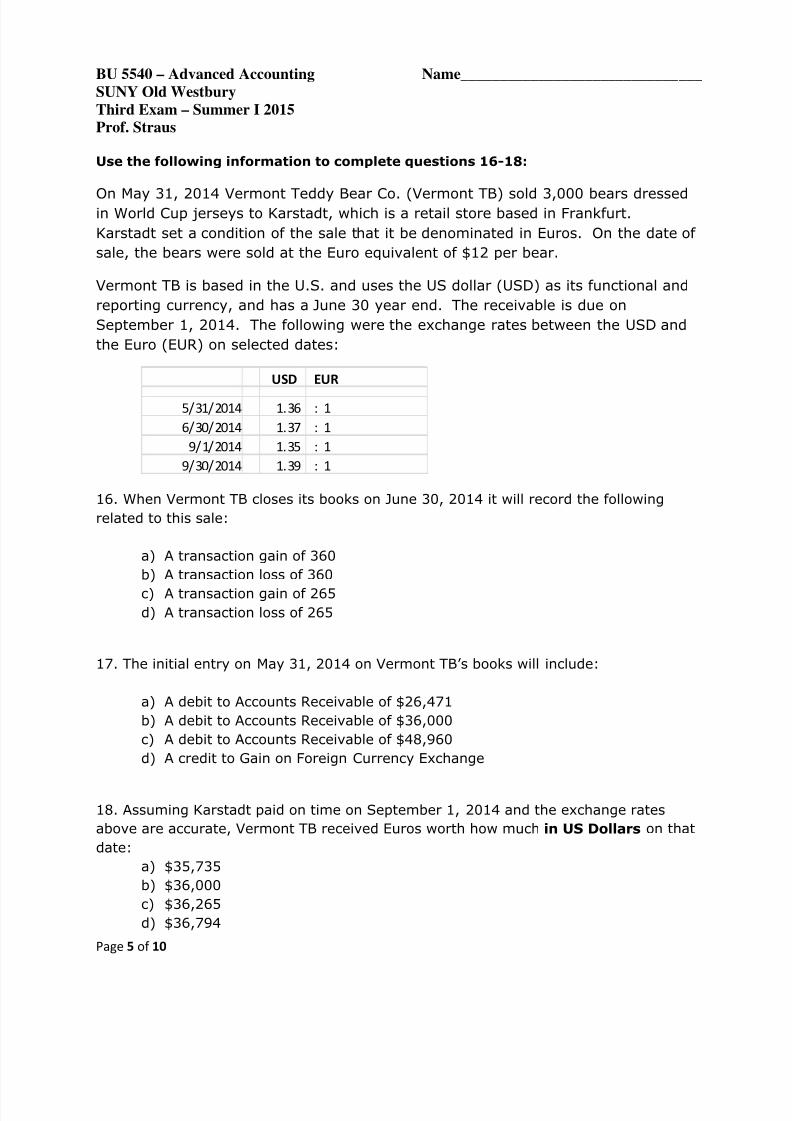

Use the following information to complete questions 16-18:

On May 31, 2014 Vermont Teddy Bear Co. (Vermont TB) sold 3,000 bears dressedin World Cup jerseys to Karstadt, which is a retail store based in Frankfurt.

Karstadt set a condition of the sale that it be denominated in Euros. On the date of

sale, the bears were sold at the Euro equivalent of $12 per bear.

Vermont TB is based in the U.S. and uses the US dollar (USD) as its functional and

reporting currency, and has a June 30 year end. The receivable is due on

September 1, 2014. The following were the exchange rates between the USD and

the Euro (EUR) on selected dates:

16. When Vermont TB closes its books on June 30, 2014 it will record the following

related to this sale:

a) A transaction gain of 360

b) A transaction loss of 360

c) A transaction gain of 265

d) A transaction loss of 265

17. The initial entry on May 31, 2014 on Vermont TB’s books will include:

a) A debit to Accounts Receivable of $26,471

b) A debit to Accounts Receivable of $36,000

c) A debit to Accounts Receivable of $48,960

d) A credit to Gain on Foreign Currency Exchange

18. Assuming Karstadt paid on time on September 1, 2014 and the exchange rates

above are accurate, Vermont TB received Euros worth how much in US Dollars on that

date:

a) $35,735

b) $36,000

c) $36,265

d) $36,794

USD EUR

5/31/2014 1.36 : 1

6/30/2014 1.37 : 1

9/1/2014 1.35 : 1

9/30/2014 1.39 : 1

7/18/2019 BU5540 Exam 3 Summer I 2015(1)

http://slidepdf.com/reader/full/bu5540-exam-3-summer-i-20151 6/10

BU 5540 – Advanced Accounting Name_______________________________

SUNY Old Westbury

Third Exam – Summer I 2015

Prof. Straus

Page

6 of 10

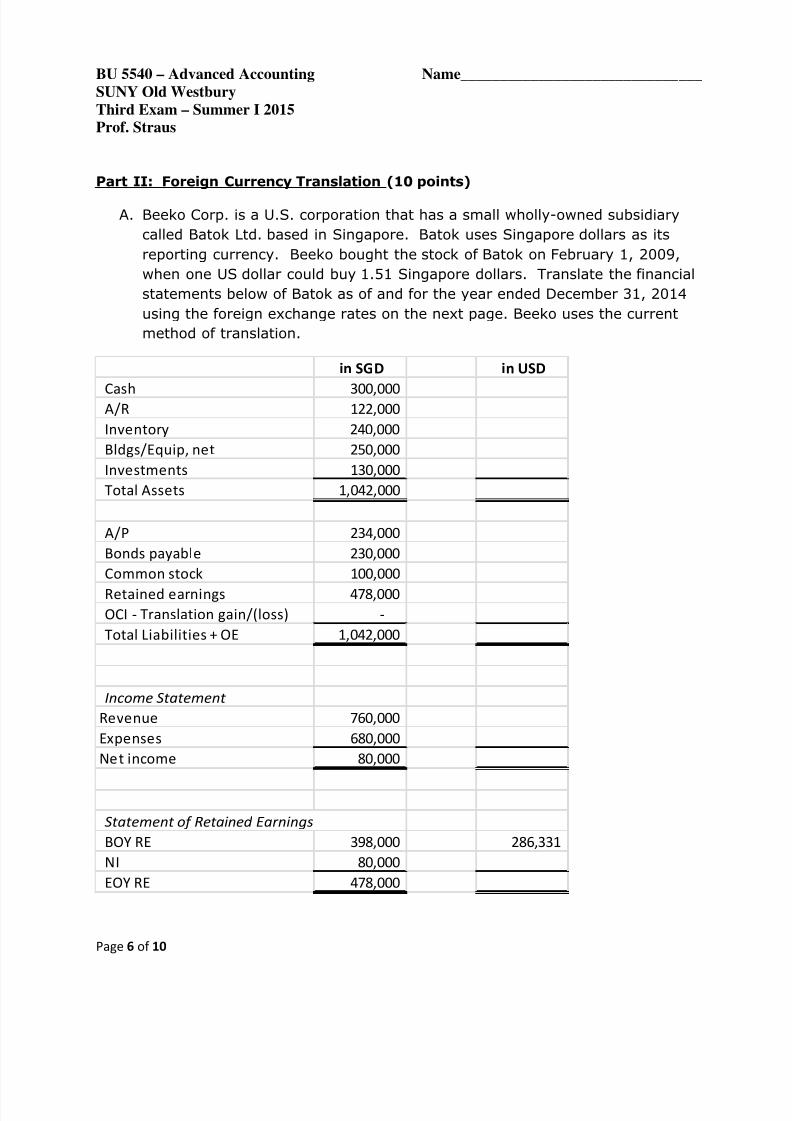

Part II: Foreign Currency Translation (10 points)

A. Beeko Corp. is a U.S. corporation that has a small wholly-owned subsidiary

called Batok Ltd. based in Singapore. Batok uses Singapore dollars as its

reporting currency. Beeko bought the stock of Batok on February 1, 2009,

when one US dollar could buy 1.51 Singapore dollars. Translate the financial

statements below of Batok as of and for the year ended December 31, 2014

using the foreign exchange rates on the next page. Beeko uses the current

method of translation.

in SGD in USD

Cash 300,000 A/R 122,000

Inventory 240,000

Bldgs/Equip, net 250,000

Investments 130,000

Total Assets 1,042,000

A/P 234,000

Bonds payable 230,000

Common stock 100,000

Retained earnings 478,000

OCI ‐ Translation gain/(loss) ‐

Total Liabilities + OE 1,042,000

Income Statement

Revenue 760,000

Expenses 680,000

Net income 80,000

Statement

of

Retained

Earnings

BOY RE 398,000 286,331

NI 80,000

EOY RE 478,000

7/18/2019 BU5540 Exam 3 Summer I 2015(1)

http://slidepdf.com/reader/full/bu5540-exam-3-summer-i-20151 7/10

BU 5540 – Advanced Accounting Name_______________________________

SUNY Old Westbury

Third Exam – Summer I 2015

Prof. Straus

Page

7 of 10

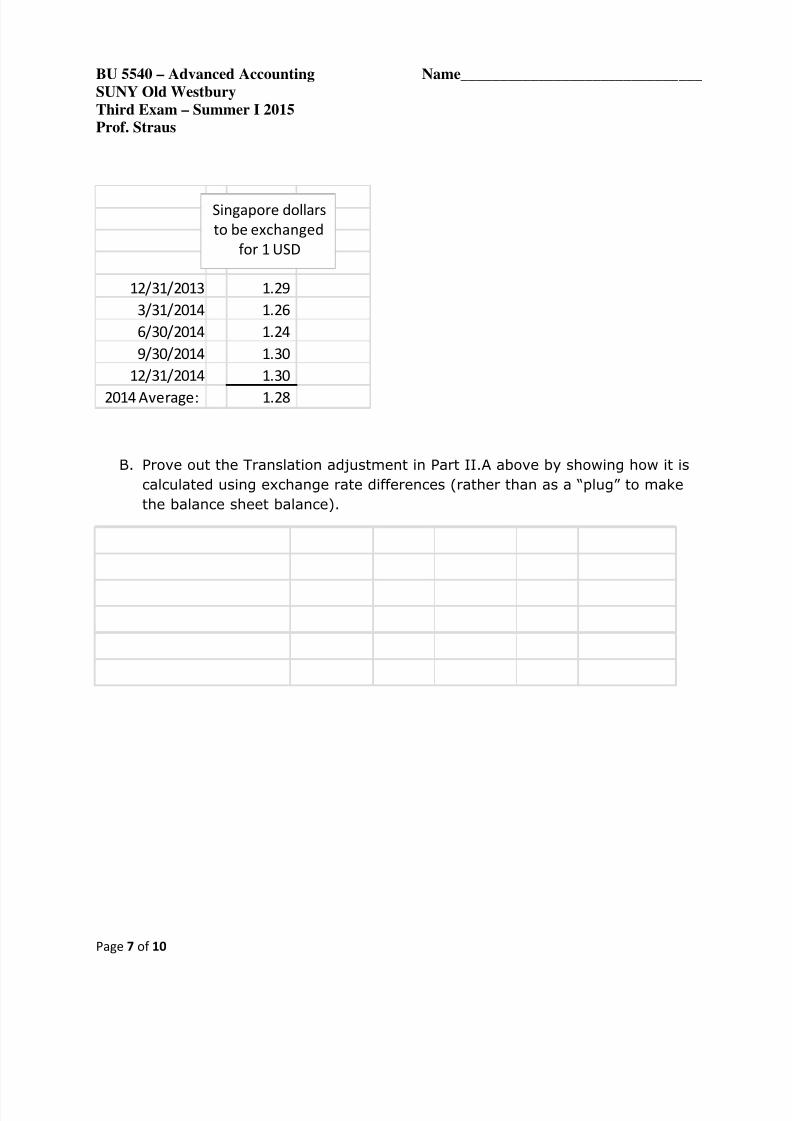

B. Prove out the Translation adjustment in Part II.A above by showing how it is

calculated using exchange rate differences (rather than as a “plug” to make

the balance sheet balance).

12/31/2013 1.29

3/31/2014 1.26

6/30/2014 1.24

9/30/2014 1.30

12/31/2014 1.30

2014 Average: 1.28

Singapore

dollars

to be exchanged

for 1 USD

7/18/2019 BU5540 Exam 3 Summer I 2015(1)

http://slidepdf.com/reader/full/bu5540-exam-3-summer-i-20151 8/10

BU 5540 – Advanced Accounting Name_______________________________

SUNY Old Westbury

Third Exam – Summer I 2015

Prof. Straus

Page

8 of 10

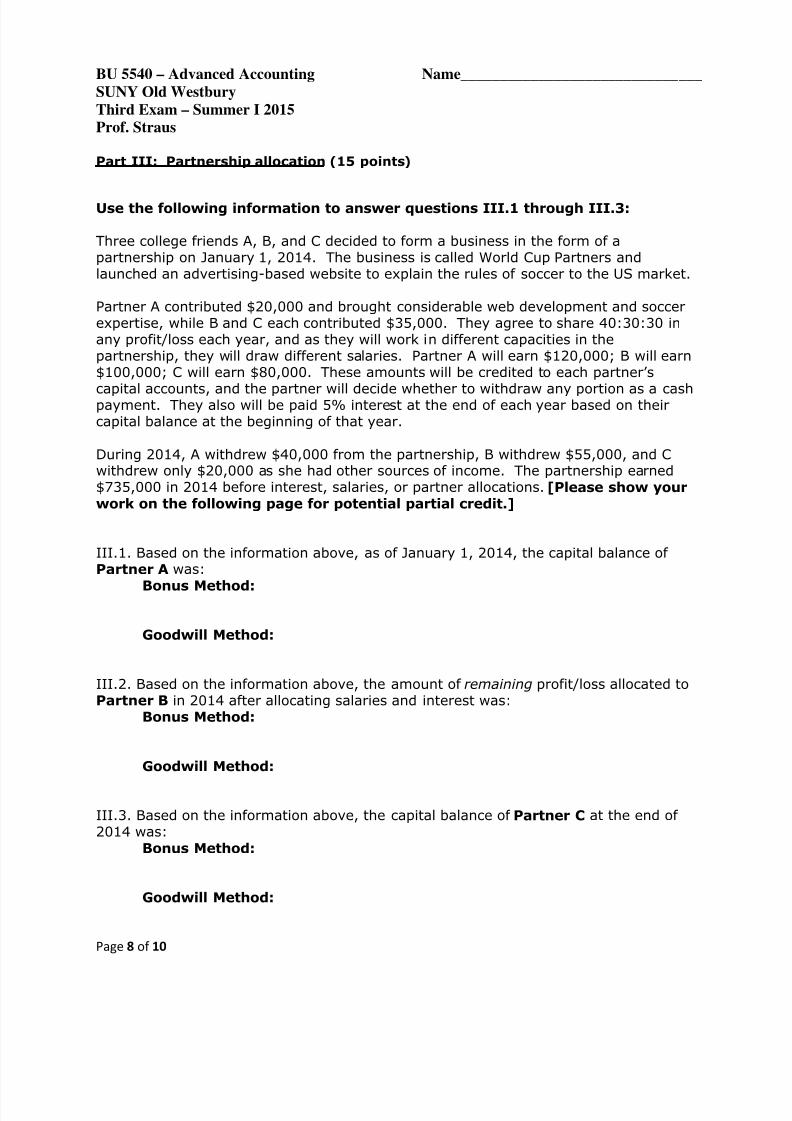

Part III: Partnership allocation (15 points)

Use the following information to answer questions III.1 through III.3:

Three college friends A, B, and C decided to form a business in the form of apartnership on January 1, 2014. The business is called World Cup Partners andlaunched an advertising-based website to explain the rules of soccer to the US market.

Partner A contributed $20,000 and brought considerable web development and soccerexpertise, while B and C each contributed $35,000. They agree to share 40:30:30 inany profit/loss each year, and as they will work in different capacities in thepartnership, they will draw different salaries. Partner A will earn $120,000; B will earn$100,000; C will earn $80,000. These amounts will be credited to each partner’s

capital accounts, and the partner will decide whether to withdraw any portion as a cashpayment. They also will be paid 5% interest at the end of each year based on theircapital balance at the beginning of that year.

During 2014, A withdrew $40,000 from the partnership, B withdrew $55,000, and Cwithdrew only $20,000 as she had other sources of income. The partnership earned$735,000 in 2014 before interest, salaries, or partner allocations. [Please show yourwork on the following page for potential partial credit.]

III.1. Based on the information above, as of January 1, 2014, the capital balance ofPartner A was:

Bonus Method:

Goodwill Method:

III.2. Based on the information above, the amount of remaining profit/loss allocated toPartner B in 2014 after allocating salaries and interest was:

Bonus Method:

Goodwill Method:

III.3. Based on the information above, the capital balance of Partner C at the end of2014 was:

Bonus Method:

Goodwill Method:

7/18/2019 BU5540 Exam 3 Summer I 2015(1)

http://slidepdf.com/reader/full/bu5540-exam-3-summer-i-20151 9/10

BU 5540 – Advanced Accounting Name_______________________________

SUNY Old Westbury

Third Exam – Summer I 2015

Prof. Straus

Page

9 of 10

Bonus Method A B C Total

Initial Capital

Goodwill Metho A B C Total

Initial Capital

7/18/2019 BU5540 Exam 3 Summer I 2015(1)

http://slidepdf.com/reader/full/bu5540-exam-3-summer-i-20151 10/10

BU 5540 – Advanced Accounting Name_______________________________

SUNY Old Westbury

Third Exam – Summer I 2015

Prof. Straus

Page

10 of 10

Part IV: Partnership formation/operation (24 points)

Complete the following problems from Chapter 14 in the textbook in Excel, and show allwork in arriving at the answers. No credit will be given if the correct letter answer ischosen if you do not show the calculation correctly in Excel. Attach your Excel fileseparately.

Problems from pages 657-659:

5.

6.

7.

8.

9.

10.

13.

14.

Part V: Partnership liquidation (15 points)

Complete the following problems from Chapter 15 in the textbook in Excel, and show allwork in arriving at the answers. No credit will be given if the correct letter answer ischosen if you do not show the calculation correctly in Excel. Attach your Excel fileseparately.

Problems from page 690:

7.

8.

9.