Embed Size (px)

Citation preview

Building a bridge between Ministry of Health (MoH) & Ministry of Finance (MoF) for tobacco taxes

Ayda A. Yurekli, PhD Coordinator Tobacco Control Economics Tobacco Free Initiative WHO

Asian Focal Points for Tobacco Control Meeting, Bangkok, September 5, 2011

Why Tax Tobacco? Two major reasons MoH & MoF

Promote public health

Raise revenue

Tax tobacco products Promote public health

"The Parties recognize that

price and tax measures are an effective and important means of reducing tobacco consumption by various segments of the population, in particular young persons.”

(WHO Framework Convention on Tobacco Control, Article 6)

Health effects of tax & price increases

Tax and price increases Induce current users to try to quit

Keep former users from restarting

Prevent potential users from starting

Reduce consumption among those who

continue to use

Objectives of Public Health With respect to reducing consumption by tax policy

1. Retail price increases via tax increases 2. Price gap among price bands reduces, so

that 1. Substitution from high to cheap cigarettes is

reduced 2. Expected reduction by quitting or reducing level

of consumption is achieved

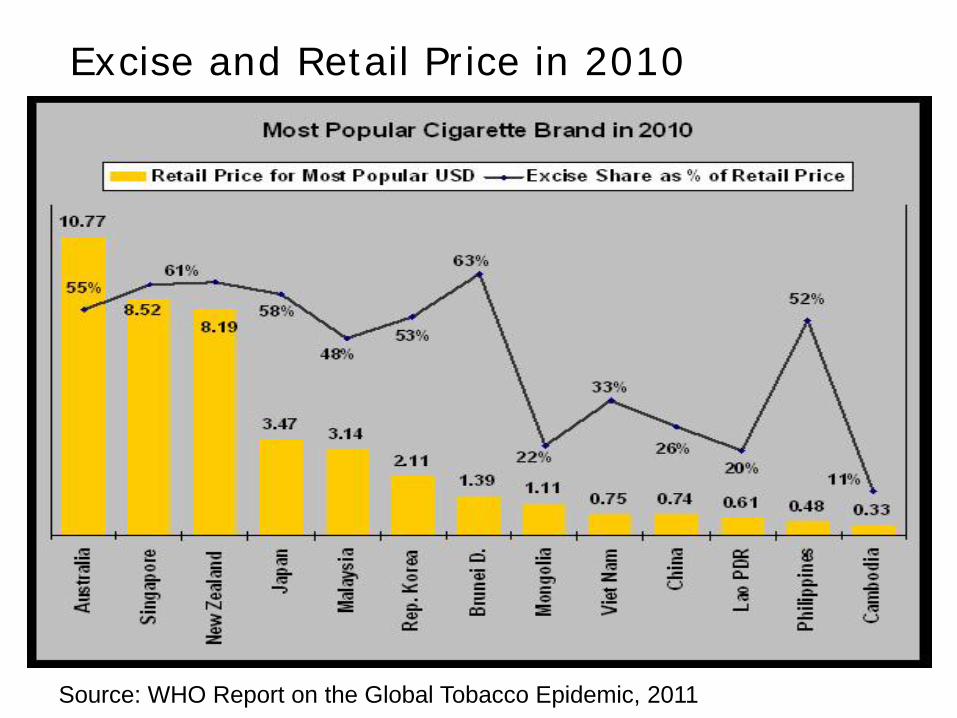

Excise and Retail Price in 2010

Source: WHO Report on the Global Tobacco Epidemic, 2011

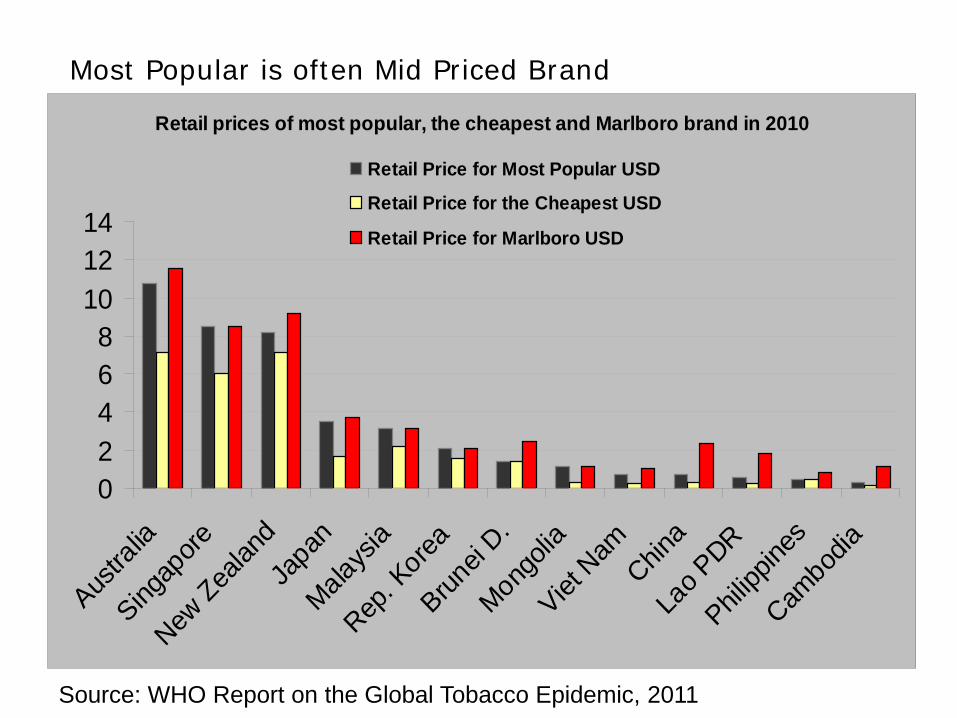

Most Popular is often Mid Priced Brand

Retail prices of most popular, the cheapest and Marlboro brand in 2010

02468

101214

Austra

lia

Singap

ore

New Zea

landJa

pan

Malays

ia

Rep. K

orea

Brunei

D.

Mongo

lia

Viet N

amChin

a

Lao P

DR

Philipp

ines

Cambo

dia

Retail Price for Most Popular USD

Retail Price for the Cheapest USD

Retail Price for Marlboro USD

Source: WHO Report on the Global Tobacco Epidemic, 2011

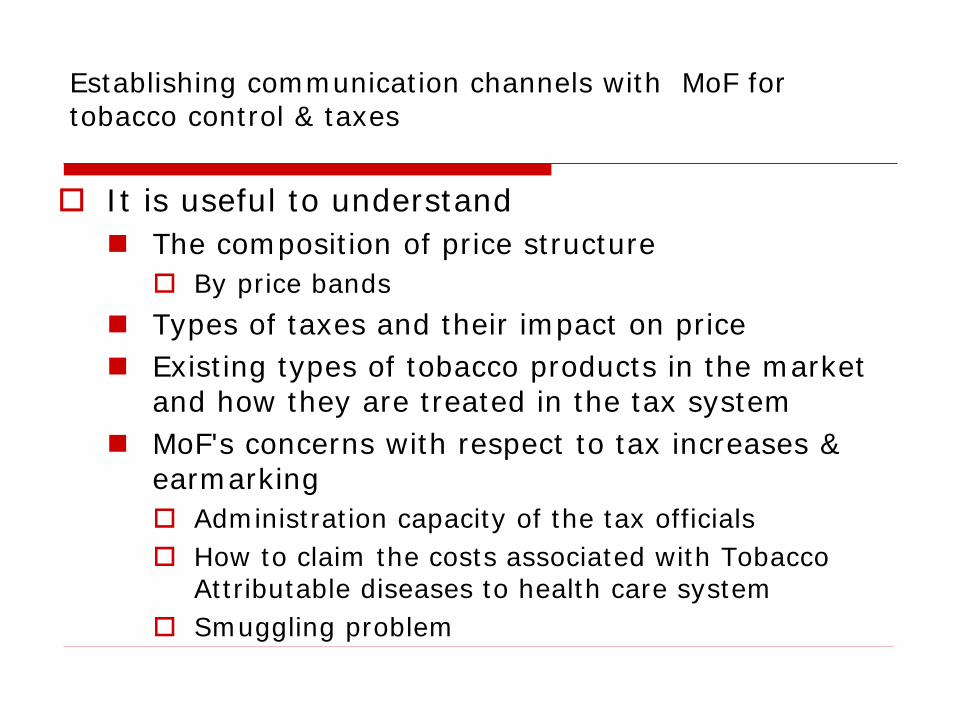

Establishing communication channels with MoF for tobacco control & taxes

It is useful to understand The composition of price structure By price bands

Types of taxes and their impact on price Existing types of tobacco products in the market

and how they are treated in the tax system MoF's concerns with respect to tax increases &

earmarking Administration capacity of the tax officials How to claim the costs associated with Tobacco

Attributable diseases to health care system Smuggling problem

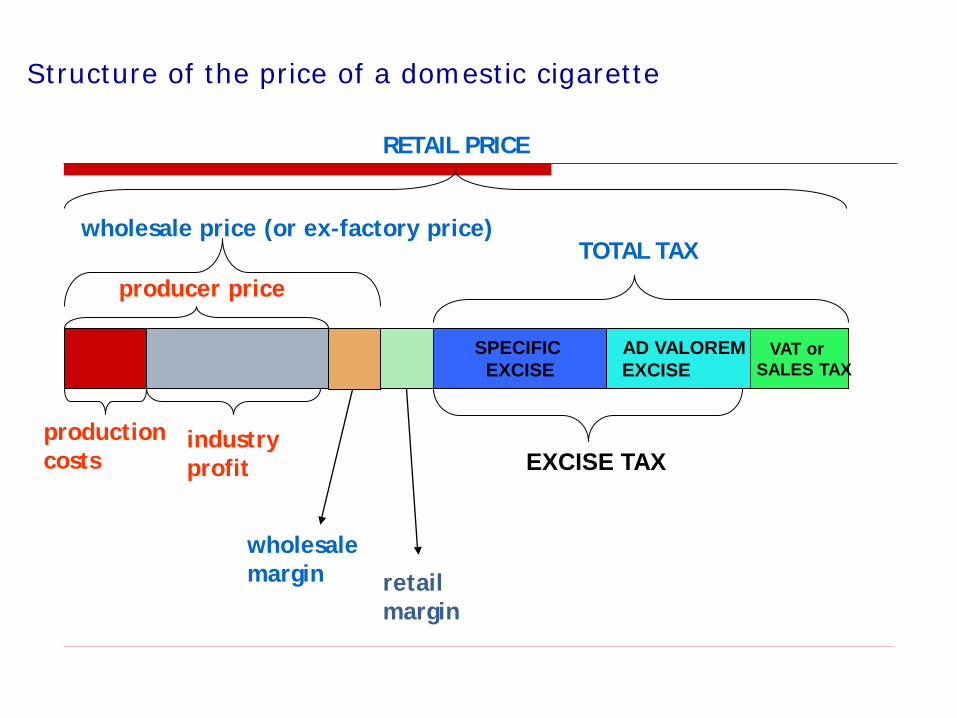

Structure of the price of a domestic cigarette

wholesale price (or ex-factory price)

RETAIL PRICE

TOTAL TAX

AD VALOREM EXCISE

retail margin

production costs

industry profit

wholesale margin

SPECIFIC EXCISE

producer price

VAT or SALES TAX

EXCISE TAX

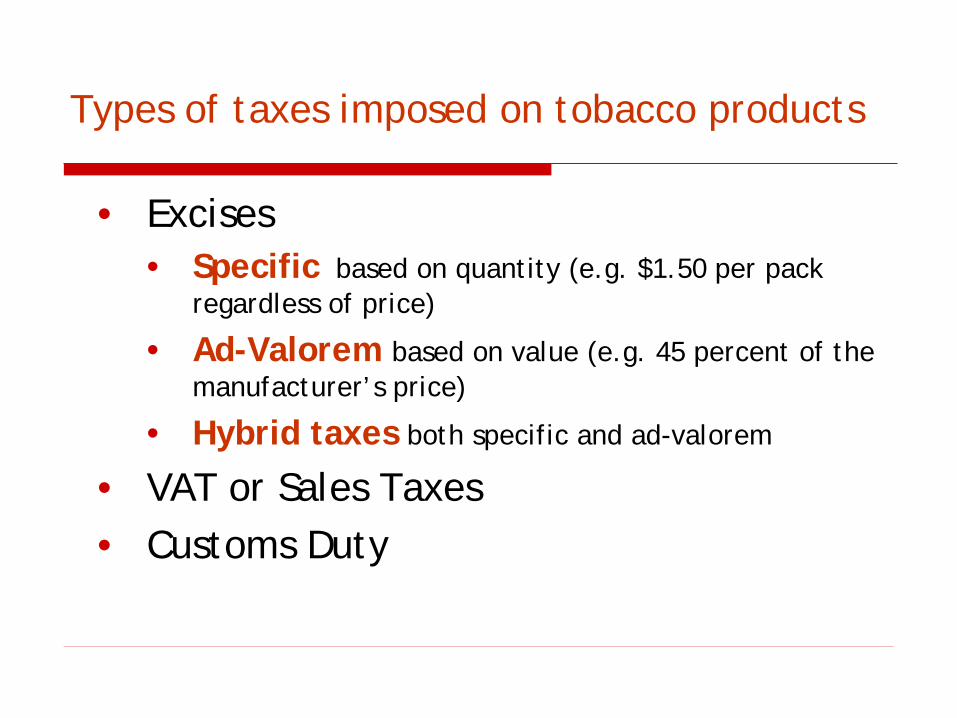

Types of taxes imposed on tobacco products

• Excises • Specific based on quantity (e.g. $1.50 per pack

regardless of price)

• Ad-Valorem based on value (e.g. 45 percent of the manufacturer’s price)

• Hybrid taxes both specific and ad-valorem

• VAT or Sales Taxes • Customs Duty

It is essential to know how to impose types of excise taxes based on country situation

Especially which excise would help achieving higher revenues while reducing consumption

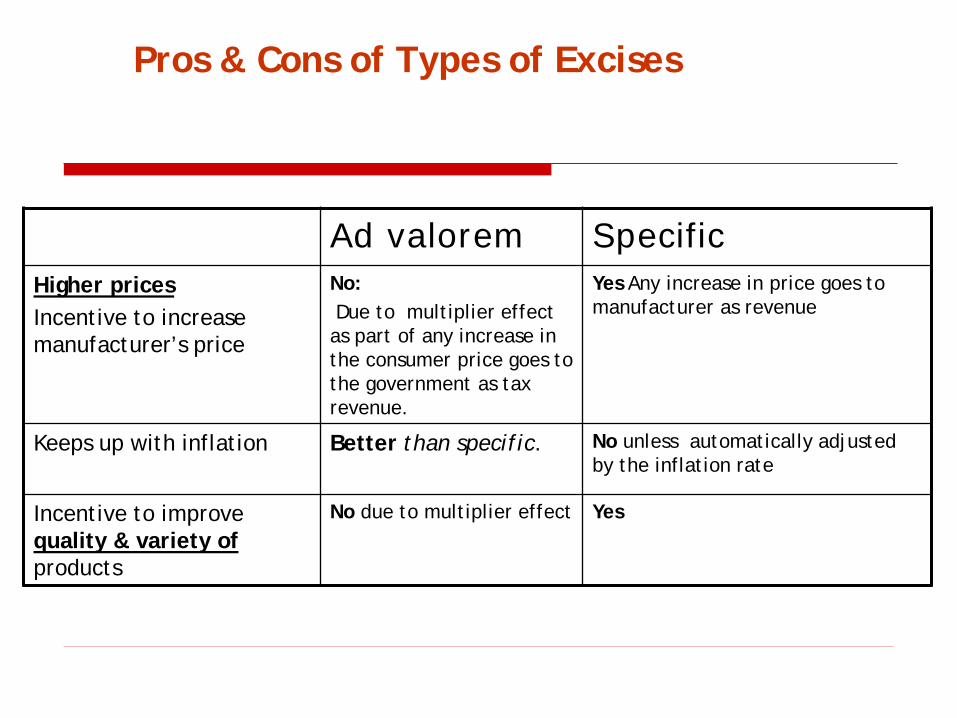

Pros & Cons of Types of Excises

Ad valorem Specific Higher prices Incentive to increase manufacturer’s price

No: Due to multiplier effect as part of any increase in the consumer price goes to the government as tax revenue.

Yes Any increase in price goes to manufacturer as revenue

Keeps up with inflation Better than specific.

No unless automatically adjusted by the inflation rate

Incentive to improve quality & variety of products

No due to multiplier effect Yes

Pros & Cons of Types of Excises

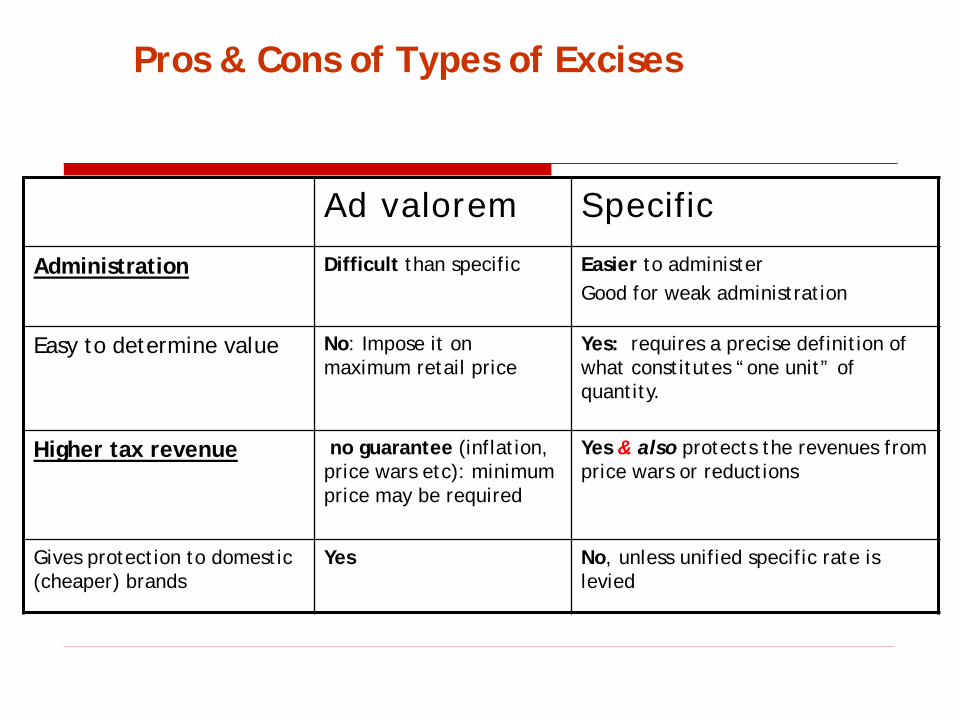

Ad valorem Specific Administration Difficult than specific

Easier to administer Good for weak administration

Easy to determine value No: Impose it on maximum retail price

Yes: requires a precise definition of what constitutes “one unit” of quantity.

Higher tax revenue no guarantee (inflation, price wars etc): minimum price may be required

Yes & also protects the revenues from price wars or reductions

Gives protection to domestic (cheaper) brands

Yes No, unless unified specific rate is levied

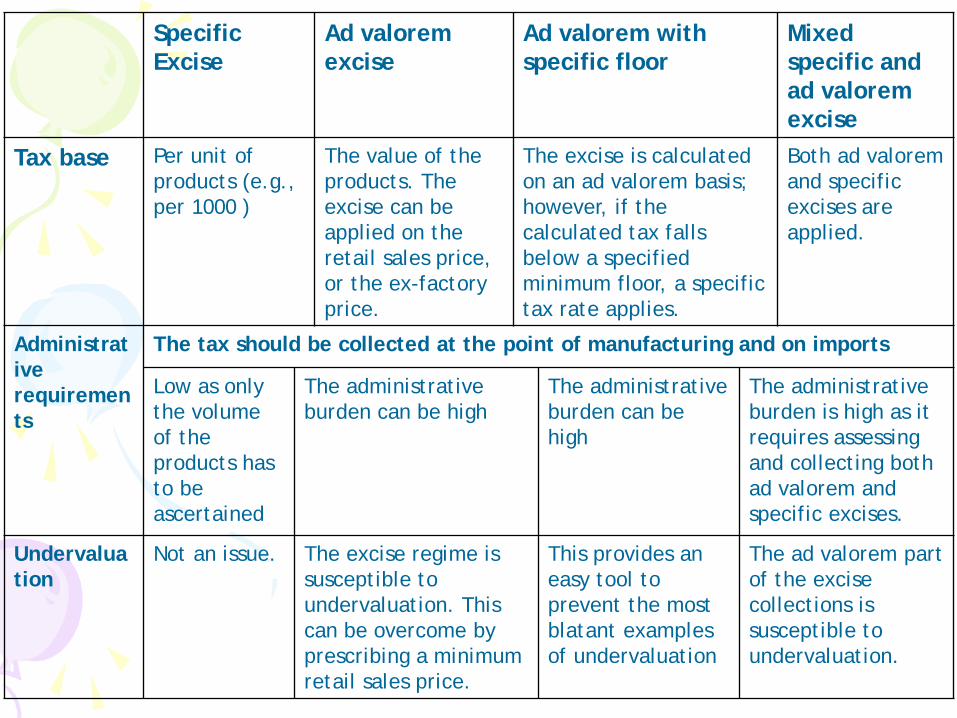

Specific Excise

Ad valorem excise

Ad valorem with specific floor

Mixed specific and ad valorem excise

Tax base Per unit of products (e.g., per 1000 )

The value of the products. The excise can be applied on the retail sales price, or the ex-factory price.

The excise is calculated on an ad valorem basis; however, if the calculated tax falls below a specified minimum floor, a specific tax rate applies.

Both ad valorem and specific excises are applied.

Administrative requirements

The tax should be collected at the point of manufacturing and on imports

Low as only the volume of the products has to be ascertained

The administrative burden can be high

The administrative burden can be high

The administrative burden is high as it requires assessing and collecting both ad valorem and specific excises.

Undervaluation

Not an issue. The excise regime is susceptible to undervaluation. This can be overcome by prescribing a minimum retail sales price.

This provides an easy tool to prevent the most blatant examples of undervaluation

The ad valorem part of the excise collections is susceptible to undervaluation.

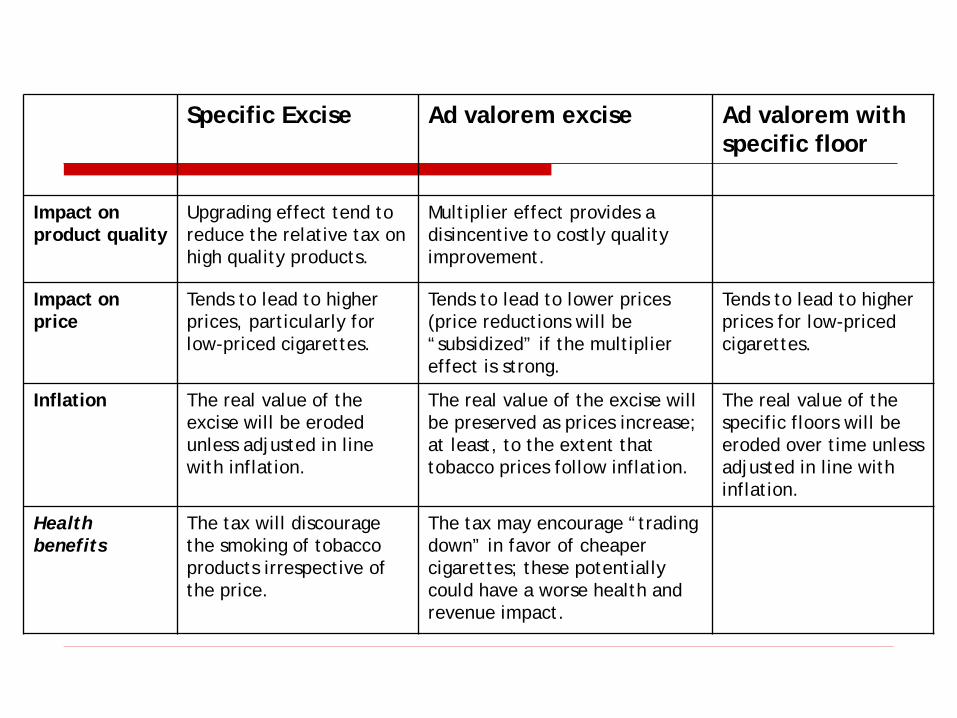

Specific Excise Ad valorem excise Ad valorem with specific floor

Impact on product quality

Upgrading effect tend to reduce the relative tax on high quality products.

Multiplier effect provides a disincentive to costly quality improvement.

Impact on price

Tends to lead to higher prices, particularly for low-priced cigarettes.

Tends to lead to lower prices (price reductions will be “subsidized” if the multiplier effect is strong.

Tends to lead to higher prices for low-priced cigarettes.

Inflation The real value of the excise will be eroded unless adjusted in line with inflation.

The real value of the excise will be preserved as prices increase; at least, to the extent that tobacco prices follow inflation.

The real value of the specific floors will be eroded over time unless adjusted in line with inflation.

Health benefits

The tax will discourage the smoking of tobacco products irrespective of the price.

The tax may encourage “trading down” in favor of cheaper cigarettes; these potentially could have a worse health and revenue impact.

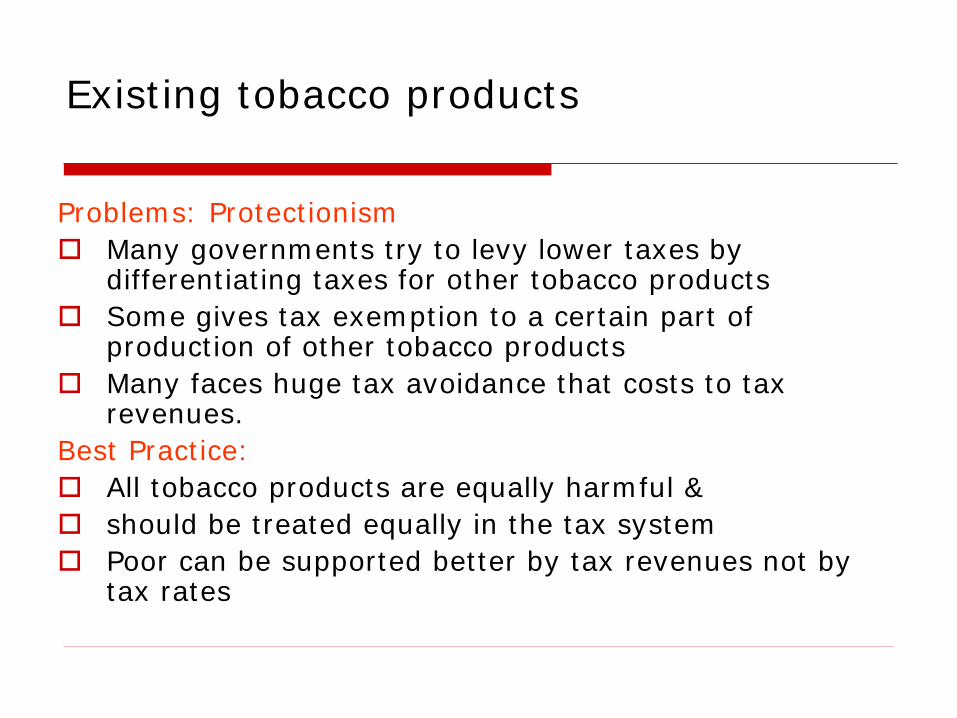

Existing tobacco products

Problems: Protectionism Many governments try to levy lower taxes by

differentiating taxes for other tobacco products Some gives tax exemption to a certain part of

production of other tobacco products Many faces huge tax avoidance that costs to tax

revenues. Best Practice: All tobacco products are equally harmful & should be treated equally in the tax system Poor can be supported better by tax revenues not by

tax rates

Concerns with the differential excise system

Public Health Concern Lead to other changes in tobacco use behavior &

undermines the full impact of higher taxes on consumption. substitution to cheaper products or brands

Revenue Concern Reduced expected revenue Changing market structure of brand share

Concerns for higher taxes

As consumption reduces, the revenues decreases – FALSE

As tax increases, smuggling increases Partly true But Level of smuggling cannot be explained

entirely by taxes.

Tax tobacco products Raise revenue

Efficient revenue generation Historically, the primary motive - still

true in many countries today Very efficient source of revenue given: Low share of tax in price in most countries Relatively inelastic demand for tobacco

products Few producers and few close substitutes,

in general

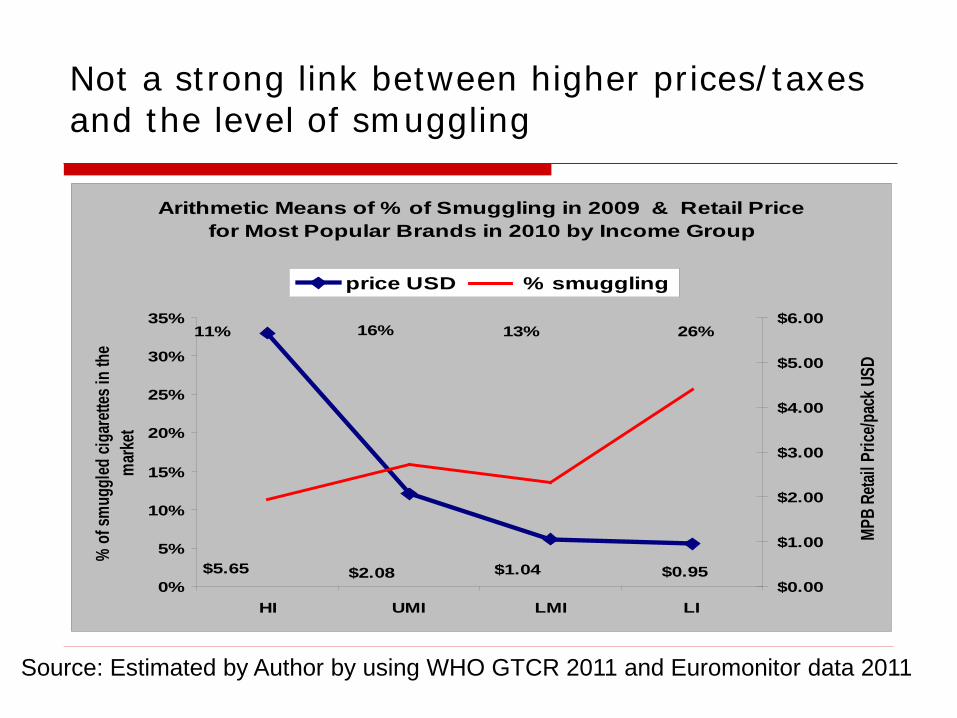

Not a strong link between higher prices/taxes and the level of smuggling

Arithmetic Means of % of Smuggling in 2009 & Retail Price for Most Popular Brands in 2010 by Income Group

$2.08 $0.95$1.04$5.65

26%13%16%11%

0%

5%

10%

15%

20%

25%

30%

35%

HI UMI LMI LI

% o

f sm

uggl

ed ci

gare

ttes i

n th

e m

arke

t

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

MPB

Retai

l Pric

e/pac

k USD

price USD % smuggling

Source: Estimated by Author by using WHO GTCR 2011 and Euromonitor data 2011

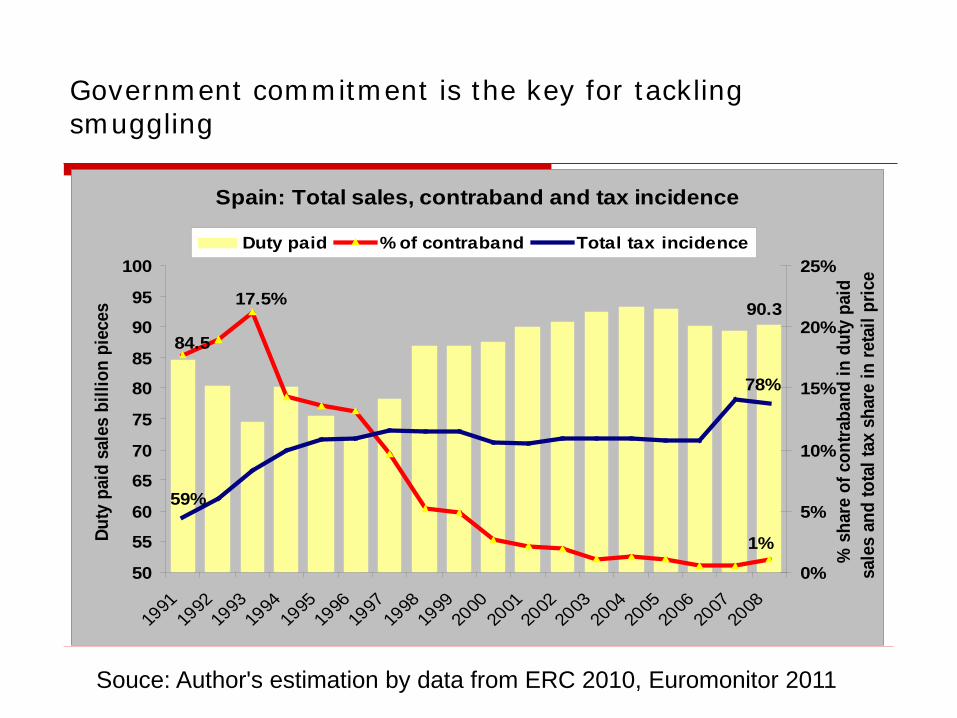

Government commitment is the key for tackling smuggling

Spain: Total sales, contraband and tax incidence

90.3

84.5

17.5%

1%

78%

59%

50

55

60

65

70

75

80

85

90

95

100

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

Duty

pai

d sa

les

billi

on p

iece

s

0%

5%

10%

15%

20%

25%

% s

hare

of c

ontra

band

in d

uty

paid

sa

les

and

tota

l tax

sha

re in

reta

il pr

ice

Duty paid % of contraband Total tax incidence

Souce: Author's estimation by data from ERC 2010, Euromonitor 2011

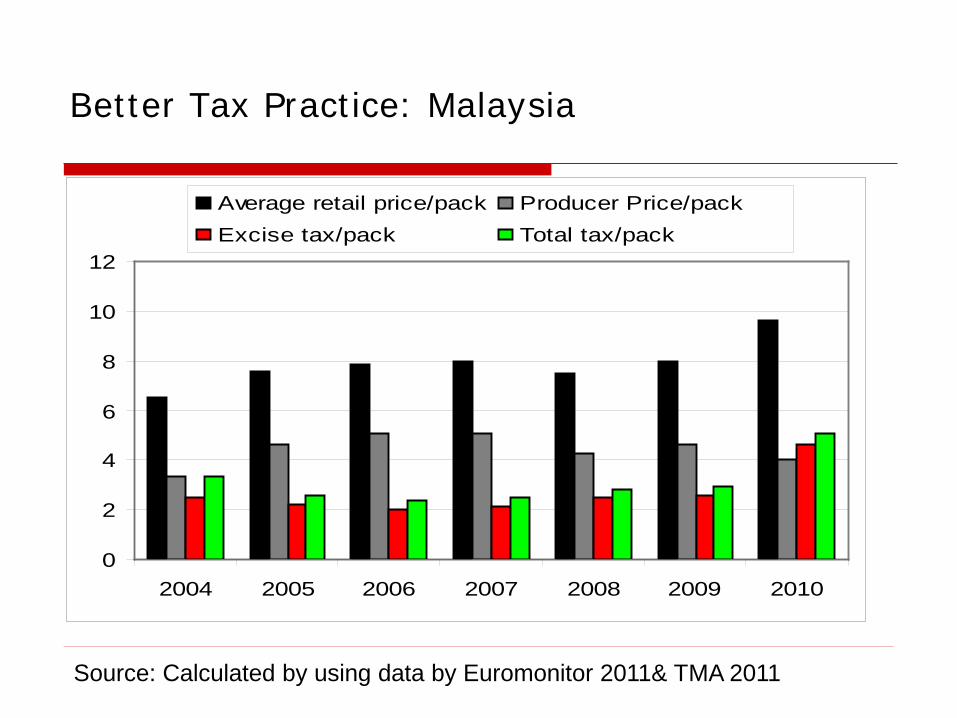

Better Tax Practice: Malaysia

0

2

4

6

8

10

12

2004 2005 2006 2007 2008 2009 2010

Average retail price/pack Producer Price/packExcise tax/pack Total tax/pack

Source: Calculated by using data by Euromonitor 2011& TMA 2011

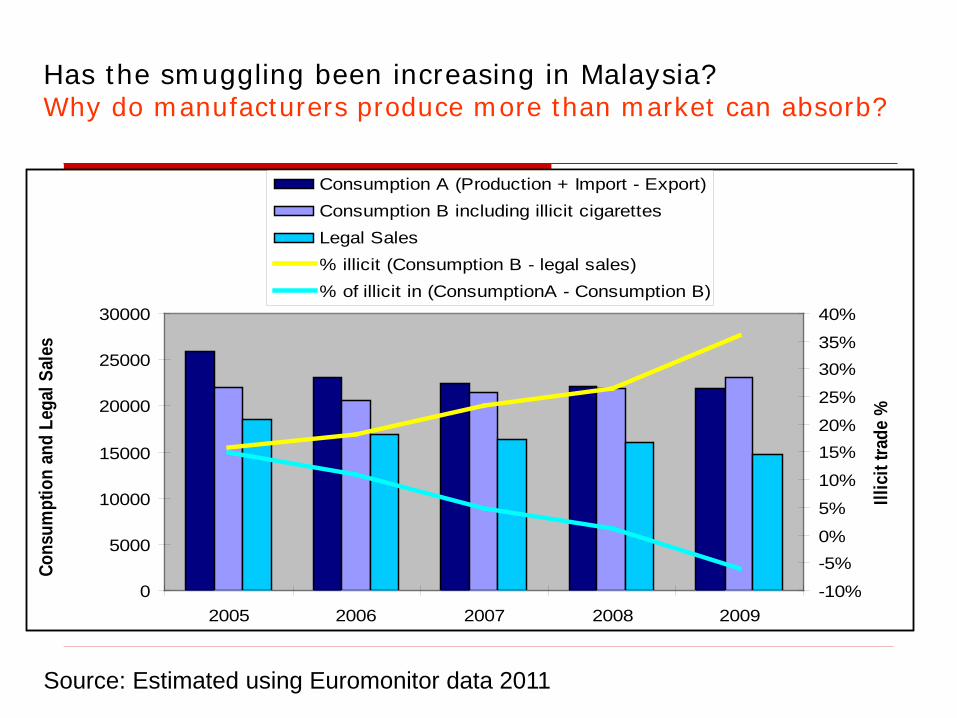

Has the smuggling been increasing in Malaysia? Why do manufacturers produce more than market can absorb?

Source: Estimated using Euromonitor data 2011

0

5000

10000

15000

20000

25000

30000

2005 2006 2007 2008 2009

Cons

umpt

ion

and

Lega

l Sal

es

-10%

-5%0%

5%

10%

15%20%

25%

30%35%

40%

Illic

it tra

de %

Consumption A (Production + Import - Export)Consumption B including illicit cigarettesLegal Sales% illicit (Consumption B - legal sales) % of illicit in (ConsumptionA - Consumption B)

Conclusion

MoH may lead to multi-sectoral collaboration in the government for tobacco control

Although revenue generation is the focus, MoF is also sensitive to public health concerns

Therefore, Reaching out MoF is the key for better tobacco tax

policy implementation Speaking MoF's language is important but it is equally important to understanding MoF's concerns

& constraints and finding solutions within the government