Embed Size (px)

Citation preview

1

Buffett’sAssetAllocationAdvice:TakeIt…WithaTwist

JavierEstradaIESEBusinessSchool,DepartmentofFinance,Av.Pearson21,08034Barcelona,Spain

Tel:+34932534200,Fax:+34932534343,Email:[email protected]

AbstractOneofthemostimportantdecisionsretireesneedtomakeistheassetallocationoftheirportfolios.Theycanhaveastaticoradynamicallocation,andsimplicityusuallyfavorstheformer.WarrenBuffettrecentlyaddedanothervoteforstaticallocationsbyrevealingthathehadadvisedatrusteetosplitthebequesthiswifewillreceive90%instocksand10%inshort‐termbonds.Theevidencediscussedhereshowsthat,relativetootherstaticallocations,a90/10splithasaverylowfailurerateandprovidesinvestorswithverygoodupsidepotentialanddownsideprotection.Theevidencealsoshowsthattwominortwiststothe90/10splitresultintwoverysimpledynamicstrategieswithevenbetterupsidepotentialanddownsideprotection.

November,2015

1.Introduction

Retirees need to carefully balance the risk of spending too much and outliving their

savingswiththeriskofspendingtoo littleand lowering their lifestyleunnecessarily.The two

maintoolstheycanusetoavoidfallingoneithersideofthecliffaretheportfolio’swithdrawal

rate and asset allocation. Regarding the latter, in his 2013 letter to Berkshire Hathaway

shareholders,WarrenBuffettdiscussedthesimpleadvicehegavetothetrusteethatwillmanage

thebequesthiswifewillreceive:

“WhatIadvisehereisessentiallyidenticaltocertaininstructionsI’velaidoutinmywill.One bequestprovides that cashwill be delivered toa trustee formywife’sbenefit…Myadvicetothetrusteecouldnotbemoresimple:Put10%ofthecashinshort‐termgovernmentbondsand90% inavery low‐costS&P500 index fund.(IsuggestVanguard’s.)Ibelievethetrust’slong‐termresultsfromthispolicywillbesuperiortothoseattainedbymostinvestors–whetherpensionfunds,institutionsorindividuals–whoemployhigh‐feemanagers.”(Page20)

Buffettdoessuggestinhisletterthatinvestorsshouldfollowasimpleapproach,passively

investinginabroadly‐diversified,low‐costportfolio;hedoesnotsuggestorimply,however,that

investorsshouldhavea90/10stock/bondallocation.Andyethiscommentbegsthequestion:Is

theassetallocationBuffettadvisedforhiswifeappropriateforotherinvestors?Ifyes,why?If

not,whynot?

IwouldliketothankJackRaderforhiscomments.JavierZazurcaandDavidTamayoprovidedvaluableresearchassistance.Theviewsexpressedbelowandanyerrorsthatmayremainareentirelymyown.

2

AnobviousdistinctionbetweenBuffett’swifeandtheaverageinvestorquicklycomesto

mind.Theaverageinvestorneedstoimplementanassetallocationthatcarefullybalancesthetwo

risksalreadymentioned,overspendingandunderspending.Buffett’swife,however,islikelyto

receiveanestegglargeenoughsothatshewillnothavetoworryabouteitherrisk.Putdifferently,

justaboutanyassetallocationwillenableBuffett’swifetolivecomfortablyandstilloutliveher

portfolio,whichisnotthecaseformostinvestors.

Thatsaid,thisarticleevaluatesthemeritsofthe90/10allocationthatBuffettadvisedfor

hiswife,relativetootherstaticallocationswithdifferentstock/bondproportions,forinvestors

atlarge.Furthermore,itexplorestwominortwiststothe90/10allocation,onethataccountsfor

thebehaviorofthestockmarket,andtheotherthataccountsfortherelativebehaviorofthestock

andbondmarkets.

Inanutshell,theevidencediscussedheresuggeststhat,besideshavingaverylowfailure

rate,the90/10allocationresultsinaninterestingmiddlegroundbetweentheupsidepotential

ofmoreaggressive staticallocationsand thedownsideprotectionofmoreconservativestatic

allocations.Perhapsmoreinterestingly,theminortwistsconsideredresult intwoverysimple

dynamicstrategiesthatincreaseboththeupsidepotentialandthedownsideprotectionofthe

90/10allocationsuggestedbyBuffett.

Therestofthearticleisorganizedasfollows.Section2discussesinmoredetailtheissue

at stake; section3 discusses the evidence, first considering several static strategies, and then

consideringtwosimpletwiststothe90/10allocation;andsection4providesanassessment.

2.TheIssue

Aretiree’spropermanagementofhisnesteggrequiresacarefulbalancingoftwofinancial

risks.Ontheonehand,theretireemayspendtoomuchandoutlivehissavings;ontheotherhand,

the retireemay unnecessarily lower his lifestyle and end upwith an unintended bequest. A

massiveliteratureonsustainableretirementportfoliosultimatelyseekstoguideretireesonhow

toproperly balance these risks. It iswidelyacknowledged thatBengen (1994) is the seminal

articlethatinspiredthevastamountofresearchproducedonthistopic.

Bengen (1994) pioneered the idea of considering withdrawal rates over all possible

historicalrolling(overlapping)periods.Heaimedtofindhowmanyyearsaportfoliowouldhave

lasted given an initial withdrawal rate and subsequent inflation‐adjusted withdrawals,

performingtheevaluationatthebeginningofeveryyearstartingin1926.1Givena50‐50stock‐

1Theinitialwithdrawalrateisdefinedastheinitialwithdrawalrelativetothevalueoftheportfolioatthebeginningofretirement.Unlessotherwisestated,inthisliteraturea‘withdrawalrate’typicallyreferstotheinitialwithdrawalrate,implicitlyassumingsubsequentinflation‐adjustedwithdrawals.Notethatthisimpliesthatthecurrentwithdrawalrate(thewithdrawalrelativetothevalueoftheportfolioatanypointintime)canfluctuatewidelyovertime.

3

bondallocationhefoundthata3%withdrawalratewouldhaveneverexhaustedaportfolioin

lessthan50years,anda4%withdrawalratewouldhaveneverexhaustedaportfolioinlessthan

33years.Hecalleda5%withdrawalrate‘risky’andwithdrawalrates6%orhigher‘gambling’

becausetheywouldhaveexhaustedaportfoliomuchsoonerovermanyhistoricalperiods.He

alsocalledthe4%withdrawalrate‘safe’becauseitneverexhaustedaportfolioinlessthan30

years,whichhethoughtofastheminimumrequirementofportfoliolongevity.Thiswastheorigin

ofthewell‐knownandwidely‐used‘4%rule.’

2.1.SomeRelevantDifferences

Thevast literature spannedbyBengen (1994)doesnotofferaconsensus regarding a

sustainable withdrawal rate for retirees. This is the case because different articles consider

different methodologies, time periods, assets, asset allocations, acceptable failure rates, and

retirementperiods,tonamebutsomedifferences,andthereforereachverydifferentconclusions

both on the sustainability of the 4% withdrawal rate and on the specific withdrawal rate

recommendedtoretirees.

Mostofthearticlesintheliteraturerelyononeoftwomethodologies,historicalrolling

(overlapping) periods andMonte Carlo (or bootstrapping) simulations. Bengen (1994, 1996,

1997)andCooleyetal(1998)areearlyapplicationsofthefirstmethodology;Pye(2000)and

Ameriksetal (2001)areearlyapplicationsof thesecond.Cooleyetal (2003b) compareboth

approaches and find that their results and recommendations sometimes are similar and

sometimesdiffer.Theydonottakesidesonwhichmethodologyisbetterandultimatelyargue

thatwhicheverapproachhappenstomoreaccuratelyreflectthe(unknown)distributionoffuture

returnswillproducethemoreplausibleresultsandrecommendations.

Thearticlesintheliteraturealsodifferintheassetstheyconsider.Althoughmostarticles

focusonstocksandbonds,differenttypesofstocksandbondsanddifferentassetclasseswere

introduced over time. Bengen (1997) considers small‐cap stocks; Pye (2000) considers TIPS;

Cooleyetal(2003a)considerinternational(EAFE)stocks;Guyton(2004)considersvaluestocks;

andCassaday(2006)considersrealestateandcommodities.

Animportantaspect,whichdifferswidelyacrossthearticlesintheliterature,isthefailure

rateconsideredtobeacceptabletoaretiree.Inotherwords,differentwithdrawalratesimply

differentprobabilitiesof portfoliodepletionbefore the endof the retirementperiod, someof

whicharetireemayfindacceptableandsomeofwhichhemaynot.Ononeextreme,Cooleyetal

(2003b,2011)arguethata25%failurerateisreasonable;ontheother,Terry(2003)arguesthat

failure rates 5%or higher are unacceptable. Spitzer et al (2007) plot a relationship between

withdrawalratesandfailureratesandhighlightthata4%withdrawalratecanbethoughtofas

safeaslongasa6%probabilityoffailureisacceptable.

4

Theretirementperiodsconsideredintheliteraturealsovarywidely.Although30years

seemstobeby far themostwidely‐usedalternative(andtheoneusedin thisarticle),onone

extremeCooleyetal(2005)focusonafive‐yearperiod,andontheotherBlanchettandFrank

(2009)considerupto50years.Somearticlestakeadifferentapproachandbasetheexpected

retirementperiodonmortalitytables,suchasMilevskyandRobinson(2005),StoutandMitchell

(2006),andSheikhetal(2014).

Finally,manyarticlesintheliteratureconsideraninitialwithdrawalrateandsubsequent

inflation‐adjustedwithdrawals,suchasBengen(1994,1996),whopioneeredtheapproach.Many

other articles, however, consider a wide variety of dynamic withdrawal rules, most of them

dependingonportfolioperformance.Someaddsimple floors and ceilings to thewithdrawals,

suchasBengen(2001)andJaconettietal(2013);someaddmorecomplexfloorsandceilings,

suchasGuytonandKlinger(2006)andStout(2008);2somemakeperiodicre‐evaluationsoflife

expectancy(Dusetal,2005),theprobabilityoffailure(BlanchettandFrank,2009),orseveral

variables(Sheikhetal,2014);andsomelinkthewithdrawalratetofundamentalvariablessuch

asthecyclically‐adjustedP/Eratio(Kitces,2008;Pfau,2011;andKitcesandPfau,2014).

2.2.TheEvolutionofAssetAllocationDuringRetirement

Mostofthearticlesintheliteratureconsiderdifferentassetallocations.Inhispioneering

article,forexample,Bengen(1994)basesmostofhisdiscussionona50‐50stock‐bondallocation

butalsoconsidersportfolioswith0%,25%,75%,and100%instocks(andtherestinbonds).

Considering different asset allocations, however, is different from considering how the asset

allocationshouldevolveduringretirement,whichisthefocusofthisarticle.3Threepossibilities

areconsideredhere,namely,declining‐equity(DE)strategies,rising‐equity(RE)strategies,and

staticstrategies.

Bengen(1994)doesnotexplicitlyconsidertheevolutionoftheassetallocationduring

retirement, but he does recommend a 50‐75%exposure to stocks and argues that it “can be

maintained throughout retirement.” Bengen (1996), in turn, explicitly considerswhether the

assetallocationshouldbeadjustedduringtheretirementperiod.Moreprecisely,heconsiders

annualreductionsintheallocationtostocksbetween0.5%and3%;findsanegativerelationship

betweentherateofdecreaseoftheallocationtostocksandsustainablewithdrawalrates;and

2Itisfarfromclearthatmorecomplexrulesimproveuponsimplerones.Infact,someofthecomplexrulesinthe literatureseemtobemeticulouslydesignedtoworkwell(orbetterthansimpleralternatives) insample.Thisoverfittingofthedataoftenleadstopoorbehavioroutofsample.3Thearticlesthatconsiderdifferentassetallocations,butnotitsevolutionduringtheretirementperiod,tendtoagreethatahigherexposuretostocksismorelikelytosupportahigherwithdrawalrate.Earlyrecommendations, such asCooley et al (1998), suggest an exposure to stocks of at least 50%;Bengen(1994)recommendsa50‐75%exposure,andMilevskyetal(1997)arguethatmanyretireeswouldbenefitfroma70‐100%exposure.

5

ultimatelyrecommendstophasedowntheexposuretostocksattheannualrateof1%(asthe

‘ageinbonds’rulewould).Sheikhetal(2014)alsorecommendaDEstrategy,andthereforean

increasingly‐conservativeportfolio,duringretirement.

Unsurprisingly,noteverybodyagreeswiththisrecommendation.Infact,somearguejust

theoppositeandrecommendanREstrategy.SpitzerandSingh(2006,2007)suggestthatretirees

shouldfirstmakewithdrawalsfromthebondportionoftheirportfolios,andstartwithdrawing

fromstocks only afterbonds are depleted. This recommendationwould gradually reduce the

exposuretobondsintheportfolio,thusimplyinganREglidepathandanincreasinglyaggressive

portfolio.PfauandKitces(2014)explicitlycompareDEandREstrategiesduringretirementand

findthatthelatter,whichtheyrecommend,exposeretireestoalowerprobabilityoffailure.

An intermediate possibility is a static or constant‐equity strategy. Blanchett (2007)

considers several types of rising/declining/static‐equity strategies; finds that despite their

simplicitystaticallocationsare“remarkablyefficient”distributionstrategies;andconcludesthat

a60‐40stock‐bondallocationislikelytobeoptimalformostretirees.Cohenetal(2010)argue

thatforanygivenDEstrategy,astaticstrategywithahigherrisk‐adjustedreturncanbecreated

and ultimately recommend a 32‐68 stock‐bond static allocation for retirees. Kitces and Pfau

(2014)alsoconsiderseveraltypesofrising/declining/static‐equitystrategiesandfindthata60‐

40stock‐bondallocationisnearlyoptimalinmostsituations.Theresultsdiscussedinthenext

section also yield support both to static strategies in general and (the all‐equity strategy

notwithstanding)toa60‐40stock‐bondallocationinparticular.

Afinalpossibilityisastrategyinwhichtheexposuretostocksneitherdeclinesorrisesat

apredeterminedratenordoes it remainsconstant; rather, theassetallocation isdynamically

adjusted depending on the value of some observable (technical or fundamental) variable.

Garrison et al (2010), for example, use a 12‐month moving average of large‐cap stocks to

determinewhetheraportfolioshouldbefullyinvestedinbondsorstocks.Pfau(2012),inturn,

uses thecyclically‐adjustedP/Eratio todeterminewhether the exposure to stocks shouldbe

25%,50%,or75%,with the rest invested inbonds.Botharticles findsupport for adynamic,

valuation‐basedassetallocationapproach.

Needlesstosay,bothstaticanddynamicstrategieshaveprosandcons.Staticstrategies

aresimpleandrequirelittleinformation.However,theymaygetincreasinglydifficultforretirees

tomaintainiftheallocationisaggressive(thinka90/10splitforan70‐yearoldindividualwitha

modest portfolio) and ignore valuation considerations even in extreme situations (think

December,1999).

Dynamicstrategies,ontheotherhand,seemto‘feelright’inthesensethattheymayget

progressivelymoreconservative(thinktheage‐in‐bondsrule)ortakevaluationconsiderations

intoaccount, thusaiming toavoidhighexposure toovervaluedassets.However, theymaybe

6

difficultforretireestoimplementandrequireinformationaboutvaluationthatretireesmaynot

haveorunderstand.

Bothstaticanddynamicstrategiesareconsideredinthisarticle.Amongtheformer,eight

assetallocationswithvaryingstock/bondproportionsareevaluated,withspecialattentiontothe

90/10split suggestedbyBuffett.Among the latter, twominor (valuation‐based) twists to the

90/10allocationareevaluatedandcomparedtoboththe90/10andthe60/40allocations;the

firsttwistfocusesonthevaluationofthestockmarketandthesecondontherelativevaluation

ofthestockandbondmarkets.

Importantly,thetwodynamictwistsconsideredinthisarticlearetrivialtoimplement.

Retireesonlyneedinformationabouttheperformanceofstocks,orthatofstocksandbonds,over

thepreviousyear,whichispubliclyandwidelyavailable.Retireesdonotneedtoknowtoolsof

fundamentalanalysis(suchastheP/EorCAPE)ortechnicalanalysis(suchasmovingaverages

orcharts),nordotheyneedtomakejudgementsonthevaluationofstocksandbonds.

3.Evidence

ThissectiondiscussestheevidenceasitappliestotheUSmarketoverthe115‐yearperiod

between 1900 and2014. The first part discusses the data andmethodology; the secondpart

evaluatesstaticstrategies;andthethirdpartevaluatestwosimpledynamictwiststothe90/10

allocation.

3.1.DataandMethodology

TheanalysisisbasedonthetwoassetclassessuggestedbyBuffett,stocksandshort‐term

government bonds (US Treasury bills), both represented by Dimson‐Marsh‐Staunton indices,

describedindetailinDimsonetal(2002,2015).Returnsareannual,adjustedbyinflation,and

account for capital gains/losses and cash flows. Over the 1900‐2014 period considered here

stocks and bonds hadmean annual compound (real) returns of 6.5% and 0.9%,with annual

volatilityof20.0%and4.6%.

BecauseBuffettdoesnotintendtorecommendthe90/10allocationtoallinvestorsand

isthereforesketchyondetails,afewassumptionswillbemadetoevaluatetheperformanceof

this strategy. It will be assumed, first, that Buffett suggests tomaintain the 90/10 allocation

constantovertime;second,thatinordertomaintainthe90/10allocationconstanttheportfolio

isrebalancedonceayear;andthird,thattheannualwithdrawalismadeproportionaltotheasset

allocation, which implies withdrawing 90% from stocks and 10% from bonds. The last two

assumptions,annualrebalancingandproportionalwithdrawals,willbeappliedtoalltheother

staticstrategiesconsidered.Thesecondassumption,annualrebalancing,willalsobeappliedto

thetwodynamictwiststothe90/10allocation.

7

The analysis is based on a $1,000 nest egg at the beginning of retirement, an initial

withdrawalof4%ofthenestegg,subsequentwithdrawalsannuallyadjustedbyinflation,anda

30‐year retirementperiod.At thebeginningof eachyear the annualwithdrawal ismade, the

portfolioisthenrebalanced(shouldthestrategycallforrebalancing)tothetargetallocationfor

theyear,andthenitcompoundsattheobservedreturnofstocksandbondsforthatyear.This

processisrepeatedatthebeginningofeachyearduringthe30‐yearretirementperiod,attheend

ofwhichtheportfoliohasaterminalwealthorbequestthatmaybepositiveor0.Thefirst30‐

yearretirementperiodconsideredis1900‐1929andthelastoneis1985‐2014,foratotalof86

rolling(overlapping)periods.

Theanalysisfocusesonthefailurerate,aswellasontheupsidepotentialanddownside

protectionprovidedbythestrategiesconsidered.Thefailurerateisdefinedastheproportionof

the86 retirementperiods considered inwhich theportfoliowasdepletedbefore30 years; if

history is any guide, this failure rate should be a good proxy for the expected probability of

portfolio failure. Both upside potential and downside protection are assessed from the

distributionofterminalwealthorbequest,whichresultsfromaggregatingthe86wealthlevels

attheendofeachofthe86periodsconsidered.

3.2.StaticStrategies

ThefirststepinordertoassessBuffett’sadviceistoconsiderseveralstaticstock/bond

allocationsthatcanbecomparedtothe90/10allocationsuggestedbyBuffett.Tothatpurpose,

Exhibit1reportstheresultsforeightstaticstrategieswithstock/bondallocationsrangingfrom

100/0to30/70,inallcasesrebalancedannuallytothestatedproportions.Theanalysisofupside

potentialanddownsideprotectionfollowsalongthelinessuggestedbyEstrada(2014a,2014b,

2014c,2016).

Thestrategies thatcall forequityholdingsbetween100%and40%havevery similar

failurerates,nothigherthan3.5%.Onlywhentheproportionofstocksisatorbelow30%the

failurerateincreasesconsiderably,inallcasesabove10%.4Althoughtherearevariedopinions

regardingwhatisanacceptablefailurerate,mostpractitionersseemtoagreethatfailurerates

below5%shouldbeviewedasacceptablebymostretirees.Inshort,althoughthe60/40strategy

neverfailed,the100/0and40/60failed3.5%ofthetime,andBuffett’s90/10failed2.3%ofthe

time,theredoesnotseemtobeasubstantialdifferenceinthefailureratesofportfoliosholding

atleast40%instocks.

4Astheexhibitshows,the30/70strategyhasafailurerateof12.8%.Strategieswithlowerproportionofstocks(20‐80,10‐90,and0‐100)havesubstantiallyhigherfailurerates(25.6%,43.0%,67.4%)andareneitherreportedintheexhibitnorfurtherconsideredintheanalysis.

8

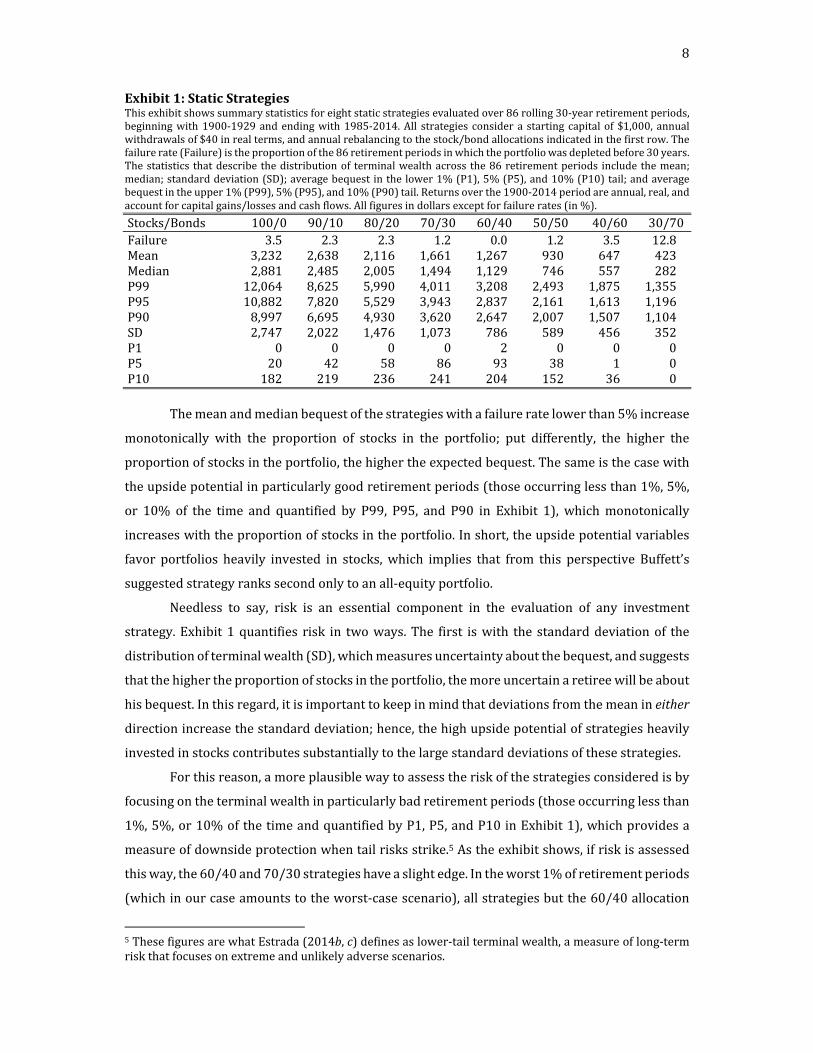

Exhibit1:StaticStrategiesThisexhibitshowssummarystatisticsforeightstaticstrategiesevaluatedover86rolling30‐yearretirementperiods,beginningwith1900‐1929andendingwith1985‐2014.All strategies considera starting capitalof $1,000, annualwithdrawalsof$40inrealterms,andannualrebalancingtothestock/bondallocationsindicatedinthefirstrow.Thefailurerate(Failure)istheproportionofthe86retirementperiodsinwhichtheportfoliowasdepletedbefore30years.Thestatistics thatdescribe thedistributionof terminalwealthacross the86retirementperiods include themean;median;standarddeviation(SD);averagebequestinthelower1%(P1),5%(P5),and10%(P10)tail;andaveragebequestintheupper1%(P99),5%(P95),and10%(P90)tail.Returnsoverthe1900‐2014periodareannual,real,andaccountforcapitalgains/lossesandcashflows.Allfiguresindollarsexceptforfailurerates(in%).

Stocks/Bonds 100/0 90/10 80/20 70/30 60/40 50/50 40/60 30/70Failure 3.5 2.3 2.3 1.2 0.0 1.2 3.5 12.8Mean 3,232 2,638 2,116 1,661 1,267 930 647 423Median 2,881 2,485 2,005 1,494 1,129 746 557 282P99 12,064 8,625 5,990 4,011 3,208 2,493 1,875 1,355P95 10,882 7,820 5,529 3,943 2,837 2,161 1,613 1,196P90 8,997 6,695 4,930 3,620 2,647 2,007 1,507 1,104SD 2,747 2,022 1,476 1,073 786 589 456 352P1 0 0 0 0 2 0 0 0P5 20 42 58 86 93 38 1 0P10 182 219 236 241 204 152 36 0 Themeanandmedianbequestofthestrategieswithafailureratelowerthan5%increase

monotonically with the proportion of stocks in the portfolio; put differently, the higher the

proportionofstocksintheportfolio,thehighertheexpectedbequest.Thesameisthecasewith

theupsidepotentialinparticularlygoodretirementperiods(thoseoccurringlessthan1%,5%,

or 10% of the time and quantified by P99, P95, and P90 in Exhibit 1), whichmonotonically

increaseswiththeproportionofstocksintheportfolio.Inshort,theupsidepotentialvariables

favor portfolios heavily invested in stocks,which implies that from this perspective Buffett’s

suggestedstrategyrankssecondonlytoanall‐equityportfolio.

Needless to say, risk is an essential component in the evaluation of any investment

strategy.Exhibit1quantifies risk in twoways.The first iswith the standarddeviationof the

distributionofterminalwealth(SD),whichmeasuresuncertaintyaboutthebequest,andsuggests

thatthehighertheproportionofstocksintheportfolio,themoreuncertainaretireewillbeabout

hisbequest.Inthisregard,itisimportanttokeepinmindthatdeviationsfromthemeanineither

directionincreasethestandarddeviation;hence,thehighupsidepotentialofstrategiesheavily

investedinstockscontributessubstantiallytothelargestandarddeviationsofthesestrategies.

Forthisreason,amoreplausiblewaytoassesstheriskofthestrategiesconsideredisby

focusingontheterminalwealthinparticularlybadretirementperiods(thoseoccurringlessthan

1%,5%,or10%ofthetimeandquantifiedbyP1,P5,andP10inExhibit1),whichprovidesa

measureofdownsideprotectionwhentailrisksstrike.5Astheexhibitshows,ifriskisassessed

thisway,the60/40and70/30strategieshaveaslightedge.Intheworst1%ofretirementperiods

(whichinourcaseamountstotheworst‐casescenario),allstrategiesbutthe60/40allocation

5ThesefiguresarewhatEstrada(2014b,c)definesaslower‐tailterminalwealth,ameasureoflong‐termriskthatfocusesonextremeandunlikelyadversescenarios.

9

fail; in the worst 5% of retirement periods, the 60/40 allocation yields the highest terminal

wealth; and in theworst 10% of retirement periods, the 70/30 allocation yields the highest

terminalwealth.

Importantly, the90/10strategysuggestedbyBuffettdoesnotperformmuchworsein

termsofdownsideprotection.Toputthefiguresaboveinperspective,recallthattheanalysisis

performed in real terms and that the annual withdrawal is $40. Hence, in the worst 5% of

retirementperiods(P5),the90/10allocationunderperformsthe60/40splitbyjustabitmore

thanthevalueofoneannualwithdrawal(whichfollowsfromcomparing$42to$93);andinthe

worst10%ofretirementperiods(P10),the90/10allocationunderperformsthe70/30splitby

justabitmorethanthevalueofhalfanannualwithdrawal(comparing$219to$241).

Inshort,then,asfarasstaticstrategiesisconcerned,Buffett’ssuggestedallocationhasa

very low(althoughnot the lowest) failurerate;averyhigh (althoughnot thehighest)upside

potential;andprovidesverygood(butnotthebest)downsideprotectionwhentailrisksstrike.

Putdifferently,Buffett’ssuggestedallocationseemstoprovideamiddlegroundbetweenthebest‐

performing strategy (100/0) in terms of upside potential and the best‐performing strategies

(60/40and70/30)intermsofdownsideprotection.

3.3.TweakingBuffett’sAdvice

TheevidencediscussedsofarsuggeststhatBuffett’sadviceis(perhapsunsurprisingly)

bothsoundandsimpleenoughforanyretireetoimplement,atleastasfarasstaticstrategiesis

concerned.Thatsaid,itmaybeworthexploringtwominordynamictwists,bothofwhicharevery

simpletoimplement.

Thefirsttwist(T1)relatestheannualwithdrawaltothebehaviorofthestockmarketin

thepreviousyear.Moreprecisely,ifstockshavegoneup,theretireetakestheannualwithdrawal

fromstocksandthenrebalancestheportfoliobacktothe90/10allocation;ifstockshavegone

down,theretireetakestheannualwithdrawalfrombondsanddoesnotrebalancetheportfolio.

Thesecondtwist(T2)relatestheannualwithdrawaltotherelativebehaviorofthestock

andbondmarketsinthepreviousyear.Moreprecisely,ifthereturnofstockshasbeenhigher

thanthatofbonds,theretireetakestheannualwithdrawalfromstocksandthenrebalancesthe

portfoliobacktothe90/10allocation;ifthereturnofstockshasbeenlowerthanthatofbonds,

theretireetakestheannualwithdrawalfrombondsanddoesnotrebalancetheportfolio.

Thesedynamictwistsaimtoavoidwithdrawingfromstockswhenthesehavegonedown

(T1)orperformedworsethanbonds(T2).Fromthisperspective,theyareinspiredinthebucket

approachwidelydiscussedbyChristineBenzinseveralMorningstararticles,andareultimately

basedontheconceptofmeanreversioninstocks.Withdrawingfrombondswhenstockshave

performedbadly,inabsoluteorrelativeterms,buysthetimethatstocksneedtosoonerorlater

10

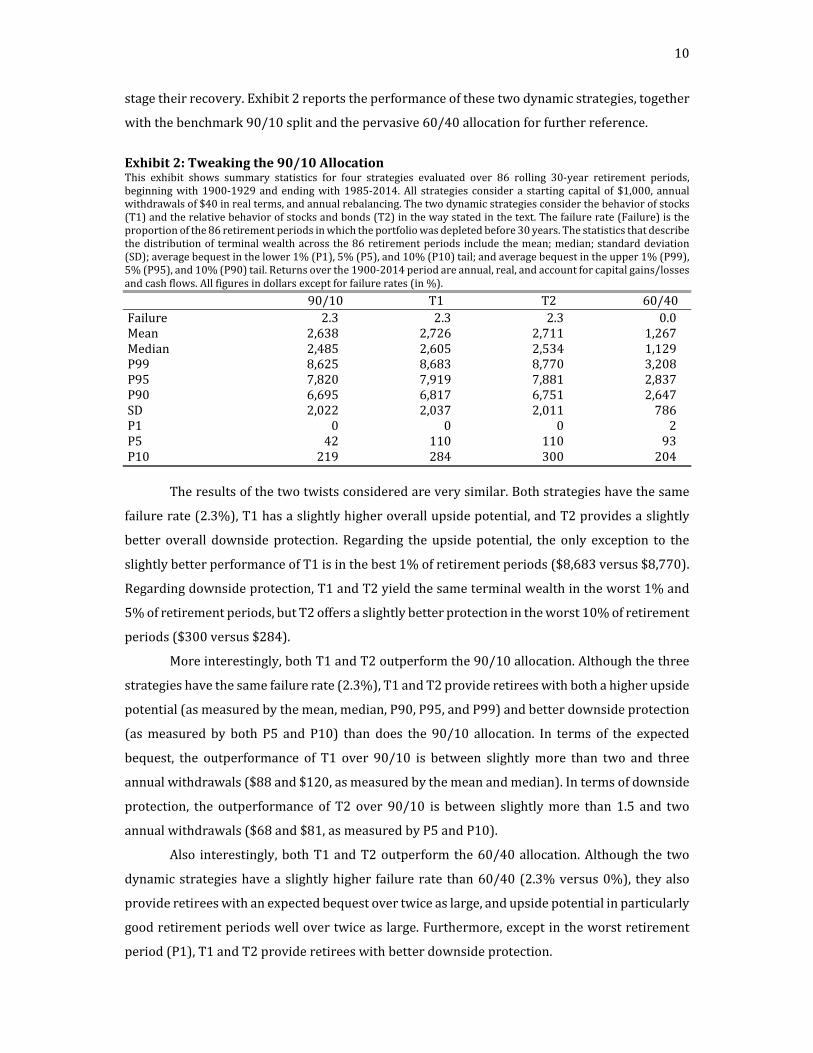

stagetheirrecovery.Exhibit2reportstheperformanceofthesetwodynamicstrategies,together

withthebenchmark90/10splitandthepervasive60/40allocationforfurtherreference.

Exhibit2:Tweakingthe90/10AllocationThis exhibit shows summary statistics for four strategies evaluated over 86 rolling 30‐year retirement periods,beginningwith1900‐1929andendingwith1985‐2014.All strategies considera starting capitalof $1,000, annualwithdrawalsof$40inrealterms,andannualrebalancing.Thetwodynamicstrategiesconsiderthebehaviorofstocks(T1)andtherelativebehaviorofstocksandbonds(T2)inthewaystatedinthetext.Thefailurerate(Failure)istheproportionofthe86retirementperiodsinwhichtheportfoliowasdepletedbefore30years.Thestatisticsthatdescribethedistributionofterminalwealthacrossthe86retirementperiodsincludethemean;median;standarddeviation(SD);averagebequestinthelower1%(P1),5%(P5),and10%(P10)tail;andaveragebequestintheupper1%(P99),5%(P95),and10%(P90)tail.Returnsoverthe1900‐2014periodareannual,real,andaccountforcapitalgains/lossesandcashflows.Allfiguresindollarsexceptforfailurerates(in%).

90/10 T1 T2 60/40Failure 2.3 2.3 2.3 0.0Mean 2,638 2,726 2,711 1,267Median 2,485 2,605 2,534 1,129P99 8,625 8,683 8,770 3,208P95 7,820 7,919 7,881 2,837P90 6,695 6,817 6,751 2,647SD 2,022 2,037 2,011 786P1 0 0 0 2P5 42 110 110 93P10 219 284 300 204 Theresultsofthetwotwistsconsideredareverysimilar.Bothstrategieshavethesame

failurerate(2.3%),T1hasaslightlyhigheroverallupsidepotential,andT2providesaslightly

better overall downside protection. Regarding theupsidepotential, the only exception to the

slightlybetterperformanceofT1isinthebest1%ofretirementperiods($8,683versus$8,770).

Regardingdownsideprotection,T1andT2yieldthesameterminalwealthintheworst1%and

5%ofretirementperiods,butT2offersaslightlybetterprotectionintheworst10%ofretirement

periods($300versus$284).

Moreinterestingly,bothT1andT2outperformthe90/10allocation.Althoughthethree

strategieshavethesamefailurerate(2.3%),T1andT2provideretireeswithbothahigherupside

potential(asmeasuredbythemean,median,P90,P95,andP99)andbetterdownsideprotection

(asmeasured by both P5 andP10) than does the 90/10 allocation. In terms of the expected

bequest, the outperformance of T1 over 90/10 is between slightlymore than two and three

annualwithdrawals($88and$120,asmeasuredbythemeanandmedian).Intermsofdownside

protection, the outperformance of T2 over 90/10 is between slightlymore than 1.5 and two

annualwithdrawals($68and$81,asmeasuredbyP5andP10).

Also interestingly,bothT1andT2outperformthe60/40allocation.Although the two

dynamicstrategieshaveaslightlyhigher failurerate than60/40(2.3%versus0%), theyalso

provideretireeswithanexpectedbequestovertwiceaslarge,andupsidepotentialinparticularly

goodretirementperiodswellovertwiceaslarge.Furthermore,exceptintheworstretirement

period(P1),T1andT2provideretireeswithbetterdownsideprotection.

11

Finally,althoughitcanhardlybearguedthatobservingtheperformanceofthestockand

bondmarkets is challenging, it is in fact simpler to justobserve theperformanceof thestock

market(which,ingeneral,ismorereadilyavailablethanthatofthebondmarket).Thus,giventhe

verysimilarperformanceofthetwotwistsconsidered,T1,whichonlyrequirestoobservethe

performanceofstocks,maybeviewedashavingaslightedgeoverT2,whichrequirestoobserve

theperformanceofbothstocksandbonds.

4.Assessment

Thereisamassiveliteraturethatdiscussestwoofthemostimportantfinancialdecisions

retireesneedtomake,namely,thewithdrawalrateandtheassetallocationoftheirportfolios.

This article focused on the latter, and more specifically on the performance of the 90/10

allocationWarrenBuffettadvisedatrusteetoimplementforthebequesthiswifewillreceive.

This 90/10 allocation was evaluated first relative to other static strategies, and then

relative to twoverysimple,dynamic,valuation‐basedstrategies.Eachof the latteronlyadda

minor twist to theallocationsuggestedbyBuffett,basedon theperformanceof stocksor the

relativeperformanceofstocksandbonds.

Whencomparedtootherstaticallocations,the90/10splitsuggestedbyBuffettperforms

wellintermsofthefailurerate,upsidepotential,anddownsideprotection.Infact,itprovidesan

interestingmiddlegroundbetweentheupsidepotentialofmoreaggressivestaticallocationsand

thedownsideprotectionofmoreconservativestaticallocations.Putdifferently,Buffett’sadvice

provestobe(unsurprisingly)notonlysimplebutalsosound.

Thatsaid,thetwosimpletwistsconsideredhereimproveboththeupsidepotentialand

thedownsideprotectionof the90/10allocation.These two twists require retireesneither to

collectvastamountsofinformationnortomakeanyvaluationjudgmentsbutonlytoobservethe

performanceof thestockmarket,or the relativeperformanceof thestockandbondmarkets.

Eitherway,retireescan,withlittleeffort, improveupontheresultsofthe90/10allocation.In

fact,becausetheperformanceofthetwotwistsconsideredissosimilar,retireesmaywanttolean

towards the first one (T1) and simply adjust their asset allocation according to theobserved

performanceofstocks.

Buffett’sassetallocationadviceissoundandsimple,andyetmanyretireesmaybalkat

thethoughtofholdingsuchanaggressiveportfolio.Ifthatisthecase,thetwotwistsconsidered

here may help a little, but probably not enough. However, those retirees that find a 90/10

portfolioacceptablearelikelytofindthatwithaninsignificantadditionaleffort,observingthe

performanceofstocksandimplementingthefirsttwistdiscussed,theyarelikelytoimprovethe

performanceoftheirportfolios.

12

ReferencesAmeriks,John,RobertVeres,andMarkWarshawsky(2001).“MakingRetirementIncomeLastaLifetime.”JournalofFinancialPlanning,December,60‐76.Bengen, William (1994). “Determining Withdrawal Rates Using Historical Data.” Journal ofFinancialPlanning,October,171‐180.Bengen,William(1996).“AssetAllocationforaLifetime.”JournalofFinancialPlanning,August,58‐67.Bengen,William (1997). “Conserving Client PortfoliosDuringRetirement, Part III.” Journal ofFinancialPlanning,December,84‐97.Bengen,William (2001). “Conserving Client PortfoliosDuringRetirement, Part IV.” Journal ofFinancialPlanning,May,110‐119.Blanchett,David(2007).“DynamicAllocationStrategiesforDistributionPortfolios:DeterminingtheOptimalDistributionGlidePath.”JournalofFinancialPlanning,December,68‐81.Blanchett,David,andLarryFrank(2009). “ADynamicandAdaptiveApproachtoDistributionPlanningandMonitoring.”JournalofFinancialPlanning,April,52‐66.Cassaday, Stephan (2006). “DIESEL: A System for Generating Cash Flow During Retirement.”JournalofFinancialPlanning,September,50‐65.Cohen,Josh,GrantGardner,andYuan‐AnFan(2010).“ShouldTargetDateFundGlidePathsBeManaged‘To’or‘Through’Retirement?”RussellResearch,April,1‐7.Cooley, Philip, Carl Hubbard, and Daniel Walz (1998). “Retirement Savings: Choosing aWithdrawal Rate That Is Sustainable.” Journal of the American Association of IndividualInvestors,February,16‐21.Cooley, Philip, Carl Hubbard, and Daniel Walz (2003a). “Does International DiversificationIncrease the SustainableWithdrawal Rates from Retirement Portfolios?” Journal of FinancialPlanning,January,74‐80.Cooley,Philip,CarlHubbard,andDanielWalz(2003b).“AComparativeAnalysisofRetirementPortfolioSuccessRates:SimulationVersusOverlappingPeriods.”FinancialServicesReview,12,115‐128.Cooley,Philip,CarlHubbard,andDanielWalz(2005). “RetirementWithdrawals:WhatRate IsSafe When Time Is Short and Uncertain.” Journal of the American Association of IndividualInvestors,January,4‐9.Cooley,Philip,CarlHubbard,andDanielWalz(2011).“PortfolioSuccessRates:WheretoDrawtheLine.”JournalofFinancialPlanning,April,48‐60.Dimson,Elroy,PaulMarsh,andMikeStaunton(2002).TriumphoftheOptimists–101YearsofInvestmentReturns.PrincetonUniversityPress.Dimson,Elroy,PaulMarsh,andMikeStaunton(2015).“CreditSuisseGlobalInvestmentReturnsYearbook2015.”CreditSuisse,February.

13

Dus,Ivica,RaimondMaurer,andOliviaMitchell(2005).“BettingonDeathandCapitalMarketsinRetirement: A Shortfall Risk Analysis of Life Annuities Versus Phased Withdrawal Plans.”FinancialServicesReview,14,169‐196.Estrada, Javier (2014a). “The Glidepath Illusion: An International Perspective.” Journal ofPortfolioManagement,Summer,52‐64.Estrada,Javier(2014b).“RethinkingRisk.”JournalofAssetManagement,15,4,239‐259.Estrada, Javier (2014c). “Rethinking Risk (II): The Size and Value Effects.” Journal ofWealthManagement,Winter,78‐83.Estrada, Javier (2016). “The Retirement Glidepath: An International Perspective.” Journal ofInvesting,forthcoming.Garrison, Michael, Carlos Sera, and Jeffrey Cribbs (2010). “A Simple Dynamic Strategy forPortfoliosTakingWithdrawals:TheCaseforUsinga12‐MonthSimpleMovingAverage.”JournalofFinancialPlanning,February,51‐61.Guyton, Jonathan (2004). “DecisionRulesandPortfolioManagement forRetirees: Is the ‘Safe’InitialWithdrawalRateTooSafe?”JournalofFinancialPlanning,October,54‐62.Guyton,Jonathan,andWilliamKlinger(2006).“DecisionRulesandMaximumInitialWithdrawalRates.”JournalofFinancialPlanning,March,48‐58.Jaconetti,Colleen,FrancisKinniry,andMichaelDiJoseph(2013).“AMoreDynamicApproachToSpendingForInvestorsinRetirement.”VanguardResearch,October,1‐12.Kitces,Michael(2008).“ResolvingtheParadox:IstheSafeWithdrawalRateSometimesTooSafe.”TheKitcesReport,May,1‐13.Kitces,Michael,andWadePfau(2014).“RetirementRisk,EquityGlidepaths,andValuation‐BasedAssetAllocation.”Workingpaper.Milevsky,Moshe,andChrisRobinson(2005).“ASustainableSpendingRateWithoutSimulation.”FinancialAnalystsJournal,November/December,89‐100.Milevsky,Moshe,KwokHo,andChrisRobinson(1997).“AssetAllocationViatheConditionalFirstExit Time or How To Avoid Outliving Your Money.” Review of Quantitative Finance andAccounting,9,53‐70.Pfau,Wade(2011).“CanWePredicttheSustainableWithdrawalRateforNewRetirees?”JournalofFinancialPlanning,August,40‐47.Pfau,Wade (2012). “WithdrawalRates, SavingsRates, andValuation‐BasedAsset Allocation.”JournalofFinancialPlanning,April,34‐40.Pfau,Wade, andMichaelKitces (2014). “ReducingRetirementRiskwithaRisingEquityGlidePath.”JournalofFinancialPlanning,January,38‐48.Pye,Gordon (2000). “Sustainable InvestmentWithdrawals.” Journal ofPortfolioManagement,Summer,73‐83.

14

Sheikh,Abdullah,KatherineRoy,andAnneLester(2014).“Breakingthe4%Rule.DynamicallyAdapting Asset Allocation and Withdrawal Rates To Make the Most of Retirement Assets.”JPMorgan,RetirementInsights,February,1‐32.Spitzer, John, and Sandeep Singh (2006). “Extending Retirement Payouts by Optimizing theSequenceofWithdrawals.”JournalofFinancialPlanning,April,52‐61.Spitzer, John, and Sandeep Singh (2007). “Is Rebalancing a Portfolio During RetirementNecessary?”JournalofFinancialPlanning,June,46‐57.Spitzer,John,JeffreyStrieter,andSandeepSingh(2007).“GuidelinesforWithdrawalRatesandPortfolioSafetyDuringRetirement.”JournalofFinancialPlanning,October,52‐59.Stout, Gene (2008). “Stochastic Optimization of Retirement Portfolio Asset Allocations andWithdrawals.”FinancialServicesReview,17,1‐15.Stout, Gene, and JohnMitchell (2006). “Dynamic RetirementWithdrawal Planning.” FinancialServicesReview,15,117‐131.Terry,Rory(2003).“TheRelationBetweenPortfolioCompositionandSustainableWithdrawalRates.”JournalofFinancialPlanning,May,64‐78.